Marcato Capital Management LP One Montgomery Street Suite 3250 San Francisco, CA 94104 | E info@marcatollc.com P 415.796.6350 F 415.651.8866 |

| 1. | How serious is the Company about pursuing a REIT conversion or REIT spin-off transaction? Is the Company simply “exploring” or has the Board in fact determined that this course is attractive and the Company is “pursuing” it? |

| 2. | Is the Company itself converting to a REIT or is the Company considering the formation and spin-off of its real estate into a separate REIT (commonly referred to as a PropCo/OpCo structure)? |

| 3. | How should investors think about the pro forma Income Statements and Balance Sheets of the new companies? |

| 4. | How long will a process take and what are the gating items for completion of a transaction? |

| 5. | Is the Company considering the sale of some or all of the real estate assets to existing triple-net lease companies as an alternative to a spin-off? |

LIFE TIME FITNESS SEPTEMBER 2014

DISCLOSURE 1 Marcato Capital Management LP (“Marcato”) is an SEC - registered investment adviser based in San Francisco, California. Marcato p rovides investment advisory services to its proprietary private investment funds (each a “Marcato Fund” collectively, the “Marcato Funds”). This presentation with respect to Life Time Fitness, Inc. (the “Presentation”) is for informational purposes only and it does no t have regard to the specific investment objective, financial situation, suitability or particular need of any specific person who may receive the Presenta tio n, and should not be taken as advice on the merits of any investment decision. The views expressed in the Presentation represent the opinions of Marcato, and are based on publicly available information and Marcato analyses. Certain financial information and data used in the Presentation have been derive d o r obtained from filings made with the Securities and Exchange Commission (“SEC”) by the issuer or other companies that Marcato considers comparable. Ma rcato has not sought or obtained consent from any third party to use any statements or information indicated in the Presentation as having bee n obtained or derived from a third party. Any such statements or information should not be viewed as indicating the support of such third party fo r t he views expressed. Information contained in the Presentation has not been independently verified by Marcato, and. Marcato disclaims any and al l l iability as to the completeness or accuracy of the information and for any omissions of material facts. Marcato undertakes no obligation to cor rec t, update or revise the Presentation or to otherwise provide any additional materials. Neither Marcato nor any of its affiliates makes any represent ati on or warranty, express or implied, as to the accuracy, fairness or completeness of the information contained herein and the recipient agrees and acknow led ges that it will not rely on any such information. The Presentation may contain forward - looking statements which reflect Marcato’s views with respect to, among other things, futur e events and financial performance. Forward - looking statements are subject to various risks and uncertainties and assumptions. If one or more of the risks or uncertainties materialize, or if Marcato’s underlying assumptions prove to be incorrect, the actual results may vary materially from outcom es indicated by these statements. Accordingly, forward - looking statements should not be regarded as a representation by Marcato that the future plans , estimates or expectations contemplated will ever be achieved. The securities or investment ideas listed are not presented in order to suggest or show profitability of any or all transacti ons . There should be no assumption that any specific portfolio securities identified and described in the Presentation were or will be profitable. Under no circ ums tances is the Presentation to be used or considered as an offer to sell or a solicitation of an offer to buy any security, nor does the Presentation constitut e e ither an offer to sell or a solicitation of an offer to buy any interest in the Marcato Funds. Any such offer would only be made at the time a qualified offeree receives the Confidential Explanatory Memorandum of a Marcato Fund. Any investment in the Marcato Funds is speculative and involves subst ant ial risk, including the risk of losing all or substantially all of such investment. Marcato may change its views or its investment positions described in the Presentation at any time as it deems appropriate. Mar cato may buy or sell or otherwise change the form or substance of any of its investments in any manner permitted by law and expressly disclaims any o bli gation to notify the market, a recipient of the Presentation or any other party of any such changes.

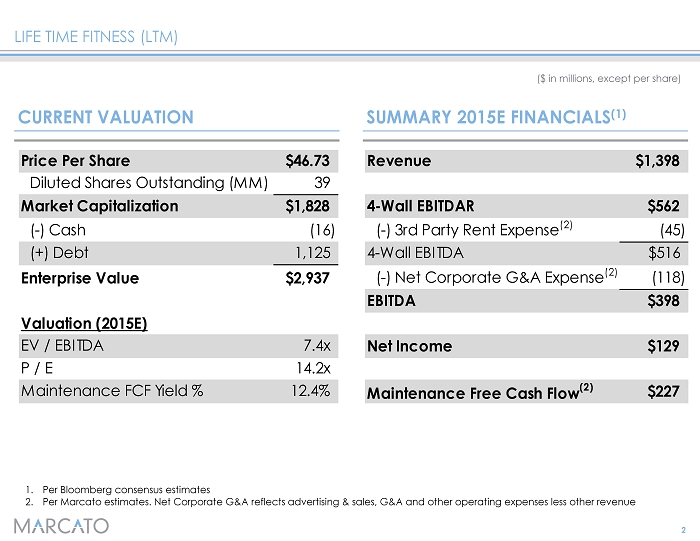

Revenue $1,398 4-Wall EBITDAR $562 (-) 3rd Party Rent Expense (2) (45) 4-Wall EBITDA $516 (-) Net Corporate G&A Expense (2) (118) EBITDA $398 Net Income $129 Maintenance Free Cash Flow (2) $227 LIFE TIME FITNESS ( LTM ) 2 CURRENT VALUATION SUMMARY 2015E FINANCIALS (1) 1. Per Bloomberg consensus estimates 2. Per Marcato estimates. Net Corporate G&A reflects advertising & sales, G&A and other operating expenses less other revenue ($ in millions, except per share) Price Per Share $46.73 Diluted Shares Outstanding (MM) 39 Market Capitalization $1,828 (-) Cash (16) (+) Debt 1,125 Enterprise Value $2,937 Valuation (2015E) EV / EBITDA 7.4x P / E 14.2x Maintenance FCF Yield % 12.4%

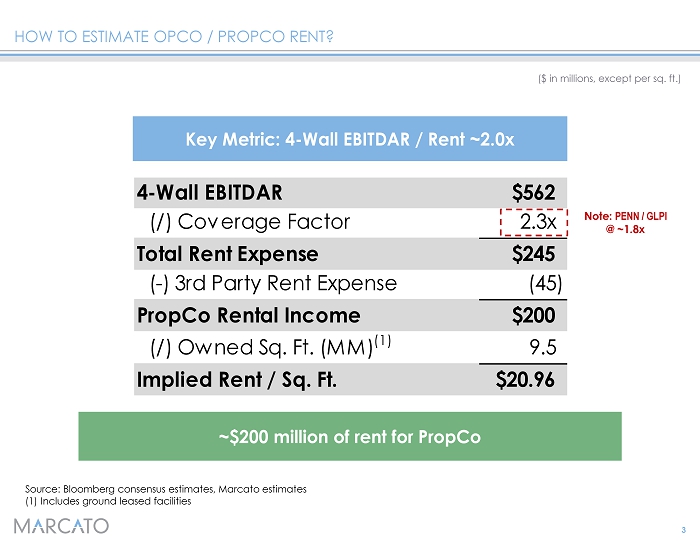

HOW TO ESTIMATE OPCO / PROPCO RENT? 3 Key Metric: 4 - Wall EBITDAR / Rent ~2.0x ($ in millions, except per sq. ft.) Source : Bloomberg consensus estimates, Marcato estimates (1) Includes ground leased facilities ~$200 million of rent for PropCo Note: PENN / GLPI @ ~1.8x 4-Wall EBITDAR $562 (/) Coverage Factor 2.3x Total Rent Expense $245 (-) 3rd Party Rent Expense (45) PropCo Rental Income $200 (/) Owned Sq. Ft. (MM) (1) 9.5 Implied Rent / Sq. Ft. $20.96

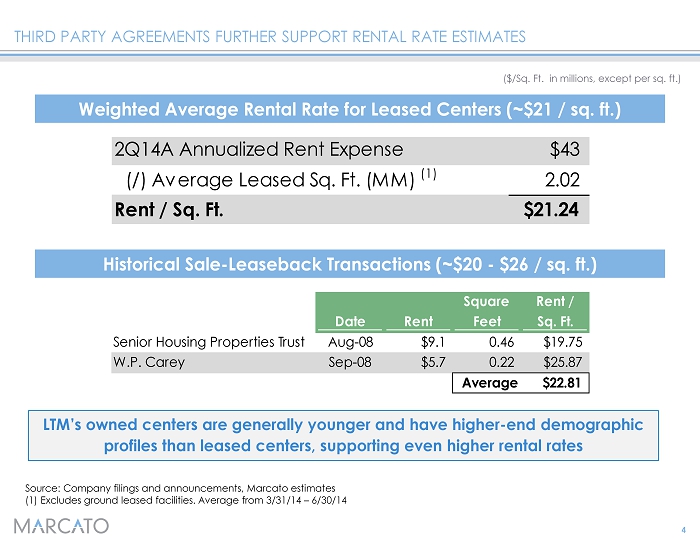

THIRD PARTY AGREEMENTS FURTHER SUPPORT RENTAL RATE ESTIMATES 4 ($/Sq. Ft. in millions, except per sq. ft.) Source : Company filings and announcements, Marcato estimates (1) Excludes ground leased facilities. Average from 3/31/14 – 6/30/14 Historical Sale - Leaseback Transactions (~$20 - $26 / sq. ft.) Weighted Average Rental Rate for Leased Centers (~$21 / sq. ft.) 2Q14A Annualized Rent Expense $43 (/) Average Leased Sq. Ft. (MM) (1) 2.02 Rent / Sq. Ft. $21.24 LTM’s owned centers are generally younger and have higher - end demographic profiles than leased centers, supporting even higher rental rates Square Rent / Date Rent Feet Sq. Ft. Senior Housing Properties Trust Aug-08 $9.1 0.46 $19.75 W.P. Carey Sep-08 $5.7 0.22 $25.87 Average $22.81

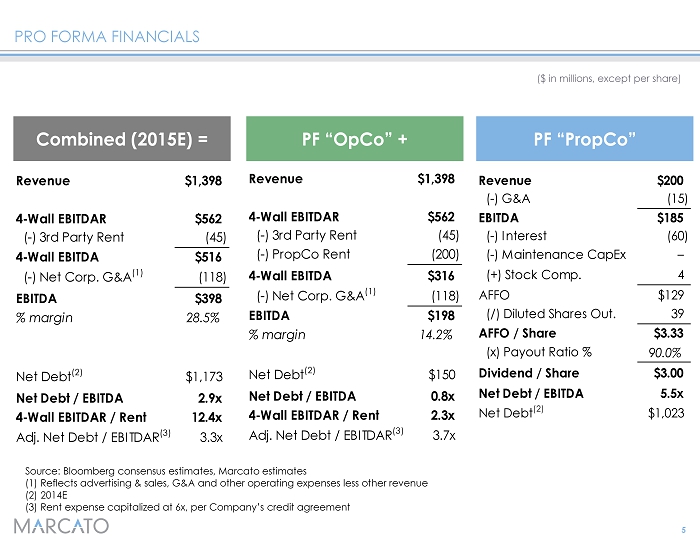

Revenue $200 (-) G&A (15) EBITDA $185 (-) Interest (60) (-) Maintenance CapEx – (+) Stock Comp. 4 AFFO $129 (/) Diluted Shares Out. 39 AFFO / Share $3.33 (x) Payout Ratio % 90.0% Dividend / Share $3.00 Net Debt / EBITDA 5.5x Net Debt (2) $1,023 Revenue $1,398 4-Wall EBITDAR $562 (-) 3rd Party Rent (45) (-) PropCo Rent (200) 4-Wall EBITDA $316 (-) Net Corp. G&A (1) (118) EBITDA $198 % margin 14.2% Net Debt (2) $150 Net Debt / EBITDA 0.8x 4-Wall EBITDAR / Rent 2.3x Adj. Net Debt / EBITDAR (3) 3.7x PRO FORMA FINANCIALS 5 Combined (2015E) = ($ in millions, except per share) Source: Bloomberg consensus estimates, Marcato estimates (1) Reflects advertising & sales, G&A and other operating expenses less other revenue (2) 2014E (3) Rent expense capitalized at 6x, per Company’s credit agreement PF “ OpCo ” + PF “ PropCo ” Revenue $1,398 4-Wall EBITDAR $562 (-) 3rd Party Rent (45) 4-Wall EBITDA $516 (-) Net Corp. G&A (1) (118) EBITDA $398 % margin 28.5% Net Debt (2) $1,173 Net Debt / EBITDA 2.9x 4-Wall EBITDAR / Rent 12.4x Adj. Net Debt / EBITDAR (3) 3.3x

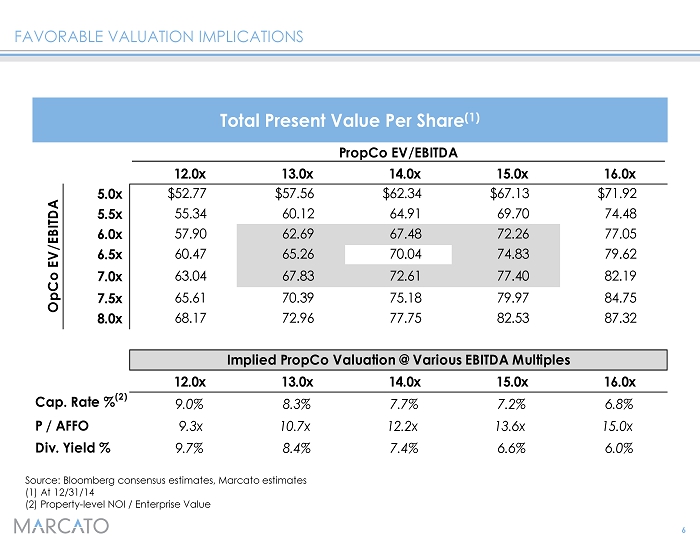

FAVORABLE VALUATION IMPLICATIONS 6 Source: Bloomberg consensus estimates, Marcato estimates (1) At 12/31/14 (2) Property - level NOI / Enterprise Value Total Present Value Per Share (1) PropCo EV/EBITDA 12.0x 13.0x 14.0x 15.0x 16.0x 5.0x $52.77 $57.56 $62.34 $67.13 $71.92 5.5x 55.34 60.12 64.91 69.70 74.48 6.0x 57.90 62.69 67.48 72.26 77.05 6.5x 60.47 65.26 70.04 74.83 79.62 7.0x 63.04 67.83 72.61 77.40 82.19 7.5x 65.61 70.39 75.18 79.97 84.75 8.0x 68.17 72.96 77.75 82.53 87.32 Implied PropCo Valuation @ Various EBITDA Multiples 12.0x 13.0x 14.0x 15.0x 16.0x Cap. Rate % (2) 9.0% 8.3% 7.7% 7.2% 6.8% P / AFFO 9.3x 10.7x 12.2x 13.6x 15.0x Div. Yield % 9.7% 8.4% 7.4% 6.6% 6.0% OpCo EV/EBITDA

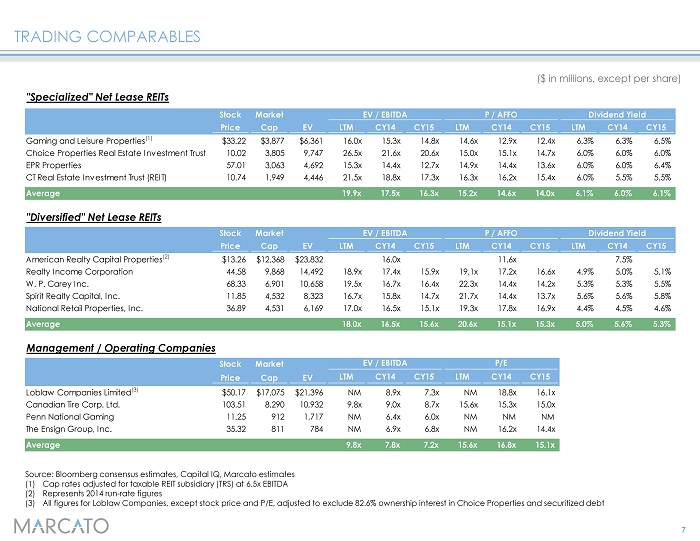

TRADING COMPARABLES 7 ($ in millions, except per share) Source: Bloomberg consensus estimates, Capital IQ, Marcato estimates (1) Cap rates adjusted for taxable REIT subsidiary ( TRS ) at 6.5x EBITDA (2) Represents 2014 run - rate figures (3) All figures for Loblaw Companies, except stock price and P/E, adjusted to exclude 82.6% ownership interest in Choice Properties a nd securitized debt "Specialized" Net Lease REITs Stock Market EV / EBITDA P / AFFO Dividend Yield Price Cap EV LTM CY14 CY15 LTM CY14 CY15 LTM CY14 CY15 Gaming and Leisure Properties (1) $33.22 $3,877 $6,361 16.0x 15.3x 14.8x 14.6x 12.9x 12.4x 6.3% 6.3% 6.5% Choice Properties Real Estate Investment Trust 10.02 3,805 9,747 26.5x 21.6x 20.6x 15.0x 15.1x 14.7x 6.0% 6.0% 6.0% EPR Properties 57.01 3,063 4,692 15.3x 14.4x 12.7x 14.9x 14.4x 13.6x 6.0% 6.0% 6.4% CT Real Estate Investment Trust (REIT) 10.74 1,949 4,446 21.5x 18.8x 17.3x 16.3x 16.2x 15.4x 6.0% 5.5% 5.5% Average 19.9x 17.5x 16.3x 15.2x 14.6x 14.0x 6.1% 6.0% 6.1% "Diversified" Net Lease REITs Stock Market EV / EBITDA P / AFFO Dividend Yield Price Cap EV LTM CY14 CY15 LTM CY14 CY15 LTM CY14 CY15 American Realty Capital Properties (2) $13.26 $12,368 $23,832 16.0x 11.6x 7.5% Realty Income Corporation 44.58 9,868 14,492 18.9x 17.4x 15.9x 19.1x 17.2x 16.6x 4.9% 5.0% 5.1% W. P. Carey Inc. 68.33 6,901 10,658 19.5x 16.7x 16.4x 22.3x 14.4x 14.2x 5.3% 5.3% 5.5% Spirit Realty Capital, Inc. 11.85 4,532 8,323 16.7x 15.8x 14.7x 21.7x 14.4x 13.7x 5.6% 5.6% 5.8% National Retail Properties, Inc. 36.89 4,531 6,169 17.0x 16.5x 15.1x 19.3x 17.8x 16.9x 4.4% 4.5% 4.6% Average 18.0x 16.5x 15.6x 20.6x 15.1x 15.3x 5.0% 5.6% 5.3% Management / Operating Companies Stock Market EV / EBITDA P/E EBITDAR Price Cap EV LTM CY14 CY15 LTM CY14 CY15 Loblaw Companies Limited (3) $50.17 $17,075 $21,396 NM 8.9x 7.3x NM 18.8x 16.1x Canadian Tire Corp. Ltd. 103.51 8,290 10,932 9.8x 9.0x 8.7x 15.6x 15.3x 15.0x Penn National Gaming 11.25 912 1,717 NM 6.4x 6.0x NM NM NM The Ensign Group, Inc. 35.32 811 784 NM 6.9x 6.8x NM 16.2x 14.4x Average 9.8x 7.8x 7.2x 15.6x 16.8x 15.1x

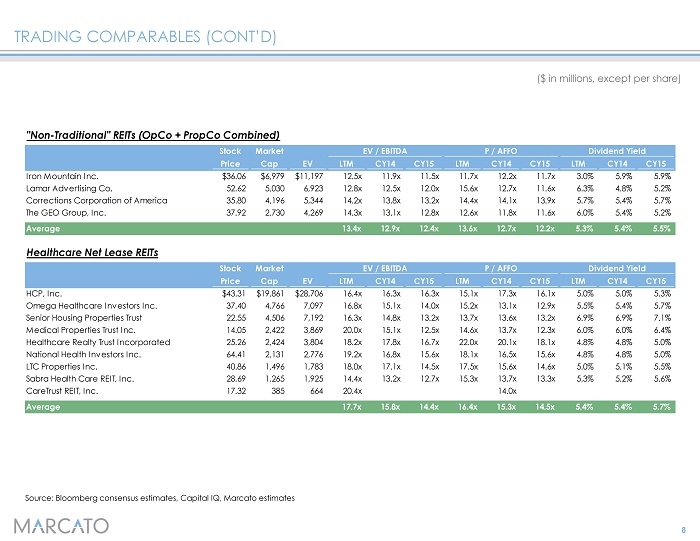

TRADING COMPARABLES (CONT’D) 8 ($ in millions, except per share) Source: Bloomberg consensus estimates, Capital IQ, Marcato estimates "Non-Traditional" REITs (OpCo + PropCo Combined) Stock Market EV / EBITDA P / AFFO Dividend Yield Price Cap EV LTM CY14 CY15 LTM CY14 CY15 LTM CY14 CY15 Iron Mountain Inc. $36.06 $6,979 $11,197 12.5x 11.9x 11.5x 11.7x 12.2x 11.7x 3.0% 5.9% 5.9% Lamar Advertising Co. 52.62 5,030 6,923 12.8x 12.5x 12.0x 15.6x 12.7x 11.6x 6.3% 4.8% 5.2% Corrections Corporation of America 35.80 4,196 5,344 14.2x 13.8x 13.2x 14.4x 14.1x 13.9x 5.7% 5.4% 5.7% The GEO Group, Inc. 37.92 2,730 4,269 14.3x 13.1x 12.8x 12.6x 11.8x 11.6x 6.0% 5.4% 5.2% Average 13.4x 12.9x 12.4x 13.6x 12.7x 12.2x 5.3% 5.4% 5.5% Healthcare Net Lease REITs Stock Market EV / EBITDA P / AFFO Dividend Yield Price Cap EV LTM CY14 CY15 LTM CY14 CY15 LTM CY14 CY15 HCP, Inc. $43.31 $19,861 $28,706 16.4x 16.3x 16.3x 15.1x 17.3x 16.1x 5.0% 5.0% 5.3% Omega Healthcare Investors Inc. 37.40 4,766 7,097 16.8x 15.1x 14.0x 15.2x 13.1x 12.9x 5.5% 5.4% 5.7% Senior Housing Properties Trust 22.55 4,506 7,192 16.3x 14.8x 13.2x 13.7x 13.6x 13.2x 6.9% 6.9% 7.1% Medical Properties Trust Inc. 14.05 2,422 3,869 20.0x 15.1x 12.5x 14.6x 13.7x 12.3x 6.0% 6.0% 6.4% Healthcare Realty Trust Incorporated 25.26 2,424 3,804 18.2x 17.8x 16.7x 22.0x 20.1x 18.1x 4.8% 4.8% 5.0% National Health Investors Inc. 64.41 2,131 2,776 19.2x 16.8x 15.6x 18.1x 16.5x 15.6x 4.8% 4.8% 5.0% LTC Properties Inc. 40.86 1,496 1,783 18.0x 17.1x 14.5x 17.5x 15.6x 14.6x 5.0% 5.1% 5.5% Sabra Health Care REIT, Inc. 28.69 1,265 1,925 14.4x 13.2x 12.7x 15.3x 13.7x 13.3x 5.3% 5.2% 5.6% CareTrust REIT, Inc. 17.32 385 664 20.4x 14.0x Average 17.7x 15.8x 14.4x 16.4x 15.3x 14.5x 5.4% 5.4% 5.7%