Annual Report

Contents

ANZ Annual Report 2009 1

Chairman’s Report

A MESSAGE FROM CHARLES GOODE

ANZ delivered a solid result in 2009 against the backdrop of the global financial crisis and a major downturn in the world economy.

Our Performance

ANZ’s statutory profit after tax for the year ended 30 September 2009 was $2,943 million, down 11%, reflecting higher provisions. With an increase in the weighted average number of shares of 16%, this led to a fall in earnings per share of 23%. The dividend for the year was $1.02 per share fully franked, down 25%.

Excluding the impact of $829 million from one-off items, hedging timing differences and non-continuing businesses our underlying profit1 for 2009 was $3,772 million, up 10%.

Underlying revenue growth of 17% was strong while costs increased by 12%, with our underlying cost-to-income ratio at 42.2%, down from 44%. Provisions were at cyclical highs with the total credit impairment charge up 46% to $3,056 million, with increases across all regions but most pronounced in New Zealand.

Importantly, ANZ maintained its AA-credit rating, one of only 11 banks remaining in the world with a AA-rating.

These results were achieved at a time the global financial system and the world economy came under extraordinary pressure and they reflect the very significant efforts of our management and our staff during the year. I thank them for their contribution.

Capital Management

During 2009 ANZ took further steps to manage its capital position and funding programs to ensure we were strongly positioned given the difficult financial and economic conditions.

In May, we undertook a fully underwritten $2.5 billion institutional share placement. In July, we completed a Share Purchase Plan for retail shareholders which saw us issue $2.2 billion of ordinary equity.

Over 40% of our retail shareholders participated, making it one of the most successful Share Placement Plans undertaken by an Australian company. The new shares were issued at $14.40 compared to ANZ’s year-end share price of $24.39 representing a strong return to participating shareholders.

Including the underwritten Dividend Reinvestment Plan in July, ANZ raised $5.7 billion of ordinary equity and the Group ended 2009 as one of the world’s best capitalised banks.

ANZ’s Tier 1 capital ratio was 10.6% at the end of 2009 compared to 7.7% a year earlier. Adjusting for the acquisitions we made during the year but which have not yet been completed, the pro-forma Tier 1 ratio is estimated to be 9.5%.

Expansion and Growth

Our financial performance and strong capital position allowed ANZ to capitalise on significant strategic opportunities that arose during the year and our super regional strategy was advanced through both organic growth and acquisitions.

In August, we announced an agreement to acquire certain selected businesses of the Royal Bank of Scotland (RBS) in East Asia for approximately US$550 million (A$626 million).

The acquisition includes the RBS Retail, Wealth and Commercial businesses in Taiwan, Singapore, Indonesia and Hong Kong and the Institutional businesses in Taiwan, the Philippines and Vietnam. It creates a new platform for our Retail and Wealth businesses in Asia.

ANZ also moved to strengthen its franchise in Australia and New Zealand with an agreement to acquire the 51% held by the ING Group in the ANZ-ING wealth management and life insurance joint ventures.

Board Changes

John Morschel, one of Australia’s most respected business leaders, has agreed to succeed me as Chairman in February 2010.

John has been a director of ANZ since October 2004 and has made a major contribution since joining the Board. He has extensive experience as a chief executive and more recently as a non-executive director and chairman of major Australian and international companies. John also brings to the role a strong background in banking and financial services. He will make an excellent Chairman for ANZ.

We have also welcomed three new directors to the Board during the year – Peter Hay, Alison Watkins and Lee Hsien Yang – to facilitate a transition with the planned retirements of some Directors.

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses, timing differences on economic hedges, and acquisition related costs. Refer page 6. |

2ANZ Annual Report 2009

CHAIRMAN’S REPORT (continued)

Peter Hay has a strong background in company law and investment banking advisory work, with strong experience in mergers and acquisitions. Alison Watkins is an experienced CEO and established director with a grounding in finance and accounting. Lee Hsien Yang is one of Asia’s most respected business leaders and has considerable knowledge of the region.

I would also like to acknowledge the outstanding contribution made to ANZ over 15 years by Margaret Jackson who retired from the Board in April 2009.

Customers and the Community

While the global financial and economic conditions have been testing, ANZ has maintained the momentum established in recent years by focusing on its customers and contributing to the community.

In Australia, we maintained the highest level of customer satisfaction of any of the major banks and we began the roll out of our new global brand identity and positioning for ANZ.

A number of the communities in which ANZ operates experienced disasters during the year. These included natural disasters in Asia and the Pacific and the bushfires in Victoria. ANZ contributed to the relief efforts through donations, direct grants and the efforts of many ANZ staff.

During 2009, ANZ was named as the most sustainable bank globally in the Dow Jones Sustainability Index for the third consecutive year.

Outlook

Looking ahead, the actions taken by governments around the world have gained traction and are now moderating the effects of the global economic downturn.

While it is clear that Australia and Asia have weathered the crisis better than the US and Europe, there is still uncertainty about the shape of the recovery and it is prudent to be cautious. In New Zealand, there are early signs the economy has stabilised, however economic recovery is likely to be slow.

At ANZ, we are facing some headwinds in 2010 including the strength of the Australian dollar, a less favourable global markets environment and a 13% increase in the weighted average number of shares to be serviced.2 Our regional growth focus however puts us in a unique position to capitalise on Asia’s recovery and growth.

However, we also have some tail winds with the recovery in the economies of Australia, New Zealand and the region, continued profitable expansion in East Asia and a moderation in the outlook for doubtful debts.

We have a strong management team, a strong capital position, strong liquidity and a well thought out strategy to be a super regional bank. The bank is being managed for the medium term and the outlook is for an improvement in profits in 2010 and a strong 2011.

CHARLES GOODE

CHAIRMAN

| 2 | Shares on issue at 30 September 2009 divided by weighted average number of shares during 2009. |

Chairman’s Report3

Chief Executive Officer’s Report

A MESSAGE FROM MICHAEL SMITH

Two years ago, we took a decision at ANZ that although we had great individual businesses in Australia, New Zealand and Asia Pacific, there was a unique opportunity to create value for shareholders by becoming a super regional bank – a bank of global quality with regional focus.

2009 represents a turning point in delivering that aspiration. We’ve worked hard to reposition ANZ to face up to what we called the ‘new reality’ following the global financial crisis and we’ve built a strong foundation through careful, disciplined management of our balance sheet, capital and liquidity.

At the same time, we’ve made significant progress in completing change and remediation in the business in order to place ANZ on a new footing. Together, that’s allowed us to shift our focus this year to the opportunities that are available to a strongly capitalised bank and to the growth available in our region which is now the best performing region in the world economy.

Our operating environment

Our 2009 financial year began just weeks after the collapse of Lehman Brothers, one of the leading Wall Street investment banks. In the weeks that followed some household names in finance disappeared and as at the end of 2009 over 100 banks in the United States had failed and many of what were the world’s largest banks are now effectively in the hands of their respective national governments.

As the financial crisis unfolded, its impact on the world economy became very clear. As a result we’ve seen unprecedented action by governments to save the global financial system and to rescue the world economy which entered into the most globalised downturn since the Great Depression.

In Australia, even with provisions at or near cyclical highs, Australian banks are in good shape relative to their international peers. Today, Australia’s four major banks, including ANZ, are among just 11 AA-rated banks left in the world.

In this very difficult environment, ANZ has consistently called the trends early in the economic cycle and the global financial situation.

Today, in Australia and in Asia, the economies are showing early positive signs of recovery and although the economic cycle is still playing out, there are reasons for optimism.

In the region, China and India are continuing to show good growth and we believe the urbanisation and fundamental transformation occurring in those economies will see that growth continue.

We strongly believe Asia will be an engine for global growth for many decades to come, and given the trade and investment flows between Australia and New Zealand and Asia, it’s an essential part of the long-term growth strategy for any business.

Our business performance

In this environment, ANZ has remained financially strong, maintained momentum in the business and worked hard to position ANZ for future growth.

Statutory profit for the year was $2.9 billion, down 11%. Taking into account the impact of some one off items and non-continuing businesses, underlying profit1 increased 10% to $3.8 billion.

Australia performed well with underlying profit* up 13% to $2,560 million. The Retail and Institutional businesses in the region were standout performers. Commercial produced a credible result, given the difficult year experienced by middle market and small business managers.

Importantly we are also delivering for our customers. ANZ remains the highest rated of the major banks when it comes to customer satisfaction.

In New Zealand, trading conditions remained challenging. New Zealand’s economic downturn has been more pronounced and protracted than that in Australia and while we maintained our market leading position, the economic environment led to a 34% decline in underlying profit after tax to $513 million.

The Asia Pacific, Europe & America region produced an outstanding performance with underlying profit up 81% to $699 million, with strong contributions from our partnerships and the Institutional business driving much of this growth.

ANZ has continued to invest significantly in the region including deepening the Institutional business and advancing the Retail and Wealth platforms. We’ve continued to build our branch networks in Indonesia, Vietnam and China and are acquiring business in six countries in Asia from the Royal Bank of Scotland.

The Institutional Division has turned around its performance, delivering an underlying profit of $1.4 billion, up 82% on last year. A key feature of the Institutional result was Global Markets revenue growth with both customer flow and trading revenue up strongly. Interest rate and general market volatility coupled with increased customer penetration drove the significant increase in revenue within the Global Markets business.

The Institutional team leveraged their strong revenue growth to make investments in improved systems and processes and to begin to grow frontline staff numbers.

Strategic growth

During 2009, we’ve been able to take advantage of the global financial crisis and ANZ’s strong balance sheet to advance our super regional strategy.

In August we reached agreement with the Royal Bank of Scotland Group to acquire selected RBS businesses in East Asia for around US$550 million ($626 million) delivering a further stepping stone in our super regional strategy and creating a new platform for our businesses in Asia.

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses, timing differences on economic hedges, and acquisition related costs. Refer page 6. |

4ANZ Annual Report 2009

CHIEF EXECUTIVE OFFICER’S REPORT (continued)

The acquisition, which is still subject to regulatory approvals, includes the RBS retail, wealth and commercial businesses in Taiwan, Singapore, Indonesia and Hong Kong, and the institutional businesses in Taiwan, the Philippines and Vietnam.

Together, the businesses are an attractive portfolio of well provisioned banking assets at a reasonable price which complement our existing businesses across China, Indochina and South East Asia and provide our franchise with further growth momentum.

In September, we signed an agreement with ING to acquire its 51% shareholding in the ANZ-ING joint ventures in Australia and New Zealand for $1.76 billion. The transaction brings certainty to our wealth management position through full ownership of what is an established specialist wealth management and protection business with a 120-year history in Australia.

Importantly for shareholders, it will be accretive to underlying earnings in 2010 before some significant revenue and cost synergies.

In the medium term, it also gives us a foundation to build a significant wealth business with the flexibility to pursue further growth opportunities without the constraints of a joint venture structure.

Organisational capability

This year we’ve also put a new customer focused business model and organisation structure in place. A new competitive era and strategy demanded a new business model and structure, one that can support our aspirations to become a super regional bank.

We are now organised around three key regions – Australia, New Zealand and Asia Pacific, Europe and America with Institutional operating as a global business. We have also put in place a simpler, less complex structure for Operations, Technology, Human Resources, Finance and Risk.

We’ve continued to reshape our top management team during the year, with several new appointments made.

The latest addition, which completes the management team, is the appointment of Phillip Chronican to lead the Australia Division. Phillip joins ANZ after a 27-year career with Westpac where he built a reputation as one of Australia’s leading banking executives.

Also this year, Joyce Phillips joined ANZ as head of Strategy, M&A, Marketing and Innovation from GE and Citigroup and Shayne Elliott, was appointed as head of Institutional also from Citigroup and most recently EFG-Hermes.

Our customers and brand

Part of our strategy is to design our business around our customers’ needs, not our product lines. We made significant progress with this with our new organisation structure.

But we also need to shift our thinking from selling commoditised product to looking at differentiating the way we market ourselves, the way we package and segment our offering and the way we service our customers. Part of that involves investing in developing a great regional brand and so this year we’ve worked hard to develop a new global brand identity and positioning for ANZ in support of our super regional strategy.

Having one strong, unified brand across all our geographies, which tells the world that we are ‘One ANZ’ wherever customers choose to deal with us, is an important part of our future growth. It identifies who we are as a business and what we stand for.

The new brand identity and positioning followed 18 months of detailed research involving more than 1,300 customers and 250 staff in Australia, New Zealand and Asia Pacific that showed our customers want us to care about them as people and appreciate how complex life has become.

As part of the launch, we introduced a new global tagline, ‘We live in your world’.

This aspiration is at the heart of our brand promise – no matter where our customers deal with us, we want to give them one high standard of experience, based on understanding their world better than anyone else.

We know there’s a lot to do to really deliver on this and all our people are committed to the task.

2009 and the future

Reflecting on what has been a full year of activity at ANZ, we’ve remained financially very strong, we have a very clear growth strategy and we have a very experienced team of real bankers to make sure we keep hitting our targets and growing the bank with an acceptable risk profile. In doing so, I believe we have created real value for shareholders.

Looking forward to 2010, we are going to have to manage continuing volatility in financial markets and the global economy. The recovery in Europe and the United States is still in a very sensitive position and there’s going to be good and bad news in the slow advance forward.

I also want to sound a note of caution. While the inevitable aftermath of the recent failures in the financial system and in business is going to be greater regulation, in my view, the real challenge is for governments to avoid acting on populist rhetoric. Regulators and business need to work together to identify how we create the right balance between free markets which are the best tool we know for fostering innovation and generating wealth, and ensuring there is a watchful eye from regulators that can help markets avoid overshooting and spinning out of control.

Against this backdrop, ANZ is clearly established as one of the best capitalised banks in the world. We have largely completed the remediation and change needed in parts of the business and we have taken advantage of opportunities to grow, as we progress on our journey to build a super regional bank that delivers performance and growth for our shareholders, customers and the communities in which we operate.

CHIEF EXECUTIVE OFFICER

Chief Executive Officer’s Report5

Chief Financial Officer’s Report

A MESSAGE FROM PETER MARRIOTT

ANZ reported a profit after tax of $2,943 million for the year ended 30 September 2009.

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Net interest income | | | 9,808 | | | | 7,850 | | | | 25 | % |

Other operating income | | | 3,802 | | | | 4,309 | | | | -12 | % |

| | | | | | | | | | | | |

Operating income | | | 13,610 | | | | 12,159 | | | | 12 | % |

Operating expenses | | | (6,225 | ) | | | (5,696 | ) | | | 9 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 7,385 | | | | 6,463 | | | | 14 | % |

Provision for credit impairment | | | (3,005 | ) | | | (1,948 | ) | | | 54 | % |

| | | | | | | | | | | | |

Profit before income tax | | | 4,380 | | | | 4,515 | | | | -3 | % |

Income tax expense | | | (1,435 | ) | | | (1,188 | ) | | | 21 | % |

Minority interest | | | (2 | ) | | | (8 | ) | | | -75 | % |

| | | | | | | | | | | | |

Profit attributable to shareholders of the Company | | | 2,943 | | | | 3,319 | | | | -11 | % |

| | | | | | | | | | | | |

Underlying profit

Profit has been adjusted to exclude non-core items to arrive at underlying profit, the result for the ongoing business activities of the Group. The principles set out in the Australian Institute of Company Directors’ (AICD’s) and the Financial Services Institute of Australasia’s (Finsia’s) joint recommendations “Principles for reporting of non-statutory profit information” have been adopted in determining underlying profit.

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Statutory profit attributable to shareholders of the Company | | | 2,943 | | | | 3,319 | | | | -11 | % |

Adjust for the following gains/(losses) included in statutory profit (net of tax) | | | | | | | | | | | | |

Tax on New Zealand Conduits | | | (196 | ) | | | — | | | | n/a | |

Economic hedging – fair value gains/(losses) (incl. revenue and net investment hedges) | | | (227 | ) | | | 217 | | | | large | |

Gain on Visa shares | | | — | | | | 248 | | | | -100 | % |

Organisational transformation costs (incl. One ANZ restructuring) | | | (100 | ) | | | (152 | ) | | | -34 | % |

Impairment of intangible – Origin Australia | | | — | | | | (24 | ) | | | -100 | % |

New Zealand tax rate change | | | — | | | | 1 | | | | -100 | % |

ANZ share of ING NZ investor settlement | | | (121 | ) | | | — | | | | n/a | |

Non continuing businesses | | | | | | | | | | | | |

Credit intermediation trades | | | (69 | ) | | | (371 | ) | | | -81 | % |

Other | | | (116 | ) | | | (26 | ) | | | large | |

| | | | | | | | | | | | |

Underlying profit | | | 3,772 | | | | 3,426 | | | | 10 | % |

| | | | | | | | | | | | |

Underlying profit by key line item | | | | | | | | | | | | |

Net interest income | | | 9,810 | | | | 7,855 | | | | 25 | % |

Other operating income1 | | | 4,557 | | | | 4,440 | | | | 3 | % |

| | | | | | | | | | | | |

Operating income | | | 14,367 | | | | 12,295 | | | | 17 | % |

Operating expenses | | | (6,068 | ) | | | (5,406 | ) | | | 12 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 8,299 | | | | 6,889 | | | | 20 | % |

Provision for credit impairment1 | | | (3,056 | ) | | | (2,090 | ) | | | 46 | % |

| | | | | | | | | | | | |

Profit before income tax | | | 5,243 | | | | 4,799 | | | | 9 | % |

Income tax expense | | | (1,469 | ) | | | (1,365 | ) | | | 8 | % |

Minority interest | | | (2 | ) | | | (8 | ) | | | -75 | % |

| | | | | | | | | | | | |

Profit attributable to shareholders of the Company | | | 3,772 | | | | 3,426 | | | | 10 | % |

| | | | | | | | | | | | |

| 1 | Credit valuation adjustments on defaulted or impaired exposures of $82 million are reclassified as provision for credit impairment (Sep 2008: $156 million). |

6ANZ Annual Report 2009

CHIEF FINANCIAL OFFICER’S REPORT (continued)

ANZ reported a profit attributable to shareholders of the Company of $2,943 million for the year ended 30 September 2009, down $376 million or 11% from $3,319 million for the year ended 30 September 2008. Growth in profit before credit impairment and income tax of 14% was offset by an increase in provision for credit impairment of $1,057 million or 54% and a higher effective tax rate, largely as a result of a $196 million provision for New Zealand conduit transactions.

Analysis of business performance on an underlying basis by major income and expense categories follows.

Net Interest Income

Net interest income increased $1,955 million (25%) to $9,810 million for the year ended 30 September 2009. Net interest income was driven by an increase in average interest earning assets of 9% and growth in average deposits and other borrowings of 12% as well as an increase in net interest margin of 28 basis points, or 16 basis points excluding cash flow on derivatives.

The increase in average interest earning assets included a 7% increase in net advances, primarily in Mortgages within Australia region, reflecting increased market share and customer demand. Other interest earning assets increased 22% driven by increases in trading and available-for-sale assets, interbank lending and higher liquid assets.

Average deposits and other borrowings increased 12% with customer deposits growing by 16%. Australia region grew by 16% due primarily to an uplift in term deposits driven by competitive pricing and customer acquisition. Asia Pacific, Europe & America region grew by 57%, spread across all countries driven by deposit raising strategies and customer acquisitions. Customer deposits grew by $31.1 billion (16%).

Net interest margin was up 28 basis points to 2.29% (or 16 basis points excluding the impact of cash flow on derivatives). The key drivers of the improved margin performance were:

| • | | Improved asset margin from repricing activities and rate adjustments (+45 basis points) which were required to offset higher funding costs and increased risk in the loan book as a result of the flow through effects of the global credit crisis. Higher funding costs came through as an increase in wholesale funding costs (-6 basis points), lower margin on deposits (-28 basis points) and lower interest on capital (-7 basis points). |

| • | | Markets (+17 basis points) continued to perform strongly in their balance sheet businesses (+8 basis points) and the impact of funding benefits associated with unrealised trading gains and losses on derivatives (+12 basis points) $524 million directly offset in other operating income, partly offset by the mix impact of Markets balance sheet on the Group (-3 basis points). |

| • | | Additional capital raised during 2009, mainly through the share purchase and share placement plans, had a +4 basis points mix impact on margin. |

| • | | Other asset and funding mix changes (+4 basis point) were as a result of a lower proportion of wholesale funding (+7 basis points), favourable benefit from non interest bearing items (-3 basis point). Asset mix impact was neutral. |

| • | | Other items (-1 basis point) include New Zealand lower mortgage prepayment income (-1 basis point) driven by the downward movement in New Zealand market rates, higher sub-debt premiums (-1 basis point) and other net impacts (+1 basis point). |

Other Operating Income

Other operating income increased $117 million (3%) to $4,557 million for the year ended 30 September 2009. Major movements include:

| • | | Fee income increased $80 million (3%). Lending fee income increased $169 million (28%) due mainly to the Institutional business across the regions. Non-lending fee income decreased $89 million (4%) with Investment and Insurance Products down $48 million as a result of downturn in investment markets. Relationship Banking decreased $18 million and Specialised Lending reduced $17 million both driven by lower lending volumes. |

| • | | Net foreign exchange earnings increased $243 million (35%) principally in Markets Australia with a $134 million increase as a result of volatility in global currency markets and higher sales volumes and in Asia Pacific, Europe & America grew $103 million reflecting increased earnings in Taiwan and Korea, United Kingdom and Europe and Indonesia. New Zealand increased $26 million due to strong Institutional earnings. |

| • | | Profit on trading instruments decreased $194 million (38%) which included a $524 million decrease in unrealised trading gains offset in net interest income. Excluding the offset, the Markets business performed strongly benefiting from increased volatility in the interest rate market and higher sales volumes. |

Operating Expenses

Operating expenses increased $662 million (12%) for the year ended 30 September 2009. Across the Group, movements in exchange rates contributed 1% of the increase. Excluding this, around 35% of the dollar cost growth was attributable to Asia Pacific, Europe & America (costs up 54%) with substantial investment in expanding branch networks across the region, and increased resources to drive the growth agenda. Within the Australia and New Zealand regions, Institutional drove the majority of the cost growth, up 19% and representing 32% of the Group’s total cost growth through investment in the “Rebuild and Refocus” program and increased remuneration costs. Elsewhere in Australia, costs in the Australian division were up only 4%, however there was an increase in centrally funded transformation projects and infrastructure investment in the Group Centre. Cost growth was limited to 1% (or 4% in NZD) in New Zealand region. Further details on the major expense categories are on the following page.

Chief Financial Officer’s Report 7

CHIEF FINANCIAL OFFICER’S REPORT (continued)

| • | | Personnel costs were up $349 million (11%) as a result of growth in remuneration costs associated with attracting and retaining talent and additional bankers and specialists to support growth. Asia Pacific, Europe & America increased staff numbers by 827 employees due to continued growth in the business. |

| • | | Premises costs increased $45 million (9%), driven mainly by a $30 million higher rental expense reflecting additional space requirements, the impact of the sale and leaseback program and market rental growth. |

| • | | Computer costs grew $157 million (26%), due to increased software purchased of $50 million including higher licence costs and increasing technology initiatives, higher amortisation charges of $31 million, a $24 million increase in software written-off, a $15 million increase on computer contractors, $11 million increase in rentals and repairs, $8 million higher data communications costs and a $23 million increase in other computer costs which include super regional network costs. |

| • | | Other expenses increased $111 million (11%) with minor movements across many categories. Professional fees grew $21 million including an increase in Group Centre due to various project work. Advertising costs increased $13 million due mainly to increased marketing costs in South Asia. Card processing costs increased $9 million reflecting increased volumes. New Zealand other expenses increased $26 million including the impact from the acquisition of a controlled entity during the second half of 2008. Travel costs reduced $22 million due to increased focus on cost management. |

Provision for Credit Impairment

Provision for credit impairment charge increased $966 million from 2008 to $3,056 million. The challenging economic environment, reducing business confidence and rising levels of commercial losses combined to put pressure on the provisioning levels. The individual provision charge increased across all regions partially offset by a decrease in collective provision charge, primarily as a result of a release of concentration risk provision taken up in 2008 as losses were crystallised, a lower economic cycle adjustment charge and reduced lending volumes.

Total individual provision charge increased $1,542 million to $2,814 million from 2008. The increase in Australia of $1,199 million was driven by higher loss rates across all portfolios within the region, and rising levels of bankruptcies and commercial losses in line with higher business liquidations and lower realisable asset values as well as the large single provisions raised for customers within the Commercial Property, Finance and Brokering Services portfolios in Institutional Australia. The increase in New Zealand of $349 million occurred across all segments as weaker global and local economic conditions impacted export, household incomes, consumer spending and business sectors. The Asia Pacific, Europe & America increase of $72 million was due to higher losses in South Asia, Indonesia Cards as well as commercial property downgrades in Cambodia and North Asia.

The collective provision charge decreased $576 million during the year to $242 million, with a decrease in Australia partially offset by increases in New Zealand and Asia Pacific, Europe & America. The decrease in Australia was due mainly to lower institutional lending and concentration provision releases following defaults by a small number of large customers within Institutional crystallising losses which were provided for in 2008. This was partly offset by increases within the Cards portfolio due to higher delinquencies and bankruptcies, and risk deterioration in Esanda and Investment and Insurance Products. The New Zealand charge increased $127 million reflecting a rise in unsecured consumer delinquencies and a weakening risk profile across the portfolio. Unfavourable risk movements were also experienced in Asia Pacific, Europe & America, particularly across Europe and America and this, coupled with refinements to methodology, resulted in increased charges of $106 million.

8ANZ Annual Report 2009

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Credit Risk on Derivatives

ANZ recognised $135 million of credit risk on derivatives during the year as a reduction to other income in the Income Statement in the statutory accounts. The charge relating to the credit intermediation trades are part of the adjustments to arrive at underlying profit. The decrease of $552 million over the 2008 year resulted from narrowing credit spreads.

| | | | | | | | |

| | | 2009

$m | | | 2008

$m | |

Credit risk on derivatives | | | | | | | | |

Credit intermediation trade related | | | 53 | | | | 531 | |

Credit risk on impaired derivatives | | | 82 | | | | 156 | |

| | | | | | | | |

Credit risk on derivatives | | | 135 | | | | 687 | |

| | | | | | | | |

This charge arose from:

| • | | changes to the creditworthiness of counterparties to our structured credit intermediation trades, |

| • | | defaults on customer derivative exposures with two mining companies and a financial institution, and |

| • | | changes in counterparty credit ratings on the remainder of our derivatives portfolio. |

ANZ entered into a series of structured credit intermediation trades from 2004 to 2007. The underlying structures involve credit default swaps (CDS) over synthetic collateralised debt obligations (CDOs) (78%), portfolios of external collateralised loan obligations (CLOs) (13%) or specific bonds/floating rate notes (FRNs) (9%).

ANZ sold protection using credit default swaps over these structures and then to mitigate risk purchased protection via credit default swaps over the same trades from eight US financial guarantors.

As derivatives, both the sold protection and purchased protection are marked-to-market. Prior to the commencement of the global credit crisis, gains and losses were not significant and offset each other in income.

At 30 September 2009, the value of the obligation under the sold protection is USD 897 million, for which the purchased protection has produced only a partial offset as:

| • | | one of the purchased protection counterparties has defaulted and many of the remaining were downgraded, and |

| • | | ANZ has made a credit valuation adjustment on the remaining counterparties reflective of changes to credit spreads. |

The current charge includes $85 million in realised losses relating to restructuring trades to reduce risks which were unhedged due to default by the purchased protection counterparty. It also includes net foreign exchange hedging losses.

The credit risk expense on structured credit derivatives is very volatile reflecting the impact of market movements in credit spreads and USD/AUD rates. It is likely there will continue to be substantial volatility in this market value.

Impaired assets

Gross impaired loans at $4,392 million represent a $2,642 million increase over 30 September 2008, driven mainly by increases in Australia and New Zealand. The increase in Australia was predominantly across entities within the Institutional Relationships, Corporate Banking and Financial Institution portfolios, with the ten largest impaired loan customers representing 60% of the total Australia gross impaired loans balance. There was an increase in Australia division across most businesses, as deterioration in the economic environment resulted in higher levels of default, particularly within Esanda, Business Banking and Investment and Insurance Products. The New Zealand increase of $699 million was driven primarily by customer downgrades in the small business, commercial, agribusiness segments and mortgages portfolios. Asia Pacific, Europe & America increased slightly, driven by increases in Europe and America.

Capital and funding

ANZ took early and measured steps to manage its capital and funding programs throughout the global financial crisis. This included initiatives to strengthen the balance sheet, boost liquidity and the quantity and composition of capital, to stay ahead of changes in the cycle and to allow the Group to capitalise on opportunities that have and will arise.

ANZ’s capital base has been progressively strengthened since late 2007 but most recently through the raising of $5.7 billion of ordinary equity. The Group’s Tier 1 capital ratio was 10.6% at the end of September 2009 compared to 7.7% a year ago. Adjusting for the announced acquisitions of certain RBS assets in Asia and the ING Group’s share of the ING Australia and ING New Zealand joint ventures, the pro-forma Tier 1 ratio reduces to 9.5%.

Global liquidity conditions have improved over the year. Deposit growth has been strong with the proportion of total funding from customers increasing from 50% to 55%. ANZ executed its full year term wholesale funding requirements well ahead of schedule raising a total of $25.8 billion. A combination of stronger deposit growth and consistent term debt issuance has reduced the reliance on short term wholesale funding from 22% to 17%.

Chief Financial Officer’s Report 9

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Balance Sheet Summary

| | | | | | | | | | | | |

| | | 2009

$m | | | 2008

$m | | | Movt | |

Assets | | | | | | | | | | | | |

Liquid assets | | | 25,317 | | | | 25,030 | | | | 1 | % |

Due from other financial institutions | | | 4,985 | | | | 9,862 | | | | -49 | % |

Trading and available-for-sale assets | | | 47,566 | | | | 32,657 | | | | 46 | % |

Derivative financial instruments | | | 37,404 | | | | 36,941 | | | | 1 | % |

Net loans and advances including acceptances | | | 345,769 | | | | 349,851 | | | | -1 | % |

Other | | | 15,946 | | | | 15,952 | | | | 0 | % |

| | | | | | | | | | | | |

Total Assets | | | 476,987 | | | | 470,293 | | | | 1 | % |

| | | | | | | | | | | | |

Liabilities | | | | | | | | | | | | |

Due to other financial institutions | | | 19,924 | | | | 20,092 | | | | -1 | % |

Deposits and other borrowings | | | 294,370 | | | | 283,966 | | | | 4 | % |

Derivative financial instruments | | | 36,516 | | | | 31,927 | | | | 14 | % |

Liability for acceptances | | | 13,762 | | | | 15,297 | | | | -10 | % |

Bonds and notes | | | 57,260 | | | | 67,323 | | | | -15 | % |

Other | | | 22,726 | | | | 25,136 | | | | -10 | % |

| | | | | | | | | | | | |

Total liabilities | | | 444,558 | | | | 443,741 | | | | 0 | % |

| | | | | | | | | | | | |

Total equity | | | 32,429 | | | | 26,552 | | | | 22 | % |

| | | | | | | | | | | | |

Analysis of movements in balance sheet captions on a statutory basis is set out on the following page.

10ANZ Annual Report 2009

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Growth in the balance sheet was subdued reflecting the challenging economic environment experienced during the last twelve months with asset growth of $6.7 billion or 1% and liability growth of $0.8 billion. Movements in exchange rates have resulted in a decrease of $6.7 billion for the year ended 30 September 2009. Excluding the impact of exchange rates, total assets increased 3%.

Movements in the major asset and liability categories include:

| • | | Liquid assets increased $0.3 billion to $25.3 billion at 30 September 2009. Strong growth was evident in America (up $4.5 billion) due primarily to an increase in bills receivable and Singapore (up $2.2 billion) within bank certificates of deposits where funds were redeployed from interbank placements for better yields. This was partially offset by reductions in the United Kingdom of $2.9 billion, New Zealand of $1.4 billion and Group Treasury of $0.9 billion. |

| • | | Due from other financial institutions decreased $4.9 billion to $5.0 billion at 30 September 2009 due mainly to a reduction in interbank lending volumes in Transaction Banking in Australia and Singapore. |

| • | | Trading and available-for-sale assets increased $14.9 billion to $47.6 billion at 30 September 2009, primarily in trading securities within the Markets business in Australia due to a build up in liquidity levels. These securities are high quality paper. |

| • | | Derivative assets increased $0.5 billion to $37.4 billion at 30 September 2009 and derivative liabilities increased $4.6 billion to $36.5 billion at 30 September 2009. The increase was driven by volatility in foreign exchange, interest rate and credit derivative markets. |

| • | | Net loans and advances including acceptances contracted slightly by 1% to $345.8 billion at 30 September 2009. Australia grew by $0.7 billion, with housing loans in Mortgages increasing by $12.7 billion (10%), partially offset by reduced lending in Institutional, primarily in Specialised Lending and Markets, of $12.1 billion (20%) driven by equity raisings in capital markets and widespread deleveraging prompting paydown of loan balances. New Zealand declined by $2.4 billion or 3%. |

| | | Excluding the impact of exchange rates the contraction was smaller at $0.7 billion (1%), with growth in Rural Banking of $1.2 billion (8%) being offset by reductions in the Institutional business of $0.9 billion (13%) and Corporate & Commercial Banking of $0.6 billion (5%). Asia Pacific, Europe & America decreased $2.4 billion (11%) due to a reduction in the United Kingdom and America of $1.4 billion (18%). |

| • | | Deposits and other borrowings increased $10.4 billion to $294.4 billion at 30 September 2009. Excluding the impact of exchange rate movements, deposits and other borrowings increased $14.6 billion (5%), driven by an increase in customer deposits of $29.4 billion (14%), partly offset by a decrease in wholesale funding of $14.8 billion (19%). Australia increased $10.6 billion (6%) predominantly driven by the robust growth in retail deposits. Growth was mainly in Deposits ($15.5 billion), partly offset by decreases in Esanda of $9.1 billion, following the winding back of debentures, and Group Treasury ($5.4 billion). New Zealand Businesses decreased $5.9 billion (9%) driven by a reduction in commercial paper issued by Treasury. Asia Pacific, Europe & America increased $5.7 billion (16%) primarily from Singapore through successful initiatives to raise deposit levels and additional certificates of deposit issued in the United Kingdom for funding requirements. |

| • | | Bonds and notes decreased $10.1 billion to $57.3 billion at 30 September 2009 driven by exchange rate movements. |

Chief Financial Officer’s Report11

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Australia Region

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Net interest income | | | 7,085 | | | | 5,677 | | | | 25 | % |

Other external operating income | | | 2,677 | | | | 2,849 | | | | -6 | % |

| | | | | | | | | | | | |

Operating income | | | 9,762 | | | | 8,526 | | | | 14 | % |

Operating expenses | | | (4,034 | ) | | | (3,677 | ) | | | 10 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 5,278 | | | | 4,849 | | | | 18 | % |

Provision for credit impairment | | | (2,053 | ) | | | (1,663 | ) | | | 23 | % |

| | | | | | | | | | | | |

Profit before income tax | | | 3,675 | | | | 3,186 | | | | 15 | % |

Income tax expense | | | (1,113 | ) | | | (917 | ) | | | 21 | % |

Minority interest | | | (2 | ) | | | (2 | ) | | | 0 | % |

| | | | | | | | | | | | |

Underlying profit | | | 2,560 | | | | 2,267 | | | | 13 | % |

| | | | | | | | | | | | |

Adjustments between statutory profit and underlying profit1 | | | (476 | ) | | | (160 | ) | | | large | |

| | | | | | | | | | | | |

Profit | | | 2,084 | | | | 2,107 | | | | -1 | % |

| | | | | | | | | | | | |

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses, timing differences on economic hedges, and acquisition related costs. Refer page 6. |

Profit after tax decreased $23 million or 1% to $2,084 million for the year ended 30 September 2009. On an underlying basis profit increased $293 million (13%).

Significant influences on underlying profit were:

| • | | Net interest income increased 25% driven by an increase in net interest margin of 29 basis points, while average net loans and advances grew by 7% and average deposits grew by 11%. Higher funding benefits associated with unrealised trading gains (offset by a decrease in trading income) had an 11 basis point positive impact. Excluding this, margin improved by 18 basis points with higher margins in Australia division in Retail and Commercial reflecting repricing for risk and recouping higher funding costs and increased margins in Institutional Australia reflecting repricing on the corporate lending book and management of interest rate risk in Markets. Growth in balance sheet volume was driven by Australia division, with Retail customer deposits up 28% reflecting increased market share and net loans and advances up 10% in Mortgages. |

| • | | Other external operating income decreased 6%. Excluding the offset to the derivative funding benefit in net interest income, other external operating income increased 5% driven by strong trading and sales revenues generated in a volatile market and favourable growth in Retail driven by fee revenue mainly in Deposits. This was partially offset by a decline in income in Wealth from lower investment and advisory income and a lower contribution from the INGA business. |

| • | | Operating expenses increased 10% or $357 million. Institutional Australia increased 21% or $178 million due primarily to investment in frontline staff and systems, salary inflation and remuneration costs. Australia division increased 4% or $114 million with increased volume growth related personnel in service delivery and collections areas, salary inflation, premises costs and investment in systems, partly offset by savings due to productivity, restructuring and offshoring activities. Increases of $61 million within Group Centre include increased expenditure on transformation activity. |

| • | | Provision for credit impairment increased $390 million (23%). The individual provision charge increased by $1,199 million driven by higher loss rates across all portfolios and increased bankruptcies, liquidations and a significant reduction in Retail resale options. In addition, Institutional Australia experienced several large single name provisions. The collective provision charge decreased by $809 million with the release of collective provision provided in 2008 as actual losses crystallised and flowed through the 2009 individual provision charge within Institutional Australia, partly offset by increases within the Cards portfolio due to higher delinquencies and bankruptcies and Esanda and Wealth due to risk deterioration. |

12ANZ Annual Report 2009

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Asia Pacific, Europe and America Region

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Net interest income | | | 846 | | | | 473 | | | | 79 | % |

Other external operating income | | | 1,121 | | | | 736 | | | | 52 | % |

| | | | | | | | | | | | |

Operating income | | | 1,967 | | | | 1,209 | | | | 63 | % |

Operating expenses | | | (852 | ) | | | (554 | ) | | | 54 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 1,115 | | | | 655 | | | | 70 | % |

Provision for credit impairment | | | (276 | ) | | | (176 | ) | | | 57 | % |

| | | | | | | | | | | | |

Profit before income tax | | | 839 | | | | 479 | | | | 75 | % |

Income tax expense | | | (140 | ) | | | (87 | ) | | | 61 | % |

Minority interest | | | — | | | | (6 | ) | | | -100 | % |

| | | | | | | | | | | | |

Underlying profit | | | 699 | | | | 386 | | | | 81 | % |

| | | | | | | | | | | | |

Adjustments between statutory profit and underlying profit1 | | | 1 | | | | (5 | ) | | | large | |

| | | | | | | | | | | | |

Profit | | | 700 | | | | 381 | | | | 84 | % |

| | | | | | | | | | | | |

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses, timing differences on economic hedges, and acquisition related costs. Refer page 6. |

Profit after tax increased $319 million or 84% (55% excluding exchange rate impacts) to $700 million for the year ended 30 September 2009 (on an underlying basis profit grew $313 million or 81%).

This increase was driven by strong growth in the Institutional business as it benefited from currency and rates volatility in the region particularly in the early part of the year. Continued investment in front office sales capability generated a significant increase in trade sales. The Asia Partnerships also contributed significantly to the result with increased equity accounted earnings, particularly from Shanghai Rural Commercial Bank (SRCB) and Bank of Tianjin (BoT) in China and AMMB Holdings Berhad (AMMB) in Malaysia (including improved assessment of credit provisioning requirements), offsetting an impairment charge relating to the carrying value of our investment in Saigon Securities Inc (SSI) in Vietnam.

Operating expenses increased as a result of the continued investment in the key strategic markets of Indonesia, Vietnam and China as well as building our operating and support capabilities.

Key factors affecting the underlying result were:

| • | | Net interest income increased by 79% (43% excluding exchange rate impacts) due to significant increases in our Global Markets business. While net loans and advances were down 11% year on year as we de-risked our balance sheet, overall external assets were up 3% due primarily to increased Markets activities. Customer deposits grew a healthy 35% improving our deposits to loans ratio to 160%. Margins increased by 47 basis points to 170 basis points (18 basis points increase excluding cash flow on derivatives). |

| • | | Other external operating income grew by 52% (40% excluding exchange rate impacts), of which more than half was contributed by equity accounted earnings from our Asia Partnerships which included benefit from reassessed credit provisioning requirements. Fee and other income were significantly higher in the Markets businesses leveraging off volatility in the currency markets. |

| • | | Operating expenses increased 54% (32% excluding exchange rate impacts) through a combination of new investments, and growth across the region in employee numbers. Employees increased by 1,786 as we continue to build core capability in the region and increase our operations and technology support staff in Bangalore. |

| • | | Provision for credit impairment increased by 57% ($100 million) due primarily to risk grade decreases and an additional $43 million as a result of a refinement to the collective provision calculation in 2009. |

Chief Financial Officer’s Report 13

CHIEF FINANCIAL OFFICER’S REPORT (continued)

New Zealand Region

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Net interest income | | | 1,879 | | | | 1,705 | | | | 10 | % |

Other external operating income | | | 759 | | | | 855 | | | | -11 | % |

| | | | | | | | | | | | |

Operating income | | | 2,638 | | | | 2,560 | | | | 3 | % |

Operating expenses | | | (1,182 | ) | | | (1,175 | ) | | | 1 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 1,456 | | | | 1,385 | | | | 5 | % |

Provision for credit impairment | | | (727 | ) | | | (251 | ) | | | large | |

| | | | | | | | | | | | |

Profit before income tax | | | 729 | | | | 1,134 | | | | -36 | % |

Income tax expense | | | (216 | ) | | | (361 | ) | | | -40 | % |

| | | | | | | | | | | | |

Underlying profit | | | 513 | | | | 773 | | | | -34 | % |

| | | | | | | | | | | | |

Adjustments between statutory profit and underlying profit1 | | | (354 | ) | | | 58 | | | | large | |

| | | | | | | | | | | | |

Profit | | | 159 | | | | 831 | | | | -81 | % |

| | | | | | | | | | | | |

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses, timing differences on economic hedges, and acquisition related costs. Refer page 6. |

Profit decreased 81% impacted by negative adjustments between statutory profit and underlying profit of $412 million, principally tax provisioning on Conduits and the ING investor settlement. After excluding adjustments to arrive at statutory profit, underlying profit reduced 34%, largely driven by a $344 million after tax increase in credit impairment expense, with credit cycle impacts felt across all businesses. Operating income in the New Zealand Businesses declined 7%, with lending growth constrained by de-leveraging underway in the consumer and business sectors, and net interest margin contracting as a result of deposit competition. The Institutional business, however, delivered a 33% increase in revenue, with Markets taking advantage of opportunities presented by volatility during the first half.

| • | | Net interest income increased 10%. After adjusting for a $185 million increase in net interest income from derivative and liquidity positions that was offset by a decrease in trading income, net interest income was down 1%. The result was driven by a strong contribution from positioning the balance sheet (mismatch earnings) and earnings on higher levels of retained capital, moderated by margin contraction of 26 basis points in our core Retail and Commercial businesses. Margin contraction reflected intensified competition for deposits driven by increased wholesale funding spreads, and the delay in passing these costs on due to the predominance of fixed rate mortgages in the lending book, as well as adverse break costs on mortgages as customers take advantage of falling interest rates. |

| • | | Excluding the change in composition of the derivative and liquidity result referred to above, other external operating income increased 10%, largely reflecting a strong Markets result. |

| • | | Operating expenses increased 1%. Costs have been well managed, reflecting benefits from business transformation strategies that have been in place over the last year, as well as from strong control of discretionary expenditure. These have offset the increase in costs from the acquisition of a subsidiary as part of a debt restructure, higher remuneration costs in Institutional and higher business transformation costs. |

| • | | Provision for credit impairment charge increased $476 million as a result of credit cycle impacts across the businesses. The individual provision charge increased $349 million, reflecting an increase in loss rate from the relatively low level of 20 basis points in the 2008 year to 64 basis points in 2009. This was largely from general deterioration across the book, with the largest increase in the Commercial businesses, albeit from relatively low levels in 2008. An increase of $42 million in Institutional largely related to a single name exposure. The collective provision charge increased $130 million with the largest increases in the Commercial businesses as a result of economic cycle risk adjustments booked in the second half. The total provision coverage (ratio of total provisions held to credit risk weighted assets) at September 2009 was strong at 2.12%, up from 1.11% in 2008. |

14ANZ Annual Report 2009

CHIEF FINANCIAL OFFICER’S REPORT (continued)

Institutional Division

(Global line of business, also included in each of the regions discussed on pages 12 to 14).

| | | | | | | | | | | | |

Income Statement ($m) | | 2009 | | | 2008 | | | Movt | |

Net interest income | | | 3,041 | | | | 1,823 | | | | 67 | % |

Other operating income | | | 1,907 | | | | 1,801 | | | | 6 | % |

| | | | | | | | | | | | |

Operating income | | | 4,948 | | | | 3,624 | | | | 37 | % |

Operating expenses | | | (1,583 | ) | | | (1,245 | ) | | | 27 | % |

| | | | | | | | | | | | |

Profit before credit impairment and income tax | | | 3,365 | | | | 2,379 | | | | 41 | % |

Provision for credit impairment | | | (1,408 | ) | | | (1,281 | ) | | | 10 | % |

| | | | | | | | | | | | |

Profit before income tax | | | 1,957 | | | | 1,098 | | | | 78 | % |

Income tax expense and minority interest | | | (556 | ) | | | (327 | ) | | | 70 | % |

| | | | | | | | | | | | |

Underlying profit | | | 1,401 | | | | 771 | | | | 82 | % |

| | | | | | | | | | | | |

Profit after tax increased $630 million or 82% to $1,401 million for the year ended 30 September 2009.

The refocus on Institutional’s global client segment propositions drove revenue in areas of core client demand. Interest rate and general market volatility and increased customer focus delivered Global Markets trading and sales revenue growth of 77%. Transaction Banking revenue grew by 12% and Specialised Lending revenue grew by 23%. Net lending assets fell by 18% during the year, where an increase in equity raisings in capital markets and a general response to the economic environment prompted the pay down of lending. Net interest margin (excluding cash flow on derivatives) increased by 32 basis points in response to widening credit spreads and repricing for risk. Customer deposits increased by $12.5 billion during the year reflecting our focus on core client needs in a volatile environment while reducing reliance on wholesale borrowing. Expenses grew by 27% reflecting the investment in the “Rebuild and Refocus” program and building our client franchises particularly in Asia where employee numbers increased by 188 to support business growth in that region. In addition, remuneration costs increased associated with attracting experienced bankers and specialist staff.

Provision for credit impairment was up 10%. Individual provisions of $1.5 billion were predominantly in Australia in the first half, largely related to securities lending, property exposures, agribusiness and a limited number of corporate names. This was offset in part by a net release of collective provision of $136 million, reflecting the release of some of the $300 million concentration risk and economic cycle collective provision booked in the prior financial year for exposures to financial services and property sectors which crystallised during the year, lower volumes and allowance for concentration risks at the end of the year. Net non performing loans grew to $1.8 billion, although the rate of growth slowed significantly in the second half.

Significant factors affecting the result were as follows:

| • | | Global Markets revenue increased 77% to $2.2 billion with strong trading and sales revenues generated in a volatile market. |

| • | | Net interest margin increased by 69 basis points to 2.05%. Excluding the impact of higher funding benefits associated with unrealised trading gains (offset by an equivalent decrease in trading income), net interest margin increased 32 basis points reflecting widening spreads and repricing for risk. |

| • | | Asia Pacific, Europe & America revenue increased reflecting strategic investment in the region. |

| • | | New Zealand revenue growth was 33%, despite poor local economic conditions. Revenue growth was driven mainly by Global Markets. |

Chief Financial Officer’s Report 15

Ten Year Summary

| | | | | | | | | | | | | | | | | | |

| | | | | 2009

$m | | | 2008

$m | | | 2007

$m | | | 2006

$m | |

Financial Performance1 | | | | | | | | | | | | | | | | |

Net interest income | | | 9,810 | | | | 7,855 | | | | 7,302 | | | | 6,943 | |

Other operating income | | | 4,557 | | | | 4,440 | | | | 3,765 | | | | 3,146 | |

Operating expenses | | | (6,068 | ) | | | (5,406 | ) | | | (4,953 | ) | | | (4,605 | ) |

Profit before income tax, credit impairment and non-core items1 | | | 8,299 | | | | 6,889 | | | | 6,114 | | | | 5,484 | |

Provision for credit impairment | | | (3,056 | ) | | | (2,090 | ) | | | (567 | ) | | | (407 | ) |

Income tax expense | | | (1,469 | ) | | | (1,365 | ) | | | (1,616 | ) | | | (1,486 | ) |

Minority interest | | | (2 | ) | | | (8 | ) | | | (7 | ) | | | (4 | ) |

| | | | | | | | | | | | | | | | | | |

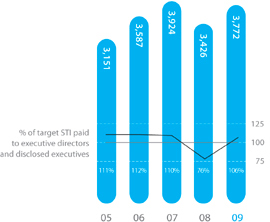

Underlying profit1 | | | 3,772 | | | | 3,426 | | | | 3,924 | | | | 3,587 | |

Adjustments between statutory profit and underlying profit1 | | | (829 | ) | | | (107 | ) | | | 256 | | | | 101 | |

| | | | | | | | | | | | | | | | | | |

Profit attributable to shareholders of the Company | | | 2,943 | | | | 3,319 | | | | 4,180 | | | | 3,688 | |

| | | | | | | | | | | | | | | | | | |

Financial Position | | | | | | | | | | | | | | | | |

Assets2 | | | 476,987 | | | | 470,293 | | | | 392,773 | | | | 334,640 | |

Net Assets | | | 32,429 | | | | 26,552 | | | | 22,048 | | | | 19,906 | |

Tier 1 capital ratio3 | | | 10.6 | % | | | 7.7 | % | | | 6.7 | % | | | 6.8 | % |

Return on average ordinary equity4,5 | | | 10.3 | % | | | 14.5 | % | | | 20.9 | % | | | 20.7 | % |

Return on average assets4 | | | 0.6 | % | | | 0.8 | % | | | 1.2 | % | | | 1.1 | % |

Cost to income ratio6 | | | 42.2 | % | | | 44.0 | % | | | 44.9 | % | | | 45.6 | % |

| | | | | | | | | | | | | | | | | | |

Shareholder value – ordinary shares | | | | | | | | | | | | | | | | |

Total return to shareholders | | | | | | | | | | | | | | | | |

(share price movement plus dividends) | | | 40.3 | % | | | -33.5 | % | | | 15.6 | % | | | 17.1 | % |

Market capitalisation | | | 61,085 | | | | 38,263 | | | | 55,382 | | | | 49,331 | |

Dividend | | | 102c | | | | 136c | | | | 136c | | | | 125c | |

| Franked portion | | –interim | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % |

| | – final | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % |

| Share price7 | | – high | | $ | 24.99 | | | $ | 31.74 | | | $ | 31.50 | | | $ | 28.66 | |

| | – low | | $ | 11.83 | | | $ | 15.07 | | | $ | 25.75 | | | $ | 22.70 | |

| | –30 Sep | | $ | 24.39 | | | $ | 18.75 | | | $ | 29.70 | | | $ | 26.86 | |

| | | | | | | | | | | | | | | | | | |

Share information | | | | | | | | | | | | | | | | |

(per fully paid ordinary share) | | | | | | | | | | | | | | | | |

Earnings per share7 | | | 131.0c | | | | 170.4c | | | | 224.1c | | | | 200.0c | |

Dividend payout ratio8 | | | 82.3 | % | | | 82.7 | % | | | 60.9 | % | | | 62.6 | % |

Net tangible assets per ordinary share9 | | $ | 11.02 | | | $ | 10.72 | | | $ | 9.36 | | | $ | 8.53 | |

No. of fully paid ordinary shares issued (millions) | | | 2,504.5 | | | | 2,040.7 | | | | 1,864.7 | | | | 1,836.6 | |

Dividend Reinvestment Plan (DRP) issue price | | | | | | | | | | | | | | | | |

| | –interim | | $ | 15.16 | | | $ | 20.82 | | | $ | 29.29 | | | $ | 26.50 | |

| | – final | | | — | | | $ | 13.58 | | | $ | 27.33 | | | $ | 28.25 | |

| | | | | | | | | | | | | | | | | | |

Other information | | | | | | | | | | | | | | | | |

Points of representation10 | | | 1,352 | | | | 1,340 | | | | 1,327 | | | | 1,265 | |

No. of employees (full time equivalents) | | | 37,687 | | | | 36,925 | | | | 34,353 | | | | 32,256 | |

No. of shareholders11 | | | 396,181 | | | | 376,813 | | | | 327,703 | | | | 291,262 | |

| | | | | | | | | | | | | | | | | | |

| 1 | Adjusted for material items that are not part of the normal ongoing operations of the Group including one-off gains and losses, gains and losses on the sale of businesses, non-continuing businesses timing differences on economic hedges, and acquisition related costs, refer page 6. Prior to 2009 these were adjustments to arrive at cash profit in accordance with market convention. |

| 2 | From 2000 to 2001, consolidated assets include the statutory funds of ANZ Life as required by an accounting standard. For the year 2004, consolidated assets include the statutory funds of NBNZ Life Insurance Limited. ANZ Life was sold in May 2002 and NBNZ Life Insurance was sold on 30 September 2005. |

| 3 | Calculated in accordance with Australian Prudential Regulation Authority requirements effective at the relevant date. Basel II has been applied from 1 January 2008. |

| 4 | Excludes minority interest. The 2005 ratio has been calculated on an IFRS basis that is comparable with that of 2006. |

| 5 | For the periods 2000 to 2002, the return on average ordinary equity calculation accrues the dividend over the year. From 2003, dividends may no longer be accrued and are not included in the calculation of return on average ordinary equity. |

16ANZ Annual Report 2009

TEN YEAR SUMMARY (continued)

| | | | | | | | | | | | | | | | | | | | | | |

| | | | Previous AGAAP | |

2005 $m | | | 2004

$m | | | 2003

$m | | | 2002

$m | | | 2001

$m | | | 2000

$m | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 6,371 | | | | 5,252 | | | | 4,311 | | | | 4,018 | | | | 3,833 | | | | 3,801 | |

| | 2,935 | | | | 3,267 | | | | 2,808 | | | | 2,796 | | | | 2,573 | | | | 2,583 | |

| | (4,340 | ) | | | (4,005 | ) | | | (3,228 | ) | | | (3,153 | ) | | | (3,092 | ) | | | (3,314 | ) |

| | 4,966 | | | | 4,514 | | | | 3,891 | | | | 3,661 | | | | 3,314 | | | | 3,070 | |

| | (565 | ) | | | (632 | ) | | | (614 | ) | | | (610 | ) | | | (531 | ) | | | (502 | ) |

| | (1,247 | ) | | | (1,147 | ) | | | (926 | ) | | | (880 | ) | | | (911 | ) | | | (863 | ) |

| | (3 | ) | | | (4 | ) | | | (3 | ) | | | (3 | ) | | | (2 | ) | | | (2 | ) |

| | | | | | | | | | | | | | | | | | | | | | |

| | 3,151 | | | | 2,731 | | | | 2,348 | | | | 2,168 | | | | 1,870 | | | | 1,703 | |

| | 24 | | | | 84 | | | | — | | | | 154 | | | | — | | | | 44 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 3,175 | | | | 2,815 | | | | 2,348 | | | | 2,322 | | | | 1,870 | | | | 1,747 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 300,885 | | | | 259,345 | | | | 195,591 | | | | 183,105 | | | | 185,493 | | | | 172,467 | |

| | 19,538 | | | | 17,925 | | | | 13,787 | | | | 11,465 | | | | 10,551 | | | | 9,807 | |

| | 6.9 | % | | | 6.9 | % | | | 7.7 | % | | | 7.9 | % | | | 7.5 | % | | | 7.4 | % |

| | 18.3 | % | | | 19.1 | % | | | 20.6 | % | | | 21.6 | % | | | 20.2 | % | | | 19.3 | % |

| | 1.1 | % | | | 1.2 | % | | | 1.2 | % | | | 1.3 | % | | | 1.1 | % | | | 1.1 | % |

| | 46.6 | % | | | 45.3 | % | | | 45.1 | % | | | 46.0 | % | | | 48.0 | % | | | 51.7 | % |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 32.6 | % | | | 17.0 | % | | | 6.7 | % | | | 15.3 | % | | | 26.2 | % | | | 36.3 | % |

| | 43,834 | | | | 34,586 | | | | 27,314 | | | | 26,544 | | | | 23,783 | | | | 20,002 | |

| | 110c | | | | 101c | | | | 95c | | | | 85c | | | | 73c | | | | 64c | |

| | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % |

| | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % | | | 100 | % |

| $ | 24.45 | | | $ | 19.44 | | | $ | 18.45 | | | $ | 19.70 | | | $ | 16.71 | | | $ | 12.87 | |

| $ | 19.02 | | | $ | 15.94 | | | $ | 15.01 | | | $ | 15.23 | | | $ | 12.63 | | | $ | 9.18 | |

| $ | 24.00 | | | $ | 19.02 | | | $ | 17.17 | | | $ | 16.88 | | | $ | 15.28 | | | $ | 12.70 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 169.5c | | | | 153.1c | | | | 142.4c | | | | 141.4c | | | | 112.7c | | | | 102.5c | |

| | 65.0 | % | | | 67.5 | % | | | 64.2 | % | | | 57.8 | % | | | 62.0 | % | | | 59.1 | % |

| $ | 7.77 | | | $ | 7.51 | | | $ | 7.49 | | | $ | 6.58 | | | $ | 5.96 | | | $ | 5.49 | |

| | 1,826.4 | | | | 1,818.4 | | | | 1,521.7 | | | | 1,503.9 | | | | 1,488.3 | | | | 1,506.2 | |

| | | | | | | | | | | | | | | | | | | | | | |

| $ | 21.85 | | | $ | 17.84 | | | $ | 18.48 | | | $ | 19.24 | | | $ | 15.05 | | | $ | 11.62 | |

| $ | 23.85 | | | $ | 19.95 | | | $ | 16.61 | | | $ | 18.32 | | | $ | 18.33 | | | $ | 14.45 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | 1,223 | | | | 1,190 | | | | 1,019 | | | | 1,018 | | | | 1,056 | | | | 1,087 | |

| | 30,976 | | | | 28,755 | | | | 23,137 | | | | 22,482 | | | | 22,501 | | | | 23,134 | |

| | 263,467 | | | | 252,072 | | | | 223,545 | | | | 198,716 | | | | 181,667 | | | | 179,829 | |

| | | | | | | | | | | | | | | | | | | | | | |

| 6 | Excludes non-core items. Periods prior to 2005 also exclude goodwill amortisation. The 2005 ratio has been calculated on an IFRS basis that is comparable with that of 2006. |

| 7 | Periods prior to 2004 adjusted for the bonus elements of the November 2003 Rights Issue. |

| 8 | From 2003, the dividend payout ratio includes the final dividend proposed but not provided for in accordance with changes to accounting standards effective from the September 2003 financial year. |

| 9 | Equals shareholders’ equity less preference share capital, goodwill, software and other intangible assets divided by the number of ordinary shares. For periods prior to 2005, this equals shareholders’ equity less preference share capital and unamortised goodwill divided by the number of ordinary shares. |

| 10 | Includes branches, offices, representative offices and agencies. |

| 11 | Excludes employees whose only ANZ shares are held in trust under ANZ employee share schemes. |

Ten Year Summary 17

Directors’ Report

The directors present their report together with the Financial Report of the consolidated entity (the Group), being Australia and New Zealand Banking Group Limited (the Company) and its controlled entities, for the year ended 30 September 2009 and the Independent Auditor’s Report thereon. The information is provided in conformity with the Corporations Act 2001.

Principal Activities

The Group provides a broad range of banking and financial products and services to retail, small business, corporate and institutional clients.

The Group conducts its operations primarily in Australia and New Zealand and the Asia Pacific region. It also operates in a number of other countries including the United Kingdom and the United States.

At 30 September 2009, the Group had 1,352 branches and other points of representation worldwide excluding Automatic Teller Machines (ATMs).

Result

Consolidated profit after income tax attributable to shareholders of the Company was $2,943 million, a decrease of 11% over the prior year.

Strong growth in profit before credit impairment and income tax of $922 million or 14% was offset by an increase in the provision for credit impairment of $1,057 million or 54% reflecting the challenging economic conditions evident in each of the regions, but most pronounced in New Zealand.

Balance sheet growth was curtailed with total assets increasing 1% and total liabilities were largely in line with prior year.

Movements within the major components include:

| • | | Net advances growth contracted by 1% with growth in Mortgages within Australia of $12.7 billion offset by a reduction in lending in Institutional Australia of $12.2 billion as corporates deleveraged. |

| • | | Customer deposits and other funding liabilities increased by 14%, reducing the reliance on short term wholesale funding. During 2009, $25.8 billion of term wholesale debt was raised. |

Further details are contained on pages 6 to 15 of this Annual Report.

Stateof Affairs

In the directors’ opinion, there have been no significant changes in the state of affairs of the Group during the financial year, other than:

Impaired financial assets – an increase in gross non-performing loans of $2.6 billion over 30 September 2008 mainly reflected a number of downgrades in Australia and New Zealand as deterioration in the economic environment resulted in a higher level of default. The rate of growth in impaired financial assets slowed in the second half of the financial year.

Capital raisings – ANZ ordinary shares of $2.5 billion were raised via an institutional placement, a further $2.2 billion through a Share Purchase Plan to existing shareholders, and the final 2008 dividend was fully underwritten.

Organisational structure – Esanda Finance Corporation Limited transitioned from a wholly owned subsidiary towards being a division of the Company and ANZ established a licensed banking branch in New Zealand.

Asia expansion – ANZ is continuing to progress its super regional growth strategy with further branch expansion in Indonesia and Vietnam. In addition, ANZ is the one of the first International banks to open a rural bank in Western China.

Refer also to ‘Events Since the End of the Financial Year’ below for details on acquisitions which are expected to occur in 2010.

Further review of matters affecting the Group’s state of affairs is also contained in the Chief Financial Officer’s Report on pages 6 to 15 of this Annual Report.

Dividends

The directors propose that a final fully franked dividend of 56 cents per fully paid ordinary share shall be paid on 18 December 2009. The proposed payment amounts to approximately $1,403 million.

During the financial year, the following fully franked dividends were paid on fully paid ordinary shares:

| | | | | | | | | | | | |

Type | | Cents

per share | | | Amount before bonus

option plan adjustment

$m | | | Date of

payment | |

Final 2008 | | | 74 | | | | 1,514 | | | | 18 December 2008 | |

Interim 2009 | | | 46 | | | | 993 | | | | 1 July 2009 | |

The proposed final dividend of 56 cents together with the interim dividend of 46 cents brings total dividends in relation to the year ended 30 September 2009 to 102 cents fully franked.

Review of Operations

Review of the Group during the financial year and the results of those operations, including an assessment of the financial position and business strategies of the Group, is contained in the Chairman’s Report, the Chief Executive Officer’s Report and the Chief Financial Officer’s Report on pages 2 to 15 of this Annual Report.

18ANZ Annual Report 2009

DIRECTORS’ REPORT (continued)

Events Since the End of the Financial Year

On 25 September 2009, the Company announced it had reached agreement with ING Groep to acquire ING Groep’s 51% shareholdings in the ANZ-ING wealth management and life insurance joint ventures in Australia and New Zealand for $1,760 million, taking its ownership interest to 100%. Completion is subject to various conditions, including regulatory approval, and is expected to occur during the fourth quarter of calendar 2009. Once completed, the acquisition will result in the Group fully consolidating the assets, liabilities and operations of ING Australia Limited (“INGA”) and ING (NZ) Holdings Limited (“INGNZ”) and its subsidiary companies into the Group’s results. At acquisition date, under the step acquisition provisions of AASB3R Business Combinations (Revised) which will come into effect in 2010, the Group will remeasure its existing 49% interests which are accounted for under the equity method at acquisition date fair values and will recognise the resulting gain or loss in the income statement.

On 4 August 2009 the Company announced it had reached agreement with Royal Bank of Scotland Group plc to acquire selected businesses in Taiwan, Singapore, Indonesia1, Hong Kong, Phillipines and Vietnam. The purchase price is based on the fully recapitalised net tangible book value of these businesses plus a premium of USD50 million and whilst the ultimate purchase price is not determinable until completion it is estimated to amount to approximately USD550 million (AUD626 million). Each acquisition is subject to regulatory approval in the relevant jurisdictions, which is expected to occur from late calendar 2009 through 2010. Accordingly these acquisitions are expected to be progressively consolidated into the 2010 results including the impacts of acquisition accounting, integration and acquisition costs.

| 1 | The Indonesian business will be acquired through ANZ’s 85% owned subsidiary P.T. Bank Pan Indonesia. |

FutureDevelopments

Details of likely developments in the operations of the Group and its prospects in future financial years are contained in this Annual Report under the Chairman’s Report. In the opinion of the directors, disclosure of any further information would be likely to result in unreasonable prejudice to the Group.

Environmental Regulation

ANZ recognises our obligations to our stakeholders – customers, shareholders, staff and the community – to operate in a way that advances sustainability and mitigates our environmental impact. Our commitment to improve our environmental performance is integral to successfully navigating responsible growth.

We acknowledge that we have an impact on the environment:

| • | | directly through the conduct of our business operations; and |