Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration Nos. 333-209766

333-209766-01

333-209766-02

Prospectus dated June 23, 2016

Cabela’s Credit Card Master Note Trust

Issuing Entity

(CIK: 0001592145)

| WFB Funding, LLC | World’s Foremost Bank | |

Depositor (CIK: 0001540723) | Originator, Sponsor, Bank and Servicer (CIK: 0001602985) | |

| $1,000,000,000 Series 2016-I Asset-Backed Notes | ||

Class A-1 Notes | Class A-2 Notes | |||

Principal amount | $570,000,000 | $280,000,000 | ||

Interest rate | 1.78% per year | One-month LIBOR plus 0.85% per year | ||

Interest payment dates | Monthly on the 15th, beginning August 15, 2016 | Monthly on the 15th, beginning August 15, 2016 | ||

Expected principal payment date | June 17, 2019 | June 17, 2019 | ||

Final maturity date | June 15, 2022 | June 15, 2022 | ||

Price to public | $569,911,650 (or 99.98450%) | $280,000,000 (or 100.00000%) | ||

Underwriting discount | $1,567,500 (or 0.275%) | $700,000 (or 0.250%) | ||

Proceeds to issuing entity | $568,344,150 (or 99.70950%) | $279,300,000 (or 99.75000%) |

The issuing entity will also issue $80,000,000 Class B notes, $42,500,000 Class C notes and $27,500,000 Class D notes as part of Series 2016-I. Only the Class A notes are offered hereby.

The issuing entity may offer and sell Series 2016-I notes having an aggregate initial principal amount that is either greater or less than the amount shown above. In that event, the initial principal amount of each Class of notes will be proportionately increased or decreased.

Each class of notes benefits from credit enhancement in the form of subordination of any junior classes of notes and a cash collateral account and, primarily for the benefit of the Class C notes and the Class D notes, a spread account. The notes will be paid from the issuing entity’s assets consisting primarily of a Series 2004-1 certificate issued by the Cabela’s Master Credit Card Trust. The primary assets of the Cabela’s Master Credit Card Trust consist of receivables in a portfolio of VISA® (and, potentially if issued in the future, other payment networks) revolving credit card accounts owned by World’s Foremost Bank.

We expect to issue your series of notes in book-entry form on or about June 29, 2016.

You should consider carefully therisk factors beginning on page 20 in this prospectus.

A note is not a deposit and neither the notes nor the underlying accounts or receivables are insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. The notes are obligations of Cabela’s Credit Card Master Note Trust only and are not obligations of, and do not represent an interest in, WFB Funding, LLC, World’s Foremost Bank, any of their affiliates or any other person.

Neither the Securities and Exchange Commission nor any state securities commission has approved these notes or determined that this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Underwriters of the Class A-1and A-2 notes

| Wells Fargo Securities | RBC Capital Markets |

BofA Merrill Lynch

Table of Contents

Important Notice about Information Presented in this

Prospectus

We (WFB Funding, LLC) provide information to you about the notes in this prospectus. You should rely only on the information provided in this prospectus, including the information incorporated by reference. We have not authorized anyone to provide you with different information. We are not offering the notes in any state where the offer is not permitted.

We include cross-references in this prospectus to captions in these materials where you can find further related discussions. The Table of Contents in this prospectus provides the pages on which these captions are located.

This prospectus uses defined terms. You can find a glossary of these terms under the caption “Glossary of Terms for Prospectus” beginning on page 132 of this prospectus.

Recent Developments

We are a direct subsidiary of World’s Foremost Bank and an indirect subsidiary of Cabela’s Incorporated. The accounts designated to the trust have been originated in substantial part to retail customers of Cabela’s. Transactions on the accounts produce credits which the cardholder may apply to future purchases at Cabela’s.

On December 2, 2015, Cabela’s announced that its Board of Directors has initiated a process to explore and evaluate a wide range of strategic alternatives to further enhance shareholder value. Cabela’s has publicly disclosed that its Board of Directors and management team, working with advisers, plan to proceed in a timely and orderly manner, but have not set a definitive timetable for completion of this process. There can be no assurances that this review process will result in a sale transaction or other strategic alternative of any kind. Cabela’s files periodic reports with the SEC which are available to the public on the SEC Internet site (http://www.sec.gov).

Please also see“Risk Factors—The ongoing exploration of strategic alternatives by Cabela’s Incorporated may impact its business, the bank or the notes,” “—payment and origination patterns of receivables finance charge rates and credit card usage could reduce collections and may affect the timing and amount of payments to you,” “— We may assign our obligations as depositor and the bank may assign its obligations as servicer,” “—The bank depends on access to funding under variable funding notes to fund new receivables,” and “The Bank’s Credit Card Activities – General” and “—Marketing and Underwriting”in this prospectus.

Certain Volcker Rule Considerations

Cabela’s Credit Card Master Note Trust is not now, and immediately following the issuance of the Series 2016-I notes pursuant to the indenture will not be, a “covered fund” for purposes of regulations adopted under Section 13 of the Bank Holding Company Act of 1956 (the “BHCA”), commonly known as the “Volcker Rule.” In reaching this conclusion, although other statutory or regulatory exemptions under the Investment Company Act of 1940, as amended (the “Investment Company Act”), and under the Volcker Rule and its related regulations may be available, we have relied on the determinations that:

| • | Cabela’s Credit Card Master Note Trust may rely on the exemption from registration under the Investment Company Act provided by Rule 3a-7 thereunder, and, accordingly |

| • | Cabela’s Credit Card Master Note Trust may rely on the exemption from the definition of a covered fund under the Volcker Rule made available to entities that do not rely solely on Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act for their exemption from registration under the Investment Company Act. |

Table of Contents

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 4 | ||||

| 4 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

| 13 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 20 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| 50 |

i

Table of Contents

| 50 | ||||

| 50 | ||||

| 50 | ||||

| 51 | ||||

| 51 | ||||

| 52 | ||||

| 52 | ||||

| 53 | ||||

| 53 | ||||

| 53 | ||||

| 53 | ||||

| 54 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 56 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 57 | ||||

| 58 | ||||

| 58 | ||||

| 60 | ||||

Representations and Warranties; Required Removal of Receivables | 61 | |||

| 62 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 67 | ||||

| 68 | ||||

| 68 | ||||

| 69 | ||||

| 71 | ||||

| 72 | ||||

| 74 | ||||

| 75 | ||||

| 75 | ||||

| 75 | ||||

| 77 | ||||

| 77 | ||||

| 78 | ||||

| 80 | ||||

| 81 | ||||

| 82 | ||||

| 82 | ||||

| 82 | ||||

| 82 | ||||

| 83 | ||||

Defaulted Receivables; Dilution; Investor Charge-Off; Reduction Amounts | 83 | |||

| 84 | ||||

| 84 |

ii

Table of Contents

| 84 | ||||

| 85 | ||||

| 86 | ||||

| 87 | ||||

| 87 | ||||

| 89 | ||||

| 90 | ||||

| 90 | ||||

| 92 | ||||

| 92 | ||||

| 92 | ||||

| 92 | ||||

| 92 | ||||

| 93 | ||||

| 94 | ||||

| 94 | ||||

| 94 | ||||

| 95 | ||||

| 95 | ||||

Transfer of the Series 2004-1 Certificate to the Issuing Entity | 95 | |||

| 95 | ||||

| 97 | ||||

| 97 | ||||

| 97 | ||||

| 97 | ||||

| 98 | ||||

| 99 | ||||

| 99 | ||||

| 100 | ||||

| 100 | ||||

| 100 | ||||

| 101 | ||||

| 102 | ||||

| 102 | ||||

| 102 | ||||

| 102 | ||||

| 103 | ||||

| 104 | ||||

| 105 | ||||

| 107 | ||||

| 111 | ||||

| 113 | ||||

| 114 | ||||

| 114 | ||||

| 115 | ||||

| 115 | ||||

| 115 | ||||

| 115 | ||||

Claims and Defenses of Accountholders Against the Master Trust | 117 | |||

| 117 | ||||

| 118 | ||||

| 120 | ||||

| 121 | ||||

| 121 | ||||

Tax Classification of the Master Trust, Issuing Entity and the Notes | 122 | |||

| 123 |

iii

Table of Contents

| 125 | ||||

| 126 | ||||

| 126 | ||||

| 126 | ||||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| 129 | ||||

| 129 | ||||

| 130 | ||||

| 130 | ||||

| 130 | ||||

| 131 | ||||

| 132 | ||||

| A-I-1 | ||||

| A-I-1 | ||||

| A-I-1 | ||||

| A-I-3 | ||||

| A-I-3 | ||||

| A-I-4 | ||||

| A-I-4 | ||||

| A-I-7 | ||||

| A-I-8 | ||||

| A-I-8 | ||||

| A-I-8 | ||||

| A-I-9 | ||||

| A-I-9 | ||||

| A-I-9 | ||||

| A-I-10 | ||||

| A-I-10 | ||||

| A-I-10 | ||||

| A-I-10 | ||||

| A-I-11 | ||||

| A-I-12 | ||||

| A-II-1 | ||||

| A-II-1 | ||||

| A-II-1 | ||||

| A-II-2 | ||||

| A-III-1 | ||||

Global Clearance, Settlement and Tax Documentation Procedures | A-III-1 | |||

| A-III-1 | ||||

| A-III-1 | ||||

| A-III-2 |

iv

Table of Contents

| Issuing Entity: | Cabela’s Credit Card Master Note Trust | |

| Depositor/Securitizer: | WFB Funding, LLC | |

| Originator, Sponsor, Bank and Servicer: | World’s Foremost Bank | |

| Indenture Trustee: | U.S. Bank National Association | |

| Owner Trustee: | Wells Fargo Delaware Trust Company, National Association | |

| Asset Representations Reviewer: | Clayton Fixed Income Services LLC | |

| Expected Closing Date: | On or about June 29, 2016 | |

| Clearance and Settlement: | DTC/Clearstream/Euroclear | |

| Denominations: | $1,000 and in integral multiples of $1,000 | |

| Servicing Fee Rate: | 2% per annum | |

| Initial Allocation Amount: | $1,000,000,000 | |

| Primary Assets of the Issuing Entity: | An interest in receivables originated in VISA® (and, potentially if issued in the future, other payment networks) revolving credit card accounts owned by World’s Foremost Bank. | |

| Offered Notes: | The Class A-1 and A-2 notes are offered by this prospectus. | |

Series 2016-I | ||||||||||

| Class | Amount | % of Series 2016-I Notes | ||||||||

Class A-1 notes Class A-2 notes | $ $ | 570,000,000 280,000,000 |

|

| 57.00 28.00 | % % | ||||

Class B notes1 | $ | 80,000,000 | 8.00 | % | ||||||

Class C notes1 | $ | 42,500,000 | 4.25 | % | ||||||

Class D notes1 | $ | 27,500,000 | 2.75 | % | ||||||

|

|

|

| |||||||

Total | $ | 1,000,000,000 | 100.00 | % | ||||||

|

|

|

| |||||||

| 1 | The Class B notes, Class C notes and Class D notes are not offered hereby. |

1

Table of Contents

Class A-1 | Class A-2 | |||

| Initial Note Principal Balance: | $570,000,000 | $280,000,000 | ||

| Anticipated Ratings: | We expect each class of the offered notes to receive credit ratings from at least two nationally recognized statistical rating organizations hired by us to rate the offered notes, each a “Hired Agency” and, collectively, the “Hired Agencies.” | |||

| Credit Enhancement: | Subordination of Class B, Class C and Class D notes, and amounts available in the cash collateral account | |||

| Interest Rate: | 1.78% per year | one-month LIBOR plus 0.85% per year | ||

| Interest Accrual Method: | 30/360 | actual/360 | ||

| Distribution Dates: | 15th day of each month, or if that day is not a business day, the next business day | |||

| First Distribution Date: | August 15, 2016 | August 15, 2016 | ||

| Interest Rate Index Reset Date: | N/A | 2 London business days before each distribution date | ||

Commencement of Accumulation Period (subject to adjustment): | June 1, 2018 | June 1, 2018 | ||

| Expected Principal Payment Date: | June 17, 2019 | June 17, 2019 | ||

| Final Maturity Date: | June 15, 2022 | June 15, 2022 | ||

| ERISA Eligibility: | Yes, subject to important considerations described under “ERISA Considerations” in this prospectus. | |||

| Debt for United States Federal Income Tax Purposes: | Yes, subject to important considerations described under “United States Federal Income Tax Consequences” in this prospectus. | |||

2

Table of Contents

This summary is a simplified presentation of the major structural components of Series 2016-I. It does not contain all of the information that you need to consider in making your investment decision. You should carefully read this entire document and this prospectus before you purchase any notes.

3

Table of Contents

Originator, Sponsor, Bank and Servicer

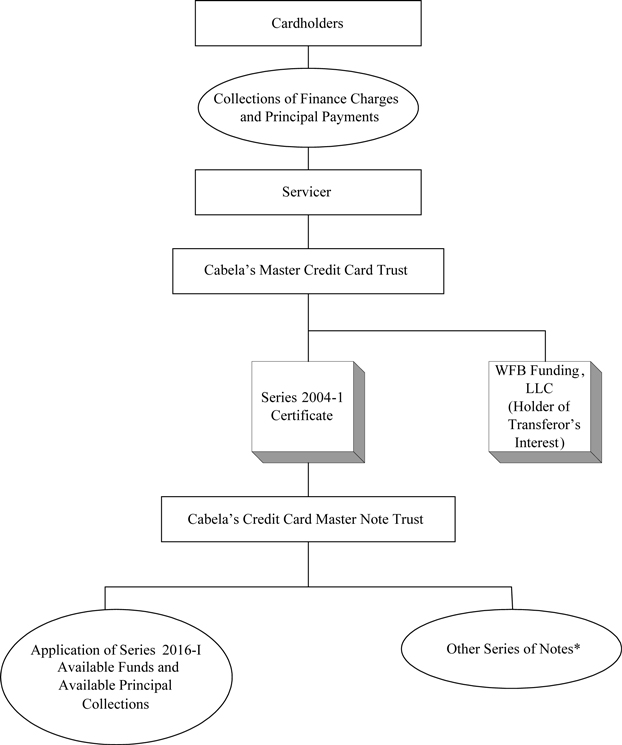

World’s Foremost Bank is a Nebraska state FDIC-insured bank that is organized as a limited purpose credit card bank and is a wholly-owned subsidiary of Cabela’s Incorporated. The bank originates the credit card accounts that have been designated to the master trust and transfers the receivables in those accounts to us under a receivables purchase agreement. The bank is also the sponsor of the transactions described in this prospectus and as such structures each issuance of notes by the issuing entity. The bank also acts as servicer for the master trust and the issuing entity and as administrator for the issuing entity.

We are a limited liability company formed under the laws of the State of Nebraska. We are owned by the bank and its wholly-owned subsidiary WFB Funding Corporation. We purchase receivables arising in the credit card accounts that have been designated to the master trust and transfer those receivables to the master trust under the pooling and servicing agreement. We also hold the transferor’s interest in the master trust.

Our address is One Cabela Drive, Sidney, Nebraska 69160. Our telephone number is (402) 323-5958.

Cabela’s Master Credit Card Trust is a common law trust formed by the bank in 2001 under a pooling and servicing agreement that has been amended and may in the future be amended from time to time. We sometimes refer to the Cabela’s Master Credit Card Trust as the “master trust.” The February 2003 amendment, among other things, designated us as transferor in replacement of the bank. The bank has transferred some of the credit card receivables directly to the master trust under the pooling and servicing agreement prior to the February 2003 amendment, and beginning on the date of the February 2003 amendment, we have transferred the receivables sold to us by the bank under the receivables purchase agreement to the master trust under the pooling and servicing agreement.

The Series 2004-1 certificate will be the primary source of funds for the payment of principal and interest on the Series 2016-I notes. On the expected issuance date of the Series 2016-I notes, the Series 2004-1 certificate will be the only outstanding series of investor certificates issued by the master trust. At any time when no series of investor certificates is outstanding, other than the Series 2004-1 certificate held by the issuing entity, we may cause the master trust to terminate, at which time the receivables will be transferred to the issuing entity and held directly by the issuing entity as collateral for the notes.

We refer to the entity – either the master trust or the issuing entity – that holds the receivables at any given time as the trust.

The notes will be issued by Cabela’s Credit Card Master Note Trust, a Delaware statutory trust, which is referred to in this prospectus as the issuing entity. The notes will be issued under an indenture supplement to an indenture, each between the issuing entity and the indenture trustee and represent debt of the issuing entity.

U.S. Bank National Association, a national banking association, is the trustee of the master trust for each series of investor certificates issued by the master trust, including the Series 2004-1 certificate.

Under the terms of the pooling and servicing agreement, the role of the master trust trustee is limited. See, “Cabela’s Master Credit Card Trust – Master Trust Trustee.”

4

Table of Contents

U.S. Bank National Association, a national banking association, is the indenture trustee under the indenture for each series of notes issued by the issuing entity, including your series of notes.

Under the terms of the indenture, the role of the indenture trustee is limited. See,“The Indenture Trustee.”

Wells Fargo Delaware Trust Company, National Association, a national banking association, is the owner trustee of the issuing entity.

Under the terms of the trust agreement, the role of the owner trustee is limited. See,“The Trust Agreement – Owner Trustee.”

Asset Representations Reviewer

Clayton Fixed Income Services LLC, a Delaware limited liability company, is the asset representations reviewer under the asset representations review agreement. For additional information about the asset representations reviewer, see “New Requirements for SEC Shelf Registration – Asset Representations Review – Asset Representations Reviewer.”

The Series 2016-I Notes will be secured by a pledge of the Series 2004-1 certificate, which represents a beneficial interest in a pool of receivables that arise under World’s Foremost Bank’s VISA® (and, potentially if issued in the future, other payment networks) revolving credit card accounts. The amount of your series’ claim on the receivables, which we refer to as the allocation amount, will initially equal $1,000,000,000.

The bank has designated a portion of the eligible accounts from its portfolio of credit card accounts and has transferred the receivables in those accounts either directly to Cabela’s Master Credit Card Trust or to us. We have, in turn, transferred the receivables sold to us by the bank to the master trust. We refer to the accounts that have been designated as trust accounts as the trust portfolio. The master trust has issued a Series 2004-1 certificate representing an interest in the receivables and the other assets of the master trust to us. We have transferred that Series 2004-1 certificate to the issuing entity and the Series 2004-1 certificate serves as collateral for the notes.

The receivables in the trust portfolio as of March 31, 2016 were as follows:

| • | total receivables: $4,859,518,475.40 |

| • | principal receivables: $4,824,322,999.78 |

| • | finance charge receivables: $35,195,475.62 |

| • | total accounts designated to the trust: 3,166,941 |

On June 9, 2016, we gave notice of our intent to designate additional accounts to the master trust on June 23, 2016. As of June 9, 2016, these additional accounts consisted of approximately 105,802 accounts with an aggregate receivables balance of approximately $53,495,513.86. These receivables are not included in the tables and other master trust portfolio information included in this prospectus.

5

Table of Contents

As of March 31, 2016,

| • | The accounts designated for the trust portfolio had an average principal receivable balance of approximately $1,523.34 and an average credit limit of approximately $12,404.03. |

| • | The percentage of the aggregate total receivable balance to the aggregate total credit limit was approximately 12.37%. |

| • | The weighted average age of the accounts was approximately 89 months. |

Compliance with Underwriting Criteria

As described under “The Bank’s Credit Card Activities—Marketing and Underwriting” and “The Bank’s Credit Card Activities—Credit Limit Management and Authorization” and in “Annex I:Review of Pool Asset Disclosure—Compliance with Underwriting Criteria” in this prospectus, the bank makes all underwriting decisions using an automated credit evaluation system that uses credit bureau scores, a proprietary score card and a proprietary decisioning system that is operated by a third party to determine an applicant’s risk. The bank’s portfolio management department performs monthly testing on applications to ensure that the automated system is processing applications as intended and reports the results of this testing to the bank’s credit committee monthly. The bank’s portfolio management department also performs periodic evaluations and testing of compliance with the bank’s credit card underwriting policy and process guidelines. The bank’s credit committee reviews and inspects these controls on a periodic basis. Such evaluations, testing, inspections and reviews are designed to provide reasonable assurance that the application process produces credit accounts that comply with the bank’s underwriting policies. These reviews and inspections produced no significant deviations relating to the bank’s credit underwriting or credit line management processes in 2015 or the three months ended March 31, 2016.

Addition of Assets to the Trust

When an account has been designated as a trust account, World’s Foremost Bank continues to own the account but we buy all receivables existing at the time of designation or created later and transfer them to the trust. The bank has the option to designate additional accounts, which must meet the criteria for eligible accounts described in the definition of “Eligible Account” in the “Glossary of Terms for Prospectus” in this prospectus, to be included as trust accounts from time to time. If the volume of additional accounts designated exceeds specified periodic limitations, then additional new accounts can only be designated if the Rating Agency Condition is satisfied.

See “Cabela’s Master Credit Card Trust—Addition of Master Trust Assets” in this prospectus for a more detailed description of these and other limitations on our ability to designate additional accounts. In addition, the bank is required to designate additional accounts as trust accounts if the amount of principal receivables held by the trust falls below a specified minimum or if the average transferor’s interest falls below a specified minimum transferor’s interest for any monthly period, as more fully described in “Cabela’s Master Credit Card Trust—Addition of Master Trust Assets” in this prospectus.

Removal of Assets from the Trust

Optional Removals

We have the right to remove accounts from the list of designated accounts and to require the reassignment to us or our designee of all receivables in the removed accounts. We may remove accounts and reassign the receivables in the removed accounts to us or our designee provided that, among other things, the removal will not cause a pay out event to occur for any series of investor certificates and the Rating Agency Condition is satisfied. In addition, we must represent and warrant that either: (a) we did not utilize any selection procedures that we believed to be materially adverse to the certificateholders in selecting the removed accounts, or (b) the removed accounts were identified for removal because of third-party cancellation or expiration of an affinity, private-label, agent bank, or other similar arrangement. See “Cabela’s Master Credit Card Trust—Removal of Master Trust Assets” in this prospectus.

6

Table of Contents

Required Removals

We are required to automatically accept a reassignment of receivables from the trust if either we or the servicer discover that the receivables did not satisfy eligibility requirements in some material respect at the time that we transferred them to the trust, and the ineligibility results in a charge-off or in impairment of the trust’s rights in the receivables or their proceeds. Except under limited circumstances, there will be a 30 day cure period. Similarly, the servicer is required to purchase receivables from the trust if the servicer fails to satisfy any of its obligations in connection with the transferred receivables or trust accounts, and the failure results in a material impairment of the receivables or subjects their proceeds to a conflicting lien. These reassignment and purchase obligations and applicable cure periods are more fully described in “Cabela’s Master Credit Card Trust—Representations and Warranties; Required Removal of Receivables” and “Cabela’s Master Credit Card Trust—Servicer Covenants” in this prospectus.

Other Claims on the Receivables

Other Series of Notes

The issuing entity has issued other series of variable funding notes and term notes and may issue other series of notes from time to time in the future. A summary of the series of notes expected to be outstanding on the closing date is in “Annex II: Other Securities Outstanding” included at the end of this prospectus. Neither you nor any other noteholder will have the right to consent to the issuance of future series of variable funding notes or term notes.

No new series of variable funding notes or term notes may be issued unless we satisfy the conditions described in “Description of the Notes—New Issuances of Notes” in this prospectus, including:

| • | the Rating Agency Condition is satisfied; |

| • | we certify that (1) the issuing entity reasonably believes that the new issuance will not have an adverse effect or result in an early redemption event for any outstanding series of notes, and (2) all conditions precedent to the execution, authentication and delivery of the new series of notes have been satisfied; |

| • | delivery of an opinion with respect to certain tax matters; |

| • | the issuing entity delivers to the indenture trustee the related indenture supplement, any enhancement and any enhancement agreement; and |

| • | on the new issuance day (1) we would not be required to add additional accounts under the pooling and servicing agreement, and (2) the transferor’s interest would at least be equal to the Minimum Transferor’s Interest. |

The Transferor’s Interest

We own the interest, called the transferor’s interest, in the receivables and the other assets of the master trust not supporting your series of notes or any other series of notes or investor certificates. The transferor’s interest does not provide credit enhancement for your series of notes, or any other series of notes. We are required to maintain a Minimum Transferor’s Interest, which is calculated as described in “Glossary of Terms for Prospectus.” See, “Cabela’s Master Credit Card Trust—Addition of Master Trust Assets” in this prospectus for a description of the circumstances on which we will be required to designate additional accounts as trust accounts if the transferor’s interest falls below the Minimum Transferor’s Interest.

7

Table of Contents

Allocations of Collections and Losses

Your notes represent the right to principal and interest payments from a portion of the collections on the receivables. See the diagram on page 16, which summarizes the application of finance charge collections and principal collections by the servicer. The servicer will also allocate to your series a portion of defaulted receivables and will also allocate a portion of the dilution on the receivables to your series if the dilution is not offset by the amount of the transferor’s interest and we fail to comply with our obligation to reimburse the trust for the dilution. Dilution means any reduction to the principal balances of receivables made by the servicer because of merchandise returns or any other reason except losses or payments. Dilution also includes reductions due to a debt cancellation or reduction program that cannot be recovered from insurance or the program’s reserves.

The portion of collections, defaulted receivables and uncovered dilution allocated to your series will be based mainly upon the ratio of the allocation amount for your series (minus funds then on deposit in the principal funding account) to the sum of the allocation amounts for all outstanding series of notes (minus funds then on deposit in the principal funding account of all outstanding series of notes). The way this ratio is calculated will vary during each of three periods that may apply to your notes:

| • | Therevolving period, which will begin on the closing date and end when either of the other two periods begins. |

| • | Theaccumulation period, which is scheduled to begin on June 1, 2018 and end on May 31, 2019. However, if an early redemption event occurs before the accumulation period begins, there will be no accumulation period and an early redemption period will begin. Unless an early redemption event occurs during the accumulation period, the accumulation period will end upon the Series Termination Date. If an early redemption event occurs during the accumulation period, the accumulation period will end, and an early redemption period will begin. Under some circumstances, the beginning of the accumulation period may be delayed, or if it has already begun, may be suspended. During this delay or upon the suspension of the accumulation period, the revolving period will continue or resume, as appropriate. Throughout the accumulation period we will accumulate collections of principal receivables for later distribution to you. |

| • | Theearly redemption period, which will only occur if one or more adverse events, known as early redemption events, occurs and will continue until the Series Termination Date. |

For most purposes, the allocation amount (minus funds then on deposit in the principal funding account) used in determining these ratios will be measured as of and will be reset no less frequently than at the end of each month. However, for allocations of principal collections during the accumulation period or the early redemption period, the allocation amount as of the end of the revolving period will be used.

The allocation amount for your series is:

| • | the original principal amount of the 2016-I notes,minus |

| • | principal payments on the Series 2016-I notes,minus |

| • | the amount of any principal collections reallocated to cover interest and servicing payments for your series to the extent not reimbursed from finance charge collections and investment earnings allocated to your series,minus |

| • | your series’ share of defaults and uncovered dilution to the extent not reimbursed from finance charge collections and investment earnings allocated to your series. |

A reduction to the allocation amount because of reallocated principal collections, defaults or uncovered dilution will be reversed to the extent that your series has available finance charge collections and investment earnings available for this purpose in future periods. If a reduction to the allocation amount because of reallocated principal collections or defaults or uncovered dilution is not reversed, not all of the principal for your series of notes may be paid.

8

Table of Contents

Subject to some limitations, we may elect to treat a percentage of the principal receivables in the trust as finance charge receivables for purposes of the allocations described in this prospectus. We may from time to time, and subject to some limitations, increase or reduce or eliminate the percentage used for this purpose. This percentage will initially be zero.

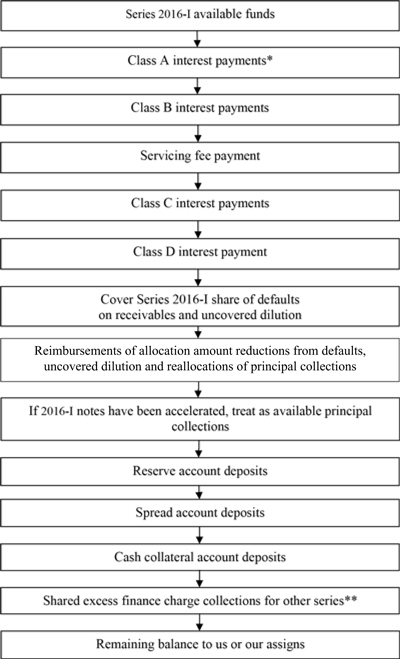

Application of Available Funds

Each month, the issuing entity will apply available funds for the preceding month, together with amounts withdrawn from the spread account and cash collateral account (subject to certain limitations), in the following order of priority:

| • | to pay interest on the Class A notes, except that if the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amounts owed) of the amount available; |

| • | to pay interest on the Class B notes; |

| • | to pay servicing fees for your series; |

| • | to pay interest on the Class C notes; |

| • | to pay interest on the Class D notes; |

| • | to cover your series’ share of defaulted receivables and uncovered dilution for the prior calendar month; |

| • | to reinstate any prior reductions in your series allocation amount on account of defaulted receivables, uncovered dilution or reallocated principal collections, in each case that have not been reimbursed; |

| • | if an event of default has occurred and the maturity of your series of notes has been accelerated, to pay principal on your series of notes; |

| • | in limited circumstances, to make deposits into a reserve account; |

| • | to make deposits, if required, into the spread account; |

| • | to make deposits, if required, into the cash collateral account; |

| • | to other series that share excess finance charge collections with Series 2016-I; and |

| • | any remaining balance to us or our assigns. |

For a description of how available funds are calculated, see “Description of Series Provisions—Application of Available Funds” in this prospectus. No other series of variable funding notes or term notes currently outstanding or to be issued in the future will be entitled to receive distributions from available funds allocated to Series 2016-I. However, each outstanding series of variable funding notes and term notes indicated on “Annex II—Other Securities Outstanding” will share excess finance charge collections with Series 2016-I, and any other series of variable funding notes or term notes issued in the future may also share excess finance charge collections with Series 2016-I if such other series is included in group I. The above application of available funds is summarized in the diagram on page 17.

9

Table of Contents

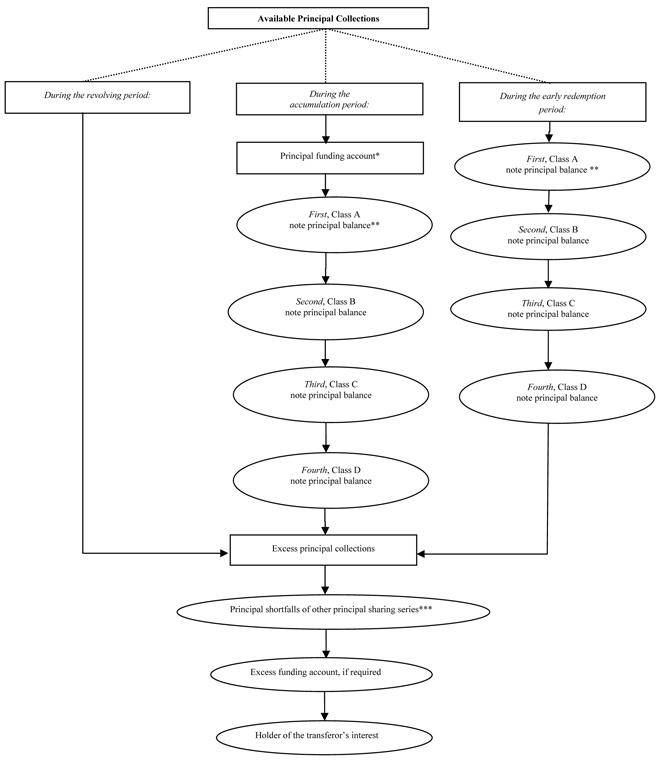

Application of Available Principal Collections

Each month, the issuing entity will apply available principal collections as follows:

Revolving Period

During the revolving period, no principal will be paid or accumulated in a trust account for you.

Accumulation Period

During the accumulation period, available principal collections will be deposited in a trust account, up to a specified controlled deposit amount on each distribution date. Amounts on deposit in that account will be paid, first, to the Class A noteholders until the Class A notes are paid in full, except that if the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amounts owed) of the amount available, then to the Class B noteholders until the Class B notes are paid in full, then to the Class C noteholders until the Class C notes are paid in full, and then to the Class D noteholders until the Class D notes are paid in full, on the expected principal payment date for the notes, unless an early redemption event occurs. If an early redemption event does not occur, the accumulation period will end on the Series Termination Date.

Early Redemption Period

An early redemption period for your series will start if an early redemption event occurs. The early redemption events for your series are described below in this summary under “Description of Series Provisions—Early Redemption Events” in this prospectus and under “Description of the Notes—Early Redemption Events” in this prospectus. During the early redemption period, available principal collections will be paid monthly—without any limitation based on the controlled deposit amount—first to the Class A noteholders, except that if the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amounts owed) of the amount available, then to the Class B noteholders, then to the Class C noteholders and then to the Class D noteholders, in each case until the Series Termination Date.

Reallocation of Principal Collections

During any of the above periods, available principal collections may be reallocated, if necessary, to make required payments of interest on the Class A notes and the Class B notes, monthly servicing fee payments, and required payments of interest on the Class C notes that are not made from available funds. This reallocation is one of the ways that the more senior classes of notes obtain the benefit of subordination, as described in the next section of this summary. The amount of reallocated principal collections is limited by the amount of available subordination.

Shared Principal Collections

No other series of variable funding notes or term notes currently outstanding or to be issued in the future will be entitled to receive distributions from available principal collections allocated to Series 2016-I. At all times, however, available principal collections that are not needed for payments on your series will first be made available to each outstanding series of variable funding notes and term notes indicated on “Annex II—Other Securities Outstanding” and any other series of variable funding notes or term notes issued in the future that is included in group I, and second, paid to us or our assigns. See “Description of the Notes—Shared Principal Collections” in this prospectus.

For a description of how available principal collections are calculated, see “Description of Series Provisions—Principal Payments and Deposits” in this prospectus. The above applications of available principal collections are summarized in the diagram on page 19.

10

Table of Contents

Credit enhancement for your series includes subordination, amounts available in the cash collateral account and, primarily for the Class C noteholders and the Class D noteholders, amounts available in the spread account, each as described below. Credit enhancement for your series is for the benefit of your series only, and you are not entitled to the benefits of credit enhancement available to other series.

Subordination

TheClass A-1 notes andClass A-2 notes arepari passu. We refer to theClass A-1 notes and theClass A-2 notes together as the “Class A notes.” Credit enhancement for the Class A notes includes the subordination of the Class B notes, the Class C notes and the Class D notes.

Credit enhancement for the Class B notes includes the subordination of the Class C notes and the Class D notes.

Credit enhancement for the Class C notes includes the subordination of the Class D notes.

Subordination serves as credit enhancement in the following way: The more subordinated, or junior, classes of notes will not receive payment of interest or principal until required payments have been made to the more senior classes. As a result, subordinated classes will absorb any shortfalls in collections or deterioration in the collateral for the notes prior to senior classes.

Spread Account

Credit enhancement is also available to the Class C noteholders and the Class D noteholders in the form of amounts available in the spread account. The spread account initially will not be funded. The issuing entity will make monthly deposits into the spread account from available funds to the extent the spread account is not funded to the required level. The required level will be adjusted based on the performance of the receivables.

If available funds and available principal collections available to the Class C notes and the Class D notes are insufficient to pay the interest and principal due on the Class C notes and the Class D notes, the indenture trustee will use the funds on deposit in the spread account, if any, to make up the shortfall, first to the Class C noteholders and then to the Class D noteholders. Under certain conditions, after the payment of the principal of the Class C notes and the Class D notes in full, the remaining funds on deposit in the spread account, if any, may be used to make up a principal shortfall to the Class A notes, except that if the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amounts owed) of the amount available, and then to the Class B notes, in that order of priority. See “Description of Series Provisions—Spread Account; Required Spread Account Amount” in this prospectus.

Cash Collateral Account

Credit enhancement is available to your series of notes in the form of amounts available in the cash collateral account. If available funds, amounts withdrawn from the spread account and reallocated principal collections are insufficient to pay interest on the Class A notes, Class B notes, Class C notes and Class D notes, as applicable, the indenture trustee will use the funds on deposit in the cash collateral account up to the available cash collateral account amount, if any, to make up the shortfall. See “Description of Series Provisions—Cash Collateral Account” in this prospectus.

In certain circumstances funds on deposit in the cash collateral account will be used to make principal payments on your series of notes. See “Description of Series Provisions—Cash Collateral Account” in this prospectus.

11

Table of Contents

The cash collateral account initially will not be funded. After your series of notes are issued, deposits into the cash collateral account, if required, will be made each month to the extent of available funds up to the required levels as described under “Description of Series Provisions—Cash Collateral Account” in this prospectus.

The issuing entity will begin to repay the principal of the notes before the expected principal payment date if an early redemption event occurs. An early redemption event will occur if the Three-Month Average Excess Spread Percentage for any monthly period is less than zero, which may happen if the finance charge collections on the receivables are too low or if defaults are too high. An early redemption event will also occur if the average of the Monthly Principal Payment Rate for any three consecutive calendar months is less than 15%, which may happen if the principal collections on the receivables are too low.

The other early redemption events are:

| • | Our failure, or the failure of the servicer or the issuing entity, to make required payments or deposits or material failure to perform other obligations, subject to applicable grace periods; |

| • | Material inaccuracies in representations and warranties of the servicer or the issuing entity, subject to applicable grace periods; |

| • | The indenture trustee fails to have a valid and perfected first priority security interest in any of the assets of the issuing entity that secure the notes; |

| • | An event of default occurs for the Series 2016-I notes and their final maturity date is accelerated; |

| • | Any Series 2016-I notes are not paid in full on the expected principal payment date; |

| • | During any period of 20 consecutive days, the transferor’s interest average over that period is less than 5.0% of the average principal receivables, and we (i) fail to designate sufficient additional accounts, and (ii) fail to transfer receivables from such additional accounts to the trust on or before the tenth business day following such 20-day period; |

| • | The issuing entity or the master trust is subject to registration as an investment company under the 1940 Act; or |

| • | The occurrence of a pay out event described under “Cabela’s Master Credit Card Trust—Pay Out Events” in this prospectus. |

See “Description of Series Provisions—Early Redemption Events” in this prospectus for a more detailed description of the early redemption events.

The Series 2016-I notes are subject to events of default described under “The Indenture—Events of Default; Rights upon Event of Default” in this prospectus. These include, among other things:

| • | the failure to pay interest for five days after it is due or to pay principal when it is due on the final maturity date; |

| • | the default in the performance or observance of any covenant or agreement of the issuing entity under the indenture, or any representation or warranty of the issuing entity in the indenture is incorrect in any material respect as of the time it is made, if such default has a material adverse effect on the noteholders and continues unremedied for a period of 60 days after notice to the issuing entity and us by the indenture trustee or any series enhancer, or to the issuing entity, the indenture trustee and us by noteholders of any outstanding series holding at least fifty percent of the outstanding principal amount of such series; or |

12

Table of Contents

| • | an event of bankruptcy, insolvency or similar events relating to the issuing entity or the owner of the trust accounts. |

In the case of an event of default involving bankruptcy, insolvency or similar events relating to the issuing entity or the owner of the trust accounts, the principal amount of the Series 2016-I notes automatically will become immediately due and payable. If any other event of default occurs and continues with respect to the Series 2016-I notes, the indenture trustee or holders of more than 50% of the then-outstanding principal balance of the Series 2016-I notes may declare the principal amount of the Series 2016-I notes to be immediately due and payable. These declarations may be rescinded by holders of more than 50% of the then-outstanding principal balance of the Series 2016-I notes if the related event of default has been cured, subject to the conditions described under “The Indenture—Events of Default; Rights upon Event of Default” in this prospectus.

After an event of default and the acceleration of the Series 2016-I notes, collections allocated to Series 2016-I and the series’ share of funds on deposit in the collection account and the excess funding account will be applied to pay principal of and interest on the Series 2016-I notes to the extent permitted by law. If the indenture trustee sells a portion of the Series 2004-1 certificate (subject to certain conditions) or otherwise collects money or property on behalf of the holders of the Series 2016-I notes, that money or property will be applied first to pay any amounts owed to the indenture trustee pursuant to the indenture and then, to make payments on the Series 2016-I notes.

To the extent the indenture trustee sells a portion of the Series 2004-1 certificate, the portion that may be sold by the indenture trustee is limited to an amount equal to the allocation amount of the Series 2016-I notes. Following such sale and the application of the sale proceeds, amounts then held in the collection account, the excess funding account and any series accounts for the Series 2016-I notes and amounts available under any credit enhancement relating to the Series 2016-I notes pursuant to the indenture, the Series 2016-I notes will no longer be entitled to any allocation of collections or other property constituting the collateral of the issuing entity under the indenture.

Amounts in the spread account will be available to pay interest payments on the Class C notes and the Class D notes, and upon the earlier to occur of the final maturity date, the date the outstanding principal balances of Class A notes and Class B notes are reduced to zero or an event of default and acceleration of the Series 2016-I notes, these amounts will be used to fund any shortfall in principal payments on the Class C notes and Class D notes.

If the Series 2016-I notes are accelerated or the issuing entity fails to pay the principal of the Series 2016-I notes on the final maturity date, subject to the conditions described in this prospectus under “The Indenture—Events of Default; Rights upon Event of Default”, the indenture trustee may, if legally permitted, cause the issuing entity to sell a portion of the Series 2004-1 certificate in an amount equal to the allocation amount for Series 2016-I.

At the option of the servicer, we will purchase your notes when the outstanding principal amount for your series has been reduced to 10% or less of the initial principal amount. See “Description of the Notes—Final Payment of Principal” in this prospectus. The servicer will give the indenture trustee at least thirty days’ prior written notice of the date on which the servicer intends to direct us to make an optional redemption.

The servicer for the master trust is World’s Foremost Bank. World’s Foremost Bank, as servicer, receives a fee for its servicing activities. The issuing entity as the holder of the Series 2004-1 certificate pays the certificateholder servicing fee to the servicer for each transfer date in an amount equal to one-twelfth of the product of (a) 2% and (b) the investor interest for Series 2004-1 on the last day of the prior monthly period. The share of the certificateholder servicing fee allocable to Series 2016-I for each transfer date will be equal to the ratio of the average allocation amount for Series 2016-I during the related month to the average allocation amount for all outstanding series of notes for the related month. The servicing fee allocable to Series 2016-I for each transfer date will be paid from your series’ available funds as described in “—Application of Available Funds” above and in “Description of Series Provisions—Application of Available Funds” in this prospectus.

13

Table of Contents

Fees and Expenses for Asset Review

The asset representations reviewer will be paid an annual fee in accordance with the asset representations review agreement. In addition, following the completion of a review and delivery of the final review report, the asset representations reviewer will be entitled to receive a review fee. The Servicer will pay the annual and review fees of the asset representations reviewer and will reimburse the asset representations reviewer for its reasonable travel expenses for a review.

Subject to important considerations described under “United States Federal Income Tax Consequences” in this prospectus, Kutak Rock LLP, as special federal tax counsel to the issuing entity, is of the opinion that under existing law the Series 2016-I notes (other than the Class D notes and notes retained by the bank or by a person treated as an entity disregarded as separate from the bank for United States federal income tax purposes) will be characterized as debt for federal income tax purposes and that neither the master trust nor the issuing entity will be classified as an association or constitute a publicly traded partnership taxable as a corporation for United States federal income tax purposes. By your acceptance of a Series 2016-I note, you will agree to treat your Series 2016-I notes as debt for United States federal, state and local income and franchise tax purposes. See “United States Federal Income Tax Consequences” in this prospectus for additional information concerning the application of United States federal income tax laws.

Subject to important considerations described under “ERISA Considerations” in this prospectus, the Class A notes are eligible for purchase by persons investing assets of employee benefit plans and retirement accounts, including individual retirement accounts. If you are contemplating purchasing the Series 2016-I notes offered hereunder on behalf of or with plan assets of any plan or retirement account, we suggest that you consult with counsel regarding whether the purchase or holding of such Series 2016-I notes could give rise to a transaction prohibited or not otherwise permissible under Title I of the Employee Retirement Income Security Act of 1974, as amended (“ERISA”) or Section 4975 of the Internal Revenue Code of 1986, as amended, referred to as the “Code” or other applicable state law. Each purchaser that purchases a note offered hereunder will be deemed to represent and warrant that either (i) it is not acquiring the note with assets of (or on behalf of) a benefit plan or any other plan that is subject to the fiduciary responsibility provisions of Title I of ERISA or Section 4975 of the Code, any entity deemed to hold “plan assets” of either of the foregoing or any plan that is subject to any law that is substantially similar to the fiduciary responsibility or prohibited transaction provisions of Title I of ERISA or Section 4975 of the Code, or (ii) its acquisition, holding and disposition of the note will not result in a non-exempt prohibited transaction under ERISA or Section 4975 of the Code or anon-exempt violation of any substantially similar applicable law. See “ERISA Considerations”in this prospectus.

There are material risks associated with an investment in the Series 2016-I notes, and you should consider the matters set forth under “Risk Factors”beginning on page 20 below.

Any rating assigned to the notes by a credit rating agency will reflect the rating agency’s assessment solely of the likelihood that noteholders will receive payments of interest when due and the ultimate payment of principal on the final maturity date. A rating does not address the likelihood of payment of principal of a note on its expected principal payment date. In addition, a rating does not address the possibility of an early payment or acceleration of a note, which would be caused by an early redemption event or an event of default. A rating is based primarily on the rating agency’s evaluation of receivables in the trust and the credit enhancement provided. The rating is not a recommendation to purchase, hold or sell any notes. The rating does not constitute a comment as to the marketability of any notes, any market price or suitability for a particular investor. Ratings on the notes are expected to be monitored by the Hired Agencies while the notes are outstanding. Any rating can be changed or withdrawn by a rating agency at any time. In addition, a rating agency not hired by the depositor to rate the notes may provide an unsolicited rating that differs from (or is lower than) the rating on the notes provided by a Hired Agency.

14

Table of Contents

CUSIP/ISIN Numbers of Offered Notes

The Committee on Uniform Securities Identification Procedures (“CUSIP”) numbers and the International Securities Identification Numbers (“ISIN”) assigned to the offered notes will be as follows:

| Class | CUSIP | ISIN | ||

Class A-1 | 126802DN4 | US126802DN45 | ||

Class A-2 | 126802DP9 | US126802DP92 |

15

Table of Contents

Application of Finance Charge Collections

and Principal Collections Received by World’s Foremost Bank as

Servicer of Cabela’s Master Credit Card Trust

| * | As of the date of this prospectus, there are nine outstanding series of term notes and three outstanding series of variable funding notes. |

16

Table of Contents

Application of Series 2016-I

Available Funds

| * | If the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amount owed) of the amount available. |

17

Table of Contents

| ** | Each outstanding series of variable funding notes and term notes indicated on “Annex II – Other Securities Outstanding” will share excess finance charge collections with Series 2016-I, and any other series of variable funding notes or term notes issued in the future may also share excess finance charge collections with Series 2016-I if such other series is included in group I. |

18

Table of Contents

Application of Series 2016-I

Available Principal Collections

| * | For release on the earlier of the expected principal payment date or the first distribution date of the early redemption period. |

19

Table of Contents

| ** | If the amount available is not sufficient to pay all amounts due to theClass A-1 noteholders and theClass A-2 noteholders, thenClass A-1 andClass A-2 will each receive their pro rata share (based on the amount owed) of the amount available. |

| *** | Each outstanding series of variable funding notes and term notes indicated on “Annex II – Other Securities Outstanding” is a principal sharing series with Series 2016-I, and any other series of variable funding notes or term notes issued in the future may also be a principal sharing series with Series 2016-I if such other series is included in group I. |

This prospectus uses defined terms. You can find a glossary of terms under the caption “Glossary of Terms for Prospectus” beginning on page 132 in this prospectus.

The following is a summary of the principal risk factors that apply to an investment in the notes. You should consider the following risk factors before deciding whether to purchase the Series 2016-I notes.

The ongoing exploration of strategic alternatives by Cabela’s Incorporated may impact its business, the bank or the notes.

On December 2, 2015, Cabela’s Incorporated (“Cabela’s”), the sole shareholder of the bank, announced that its Board of Directors had initiated a process to explore and evaluate a wide range of strategic alternatives to further enhance Cabela’s shareholder value.

That process has continued and is ongoing. The Cabela’s Board of Directors has not set a definitive timetable for the completion of the process. The results of this strategic alternatives review process could include, but are not limited to, a sale of Cabela’s or one of its businesses, including a sale of the bank or its assets, or a transaction combining a sale of the bank or all or a portion of its assets to one or more purchasers and a sale of the parent company (including all of its merchandising business) to one or more other purchasers. Any such transaction could adversely impact Cabela’s business, the bank and the Cabela’s Club program.

A transaction involving the bank or its assets could involve the sale of the bank’s interest in all of its credit card accounts, including those designated to the master trust, and its equity interest in the transferor, along with the transfer of ongoing funding responsibility for the Cabela’s Club program to such a purchaser. Such a transaction could also result in a change in the identity of the servicer or the administrator without your consent. If such a transaction occurs, we do not expect that any purchaser of the Cabela’s Club program would continue to use the issuing entity to access the securitization market to fund the program. As a result, any such transaction could adversely affect the liquidity for the notes. In addition, in connection with a transaction involving the bank, the purchaser or Cabela’s may seek to repurchase some or all of the notes. Any such repurchases may further adversely affect the liquidity for any notes that remain outstanding. If any such repurchases resulted in the outstanding principal amount of the notes being less than 10% of the initial principal amount, the servicer would have the ability to optionally redeem such outstanding notes prior to the expected principal payment date. See, “Structural Summary – Optional Redemptions”.

There can be no assurance that this strategic alternatives review process will result in a sale transaction or other strategic alternative of any kind involving Cabela’s or the bank. Cabela’s does not intend to disclose developments or provide further updates on the progress or status of this process unless it deems further disclosure is appropriate or required.

It may not be possible to find an investor to purchase your notes.

The underwriters may assist in resales of the notes but they are not required to do so. A secondary market for any notes may not develop. If a secondary market does develop, it might not continue or it might not be sufficiently liquid to allow you to resell any of your notes. You may not be able to resell your notes at all, or may be able to do so only at a substantial loss. Events in the financial markets, including increased illiquidity,de-valuation of various

20

Table of Contents

assets in secondary markets and the lowering of ratings on certainasset-backed securities, may adversely affect the liquidity and/or reduce the market price of your notes. You should not purchase the notes unless you understand and know you can bear the investment risk.

Some liens would be given priority over your notes which could cause delayed or reduced payments.

We and the bank intend for the transfer of the receivables to be a sale. However, a court could conclude that we or the bank own the receivables and the trust only holds a security interest. Even if the court would reach this conclusion, however, steps will be taken to give the trust a first-priority, perfected security interest in the receivables.

If a court were to conclude that the trust has only a security interest, a tax or governmental lien or other lien imposed under applicable state or federal law without consent upon our property or the bank’s property arising before receivables are transferred to the trust may be senior to the trust’s interest in the receivables. In addition, the relevant documents permit the bank to transfer the receivables to us subject to liens for taxes that are not yet due or are being contested. Regardless of whether the transfer of the receivables is a sale or a secured borrowing, if any such liens exist, the claims of the creditors holding such liens would be superior to our rights and the rights of the trust, thereby possibly delaying or reducing payments on the notes. Additionally, if a receiver or conservator were appointed for the bank, the fees and expenses of the receiver or conservator might be paid from the receivables before the trust receives any payments on the receivables. In addition, the trust may not have a first-priority perfected security interest in collections that have been commingled with other funds and collections will generally be commingled with other funds of the servicer for two days prior to deposit in a trust account. If any of these events were to occur, payments to you could be delayed or reduced. See “Material Legal Aspects of the Receivables—Matters Relating to Transfer of Receivables” and “Cabela’s Master Credit Card Trust—Representations and Warranties; Required Removal of Receivables” in this prospectus.

In addition, a tax or governmental lien imposed under applicable state or federal law without our consent on our property may be senior to the issuing entity’s interest in the Series 2004-1 certificate.

If a conservator or receiver were appointed for World’s Foremost Bank, or if we become a debtor in a bankruptcy case, delays or reductions in payment of your notes could occur.

If the bank were to become insolvent, or if the bank were to violate laws or regulations applicable to it, the Federal Deposit Insurance Corporation (the “FDIC”) could act as conservator or receiver for the bank. In that role, the FDIC would have broad powers to repudiate contracts to which the bank was party if the FDIC determined that the contracts were burdensome and that repudiation would promote the orderly administration of the bank’s affairs. Among the contracts that might be repudiated are the receivables purchase agreement under which the bank transfers receivables to us and the pooling and servicing agreement under which the bank has agreed to service the receivables. Also, if the FDIC were acting as the bank’s conservator or receiver, the FDIC might have the power to extend its repudiation and avoidance powers to us because we are a wholly-owned subsidiary of the bank.

We have structured the transfer of receivables under the receivables purchase agreement between the bank and us with the intent that they be characterized as legal true sales. If the transfers are so characterized, then the FDIC should not be able to recover or reclaim the transferred receivables using its repudiation powers. However, if those transfers are not respected as legal true sales, then we would be treated as having made a loan to the bank secured by the transferred receivables. The FDIC ordinarily has the power to repudiate secured loans and then recover the collateral after paying damages (as described below) to the lenders.

The FDIC has, however, made statements suggesting that it has the power to recover any asset that is shown on the bank’s balance sheet, and stated that determination of whether or not there has been a legal true sale would take time, possibly causing delays in payment. The transfers of the receivables by the bank to us will not be treated as sales for accounting purposes and the receivables will be shown on the bank’s balance sheet. If the FDIC were to successfully assert the transfer of receivables under the receivables purchase agreement between the bank and us was not a legal true sale, then we would be treated as having made a loan to the bank, secured by the transferred receivables. If the FDIC repudiated that loan, the amount of compensation that the FDIC would be required to pay would be limited to “actual direct compensatory damages,” as determined as of the date of the FDIC’s appointment as conservator or receiver of the bank. There is no statutory definition of “actual direct compensatory damages,” but the term does not include damages for lost profit or opportunity.

21

Table of Contents

The staff of the FDIC takes the position that upon repudiation, these damages would not include interest accrued through the date of actual repudiation, so the issuing entity would receive interest only through the date of appointment of the FDIC as conservator or receiver. The FDIC may repudiate a contract with a “reasonable time” of its appointment and the issuing entity may not have a claim for interest accrued during that period. In addition, in one case involving a repudiation by the Resolution Trust Corporation, a sister agency of the FDIC, of certain secured zero-coupon bonds issued by a savings association, a United States federal district court held that “actual direct compensatory damages” in the case of a market security meant the market value of the repudiated bonds as of the date of repudiation. If the court’s view were applied to determine the “actual compensatory damages” in the circumstances described above, the amount of damages could, depending on the circumstances existing on the date of repudiation, be less than principal amount of the related securities and the interest accrued thereon to the date of payment.

We believe that some of the powers of the FDIC described above have been limited as a result of “safe harbors” adopted by the FDIC in a regulation entitled “Treatment of financial assets in connection with securitization or participation,” which is referred to as the FDIC rule in this prospectus. The FDIC has adopted four different “safe harbors,” each of which limits the powers that the FDIC can exercise in the insolvency of an insured depository institution when it is appointed as receiver or conservator. The relevant safe harbor for the master trust will be the safe harbor for obligations of revolving trusts or master trusts, for which one or more obligations were issued prior to September 27, 2010, and the discussion of the FDIC rule in this prospectus is limited to that safe harbor. Although the FDIC has the power to repeal or amend its own rules, the FDIC rule states that any repeal or amendment of that rule will not apply to transfers of financial assets made before the repeal or modification.

Under the applicable safe harbor, the FDIC has stated that, if certain conditions are met, the FDIC will not use its repudiation power to reclaim, recover or recharacterize as property of an FDIC-insured bank any financial assets transferred by that bank in connection with a securitization transaction. The applicability of the safe harbor to the master trust and the securitizations contemplated by this prospectus requires, among other things, that the transfers of receivables meet the conditions for sale accounting treatment under generally accepted accounting principles in effect for the reporting periods prior to November 15, 2009.

We have structured the issuance of the notes with the intention that the transfers of the receivables by the bank would have the benefit of the safe harbor. The bank believes that the transfers meet these conditions; however, no independent audit or review has been made regarding the bank’s determination that the transfers of receivables made on and after December 31, 2009 meet the conditions for sale accounting treatment under generally accepted accounting principles in effect for the reporting periods prior to November 15, 2009.

If the FDIC (a) were to assert that (i) the FDIC rule does not apply to these transfers of receivables, (ii) these transfers fail to comply with any other condition specified in the FDIC rule or (iii) these transactions do not comply with certain banking laws or, (b) were to (i) require the indenture trustee or other transaction parties to go through an administrative claims procedure established by the FDIC in order to obtain payment on the notes or (ii) request a stay of any actions by any of those parties to enforce the applicable agreement, then payments of principal and interest on your notes could be delayed and, if the FDIC were successful, possibly reduced.

Regardless of whether the FDIC rule applies or the transfers under the receivables purchase agreement between the bank and us are respected as true sales, the FDIC, as receiver or conservator of the bank, could—

| • | require the indenture trustee or any of the other transaction parties to go through the administrative claims procedure established by the FDIC to establish its rights to payments collected on the receivables; |

| • | obtain a stay of any actions by any of those parties to enforce the transaction documents against the bank; |

22

Table of Contents

| • | repudiate the bank’s on-going obligations under the transaction documents, such as the bank’s on-going obligations to service the receivables and its duty to collect and remit payments on the receivables; or |

| • | prior to any repudiation of a servicing agreement, prevent the indenture trustee and other transaction parties from appointing a successor servicer. |

In addition, for 90 days after the FDIC is appointed as receiver or 45 days after the FDIC is appointed as conservator, as applicable, the Federal Deposit Insurance Act (FDIA), in certain circumstances, requires the consent of the FDIC before any party could exercise any right or power to terminate, accelerate or declare a default under any contract to which an insolvent bank is a party. During the same period, the FDIC’s consent would also be needed for any attempt to obtain possession of or exercise control over any property of the bank or affect any contractual rights of the bank.

We are a wholly-owned bankruptcy remote subsidiary of the bank and our limited liability company agreement limits the nature of our business. If, however, we became a debtor in a bankruptcy case, and either our transfer of the receivables to the master trust or our transfer of the Series 2004-1 certificate to the issuing entity were construed as a grant of a security interest to secure a borrowing, your payments of outstanding principal and interest could be delayed and possibly reduced.

Because we are a wholly-owned subsidiary of the bank, certain banking laws and regulations may apply to us, and if we were found to have violated any of these laws or regulations, payments to you could be delayed or reduced. In addition, if the bank entered conservatorship or receivership, the FDIC could seek to exercise control over the receivables, the Series 2004-1 certificate or our other assets on an interim or a permanent basis. Although steps have been taken to minimize this risk, the FDIC could argue that—

| • | our assets (including the receivables and the Series 2004-1 certificate) constitute assets of the bank available for liquidation and distribution by a conservator or receiver for the bank; |

| • | we and our assets (including the receivables and the Series 2004-1 certificate) should be substantively consolidated with the bank and its assets; or |

| • | the FDIC’s control over the receivables or the Series 2004-1 certificate is necessary for the bank to reorganize or to protect the public interest. |

If these or similar arguments were made, whether successfully or not, payments to you could be delayed or reduced. Furthermore, regardless of any decision made by the FDIC or ruling made by a court, the fact that the bank has entered conservatorship or receivership could have an adverse effect on the liquidity and value of the notes.

In the receivership of an unrelated national bank, the FDIC successfully argued that certain of its rights and powers extended to a statutory trust formed and owned by that national bank in connection with a securitization of credit card receivables. If the bank were to enter conservatorship or receivership, the FDIC could argue that its rights and powers extend to us, the master trust or the issuing entity. If the FDIC were to take this position and seek to repudiate or otherwise affect the rights of the indenture trustee, the master trust, the issuing entity or other parties to the transaction under the transaction documents, losses to noteholders could result.

If a conservator or receiver were appointed for the bank, or if we were to become a debtor in a bankruptcy case, an early payment of principal on all outstanding series could result. Under the terms of the agreement that governs the transfer of the receivables from us to the master trust, new principal receivables would not be transferred to the master trust. However, the conservator or the receiver may have the power, regardless of the terms of that agreement, to prevent the early payment of principal or to require new principal receivables to continue being transferred. The conservator or receiver may also have the power to alter the terms of payment on the Series 2004-1 certificate or your notes. In addition, the conservator or receiver would have the power to prevent either the indenture trustee or the noteholders from appointing a new servicer or to direct the servicer to stop servicing the receivables or providing administrative services, or to increase the amount or the priority of the servicing fee or administrative fee due to the bank or otherwise alter the terms under which the bank services the receivables or provides administrative services to us or the issuing entity. See “Material Legal Aspects of the Receivables—Matters Relating to Insolvency and Bankruptcy” in this prospectus.

23

Table of Contents

There may be other provisions in the transaction documents that purport to deal with the bankruptcy or insolvency of the bank, us, the master trust, the issuing entity, or other parties to the transactions, but such provisions may not be enforceable.

Allocations of charged-off receivables or uncovered dilution could reduce payments to you.

The primary risk associated with extending credit under the credit card accounts is the risk of default or bankruptcy of the customer, resulting in the customer’s account balance being charged-off as uncollectible. We rely principally on the customer’s creditworthiness for repayment of the account. The bank may not be able to successfully identify and evaluate the creditworthiness of cardholders to minimize delinquencies and losses.

The rate of charge-offs in the credit card accounts designated to the trust portfolio are subject to a variety of factors which may cause the future rate of charge-offs to differ from current and historical results. These factors include overall conditions in the economy and financial markets, the rate of inflation, unemployment levels, real estate values, mortgage foreclosure rates and interest rates. An increase to the unemployment rate or a decline in housing prices, among other things, could adversely impact the performance of the trust portfolio. An increase in defaults or net charge-offs beyond historical levels will reduce the excess spread available from the trust and could result in a reduction in finance charge collections and the amount of outstanding balances in the trust portfolio. These reductions could result in an early redemption event for your notes or could result in an acceleration of payment or reduced payments on your notes.