Exhibit 99.1

Highlights of continuing operations for the three and six months ended September 30, 2014 included:

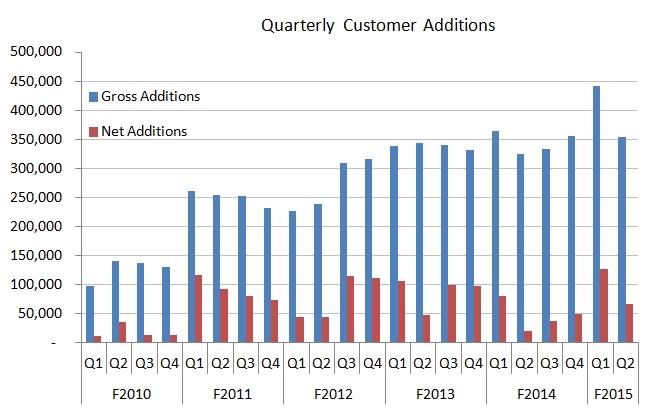

| · | Gross customer additions of 354,000, for the second quarter up 9% compared to 324,000 in the second quarter of fiscal 2014. This represents the highest number of customers ever signed by the Company in the second quarter. Year to date, gross customer additions are 795,000, up 16% year over year. |

| · | Net customer additions of 67,000 in the second quarter an increase of 235% versus net additions of 20,000 in the second quarter of fiscal 2014. Year to date net additions of 194,000 exceed fiscal 2014 total net additions of 188,000. Customer base up 7% year over year to 4.6 million. |

| · | Gross margin of $132.5 million, up 17%. Six months gross margin of $255.9 million, up 17%. |

| · | Base EBITDA from continuing operations of $31.7 million, up 12%. Base Funds from continuing operations was $23.8 million, up 1%. Year to date Base EBITDA is $61.9 million up 26%. Year to date Base FFO of $39.3 million, up 16%. |

Message from the Co-Chief Executive Officers

Fellow Shareholders,

Our second quarter showed continued positive trends within fiscal 2015. We are very pleased with our financial and operational results during the second quarter, which continues a strong start to our fiscal year. For the future, the most promising trend was our gross and net customer additions. The results reflect the largest number of customer additions for the second quarter in the Company’s history. Combined with the first quarter’s record additions, our net additions for six months are 194,000, up 94% from fiscal 2014. Both our divisions performed strongly with gross margin up 13% for the Consumer division and 27% for the Commercial division.

Overall, gross margin for the second quarter was up 17% compared to the prior year. This reflects improved profitability as overall customer growth was 7%. We benefitted from lower balancing charges compared to a year ago but the results are clearly positive. This profitability was partly driven by higher new customer margins in that both new consumer and commercial customers added or renewed were at higher margins than customers lost. A year ago, the opposite was true for both divisions.

Our second quarter 12% Base EBITDA growth and 1% Base Funds from operations growth and our six months 26% Base EBITDA growth and 16% Base FFO growth provide evidence that our business is growing and generating solid returns. As we’ve said previously, we remain committed to enhancing our balance sheet by reducing our debt levels and refocusing our portfolio towards our core business. We are focused on growing our business through innovative energy products that provide our customers with enhanced value.

| For the three months ended Sept 30 | |||

| (Millions of dollars except where indicated and per share amounts) | Fiscal 2015 | Fiscal 2014 | % increase (decrease) |

| Sales | $918.3 | $833.7 | 10% |

| Gross margin | 132.5 | 113.5 | 17% |

| Administrative expenses | 38.3 | 29.4 | 30% |

| Selling & marketing expenses | 53.1 | 46.8 | 13% |

| Finance costs | 18.7 | 16.6 | 13% |

| Loss from continuing operations | (94.3) | (111.8) | |

| Profit (loss) from discontinued operations | (40.9) | 1.6 | |

| Loss | (135.2) | (110.2) | |

| Loss per share from continuing operations available to shareholders - basic | (0.67) | (0.79) | |

| Loss per share from continuing operations available to shareholders - diluted | (0.67) | (0.79) | |

| Dividends/distributions | 18.6 | 30.9 | (40)% |

| Base EBITDA from continuing operations | 31.7 | 28.3 | 12% |

| Base Funds from continuing operations | 23.8 | 23.5 | 1% |

| Payout ratio on Base Funds from continuing operations | 78% | 131% | |

| For the six months ended September 30 | |||

| (Millions of dollars except where indicated and per share amounts) | Fiscal 2015 | Fiscal 2014 | % increase (decrease) |

| Sales | $1,739.3 | $1,561.8 | 11% |

| Gross margin | 255.9 | 219.4 | 17% |

| Administrative expenses | 71.3 | 59.2 | 20% |

| Selling & marketing expenses | 108.3 | 97.6 | 11% |

| Finance costs | 37.5 | 33.4 | 12% |

| Loss from continuing operations | (140.0) | (151.4) | |

| Profit (loss) from discontinued operations | (34.1) | (0.7) | |

| Loss | (174.1) | (152.0) | |

| Loss per share from continuing operations available to shareholders - basic | (0.98) | (1.07) | |

| Loss per share from continuing operations available to shareholders - diluted | (0.98) | (1.07) | |

| Dividends/distributions | 49.6 | 61.6 | (20)% |

| Base EBITDA from continuing operations | 61.9 | 49.0 | 26% |

| Base Funds from continuing operations | 39.3 | 33.9 | 16% |

| Payout ratio on Base Funds from continuing operations | 126% | 182% | |

| Embedded gross margin | 1,755,200 | 1,637,200 | 7% |

| Total customers (RCE's) | 4,604,000 | 4,322,000 | 7% |

Adding Customers

Customer additions in the second quarter were 354,000, 9% more than the second quarter of fiscal 2014. Net additions were 67,000 for the quarter up 235% from a year earlier. Year to date, 795,000 gross customer additions have resulted in net additions of 194,000, up 94% from a year earlier. The overall customer base grew to 4.6 million, up 7% from a year earlier.

Gross additions were generated from all sales channels with 180,000 new commercial customers, up 13% from the 160,000 added in the second quarter of fiscal 2014. Consumer additions totaled 174,000, up 6% from 164,000 added in the prior comparable quarter. With record sales year to date, total outstanding customer complaints remain at 1.4 per 10,000 customers, well below the Company’s target of not more than 5 complaints for every 10,000 customers.

| July 1, | Failed to | Sept 30, | % increase | Sept 30, | % increase | |||

| 2014 | Additions | Attrition | renew | 2014 | (decrease) | 2013 | (decrease) | |

| Consumer Energy | ||||||||

| Gas | 734,000 | 46,000 | (42,000) | (11,000) | 727,000 | (1)% | 771,000 | (6)% |

| Electricity | 1,208,000 | 128,000 | (91,000) | (25,000) | 1,220,000 | 1% | 1,206,000 | 1% |

| Total Consumer RCEs | 1,942,000 | 174,000 | (133,000) | (36,000) | 1,947,000 | 0% | 1,977,000 | (2)% |

| Commercial Energy | ||||||||

| Gas | 204,000 | 15,000 | (3,000) | (8,000) | 208,000 | 2% | 205,000 | 1% |

| Electricity | 2,391,000 | 165,000 | (43,000) | (64,000) | 2,449,000 | 2% | 2,140,000 | 14% |

| Total Commercial RCEs | 2,595,000 | 180,000 | (46,000) | (72,000) | 2,657,000 | 2% | 2,345,000 | 13% |

| Total RCEs | 4,537,000 | 354,000 | (179,000) | (108,000) | 4,604,000 | 1% | 4,322,000 | 7% |

Maintaining Customers

The combined attrition rate for Just Energy was 15% for the trailing 12 months ended September 30, 2014, down 1% from attrition reported in the first quarter. Consumer attrition (27%) improved by 1% from the first quarter while commercial attrition remained at 6%.

Attrition is and will remain a key driver of the Company’s financial success. Consumer attrition rates remain high. This has been highly correlated to “bill shock” as consumers on fixed prices saw consumption rise sharply during the cold weather experienced last winter resulting in much higher than expected bills. Current gas price volatility and expectations for higher electricity prices should both contribute to a possible reduction in attrition in future periods.

Renewal rates improved slightly versus that reported in the first quarter with Consumer renewals unchanged at 75% and commercial renewals up 1% to 64% on a trailing 12-month basis. This indicates continued satisfaction with the Company’s products and services. Commercial renewals are often subject to competitive bid and will inevitably be more volatile than consumer renewals. Overall management sees stability in renewals at around current levels.

Profitability

Just Energy had significantly improved operating results in the three and six months ended September 30, 2014 compared to fiscal 2014. Note that all comparisons to prior periods exclude the results of National Home Services and Hudson Energy Solar due to their classification as discontinued operations. Gross margin for the quarter was $132.5 million, up 17% from $113.5 million in fiscal 2014. Year to date, gross margin is $255.9 million up 17% from the prior comparable period. Second quarter Base EBITDA from continuing operations was $31.7 million, up 12% from $28.3 million in the prior comparable period. Year to date Base EBITDA is $61.9 million, up 26% versus fiscal 2014. Base Funds from continuing operations for the second quarter were $23.8 million, up 1% from $23.5 million a year earlier. Year to date, Base FFO is $39.3 million up 16% versus fiscal 2014.

Based on the first two quarters, Base EBITDA growth from continuing operations is 26%. The 16% increase in Base Funds from operations year to date generates, based on the current $0.50 annual dividend, a pro-forma payout ratio of 79% over the past 12-months, tracking toward the Company’s goal to reduce its payout ratio toward its long term target range of below 65%. The Company’s payout ratio has been well above 100% for the past several years.

The following factors drove profitability in the second quarter:

| · | The 7% year over year growth in customers led to a 17% increase in gross margin. This reflects the fact that the annual margin on customers added or renewed exceeded the annual margin on customers lost. This fiscal 2015 result to date reverses a longstanding downward trend on margins. In addition, gross margin increased as a result of lower electricity balancing costs compared to a year earlier. Embedded margin in the customer base grew 7% as well, reflecting the higher number of customers and a higher U.S. dollar exchange rate. Despite a 2% decrease in the Consumer customer base, Consumer margin rose 13%. Consumer customers added or renewed in the quarter were at higher margins ($188 per year) than the margin on customers lost ($183 per year). |

| · | Commercial division margins were up 27% reflecting 13% increase in customers. Margins on new and renewed customers were $80 per year up sharply from a year earlier and higher than the $73 on customers lost during the period. The higher margin is a conscious decision by management to reduce low margin Commercial business and focus on more profitable customer segments. |

| · | The 30% increase in administrative expenses seen year over year in the second quarter compares to the 7% increase in customer base. The guidance provided by management for fiscal 2015 anticipated administrative costs growing more rapidly than margin for the year. On October 8, 2014, Just Energy announced that a jury in the Federal Court of the Northern District of Ohio reached a verdict supporting the plaintiffs’ class and collective action in the Hurt, et al vs. Commerce Energy, Inc. et al lawsuit. Just Energy disagrees with the result and strongly believes it complied with the law and plans on appealing. Over and above the expected administrative cost increase were current and provisioned future legal costs related to the Hurt action and a provision against any eventual award. These expenses added approximately $4 million to second quarter administrative costs. |

| · | Selling and marketing expenses, which consist of commissions paid to independent sales contractors, brokers and independent representatives as well as sales-related corporate costs, were $53.1 million, an increase of 13% from $46.8 million in the second quarter of fiscal 2014. This was higher than the 9% increase in customers added. The difference is due to higher amortization of contract initiation costs related to Commercial contracts signed in prior periods where commissions were advanced upfront. There are also a growing number of Consumer division customers generated by online sales channels where commissions are paid on a residual basis as the customer flows rather than upfront. |

| · | Year to date, bad debt amounted to 2.3% of relevant sales, up from 2.1% in the comparable period of fiscal 2014 and down from the 2.4% reported in the first quarter and within the target range of 2%-3%. |

Base Funds from operations are up 1% in the second quarter compared to a year earlier, less than the increase in Base EBITDA. There were two major components to this slower growth. The first is a $2.7 million increase in the income tax provision. This is due largely to the settlement of prior period tax audits in the quarter. The Company expects only nominal cash taxes for the remainder of fiscal 2015. Finance cost were $18.7 million, up from $16.6 million a year earlier but down slightly from the first quarter of fiscal 2015. These charges will remain in this range until the closing of the NHS sale and the related reduction of continuing debt.

We continue to move forward with the de-levering of our balance sheet. We have closed the sale of our Hudson Solar commercial solar business and the sale of National Home Services is in process. While we do not control the closing date of this transaction, upon closing, the proceeds will considerably reduce our debt and further improve our payout ratio.

Outlook

The second quarter of fiscal 2015 showed higher than expected gross and net customer additions, sales, gross margin, Base EBITDA and Base Funds from continuing operations. Management reaffirms its comfort with its published fiscal 2015 Base EBITDA growth guidance of $163 million to $173 million.

Debt reduction remains a clear priority of management. Based on the selling price of NHS, the Company believes total debt will be below the target ratio of four times EBITDA on the closing of these transactions. Management expects continued reductions in debt going forward. Because of factors beyond Just Energy control, the NHS sale has not yet closed due to the continuing regulatory review. However, we are optimistic for a close in the coming months.

Just Energy retains a strong interest in participating in the sale of solar energy to residential homeowners. The Company is exploring non-capital-intensive methods of offering residential solar and will provide shareholders with regular updates as to progress as it continues to review possible options for entry into this market.

Overall, we believe fiscal 2015 is off to an excellent start. We are adding customers, increasing margins, improving attrition and renewal rates, as well as reducing debt while building future value.

We want to thank the Just Energy team for their efforts during the quarter.

Yours sincerely,

| Deb Merril | James Lewis |

| Co-Chief Executive Officer | Co-Chief Executive Officer |