| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226850-02 | ||

| Dated May 13, 2019 | BBCMS 2019-C3 |

Free Writing Prospectus Structural and Collateral Term Sheet | |||

BBCMS Mortgage Trust 2019-C3

| |||

$936,649,542 (Approximate Mortgage Pool Balance) | |||

$823,080,000 (Approximate Offered Certificates) | |||

Barclays Commercial Mortgage Securities LLC Depositor

| |||

Commercial Mortgage Pass-Through Certificates, Series 2019-C3

| |||

Barclays Capital Real Estate Inc. Societe Generale Financial Corporation KeyBank National Association UBS AG Natixis Real Estate Capital LLC Rialto Mortgage Finance, LLC Mortgage Loan Sellers

| |||

| Barclays | Natixis | Société Générale | UBS Securities LLC |

| Co-Lead Managers and Joint Bookrunners | |||

KeyBanc Capital Markets Co-Manager

|

| Drexel Hamilton Co-Manager

| |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| Dated May 13, 2019 | BBCMS 2019-C3 |

This material is for your information, and none of Barclays Capital Inc., SG Americas Securities, LLC, UBS Securities LLC, Natixis Securities Americas LLC, KeyBanc Capital Markets Inc. and Drexel Hamilton, LLC (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226850) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Barclays Capital Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-888-603-5847. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2019-C3 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Indicative Capital Structure | ||

Publicly Offered Certificates

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| A-1 | AAA(sf) / AAAsf / AAA(sf) | $16,654,000 | 30.000% | 2.88 | 7/19-2/24 | 42.1% | 16.0% |

| A-2 | AAA(sf) / AAAsf / AAA(sf) | $30,000,000 | 30.000% | 4.68 | 2/24-2/24 | 42.1% | 16.0% |

| A-3 | AAA(sf) / AAAsf / AAA(sf) | (6) | 30.000% | (6) | (6) | 42.1% | 16.0% |

| A-4 | AAA(sf) / AAAsf / AAA(sf) | (6) | 30.000% | (6) | (6) | 42.1% | 16.0% |

| A-SB | AAA(sf) / AAAsf / AAA(sf) | $36,000,000 | 30.000% | 7.02 | 2/24-8/28 | 42.1% | 16.0% |

| X-A | AAA(sf) / AAAsf / AAA(sf) | $655,654,000(7) | N/A | N/A | N/A | N/A | N/A |

| X-B | NR / A-sf / AAA(sf) | $167,426,000(8) | N/A | N/A | N/A | N/A | N/A |

| A-S | AA(sf) / AAAsf / AAA(sf) | $87,811,000 | 20.625% | 9.90 | 4/29-5/29 | 47.8% | 14.1% |

| B | NR / AA-sf / AA(sf) | $39,808,000 | 16.375% | 9.93 | 5/29-5/29 | 50.3% | 13.4% |

| C | NR / A-sf / A-(sf) | $39,807,000 | 12.125% | 9.93 | 5/29-5/29 | 52.9% | 12.7% |

Privately Offered Certificates(9)

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Credit Support(2) | Expected Weighted Avg. Life (years)(3) | Expected Principal Window(3) | Certificate Principal to Value Ratio(4) | Underwritten NOI Debt Yield(5) |

| X-D | NR / BBBsf / BBB+(sf) | $18,349,000(10) | N/A | N/A | N/A | N/A | N/A |

| D | NR / BBBsf / BBB+(sf) | $18,349,000 | 10.166% | 9.93 | 5/29-5/29 | 54.1% | 12.5% |

| E-RR | NR / BBB-sf / BBB-(sf) | $27,313,000 | 7.250% | 9.93 | 5/29-5/29 | 55.8% | 12.1% |

| F-RR | NR / BB+sf / BB+(sf) | $11,708,000 | 6.000% | 9.93 | 5/29-5/29 | 56.6% | 11.9% |

| G-RR | NR / BB-sf / BB-(sf) | $10,537,000 | 4.875% | 9.93 | 5/29-5/29 | 57.3% | 11.8% |

| H-RR | NR / B-sf / B(sf) | $9,367,000 | 3.875% | 9.93 | 5/29-5/29 | 57.9% | 11.7% |

| J-RR | NR / NR / NR | $36,295,542 | 0.000% | 9.93 | 5/29-5/29 | 60.2% | 11.2% |

| (1) | In the case of each such Class, subject to a permitted variance of plus or minus 5%. In addition, the notional amounts of the Class X-A, Class X-B and Class X-D Certificates may vary depending upon the final pricing of the Classes of Principal Balance Certificates whose Certificate Balances comprise such notional amounts, and, if as a result of such pricing the pass-through rate of any Class of the Class X-A, Class X-B or Class X-D Certificates, as applicable, would be equal to zero at all times, such Class of Certificates will not be issued on the closing date of this securitization. |

| (2) | The credit support percentages set forth for Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates represent the approximate initial credit support for the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates in the aggregate. |

| (3) | Assumes 0% CPR / 0% CDR and a June 11, 2019 closing date. Based on modeling assumptions as described in the Preliminary Prospectus dated May 13, 2019 (the “Preliminary Prospectus”). |

| (4) | The “Certificate Principal to Value Ratio” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates. The Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificate Principal to Value Ratios are calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (5) | The “Underwritten NOI Debt Yield” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage loans and (b) the total initial Certificate Balance of all of the Classes of Principal Balance Certificates divided by the total initial Certificate Balance for such Class and all Classes of Principal Balance Certificates senior to such Class of Certificates. The Underwritten NOI Debt Yield for each of the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

| (6) | The exact initial certificate balances of the Class A-3 and Class A-4 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, weighted average lives and expected principal windows of the Class A-3 and Class A-4 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial available certificate balance of the Class A-3 and Class A-4 certificates is expected to be approximately $573,000,000, subject to a variance of plus or minus 5%. |

| Class of Certificates | Expected Range of Approximate Initial Certificate Balance | Expected Range of Weighted Avg. Life (Yrs) | Expected Range of Principal Window | |

| Class A-3 | $100,000,000 – $325,000,000 | 9.40 – 9.61 | 8/28-11/28 – 8/28-4/29 | |

| Class A-4 | $248,000,000 – $473,000,000 | 9.77 – 9.84 | 4/29-4/29 – 11/28-4/29 |

| (7) | The Notional Amount of the Class X-A Certificates will be equal to the aggregate Certificate Balance of the Class A-1, Class A-2, Class A-3, Class A-4 and Class A-SB Certificates outstanding from time to time. |

| (8) | The Notional Amount of the Class X-B Certificates will be equal to the aggregate Certificate Balance of the Class A-S, Class B and Class C Certificates outstanding from time to time. |

| (9) | The Class X-D, Class D, Class E-RR, Class F-RR, Class G-RR, Class H-RR and Class J-RR Certificates are not being offered by the Preliminary Prospectus and this Term Sheet. The Class R Certificates are not shown above. |

| (10) | The Notional Amount of the Class X-D Certificates will be equal to the aggregate Certificate Balance of the Class D outstanding from time to time. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Summary of Transaction Terms | ||

| Securities Offered: | $823,080,000 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Co-Lead Managers and Joint Bookrunners: | Barclays Capital Inc., SG Americas Securities, LLC, UBS Securities LLC, and Natixis Securities Americas LLC. |

| Co-Managers: | KeyBanc Capital Markets Inc. and Drexel Hamilton, LLC. |

| Mortgage Loan Sellers: | Barclays Capital Real Estate Inc. (“Barclays”) (29.7%), Societe Generale Financial Corporation (“SGFC”) (28.5%), KeyBank National Association (“KeyBank”) (13.0%), UBS AG (“UBS”) (12.7%), Natixis Real Estate Capital LLC (“Natixis”) (9.9%) and Rialto Mortgage Finance, LLC (“Rialto”) (6.2%). |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association. |

| Special Servicer: | Midland Loan Services, a Division of PNC Bank, National Association. |

| Directing Certificateholder: | KKR Real Estate Credit Opportunity Partners Aggregator I L.P. (or its affiliate). |

| Trustee: | Wells Fargo Bank, National Association. |

| Certificate Administrator: | Wells Fargo Bank, National Association. |

| Operating Advisor: | Pentalpha Surveillance LLC. |

| Asset Representations Reviewer: | Pentalpha Surveillance LLC. |

| Rating Agencies: | S&P Global Ratings, acting through Standard & Poor’s Financial Services LLC (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, Inc. (“KBRA”). |

| U.S. Credit Risk Retention: | Barclays Capital Real Estate Inc., is expected to act as the “retaining sponsor” for this securitization and intends to satisfy the U.S. credit risk retention requirements (i) through the purchase by KKR Real Estate Credit Opportunity Partners (AIV) Aggregator I L.P., a “majority-owned affiliate” of the “third party purchaser” (each as defined in the credit risk retention rules), which is expected to be KKR Real Estate Credit Opportunity Partners Aggregator I L.P. of the Class E-RR, Class F-RR, Class G-RR, Class H-RR and Class J-RR certificates (collectively, the “Horizontal Risk Retention Certificates”) with an estimated aggregate initial Certificate Balance of $95,220,542 and representing approximately 5.03% of the aggregate fair value of the certificates (other than the Class R Certificates) as of the Closing Date. The Horizontal Risk Retention Certificates will constitute an “eligible horizontal residual interest” (as such term is defined in the credit risk retention rules).

The third party purchaser will be required to comply with the hedging, transfer and financing restrictions applicable to a “retaining sponsor” under the credit risk retention rules, which generally prohibit the transfer of the applicable certificates except to a “majority-owned affiliate” of the “retaining sponsor”. The restrictions on hedging and transfer under the credit risk retention rules as in effect on the closing date of this transaction will expire on and after the date that is the latest of (i) the date on which the aggregate principal balance of the mortgage loans has been reduced to 33% of the aggregate principal balance of the mortgage loans as of the Cut-off Date; (ii) the date on which the total unpaid principal obligations under the certificates has been reduced to 33% of the aggregate total unpaid principal obligations under the certificates as of the Closing Date; or (iii) two years after the Closing Date.

For additional information, see “Credit Risk Retention” in the Preliminary Prospectus.

|

| EU Credit Risk Retention: | None of the sponsors, the depositor or any other party to the transaction intends to retain a material net economic interest in the securitization constituted by the issue of the certificates in a manner that would satisfy the requirements of the European Union Regulation (EU) 2017/2402. In addition, no such person undertakes to take any other action which may be required by any investor for the purposes of its compliance with any applicable requirement under such Regulation. Furthermore, the transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Closing Date: | On or about June 11, 2019. |

| Cut-off Date: | With respect to each mortgage loan, the related due date in June 2019, or in the case of any mortgage loan that has its first due date after June 2019, the date that would have been its due date in June 2019 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month. |

| Distribution Date: | The 4th business day after the Determination Date in each month, commencing in July 2019. |

| Determination Date: | 11th day of each month, or if the 11th day is not a business day, the next succeeding business day, commencing in July 2019. |

| Assumed Final Distribution Date: | The Distribution Date in May 2029 which is the latest anticipated repayment date of the Certificates. |

| Rated Final Distribution Date: | The Distribution Date in May 2052. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC “regular interests” for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class X-A, Class X-B, Class A-S, Class B and Class C Certificates (the “Publicly Offered Certificates”) will be offered publicly. The Class X-D, Class D, Class E-RR, Class F-RR, Class G-RR, Class H-RR, Class J-RR and Class R Certificates (the “Privately Offered Certificates”) will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The Certificates will not constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Summary of Transaction Terms | ||

| Optional Termination: | On any Distribution Date on which the aggregate principal balance of the pool of mortgage loans is less than 1% of the aggregate principal balance of the mortgage loans as of the cut-off date, certain entities specified in the Preliminary Prospectus will have the option to purchase all of the remaining mortgage loans (and all property acquired through exercise of remedies in respect of any mortgage loan) at the price specified in the Preliminary Prospectus. Refer to “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus. |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B Certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B Certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| Analytics: | The transaction is expected to be modeled by Intex Solutions, Inc. and Trepp, LLC and is expected to be available on Bloomberg L.P., BlackRock Financial Management, Inc., Interactive Data Corp., CMBS.com, Inc., Markit Group Limited, Moody’s Analytics, MBS Data, LLC and Thomson Reuters Corporation. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. REFER TO THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of | Number of Mortgaged | Aggregate | % of IPB |

| Barclays | 13 | 35 | $278,095,779 | 29.7% |

| SGFC | 16 | 75 | $266,778,013 | 28.5% |

| KeyBank | 6 | 15 | $122,025,999 | 13.0% |

| UBS AG | 7 | 378 | $119,096,111 | 12.7% |

| Natixis | 3 | 6 | $92,626,787 | 9.9% |

| RMF | 5 | 8 | $58,026,853 | 6.2% |

| Total: | 50 | 517 | $936,649,542 | 100.0% |

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $936,649,542 | |

| Number of Mortgage Loans: | 50 | |

| Number of Mortgaged Properties: | 517 | |

| Average Cut-off Date Balance per Mortgage Loan: | $18,732,991 | |

| Weighted Average Current Mortgage Rate: | 4.80232% | |

| 10 Largest Mortgage Loans as % of IPB: | 45.4% | |

| Weighted Average Remaining Term to Maturity: | 115 months | |

| Weighted Average Seasoning: | 3 months | |

| Credit Statistics | ||

| Weighted Average UW NCF DSCR(1)(2): | 1.93x | |

| Weighted Average UW NOI Debt Yield(1)(3): | 11.2% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(1)(4): | 60.2% | |

| Weighted Average Maturity Date LTV(1)(4): | 56.0% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 18.8% | |

| % of Mortgaged Loans with Single Tenants(5): | 14.7% | |

| % of Mortgaged Loans secured by multiple Properties: | 42.2% | |

| Amortization | ||

| Weighted Average Original Amortization Term(6): | 358 months | |

| Weighted Average Remaining Amortization Term(6): | 357 months | |

| % of Mortgage Loans with Interest-Only: | 52.9% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 34.0% | |

| % of Mortgage Loans with Amortizing Balloon: | 13.1% | |

| Lockboxes(7) | ||

| % of Mortgage Loans with Hard Lockboxes: | 58.0% | |

| % of Mortgage Loans with Springing Lockboxes: | 36.6% | |

| % of Mortgage Loans with Soft Lockboxes: | 5.3% | |

| % of Mortgage Loans with No Lockbox: | 0.0% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 76.3% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 36.5% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves(8): | 79.1% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(9): | 40.3% | |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (4) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (5) | Excludes mortgage loans that are secured by multiple properties with multiple tenants. |

| (6) | Excludes 18 mortgage loans that are interest-only for the entire term. |

| (7) | For a more detailed description of Lockboxes, refer to “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. In the case of Loan No. 8, the loan is structured with a soft lockbox for residential tenants and a hard lockbox for commercial tenants and is considered a Soft Lockbox for calculations shown. |

| (8) | CapEx Reserves include FF&E reserves for hotel properties. |

| (9) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, mixed use and industrial properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Ten Largest Mortgage Loans | |||||||||||||

| No. | Loan Name | City, State | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW NCF DSCR(1) | UW NOI Debt Yield(1)(2) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | |

| 1 | SSTII Self Storage Portfolio II | Various, Various | KeyBank | 10 | $57,200,000 | 6.1% | 6,903 | Self Storage | 1.74x | 8.9% | 59.4% | 59.4% | |

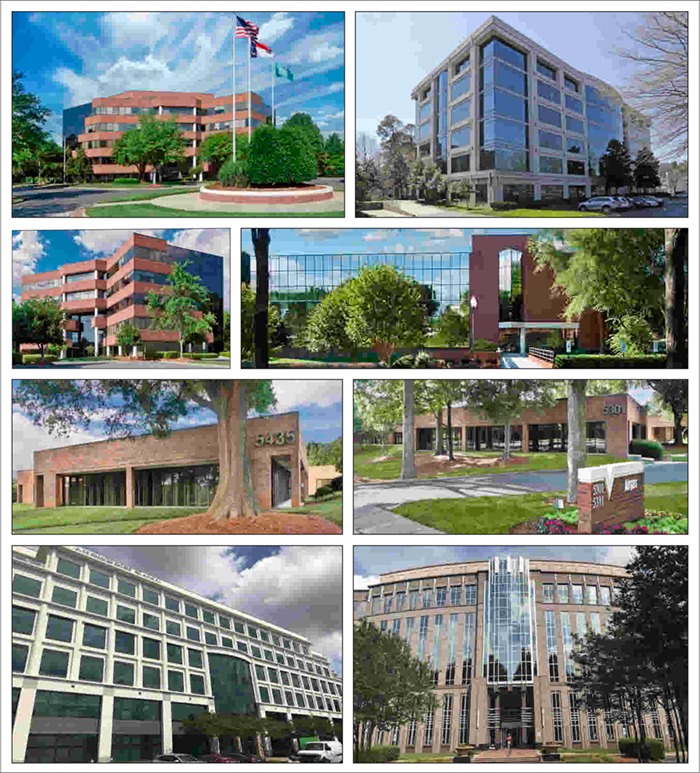

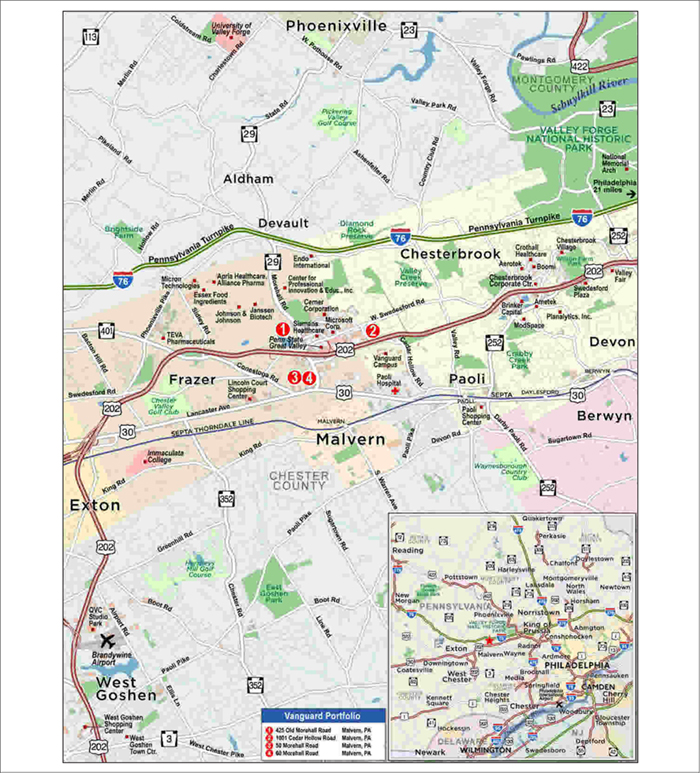

| 2 | Vanguard Portfolio | Malvern, PA | Natixis | 4 | $55,000,000 | 5.9% | 568,658 | Office | 2.03x | 10.1% | 61.8% | 61.8% | |

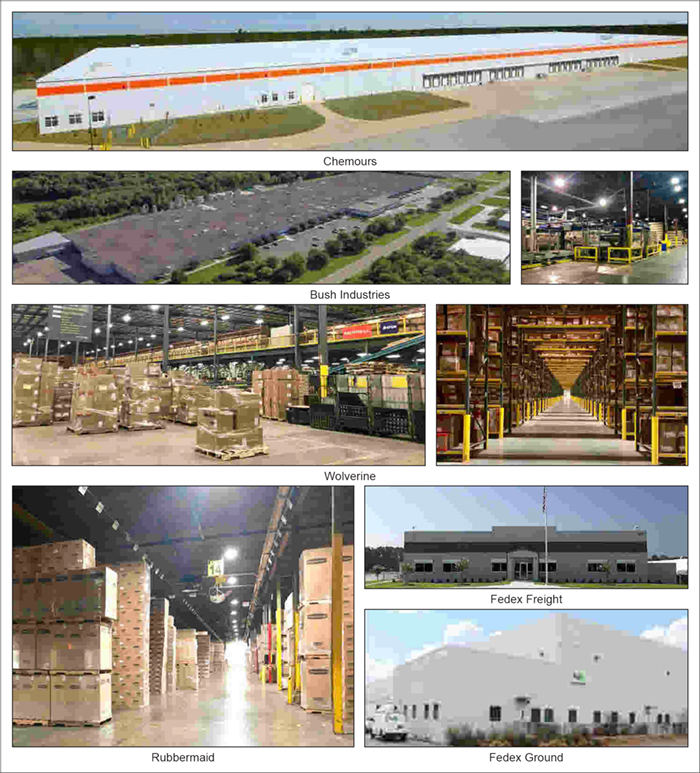

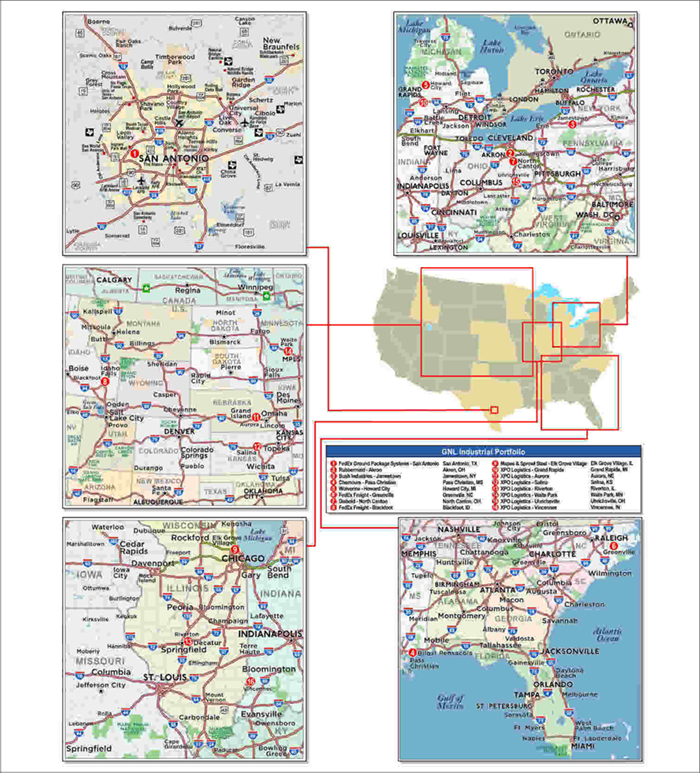

| 3 | GNL Industrial Portfolio | Various, Various | SGFC | 16 | $48,750,000 | 5.2% | 2,443,208 | Industrial | 1.98x | 9.8% | 65.0% | 65.0% | |

| 4 | SWVP Portfolio | Various, Various | SGFC | 4 | $45,000,000 | 4.8% | 1,192 | Hotel | 2.04x | 11.9% | 59.6% | 59.6% | |

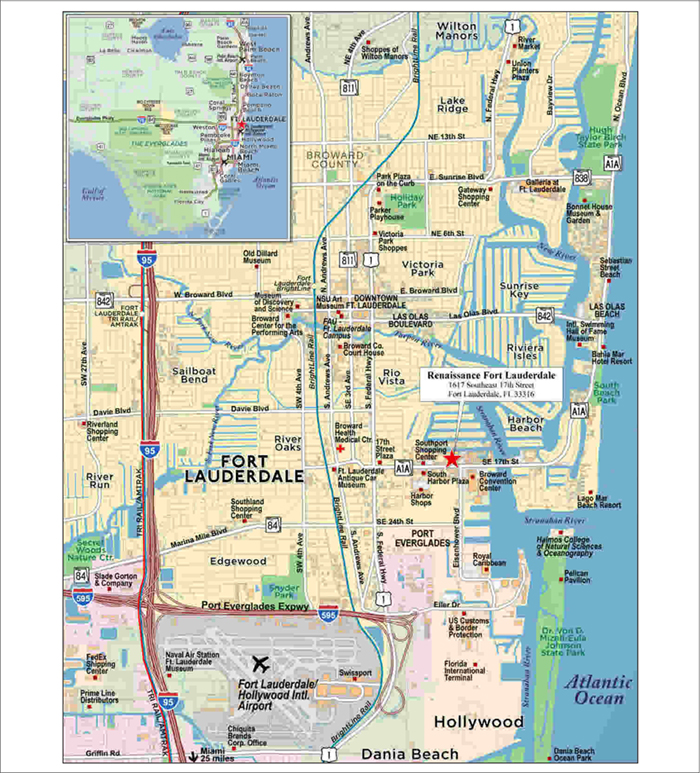

| 5 | Renaissance Fort Lauderdale | Fort Lauderdale, FL | Barclays | 1 | $42,275,000 | 4.5% | 236 | Hotel | 2.29x | 13.2% | 60.9% | 60.9% | |

| 6 | ATRIA Corporate Center | Plymouth, MN | Barclays | 1 | $41,250,000 | 4.4% | 360,047 | Office | 1.65x | 12.1% | 71.6% | 61.8% | |

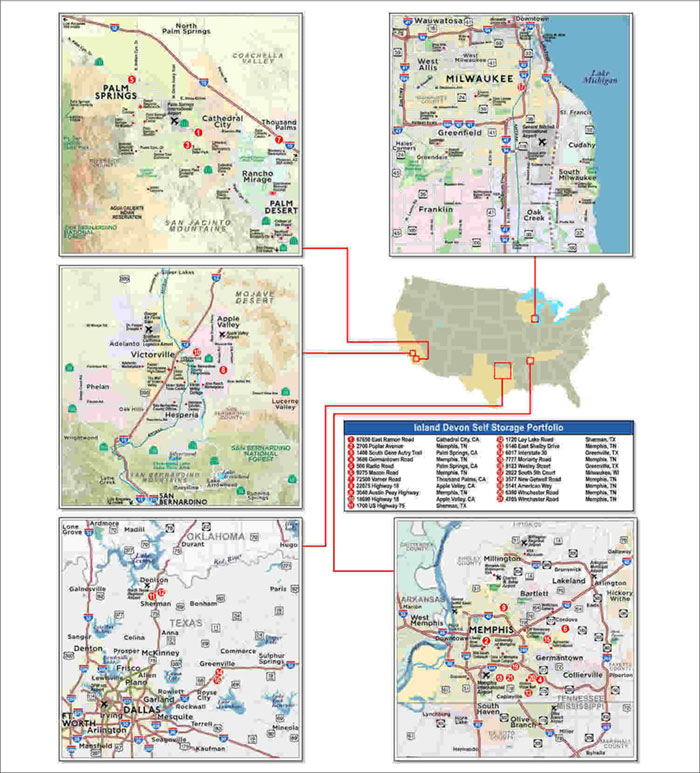

| 7 | Inland Devon Self Storage Portfolio | Various, Various | Barclays | 21 | $41,000,000 | 4.4% | 10,824 | Self Storage | 1.63x | 9.7% | 57.8% | 52.6% | |

| 8 | NEMA San Francisco | San Francisco, CA | Natixis | 1 | $35,000,000 | 3.7% | 754 | Multifamily | 2.27x | 10.3% | 37.7% | 37.7% | |

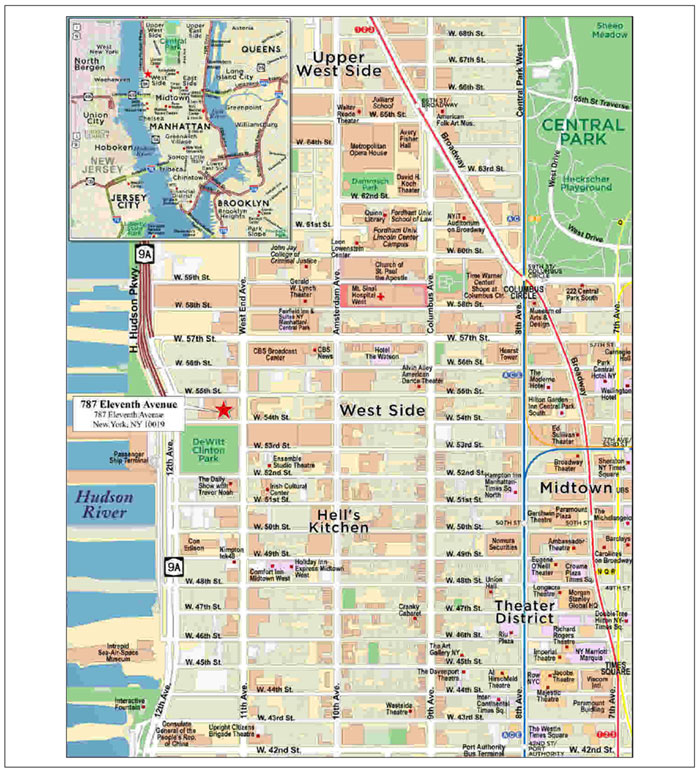

| 9 | 787 Eleventh Avenue | New York, NY | SGFC | 1 | $30,000,000 | 3.2% | 513,638 | Mixed Use | 3.01x | 14.4% | 26.9% | 26.9% | |

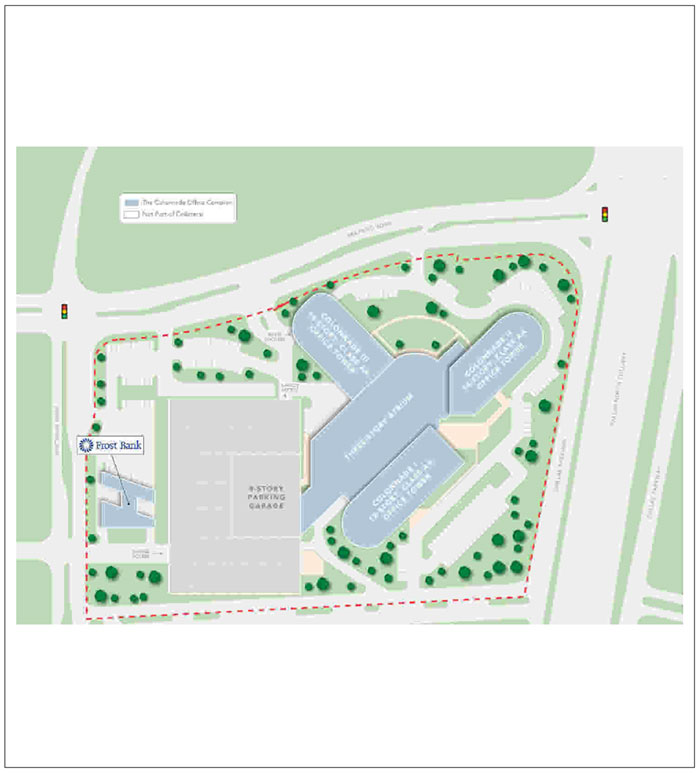

| 10 | The Colonnade Office Complex | Addison, TX | UBS AG | 1 | $30,000,000 | 3.2% | 1,080,180 | Office | 3.87x | 19.1% | 30.2% | 30.2% | |

| Top 3 Total/Weighted Average | 30 | $160,950,000 | 17.2% | 1.91x | 9.6% | 61.9% | 61.9% | ||||||

| Top 5 Total/Weighted Average | 35 | $248,225,000 | 26.5% | 2.00x | 10.6% | 61.3% | 61.3% | ||||||

| Top 10 Total/Weighted Average | 60 | $425,475,000 | 45.4% | 2.16x | 11.5% | 55.4% | 54.0% | ||||||

| Non-Top 10 Total/Weighted Average | 457 | $511,174,542 | 54.6% | 1.74x | 11.0% | 64.2% | 57.8% | ||||||

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (3) | In the case of Loan Nos. 1, 4 and 5, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Total Mortgage Loan Cut-off Date Balance(1) | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 1 | SSTII Self Storage Portfolio II | KeyBank | $57,200,000 | $104,000,000 | BBCMS 2019-C3 | Midland | Midland | CF 2019-CF1 | $46,800,000 |

| 2 | Vanguard Portfolio | Natixis | $55,000,000 | $116,842,500 | BBCMS 2019-C3(2) | Midland | Midland | Future Securitization(s) | $61,842,500 |

| 3 | GNL Industrial Portfolio | SGFC | $48,750,000 | $97,500,000 | (3) | (3) | (3) | Future Securitization(s) | $48,750,000 |

| 4 | SWVP Portfolio | SGFC | $45,000,000 | $200,000,000 | BBCMS 2019-C3 | Midland | Midland | Future Securitization(s) | $155,000,000 |

| 7 | Inland Devon Self Storage Portfolio | Barclays | $41,000,000 | $71,000,000 | BBCMS 2019-C3 | Midland | Midland | WFCM 2019-C50(4) | $30,000,000 |

| 8 | NEMA San Francisco | Natixis | $35,000,000 | $205,000,000 | NCMS 2019-NEMA(2) | KeyBank | Situs | NCMS 2019-NEMA Future Securitization(s) | $130,000,000 $40,000,000 |

| 9 | 787 Eleventh Avenue | SGFC | $30,000,000 | $175,000,000 | SGCMS 2019-787E(2) | Wells | AEGON | SGCMS 2019-787E, CSAIL 2019-C15, Future Securitization(s) | $70,000,000 $45,000,000 $30,000,000 |

| 10 | The Colonnade Office Complex | UBS AG | $30,000,000 | $105,000,000 | UBS 2019-C16(2) | Midland | Midland | UBS 2019-C16, WFCM 2019-C50(4) | $47,000,000 $28,000,000 |

| 11 | Wolverine Portfolio | UBS AG | $30,000,000 | $59,000,000 | BBCMS 2019-C3 | Midland | Midland | WFCM 2019-C50(4) | $29,000,000 |

| 13 | Kings Mountain Center | SGFC | $25,000,000 | $42,000,000 | BBCMS 2019-C3 | Midland | Midland | Future Securitization(s) | $17,000,000 |

| 18 | ExchangeRight Net Leased Portfolio 26 | SGFC | $20,000,000 | $55,000,000 | (3) | (3) | (3) | Future Securitization(s) | $35,000,000 |

| 19 | Patuxent Crossing | Barclays | $20,000,000 | $36,575,000 | BBCMS 2019-C3 | Midland | Midland | Future Securitization(s) | $16,575,000 |

| 21 | The Block Northway | UBS AG | $17,000,000 | $84,000,000 | BBCMS 2019-C3 | Midland | Midland | WFCM 2019-C50(4) UBS 2019-C16 Future Securitization(s) | $25,000,000 $23,000,000 $19,000,000 |

| 22 | Goodyear Portfolio | RMF | $16,000,000 | $50,500,000 | WFCM 2019-C50(2)(4) | Wells | Rialto | WFCM 2019-C50(4) | $34,500,000 |

| 23 | ExchangeRight Net Leased Portfolio 24 | SGFC | $15,000,000 | $54,165,000 | CSAIL 2019-C15 | Midland | Midland | CSAIL 2019-C15 UBS 2018-C15 | $35,000,000 $4,165,000 |

| 26 | Heartland Dental Medical Office Portfolio | UBS AG | $14,396,111 | $179,206,759 | WFCM 2019-C50(4) | Wells | Rialto | UBS 2018-C14 WFCM 2019-C50(4) UBS 2018-C15 UBS 2019-C16 Future Securitization(s) | $44,000,000 $22,000,000 $55,000,000 $25,000,000 $20,000,000 |

| 32 | ILPT Hawaii Portfolio | UBS AG | $10,000,000 | $650,000,000 | ILPT 2019-SURF | Midland | Rialto | ILPT Trust 2019-SURF BANK 2019-BNK17 UBS 2019-C16 Future Securitization(s) | $390,000,000 $50,000,000 $23,000,000 $177,000,000 |

| 33 | Southern Motion Industrial Portfolio | UBS AG | $10,000,000 | $41,690,000 | UBS 2019-C16 | Midland | Midland | UBS 2019-C16 | $31,690,000 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Total Mortgage Loan Cut-off Date Balance(1) | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 36 | Christiana Mall | SGFC | $9,704,000 | $338,000,000 | BBCMS 2018-CHRS | Wells | Wells | BBCMS 2018-CHRS WFCM 2018-C47 BBCMS 2018-C2 WFCM 2018-C48 UBS 2018-C13 UBS 2018-C14 UBS 2018-C15 DBGS 2018-C1 | $284,320,000 $50,000,000 $54,840,000 $28,000,000 $30,000,000 $30,000,000 $10,000,000 $53,136,000 |

| (1) | In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the Total Mortgage Loan Cut-off Date Balance excludes the related Subordinate Companion Loans. |

| (2) | Control rights are currently exercised by the holder of the related Subordinate Companion Loan until the occurrence and during the continuance of a control appraisal period for the related Whole Loan, as described under “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans”in the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 3 and 19, the related whole loan will be serviced under the BBCMS 2019-C3 pooling and servicing agreement until such time that the controllingpari passu companion loan is securitized, at which point the whole loan will be serviced under the related pooling and servicing agreement. The initial controlling noteholder is Column, or an affiliate, as holder of the related controllingpari passu companion loan. |

| (4) | The WFCM 2019-C50 securitization is expected to close on or about May 14, 2019. |

| Additional Debt Summary |

No. | Loan Name | Trust | Pari Passu Loan(s) Cut-off Date Balance | Subordinate Debt Cut-off Date Balance(1) | Total Debt Cut-off Date Balance | Mortgage Loan UW NCF DSCR(2) | Total Debt UW NCF DSCR | Mortgage Loan | Total Debt Cut-off Date LTV | Mortgage Loan UW NOI Debt Yield(2) | Total Debt UW NOI Debt Yield |

| 2 | Vanguard Portfolio | $55,000,000 | $61,842,500 | $12,982,500 | $129,825,000 | 2.03x | 1.68x | 61.8% | 68.6% | 10.1% | 9.0% |

| 8 | NEMA San Francisco | $35,000,000 | $170,000,000 | $179,000,000 | $384,000,000 | 2.27x | 1.15x | 37.7% | 70.6% | 10.3% | 5.5% |

| 9 | 787 Eleventh Avenue | $30,000,000 | $145,000,000 | $235,000,000 | $410,000,000 | 3.01x | 1.17x | 26.9% | 63.1% | 14.4% | 6.2% |

| 10 | The Colonnade Office Complex | $30,000,000 | $75,000,000 | $135,000,000 | $240,000,000 | 3.87x | 1.35x | 30.2% | 69.0% | 19.1% | 8.4% |

| 22 | Goodyear Portfolio | $16,000,000 | $34,500,000 | $9,861,676 | $60,361,676 | 2.22x | 1.38x | 57.2% | 68.4% | 11.1% | 9.3% |

| 36 | Christiana Mall | $9,704,000 | $328,296,000 | $212,000,000 | $550,000,000 | 3.15x | 1.93x | 32.5% | 52.9% | 13.8% | 8.5% |

| (1) | In the case of Loan Nos. 2, 8, 9, 22 and 36, subordinate debt represents one or more Subordinate Companion Loans. In the case of Loan No. 10, subordinate debt represents one or more Subordinate Companion Loans and a mezzanine loan. |

| (2) | In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI Debt Yield calculations include any related Pari Passu Companion Loans, but exclude the related Subordinate Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

Weighted Average

| ||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2)(4) | Cut-off Date LTV(2)(5) | Maturity Date LTV(2)(5) |

| Office | Suburban | 13 | $187,720,000 | 20.0% | 2.08x | 12.3% | 62.4% | 56.9% |

| Data Center | 1 | 25,000,000 | 2.7% | 1.75x | 11.5% | 56.0% | 51.4% | |

| CBD | 1 | 21,000,000 | 2.2% | 1.76x | 9.2% | 64.8% | 64.8% | |

| Medical | 149 | 15,144,012 | 1.6% | 1.69x | 11.3% | 56.6% | 50.0% | |

| Subtotal: | 164 | $248,864,012 | 26.6% | 1.99x | 11.9% | 61.6% | 56.6% | |

| Hotel | Full Service | 6 | $114,245,629 | 12.2% | 2.16x | 13.3% | 61.0% | 58.3% |

| Limited Service | 7 | 37,439,732 | 4.0% | 1.87x | 14.5% | 64.9% | 51.7% | |

| Extended Stay | 2 | 21,142,954 | 2.3% | 1.70x | 12.6% | 63.1% | 52.4% | |

| Select Service | 1 | 13,570,000 | 1.4% | 1.96x | 14.2% | 64.0% | 56.6% | |

| Subtotal: | 16 | $186,398,314 | 19.9% | 2.04x | 13.6% | 62.2% | 56.2% | |

| Self Storage | Self Storage | 33 | $125,850,000 | 13.4% | 1.73x | 9.1% | 59.1% | 57.0% |

| Retail | Anchored | 5 | $57,568,975 | 6.1% | 1.58x | 10.8% | 68.7% | 60.3% |

| Freestanding | 41 | 37,185,406 | 4.0% | 1.94x | 9.3% | 61.2% | 61.2% | |

| Unanchored | 2 | 10,415,000 | 1.1% | 1.41x | 9.7% | 69.0% | 59.7% | |

| Super Regional Mall | 1 | 9,704,000 | 1.0% | 3.15x | 13.8% | 32.5% | 32.5% | |

| Subtotal: | 49 | $114,873,380 | 12.3% | 1.81x | 10.5% | 63.2% | 58.2% | |

| Industrial | Flex | 14 | $42,658,540 | 4.6% | 1.95x | 11.2% | 62.8% | 60.1% |

| Warehouse/Distribution | 14 | 37,615,374 | 4.0% | 1.80x | 9.7% | 64.4% | 62.5% | |

| Manufacturing | 9 | 20,700,000 | 2.2% | 1.86x | 10.8% | 65.3% | 60.9% | |

| Warehouse | 2 | 4,080,000 | 0.4% | 1.95x | 10.0% | 65.5% | 64.7% | |

| Subtotal: | 39 | $105,053,914 | 11.2% | 1.88x | 10.5% | 64.0% | 61.3% | |

| Multifamily | Garden | 2 | $38,727,856 | 4.1% | 1.51x | 8.8% | 69.3% | 64.0% |

| High Rise | 1 | 35,000,000 | 3.7% | 2.27x | 10.3% | 37.7% | 37.7% | |

| Subtotal: | 3 | $73,727,856 | 7.9% | 1.87x | 9.5% | 54.3% | 51.5% | |

| Manufactured Housing | Manufactured Housing | 11 | $39,840,000 | 4.3% | 1.34x | 8.3% | 67.1% | 62.0% |

| Mixed Use | Retail/Office | 1 | $30,000,000 | 3.2% | 3.01x | 14.4% | 26.9% | 26.9% |

| Medical/Retail | 23 | 2,566,693 | 0.3% | 1.59x | 11.8% | 55.1% | 46.6% | |

| Subtotal: | 24 | $32,566,693 | 3.5% | 2.90x | 14.2% | 29.1% | 28.5% | |

| Other | Leased Fee | 177 | $9,440,087 | 1.0% | 2.40x | 10.6% | 45.2% | 45.2% |

| Parking | 1 | 35,286 | 0.0% | 2.40x | 10.6% | 45.2% | 45.2% | |

| Subtotal: | 178 | $9,475,373 | 1.0% | 2.40x | 10.6% | 45.2% | 45.2% | |

| Total / Weighted Average: | 517 | $936,649,542 | 100.0% | 1.93x | 11.2% | 60.2% | 56.0% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (4) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (5) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

[THIS PAGE INTENTIONALLY LEFT BLANK]

11

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) |

Weighted Average | ||||||||||

State | Number of Properties | Cut-off Date Principal Balance | % of IPB |

| UW NCF DSCR(2)(3) | UW NOI Debt Yield(2)(4) | Cut-off Date LTV(2)(5) | Maturity Date LTV(2)(5) | ||

| California | 12 | $120,943,153 | 12.9% | 1.85x | 9.9% | 54.8% | 51.9% | |||

| Florida | 54 | 93,243,789 | 10.0% | 1.98x | 11.9% | 61.7% | 59.0% | |||

| Pennsylvania | 8 | 72,824,148 | 7.8% | 1.88x | 9.8% | 63.4% | 62.1% | |||

| Texas | 27 | 72,611,531 | 7.8% | 2.71x | 14.9% | 49.2% | 46.1% | |||

| North Carolina | 6 | 61,421,391 | 6.6% | 1.75x | 11.2% | 59.9% | 55.4% | |||

| New York | 3 | 60,300,000 | 6.4% | 2.31x | 11.5% | 46.5% | 46.5% | |||

| Minnesota | 4 | 45,940,027 | 4.9% | 1.68x | 11.8% | 70.6% | 61.8% | |||

| Ohio | 17 | 31,898,594 | 3.4% | 2.06x | 10.3% | 61.0% | 60.5% | |||

| Michigan | 10 | 30,938,195 | 3.3% | 1.44x | 8.7% | 68.7% | 63.3% | |||

| Louisiana | 3 | 30,876,293 | 3.3% | 2.01x | 12.0% | 60.3% | 58.3% | |||

| Wisconsin | 12 | 30,800,483 | 3.3% | 1.76x | 12.2% | 68.6% | 59.5% | |||

| Massachusetts | 3 | 28,009,031 | 3.0% | 1.53x | 8.9% | 65.8% | 61.1% | |||

| Colorado | 2 | 27,091,928 | 2.9% | 2.15x | 16.0% | 63.5% | 52.1% | |||

| District of Columbia | 1 | 21,000,000 | 2.2% | 1.76x | 9.2% | 64.8% | 64.8% | |||

| Oregon | 2 | 20,227,856 | 2.2% | 1.57x | 9.3% | 70.1% | 59.9% | |||

| Maryland | 3 | 20,233,005 | 2.2% | 1.56x | 10.7% | 74.7% | 63.9% | |||

| Alabama | 4 | 19,101,128 | 2.0% | 1.62x | 11.2% | 69.1% | 60.8% | |||

| Tennessee | 24 | 18,983,953 | 2.0% | 1.67x | 9.8% | 58.1% | 53.3% | |||

| Illinois | 31 | 16,937,945 | 1.8% | 1.89x | 11.8% | 64.9% | 57.9% | |||

| Mississippi | 7 | 15,650,000 | 1.7% | 1.82x | 11.1% | 65.4% | 59.6% | |||

| Nevada | 3 | 14,974,953 | 1.6% | 1.74x | 8.9% | 59.4% | 59.4% | |||

| Indiana | 16 | 12,638,962 | 1.3% | 1.68x | 12.2% | 63.3% | 54.3% | |||

| Virginia | 5 | 11,021,611 | 1.2% | 1.43x | 9.7% | 68.5% | 59.6% | |||

| Hawaii | 186 | 10,000,000 | 1.1% | 2.40x | 10.6% | 45.2% | 45.2% | |||

| Delaware | 1 | 9,704,000 | 1.0% | 3.15x | 13.8% | 32.5% | 32.5% | |||

| South Carolina | 19 | 9,660,741 | 1.0% | 1.72x | 9.2% | 58.9% | 58.0% | |||

| Georgia | 19 | 9,428,882 | 1.0% | 1.88x | 12.3% | 62.4% | 53.5% | |||

| New Mexico | 3 | 5,394,670 | 0.6% | 2.13x | 16.0% | 61.6% | 49.2% | |||

| Washington | 1 | 4,481,373 | 0.5% | 1.73x | 13.6% | 66.9% | 56.7% | |||

| Connecticut | 1 | 2,626,787 | 0.3% | 1.41x | 13.0% | 73.6% | 62.5% | |||

| Idaho | 1 | 2,250,000 | 0.2% | 1.98x | 9.8% | 65.0% | 65.0% | |||

| Iowa | 1 | 1,504,016 | 0.2% | 2.04x | 9.5% | 62.0% | 62.0% | |||

| Missouri | 8 | 1,059,216 | 0.1% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| Nebraska | 3 | 956,948 | 0.1% | 1.92x | 10.1% | 63.4% | 62.0% | |||

| Kansas | 2 | 864,945 | 0.1% | 1.95x | 10.0% | 64.3% | 63.6% | |||

| Oklahoma | 5 | 359,448 | 0.0% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| Kentucky | 4 | 286,950 | 0.0% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| Arizona | 3 | 205,667 | 0.0% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| Arkansas | 2 | 170,566 | 0.0% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| New Hampshire | 1 | 27,357 | 0.0% | 1.59x | 11.8% | 55.1% | 46.6% | |||

| Total / Weighted Average: | 517 | $936,649,542 | 100.0% | 1.93x | 11.2% | 60.2% | 56.0% | |||

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (3) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (4) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (5) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||

| $2,626,787 | - | $9,999,999 | 17 | $111,084,377 | 11.9% | 5.10236% | 117 | 1.83x | 12.3% | 62.9% | 54.0% |

| $10,000,000 | - | $19,999,999 | 14 | 191,619,537 | 20.5% | 4.85609% | 117 | 1.73x | 10.9% | 64.4% | 57.7% |

| $20,000,000 | - | $29,999,999 | 8 | 178,470,629 | 19.1% | 4.77948% | 118 | 1.77x | 10.7% | 64.0% | 59.3% |

| $30,000,000 | - | $39,999,999 | 4 | 125,000,000 | 13.3% | 4.60167% | 102 | 2.60x | 12.9% | 41.0% | 39.4% |

| $40,000,000 | - | $49,999,999 | 5 | 218,275,000 | 23.3% | 4.66968% | 118 | 1.92x | 11.3% | 63.0% | 60.2% |

| $50,000,000 | - | $57,200,000 | 2 | 112,200,000 | 12.0% | 4.93137% | 115 | 1.88x | 9.5% | 60.6% | 60.6% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||

| 4.14000 | - | 4.49999 | 6 | $165,454,000 | 17.7% | 4.35044% | 117 | 2.05x | 10.0% | 53.3% | 52.0% |

| 4.50000 | - | 4.99999 | 26 | 562,805,530 | 60.1% | 4.78936% | 114 | 2.00x | 11.9% | 61.1% | 56.6% |

| 5.00000 | - | 5.49999 | 14 | 181,210,752 | 19.3% | 5.11987% | 117 | 1.64x | 10.2% | 63.7% | 58.9% |

| 5.50000 | - | 5.94000 | 4 | 27,179,261 | 2.9% | 5.70452% | 115 | 1.66x | 13.0% | 60.7% | 50.3% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||

| Original Term to Maturity in Months |

Weighted Average | |||||||||

| Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) |

| 60 | 1 | $30,000,000 | 3.2% | 4.56800% | 56 | 3.87x | 19.1% | 30.2% | 30.2% |

| 120 | 49 | 906,649,542 | 96.8% | 4.81008% | 117 | 1.86x | 11.0% | 61.2% | 56.9% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% |

| Remaining Term to Maturity in Months |

| Weighted Average | |||||||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||||||

| 56 | - | 60 | 1 | $30,000,000 | 3.2% | 4.56800% | 56 | 3.87x | 19.1% | 30.2% | 30.2% | ||||

| 110 | - | 119 | 49 | 906,649,542 | 96.8% | 4.81008% | 117 | 1.86x | 11.0% | 61.2% | 56.9% | ||||

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||||||

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (4) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) |

| Interest Only | 18 | $495,269,000 | 52.9% | 4.74328% | 113 | 2.18x | 11.0% | 54.8% | 54.8% |

| 300 | 4 | 18,106,702 | 1.9% | 5.33608% | 118 | 1.95x | 15.7% | 63.7% | 48.3% |

| 360 | 28 | 423,273,841 | 45.2% | 4.84858% | 118 | 1.63x | 11.3% | 66.4% | 57.8% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% |

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||||||

| Interest Only | 18 | $495,269,000 | 52.9% | 4.74328% | 113 | 2.18x | 11.0% | 54.8% | 54.8% | ||||||

| 297 | - | 299 | 4 | 18,106,702 | 1.9% | 5.33608% | 118 | 1.95x | 15.7% | 63.7% | 48.3% | ||||

| 353 | - | 360 | 28 | 423,273,841 | 45.2% | 4.84858% | 118 | 1.63x | 11.3% | 66.4% | 57.8% | ||||

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||||||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) |

| Interest Only | 18 | $495,269,000 | 52.9% | 4.74328% | 113 | 2.18x | 11.0% | 54.8% | 54.8% |

| IO-Balloon | 18 | 318,607,500 | 34.0% | 4.76226% | 118 | 1.58x | 10.7% | 67.1% | 59.3% |

| Balloon | 14 | 122,773,042 | 13.1% | 5.14449% | 118 | 1.82x | 13.5% | 64.4% | 52.6% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(2)(4) |

| Weighted Average | ||||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | |||

| 1.28x | - | 1.39x | 4 | $55,882,500 | 6.0% | 4.97829% | 117 | 1.32x | 8.8% | 69.1% | 61.8% | |

| 1.40x | - | 1.49x | 6 | 75,109,643 | 8.0% | 4.89395% | 118 | 1.44x | 9.6% | 69.0% | 60.7% | |

| 1.50x | - | 1.59x | 5 | 80,746,111 | 8.6% | 5.12356% | 117 | 1.56x | 10.5% | 68.1% | 61.2% | |

| 1.60x | - | 1.69x | 4 | 111,104,884 | 11.9% | 4.64539% | 118 | 1.64x | 11.1% | 65.4% | 57.5% | |

| 1.70x | 1.79x | 9 | 156,590,834 | 16.7% | 4.89827% | 117 | 1.75x | 10.4% | 61.1% | 57.7% | ||

| 1.80x | - | 1.99x | 10 | 137,772,444 | 14.7% | 4.67033% | 119 | 1.95x | 11.1% | 63.4% | 59.4% | |

| 2.00x | - | 2.99x | 9 | 249,739,128 | 26.7% | 4.79523% | 117 | 2.15x | 11.8% | 57.1% | 55.6% | |

| 3.00x | - | 3.87x | 3 | 69,704,000 | 7.4% | 4.51134% | 89 | 3.40x | 16.3% | 29.1% | 29.1% | |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | |||

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (4) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(2)(4) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||

| 26.9% | - | 49.9% | 5 | $114,704,000 | 12.2% | 4.47079% | 100 | 2.97x | 14.0% | 33.1% | 33.1% |

| 50.0% | - | 59.9% | 9 | 234,936,111 | 25.1% | 4.79122% | 118 | 1.81x | 10.2% | 58.1% | 56.2% |

| 60.0% | - | 64.9% | 15 | 255,252,688 | 27.3% | 4.88006% | 117 | 1.98x | 11.9% | 62.6% | 58.3% |

| 65.0% | - | 69.9% | 13 | 216,652,102 | 23.1% | 4.86099% | 118 | 1.64x | 10.3% | 67.4% | 61.9% |

| 70.0% | - | 74.9% | 8 | 115,104,643 | 12.3% | 4.87254% | 118 | 1.56x | 11.0% | 72.8% | 62.4% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||

| LTV Ratios as of the Maturity Date(1)(2)(4) |

Weighted Average | |||||||||||

| Range of Maturity Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) | ||

| 26.9% | - | 49.9% | 10 | $147,206,812 | 15.7% | 4.69744% | 103 | 2.71x | 14.0% | 39.0% | 36.3% |

| 50.0% | - | 59.9% | 20 | 347,873,088 | 37.1% | 4.82966% | 118 | 1.82x | 11.2% | 60.7% | 56.1% |

| 60.0% | - | 64.9% | 18 | 368,819,643 | 39.4% | 4.82418% | 117 | 1.74x | 10.6% | 67.2% | 62.0% |

| 65.0% | - | 66.1% | 2 | 72,750,000 | 7.8% | 4.77304% | 119 | 1.83x | 9.3% | 65.4% | 65.4% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) |

| Defeasance | 41 | $736,108,789 | 78.6% | 4.86519% | 115 | 1.92x | 11.3% | 61.4% | 57.1% |

| Defeasance or Yield Maintenance | 4 | $67,626,787 | 7.2% | 4.59674% | 117 | 2.39x | 12.7% | 42.2% | 40.0% |

| Yield Maintenance | 5 | 132,913,967 | 14.2% | 4.55877% | 118 | 1.75x | 10.1% | 62.8% | 58.2% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(4) | Maturity Date LTV(1)(4) |

| Refinance | 29 | $500,429,989 | 53.4% | 4.87455% | 114 | 2.01x | 11.6% | 57.2% | 52.9% |

| Acquisition | 18 | 367,469,553 | 39.2% | 4.75899% | 117 | 1.81x | 11.0% | 64.0% | 59.4% |

| Recapitalization | 3 | 68,750,000 | 7.3% | 4.50820% | 118 | 2.00x | 10.2% | 62.2% | 60.9% |

| Total / Weighted Average: | 50 | $936,649,542 | 100.0% | 4.80232% | 115 | 1.93x | 11.2% | 60.2% | 56.0% |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 7, 8, 9, 10, 11, 13, 18, 19, 21, 22, 23, 26, 32, 33 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 8, 9, 10, 22 and 36, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. In the case of Loan No. 22, the UW NCF DSCR was calculated using the sum of interest payments over the first 12 months following the Cut-off Date, as the Whole Loan amortizes on a 30-year amortization schedule with all amortization being applied to the Note B through April 1, 2029 as provided on Annex F in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 21, the UW NOI Debt Yield calculation includes a deduction for a holdback reserve in the amount of $2,200,000, to be released to the borrower (at the borrower’s request) provided that the debt yield (as calculated in the loan documents) at the mortgaged property is not less than 9.0%. The U/W NOI Debt Yield and U/W NCF Debt Yield are calculated net of the $2,200,000 achievement reserve. The unadjusted U/W NOI Debt Yield and U/W NCF Debt Yield are 8.8% and 8.7%, respectively, based on the full Cut-Off Date Balance. All LTVs and DSCRs are calculated assuming the full loan amount of $84,000,000. |

| (4) | In the case of Loan Nos. 1, 4, 5, 33, 34 and 41, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical or as stabilized assumptions. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Collateral Characteristics | ||

| Previous Securitization History(1) |

| No. | Mortgage Loan Seller | Loan Name | Location | Property Type | Cut-off Date Principal Balance | % of IPB | Previous Securitization |

| 11.01 | UBS AG | Apple Tree Estates | Walker, MI | Manufactured Housing | $5,490,000 | 0.6% | LBUBS 2006-C7 |

| 11.02 | UBS AG | South Lyon | South Lyon, MI | Manufactured Housing | $5,095,424 | 0.5% | LBUBS 2006-C7 |

| 11.03 | UBS AG | Metro Commons | Romulus, MI | Manufactured Housing | $4,402,881 | 0.5% | LBUBS 2006-C7 |

| 11.04 | UBS AG | Brighton Village | Brighton, MI | Manufactured Housing | $4,306,780 | 0.5% | LBUBS 2006-C7 |

| 11.05 | UBS AG | College Heights | Auburn Hills, MI | Manufactured Housing | $3,000,508 | 0.3% | LBUBS 2006-C7 |

| 11.06 | UBS AG | Hillcrest | Kalamazoo, MI | Manufactured Housing | $2,062,881 | 0.2% | LBUBS 2006-C7 |

| 11.07 | UBS AG | Royal Village | Toledo, OH | Manufactured Housing | $1,817,797 | 0.2% | LBUBS 2006-C7 |

| 11.08 | UBS AG | Fernwood | Deland, FL | Manufactured Housing | $1,462,881 | 0.2% | LBUBS 2006-C7 |

| 11.09 | UBS AG | Satellite Bay | Clearwater, FL | Manufactured Housing | $1,189,322 | 0.1% | LBUBS 2006-C7 |

| 11.10 | UBS AG | Chalet Village | Tampa, FL | Manufactured Housing | $1,171,525 | 0.1% | LBUBS 2006-C7 |

| 14 | RMF | The Falls In Hudson | Hudson, NY | Multifamily | $24,000,000 | 2.6% | SGCP 2018-FL1 |

| 22 | RMF | Goodyear Portfolio | Akron, OH | Industrial | $16,000,000 | 1.7% | COMM 2014-CCRE21 |

| 22.01 | RMF | Innovation Tech Center | Akron, OH | Industrial | $13,688,497 | 1.5% | COMM 2014-CCRE21 |

| 22.02 | RMF | Research Center | Akron, OH | Industrial | $985,989 | 0.1% | COMM 2014-CCRE21 |

| 22.03 | RMF | Tire Testing | Akron, OH | Industrial | $823,159 | 0.1% | COMM 2014-CCRE21 |

| 22.04 | RMF | North Archwood | Akron, OH | Industrial | $502,355 | 0.1% | COMM 2014-CCRE21 |

| 23.04 | SGFC | Walgreens - Lawrenceville, GA | Lawrenceville, GA | Retail | $944,337 | 0.1% | GSMS 2013-GCJ16 |

| 34 | Barclays | Candlewood Suites Indianapolis Downtown Medical District | Indianapolis, IN | Hotel | $9,954,884 | 1.1% | WFRBS 2014-C19 |

| 36 | SGFC | Christiana Mall | Newark, DE | Retail | $9,704,000 | 1.0% | MSC 2011-C1 |

| 45 | SGFC | Town Plaza Leesville | Leesville, LA | Retail | $5,468,975 | 0.6% | WFRBS 2011-C3 |

| (1) | The table above represents the properties for which the previously existing debt was most recently securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Class A-2(1) | ||

No. | Loan Name | Location | Cut-off Date Balance | % of IPB | Maturity Date Balance | % of Certificate Class(2) | Original Loan Term | Remaining Loan Term | UW NCF DSCR(3) | UW NOI Debt Yield(3) | Cut-off Date LTV(3) | Maturity Date LTV(3) |

| 10 | The Colonnade Office Complex | Addison, TX | $30,000,000 | 3.2% | $30,000,000 | 100.0% | 60 | 56 | 3.87x | 19.1% | 30.2% | 30.2% |

| Total / Weighted Average: | $30,000,000 | 3.2% | $30,000,000 | 100.0% | 60 | 56 | 3.87x | 19.1% | 30.2% | 30.2% | ||

| (1) | The table above presents the mortgage loan whose balloon payment would be applied to pay down the certificate balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each Class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Maturity Date Balance divided by the initial Class A-2 Certificate Balance. |

| (3) | The UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loans. The UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| Structural and Collateral Term Sheet | BBCMS 2019-C3 | |

| Structural Overview | ||

| ■ Accrual: | Each Class of Certificates (other than the Class R Certificates) will accrue interest on a 30/360 basis. The Class R Certificates will not accrue interest. | |