UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2022

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report _____________

For the transition period from _____________ to _____________

Commission File Number: 001-35755

Bit Brother Limited

(Exact name of Registrant as specified in its charter)

___________________________________________

(Translation of Registrant’s name into English)

British Virgin Islands

(Jurisdiction of incorporation or organization)

15/F, Block A, Kineer Business Centre

53 Binjiang Road, Yuelu District

Changsha, Hunan Province, China 410023

(Address of principal executive offices)

Xianlong Wu

Chief Executive Officer

15/F, Block A, Kineer Business Centre

53 Binjiang Road, Yuelu District

Changsha, Hunan Province, China 410023

People’s Republic of China

Tel: +86 0731-85133570

Email: jack.wu@bitbrother.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered | |

| Class A Ordinary Shares | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Not Applicable

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Not Applicable

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of June 30, 2022, the issuer had 116,773,794 Class A ordinary shares issued and outstanding and 975,000 Class B ordinary shares issued and outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer | ☒ |

| Emerging growth company | ☐ | ||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

i

INTRODUCTORY NOTES

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

| ● | the “Company,” “we,” “us,” “our company” and “our” refer to Bit Brother Limited, formerly Urban Tea, Inc. (together with its subsidiaries and affiliated entities, except for when the context indicates otherwise); |

| ● | “BVI” are to the British Virgin Islands; |

| ● | “Hong Kong” are to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| ● | “PRC” and “China” are to the People’s Republic of China; |

| ● | “SEC” are to the Securities and Exchange Commission; |

| ● | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

| ● | “Securities Act” are to the Securities Act of 1933, as amended; |

| ● | “Renminbi” and “RMB” are to the legal currency of China; |

| ● | “Hong Kong dollars,” “HKD” and “HK$” are to the legal currency of Hong Kong; and |

| ● | “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States. |

Our financial statements are expressed in U.S. dollars, which is our reporting currency. Certain financial data in this annual report on Form 20-F is converted into U.S. dollars solely for the reader’s convenience. Unless otherwise noted, all conversions from Renminbi to U.S. dollars in this annual report on Form 20-F were made at a rate of RMB 6.4544 to US$1.00, the average exchange rate for the fiscal year ended June 30, 2022 as set forth at www.x-rates.com. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, at the rate stated above, or at all.

ii

FORWARD-LOOKING STATEMENTS

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; and any statements regarding future economic conditions or performance, as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements. Potential risks and uncertainties include, among other things, the possibility that we may not be able to maintain or increase our net revenues and profits due to our failure to anticipate market demand and develop new products, our failure to execute our business expansion plan, changes in domestic and foreign laws, regulations and taxes, changes in economic conditions, uncertainties related to China’s legal system and economic, political and social events in China, a general economic downturn, a downturn in the securities markets, and other risks and uncertainties which are generally set forth under Item 3 “Key information—D. Risk Factors” and elsewhere in this report.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation, except as required by law, to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

iii

PART I

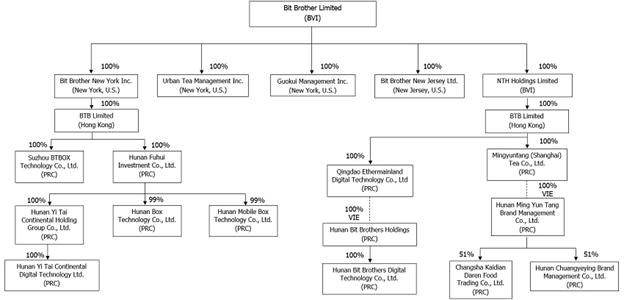

We are an offshore holding company conducting part of our operations in China through Hunan Ming Yun Tang Brand Management Co., Ltd., or Hunan MYT, and Hunan Bit Brothers Holding Co., Ltd., or Hunan BTB, the variable interest entities, and their subsidiaries. You are not investing in Hunan MYT, or Hunan BTB, our VIEs. Neither we nor our subsidiaries own any share in Hunan MYT or Hunan BTB. Instead, we control and receive the economic benefits of Hunan MYT and Hunan BTB’s business operation through a series of contractual arrangements, also known as VIE Agreements, dated November 19, 2018 and May 13, 2021, respectively. The VIE Agreements are designed to provide our wholly-foreign owned entities, Mingyuntang (Shanghai) Tea Co., Ltd. and Qingdao Ether Continent Digital Technology Co., Ltd., with the power, rights, and obligations equivalent in all material respects to those it would possess as the principal equity holders of Hunan MYT and Hunan BTB, including absolute control rights and the rights to the assets, property, and revenues of Hunan MYT and Hunan BTB. As a result of our direct ownership in the WFOEs and the VIE Agreements, we are regarded as the primary beneficiary of the VIEs. See “Business — Contractual Agreements between WFOEs and Hunan MYT and Hunan BTB” for a summary of these VIE Agreements.

Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to the validity and enforcement of the VIE Agreements. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard. The VIE Agreements may not be effective in providing control over the VIEs. We may also subject to sanctions imposed by PRC regulatory agencies including Chinese Securities Regulatory Commission if we fail to comply with their rules and regulations. We may also be subject to PRC laws relating to, among others, data security and restrictions over foreign investments due to the complexity of the regulatory regime in China, and the recent statements and regulatory actions by the PRC government relating to data security may affect our remaining business operations in China or even our ability to offer securities in the United States. Neither we nor any of our subsidiaries has obtained the approval from either the China Securities Regulatory Commission (the “CSRC”) or the Cyberspace Administration of China (the “CAC”) for any offering we may have in the future, and we do not intend to obtain the approval from either the CSRC or the CAC in connection with any such offering, since we do not believe, based upon advice of our PRC counsel, Taihang Group, that such approval is required under these circumstances or for the time being. We cannot assure you, however, that regulators in China will not take a contrary view or will not subsequently require us to undergo the approval procedures and subject us to penalties for non-compliance. See “Risk Factors—Risks Related to Doing Business in China—Recent regulatory developments in China may subject us to additional regulatory review and disclosure requirement, expose us to government interference, or otherwise restrict our ability to offer securities and raise capitals outside China, all of which could materially and adversely affect our business and the value of our securities.”

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Implications of Being a Foreign Private Issuer and a China based company.

We are a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions of the securities rules and regulations in the United States that are applicable to U.S. domestic issuers. Moreover, the information we are required to file with or furnish to the SEC will be less extensive and less timely compared to that required to be filed with the SEC by U.S. domestic issuers. In addition, as a company incorporated in the British Virgin Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from the Nasdaq listing standards. These practices may afford less protection to shareholders than they would enjoy if we complied fully with the Nasdaq listing standards.

1

We are an offshore holding company conducting part of our operations in China through the VIEs and their subsidiaries. You are not investing in the VIEs. Neither we nor our subsidiaries own any share in the VIEs. Instead, we control and receive the economic benefits of the VIEs’ business operations through a series of contractual arrangements, also known as VIE Agreements, dated November 19, 2018, and May 13, 2021. The VIE Agreements are designed to provide our WFOEs, Mingyuntang (Shanghai) Tea Co., Ltd., or Shanghai MYT, and Qingdao Ether Continent Digital Technology Co., Ltd., or Qingdao ECDT, with the power, rights, and obligations equivalent in all material respects to those it would possess as the principal equity holders of the VIEs, including absolute control rights and the rights to the assets, property, and revenues of the VIEs. As a result of our direct ownership in the WFOE and the VIE Agreements, we are regarded as the primary beneficiary of the VIEs. See “Business — Contractual Agreements between WFOEs and Hunan MYT, and Hunan BTB” for a summary of these VIE Agreements.

Because of our corporate structure, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to the validity and enforcement of the VIE Agreements. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard. Our VIE Agreements may not be effective in providing control over the VIEs. We may also subject to sanctions imposed by PRC regulatory agencies including Chinese Securities Regulatory Commission if we fail to comply with their rules and regulations. We may also be subject to PRC laws relating to, among others, data security and restrictions over foreign investments due to the complexity of the regulatory regime in China, and the recent statements and regulatory actions by the PRC government relating to data security may affect our remaining business operations in China or even our ability to offer securities in the United States. Neither we nor any of our subsidiaries has obtained the approval from either the China Securities Regulatory Commission (the “CSRC”) or the Cyberspace Administration of China (the “CAC”) for any offering we may have in the future, and we do not intend to obtain the approval from either the CSRC or the CAC in connection with any such offering, since we do not believe, based upon advice of our PRC counsel, Taihang Group, that such approval is required under these circumstances or for the time being. We cannot assure you, however, that regulators in China will not take a contrary view or will not subsequently require us to undergo the approval procedures and subject us to penalties for non-compliance. See “Risk Factors—Risks Related to Doing Business in China—Recent regulatory developments in China may subject us to additional regulatory review and disclosure requirement, expose us to government interference, or otherwise restrict our ability to offer securities and raise capitals outside China, all of which could materially and adversely affect our business and the value of our securities.”

The following are summaries of the VIE Agreements:

On November 19, 2018, Shanghai MYT entered into a series of VIE agreements with Hunan MYT and its shareholder Peng Fang. The VIE agreements are designed to provide Shanghai MYT with the power, rights and obligations equivalent in all material respects to those it would possess as the sole equity holder of Hunan MYT, including absolute control rights and the rights to the management, operations, assets, property and revenue of Hunan MYT. The purpose of the VIE agreements is solely to give Shanghai MYT the exclusive control over Hunan MYT’s management and operations. Hunan MYT commenced operations in December 2018, and was engaged in the specialty tea product distribution and retail business by provision of high-quality tea beverages in its tea shop chain.

2

On May 13, 2021, Qingdao ECDT entered into a series of VIE agreements with Hunan BTB and its shareholders. The VIE agreements are designed to provide Qingdao ECDT with the power, rights and obligations equivalent in all material respects to those it would possess as the controlling equity holder of Hunan BTB, including absolute control rights and the rights to the management, operations, assets, property and revenue of Hunan BTB. The purpose of the Hunan BTB VIE agreements is solely to give Qingdao ECDT the exclusive control over Hunan BTB’s management and operations. Hunan BTB commenced operations in May, 2021, and has begun conducting research and development of its cryptocurrency distribution platform and application solutions.

As of June 30, 2022 and 2021, the consolidated VIEs accounted for an aggregate of 44.2% and 25.8% of our total assets, respectively. As of June 30 and 2022 and 2021, $0.92 million and $1.35 million of cash and cash equivalents were denominated in RMB, respectively.

Our ability to pay dividends depends upon dividends paid by our operating entities. If the operating entity incurs debt on its own behalf, the instruments governing its debt may restrict its ability to pay dividends to us.

The operating entity in China will be permitted to pay dividends to us only out of its retained earnings, if any, as determined in accordance with the Accounting Standards for Business Enterprise as promulgated by the Ministry of Finance of the PRC, or PRC GAAP. In accordance with PRC company laws, any consolidated VIEs in China must make appropriations from its after-tax profits to non-distributable reserve funds including (i) statutory surplus fund and (ii) discretionary surplus fund. The appropriation to the statutory surplus fund must be at least 10% of the after-tax profits calculated in accordance with PRC GAAP. Appropriation is not required if the statutory surplus fund has reached 50% of the registered capital of the consolidated VIEs. Appropriation to discretionary surplus fund will be made at the discretion of the consolidated VIEs.

Pursuant to the law applicable to China’s foreign investment enterprises, an operating entity that is a foreign investment enterprise in the PRC has to make appropriation from its after-tax profit, as determined under PRC GAAP, to reserve funds including (i) general reserve fund, (ii) enterprise expansion fund and (iii) staff bonus and welfare fund. The appropriation to the general reserve fund must be at least 10% of the after-tax profits calculated in accordance with PRC GAAP. Appropriation is not required if the reserve fund has reached 50% of the registered capital of the operating company. Appropriation to the other two reserve funds is at the discretion of the operating company in China.

As an offshore holding company, we will be permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to the operating entities (as a subsidiary) in China only through loans or capital contributions, and to the consolidated affiliated entity only through loans, in each case subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to the onshore entities (i.e. the PRC subsidiaries and VIE entities), we will be required to make filings about details of the loans with SAFE in accordance with relevant PRC laws and regulations. The PRC subsidiaries and VIE entities that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations.

As of the date of this report, there have not been any dividends or distributions made to the holding company, nor have there been any dividends or distributions made to U.S. investors. We are subject to restrictions on foreign exchange and our ability to transfer cash between entities, across borders, and to U.S. investors. We are also subject to restrictions and limitations on our ability to distribute earnings from our businesses, including subsidiaries and/or consolidated VIEs, to our holding company and U.S. investors as well as the ability to settle amounts owed under the VIE agreements. See “Risks Related to Doing Business in China — Governmental control of currency conversion may limit our ability to utilize our net revenue effectively and our ability to transfer cash between our PRC subsidiaries and us, across borders, and to investors and affect the value of your investment”

3

The following financial information of the VIEs in the PRC was recorded in the accompanying consolidated financial statements:

| June 30, 2022 | June 30, 2021 | |||||||

| ASSETS | ||||||||

| Cash | $ | 922,197 | $ | 1,348,776 | ||||

| Short-term investments | - | 116,417 | ||||||

| Inventories | 121,733 | 104,296 | ||||||

| Loan due from a third party | - | 12,301,391 | ||||||

| Other current assets | 51,004 | 241,239 | ||||||

| Long-term investment | 1,100,294 | 1,144,306 | ||||||

| Goodwill | 227,683 | - | ||||||

| Property and equipment, net | 2,278,091 | 758,302 | ||||||

| Deposits for plant, property and equipment | 45,755,946 | 1,006,234 | ||||||

| Other noncurrent assets | 131,266 | 271,284 | ||||||

| Total Assets | $ | 50,588,214 | $ | 17,292,785 | ||||

| Other liabilities | 666,841 | 218,577 | ||||||

| Total Liabilities | $ | 666,841 | $ | 218,577 | ||||

| For the Years Ended June 30, | ||||||||||||

| 2022 | 2021 | 2020 | ||||||||||

| Revenue | $ | 765,094 | $ | 358,515 | $ | 448,000 | ||||||

| Net loss | (2,671,274 | ) | (401,387 | ) | (1,558,038 | ) | ||||||

PCAOB Inspection

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. The HFCA Act states if the SEC determines that a company has filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit such ordinary shares from being traded on a national securities exchange or in the over the counter trading market in the U.S. The Company’s auditors, Centurion ZD CPA & Co., is subject to the PCAOB’s inspection.

Our independent registered public accounting firm is located in and organized under the laws of Hong Kong and China. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”) governing inspections and investigations of audit firms based in mainland China and Hong Kong, taking the first step toward opening access for the PCAOB to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. However, uncertainties still exist as to whether and how this new Protocol will be implemented and whether the PCAOB can make a determination that it is able to inspect and investigate completely in mainland China and Hong Kong. When the PCAOB reassesses its determinations by the end of 2022, it could determine that it is still unable to inspect and investigate completely audit firms based in mainland China and Hong Kong.

Risk Factors Summary

Investing in our ordinary shares involves a high degree of risk. Below is a summary of material factors that make an investment in our ordinary shares speculative or risky. Importantly, this summary does not address all of the risks that we face. Please refer to the information contained in and incorporated by reference under the heading “Risk Factors” on page 5 of this annual report for additional discussion of the risks summarized in this risk factor summary as well as other risks that we face. These risks include, but are not limited to, the following:

| ● | The outbreak of the COVID-19 has negatively impacted our business operations and is expected to continue to have an adverse impact on our planned operations. |

| ● | We are a holding company with no material operations of our own, we conduct a substantial majority of our operations through our subsidiaries established in the PRC and VIE. We control and receive the economic benefits of our VIE’s business operations through certain contractual arrangements. Our Class A ordinary shares are shares of our offshore holding company instead of shares of our VIE in China. |

| ● | If the PRC government deems that the contractual arrangements in relation to the VIEs do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. |

4

| ● | Contractual arrangements in relation to our variable interest entities may be subject to scrutiny by the PRC tax authorities and they may determine that we or our PRC variable interest entity owe additional taxes, which could negatively affect our results of operations and the value of your investment. |

| ● | Because we are a British Virgin Islands corporation and all of our business is conducted in the PRC, you may be unable to bring an action against us or our officers and directors or to enforce any judgment you may obtain. |

| ● | PRC regulations relating to investments in offshore companies by PRC residents may subject our PRC-resident beneficial owners or our PRC subsidiaries to liability or penalties, limit our ability to inject capital into our PRC subsidiaries or limit our PRC subsidiaries’ ability to increase their registered capital or distribute profits. |

| ● | We are a “foreign private issuer” and our disclosure obligations differ from those of U.S. domestic reporting companies. As a result, we may not provide you the same information as U.S. domestic reporting companies or we may provide information at different times, which may make it more difficult for you to evaluate our performance and prospects. |

| A. | [Reserved] |

| B. | Capitalization and indebtedness. |

Not applicable.

| C. | Reasons for the offer and use of proceeds. |

Not applicable.

| D. | Risk factors. |

You should carefully consider the following risk factors in addition to the other information included or incorporated by reference in this report, including matters addressed in the section entitled “Forward-Looking Statements”. We caution you not to place undue reliance on the forward-looking statements contained in this report, which speak only as of the date hereof.

The risks and uncertainties described below include all of the material risks applicable to us; however, they are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations.

Risks Relating to Our Corporate Structure

We do not have direct ownership of our operating entities in China, but have control rights and the rights to the assets, property, and revenue of the VIEs through VIE Agreements, which may not be effective in providing control over the VIEs.

We do not have direct ownership of our operating entities in China, but have control rights and the rights to the assets, property, and revenue of the VIEs through VIE Agreements. A portion of our current revenue is derived from the VIEs in China. To comply with PRC laws and regulations, we do not intend to have an equity ownership interest in the VIEs but rely on VIE Agreements with the VIEs to control and operate its businesses. However, as discussed above, these VIE Agreements may not be effective from PRC laws in providing us with the necessary control over the VIEs and its operations. Any deficiency in these VIE Agreements may result in our loss of control over the management and operations of the VIEs, which will result in a significant loss in the value of an investment in our company. Because of the practical restrictions on direct foreign equity ownership imposed by the Hunan provincial government authorities, we must rely on contractual rights through our VIE structure to effect control over and management of the VIEs, which exposes us to the risk of potential breach of contract by the shareholders of the VIEs.

Because we are an offshore holding company and conduct our business the VIEs in China, if we fail to comply with applicable PRC law, we could be subject to severe penalties and our business could be adversely affected.

We are an offshore holding company and operate a portion of our business through the VIEs in China through VIE Agreements, as a result of which, under United States generally accepted accounting principles, the assets and liabilities of the VIEs are treated as our assets and liabilities and the results of operations of the VIEs are treated in all respects as if they were the results of our operations. There are uncertainties regarding the interpretation and application of PRC laws, rules and regulations, including but not limited to the laws, rules and regulations governing the validity and enforcement of the VIE Agreements between the WFOEs and the VIEs.

The Provisions Regarding Mergers and Acquisitions of Domestic Projects by Foreign Investors (the “M&A Rules”) requires an overseas special purpose vehicle that are controlled by PRC companies or individuals formed for the purpose of seeking a public listing on an overseas stock exchange through acquisitions of PRC domestic companies using shares of such special purpose vehicle or held by its shareholders as considerations to obtain the approval of the China Securities Regulatory Commission, or the CSRC, prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. However, the application of the M&A Rules remains unclear. If CSRC approval is required, it is uncertain whether it would be possible for us to obtain the approval. Any failure to obtain or delay in obtaining CSRC approval for our offerings would subject us to sanctions imposed by the CSRC and other PRC regulatory agencies.

Furthermore, on December 28, 2021, the Cyberspace Administration of China (“CAC”) and other relevant PRC governmental authorities jointly promulgated the Cybersecurity Review Measures, which became effective on February 15, 2022. According to the Cybersecurity Review Measures, a cybersecurity review assesses potential national security risks that may be brought about by any procurement, data processing, or overseas listing. The Cybersecurity Review Measures require that an online platform operator which possesses the personal information of at least one million users must apply for a cybersecurity review by the CAC if it intends to be listed in foreign countries.

5

If WFOEs, the VIEs or their ownership structure or the VIE Agreements are determined to be in violation of any existing or future PRC laws, rules or regulations, or WFOEs or the VIEs fail to obtain or maintain any of the required governmental permits or approvals, the relevant PRC regulatory authorities would have broad discretion in dealing with such violations, including:

| ● | revoking the business and operating licenses of WFOEs or the VIEs; | |

| ● | discontinuing or restricting the operations of WFOEs or the VIEs; | |

| ● | imposing conditions or requirements with which we, WFOEs, or the VIEs may not be able to comply; | |

| ● | requiring us, WFOEs, or the VIEs to restructure the relevant ownership structure or operations which may significantly impair the rights of the holders of our Class A Ordinary Shares in the equity of the VIEs; and | |

| ● | imposing fines. |

We cannot assure you that the PRC courts or regulatory authorities may not determine that our corporate structure and VIE Agreements violate PRC laws, rules or regulations. If the PRC courts or regulatory authorities determine that our contractual arrangements are in violation of applicable PRC laws, rules or regulations, our VIE Agreements will become invalid or unenforceable, and the VIEs will not be treated as VIE entities and we will not be entitled to treat the VIEs’ assets, liabilities and results of operations as our assets, liabilities and results of operations, which could effectively eliminate the assets, revenue and net income of the VIEs from our balance sheet, which would most likely require us to cease conducting our business and would result in the delisting of our Class A Ordinary Shares from Nasdaq Capital Market and a significant impairment in the market value of our Class A Ordinary Shares.

We may have difficulty in enforcing any rights we may have under the VIE Agreements in PRC.

As all of our VIE Agreements with the VIEs are governed by the PRC laws and provide for the resolution of disputes through arbitration in the PRC, they would be interpreted in accordance with PRC law and any disputes would be resolved in accordance with PRC legal procedures. The legal environment in the PRC is not as developed as in the United States. As a result, uncertainties in the PRC legal system could further limit our ability to enforce these VIE Agreements. Furthermore, these VIE Agreements may not be enforceable in China if PRC government authorities or courts take a view that such VIE Agreements contravene PRC laws and regulations or are otherwise not enforceable for public policy reasons. In the event we are unable to enforce these VIE Agreements, we may not be able to exert effective control over the VIEs, and our ability to conduct our business may be materially and adversely affected.

The approval of the China Securities Regulatory Commission and other compliance procedures may be required in connection with any offering in the future, and, if required, we cannot predict whether we will be able to obtain such approval. As a result, both you and us face uncertainty about future actions by the PRC government that could significantly affect the operating company’s financial performance and the enforceability of the VIE Agreements.

The Provisions Regarding Mergers and Acquisitions of Domestic Projects by Foreign Investors (the “M&A Rules”) requires an overseas special purpose vehicle that are controlled by PRC companies or individuals formed for the purpose of seeking a public listing on an overseas stock exchange through acquisitions of PRC domestic companies using shares of such special purpose vehicle or held by its shareholders as considerations to obtain the approval of the China Securities Regulatory Commission, or the CSRC, prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. However, the application of the M&A Rules remains unclear. If CSRC approval is required, it is uncertain whether it would be possible for us to obtain the approval. Any failure to obtain or delay in obtaining CSRC approval would subject us to sanctions imposed by the CSRC and other PRC regulatory agencies.

Our PRC legal counsel has advised us based on their understanding of the current PRC laws, regulations and rules that the CSRC’s approval may not be required for the listing and trading of our Class A Ordinary Shares on the Nasdaq Capital Market, given that: (i) the CSRC currently has not issued any definitive rule or interpretation concerning whether offerings like ours are subject to this regulation, (ii) we establish our WFOE by means of direct investment and acquiring equity interest or assets of an entity other than “PRC domestic company” as defined under the M&A Rules, and (iii) no explicit provision in the M&A Rules clearly classifies VIE Agreements as a type of transaction subject to such Rules.

6

However, our PRC legal counsel has further advised us that there remains some uncertainty as to how the M&A Rules will be interpreted or implemented in the context of an overseas offering and its opinions summarized above are subject to any new laws, regulations and rules or detailed implementations and interpretations in any form relating to the M&A Rules. We cannot assure you that relevant PRC regulatory agencies, including the CSRC, would reach the same conclusion as our PRC legal counsel does. If it is determined that CSRC approval is required for our offerings, we may face sanctions by the CSRC or other PRC regulatory agencies for failure to obtain or delay in obtaining CSRC approval for our offerings. These sanctions may include fines and penalties on our operations in China, limitations on our operating privileges in China, delays in or restrictions on the repatriation of the proceeds from our offerings into the PRC, restrictions on or prohibition of the payments or remittance of dividends by our subsidiaries in China, or other actions that could have a material and adverse effect on our business, reputation, financial condition, results of operations, prospects, as well as the trading price of the Class A Ordinary Shares. The CSRC or other PRC regulatory agencies may also take actions requiring us, or making it advisable for us, to halt our offerings before the settlement and delivery of the Class A Ordinary Shares that we are offering. Consequently, if you engage in market trading or other activities in anticipation of and prior to the settlement and delivery of the Class A Ordinary Shares we are offering, you would be doing so at the risk that the settlement and delivery may not occur. In addition, if the CSRC or other regulatory agencies later promulgate new rules or explanations requiring that we obtain their approvals for our offerings, we may be unable to obtain a waiver of such approval requirements.

Recently, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Severe and Lawful Crackdown on Illegal Securities Activities, which was available to the public on July 6, 2021. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies.

Furthermore, on December 24, 2021, the CSRC and relevant departments of the State Council released the Administrative Provisions and the Filing Measures, both of which had a comment period that expired on January 23, 2022. The Draft Rules Regarding Overseas Listing aim to lay out the filing regulation arrangement for both direct and indirect overseas listing and clarify the determination criteria for indirect overseas listing in overseas markers. Where an enterprise whose principal business activities are conducted in the PRC seeks to issue and list its shares in the name of an overseas enterprise based on equity, assets, income, or other similar rights and interests of the relevant domestic enterprise in the PRC, such activities are deemed an indirect overseas issuance and listing. According to the Draft Rules Regarding Overseas Listings, among other things, after making initial applications with overseas stock markets for initial public offerings or listings, or after the completion of issuance of overseas listed securities by the overseas listed issuer, all China-based companies shall file the required filing materials with the CSRC within three working days. In addition, overseas offerings and listings may be prohibited for such China-based companies when any of the following applies: (i) if the intended securities offerings and listings are specifically prohibited by the PRC laws and regulations; (ii) if the intended securities offerings and listings may constitute a threat to, or endanger national security as reviewed and determined by competent authorities under the State Council in accordance with laws; (iii) if there are material ownership disputes over applicants’ equity interests, major assets, core technologies, or the others; (iv) if, in the past three years, applicants’ domestic enterprises, controlling shareholders, or de facto controllers have committed corruption, bribery, embezzlement, misappropriation of property, or other criminal offenses disruptive to the order of the socialist market economy, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (v) if, in the past three years, any directors, supervisors, or senior executives of applicants have been subject to administrative punishments for severe violations, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; or (vi) other circumstances as prescribed by the State Council. The Administrative Provisions further stipulate that a fine between RMB1 million (approximately $157,255) and RMB10 million (approximately $1,572,550) may be imposed if an applicant fails to fulfill the filing requirements with the CSRC or conducts an overseas offering or listing in violation of the Draft Rules Regarding Overseas Listings, and in cases of severe violations, a parallel order to suspend relevant businesses or halt operations for rectification may be issued, and relevant business permits or operational license revoked.

As of the date of this annual report, the Draft Rules Regarding Overseas Listings have been released for public comment only and have not been formally promulgated, and neither we, our subsidiaries, nor any of the PRC operating entities have been required to complete the filing procedures. However, uncertainties remain as to its enactment or future interpretations and implementations.

PRC laws and regulations governing our current business operations are sometimes vague and uncertain and any changes in such laws and regulations may impair our ability to operate profitable.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations including, but not limited to, the laws and regulations governing our business and the enforcement and performance of our arrangements with customers in certain circumstances. The laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness and interpretation of newly enacted laws or regulations, including amendments to existing laws and regulations, may be delayed, and our business may be affected if we rely on laws and regulations which are subsequently adopted or interpreted in a manner different from our understanding of these laws and regulations. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business.

On July 6, 2021, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly issued a document to crack down on illegal activities in the securities market and promote the high-quality development of the capital market, which, among other things, requires the relevant governmental authorities to strengthen cross-border oversight of law-enforcement and judicial cooperation, to enhance supervision over China-based companies listed overseas, and to establish and improve the system of extraterritorial application of the PRC securities laws. Since this document is relatively new, uncertainties still exist in relation to how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on companies like us.

7

Regulations relating to offshore investment activities by PRC residents may limit our ability to acquire PRC companies and could adversely affect our business.

In July 2014, State Administration of Foreign Exchange, or SAFE, promulgated the Circular on Issues Concerning Foreign Exchange Administration Over the Overseas Investment and Financing and Roundtrip Investment by Domestic Residents Via Special Purpose Vehicles, or Circular 37, which replaced Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Corporate Financing and Roundtrip Investment through Offshore Special Purpose Vehicles, or Circular 75. Circular 37 requires PRC residents to register with local branches of SAFE in connection with their direct establishment or indirect control of an offshore entity, referred to in Circular 37 as a “special purpose vehicle” for the purpose of holding domestic or offshore assets or interests. Circular 37 further requires amendment to a PRC resident’s registration in the event of any significant changes with respect to the special purpose vehicle, such as an increase or decrease in the capital contributed by PRC individuals, share transfer or exchange, merger, division or other material event. Under these regulations, PRC residents’ failure to comply with specified registration procedures may result in restrictions being imposed on the foreign exchange activities of the relevant PRC entity, including the payment of dividends and other distributions to its offshore parent, as well as restrictions on capital inflows from the offshore entity to the PRC entity, including restrictions on its ability to contribute additional capital to its PRC subsidiaries. Further, failure to comply with the SAFE registration requirements could result in penalties under PRC law for evasion of foreign exchange regulations.

Although we believe that our agreements relating to our structure are in compliance with current PRC regulations, we cannot assure you that the PRC government would agree that these VIE Agreements comply with PRC licensing, registration or other regulatory requirements, with existing policies or with requirements or policies that may be adopted in the future.

Uncertainties exist with respect to the interpretation and implementation of the Foreign Investment Law and how it may impact the viability of our current corporate structure, corporate governance and business operations.

On March 15, 2019, the National People’s Congress approved the Foreign Investment Law, which has come into effect on January 1, 2020 and replaced the trio of existing laws regulating foreign investment in China, namely, the Sino-foreign Equity Joint Venture Enterprise Law, the Sino-foreign Cooperative Joint Venture Enterprise Law and the Wholly Foreign-invested Enterprise Law, together with their implementation rules and ancillary regulations. The Foreign Investment Law embodies an expected PRC regulatory trend to rationalize its foreign investment regulatory regime in line with prevailing international practice and the legislative efforts to unify the corporate legal requirements for both foreign and domestic investments. However, since it is relatively new, uncertainties still exist in relation to its interpretation and implementation. For instance, under the Foreign Investment Law, “foreign investment’’ refers to the investment activities directly or indirectly conducted by foreign individuals, enterprises or other entities in China. Though it does not explicitly classify VIE Agreements as a form of foreign investment, there is no assurance that operation conducted by foreign investors or foreign-invested enterprises via contractual arrangement would not be interpreted as a type of indirect foreign investment activities under the definition in the future. In addition, the definition contains a catch-all provision which includes investments made by foreign investors through means stipulated in laws or administrative regulations or other methods prescribed by the State Council. Therefore, it still leaves leeway for future laws, administrative regulations or provisions promulgated by the Stale Council to provide for VIE Agreements as a form of foreign investment. In any of these cases, it will be uncertain whether our VIE Agreements will be deemed to be in violation of the market access requirements for foreign investment under the PRC laws and regulations. Furthermore, if future laws, administrative regulations or provisions prescribed by the State Council mandate further actions to be taken by companies with respect to existing VIE Agreements, we may face substantial uncertainties as to whether we can complete such actions in a timely manner, or at all. Failure to take timely and appropriate measures to cope with any of these or similar regulatory compliance challenges could materially and adversely affect our current corporate structure, corporate governance and business operations.

Risks Relating to the Planned Blockchain and Cryptocurrency Mining Business

Investment in our new line of business could present risks not originally contemplated.

The Company plans on investing in its planned expansion into the blockchain and cryptocurrency mining business. New ventures are inherently risky and may not be successful. In evaluating such endeavors, we are required to make difficult judgments regarding the value of business strategies, opportunities, technologies and other assets, and the risks and cost of potential liabilities. Furthermore, these investments involve certain other risks and uncertainties, including the risks involved with entering new competitive categories or regions, the difficulty in integrating the new business, and the challenges in achieving strategic objectives and other benefits expected from our investment.

8

If we are unable to successfully execute our planned blockchain and cryptocurrency mining business plan, it would affect our financial and business condition and results of operations.

Our previously announced growth strategy included the expansion of our operations to include a blockchain and cryptocurrency mining business. There are various risks related to these efforts, including the risk that these efforts may not provide the expected benefits in our anticipated time frame, if at all, and may prove costlier than expected; and the risk of adverse effects to our business, results of operations and liquidity if past and future undertakings, and the associated changes to our business, do not prove to be cost effective or do not result in the cost savings and other benefits at the levels that we anticipate. Our intentions and expectations with regard to the execution of our business plan, and the timing of any related initiatives, are subject to change at any time based on management’s subjective evaluation of our overall business needs. If we are unable to successfully execute our business plan, whether due to failure to realize the anticipated benefits from our business initiatives in the anticipated time frame or otherwise, we may be unable to achieve our financial targets.

Cryptocurrency mining relies on a steady and inexpensive power supply for operating mining farms and running mining hardware. Failure to access a large quantity of power at reasonable costs could significantly increase our operating expenses and adversely affect our demand for our mining machines.

Cryptocurrency mining consumes a significant amount of energy power to process the computations and cool down the mining hardware. Therefore, a steady and inexpensive power supply is critical to cryptocurrency mining. There can be no assurance that the operations of our planned cryptocurrency mining business will not be affected by power shortages or an increase in energy prices in the future. In addition, as we intend to establish and operate mining machines and engage in key mainstream cryptocurrencies mining activities, such as Bitcoin, in the near future, any increase in energy prices or a shortage in power supply in the area of our mining machines may be located will increase our potential mining costs and reduce the expected economic returns from our mining operation significantly.

In particular, the power supply could be disrupted by natural disasters, such as floods, mudslides and earthquakes, or other similar events beyond our control. Further, we may experience power shortages due to seasonal variations in the supply of certain types of power such as hydroelectricity. Power shortages, power outages or increased power prices could adversely affect our mining businesses. Under such circumstances, our business, results of operations and financial condition could be materially and adversely affected.

Shortages in, or rises in the prices of mining machines may adversely affect our business

Given the long production period to manufacture and assemble mining machines, there is no assurance that we can acquire enough mining machines for our planned cryptocurrency mining. We may rely on third parties to supply mining machines to us, and shortages of mining machines or any delay in delivery of our orders could seriously interrupt our operations. The scale of our cryptocurrency mining capacity depends on obtaining adequate mining machines on a timely basis and at competitive prices. Shortages of mining machines could result in reduced mining capacity, as well as an increase in operation costs, which could materially delay the completion of our mining capacity and commencement of our mining. As a result, our business, results of operations and reputation could be materially and adversely affected.

We may not be able to develop our cryptocurrency mining capacity because we may fail to anticipate or adapt to technology innovations in a timely manner, or at all.

The cryptocurrencies mining industry is experiencing rapid technological changes. Failure to anticipate technology innovations or adapt to such innovations in a timely manner, or at all, may result in our research becoming obsolete at sudden and unpredictable intervals and, accordingly, we may not successfully develop our mining capacity at all. To establish our cryptocurrency mining capacity, we will invest heavily in technology research and development. The process of research and developing new technologies in cryptocurrency is inherently complex and involves significant uncertainties. There are a number of risks, including the following:

| ● | our research and development efforts may fail in resulting in the development or commercialization of new technologies or ideas in blockchain or cryptocurrency; |

| ● | our research and development efforts may fail to translate new product plans into commercially feasible products; |

| ● | our new technologies or new products may not be well received by the markets; |

9

| ● | we may not have adequate funding and resources necessary for continual investments in research and development; |

| ● | even assuming our technologies and products become marketable or profitable, they may become obsolete due to rapid advancements in technology and changes in the mainstream markets; and |

| ● | our newly developed technologies may not be protected as proprietary intellectual property rights. |

Our research and development efforts may not yield the expected results, or may prove to be futile due to the lack of market demand. Further, any failure to anticipate the next-generation technology roadmap or changes in the mainstream markets or to timely develop new or enhanced technologies in response could result in loss of our business.

It is now illegal to engage in digital asset transactions including bitcoin mining operations in the PRC, the ruling of which may adversely affect us.

The PRC has now taken harsh regulatory action to ban cryptocurrency mining operations and to severely restrict the right to acquire, own, hold, sell or use these bitcoin assets or to exchange them for fiat currency. Such restrictions may adversely affect us as the large-scale use of cryptocurrencies as a means of exchange is presently confined to certain regions globally. Ongoing and future regulatory actions may impact our ability to continue to operate, and such actions could affect our ability to continue as a going concern or to pursue our business strategy at all, which could have a material adverse effect on our business, prospects or operations.

On May 21, 2021, the Financial Stability and Development of the State Council in China proposed to “crack down on bitcoin mining and trading.” After that, the related local governments began to issue corresponding measures in succession to respond to the central government, including Xinjiang Changji Hui Autonomous Prefecture Development and Reform Commission issuing a notice on the immediate shutdown of enterprises engaged in cryptocurrency mining on June 9, 2021, and Sichuan Provincial Development and Reform Commission and Sichuan Energy Bureau issuing a notice on the shutdown of cryptocurrency mining projects. On September 3, 2021, the Notification on Rectification of the Virtual Currency “Mining” Activities (or the Notification Fa Gai Yun Xing [2021] No. 1283) was issued. On September 24, 2021, the newly issued Notification of Overhauling the Mining Activity of Cryptocurrency (or the Notification No. 1283) banned all new cryptocurrency operations in China.

In consideration of the PRC government’s attitude and our business plan, we will not conduct any cryptocurrency mining operations or cryptocurrency trading operations in the PRC.

We may face intense industry competition.

Cryptocurrency mining, security, and insurance is in a highly competitive environment. Our competitors include companies that may have a longer history, larger market share, greater brand recognition, greater financial resources in research or other competitive advantages. We anticipate that competition will increase as cryptocurrencies gain greater acceptance and more players join the market of cryptocurrency mining and mining farm operations.

Strong competition in the market may require us to increase our marketing expenses and sales expenses, if any, or otherwise invest greater resources to gain market shares and expand our mining capacities as needed to adequately compete. Such efforts may negatively impact our profitability. If we are unable to effectively meet our business plans in the competitive landscape, our business, financial conditions and results of operations may be adversely affected.

Because cryptocurrencies may be determined to be investment securities, we may inadvertently violate the Investment Company Act and incur large losses as a result and potentially be required to register as an investment company or terminate operations and we may incur third party liabilities.

In recent years, the SEC has ruled that the two most valuable cryptocurrencies—Bitcoin and Ethereum—are not securities. We therefore believe that we will not be deemed to be engaged in the business of investing, reinvesting, or trading in securities, and we shall not hold ourselves out as being engaged in those activities. However, under the Investment Company Act a company may be deemed an investment company under section 3(a)(1)(C) thereof if the value of its investment securities is more than 40% of its total assets (exclusive of government securities and cash items) on an unconsolidated basis.

10

As a result of our planned investments and our mining activities, including investments in which we do not have a controlling interest, the investment securities we hold could exceed 40% of our total assets, exclusive of cash items and, accordingly, we could determine that we have become an inadvertent investment company. The bitcoins we own, acquire or mine may be deemed an investment security by the SEC, although we do not believe any of the cryptocurrencies we own, acquire or mine are securities. An inadvertent investment company can avoid being classified as an investment company if it can rely on one of the exclusions under the Investment Company Act. One such exclusion, Rule 3a-2 under the Investment Company Act, allows an inadvertent investment company a grace period of one year from the earlier of (a) the date on which an issuer owns securities and/or cash having a value exceeding 50% of the issuer’s total assets on either a consolidated or unconsolidated basis and (b) the date on which an issuer owns or proposes to acquire investment securities having a value exceeding 40% of the value of such issuer’s total assets (exclusive of government securities and cash items) on an unconsolidated basis. We may take actions to cause the investment securities held by us to be less than 40% of our total assets, which may include acquiring assets with our cash and bitcoin on hand or liquidating our investment securities or bitcoin or seeking a no-action letter from the SEC if we are unable to acquire sufficient assets or liquidate sufficient investment securities in a timely manner.

As the Rule 3a-2 exception is available to a company no more than once every three years, and assuming no other exclusion were available to us, we would have to keep within the 40% limit for at least three years after we cease being an inadvertent investment company. This may limit our ability to make certain investments or enter into joint ventures that could otherwise have a positive impact on our earnings. In any event, we do not intend to become an investment company engaged in the business of investing and trading securities.

Classification as an investment company under the Investment Company Act requires registration with the SEC. If an investment company fails to register, it would have to stop doing almost all business, and its contracts would become voidable. Registration is time consuming and restrictive and would require a restructuring of our operations, and we would be very constrained in the kind of business we could do as a registered investment company. Further, we would become subject to substantial regulation concerning management, operations, transactions with affiliated persons and portfolio composition, and would need to file reports under the Investment Company Act regime. The cost of such compliance would result in the Company incurring substantial additional expenses, and the failure to register if required would have a materially adverse impact to conduct our operations.

Risks Relating to our Tea and Light Foods Business

We may not be able to successfully implement our growth strategy on a timely basis or at all, which could harm our results of operations.

Our continued growth depends, in large part, on our ability to open new stores and to operate those stores successfully.

Our ability to successfully open and operate new stores depends on many factors, including:

| ● | Our ability to increase brand awareness in the PRC and the U.S. and to increase tea consumption in areas where we open stores; |

| ● | the identification and availability of suitable sites for store locations, the availability of which is beyond our control; |

| ● | the negotiation of acceptable lease terms; |

| ● | the maintenance of adequate distribution capacity, information systems and other operational system capabilities; |

| ● | integrating new managed and JV stores into our existing stores; |

| ● | buying, distribution and other support operations; |

| ● | the hiring, training and retention of store management and other qualified personnel; |

| ● | assimilating new store employees into our corporate culture; |

11

| ● | the effective sourcing and management of inventory to meet the needs of our stores on a timely basis; |

| ● | the availability of sufficient levels of cash flow and financing to support our expansion; and |

| ● | the short-term and long-term effects of COVID-19 on the food services industry in both the PRC and the U.S. |

Unavailability of attractive store locations, delays in the acquisition or opening of new stores, delays or costs resulting from a decrease in commercial development due to capital constraints, difficulties in staffing and operating new store locations or lack of customer acceptance of stores in new market areas may negatively impact our new store growth and the costs or the profitability associated with new stores.

Additionally, some of our new stores may be located in areas where we have little experience or a lack of brand recognition. Those markets may have different competitive conditions, market conditions, consumer tastes and discretionary spending patterns than our existing markets, which may cause these new stores to be less successful than stores in our existing markets. Other new stores may be located in areas where we have existing stores. Although we have experience in these markets, increasing the number of locations in these markets may result in inadvertent over-saturation of markets and temporarily or permanently divert customers and sales from our existing stores, thereby adversely affecting our overall financial performance.

Accordingly, we cannot assure you that we will achieve our planned growth or, even if we are able to grow our store base as planned, that any new stores will perform as planned. If we fail to successfully implement our growth strategy, we will not be able to sustain the rapid growth in sales and profits that we expect, which would likely have an adverse impact on the price of our Class A ordinary shares.

Our business largely depends on a strong brand image, and if we are unable to maintain and enhance our brand image, particularly in new markets where we have limited brand recognition, we may be unable to increase or maintain our level of sales.

We believe that our brand image and brand awareness has contributed significantly to the success of our business. We also believe that maintaining and enhancing our brand image, particularly in new markets where we have limited brand recognition, is important to maintaining and expanding our customer base. Our ability to successfully integrate new stores into their surrounding communities, to expand into new markets or to maintain the strength and distinctiveness of our brand in our existing markets will be adversely impacted if we fail to connect with our target customers. Maintaining and enhancing our brand image may require us to make substantial investments in areas such as merchandising, marketing, store operations, community relations, store graphics and employee training, which could adversely affect our cash flow and which may ultimately be unsuccessful. Furthermore, our brand image could be jeopardized if we fail to maintain high standards for merchandise quality, if we fail to comply with local laws and regulations or if we experience negative publicity or other negative events that affect our image and reputation. Some of these risks may be beyond our ability to control, such as the effects of negative publicity regarding our suppliers. Failure to successfully market and maintain our brand image in new and existing markets could harm our business, results of operations and financial condition.

Our limited operating experience and limited brand recognition in other regions may limit our expansion strategy and cause our business and growth to suffer.

Our future growth depends, to a considerable extent, on our expansion efforts outside of Hunan province and New York City into other regions of the PRC and the U.S. Our current operations are based largely in the Hunan province and New York City. We have a limited number of customers and limited experience in operating outside of Hunan and New York City. We also have limited experience with market practices outside of Hunan and New York City and cannot guarantee that we will be able to penetrate or successfully operate in any market outside of Hunan and New York City. We may also encounter difficulty expanding in other regions’ markets because of limited brand recognition. In particular, we have no assurance that our marketing efforts will prove successful outside of the narrow geographic regions in which they have been used. In addition, because tea consumption is greater in Hunan than some other regions of the PRC on a per capita basis, we may encounter challenges in those regions in establishing consumer awareness and loyalty or interest in our products and our brand to a different degree than in Hunan. The expansion into other regions may also present competitive, merchandising, forecasting and distribution challenges that are different from or more severe than those we currently face. Failure to develop new markets outside of Hunan and New York City or disappointing growth outside of Hunan and New York City may harm our business and results of operations.

12

We face significant competition from other specialty tea and beverage retailers and retailers of grocery products, which could adversely affect us and our growth plans.

The Chinese tea market is highly fragmented. We compete directly with a large number of relatively small independently owned tea retailers and a number of regional and national tea retailers, as well as retailers of grocery products, including loose-leaf tea and tea bags and other beverages. We compete with these retailers on the basis of taste, quality and price of product offered, atmosphere, location, customer service and overall customer experience. We must spend considerable resources to differentiate our customer experience. Some of our competitors may have greater financial, marketing and operating resources than we do. Therefore, despite our efforts, our competitors may be more successful than us in attracting customers. In addition, as we continue to drive growth in our category in Hunan, our success, combined with relatively low barriers to entry, may encourage new competitors to enter the market. As we continue to expand geographically, we expect to encounter additional regional and local competitors.

We plan to use primarily cash from our prior offering as well as our operations to finance our growth strategy, and if we are unable to maintain sufficient levels of cash flow we may not meet our growth expectations.

We intend to finance our growth through the cash flows generated by our existing stores and the net proceeds from our previous and future financings. Our primary source of financing for our growth will be cash from our prior offering as well as our operations. However, if our stores are not profitable or if our store profits decline, we may not have the cash flow necessary in order to pursue or maintain our growth strategy. We may also be unable to obtain any necessary financing on commercially reasonable terms to pursue or maintain our growth strategy. If we are unable to pursue or maintain our growth strategy, the market price of our Class A ordinary shares could decline and our results of operations and profitability could suffer.

The planned addition of a significant number of new stores each year will require us to continue to expand and improve our operations and could strain our operational, managerial and administrative resources, which may adversely affect our business.

Our growth strategy calls for the opening of a significant number of new stores each year and our continued expansion will place increased demands on our operational, managerial, administrative and other resources, which may be inadequate to support our expansion. Our senior management team may be unable to effectively address challenges involved with expansion forecasts for years ended on June 30, 2023 and 2024. Managing our growth effectively will require us to continue to enhance our store management systems, financial and management controls and information systems and to hire, train and retain regional directors, district managers, store managers and other personnel. Implementing new systems, controls and procedures and these additions to our infrastructure and any changes to our existing operational, managerial, administrative and other resources could negatively impact our results of operations and financial condition.

Any decrease in customer traffic in the shopping malls or other locations in which our stores are located could cause our sales to be less than expected.

Our stores are located in shopping malls, other shopping centers and street locations. Sales at these stores are derived, to a significant degree, from the volume of customer traffic in those locations and in the surrounding area. Our stores benefit from the current popularity of shopping malls and centers as shopping destinations and their ability to generate customer traffic in the vicinity of our stores. Our sales volume and customer traffic may be adversely affected by, among other things:

| ● | economic downturns in the PRC or regionally; |

| ● | high fuel prices; |

| ● | changes in consumer demographics; |

| ● | a decrease in popularity of shopping malls or centers in which a significant number of our stores are located; |

| ● | the closing of a shopping mall’s or center’s “anchor” store or the stores of other key tenants; |

| ● | a deterioration in the financial condition of shopping mall and center operators or developers which could, for example, limit their ability to maintain and improve their facilities; or |

| ● | the effects of COVID-19. |

13

A reduction in customer traffic as a result of these or any other factors could have a material adverse effect on us.

In addition, severe weather conditions and other catastrophic occurrences in areas in which we have stores may have a material adverse effect on our results of operations. Such conditions may result in physical damage to our stores, loss of inventory, decreases in customer traffic and closure of one or more of our stores. Any of these factors may disrupt our business and have a material adverse effect on our financial condition and results of operations.

If we are unable to attract, train, assimilate and retain employees that embody our culture, including store personnel, store and district managers and regional directors, we may not be able to grow or successfully operate our business.

Our success depends in part upon our ability to attract, train, assimilate and retain a sufficient number of employees, including store managers, district managers and regional directors, who understand and appreciate our culture, are able to represent our brand effectively and establish credibility with our customers. If we are unable to hire and retain store personnel capable of consistently providing a high level of customer service, as demonstrated by their enthusiasm for our culture, understanding of our customers and knowledge of tea beverages, light meals, baked goods, tea accessories and other tea-related merchandise we offer, our ability to open new stores may be impaired, the performance of our existing and new stores could be materially adversely affected and our brand image may be negatively impacted. In addition, the rate of employee turnover in the retail industry is typically high and finding qualified candidates to fill positions may be difficult. Our planned growth will require us to attract, train and assimilate even more personnel. Any failure to meet our staffing needs or any material increases in team member turnover rates could have a material adverse effect on our business or results of operations. We also rely on temporary or seasonal personnel to staff our stores and distribution centers, especially during Chinese New Year. We cannot guarantee that we will be able to find adequate temporary or seasonal personnel to staff our operations when needed, which may strain our existing personnel and negatively impact our operations.

Because our tea and light meals business is highly concentrated on a single, discretionary product category, which includes tea beverages, light meals, baked goods, tea accessories and other tea-related merchandise, we are vulnerable to changes in consumer preferences and in economic conditions affecting disposable income that could harm our financial results.