UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED ON DECEMBER 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

COMMISSION FILE NUMBER: 001-35575

Cencosud S.A.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Republic of Chile

(Jurisdiction of incorporation or organization)

Av. Kennedy 9001, Piso 6

Las Condes, Santiago, Chile

+56 (2) 2959-0804

(Address of principal executive offices)

Maria Soledad Fernández / Natalia Nacif / Ignacio Reyes

Av. Kennedy 9001 6th Floor

Email: IR@cencosud.cl / Mariasoledad.fernandez@cencosud.cl

Tel: +56229590545 / +56229590368

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |

Title of Each Class | | Name of Each Exchange on Which Registered |

| American Depositary Shares | | New York Stock Exchange |

| Common Shares, no par value | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

The number of outstanding shares of each of the issuer’s classes of capital stock as of December 31, 2014: 2,828,723,963 Common Shares, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | |

U.S. GAAP ¨ | | International Financial Reporting Standards as issued by the International Accounting Standards Board x | | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the Registrant has elected to follow: Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements that are based on our current expectations, assumptions, estimates and projections about us and our industry. These forward-looking statements can be identified by words or phrases such as “anticipate,” “believe,” “continue,” “estimate,” “expect,” “intend,” “is/are likely to,” “may,” “plan,” “should,” “would,” or other similar expressions. The forward-looking statements included in this annual report relate to, among others:

| | • | | changes in general economic, business or political or other conditions in Chile, Argentina, Brazil, Peru, Colombia or elsewhere in Latin America or the global markets; |

| | • | | changes in capital markets in general that may affect policies or attitudes towards investing in Chile, Argentina, Brazil, Peru, Colombia or securities issued by companies in such countries; |

| | • | | the monetary and interest rate policies of the Central Banks of Chile, Argentina, Brazil, Peru and Colombia; or elsewhere in Latin American or global markets. |

| | • | | high levels of inflation or deflation; |

| | • | | unanticipated increases in financing and other costs or our inability to obtain additional debt or equity financing on attractive terms; |

| | • | | movements in interest and/or foreign exchange rates, and movements in equity prices or other rates or prices; |

| | • | | changes in, or failure to comply with, applicable regulations, or changes in taxes; |

| | • | | loss of market share or changes in competition and pricing environments in the industries in which we operate; |

| | • | | difficulties in successfully integrating recent and future acquisitions into our operations; |

| | • | | our inability to hedge certain risks economically; |

| | • | | changes in consumer spending and saving habits; |

| | • | | implementation of new technologies; |

| | • | | limitations on our ability to open new stores and operate them profitably; |

| | • | | difficulties in completing proposed store openings, expansions or remodelings; |

| | • | | difficulties in acquiring and developing land in Chile, Argentina, Brazil, Peru or Colombia, and restrictions on opening new large stores in any such countries; and |

| | • | | the factors discussed under the section entitled “Risk Factors” in this annual report as well as risks included in the Company’s other filings and submissions with the United States Securities and Exchange Commission. |

These forward-looking statements involve various risks and uncertainties. Although we believe that the expectations expressed in these forward-looking statements are reasonable, our expectations may turn out to be incorrect. Our actual results could be materially different from our expectations. In light of the risks and uncertainties described above, the estimates and forward-looking statements discussed in this annual report might not occur, and our future results and our performance may differ materially from those expressed in these forward-looking statements due to, including, but not limited to, the factors mentioned above. Because of these uncertainties, you should not make any investment decision based on these estimates and forward-looking statements.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events.

1

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

General

In this annual report, unless otherwise specified or if the context so requires:

| | • | | References to the terms “Cencosud S.A.,” “we,” “us,” “our,” and “our company” refer to the registrant, Cencosud S.A., a corporation organized under the form of asociedad anónima under the laws of Chile, and its consolidated subsidiaries, unless otherwise indicated. |

| | • | | References to “$,” “U.S.$,” “U.S. dollars,” “dollars” and “USD” are to U.S. dollars. |

| | • | | References to “Chilean pesos” or “Ch$” are to Chilean pesos, the official currency of Chile. |

| | • | | References to “Argentine pesos” or “Ar$” are to Argentine pesos, the official currency of Argentina. |

| | • | | References to “Brazilian Real,” “Real,” “Reais” or “R$” are to the Brazilian real, the official currency of Brazil. |

| | • | | References to “Nuevo Sol,” “Nuevos Soles” or “S/.” are to Peruvian nuevos soles, the official currency of Peru. |

| | • | | References to “Colombian pesos” or “Col$” are to Colombian pesos, the official currency of Colombia. |

| | • | | References to “UF” are toUnidades de Fomento. The UF is an inflation-indexed Chilean monetary unit with a value in Chilean pesos that is adjusted daily to reflect changes in the official Consumer Price Index (“CPI”) of theInstituto Nacional de Estadísticas (the “Chilean National Institute of Statistics”). The UF is adjusted in monthly cycles. Each day in the period beginning on the tenth day of the current month through the ninth day of the succeeding month, the nominal peso value of the UF is indexed up (or down in the event of deflation) in order to reflect a proportionate amount of the change in the Chilean consumer price index during the prior calendar month. As of December 31, 2014, UF1.00 was equivalent to U.S.$40.58 and Ch$24,627.101, in each case based on the observed exchange rate reported by the Central Bank of Chile. |

This annual report contains translations of certain Chilean peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the Chilean peso amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rates indicated, at any particular rate or at all. Unless otherwise indicated, the exchange rate used in converting Chilean pesos into U.S. dollars for amounts presented as of and for the year ended December 31, 2014 is based on the observed exchange rate (dólar observado) reported by the Central Bank of Chile (the “Chilean Central Bank”) for December 31, 2014, which was Ch$606.75 per U.S.$1.00. The rates reported by the Chilean Central Bank for December 31, 2014 are based upon the observed exchange rate published by the Chilean Central Bank on the first business day following the respective period. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

Financial Statements

The financial information contained in this annual report includes our audited consolidated financial statements as of December 31, 2014 and 2013 and for the years ended December 31, 2014, 2013 and 2012 together with the notes thereto, prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (the “IASB”), which we refer to in this annual report as our “Audited Consolidated Financial Statements.” Our date of adoption of IFRS was January 1, 2010.

Our Audited Consolidated Financial Statements have been audited by PricewaterhouseCoopersConsultores, Auditores y Compañia Limitada, an independent registered public accounting firm, whose report on our Audited Consolidated Financial Statements appears elsewhere in this annual report. We maintain our books and records in Chilean pesos and prepare consolidated financial statements in accordance with IFRS.

Unless otherwise noted, the financial data presented herein as of and for each of the five years ended December 31, 2014 is stated in Chilean pesos, our functional and reporting currency.

2

Our audited consolidated financial statements have been prepared on the accrual basis of accounting, except for those items accounted for at fair value (for example, investment properties and certain financial assets, such as options and derivative financial instruments), and include the accounts of the Company and its subsidiaries, including Banco Paris. All significant inter-company balances and transactions have been eliminated in consolidation.

The financial statements as of and for the year ended December 31, 2013 presented in this form 20-F differ from the local financial statements as of and for the year ended December 31, 2013 published in Chile on March 28, 2014 and furnished to the SEC on form 6K on March 31, 2014, due to the inclusion in this report of a Ch$20,000 million lawsuit provision related to the April 24, 2013 ruling from the Chilean Supreme Court on the Class action suit filed by theServicio Nacional del Consumidor (the National Consumer Service) against Cencosud Administradora de Tarjetas S.A. (“CAT”). For further information on this matter, please see “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Legal and Administrative Proceedings” in this Annual Report. Financial statements presented in this annual report also differ due to the inclusion of the effect on deferred income tax liabilities of the Chilean tax reform that took place in 2014 as an effect on equity for the financial statements filed with our regulator in Chile in accordance with regulator issue Circular 856 dated October of 17, 2014. The effect of the Chilean tax reform on the financial statements included herein was against the company’s results in accordance with IAS 12. Please see Note 2 of the Financial Statements.

On June 20, 2014, Cencosud, together with its subsidiaries Cencosud Retail S.A. and Easy S.A., entered into a framework agreement (the “Joint Venture Framework Agreement”) with The Bank of Nova Scotia (“BNS”) and its wholly owned subsidiary Scotiabank Chile, to further develop, on a joint basis, the retail finance business in Chile (hereinafter, the “Business”). The Joint Venture Framework Agreement provides that the Business shall be operated through (i) Cencosud Administradora de Tarjetas S.A. (“CAT”), a subsidiary of Cencosud that is in the business of issuing credit cards, and (ii) Cencosud Administradora de Procesos S.A., Cencosud Servicios Integrales S.A. and Cencosud Corredores de Seguros y Servicios Ltda., or other companies to be established by Cencosud for purposes of the Joint Venture Framework Agreement, to assist in developing the Business, including information processing and collection activities related thereto (together with CAT, hereinafter, the “Subject Companies”). As part of the agreement, Scotiabank Chile will acquire a fifty-one percent (51%) controlling interest of each of the Subject Companies, with Cencosud retaining the remaining forty-nine percent (49%) non-controlling interest of each of the Subject Companies. This framework agreement has a lifespan of 15 years.

Cencosud prepares and reports its financial statements under IFRS. Under IFRS Standard N 5 (“IFRS 5”), “Disposal of subsidiaries, business and non-current assets”, the Subject Companies, which comprise the Chilean portion of our financial services segment, are considered as of June 20, 2014, to be “Assets held for sale” as a result of Cencosud’s commitment to sell a controlling interest to an unrelated party under the Joint Venture Framework Agreement, the occurrence of which received Chilean regulatory approval for its full execution on April 13, 2015. We expect full execution of the framework agreement in early May 2015.

IFRS 5 requires that (a) assets that meet the criteria to be classified as held for sale be measured at the lower of carrying amount andfair value lesscosts to sell, and depreciation on such assets shall cease; and (b) assets that meet the criteria to be classified as held for sale be presented separately in the statement of financial position and the results of discontinued operations, net of tax, and be presented separately in the statement of comprehensive income. Net cash flows attributable to the operating, investing and financing activities of discontinued operations are required to be disclosed either in the notes to the financial statements or in the financial statements themselves. IFRS 5 requires that a company “re-present” its financial disclosure of discontinued operations for all prior periods presented in the financial statements so that the disclosures relate to all operations that have been discontinued by the end of the reporting period for the latest period presented.

Special Note Regarding Non-IFRS Financial Measures

This annual report makes reference to certain non-IFRS measures, namely EBIT, EBITDA and Adjusted EBITDA from continuing operations. These non-IFRS measures are not recognized measures under IFRS, do not have a standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies. Rather, these measures are provided as additional information to complement IFRS measures by providing further understanding of the Company’s results of operations from management’s perspective. Accordingly, they should not be considered in isolation nor as a substitute for analysis of our financial information reported under IFRS.

EBIT represents profit attributable to controlling shareholders before net interest expense and income taxes. EBITDA represents EBIT plus depreciation and amortization expense. Adjusted EBITDA represents EBITDA as further adjusted to reflect items set forth in the table below. We have included EBIT, EBITDA and Adjusted EBITDA to provide investors with a supplemental measure of our operating performance.

We believe EBIT, EBITDA and Adjusted EBITDA are an important supplemental measure of operating performance because they eliminate items that have less bearing on our operating performance and thus highlight trends in our core business that may not otherwise be apparent when relying solely on IFRS financial measures. We also believe that securities analysts, investors and other interested parties frequently use EBITDA in the evaluation of issuers, many of which present EBITDA when reporting their results.

3

Our management also uses EBITDA and Adjusted EBITDA in order to facilitate operating performance comparisons from period to period, prepare annual operating budgets, assess our ability to meet our future debt service, capital expenditure and working capital requirements and assess our ability to pay dividends on our capital stock.

EBIT, EBITDA and Adjusted EBITDA have important limitations as analytical tools. For example, neither EBIT, EBITDA nor Adjusted EBITDA reflect (a) our cash expenditures, or future requirements for capital expenditures or contractual commitments; (b) changes in, or cash requirements for, our working capital needs; (c) the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; and (d) tax payments or distributions to our parent to make payments with respect to taxes attributable to us that represent a reduction in cash available to us. Although we consider the items excluded in the calculation of non-IFRS measures to be less relevant to evaluate our performance, some of these items may continue to take place and accordingly may reduce the cash available to us.

We believe that the presentation of the non-IFRS measures described above is appropriate. However, these non-IFRS measures have important limitations as analytical tools, and you should not consider them in isolation, or as substitutes for analysis of our results as reported under IFRS. Because of these limitations, we primarily rely on our results as reported in accordance with IFRS and use EBIT, EBITDA and Adjusted EBITDA only supplementally. In addition, because other companies may calculate EBITDA and Adjusted EBITDA differently than we do, EBITDA may not be, and Adjusted EBITDA as presented in this report is not, comparable to similarly titled measures reported by other companies.

A reconciliation of our profit (loss) attributable to controlling shareholders, the most directly comparable IFRS financial measure, to EBITDA and to Adjusted EBITDA is set forth below:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$) | | | (in millions of Ch$) | |

Profit attributable to controlling shareholders | | | 251 | | | | 152,233 | | | | 241,408 | | | | 216,911 | | | | 241,329 | | | | 258,384 | |

Profit attributable to non-controlling shareholders | | | (1 | ) | | | (748 | ) | | | 166 | | | | 2,851 | | | | 10,559 | | | | 10,220 | |

Profit from Continuing Operations | | | 250 | | | | 151,485 | | | | 241,573 | | | | 219,762 | | | | 251,888 | | | | 268,604 | |

Financial expense (net) | | | 355 | | | | (215,456 | ) | | | (217,857 | ) | | | (170,399 | ) | | | (105,054 | ) | | | (59,680 | ) |

Income tax charge | | | (208 | ) | | | (125,932 | ) | | | (94,068 | ) | | | (92,226 | ) | | | (111,305 | ) | | | (67,361 | ) |

EBIT from Continuing Operations | | | 812 | | | | 492,872 | | | | 553,498 | | | | 482,387 | | | | 468,247 | | | | 395,645 | |

Depreciation and amortization | | | (330 | ) | | | (200,043 | ) | | | (189,038 | ) | | | (138,941 | ) | | | (117,498 | ) | | | (162,995 | ) |

EBITDA from Continuing Operations | | | 1,142 | | | | 692,915 | | | | 742,536 | | | | 713,553 | | | | 585,745 | | | | 558,639 | |

Exchange differences | | | (39 | ) | | | (23,643 | ) | | | (25,054 | ) | | | (12,053 | ) | | | (1,577 | ) | | | (2,051 | ) |

Increase on revaluation of investment properties(1) | | | 166 | | | | 100,773 | | | | 95,110 | | | | 98,633 | | | | 72,798 | | | | 37,573 | |

Losses from indexation | | | (65 | ) | | | (39,576 | ) | | | (18,885 | ) | | | (23,538 | ) | | | (27,641 | ) | | | (16,705 | ) |

Adjusted EBITDA from Continuing Operations | | | 1,080 | | | | 655,361 | | | | 691,365 | | | | 650,510 | | | | 539,011 | | | | 502,310 | |

As a % of revenues | | | | | | | | |

Profit from Continuing Operations | | | 1.4 | % | | | 1.4 | % | | | 2.4 | % | | | 2.5 | % | | | 3.3 | % | | | 4.3 | % |

Financial income (expenses) | | | (2.0 | )% | | | (2.0 | )% | | | (2.1 | )% | | | (1.9 | )% | | | (1.4 | )% | | | (1.0 | )% |

Income tax charge | | | (1.2 | )% | | | (1.2 | )% | | | (0.9 | )% | | | (1.0 | )% | | | (1.5 | )% | | | (1.1 | )% |

EBIT from Continuing Operations | | | 4.6 | % | | | 4.6 | % | | | 5.5 | % | | | 5.4 | % | | | 6.2 | % | | | 6.6 | % |

Depreciation and amortization | | | (1.9 | )% | | | (1.9 | )% | | | (1.9 | )% | | | (1.6 | )% | | | (1.5 | )% | | | (2.7 | )% |

EBITDA from Continuing Operations | | | 6.5 | % | | | 6.5 | % | | | 7.3 | % | | | 8.0 | % | | | 7.7 | % | | | 9.3 | % |

Exchange differences | | | (0.2 | )% | | | (0.2 | )% | | | (0.2 | )% | | | (0.1 | )% | | | (0.0 | )% | | | (0.0 | )% |

Increase on revaluation of investment properties(1) | | | 0.9 | % | | | 0.9 | % | | | 0.9 | % | | | 1.1 | % | | | 1.0 | % | | | 0.6 | % |

Losses from indexation | | | (0.4 | )% | | | (0.4 | )% | | | (0.2 | )% | | | (0.3 | )% | | | (0.4 | )% | | | (0.3 | )% |

Adjusted EBITDA from Continuing Operations | | | 6.1 | % | | | 6.1 | % | | | 6.8 | % | | | 7.3 | % | | | 7.1 | % | | | 8.3 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

4

A reconciliation of our profit (loss) attributable to controlling shareholders, the most directly comparable IFRS financial measure, to EBITDA from continuing operations and to Adjusted EBITDA from continuing operations per business segment is included below:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Information by segment | | Supermarkets | | | Shopping

centers | | | Home

improvement

stores | | | Department

stores | | | Financial

services | | | Other | | | Consolidated

total | |

| | | | | | | | | | | | | | | Continuing

Operations | | | | | | Continuing

Operations | |

| | | Year ended December 31, 2014 (in millions of Ch$) | |

Profit (loss) attributable to controlling shareholders | | | 289,603 | | | | 259,362 | | | | 98,786 | | | | (4,575 | ) | | | 36,100 | | | | (527,042 | ) | | | 152,233 | |

Profit attributable to non-controlling shareholders | | | — | | | | — | | | | — | | | | — | | | | — | | | | (748 | ) | | | (748 | ) |

Profit from Continuing Operations | | | 289,603 | | | | 259,362 | | | | 98,786 | | | | (4,575 | ) | | | 36,100 | | | | (527,790 | ) | | | 151,485 | |

| | | | | | | |

Financial expense (net) | | | | | | | | | | | | | | | | | | | | | | | (215,456 | ) | | | (215,456 | ) |

| | | | | | | |

Income tax charge | | | | | | | | | | | | | | | | | | | | | | | (125,932 | ) | | | (125,932 | ) |

| | | | | | | |

EBIT from continuing operations | | | 289,603 | | | | 259,362 | | | | 98,786 | | | | (4,575 | ) | | | 36,100 | | | | (186,403 | ) | | | 492,872 | |

| | | | | | | |

Depreciation and amortization | | | (134,505 | ) | | | (5,488 | ) | | | (20,363 | ) | | | (26,429 | ) | | | (1,942 | ) | | | (11,316 | ) | | | (200,043 | ) |

| | | | | | | |

EBITDA from continuing operations | | | 424,108 | | | | 264,849 | | | | 119,148 | | | | 21,854 | | | | 38,042 | | | | (175,087 | ) | | | 692,915 | |

| | | | | | | |

Exchange differences | | | | | | | | | | | | | | | | | | | | | | | (23,643 | ) | | | (23,643 | ) |

| | | | | | | |

Increase on revaluation of investment properties(1) | | | | | | | 114,438 | | | | | | | | | | | | | | | | | | | | 114,438 | |

| | | | | | | |

Losses from indexation | | | | | | | | | | | | | | | | | | | | | | | (39,576 | ) | | | (39,576 | ) |

| | | | | | | |

Adjusted EBITDA from continuing operations | | | 424,108 | | | | 150,412 | | | | 119,148 | | | | 21,854 | | | | 38,042 | | | | (111,868 | ) | | | 641,696 | |

| | | | | | | |

As a % of revenues | | | 5.2 | % | | | 70.0 | % | | | 9.8 | % | | | 2.2 | % | | | 32.3 | % | | | N.A. | | | | 6.0 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Information by segment | | Supermarkets | | | Shopping

centers | | | Home

improvement

stores | | | Department

stores | | | Financial

services | | | Other | | | Consolidated

total | |

| | | | | | | | | | | | | | | Continuing

Operations | | | | | | Continuing

Operations | |

| | | Year ended December 31, 2013 (in millions of Ch$) | |

Profit (loss) attributable to controlling shareholders | | | 304,654 | | | | 247,586 | | | | 80,042 | | | | 24,754 | | | | 40,046 | | | | (455,510 | ) | | | 241,573 | |

Profit attributable to non-controlling shareholders | | | — | | | | — | | | | — | | | | — | | | | — | | | | (165 | ) | | | (165 | ) |

Profit from Continuing Operations | | | 304,654 | | | | 247,586 | | | | 80,042 | | | | 24,754 | | | | 40,046 | | | | (455,675 | ) | | | 241,408 | |

| | | | | | | |

Financial expense (net) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (217,857 | ) | | | (217,857 | ) |

| | | | | | | |

Income tax charge | | | — | | | | — | | | | — | | | | — | | | | — | | | | (94,068 | ) | | | (94,068 | ) |

| | | | | | | |

EBIT from continuing operations | | | 304,654 | | | | 247,586 | | | | 80,042 | | | | 24,754 | | | | 40,046 | | | | (143,750 | ) | | | 553,333 | |

| | | | | | | |

Depreciation and amortization | | | (130,205 | ) | | | (3,950 | ) | | | (19,481 | ) | | | (24,610 | ) | | | (4,238 | ) | | | (6,554 | ) | | | (189,038 | ) |

| | | | | | | |

EBITDA from continuing operations | | | 434,859 | | | | 251,536 | | | | 99,523 | | | | 49,364 | | | | 44,284 | | | | (137,196 | ) | | | 742,371 | |

| | | | | | | |

Exchange differences | | | — | | | | — | | | | — | | | | — | | | | — | | | | (25,054 | ) | | | (25,054 | ) |

| | | | | | | |

Increase on revaluation of investment properties(1) | | | — | | | | 95,110 | | | | — | | | | — | | | | — | | | | — | | | | 95,110 | |

| | | | | | | |

Losses from indexation | | | — | | | | — | | | | — | | | | — | | | | — | | | | (18,885 | ) | | | (18,885 | ) |

| | | | | | | |

Adjusted EBITDA from continuing operations | | | 434,859 | | | | 156,426 | | | | 99,523 | | | | 49,364 | | | | 44,284 | | | | (93,257 | ) | | | 691,200 | |

| | | | | | | |

As a % of revenues | | | 5.7 | % | | | 76.2 | % | | | 8.5 | % | | | 5.1 | % | | | 54.2 | % | | | N.A. | | | | 6.8 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

5

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Information by segment | | Supermarkets | | | Shopping

Centers | | | Home

improvement

stores | | | Department

stores | | | Financial

services | | | Other | | | Consolidated

total | |

| | | | | | | | | | | | | | | Continuing

Operations | | | | | | Continuing

Operations | |

| | | Year ended December 31, 2012 (in millions of Ch$) | |

Profit (loss) attributable to controlling shareholders | | | 314,538 | | | | 222,701 | | | | 73,646 | | | | 20,231 | | | | (9,431 | ) | | | (404,773 | ) | | | 216,911 | |

Profit attributable tonon-controlling shareholders | | | — | | | | — | | | | — | | | | — | | | | — | | | | 2,851 | | | | 2,851 | |

Profit from Continuing Operations | | | 314,538 | | | | 222,701 | | | | 73,646 | | | | 20,231 | | | | (9,431 | ) | | | (401,923 | ) | | | 219,762 | |

| | | | | | | |

Financial expense (net) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (170,399 | ) | | | (170,399 | ) |

| | | | | | | |

Income tax charge | | | — | | | | — | | | | — | | | | — | | | | — | | | | (92,226 | ) | | | (92,226 | ) |

| | | | | | | |

EBIT from continuing operations | | | 314,538 | | | | 222,701 | | | | 73,646 | | | | 20,231 | | | | (9,431 | ) | | | (139,298 | ) | | | 482,387 | |

| | | | | | | |

Depreciation and amortization | | | (89,454 | ) | | | (2,606 | ) | | | (17,740 | ) | | | (22,896 | ) | | | (955 | ) | | | (5,290 | ) | | | (138,941 | ) |

| | | | | | | |

EBITDA from continuing operations | | | 403,992 | | | | 225,307 | | | | 91,386 | | | | 43,127 | | | | (8,476 | ) | | | (134,008 | ) | | | 621,328 | |

| | | | | | | |

Exchange differences | | | — | | | | — | | | | — | | | | — | | | | — | | | | (12,053 | ) | | | (12,053 | ) |

| | | | | | | |

Increase on revaluation of investment properties(1) | | | — | | | | 98,633 | | | | — | | | | — | | | | — | | | | — | | | | 98,633 | |

| | | | | | | |

Losses from indexation | | | — | | | | — | | | | — | | | | — | | | | — | | | | (23,538 | ) | | | (23,538 | ) |

| | | | | | | |

Adjusted EBITDA from continuing operations | | | 403,992 | | | | 126,674 | | | | 91,386 | | | | 43,127 | | | | (8,476 | ) | | | (98,418 | ) | | | 558,285 | |

| | | | | | | |

As a % of revenues | | | 6.0 | % | | | 73.6 | % | | | 8.6 | % | | | 4.9 | % | | | (14.5 | )% | | | N/A | | | | 6.3 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Information by segment | | Supermarkets | | | Shopping

centers | | | Home

improvement

stores | | | Department

stores | | | Financial

services | | | Other | | | Consolidated

total | |

| | | | | | | | | | | | | | | Continuing

Operations | | | | | | Continuing

Operations | |

| | | Year ended December 31, 2011 (in millions of Ch$) | |

Profit (loss) attributable to controlling shareholders | | | 299,605 | | | | 170,391 | | | | 67,291 | | | | 29,698 | | | | 6,964 | | | | (332,621 | ) | | | 241,329 | |

Profit attributable to non-controlling shareholders | | | — | | | | — | | | | — | | | | — | | | | — | | | | 10,559 | | | | 10,559 | |

Profit from Continuing Operations | | | 299,605 | | | | 170,391 | | | | 67,291 | | | | 29,698 | | | | 6,964 | | | | (322,062 | ) | | | 251,888 | |

| | | | | | | |

Financial expense (net) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (105,054 | ) | | | (105,054 | ) |

| | | | | | | |

Income tax charge | | | — | | | | — | | | | — | | | | — | | | | — | | | | (111,305 | ) | | | (111,305 | ) |

| | | | | | | |

EBIT from continuing operations | | | 299,605 | | | | 170,391 | | | | 67,291 | | | | 29,698 | | | | 6,964 | | | | (105,703 | ) | | | 468,247 | |

Depreciation and amortization | | | (76,559 | ) | | | (2,344 | ) | | | (16,501 | ) | | | (17,292 | ) | | | (261 | ) | | | (4,541 | ) | | | (117,498 | ) |

EBITDA from continuing operations | | | 376,164 | | | | 172,735 | | | | 83,792 | | | | 46,990 | | | | 7,225 | | | | (101,162 | ) | | | 585,745 | |

Exchange differences | | | — | | | | — | | | | — | | | | — | | | | — | | | | (1,577 | ) | | | (1,577 | ) |

| | | | | | | |

Increase on revaluation of investment properties(1) | | | — | | | | 72,798 | | | | — | | | | — | | | | — | | | | — | | | | 72,798 | |

Losses from indexation | | | — | | | | — | | | | — | | | | — | | | | — | | | | (27,641 | ) | | | (27,641 | ) |

Adjusted EBITDA from continuing operations | | | 376,164 | | | | 99,937 | | | | 83,792 | | | | 46,990 | | | | 7,225 | | | | (75,097 | ) | | | 539,011 | |

As a % of revenues | | | 6.8 | % | | | 77.0 | % | | | 8.8 | % | | | 6.8 | % | | | 2.7 | % | | | N/A | | | | 7.1 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

6

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Information by segment | | Supermarkets | | | Shopping

centers | | | Home

improvement

Stores | | | Department

stores | | | Financial

services

continuing

operations | | | Other | | | Consolidated

total

continuing

operations | |

| | | Year ended December 31, 2010 (in millions of Ch$) | |

| | | | | | | |

Profit (loss) attributable to controlling shareholders | | | 249,364 | | | | 122,349 | | | | 53,352 | | | | 24,584 | | | | 36,162 | | | | (227,427 | ) | | | 258,384 | |

Profit attributable to non-controlling shareholders | | | — | | | | — | | | | — | | | | — | | | | — | | | | 10,220 | | | | 10,220 | |

Net Income | | | 249,364 | | | | 122,349 | | | | 53,352 | | | | 24,584 | | | | 36,162 | | | | (217,207 | ) | | | 268,604 | |

Financial Expense (net) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (59,680 | ) | | | (59,680 | ) |

Income tax charge | | | | | | | | | | | | | | | | | | | | | | | (67,361 | ) | | | (67,361 | ) |

EBIT from continuing operations | | | 249,364 | | | | 122,349 | | | | 53,352 | | | | 24,584 | | | | 36,162 | | | | (90,166 | ) | | | 395,645 | |

Depreciation and amortization | | | (58,347 | ) | | | (4,300 | ) | | | (16,435 | ) | | | (16,211 | ) | | | (181 | ) | | | (67,520 | ) | | | (162,995 | ) |

EBITDA from continuing operations | | | 307,711 | | | | 126,649 | | | | 69,787 | | | | 40,795 | | | | 36,343 | | | | (22,646 | ) | | | 558,639 | |

Exchange differences | | | — | | | | — | | | | — | | | | — | | | | — | | | | (2,051 | ) | | | (2,051 | ) |

Increase on revaluation of investment properties(1) | | | — | | | | 37,573 | | | | — | | | | — | | | | — | | | | | | | | 37,573 | |

Losses from indexation | | | | | | | | | | | | | | | | | | | | | | | (16,705 | ) | | | (16,705 | ) |

Adjusted EBITDA from continuing operations | | | 307,711 | | | | 89,076 | | | | 69,787 | | | | 40,795 | | | | 36,343 | | | | (41,402 | ) | | | 502,310 | |

As a % of revenues | | | 6.9 | % | | | 76.1 | % | | | 8.5 | % | | | 6.6 | % | | | 170.8 | % | | | N/A | | | | 8.3 | % |

| (1) | Represents a fair value adjustment of investment properties, as calculated using the discounted cash flows valuation method. |

Rounding

Certain figures included in this annual report and in our financial statements have been rounded for ease of presentation. Percentage figures included in this annual report have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this annual report may vary from those obtained by performing the same calculations using the figures in our financial statements. Certain other amounts that appear in this annual report may not sum due to rounding.

Operating Data

Calculations of revenues from ordinary activities for our shopping centers presented in this annual report exclude inter-company lease payments to our shopping centers from stores owned by us. Unless otherwise noted, calculations of gross leasable area for our shopping centers do not include the square meters occupied by our stores.

As used herein, the term “same-store sales” reflects the sales of our stores operating throughout the same months of both financial periods being compared. If a store did not operate for a full month of either of the financial periods being compared, we exclude its sales for such month from both financial periods. For example, if a new store was opened on July 1, 2012 and operated throughout the last six months of 2012, (i) our “same-store sales” data would include the sales of that store for the last six months of 2012 and the last six months of 2013 and (ii) we would account for the sales of the new store during the first six months of 2013 as sales from a newly opened store. Our calculations of same-store sales data may differ from same-store sales calculations of other retailers. Unless otherwise noted, we have presented calculations of same-store sales in nominal local currency.

7

Industry and Market Data

None of the Argentine, Brazilian, Chilean, Peruvian or Colombian governments publish definitive data regarding the supermarket, home improvement store, department store, shopping center or financial services industries.

General

This annual report contains data related to the economic conditions in the markets in which we operate. Unless otherwise indicated, information in this annual report concerning economic conditions is based on publicly available information from third-party sources which we believe to be reasonable. The economic conditions in the markets in which we operate may deteriorate, and those economies may not grow at the rates projected by market data, or at all. The deterioration of the economic conditions in the markets in which we operate may have a material adverse effect on our business, results of operations, financial condition and the market price of our shares of common stock and American Depositary Shares (“ADSs”).

Chile

Market data and other statistical information (other than with respect to our financial results and performance) used throughout this annual report are based on independent industry publications, government publications, reports by market research firms or other published independent sources, such as theInstituto Nacional de Estadísticas (the Chilean National Institute of Statistics, or “INE”), a governmental agency that publishes information based on its independent data, theAsociación Gremial de Supermercados de Chile (the Chilean Supermarkets Association, or “ASACH”), which publishes certain data with respect to supermarkets in Chile, and A.C. Nielsen Chile S.A., which publishes data with respect to the supermarket industry in Chile. Certain other shopping center statistics for Chile are published by the International Council for Shopping Centers.

Argentina

Market data and other statistical information (other than with respect to our financial results and performance) used throughout this annual report are based on independent industry publications, government publications, reports by market research firms or other published independent sources, such as theInstituto Nacional de Estadísticas y Censos (the Argentine National Institute of Statistics and Census, or “INDEC”), a governmental agency that publishes information based on its independent data, and A.C. Nielsen Argentina, which publishes market share data with respect to the supermarket industry in Argentina. In addition, theCamara Argentina de Shopping Centers (the Argentine Chamber of Shopping Centers, or “CASC”) currently publishes market share data with respect to shopping centers in Argentina. Certain other shopping center statistics for Argentina are published by the International Council for Shopping Centers.

Brazil

We have included certain information with respect to Brazil based on reports prepared by established public sources, such as the Central Bank of Brazil, theInstituto Brasileiro de Geografia e Estatística (the Brazilian Institute of Geography and Statistics, or “IBGE”), theInstituto de Pesquisa Econômica Aplicada (the Institute of Applied Economic Research, or “IPEA”), theAssociação Brasileira de Supermercados (the Brazilian Association of Supermarkets, or “ABRAS”), and theFundação Getúlio Vargas (the Getúlio Vargas Foundation). Unless otherwise indicated, all macroeconomic information relating to Brazil was obtained from the Central Bank of Brazil, IBGE and the Getúlio Vargas Foundation.

Peru

Macroeconomic data from Peru included in this annual report is derived from public entities, such as the Central Bank of Peru, the Instituto Nacional de Estadísitcas e Informática (the National Institute of Statistics and Computing, or “INEI”),Corporación de Compañías de Research (Research Companies Corporation, or “CCR”) or by Apoyo Consulting. Some data are also based on our estimates, which are derived from our review of internal surveys, as well as independent sources. Although we believe these sources are reliable, we have not independently verified the information provided by third parties. In addition, these sources may use different definitions of the relevant markets than those we present. Data regarding our industry are intended to provide general guidance but are inherently imprecise.

Colombia

Market and certain other data relating to Colombia used in this annual report was obtained from our own research, surveys or studies conducted by third parties and industry or general publications and other publicly available sources. Industry and general publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. Certain data is based on published information made available by the Colombian

8

government and its agencies, such as theDepartamento Administrativo Nacional de Estadística (the National Administrative Department of Statistics, or “DANE”) and theBanco de la Republica (“Colombian Central Bank”). Although we believe these sources to be reliable, we do not guarantee the accuracy of the information.

Other Information

According to the ASACH, “hypermarkets” are defined as retail stores with more than 10,000 square meters of selling space, offering more than 25,000 products and having more than 40 cashiers. ASACH defines “supermarkets” as retail stores having up to 6,000 square meters of selling space, between 400 and 10,000 products and ten to 25 cashiers. We consolidate the results of our supermarkets and hypermarkets under our “supermarkets” segment. Therefore, unless otherwise noted, our discussions of “supermarkets” in this annual report include ourSanta Isabel supermarkets,Jumbohypermarkets and supermarkets in Chile,DiscoandSuper Vea supermarkets andJumbohypermarkets and supermarkets in Argentina,Bretas, GBarbosa,Mercantil Rodrigues,Perini andPrezunic supermarkets in Brazil,Jumbo andMetro supermarkets in Colombia andWong andMetro supermarkets and hypermarkets in Peru. By “home improvement” stores we mean retail establishments that sell a wide assortment of building materials and home improvement and lawn and garden products and provide certain related services. Our “home improvement stores” refer to our home improvement stores operated under theEasyandBlaistenbrand names, including ourEasy stores in Chile, Argentina and Colombia. By “department stores” we mean retail establishments that market a varied assortment of apparel, electronic and household goods. These stores currently operate in Chile and Peru under ourParis andJohnson brands. References to “stores” refer collectively to our hypermarkets, supermarkets, department stores and home improvement stores.

One meter equals approximately 3.3 feet or 1.1 yards and one square meter equals approximately 10.8 square feet.

We own or have rights to use the trademarks, service marks and trade names that we use in conjunction with the operation of our business. Some of the more important trademarks that we own or have rights to use that appear in this annual report include: Jumbo®, Jumbo Más®, Easy®, Más Easy®, Santa Isabel®, Disco®, Vea®, Super Vea®, Blaisten®, Johnson®, Paris®, Más Paris®, Seguros Cencosud®, Banco Paris®, Circulo Más®, Wong®, Metro®, GBarbosa®, Perini®, Bretas®, Mercantil Rodrigues®, Nectar® , which is replaced by the brandCencosud Puntos® as our loyalty program as of March 31, 2014 in Chile and Colombia) , Tarjeta Cencosud®, Banco Cencosud®, Costaner Center®, Vive Chevere® and Prezunic®, each of which may be registered or trademarked in any of Argentina, Brazil, Chile, Colombia, Peru or other jurisdictions. Solely for convenience, we may refer to our trademarks, service marks and trade names in this annual report without the ™ and® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent permitted under applicable law, our rights to our trademarks, service marks and trade names. Each trademark, trade name or service mark of any other company appearing in this annual report is, to our knowledge, owned by such other company.

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. SELECTED FINANCIAL DATA

Selected Financial and Operating Data

The following tables set forth our summary consolidated financial information under IFRS. You should read the information contained in these tables in conjunction with “Item 5. Operating and Financial Review and Prospects,” “Item 8. Financial Information,” “Item 18. Financial Statements.” and the consolidated financial statements and the accompanying notes included elsewhere in this annual report.

The financial information as of December 31, 2014 and 2013 and for the years ended December 31, 2014, 2013 and 2012 has been derived from our Audited Consolidated Financial Statements included elsewhere in this annual report. The selected statement of

9

operations data with respect to fiscal year ended December 31, 2011 and 2010 and the selected balance sheet data as of December 31, 2012 have been derived from the Company’s consolidated financial statements not included herein. We maintain our books and records in Chilean pesos and prepare consolidated financial statements in accordance with IFRS. Our date of adoption of IFRS was January 1, 2010. The following financial and operating information should be read in conjunction with, and is qualified in its entirety by reference to, our Audited Consolidated Financial Statements included elsewhere in this annual report.

Unless otherwise noted, U.S. dollar amounts have been translated from Chilean pesos based on thedólar observado, or observed exchange rate of Ch$606.75 per U.S.$1.00 as of December 31, 2014, as reported by the Chilean Central Bank. We make no representation that the Chilean peso or the U.S. dollar amounts referred to herein actually represent, could have been or could be converted into U.S. dollars or Chilean pesos, as the case may be, at the rates indicated, at any particular rate or at all.

In our opinion, the summary consolidated financial data presented in the tables below includes all adjustments necessary to present fairly in all material respects our financial condition and results of operations at the dates and the periods presented. The results of operations presented below are not necessarily indicative of future performance.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Income statement data: | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of

U.S.$) | | | | | | | | | (in millions of Ch$) | | | | | | | |

Revenues from ordinary activities, continuing operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Supermarkets | | | 13,447 | | | | 8,159,237 | | | | 7,682,993 | | | | 6,733,610 | | | | 5,556,271 | | | | 4,452,759 | |

Home improvement stores | | | 2,019 | | | | 1,225,616 | | | | 1,176,890 | | | | 1,063,086 | | | | 948,641 | | | | 819,838 | |

Department stores | | | 1,634 | | | | 991,442 | | | | 970,360 | | | | 886,075 | | | | 690,772 | | | | 622,719 | |

Shopping Centers | | | 354 | | | | 214,850 | | | | 205,332 | | | | 172,104 | | | | 129,727 | | | | 116,991 | |

Financial Services | | | 194 | | | | 117,679 | | | | 81,651 | | | | 58,454 | | | | 267,874 | | | | 21,283 | |

Other(1) | | | 4 | | | | 2,205 | | | | 16,932 | | | | 12,022 | | | | 11,520 | | | | 3,657 | |

Total revenues from ordinary activities | | | 17,653 | | | | 10,711,029 | | | | 10,134,158 | | | | 8,925,351 | | | | 7,604,806 | | | | 6,236,974 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Income statement data: | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$) | | | (in millions of Ch$) | |

Cost of sales: | | | | | | | | | | | | | | | | |

Supermarkets | | | (10,225 | ) | | | (6,204,110 | ) | | | (5,782,590 | ) | | | (5,057,477 | ) | | | (4,177,664 | ) | | | (3,355,796 | ) |

Home improvement stores | | | (1,319 | ) | | | (800,342 | ) | | | (787,402 | ) | | | (711,500 | ) | | | (647,337 | ) | | | (561,006 | ) |

Department stores | | | (1,222 | ) | | | (741,279 | ) | | | (701,530 | ) | | | (644,668 | ) | | | (499,413 | ) | | | (446,769 | ) |

Shopping Centers | | | (46 | ) | | | (28,029 | ) | | | (23,341 | ) | | | (27,213 | ) | | | (19,448 | ) | | | (17,858 | ) |

Financial Services | | | (64 | ) | | | (39,046 | ) | | | (25,938 | ) | | | (21,082 | ) | | | (14,028 | ) | | | (6,102 | ) |

Other (1) | | | (3 | ) | | | (1,967 | ) | | | (3,451 | ) | | | (2,294 | ) | | | (5,421 | ) | | | (5,343 | ) |

Total cost of sales | | | (12,880 | ) | | | (7,814,773 | ) | | | (7,324,252 | ) | | | (6,464,234 | ) | | | (5,363,313 | ) | | | (4,392,874 | ) |

Gross profit: | | | | | | | | | | | | | | | | | | | | |

Supermarkets | | | 3,222 | | | | 1,955,127 | | | | 1,900,404 | | | | 1,676,133 | | | | 1,378,607 | | | | 1,096,963 | |

Home improvement stores | | | 701 | | | | 425,275 | | | | 389,487 | | | | 351,586 | | | | 301,303 | | | | 258,832 | |

Department stores | | | 412 | | | | 250,163 | | | | 268,830 | | | | 241,407 | | | | 191,359 | | | | 175,950 | |

Shopping Centers | | | 308 | | | | 186,821 | | | | 181,991 | | | | 144,891 | | | | 110,278 | | | | 99,133 | |

Financial Services | | | 130 | | | | 78,632 | | | | 55,713 | | | | 37,372 | | | | 31,286 | | | | 15,181 | |

Other(1) | | | 0 | | | | 238 | | | | 13,481 | | | | 9,728 | | | | 6,099 | | | | (1,686 | ) |

Total gross profit | | | 4,773 | | | | 2,896,256 | | | | 2,809,907 | | | | 2,461,117 | | | | 2,018,933 | | | | 1,644,373 | |

Administrative expenses, distribution costs and other expenses | | | (4,113 | ) | | | (2,495,436 | ) | | | (2,357,582 | ) | | | (2,048,390 | ) | | | (1,602,881 | ) | | | (1,371,074 | ) |

Other revenues by function | | | 189 | | | | 114,438 | | | | 108,291 | | | | 107,011 | | | | 85,107 | | | | 43,871 | |

Participation in earnings of associates | | | 10 | | | | 6,208 | | | | 10,289 | | | | 5,642 | | | | 5,779 | | | | 7,514 | |

Financial income | | | 11 | | | | 6,709 | | | | 5,999 | | | | 8,231 | | | | 10,713 | | | | 14,754 | |

Financial expenses | | | (366 | ) | | | (222,165 | ) | | | (223,856 | ) | | | (178,631 | ) | | | (115,767 | ) | | | (84,693 | ) |

Other earnings | | | 57 | | | | 34,624 | | | | 26,366 | | | | (7,403 | ) | | | (12,626 | ) | | | 13,786 | |

Exchange differences | | | (39 | ) | | | (23,643 | ) | | | (25,054 | ) | | | (12,053 | ) | | | 1,577 | | | | (2,055 | ) |

Losses from indexation | | | (65 | ) | | | (39,576 | ) | | | (18,885 | ) | | | (23,538 | ) | | | (27,641 | ) | | | (16,747 | ) |

Income (loss) before taxes | | | 457 | | | | 277,416 | | | | 335,476 | | | | 311,988 | | | | 363,193 | | | | 326,713 | |

Income tax charge | | | (208 | ) | | | (125,932 | ) | | | (94,068 | ) | | | (92,226 | ) | | | (111,305 | ) | | | (72,856 | ) |

Profit from Continuing Operations | | | 251 | | | | 151,485 | | | | 241,408 | | | | 219,762 | | | | 251,888 | | | | 253,858 | |

10

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Income statement data: | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$) | | | (in millions of Ch$) | |

Profit from Discontinued Operations | | | 21 | | | | 12,662 | | | | 8,357 | | | | 33,047 | | | | | | | | 52,623 | |

Net Income | | | 271 | | | | 164,146 | | | | 249,765 | | | | 252,809 | | | | | | | | 296,261 | |

Profit attributable to non-controlling shareholders | | | 1 | | | | (748 | ) | | | (165 | ) | | | 2,851 | | | | 33,004 | | | | 10,220 | |

Profit attributable to controlling shareholders | | | 272 | | | | 164,894 | | | | 249,930 | | | | 249,958 | | | | 284,892 | | | | 296,261 | |

Net earnings attributable to shareholders per share for continuing operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic(2) | | | 0.0887 | | | | 53.8 | | | | 87.4 | | | | 93.20 | | | | 106.60 | | | | 130.85 | |

Diluted(2) | | | 0.0887 | | | | 53.8 | | | | 86.8 | | | | 92.30 | | | | 105.50 | | | | 129.56 | |

Net earnings attributable to shareholders per share for discontinued operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic(2) | | | 0.0074 | | | | 4.50 | | | | 3.0 | | | | 14.2 | | | | 14.6 | | | | 130.85 | |

Diluted(2) | | | 0.0074 | | | | 4.50 | | | | 3.0 | | | | 14.2 | | | | 14.4 | | | | 129.56 | |

Number of Shares | | | | | | | | | | | | | | | | | | | | | | | | |

Total number of Shares | | | 2,828,723,963 | | | | 2,828,723,963 | | | | 2,828,723,963 | | | | 2,507,103,215 | | | | 2,264,103,215 | | | | 2,264,103,215 | |

Dividends per share: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic(2) | | | 0.0402 | | | | 21.09 | | | | 28.85 | | | | 22.88 | | | | 34.65 | | | | 24.26 | |

Diluted(2) | | | 0.0398 | | | | 20.93 | | | | 28.64 | | | | 22.66 | | | | 34.31 | | | | 24.26 | |

| (1) | Includes the results of our Aventura entertainment centers, our loyalty programs and corporate back-office operations. See “Item 4. Information on the Company—B. Business Overview—Our Company.” |

| (2) | In U.S. dollars U.S. dollars and Chilean pesos. |

In November 2012, we completed the acquisition of Carrefour Societe Anonyme’s (Carrefour) supermarket operations in Colombia See “Item 4. Information on the Company—A. History and Development of the Company—History.”

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | As of December 31, | |

Balance sheet data: | | 2014 | | | 2014 | | | 2013 | | | 2012(1) | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$) | | | (in millions of Ch$) | |

Total current assets | | | 4,948 | | | | 3,002,468 | | | | 2,425,219 | | | | 2,316,812 | | | | 2,085,636 | | | | 1,582,309 | |

Property, plant, equipment and investment property net | | | 7,702 | | | | 4,673,321 | | | | 4,670,316 | | | | 4,605,872 | | | | 3,538,672 | | | | 2,913,644 | |

Other assets | | | 5,011 | | | | 3,040,715 | | | | 2,969,699 | | | | 2,820,906 | | | | 2,019,780 | | | | 1,839,516 | |

Total assets | | | 17,662 | | | | 10,716,503 | | | | 10,065,234 | | | | 9,743,590 | | | | 7,644,088 | | | | 6,335,469 | |

Total current liabilities | | | 5,173 | | | | 3,138,770 | | | | 2,951,699 | | | | 3,336,630 | | | | 2,331,280 | | | | 1,919,094 | |

| |

| | | As of December 31, | |

| Balance sheet data: | | 2014 | | | 2014 | | | 2013 | | | 2012(1) | | | 2011 | | | 2010 | |

Total non-current liabilities | | | 5,416 | | | | 3,286,247 | | | | 2,852,168 | | | | 3,008,748 | | | | 2,362,201 | | | | 1,726,781 | |

Total liabilities | | | 10,589 | | | | 6,425,017 | | | | 5,803,867 | | | | 6,345,378 | | | | 4,693,482 | | | | 3,645,876 | |

Non-controlling interest | | | (1 | ) | | | (832 | ) | | | 100 | | | | 678 | | | | 87,750 | | | | 74,886 | |

Net equity attributable to controlling shareholders | | | 7,074 | | | | 4,292,318 | | | | 4,261,267 | | | | 3,397,534 | | | | 2,862,856 | | | | 2,614,707 | |

Total net equity and liabilities | | | 17,662 | | | | 10,716,503 | | | | 10,065,234 | | | | 9,743,590 | | | | 7,644,088 | | | | 6,335,469 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Assets for the 2012 period were adjusted as goodwill related to the Johnson acquisition was adjusted. |

11

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Other financial data: | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$)(1) | | | (in millions of Ch$)(1) | |

Cash Flow Data | | | | | | | | | | | | | | | | | | | | | | | | |

Net cash provided by (used in): | | | | | | | | | | | | | | | | | | | | | | | | |

Operating activities | | | 643 | | | | 390,239 | | | | 364,782 | | | | 718,715 | | | | 567,739 | | | | 407,174 | |

Investing activities | | | (385 | ) | | | (233,396 | ) | | | (320,507 | ) | | | (1,873,568 | ) | | | (623,753 | ) | | | (413,676 | ) |

Financing activities | | | (185 | ) | | | (112,378 | ) | | | (107,029 | ) | | | 1,246,077 | | | | 89,607 | | | | 5,086 | |

Other Financial Information | | | | | | | | | | | | | | | | | | | | | | | | |

Capital expenditures | | | (607 | ) | | | (227,423 | ) | | | (317,709 | ) | | | (573,650 | ) | | | (616,336 | ) | | | (349,793 | ) |

Depreciation and amortization | | | (333 | ) | | | (202,343 | ) | | | (191,500 | ) | | | (141,450 | ) | | | (120,174 | ) | | | (162,995 | ) |

Adjusted EBITDA from continuing operations(2) | | | 1,057 | | | | 641,696 | | | | 691,200 | | | | 558,285 | | | | 539,011 | | | | 502,310 | |

Financial Ratios | | | | | | | | | | | | | | | | | | | | | | | | |

Gross margin(3) | | | 27.0 | % | | | 27.0 | % | | | 27.7 | % | | | 27.6 | % | | | 26.5 | % | | | 26.4 | % |

Net margin(4) | | | 1.4 | % | | | 1.4 | % | | | 2.4 | % | | | 2.5 | % | | | 3.3 | % | | | 4.9 | % |

Current ratio(5) | | | 0.96 | x | | | 0.96 | x | | | 0.82 | x | | | 0.77 | x | | | 0.88 | x | | | 0.92 | x |

| (1) | Except financial ratios. |

| (2) | See “Presentation of Financial and Other Information” for the definition of Adjusted EBITDA and the reconciliation of Adjusted EBITDA to IFRS measures. |

| (3) | Consolidated gross profit divided by consolidated revenues from ordinary activities. |

| (4) | Consolidated net income divided by consolidated revenues from ordinary activities. |

| (5) | Consolidated current assets divided by consolidated current liabilities. |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Comprehensive income: | | 2014 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of U.S.$) | | | (in millions of Ch$) | |

Comprehensive income attributable to controlling shareholders | | | 125 | | | | 76,055 | | | | 94,725 | | | | 34,002 | | | | 357,049 | | | | 201,686 | |

Comprehensive (loss) income attributable to non-controlling shareholders | | | (1 | ) | | | (881 | ) | | | (168 | ) | | | (5,354 | ) | | | 12,865 | | | | 253 | |

Total comprehensive income | | | 124 | | | | 75,174 | | | | 94,557 | | | | 28,648 | | | | 369,913 | | | | 201,939 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Operating data: | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

Number of Stores | | | | | | | | | | | | | | | | | | | | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 224 | | | | 224 | | | | 214 | | | | 189 | | | | 163 | |

Argentina | | | 290 | | | | 290 | | | | 288 | | | | 269 | | | | 256 | |

Brazil | | | 219 | | | | 221 | | | | 204 | | | | 152 | | | | 130 | |

Peru | | | 87 | | | | 87 | | | | 86 | | | | 74 | | | | 64 | |

Colombia | | | 100 | | | | 100 | | | | 96 | | | | 0 | | | | 0 | |

Supermarkets subtotal | | | 922 | | | | 922 | | | | 888 | | | | 684 | | | | 613 | |

Home Improvement Stores: | | | | |

Chile | | | 32 | | | | 32 | | | | 31 | | | | 29 | | | | 29 | |

Argentina | | | 48 | | | | 48 | | | | 47 | | | | 48 | | | | 49 | |

Colombia | | | 9 | | | | 9 | | | | 4 | | | | 4 | | | | 4 | |

Home improvement stores subtotal | | | 89 | | | | 89 | | | | 82 | | | | 81 | | | | 82 | |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 77 | | | | 77 | | | | 78 | | | | 35 | | | | 34 | |

Peru | | | 6 | | | | 6 | | | | 0 | | | | 0 | | | | 0 | |

Department stores subtotal | | | 83 | | | | 83 | | | | 78 | | | | 35 | | | | 34 | |

Shopping Centers: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 25 | | | | 25 | | | | 9 | | | | 9 | | | | 9 | |

Argentina | | | 18 | | | | 18 | | | | 18 | | | | 14 | | | | 14 | |

Peru | | | 4 | | | | 3 | | | | 2 | | | | 2 | | | | 2 | |

Colombia | | | 2 | | | | 2 | | | | 0 | | | | 0 | | | | 0 | |

Shopping centers subtotal | | | 48 | | | | 48 | | | | 29 | | | | 25 | | | | 25 | |

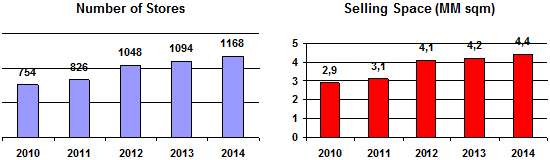

Total | | | 1123 | | | | 1123 | | | | 1076 | | | | 825 | | | | 754 | |

12

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Operating data: | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| Total Selling Space(1) | | (in square meters) | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 546,236 | | | | 546,236 | | | | 524,677 | | | | 463,834 | | | | 406,555 | |

Argentina | | | 519,171 | | | | 519,171 | | | | 522,270 | | | | 502,682 | | | | 455,808 | |

Brazil | | | 602,194 | | | | 596,746 | | | | 552,764 | | | | 391,485 | | | | 332,626 | |

Peru | | | 259,360 | | | | 259,360 | | | | 258,762 | | | | 233,331 | | | | 209,642 | |

Colombia | | | 428,469 | | | | 428,469 | | | | 416,699 | | | | 0 | | | | 0 | |

Supermarkets subtotal | | | 2,386,981 | | | | 2,349,981 | | | | 2,275,172 | | | | 1,591,332 | | | | 1,404,631 | |

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Operating data: | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

Home Improvement Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 307,853 | | | | 307,853 | | | | 299,806 | | | | 276,325 | | | | 273,625 | |

Argentina | | | 373,490 | (2) | | | 373,490 | (2) | | | 369,067 | (2) | | | 391,485 | | | | 392,645 | |

Colombia | | | 75,732 | | | | 75,732 | | | | 37,060 | | | | 35,360 | | | | 34,309 | |

Home improvement stores subtotal | | | 757,074 | | | | 757,074 | | | | 705,933 | | | | 703,170 | | | | 700,579 | |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 371,891 | | | | 371,891 | | | | 377,191 | | | | 272,388 | | | | 234,489 | |

Peru | | | 32,222 | | | | 32,222 | | | | 0 | | | | 0 | | | | 0 | |

Department stores subtotal | | | 404,113 | | | | 404,113 | | | | 377,191 | | | | 272,388 | | | | 234,489 | |

Shopping Centers:(3) | | | | | | | | | | | | | | | | | | | | |

Chile | | | 433,053 | | | | 412,418 | | | | 410,117 | | | | 282,693 | | | | 273,983 | |

Argentina | | | 241,410 | | | | 241,410 | | | | 241,410 | | | | 227,396 | | | | 214,002 | |

Peru | | | 15,514 | | | | 58,388 | | | | 41,303 | | | | 54,750 | | | | 54,750 | |

Colombia | | | 14,514 | | | | 14,514 | | | | 0 | | | | 0 | | | | 0 | |

Shopping centers subtotal | | | 800,272 | | | | 756,264 | | | | 692,830 | | | | 564,839 | | | | 542,735 | |

Total | | | 4,237,899 | | | | 4,237,899 | | | | 4,051,126 | | | | 3,131,729 | | | | 2,882,434 | |

| |

| Average Selling Space per Store(4) | | (in square meters) | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 2,439 | | | | 2,439 | | | | 2,452 | | | | 2,454 | | | | 2,494 | |

Argentina | | | 1,790 | | | | 1,790 | | | | 1,813 | | | | 1,869 | | | | 1,781 | |

Brazil | | | 2,700 | | | | 2,700 | | | | 2,710 | | | | 2,576 | | | | 2,559 | |

Peru | | | 2,981 | | | | 2,981 | | | | 3,009 | | | | 3,153 | | | | 3,276 | |

Colombia | | | 4,285 | | | | 4,285 | | | | 0 | | | | 0 | | | | 0 | |

Supermarkets subtotal | | | 2,549 | | | | 2,549 | | | | 2,562 | | | | 2,327 | | | | 2,291 | |

Home Improvement Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 9,620 | | | | 9,620 | | | | 9,671 | | | | 9,528 | | | | 9,435 | |

Argentina | | | 7,781 | | | | 7,781 | | | | 7,852 | | | | 8,156 | | | | 7,435 | |

Colombia | | | 8,415 | | | | 8,415 | | | | 9,265 | | | | 8,840 | | | | 8,577 | |

Home improvement stores subtotal | | | 8,506 | | | | 8,506 | | | | 8,609 | | | | 8,681 | | | | 8,198 | |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 4,830 | | | | 4,830 | | | | 4,836 | | | | 7,783 | | | | 6,897 | |

Peru | | | 5,370 | | | | 5,370 | | | | 0 | | | | 0 | | | | 0 | |

Department stores subtotal | | | 4,869 | | | | 4,869 | | | | 4,836 | | | | 7,783 | | | | 6,897 | |

Shopping Centers: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 17,322 | | | | 16,497 | | | | 42,987 | | | | 31,410 | | | | 30,443 | |

Argentina | | | 12,796 | | | | 13,412 | | | | 15,761 | | | | 16,243 | | | | 15,286 | |

Peru | | | 17,798 | | | | 19,463 | | | | 16,839 | | | | 27,375 | | | | 27,375 | |

Colombia | | | 7,257 | | | | 7,257 | | | | 0 | | | | 0 | | | | 0 | |

Shopping centers subtotal | | | 15,099 | | | | 15,140 | | | | 25,620 | | | | 22,594 | | | | 21,709 | |

| |

| Average Sales per Store(5) | | (in millions of Ch$) | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 9,894 | | | | 9,943 | | | | 9,617 | | | | 9,662 | | | | 10,371 | |

Argentina | | | 6,254 | | | | 6,162 | | | | 6,083 | | | | 5,776 | | | | 5,352 | |

Brazil | | | 9,837 | | | | 9,067 | | | | 10,270 | | | | 10,211 | | | | 6,484 | |

Peru | | | 9,617 | | | | 8,569 | | | | 8,360 | | | | 8,439 | | | | 8,744 | |

Colombia | | | 9,999 | | | | 9,185 | | | | 1,189 | (6) | | | 0 | | | | 0 | |

Supermarkets subtotal | | | 8,736 | | | | 8,228 | (7) | | | 8,356 | (7) | | | 8,123 | | | | 7,276 | |

13

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Operating data: | | 2013 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of Ch$) | |

Home Improvement Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 14,107 | | | | 14,022 | | | | 12,915 | | | | 12,672 | | | | 11,577 | |

Argentina | | | 13,859 | | | | 14,209 | | | | 13,191 | | | | 11,287 | | | | 9,205 | |

Colombia | | | 6,717 | | | | 9,449 | (8) | | | 10,682 | | | | 9,845 | | | | 8,272 | |

Home improvement stores subtotal | | | 13,179 | | | | 13,858 | | | | 12,964 | | | | 11,712 | | | | 9,998 | |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 12,053 | | | | 12,413 | | | | 11,360 | | | | 19,736 | | | | 18,315 | |

Peru | | | 4,360 | | | | 2,430 | | | | | | | | | | | | | |

Department stores subtotal | | | 11,945 | | | | 11,691 | | | | 11,360 | | | | 19,736 | | | | 18,315 | |

14

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

Operating data: | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | | (in millions of Ch$) | |

Shopping Centers: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 11,284 | | | | 11,284 | | | | 9,309 | | | | 7,167 | | | | 6,095 | |

Argentina | | | 4,620 | | | | 4,620 | | | | 4,365 | | | | 4,262 | | | | 3,810 | |

Peru | | | 4,852 | | | | 4,852 | | | | 2,301 | | | | 2,783 | | | | 4,401 | |

Colombia | | | 8,642 | | | | 8,642 | | | | | | | | | | | | | |

Shopping centers subtotal | | | 7,080 | | | | 7,080 | | | | 5,939 | | | | 5,189 | | | | 4,680 | |

| |

| Increase (Decrease) in Same-Store Sales(9) | | (%) | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 4.3 | % | | | 1.6 | % | | | 4.8 | % | | | 4.7 | % | | | 5.9 | % |

Argentina | | | 29.0 | % | | | 17.3 | % | | | 18.5 | % | | | 22.5 | % | | | 25.2 | % |

Brazil | | | (0.6 | )% | | | (0.5 | )% | | | 0.5 | % | | | 1.4 | % | | | 7.1 | % |

Peru | | | 4.6 | % | | | 1.5 | % | | | 4.2 | % | | | 6.5 | % | | | (2.3 | %) |

Colombia | | | (1.5 | )% | | | (7.4 | )% | | | | | | | | | | | | |

Home Improvement Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 2.7 | % | | | 6.1 | % | | | 6.3 | % | | | 4.9 | % | | | 23.7 | % |

Argentina | | | 27.5 | % | | | 30.3 | % | | | 26.6 | % | | | 32.3 | % | | | 27.8 | % |

Colombia | | | (3.4 | )% | | | 0.3 | % | | | 4.1 | % | | | 11.8 | % | | | (3.6 | %) |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | (0.5 | )% | | | 4.7 | % | | | 5.3 | % | | | 5.2 | % | | | 19.7 | % |

| |

| Sales per Square Meter(10) | | (in millions of Ch$) | |

Supermarkets: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 4.15 | | | | 4.08 | | | | 3.92 | | | | 3.94 | | | | 4.13 | |

Argentina | | | 3.43 | | | | 3.44 | | | | 3.35 | | | | 3.09 | | | | 3.01 | |

Brazil | | | 3.58 | | | | 3.36 | | | | 3.79 | | | | 4.08 | | | | 2.53 | |

Peru | | | 3.20 | | | | 2.87 | | | | 2.78 | | | | 2.68 | | | | 2.67 | |

Colombia | | | 2.35 | | | | 2.14 | | | | 0.28 | (11) | | | | | | | | |

Supermarkets subtotal | | | 3.42 | | | | 3.52 | | | | 3.56 | (12) | | | 3.52 | | | | 3.17 | |

Home Improvement Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 1.48 | | | | 1.46 | | | | 1.34 | | | | 1.33 | | | | 1.23 | |

Argentina | | | 1.81 | | | | 1.83 | | | | 1.68 | | | | 1.38 | | | | 1.24 | |

Colombia | | | 1.04 | (13) | | | 1.04 | (13) | | | 1.15 | | | | 1.11 | | | | 0.96 | |

Home improvement stores subtotal | | | 1.57 | | | | 1.62 | | | | 1.51 | | | | 1.35 | | | | 1.22 | |

Department Stores: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 2.54 | | | | 2.57 | | | | 2.35 | | | | 2.54 | | | | 2.66 | |

Peru | | | 0.10 | | | | 0.45 | | | | 0 | | | | 0 | | | | 0 | |

Department stores subtotal | | | 2.36 | (14) | | | 2.57 | (14) | | | 2.35 | | | | 2.54 | | | | 2.66 | |

Shopping Centers: | | | | | | | | | | | | | | | | | | | | |

Chile | | | 0.28 | | | | 0.26 | | | | 0.22 | | | | 0.23 | | | | 0.20 | |

Argentina | | | 0.24 | | | | 0.29 | | | | 0.28 | | | | 0.26 | | | | 0.25 | |

Peru | | | 0.24 | | | | 0.24 | | | | 0.14 | | | | 0.10 | | | | 0.16 | |

Colombia | | | 0.70 | | | | 0.30 | | | | | | | | | | | | | |

Shopping centers subtotal | | | 0.27 | | | | 0.27 | | | | 0.23 | | | | 0.23 | | | | 0.20 | |

Total number of store employees(15) | | | 153,234 | | | | 154,603 | | | | 146,424 | | | | 131,505 | | | | 126,485 | |

| (1) | In square meters at period end. |

| (2) | Due to change in criteria for selling space 2012 figures were modified in order to have comparable figures for 2012 and subsequent periods. This new criteria excludes check-out area and aisles. |

| (3) | Total leasable space for shopping centers does not include selling space occupied by related parties in our shopping centers. |

| (4) | Total square meters of selling space or leasable space, as applicable, at the fiscal period end divided by the total number of stores or shopping centers, as applicable, at period end. |

| (5) | Sales for the fiscal period divided by the number of stores or shopping centers, as applicable, at the end of the fiscal period. |

| (6) | This value takes into consideration only one month of sales for our supermarket operation in Colombia for the 2012 fiscal period. |

15

| (7) | This average does not include sales and stores of our Colombian supermarket operations. |

| (8) | This value does not take into consideration stores opened in Colombia in the month of December 2013. |

| (9) | Reflects the sales of our stores operating throughout the same months of both financial periods being compared. If a store did not operate for a full month of either of the financial periods being compared, we exclude its sales for such month from both financial periods. For example, if a new store was opened on July 1, 2013 and operated throughout the last six months of 2013, (i) “same-store sales” would include the sales of that store for the last six months of 2013 and the last six months of 2014 and (ii) we would consider the sales of the new store during the first six months of 2014 as sales from a newly opened store. Calculated in local currency. |

| (10) | Sales for the period divided by the square meters of selling space or leasable space, as applicable, at the end of each month during the period. |

| (11) | Data for sales in Colombia only reflect the operational result for the month of December 2012 as the former operations of Carrefour in the country were consolidated into Cencosud’s financial statements as of November 30, 2012. |

| (12) | Average sales per square meter exclude sales and selling space for the Colombian supermarket operations. |

| (13) | Excludes stores opened in December 2013. |

| (14) | Excludes Paris Peru Stores |

| (15) | Number of full-time employee equivalents at period end. |

Exchange Rates

Chile

Chile has two currency markets, theMercado Cambiario Formal (the “Formal Exchange Market”) and theMercado Cambiario Informal (the “Informal Exchange Market”). The Formal Exchange Market is comprised of banks and other entities authorized by the Chilean Central Bank. The Informal Exchange Market is comprised of entities that are not expressly authorized to operate in the Formal Exchange Market, such as certain foreign exchange houses and travel agencies, among others. The Chilean Central Bank is empowered to require that certain purchases and sales of foreign currencies be carried out on the Formal Exchange Market. See also “Item 10. Additional Information—D. Exchange Controls—Foreign Exchange Controls—Chile.”

Both the Formal and Informal Exchange Markets are driven by free market forces. Current regulations require that the Chilean Central Bank be informed of certain transactions and that they be effected through the Formal Exchange Market.

The U.S. dollar observed exchange rate (dólar observado), which is reported by the Chilean Central Bank and published daily in the Official Gazette (Diario Oficial), is the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. The Chilean Central Bank has the power to intervene by buying or selling foreign currency on the Formal Exchange Market to attempt to maintain the observed exchange rate within a desired range. During the past few years the Chilean Central Bank has attempted to keep the observed exchange rate within a certain range only under special circumstances. Although the Chilean Central Bank is not required to purchase or sell dollars at any specific exchange rate, it generally uses spot rates for its transactions. Other banks generally carry out authorized transactions at spot rates as well.

The Informal Exchange Market reflects transactions carried out at an informal exchange rate (the “informal exchange rate”). There are no limits imposed on the extent to which the rate of exchange in the Informal Exchange Market can fluctuate above or below the observed exchange rate. In recent years, the variation between the observed exchange rate and the informal exchange rate has not been significant.

The following table sets forth the annual low, high, average and period end observed exchange rate for U.S. dollars for the periods presented, as reported by the Chilean Central Bank. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

| | | | | | | | | | | | | | | | |

| | | Daily observed exchange rate Ch$ per U.S.$ | |

| | | High(1) | | | Low(1) | | | Average(2) | | | Period end(3) | |

Year ended December 31, | | | | | | | | | | | | | | | | |

2010 | | | 549.17 | | | | 468.01 | | | | 510.21 | | | | 468.01 | |

2011 | | | 533.74 | | | | 455.91 | | | | 483.57 | | | | 519.20 | |

2012 | | | 519.69 | | | | 469.65 | | | | 486.59 | | | | 479.96 | |

2013 | | | 533.95 | | | | 466.50 | | | | 495.18 | | | | 524.61 | |

2014 | | | 621.41 | | | | 527.53 | | | | 570.33 | | | | 606.75 | |

Month end | | | | | | | | | | | | | | | | |

October 31, 2014 | | | 598.64 | | | | 527.53 | | | | 538.36 | | | | 553.84 | |

November 30, 2014 | | | 605.46 | | | | 580.62 | | | | 593.91 | | | | 605.46 | |

16

| | | | | | | | | | | | | | | | |

| | | Daily observed exchange rate Ch$ per U.S.$ | |

| | | High(1) | | | Low(1) | | | Average(2) | | | Period end(3) | |

December 31, 2014 | | | 621.41 | | | | 606.75 | | | | 612.98 | | | | 606.75 | |

January 31, 2015 | | | 632.03 | | | | 612.47 | | | | 622.11 | | | | 632.03 | |