LaPorte Bancorp, Inc. LPSB Annual Shareholder Meeting May 14, 2013 Michele M. Thompson – President & Chief Financial Officer Exhibit 99.1 |

Forward-Looking Statements The presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and are including this statement for purposes of said safe harbor provisions. You can identify these forward- looking statements through our use of the words such as “may”, “will”, “anticipate”, “assume”, “should”, “indicate”, “would”, “believe”, “contemplate”, “expect”, “estimate”, “continue”, “plan”, “project”, “could”, “intend”, “target” and other similar words and expressions of the future. These forward-looking statements include, but are not limited to: These forward-looking statements are based on current beliefs and expectations of our management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. 2 Statements of our goals, intentions and expectations; Statements regarding our business plans, prospects, growth and operating strategies; Statements regarding the asset quality of our loan and investment portfolios; and Estimates of our risks and future costs and benefits. |

Forward-Looking Statements (continued) general economic conditions, either nationally or in our market areas, that are worse than expected; changes in prevailing real estate values and loan demand, both nationally and within our current and future market area; inflation and changes in the interest rate environment that reduce our margins or reduce the fair value of financial instruments; increased competitive pressures among financial services companies; changes in consumer spending, borrowing and savings habits; the amount of assessments and premiums we are required to pay for FDIC deposit insurance; legislative or regulatory changes that affect our business, including the Dodd-Frank Act and its impact on our compliance costs or capital requirements; changes in accounting policies and practices, as may be adopted by the bank regulatory agencies, the financial Accounting Standards Board, the Securities and Exchange Commission and Public Company Accounting Oversight Board; our ability to successfully manage our commercial lending; our ability to enter new markets successfully and capitalize on growth opportunities; our ability to successfully integrate acquired entities; changes in our organization, compensation and benefit plans; changes in the financial condition, results of operations or future prospects of issuers or securities that we own; the financial health of certain entities, including government sponsored enterprises, the securities of which are owned or acquired by us; adverse changes in the securities market; the costs, effects and outcomes of existing or future litigation; the economic impact of past and any future terrorist attacks, acts of war or threats thereof and the response of the United States to any such threat and attacks; the success of our mortgage warehouse lending program, including the impact of the Dodd-Frank Act on the mortgage companies; and our ability to manage the risks associated with the foregoing factors as well as the anticipated factors. 3 The following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations express in the forward-looking statements: This list of important factors in not all inclusive. For a discussion of these and other risks that may cause actual results to differ from expectations, please refer to the Company’s Prospectus dated August 10, 2012 on file with the SEC. Readers are cautioned not to place undue reliance on the forward-looking statements contained herein, which speak only as of the date of the Presentation. Except as required by applicable law or regulation, we do not undertake, and specifically disclaim any obligation, to update any forward-looking statements, whether written or oral, that may be made from time to time by or on behalf of the Company or The LaPorte Savings Bank. |

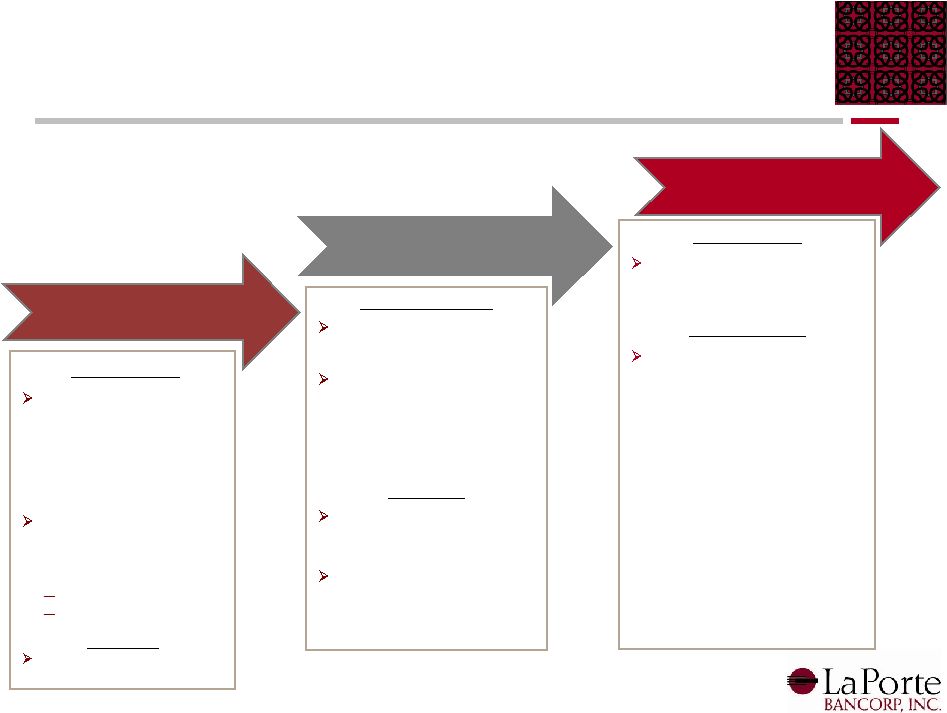

LaPorte Bancorp, Inc. Timeline 4 2007 - 2008 2009 - 2011 2012 - 2013 October 2007 LaPorte raises $13 million of common equity in its initial public offering and converts into a mutual holding company structure LaPorte simultaneously completes acquisition of City Savings Financial Corp. July 2008 LaPorte opens Westville branch September 2009 LaPorte establishes its mortgage warehouse lending division Enters into a partnership with Harbour Trust & Investment Management Company to provide ongoing trust services to the Bank’s client base July 2011 Michele Thompson is appointed CFO and President Lee Brady is named chairman of the bank’s Board of Directors October 2012 LaPorte completes its second step conversion and raises $27 million of common equity February 2013 LaPorte opens Slicer branch in a cooperative partnership with LaPorte High School $127 million in assets $85 million in deposits |

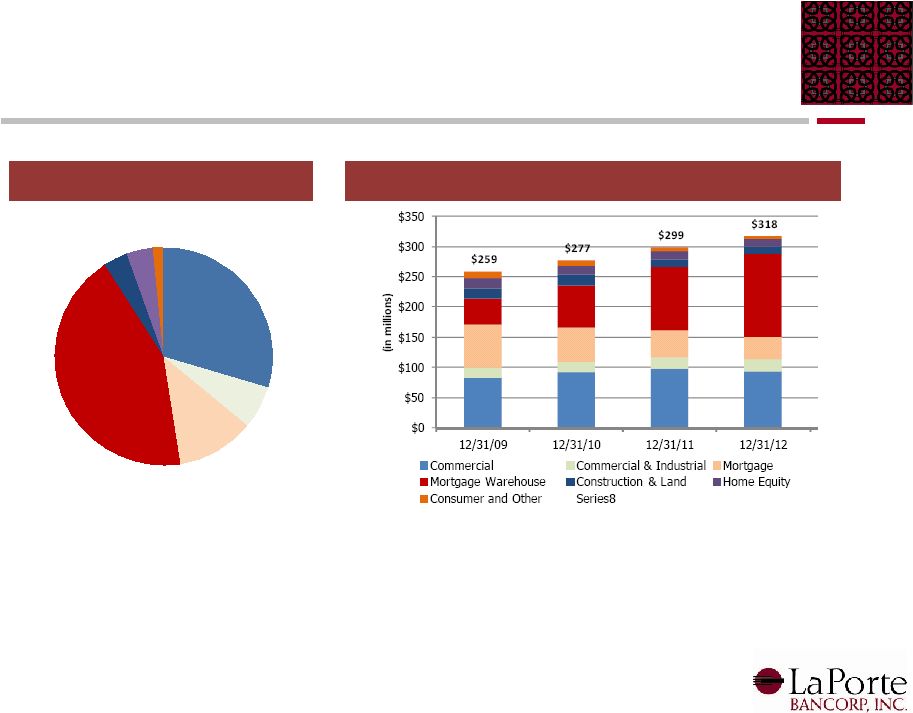

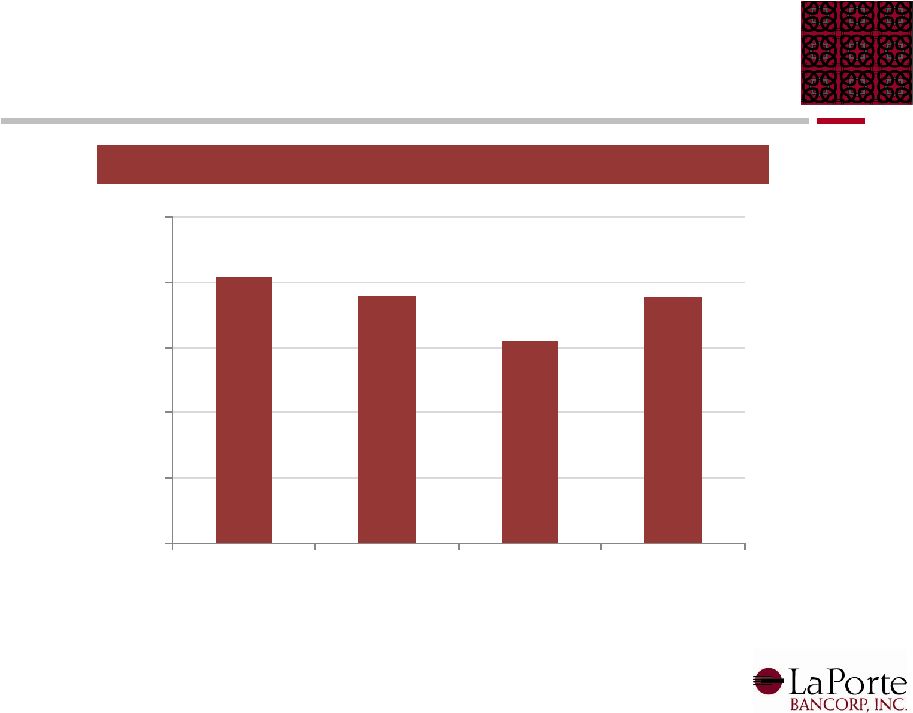

Loan Composition 5 Historical Loan Trends ($MM) Loan Composition 29.6% 6.3% 11.6% 43.3% 3.7% 3.9% 1.6% Note: Total loans excludes deferred loan fees and loans held for sale |

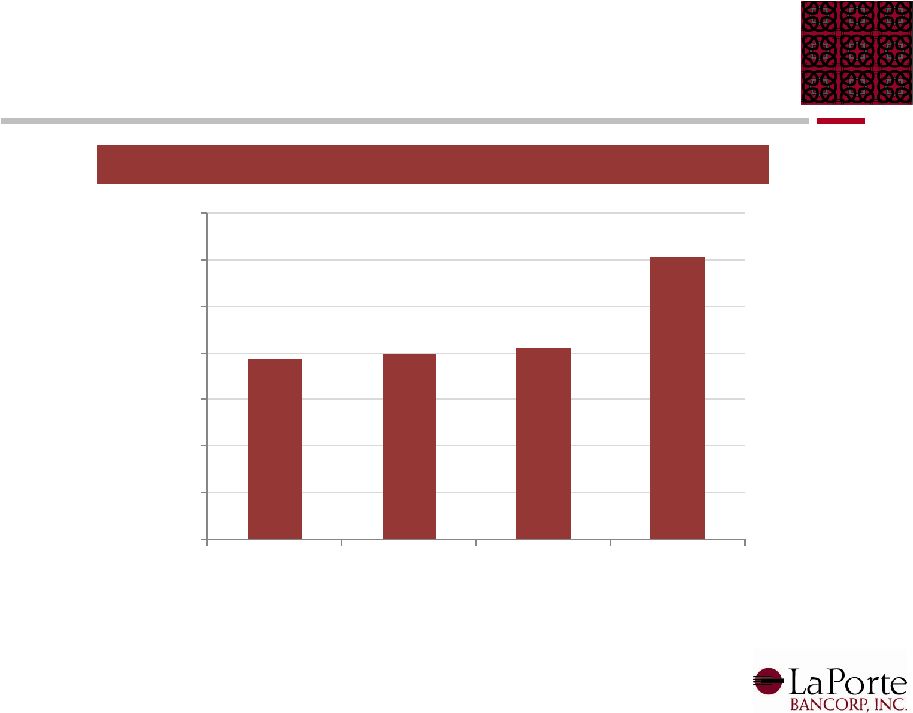

Deposit Composition 6 Historical Deposit Trends ($MM) Deposit Composition 14.6% 49.6% 35.8% |

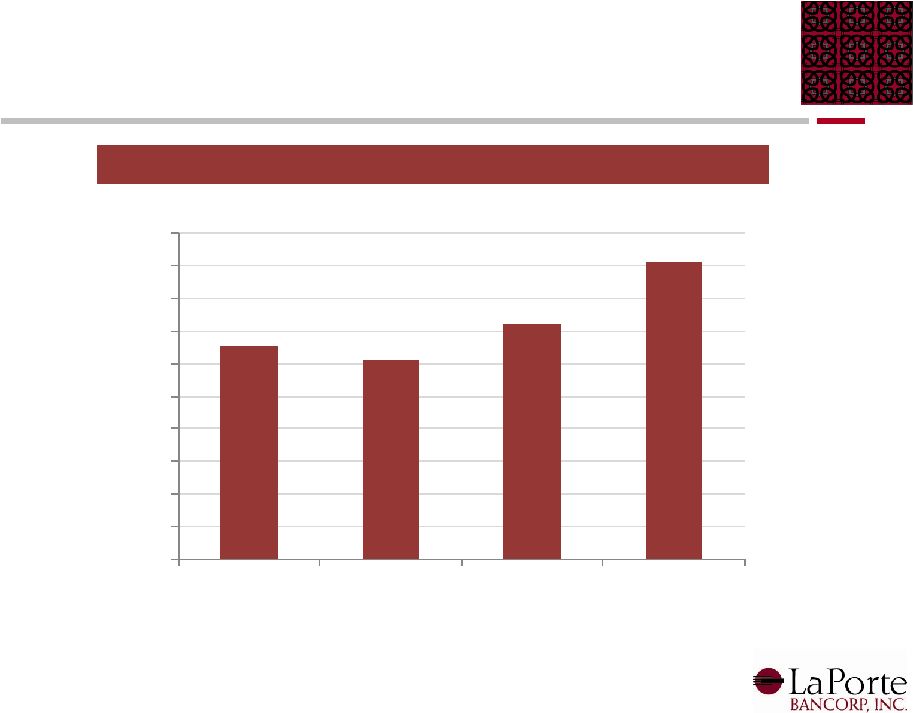

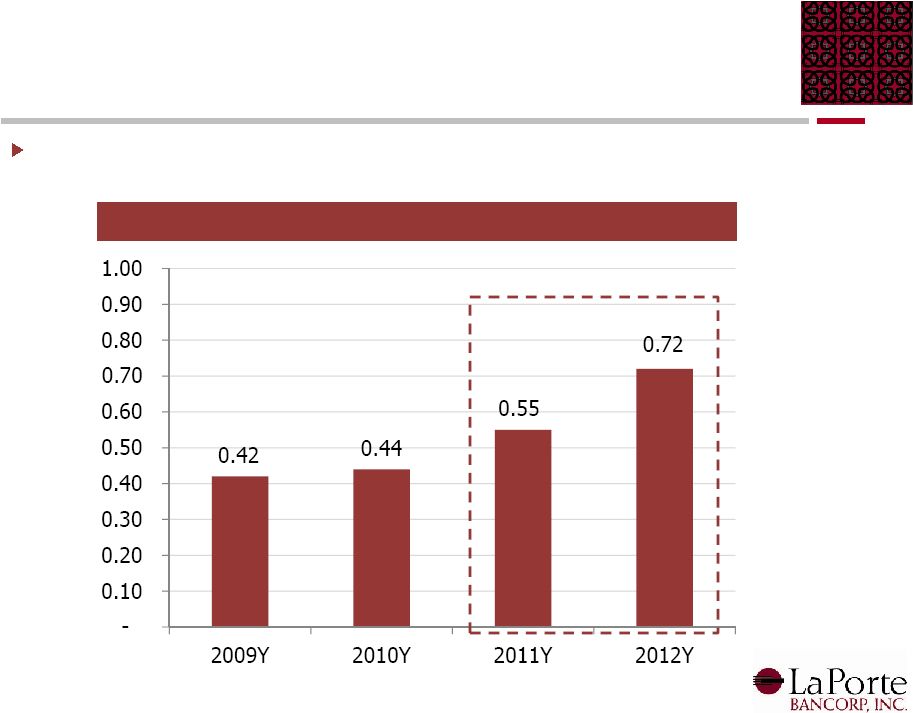

Return on Average Assets (ROAA) 7 Return on Average Assets (ROAA) (%) 0.65 0.61 0.72 0.91 0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 1.00 2009Y 2010Y 2011Y 2012Y |

Return on Average Equity (ROAE) 8 Return on Average Equity (ROAE) (%) 5.25 5.12 6.15 6.91 0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 2009Y 2010Y 2011Y 2012Y |

Net Interest Margin (NIM) 9 Net Interest Margin (NIM) (%) 3.21 3.59 3.31 3.57 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 2009Y 2010Y 2011Y 2012Y |

Efficiency Ratio 10 Efficiency Ratio (%) 74.66 62.06 68.36 63.34 0.00 10.00 20.00 30.00 40.00 50.00 60.00 70.00 80.00 2009Y 2010Y 2011Y 2012Y |

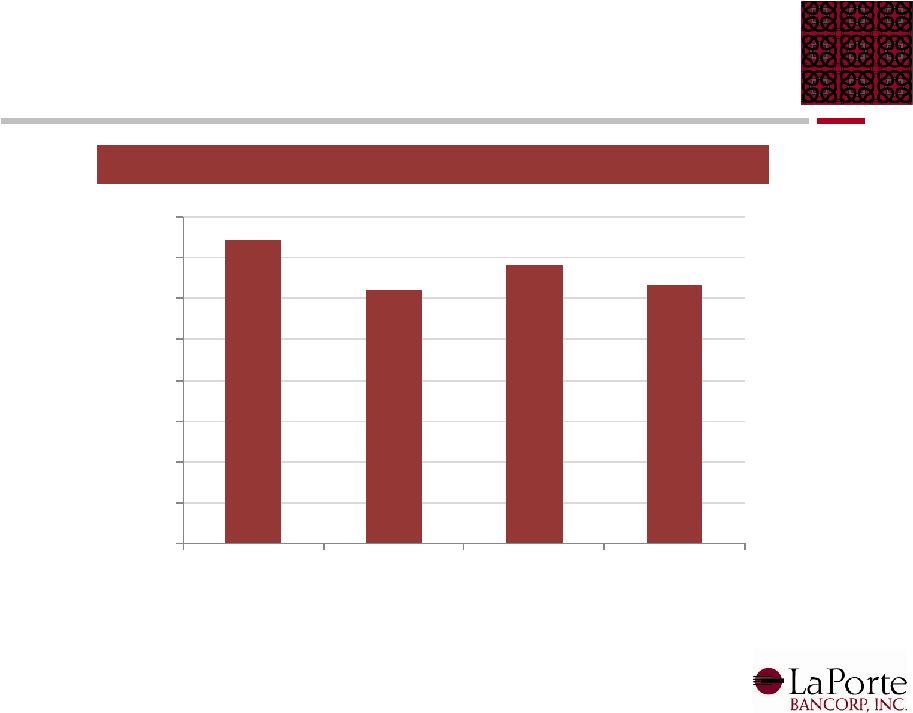

Non-performing Assets / Assets 11 NPAs/ Assets (%) 1 (1) NPAs/Assets includes TDRs 2.04 1.89 1.55 1.88 0.00 0.50 1.00 1.50 2.00 2.50 2009Y 2010Y 2011Y 2012Y |

Tangible Book Value Per Share 12 Tangible Book Value Per Share ($) $7.76 $7.95 $8.21 $12.13 $- $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 2009Y* 2010Y* 2011Y* 2012Y *2009, 2010 and 2011 tangible book value per share are exchange ratio adjusted |

Consistent Growth in Earnings Per Share Our management team has been consistently focused on generating profits for our shareholders 13 Earnings Per Share ($) 1 (1) EPS calculation is exchange ratio adjusted |

Strong Capital Position LaPorte maintains a low risk profile with strong capital levels 14 Strong Capital Levels |

Questions? |