| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226850-01 | ||

| Dated November 26, 2018 | BBCMS 2018-C2 |

Free Writing Prospectus Structural and Collateral Term Sheet | ||

BBCMS Mortgage Trust 2018-C2

| ||

$891,853,554 (Approximate Mortgage Pool Balance) | ||

$788,175,578 (Approximate Offered Certificates) | ||

Barclays Commercial Mortgage Securities LLC Depositor | ||

| | ||

COMMERCIAL MORTGAGE PASS-THROUGH CERTIFICATES, SERIES 2018-C2 | ||

| | ||

Barclays Bank PLC Starwood Mortgage Capital LLC Cantor Commercial Real Estate Lending, L.P. KeyBank National Association Mortgage Loan Sellers | ||

| Barclays Co-Lead Manager and Joint Bookrunner | Cantor Fitzgerald & Co. Co-Lead Manager and Joint Bookrunner | |

KeyBanc Capital Markets Co-Manager

| Drexel Hamilton Co-Manager | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

|  |

| Dated November 26, 2018 | BBCMS 2018-C2 |

This material is for your information, and none of Barclays Capital Inc., Cantor Fitzgerald & Co., KeyBanc Capital Markets Inc. and Drexel Hamilton, LLC (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226850) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Barclays Capital Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-888-603-5847. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2018-C2 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 2 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Indicative Capital Structure | ||

Publicly Offered Certificates

| Class | Expected Ratings (S&P / Fitch / DBRS) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Available Certificate Balance or Notional Amount(1) | Approximate Initial Retained Certificate Balance or Notional Amount(1)(2) | Approximate Initial Credit Support(3) | Expected Weighted Avg. Life (years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Underwritten NOI Debt Yield(6) |

| A-1 | AAA(sf) / AAAsf / AAA(sf) | $12,775,374 | $12,286,000 | $489,374 | 30.000% | 2.70 | 1/19 – 5/23 | 41.1% | 16.6% |

| A-2 | AAA(sf) / AAAsf / AAA(sf) | $10,398,254 | $10,000,000 | $398,254 | 30.000% | 4.40 | 5/23 – 5/23 | 41.1% | 16.6% |

| A-3 | AAA(sf) / AAAsf / AAA(sf) | $30,154,934 | $29,000,000 | $1,154,934 | 30.000% | 6.90 | 11/25 – 11/25 | 41.1% | 16.6% |

| A-4 | AAA(sf) / AAAsf / AAA(sf) | (7) | (7) | (7) | 30.000% | (7) | (7) | 41.1% | 16.6% |

| A-5 | AAA(sf) / AAAsf / AAA(sf) | (7) | (7) | (7) | 30.000% | (7) | (7) | 41.1% | 16.6% |

| A-SB | AAA(sf) / AAAsf / AAA(sf) | $34,314,800 | $33,000,000 | $1,314,800 | 30.000% | 7.07 | 5/23 – 4/28 | 41.1% | 16.6% |

| X-A(8) | AAA(sf) / AAAsf / AAA(sf) | $624,297,488 | $600,386,000 | $23,911,488 | N/A | N/A | N/A | N/A | N/A |

| X-B(9) | NR / A-sf / AA(sf) | $163,878,090 | $157,601,000 | $6,277,090 | N/A | N/A | N/A | N/A | N/A |

| A-S | AA(sf) / AAAsf / AAA(sf) | $84,726,087 | $81,481,000 | $3,245,087 | 20.500% | 9.99 | 12/28 – 12/28 | 46.7% | 14.6% |

| B | NR / AA-sf / AA(high)(sf) | $40,133,410 | $38,596,000 | $1,537,410 | 16.000% | 9.99 | 12/28 – 12/28 | 49.3% | 13.8% |

| C | NR / A-sf / AA(low)(sf) | $39,018,593 | $37,524,000 | $1,494,593 | 11.625% | 9.99 | 12/28 – 12/28 | 51.9% | 13.1% |

Privately Offered Certificates(10)

| Class | Expected Ratings (S&P / Fitch / DBRS) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Available Certificate Balance or Notional Amount(1) | Approximate Initial Retained Certificate Balance or Notional Amount(1)(2) | Approximate Initial Credit Support | Expected Weighted Avg. Life (years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Underwritten NOI Debt Yield(6) | |||

| X-D(11) | NR / BBB-sf / BBB(high)(sf) | $43,477,861 | $41,812,000 | $1,665,861 | N/A | N/A | N/A | N/A | N/A | |||

| X-F(12) | NR / BB-sf / BBB(low)(sf) | $20,066,705 | $19,298,000 | $768,705 | N/A | N/A | N/A | N/A | N/A | |||

| X-G(13) | NR / B-sf / BB(low)(sf) | $8,918,535 | $8,576,000 | $342,535 | N/A | N/A | N/A | N/A | N/A | |||

| D | NR / BBBsf / A(sf) | $24,525,973 | $23,586,000 | $939,973 | 8.875% | 9.99 | 12/28 – 12/28 | 53.5% | 12.7% | |||

| E | NR / BBB-sf / BBB(sf) | $18,951,888 | $18,226,000 | $725,888 | 6.750% | 9.99 | 12/28 – 12/28 | 54.7% | 12.4% | |||

| F | NR / BB-sf / BB(high)(sf) | $20,066,705 | $19,298,000 | $768,705 | 4.500% | 9.99 | 12/28 – 12/28 | 56.1% | 12.1% | |||

| G | NR / B-sf / B(high)(sf) | $8,918,535 | $8,576,000 | $342,535 | 3.500% | 9.99 | 12/28 – 12/28 | 56.6% | 12.0% | |||

| H-RR | NR / NR / B(low)(sf) | $7,803,719 | $7,504,000 | $299,719 | 2.625% | 9.99 | 12/28 – 12/28 | 57.2% | 11.9% | |||

| J-RR | NR / NR / NR | $23,411,156 | $22,514,000 | $897,156 | 0.000% | 9.99 | 12/28 – 12/28 | 58.7% | 11.6% | |||

| (1) | In the case of each such Class, subject to a permitted variance of plus or minus 5%, including in connection with any variation in the certificate balances and notional amounts of the classes comprising the VRR Interest following the calculation of the actual fair value of the ABS interests (as such term is defined in Regulation RR) issued by the issuing entity. |

| (2) | On the Closing Date, SMC will cause a majority-owned affiliate to purchase from the underwriters the certificates (other than the Class S and Class R certificates) with the initial certificate balances or notional amounts, as applicable, as set forth in the table above under “Approximate Initial Retained Certificate Balance or Notional Amount” as well as an approximately 3.83% interest in the Class S certificates, as further described in “Credit Risk Retention” in the Preliminary Prospectus. |

| (3) | The credit support percentages set forth for Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates represent the approximate initial credit support for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates in the aggregate. |

| (4) | Assumes 0% CPR / 0% CDR and a December 20, 2018 closing date. Based on modeling assumptions as described in the Preliminary Prospectus dated November 27, 2018 (the “Preliminary Prospectus”). |

| (5) | The “Certificate Principal to Value Ratio” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates. The Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificate Principal to Value Ratios are calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (6) | The “Underwritten NOI Debt Yield” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage loans and (b) the total initial Certificate Balance of all of the Classes of Principal Balance Certificates divided by the total initial Certificate Balance for such Class and all Classes of Principal Balance Certificates senior to such Class of Certificates. The Underwritten NOI Debt Yield for each of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 3 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Indicative Capital Structure | ||

| (7) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and expected principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial available certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $516,100,000, subject to a variance of plus or minus 5%. |

| Class of Certificates | Expected Range of Initial Certificate Balance | Expected Range of Initial Available Certificate Balance | Expected Range of Initial Retained Certificate Balance | Expected Range of Weighted Avg. Life (Yrs) | Expected Principal | |||||

| Class A-4 | $103,982,531 – $249,558,075 | $100,000,000 – $240,000,000 | $3,982,531 – $9,558,075 | 9.59 – 9.71 | 4/28 – 8/28 / 4/28 – 10/28 | |||||

| Class A-5 | $287,096,051 – $432,671,595 | $276,100,000 – $416,100,000 | $10,996,051 – $16,571,595 | 9.87 – 9.84 | 10/28 – 12/28 / 8/28 – 12/28 |

| (8) | The Notional Amount of the Class X-A Certificates will be equal to the aggregate Certificate Balance of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates outstanding from time to time. |

| (9) | The Notional Amount of the Class X-B Certificates will be equal to the aggregate Certificate Balance of the Class A-S, Class B and Class C Certificates outstanding from time to time. |

| (10) | The Class X-D, Class X-F, Class X-G, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates are not being offered by the Preliminary Prospectus and this Term Sheet. The Class S and Class R Certificates are not shown above. |

| (11) | The Notional Amount of the Class X-D Certificates will be equal to the aggregate Certificate Balance of the Class D and Class E Certificates outstanding from time to time. |

| (12) | The Notional Amount of the Class X-F Certificates will be equal to the Certificate Balance of the Class F Certificates outstanding from time to time. |

| (13) | The Notional Amount of the Class X-G Certificates will be equal to the Certificate Balance of the Class G Certificates outstanding from time to time. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 4 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Summary of Transaction Terms | ||

| Securities Offered: | $788,175,578 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Co-Lead Managers and Joint Bookrunners: | Barclays Capital Inc. and Cantor Fitzgerald & Co.. |

| Co-Managers: | KeyBanc Capital Markets Inc. and Drexel Hamilton, LLC |

| Mortgage Loan Sellers: | Starwood Mortgage Capital LLC (“SMC”) (34.0%), Barclays Bank PLC (“Barclays”) (33.6%), Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (16.9%), and KeyBank National Association (“KeyBank”) (15.4%). |

| Master Servicer: | Wells Fargo Bank, National Association. |

| Special Servicer: | LNR Partners, LLC (“LNR”). |

| Directing Certificateholder: | LNR Securities Holdings, LLC (or its affiliate). |

| Trustee: | Wilmington Trust, National Association. |

| Certificate Administrator: | Wells Fargo Bank, National Association. |

| Operating Advisor: | Park Bridge Lender Services LLC. |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC. |

| Rating Agencies: | S&P Global Ratings, acting through Standard & Poor’s Financial Services LLC (“S&P”), Fitch Ratings, Inc. (“Fitch”) and DBRS, Inc. (“DBRS”). |

| U.S. Credit Risk Retention: | SMC, an indirect wholly-owned subsidiary of Starwood Property Trust, Inc., is expected to act as the “retaining sponsor” for this securitization and intends to satisfy the U.S. credit risk retention requirements (i) through the purchase by Starwood Conduit CMBS Vertical Retention I LLC, a “majority-owned affiliate,” of an “eligible vertical interest” (each as defined in Regulation RR), which will consist of approximately 3.83% of the certificate balance, notional amount or percentage interest of each class of certificates (other than the Class R Certificates) (the “VRR Interest”) issued by the issuing entity and (ii) through the purchase by Starwood Conduit CMBS Horizontal BBCMS 2018-C2 LLC, a “majority-owned affiliate,” of an “eligible horizontal residual interest” (each as defined in Regulation RR), which will consist of the portion of the Class H-RR and Class J-RR Certificates not included in the VRR Interest.

SMC, in its capacity as the “retaining sponsor” for this transaction, will be required to comply with the hedging, transfer and financing restrictions applicable to a “retaining sponsor” under the credit risk retention rules, which generally prohibit the transfer of the applicable certificates except to a “majority-owned affiliate” of the “retaining sponsor”. The restrictions on hedging and transfer under the credit risk retention rules as in effect on the closing date of this transaction will expire on and after the date that is the latest of (i) the date on which the aggregate principal balance of the mortgage loans has been reduced to 33% of the aggregate principal balance of the mortgage loans as of the Cut-off Date; (ii) the date on which the total unpaid principal obligations under the certificates has been reduced to 33% of the aggregate total unpaid principal obligations under the certificates as of the Closing Date; or (iii) two years after the Closing Date.

For additional information, see “Credit Risk Retention” in the Preliminary Prospectus.

|

| EU Credit Risk Retention: | The transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Closing Date: | On or about December 20, 2018. |

| Cut-off Date: | With respect to each mortgage loan, the related due date in December 2018, or with respect to any mortgage loan that has its first due date in January 2019, the date that would otherwise have been the related due date in December 2018. |

| Distribution Date: | The 4th business day after the Determination Date in each month, commencing in January 2019. |

| Determination Date: | 11thday of each month, or if the 11th day is not a business day, the next succeeding business day, commencing in January 2019. |

| Assumed Final Distribution Date: | The Distribution Date in December 2028 which is the latest anticipated repayment date of the Certificates. |

| Rated Final Distribution Date: | The Distribution Date in December 2051. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC “regular interests” for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class X-A, Class X-B, Class A-S, Class B and Class C Certificates (the “Publicly Offered Certificates”) will be offered publicly. The Class X-D, Class X-F, Class X-G, Class D, Class E, Class F, Class G, Class H-RR, Class J-RR, Class S and Class R Certificates (the “Privately Offered Certificates”) will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The Certificates will not constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 5 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Summary of Transaction Terms | ||

| Optional Termination: | On any Distribution Date on which the aggregate principal balance of the pool of mortgage loans is less than 1% of the aggregate principal balance of the mortgage loans as of the cut-off date, certain entities specified in the Preliminary Prospectus will have the option to purchase all of the remaining mortgage loans (and all property acquired through exercise of remedies in respect of any mortgage loan) at the price specified in the Preliminary Prospectus. Refer to “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus. |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B Certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B Certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| Analytics: | The transaction is expected to be modeled by Intex Solutions, Inc. and Trepp, LLC and is expected to be available on Bloomberg L.P., BlackRock Financial Management, Inc., Interactive Data Corporation, CMBS.com, Inc., Markit Group Limited, Moody’s Analytics, MBS Data, LLC and Thomson Reuters Corporation. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. REFER TO THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 6 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate | % of IPB |

| SMC | 16 | 46 | $303,274,768 | 34.0% |

| Barclays | 16 | 19 | 274,947,456 | 30.8 |

| KeyBank | 5 | 11 | 137,656,330 | 15.4 |

| CCRE | 6 | 9 | 125,975,000 | 14.1 |

| Barclays/CCRE(1) | 1 | 2 | 50,000,000 | 5.6 |

| Total: | 44 | 87 | $891,853,554 | 100.0% |

| (1) | In the case of Loan No. 4, Barclays is acting as loan seller with respect to Note A-4 with a principal balance of $25,000,000, and CCRE is acting as loan seller with respect to Note A-6 with a principal balance of $25,000,000. |

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $891,853,554 | |

| Number of Mortgage Loans: | 44 | |

| Number of Mortgaged Properties: | 87 | |

| Average Cut-off Date Balance per Mortgage Loan: | $20,269,399 | |

| Weighted Average Current Mortgage Rate: | 4.99123% | |

| 10 Largest Mortgage Loans as % of IPB: | 48.8% | |

| Weighted Average Remaining Term to Maturity(1): | 116 months | |

| Weighted Average Seasoning: | 1 month | |

| Credit Statistics | ||

| Weighted Average UW NCF DSCR(2)(3): | 1.95x | |

| Weighted Average UW NOI Debt Yield(2): | 11.6% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(2)(4): | 58.7% | |

| Weighted Average Maturity Date/ARD LTV(1)(2)(4): | 55.0% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 12.6% | |

| % of Mortgaged Properties with Single Tenants: | 16.2% | |

| Amortization | ||

| Weighted Average Original Amortization Term(5): | 359 months | |

| Weighted Average Remaining Amortization Term(5): | 359 months | |

| % of Mortgage Loans with Interest-Only: | 47.6% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 36.2% | |

| % of Mortgage Loans with Amortizing Balloon: | 12.8% | |

| % of Mortgage Loans with Interest-Only followed by ARD-Structure: | 3.4% | |

| Lockboxes(6) | ||

| % of Mortgage Loans with Hard Lockboxes: | 52.3% | |

| % of Mortgage Loans with Springing Lockboxes: | 36.3% | |

| % of Mortgage Loans with Soft Lockboxes: | 7.9% | |

| % of Mortgage Loans with No Lockbox: | 3.6% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 73.6% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 48.1% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves(7): | 71.4% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(8): | 34.8% | |

| (1) | In the case of Loan No. 10 with an anticipated repayment date, as of the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 10, 11, 12, 13, 14, 16, 19, 23, 24 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | In the case of Loan No. 30, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 3, 11.02, 12, 16 and 41, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (5) | Excludes 17 mortgage loans that are interest-only for the entire term or until the anticipated repayment date, as applicable. |

| (6) | For a more detailed description of Lockboxes, refer to “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (7) | CapEx Reserves include FF&E reserves for hotel properties. |

| (8) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, mixed use and industrial properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 7 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Ten Largest Mortgage Loans | |||||||||||||

| No. | Loan Name | City, State | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms | Property Type | UW NCF DSCR(1) | UW NOI Debt Yield(1) | Cut-off Date LTV(1)(2) | Maturity Date/ARD LTV(1)(2)(3) | |

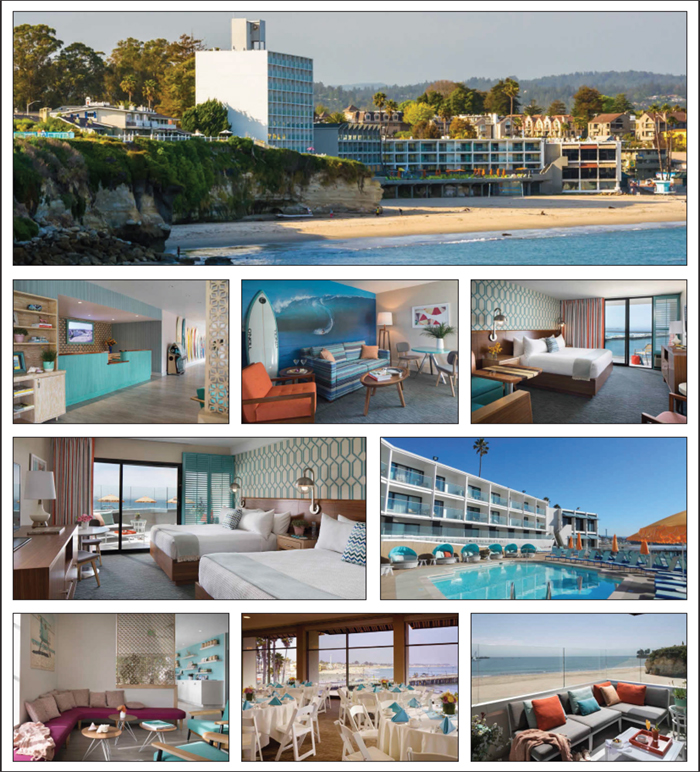

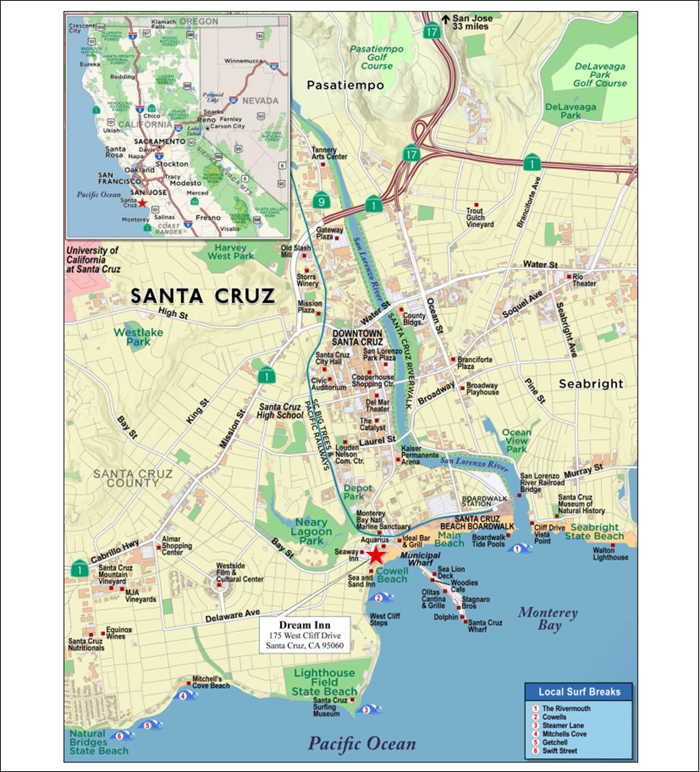

| 1 | Dream Inn | Santa Cruz, CA | KeyBank | 1 | $55,000,000 | 6.2% | 165 | Hotel | 2.38x | 13.3% | 55.0% | 55.0% | |

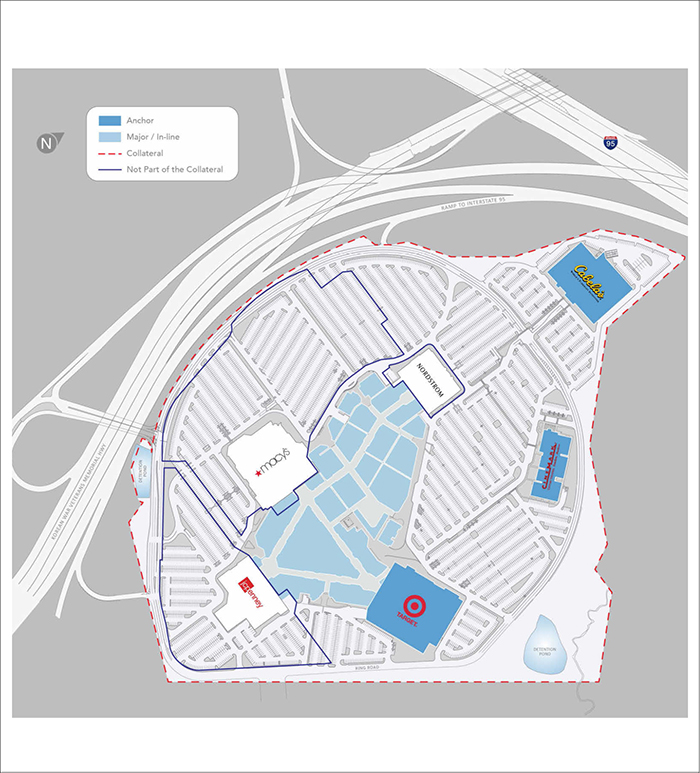

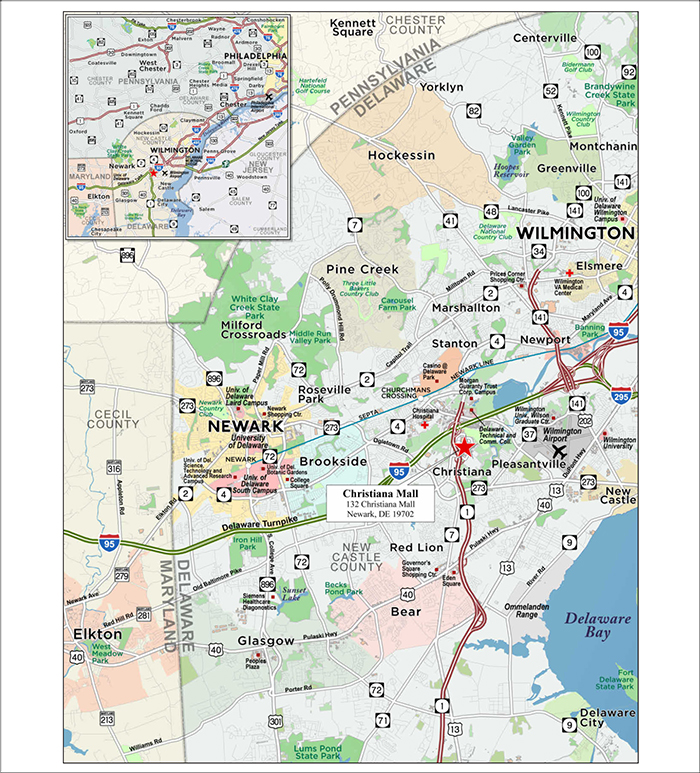

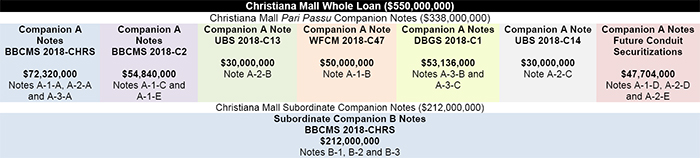

| 2 | Christiana Mall | Newark, DE | Barclays | 1 | $54,840,000 | 6.1% | 779,084 | Retail | 3.15x | 13.8% | 32.5% | 32.5% | |

| 3 | GNL Portfolio | Various, Various | KeyBank | 7 | $54,175,000 | 6.1% | 647,713 | Various | 2.08x | 11.0% | 57.2% | 57.2% | |

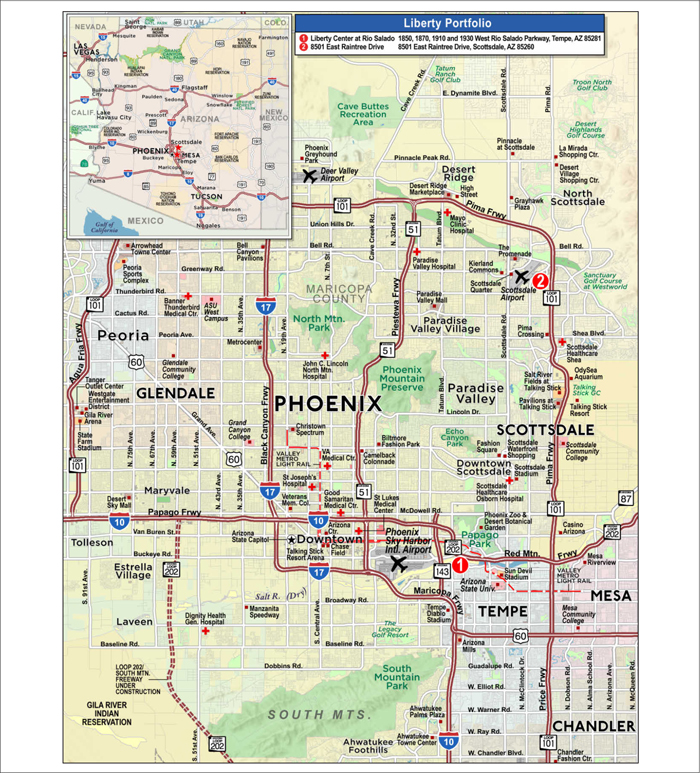

| 4 | Liberty Portfolio | Various, AZ | Barclays/CCRE | 2 | $50,000,000 | 5.6% | 805,746 | Office | 1.77x | 9.1% | 64.6% | 64.6% | |

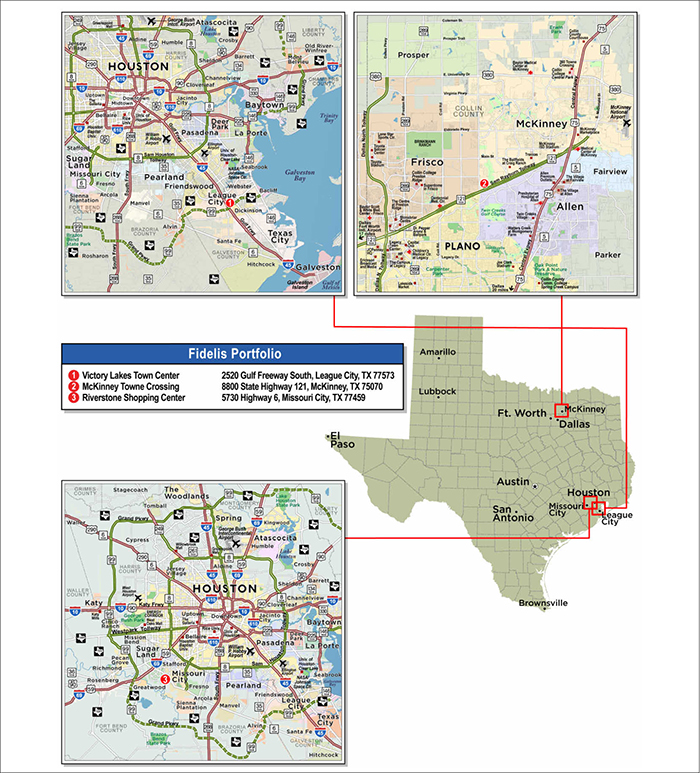

| 5 | Fidelis Portfolio | Various, TX | SMC | 3 | $49,188,389 | 5.5% | 885,707 | Retail | 1.74x | 11.9% | 63.7% | 52.5% | |

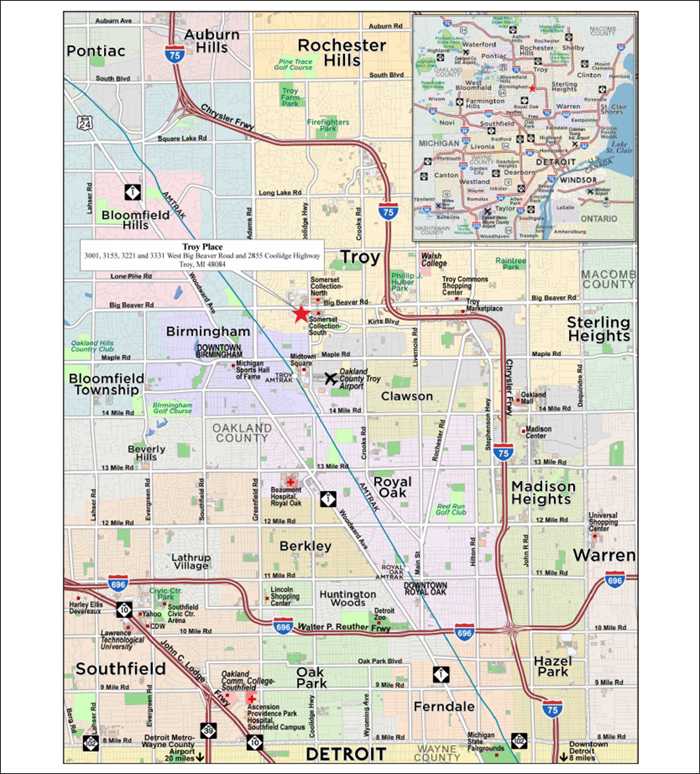

| 6 | Troy Place | Troy, MI | SMC | 1 | $40,000,000 | 4.5% | 756,845 | Office | 2.47x | 15.2% | 53.0% | 53.0% | |

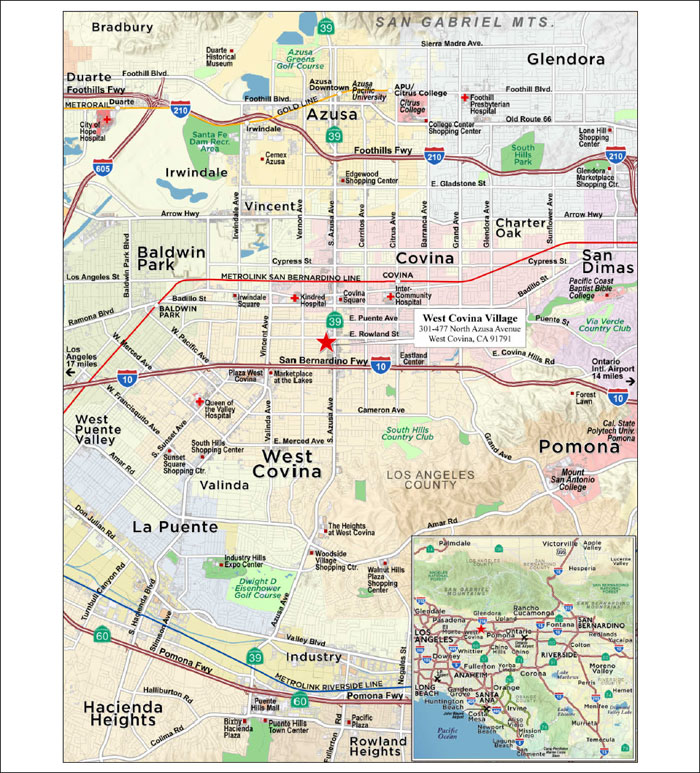

| 7 | West Covina Village | West Covina, CA | SMC | 1 | $36,000,000 | 4.0% | 220,000 | Mixed Use | 1.37x | 10.0% | 58.4% | 53.3% | |

| 8 | AVR Embassy Suites Fort Worth | Fort Worth, TX | CCRE | 1 | $35,200,000 | 3.9% | 156 | Hotel | 1.70x | 12.9% | 64.6% | 60.1% | |

| 9 | Residence Inn by Marriott Phoenix Desert View at Mayo Clinic | Phoenix, AZ | SMC | 1 | $31,000,000 | 3.5% | 208 | Hotel | 1.56x | 12.3% | 59.5% | 52.2% | |

| 10 | Home Depot Technology Center | Marietta, GA | Barclays | 1 | $30,000,000 | 3.4% | 347,498 | Office | 1.77x | 9.3% | 66.5% | 66.5% | |

| Top 3 Total/Weighted Average | 9 | $164,015,000 | 18.4% | 2.54x | 12.7% | 48.2% | 48.2% | ||||||

| Top 5 Total/Weighted Average | 14 | $263,203,389 | 29.5% | 2.24x | 11.9% | 54.2% | 52.1% | ||||||

| Top 10 Total/Weighted Average | 19 | $435,403,389 | 48.8% | 2.07x | 12.0% | 56.5% | 53.9% | ||||||

| Non-Top 10 Total/Weighted Average | 68 | $456,450,165 | 51.2% | 1.84x | 11.3% | 60.7% | 55.9% | ||||||

| (1) | In the case of Loan Nos. 2, 3, 4, 5 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan No. 2, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | In the case of Loan No. 3, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (3) | In the case of Loan No.10 with an anticipated repayment date, Maturity Date/ARD LTV is calculated as of the related anticipated repayment date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 8 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Pari Passu Loan(s) Cut-off Date Balance | Total Mortgage Loan Cut-off Date Balance(1) | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Control Rights |

| 2 | Christiana Mall | Barclays | $54,840,000 | $283,160,000 | $338,000,000 | BBCMS 2018-CHRS | Wells Fargo | Wells Fargo | BBCMS 2018-CHRS |

| 3 | GNL Portfolio | KeyBank | $54,175,000 | $44,325,000 | $98,500,000 | BBCMS 2018-C2 | Wells Fargo | LNR | BBCMS 2018-C2 |

| 4 | Liberty Portfolio | Barclays/CCRE | $50,000,000 | $115,700,000 | $165,700,000 | BMARK 2018-B7 | KeyBank | LNR | BMARK 2018-B7 |

| 5 | Fidelis Portfolio | SMC | $49,188,389 | $44,898,124 | $94,086,513 | BBCMS 2018-C2 | Wells Fargo | LNR | BBCMS 2018-C2 |

| 10 | Home Depot Technology Center | Barclays | $30,000,000 | $14,300,000 | $44,300,000 | BBCMS 2018-C2 | Wells Fargo | LNR | BBCMS 2018-C2 |

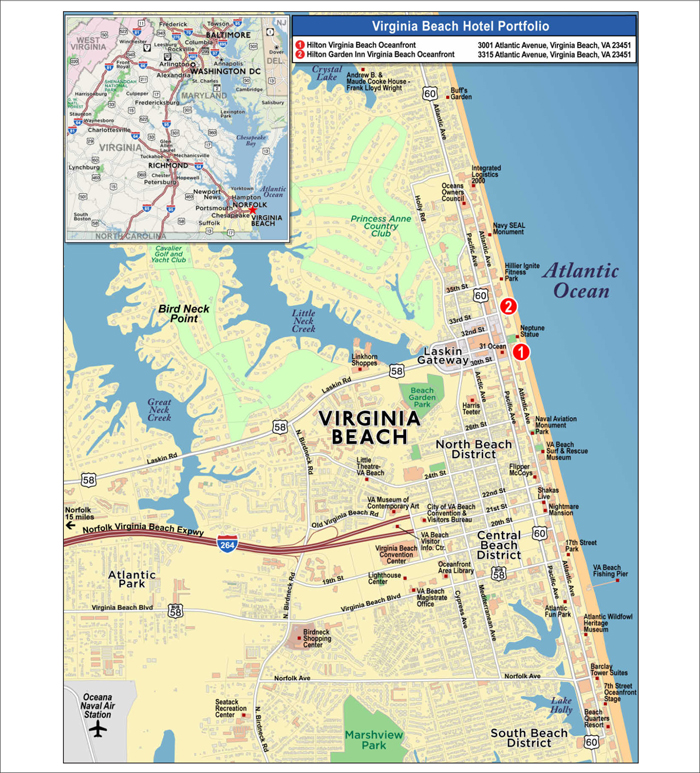

| 11 | Virginia Beach Hotel Portfolio | Barclays | $30,000,000 | $60,000,000 | $90,000,000 | WFCM 2018-C47 | Wells Fargo | Midland | WFCM 2018-C47 |

| 12 | Moffett Towers - Buildings E,F,G | CCRE | $25,000,000 | $259,000,000 | $284,000,000 | DBGS 2018-C1 | Wells Fargo | Rialto | DBGS 2018-C1 |

| 13 | Shelbourne Global Portfolio II | CCRE | $25,000,000 | $30,000,000 | $55,000,000 | BBCMS 2018-C2 | Wells Fargo | LNR | BBCMS 2018-C2 |

| 14 | Zenith Ridge | SMC | $25,000,000 | $65,000,000 | $90,000,000 | CD 2018-CD7 | KeyBank | Rialto | CD 2018-CD7 |

| 16 | Moffett Towers II - Building 1 | Barclays | $22,000,000 | $146,000,000 | $168,000,000 | BMARK 2018-B6 | KeyBank | Midland | BMARK 2018-B6 |

| 19 | The Shops at Solaris | CCRE | $20,000,000 | $50,000,000 | $70,000,000 | BMARK 2018-B7 | KeyBank | LNR | BMARK 2018-B7 |

| 23 | One River Place | Barclays | $15,000,000 | $10,000,000 | $25,000,000 | BBCMS 2018-C2 | Wells Fargo | LNR | BBCMS 2018-C2 |

| 24 | Alex Park South | KeyBank | $14,900,000 | $28,000,000 | $42,900,000 | MSC 2018-L1 | Midland | Midland | MSC 2018-L1 |

| 30 | Fair Oaks Mall | Barclays | $10,918,207 | $162,780,537 | $173,698,743 | BANK 2018-BNK12 | Wells Fargo | Midland | BANK 2018-BNK12(2) |

| (1) | In the case of Loan Nos. 2 and 30, the Total Mortgage Loan Cut-off Date Balance excludes the related Subordinate Companion Loans. |

| (2) | Currently exercised by Annaly CRE LLC, as holder of the Subordinate Companion Loans until the occurrence and during the a Fair Oaks Mall B Note Control Appraisal Period, as described under “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Fair Oaks Mall Whole Loan—Consultation and Control”in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 9 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Additional Debt Summary |

No. | Loan Name | Trust | Pari Passu Loan(s) Cut-off Date Balance | Subordinate Debt Cut-off Date Balance(1) | Total Debt Cut-off Date Balance | Mortgage Loan UW NCF DSCR(2) | Total Debt UW NCF DSCR | Mortgage Loan | Total Debt Cut-off Date LTV(3) | Mortgage Loan UW NOI Debt Yield(2) | Total Debt UW NOI Debt Yield |

| 2 | Christiana Mall | $54,840,000 | $283,160,000 | $212,000,000 | $550,000,000 | 3.15x | 1.93x | 32.5% | 52.9% | 13.8% | 8.5% |

| 12 | Moffett Towers - Buildings E,F,G | $25,000,000 | $259,000,000 | $216,000,000 | $500,000,000 | 2.97x | 1.41x | 40.2% | 70.8% | 12.6% | 7.2% |

| 16 | Moffett Towers II - Building 1 | $22,000,000 | $146,000,000 | $112,000,000 | $280,000,000 | 2.00x | 1.17x | 46.8% | 78.1% | 11.5% | 6.9% |

| 30 | Fair Oaks Mall | $10,918,207 | $162,780,537 | $84,367,961 | $258,066,704 | 2.89x | 1.64x | 31.8% | 47.3% | 17.2% | 11.6% |

| (1) | In the case of Loan Nos. 2 and 30, subordinate debt represents one or more Subordinate Companion Loans. In the case of Loan Nos. 12 and 16, subordinate debt represents one or more mezzanine loans. |

| (2) | In the case of Loan Nos. 2 and 30, Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI Debt Yield calculations include any related Pari Passu Companion Loans, but exclude the related Subordinate Companion Loans. |

| (3) | In the case of Loan Nos. 12 and 16, the Mortgage Loan Cut-off Date LTV and the Total Cut-off Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 10 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

Weighted Average | ||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date/ARD LTV(2)(4)(5) |

| Office | Suburban | 16 | $293,453,992 | 32.9% | 1.90x | 11.1% | 60.4% | 58.4% |

| CBD | 2 | 27,482,682 | 3.1 | 2.89x | 12.5% | 41.7% | 41.7% | |

| R&D Lab | 2 | 9,325,975 | 1.0 | 2.08x | 11.0% | 57.2% | 57.2% | |

| Subtotal: | 20 | $330,262,649 | 37.0% | 1.99x | 11.2% | 58.8% | 57.0% | |

| Retail | Anchored | 9 | $123,850,605 | 13.9% | 1.73x | 11.2% | 65.0% | 57.9% |

| Super Regional Mall | 2 | 65,758,207 | 7.4 | 3.11x | 14.4% | 32.4% | 32.0% | |

| Lifestyle Center | 1 | 20,000,000 | 2.2 | 2.46x | 11.1% | 46.7% | 46.7% | |

| Unanchored | 1 | 6,750,000 | 0.8 | 1.76x | 9.9% | 56.3% | 56.3% | |

| Freestanding | 1 | 5,016,614 | 0.6 | 1.65x | 9.5% | 59.0% | 59.0% | |

| Subtotal: | 14 | $221,375,426 | 24.8% | 2.21x | 12.1% | 53.2% | 49.2% | |

| Hotel | Full Service | 4 | $120,200,000 | 13.5% | 2.05x | 13.1% | 61.3% | 57.6% |

| Extended Stay | 1 | 31,000,000 | 3.5 | 1.56x | 12.3% | 59.5% | 52.2% | |

| Limited Service | 3 | 19,478,007 | 2.2 | 2.04x | 15.3% | 59.8% | 48.9% | |

| Subtotal: | 8 | $170,678,007 | 19.1% | 1.96x | 13.2% | 60.8% | 55.7% | |

| Mixed Use | Retail/Office | 2 | $57,025,000 | 6.4% | 1.37x | 9.7% | 62.2% | 57.2% |

| Office/Industrial | 1 | 16,454,545 | 1.8 | 1.89x | 11.4% | 58.7% | 58.7% | |

| Subtotal: | 3 | $73,479,545 | 8.2% | 1.49x | 10.1% | 61.4% | 57.5% | |

| Multifamily | Garden | 26 | $37,462,498 | 4.2% | 1.64x | 10.0% | 60.9% | 57.7% |

| Mid-Rise | 2 | 2,217,502 | 0.2 | 2.00x | 10.7% | 59.9% | 59.9% | |

| Subtotal: | 28 | $39,680,000 | 4.4% | 1.66x | 10.1% | 60.8% | 57.9% | |

| Industrial | Warehouse | 4 | $20,730,540 | 2.3% | 1.50x | 10.9% | 70.5% | 61.1% |

| Flex | 5 | 16,397,846 | 1.8 | 1.45x | 10.6% | 69.8% | 58.0% | |

| Warehouse/Distribution | 1 | 1,949,543 | 0.2 | 2.08x | 11.0% | 57.2% | 57.2% | |

| Subtotal: | 10 | $39,077,928 | 4.4% | 1.51x | 10.8% | 69.5% | 59.6% | |

| Self Storage | Self Storage | 4 | $17,300,000 | 1.9% | 1.42x | 9.7% | 64.0% | 56.0% |

| Total / Weighted Average: | 87 | $891,853,554 | 100.0% | 1.95x | 11.6% | 58.7% | 55.0% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 10, 11, 12, 13, 14, 16, 19, 23, 24 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2 and 30 the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | In the case of Loan No. 30, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. Nos. 3, 11.02, 12, 16 and 41, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (5) | In the case of Loan No.10 with an anticipated repayment date, Maturity Date/ARD LTV are calculated as of the related anticipated repayment date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 11 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) |

Weighted Average | ||||||||||

State | Number of Properties | Cut-off Date | % of | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date/ARD LTV(2)(4)(5) | |||

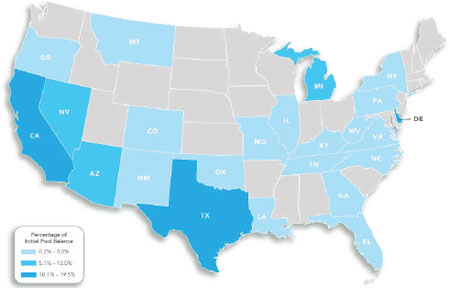

| California | 8 | $174,075,607 | 19.5% | 2.11x | 11.8% | 52.9% | 51.0% | |||

| Texas | 12 | 122,366,276 | 13.7 | 1.75x | 12.0% | 63.2% | 55.7% | |||

| Delaware | 4 | 94,840,000 | 10.6 | 2.72x | 13.1% | 42.3% | 42.3% | |||

| Arizona | 3 | 81,000,000 | 9.1 | 1.69x | 10.3% | 62.6% | 59.9% | |||

| Nevada | 4 | 66,935,000 | 7.5 | 1.43x | 9.8% | 69.5% | 63.4% | |||

| Michigan | 4 | 54,025,000 | 6.1 | 2.16x | 13.7% | 56.9% | 54.7% | |||

| Virginia | 3 | 40,918,207 | 4.6 | 2.12x | 14.2% | 59.1% | 51.6% | |||

| Illinois | 27 | 40,709,114 | 4.6 | 1.71x | 10.4% | 66.1% | 61.9% | |||

| Georgia | 3 | 39,200,000 | 4.4 | 1.69x | 9.4% | 65.4% | 63.7% | |||

| Pennsylvania | 3 | 33,400,625 | 3.7 | 1.60x | 10.8% | 67.5% | 61.2% | |||

| West Virginia | 1 | 24,700,000 | 2.8 | 2.11x | 11.6% | 60.3% | 60.3% | |||

| Colorado | 1 | 20,000,000 | 2.2 | 2.46x | 11.1% | 46.7% | 46.7% | |||

| Missouri | 2 | 15,765,731 | 1.8 | 1.73x | 11.2% | 66.5% | 60.7% | |||

| Tennessee | 2 | 15,565,137 | 1.7 | 1.85x | 13.4% | 66.9% | 55.2% | |||

| New York | 1 | 14,900,000 | 1.7 | 1.32x | 10.1% | 65.0% | 58.1% | |||

| Oregon | 1 | 13,400,000 | 1.5 | 2.24x | 11.0% | 59.3% | 59.3% | |||

| Louisiana | 2 | 11,000,000 | 1.2 | 1.51x | 9.7% | 55.3% | 53.3% | |||

| North Carolina | 1 | 8,500,000 | 1.0 | 1.72x | 12.8% | 59.4% | 49.5% | |||

| Oklahoma | 1 | 5,584,686 | 0.6 | 1.32x | 9.8% | 68.9% | 57.5% | |||

| Florida | 1 | 5,400,000 | 0.6 | 1.84x | 10.4% | 56.8% | 56.8% | |||

| New Mexico | 1 | 4,308,386 | 0.5 | 1.65x | 9.5% | 59.0% | 59.0% | |||

| Kentucky | 1 | 3,310,244 | 0.4 | 2.08x | 11.0% | 57.2% | 57.2% | |||

| Montana | 1 | 1,949,543 | 0.2 | 2.08x | 11.0% | 57.2% | 57.2% | |||

| Total / Weighted Average: | 87 | $891,853,554 | 100.0% | 1.95x | 11.6% | 58.7% | 55.0% | |||

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 10, 11, 12, 13, 14, 16, 19, 23, 24 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2 and 30 the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | In the case of Loan No. 30, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. Nos. 3, 11.02, 12, 16 and 41, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (5) | In the case of Loan No.10 with an anticipated repayment date, Maturity Date/ARD LTV are calculated as of the related anticipated repayment date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 12 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) |

| Interest Only | 17 | $454,245,000 | 50.9% | 4.83891% | 116 | 2.27x | 11.8% | 53.7% | 53.7% |

| 300 | 1 | 3,994,200 | 0.4 | 5.96900% | 119 | 2.22x | 19.0% | 53.3% | 41.3% |

| 360 | 26 | 433,614,354 | 48.6 | 5.14179% | 117 | 1.61x | 11.3% | 63.9% | 56.4% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% |

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) | ||

| Interest Only | 17 | $454,245,000 | 50.9% | 4.83891% | 116 | 2.27x | 11.8% | 53.7% | 53.7% | ||

| 299 | - | 300 | 1 | 3,994,200 | 0.4 | 5.96900% | 119 | 2.22x | 19.0% | 53.3% | 41.3% |

| 353 | - | 360 | 26 | 433,614,354 | 48.6 | 5.14179% | 117 | 1.61x | 11.3% | 63.9% | 56.4% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% | ||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) |

| Interest Only | 16 | $424,245,000 | 47.6% | 4.82745% | 119 | 2.31x | 12.0% | 52.8% | 52.8% |

| IO-Balloon | 19 | 323,047,500 | 36.2 | 5.17295% | 118 | 1.55x | 11.0% | 64.6% | 58.0% |

| Balloon | 8 | 114,561,054 | 12.8 | 5.08275% | 112 | 1.80x | 12.6% | 61.7% | 51.3% |

| ARD-Interest Only | 1 | 30,000,000 | 3.4 | 5.00100% | 83 | 1.77x | 9.3% | 66.5% | 66.5% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(2)(4) |

| Weighted Average | |||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) | ||

| 1.29x | - | 1.39x | 7 | $121,777,179 | 13.7% | 5.35812% | 119 | 1.35x | 9.7% | 64.7% | 57.8% |

| 1.40x | - | 1.49x | 5 | 49,643,830 | 5.6 | 5.24425% | 118 | 1.42x | 10.1% | 71.6% | 62.4% |

| 1.50x | - | 1.59x | 6 | 98,385,000 | 11.0 | 5.20346% | 118 | 1.54x | 11.1% | 64.2% | 58.0% |

| 1.60x | - | 1.69x | 2 | 15,242,942 | 1.7 | 5.22013% | 119 | 1.66x | 10.5% | 63.8% | 58.9% |

| 1.70x | 1.79x | 6 | 179,638,389 | 20.1 | 5.07708% | 113 | 1.75x | 10.8% | 64.1% | 59.7% | |

| 1.80x | - | 1.99x | 4 | 63,400,000 | 7.1 | 5.23251% | 118 | 1.87x | 12.2% | 62.6% | 58.0% |

| 2.00x | - | 2.99x | 13 | 308,926,214 | 34.6 | 4.75431% | 116 | 2.34x | 12.7% | 52.8% | 52.1% |

| 3.00x | - | 3.15x | 1 | 54,840,000 | 6.1 | 4.27750% | 116 | 3.15x | 13.8% | 32.5% | 32.5% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% | ||

| (1) | In the case of Loan No. 10 with an anticipated repayment date, as of the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 10, 11, 12, 13, 14, 16, 19, 23, 24 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | In the case of Loan Nos. 3, 11.02, 12, 16 and 41, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (4) | In the case of Loan No. 30, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 13 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(2)(3) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) | ||

| 31.8% | - | 49.9% | 6 | $135,758,207 | 15.2% | 4.22339% | 111 | 2.78x | 13.1% | 38.5% | 37.6% |

| 50.0% | - | 59.9% | 16 | 331,699,200 | 37.2 | 5.16646% | 120 | 2.01x | 12.0% | 56.5% | 54.8% |

| 60.0% | - | 64.9% | 7 | 183,322,196 | 20.6 | 5.07653% | 118 | 1.78x | 11.2% | 63.8% | 58.8% |

| 65.0% | - | 69.9% | 11 | 191,793,509 | 21.5 | 5.09136% | 112 | 1.54x | 10.4% | 67.9% | 61.4% |

| 70.0% | - | 75.0% | 4 | 49,280,442 | 5.5 | 5.21995% | 119 | 1.48x | 10.6% | 73.7% | 64.2% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% | ||

| LTV Ratios as of the Maturity Date/ARD(1)(2)(3) |

Weighted Average | |||||||||||

| Range of Maturity Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) | ||

| 29.7% | - | 49.9% | 9 | $150,752,407 | 16.9% | 4.35450% | 112 | 2.69x | 13.2% | 40.3% | 38.5% |

| 50.0% | - | 54.9% | 7 | 186,072,196 | 20.9 | 5.20519% | 119 | 1.87x | 12.5% | 58.0% | 52.4% |

| 55.0% | - | 59.9% | 17 | 304,656,452 | 34.2 | 5.12469% | 119 | 1.87x | 11.3% | 61.2% | 57.7% |

| 60.0% | - | 64.9% | 8 | 191,010,000 | 21.4 | 5.03260% | 118 | 1.68x | 10.6% | 65.9% | 62.5% |

| 65.0% | - | 66.6% | 3 | 59,362,500 | 6.7 | 5.11946% | 101 | 1.59x | 9.6% | 70.7% | 66.2% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) |

| Defeasance | 36 | $688,212,986 | 77.2% | 5.04957% | 116 | 1.93x | 11.7% | 59.0% | 55.6% |

| Yield Maintenance | 6 | 156,640,568 | 17.6 | 5.02629% | 119 | 1.84x | 11.1% | 61.7% | 56.3% |

| Defeasance or Yield Maintenance | 2 | $47,000,000 | 5.3 | 4.02004% | 115 | 2.52x | 12.1% | 43.3% | 41.4% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3)(4) | UW NOI DY(2) | Cut-off Date LTV(2)(3) | Maturity Date/ARD LTV(1)(2)(3) |

| Refinance | 27 | $542,747,544 | 60.9% | 4.96347% | 117 | 2.14x | 12.2% | 54.3% | 52.0% |

| Acquisition | 15 | 324,606,010 | 36.4 | 5.10931% | 115 | 1.63x | 10.6% | 66.8% | 60.8% |

| Recapitalization | 2 | 24,500,000 | 2.7 | 4.04152% | 113 | 1.95x | 11.4% | 47.4% | 43.0% |

| Total / Weighted Average: | 44 | $891,853,554 | 100.0% | 4.99123% | 116 | 1.95x | 11.6% | 58.7% | 55.0% |

| (1) | In the case of Loan No. 10 with an anticipated repayment date, as of the related anticipated repayment date. |

| (2) | In the case of Loan Nos. 2, 3, 4, 5, 10, 11, 12, 13, 14, 16, 19, 23, 24 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2 and 30, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loan. |

| (3) | In the case of Loan Nos. 3, 11.02, 12, 16 and 41, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (4) | In the case of Loan No. 30, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 14 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Collateral Characteristics | ||

| Previous Securitization History(1) |

| No. | Mortgage Loan Seller | Loan Name | Location | Property Type | Cut-off Date Principal Balance | % of IPB | Previous Securitization |

| 2 | Barclays | Christiana Mall | Newark, DE | Retail | $54,840,000 | 6.1% | MSC 2011-C1 |

| 7 | SMC | West Covina Village | West Covina, CA | Mixed Use | $36,000,000 | 4.0% | CSMC 2006-C5 |

| 8 | CCRE | AVR Embassy Suites Fort Worth | Fort Worth, TX | Hotel | $35,200,000 | 3.9% | WFCM 2010-C1 |

| 9 | SMC | Residence Inn by Marriott Phoenix Desert View at Mayo Clinic | Phoenix, AZ | Hotel | $31,000,000 | 3.5% | UBSBB 2012-C3 |

| 11 | Barclays | Virginia Beach Hotel Portfolio | Virginia Beach, VA | Hotel | $30,000,000 | 3.4% | JPMBB 2014-C21 |

| 12 | CCRE | Moffett Towers - Buildings E,F,G | Sunnyvale, CA | Office | $25,000,000 | 2.8% | COMM 2013-CR8 |

| 19 | CCRE | The Shops at Solaris | Vail, CO | Retail | $20,000,000 | 2.2% | CFCRE 2011-C2 |

| 21.01 | SMC | 808 West 76th Street | Chicago, IL | Multifamily | $1,423,397 | 0.2% | GSMS 2012-GC6 |

| 21.02 | SMC | 6000 South Prairie Avenue | Chicago, IL | Multifamily | $1,228,616 | 0.1% | GSMS 2012-GCJ9 |

| 21.03 | SMC | 9244 South Saginaw Avenue | Chicago, IL | Multifamily | $1,153,700 | 0.1% | GSMS 2012-GCJ9 |

| 21.04 | SMC | 4853 South Prairie Avenue | Chicago, IL | Multifamily | $1,063,802 | 0.1% | GSMS 2012-GCJ9 |

| 21.05 | SMC | 7348 South Dr. Martin Luther King Jr. Drive | Chicago, IL | Multifamily | $973,903 | 0.1% | GSMS 2012-GCJ9 |

| 21.06 | SMC | 7944 South Paulina Street | Chicago, IL | Multifamily | $958,920 | 0.1% | GSMS 2012-GC6 |

| 21.07 | SMC | 7801 South Saginaw Avenue | Chicago, IL | Multifamily | $794,105 | 0.1% | GSMS 2012-GCJ9 |

| 21.08 | SMC | 8200 South Ingleside Avenue | Chicago, IL | Multifamily | $779,122 | 0.1% | GSMS 2012-GCJ9 |

| 21.09 | SMC | 1514 West 77th Street | Chicago, IL | Multifamily | $764,139 | 0.1% | GSMS 2012-GC6 |

| 21.10 | SMC | 8000 South Drexel Avenue | Chicago, IL | Multifamily | $764,139 | 0.1% | GSMS 2012-GCJ9 |

| 21.11 | SMC | 8001 South Marshfield Avenue | Chicago, IL | Multifamily | $734,173 | 0.1% | GSMS 2012-GC6 |

| 21.12 | SMC | 1717 West 77th Street | Chicago, IL | Multifamily | $689,224 | 0.1% | GSMS 2012-GC6 |

| 21.13 | SMC | 1815 West 77th Street | Chicago, IL | Multifamily | $659,257 | 0.1% | GSMS 2012-GC6 |

| 21.14 | SMC | 1704 West 77th Street | Chicago, IL | Multifamily | $629,291 | 0.1% | GSMS 2012-GC6 |

| 21.15 | SMC | 1738 West 77th Street | Chicago, IL | Multifamily | $614,308 | 0.1% | GSMS 2012-GC6 |

| 21.16 | SMC | 8231 South Ellis Avenue | Chicago, IL | Multifamily | $599,325 | 0.1% | GSMS 2012-GCJ9 |

| 21.17 | SMC | 1735 West 79th Street | Chicago, IL | Multifamily | $569,359 | 0.1% | GSMS 2012-GC6 |

| 21.18 | SMC | 1448 West 83rd Street | Chicago, IL | Multifamily | $554,376 | 0.1% | GSMS 2012-GC6 |

| 21.19 | SMC | 8155 South Maryland Avenue | Chicago, IL | Multifamily | $554,376 | 0.1% | GSMS 2012-GCJ9 |

| 21.20 | SMC | 8515 South Green Street | Chicago, IL | Multifamily | $494,443 | 0.1% | GSMS 2012-GC6 |

| 21.21 | SMC | 8001 South Carpenter Street | Chicago, IL | Multifamily | $449,494 | 0.1% | GSMS 2012-GC6 |

| 21.22 | SMC | 7914 South Kingston Avenue | Chicago, IL | Multifamily | $449,494 | 0.1% | GSMS 2012-GCJ9 |

| 21.23 | SMC | 8255 South Maryland Avenue | Chicago, IL | Multifamily | $449,494 | 0.1% | GSMS 2012-GCJ9 |

| 21.24 | SMC | 8514 South Crandon Avenue | Chicago, IL | Multifamily | $404,544 | 0.0% | GSMS 2012-GCJ9 |

| 28 | Barclays | Bridgeport Center | Tigard, OR | Office | $13,400,000 | 1.5% | JPMBB 2013-C15 |

| 29 | SMC | Southern Highlands Corporate Center | Las Vegas, NV | Office | $12,250,000 | 1.4% | GSMS 2007-GG10 |

| 32 | KeyBank | Marketplace Center at Murfreesboro | Murfreesboro, TN | Retail | $8,581,330 | 1.0% | FORT CRE 2016-1 |

| (1) | The table above represents the properties for which the previously existing debt was most recently securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 15 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 |

| Class A-2(1) | |

No. | Loan Name | Location | Cut-off Date Balance | % of | Maturity Date/ARD Balance | % of Certificate Class(2) | Original Loan Term | Remaining Loan Term | UW NCF | UW NOI Debt | Cut-off Date | Maturity Date/ARD |

| 30 | Fair Oaks Mall | Fairfax, VA | $10,918,207 | 1.2% | $10,193,150 | 98.0% | 60 | 53 | 2.89x | 17.2% | 31.8% | 29.7% |

| Total / Weighted Average: | $10,918,207 | 1.2% | $10,193,150 | 98.0% | 60 | 53 | 2.89x | 17.2% | 31.8% | 29.7% | ||

| (1) | The table above presents the mortgage loan whose balloon payment would be applied to pay down the certificate balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each Class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Maturity Date/ARD Balance divided by the initial Class A-2 Certificate Balance. |

| (3) | The UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the Cut-off Date based on the assumed principal payment schedule provided on Annex F to the Preliminary Prospectus. |

| (4) | The UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loans. The UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 16 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Class A-3(1) | ||

No. | Loan Name | Location | Cut-off Date Balance | % of | Maturity Date/ARD Balance | % of Certificate Class(2) | Original Loan Term | Remaining Loan Term | UW NCF | UW NOI Debt | Cut-off Date | Maturity Date/ARD |

| 10 | Home Depot Technology Center | Marietta, GA | $30,000,000 | 3.4% | $30,000,000 | 99.5% | 84 | 83 | 1.77x | 9.3% | 66.5% | 66.5% |

| Total / Weighted Average: | $30,000,000 | 3.4% | $30,000,000 | 99.5% | 84 | 83 | 1.77x | 9.3% | 66.5% | 66.5% | ||

| (1) | The table above presents the mortgage loan whose balloon payment would be applied to pay down the certificate balance of the Class A-3 Certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each Class of Certificates, including the Class A-3 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Maturity Date/ARD Balance divided by the initial Class A-3 Certificate Balance. |

| (3) | The UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 17 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Structural Overview | ||

| ■ Accrual: | Each Class of Certificates (other than the Class S and Class R Certificates) will accrue interest on a 30/360 basis. The Class S and Class R Certificates will not accrue interest. On each Distribution Date, any excess interest collected in respect of any mortgage loan in the trust with an anticipated repayment date, solely to the extent received from the related borrower during the related collection period will be distributed to the holders of the Class S Certificates. | |

| ■ Distribution of Interest: | On each Distribution Date, accrued interest for each Class of Certificates (other than the Class S and Class R Certificates) at the applicable pass-through rate will be distributed in the following order of priority to the extent of available funds: first, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class X-A, Class X-B, Class X-D, Class X-F and Class X-G Certificates (the “Senior Certificates”), on apro rata basis, based on the interest entitlement for each such Class on such date, and then to the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates, in that order, in each case until the interest entitlement for such date payable to each such Class is paid in full.

The pass-through rate applicable to each of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates on each Distribution Date, will be aper annum rate equal to one of (i) a fixed rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), (iii) the lesser of a specified fixed pass-through rate and the rate described in clause (ii) above or (iv) the rate described in clause (ii) above less a specified percentage.

The pass-through rate for the Class X-A Certificates for any Distribution Date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the weighted average of the pass-through rates on the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates for the related Distribution Date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to that Distribution Date.

The pass-through rate for the Class X-B Certificates for any Distribution Date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the weighted average of the pass-through rates on the Class A-S, Class B and Class C Certificates for the related Distribution Date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to the Distribution Date.

The pass-through rate for the Class X-D Certificates for any Distribution Date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the weighted average of the pass-through rates on the Class D and Class E Certificates for the related Distribution Date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to the Distribution Date.

The pass-through rate for the Class X-F Certificates for any Distribution Date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the pass-through rate on the Class F Certificates for the related Distribution Date.

The pass-through rate for the Class X-G Certificates for any Distribution Date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the pass-through rate on the Class G Certificates for the related Distribution Date.

The Class S Certificates will not have a pass-through rate. On each Distribution Date, any excess interest collected in respect of any mortgage loan in the trust with an anticipated |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 18 | |

| Structural and Collateral Term Sheet | BBCMS 2018-C2 | |

| Structural Overview | ||

| repayment date, solely to the extent received from the related borrower during the related collection period, will be distributed to the holders of the Class S Certificates.

See “Description of the Certificates—Distributions” in the Preliminary Prospectus. | ||

| ■ Distribution of Principal: | On any Distribution Date prior to the Cross-Over Date, payments in respect of principal of the Certificates will be distributed:

first, to the Class A-SB Certificates until the Certificate Balance of the Class A-SB Certificates is reduced to the Class A-SB planned principal balance for the related Distribution Date set forth in Annex E to the Preliminary Prospectus, second, to the Class A-1 Certificates, until the Certificate Balance of such Class is reduced to zero, third, to the Class A-2 Certificates, until the Certificate Balance of such Class is reduced to zero, fourth, to the Class A-3 Certificates, until the Certificate Balance of such Class is reduced to zero, fifth, to the Class A-4 Certificates, until the Certificate Balance of such Class is reduced to zero, sixth, to the Class A-5 Certificates, until the Certificate Balance of such Class is reduced to zero and seventh, to the Class A-SB Certificates, until the Certificate Balance of such Class is reduced to zero and then to the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates, in that order, until the Certificate Balance of each such Class is reduced to zero.

On any Distribution Date on or after the Cross-Over Date, payments in respect of principal of the Certificates will be distributed to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates,pro rata based on the Certificate Balance of each such Class until the Certificate Balance of each such Class is reduced to zero.

The “Cross-Over Date” means the Distribution Date on which the aggregate Certificate Balances of the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates have been reduced to zero as a result of the allocation of realized losses to such Classes.

The Class X-A, Class X-B, Class X-D, Class X-F and Class X-G Certificates (the “Class X Certificates”) will not be entitled to receive distributions of principal; however, the notional amount of the Class X-A Certificates will be reduced by the aggregate amount of principal distributions, realized losses and trust fund expenses, if any, allocated to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-SB Certificates, the notional amount of the Class X-B Certificates will be reduced by the aggregate amount of principal distributions, realized losses and trust fund expenses, if any, allocated to the Class A-S, Class B and Class C Certificates, the notional amount of the Class X-D Certificates will be reduced by the aggregate amount of principal distributions, realized losses and trust fund expenses, if any, allocated to the Class D and Class E Certificates, the notional amount of the Class X-F Certificates will be reduced by the amount of principal distributions, realized losses and trust fund expenses, if any, allocated to the Class F Certificates and the notional amount of the Class X-G Certificates will be reduced by the amount of principal distributions, realized losses and trust fund expenses, if any, allocated to the Class G Certificates.

The Class S Certificates have no certificate balance, notional amount, credit support, pass-through rate, rated final distribution date or rating, and will not be entitled to distributions of principal. The Class S Certificates are entitled to distributions of excess interest collected on the mortgage loan with an anticipated repayment date solely to the extent received from the related borrower and will represent beneficial ownership of the grantor trust, as further described in “Description of the Certificates—Distributions” in the Preliminary Prospectus.

| |

| ■ Yield Maintenance / Fixed Penalty Allocation: | For purposes of the distribution of Yield Maintenance Charges on any Distribution Date, Yield Maintenance Charges collected in respect of the mortgage loans will first be allocated pro rata among four groups (based on the aggregate amount of principal distributed to the Principal Balance Certificates in each group), consisting of (a) the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-SB, and Class X-A Certificates (“YM Group A”), (b) the Class A-S, Class B, Class C and Class X-B Certificates (“YM Group BC”), (c) the Class D, Class E and Class X-D Certificates (“YM Group DE”), (d) the Class F and Class X-F Certificates (“YM Group F”), (e) the Class G and Class X-G Certificates (“YM Group G”) and (f) the Class H-RR and the Class J-RR Certificates (“YM Group HJ-RR”). As among the Classes of Certificates in each YM |