| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226850-10 | ||

| Dated September 9, 2021 | BBCMS 2021-C11 |

Free Writing Prospectus Structural and Collateral Term Sheet | ||

BBCMS Mortgage Trust 2021-C11 | ||

$988,043,799 (Approximate Mortgage Pool Balance) | ||

$865,773,000 (Approximate Offered Certificates) | ||

Barclays Commercial Mortgage Securities LLC Depositor

| ||

Commercial Mortgage Pass-Through Certificates, Series 2021-C11 | ||

Barclays Capital Real Estate Inc. Societe Generale Financial Corporation SSOF SCRE AIV, L.P. UBS AG LMF Commercial, LLC BSPRT CMBS Finance, LLC Natixis Real Estate Capital LLC Mortgage Loan Sellers

| ||

| Barclays | UBS Securities LLC Co-Lead Managers and Joint Bookrunners | Société Générale |

| Academy Securities Co-Manager | Mischler Financial Group, Inc. Co-Manager | Natixis Co-Manager |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| Dated September 9, 2021 | BBCMS 2021-C11 |

This material is for your information, and none of Barclays Capital Inc., SG Americas Securities, LLC, UBS Securities LLC, Natixis Securities Americas LLC, Academy Securities, Inc. or Mischler Financial Group, Inc. (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226850) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Barclays Capital Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-888-603-5847. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2021-C11 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| Structural and Collateral Term Sheet | BBCMS 2021-C11 |

| Indicative Capital Structure | |

Publicly Offered Certificates

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Available Certificate Balance or Notional Amount(1) | Approximate Initial Retained Certificate Balance or Notional Amount(1)(2) | Approximate Initial Credit Support(3) | Expected Weighted Avg. Life (years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Underwritten NOI Debt Yield(6) |

| A-1 | AAA(sf)/AAAsf/AAA(sf) | $23,677,000 | $22,828,000 | $849,000 | 30.000% | 2.77 | 10/21-5/26 | 41.2% | 15.3% |

| A-2 | AAA(sf)/AAAsf/AAA(sf) | $33,000,000 | $31,817,000 | $1,183,000 | 30.000% | 4.63 | 5/26-5/26 | 41.2% | 15.3% |

| A-SB | AAA(sf)/AAAsf/AAA(sf) | $41,720,000 | $40,224,000 | $1,496,000 | 30.000% | 7.00 | 5/26-1/31 | 41.2% | 15.3% |

| A-3 | AAA(sf)/AAAsf/AAA(sf) | $98,671,000 | $95,134,000 | $3,537,000 | 30.000% | 6.89 | 6/28-9/28 | 41.2% | 15.3% |

| A-4 | AAA(sf)/AAAsf/AAA(sf) | (7) | (7) | (7) | 30.000% | (7) | (7) | 41.2% | 15.3% |

| A-5 | AAA(sf)/AAAsf/AAA(sf) | (7) | (7) | (7) | 30.000% | (7) | (7) | 41.2% | 15.3% |

| X-A | AAA(sf)/AAAsf/AAA(sf) | $691,630,000(8) | $666,839,000(8) | $24,791,000(8) | N/A | N/A | N/A | N/A | N/A |

| X-B | NR/A-sf/AAA(sf) | $174,143,000(9) | $167,900,000(9) | $6,243,000(9) | N/A | N/A | N/A | N/A | N/A |

| A-S | AA+(sf)/AAAsf/AAA(sf) | $86,454,000 | $83,355,000 | $3,099,000 | 21.250% | 9.91 | 8/31-9/31 | 46.3% | 13.6% |

| B | AA-(sf)/AA-sf/AA(sf) | $44,462,000 | $42,868,000 | $1,594,000 | 16.750% | 9.96 | 9/31-9/31 | 49.0% | 12.9% |

| C | NR/A-sf/A(sf) | $43,227,000 | $41,677,000 | $1,550,000 | 12.375% | 9.96 | 9/31-9/31 | 51.5% | 12.2% |

Privately Offered Certificates(10)

| Class | Expected Ratings (S&P / Fitch / KBRA) | Approximate Initial Certificate Balance or Notional Amount(1) | Approximate Initial Available Certificate Balance or Notional Amount(1) | Approximate Initial Retained Certificate Balance or Notional Amount(1)(2) | Approximate Initial Credit Support(3) | Expected Weighted Avg. Life (years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Underwritten NOI Debt Yield(6) |

| X-D | NR/BBB-sf/BBB-(sf) | $50,637,000(11) | $48,821,000(11) | $1,816,000(11) | N/A | N/A | N/A | N/A | N/A |

| X-F | NR/BB+sf/BB+(sf) | $12,351,000(12) | $11,908,000(12) | $443,000(12) | N/A | N/A | N/A | N/A | N/A |

| X-G | NR/BB-sf/BB(sf) | $9,880,000(13) | $9,525,000(13) | $355,000(13) | N/A | N/A | N/A | N/A | N/A |

| D | NR/BBBsf/BBB+(sf) | $27,171,000 | $26,197,000 | $974,000 | 9.625% | 9.96 | 9/31-9/31 | 53.1% | 11.8% |

| E | NR/BBB-sf/BBB-(sf) | $23,466,000 | $22,624,000 | $842,000 | 7.250% | 9.96 | 9/31-9/31 | 54.5% | 11.5% |

| F | NR/BB+sf/BB+(sf) | $12,351,000 | $11,908,000 | $443,000 | 6.000% | 9.96 | 9/31-9/31 | 55.3% | 11.4% |

| G | NR/BB-sf/BB(sf) | $9,880,000 | $9,525,000 | $355,000 | 5.000% | 9.96 | 9/31-9/31 | 55.9% | 11.3% |

| H-RR | NR/B-sf/B(sf) | $9,881,000 | $9,526,000 | $355,000 | 4.000% | 9.96 | 9/31-9/31 | 56.4% | 11.1% |

| J-RR | NR/NR/NR | $39,521,799 | $38,105,000 | $1,416,799 | 0.000% | 9.96 | 9/31-9/31 | 58.8% | 10.7% |

| (1) | In the case of each such Class, subject to a permitted variance of plus or minus 5%, including in connection with any variation in the certificate balances and notional amounts of the classes comprising the VRR Interest following the calculation of the actual fair value of the ABS interests (as such term is defined in Regulation RR) issued by the issuing entity. |

| (2) | On the Closing Date, Sabal (a sponsor and an affiliate of the special servicer) will cause a majority-owned affiliate to purchase from the underwriters the certificates (other than the Class R certificates) with the initial certificate balances or notional amounts, as applicable, as set forth in the table above under “Approximate Initial Retained Certificate Balance or Notional Amount”, as further described in “Credit Risk Retention” in the Preliminary Prospectus. |

| (3) | The credit support percentages set forth for Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates represent the approximate initial credit support for the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates in the aggregate. |

| (4) | Assumes 0% CPR / 0% CDR and a September 29, 2021 closing date. Based on modeling assumptions as described in the Preliminary Prospectus dated September 10, 2021 (the “Preliminary Prospectus”). |

| (5) | The “Certificate Principal to Value Ratio” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans, and (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates. The Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificate Principal to Value Ratios are calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (6) | The “Underwritten NOI Debt Yield” for any Class of Principal Balance Certificates (other than the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates) is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates and the denominator of which is the total initial Certificate Balance for such Class and all Classes of Principal Balance Certificates senior to such Class of Certificates. The Underwritten NOI Debt Yield for each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates is calculated in the aggregate for those Classes as if they were a single Class. Investors should note, however, that net operating income from any mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

| (7) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, expected weighted average lives and expected principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $494,562,000, subject to a variance of plus or minus 5%. The initial certificate balance of the certificates to be retained by SSOF VRR, LLC related to the Class A-4 and Class A-5 certificates will be an amount equal to approximately 3.584% of the approximate initial certificate balance of such class, as further described in “Credit Risk Retention.” In the event that the Class A-5 certificates are issued with an initial certificate balance of $494,562,000, the Class A-4 certificates will not be issued and the Class A-5 will be renamed the Class A-4. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Indicative Capital Structure | ||

| Class of Certificates | Expected Range of Approximate Initial Certificate Balance | Expected Range of Approximate Initial Available Certificate Balance | Expected Range of Approximate Initial Retained Certificate Balance | Expected Range of Weighted Avg. Life (Yrs) | Expected Range of Principal Window | ||

| Class A-4 | $0 - $233,364,000 | $0 - $225,000,000 | $0 - $8,364,000 | N/A – 9.14 | N/A – 12/29-7/31 | ||

| Class A-5 | $261,198,000 – $494,562,000 | $251,836,000 - $476,836,000 | $9,362,000 – $17,726,000 | 9.84 – 9.51 | 7/31-8/31 – 12/29-8/31 |

| (8) | The Notional Amount of the Class X-A Certificates will be equal to the aggregate Certificate Balance of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4 and Class A-5 Certificates outstanding from time to time. |

| (9) | The Notional Amount of the Class X-B Certificates will be equal to the aggregate Certificate Balance of the Class A-S, Class B and Class C Certificates outstanding from time to time. |

| (10) | The Class X-D, Class X-F, Class X-G, Class D, Class E, Class F, Class G, Class H-RR and Class J-RR Certificates are not being offered by the Preliminary Prospectus and this Term Sheet. The Class R Certificates are not shown above. |

| (11) | The Notional Amount of the Class X-D Certificates will be equal to the aggregate Certificate Balance of the Class D and Class E Certificates outstanding from time to time. |

| (12) | The Notional Amount of the Class X-F Certificates will be equal to the Certificate Balance of the Class F Certificates outstanding from time to time. |

| (13) | The Notional Amount of the Class X-G Certificates will be equal to the Certificate Balance of the Class G Certificates outstanding from time to time. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Summary of Transaction Terms | ||

| Securities Offered: | $865,773,000 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Co-Lead Managers and Joint Bookrunners: | Barclays Capital Inc., SG Americas Securities, LLC and UBS Securities LLC. |

| Co-Managers: | Natixis Securities Americas LLC, Academy Securities, Inc. and Mischler Financial Group, Inc. |

| Mortgage Loan Sellers: | Barclays Capital Real Estate Inc. (“Barclays”) (26.3%), Societe Generale Financial Corporation (“SGFC”) (20.0%), SSOF SCRE AIV, L.P. (“Sabal”) (17.8%), UBS AG (“UBS AG”) (16.7%), LMF Commercial, LLC (“LMF”) (7.8%), BSPRT CMBS Finance, LLC (“BSPRT”) (7.0%) and Natixis Real Estate Capital LLC (“Natixis”) (4.5%). |

| Master Servicer: | Wells Fargo Bank, National Association. |

| Special Servicer: | SCP Servicing, LLC. |

| Trustee: | Wilmington Trust, National Association. |

| Certificate Administrator: | Wells Fargo Bank, National Association. |

| Operating Advisor: | Park Bridge Lender Services LLC. |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC. |

| Rating Agencies: | S&P Global Ratings, acting through Standard & Poor’s Financial Services LLC (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, LLC (“KBRA”). |

| Initial Majority Controlling Class Certificateholder: | Sabal Strategic Opportunities Fund, L.P. or an affiliate |

| U.S. Credit Risk Retention: | Sabal is expected to act as the “retaining sponsor,” for this securitization and intends to satisfy the U.S. credit risk retention requirements (i) through the purchase by SSOF VRR LLC, a “majority-owned affiliate,” of an “eligible vertical interest” (each as defined in Regulation RR), which will consist of approximately 3.584% of the certificate balance, notional amount or percentage interest of each class of certificates (other than the Class R Certificates) (the “VRR Interest”) issued by the issuing entity and (ii) through the purchase by Sabal Strategic Opportunities Fund, L.P., a “majority-owned affiliate,” of an “eligible horizontal residual interest” (each as defined in Regulation RR), which will consist of the portion of the Class H-RR and Class J-RR Certificates not included in the VRR Interest. Sabal, in its capacity as the “retaining sponsor” for this transaction, will be required to comply with the hedging, transfer and financing restrictions applicable to a “retaining sponsor” under the credit risk retention rules, which generally prohibit the transfer of the applicable certificates except to a “majority-owned affiliate” of the “retaining sponsor”. The restrictions on hedging and transfer under the credit risk retention rules as in effect on the closing date of this transaction will expire on and after the date that is the latest of (i) the date on which the aggregate principal balance of the mortgage loans has been reduced to 33% of the aggregate principal balance of the mortgage loans as of the Cut-off Date; (ii) the date on which the total unpaid principal obligations under the certificates has been reduced to 33% of the aggregate total unpaid principal obligations under the certificates as of the Closing Date; or (iii) two years after the Closing Date. For additional information, see “Credit Risk Retention” in the Preliminary Prospectus. |

| EU Credit Risk Retention: | The transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Closing Date: | On or about September 29, 2021. |

| Cut-off Date: | With respect to each mortgage loan, the related due date in September 2021, or in the case of any mortgage loan that has its first due date after September 2021, the date that would have been its due date in September 2021 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month. |

| Distribution Date: | The 4th business day after the Determination Date in each month, commencing in October 2021. |

| Determination Date: | 11th day of each month, or if the 11th day is not a business day, the next succeeding business day, commencing in October 2021. |

| Assumed Final Distribution Date: | The Distribution Date in September 2031, which is the latest anticipated repayment date of the Certificates. |

| Rated Final Distribution Date: | The Distribution Date in September 2054. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC “regular interests” for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-5, Class X-A, Class X-B, Class A-S, Class B and Class C Certificates (the “Publicly Offered Certificates”) will be offered publicly. The Class X-D, Class X-F, Class X-G, Class D, Class E, Class F, Class G, Class H-RR, Class J-RR and Class R Certificates (the “Privately Offered Certificates”) will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors (other than the Class R Certificates) and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The Certificates will not constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Summary of Transaction Terms | ||

| Optional Termination: | On any Distribution Date on which the aggregate principal balance of the pool of mortgage loans is less than 1% of the aggregate principal balance of the mortgage loans as of the Cut-off Date, certain entities specified in the Preliminary Prospectus will have the option to purchase all of the remaining mortgage loans (and all property acquired through exercise of remedies in respect of any mortgage loan) at the price specified in the Preliminary Prospectus. Refer to “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus. |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B Certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B Certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| Analytics: | The transaction is expected to be modeled by Intex Solutions, Inc. and Trepp, LLC and is expected to be available on Bloomberg, L.P., Trepp, LLC, Intex Solutions, Inc., Interactive Data Corp., Markit Group Limited, BlackRock Financial Management, Inc., CMBS.com, Moody’s Analytics, MBS Data, LLC, RealInsight, KBRA Analytics, LLC, Thomson Reuters Corporation, DealView Technologies Ltd. and CRED iQ. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. REFER TO THE “SUMMARY OF RISK FACTORS” AND “RISK FACTORS” SECTIONS OF THE PRELIMINARY PROSPECTUS. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of | Number of Mortgaged | Aggregate | % of IPB |

| Barclays | 16 | 25 | $259,707,000 | 26.3% |

| SGFC | 12 | 12 | $197,393,695 | 20.0% |

| Sabal | 34 | 34 | $176,215,002 | 17.8% |

| UBS AG | 10 | 70 | $164,811,384 | 16.7% |

| LMF | 12 | 22 | $76,751,795 | 7.8% |

| BSPRT | 8 | 8 | $69,114,924 | 7.0% |

| Natixis | 2 | 2 | $44,050,000 | 4.5% |

| Total: | 94 | 173 | $988,043,799 | 100.0% |

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $988,043,799 | |

| Number of Mortgage Loans: | 94 | |

| Number of Mortgaged Properties: | 173 | |

| Average Cut-off Date Balance per Mortgage Loan: | $10,511,104 | |

| Weighted Average Current Mortgage Rate: | 3.55269% | |

| 10 Largest Mortgage Loans as % of IPB: | 37.4% | |

| Weighted Average Remaining Term to Maturity: | 111 months | |

| Weighted Average Seasoning: | 3 months | |

| Credit Statistics | ||

| Weighted Average UW NCF DSCR(1)(2): | 2.49x | |

| Weighted Average UW NOI Debt Yield(1): | 10.7% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(1)(3): | 58.8% | |

| Weighted Average Maturity Date LTV(1)(3): | 54.3% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 15.3% | |

| % of Mortgaged Loans with Single Tenants(4): | 17.3% | |

| % of Mortgaged Loans secured by Multiple Properties: | 12.4% | |

| Amortization | ||

| Weighted Average Original Amortization Term(5): | 353 months | |

| Weighted Average Remaining Amortization Term(5): | 351 months | |

| % of Mortgage Loans with Interest-Only: | 57.3% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 27.6% | |

| % of Mortgage Loans with Amortizing Balloon: | 15.1% | |

| Lockboxes(6) | ||

| % of Mortgage Loans with Hard Lockboxes: | 49.1% | |

| % of Mortgage Loans with Springing Lockboxes: | 46.7% | |

| % of Mortgage Loans with Soft Lockboxes: | 4.2% | |

| % of Mortgage Loans with No Lockbox: | 0.0% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 72.9% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 62.6% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves: | 62.4% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(7): | 50.5% | |

| (1) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (3) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (4) | Excludes mortgage loans that are secured by multiple properties with multiple tenants. |

| (5) | Excludes 42 mortgage loans that are interest-only for the entire term. |

| (6) | For a more detailed description of Lockboxes, refer to “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. In the case of Loan No. 25, the mortgage loan is structured with a soft lockbox for residential tenants and a hard lockbox for commercial tenants and is considered a Soft Lockbox in the calculations shown. |

| (7) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, mixed use and industrial properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Ten Largest Mortgage Loans |

| No. | Loan Name | City, State | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW NCF DSCR(1) | UW NOI Debt Yield(1) | Cut-off Date LTV(1) | Maturity Date LTV(1) |

| 1 | One SoHo Square | New York, NY | Barclays | 1 | $70,000,000 | 7.1% | 786,891 | Office | 4.88x | 13.6% | 34.8% | 34.8% |

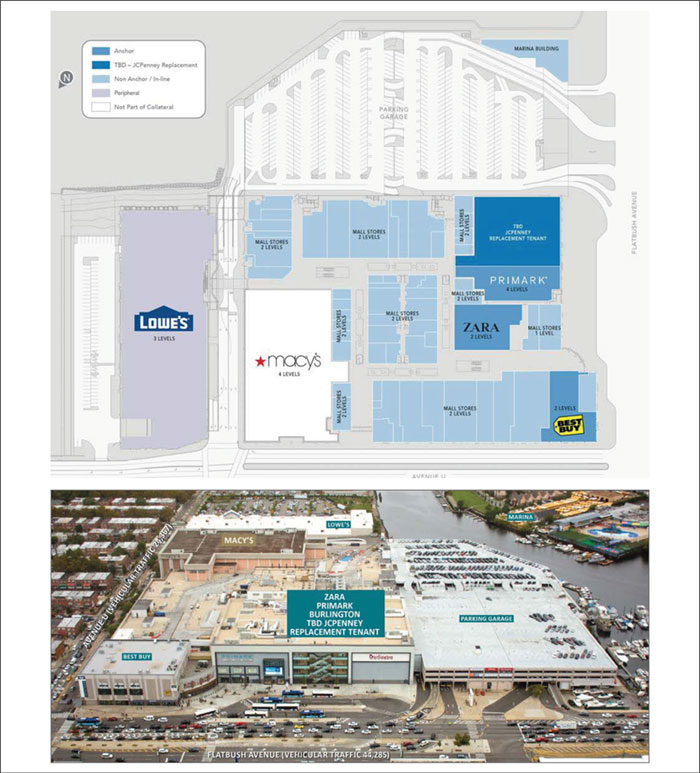

| 2 | Kings Plaza | Brooklyn, NY | SGFC | 1 | $47,945,946 | 4.9% | 811,797 | Retail | 3.07x | 10.7% | 54.1% | 54.1% |

| 3 | Parkway Irvine | Irvine, CA | SGFC | 1 | $37,000,000 | 3.7% | 209,831 | Industrial | 2.91x | 9.6% | 59.3% | 59.3% |

| 4 | Broadacres Office Park | Bloomfield, NJ | Natixis | 1 | $33,000,000 | 3.3% | 396,226 | Office | 3.73x | 14.8% | 58.7% | 58.7% |

| 5 | Fleet Farm Mixed Use | Appleton, WI | SGFC | 1 | $33,000,000 | 3.3% | 431,440 | Mixed Use | 1.88x | 10.9% | 60.0% | 54.0% |

| 6 | Morris Corporate Center | Parsippany, NJ | UBS AG | 1 | $32,500,000 | 3.3% | 541,195 | Office | 1.90x | 11.1% | 68.2% | 58.1% |

| 7 | 15-17 Park Avenue | New York, NY | SGFC | 1 | $31,000,000 | 3.1% | 97 | Multifamily | 2.04x | 7.0% | 61.9% | 61.9% |

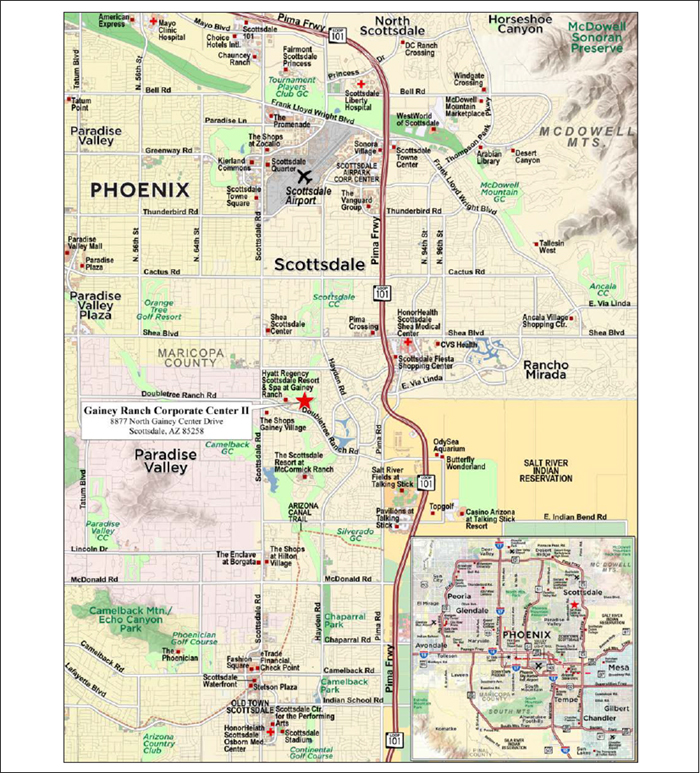

| 8 | Gainey Ranch Corporate Center II | Scottsdale, AZ | BSPRT | 1 | $29,175,000 | 3.0% | 203,642 | Office | 3.68x | 13.0% | 47.1% | 47.1% |

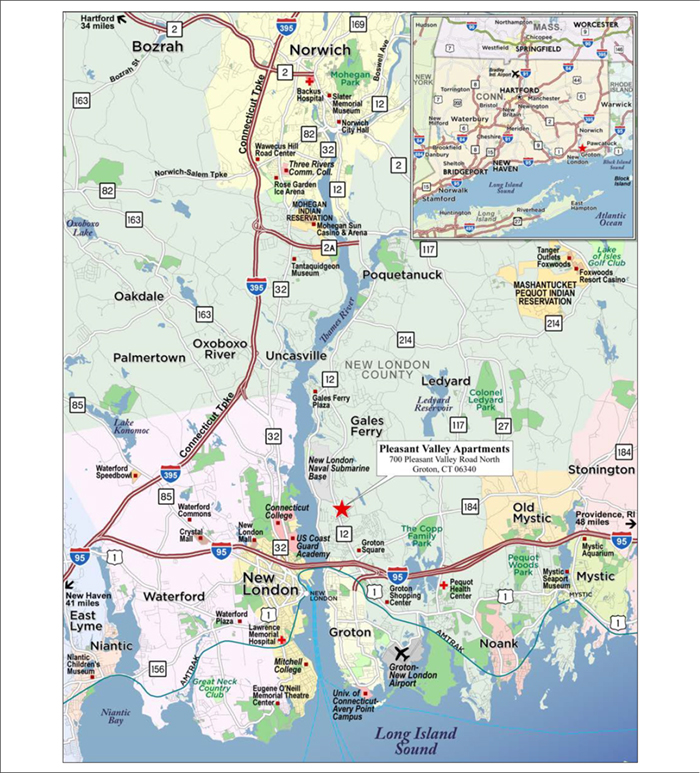

| 9 | Pleasant Valley Apartments | Groton, CT | Barclays | 1 | $28,930,000 | 2.9% | 132 | Multifamily | 2.21x | 7.5% | 69.4% | 69.4% |

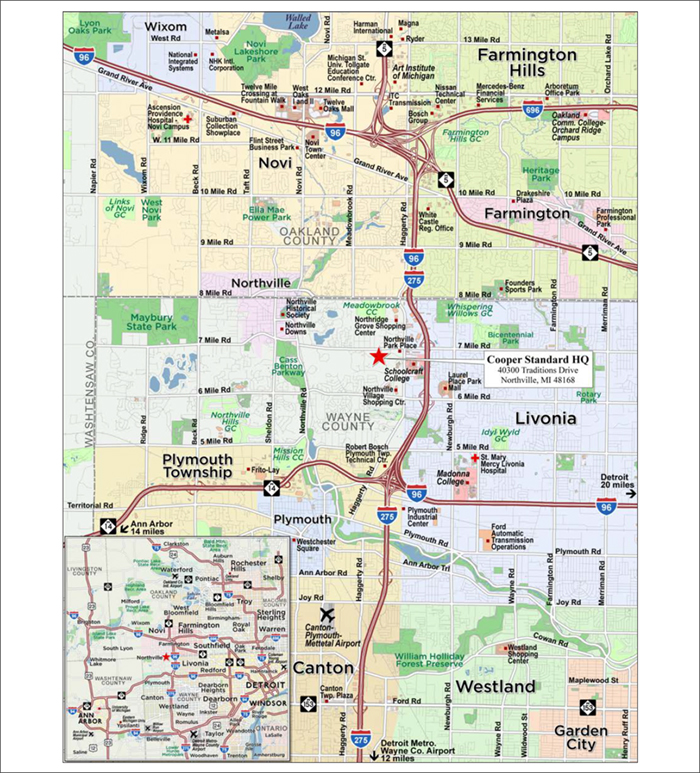

| 10 | Cooper Standard HQ | Northville, MI | UBS AG | 1 | $27,300,000 | 2.8% | 110,165 | Office | 1.93x | 11.0% | 63.8% | 53.3% |

| Top 3 Total/Weighted Average | 3 | $154,945,946 | 15.7% | 3.85x | 11.7% | 46.6% | 46.6% | ||||

| Top 5 Total/Weighted Average | 5 | $220,945,946 | 22.4% | 3.54x | 12.1% | 50.4% | 49.5% | ||||

| Top 10 Total/Weighted Average | 10 | $369,850,946 | 37.4% | 3.06x | 11.2% | 55.2% | 53.0% | ||||

| Non-Top 10 Total/Weighted Average(1)(2) | 163 | $618,192,853 | 62.6% | 2.14x | 10.3% | 60.9% | 55.1% | ||||

| (1) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (2) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Total | Controlling | Master Servicer | Special | Related Pari Passu | Related Pari Passu Loan(s) Original Balance |

| 1 | One SoHo Square | Barclays | $70,000,000 | $470,000,000 | SOHO 2021-SOHO(2) | KeyBank | Midland | SOHO 2021-SOHO BMARK 2021-B28 Future Securitization(s) | $1,000,000 $135,000,000 $264,000,000 |

| 2 | Kings Plaza | SGFC | $47,945,946 | $487,000,000 | BMARK 2020-B17 | Midland | Midland | BMARK 2020-B17 DBJPM 2020-C9 BMARK 2020-B18 BMARK 2020-B16 BMARK 2020-IG1 BBCMS 2020-C6 BMARK 2020-B21 WFCM 2020-C55 BANK 2020-BNK25 BBCMS 2021-C10 | $32,000,000 $20,000,000 $14,108,108 $50,000,000 $55,000,000 $60,000,000 $30,000,000 $82,945,946 $75,000,000 $20,000,000 |

| 6 | Morris Corporate Center | UBS AG | $32,500,000 | $82,000,000 | BBCMS 2021-C10 | KeyBank | Rialto | BBCMS 2021-C10 | $49,500,000 |

| 11 | 356-362 E 148th Street | Barclays | $24,000,000 | $38,000,000 | BBCMS 2021-C11 | Wells | Sabal | Future Securitization(s) | $14,000,000 |

| 15 | Wyndham National Hotel Portfolio | UBS AG | $19,130,750 | $138,697,940 | UBS 2019-C18 | Wells | Rialto | UBS 2019-C18 BBCMS 2021-C10 Future Securitization(s) | $35,000,000 $10,000,000 $80,000,000 |

| 21 | Rollins Portfolio | UBS AG | $15,000,000 | $39,400,000 | WFCM 2021-C60 | Wells | Midland | WFCM 2021-C60 | $24,400,000 |

| (1) | In the case of Loan Nos. 1 and 2, the Total Mortgage Loan Cut-off Date Balance excludes the related Subordinate Companion Loan(s) and/or mezzanine loan(s). |

| (2) | In the case of Loan No. 1, control rights are currently exercised by the holder of the related Subordinate Companion Loan(s) until the occurrence and during the continuance of a control appraisal period for the related Whole Loan, as described under “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Additional Debt Summary |

No. | Loan Name | Trust | Pari Passu | Subordinate | Total Debt Cut- | Mortgage Loan UW NCF DSCR(2) | Total | Mortgage Loan | Total Debt | Mortgage Loan UW NOI Debt Yield(2) | Total |

| 1 | One SoHo Square | $70,000,000 | $400,000,000 | $435,000,000 | $905,000,000 | 4.88x | 2.28x | 34.8% | 67.0% | 13.6% | 7.1% |

| 2 | Kings Plaza | $47,945,946 | $439,054,054 | $53,000,000 | $540,000,000 | 3.07x | 1.73x | 54.1% | 60.0% | 10.7% | 9.6% |

| 4 | Broadacres Office Park | $33,000,000 | $0 | $7,000,000 | $40,000,000 | 3.73x | 2.43x | 58.7% | 71.2% | 14.8% | 12.2% |

| (1) | In the case of Loan No. 1, subordinate debt represents one or more Subordinate Companion Loans ($315,000,000) and a mezzanine loan ($120,000,000). In the case of Loan Nos. 2 and 4, subordinate debt represents a mezzanine loan. |

| (2) | Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI Debt Yield calculations include any related Pari Passu Companion Loans (if applicable), but exclude the related Subordinate Companion Loans and mezzanine loan(s). |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

COVID-19 Update(1) |

Mortgage Loan | Information as of Date | Origination Date | Property Name | Property | July Debt Service Payment Received | August | Forbearance or Other Debt Service | Other Loan Modification Requested | Lease Modification or Rent | PPP Loan Received | Occupied SF/Unit | UW June | Occupied SF/Unit | UW July |

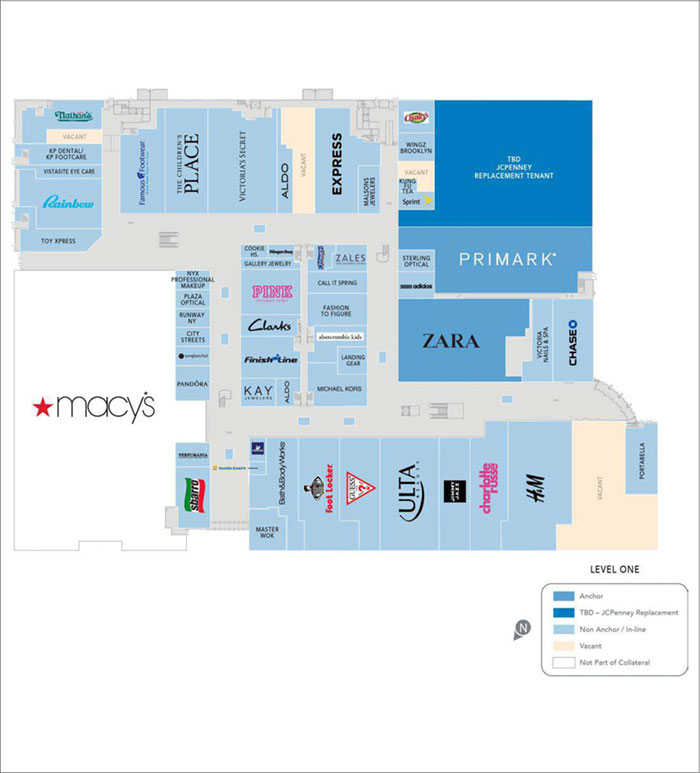

| SGFC | 8/31/202 | 12/3/2019 | Kings Plaza | Retail | Y | Y | N | N | Y(4) | N | NAP | 93.5% | NAP | 99.1% |

| UBS AG | 8/23/2021 | 11/27/2019 | Wyndham National Hotel Portfolio | Hospitality | Y | Y | N | N | N | N | NAP | NAP | NAP | NAP |

| SGFC | 8/31/2021 | 3/2/2020 | Homewood Suites Katy | Hospitality | Y | Y | Y(5) | N | N | Y(5) | NAP | NAP | NAP | NAP |

| Sabal | 8/26/2021 | 3/6/2020 | College Metcalf | Mixed Use | Y | Y | N | N | Y(6) | N | 100.0% | 100.0% | 100.0% | 100.0% |

| SGFC | 8/31/2021 | 3/2/2020 | Holiday Inn Express Alamogordo | Hospitality | Y | Y | N | N | N | N | NAP | NAP | NAP | NAP |

| LMF | 8/31/2021 | 2/27/2020 | Best Western Hampton Coliseum Inn | Hospitality | Y | Y | Y(7) | Y(7) | NAP | N | NAP | NAP | NAP | NAP |

| (1) | The table contains information regarding the status of the Mortgage Loans originated in or prior to March 2020 and of the related Mortgaged Properties, in each case as of the date found in the “Information as-of Date” column below. The information provided in the columns labeled “Lease Modification or Rent Relief Requested (Y/N)”, “PPP Loan Received by Borrower (Y/N)”, “Occupied SF/Unit Making Full June Payment (%)” and “Occupied SF/Unit Making Full July Payment (%)” as well as the information found in the footnotes to the table (such information collectively, the “Borrower Information”) was provided by the related borrower sponsors via phone conversations and email communications. The Borrower Information has not been independently verified by the Mortgage Loan Sellers, the Underwriters or any other party, and there can be no assurances that the Borrower Information was comprehensive and accurate when received, or as of the date of this term sheet. |

The cumulative effects of the COVID-19 pandemic on the global economy may cause tenants to be unable to pay their rent and borrowers to be unable to pay debt service under the Mortgage Loans. As a result, we cannot assure you that the information in the following table is indicative of future performance or that tenants or borrowers will not seek rent or debt service relief (including forbearance arrangements) or other lease or loan modifications in the future. Such actions may lead to shortfalls and losses on the Certificates. See “Risk Factors—Risks Related to Market Conditions and Other External Factors—Current Coronavirus Pandemic Has Adversely Affected the Global Economy and Will Likely Adversely Affect the Performance of the Mortgage Loans” in the Preliminary Prospectus.

| (2) | Forbearance or Other Debt Service Relief Requested (Y/N) and Other Loan Modification Requested (Y/N) reflect situations where a request was made and not withdrawn. |

| (3) | Lease Modification or Rent Relief Requested (Y/N) excludes residential tenants and self-storage tenants and includes any commercial tenant that has requested a lease modification or rent relief. |

| (4) | Although June and July 2021 collections were reported by the borrower, an accurate estimate of the percentage of Total Occupied SF/Unit Making Full Rent Payment (%) for June and July 2021 cannot be determined for the Kings Plaza Mortgage Loan based on the source documentation of the aged receivable reports received from the borrower sponsor, which only reported the balances for gross amounts due over 30 day increments for each tenant. According to the borrower sponsor, 31 tenants (collectively approximately 11.3% of total NRA and approximately 20.6% of UW Base Rent) have executed deferment agreements. However, these tenants are currently not in deferment and are paying current rent. JCPenney closed its store at the Kings Plaza Mortgaged Property on October 31, 2020. On May 10, 2021, the borrower sponsor’s CEO, Thomas O’Hern, reported on a Q1 2021 earnings call, it would be announcing a new store commitment for the Kings Plaza Mortgaged Property. As of the date of this term sheet no further announcement has been made. In addition: |

| ● | The following tenants have not reopened: Master Wok, Nathan’s Famous, Haagen Dazs (kiosk) and Starbucks (collectively, 0.8% of NRA and 1.0% of UW Base Rent). |

| ● | The following tenants have vacated the Kings Plaza Mortgaged Property: JCPenney, Clique (kiosk), Fashion to Figure, GNC, Landing Gear, New York & Company, NYX, Parfois and Pounds Lifestyle Boutique (collectively, 13.8% of NRA and 4.6% of UW Base Rent). |

| ● | GNC and JCPenney (collectively 11.9% of NRA and 2.3% of UW Base Rent) have declared bankruptcy and vacated the premises. The Forever 21 lease was assumed with the term extended to January 31, 2023, and such space was underwritten as vacant. The Charlotte Russe (1.0% of NRA and 0.7% of UW Base Rent) lease was assumed with a term through July 31, 2021, and currently negotiating a 2-year lease renewal. With respect to ALDO/ALDO Accessories (0.4% of NRA and 1.5% of UW Base Rent), the leases were assumed with terms through January 1, 2026 and January 31, 2022, respectively. |

| (5) | On May 1, 2020, the loan agreement was modified to (i) defer the May 2020, June 2020 and July 2020 principal payments, (ii) pay the June 2020 and July 2020 interest out of the hotel’s upfront PIP reserve and (iii) waive the ongoing FF&E reserve for May, June and July 2020. As a result of the Mortgaged Property’s rebound in Q3 2020 and Q4 2020, the borrower sponsor repaid all of the deferred payments/escrows (approximately $125K) in December 2020 and the loan has remained current. The related borrower sponsor obtained an unsecured loan in the amount of $158,800 under the Coronavirus Aid, Relief and Economic Security Act’s Payment Protection Program (a “PPP Loan”). Pursuant to a modification of the loan agreement, dated May 1, 2020, the lender consented to the PPP Loan and the PPP Loan was included as permitted debt under the related Mortgage Loan documents. |

| (6) | Seven tenants (collectively, approximately 19.0% of NRA and approximately 30.7% of UW Base Rent) received various COVID-19 related rent and recovery deferments in 2020 which deferments have since all ended. Such deferred amounts are scheduled to be repaid over periods ranging from 2 months to 12 months. The deferments totaled approximately $104,400, with the single largest deferment of $30,923 related to The Shack tenant. These deferred amounts are all scheduled to be fully repaid by the end of 2021. Additionally, 100.0% of Occupied SF/Unit Making Full August Payment (%) and 100.0% UW August Base Rent Paid (%) were collected for August 2021. |

| (7) | From April through September 2020, the borrower paid debt service; however, collections of tax and insurance reserves were deferred (and the borrower paid taxes and shortfalls in insurance premiums when due) and collections for capital expenditures were waived. Additionally, the lender entered into a forbearance agreement with the borrower, which deferred interest payments for four months from December 2020 through March 2021 (the total amount deferred was $41,892). The borrower is required to pay $41,892 in monthly installments of $3,491, starting in April 2021. The borrower is current on its repayments. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Structural and Collateral Term Sheet | BBCMS 2021-C11 |

| Collateral Characteristics | |

| Mortgaged Properties by Type(1) |

Weighted Average | ||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Office | Suburban | 12 | $172,072,958 | 17.4% | 2.62x | 12.2% | 60.2% | 54.3% |

| CBD | 4 | 105,632,676 | 10.7 | 4.05x | 12.3% | 43.2% | 42.7% | |

| Medical | 3 | 11,987,500 | 1.2 | 1.77x | 9.8% | 57.9% | 52.7% | |

| Subtotal: | 19 | $289,693,133 | 29.3% | 3.10x | 12.1% | 53.9% | 50.0% | |

| Multifamily | Garden | 27 | $160,624,472 | 16.3% | 1.90x | 8.9% | 66.4% | 60.8% |

| High Rise | 1 | 31,000,000 | 3.1 | 2.04x | 7.0% | 61.9% | 61.9% | |

| Low Rise | 3 | 16,500,000 | 1.7 | 1.95x | 7.8% | 61.9% | 61.9% | |

| Age Restricted | 1 | 15,080,000 | 1.5 | 2.19x | 8.1% | 60.3% | 60.3% | |

| Mid Rise | 2 | 11,500,000 | 1.2 | 1.85x | 8.7% | 67.5% | 62.3% | |

| Subtotal: | 34 | $234,704,472 | 23.8% | 1.94x | 8.5% | 65.1% | 61.1% | |

| Retail | Anchored | 6 | $53,294,067 | 5.4% | 2.38x | 12.0% | 57.6% | 50.6% |

| Super Regional Mall | 1 | 47,945,946 | 4.9 | 3.07x | 10.7% | 54.1% | 54.1% | |

| Single Tenant | 4 | 19,810,000 | 2.0 | 2.47x | 9.8% | 61.0% | 59.0% | |

| Unanchored | 5 | 17,498,763 | 1.8 | 1.81x | 9.7% | 63.6% | 54.5% | |

| Subtotal: | 16 | $138,548,776 | 14.0% | 2.56x | 11.0% | 57.6% | 53.5% | |

| Industrial | Flex | 18 | $85,435,000 | 8.6% | 2.62x | 9.9% | 60.3% | 58.2% |

| Manufacturing | 2 | 30,251,500 | 3.1 | 2.51x | 9.9% | 53.6% | 49.7% | |

| Warehouse | 2 | 3,344,212 | 0.3 | 1.54x | 11.2% | 53.1% | 38.8% | |

| Subtotal: | 22 | $119,030,712 | 12.0% | 2.56x | 9.9% | 58.4% | 55.5% | |

| Mixed Use | Retail / Industrial | 1 | $33,000,000 | 3.3% | 1.88x | 10.9% | 60.0% | 54.0% |

| Retail / Office | 2 | 30,380,000 | 3.1 | 2.45x | 12.4% | 52.4% | 44.1% | |

| Multifamily / Retail | 6 | 30,330,000 | 3.1 | 1.80x | 8.5% | 64.7% | 58.6% | |

| Multifamily / Retail / Office | 2 | 11,950,000 | 1.2 | 1.59x | 6.3% | 62.0% | 62.0% | |

| Retail / Multifamily | 4 | 10,725,000 | 1.1 | 1.84x | 7.6% | 59.5% | 59.5% | |

| Subtotal: | 15 | $116,385,000 | 11.8% | 1.98x | 9.9% | 59.4% | 53.9% | |

| Hospitality | Limited Service | 46 | $27,107,707 | 2.7% | 1.96x | 15.9% | 63.0% | 46.6% |

| Extended Stay | 1 | 9,274,780 | 0.9 | 2.46x | 16.2% | 66.7% | 54.5% | |

| Subtotal: | 47 | $36,382,487 | 3.7% | 2.09x | 16.0% | 64.0% | 48.6% | |

| Self Storage | 11 | $33,725,219 | 3.4% | 2.50x | 11.6% | 54.2% | 49.8% | |

| Manufactured Housing | 9 | $19,574,000 | 2.0% | 2.66x | 10.1% | 58.6% | 56.3% | |

| Total / Weighted Average: | 173 | $988,043,799 | 100.0% | 2.49x | 10.7% | 58.8% | 54.3% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (3) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (4) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) |

Weighted Average | |||||||

State | Number of | Cut-off Date | % of IPB | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| New York | 25 | $257,243,153 | 26.0% | 3.01x | 10.3% | 53.6% | 52.6% |

| California | 20 | 85,963,633 | 8.7 | 2.56x | 10.5 | 56.8 | 52.2 |

| Georgia | 14 | 72,306,415 | 7.3 | 2.44x | 10.1 | 58.7 | 55.6 |

| Texas | 11 | 67,058,864 | 6.8 | 2.27x | 10.3 | 60.5 | 54.5 |

| New Jersey | 2 | 65,500,000 | 6.6 | 2.82x | 13.0 | 63.4 | 58.4 |

| Florida | 11 | 57,377,202 | 5.8 | 1.90x | 9.7 | 60.5 | 54.8 |

| Arizona | 7 | 51,120,973 | 5.2 | 3.09x | 11.8 | 51.0 | 49.5 |

| Michigan | 5 | 46,030,000 | 4.7 | 2.07x | 10.7 | 61.5 | 53.3 |

| Illinois | 11 | 45,035,000 | 4.6 | 1.98x | 10.1 | 67.7 | 60.5 |

| Pennsylvania | 7 | 43,170,248 | 4.4 | 1.76x | 10.0 | 64.5 | 55.5 |

| Connecticut | 2 | 34,930,000 | 3.5 | 2.18x | 7.6 | 67.7 | 67.7 |

| Wisconsin | 1 | 33,000,000 | 3.3 | 1.88x | 10.9 | 60.0 | 54.0 |

| Ohio | 5 | 27,264,154 | 2.8 | 1.92x | 10.2 | 61.1 | 51.2 |

| Maryland | 3 | 17,535,549 | 1.8 | 2.07x | 11.0 | 60.9 | 54.1 |

| Utah | 2 | 16,303,982 | 1.7 | 2.49x | 10.6 | 65.0 | 64.6 |

| New Mexico | 5 | 13,370,885 | 1.4 | 2.25x | 14.9 | 55.0 | 41.4 |

| Kansas | 6 | 9,108,118 | 0.9 | 3.30x | 13.8 | 58.4 | 55.0 |

| Puerto Rico | 1 | 6,870,000 | 0.7 | 2.24x | 8.9 | 68.7 | 68.7 |

| Missouri | 3 | 5,959,343 | 0.6 | 1.33x | 8.8 | 71.3 | 58.8 |

| Oklahoma | 2 | 5,882,431 | 0.6 | 1.48x | 9.5 | 67.5 | 61.0 |

| Alabama | 1 | 4,632,676 | 0.5 | 2.35x | 13.7 | 50.6 | 40.5 |

| Virginia | 3 | 4,386,366 | 0.4 | 2.47x | 16.9 | 57.9 | 47.1 |

| Wyoming | 6 | 3,896,378 | 0.4 | 1.69x | 14.7 | 64.5 | 46.7 |

| Tennessee | 2 | 2,662,224 | 0.3 | 1.57x | 12.0 | 55.7 | 40.6 |

| South Carolina | 1 | 2,626,723 | 0.3 | 1.43x | 9.0 | 55.9 | 44.9 |

| Washington | 1 | 2,346,268 | 0.2 | 5.56x | 29.1 | 18.9 | 14.5 |

| Nebraska | 4 | 2,208,113 | 0.2 | 1.69x | 14.7 | 64.5 | 46.7 |

| Montana | 2 | 795,087 | 0.1 | 1.69x | 14.7 | 64.5 | 46.7 |

| Iowa | 2 | 718,512 | 0.1 | 1.69x | 14.7 | 64.5 | 46.7 |

| Colorado | 2 | 686,059 | 0.1 | 2.31x | 13.8 | 51.5 | 40.9 |

| Nevada | 1 | 553,895 | 0.1 | 1.69x | 14.7 | 64.5 | 46.7 |

| Oregon | 1 | 537,087 | 0.1 | 1.69x | 14.7 | 64.5 | 46.7 |

| Louisiana | 1 | 389,634 | 0.0 | 1.69x | 14.7 | 64.5 | 46.7 |

| South Dakota | 1 | 292,189 | 0.0 | 1.69x | 14.7 | 64.5 | 46.7 |

| North Dakota | 1 | 203,197 | 0.0 | 1.69x | 14.7 | 64.5 | 46.7 |

| Minnesota | 1 | 79,441 | 0.0 | 1.69x | 14.7 | 64.5 | 46.7 |

| Total / Weighted Average: | 173 | $988,043,799 | 100.0% | 2.49x | 10.7% | 58.8% | 54.3% |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (3) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (4) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| $2,070,000 | - | $4,999,999 | 35 | $119,727,563 | 12.1% | 3.86624% | 115 | 2.07x | 10.4% | 59.5% | 52.9% |

| $5,000,000 | - | $9,999,999 | 31 | 214,256,273 | 21.7% | 3.74707% | 117 | 2.22x | 10.6% | 61.2% | 54.8% |

| $10,000,000 | - | $19,999,999 | 15 | 216,427,518 | 21.9% | 3.67439% | 116 | 2.10x | 10.3% | 62.6% | 57.2% |

| $20,000,000 | - | $29,999,999 | 6 | 153,186,500 | 15.5% | 3.47826% | 115 | 2.42x | 10.0% | 58.8% | 55.3% |

| $30,000,000 | - | $39,999,999 | 5 | 166,500,000 | 16.9% | 3.39134% | 106 | 2.51x | 10.7% | 61.5% | 58.4% |

| $40,000,000 | - | $70,000,000 | 2 | 117,945,946 | 11.9% | 2.98245% | 90 | 4.14x | 12.4% | 42.6% | 42.6% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 2.72467 | - | 3.24999 | 14 | $221,755,225 | 22.4% | 3.00369% | 104 | 3.80x | 12.3% | 45.8% | 44.9% |

| 3.25000 | - | 3.74999 | 34 | 487,749,167 | 49.4% | 3.50396% | 112 | 2.29x | 10.4% | 61.6% | 57.2% |

| 3.75000 | - | 3.99999 | 20 | 143,999,862 | 14.6% | 3.86054% | 117 | 1.83x | 8.5% | 64.5% | 60.1% |

| 4.00000 | - | 4.24999 | 15 | 78,760,108 | 8.0% | 4.12579% | 115 | 1.76x | 10.6% | 64.8% | 54.9% |

| 4.25000 | - | 4.49999 | 7 | 27,385,638 | 2.8% | 4.30913% | 119 | 1.50x | 9.6% | 63.5% | 55.0% |

| 4.50000 | - | 4.74999 | 2 | 6,903,988 | 0.7% | 4.57688% | 91 | 2.20x | 14.6% | 51.8% | 45.6% |

| 4.75000 | - | 5.01000 | 2 | 21,489,811 | 2.2% | 4.86756% | 101 | 1.65x | 14.0% | 63.7% | 46.8% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| Original Term to Maturity in Months |

Weighted Average | |||||||||

| Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| 60 | 1 | $33,000,000 | 3.3% | 3.54540% | 56 | 3.73x | 14.8% | 58.7% | 58.7% |

| 84 | 4 | 99,031,500 | 10.0% | 2.91598% | 83 | 4.21x | 12.4% | 39.6% | 39.5% |

| 120 | 89 | 856,012,299 | 86.6% | 3.62663% | 117 | 2.24x | 10.3% | 61.0% | 55.9% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% |

| Remaining Term to Maturity in Months |

| Weighted Average | |||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 56 | 1 | $33,000,000 | 3.3% | 3.54540% | 56 | 3.73x | 14.8% | 58.7% | 58.7% | ||

| 81 | - | 103 | 10 | 190,709,933 | 19.3% | 3.35072% | 91 | 3.50x | 12.7% | 48.6% | 45.6% |

| 112 | - | 115 | 7 | 50,357,828 | 5.1% | 3.96834% | 113 | 2.00x | 10.0% | 60.0% | 54.8% |

| 116 | - | 120 | 76 | 713,976,038 | 72.3% | 3.57766% | 119 | 2.19x | 10.0% | 61.4% | 56.4% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| (1) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (3) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Interest Only | 42 | $565,809,946 | 57.3% | 3.37018% | 107 | 2.96x | 10.2% | 56.0% | 56.0% |

| 270 | 1 | 19,130,750 | 1.9% | 4.85000% | 99 | 1.69x | 14.7% | 64.5% | 46.7% |

| 300 | 4 | 20,392,641 | 2.1% | 3.65237% | 115 | 2.03x | 13.6% | 52.8% | 38.0% |

| 360 | 47 | 382,710,462 | 38.7% | 3.75237% | 117 | 1.84x | 10.9% | 62.9% | 53.1% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% |

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| Interest Only | 42 | $565,809,946 | 57.3% | 3.37018% | 107 | 2.96x | 10.2% | 56.0% | 56.0% | ||

| 249 | - | 299 | 5 | 39,523,392 | 4.0% | 4.23206% | 107 | 1.86x | 14.1% | 58.5% | 42.2% |

| 342 | - | 354 | 4 | 25,176,596 | 2.5% | 4.17179% | 108 | 2.33x | 14.7% | 58.2% | 47.4% |

| 356 | - | 360 | 43 | 357,533,865 | 36.2% | 3.72283% | 118 | 1.81x | 10.7% | 63.2% | 53.5% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Interest Only | 42 | $565,809,946 | 57.3% | 3.37018% | 107 | 2.96x | 10.2% | 56.0% | 56.0% |

| Interest Only, Amortizing Balloon | 30 | 272,662,000 | 27.6% | 3.68404% | 118 | 1.78x | 10.5% | 64.4% | 55.5% |

| Amortizing Balloon | 22 | 149,571,853 | 15.1% | 4.00367% | 114 | 1.96x | 12.6% | 59.0% | 45.9% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(1)(2) |

| Weighted Average | |||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 1.25x | - | 1.59x | 20 | $98,517,590 | 10.0% | 4.07090% | 118 | 1.45x | 8.5% | 66.4% | 56.5% |

| 1.60x | - | 1.69x | 6 | 58,263,264 | 5.9% | 4.17436% | 112 | 1.67x | 10.2% | 67.1% | 58.7% |

| 1.70x | - | 1.79x | 10 | 76,577,702 | 7.8% | 3.82530% | 118 | 1.73x | 10.2% | 64.6% | 55.3% |

| 1.80x | - | 1.89x | 5 | 64,305,000 | 6.5% | 3.58117% | 118 | 1.86x | 10.6% | 60.2% | 53.6% |

| 1.90x | - | 1.99x | 5 | 82,350,000 | 8.3% | 3.63210% | 116 | 1.92x | 11.0% | 64.1% | 55.0% |

| 2.00x | - | 2.49x | 26 | 264,509,572 | 26.8% | 3.58186% | 117 | 2.16x | 9.6% | 60.7% | 57.3% |

| 2.50x | - | 2.99x | 10 | 122,743,457 | 12.4% | 3.31309% | 112 | 2.79x | 10.3% | 59.5% | 58.6% |

| 3.00x | - | 3.99x | 8 | 134,930,946 | 13.7% | 3.33733% | 96 | 3.47x | 12.5% | 53.6% | 53.6% |

| 4.00x | - | 5.56x | 4 | 85,846,268 | 8.7% | 2.78660% | 90 | 4.92x | 14.4% | 33.9% | 33.7% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| (1) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (3) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(1)(3) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 18.9% | - | 49.9% | 12 | $166,655,225 | 16.9% | 2.98575% | 99 | 4.03x | 13.1% | 40.5% | 39.3% |

| 50.0% | - | 59.9% | 27 | 274,642,926 | 27.8% | 3.56134% | 107 | 2.60x | 11.3% | 56.2% | 52.5% |

| 60.0% | - | 64.9% | 22 | 255,487,165 | 25.9% | 3.79949% | 116 | 1.92x | 9.6% | 62.4% | 56.9% |

| 65.0% | - | 69.9% | 28 | 263,438,482 | 26.7% | 3.62042% | 117 | 2.04x | 9.7% | 67.9% | 62.7% |

| 70.0% | - | 73.4% | 5 | 27,820,000 | 2.8% | 3.95580% | 119 | 1.44x | 8.5% | 73.0% | 59.6% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| LTV Ratios as of the Maturity Date/ARD(1)(3) |

Weighted Average | |||||||||||

| Range of Maturity Date/ARD LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | ||

| 14.5% | - | 49.9% | 29 | $295,064,883 | 29.9% | 3.41817% | 106 | 3.11x | 12.8% | 47.8% | 41.8% |

| 50.0% | - | 59.9% | 36 | 398,838,917 | 40.4% | 3.60127% | 110 | 2.30x | 10.7% | 62.0% | 56.2% |

| 60.0% | - | 64.9% | 18 | 169,920,000 | 17.2% | 3.67356% | 118 | 1.95x | 8.3% | 64.0% | 61.9% |

| 65.0% | - | 69.9% | 11 | 124,220,000 | 12.6% | 3.55092% | 118 | 2.32x | 8.5% | 67.4% | 67.4% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Defeasance | 75 | $649,166,470 | 65.7% | 3.61499% | 117 | 2.18x | 10.1% | 61.6% | 56.6% |

| Yield Maintenance | 17 | 253,877,330 | 25.7% | 3.64199% | 104 | 2.58x | 11.3% | 57.7% | 53.2% |

| Defeasance or Yield Maintenance | 2 | 85,000,000 | 8.6% | 2.81023% | 89 | 4.54x | 12.9% | 40.2% | 40.2% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term | UW NCF DSCR(1)(2) | UW NOI DY(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) |

| Refinance | 57 | $599,501,214 | 60.7% | 3.49088% | 112 | 2.51x | 10.2% | 57.9% | 54.0% |

| Acquisition | 34 | 349,354,779 | 35.4% | 3.66345% | 108 | 2.52x | 11.5% | 59.4% | 54.8% |

| Recapitalization | 3 | 39,187,807 | 4.0% | 3.51093% | 117 | 1.84x | 11.0% | 66.1% | 55.1% |

| Total / Weighted Average: | 94 | $988,043,799 | 100.0% | 3.55269% | 111 | 2.49x | 10.7% | 58.8% | 54.3% |

| (1) | In the case of Loan Nos. 1, 2, 6, 11, 15 and 21, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 2 and 4, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loans and/or mezzanine loans. |

| (2) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (3) | In the case of Loan Nos. 14 and 15, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on an as portfolio assumption or an as-complete assumption, respectively. Refer to “Description of the Mortgage Pool—Assessment of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Collateral Characteristics | ||

Previous Securitization History(1) | |||||||

| No. | Mortgage Loan Seller | Loan Name | Location | Property Type | Cut-off Date Principal Balance | % of IPB | Previous Securitization |

| 3 | SGFC | Parkway Irvine | Irvine, CA | Industrial | $37,000,000 | 3.7% | WFRBS 2012-C7 |

| 5 | SGFC | Fleet Farm Mixed Use | Appleton, WI | Mixed Use | $33,000,000 | 3.3% | CSMC 2016-MFF |

| 12 | UBS AG | Murrieta Spectrum | Murrieta, CA | Mixed Use | $23,030,000 | 2.3% | COMM 2015-LC23 |

| 14.01 | LMF | Jefferson Heights | Watertown, NY | Multifamily | $6,500,000 | 0.7% | FREMF 2016-K53 |

| 14.04 | LMF | Solar Building | Watertown, NY | Mixed Use | $2,300,000 | 0.2% | FREMF 2016-K53 |

| 18 | Barclays | Cumberland Marketplace | Mechanicsburg, PA | Retail | $16,263,000 | 1.6% | UBSCM 2012-C1 |

| 20 | Barclays | Attiva - Park Fort Worth, TX | Fort Worth, TX | Multifamily | $15,080,000 | 1.5% | FREMF 2018-KF55 |

| 23 | UBS AG | Chandler Business Center | Chandler, AZ | Industrial | $12,580,000 | 1.3% | A10 2015-1 |

| 94 | Sabal | Houston Self Storage | Houston, TX | Self Storage | $2,070,000 | 0.2% | BBCMS 2017-C1 |

| (1) | The table above represents the properties for which the previously existing debt was most recently securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Class A-2(1) | ||

No. | Loan Name | Location | Cut-off Date | % of | Maturity | % of | Original | Remaining | UW | UW NOI | Cut-off | Maturity |

| 4 | Broadacres Office Park | Bloomfield, NJ | $33,000,000 | 3.3% | $33,000,000 | 100.0% | 60 | 56 | 3.73x | 14.8% | 58.7% | 58.7% |

| Total / Weighted Average: | $33,000,000 | 3.3% | $33,000,000 | 100.0% | 60 | 56 | 3.73x | 14.8% | 58.7% | 58.7% | ||

| (1) | The table above presents the mortgage loans whose balloon payment would be applied to pay down the certificate balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date or the anticipated repayment date. Each Class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Maturity Date Balance divided by the initial Class A-2 Certificate Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

18

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Class A-3(1) | ||

No. | Loan Name | Location | Cut-off Date | % of | Maturity | % of | Original | Remaining | UW | UW NOI | Cut-off | Maturity Date |

| 1 | One SoHo Square | New York, NY | $70,000,000 | 7.1% | $70,000,000 | 70.9% | 84 | 83 | 4.88x | 13.6% | 34.8% | 34.8% |

| 13 | Merit Medical Systems | Houston, TX | 20,751,500 | 2.1% | 20,751,500 | 21.0% | 84 | 84 | 2.86x | 9.5% | 49.6% | 49.6% |

| 68 | Anytime Self-Storage Arizona Portfolio | Various, AZ | 4,250,000 | 0.4% | 3,889,568 | 3.9% | 84 | 84 | 1.91x | 11.9% | 46.5% | 42.6% |

| 72 | 376 Larkfield Road | East Northport, NY | 4,030,000 | 0.4% | 4,030,000 | 4.1% | 84 | 81 | 2.03x | 8.2% | 65.0% | 65.0% |

| Total / Weighted Average: | $99,031,500 | 10.0% | $98,671,068 | 100.0% | 84 | 83 | 4.21x | 12.4% | 39.6% | 39.5% | ||

| (1) | The table above presents the mortgage loans whose balloon payment would be applied to pay down the certificate balance of the Class A-3 Certificates, assuming a 0% CPR and applying the “Modeling Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date or the anticipated repayment date. Each Class of Certificates, including the Class A-3 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information does not take into account subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Maturity Date Balance divided by the initial Class A-3 Certificate Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

19

| Structural and Collateral Term Sheet | BBCMS 2021-C11 | |

| Structural Overview | ||

| ■ Assets: | The Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-5, Class X-A, Class X-B, Class X-D, Class X-F, Class X-G, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H-RR, Class J-RR and Class R Certificates (collectively, the “Certificates”), will be entitled to distributions solely with respect to the mortgage loans. | |

| ■ Accrual: | Each Class of Certificates (other than Class R Certificates) will accrue interest on a 30/360 basis. The Class R Certificates will not accrue interest. | |