UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-22658 |

Nuveen Real Asset Income and Growth Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

31 December 2021

Nuveen Closed-End Funds

| | |

| JRS | | Nuveen Real Estate Income Fund |

| JRI | | Nuveen Real Asset Income and Growth Fund |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #2 or (ii) by logging into your Investor Center account at www.computershare.com/investor and clicking on “Communication Preferences”. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

IMPORTANT DISTRIBUTION NOTICE

for Shareholders of the Nuveen Real Estate Income Fund (JRS)

Annual Shareholder Report for the period ending December 31, 2021

The Nuveen Real Estate Income Fund (JRS) seeks to offer attractive cash flow to its shareholders, by converting the expected long-term total return potential of the Fund’s investments in REITs into regular quarterly distributions. Following is a discussion of the Managed Distribution Policy the Fund uses to achieve this.

The Fund pays quarterly common share distributions that seek to convert the Fund’s expected long-term total return potential into regular cash flow. As a result, the Fund’s regular common share distributions (presently $0.1900 per share) may be derived from a variety of sources, including:

| | • | | distributions from portfolio companies (REITs), |

| | • | | realized capital gains or, |

| | • | | possibly, returns of capital representing in certain cases unrealized capital appreciation. |

Such distributions are sometimes referred to as “managed distributions.” The Fund seeks to establish a distribution rate that roughly corresponds to the Adviser’s projections of the total return that could reasonably be expected to be generated by the Fund over an extended period of time. The Adviser may consider many factors when making such projections, including, but not limited to, long-term historical returns for the asset classes in which the Fund invests. As portfolio and market conditions change, the distribution amount and distribution rate on the Common Shares under the Fund’s Managed Distribution Policy could change.

When it pays a distribution, the Fund provides holders of its Common Shares a notice of the estimated sources of the Fund’s distributions (i.e., what percentage of the distributions is estimated to constitute ordinary income, short-term capital gains, long-term capital gains, and/or a non-taxable return of capital) on a year-to-date basis. It does this by posting the notice on its website (www.nuveen.com/cef), and by sending it in written form.

You should not draw any conclusions about the Fund’s investment performance from the amount of this distribution or from the terms of the Fund’s Managed Distribution Policy. The Fund’s actual financial performance will likely vary from month-to-month and from year-to-year, and there may be extended periods when the distribution rate will exceed the Fund’s actual total returns. The Managed Distribution Policy provides that the Board may amend or terminate the Policy at any time without prior notice to Fund shareholders. There are presently no reasonably foreseeable circumstances that might cause the Fund to terminate its Managed Distribution Policy.

Table of Contents

3

Chair’s Letter to Shareholders

Dear Shareholders,

We have seen a nearly full recovery in the economy and began to approach more normalcy in our daily lives, enabled by unprecedented help from governments and central banks and the development of effective COVID-19 vaccines and therapies.

As crisis-related monetary and fiscal supports are phasing out, global economic growth is expected to moderate from post-pandemic peak growth toward a more sustainable pace of expansion. In the U.S., the rapid rebound in the economy has pushed consumer prices higher, and ongoing supply chain disruptions have kept the inflation rate elevated for longer than expected. With the economy and employment on strong footing, the Federal Reserve is ending its pandemic bond buying program and will begin raising short-term interest rates in 2022 to help keep inflation in check. The Fed now faces the challenge of counteracting inflation pressures without stifling economic growth, which the markets will be watching closely. On the fiscal side, government spending will be lower from here, but the U.S. will begin funding projects with the $1.2 trillion Infrastructure Investment and Jobs Act enacted on November 15, 2021, and Europe, Japan and China are also expected to roll out fiscal support in 2022.

Inflation levels, the timing of monetary policy normalization and the global economy’s response to tighter financial conditions will be a key focus in the markets. We anticipate periodic volatility as markets digest incoming data on these impacts, as well as COVID-19 headlines, as there is still uncertainty about the course of the pandemic. Short-term market fluctuations can provide your Fund opportunities to invest in new ideas as well as upgrade existing positioning while providing long-term value for shareholders. For more than 120 years, the careful consideration of risk and reward has guided Nuveen’s focus on delivering long-term results to our shareholders.

To learn more about how your portfolio can take advantage of new opportunities arising from the normalizing global economy, we encourage you to review your time horizon, risk tolerance and investment goals with your financial professional.

On behalf of the other members of the Nuveen Fund Board, I look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chair of the Board

February 22, 2022

4

Portfolio Managers’ Comments

Nuveen Real Estate Income Fund (JRS)

Nuveen Real Asset Income and Growth Fund (JRI)

Nuveen Real Estate Income Fund (JRS) features portfolio management by a team of real estate investment professionals at Security Capital Research & Management Incorporated (Security Capital), a wholly-owned subsidiary of JPMorgan Chase & Company. Anthony R. Manno Jr., Kenneth D. Statz, Kevin W. Bedell and Nathan J. Gear, CFA, lead the team.

Nuveen Real Asset Income and Growth Fund (JRI) features portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Fund’s investment adviser. The Fund’s portfolio managers are Jay L. Rosenberg, Jean C. Lin, CFA, Brenda A. Langenfeld, CFA, Tryg T. Sarsland and Benjamin T. Kerl. Effective October 1, 2021, Benjamin T. Kerl joined the Nuveen Real Asset Income and Growth Fund (JRI) portfolio management team.

Here the Funds’ portfolio management teams review economic and financial market conditions, key investment strategies and the performance of the Funds for the twelve-month reporting period ended December 31, 2021. For more information on the Funds’ investment objectives and policies, please refer to the Shareholder Update section at the end of the report.

What factors affected the economy and financial markets during the twelve-month reporting period ended December 31, 2021?

The U.S. economic recovery remained on course over the twelve-month reporting period, despite setbacks from the COVID-19 virus and higher-than-expected inflation readings. Since the pandemic reached the U.S. in early 2020, the federal government has enacted $5.3 trillion in crisis-related aid and the U.S. Federal Reserve (Fed) has kept borrowing rates low for businesses and individuals and kept the credit system stable. These measures, along with increasing vaccinations and improved treatments, helped the economy to reopen and activity to rebound during 2021, despite additional COVID-19 surges caused by new, more contagious variants. U.S. gross domestic product (GDP) rose at an annualized 6.9% in the fourth quarter of 2021, accelerating from 2.3% in the third quarter when the delta variant weighed on economic activity, according to the Bureau of Economic Analysis “advance” estimate. Also according to the “advance” estimate, in 2021 overall, GDP grew 5.7%, rebounding from the contraction of -3.4% in 2020.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

The return of consumer demand to the economy put upward pressure on inflation in 2021. However, as supply chains remained under stress and labor shortages continued, in part because of resurgences of the virus around the world, inflation appeared to be more durable than initially expected. The Fed responded by reducing its pandemic-era support programs and signaled that rate increases were likely in 2022. Financial markets grew more concerned about the timing and size of these monetary policy shifts and their implications for the broader economic outlook, which led to short-term volatility in interest rates and stock prices. However, strong corporate earnings and a lessening economic impact from each subsequent wave of the virus supported a more optimistic view that ultimately drove stock prices and interest rates higher over 2021.

After underperforming for most of 2020, cyclical and value areas of the market, including real estate, enjoyed a resurgence of investor interest during 2021. Investors flocked to the real estate sector, which stood to benefit as more people received vaccinations and global mobility increased, driving higher utilization and occupancy rates. With the additional backdrop of rebounding U.S. economic growth and strong broader equity returns, the U.S. real estate investment trust (REIT) common equity segment generated near-record returns in 2021. Global REITs also performed well as investors returned to the previously out-of-favor sector segment in the first half of the reporting period, but the segment did not reach the same heights as U.S. REITs. Several challenges posed headwinds for global real estate in the second half of the reporting period, including higher interest rates in the U.S. and the Evergrande Group situation in China. China Evergrande Group, one of the country’s largest and most indebted residential real estate developers, defaulted on its bonds in December 2021, which impacted property across the pan-Asian region.

Global infrastructure equities also produced solid double-digit gains over the reporting period but underlying industry returns within the sector were fairly divergent. The highly cyclical pipeline industry was a top performer based on investor anticipation of a recovery in economic activity and increased demand for crude oil as people begin to travel again. Perpetual preferred securities saw spreads continue to normalize in 2021 from significant dislocation early during the COVID-19 crisis, posting modestly positive returns but lagging REIT equities. In the fixed income market, the high yield corporate sector performed well as spreads tightened. The segment benefited from a favorable backdrop that

included the economic rebound, low default rates, continued investor demand for higher yielding securities, strong corporate balance sheets and moderate net issuance supply.

Nuveen Real Estate Income Fund (JRS)

What key strategies were used to manage the Fund during the twelve-month reporting period ended December 31, 2021?

The Fund’s investment objective is high current income and capital appreciation. The Fund invests primarily in income-producing common stocks, preferred stocks, convertible preferred stocks and debt securities issued by real estate companies. At least 75% of the Fund’s managed assets will be in securities rated investment grade. The Fund uses leverage. Leverage is discussed in more detail later in the Fund Leverage Section of this report.

During the reporting period, Security Capital sought to maintain significant property type and geographic diversification while taking into account company credit quality, sector, and security-type allocations. Investment decisions were based on a multi-layered analysis of the company, the real estate it owns, its management and the relative price of the security, with a focus on securities that Security Capital believes will be best positioned to generate sustainable income and potential price appreciation over the long run. In addition to fundamental security research, the proportion of the Fund invested in common equity versus preferred, fixed income and cash investments is a key tactic Security Capital used to manage risk at the portfolio level.

How did the Fund perform during the twelve-month reporting period ended December 31, 2021?

For the twelve-month reporting period ended December 31, 2021, the Fund’s portfolio outperformed the JRS Blended

6

Benchmark. For the purposes of this Performance Commentary, references to relative performance are in comparison to the components of the JRS Blended Benchmark. Effective April 1, 2021, the JRS Blended Benchmark was updated to consist of: 60% Wilshire U.S. Real Estate Securities Index (WILRESI) and 40% FTSE Nareit Preferred Stock Index. Benchmark performance prior to April 1, 2021 reflects the JRS Blended Benchmark’s previous composition of: 60% Wilshire U.S. Real Estate Securities Index (WILRESI) and 40% Wells Fargo Hybrid & Preferred Securities REIT Index. These changes were made because of the decommissioning of the previously used Wells Fargo Hybrid & Preferred Securities REIT Index on March 31, 2021.

The main factors that contributed to the portfolio’s relative performance included an underweight in health care and security selection in self-storage and single-family rental. Pricing for health care companies continued to be weighed down in 2021 by the challenged operating environment for the senior living and skilled nursing segments, including depressed occupancy levels and staffing cost pressures. As a result, the portfolio’s underweight was a top contributor. Self-storage companies have outperformed during the COVID-19 crisis based on the segment’s diverse, recession-resistant demand as well as healthy balance sheets. While investors have been wary of active new supply, leasing activity in 2021 cemented some positive trends for self-storage occupancy and pricing as the transition and displacement realities of the work-from-anywhere economy have been increasingly evident in demand for self-storage. Single-family for rent fundamentals soared in 2021 as aging millennials drove demand for homes well above the supply constrained markets. Leading contributors also included an underweight in the portfolio’s health care sector holding Ventas, Inc. and investments in self-storage holding CubeSmart and single-family rental holding American Homes 4 Rent. The portfolio continues to hold these positions given the strong rent growth environment for the storage and single-family rental sectors.

The portfolio’s outperformance was partially offset by investments in the hotel sector. After a strong rebound in hotel stock pricing from COVID-19 pre-vaccine lows, investors in 2021 shifted focus to the operating pressures and uncertainties for urban, business-oriented hotels comprising a large segment of company portfolios. These issues include the extent and timing of the return of profitable business travel and international tourists, as well as margin pressure from staffing costs and availability. Host Hotels & Resorts, Inc. was the leading detractor in this sector. The Fund continues to hold the position. In the context of an improving fundamental environment, the Fund’s portfolio management team believes the current pricing of Host Hotels & Resorts, Inc. remains attractive.

Nuveen Real Asset Income and Growth Fund (JRI)

What key strategies were used to manage the Fund during the twelve-month reporting period ended December 31, 2021?

The Fund seeks to deliver a high level of current income and long-term capital appreciation by investing in real asset-related companies across the world and the capital structure, including common stocks, preferred securities, and debt. Real asset-related companies include those engaged in owning, operating, or developing infrastructure projects, facilities, and services, as well as real estate investment trust (REITs). The Fund uses leverage. Leverage is discussed in more detail later in the Fund Leverage Section of this report.

The Fund attempts to add value versus the comparative blended performance benchmark in two ways: by re-allocating among the five main security types when the investment team sees pockets of value at differing times and, more importantly, through individual security selection. COVID vaccine announcements in late 2020 provided the catalyst for rebalancing the Fund’s sector exposures, which continued throughout 2021. By the end of the reporting period, sector exposures were more closely aligned with what investors could expect under more normal market conditions.

Throughout the reporting period, the portfolio management team increased the Fund’s equity exposure, shifting from an underweight to an overweight relative to the blended benchmark. Pipelines within infrastructure equity represented the largest increase, an area that has been positively impacted by the economic recovery, higher commodity prices and

7

Portfolio Managers’ Comments (continued)

attractive valuations. Within real estate equity, the portfolio management team increased retail, net lease, office and gaming exposures to capitalize on the economic reopening theme. Industrial equities remained an area of focus for the Fund because the segment continued to demonstrate strong underlying fundamentals. The preferred securities and high yield debt segments served as sources of funds for the equity increases and ended the reporting period as underweights relative to the blended benchmark. Valuations were less attractive in these areas as spreads continued to narrow and yield characteristics in the equity universe became more attractive in relative terms. These segments also have higher sensitivity to changes in interest rates relative to the equity universe.

How did the Fund perform during the twelve-month reporting period ended December 31, 2021?

For the twelve-month reporting period ended December 31, 2021, the Fund’s portfolio outperformed the JRI Blended Benchmark. For the purposes of this Performance Commentary, references to relative performance are in comparison to the JRI Blended Benchmark. Effective April, 1, 2021, the JRI Blended Benchmark was updated to consist of: 1) 25% FTSE EPRA Nareit Developed Index (Net), 2) 22% S&P Global Infrastructure Index (Net), 3) 20% ICE Hybrid & Preferred Infrastructure 7% Issuer Constrained Custom Index, 4) 13% FTSE Nareit Preferred Stock Index and 5) 20% Bloomberg U.S. Corporate High Yield Bond Index. These changes were made because of the decommissioning of the previously used Wells Fargo Hybrid & Preferred Securities REIT Index on March 31, 2021, and to better reflect the securities held in the Fund and its actual and expected positioning.

During the reporting period, the Fund’s portfolio benefited from security selection within infrastructure equities, real estate preferred securities and infrastructure preferreds. Stock selection was favorable among infrastructure equities primarily led by the portfolio’s lack of exposure to airports, an overweight to electric transmission stocks and an underweight to toll roads. Although the airport group enjoyed a rebound in December 2021, overall it lagged for the reporting period as concerns around COVID-19 vaccination rates and the omicron variant weighed on transportation related stocks. This segment represents a material weight in the infrastructure index, while the portfolio typically contains limited or no exposure to airport stocks because of their lower dividend yields.

Within the portfolio’s real estate preferred exposure, an underweight to self-storage contributed to performance as preferred shares in that space dramatically underperformed their equity counterparts. The portfolio’s security selection in the infrastructure preferred category was also favorable, although an overweight to the sector offset some of the positive performance. The portfolio’s preference for institutional preferred securities and fixed-to-fixed or fixed-to-floating rate structures also aided performance. These securities typically exhibit lower interest rate sensitivity and were generally less impacted by rising interest rates.

Debt holdings within the Fund’s portfolio detracted modestly from relative performance. The portfolio’s overweight to utilities was the primary reason for the underperformance as the group fell short of many other areas that stand to benefit more from the anticipated economic recovery. Investors may have also been expecting further weakness from the utilities segment because of the potential for corporate tax hikes under the Biden administration, which could affect utilities more adversely relative to other higher growth sectors.

During the reporting period, the Fund continued to use interest rate futures to partially hedge the portfolio against movements in interest rates. The interest rate futures had a negligible impact on performance during the reporting period.

8

Fund Leverage

IMPACT OF THE FUNDS’ LEVERAGE STRAGEGY ON PERFORMANCE

One important factor impacting the returns of the Funds’ common shares relative to its comparative benchmarks was the Funds’ use of leverage through bank borrowings. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that the Fund pays on its leveraging instruments are lower than the interest the Fund earns on its portfolio securities that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value. All this will make the shares’ total return performance more variable over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term interest rates. While fund leverage expenses are somewhat higher than their recent lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

The Funds’ use of leverage had a positive impact on total return performance during this reporting period.

The Funds also continued to use interest rate swap contracts to partially hedge the interest cost of leverage. The impact of the swap contracts on total return performance was positive during this reporting period.

As of December 31, 2021, the Funds’ percentages of leverage are as shown in the accompanying table.

| | | | | | | | |

| | | JRS | | | JRI | |

Effective Leverage* | | | 27.39 | % | | | 29.29 | % |

Regulatory Leverage* | | | 27.39 | % | | | 29.29 | % |

| * | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in the Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

THE FUNDS’ REGULATORY LEVERAGE

Bank Borrowings

As noted previously, the Funds employ leverage through the use of bank borrowings. The Funds’ bank borrowing activities are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | Outstanding

Balance as of

January 1, 2021 | | | Draws | | | Paydowns | | | Outstanding

Balance as of

December 31, 2021 | | | Average

Balance

Outstanding | | | | | | Draws | | | Paydowns | | | Outstanding

Balance as of

February 25, 2022 | |

| JRS | | | $110,000,000 | | | | $34,000,000 | | | | $ — | | | | $144,000,000 | | | | $126,190,411 | | | | | | | | $ — | | | | $ — | | | | $144,000,000 | |

| JRI | | | $166,035,000 | | | | $31,900,000 | | | | $ — | | | | $197,935,000 | | | | $182,092,260 | | | | | | | | $ — | | | | $ — | | | | $197,935,000 | |

Refer to Notes to Financial Statements, Note 8 – Borrowing Arrangements for further details.

9

Common Share Information

JRS DISTRIBUTION INFORMATION

The following 19(a) Notice presents JRS’s most current distribution information as of November 30, 2021 as required by certain exempted regulatory relief the Fund has received.

Because the ultimate tax character of your distributions depends on the Fund’s performance for its entire fiscal year (which is the calendar year for the Fund) as well as certain fiscal year-end (FYE) tax adjustments, estimated distribution source information you receive with each distribution may differ from the tax information reported to you on your Fund’s IRS Form 1099 statement.

DISTRIBUTION INFORMATION – AS OF NOVEMBER 30, 2021

This notice provides shareholders with information regarding fund distributions, as required by current securities laws. You should not draw any conclusions about the Fund’s investment performance from the amount of this distribution or from the terms of the Fund’s Managed Distribution Policy.

The Fund may in certain periods distribute more than its income and net realized capital gains. In such instances, a portion of the distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund’s investment performance and should not be confused with “yield” or “income.”

The amounts and sources of distributions set forth below are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund’s investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. More details about the Fund’s distributions and the basis for these estimates are available on www.nuveen.com/cef.

The following table provides estimates of the Fund’s distribution sources, reflecting year-to-date cumulative experience through the latest month-end. The Fund attributes these estimates equally to each regular distribution throughout the year. Consequently, the estimated information shown below is for the current distribution, and also represents an updated estimate for all prior months in the year.

Data as of November 30, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Estimated Per Share Sources of Distribution1 | | | Estimated Percentage of the Distribution1 | |

| JRS (FYE 12/31) | | Per Share

Distribution | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital | |

Current Quarter | | | $0.1900 | | | | $0.0056 | | | | $0.0595 | | | | $0.1248 | | | | $0.0000 | | | | 3.0 | % | | | 31.3 | % | | | 65.7 | % | | | 0.0 | % |

Fiscal YTD | | | $0.7600 | | | | $0.0225 | | | | $0.2382 | | | | $0.4994 | | | | $0.0000 | | | | 3.0 | % | | | 31.3 | % | | | 65.7 | % | | | 0.0 | % |

| 1 | Net investment income (NII) is a projection through the end of the current calendar quarter using actual data through the stated month-end date above. Capital gain amounts are as of the stated date above. JRS owns REIT securities which attribute their distributions to various sources including NII, gains, and return of capital. The estimated per share sources above include an allocation of the NII based on prior year attributions which can be expected to differ from the actual final attributions for the current year. |

10

The following table provides information regarding JRS’ distributions and total return performance over various time periods. This information is intended to help you better understand whether returns for the specified time periods were sufficient to meet distributions.

Data as of November 30, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | Annualized | | | Cumulative | |

JRS (FYE 12/31)

Inception Date | | Quarterly

Distribution | | | Fiscal YTD

Distribution | | | Net Asset Value (NAV) | | | 5-Year

Return on NAV | | | Fiscal YTD

Dist Rate on NAV1 | | | Fiscal YTD

Return on NAV | | | Fiscal YTD

Dist Rate on NAV1 | |

Nov 2001 | | | $0.1900 | | | | $0.7600 | | | | $12.32 | | | | 10.34 | % | | | 6.17 | % | | | 34.48 | % | | | 6.17 | % |

| 1 | As a percentage of 11/30/21 NAV. |

DISTRIBUTION INFORMATION – AS OF DECEMBER 31, 2021

The following tables provide information regarding the Fund’s common share distributions and total return performance for the fiscal year ended December 31, 2021. This information is intended to help you better understand whether the Fund’s returns for the specified time period were sufficient to meet its distributions.

Data as of December 31, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Per Share Sources of Distribution | | | Percentage of the Distribution | |

| JRS (FYE 12/31) | | Per Share

Distribution | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital1 | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital1 | |

Fiscal YTD | | | $0.7600 | | | | $0.2039 | | | | $0.3979 | | | | $0.1582 | | | | $0.0000 | | | | 26.83% | | | | 52.35% | | | | 20.82% | | | | 0.00% | |

| | | | | | | | | | | | | | | | |

| | | | | | Annualized | |

| JRS (FYE 12/31) Inception Date | | Net Asset

Value (NAV) | | | 1-Year

Return on NAV | | | 5-Year

Return on NAV | | | Fiscal YTD

Dist Rate on NAV | |

Nov 2001 | | | $13.22 | | | | 46.38% | | | | 11.33% | | | | 5.75% | |

| 1 | Return of Capital may represent unrealized gains, return of shareholder’s principal, or both. In certain circumstances, all or a portion of the return of capital may be characterized as ordinary income under federal tax law. The actual tax characterization will be provided to shareholders on Form 1099-DIV shortly after calendar year-end. |

JRI’s DISTRIBUTION INFORMATION

The following information regarding the Fund’s distributions is current as of December 31, 2021, the Fund’s fiscal and tax year end, and may differ from previously issued distribution notifications. This notice provides shareholders with information regarding Fund distributions, as required by current securities laws. You should not draw any conclusions about the Fund’s investment performance from the amount of the distribution or from the terms of the Fund’s Managed Distribution Policy.

The Fund may in certain periods distribute more than its income and net realized capital gains, and the Fund currently estimates that it has done so for the fiscal year-to-date period. In such instances, a portion of the distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund’s investment performance and should not be confused with “yield” or “income.”

The amounts and sources of distributions reported in this notice are for financial reporting purposes and are not being provided for tax reporting purposes. The actual amounts and character of the distributions for tax reporting purposes will be reported to shareholders on Form 1099-DIV which will be sent to shareholders shortly after calendar year-end. More details about the Fund’s distributions and the basis for these estimates are available on www.nuveen.com/cef.

11

Common Share Information (continued)

The following tables provide information regarding the Fund’s common share distributions and total return performance for the fiscal year ended December 31, 2021. This information is intended to help you better understand whether the Funds’ returns for the specified time period were sufficient to meet its distributions.

Data as of December 31, 2021

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Per Share Sources of Distribution | | | | | | Percentage of the Distribution | |

| JRI (FYE 12/31) | | Per Share

Distribution | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital1 | | | | | | Net

Investment

Income | | | Long-Term

Gains | | | Short-Term

Gains | | | Return of

Capital1 | |

Fiscal YTD | | $ | 1.1580 | | | $ | 1.0889 | | | $ | 0.0000 | | | $ | 0.0000 | | | $ | 0.0691 | | | | | | | | 94.03 | % | | | 0.00 | % | | | 0.00 | % | | | 5.97 | % |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Annualized | |

| JRI (FYE 12/31) Inception Date | | Net Asset

Value (NAV) | | | | | | 1-Year

Return on NAV | | | 5-Year

Return on NAV | | | Fiscal YTD

Dist Rate on NAV | |

Apr 2012 | | $ | 17.41 | | | | | | | | 17.73 | % | | | 6.54 | % | | | 6.65 | % |

| 1 | Return of Capital may represent unrealized gains, return of shareholder’s principal, or both. In certain circumstances, all or a portion of the return of capital may be characterized as ordinary income under federal tax law. The actual tax characterization will be provided to shareholders on Form 1099-DIV shortly after calendar year-end. |

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closed-end-funds, along with other Nuveen closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE REPURCHASES

During August 2021, the Funds’ Board of Trustees reauthorized an open-market share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding common shares.

As of December 31, 2021, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired common shares as shown in the accompanying table.

| | | | | | | | |

| | | JRS | | | JRI | |

Common shares cumulatively repurchased and retired | | | 0 | | | | 206,500 | |

Common shares authorized for repurchase | | | 2,885,000 | | | | 2,745,000 | |

During the current reporting period, the Funds did not repurchase any of their outstanding common shares.

OTHER COMMON SHARE INFORMATION

As of December 31, 2021, the Funds’ common share prices were trading at a premium/(discount) to their common share NAVs and trading at an average premium/(discount) to NAV during the current reporting period, as follows.

| | | | | | | | |

| | | JRS | | | JRI | |

Common share NAV | | $ | 13.22 | | | $ | 17.41 | |

Common share price | | $ | 12.82 | | | $ | 16.12 | |

Premium/(Discount) to NAV | | | (3.03 | )% | | | (7.41 | )% |

Average premium/(discount) to NAV | | | (7.65 | )% | | | (8.91 | )% |

12

THIS PAGE INTENTIONALLY LEFT BLANK

13

| | |

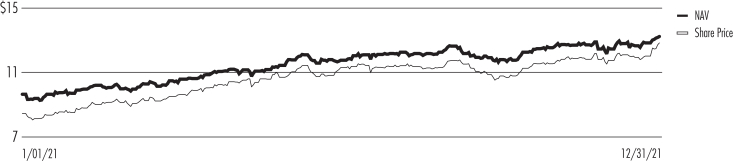

| JRS | | Nuveen Real Estate Income Fund Performance Overview and Holding Summaries as of December 31, 2021 |

Refer to the Glossary of Terms Used in this Report for further definitions of terms used in this section.

Average Annual Total Returns as of December 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JRS at Common Share NAV | | | 46.38% | | | | 11.33% | | | | 11.89% | |

| JRS at Common Share Price | | | 62.73% | | | | 12.56% | | | | 11.07% | |

| Wilshire U.S. Real Estate Securities Index (WILRESI) | | | 46.11% | | | | 11.05% | | | | 11.64% | |

| JRS Blended Benchmark1,2 | | | 29.21% | | | | 9.57% | | | | 9.94% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of December 31, 2021 – Common Share Price

| 1 | For purposes of Fund performance, relative results are measured against this benchmark/index. |

| 2 | JRS Blended Benchmark consists of: Effective April 1, 2021, and thereafter: 1) 60% Wilshire U.S. Real Estate Securities Index (WILRESI) and 2) 40% FTSE Nareit Preferred Stock Index. Prior to April 1, 2021: 1) 60% Wilshire U.S. Real Estate Securities Index (WILRESI) and 2) 40% Wells Fargo Hybrid & Preferred Securities REIT Index (index was discontinued on April 1, 2021). Refer to the Glossary of Terms Used in This Report for further details on the Fund’s Blended Benchmark compositions. |

14

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Real Estate Investment Trust Common Stocks | | | 90.8% | |

| Real Estate Investment Trust Preferred Stocks | | | 36.8% | |

| Corporate Bonds | | | 4.6% | |

| Repurchase Agreements | | | 6.1% | |

| Other Assets Less Liabilities | | | (0.6)% | |

Net Assets Plus Borrowings | | | 137.7% | |

| Borrowings | | | (37.7)% | |

Net Assets | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed-income securities)

| | | | |

| A | | | 17.8% | |

| BBB | | | 52.6% | |

| BB or Lower | | | 12.6% | |

| N/R (not rated) | | | 17.0% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Specialized | | | 21.1% | |

| Residential | | | 18.4% | |

| Office | | | 15.5% | |

| Industrial | | | 13.1% | |

| Retail | | | 12.8% | |

| Hotels | | | 5.0% | |

| Other1 | | | 9.7% | |

| Repurchase Agreements | | | 4.4% | |

Total | | | 100% | |

Top Five Common Stock Holdings

(% of total investments)

| | | | |

| Prologis Inc | | | 8.1% | |

| Public Storage | | | 4.3% | |

| Digital Realty Trust Inc | | | 3.6% | |

| Equinix Inc | | | 3.5% | |

| Equity Residential | | | 3.4% | |

Top Five Preferred Stock Issuers

(% of total investments)

| | | | |

| Public Storage | | | 4.9% | |

| Highwoods Properties Inc | | | 3.0% | |

| Vornado Realty Trust | | | 2.9% | |

| Kimco Realty Corp | | | 1.7% | |

| Digital Realty Trust Inc | | | 1.3% | |

| 1 | See the Portfolio of Investments for the remaining industries comprising “Other” and not listed in the Portfolio Composition above. |

15

| | |

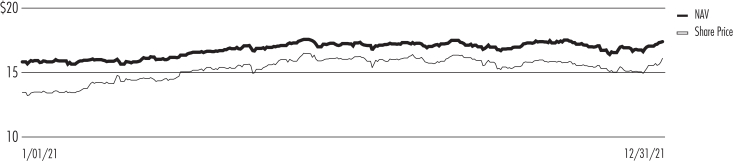

| JRI | | Nuveen Real Asset Income and Growth Fund Performance Overview and Holding Summaries as of December 31, 2021 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

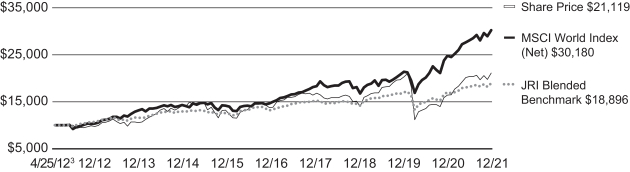

Average Annual Total Returns as of December 31, 2021

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | Since

Inception | |

| JRI at Common Share NAV | | | 17.73% | | | | 6.54% | | | | 8.39% | |

| JRI at Common Share Price | | | 29.09% | | | | 8.86% | | | | 8.02% | |

| MSCI World Index (Net) | | | 21.82% | | | | 15.03% | | | | 12.08% | |

| JRI Blended Benchmark1,2 | | | 11.23% | | | | 7.32% | | | | 6.91% | |

Since inception returns are from 4/25/12. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of December 31, 2021 – Common Share Price

| 1 | For purposes of Fund performance, relative results are measured against this benchmark/index. |

| 2 | JRI Blended Benchmark consists of: Effective April 1, 2021, and thereafter: 1) 25% FTSE EPRA Nareit Developed Index (Net), 2) 22% S&P Global Infrastructure Index (Net), 3) 20% ICE Hybrid & Preferred Infrastructure 7% Issuer Constrained Custom Index, 4) 20% Bloomberg U.S. Corporate High Yield Bond Index and 5) 13% FTSE Nareit Preferred Stock Index. Prior to April 1, 2021: 1) 28% S&P Global Infrastructure Index (Net), 2) 21% FTSE EPRA Nareit Developed Index (Net), 3) 18% Wells Fargo Hybrid & Preferred Securities REIT Index (index was discontinued on April 1, 2021), 4) 18% Bloomberg U.S. Corporate High Yield Bond Index and 5) 15% Bloomberg Global Capital Securities Index. Refer to the Glossary of Terms Used in This Report for further details on the Fund’s Blended Benchmark compositions. |

| 3 | Value on 4/25/12 is $19.10, which represents the Fund’s public offering price less sales load. |

16

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Real Estate Investment Trust Common Stocks | | | 37.2% | |

| Common Stocks | | | 37.1% | |

| Corporate Bonds | | | 20.2% | |

| $25 Par (or similar) Retail Preferred | | | 17.5% | |

| $1,000 Par (or similar) Institutional Preferred | | | 13.5% | |

| Convertible Preferred Securities | | | 8.9% | |

| Investment Companies | | | 1.2% | |

| Variable Rate Senior Loan Interests | | | 0.6% | |

| Convertible Bonds | | | 0.6% | |

| Mortgage-Backed Securities | | | 0.3% | |

| Repurchase Agreements | | | 4.4% | |

| Other Assets Less Liabilities | | | (0.1)% | |

Net Assets Plus Borrowings | | | 141.4% | |

| Borrowings | | | (41.4)% | |

Net Assets | | | 100% | |

Top Five Common Stock Holdings

(% of total common stocks)

| | | | |

| Williams Cos Inc | | | 6.8% | |

| Enbridge Inc | | | 4.9% | |

| SSE PLC | | | 4.5% | |

| Enel SpA | | | 3.6% | |

| National Grid PLC, ADR | | | 3.3% | |

Portfolio Composition

(% of total investments)

| | | | |

Real Estate Investment Trust Common Stocks | | | 26.3% | |

| Electric Utilities | | | 13.8% | |

| Oil, Gas & Consumable Fuels | | | 13.7% | |

| Equity Real Estate Investment Trust | | | 10.2% | |

| Multi-Utilities | | | 8.6% | |

| Gas Utilities | | | 3.7% | |

| Real Estate Management & Development | | | 3.6% | |

| Independent Power & Renewable Electricity Producers | | | 2.9% | |

| Diversified Telecommunication Services | | | 2.2% | |

| Other1 | | | 11.9% | |

| Repurchase Agreements | | | 3.1% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total fixed-income investments)

| | | | |

| AAA | | | 0.3% | |

| AA | | | 0.1% | |

| A | | | 3.1% | |

| BBB | | | 46.1% | |

| BB or Lower | | | 37.3% | |

| N/R (not rated) | | | 13.1% | |

Total | | | 100% | |

Country Allocation2

(% of total investments)

| | | | |

| United States | | | 54.9% | |

| Canada | | | 14.2% | |

| United Kingdom | | | 5.1% | |

| Australia | | | 4.2% | |

| Italy | | | 3.3% | |

| Singapore | | | 3.0% | |

| France | | | 2.3% | |

| Spain | | | 2.3% | |

| Hong Kong | | | 1.8% | |

| Japan | | | 1.0% | |

| Other | | | 7.9% | |

Total | | | 100% | |

| 1 | See the Portfolio of Investments for the remaining industries comprising “Other” and not listed in the Portfolio Composition above. |

| 2 | Includes 4.8% (as a percentage of total investments) in emerging markets countries. |

17

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees

Nuveen Real Estate Income Fund

Nuveen Real Asset Income and Growth Fund:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Real Estate Income Fund and Nuveen Real Asset Income and Growth Fund (the Funds), including the portfolios of investments, as of December 31, 2021, the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the five-year period then ended. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of December 31, 2021, the results of their operations and cash flows for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of December 31, 2021, by correspondence with custodians and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

February 28, 2022

18

| | |

| JRS | | Nuveen Real Estate Income Fund Portfolio of Investments December 31, 2021 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | LONG-TERM INVESTMENTS – 132.2% (95.6% of Total Investments) | | | | | | | | | | | | | | | | |

| | | |

| | | | REAL ESTATE INVESTMENT TRUST COMMON STOCKS – 90.8% (65.7% of Total Investments) | | | | | | | | | |

| | | | | |

| | | | Health Care – 6.5% (4.7% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 335,638 | | | Healthpeak Properties Inc | | | | | | | | | | | | | | $ | 12,113,175 | |

| | 115,520 | | | Ventas Inc | | | | | | | | | | | | | | | 5,905,382 | |

| | 78,511 | | | Welltower Inc | | | | | | | | | | | | | | | 6,733,889 | |

| | | | Total Health Care | | | | | | | | | | | | | | | 24,752,446 | |

| | | | | |

| | | | Hotels – 3.3% (2.4% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 424,396 | | | Host Hotels & Resorts Inc, (2) | | | | | | | | | | | | | | | 7,380,247 | |

| | 288,882 | | | Xenia Hotels & Resorts Inc, (2) | | | | | | | | | | | | | | | 5,231,653 | |

| | | | Total Hotels | | | | | | | | | | | | | | | 12,611,900 | |

| | | | | |

| | | | Industrial – 15.3% (11.1% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 161,532 | | | First Industrial Realty Trust Inc | | | | | | | | | | | | | | | 10,693,419 | |

| | 333,615 | | | LXP Industrial Trust | | | | | | | | | | | | | | | 5,211,066 | |

| | 253,191 | | | Prologis Inc | | | | | | | | | | | | | | | 42,627,237 | |

| | | | Total Industrial | | | | | | | | | | | | | | | 58,531,722 | |

| | | | | |

| | | | Office – 11.5% (8.3% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 71,339 | | | Alexandria Real Estate Equities Inc | | | | | | | | | | | | | | | 15,905,743 | |

| | 38,778 | | | Boston Properties Inc | | | | | | | | | | | | | | | 4,466,450 | |

| | 382,050 | | | Brandywine Realty Trust | | | | | | | | | | | | | | | 5,127,111 | |

| | 231,298 | | | Douglas Emmett Inc | | | | | | | | | | | | | | | 7,748,483 | |

| | 263,263 | | | Hudson Pacific Properties Inc | | | | | | | | | | | | | | | 6,505,229 | |

| | 35,808 | | | SL Green Realty Corp | | | | | | | | | | | | | | | 2,567,433 | |

| | 85,778 | | | Veris Residential Inc, (2) | | | | | | | | | | | | | | | 1,576,600 | |

| | | | Total Office | | | | | | | | | | | | | | | 43,897,049 | |

| | | | | |

| | | | Residential – 23.0% (16.7% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 320,972 | | | American Homes 4 Rent, Class A | | | | | | | | | | | | | | | 13,997,589 | |

| | 83,567 | | | Apartment Income REIT Corp | | | | | | | | | | | | | | | 4,568,608 | |

| | 67,117 | | | AvalonBay Communities Inc, (3) | | | | | | | | | | | | | | | 16,953,083 | |

| | 64,394 | | | Camden Property Trust | | | | | | | | | | | | | | | 11,505,920 | |

| | 50,791 | | | Equity LifeStyle Properties Inc | | | | | | | | | | | | | | | 4,452,339 | |

| | 201,129 | | | Equity Residential | | | | | | | | | | | | | | | 18,202,174 | |

| | 223,200 | | | Invitation Homes Inc | | | | | | | | | | | | | | | 10,119,888 | |

| | 133,187 | | | Tricon Residential Inc | | | | | | | | | | | | | | | 2,035,097 | |

| | 100,725 | | | UDR Inc | | | | | | | | | | | | | | | 6,042,493 | |

| | | | Total Residential | | | | | | | | | | | | | | | 87,877,191 | |

| | | | | |

| | | | Retail – 11.0% (7.9% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 71,745 | | | Brixmor Property Group Inc | | | | | | | | | | | | | | | 1,823,040 | |

| | 76,350 | | | Federal Realty Investment Trust | | | | | | | | | | | | | | | 10,408,032 | |

| | 438,651 | | | Kite Realty Group Trust | | | | | | | | | | | | | | | 9,553,819 | |

| | 425,868 | | | Macerich Co | | | | | | | | | | | | | | | 7,358,999 | |

| | 79,804 | | | Simon Property Group Inc | | | | | | | | | | | | | | | 12,750,285 | |

| | | | Total Retail | | | | | | | | | | | | | | | 41,894,175 | |

| | | | | |

| | | | Specialized – 20.2% (14.6% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 207,502 | | | CubeSmart | | | | | | | | | | | | | | | 11,808,939 | |

| | 106,954 | | | Digital Realty Trust Inc | | | | | | | | | | | | | | | 18,916,954 | |

| | 21,910 | | | Equinix Inc | | | | | | | | | | | | | | | 18,532,354 | |

| | 22,421 | | | Life Storage Inc | | | | | | | | | | | | | | | 3,434,449 | |

| | 60,370 | | | Public Storage | | | | | | | | | | | | | | | 22,612,187 | |

| | 60,795 | | | VICI Properties Inc | | | | | | | | | | | | | | | 1,830,538 | |

| | | | Total Specialized | | | | | | | | | | | | | | | 77,135,421 | |

| | | | Total Real Estate Investment Trust Common Stocks (cost $220,567,772) | | | | | | | | | | | | | | | 346,699,904 | |

19

| | |

| |

| JRS | | Nuveen Real Estate Income Fund (continued) |

| | Portfolio of Investments December 31, 2021 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | Coupon | | | | | | Ratings (4) | | | Value | |

| | | |

| | | | REAL ESTATE INVESTMENT TRUST PREFERRED STOCKS – 36.8% (26.6% of Total Investments) | | | | | | | | | |

| | | | | |

| | | | Diversified – 2.2% (1.6% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 35,010 | | | Armada Hoffler Properties Inc | | | 6.750% | | | | | | | | N/R | | | $ | 942,480 | |

| | 10,130 | | | CTO Realty Growth Inc | | | 6.375% | | | | | | | | N/R | | | | 266,419 | |

| | 43,965 | | | DigitalBridge Group Inc | | | 7.125% | | | | | | | | N/R | | | | 1,158,917 | |

| | 35,015 | | | DigitalBridge Group Inc | | | 7.150% | | | | | | | | N/R | | | | 914,241 | |

| | 7,350 | | | PS Business Parks Inc | | | 4.875% | | | | | | | | BBB | | | | 198,891 | |

| | 120,575 | | | PS Business Parks Inc | | | 5.200% | | | | | | | | BBB | | | | 3,145,802 | |

| | 74,625 | | | PS Business Parks Inc | | | 5.250% | | | | | | | | BBB | | | | 1,924,579 | |

| | | | Total Diversified | | | | | | | | | | | | | | | 8,551,329 | |

| | | | | |

| | | | Health Care – 0.2% (0.1% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 5,765 | | | Diversified Healthcare Trust | | | 5.625% | | | | | | | | BB– | | | | 127,349 | |

| | 28,875 | | | Diversified Healthcare Trust | | | 6.250% | | | | | | | | BB– | | | | 654,019 | |

| | | | Total Health Care | | | | | | | | | | | | | | | 781,368 | |

| | | | | |

| | | | Hotels – 3.6% (2.6% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 95,245 | | | Chatham Lodging Trust | | | 6.625% | | | | | | | | N/R | | | | 2,524,945 | |

| | 132,110 | | | DiamondRock Hospitality Co | | | 8.250% | | | | | | | | N/R | | | | 3,687,190 | |

| | 6,460 | | | Hersha Hospitality Trust | | | 6.500% | | | | | | | | N/R | | | | 147,934 | |

| | 9,075 | | | Hersha Hospitality Trust | | | 6.500% | | | | | | | | N/R | | | | 209,360 | |

| | 57,425 | | | Hersha Hospitality Trust | | | 6.875% | | | | | | | | N/R | | | | 1,354,656 | |

| | 52,750 | | | Pebblebrook Hotel Trust | | | 5.700% | | | | | | | | N/R | | | | 1,297,650 | |

| | 22,025 | | | Pebblebrook Hotel Trust | | | 6.300% | | | | | | | | N/R | | | | 556,792 | |

| | 88,755 | | | Pebblebrook Hotel Trust | | | 6.375% | | | | | | | | N/R | | | | 2,330,706 | |

| | 30,100 | | | Sunstone Hotel Investors Inc | | | 5.700% | | | | | | | | N/R | | | | 755,660 | |

| | 28,325 | | | Sunstone Hotel Investors Inc | | | 6.125% | | | | | | | | N/R | | | | 724,554 | |

| | | | Total Hotels | | | | | | | | | | | | | | | 13,589,447 | |

| | | | | |

| | | | Industrial – 2.7% (2.0% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 32,985 | | | Monmouth Real Estate Investment Corp | | | 6.125% | | | | | | | | N/R | | | | 832,541 | |

| | 10,115 | | | Plymouth Industrial REIT Inc | | | 7.500% | | | | | | | | N/R | | | | 268,048 | |

| | 59,877 | | | Prologis Inc, (5) | | | 8.540% | | | | | | | | BBB | | | | 3,664,473 | |

| | 160,295 | | | Rexford Industrial Realty Inc | | | 5.625% | | | | | | | | BB+ | | | | 4,196,523 | |

| | 57,851 | | | Rexford Industrial Realty Inc | | | 5.875% | | | | | | | | BB+ | | | | 1,504,126 | |

| | | | Total Industrial | | | | | | | | | | | | | | | 10,465,711 | |

| | | | | |

| | | | Office – 9.9% (7.2% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 12,713 | | | Highwoods Properties Inc, (5) | | | 8.625% | | | | | | | | Baa3 | | | | 15,891,250 | |

| | 102,450 | | | Hudson Pacific Properties Inc, (2) | | | 4.750% | | | | | | | | Baa3 | | | | 2,672,920 | |

| | 152,510 | | | SL Green Realty Corp | | | 6.500% | | | | | | | | Ba1 | | | | 4,023,214 | |

| | 102,200 | | | Vornado Realty Trust | | | 4.450% | | | | | | | | Baa3 | | | | 2,524,340 | |

| | 177,244 | | | Vornado Realty Trust | | | 5.250% | | | | | | | | Baa3 | | | | 4,530,357 | |

| | 232,045 | | | Vornado Realty Trust | | | 5.250% | | | | | | | | Baa3 | | | | 6,146,872 | |

| | 83,219 | | | Vornado Realty Trust | | | 5.400% | | | | | | | | Baa3 | | | | 2,097,119 | |

| | | | Total Office | | | | | | | | | | | | | | | 37,886,072 | |

| | | | | |

| | | | Residential – 2.4% (1.7% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 40,730 | | | American Homes 4 Rent | | | 5.875% | | | | | | | | BB | | | | 1,071,199 | |

| | 65,105 | | | American Homes 4 Rent | | | 5.875% | | | | | | | | BB | | | | 1,668,641 | |

| | 117,810 | | | American Homes 4 Rent | | | 6.250% | | | | | | | | Ba1 | | | | 3,186,761 | |

| | 34,373 | | | Mid-America Apartment Communities Inc | | | 8.500% | | | | | | | | BBB– | | | | 2,166,874 | |

| | 12,330 | | | UMH Properties Inc | | | 6.375% | | | | | | | | N/R | | | | 320,333 | |

| | 23,603 | | | UMH Properties Inc | | | 6.750% | | | | | | | | N/R | | | | 614,622 | |

| | | | Total Residential | | | | | | | | | | | | | | | 9,028,430 | |

| | | | | |

| | | | Retail – 6.8% (4.9% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 99,995 | | | Agree Realty Corp | | | 4.250% | | | | | | | | Baa3 | | | | 2,371,881 | |

| | 147,810 | | | Federal Realty Investment Trust | | | 5.000% | | | | | | | | BBB | | | | 3,761,764 | |

| | 162,207 | | | Kimco Realty Corp | | | 5.125% | | | | | | | | Baa2 | | | | 4,142,767 | |

| | 187,728 | | | Kimco Realty Corp | | | 5.250% | | | | | | | | Baa2 | | | | 4,894,069 | |

| | 129,000 | | | Saul Centers Inc | | | 6.000% | | | | | | | | N/R | | | | 3,543,630 | |

| | 4,870 | | | Saul Centers Inc | | | 6.125% | | | | | | | | N/R | | | | 126,620 | |

| | 5,494 | | | Simon Property Group Inc | | | 8.375% | | | | | | | | BBB | | | | 379,141 | |

20

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | Coupon | | | | | | Ratings (4) | | | Value | |

| | | | | |

| | | | Retail (continued) | | | | | | | | | | | | |

| | | | | |

| | 116,200 | | | SITE Centers Corp | | | 6.375% | | | | | | | | BB+ | | | $ | 2,989,826 | |

| | 22,845 | | | Spirit Realty Capital Inc | | | 6.000% | | | | | | | | Baa3 | | | | 587,573 | |

| | 53,645 | | | Urstadt Biddle Properties Inc | | | 5.875% | | | | | | | | N/R | | | | 1,371,703 | |

| | 60,825 | | | Urstadt Biddle Properties Inc | | | 6.250% | | | | | | | | N/R | | | | 1,571,110 | |

| | | | Total Retail | | | | | | | | | | | | | | | 25,740,084 | |

| | | | | |

| | | | Specialized – 9.0% (6.5% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | 86,400 | | | Digital Realty Trust Inc | | | 5.200% | | | | | | | | Baa3 | | | | 2,313,792 | |

| | 94,925 | | | Digital Realty Trust Inc | | | 5.250% | | | | | | | | Baa3 | | | | 2,471,847 | |

| | 73,860 | | | Digital Realty Trust Inc | | | 5.850% | | | | | | | | Baa3 | | | | 2,033,366 | |

| | 21,150 | | | EPR Properties | | | 5.750% | | | | | | | | Ba1 | | | | 534,249 | |

| | 51,191 | | | National Storage Affiliates Trust | | | 6.000% | | | | | | | | N/R | | | | 1,332,502 | |

| | 33,800 | | | Public Storage | | | 3.875% | | | | | | | | A3 | | | | 851,760 | |

| | 9,735 | | | Public Storage | | | 3.900% | | | | | | | | A3 | | | | 244,348 | |

| | 100,000 | | | Public Storage | | | 4.000% | | | | | | | | A3 | | | | 2,509,000 | |

| | 30,525 | | | Public Storage, (2) | | | 4.000% | | | | | | | | A3 | | | | 764,041 | |

| | 75,615 | | | Public Storage | | | 4.125% | | | | | | | | A3 | | | | 1,910,791 | |

| | 79,525 | | | Public Storage | | | 4.625% | | | | | | | | A3 | | | | 2,129,679 | |

| | 21,030 | | | Public Storage | | | 4.700% | | | | | | | | A3 | | | | 555,613 | |

| | 25,629 | | | Public Storage | | | 4.750% | | | | | | | | A3 | | | | 675,068 | |

| | 80,955 | | | Public Storage | | | 4.875% | | | | | | | | A3 | | | | 2,164,737 | |

| | 147,424 | | | Public Storage | | | 5.050% | | | | | | | | A3 | | | | 3,782,900 | |

| | 375,335 | | | Public Storage | | | 5.600% | | | | | | | | A3 | | | | 10,201,605 | |

| | | | Total Specialized | | | | | | | | | | | | | | | 34,475,298 | |

| | | | Total Real Estate Investment Trust Preferred Stocks (cost $135,767,325) | | | | | | | | 140,517,739 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (4) | | | Value | |

| | | | | |

| | | | CORPORATE BONDS – 4.6% (3.3% of Total Investments) | | | | | | | | | | | | | | | | |

| | | | |

| | | | Equity Real Estate Investment Trust – 4.6% (3.3% of Total Investments) | | | | | | | | | | |

| | | | | |

| $ | 2,622 | | | Boston Properties LP | | | 3.650% | | | | 2/01/26 | | | | BBB+ | | | $ | 2,808,926 | |

| | 1,911 | | | Equinix Inc | | | 1.000% | | | | 9/15/25 | | | | BBB | | | | 1,853,668 | |

| | 1,514 | | | Kimco Realty Corp | | | 2.800% | | | | 10/01/26 | | | | BBB+ | | | | 1,573,616 | |

| | 2,282 | | | Realty Income Corp | | | 3.000% | | | | 1/15/27 | | | | A– | | | | 2,407,363 | |

| | 1,984 | | | Regency Centers LP | | | 2.950% | | | | 9/15/29 | | | | BBB+ | | | | 2,058,608 | |

| | 1,824 | | | Ventas Realty LP | | | 3.250% | | | | 10/15/26 | | | | BBB+ | | | | 1,931,502 | |

| | 1,466 | | | Vornado Realty LP | | | 2.150% | | | | 6/01/26 | | | | Baa2 | | | | 1,464,910 | |

| | 3,127 | | | Welltower Inc | | | 4.250% | | | | 4/01/26 | | | | BBB+ | | | | 3,425,504 | |

| $ | 16,730 | | | Total Corporate Bonds (cost $17,653,879) | | | | | | | | | | | | | | | 17,524,097 | |

| | | | Total Long-Term Investments (cost $373,988,976) | | | | | | | | | | | | | | | 504,741,740 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | | | | Value | |

| | | | | |

| | | | SHORT-TERM INVESTMENTS – 6.1% (4.4% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | | | REPURCHASE AGREEMENTS – 6.1% (4.4% of Total Investments) | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 23,298 | | | Repurchase Agreement with Fixed Income Clearing Corporation, dated 12/31/21, repurchase price $23,297,885, collateralized by $23,923,700, U.S. Treasury Bonds, 1.875%, due 2/15/41, value $23,763,896 | | | 0.000% | | | | 1/03/22 | | | | | | | $ | 23,297,885 | |

| | | | Total Short-Term Investments (cost $23,297,885) | | | | | | | | | | | | | | | 23,297,885 | |

| | | | Total Investments (cost $397,286,861) – 138.3% | | | | | | | | | | | | | | | 528,039,625 | |

| | | | Borrowings – (37.7)% (6), (7) | | | | | | | | | | | | | | | (144,000,000 | ) |

| | | | Other Assets Less Liabilities – (0.6)% (8) | | | | | | | | | | | | | | | (2,224,882 | ) |

| | | | Net Assets Applicable to Common Shares – 100% | | | | | | | | | | | | | | $ | 381,814,743 | |

21

| | |

| |

| JRS | | Nuveen Real Estate Income Fund (continued) |

| | Portfolio of Investments December 31, 2021 |

Investments in Derivatives

Interest Rate Swaps – OTC Uncleared

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Notional

Amount | | | Fund

Pay/Receive

Floating Rate | | | Floating Rate Index | | | Fixed Rate

(Annualized) | | | Fixed Rate

Payment

Frequency | | | Effective

Date (9) | | | Optional

Termination

Date | | | Maturity

Date | | | Value | | | Unrealized

Appreciation

(Depreciation) | |

Morgan Stanley Capital Services LLC | | $ | 72,400,000 | | | | Receive | | | | 1-Month LIBOR | | | | 1.994 | % | | | Monthly | | | | 6/01/18 | | | | 7/01/25 | | | | 7/01/27 | | | $ | (3,509,484 | ) | | $ | (3,509,484 | ) |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets applicable to common shares unless otherwise noted. |

| (2) | Non-income producing; issuer has not declared an ex-dividend date within the past twelve months. |

| (3) | Investment, or portion of investment, has been pledged to collateralize the net payment obligations for investments in derivatives. |

| (4) | For financial reporting purposes, the ratings disclosed are the highest of Standard & Poor’s Group (“Standard & Poor’s”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch, Inc. (“Fitch”) rating. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Ratings below BBB by Standard & Poor’s, Baa by Moody’s or BBB by Fitch are considered to be below investment grade. Holdings designated N/R are not rated by any of these national rating agencies. Ratings are not covered by the report of independent registered public accounting firm. |

| (5) | For fair value measurement disclosure purposes, investment classified as Level 2. |

| (6) | Borrowings as a percentage of Total Investments is 27.3%. |

| (7) | The Fund may pledge up to 100% of its eligible investments (excluding any investments separately pledged as collateral for specific investments in derivatives, when applicable) in the Portfolio of Investments as collateral for borrowings. As of the end of the reporting period investments with a value of $302,312,573 have been pledged as collateral for borrowings. |

| (8) | Other assets less liabilities includes the unrealized appreciation (depreciation) of certain over-the-counter (“OTC”) derivatives as presented on the Statement of Assets and Liabilities, when applicable. The unrealized appreciation (depreciation) of OTC cleared and exchange-traded derivatives is recognized as part of the cash collateral at brokers and/or the receivable or payable for variation margin as presented on the Statement of Assets and Liabilities, when applicable. |

| (9) | Effective date represents the date on which both the Fund and counterparty commence interest payment accruals on each contract. |

| LIBOR | London Inter-Bank Offered Rate |

| REIT | Real Estate Investment Trust |

See accompanying notes to financial statements.

22

| | |

| JRI | | Nuveen Real Asset Income

and Growth Fund Portfolio of Investments December 31, 2021 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares | | | | | Description (1) | | | | | | | | | | | | | | | | | Value | |

| | | | | | | | |

| | | | | | LONG-TERM INVESTMENTS – 137.1% (96.9% of Total Investments) | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | REAL ESTATE INVESTMENT TRUST COMMON STOCKS – 37.2% (26.3% of Total Investments) | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | | | | Diversified – 5.6% | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | 436,826 | | | | | Abacus Property Group, (2) | | | | | | | | | | | | | | | | | | | | | | $ | 1,204,416 | |

| | 25,351 | | | | | Alpine Income Property Trust Inc | | | | | | | | | | | | | | | | | | | | | | | 508,034 | |

| | 178,019 | | | | | Charter Hall Long Wale, (2) | | | | | | | | | | | | | | | | | | | | | | | 654,222 | |

| | 9,729 | | | | | Cofinimmo SA, (2) | | | | | | | | | | | | | | | | | | | | | | | 1,553,948 | |

| | 13,005 | | | | | Gecina SA, (2) | | | | | | | | | | | | | | | | | | | | | | | 1,819,799 | |

| | 50,669 | | | | | Global Net Lease Inc | | | | | | | | | | | | | | | | | | | | | | | 774,222 | |

| | 449,448 | | | | | GPT Group, (2) | | | | | | | | | | | | | | | | | | | | | | | 1,772,261 | |

| | 416,153 | | | | | Growthpoint Properties Australia Ltd, (2) | | | | | | | | | | | | | | | | | | | | | | | 1,319,666 | |

| | 1,176,359 | | | | | Home Reit PLC, (2) | | | | | | | | | | | | | | | | | | | | | | | 2,077,585 | |

| | 338 | | | | | Hulic Reit Inc, (2) | | | | | | | | | | | | | | | | | | | | | | | 508,559 | |

| | 23,691 | | | | | ICADE, (2) | | | | | | | | | | | | | | | | | | | | | | | 1,704,595 | |

| | 42,604 | | | | | Land Securities Group PLC, (2) | | | | | | | | | | | | | | | | | | | | | | | 449,641 | |

| | 358,952 | | | | | LXI REIT Plc, (2) | | | | | | | | | | | | | | | | | | | | | | | 707,837 | |

| | 4,479 | | | | | Star Asia Investment Corp, (2) | | | | | | | | | | | | | | | | | | | | | | | 2,462,359 | |

| | 1,029,822 | | | | | Stockland, (2) | | | | | | | | | | | | | | | | | | | | | | | 3,177,016 | |

| | 581,010 | | | | | Stride Property Group | | | | | | | | | | | | | | | | | | | | | | | 839,640 | |

| | 62,973 | | | | | WP Carey Inc | | | | | | | | | | | | | | | | | | | | | | | 5,166,935 | |

| | | | | | Total Diversified | | | | | | | | | | | | | | | | | | | | | | | 26,700,735 | |

| | | | | | | | |

| | | | | | Health Care – 3.9% | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | 3,059 | | | | | CareTrust REIT Inc | | | | | | | | | | | | | | | | | | | | | | | 69,837 | |

| | 100,655 | | | | | Medical Properties Trust Inc | | | | | | | | | | | | | | | | | | | | | | | 2,378,478 | |

| | 331,249 | | | | | NorthWest Healthcare Properties Real Estate Investment Trust | | | | | | | | | | | | | | | | | | | | | | | 3,616,387 | |

| | 78,122 | | | | | Omega Healthcare Investors Inc | | | | | | | | | | | | | | | | | | | | | | | 2,311,630 | |

| | 328,900 | | | | | Physicians Realty Trust | | | | | | | | | | | | | | | | | | | | | | | 6,193,187 | |

| | 147,473 | | | | | Sabra Health Care REIT Inc | | | | | | | | | | | | | | | | | | | | | | | 1,996,784 | |