Filed Pursuant to Rule 424(b)(3)

Registration No. 333-182290

PROSPECTUS

Community Choice Financial Inc.

OFFER TO EXCHANGE

Up to $395,000,000 aggregate principal amount of its 10.75% Senior Secured Notes due 2019

registered under the Securities Act of 1933 for

any and all outstanding 10.75% Senior Secured Notes due 2019

that were issued on April 29, 2011

· We are offering to exchange new registered 10.75% senior secured notes due 2019, which we refer to herein as the “exchange notes,” for all of our outstanding unregistered 10.75% senior secured notes due 2019 that were issued on April 29, 2011, which we refer to herein as the “original notes.” We refer herein to the exchange notes and the original notes, collectively, as the “notes.”

· The exchange offer expires at 5:00 p.m., New York City time, on October 19, 2012, unless extended.

· The exchange offer is subject to customary conditions that we may waive.

· All outstanding original notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer will be exchanged for the exchange notes.

· Tenders of outstanding notes may be withdrawn at any time before 5:00 p.m., New York City time, on the expiration date of the exchange offer.

· The exchange of original notes for exchange notes will not be a taxable exchange for U.S. federal income tax purposes.

· We will not receive any proceeds from the exchange offer.

· The terms of the exchange notes to be issued are substantially identical to the terms of the original notes, except that the exchange notes will not have transfer restrictions and you will not have registration rights.

· In order to accept this exchange offer, you must deliver your original notes and a properly completed and duly executed letter of transmittal to the exchange agent prior to the expiration of the exchange offer. For more information on how to tender your original notes, see “The Exchange Offer.”

· If you fail to tender your original notes, you will continue to hold unregistered securities and it may be difficult for you to transfer them.

· There is no established trading market for the exchange notes, and we do not intend to apply for listing of the exchange notes on any securities exchange or market quotation system.

We are an “emerging growth company” and are eligible for reduced reporting requirements.

See “Risk Factors” beginning on page 19 for a discussion of matters you should consider before you participate in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is September 20, 2012.

1 | |

19 | |

47 | |

48 | |

49 | |

49 | |

50 | |

51 | |

59 | |

62 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 66 |

98 | |

121 | |

147 | |

149 | |

151 | |

153 | |

238 | |

241 | |

246 | |

246 | |

246 | |

246 | |

F-1 |

No dealer, salesperson or other individual has been authorized to give any information or to make any representations not contained in this prospectus in connection with the exchange offer. If given or made, such information or representations must not be relied upon as having been authorized by us. Neither the delivery of this prospectus nor any sale made hereunder shall, under any circumstances, create any implications that there has not been any change in the facts set forth in this prosecutes or in our affairs since the date hereof.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal accompanying this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended, or the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of the exchange notes received in exchange for original notes where such original notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the expiration of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resales. See “Plan of Distribution.”

NOTICE TO INVESTORS

This prospectus contains summaries of the terms of certain agreements that we believe to be accurate in all material respects. However, we refer you to the actual agreements for complete information relating to those agreements. All summaries of such agreements contained in this prospectus or incorporated by reference into this prospectus are qualified in their entirety by this reference. To the extent that any such agreement is attached as an exhibit to this registration statement, we will make a copy of such agreement available to you upon request. We will provide this information to you at no charge upon written or oral request directed to Investor Relations, 7001 Post Road, Suite 200, Dublin, Ohio 43016 (telephone number (614) 798-5900). In order to ensure timely delivery of this information, any request should be made by October 12, 2012, five business days prior to the expiration date of the exchange offer.

The notes will be available in book-entry form only. The notes exchanged pursuant to this prospectus will be issued in the form of one or more global certificates, which will be deposited with, or on behalf of, The Depository Trust Company, or DTC, and registered in its name or in the name of Cede & Co., its nominee. Beneficial interests in the global certificates will be shown on, and transfer of the global certificates will be effected only through, records maintained by DTC and its participants. After the initial issuance of the global certificates, notes in certificated form will be issued in exchange for global certificates only in the limited circumstances set forth in the indenture, dated as of April 29, 2011, or the Indenture, governing the notes. See “Book-Entry, Delivery and Form.” U.S. Bank National Association, as trustee under the Indenture or as collateral agent under the Indenture, credit agreement governing our revolving credit facility and the collateral agreement, has not reviewed this prospectus and has made no representations as to the information contained herein.

INDUSTRY AND MARKET DATA AND PERFORMANCE DATA

This prospectus includes information regarding the retail financial services industry and various markets in which we compete. When we refer to our position in the industry, such market position is based on the number of retail stores we operate and not on our revenues or volumes. Where possible, this information is derived from third-party sources that we believe are reliable, including the Federal Deposit Insurance Corporation, or FDIC, Mercator Advisory Group, or Mercator, Stephens Inc., or Stephens, the Federal Reserve Bank of New York, the National Bureau of Economic Research, or NBER, Bretton Woods, Inc., or Bretton Woods, and Financial Service Centers of America, Inc., or FiSCA. In other cases, this information is based on estimates made by our management, based on their industry and market knowledge and information from third-party sources. However, this data is subject to change and cannot be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be reliable.

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you. You should read the entire prospectus and the information incorporated by reference in this prospectus carefully, including the historical consolidated financial statements and pro forma consolidated statements of operations and the related notes included elsewhere in this prospectus, before you decide to participate in the exchange offer. This prospectus contains forward-looking statements, which involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed in the “Risk Factors” and other sections of this prospectus. When we present historical financial information on a “pro forma basis”, we provide such information after giving effect to each of the acquisition of CCCS Corporate Holdings, Inc., which we completed in April 2011, and the acquisition of 10 stores in Illinois, which we completed in March 2011, and to each of the offering of our original notes and the establishment of our $40 million revolving credit facility, or our Revolving Credit Facility, each of which we completed in April 2011, as described in more detail under “Unaudited Pro Forma Consolidated Financial Information”. In this prospectus, unless the context requires otherwise, references to “CCFI”, “Issuer”, “we”, “our”, “us” or the “Company” refer to Community Choice Financial Inc. and to our predecessor, CheckSmart Financial Holdings Corp., as the context requires. Unless indicated otherwise, all data in this prospectus is presented as June 30, 2012.

Overview

In the opinion of management, we believe we are a leading retailer of alternative financial services to unbanked and underbanked consumers through a network 438 retail storefronts across 14 states. The Company also offers short-term consumer loans via our recently acquired Internet company which services customers in 19 states. We focus on providing a wide range of convenient consumer financial products and services to help customers manage their day-to-day financial needs, including short-term consumer loans, medium-term loans, title loans, check cashing, prepaid debit cards, money transfers, bill payments and money orders. Although the majority of our customers have banking relationships, we believe that our customers use our financial services because they are convenient, easy to understand, and in many instances, more affordable than available alternatives.

We strive to provide customers with unparalleled customer service in a safe, clean and welcoming environment. Our stores are located in highly visible, accessible locations that allow customers convenient and immediate access to our services. Our professional work environment combines high employee performance standards, incentive-based pay and a wide array of training programs to incentivize our employees to provide superior customer service. We believe that this approach has enabled us to build strong customer loyalty, putting us in a position to expand and continue to capitalize on our innovative product offerings. See “Certain Financial Measures and Other Information” for an explanation of how we calculate these metrics.

We serve the large and growing market of individuals who have limited or no access to traditional sources of consumer credit and financial services. A study conducted by the FDIC published in 2009 indicates 25.6% of U.S. households are either unbanked or underbanked, representing approximately 60 million adults. As traditional financial institutions increase fees for consumer services, such as checking accounts and debit cards, and tighten credit standards as a result of economic and other market driven developments, consumers have looked elsewhere for less expensive and more convenient alternatives to meet their financial needs. According to a recent Federal Reserve Bank of New York report, total consumer credit outstanding has declined over $1.4 trillion since its peak in the third quarter of 2008. This contraction in the supply of consumer credit has resulted in significant unmet demand for consumer loan products.

For the year ended December 31, 2011, we generated $306.9 million in revenue and $16.9 million in net income. For the six months ended June 30, 2012, we generated $173.0 million in revenue and $7.2 million in net income. As of June 30, 2012, we had $517.4 million of total assets and $68.7 million of stockholders’ equity.

Our measurement of comparable store sales growth as of December 31, 2011 includes stores which we operated for the full year of 2011 and which were open for the full year of 2010. As of December 31, 2011 we had 280 stores included in this measurement. These stores achieved comparable sales growth of 7.3% for the year ended December 31, 2011 as compared to the year ended December 31, 2010. Our measurement of sales growth as of June 30, 2012 similarly includes stores open for the twelve month periods ended June 30, 2012 and 2011 and was 5.7%.

Products and Services

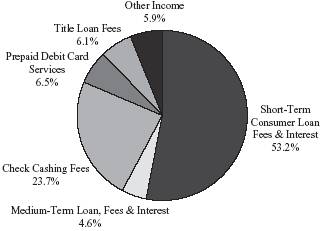

We offer several convenient, fee-based services to meet the needs of our customers, including short-term consumer loans, medium-term loans, title loans, check cashing, prepaid debit cards, money transfers, bill payments, money orders, international and domestic prepaid phone cards, tax preparation, auto insurance, motor vehicle registration services and other ancillary retail financial services. The following chart reflects the major categories of services that we currently offer and the revenues from these services for the year ended December 31, 2011:

Revenue by Product Group |

|

Consumer Loans. We offer a variety of consumer loan products and services. We believe that our customers find our consumer loan products and services to be convenient, transparent and lower-cost alternatives to other, more expensive short-term options, such as incurring returned item fees, credit card late fees, overdraft or overdraft protection fees, utility late payment, disconnect and reconnect fees and other charges imposed by other financing sources when they do not have sufficient funds to cover unexpected expenses or other needs. Our customers often have limited access to more traditional sources of consumer credit, such as credit cards.

The specific consumer loan products we offer vary by location, but generally include the following types of loans:

· Short-Term Consumer Loans. One of our primary products is a short-term, small-denomination consumer loan whereby a customer receives immediate cash, typically in exchange for a post-dated personal check or a pre-authorized debit from his or her bank account.

· Medium-Term Loans. In meeting our customers’ financial needs, we also offer a range of medium-term loans. Principal amounts of medium-term loans typically range from $100 to $2,501 and have maturities between three months and 24 months.

· Title Loans. Title loans are asset-based loans whereby the customer obtains cash using a vehicle as collateral.

Check Cashing. Subject to appropriate approvals, we accept all forms of checks, including payroll, government, tax refund, insurance, money order, cashiers’ and personal checks. Our check cashing fees vary depending upon the amount and type of check cashed, applicable state regulations and local market conditions.

Prepaid Debit Card Services. One of our fastest growing businesses is the sale and servicing of prepaid debit cards. As an agent for a third-party debit card provider, we offer access to reloadable prepaid debit cards with a variety of enhanced features that provide our customers with a convenient and secure method of accessing their funds in a manner that meets their individual needs. The cards are provided by Insight Card Services LLC, successor to Insight LLC, or Insight, and our stores serve as distribution points where customers can purchase cards as well as load funds onto and withdraw funds from their cards.

Other Products and Services. Introducing new products into our markets has historically created profitable revenue expansion. Other products and services that we currently offer through our stores include money transfer, bill payment, international, prepaid phone cards and a pilot auto insurance program.

Historical Acquisitions

California Acquisition. On April 29, 2011, we acquired CCCS, an alternative financial services business with similar product offerings as Checksmart Financial Holdings Corp., or CheckSmart. CheckSmart, together with CCCS and certain other parties, executed an agreement and plan of merger, under which CCFI, a newly formed holding company, acquired all outstanding shares of both CheckSmart and CCCS. We refer to this transaction as the California Acquisition. In connection with consummating the California Acquisition, we also issued $395 million in aggregate principal amount of our 10.75% senior secured notes due 2019, which we refer to as our original notes, and entered into a $40 million senior secured revolving credit facility, which we refer to as our Revolving Credit Facility.

Other Acquisitions. Since August 2009, we have also acquired:

· 10 stores in Illinois, which we acquired on March 21, 2011 in an asset purchase transaction. We refer to this transaction as the Illinois Acquisition.

· 19 stores in Alabama, which we acquired in March 2010. We refer to this transaction as the Alabama Acquisition.

· Eight stores in Michigan, which we acquired in August 2009. We refer to this transaction as the Michigan Acquisition.

Following these acquisitions, we have successfully integrated our expanded product offerings and retailing strategies at acquired stores. The stores acquired in the Alabama and Michigan Acquisitions, both owned and operated for the full year of 2011, experienced revenue growth in excess of 26% in 2011. We have invested significant resources in building a scalable company-wide platform in areas such as collections, call center operations, information technology, legal, compliance and accounting in order to quickly and successfully integrate acquired stores into our existing business.

Recent Acquisitions and Investments

Insight Investment. We acquired a 22.5% stake in Insight Holding Company LLC, or Insight Holding, in November 2011. Insight Holding is the parent company of Insight Cards Services LLC, the program manager for the Insight Card that is offered through our retail locations.

DFS Acquisition. On April 1, 2012 we acquired all of the equity interests of Direct Financial Solutions, LLC and its subsidiaries, or DFS, as well as three other affiliated entities, Direct Financial Solutions of UK Limited and its subsidiary Cash Central UK Limited, or DFS UK, DFS Direct Financial Solutions of Canada, Inc., or DFS Canada, and Reliant Software Inc., all of which we collectively refer to as the DFS Companies. The purchase price was $22,385.

DFS offers short-term loans to consumers via the Internet under a state-licensed model in compliance with the applicable laws of the jurisdiction of its customers. The operations of the DFS Companies are not presently material to the Company.

Currently, DFS offers loans, under a state-law based model, to residents of Alabama, Alaska, California, Delaware, Hawaii, Idaho, Kansas, Louisiana, Minnesota, Missouri, Nevada, North Dakota, Rhode Island, South Dakota, Utah, Washington, Wyoming, and Wisconsin, and operates as a Credit Access Business in Texas, through which it offers loans originated by an unaffiliated, third-party lender. In addition, DFS UK offers loans in the United Kingdom. DFS Canada does not currently offer any loans.

As of April 1, 2012, DFS had 76 employees, including part-time employees, primarily located at DFS’s corporate headquarters in North Logan, Utah, which manages the loan underwriting, collections, information technology, and other aspects of the DFS business. Unless stated otherwise, information in this prospectus regarding our business does not give effect to the acquisition of DFS.

Through our acquisition of DFS, we gain access to a scalable Internet-based revenue opportunity. We believe this additional retail channel will enable us to efficiently reach consumers not fully served by our existing retail locations. Our objective will be to accelerate the growth of DFS through incremental capital, application of retailing strategies and an expansion of its product offerings.

Florida Acquisition. On July 31, 2012, we acquired the assets of a retail consumer finance operator in the state of Florida for a purchase price of $42.1 million, subject to a post-closing working capital adjustment, which we refer to as the Florida Acquisition. The assets acquired in such acquisition are held by Buckeye Check Cashing of Florida II, LLC, a newly formed unrestricted subsidiary, which we refer to as our Current Unrestricted Subsidiary. This retail consumer finance company operated 54 stores in South Florida markets.

We remain in active dialogue with numerous potential acquisition targets. Our historic growth has included acquisitions, which have provided additional revenue through increasing the number of our retail locations, and growth from implementing our business plan and product offerings in newly acquired stores. We plan to continue to execute on this strategy in the future.

INDUSTRY OVERVIEW

We operate in a segment of the financial services industry that serves unbanked and underbanked consumers in need of convenient and immediate access to cash and other financial products and services, often referred to as “alternative financial services”. Our industry provides services to an estimated 60 million unbanked and underbanked consumers in the United States. Products and services offered by this industry segment include various types of short-term loans (including payday loans, title loans, small installment loans, internet loans and pawn loans), medium-term loans, check cashing, prepaid card products, rent-to-own products, bill payment services, tax preparation, money orders and money transfers. Consumers who use these services are often underserved by banks and other traditional financial institutions and referred to as “unbanked” or “underbanked” consumers.

We believe that consumers seek our industry’s services for numerous reasons, including because they often:

· prefer and trust the simplicity, transparency and convenience of our products;

· may have a dislike or distrust of banks due to confusing and complicated fee structures that are not uncommon for traditional bank products;

· require access to financial services outside of normal banking hours;

· have an immediate need for cash for sudden financial challenges and unexpected expenses;

· have been rejected for or are unable to access traditional banking or other credit services;

· seek an alternative to the high cost of bank overdraft fees, credit card and other late payment fees and utility late payment, disconnect and reconnection fees; and

· wish to avoid potential negative credit consequences of missed payments with traditional creditors.

Demand in our industry has been fueled by several demographic and socioeconomic trends, including an overall increase in the population and stagnant to declining growth in the household income for working-class individuals. In addition, many banks have reduced or eliminated services that working-class consumers require, due to the higher costs associated with serving these consumers and increased regulatory and compliance costs. The necessity for our products was highlighted by a recent paper from the NBER, which found that half of the Americans surveyed reported that it is unlikely that they would be able to gather $2,000 to cover a financial emergency, even if given a month to obtain funds. As a result of these trends, a significant number of retailers in other industries have begun to offer financial services to these consumers. The providers of these services are fragmented and range from specialty finance stores to retail stores in other industries that offer ancillary financial services.

We believe that the markets in which we operate are highly fragmented. Stephens estimates that short-term consumer lenders generated approximately $40.0 billion of domestic transaction volume in 2010 from approximately 19,500 storefronts and 150 online lenders. According to Stephens, only seven industry participants have more than 500 storefront locations, and the largest 15 operators account for less than 51% of the storefronts in the United States. FiSCA estimated that in 2007 there were approximately 13,000 check-cashing and other fee-based financial service locations in the United States that cashed approximately $58.0 billion in aggregate face amount of checks.

We anticipate consolidation within the industry will continue as a result of numerous factors, including:

· economies of scale available to larger operators;

· adoption of technology to better serve customers and control large store networks;

· increased licensing, zoning and other regulatory requirements; and

· the inability of smaller operators to form the alliances necessary to deliver new products and adapt to changes in the regulatory environment.

The prepaid debit card space is one of the most rapidly growing segments of our industry. Mercator’s analysis of the prepaid debit card industry indicates that $28.6 billion was loaded onto general-purpose reloadable cards during 2009, a 47% growth rate from 2008, and estimates that the total general-purpose reloadable card market will grow at a compound annual growth rate of 63% from 2007 to 2013, reaching an estimated $201.9 billion in load volume by 2013. A March 2011 study conducted by Bretton Woods concluded that the opening of reloadable prepaid debit card accounts may surpass the opening of new checking accounts in the coming years as a result of the fact that prepaid debit cards, particularly when combined with direct deposit, will in many instances be less expensive for consumers than traditional checking accounts.

We take an active leadership role in numerous trade organizations that represent our industry’s interests and promote best practices within the industry, including the Community Financial Services Association of America, FiSCA, the National Branded Prepaid Card Association and the American Association of Responsible Auto Lenders.

OUR ORGANIZATIONAL STRUCTURE

The following chart illustrates the organizational structure of our wholly-owned subsidiaries:

________________________________________

(1) One of our subsidiaries, Insight Capital, LLC, is the borrower under a revolving credit facility, which we refer to as the Alabama Facility. See “Description of Certain Indebtedness”.

(2) Our newly formed unrestricted subsidiary, Buckeye Check Cashing of Florida II, LLC, which we refer to as our Current Unrestricted Subsidiary, holds the assets acquired in the Florida Acquisition.

CCFI operates through 13 brands: Checksmart, Buckeye Checksmart, California Check Cashing Stores, Buckeye Title Loans, Cash1, easymoney, First Virginia, Southwest Check Cashing, Express, First Cash Advance, Check Cashing USA, Cash Central internet brand, and Foremost. We acquired the majority of these brand names through both licensing and acquisitions, and we have retained these distinct brand names to avoid customer confusion and the expense of re-branding our store locations. In the case of First Virginia, this brand evolved to differentiate the traditional Checksmart operations in Virginia from the open-ended credit product offered in Virginia solely at the First Virginia locations, and in the case of Buckeye Title Loans, this brand evolved to differentiate title-secured lending from the unsecured loan products offered at Checksmart locations.

OUR LARGEST SHAREHOLDER

Founded in 2004, Diamond Castle is a leading private equity investment firm with over $1.85 billion of capital under management. The Diamond Castle partners have an established history of successful investing at DLJ Merchant Banking Partners dating back to the early 1990s. The firm invests across a range of industries, with particular focus on the financial services, energy and power, and healthcare sectors. The Community Choice Financial investment was led by H. Eugene Lockhart, the Chairman of Financial Institutions at Diamond Castle, former President of the Global Retail Bank at Bank of America, CEO of MasterCard International and Chairman of NetSpend Corporation. In addition to Community Choice Financial, Diamond Castle’s current portfolio of companies includes Alterra Capital, EverBank Financial, Beacon Health Strategies, Managed Health Care Associates, KDC Solar and Professional Directional. Diamond Castle beneficially owns approximately 60.2% of our outstanding common shares. See “Risk Factors — Diamond Castle has substantial influence over us, and their interests in our business may be different from yours” for additional information regarding Diamond Castle’s control of us.

EMERGING GROWTH COMPANY STATUS

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. For as long as we are an “emerging growth company,” we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding advisory “say-on-pay” votes on executive compensation and shareholder advisory votes on golden parachute compensation.

Under the JOBS Act, we will remain an “emerging growth company” until the earliest of:

· the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more;

· the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement;

· the date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt; and

· the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, or the Exchange Act.

Section 107 of the JOBS Act provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to not delay such adoption of new or revised accounting standards, and such election is irrevocable.

CORPORATE INFORMATION

Community Choice Financial Inc. was formed on April 6, 2011 under the laws of the State of Ohio by the shareholders of CheckSmart Financial Holdings Inc. to be the holding company of CheckSmart Financial Holdings Corp. and to acquire the ownership interests of CCCS Corporate Holdings, Inc. through a merger. CCFI acquired CCCS through a merger on April 29, 2011. As of June 30, 2012, we owned and operated 438 stores in 14 states and lend to consumers via the internet in 19 states. We are primarily engaged in the business of providing consumer retail financial services and have grown from 179 stores in April 2006, when Diamond Castle purchased a majority interest in CheckSmart.

Our corporate offices are located at 7001 Post Road, Suite 200, Dublin, Ohio 43016. Our telephone number is (614) 798-5900 and our website is located at www.ccfi.com. Information appearing on or accessible through our website is not part of this prospectus.

SUMMARY OF THE EXCHANGE OFFER

On April 29, 2011, we issued the original notes in transactions exempt from registration under Rule 144A and Regulation S under the Securities Act. The initial purchasers of the original notes were Credit Suisse Securities (USA) LLC, Jefferies & Company, Inc. and Stephens Inc., who completed the resale of the original notes to qualified institutional buyers on April 29, 2011. In connection with the offering of the original notes, we entered into a registration rights agreement, dated as of April 29, 2011, with the initial purchasers of the original notes, or the registration rights agreement. In the registration rights agreement, we agreed to offer the exchange notes, which will be registered under the Securities Act, in exchange for the original notes. The exchange offer is intended to satisfy our obligations under the registration rights agreement. We also agreed to deliver this prospectus to the holders of the original notes. You should read the discussions under the headings “Prospectus Summary—Summary of the Terms of the Exchange Notes” and “Description of the Exchange Notes” for information regarding the exchange notes.

The Exchange Offer | This is an offer to exchange $2,000 and integral multiples of $1,000 in principal amount of the exchange notes for each $2,000 and integral multiples of $1,000 in principal amount of original notes. The exchange notes are substantially identical to the original notes, except that the exchange notes generally will be freely transferable. Based upon interpretations by the staff of the Securities and Exchange Commission, or the SEC, set forth in no actions letters issued to unrelated third parties, we believe that you can transfer the exchange notes without complying with the registration and prospectus delivery provisions of the Securities Act if you: | |

|

| |

| · | acquire the exchange notes in the ordinary course of your business; |

|

|

|

| · | are not and do not intend to become engaged in a distribution of the exchange notes; |

|

|

|

| · | are not an “affiliate” (within the meaning of the Securities Act) of ours; |

|

|

|

| · | are not a broker-dealer (within the meaning of the Securities Act) that acquired the original notes from us or our affiliates; and |

|

|

|

| · | are not a broker-dealer (within the meaning of the Securities Act) that acquired the original notes in a transaction as part of its market-making or other trading activities. |

|

| |

| If any of these conditions are not satisfied and you transfer any exchange note without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. See “The Exchange Offer—Purpose of the Exchange Offer.” You may not participate in the exchange offer if you are an “affiliate” (within the meaning of the Securities Act) or a broker-dealer that acquired outstanding notes directly from us. | |

|

| |

Registration Rights Agreement | Under the registration rights agreement, we have agreed to use our reasonable best efforts to consummate the exchange offer or cause the original notes to be registered under the Securities Act to permit resales. If we are not in compliance with our obligations under the registration rights agreement, liquidated damages will accrue on the original notes in addition to the interest that otherwise is due on the original notes. If the exchange offer is completed on the terms and within the time period contemplated by this prospectus, no liquidated damages will be payable on the original notes. The exchange notes will not contain any provisions regarding the payment of liquidated damages. See “The Exchange Offer—Liquidated Damages.” | |

|

| |

Minimum Condition | The exchange offer is not conditioned on any minimum aggregate principal amount of original notes being tendered in the exchange offer. | |

|

| |

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on October 19, 2012, unless we extend it. | |

|

| |

Exchange Date | We will accept original notes for exchange at the time when all conditions of the exchange offer are satisfied or waived. We will deliver the exchange notes promptly after we accept the original notes. | |

|

| |

Conditions to the Exchange Offer | Our obligation to complete the exchange offer is subject to certain conditions. See “The Exchange Offer—Conditions to the Exchange Offer.” We reserve the right to | |

| terminate or amend the exchange offer at any time prior to the expiration date upon the occurrence of certain specified events. |

|

|

Withdrawal Rights | You may withdraw the tender of your original notes at any time before the expiration of the exchange offer on the expiration date. Any original notes not accepted for any reason will be returned to you without expense as promptly as practicable after the expiration or termination of the exchange offer. |

|

|

Procedures for Tendering Original Notes | See “The Exchange Offer—How to Tender.” |

|

|

United States Federal Income Tax Consequences | The exchange of the original notes for the exchange notes will not be a taxable exchange for U.S. federal income tax purposes, and holders will not recognize any taxable gain or loss as a result of such exchange. See “Certain United States Federal Income Tax Considerations.” |

|

|

Effect on Holders of Original Notes | If the exchange offer is completed on the terms and within the period contemplated by this prospectus, holders of original notes will have no further registration or other rights under the registration rights agreement, except under limited circumstances. See “The Exchange Offer—Other.” |

|

|

| Holders of original notes who do not tender their original notes will continue to hold those original notes. All untendered, and tendered but unaccepted original notes, will continue to be subject to the transfer restrictions provided for in the original notes and the Indenture. To the extent that original notes are tendered and accepted in the exchange offer, the trading market, if any, for the original notes could be adversely affected. See “Risk Factors—Risks Associated with the Exchange Offer—You may not be able to sell your original notes if you do not exchange them for registered exchange notes in the exchange offer,” “Risk Factors—Your ability to sell your original notes may be significantly more limited and the price at which you may be able to sell your original notes may be significantly lower if you do not exchange them for registered exchange notes in the exchange offer” and “The Exchange Offer—Other.” |

|

|

Appraisal Rights | Holders of original notes do not have appraisal or dissenters’ rights under applicable law or the Indenture. See “The Exchange Offer—Terms of the Exchange Offer.” |

|

|

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes pursuant to the exchange offer. |

|

|

Exchange Agent | U.S. Bank National Association, the trustee under the Indenture, is serving as the exchange agent in connection with this exchange offer. |

SUMMARY OF THE TERMS OF THE EXCHANGE NOTES

Issuer | Community Choice Financial Inc. | |

|

| |

Exchange Notes | $395,000,000 in aggregate principal amount of 10.75% Senior Secured Notes due 2019. | |

|

| |

Maturity Date | May 1, 2019. | |

|

| |

Interest | 10.75% per annum, payable semi-annually on May 1 and November 1. | |

|

| |

Guarantees | The exchange notes will be guaranteed, jointly and severally, on a senior secured basis, by each of our restricted subsidiaries as of April 29, 2011 (the date we issued the original notes) and any subsequent restricted subsidiaries that guarantee our indebtedness or indebtedness of any subsidiary guarantor. See “Description of the Exchange Notes—Note Guarantees”. | |

|

| |

Collateral | The exchange notes and the guarantees will be secured by a first priority lien on substantially all the present and after-acquired tangible and intangible assets of CCFI and the subsidiary guarantors, or the Collateral, subject to certain exceptions and permitted liens (including liens on the assets of our Alabama subsidiary as security for the Alabama Facility), equal and ratable with the obligations under our Revolving Credit Facility and certain hedging obligations. See “Description of the Exchange Notes—Security for the Notes”. | |

|

| |

| The Collateral will not include certain categories of assets. See “Risk Factors—Risks Relating to the Notes—There are certain categories of property that are excluded from the Collateral”. | |

|

| |

| No appraisal of the value of the Collateral has been made in connection with the offering of original notes or the exchange offer, and the value of Collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the Collateral. The liens on the Collateral may be released without the consent of the holders of the notes if Collateral is disposed of in a transaction that complies with the Indenture and the applicable security documents. In the event of a liquidation of the Collateral, the available proceeds may not be sufficient to satisfy the obligations under the exchange notes. See “Risks Relating to the Notes—The Collateral may not be valuable enough to satisfy all the obligations secured by such Collateral” and “Description of the Exchange Notes—Security for the Notes.” | |

|

| |

Ranking | Except as described below with respect to the assets of our Alabama subsidiary that secure the Alabama Facility on a first-priority basis and secure the original notes and our Revolving Credit Facility on a second-priority basis, or the Shared Alabama Collateral, the exchange notes and the guarantees will be our and the subsidiary guarantors’ senior secured obligations and will: | |

|

| |

| · | rank pari passu in right of payment with all existing and future senior indebtedness; |

|

|

|

| · | rank senior in right of payment to all of our and the subsidiary guarantors’ future subordinated debt; |

|

|

|

| · | be effectively senior to any unsecured indebtedness to the extent of the value of the Collateral (after giving effect to any senior lien on such Collateral, including liens on the assets of our Alabama subsidiary as security for the Alabama Facility, and the contractual priority of our Revolving Credit Facility and certain |

|

| hedging obligations with respect to proceeds of the Collateral); |

|

|

|

| · | be effectively subordinated to any indebtedness that is secured by liens on assets that do not constitute a part of the Collateral, to the extent of the value of such assets; and |

|

|

|

| · | be structurally subordinated to any existing or future indebtedness and other liabilities, including preferred stock and indebtedness of any future subsidiaries that do not guarantee the exchange notes (other than indebtedness and liabilities owed to us or one of our subsidiary guarantors). |

|

| |

| With respect to the Collateral, the indebtedness and obligations under the exchange notes, our Revolving Credit Facility and certain future indebtedness and obligations permitted under the Indenture will have first-priority liens (except with respect to the Shared Alabama Collateral described below). Under the terms of the security documents, however, in the event of a foreclosure on the Collateral or insolvency proceedings, upon acceleration of obligations under our Revolving Credit Facility pursuant to applicable law, or if our obligations under our Revolving Credit Facility otherwise become due, the holders of the exchange notes will receive proceeds from such enforcement, insolvency proceeding or acceleration, only after the repayment of amounts due including interest, under our Revolving Credit Facility and certain hedging obligations. See “Description of the Exchange Notes—Security for the Notes—Designated Priority Obligations”. | |

|

| |

| With respect to the Shared Alabama Collateral, the Alabama Facility is secured by first-priority liens, and the exchange notes and our Revolving Credit Agreement are secured by second-priority liens. The Shared Alabama Collateral consists of substantially all of the assets of our Alabama subsidiary, or the Shared Alabama Collateral. The lien priority with respect to the Shared Alabama Collateral is governed by an intercreditor agreement. See “Description of the Exchange Notes—Security for the Notes—Alabama Intercreditor Arrangement”. | |

|

| |

| As of June 30, 2012, (1) our outstanding senior indebtedness was approximately $395 million, all of which was secured indebtedness; (2) we had no obligations ranking pari passu with or senior to the original notes; and (3) we had $39.5 million of availability under our Revolving Credit Facility, after deducting $0.5 million of outstanding and undrawn letters of credit thereunder, and our Alabama subsidiary had $7.0 million of availability under the Alabama Facility. Our Alabama subsidiary accounted for approximately $30.7 million, or 9.2%, of our pro forma revenue for 2011, approximately $27.2 million, or 5.3%, of our pro forma total assets and approximately $3.3 million, or 0.7%, of our pro forma total liabilities, in each case, as of December 31, 2011 (in each case, excluding intercompany balances). | |

|

| |

Optional Redemption | Prior to May 1, 2015, we may redeem the exchange notes, in whole or in part, at a price equal to 100% of the principal amount thereof plus the “make whole” premium described under “Description of the Exchange Notes—Optional Redemption”, plus accrued and unpaid interest to the redemption date. Thereafter, we may redeem some or all of the exchange notes at the redemption prices listed under “Description of the Exchange Notes—Optional Redemption”, plus accrued and unpaid interest to the redemption date. | |

|

| |

| At any time (which may be more than once) prior to May 1, 2014, we may redeem up to 35% in total of the aggregate principal amount of the notes at a redemption price of 110.750% of the aggregate principal amount thereof, plus accrued and unpaid interest to the redemption date, with the net proceeds of certain equity offerings. See “Description of the Exchange Notes—Optional Redemption”. | |

|

| |

| In addition, during each 12-month period commencing on May 1, 2011 and ending | |

| on or prior to May 1, 2015, we may redeem up to 10% of the aggregate principal amount of the notes at a redemption price equal to 103% of the principal amount thereof, plus accrued and unpaid interest to the redemption date. See “Description of the Exchange Notes—Optional Redemption”. | |

|

| |

Change of Control | If we experience certain kinds of changes of control, we must offer to purchase the notes at 101% of their principal amount, plus accrued and unpaid interest. See “Description of the Exchange Notes—Repurchase at the Option of Holders—Change of Control”. | |

|

| |

Mandatory Offer to Repurchase Following Certain Asset Sales | If we sell certain assets, under certain circumstances we must offer to repurchase the notes at par. See “Description of the Exchange Notes—Repurchase at the Option of Holders—Asset Sales”. | |

|

| |

Certain Covenants | The Indenture contains covenants that, among other things, limit our ability and the ability of our restricted subsidiaries to: | |

|

| |

| · | make restricted payments; |

|

|

|

| · | make investments; |

|

|

|

| · | incur additional debt or issue certain preferred shares; |

|

|

|

| · | create liens; |

|

|

|

| · | merge or consolidate, or sell, transfer or otherwise dispose of substantially all of our assets; |

|

|

|

| · | enter into certain transactions with affiliates; and |

|

|

|

| · | designate our subsidiaries as unrestricted. |

|

| |

| The covenants applicable to us and our restricted subsidiaries are subject to a number of important qualifications and limitations. See “Description of the Exchange Notes—Certain Covenants”. | |

|

| |

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes pursuant to the exchange offer. | |

|

| |

Absence of public market for the exchange notes | The exchange notes are a new issue of securities, and there is currently no established trading market for the exchange notes. The exchange notes generally will be freely transferable. We do not intend to apply for a listing of the exchange notes on any securities exchange or an automated dealer quotation system. Accordingly, there can be no assurance as to the development or liquidity of any market for the exchange notes. | |

|

| |

Trustee | U.S. Bank National Association is the trustee for the holders of the exchange notes. | |

Governing Law | The exchange notes, the Indenture and the other documents for the offering of the exchange notes are governed by the laws of the State of New York. |

The terms of the exchange notes are substantially identical to the original notes, except that the exchange notes generally will be freely transferable. For additional information about the exchange notes, see the section of this prospectus entitled “Description of the Exchange Notes.”

Regulatory Approvals

Other than the federal securities laws, there are no federal or state regulatory requirements that we must comply with and there are no approvals that we must obtain in connection with the exchange offer.

Participating in the exchange offer involves certain risks. You should carefully consider the information under “Risk Factors” and all other information included in this prospectus before participating in the exchange offer.

Ratio of Earnings to Fixed Charges

Our ratio of earnings to fixed charges is set forth on page 49 of this prospectus.

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table sets forth CCFI’s summary historical consolidated financial and other data, as of December 31, 2010 and 2011 and for the years ended December 31, 2009, 2010 and 2011 and as of June 30, 2011 and 2012 and for the six-month periods ended June 30, 2011 and 2012. The summary historical financial and other data as of December 31, 2010 and 2011 and for each of the years ended December 31, 2009, 2010 and 2011 have been derived from, and should be read together with, CCFI’s audited historical consolidated financial statements and the accompanying notes included elsewhere in this prospectus. The summary historical financial and other data as of June 30, 2012 and for each of the six-month periods ended June 30, 2011 and 2012 have been derived from, and should be read together with, CCFI’s unaudited historical consolidated financial statements and the accompanying notes included elsewhere in this prospectus. The summary historical financial and other data as of June 30, 2011 have been derived from CCFI’s unaudited historical consolidated financial statements not included in this prospectus. The unaudited financial data includes, in our opinion, all adjustments (consisting only of normal recurring adjustments) that are necessary for a fair presentation of our financial position and results of operations for these periods.

The results of operations for the periods presented below are not necessarily indicative of the results to be expected for any future period. You should read the following information in conjunction with “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and CCFI’s consolidated financial statements and related notes included elsewhere in this prospectus.

|

| Year Ended December 31, |

| Six-months Ended June 30, |

| |||||||||||

(In thousands) |

| 2009 |

| 2010 |

| 2011 |

| 2011 |

| 2012 |

| |||||

Revenues: |

|

|

|

|

|

|

|

|

|

|

| |||||

Finance receivable fees |

| $ | 136,957 |

| $ | 146,059 |

| $ | 196,153 |

| $ | 81,471 |

| $ | 114,895 |

|

Check cashing fees |

| 53,049 |

| 55,930 |

| 72,800 |

| 32,814 |

| 38,133 |

| |||||

Card fees |

| 2,063 |

| 10,731 |

| 19,914 |

| 8,757 |

| 8,500 |

| |||||

Other |

| 10,614 |

| 11,560 |

| 18,067 |

| 8,218 |

| 11,479 |

| |||||

Total revenues |

| 202,683 |

| 224,280 |

| 306,934 |

| 131,260 |

| 173,007 |

| |||||

Branch expenses: |

|

|

|

|

|

|

|

|

|

|

| |||||

Salaries and benefits |

| 34,343 |

| 38,759 |

| 57,411 |

| 24,129 |

| 31,528 |

| |||||

Provision for loan losses |

| 43,463 |

| 40,316 |

| 65,351 |

| 23,694 |

| 37,827 |

| |||||

Occupancy |

| 13,855 |

| 14,813 |

| 21,216 |

| 8,840 |

| 11,129 |

| |||||

Depreciation and amortization |

| 6,613 |

| 5,318 |

| 5,907 |

| 2,545 |

| 3,104 |

| |||||

Other |

| 22,652 |

| 27,994 |

| 35,515 |

| 15,728 |

| 22,534 |

| |||||

Total branch expenses |

| 120,926 |

| 127,200 |

| 185,400 |

| 74,936 |

| 106,122 |

| |||||

Branch gross profit |

| 81,757 |

| 97,080 |

| 121,534 |

| 56,324 |

| 66,885 |

| |||||

Corporate expenses |

| 31,518 |

| 33,940 |

| 44,742 |

| 21,683 |

| 25,781 |

| |||||

Registration expenses |

| — |

| — |

| — |

| — |

| 2,744 |

| |||||

Transaction expense |

| — |

| 237 |

| 9,351 |

| 8,698 |

| 1,037 |

| |||||

Depreciation and amortization |

| 568 |

| 1,222 |

| 2,332 |

| 1,012 |

| 2,466 |

| |||||

Interest expense, net |

| 11,532 |

| 8,501 |

| 34,334 |

| 11,660 |

| 22,580 |

| |||||

Equity investment loss |

| — |

| — |

| 415 |

| 216 |

| 155 |

| |||||

Nonoperating income, management fees |

| (172 | ) | (46 | ) | (46 | ) | (22 | ) | (30 | ) | |||||

Income before income taxes and discontinued operations |

| 38,311 |

| 53,226 |

| 30,406 |

| 13,077 |

| 12,122 |

| |||||

Provision for income taxes |

| 14,042 |

| 19,801 |

| 13,553 |

| 6,137 |

| 4,934 |

| |||||

Income from continuing operations |

| 24,269 |

| 33,425 |

| 16,853 |

| 6,940 |

| 7,188 |

| |||||

Discontinued operations (net of provision (benefit) for income tax of $226, ($1,346), $0, $0 and $0) |

| 368 |

| (2,196 | ) | — |

| — |

| — |

| |||||

Net income |

| 24,637 |

| 31,229 |

| 16,853 |

| 6,940 |

| 7,188 |

| |||||

Net loss attributable to non-controlling interests |

| — |

| (252 | ) | (120 | ) | (120 | ) | — |

| |||||

Net income attributable to controlling interests |

| $ | 24,637 |

| $ | 31,481 |

| $ | 16,973 |

| $ | 7,060 |

| $ | 7,188 |

|

(In thousands, except for stores data, averages, |

| Year Ended December 31, |

| Six-months Ended June 30, |

| |||||||||||

percentages or unless otherwise specified) |

| 2009 |

| 2010 |

| 2011 |

| 2011 |

| 2012 |

| |||||

Balance Sheet Data (at period end): |

|

|

|

|

|

|

|

|

|

|

| |||||

Cash and cash equivalents |

| $ | 27,959 |

| $ | 39,780 |

| $ | 65,635 |

| $ | 57,084 |

| $ | 66,875 |

|

Finance receivables, net |

| 66,035 |

| 81,337 |

| 120,451 |

| 96,997 |

| 108,192 |

| |||||

Total assets |

| 280,476 |

| 310,644 |

| 515,547 |

| 480,668 |

| 517,355 |

| |||||

Total debt |

| 193,365 |

| 188,934 |

| 395,000 |

| 395,000 |

| 395,000 |

| |||||

Total stockholders’ equity |

| 77,791 |

| 109,791 |

| 61,314 |

| 51,348 |

| 68,747 |

| |||||

Other Operating Data (unaudited): |

|

|

|

|

|

|

|

|

|

|

| |||||

Number of stores (at period end) |

| 264 |

| 282 |

| 435 |

| 433 |

| 438 |

| |||||

Short-term consumer loans data: |

|

|

|

|

|

|

|

|

|

|

| |||||

Loan volume |

| $ | 1,162,086 |

| $ | 1,237,163 |

| $ | 1,543,310 |

| $ | 651,816 |

| $ | 811,622 |

|

Number of loans |

| 2,816 |

| 2,956 |

| 3,625 |

| 1,574 |

| 1,980 |

| |||||

Average new loan size |

| $ | 412.67 |

| $ | 418.53 |

| $ | 425.72 |

| $ | 413.97 |

| $ | 409.84 |

|

Average new loan fee |

| $ | 42.79 |

| $ | 43.14 |

| $ | 46.37 |

| $ | 44.22 |

| $ | 47.42 |

|

Loan loss provision |

| $ | 28,856 |

| $ | 27,560 |

| $ | 40,636 |

| $ | 14,932 |

| $ | 20,983 |

|

Loan loss provision as a percentage of volume |

| 2.5 | % | 2.2 | % | 2.6 | % | 2.3 | % | 2.6 | % | |||||

Check cashing data: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Face amount of checks cashed |

| $ | 1,309,425 |

| $ | 1,442,501 |

| $ | 2,163,276 |

| $ | 929,135 |

| $ | 1,196,145 |

|

Number of checks cashed |

| 3,029 |

| 3,292 |

| 4,869 |

|

| 2,015 |

|

| 2,603 |

| |||

Face amount of average check |

| $ | 432.08 |

| $ | 438.13 |

| $ | 444.26 |

| $ | 461.11 |

| $ | 459.44 |

|

Average fee per check |

| $ | 17.51 |

| $ | 16.99 |

| $ | 14.95 |

| $ | 16.29 |

| $ | 14.66 |

|

Returned check expense |

| $ | 3,058 |

| $ | 3,034 |

| $ | 5,085 |

| $ | 2,013 |

| $ | 2,409 |

|

Returned check expense as a percentage of face amount of checks cashed |

| 0.2 | % | 0.2 | % | 0.2 | % | 0.2 | % | 0.2 | % | |||||

(In thousands, except for stores data, averages, |

| Year Ended December 31, |

| Six-months Ended June 30, |

| |||||||||||

percentages or unless otherwise specified) |

| 2009 |

| 2010 |

| 2011 |

| 2011 |

| 2012 |

| |||||

Medium-term loan data:(1) |

|

|

|

|

|

|

|

|

|

|

| |||||

Principal outstanding |

| $ | 3,109 |

| $ | 3,601 |

| $ | 12,174 |

| $ | 5,699 |

| $ | 12,797 |

|

Number of loans outstanding |

| 9,365 |

| 10,275 |

| 20,818 |

| 15,452 |

| 21,215 |

| |||||

Average principal outstanding |

| $ | 331.97 |

| $ | 350.47 |

| $ | 584.79 |

| $ | 368.86 |

| $ | 603.22 |

|

Average monthly percentage rate |

| 22.3 | % | 22.0 | % | 19.2 | % | 24.1 | % | 18.9 | % | |||||

Allowance as a percentage of finance receivable |

| 42.7 | % | 11.7 | % | 10.6 | % | 10.2 | % | 19.8 | % | |||||

Loan loss provision |

| $ | 6,708 |

| $ | 5,267 |

| $ | 11,470 |

| $ | 3,722 |

| $ | 6,799 |

|

Title loan data: |

|

|

|

|

|

|

|

|

|

|

| |||||

Principal outstanding |

| $ | 6,047 |

| $ | 9,541 |

| $ | 17,334 |

| $ | 9,089 |

| $ | 17,342 |

|

Number of loans outstanding |

| 6,077 |

| 9,597 |

| 15,283 |

| 9,229 |

| 18,208 |

| |||||

Average principal outstanding |

| $ | 995.00 |

| $ | 994.12 |

| $ | 1,134.20 |

| $ | 984.82 |

| $ | 952.45 |

|

Average monthly percentage rate |

| 16.0 | % | 13.8 | % | 13.3 | % | 15.8 | % | 13.0 | % | |||||

Allowance as a percentage of finance receivable |

| 12.1 | % | 5.3 | % | 5.3 | % | 6.0 | % | 6.9 | % | |||||

Loss loss provision |

| $ | 2,970 |

| $ | 3,497 |

| $ | 5,463 |

| $ | 1,697 |

| $ | 3,365 |

|

Overall company data: |

|

|

|

|

|

|

|

|

|

|

| |||||

Total revenues |

| $ | 202,683 |

| $ | 224,280 |

| $ | 306,934 |

| $ | 131,260 |

| $ | 172,281 |

|

Loan loss provisions |

| 41,592 |

| 39,358 |

| 62,654 |

| 22,364 |

| 33,556 |

| |||||

Other ancillary product provisions |

| 1,871 |

| 958 |

| 2,697 |

| 1,330 |

| 4,271 |

| |||||

Total loan loss provision |

| $ | 43,463 |

| $ | 40,316 |

| $ | 65,351 |

| 23,694 |

| 37,827 |

| ||

Total loan loss provision as a percentage of revenue |

| 21.4 | % | 18.0 | % | 21.3 | % | 18.1 | % | 21.9 | % | |||||

Other Financial Data (unaudited): |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Capital expenditures |

| $ | 2,769 |

| $ | 1,688 |

| $ | 4,261 |

| 1,136 |

| 1,893 |

| ||

(1) Loan participations are grouped with medium-term loans in our consolidated financial statements included elsewhere in this prospectus, but are excluded from these calculations.

SUMMARY UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL INFORMATION

The pro forma information set forth below gives effect to the California Acquisition, the Illinois Acquisition, the offering of our original notes and the establishment of our Revolving Credit Facility as if they had each occurred on January 1, 2011. We have derived the pro forma consolidated financial data for the year ended December 31, 2011 by calculating the historical consolidated financial data for the period ended December 31, 2011 for CCFI and for the period ended April 29, 2011 for CCCS, the date of the California Acquisition, and then applying pro forma adjustments to give effect to such transactions. The pro forma information is unaudited, is for informational purposes only and is not necessarily indicative of what our financial position or results of operations would have been had such transactions been completed as of the dates indicated and does not purport to represent what our results of operations might be for any future period.

The following summary pro forma consolidated financial data should be read in conjunction with “Selected Historical Consolidated Financial Data”, “Unaudited Pro Forma Consolidated Financial Information”, “Use of Proceeds”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, and the consolidated financial statements of CCFI and CCCS and the accompanying notes thereto included elsewhere in this prospectus.

(In thousands) |

| Year Ended |

| |

Revenue: |

|

|

| |

Finance receivable fees |

| $ | 208,093 |

|

Check cashing fees |

| 82,272 |

| |

Card fees |

| 20,611 |

| |

Other |

| 21,751 |

| |

Total revenue |

| 332,727 |

| |

Salaries and benefits |

| 65,286 |

| |

Provision for loan losses |

| 67,832 |

| |

Occupancy |

| 24,207 |

| |

Depreciation and amortization |

| 6,050 |

| |

Other |

| 37,653 |

| |

Total branch expenses |

| 201,028 |

| |

Branch gross profit |

| 131,699 |

| |

Corporate Expenses |

| 47,158 |

| |

Depreciation and amortization |

| 3,407 |

| |

Interest expense, net |

| 45,140 |

| |

Goodwill impairment |

| 28,986 |

| |

Equity investment loss |

| 415 |

| |

Non-operating income, mgmt fees |

| (46 | ) | |

Income before taxes and discontinued operations |

| 6,639 |

| |

Provision for income taxes |

| 2,523 |

| |

Total net income |

| $ | 4,116 |

|

Participating in the exchange offer involves risks. You should carefully consider the risks described below, together with the other information contained in this prospectus, before you decide to participate in the exchange offer. Any of the following risks, as well as other risks and uncertainties, could harm the value of the notes directly, or our business and financial results and thus indirectly cause the value of the notes to decline. The risks described below are not the only ones that could impact our company or the value of the notes. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition or results of operations. As a result of any of these risks, known or unknown, you may lose all or part of your investment in the notes.

Risks Relating to the Notes

Our substantial indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under the notes or other indebtedness.

We have a significant amount of indebtedness. As of June 30, 2012, our outstanding senior indebtedness was approximately $395 million, all of which was secured indebtedness, and we had availability of $39.5 million under our Revolving Credit Facility, and our Alabama subsidiary’s borrowing availability under its secured credit facility was $7 million.

Our substantial indebtedness could have important consequences to you. For example, it could:

· make it more difficult for us to satisfy our obligations with respect to the notes and our other indebtedness;

· require us to dedicate a substantial portion of our cash flow from operations to payments of principal and interest on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, business development, acquisitions, general corporate or other purposes;

· increase our vulnerability to and limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

· increase our vulnerability to general adverse economic and industry conditions;

· restrict us from making strategic acquisitions or cause us to make non-strategic divestitures;

· place us at a competitive disadvantage compared to our competitors that have less debt; and

· limit our ability to refinance our indebtedness, including the notes, or to obtain additional debt or equity financing for working capital, capital expenditures, business development, debt service requirements, acquisitions and general corporate or other purposes.

We expect to use cash flow from operations and borrowings under our revolving credit facilities to meet our current and future financial obligations, including funding our operations, debt service requirements, small acquisitions and capital expenditures. Our ability to make these payments depends on our future performance, which will be affected by financial, business, economic and other factors, many of which we cannot control. Our business may not generate sufficient cash flow from operations in the future, which could result in our being unable to repay indebtedness or to fund other liquidity needs.

Risks of leverage and debt service requirements may hamper our ability to operate and grow our revenues.

Our debt-to-equity ratio is high due to the requirement of borrowing funds to continue operations. High leverage creates risks, including the risk of default under our Revolving Credit Facility or our notes. The interest expense associated with our debt burden may be substantial and may create a significant drain on our future cash flow. These payments may also place us at a disadvantage relative to other better capitalized competitors and increase the impact of competitive pressures within our markets. For more information regarding the impact of our substantial indebtedness, please see “—Our substantial indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under our notes or other indebtedness.” As of June 30, 2012, our total debt was $395.0 million and our negative tangible capital was $207.2 million.

Despite our current level of indebtedness, we may still be able to incur substantial additional indebtedness. This could exacerbate the risks associated with our substantial indebtedness.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future. The terms of the Indenture and the agreement governing our Revolving Credit Facility limit, but do not prohibit, us or our subsidiaries from incurring additional indebtedness. If we incur any additional indebtedness the holders of that indebtedness will be entitled to share ratably with our other secured and unsecured creditors in any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or other winding-up of our business prior to any recovery by our shareholders. This may have the effect of reducing the amount of proceeds paid to you in such an event. If new indebtedness, including under our revolving credit facilities, is added to our current debt levels, the related risks that we and our subsidiaries now face could intensify, especially with respect to the demands on our liquidity as a result of increased interest commitments.

To service our indebtedness, we will require a significant amount of cash, and our ability to generate cash depends on many factors beyond our control.

Our ability to make scheduled cash payments on and to refinance our indebtedness, including the notes, and to fund planned capital expenditures will depend on our ability to generate significant operating cash flow in the future, which, to a significant extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. We may not be able to maintain a sufficient level of cash flow from operating activities to permit us to pay the principal, premium, if any, and interest on the notes and our other indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital or seek to restructure or refinance our indebtedness, including the notes. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations. In the absence of such cash flows and resources, we could face substantial liquidity problems and might be required to sell material assets or operations in an attempt to meet our debt service and other obligations. The Indenture and the agreement governing our Revolving Credit Facility will restrict our ability to conduct asset sales and/or use the proceeds from asset sales. We may not be able to consummate those asset sales to raise capital or sell assets at prices and on terms that we believe are fair and any proceeds that we receive may not be adequate to meet any debt service obligations then due. See “Description of Certain Indebtedness” and “Description of the Exchange Notes”.

We are dependent upon our lenders for financing to execute our business strategy and meet our liquidity needs. If our lenders are unable to fund borrowings under their credit commitments or we are unable to borrow, it could negatively impact our business.

We may be exposed to the risk that lenders under our Revolving Credit Facility could fail or refuse to honor their legal commitments and obligations thereunder. If our lenders are unable to fund borrowings under their credit commitments, it could be difficult to replace our Revolving Credit Facility on similar terms. A default by one of the lenders under our Revolving Credit Facility or our inability to meet the conditions required for borrowing thereunder could negatively impact our ability to finance our working capital needs, thereby negatively impacting our business.

Covenants in our debt agreements restrict our business in many ways.

The Indenture and the agreement governing our Revolving Credit Facility contain various covenants that, subject to certain exceptions, including customary baskets, generally limit our ability and our subsidiaries’ ability to, among other things:

· incur or assume liens or additional debt or provide guarantees in respect of obligations of other persons;

· issue redeemable stock and preferred stock;

· pay dividends or distributions or redeem or repurchase capital stock;

· prepay, redeem or repurchase debt;

· make loans and investments;

· enter into agreements that restrict distributions from our subsidiaries;

· sell assets and capital stock of our subsidiaries;

· engage in certain transactions with affiliates; and

· consolidate or merge with or into, or sell substantially all of our assets to, another person.

As of the end of any fiscal quarter for which we have borrowings outstanding under our Revolving Credit Facility, we must have a leverage ratio, defined as consolidated total indebtedness less excess cash, divided by EBITDA for the trailing twelve months, equal to or less than 5.0 to 1. In calculating the leverage ratio, we calculate EBITDA and excess cash, which were $98.4 million and $43.3 million, respectively, for the twelve months ended and as of December 31, 2011, pursuant to the terms of our Revolving Credit Facility.

As of June 30, 2012, our leverage ratio was 3.7 to 1. A breach of the covenants or restrictions under the indenture governing the notes or the agreement governing our revolving credit facility could result in a default under the applicable indebtedness. Any such default may allow the creditors to accelerate the related debt and may result in the acceleration of any other debt to which a cross-acceleration or cross-default provision applies. In addition, an event of default under our Revolving Credit Facility would permit the lenders thereunder to terminate all commitments to extend further credit under that facility. Furthermore, if we were unable to repay the amounts due and payable under that facility, those lenders could, pursuant to the security documents and following a consultative process between the agent for those lenders and the trustee for the holders of the notes (or, if the notes are not the largest class of first-lien indebtedness then outstanding, the representative of the holders of such largest class, with the trustee or such representative being referred to as the “applicable authorized representative”), proceed against the Collateral in which they have a first-priority security interest shared with the notes. See “Description of the Exchange Notes—Security for the Notes—Description of the Collateral” and “Description of the Exchange Notes—Security for the Notes—Security Documents; Appointment of the Collateral Agent”. In the event our lenders and holders of notes accelerate the repayment of our borrowings, we cannot assure you that we would have sufficient assets to repay such indebtedness or be able to borrow or raise additional equity in an amount sufficient to repay such indebtedness. Even if we are able to obtain new financing, it may not be on commercially reasonable terms or on terms acceptable to us. As a result of these restrictions, we may be:

· limited in how we conduct our business and execute our business strategy;

· unable to raise additional debt or equity financing to fund our operations; or

· unable to compete effectively or to take advantage of new business opportunities.

These restrictions may affect our ability to grow in accordance with our plans.

Changes in credit ratings issued by statistical rating organizations could adversely affect our costs of financing.

Credit rating agencies rate our indebtedness based on factors that include our operating results, actions that we take, their view of the general outlook for our industry and their view of the general outlook for the economy. Actions taken by the rating agencies can include maintaining, upgrading or downgrading the current rating or placing us on a watch list for possible future downgrading. Downgrading the credit rating of our indebtedness or placing us on a watch list for possible future downgrading could limit our ability to access the capital markets to meet liquidity needs and refinance maturing liabilities or increase the interest rates and our cost of financing.

Claims of holders of notes will be effectively subordinated to claims of creditors of current and any future subsidiaries that are not guarantors.