| REPORT TO SHAREHOLDERS |  | ||

| Second Quarter 2019 | |||

| MANAGEMENT'S DISCUSSION AND ANALYSIS | |||

| Table of Contents | |||

Basis of Presentation

The following Management's Discussion and Analysis ("MD&A") of the financial and operating results of Pembina Pipeline Corporation ("Pembina" or the "Company") is dated August 1, 2019, and is supplementary to, and should be read in conjunction with, Pembina's June 30, 2019 condensed consolidated interim financial statements ("Interim Financial Statements") as well as Pembina's consolidated annual financial statements ("Consolidated Financial Statements") and MD&A for the year ended December 31, 2018. All financial information has been prepared in accordance with IAS 34 Interim Financial Reporting and is expressed in Canadian dollars unless otherwise noted. Pembina adopted IFRS 16 Leases ("IFRS 16") effective January 1, 2019 using the modified retrospective approach; accordingly comparative information has not been restated. A description of Pembina's operating segments and additional information about Pembina is filed with Canadian and U.S. securities commissions, including quarterly and annual reports, annual information forms (filed with the U.S. Securities and Exchange Commission under Form 40-F), and management information circulars, can be found online at www.sedar.com, www.sec.gov and through Pembina's website at www.pembina.com.

Abbreviations

For a list of abbreviations that may be used in this MD&A, refer to the Abbreviations section of this MD&A.

Non-GAAP Financial Measures

Pembina has identified certain operating and financial performance measures that management believes provide meaningful information in assessing Pembina's underlying performance. Readers are cautioned that these measures do not have a standardized meaning prescribed by International Financial Reporting Standards ("IFRS") and therefore may not be comparable to similar measures presented by other entities. Refer to the Non-GAAP Measures section of this MD&A for a list and description, including reconciliations to the most directly comparable GAAP measure, of such non-GAAP measures.

Risk Factors and Forward-Looking Information

Management has identified the primary risk factors that could potentially have a material impact on the financial results and operations of Pembina. Such risk factors are presented in Pembina's MD&A and Annual Information Form ("AIF") for the year ended December 31, 2018. The Company’s financial and operational performance is potentially affected by a number of factors, including, but not limited to, the factors described within the Forward-Looking Statements & Information section of this MD&A. This MD&A contains forward-looking statements based on Pembina’s current expectations, estimates, projections and assumptions. This information is provided to assist readers in understanding the Company’s future plans and expectations and may not be appropriate for other purposes.

Pembina Pipeline Corporation Second Quarter 2019 1

1. ABOUT PEMBINA

Calgary-based Pembina Pipeline Corporation is a leading transportation and midstream service provider that has been serving North America's energy industry for 65 years. Pembina owns an integrated system of pipelines that transport various hydrocarbon liquids and natural gas products produced primarily in western Canada. The Company also owns gas gathering and processing facilities; an oil and natural gas liquids infrastructure and logistics business; is growing an export terminals business; and is currently constructing a petrochemical facility to convert propane into polypropylene. Pembina's integrated assets and commercial operations along the majority of the hydrocarbon value chain allow it to offer a full spectrum of midstream and marketing services to the energy sector. Pembina is committed to identifying additional opportunities to connect hydrocarbon production to new demand locations through the development of infrastructure that would extend Pembina's service offering even further along the hydrocarbon value chain. These new developments will contribute to ensuring that hydrocarbons produced in the Western Canadian Sedimentary Basin and the other basins where Pembina operates can reach the highest value markets throughout the world.

Purpose of Pembina:

To be the leader in delivering integrated infrastructure solutions connecting global markets;

| • | Customers choose us first for reliable and value-added services; |

| • | Investors receive sustainable industry-leading total returns; |

| • | Employees say we are the 'employer of choice' and value our safe, respectful, collaborative and fair work culture; and |

| • | Communities welcome us and recognize the net positive impact of our social and environmental commitment. |

2 Pembina Pipeline Corporation Second Quarter 2019

2. FINANCIAL & OPERATING OVERVIEW

Consolidated Financial Overview Three Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Revenue(3) | 1,808 | 1,743 | 65 | 4 | ||||

Net revenue(1) | 758 | 669 | 89 | 13 | ||||

| Gross profit | 629 | 511 | 118 | 23 | ||||

| Earnings | 664 | 246 | 418 | 170 | ||||

Earnings per common share – basic (dollars) | 1.23 | 0.43 | 0.80 | 186 | ||||

Earnings per common share – diluted (dollars) | 1.23 | 0.42 | 0.81 | 193 | ||||

| Cash flow from operating activities | 661 | 603 | 58 | 10 | ||||

Cash flow from operating activities per common share – basic (dollars)(1) | 1.29 | 1.20 | 0.09 | 8 | ||||

Adjusted cash flow from operating activities(1) | 550 | 558 | (8 | ) | (1 | ) | ||

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | 1.08 | 1.11 | (0.03 | ) | (3 | ) | ||

| Capital expenditures | 434 | 255 | 179 | 70 | ||||

Adjusted EBITDA(1) | 765 | 700 | 65 | 9 | ||||

Total volume (mboe/d)(2) | 3,384 | 3,385 | (1 | ) | — | |||

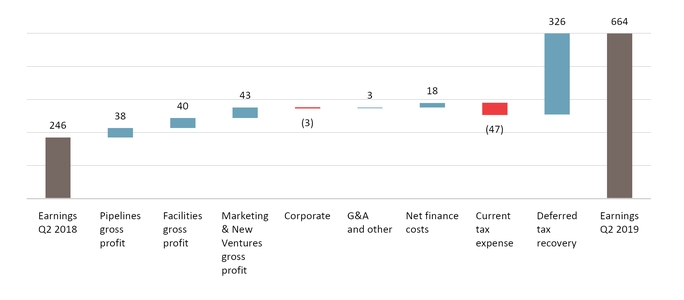

Bridge Analysis of Earnings ($ millions)

Results Overview

Earnings in the second quarter of 2019 were positively impacted by a deferred tax recovery related to the enactment of Bill 3 Job Creation Tax Cut (Alberta Corporate Tax Amendment) Act ("Bill 3"), which will reduce the Alberta tax rate from 12 percent to eight percent over a four year period. Gross profit from all three divisions increased following new assets placed into service, the recognition of variable revenue related to capital recoveries in the current period as well as deferred variable revenue from the prior period, higher terminalling revenue, combined with gains from commodity-related derivative contracts. Net finance costs decreased due to a loss related to the convertible debentures in the second quarter of 2018. An increase in current tax expense partially offset the significant deferred tax recovery.

Pembina Pipeline Corporation Second Quarter 2019 3

| Changes in Results for the Three Months Ended June 30 | ||

Revenue(3) | ▲ | $65 million increase, primarily driven by revenue associated with new Peace Phase IV and V assets, Redwater Co-generation and Burstall Ethane Storage all recently placed into service (see Projects and New Developments sections), increased terminalling revenue at Redwater for propane and butane, the recognition of variable revenue related to current and prior period capital recoveries ($22 million) and increased recovery of operating expenses. |

| Operating expenses | ▼ | $34 million increase due mainly to a $30 million recovery reclassification in the second quarter of 2018 related to the first quarter of 2018 which decreased operating expenses and increased cost of sales, combined with an increase in power costs ($6 million) as a result of higher consumption from new assets placed into service partially offset by savings associated with Redwater Co-generation, offset by lower repairs and maintenance ($3 million). |

| Share of profit from equity accounted investees | ● | Consistent with prior period. |

| Realized gain on commodity-related derivatives | ▲ | $10 million increase as derivatives moved to a gain position as contracts were settled during the period at prices that were higher than the contracted price, compared to losses that were realized during the second quarter of 2018. |

| Unrealized gain on commodity-related derivatives | ▲ | $61 million positive variance primarily due to decreases in the price of propane and butane which drove the associated derivative contracts into a gain position, compared to the loss position in the second quarter of 2018 when prices were higher. |

| General & administrative and other expense | ▲ | $12 million decrease mainly due to a decrease in long-term incentives. |

| Net finance costs | ▲ | $18 million decrease due to the loss on revaluation of the conversion feature of the convertible debentures recognized in the prior period and since matured, combined with the impact of foreign exchange gains and partially offset by the additional interest expense recognized on the adoption of IFRS 16 of $4 million. |

| Current tax expense | ▼ | $47 million increase is primarily due to the growth in earnings in the prior year that are recognized in taxable income in the current year. |

| Deferred tax recovery | ▲ | $326 million increase in deferred tax recovery primarily due to the enactment of Bill 3, which will reduce the Alberta tax rate from 12 percent to 8 percent over a four year period. |

| Earnings | ▲ | $418 million increase compared to the second quarter of 2018 driven by the items noted above. |

| Cash flow from operating activities | ▲ | $58 million increase, primarily driven by an increase in operating results after adjusting for non-cash items, $43 million change in non-cash working capital and the $12 million impact from the adoption of IFRS 16, partially offset by the $28 million decrease in distributions from equity accounted investees. |

Adjusted cash flow from operating activities(1) | ▼ | $8 million decrease largely due to the same items impacting cash flow from operating activities, discussed above, net of the $43 million change in non-cash working capital and $47 million increase in current tax expense. |

Adjusted EBITDA(1) | ▲ | $65 million increase primarily due to the contribution from new assets placed into service, combined with the recognition of variable revenue related to capital recoveries, increased terminalling and storage revenues and the $18 million impact from the adoption of IFRS 16. Included in adjusted EBITDA is $200 million (2018: $212 million) related to equity accounted investees. |

Total volume (mboe/d)(2) | ● | Consistent with prior period. Revenue volumes includes 316 mboe/d (2018: 311 mboe/d) related to equity accounted investees. |

| ▲ | Increase; | ▼ | Decrease; or | ● | No impact; | to earnings, adjusted EBITDA, cash flow from operations, adjusted cash flow from operating activities or total volumes. |

(1) | Refer to "Non-GAAP Measures". |

(2) | Total revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

(3) | Pembina corrected revenue and costs of goods sold in the Marketing & New Ventures Division in 2018. The adjustments reduce revenue and cost of goods sold for the three and six months ending June 30, 2018 ($202 million). There was no impact to earnings as a result of the adjustment. |

4 Pembina Pipeline Corporation Second Quarter 2019

Consolidated Financial Overview Six Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | |||

Revenue(3) | 3,776 | 3,580 | 196 | 5 | |||

Net revenue(1) | 1,532 | 1,388 | 144 | 10 | |||

| Gross profit | 1,217 | 1,079 | 138 | 13 | |||

| Earnings | 977 | 576 | 401 | 70 | |||

Earnings per common share – basic (dollars) | 1.79 | 1.02 | 0.77 | 75 | |||

Earnings per common share – diluted (dollars) | 1.78 | 1.02 | 0.76 | 75 | |||

| Cash flow from operating activities | 1,269 | 1,101 | 168 | 15 | |||

Cash flow from operating activities per common share – basic (dollars)(1) | 2.49 | 2.19 | 0.30 | 14 | |||

Adjusted cash flow from operating activities(1) | 1,128 | 1,088 | 40 | 4 | |||

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | 2.21 | 2.16 | 0.05 | 2 | |||

| Capital expenditures | 795 | 579 | 216 | 37 | |||

Adjusted EBITDA(1) | 1,538 | 1,388 | 150 | 11 | |||

Total volume (mboe/d)(2) | 3,394 | 3,333 | 61 | 2 | |||

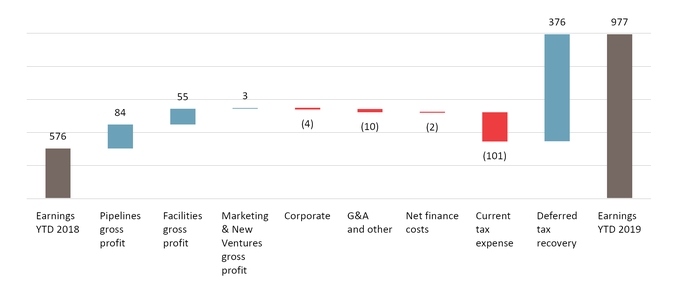

Bridge Analysis of Earnings ($ millions)

Results Overview

Earnings for the six months ended June 30, 2019 were positively impacted by the deferred tax recovery related to the enactment of Bill 3, noted above. Gross profit increased in both the Pipeline and Facilities divisions from new assets placed into service, the recognition of variable revenue related to capital recoveries in the current period as well as deferred variable revenue from the prior period, higher terminalling revenue, as well as additional customer commitments on existing assets. G&A and other expenses increased following the adoption of IFRS 16 which resulted in higher depreciation included in general and administrative expense and a corresponding reduction in rent expense, which was offset by increased salaries and wages.

Pembina Pipeline Corporation Second Quarter 2019 5

| Changes in Results for the Six Months Ended June 30 | ||

Revenue(3) | ▲ | $196 million increase, primarily driven by revenue associated with new assets recently placed into service (see Projects and New Developments sections), increased terminalling revenue, increased NGL sales volumes, a $33 million contract dispute settlement, the recognition of $22 million of variable revenue related to current and prior period capital recoveries and increased recovery of operating expenses. |

| Operating expenses | ▼ | $24 million increase largely due to increases in power costs, as a result of both increased power pool prices and higher consumption from new assets placed into service. |

| Share of profit from equity accounted investees | ▲ | $21 million increase primarily due to increased revenues from Veresen Midstream following the North Central Liquids Hub going into service in June 2018, combined with the impact of a $24 million finance gain reversal recorded in the first half of 2018, partially offset by lower margins at Aux Sable. |

| Realized gain on commodity-related derivatives | ▲ | $47 million increase due to the recognition of a gain for commodity-related derivatives that were settled during the period at prices that were higher than contracted, compared to the losses that were realized during the first quarter of 2018. |

| Unrealized loss on commodity-related derivatives | ▼ | $14 million negative variance primarily due to crude storage contracts which expired and were realized during the period. |

| General & administrative and other expense | ● | Consistent with prior period. |

| Net finance costs | ● | Consistent with prior period as $9 million in additional interest expense recognized on the adoption of IFRS 16 largely offset lower losses in fair value of non-commodity-related derivatives. |

| Current tax expense | ▼ | $101 million increase is primarily due to the growth in earnings in the prior year that are recognized in taxable income in the current year. |

| Deferred tax recovery | ▲ | $376 million increase in deferred tax recovery primarily due to the enactment of Bill 3, which will reduce the Alberta tax rate from 12 percent to 8 percent over a four year period. |

| Earnings | ▲ | $401 million increase compared to the first six months of 2018 driven by the items noted above. |

| Cash flow from operating activities | ▲ | $168 million increase, primarily driven by increase in operating results after adjusting for non-cash items, $114 million change in non-cash working capital, $16 million increase in distributions from equity accounted investees, combined with the $27 million impact from the adoption of IFRS 16, offset by $63 million increase in taxes paid. |

Adjusted cash flow from operating activities(1) | ▲ | $40 million increase largely due to the same items impacting cash flow from operating activities, discussed above, net of the $114 million change in non-cash working capital. |

Adjusted EBITDA(1) | ▲ | $150 million increase primarily due to the contribution from new assets placed into service, combined with the impact from the realized gain on commodity-related derivatives, the recognition of variable revenues related to capital recoveries, increased terminalling and storage revenues and $33 million impact from the adoption of IFRS 16. Included in adjusted EBITDA is $420 million (2018: $403 million) related to equity accounted investees. |

Total volume (mboe/d)(2) | ▲ | 61 mboe/d increase due to new assets placed into service, increased demand in the Montney and Duvernay, partially offset by lower take-or-pay commitments on the Nipisi and Mitsue systems. Revenue volumes includes 323 mboe/d (2018: 304 mboe/d) related to equity accounted investees. |

| ▲ | Increase; | ▼ | Decrease; or | ● | No impact; | to earnings, adjusted EBITDA, cash flow from operations, adjusted cash flow from operating activities or total volumes. |

(1) | Refer to "Non-GAAP Measures". |

(2) | Total revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

(3) | Pembina corrected revenue and costs of goods sold in the Marketing & New Ventures Division. The adjustments reduce revenue and cost of goods sold for the three and six months ending June 30, 2018 ($202 million). There was no impact to earnings as a result of the adjustment. |

6 Pembina Pipeline Corporation Second Quarter 2019

3. SEGMENT RESULTS

Business Overview

The Pipelines Division includes liquids and natural gas pipelines with a total capacity of approximately three million barrels of oil equivalent per day serving various markets and basins across North America. The Pipelines Division is comprised of Pembina's conventional, transmission and oil sands and heavy oil pipeline assets. The primary objectives of the Pipelines Division are to provide safe, responsible, reliable and cost-effective transportation services for customers; connect customer products to premium markets; pursue opportunities for increased throughput that enhances the return on invested capital; and follow a disciplined approach to operating expenses.

The Facilities Division includes infrastructure that provides Pembina's customers with natural gas, condensate and NGL services. Pembina's natural gas gathering and processing assets are strategically positioned in active, liquids-rich areas of the Western Canadian Sedimentary Basin and are integrated with the Company's other businesses. Pembina provides sweet and sour gas gathering, compression, condensate stabilization, and both shallow cut and deep cut gas processing services with a total capacity of approximately six billion cubic feet per day for its customers. Virtually all of the condensate and NGL extracted through these facilities is transported by Pembina's Pipelines Division. The Facilities Division includes approximately 356 thousand barrels per day of NGL fractionation, 14.3 million barrels of cavern storage, and associated terminalling facilities and the Company is currently constructing a LPG export facility on Canada's West Coast. These facilities are fully integrated with the Company’s other divisions, providing customers with the ability to access a comprehensive suite of services to enhance the value of their hydrocarbons.

The Marketing & New Ventures Division strives to maximize the value of hydrocarbon liquids and natural gas originating in the basins where the Company operates. Pembina seeks to create new markets, and further enhance existing markets, to support both the Company's and its customers' overall business interests. In particular, Pembina seeks to identify opportunities to connect hydrocarbon production to new demand locations through the development of infrastructure. Pembina strives to increase producer netbacks and product demand to improve the overall competitiveness of the basins where the Company operates. Within the Marketing & New Ventures Division, Pembina undertakes value-added commodity marketing activities including buying and selling products (natural gas, ethane, propane, butane, condensate and crude oil), commodity arbitrage, and optimizing storage opportunities. The marketing business enters into contracts for capacity on both Pembina's and third-party infrastructure, handles proprietary and customer volumes and aggregates production for onward sale. The Marketing & New Ventures Division currently includes an integrated propane dehydrogenation plant and polypropylene upgrading facility ("PDH/PP Facility"), being constructed by Pembina’s joint venture, Canada Kuwait Petrochemical Corporation ("CKPC"); and the proposed Jordan Cove LNG project.

Financial and Operational Overview by Division

| 3 Months Ended June 30 | 6 Months Ended June 30 | |||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||

| ($ millions, except where noted)(unaudited) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | ||||||||||||

| Pipelines Division | 2,518 | 360 | 472 | 2,536 | 322 | 435 | 2,513 | 700 | 929 | 2,479 | 616 | 837 | ||||||||||||

| Facilities Division | 866 | 167 | 236 | 849 | 127 | 212 | 881 | 325 | 468 | 854 | 270 | 429 | ||||||||||||

Marketing & New Ventures Division(3) | — | 100 | 97 | — | 57 | 97 | — | 193 | 218 | — | 190 | 202 | ||||||||||||

| Corporate | — | 2 | (40 | ) | — | 5 | (44 | ) | — | (1 | ) | (77 | ) | — | 3 | (80 | ) | |||||||

| Total | 3,384 | 629 | 765 | 3,385 | 511 | 700 | 3,394 | 1,217 | 1,538 | 3,333 | 1,079 | 1,388 | ||||||||||||

(1) | Pipelines and Facilities divisions are revenue volumes which are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

(2) | Refer to "Non-GAAP Measures". |

(3) | Marketed NGL volumes are excluded from volumes to avoid double counting. Refer to the "Marketing & New Ventures Division" section for further information. |

Pembina Pipeline Corporation Second Quarter 2019 7

Pipelines Division

Financial Overview Three Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Conventional Pipelines revenue(1) | 319 | 306 | 13 | 4 | ||||

Transmission Pipelines revenue(1) | 39 | 38 | 1 | 3 | ||||

Oil Sands Pipelines revenue(1) | 85 | 60 | 25 | 42 | ||||

Pipelines revenue(1) | 443 | 404 | 39 | 10 | ||||

Operating expenses(1) | 92 | 92 | — | — | ||||

| Share of profit from equity accounted investees | 67 | 65 | 2 | 3 | ||||

| Depreciation and amortization included in operations | 58 | 55 | 3 | 5 | ||||

| Gross profit | 360 | 322 | 38 | 12 | ||||

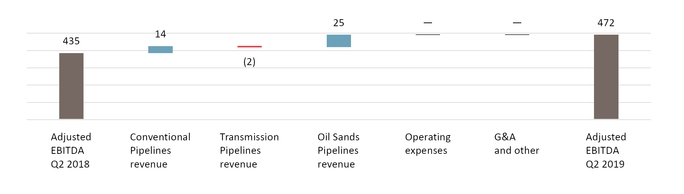

Adjusted EBITDA(2) | 472 | 435 | 37 | 9 | ||||

Volumes (mboe/d)(3) | 2,518 | 2,536 | (18 | ) | (1 | ) | ||

| Distributions from equity accounted investees | 100 | 104 | (4 | ) | (4 | ) | ||

| Change in Results | ||

Conventional Pipelines revenue(1) | ▲ | Increase due to revenues associated with Phase IV and V assets placed into service in December 2018 and higher recovery of operating expenses due to increased power costs and geotechnical spending, partially offset by lower revenues from the Western system as a result of lower capital recoveries. |

Transmission Pipelines revenue(1) | ● | Consistent with prior period. |

Oil Sands Pipelines revenue(1) | ▲ | Increase primarily due to the recognition of $16 million of deferred variable revenue related to prior period capital recoveries, combined with $6 million in increased variable revenue related to 2019 capital recoveries and higher recovery of operating expenses due to increased power pool prices and integrity work. |

Operating expenses(1) | ● | Consistent with prior period, increase in power consumption from Phase IV and V being placed into service, combined with higher repairs and maintenance costs, were largely offset by savings associated with taking over operatorship of Alberta Ethane Gathering System ("AEGS"). |

| Share of profit from equity accounted investees | ● | Consistent with prior period. |

| Depreciation and amortization included in operations | ▼ | Increase in depreciation due to larger asset base as Pembina continued to expand its conventional pipeline system, placing Phase IV and V assets into service during December 2018. |

| Distributions from equity accounted investees | ▼ | $100 million consists of $69 million (2018: $74 million) from Alliance and $30 million (2018: $30 million) from Ruby. |

Volumes (mboe/d)(3) | ▼ | Decrease in revenue volumes driven by lower take-or-pay commitment on the Nipisi and Mitsue systems, combined with a third party refinery outage that impacted the Western system, partially offset by the conventional Phase IV and V assets placed into service in December 2018. Revenue volumes includes 141 mboe/d (2018: 146 mboe/d) related to Alliance and 89 mboe/d (2018: 89 mboe/d) related to Ruby. |

Adjusted EBITDA(2) | ▲ | $37 million increase primarily due to the increase in revenues for the oil sands and conventional pipelines assets, both explained above. Included in adjusted EBITDA is $81 million (2018: $85 million) related to Alliance and $48 million (2018: $44 million) related to Ruby. |

Bridge Analysis of Adjusted EBITDA(2) ($ millions)

(1) | Includes inter-division transactions. See note 12 of the Interim Financial Statements. |

(2) | Refer to "Non-GAAP Measures". |

(3) | Revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

8 Pembina Pipeline Corporation Second Quarter 2019

Financial Overview Six Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | |||

Conventional Pipelines revenue(1) | 633 | 563 | 70 | 12 | |||

Transmission Pipelines revenue(1) | 79 | 74 | 5 | 7 | |||

Oil Sands Pipelines revenue(1) | 147 | 120 | 27 | 23 | |||

Total revenue(1) | 859 | 757 | 102 | 13 | |||

Operating expenses(1) | 190 | 177 | 13 | 7 | |||

| Share of profit from equity accounted investees | 146 | 140 | 6 | 4 | |||

| Depreciation and amortization included in operations | 115 | 104 | 11 | 11 | |||

| Gross profit | 700 | 616 | 84 | 14 | |||

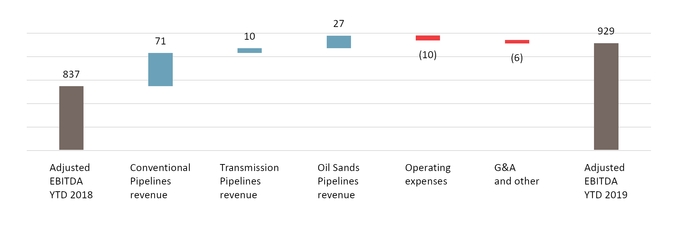

Adjusted EBITDA(2) | 929 | 837 | 92 | 11 | |||

Volumes (mboe/d)(3) | 2,513 | 2,479 | 34 | 1 | |||

| Distributions from equity accounted investees | 211 | 194 | 17 | 9 | |||

| Change in Results | ||

Conventional Pipelines revenue(1) | ▲ | Increase due to revenues associated with Phase IV and V assets placed into service in December 2018 and higher recovery of operating expenses due to increased power costs and geotechnical spending. |

Transmission Pipelines revenue(1) | ▲ | Increase due to higher average tolls on AEGS, combined with a favourable foreign exchange impact. |

Oil Sands Pipelines revenue(1) | ▲ | Increase primarily due to the recognition of $16 million of deferred variable revenue related to prior period capital recoveries, combined with $6 million in increased variable revenue related to 2019 capital recoveries and higher recovery of operating expenses due to increased power pool prices and integrity work. |

Operating expenses(1) | ▼ | Increase primarily due to increased power pool prices and increased power consumption from Phase IV and V being placed into service, combined with higher geotechnical spending for slope mitigation and increased labour costs. |

| Share of profit from equity accounted investees | ▲ | Increase due to higher revenue from Alliance and Ruby driven by favourable foreign exchange rates, combined with operating expense savings associated with transitioning to an owner-operator model for Alliance. |

| Depreciation and amortization included in operations | ▼ | Increase in depreciation due to larger asset base as Pembina placed Phase IV and V assets into service during December 2018. |

| Distributions from equity accounted investees | ▲ | $211 million consists of $150 million (2018: $135 million) from Alliance and $60 million (2018: $59 million) from Ruby. |

Volumes (mboe/d)(3) | ▲ | Increase primarily due to conventional Phase IV and V assets placed into service in December 2018, partially offset by lower take-or-pay commitment on the Nipisi and Mitsue systems and the force majeure impacting the Vantage system. Revenue volumes includes 145 mboe/d (2018: 144 mboe/d) related to Alliance and 89 mboe/d (2018: 89 mboe/d) related to Ruby. |

Adjusted EBITDA(2) | ▲ | $92 million increase primarily due to the increase in revenues for the Conventional and Oil Sands pipelines assets partially offset by the increase in operating expenses, explained above. Included in adjusted EBITDA is $176 million (2018: $175 million) related to Alliance and $101 million (2018: $91 million) related to Ruby. |

Bridge Analysis of Adjusted EBITDA(2) ($ millions)

(1) | Includes inter-division transactions. See note 12 of the condensed consolidated Interim Financial Statements. |

(2) | Refer to "Non-GAAP Measures". |

(3) | Revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

Pembina Pipeline Corporation Second Quarter 2019 9

Operational Overview

| 3 Months Ended June 30 | 6 Months Ended June 30 | |||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||

| ($ millions, except where noted)(unaudited) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | ||||||||||||

| Pipelines Division | ||||||||||||||||||||||||

| Conventional Pipelines | 895 | 217 | 252 | 900 | 210 | 241 | 888 | 425 | 492 | 833 | 378 | 440 | ||||||||||||

| Transmission Pipelines | 558 | 89 | 160 | 559 | 79 | 156 | 561 | 194 | 343 | 571 | 174 | 321 | ||||||||||||

| Oil Sands Pipelines | 1,065 | 54 | 60 | 1,077 | 33 | 38 | 1,065 | 81 | 94 | 1,075 | 64 | 76 | ||||||||||||

| Total | 2,518 | 360 | 472 | 2,536 | 322 | 435 | 2,513 | 700 | 929 | 2,479 | 616 | 837 | ||||||||||||

(1) | Revenue volumes. Revenue volumes are physical plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d. |

(2) | Refer to "Non-GAAP Measures". |

Projects & New Developments

The Pipelines Division continues to focus on the execution of various system expansions. The projects in the following table were recently placed into service and impact the Pipelines Division results.

Significant Projects(1) | In-service Date |

| Phase V Peace Pipeline Expansion | December 2018 |

| Phase IV Peace Pipeline Expansion | December 2018 |

The Pipeline Division has continued to receive strong customer demand for its transportation services, resulting in a significant and on-going build-out of its pipeline system. Collectively, the Pipeline Division projects are trending on budget.

The following outlines the projects currently underway and new developments within the Pipelines Division:

| Phase VI Peace Pipeline Expansion | ||

Capital Budget: $280 million | In-service Date: In stages starting late 2019 through mid 2020 | Status: On time, trending over budget |

| This expansion includes upgrades at Gordondale, Alberta; a 16-inch pipeline from La Glace to Wapiti, Alberta and associated pump station and terminal upgrades; and a 20-inch pipeline from Kakwa to Lator, Alberta. Detailed engineering for one section is complete with construction underway. | ||

| Phase VII Peace Pipeline Expansion | ||

Capital Budget: $950 million | In-service Date(2): First half of 2021 | Status: On time, trending under budget |

| This expansion is expected to add approximately 240 mbpd of incremental capacity upstream of Fox Creek, accessing capacity available on the pipelines downstream of Fox Creek. Included in the expansion is a new 20-inch, approximately 220-kilometer pipeline in the La Glace-Valleyview-Fox Creek corridor, as well as six new pump stations or terminal upgrades, between La Glace and Edmonton, Alberta. Front End Engineering Design ("FEED") is progressing as planned with construction expected to begin in the fourth quarter of 2019. | ||

| Phase VIII Peace Pipeline Expansion | ||

Capital Budget: $500 million | In-service Date(2): In stages starting in 2020 through the first half of 2022 | Status: On time, trending on budget |

| This expansion will include new 10-inch and 16-inch pipelines in the Gordondale to La Glace corridor as well as six new pump stations or terminal upgrades located between Gordondale and Fox Creek, Alberta. Pre-FEED and FEED work is expected to be completed in the fourth quarter of 2019. | ||

| NEBC Montney Infrastructure | ||

Capital Budget: Not disclosed separately(3) | In-service Date: Third quarter 2019 | Status: On time, trending on budget |

| This infrastructure includes producer tie-in connections to Pembina's Birch Terminal as well as upgrades to the terminal including additional storage and pumps, along with minor site modifications. Construction on the new facilities and associated lateral is in advanced stages. | ||

| Wapiti Condensate Lateral | ||

Capital Budget: Not disclosed separately(3) | In-service Date: Fourth quarter 2019 | Status: On time, trending on budget |

| This is a 12-inch lateral, which will connect growing condensate volumes from a third-party owned facility in the Pipestone Montney region into Pembina's Peace Pipeline. All early works construction has been completed. | ||

(1) | For further details on the Company's significant assets, refer to the Pembina's AIF filed at www.sedar.com (filed with the U.S. Securities and Exchange Commission at www.sec.gov under Form 40-F) and on Pembina's website at www.pembina.com. |

(2) | Subject to environmental and regulatory approvals. See "Forward-Looking Statements". |

(3) | Combined capital budget is $120 million. |

10 Pembina Pipeline Corporation Second Quarter 2019

Facilities Division

Financial Overview Three Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Gas Services net revenue(1)(2)(3) | 140 | 136 | 4 | 3 | ||||

NGL Services net revenue(1)(2)(3) | 134 | 113 | 21 | 19 | ||||

Facilities net revenue(1)(2)(3) | 274 | 249 | 25 | 10 | ||||

Operating expenses(1) | 82 | 85 | (3 | ) | (4 | ) | ||

| Share of profit from equity accounted investees | 12 | 1 | 11 | 1,100 | ||||

| Depreciation and amortization included in operations | 37 | 38 | (1 | ) | (3 | ) | ||

| Gross profit | 167 | 127 | 40 | 31 | ||||

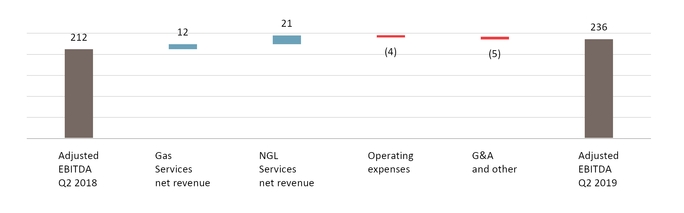

Adjusted EBITDA(3) | 236 | 212 | 24 | 11 | ||||

Volumes (mboe/d)(4) | 866 | 849 | 17 | 2 | ||||

| Distributions from equity accounted investees | 23 | 41 | (18 | ) | (44 | ) | ||

| Changes in Results | ||

Gas Services net revenue(1)(2)(3) | ▲ | Increase is largely attributable to increased operating expense recoveries as a result of higher power costs combined with additional volumes at the Saturn and Kakwa River plants. |

NGL Services net revenue(1)(2)(3) | ▲ | Increase primarily due to Redwater Co-generation and Burstall Ethane Storage going into service March 2019 and January 2019, respectively, combined with increased terminalling revenues at Redwater for propane and butane. |

Operating expenses(1) | ▲ | Decrease caused by reduction in power costs following Redwater Co-generation going into service in March 2019 and lower repairs and maintenance, partially offset by higher power consumption following Burstall Ethane Storage going into service. |

| Share of profit from equity accounted investees | ▲ | Increase is largely the result of increased volumes at Veresen Midstream due in part to the North Central Liquids Hub being placed into service in June 2018, combined with the impact of a $16 million finance gain reversal recorded during the second quarter of 2018. |

| Depreciation and amortization included in operations | ● | Consistent with prior period. |

| Distributions from equity accounted investees | ▼ | $23 million consists of $23 million (2018: $38 million) from Veresen Midstream and $nil (2018: $3 million) from Fort Corp. The decrease in Veresen Midstream distribution is primarily due to refinancing of the debt facility and associated amortization, combined with the conversion of Veresen Midstream Class B Units to Class A Units by Pembina’s joint venture partner, reducing Pembina’s distribution to its ownership percentage and eliminated further dilution of Pembina’s ownership in Veresen Midstream. |

Volumes (mboe/d)(4) | ▲ | Increased revenue volumes primarily due to additional volumes at Veresen Midstream due in part to the North Central Liquids Hub being placed into service in June 2018, increased demand in the Montney and Duvernay plays, combined with consistent volumes at Redwater. Revenue volumes includes 86 mboe/d (2018: 76 mboe/d) related to Veresen Midstream. |

Adjusted EBITDA(3) | ▲ | $24 million increase primarily due to strong NGL Services net revenues and other items, explained above. Included in adjusted EBITDA is $43 million (2018: $44 million) related to Veresen Midstream. |

Bridge Analysis of Adjusted EBITDA(3) ($ millions)

(1) | Includes inter-division transactions. See note 12 of the Interim Financial Statements. |

(2) | Revenue and cost of goods sold reported for all 2018 periods have been restated to reflect updated presentation for 2019, where the majority of cost of goods sold and corresponding revenues are reported in the Marketing & New Ventures Division. |

(3) | Refer to "Non-GAAP Measures". |

(4) | Revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

Pembina Pipeline Corporation Second Quarter 2019 11

Financial Overview Six Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Gas Services net revenue(1)(2)(3) | 285 | 274 | 11 | 4 | ||||

NGL Services net revenue(1)(2)(3) | 259 | 223 | 36 | 16 | ||||

Facilities net revenue(1)(2)(3) | 544 | 497 | 47 | 9 | ||||

Operating expenses(1) | 167 | 150 | 17 | 11 | ||||

| Share of profit from equity accounted investees | 24 | (4 | ) | 28 | (700 | ) | ||

| Depreciation and amortization included in operations | 76 | 73 | 3 | 4 | ||||

| Gross profit | 325 | 270 | 55 | 20 | ||||

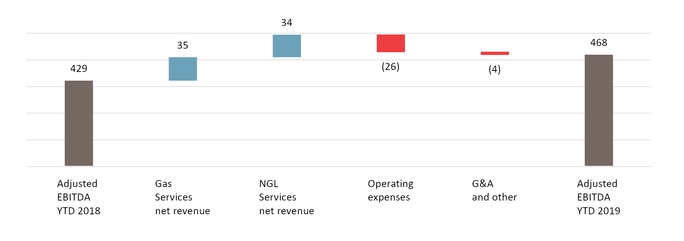

Adjusted EBITDA(3) | 468 | 429 | 39 | 9 | ||||

Volumes (mboe/d)(4) | 881 | 854 | 27 | 3 | ||||

| Distributions from equity accounted investees | 56 | 60 | (4 | ) | (7 | ) | ||

| Changes in Results | ||

Gas Services net revenue(1)(2)(3) | ▲ | Increase is largely attributable to additional demand in the Montney and Duvernay, combined with increased operating expense recoveries as a result of higher power pool prices and the turnaround at the Resthaven facility during the first quarter of 2019. |

NGL Services net revenue(1)(2)(3) | ▲ | Increase primarily due to increased terminalling revenues for propane and butane, combined with the contribution from Redwater Co-generation and Burstall Ethane Storage going into service March 2019 and January 2019, respectively, and higher volumes at Redwater on a year-to-date basis. |

Operating expenses(1) | ▼ | Increase caused by an increase in power pool prices and increased consumption from Burstall Ethane Storage being placed into service, the turnaround at the Resthaven facility and higher labour costs as a result of increased headcount. |

| Share of profit from equity accounted investees | ▲ | Increase mainly due to the contribution from Veresen Midstream following the North Central Liquids Hub going into service in June 2018, combined with the impact of a $24 million finance gain reversal recorded in the first half of 2018. |

| Depreciation and amortization included in operations | ● | Consistent with prior period. |

| Distributions from equity accounted investees | ▼ | $56 million consists of $53 million (2018: $55 million) from Veresen Midstream and $3 million (2018: $5 million) from Fort Corp. |

Volumes (mboe/d)(4) | ▲ | Increased primarily due to additional volumes at Veresen Midstream due in part to the North Central Liquids Hub being placed into service in June 2018, combined with higher volumes at the Saturn, Kakwa River and Cutbank gas plants as a result of increased customer demand and increased volumes at Redwater. Revenue volumes includes 89 mboe/d (2018: 71 mboe/d) related to Veresen Midstream. |

Adjusted EBITDA(3) | ▲ | $39 million increase primarily due to strong NGL and Gas Services revenues, explained above, combined with the North Central Liquids Hub going into service, partially offset by higher operating expenses. Included in adjusted EBITDA is $92 million (2018: $79 million) related to Veresen Midstream. |

Bridge Analysis of Adjusted EBITDA(3) ($ millions)

(1) | Includes inter-division transactions. See note 12 of the condensed consolidated Interim Financial Statements. |

(2) | Revenue and cost of goods sold reported for all 2018 periods have been restated to reflect updated presentation for 2019, where all cost of goods sold and corresponding revenues are reported in the Marketing & New Ventures Division. |

(3) | Refer to "Non-GAAP Measures". |

(4) | Revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

12 Pembina Pipeline Corporation Second Quarter 2019

Operational Overview

| 3 Months Ended June 30 | 6 Months Ended June 30 | |||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||

| ($ millions, except where noted)(unaudited) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | ||||||||||||

| Facilities Division | ||||||||||||||||||||||||

| Gas Services | 668 | 82 | 134 | 650 | 70 | 133 | 675 | 164 | 272 | 651 | 136 | 258 | ||||||||||||

| NGL Services | 198 | 85 | 102 | 199 | 57 | 79 | 206 | 161 | 196 | 203 | 134 | 171 | ||||||||||||

| Total | 866 | 167 | 236 | 849 | 127 | 212 | 881 | 325 | 468 | 854 | 270 | 429 | ||||||||||||

(1) | Revenue volumes. Revenue volumes are physical volumes plus volumes recognized from take-or-pay commitments. Volumes are stated in mboe/d, with natural gas volumes converted to mboe/d from MMcf/d at a 6:1 ratio. |

(2) | Refer to "Non-GAAP Measures". |

Projects & New Developments

The Facilities Division continues to build-out its natural gas and NGL processing and fractionation assets to service customer demand. The projects in the following table were recently placed into service and impact the Facilities Division results.

Significant Projects(1) | In-service Date |

| Redwater Co-generation | March 2019 |

| Burstall Ethane Storage | January 2019 |

| Rail Yard Expansion | December 2018 |

| Cavern Storage | Throughout 2018 |

Veresen Midstream(2) | |

| North Central Liquids Hub | June 2018 |

| Saturn Phase II Gas Plant | January 2018 |

As previously announced, during the quarter Pembina executed further agreements with Chevron Canada Limited to construct sour gas treating facilities at the Duvernay Complex (the "Duvernay Sour Treatment Facilities"). These facilities will include a 150 MMcf/d sour gas sweetening system with the potential for 300 MMcf/d of amine regeneration capability and one tonne of sulphur per day of acid gas incineration. These facilities have a capital budget of $65 million and an anticipated in-service date in the first quarter of 2020. The Duvernay Sour Treatment Facilities will have a 20-year contractual life and will be back-stopped by fixed-return arrangements.

As previously announced, in conjunction with the Duvernay Sour Treatment Facilities, additional modifications are required at the Duvernay II and Duvernay III projects to meet the new sour specifications. The capital budgets of Duvernay II and Duvernay III are $320 million and $175 million, respectively.

As previously announced, on April 4, 2019, Pembina elected to cause all of the Veresen Midstream Class B Units held by its joint venture partner to be converted to Class A Units. This election eliminated further dilution of Pembina's ownership in Veresen Midstream. Pembina's interest in Veresen Midstream subsequent to the conversion of Class B Units is 45 percent.

Collectively, the Facilities Division projects are trending on budget.

The following outlines the projects currently underway and new developments within the Facilities Division:

| Duvernay II | ||

Capital Budget: $320 million | In-service Date: Fourth quarter of 2019 | Status: On time, trending on budget |

| Duvernay II is the first tranche of infrastructure development under the 20-year infrastructure development and service agreement with Chevron Canada Limited and KUFPEC. This development includes 300 MMcf/d of raw gas separation and water removal infrastructure; a 100 MMcf/d sweet gas, shallow cut processing facility; 30 mbpd of condensate stabilization; and other associated infrastructure. Onsite mechanical construction has commenced and the majority of the long-lead equipment has been installed onsite. | ||

Pembina Pipeline Corporation Second Quarter 2019 13

| Duvernay III | ||

Capital Budget: $175 million | In-service Date(3): Mid to late 2020 | Status: On time, trending on budget |

| Duvernay III is the second tranche of infrastructure development under the 20-year infrastructure development and service agreement with Chevron Canada Limited and KUFPEC. This development includes a 100 MMcf/d sweet gas, shallow cut processing facility, 20 mbpd of condensate stabilization and other associated infrastructure. Detailed design is progressing and long-lead equipment has predominantly been ordered. | ||

| Duvernay Sour Treatment Facilities | ||

Capital Budget: $65 million | In-service Date: First quarter of 2020 | Status: On time, trending on budget |

| Sour gas treating facilities at the Duvernay Complex including 150 MMcf/d sour gas sweetening system with the potential for 300 MMcf/d of amine regeneration capability and one tonne of sulphur per day of acid gas incineration. Engineering for the project is progressing, onsite construction is expected to commence later this year. | ||

| Prince Rupert Terminal | ||

Capital Budget: $250 million | In-service Date(3): Second half of 2020 | Status: On time, trending over budget |

| The Prince Rupert LPG export terminal is located on Watson Island, British Columbia and is expected to have a permitted capacity of approximately 25 mbpd of LPG. The LPG supply will be sourced primarily from the Company's Redwater Complex. Rail yard track, plant foundations, and sphere construction has started. All sphere materials are now on site. | ||

| Hythe Developments | ||

Capital Budget(4): $185 million | In-service Date(3): Late 2020 | Status: On time, trending on budget |

| Pembina and its 45 percent owned joint venture, Veresen Midstream, will construct natural gas gathering and processing infrastructure in the Pipestone Montney region. The infrastructure consists of an expansion of up to 125 MMcf/d (56 MMcf/d net to Pembina) of sour gas processing at Veresen Midstream's existing Hythe facility and a new, approximately 60-kilometre, 12-inch sour gas pipeline, to be owned be Veresen Midstream and constructed by Pembina. In addition, various laterals will be owned and constructed by Pembina. All long-lead equipment has been ordered. | ||

| Empress Infrastructure | ||

Capital Budget: $120 million | In-service Date: Late 2020 | Status: On time, trending on budget |

| This expansion will add new fractionation and terminalling facilities, which is expected to add approximately 30 mbpd of propane-plus fractionation capacity to Pembina's Empress NGL Extraction Facility. Engineering for the project is complete and mechanical construction is underway. | ||

(1) | For further details on the Company's significant assets refer to the Pembina's AIF filed at www.sedar.com (filed with the U.S. Securities and Exchange Commission at www.sec.gov under Form 40-F) and on Pembina's website at www.pembina.com. |

(2) | Investment in equity accounted investee, which Pembina has a 45 percent interest in as of June 30, 2019. Results from Veresen Midstream impact share of profit from equity accounted investees and proportionally consolidated metrics. See note 5 to the Interim Financial Statements. |

(3) | Subject to environmental and regulatory approvals. See "Forward-Looking Statements". |

(4) | Net to Pembina. |

14 Pembina Pipeline Corporation Second Quarter 2019

Marketing & New Ventures Division

Financial Overview Three Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Marketing revenue(1)(2) | 1,210 | 1,208 | 2 | — | ||||

Cost of goods sold(1)(2) | 1,129 | 1,120 | 9 | 1 | ||||

Net revenue(1)(3) | 81 | 88 | (7 | ) | (8 | ) | ||

| Share of profit from equity accounted investees | 18 | 30 | (12 | ) | (40 | ) | ||

| Realized (gain) loss on commodity-related derivative financial instruments | (1 | ) | 9 | (10 | ) | (111 | ) | |

| Unrealized (gain) loss on commodity-related derivative financial instruments | (15 | ) | 46 | (61 | ) | (133 | ) | |

| Depreciation and amortization included in operations | 15 | 6 | 9 | 150 | ||||

| Gross profit | 100 | 57 | 43 | 75 | ||||

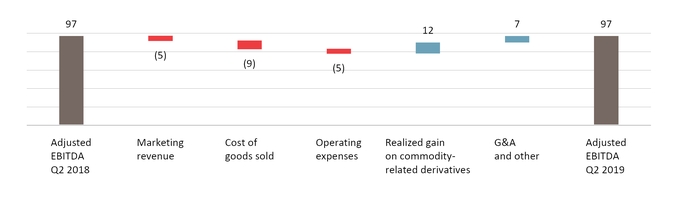

Adjusted EBITDA(3) | 97 | 97 | — | — | ||||

Volumes (mboe/d)(4) | 175 | 155 | 20 | 13 | ||||

| Distributions from equity accounted investees | 17 | 23 | (6 | ) | (26 | ) | ||

| Change in Results | ||

Marketing revenue(1)(2) | ● | Higher NGL marketed volumes were largely offset by lower pricing for propane and butane during the second quarter of 2019, combined with higher crude revenues, as a result of higher realized prices. |

Cost of goods sold(1)(2) | ▼ | Increase due to higher cost of crude driven by an increase in prices, largely offset by the decrease in propane and butane prices which reduced total cost of NGL purchases, combined with the $10 million impact of adopting IFRS 16 that reduced cost of goods sold and increased depreciation and finance costs. |

| Share of profit from equity accounted investees | ▼ | Decrease largely due to lower propane margins at Aux Sable resulting from a decrease in sales prices, combined with a narrower Chicago-AECO natural gas differential and a routine outage during June to complete regular maintenance. |

| Realized (gain) loss on commodity-related derivatives | ▲ | Increase due to the swing to a gain position for derivatives that were settled during the period at prices that were higher than the contracted price, compared to losses that were realized during the second quarter of 2018. |

| Unrealized (gain) loss on commodity-related derivatives | ▲ | Unrealized gain primarily due to a decrease in the price of propane and butane which drove the associated derivative contracts into a gain position, compared to the loss position in the second quarter of 2018 when prices were higher. |

| Depreciation and amortization included in operations | ▼ | Increase largely due to $9 million of additional depreciation on leased rail cars, which are recognized as a right-of-use asset and depreciated following the adoption of IFRS 16. |

| Distributions from equity accounted investees | ▼ | $17 million (2018: $23 million) from Aux Sable. |

Volumes (mboe/d)(4) | ▲ | Increased NGL sales volumes primarily driven by increased supply volumes at Redwater. Revenue volumes includes 29 mboe/d (2018: 37 mboe/d) related to Aux Sable. |

Adjusted EBITDA(3) | ● | Lower margins on propane and butane, explained above, were offset by the realized gain on commodity-related derivatives, combined with the $10 million impact of the adoption of IFRS 16 and lower general and administrative expenses in New Ventures. Included in adjusted EBITDA is $23 million (2018: $34 million) related to Aux Sable. |

Bridge Analysis of Adjusted EBITDA ($ millions)(3)

(1) | Includes inter-division transactions. See note 12 of the Interim Financial Statements. |

(2) | Revenue and cost of goods sold reported for all 2018 periods have been restated to reflect updated presentation for 2019, where the majority of cost of goods sold and corresponding revenues are reported in the Marketing & New Ventures Division. |

(3) | Refer to "Non-GAAP Measures". |

(4) | Marketed NGL volumes. Volumes are stated in mboe/d. |

Pembina Pipeline Corporation Second Quarter 2019 15

Financial Overview Six Months Ended June 30

Results of Operations

| ($ millions, except where noted) (unaudited) | 2019 | 2018 | Change | % Change | ||||

Marketing revenue(1)(2) | 2,606 | 2,540 | 66 | 3 | ||||

Cost of goods sold(1)(2) | 2,394 | 2,332 | 62 | 3 | ||||

Net revenue(1)(3) | 212 | 208 | 4 | 2 | ||||

| Share of profit from equity accounted investees | 23 | 36 | (13 | ) | (36 | ) | ||

| Realized (gain) loss on commodity-related derivative financial instruments | (20 | ) | 27 | (47 | ) | (174 | ) | |

| Unrealized loss on commodity-related derivative financial instruments | 30 | 16 | 14 | 88 | ||||

| Depreciation and amortization included in operations | 32 | 11 | 21 | 191 | ||||

| Gross profit | 193 | 190 | 3 | 2 | ||||

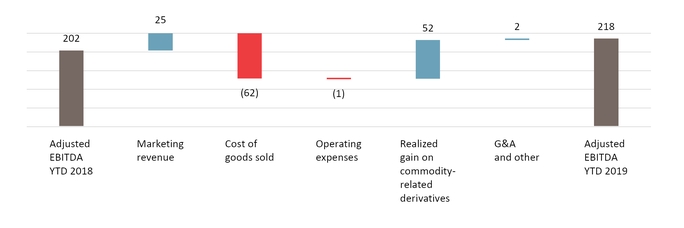

Adjusted EBITDA(3) | 218 | 202 | 16 | 8 | ||||

Volumes (mboe/d)(4) | 196 | 172 | 24 | 14 | ||||

| Distributions from equity accounted investees | 43 | 40 | 3 | 8 | ||||

| Change in Results | ||

Marketing revenue(1)(2) | ▲ | Increase primarily due to higher NGL sales volumes at Redwater and increased crude sales volumes, combined with a $33 million settlement payment from a contract dispute that was resolved during the first quarter of 2019, partially offset by lower NGL market prices. |

Cost of goods sold(1)(2) | ▼ | Increase due to the additional sales volumes noted in revenue above, partially offset by a $20 million adjustment on the adoption of IFRS 16 that reduced cost of goods sold and increased depreciation and finance costs. |

| Share of profit from equity accounted investees | ▼ | Decrease due to lower propane margins at Aux Sable resulting from lower sales prices during the second quarter of 2019, combined with an outage during June to complete regular maintenance. |

| Realized (gain) loss on commodity-related derivatives | ▲ | Increase due to the swing to a gain position for derivatives that were settled during period at prices that were higher than the contracted price, compared to the losses that were realized during the first six months of 2018. |

| Unrealized loss on commodity-related derivatives | ▼ | Increase in unrealized loss primarily due to crude storage contracts which expired and were realized during the period. |

| Depreciation and amortization included in operations | ▼ | Increase largely due to $18 million of depreciation on leased rail cars, which are recognized as a right-of-use asset and depreciated following the adoption of IFRS 16. |

| Distributions from equity accounted investees | ▲ | $43 million (2018: $40 million) from Aux Sable. |

Volumes (mboe/d)(4) | ▲ | Increased NGL sales volumes primarily driven by increased supply volumes at Redwater. Revenue volumes includes 34 mboe/d (2018: 41 mboe/d) related to Aux Sable. |

Adjusted EBITDA(3) | ▲ | $16 million increase primarily due to an increased realized gain on commodity-related derivatives, combined with the $20 million impact of the adoption of IFRS 16, partially offset by lower margins after adjusting for the $33 million settlement payment mentioned above. Included in adjusted EBITDA is $41 million (2018: $47 million) related to Aux Sable. |

Bridge Analysis of Adjusted EBITDA(3)(5)($ millions)

(1) | Includes inter-division transactions. See note 12 of the condensed consolidated Interim Financial Statements. |

(2) | Revenue and cost of goods sold reported for all 2018 periods have been restated to reflect updated presentation for 2019, where all cost of goods sold and corresponding revenues are reported in the Marketing & New Ventures Division. |

(3) | Refer to "Non-GAAP Measures". |

(4) | Marketed NGL volumes. Volumes are stated in mboe/d. |

(5) | Marketing revenue excludes the positive contract settlement of $33 million. |

16 Pembina Pipeline Corporation Second Quarter 2019

Operational Overview

| 3 Months Ended June 30 | 6 Months Ended June 30 | |||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||

| ($ millions, except where noted)(unaudited) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | Volumes(1) | Gross Profit | Adjusted EBITDA(2) | ||||||||||||

| Marketing & New Ventures Division | ||||||||||||||||||||||||

| Marketing | 175 | 100 | 100 | 155 | 57 | 108 | 196 | 193 | 227 | 172 | 190 | 219 | ||||||||||||

New Ventures(3) | — | — | (3 | ) | — | — | (11 | ) | — | — | (9 | ) | — | — | (17 | ) | ||||||||

| Total | 175 | 100 | 97 | 155 | 57 | 97 | 196 | 193 | 218 | 172 | 190 | 202 | ||||||||||||

(1) | Marketed NGL volumes. Volumes are stated in mboe/d. |

(2) | Refer to "Non-GAAP Measures". |

(3) | All New Ventures projects have not yet commenced operations and therefore have no volumes or gross profit. |

Projects & New Developments

Subsequent to the quarter, effective July 15, 2019, Pembina assumed responsibility for operating the assets of Aux Sable.

The following outlines the projects currently underway and new developments within the Marketing & New Ventures Division:

| PDH/PP Facility | ||

Capital Budget(1): $2.5 billion | In-service Date(2): Mid-2023 | Status: On time, trending on budget |

| The PDH/PP Facility will be located adjacent to Pembina's Redwater fractionation complex and will convert approximately 23,000 bpd of locally supplied propane into polypropylene, a high value recyclable polymer used in a wide range of finished products including but not limited to automobiles, medical devices, food packaging and home electronic appliances, among others. The project is in the execution phase including obtaining engineering, procurement and construction bids. Long-lead equipment order placement is largely complete. An early works construction contract has been awarded and site-clearing is complete. | ||

| Jordan Cove LNG Project (proposed) | ||

| The proposed Jordan Cove LNG project is a world-scale LNG export facility which would transport North American natural gas to world markets. The project is made up of two parts: the LNG terminal, with a planned design capacity of 7.8 million tonnes per annum and the Pacific Connector Gas pipeline which would transport natural gas from Malin, Oregon to an LNG terminal in Coos County, Oregon. | ||

| Regulatory processes for Jordan Cove are progressing. On March 29, 2019 the FERC issued a Draft Environmental Impact Statement, which provides a constructive framework for the approval of Jordan Cove essentially as proposed, with reasonable conditions that work with the project development process and with only minor suggested changes. A final FERC decision is expected by January 2020. The Oregon State permit approval with respect to the Coastal Zone Management Act is progressing. In May, the Oregon Department of Environmental Quality ("DEQ") denied the Company’s 401 permit without prejudice based on procedural reasons. The DEQ has encouraged the Company to re-apply and Pembina continues to work on a path forward. Each of the permits are a critical component of the regulatory process and enable the commercial viability and critical investment to move forward. | ||

| The Company has signed voluntary easement agreements that constitute 82 percent of the privately owned portion of the proposed pipeline route, which will allow the pipeline to cross beneath these properties. | ||

| Commercial discussions with prospective customers are ongoing as regulatory permitting is progressed. | ||

| The Company intends to seek partners for both the pipeline and liquification facility thereby reducing its 100 percent ownership interest to a net ownership interest of between 40 and 60 percent with the intention to reduce the capital, operating, and other project risks. | ||

(1) | Net to Pembina. |

(2) | Subject to environmental and regulatory approvals. |

Pembina Pipeline Corporation Second Quarter 2019 17

4. LIQUIDITY & CAPITAL RESOURCES

Available Sources of Liquidity

| June 30, 2019 | ||||

| ($ millions) | (unaudited) | December 31, 2018 | ||

Working capital(1) | (450 | ) | (477 | ) |

Variable rate debt(2) | ||||

| Bank debt | 1,000 | 1,305 | ||

| Total variable rate debt outstanding (weighted average of 2.9% (2018: 3.2%)) | 1,000 | 1,305 | ||

Fixed rate debt(2) | ||||

| Senior unsecured notes | 540 | 540 | ||

| Senior unsecured medium-term notes | 6,300 | 5,700 | ||

| Total fixed rate debt outstanding (weighted average of 4.2% (2018: 4.2%)) | 6,840 | 6,240 | ||

Finance lease liability(3) | — | 19 | ||

| Total debt outstanding | 7,840 | 7,564 | ||

| Cash and unutilized debt facilities | 2,848 | 2,372 | ||

(1) | As at June 30, 2019, working capital includes $340 million (December 31, 2018: $480 million) associated with the current portion of loans and borrowings. |

(2) | Face value. |

(3) | Finance lease liabilities reported separately following the adoption of IFRS 16, see "Changes in Accounting Policies". |

Pembina anticipates its cash flow from operating activities, the majority of which is derived from fee-based contracts, will be more than sufficient to meet its short-term and long-term operating obligations and fund its dividends. In the short term, Pembina expects to source funds required for capital projects and contributions to investments in equity accounted investees from cash, its credit facilities and by accessing the capital markets, as required. Based on its successful access to financing in the capital markets over the past several years, Pembina believes it should continue to have access to additional funds as required. Refer to "Risk Factors – Additional Financing and Capital Resources" in Pembina's MD&A and note 24 to the Consolidated Financial Statements for the year ended December 31, 2018 for more information. Management remains satisfied that the leverage employed in Pembina's capital structure is sufficient and appropriate given the characteristics and operations of the underlying asset base.

Management may make adjustments to Pembina's capital structure as a result of changes in economic conditions or the risk characteristics of the underlying assets. To maintain or modify Pembina's capital structure in the future, Pembina may renegotiate new debt terms, repay existing debt, seek new borrowing, issue additional equity and/or repurchase shares.

Pembina's credit facilities consist of an unsecured $2.5 billion (December 31, 2018: $2.5 billion) revolving credit facility which includes a $750 million accordion feature and matures in May 2024, an unsecured $1.0 billion (December 31, 2018: $1.0 billion) non-revolving term loan which matures in March 2021, and an operating facility of $20 million (December 31, 2018: $20 million) due in May 2020 and is typically renewed on an annual basis. There are no repayments due over the term of these facilities. As at June 30, 2019, Pembina had $2.8 billion (December 31, 2018: $2.4 billion) of cash and unutilized debt facilities. At June 30, 2019, Pembina had loans and borrowings (excluding deferred financing costs) of $7.8 billion (December 31, 2018: $7.5 billion). Pembina also had an additional $68 million (December 31, 2018: $69 million) in letters of credit issued pursuant to separate credit facilities. Pembina is required to meet certain specific and customary affirmative and negative financial covenants under its senior unsecured notes, medium-term notes, revolving credit, non-revolving term and operating facilities, including a requirement to maintain certain financial ratios. Pembina is also subject to customary restrictions on its operations and activities under its notes and credit facilities, including restrictions on the granting of security, incurring indebtedness and the sale of its assets.

On July 11, 2019, the Pipeline Financial Requirements Regulations (“Regulations”) issued under the National Energy Board (“NEB”) Act came into effect. The Regulations set out the absolute liability limits required for operators of NEB-regulated pipelines to respond to an unintended or uncontrolled release of commodity from a pipeline. The newly enacted Regulations require operators to demonstrate that they have, and will maintain, the prescribed financial resources to fund their respective

18 Pembina Pipeline Corporation Second Quarter 2019

absolute liability or a greater amount as determined by the NEB, including a set portion (five percent) in readily available resources. Pembina has direct ownership in NEB-regulated assets with a total absolute liability of $450 million. Pembina filed its financial resources plan with the NEB verifying its ability to meet the $450 million liability using prescribed financial resources, including $22.5 million in readily available resources, and has maintained compliance with the requirements of the NEB Act.

Covenants

Pembina's financial covenants include the following:

| Debt Instrument | Financial Covenant(1) | Ratio | Ratio at June 30, 2019 |

| Senior unsecured medium-term notes | Funded Debt to Capitalization | Maximum 0.70 | 0.35 |

| Revolving unsecured credit facility and non-revolving term loan | Debt to Capital | Maximum 0.65 | 0.34 |

| EBITDA to senior interest coverage | Minimum 2.5:1.0 | 8.91 | |

(1) | Terms as defined in relevant agreements. |

In addition to the table above, Pembina has customary covenants on its other senior unsecured notes. Pembina was in compliance with all covenants under its notes and facilities as at June 30, 2019 (December 31, 2018: in compliance).

Pembina continues to actively monitor and reassess the creditworthiness of its counterparties. Financial assurances to mitigate and reduce risk may include guarantees, letters of credit and cash. Letters of credit totaling $108 million (December 31, 2018: $122 million) were held at June 30, 2019, primarily in respect of customer trade receivables.

Outstanding Share Data(1)

| Issued and outstanding (thousands of shares) | July 29, 2019 | |

| Common shares | 511,500 | |

| Stock options | 17,098 | |

| Stock options exercisable | 8,316 | |

| Class A, Series 1 Preferred shares | 10,000 | |

| Class A, Series 3 Preferred shares | 6,000 | |

| Class A, Series 5 Preferred shares | 10,000 | |

| Class A, Series 7 Preferred shares | 10,000 | |

| Class A, Series 9 Preferred shares | 9,000 | |

| Class A, Series 11 Preferred shares | 6,800 | |

| Class A, Series 13 Preferred shares | 10,000 | |

| Class A, Series 15 Preferred shares | 8,000 | |

| Class A, Series 17 Preferred shares | 6,000 | |

| Class A, Series 19 Preferred shares | 8,000 | |

| Class A, Series 21 Preferred shares | 16,000 | |

(1) | The Company's common shareholders and Class A preferred shareholders, by separate class votes, approved a special resolution to amend the Company's articles to increase the limit on the number of Class A preferred shares the Company is authorized to issue (the “Amendment”). The Company filed Articles of Amendment effecting the Amendment on June 25, 2019. A copy of the Company’s articles can be found online at www.sedar.com. |

Financing Activity

On April 3, 2019, Pembina closed an offering of $800 million of senior unsecured medium-term notes (the "Offering"). The Offering was conducted in two tranches consisting of $400 million in senior unsecured medium-term notes, series 12, having a fixed coupon of 3.62 percent per annum, paid semi-annually, and maturing on April 3, 2029 and $400 million in senior unsecured medium-term notes, series 13, having a fixed coupon of 4.54 percent per annum, paid semi-annually, and maturing on April 3, 2049.

On May 31, 2019, Pembina completed an extension on its $2.5 billion revolving credit facility, which now matures on May 31, 2024.

Pembina Pipeline Corporation Second Quarter 2019 19

On June 13, 2019, Pembina's $200 million senior unsecured medium term note 4A matured and was fully repaid.

Credit Ratings

The following information with respect to Pembina's credit ratings is provided as it relates to Pembina's financing costs and liquidity. Specifically, credit ratings affect Pembina's ability to obtain short-term and long-term financing and the cost of such financing. A reduction in the current ratings on Pembina's debt by its rating agencies, particularly a downgrade below investment-grade ratings, could adversely affect Pembina's cost of financing and its access to sources of liquidity and capital. In addition, changes in credit ratings may affect Pembina's ability, and the associated costs, to enter into normal course derivative or hedging transactions. Credit ratings are intended to provide investors with an independent measure of credit quality of any issues of securities. The credit ratings assigned by the rating agencies are not recommendations to purchase, hold or sell the securities, nor do the ratings comment on market price or suitability for a particular investor. Any rating may not remain in effect for a given period of time or may be revised or withdrawn entirely by a rating agency in the future if, in its judgment, circumstances so warrant.

Pembina targets strong 'BBB' credit ratings. DBRS rates Pembina's senior unsecured notes and senior unsecured medium-term notes 'BBB' and Class A Preferred Shares Pfd-3. S&P's long-term corporate credit rating on Pembina is 'BBB' and its rating of the Class A Preferred Shares is P-3 (High).

Contractual Obligations

Pembina had the following contractual obligations outstanding at June 30, 2019:

Contractual Obligations(1) | Payments Due By Period | |||||||||

| ($ millions) | Total | Less than 1 year | 1 – 3 years | 3 – 5 years | After 5 years | |||||

Leases(2) | 562 | 82 | 148 | 106 | 226 | |||||

Loans and borrowings(3) | 11,715 | 694 | 2,356 | 1,526 | 7,139 | |||||

Construction commitments(4) | 1,396 | 770 | 94 | 42 | 490 | |||||

Other(5) | 278 | 32 | 71 | 55 | 120 | |||||

| Total contractual obligations | 13,951 | 1,578 | 2,669 | 1,729 | 7,975 | |||||

(1) | Pembina enters into product purchase agreements and power purchase agreements to secure supply for future operations. Purchase prices of both NGL and power are dependent on current market prices. Volumes and prices for NGL and power contracts cannot be reasonably determined and therefore an amount has not been included in the contractual obligations schedule. Product purchase agreements range from one to 10 years and involve the purchase of NGL products from producers. Assuming product is available, Pembina has secured between 24 and 105 mbpd each year up to and including 2027. Power purchase agreements range from one to 25 years and involve the purchase of power from electrical service providers. The Company has secured up to 70 megawatts per day each year up to and including 2043. |

(2) | Includes rail, office space, land and vehicle leases. |

(3) | Excluding deferred financing costs. Including interest payments on senior unsecured notes. |

(4) | Excluding significant projects that are awaiting regulatory approval at June 30, 2019, projects which Pembina is not committed to construct, and projects that are executed by equity accounted investees. See "Selected Equity Accounted Investee Information" for details regarding the nature of Pembina’s commitments to fund equity accounted investees. |

(5) | Includes $81 million in commitments related to leases that have not yet commenced. |

Pembina is, subject to certain conditions, contractually committed to the construction and operation of Phase VI and Duvernay II as well as certain pipeline connections and laterals and other corporate infrastructure. See "Forward-Looking Statements & Information".

5. CAPITAL EXPENDITURES

| 3 Months Ended June 30 | 6 Months Ended June 30 | |||||||

| ($ millions)(unaudited) | 2019 | 2018 | 2019 | 2018 | ||||

| Pipelines Division | 234 | 119 | 426 | 385 | ||||

| Facilities Division | 148 | 101 | 260 | 139 | ||||

| Marketing & New Ventures Division | 47 | 33 | 102 | 53 | ||||

| Corporate/other projects | 5 | 2 | 7 | 2 | ||||

| Total capital | 434 | 255 | 795 | 579 | ||||

Contributions to equity accounted investees(1)(2) | 28 | — | 118 | 58 | ||||

(1) | Contributions for the three months ended June 30, 2019, include $27 million (2018: $nil) to CKPC and $1 million (2018: $nil) to Aux Sable. |

(2) | Contributions for the six months ended June 30, 2019, include $90 million (2018: $nil) to CKPC, $26 million (2018: $58 million) to Veresen Midstream and $2 million (2018: $nil) to Aux Sable. |

20 Pembina Pipeline Corporation Second Quarter 2019

For the three months ended June 30, 2019, capital expenditures were $434 million, compared to $255 million during the same three-month period of 2018. For the six months ended June 30, 2019, capital expenditures were $795 million, compared to $579 million during the same six month period of 2018. In both 2019 and 2018, the Pipelines Division's capital expenditures were primarily related to Pembina's ongoing pipeline expansion projects. In 2019, the Facilities Division's capital expenditures were largely related to construction on Duvernay II, Empress Infrastructure and the Prince Rupert Terminal. In 2018, the Facilities Division's capital expenditures were largely related to construction of Duvernay II, the Burstall Ethane Storage, Redwater Co-generation and the Prince Rupert Terminal. Capital expenditures in the Marketing & New Ventures Division in both 2019 and 2018 were primarily related to the Jordan Cove LNG project.

6. DIVIDENDS

Common Share Dividends

Common share dividends are payable if, as, and when declared by Pembina's Board of Directors. The amount and frequency of dividends declared and payable is at the discretion of the Board of Directors, which considers earnings, cash flow, capital requirements, the financial condition of Pembina and other relevant factors when making its dividend determination.

On May 2, 2019, Pembina's Board of Directors approved a five percent increase to its monthly common share dividend rate (from $0.19 per common share to $0.20 per common share), commencing with the dividend paid on June 14, 2019.

Preferred Share Dividends

The holders of Pembina's Class A Preferred Shares are entitled to receive fixed cumulative dividends. Dividends on the Series 1, 3, 5, 7, 9, 11, 13 and 21 preferred shares are payable quarterly on the first day of March, June, September and December, if, as and when declared by the Board of Directors of Pembina. Dividends on the Series 15, 17 and 19 preferred shares are payable on the last day of March, June, September and December in each year, if, as and when declared by the Board of Directors.

On January 30, 2019, Pembina announced that it did not intend to exercise its right to redeem the six million Cumulative Redeemable Rate Reset Class A Preferred Shares, Series 3 ("Series 3 Shares") shares outstanding on March 1, 2019. The annual dividend rate for the Series 3 Shares for the five-year period from and including March 1, 2019 to, but excluding, March 1, 2024 will be 4.478 percent.

On March 1, 2019, Pembina announced that it did not intend to exercise its right to redeem the six million Cumulative Redeemable Rate Reset Class A Preferred Shares, Series 17 ("Series 17 Shares") shares outstanding on March 31, 2019. The annual dividend rate for the Series 17 Shares for the five-year period from and including March 31, 2019 to, but excluding, March 31, 2024 will be 4.821 percent.

On May 2, 2019, Pembina announced that it did not intend to exercise its right to redeem the 10 million Cumulative Redeemable Rate Reset Class A Preferred Shares, Series 5 ("Series 5 Shares") shares outstanding on June 3, 2019. The annual dividend rate for the Series 5 Shares for the five-year period from and including June 1, 2019 to, but excluding, June 1, 2024 will be 4.573 percent.

Pembina Pipeline Corporation Second Quarter 2019 21

7. SELECTED QUARTERLY INFORMATION

Selected Quarterly Operating Information