CU Bancorp Investor Presentation as of June 30, 2014 Exhibit 99.1 … a better banking experience |

2 Forward-Looking Statements This press release contains certain forward-looking information about CU Bancorp (the “Company”), 1 st Enterprise Bank and the combined company after the close of the transaction that is intended to be covered by the safe harbor for “forward looking statements” provided by the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact are forward-looking statements. Such statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the Company. Forward-looking statements speak only as of the date they are made and we assume no duty to update such statements. We caution readers that a number of important factors could cause actual results to differ materially from those expressed in, implied or projected by, such forward-looking statements. Risks and uncertainties include, but are not limited to: lower than expected revenues; credit quality deterioration or a reduction in real estate values could cause an increase in the allowance for credit losses and a reduction in net earnings; increased competitive pressure among depository institutions; the Company’s ability to complete future acquisitions, successfully integrate such acquired entities, or achieve expected beneficial synergies and/or operating efficiencies within expected time-frames or at all; the possibility that personnel changes will not proceed as planned; the cost of additional capital is more than expected; a change in the interest rate environment reduces net interest margins; asset/liability repricing risks and liquidity risks; legal matters could be filed against the Company and could take longer or cost more than expected to resolve or may be resolved adversely to the Company; general economic conditions, either nationally or in the market areas in which the Company does or anticipates doing business, are less favorable than expected; environmental conditions, including natural disasters and drought, may disrupt our business, impede our operations, negatively impact the values of collateral securing the Company’s loans and leases or impair the ability of our borrowers to support their debt obligations; the economic and regulatory effects of the continuing war on terrorism and other events of war, including the conflicts in the Middle East; legislative or regulatory requirements or changes adversely affecting the Company’s business; changes in the securities markets; regulatory approvals for any capital activities cannot be obtained on the terms expected or on the anticipated schedule; and, other risks that are described in CU Bancorp’s public filings with the U.S. Securities and Exchange Commission (the “SEC”). Additional risks and uncertainties relating to the proposed transaction with 1st Enterprise Bank include, but are not limited to: the ability to complete the proposed transaction, including obtaining regulatory approvals and approvals by the shareholders of CU Bancorp and 1st Enterprise Bank; the length of time necessary to consummate the proposed transaction; the ability to successfully integrate the two institutions and achieve expected synergies and operating efficiencies on the expected timeframe; unexpected costs relating to the proposed transaction; and the potential impact on the institutions’ respective businesses as a result of uncertainty surrounding the proposed transaction. If any of these risks or uncertainties materializes or if any of the assumptions underlying such forward-looking statements proves to be incorrect, CU Bancorp’s results could differ materially from those expressed in, implied or projected by such forward-looking statements. CU Bancorp assumes no obligation to update such forward-looking statements. For a more complete discussion of risks and uncertainties, investors and security holders are urged to read CU Bancorp’s annual report on Form 10-K, quarterly reports on Form 10-Q and other reports filed by CU Bancorp with the SEC. The documents filed by CU Bancorp with the SEC may be obtained at CU Bancorp’s website at www.cubancorp.com or at the SEC’s website at www.sec.gov. These documents may also be obtained free of charge from CU Bancorp by directing a request to: CU Bancorp c/o California United Bank, 15821 Ventura Boulevard, Suite 100, Encino, CA 91436. Attention: Investor Relations. Telephone 818-257-7700. CU BANCORP, CALIFORNIA UNITED BANK AND 1 ST ENTERPRISE BANK MERGER ANNOUNCEMENT On June 3, 2014, CU Bancorp announced that it had entered into an Agreement and Plan of Merger (the “Merger Agreement”) among CU Bancorp, California United and 1st Enterprise Bank, a California state-chartered commercial bank (“1st Enterprise”) pursuant to which CU Bancorp will acquire 1st Enterprise Bank by merging 1st Enterprise Bank with and into California United Bank (the “Merger”). California United Bank will survive the Merger and will continue the commercial banking operations of the combined bank following the Merger. Under the terms of the Merger Agreement, holders of 1st Enterprise Bank common stock will receive shares of CU Bancorp common stock based upon a fixed exchange ratio of 1.3450 shares of CU Bancorp common stock for each share of 1st Enterprise Bank common stock. The U.S. Treasury, as the holder of all outstanding shares of 1st Enterprise Bank preferred stock granted in connection with 1st Enterprise’s participation in the Treasury’s Small Business Lending Fund program, will receive, in exchange for these shares, a new series of CU Bancorp preferred stock having the same rights (including with respect to dividends), preferences, privileges, voting powers, limitations and restrictions as the 1st Enterprise preferred stock. The Merger is subject to customary closing conditions, including regulatory and shareholder approvals. ADDITIONAL INFORMATION ABOUT THE PROPOSED TRANSACTION WITH 1 ST ENTERPRISE BANK AND WHERE TO FIND IT Investors and security holders are urged to carefully review and consider each of CU Bancorp’s public filings with the SEC, including but not limited to its annual reports on Form 10-K, proxy statements, current reports on Form 8-K and quarterly reports on Form 10-Q. The documents filed by CU Bancorp with the SEC may be obtained free of charge at CU Bancorp’s website at www.cubancorp.com or at the SEC website at www.sec.gov. These documents may also be obtained free of charge from CU Bancorp by directing a request to: CU Bancorp c/o California United Bank, 15821 Ventura Boulevard, Suite 100, Encino, CA 91436. Attention: Investor Relations. Telephone 818-257- 7700. The information on CU Bancorp’s website is not, and shall not be deemed to be, a part of this filing or incorporated into other filings CU Bancorp makes with the SEC. In connection with the proposed merger of California United Bank with 1 st Enterprise Bank, CU Bancorp intends to file a registration statement on Form S-4 with the SEC to register the shares of CU Bancorp common stock to be issued to shareholders of 1 st Enterprise Bank. The registration statement will include a joint proxy statement of CU Bancorp and 1 st Enterprise and a prospectus of CU Bancorp, and each party will file other documents regarding the proposed transaction with the SEC. Before making any voting or investment decision, investors and security holders of CU Bancorp and 1 st Enterprise Bank are urged to carefully read the entire registration statement and joint proxy statement/prospectus, when they become available, as well as any amendments or supplements to these documents, because they will contain important information about the proposed transaction. A definitive joint proxy statement/prospectus will be sent to the shareholders of each institution seeking any required stockholder approvals. Investors and security holders will be able to obtain the registration statement and the joint proxy statement/prospectus free of charge from the SEC’s website or from CU Bancorp by writing to the address provided in the paragraph above. PARTICIPANTS IN THE SOLICITATION CU Bancorp and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of CU Bancorp and 1 st Enterprise Bank in connection with the transaction. Information about the directors and executive officers of CU Bancorp is set forth in its annual report on Form 10-K/A filed with the SEC on April 29, 2014. 1st Enterprise Bank and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of CU Bancorp and 1st Enterprise Bank in connection with the Merger. Additional information regarding the interests of these participants and other persons who may be deemed participants in the Merger may be obtained by reading the proxy statement/prospectus regarding the Merger when it becomes available. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. |

3 Investment Highlights ……….……………….……… 4 Earnings Review ...……………………..……………… 14 Appendix ………………………..…………………… 24 CUNB & FENB Merger Overview. ...……………………31 |

4 Investment Highlights Premier community-based business banking franchise serving large and diverse market Strong organic loan growth Attractive low-cost core deposit base Exceptional credit quality Growing visibility in the investment community Announced merger with 1 Enterprise Bank to create $2.2 billion “pure play” business bank in attractive Southern California market st |

5 Premier Business Banking Franchise $1.4 billion in assets, achieved by experienced management team* in nine years, through organic growth and two successful acquisitions 16 th largest publicly-owned bank by assets in combined Los Angeles, Orange and Ventura counties 279 th largest publicly-owned bank by assets in U.S. Asset CAGR of 39% since inception in 2005 through 12/31/13 Footprint includes eight branches covering L.A., Orange and Ventura counties *See appendix for management experience |

6 Sophisticated Relationship Management Team offers Solutions for Small- and Medium-Sized Businesses Sophisticated relationship management team offers personalized and responsive service focused on small- and medium-sized businesses in Los Angeles, Orange and Ventura counties Los Angeles County is the largest manufacturing center in the U.S. and would be 9 th largest state in U.S. L.A. County expected to add more than 150,000 jobs over the next two years; June 2014 unemployment rate of 8.2% projected to fall to 7.2% by end of 2015* Orange County would be 31 st largest state in U.S. Orange County unemployment rate is 5.2% as of June 2014** Three-county area is home to more than 532,000 small- and middle-market business** (defined as employing 1 to 499 workers) *Source: Forecast by Beacon Economics, February 2014; actual unemployment rate from Bureau of Labor and Statistics (BLS) **Source: County data from Los Angeles Economic Development Corporation and California EDD, as of 2012; actual unemployment rate from BLS |

7 Franchise Growth Strategies Organic Growth Offer expertise in C&I and commercial real estate lending to small and middle- market businesses Provide customers with sophisticated products and solutions Leverage relationship-based banking approach and superior service SBA lending platform expertise acquired with Premier Commercial Bank Continue recruiting “in market” talent from competitors Growth by Merger/Acquisition Strong management team experienced with successful, accretive acquisitions California Oaks State Bank (12/31/10) Premier Commercial Bank (7/31/12) 1 Enterprise Bank (Announced 6/3/14, expected to close in fourth quarter 2014) st |

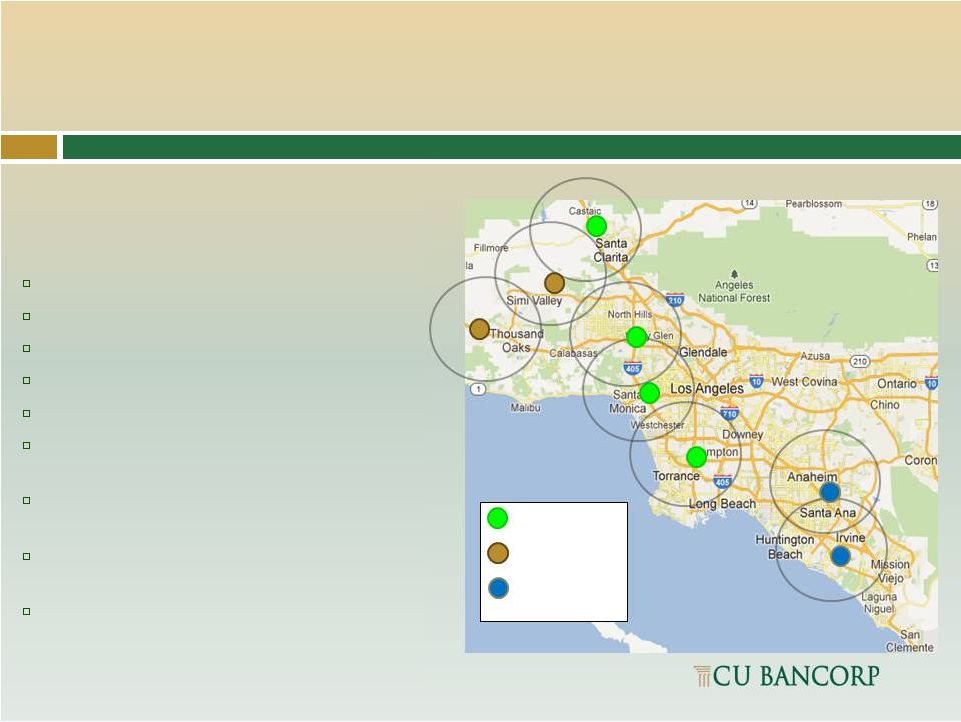

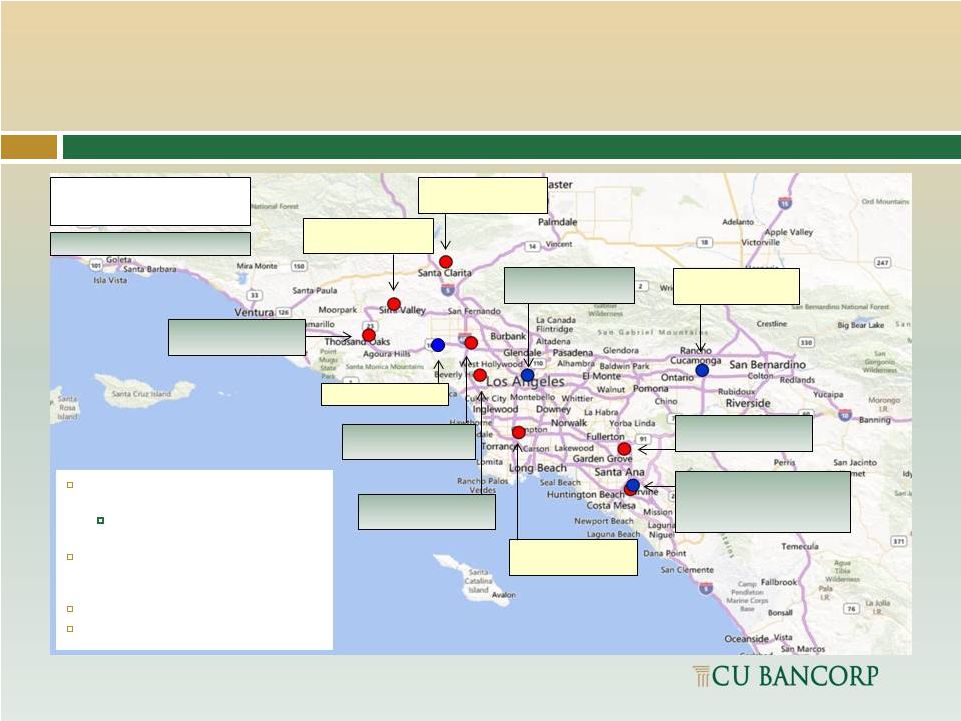

Strategic Geographic Locations Encino (2005) – Headquarters Los Angeles (2006) Santa Clarita Valley (2007) South Bay (2009) – Converted to a branch in 2010 Orange County (2010) – Loan Production Office* Simi Valley (2010) – Acquired from California Oaks State Bank Thousand Oaks (2010) – Acquired from California Oaks State Bank Anaheim (2012) – Acquired from Premier Commercial Bank Irvine/Newport Beach (2012) – Acquired from Premier Commercial Bank* CUB Branch Former COSB Branch Former PCB Branch *Combined location (August 2013) Encino 8 California United Bank has a footprint that spans the most attractive markets in Southern California: |

Announced Merger Has Attractive Footprint and Large Branch Size CUNB (8 branches) FENB (3 branches; 1 LPO) Inland Empire: FENB: $81 million Downtown LA: FENB: $331 million Irvine/Newport Beach: CUNB: $148 million FENB: $240 million Pro Forma: $388 million Santa Clarita Valley: CUNB: $94 million Simi Valley: CUNB: $14 million West LA: CUNB: $256 million San Fernando Valley: CUNB: $207 million Anaheim: CUNB: $191 million $100 Million+ Branches Woodland Hills LPO South Bay: CUNB: $55 million Conejo Valley: CUNB: $229 million Source: CUNB and FENB; branch deposits data as of March 31, 2014 9 6 of 10 pro forma branches with deposits greater than $100 million Branch consolidation in Irvine Woodland Hills LPO to be consolidated into a CUNB branch Expands CUNB’s branch presence to Downtown LA (pro forma headquarters) and Inland Empire Pro forma average branch size of approx. $185 million in deposits |

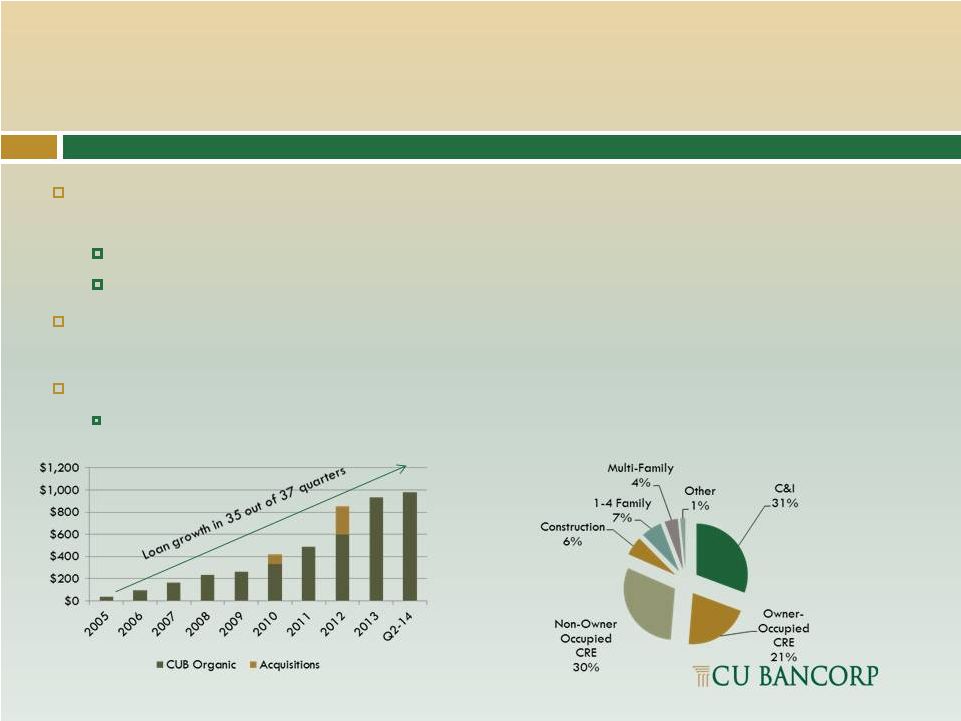

Strong Organic Loan Growth CUB lenders’ expertise allows the Bank to underwrite complex loans, while providing better service than larger banks Total loans grew 10.7% to $980 million from 2Q13 to 2Q14 Total loans grew 3.6% from 1Q14 to 2Q14, a 14.4% annualized rate 52% of total loans are commercial and industrial loans, and owner-occupied nonresidential properties—relationship-based “sticky” accounts Since inception in 2005 loan portfolio has grown to $980 million $778 million in net organic loan growth, in addition to two acquisitions Annual Loan Growth ($ in millions) Portfolio Composition 10 |

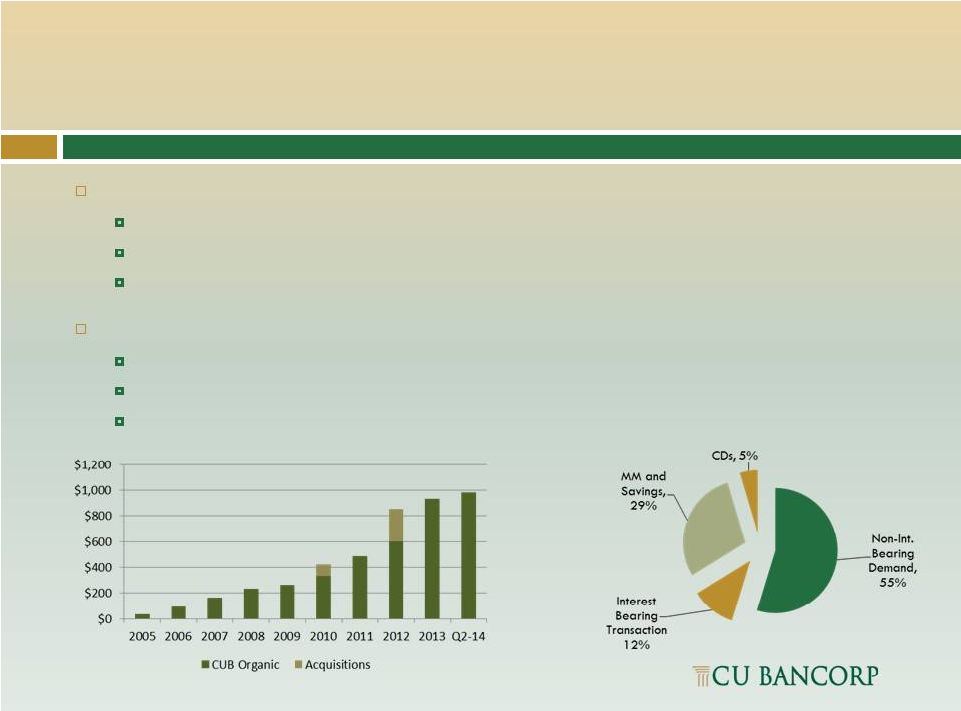

Attractive Low Cost Deposit Base Total deposits of $1.2 billion Increased $148 million or 13.4% from 2Q13 to 2Q14 Increased $42 million or 3.5% from 1Q14 to 2Q14 Cost of deposits was 0.11% in 2Q14 Non-interest bearing deposits of $682 million 55% of total deposits Up 19.5% from 2Q13 to 2Q14 Up 4.7% from 1Q14 to 2Q14, an 18.8% annualized rate Deposit Composition Total Deposit Growth Since Inception 11 |

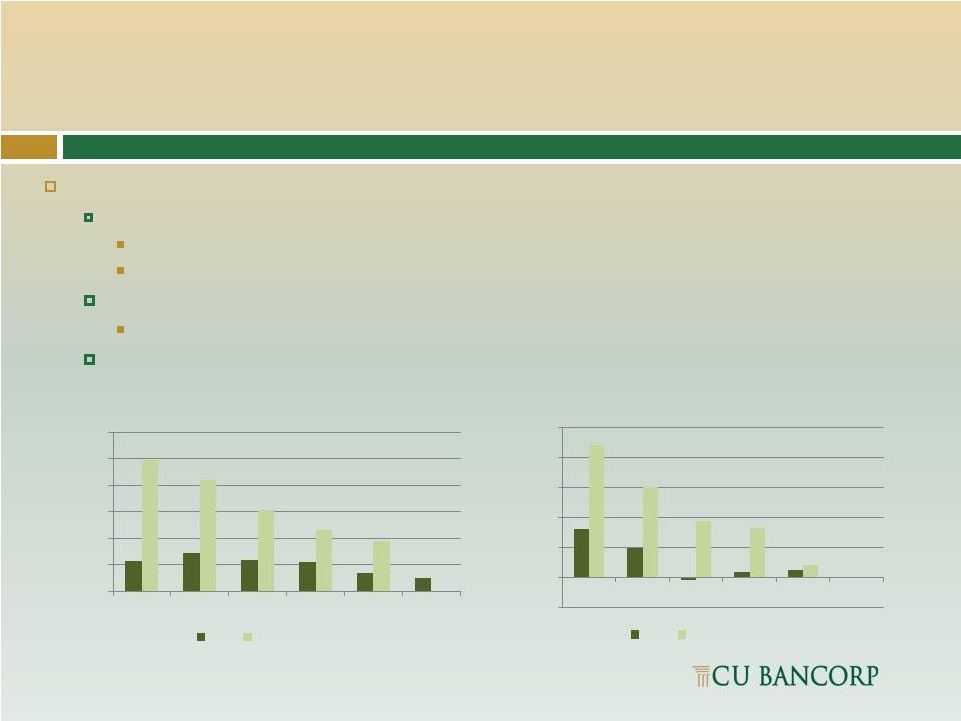

12 Strong Credit Quality Trend Continues CUB credit quality at June 30, 2014: Total nonaccrual loans of $7.0 million or 0.72% of total loans 71% of nonaccrual loans were acquired loans marked-to-market at the time of acquisition Excluding acquired loans, total nonaccrual loans were $2.0 million or 0.29% of total loans NPAs to total assets of 0.51% One REO in 2Q14 of $219 thousand, sold early in 3Q14 for approximate book value Net recoveries in 2Q14 of $53 thousand; net recoveries year to date of $198 thousand Peer group includes California banks or bank holding companies with total assets between $1.0-2.0 billion; source: SNL. NPAs to total assets Net charge-offs 1.12% 1.42% 1.19% 1.09% 0.68% 0.51% 4.94% 4.19% 3.06% 2.31% 1.89% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 2009 2010 2011 2012 2013 2Q-14 CUB Peer Group Avg. 0.80% 0.49% -0.04% 0.08% 0.12% -0.02% 2.20% 1.50% 0.94% 0.82% 0.21% 0.50% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 2009 2010 2011 2012 2013 CUB Peer Group Avg. 12 2Q-14 |

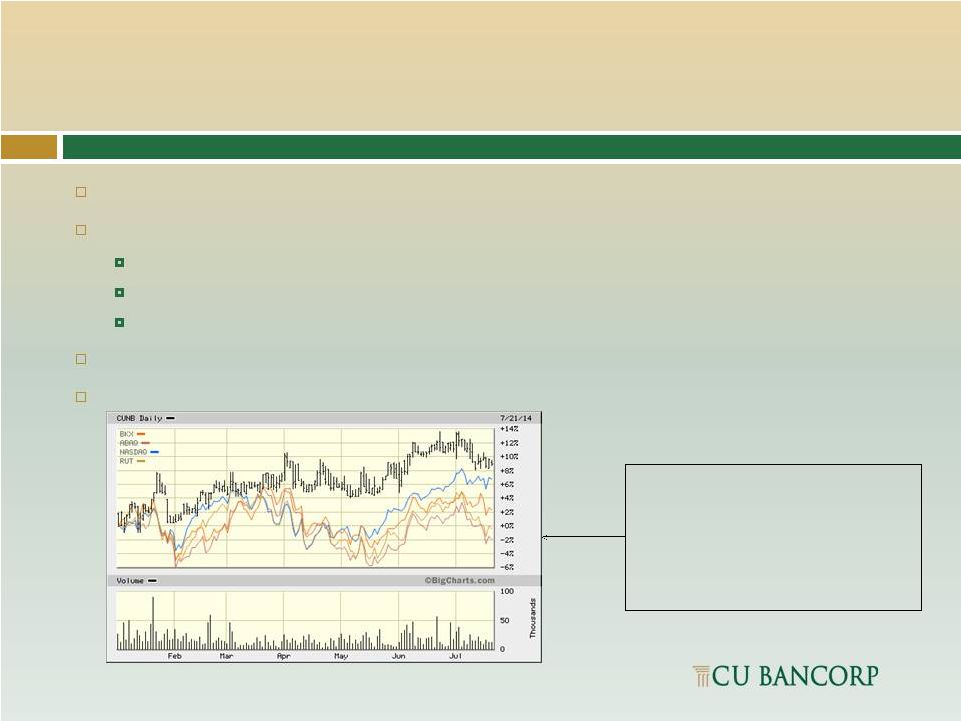

Growing Visibility in the Investment Community Surpassed $1 billion in assets in July 2012 Transferred listing to Nasdaq Capital Market in October 2012 (CUNB) 36.2% institutional ownership per 1Q14 13-f filings 11.2 million shares outstanding at 6/30/14 $211 million market cap at 7/21/14 Added to Russell Indexes in June 2013 Analyst coverage by five Wall Street brokerage firms Year to date performance vs. KBW Bank Index (BKX), Nasdaq Composite Index (NASDAQ), ABA Nasdaq Bank Index (ABAQ) and Russell 2000 Index (RUT) CUNB has had a strong performance in a challenging year. Year to date, it’s up 7.0%, compared to the NASDAQ, up 5.9%, the BKX bank index, up 1.8% and the Russell 2000 and the ABA NASDAQ Bank Index, which are down (1.5)% and (3.2)%, respectively, as of 7/21/14. 13 |

14 Earnings Review Second Quarter 2014 |

15 Second Quarter 2014 Highlights Net income of $2.4 million, 2.8% increase from $2.3 million in 2Q13 EPS of $0.21, compared to $0.22 in 2Q13 Core net income of $2.9 million, 24% increase from $2.3 million in 2Q13 Core EPS of $0.26, 18.2% increase from $0.22 in 2Q13 Total loans increased $95 million or 10.7% from 2Q13 $151 million in net organic loan growth Offset by $56 million in loan run-off from acquired portfolios Total deposits increased $148 million, or 13.4%, from 2Q13 Non-interest bearing deposits increased $111 million, or 19.5%, from 2Q13 Continued strong credit quality NPAs to total assets of 0.51%, down from 1.06% in 2Q13 Net recoveries of $53 thousand in 2Q14 |

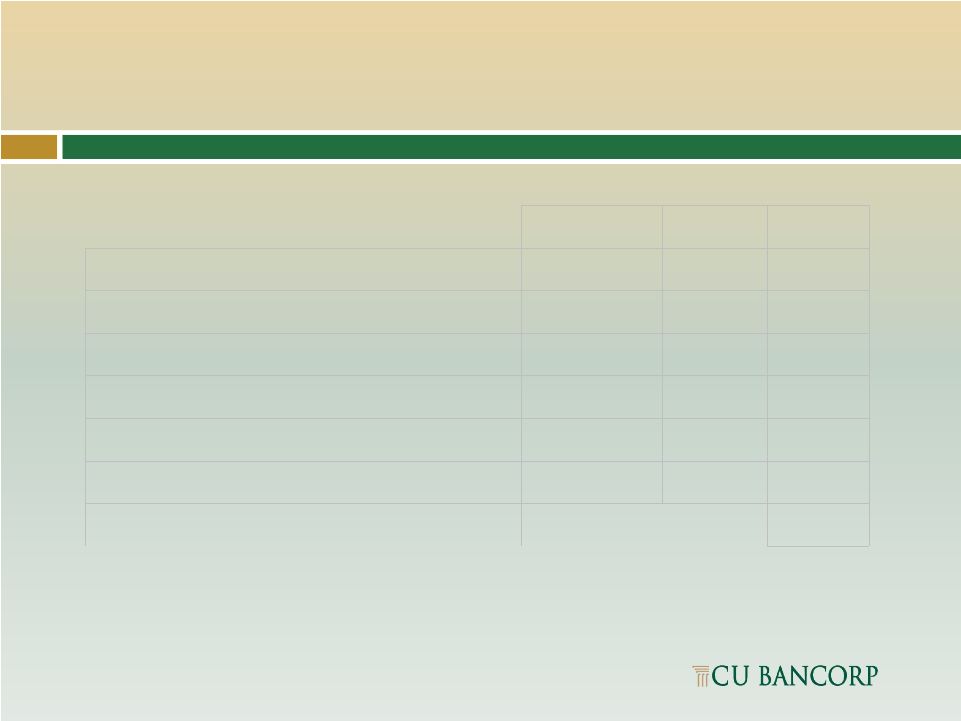

Snapshot of Income Statement for 2Q14 $ in thousands, except per share data Core net income increased 24% year over year Income Statement 2Q 14 2Q 13 % change EPS - fully diluted $0.21 $0.22 -5% Core EPS $0.26 $0.22 18% Net Income 2,386 2,321 3% Core Net Income 2,883 2,321 24% Net Interest income 12,578 12,580 0.0% Non-interest income 1,783 1,690 6% Gain on sale of SBA loans 167 60 178% Non-interest expense 9,698 9,281 4% Core non-interest expense 9,201 9,281 -1% Provision for loan losses 408 1,153 -65% 16 |

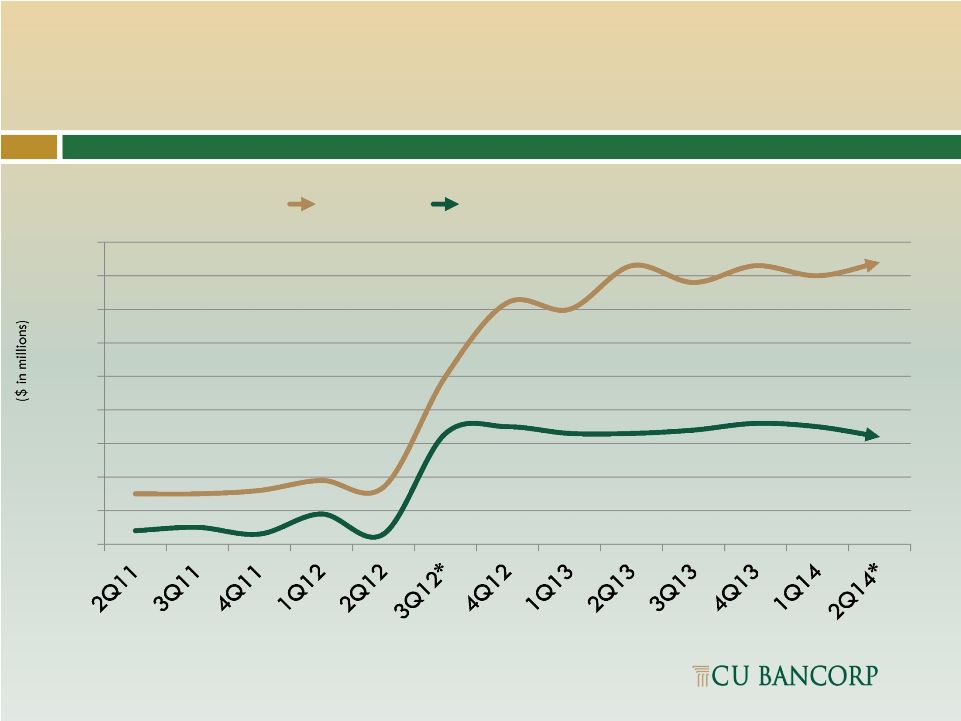

17 Improving Operating Leverage *3Q12 operating expenses excludes $2.5 million in merger-related expenses; 2Q14 excludes $497 thousand in merger-related expenses $6 $7 $8 $9 $10 $11 $12 $13 $14 $15 Revenue Operating Expenses |

Snapshot of Balance Sheet 2Q14 vs. 2Q13 $ in thousands *Non-interest bearing deposits now account for 55% of total deposits Year over year: total loans up 11%, non-interest bearing deposits up 19% Balance Sheet 2Q14 2Q13 % change Assets $1,430,313 $1,278,661 12% Total loans 979,890 885,027 11% Total deposits 1,245,280 1,097,707 13% Non-interest bearing demand deposits* 682,300 571,045 19% Shareholders' equity 145,438 129,567 12% 18 |

Snapshot of Performance Ratios 2Q14 vs. 2Q13 Performance Ratios 2Q 14 2Q 13 % change Net interest margin 3.88% 4.25% -9% ROAA 0.69% 0.73% -5% Core ROAA 0.83% 0.73% 14% ROAE 6.63% 7.16% -7% Core ROAE 8.01% 7.16% 12% Efficiency ratio 68% 65% 4% Core efficiency ratio 64% 65% -1% 19 |

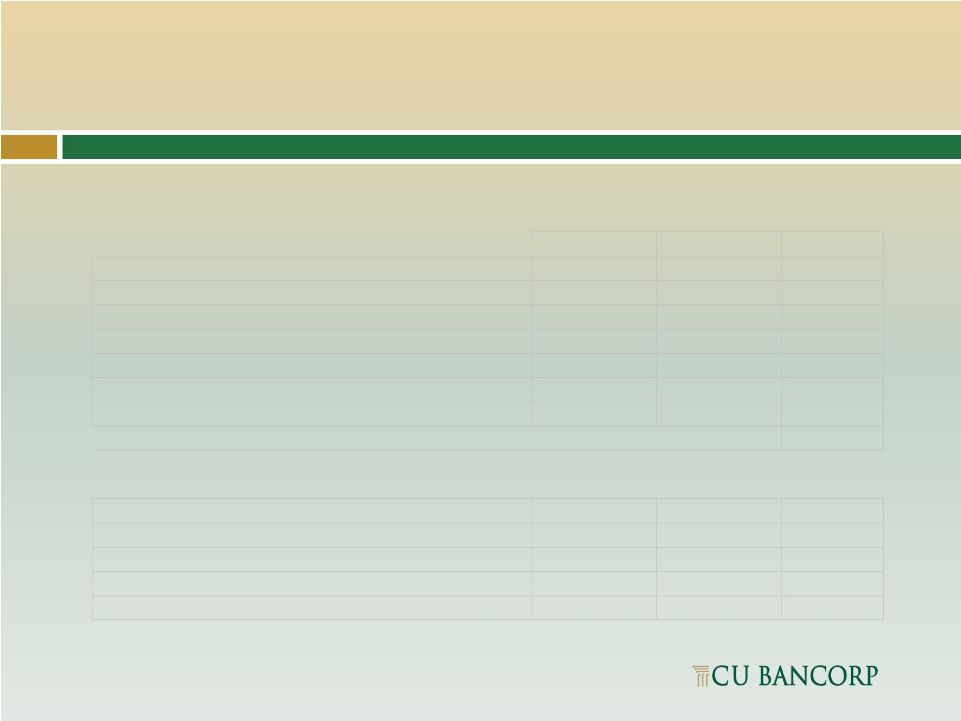

Snapshot of Income Statement and Balance Sheet 2Q14 vs. 1Q14 $ in thousands, except per share data Income Statement 2Q 14 1Q 14 % change EPS $0.21 $0.24 -13% Core EPS $0.26 $0.24 8.3% Net Income 2,386 2,666 -11% Core Net Income 2,883 2,666 8% Net Interest income 12,578 12,173 3% Non-Interest income 1,783 1,790 0% Non-Interest expense 9,698 9,549 2% Core non -interest expense 9,201 9,549 -4% Balance Sheet Assets 1,430,313 1,382,363 3% Total loans 979,890 945,507 4% Total deposits 1,245,280 1,203,398 3% Non-interest bearing demand deposits 682,300 651,645 5% Shareholders' equity 145,438 142,258 2% 20 |

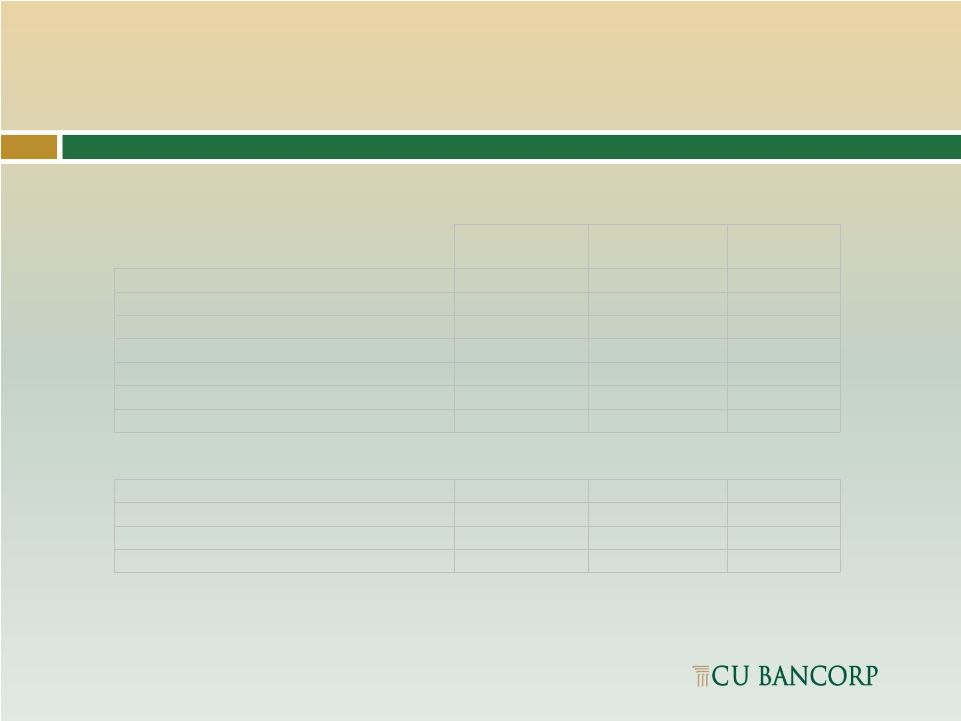

21 Snapshot of Income Statement and Balance Sheet for 1H14 & 1H13 For the Six Months Ended Income Statement 2014 2013 % change EPS $0.45 $0.42 7% Net income 5,052 4,476 13% Net Interest income 24,751 24,118 3% Non-Interest income 3,573 3,116 15% Gain on sale of SBA loans 605 410 48% Non-Interest expense 19,247 18,590 4% Provision for loan losses 483 1,287 -62% Balance Sheet Assets 1,430,313 1,278,661 12% Total loans 979,890 885,027 11% Total deposits 1,245,280 1,097,707 13% Non-interest bearing DDA 682,300 571,045 19% |

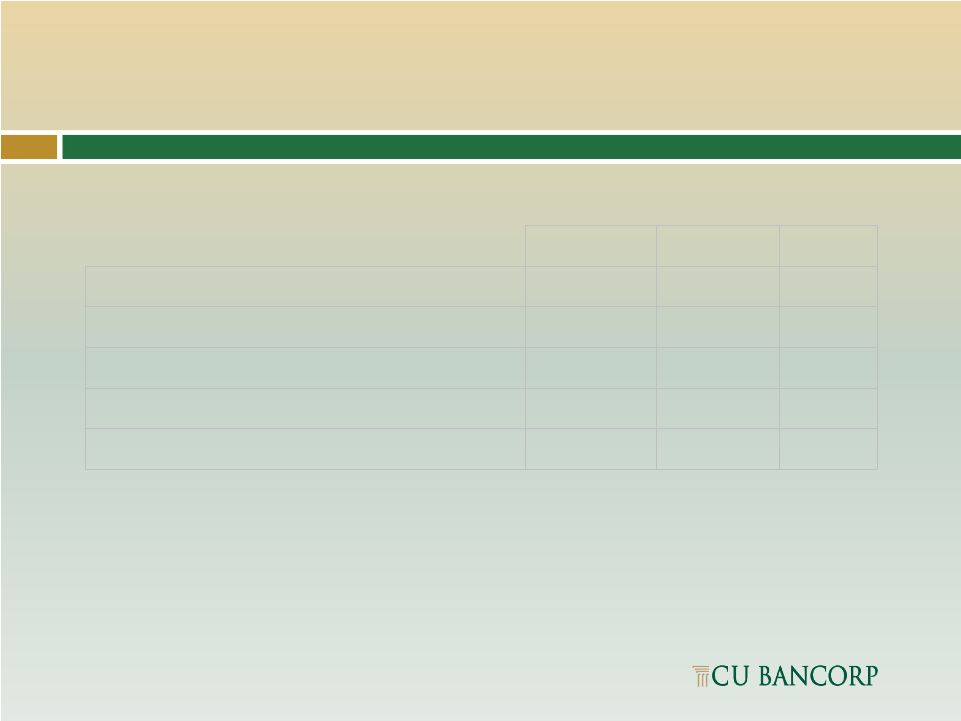

Snapshot of Shares Outstanding, Market Cap and Tangible Book Value, 2Q14 vs. 2Q13 Shares Outstanding & Market Cap 2Q 14 2Q 13 % change Share price $19.07 $15.80 21% Market cap $214,008,021 $169,601,150 26% Diluted average shares outstanding 11,159,000 10,660,000 4% Common shares issued and outstanding 11,222,235 10,734,250 5% Tangible book value $11.66 $10.78 8% 22 |

CU Bancorp is Well Capitalized by all Regulatory Ratios CU Bancorp is “well capitalized” as defined by federal regulations, which is the highest regulatory classification. Regulatory Ratios "Well Capitalized" 2Q 14 2Q 13 Tier 1 Leverage 5.0% 10.38% 9.85% Tier 1 Risk- based Capital 6.0% 11.79% 11.69% Total Risk-based Capital 10.0% 12.75% 12.60% 23 |

Appendix 24 |

Experienced Management Team *Formerly EVP at Premier Commercial Bank, N.A. Name Title Functional Banking Exp CUB Tenure David Rainer President Chief Executive Officer 34 years 9 years Anne Williams EVP Chief Operating Officer and Chief Credit Officer 34 years 9 years Karen Schoenbaum EVP Chief Financial Officer 21 years 5 years Anita Wolman EVP Chief Administrative Officer and General Counsel 37 years 9 years Sam Kunianski EVP Executive Manager – Commercial and Private Banking 30 years 8 years William Sloan EVP Executive Manager – Real Estate and Santa Clarita Regional Manager 30 years 9 years Stephen Pihl EVP Executive Manager – SBA and Orange County Regional Manager 27 years 2 years* 25 |

Asset Quality & Allowance for Loan Losses $ in thousands Asset Quality 2Q14 2Q13 % change Organic loans on non-accrual $2,046 $3,750 -45% Acquired loans on non-accrual 4,982 6,719 -26% Total non-accrual $7,028 $10,469 -33% REO 219 3,112 -93% Total non-accrual loans & REO $7,247 $13,581 -47% Net charge offs (recoveries) Qtrly -53 678 NM Non-accruals to total loans 0.72% 1.18% -39% Non-performing assets to total assets 0.51% 1.06% -52% Allowance for loan losses to total loans 1.15% 1.06% 8% ALL as % of total loans (excluding acquired loans) 1.45% 1.50% -3% Net YTD charge-offs as % of avg YTD loans -0.02% 0.08% NM ALL as % of non-accrual organic loans 551.4% 251% 120% ALL as % of total non-accrual loans (org. & acq.) 160.5% 89.9% 79% 26 |

27 Reconciliation of Non-GAAP Measures The Company utilizes the term Core Net Income, a non-GAAP financial measure. CU Bancorp’s management believes Core Net Income is useful because it is a measure utilized by management and market analysts to understand the effects of merger expenses and provides an alternative view of the Company’s performance over time and in comparison to the Company’s competitors. Core net income should not be viewed as a substitute for net income. A reconciliation of CU Bancorp’s Net Income to Core Net Income, as well as related ratios is presented in the tables below for the periods indicated: (Dollars in thousands except per share data) Three Months Ended 30-Jun-14 31-Mar-14 30-Jun-13 Net Income $ 2,386 $ 2,666 $ 2,321 Add back: Merger related expenses 497 – – Core Net Income $ 2,883 $ 2,666 $ 2,321 Average Assets $ 1,390,257 $ 1,385,845 $ 1,280,395 ROAA 0.69% 0.78% 0.73% Core ROAA* 0.83% 0.78% 0.73% Average Equity $ 144,427 $ 140,439 $ 130,010 ROAE 6.63% 7.70% 7.16% Core ROAE** 8.01% 7.70% 7.16% Diluted Average Shares Outstanding 11,159,000 11,095,000 10,660,000 Diluted Earnings Per Share $ 0.21 $ 0.24 $ 0.22 Core Diluted Earnings Per Share*** $ 0.26 $ 0.24 $ 0.22 * Core ROAA: Annualized core net income/average assets ** Core ROAE: Annualized core net income/average equity *** Core Diluted Earnings Per Share: Annualized core net income/diluted average shares outstanding Three Months Ended June 30, 2014 March 31, 2014 June 30, 2013 Net Interest Income $ 12,578 $ 12,173 $ 12,580 Non-Interest Income 1,783 1,790 1,690 Non-Interest Expense 9,698 9,549 9,281 Subtract: Merger related expenses 497 – – Core Non-Interest Expense $ 9,201 $ 9,549 $ 9,281 Efficiency Ratio 68% 68% 65% Core Efficiency Ratio* 64% 68% 65% * Core Efficiency Ratio: Core non-interest expense / (non-interest income + net interest income) |

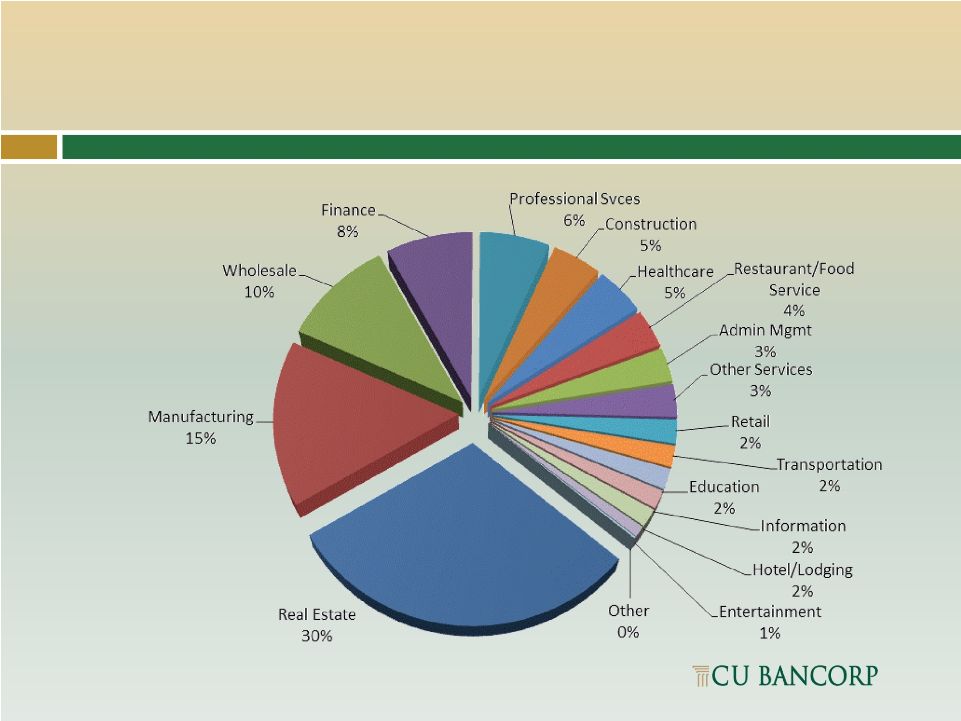

Loans by Industry – C&I and Owner-Occupied CRE 28 |

Customer Profile Our customer base reflects the diversity of industries in Southern California Significant percentage of customers involved in the manufacturing, distribution and services industries Typical customer has between $10 million and $60 million in annual sales (excluding SBA borrowers) Typical loan commitment ranges between $1 million and $5 million (excluding SBA loans) Majority of new customers come from larger banks Most new business generation results from warm leads provided by referral sources 29 |

Shareholders of CUB Acquisitions Have Been Well Rewarded 1 st Enterprise Bank (FENB) – Acquisition announced June 3, 2014 California Oaks State Bank (COSB) – Acquisition announced Aug. 25, 2010; Premier Commercial Bancorp (PCBP) – Acquisition announced Dec. 9, 2011 30 $20.00 $20.50 $21.00 $21.50 $22.00 $22.50 $23.00 $23.50 $24.00 $24.50 $25.00 $0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 $18.00 $20.00 $0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 $18.00 $20.00 COSB 8/24/10 $6.00 CUNB 7/21/14 $18.70 PCBP 12/8/11 $9.00 CUNB 7/21/14 $18.70 FENB 6/2//14 $21.75 FENB 7/21/14 $24.65 |

CUNB & FENB Merger Overview 31 |

Transaction Rationale Combination to create a $2.2 billion “pure play” business bank in Southern California Both companies have a track record of strong organic growth Scarcity value for a business banking franchise in Southern California Southern California offers an unparalleled opportunity for middle market business banks Cultural similarities Focused on small to mid-sized businesses as target clients High quality deposit base (> 50% noninterest bearing deposits and 0.11% cost of deposits) Conservative credit cultures and similar loan portfolio mix (> 50% combined C&I and OO CRE) Performance driven business development philosophy Management team comprised of veteran Southern California business bankers Complementary strengths provide opportunities for revenue synergies Partnership approach to create the “best-in-class” group of banking professionals for the pro forma company Pro forma branch network covers the greater Los Angeles market Leverages capital and increases liquidity Draws on CUNB’s strong track record of transaction execution Financially compelling projected pro forma results Strategic Partnership Enhances Value of Both Franchises Source: SNL Financial as of March 31, 2014 32 |

Summary of Terms 1 Based on CUNB closing price of $18.19 on June 2, 2014 2 Based on FENB closing price of $21.75 on June 2, 2014 3 As of March 31, 2014 Name: CU Bancorp / California United Bank Headquarters: Downtown Los Angeles (Current FENB headquarters) Management: Chairman and CEO, David I. Rainer (current Chairman, President and CEO of CUNB) Board Composition: 8 CUNB / 4 FENB Ownership: 68% CUNB / 32% FENB Consideration: 1.3450 shares of CUNB stock for each FENB share 100% stock consideration; fixed exchange ratio Equivalent to $24.47 per FENB share 13% premium to FENB’s last closing price Deal value of approximately $103 million 16.9x 2014 analyst EPS estimate 172% of tangible book value per share Timing: Expected to close in Q4 2014 President, K. Brian Horton (current President of FENB) Chief Financial Officer, Karen A. Schoenbaum (current CFO of CUNB) 33 3 2 1 1 |

Company Overviews Headquarters Encino, CA Branches 8 Total Assets ($mm) $1,382 Gross Loans ($mm) $946 Total Deposits ($mm) $1,203 Noninterest Bearing Deposits (%) 54% C&I + Own. Occ. CRE (%) 51% NPAs / Assets (%) 0.60% LTM Net Income to Common ($mm) $10.3 Headquarters Los Angeles, CA Branches 3 + 1 LPO Total Assets ($mm) $776 Gross Loans ($mm) $513 Total Deposits ($mm) $652 Noninterest Bearing Deposits (%) 49% C&I + Own. Occ. CRE (%) 59% NPAs / Assets (%) 0.57% LTM Net Income to Common ($mm) $5.3 Company Highlights Company Highlights Established in 2006 Raised $12.5 million of common equity in 2012 Funded $16.4 million of SBLF preferred equity in 2011 17.8% insider ownership Established in 2005 Completed two accretive transactions California Oaks State Bank (12/31/10) Premier Commercial Bancorp (7/31/12) Raised $22.0 million and $10.3 million of common equity in 2006 and 2011, respectively Listed on NASDAQ Capital Market in October 2012 Added to Russell 3000 Index in June 2013 12.1% insider ownership 1 Source: SNL Financial as of June 2, 2014 2 Source: Company information, as of May 15, 2014 34 1 2 |

Combination of Two Growth-Oriented Franchises Source: SNL Financial 1 Mean analyst estimate as of June 2, 2014 2 Analyst estimate as of June 2, 2014 CUNB Performance Gross Loans ($mm) Total Deposits ($mm) Net Income to Common ($mm) Gross Loans ($mm) Total Deposits ($mm) Net Income to Common ($mm) 2013 represents 1st full year impact of PCB Noninterest bearing deposits Interest bearing deposits Noninterest bearing deposits Interest bearing deposits 16% 26% FENB Performance $489 $855 $933 $946 $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 2011 2012 2013 Q12014 34% CAGR $381 $544 $632 $652 $309 $535 $600 $552 $691 $1,078 $1,232 $1,203 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 2011 2012 2013 Q12014 $293 $409 $505 $513 $0 $100 $200 $300 $400 $500 $600 2011 2012 2013 Q12014 28% CAGR $9.8 $11.3 $0.0 $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0 $16.0 2013 2014E $215 $287 $316 $322 $282 $325 $327 $330 $497 $612 $643 $652 $0 $100 $200 $300 $400 $500 $600 $700 2011 2012 2013 Q12014 $4.8 $6.1 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 $8.0 2013 2014E² 35 |

36 Key Merger Assumptions Cost savings Approximately 20% of FENB noninterest expense base Anticipate that 70% of cost savings will be realized in 2015; 100% phased-in by 2016 Consolidation of FENB’s Woodland Hills LPO Revenue synergies: opportunities identified but none assumed One-time charges: approximately $7.9 million pre-tax Preferred stock: $16.4 million of FENB SBLF preferred stock to remain outstanding 1% preferred dividend thru March 1, 2016; 9% thereafter $0.5 million initial write-down; 4 year impact using constant yield method (7.3%) Core deposit intangible: 1.1% ($7.4 million); amortized over 10 years (sum-of-the-years digits methodology) Loan mark: Credit mark write-down of 1.9% of gross loans ($10.0 million) Rate mark write-down of 0.8% of gross loans ($4.3 million) |

Financially Compelling Combination High single digits in 2015 >10% in 2016 with fully-phased in cost savings ~ 7% TBVPS dilution at close ~ 3.5 year TBVPS earn back Pro forma capital ratios at close TCE: 8.1% Tier I Leverage: 9.6% Total Risk-Based Capital: 11.5% While there are no near term plans to redeem FENB’s preferred stock, CUNB will continually evaluate the cost and amount of capital required to support the pro forma balance sheet 37 2 1 |