September 11, 2014

VIA EDGAR

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549-3561

Attention: Linda Cvrkel, Branch Chief

Re: Burger King Worldwide, Inc. Form 10-K for the year ended December 31, 2013 Filed February 21, 2014 File No. 001-35511

Dear Ms. Cvrkel:

On behalf of Burger King Worldwide, Inc. (the “Company”), set forth below is the Company’s response to comments received from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in their letter dated September 9, 2014 with respect to the above referenced Annual Report on Form 10-K of the Company (the “2013 Form 10-K”).

For reference purposes, the text of the letter has been reproduced herein with responses below each numbered comment. For your convenience, the reproduced Staff comments from the letter have been italicized.

Form 10-K for the year ended December 31, 2013

Item 1. Business

Latin American and the Caribbean (LAC), page 6

1. We note from the disclosure on page 6 that in April 2013, you contributed all of your 98 company restaurants in Mexico to a joint venture with Alsea S.A.B. de C.V., the parent of your largest franchisee in Mexico, in exchange for cash and a 20% equity stake in the joint venture and granted the joint venture exclusive master franchise rights and development rights. Please tell us how you valued and accounted for the consideration exchanged in this transaction and indicate whether any gain or loss was recognized in your financial statements as a result of this transaction. If so, please explain how any gain or loss recognized was determined and indicate where it has been classified in your results of operations.

Response:

The Company respectfully acknowledges the Staff’s comment. As disclosed in the 2013 Form 10-K, both the Company and Alsea S.A.B. de C.V. (“Alsea”) contributed their respective restaurants in Mexico to a

| ALBANY AMSTERDAM ATLANTA AUSTIN BOCA RATON BOSTON CHICAGO DALLAS DELAWARE DENVER FORT LAUDERDALE HOUSTON LAS VEGAS LONDON* LOS ANGELES MEXICO CITY+ MIAMI MILAN** NEW JERSEY NEW YORK NORTHERN VIRGINIA ORANGE COUNTY ORLANDO PHILADELPHIA PHOENIX ROME** SACRAMENTO SAN FRANCISCO SEOUL¥ SHANGHAI SILICON VALLEY TALLAHASSEE TAMPA TEL AVIV^ WARSAW~ WASHINGTON, D.C. WESTCHESTER COUNTY WEST PALM BEACH

* OPERATES AS GREENBERG TRAURIG MAHER LLP + OPERATES AS GREENBERG TRAURIG, S.C. ** STRATEGIC ALLIANCE ¥ OPERATES AS GREENBERG TRAURIG LLP FOREIGN LEGAL CONSULTANT OFFICE ^ A BRANCH OF GREENBERG TRAURIG, P.A., FLORIDA, USA ~ OPERATES AS GREENBERG TRAURIG GRZESIAK SP.K. |

Securities and Exchange Commission

September 11, 2014

Page 2 of 5

joint venture which was negotiated to be 80% owned by Alsea and 20% owned by the Company. The Company advises the Staff that the sale of its restaurants in Mexico required it to record the acquired equity interest at fair value as of the date of the acquisition, as the Company contributed its restaurant business to the joint venture and no longer controlled the restaurant business.

The parties negotiated the consideration that would be attributable to each respective party’s restaurants based on an income approach, which estimated the value of the combined entity using a valuation multiple agreed upon by the two parties. Equity was preliminarily allocated to each party based on the EBITDA of each parties’ contributed restaurants multiplied by the mutually agreed-upon EBITDA multiple. Based upon the relative EBITDA contribution of the contributed restaurants owned by the two parties, Alsea paid the Company $27.2 million of cash consideration so that the ownership of the joint venture could be the negotiated ownership percentages of 80% by Alsea and 20% by Company.

The transaction resulted in a $7.7 million gain, which was calculated as the difference between the transaction consideration and the carrying value of the Company restaurants contributed to the joint venture, including the write-off of $9.2 million of goodwill allocated from the reporting unit. The gain was recognized in “Other operating income (expense)” in the Company’s Consolidated Statement of Operations for the year ended December 31, 2013.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Business Combination Agreement Expenses, page 33

2. We note the disclosure on page 33 indicating that on April 3, 2012 Burger King Worldwide Holdings, Inc., the indirect parent company of Holdings entered into a business combination agreement and plan of merger with Justice Holdings Limited. We also note that you incurred $27 million of general and administrative expenses associated with the business combination agreement during 2012, consisting of $5.9 million of one- time share-based compensation expense as a result of the increase in your equity value implied by the business combination agreement and $21.1 million of professional fees and other transaction costs. Please explain what impact this merger transaction had on your financial statements other than the recognition of the expenses described on page 33 of MD&A. In addition, since this transaction was consummated by your parent company, please explain why you were required to recognize $27 million of expenses in your financial statements as a result of the merger. As part of your response, please also explain why you were required to revalue certain share-based compensation arrangements as a result of the merger transaction.

Response:

The Company respectfully acknowledges the Staff’s comment. As further discussed below, the Company advises the Staff that the $27 million of general and administrative expenses associated with the business combination agreement during 2012 were incurred by

GREENBERG TRAURIG, P.A.n ATTORNEYS AT LAWn WWW.GTLAW.COM

Securities and Exchange Commission

September 11, 2014

Page 3 of 5

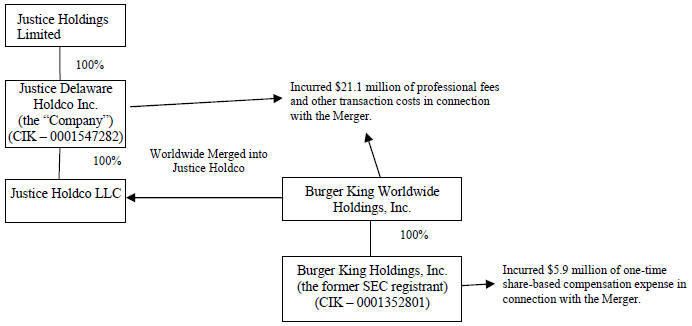

(1) Burger King Worldwide Holdings, Inc., (“Worldwide Holdings”) which was merged into Justice Holdco LLC (a subsidiary of the Company) and (2) Justice Delaware Holdco Inc. (now known as the “Company”).

As previously disclosed in the Company’s Registration Statement on Form S-1 (No. 333-181261) (the “Company’s Form S-1”), on April 3, 2012, Worldwide, entered into a Business Combination Agreement and Plan of Merger (the “Business Combination Agreement”), by and among Justice Holdings Limited, Justice Delaware Holdco Inc., Justice Holdco LLC, (a direct wholly-owned subsidiary of the Company) (“Justice Holdco”) and Worldwide Holdings. Pursuant to the terms of the Business Combination Agreement, the Company filed the Company’s Form S-1 and a Form 8-A registering the issuance of the Company’s common stock and became an SEC registrant.

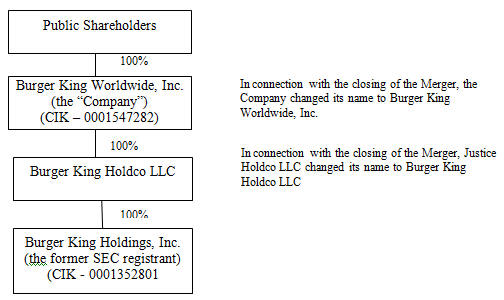

In accordance with the terms of the Business Combination Agreement, on June 20, 2012, Worldwide Holdings merged with and into Justice Holdco, with Justice Holdco continuing as the surviving company and changing its name to Burger King Holdco (the “Merger”). Upon closing of the Merger, the Company changed its name from Justice Delaware Holdco Inc. to Burger King Worldwide, Inc. and listed its shares on the New York Stock Exchange under the symbol “BKW” (“BKW”). Based on the foregoing, following the Merger, BKW became the SEC registrant, the indirect parent company of Burger King Holdings (“BKH”). Prior to the Merger, the SEC registrant was BKH.

In addition to the $21.1 million of professional fees and other transaction costs incurred by Worldwide Holdings and by the Company, BKH incurred $5.9 million of one-time share-based compensation expense. The one-time share-based compensation expense pertained to shares purchased by BKH’s employees and Burger King Corporation’s employees pursuant to the BKH’s employee bonus swap program during the first quarter of 2012, prior to the announcement of the Merger. These shares were exchanged for bonus at a per share value based on an equity valuation that did not contemplate the Merger. However, since the equity value implied by the Merger indicated these swaps were likely made below the fair market value per share, the Company engaged a third-party valuation firm to assess the fair value of these shares at the time of the swap. As a result, the Company recognized $5.9 million of one-time share-based compensation expense.

The Merger was accounted for as a transaction between shareholders and did not constitute a change in control for purposes of the Company’s debt agreements or equity compensation plans. Additionally, because no change in control occurred, the Merger did not require the application of the acquisition method of accounting. Shares outstanding in periods prior to the merger were retrospectively adjusted in periods prior to the Merger using an exchange ratio specified in the Business Combination Agreement. Consequently, other than the recognition of the $27 million of general and administrative expenses associated with the Business Combination Agreement, there was no other impact of the transaction on the Company’s financial statements.

GREENBERG TRAURIG, P.A.n ATTORNEYS AT LAWn WWW.GTLAW.COM

Securities and Exchange Commission

September 11, 2014

Page 4 of 5

For clarity, the chart below demonstrates the ownership structure of the entities prior to the transaction and after the transaction:

Before the Transaction

After the Transaction

GREENBERG TRAURIG, P.A.n ATTORNEYS AT LAWn WWW.GTLAW.COM

Securities and Exchange Commission

September 11, 2014

Page 5 of 5

Note 23. Supplemental Financial Information, page 106

3. We note that you have included condensed consolidating financial information in your financial statements for the parent, issuer, guarantors and non-guarantors of your Senior Notes. Please revise to disclose whether your subsidiary guarantors are 100% owned as required by Rule 3-10(f) of Regulation S-X.

Response:

The Company respectfully acknowledges the Staff’s comment. The Company confirms to the Staff that each of the subsidiary guarantors are 100% owned and that all future filings will include language disclosing the Company’s 100% ownership interest in accordance with Rule 3-10(f) of Regulation S-X.

*****

The Company acknowledges that (a) it is responsible for the adequacy and accuracy of the disclosure in the filings, (b) Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filings, and (c) the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

*****

We hope that the foregoing has been responsive to the Staff’s comments and look forward to resolving any outstanding issues as quickly as possible. Please direct any questions, comments or requests for further information to me at 954-768-8255 or via email atmacculloughk@gtlaw.com or to Joshua Kobza, the Company’s Executive Vice President and Chief Financial Officer, atJKobza@whopper.com.

| Very truly yours, |

| /s/ Kara L. MacCullough |

Kara L. MacCullough Greenberg Traurig, P.A. |

| cc: | Joshua Kobza, Executive Vice President, Chief Financial Officer |

| Jill Granat, Senior Vice President, General Counsel & Secretary |

GREENBERG TRAURIG, P.A.n ATTORNEYS AT LAWn WWW.GTLAW.COM