Exhibit 99.1

ANZ 2017 ANNUAL REPORT

WE WANT OUR CUSTOMERS TO VALUE US AND THE COMMUNITY TO TRUST US. FOR THIS TO HAPPEN WE KNOW THAT THINGS NEED TO CHANGE AT ANZ.

| ||||

Cover story — Latrobe Valley Bus Lines

Rhonda Renwick and her dedicated team at Latrobe Valley Bus Lines are rolling out new buses that are at the leading edge of transport technology in Australia.

Since 2015 Latrobe Valley Bus Lines has been investing in low emission technologies which improve the efficiency and environmental impact of its buses.

The newest vehicles in the fleet have been designed to dramatically reduce particulate emissions in the atmosphere. Latrobe Valley Bus Lines has been trialling new hybrid technology and will introduce eight new hybrid vehicles into the fleet over the next three years.

As the company focuses on its mission of helping the community, and providing the highest quality and safest service for its customers and employees, it has benefitted from its long-term relationship with ANZ.

“ANZ’s proactive team has a genuine understanding of our business goals, providing flexibility along with competitive banking options,” Rhonda explains. |

We are proud to be supporting a business like Latrobe Valley Bus Lines — a Certified B Corporation — which shares our commitment to helping communities thrive. It supports local manufacturing, is dedicated to fostering an inclusive and safe workplace and promotes a number of grassroots community organisations. | |||

CONTENTS

| ||||||||||||||||

| Our 2017 Reporting Suite | 3 | Our Approach to Risk Management | 34 | |||||||||||||

| 2017 Highlights | 4 | Remuneration Report | 36 | |||||||||||||

| Chairman’s Message | 6 | Directors’ Report | 62 | |||||||||||||

| CEO’s Message | 8 | Auditor’s Independence Declaration | 64 | |||||||||||||

| About our Business | 10 | Financial Report | 65 | |||||||||||||

| Our Strategy | 12 | Shareholder Information | 161 | |||||||||||||

| Our Performance | 14 | Glossary | 169 | |||||||||||||

| Governance | 24 | Contacts | 171 | |||||||||||||

2

OUR 2017 REPORTING SUITE

|

| |||||||||||||||

|

| OUR 2017

REPORTING SUITE

|

| ||||||||||||||

|

| |||||||||||||||

|

| Stakeholder expectations of corporate reporting are changing and we need to respond. We recognise that stakeholders want a more holistic understanding of how we are creating value over time — beyond the short or medium-term — and the opportunities and challenges impacting our future. A strong financial performance each year, while critical to the success of the bank, is not of itself the whole story and reflects little about who we are as an organisation and the role we play in society.

Our core reporting suite includes:

This report, our2017 Annual Report, which

Our2017 Annual Review which concisely |

| OurCorporate Governance Statement which discloses the extent to which ANZ has complied with the ASX Corporate Governance Council’s ‘Corporate Governance Principles & Recommendations — 3rd edition’. We also provide ourPrincipal Risks and Uncertainties. Both are available atanz.com/corporategovernance.

Our 2017 ANZ Corporate Sustainability Review which informs stakeholders about our performance against our material social, environmental and economic opportunities and challenges.

We will continue to evolve and improve our reporting suite over the coming years and therefore welcome feedback on this report. Please address any questions, comments or suggestions toinvestor.relations@anz.com. | |||||||||||||

|

| ANZ’s 2017 reporting suite also includes the

• News Release

• Results Presentation and Investor Discussion Pack

• Results Announcement

• The Company 2017 Financial Report

• UK DTR Submission – Principal Risks and Uncertainties

• APS 330 Pillar III Disclosure at 30 September 2017

1. 2017 Annual Reviewanz.com/annualreport 2. 2017 Corporate Governance Statementanz.com/corporategovernance 3. 2017 ANZ Corporate Sustainability Reviewanz.com/cs | ||||||||||||||

| 3 | |||||||||||||||

ANZ 2017 ANNUAL REPORT

| 1. | Cash profit excludesnon-core items included in statutory profit and is provided to assist readers in understanding the result of the ongoing business activities of the Group. |

| 2. | Total taxes borne by the Group, includes unrecovered GST/VAT, employee related taxes and other taxes. |

| 3. | Figure includes foregone revenue of $107 million, being the cost of providing low orfee-free accounts to a range of customers such as government benefit recipients,not-for-profit organisations and students. |

| 4. | From premises energy against a 2013 baseline. |

| 5. | This is the estimated number of people who have benefited from ANZ’s MoneyMinded financial education program since 2003. |

2017 HIGHLIGHTS

$6.9

BN

cash profit1

$3,415M

taxes paid2

11.9%

cash return on equity1

$131M

in community investment (includes foregone revenue)3

20% reduction in Greenhouse Gas emissions4

496,900+

people reached through our financial education program MoneyMinded5

4

2017 HIGHLIGHTS

| 6. | Includes Aboriginal and Torres Strait Islander people, people with a disability and refugees. |

| 7. | Includes assets and liabilities held for sale. |

“THE MARKETPLACE GAVE VISITORS A CHANCE TO LEARN ABOUT THE IMPORTANT JOB OUR LOCAL FARMERS DO IN PRODUCING OUR FOOD”

— Christine Linden, General Manager, Regional Business Banking, ANZ

113,127

hours volunteered by employees

250

people employed from under-represented groups6

160

CENTS

fully franked dividend for FY17

$6.9BN

funded and facilitated in low carbon and sustainable solutions since 2015

NET AFTER PROFIT TAX $M

NET AFTER PROFIT TAX (Cash1) $M

PROFIT BEFORE AND PROVISIONS INCOME TAX (Cash1) $M

LOANS NET AND ADVANCES7 $BN

CUSTOMER DEPOSITS7 $BN

During the year we held a Regional Marketplace at our head office in Docklands, where staff and visitors had the opportunity to sample and purchase the produce of several of our Victorian and Tasmanian customers.

funded and facilitated in low carbon and sustainable solutions since 2015

5

ANZ 2017 ANNUAL REPORT

| ||||||||

| ||||||||

| In 2017 ANZ produced good results for shareholders, our customers and the communities in which we operate.

Financial Outcomes

Our statutory profit was $6.4 billion, up 12%. Cash profit (which excludesnon-core items from statutory profit) was $6.9 billion, up 18%. The final dividend of 80 cents per share brought the total dividend for the year to 160 cents per share fully franked, unchanged compared to 2016. This reflects a dividend payout ratio of 68% of Cash Profit with $4.6 billion in dividends paid to shareholders, moving ANZ closer to our target fully franked payout ratio of60-65% of cash profit.

Rapid economic, technological and social changes are a hallmark of the world we live in. As one of the region’s major banks, we have a clear strategy, which is being supported by bold action, to make sure ANZ is fit and ready for this future.

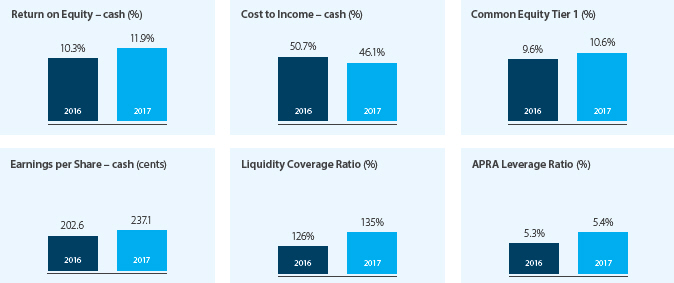

In 2017 we made good progress to becoming a better balanced, better capitalised and more efficient bank. This has seen the new shape of ANZ emerge. Our retail and commercial businesses in Australia and New Zealand now account for 53% of our capital, up from 44% at the end of 2015. Our Common Equity Tier One capital ratio reached 10.6% at the end of the year and our cost base has reduced in absolute terms with annual costs down for the first time since 1999.

| Community Engagement

Banks are facing significant challenges tore-establish the trust of the community. We need to own up to our mistakes and swiftly make things right. We have been slower than the community expects to be more transparent, to listen and to treat our customers fairly and responsibly.

What is particularly pleasing about 2017 is we have not only delivered better outcomes for shareholders, we are also making genuine progress in delivering better outcomes for customers and in rebuilding community trust.

This has been supported by the establishment of the Responsible Business Committee, led by the Chief Executive Shayne Elliott, and the revision of the charter for the Environment, Sustainability and Governance Board Committee (ESG). The aim of both Committees is to advance ANZ’s core purpose and increase focus on ESG issues.

We have committed to support the Australian Bankers’ Association Better Banking initiatives and to implementing the 21 recommendations from Stephen Sedgwick’s independent review of product sales commissions and product-based payments in Australian retail banking. The Board and the CEO are overseeing the implementation of the recommendations, with management providing regular program updates to the Board Human Resources Committee.

| ||||||

| 6 | ||||||||

CHAIRMAN’S MESSAGE

DAVID GONSKI, AC

CHAIRMAN’S MESSAGE

| ||||||||||||

| ||||||||||||

| “IN 2017 WE MADE GOOD PROGRESS TO BECOMING A BETTER BALANCED, BETTER CAPITALISED AND MORE EFFICIENT BANK. WE PAID OUT $4.6 BILLION IN DIVIDENDS.” | ||||||||||||

All recommendations are expected to be met within intended timeframes, with progress this year including; Branch and Contact Centre staff incentive plans being changed to balanced scorecard plans, creating a strong alignment between performance management and incentive rewards. All roles in the scope of the Sedgwick review are on track to have the financial objective weighting in scorecards at less than 33% for FY18 and staff recognition programs that were focused on recognising and rewarding sales outcomes have also been changed or closed. We are also working actively with the industry as part of the Combined Industry Forum in relation to responding to the Sedgwick recommendations for third parties and ASIC’s proposals for mortgage broking.

We have also delivered a range of initiatives for customers to make banking fairer and simpler. For example, in Australia we have introduced a lower interest rate credit card and removed ATM fees.

We still have much to do to rebuild community trust, however we know we need to change and we are changing.

The Board is pleased with what has been achieved in 2017 and take this opportunity of thanking all of the employees of ANZ for their hard work and dedication. | Outlook

We expect the revenue growth environment for banking will continue to be constrained as a result of intense competition and the effect of regulation, including the full impact of the major bank levy in Australia.

This environment is not new to us and our strategy is ensuring we focus only on those areas where we can deliver exceptional customer outcomes, solve real customer needs and, in doing so, make a decent return for our shareholders.

As a result, ANZ’s capital position has improved significantly and we already meet APRA’s ‘unquestionably strong’ 2020 capital target. In 2018, as we receive the proceeds from the already announced divestment ofnon-core businesses, we will have the flexibility to consider capital management initiatives.

As we continue to deliver the benefits of our strategy, we are well positioned to create value for our shareholders, customers, employees and the community in 2018 and beyond.

David Gonski, AC Chairman | |||||||||||

| 7 | ||||||||||||

ANZ 2017 ANNUAL REPORT

| ||||||||

| ||||||||

Two years ago it was clear that we needed to reshape ANZ’s future. We had a strong and successful business, however in recent times the external environment was changing faster than we were and our customers, the community and our shareholders expected much more from us.

Our strategy

To ensure ANZ adapted more quickly, we simplified our strategy to focus on being the best bank for people who want to buy and own a home, and for people who want to start, run and grow a business. In Institutional Banking, we want to be the best bank in the world for customers who move goods and money around the Asia-Pacific region.

This allowed us to focus our resources on opportunities where we have a competitive advantage and can win. However, we have also made some difficult calls. Some say the essence of strategy is choosing what not to do. We have chosen to sell businesses or investments where we were not in a winning position or developing our ANZ brand, or where they added unnecessary complexity and risk. |

This has included the divestment of our pensions and investments business in Australia, our retail and wealth businesses in six Asian countries, UDC asset finance in New Zealand, and our minority investments in China’s Shanghai Rural Commercial Bank and Metrobank Card Corporation in the Philippines.

These choices have also involved a significant reshaping of our Institutional Banking business as part of improving the capital allocation and improving returns. This year it has involved a further $18 billion reduction in Credit Risk Weighted Assets, bringing the total reduction since September 2015 to $46 billion or 27%. We are also focusing on a smaller number of customers who most value our capabilities and our network, including our presence in Asia.

Today, we are at themid-point of executing a multi-year transformation of ANZ and I am pleased to report that 2017 has seen better outcomes for shareholders and genuine progress in delivering better outcomes for customers and in rebuilding community trust.

Customers and the Community

For customers our progress includes initiatives to make banking fairer and simpler supported by an increased emphasis on innovation. For example, we extended our mobile payments leadership, established with Apple PayTM and Android PayTM, with the launch of Samsung Pay and FitBitTM Pay. Mobile payments are also important for small business and we introduced BladePayTM to support this growing opportunity.

We also believe in the value of voice-activated transactions and launched MyVoice identity and security solutions in Australia and New Zealand.

| |||||||

8

| ||||||||

CEO’S MESSAGE

SHAYNE ELLIOTT

CEO’S MESSAGE

| ||||||||||||

| ||||||||||||

We are also rebuilding trust through a focus on our core purpose: to help shape a world where people and communities thrive. We invested more than $131 million in the communities in which we operate and I am particularly proud of the impact our financial education and employment programs are having in terms of creating opportunities for more people to participate socially and economically.

We are focused on creating the right culture to support our strategy. The way in which we treat our stakeholders is reinforced by our values. Our values – the behaviours expected of our people – are not just words on a page. They are embedded in how we do things like how we manage and reward our people’s performance. They are also used as a foundation for good decision making and embedded in our operating rhythm, for example, across our Australian Branch Network.

We took a positive and proactive stance at our appearances before the Australian Parliament. We have made product, fee and rate changes to benefit customers and the community and everyone in the senior management team has spent more time in branches, call centres and regional and rural areas talking to our customers and the community. Looking ahead, we are seeking to deliver value to all our stakeholders through four factors:

• Simplicity and focus. Choosing a few things to do, doing them extremely well and stopping everything else.

• Speed to market. Listening to customers, testing, developing and launching solutions quickly and repeating at pace. | • Increase digitisation. Focusing on mobile and voice solutions for customers.

• Culture. Building a stronger sense of core purpose, ethics and fairness, and investing in people who can sense and navigate the rapidly changing world.

ANZ today is leaner, stronger and fitter; better placed to manage the changing environment while still investing in new capabilities to deliver long-term sustainable earnings growth.

We could not have achieved so much in 2017 without the sustained effort and dedication of our people, and I thank them all for their contribution.

Shayne Elliott CEO | |||||||||||

9

| ||||||||||||

“I WANT US TO BE KNOWN AS A COMPANY THAT’S RESPECTED FOR BEING FAIR AND BALANCED IN THE WAY WE THINK ABOUT ISSUES AND FOR TAKING ACTION TO MEET THE EXPECTATIONS OF OUR CUSTOMERS, EMPLOYEES AND SOCIETY.”

ANZ 2017 ANNUAL REPORT

ABOUT OUR BUSINESS |

OUR PURPOSE

Our purpose is to help shape a world in which people and communities thrive. That means striving to create a balanced, sustainable society in which everyone can take part and build a better life.

OUR CULTURE

AND VALUES

Our values are the foundation of how we work and how we bank. We recognise that we must live our values every day if we are to execute our strategy successfully and earn back the community’s trust.

To support our strategic priority to drive a purpose and values-led transformation of the bank, this year we refreshed our values with input from more than 1,000 employees. Our values, which include a strong focus on speaking up and respectfully disagreeing, are supported by our Code of Conduct and Ethics. It is a requirement that all employees comply with the Code, which contains eight guiding principles and sets the standards for the way we do business at ANZ.

OUR CORPORATE

SUSTAINABILITY FRAMEWORK

Our Corporate Sustainability Framework supports our business strategy and is aligned with the bank’s purpose. The Framework has three key areas of focus:

•Sustainable Growth

•Social and Economic Participation

•Fair and Responsible Banking

We care about:

| INTEGRITY | |||

| COLLABORATION | |||

| ACCOUNTABILITY | |||

| RESPECT | |||

| EXCELLENCE | |||

SUSTAINABLE GROWTH

FAIR AND RESPONSIBLE

BANKING

SHAPE A WORLD WHERE

PEOPLE AND COMMUNITIES

THRIVE

SOCIAL AND ECONOMIC PARTICIPATION

10

ABOUT OUR BUSINESS

Founded in 1835 and headquartered in Australia, we provide banking and financial products and services to individual and business customers, operating across 34 markets.

|

OUR DIVISIONS

Our business is structured across the following divisions:

Australia: comprises the Retail and the Corporate and Commercial Banking business units, providing a full range of banking services.

Institutional: services global institutional and business customers located in Australia, New Zealand, Asia, Europe, America, Papua New Guinea and the Middle East across three product sets: Transaction Banking, Loans & Specialised Finance and Markets.

New Zealand: comprises the Retail (including wealth management services) and Commercial business units providing a full range of banking services.

Wealth Australia: provides investment, superannuation, insurance and financial advice services.

Asia Retail & Pacific: comprises the Asia Retail and Pacific business units, connecting customers to specialists for their banking needs.

Digital banking: leads the strategic development and delivery of a superior digital experience for the bank’s customers and staff.

These divisions are supported by Group-wide functions including Technology, Services & Operations and Group Centre.

ANZ is listed on the Australian Securties Exchange (ASX) with a secondary listing on the New Zealand Exchange (NZX).

| 1. | Based on beneficial ownership. |

OUR INTERNATIONAL PRESENCE

Australia

New Zealand

International

Asia Cambodia, China, Hong Kong, India, Indonesia, Japan, Laos, Malaysia, Myanmar, the Philippines, Singapore, South Korea, Taiwan, Thailand, Vietnam

Europe France, Germany, United Kingdom |

Pacific American Samoa, Cook Islands, Fiji, Guam, Kiribati, New Caledonia, Papua New Guinea, Samoa, Solomon Islands, Timor-Leste, Tonga, Vanuatu

Middle East U.A.E. (Dubai) United States of America | EARNING COMPOSITION BY GEOGRAPHY

|

~ 8 million

Retail, commercial and instituitional customers

44,896

Full-time equivalent employees

$86.9 billion

Market capitalisation

520,000+

Shareholders. 58% 1 of ANZ’s shares are held by Institutional investors and the remaining 42%1 by Retail investors.

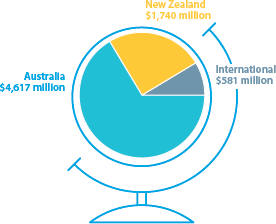

New Zealand

$1,740 million

International

$581 million

Australia

$4,617 million

11

ANZ 2017 ANNUAL REPORT

OUR STRATEGY

OUR STRATEGY IS FOCUSED ON BECOMING SIMPLER, BETTER BALANCED AND MORE SERVICE-ORIENTED TO HELP

Successful execution of our strategy will deliver consistently strong results for our shareholders, achieving a balance between growth

|

CREATE A SIMPLER, BETTER CAPITALISED, BETTER BALANCED AND MORE AGILE BANK

| FOCUS OUR EFFORTS ON AREAS WHERE WE CAN CARVE OUT A WINNING POSITION

| |||

FY17 PROGRESS

| FY17 PROGRESS

| |||

Simpler bank:

• Continued to reshape and simplify the organisation, reducing full-time equivalent staff by 4%, including 6% reduction in senior management.

• Reduced total costs in absolute terms, down year on year for the first time since 1999.

Better capitalised:

• Increased Common Equity Tier 1 capital by 96 basis points to 10.6%.

• Generated 229 basis points of organic capital, primarily driven by earnings growth and reduction in the Group’s Risk Weighted Assets (RWA).

Better balanced:

• Further rebalanced the portfolio, with capital allocated to Retail and Commercial in Australia and New Zealand increasing by 9% to 53% since 2015.

• Improved risk adjusted returns in Institutional, through a combination of $18 billion reduction in credit RWA and improvement in earnings composition of markets, transaction banking and lending.

• Progressed the sale ofnon-core businesses and minority investments, expected to deliver an estimated 80 basis points of capital once complete. |

• Established banking relationships with ~250,000 net new retail customers in Australia and New Zealand.

• In Australia, we strengthened our number 3 home loan market share position, introduced First Home Buyer coaches, and for the first time home loan accounts exceeded 1 million.

• In New Zealand, we maintained our number 1 market share position in home loans, held a leading position in overall brand consideration1 (at 51%) and increased our Retail Net Promotor Score2.

• Grew small business deposits by 9% in Australia and commercial deposits by 6% in New Zealand. | |||

FY18 PRIORITIES

|

FY18 PRIORITIES

| |||

• Complete transactions in train and further progress the sale ofnon-core businesses and minority investments.

• Continue repositioning the Institutional business, targeting further RWA reductions and improved returns.

• Deliver a step-change in our cost structure.

• Run the bank prudently, balancing growth, return and risk. | • Maintain momentum in our home loan and small business franchises to deliver consistent, above-system growth in a cautious and responsible way.

• Build Home Owner and Small Business Ecosystems to engage customers and improve the customer proposition and drive new revenue streams.

• Build our Institutional’s regional trade, cash management and markets platforms.

• Build a platform that makes payments easier, cheaper and more integrated for individuals and organisations.

|

| 1. | Source: McCulley Research Brand Tracking (online survey; first choice or seriously considered); six month rolling average. |

| 2. | Retail Market Monitor, Camorra Research, Sep’16 & Sep’17 (monthly). |

12

OUR STRATEGY

| DRIVE A PURPOSE ANDVALUES-LED TRANSFORMATION OF THE BANK |

| BUILD A SUPERIOR EVERYDAY EXPERIENCE FOR CUSTOMERS AND OUR PEOPLE TO COMPETE IN THE DIGITAL AGE | ||

FY17 PROGRESS

|

FY17 PROGRESS

| |||

• EstablishedCEO-led Responsible Business Committee and revised Charter of Environment, Sustainability and Governance Board Committee to advance ANZ’s purpose and increase focus on ESG issues.

• Contributed $131 million in community investment supported by 113,127 community volunteering hours by employees.

• Engaged our people and continued to build positive advocacy for ANZ and the industry through ‘The ANZ Way’, focusing on ANZ’s purpose, strategy, refreshed values and Code of Conduct.

• Introduced a new ‘balanced scorecard’ incentive plan in our branches and retail banking contact centres, increasing the weighting to good customer outcomes, and established a new role of Customer Fairness Advisor.

• Implemented key priorities of our revised Human Rights Standards, including strengthened customer due diligence and employee training.

|

• The only Australian major bank to offer payment options across Apple PayTM, Apple Watch Pay, Android PayTM, Samsung Pay and FitBitTM Pay — backed by the ability to make high-value transactions easier with the introduction of voice biometrics.

• Expanded accessibility features for ANZ Visa Debit cards including features to assist customers with visual impairment and reading difficulties.

• Acquired online property site RealAs to bolster our digital offering in Australia’s property market.

• Added to small business product offerings through our Employment Hero partnership while adding payments capability with BladePayTM and FastPay® Next Generation. | |||

FY18 PRIORITIES

|

FY18 PRIORITIES

| |||

• Act boldly and aligned with our purpose tore-engage with the community, regain trust and differentiate ANZ.

• Embed our values and ‘New Ways of Leading’ with all leaders across the bank.

• Continue to change the way we communicate internally to create a more transparent, open culture. |

• Simplify and standardise our technology landscape in support of our ambitions.

• Introduce ‘New Ways of Working’, to more rapidly deliver valuable new features and services to our customers, engage our people and attract new talent.

• Build the skills required to develop compelling customer propositions, unlock the value of data and optimise our core processes.

• Better utilise data to strengthen relationships, grow revenue and improve risk management.

| |||

“WITH ANZ, WE’VE FOUND A MORE PERSONALISED APPROACH. THEY’RE INTERESTED IN US BOTH AS PEOPLE, AND AS A GROWING BUSINESS.”

— Kathy Grant

Kathy Grant and Justin Davenport, Lux Design Group — clothing designers, wholesalers, importers and manufacturers.

13

ANZ 2017 ANNUAL REPORT

OUR PERFORMANCE | ||

GROUP PERFORMANCE

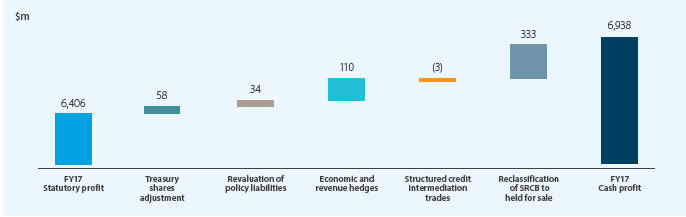

Statutory net profit after tax for the year ended 30 September 2017 increased 12% on the prior year to $6,406 million. Statutory return on equity is 11.0% and statutory earnings per share is 220.1 cents, an increase of 11% on prior year. The table below presents our performance on a statutory and cash basis.

| 2017 | 2016 | |||||||||||||||

| Statutory | Cash | Statutory | Cash | |||||||||||||

Income Statement | $m | $m | $m | $m | ||||||||||||

Net interest income | 14,872 | 14,872 | 15,095 | 15,095 | ||||||||||||

Other operating income | 5,401 | 5,617 | 5,451 | 5,499 | ||||||||||||

Operating income | 20,273 | 20,489 | 20,546 | 20,594 | ||||||||||||

Operating expenses | (9,448) | (9,448) | (10,439) | (10,439) | ||||||||||||

Profit before credit impairment and income tax | 10,825 | 11,041 | 10,107 | 10,155 | ||||||||||||

Credit impairment charge | (1,198) | (1,199) | (1,929) | (1,956) | ||||||||||||

Profit before income tax | 9,627 | 9,842 | 8,178 | 8,199 | ||||||||||||

Income tax expense andnon-controlling interests | (3,221) | (2,904) | (2,469) | (2,310) | ||||||||||||

Profit | 6,406 | 6,938 | 5,709 | 5,889 | ||||||||||||

WHY WE USE CASH PROFIT TO EXPLAIN THE GROUP’S FINANCIAL PERFORMANCE

We usenon-IFRS metrics to manage our business. In general, they capture items that can be controlled by management and reflect our business activities. We use these metrics internally to set targets and incentivise our Senior Executives and leaders through our remuneration plans. In addition, we believe focusing on underlying operations is particularly important as we continue to strategically reposition ourselves to create a simpler, better capitalised, better balanced and more agile bank.

Since 1 October 2012, the Group has used cash profit to measure performance of business activities. It is an industry wide measure which enables comparison with our peer group. We calculate cash profit by adjusting statutory profit fornon-core items. Cash profit is not subject to review or audit by the external auditor. Our external auditor has informed the Audit Committee that adjustments have been determined on a consistent basis across each of the periods presented.

14

OUR PERFORMANCE

ADJUSTMENTS BETWEEN STATUTORY PROFIT AND CASH PROFIT

Description of adjustments between statutory profit and cash profit:

| ||

| Adjustment | Reason for the adjustment | |

Treasury shares adjustment | Wealth Australia holds ANZ shares as investments backing policy liabilities which are revalued through the Income Statement. These shares are deemed to be Treasury shares and all dividends and realised and unrealised gains and losses associated with the shares are eliminated for statutory purposes. From a cash profit perspective, earnings on these shares are included to ensure there is no asymmetrical impact between policy liabilities and the assets held to support such liabilities. | |

Revaluation of policy liabilities | To calculate certain policy liabilities, projected future cash flows on insurance contracts are discounted at a market discount rate to the present value of the obligation. Any change is reflected in the Income Statement each period. The volatility from changes in market discount rates is removed from cash profit each year as the impact reverts to zero over the life of the insurance contract. | |

Economic hedges and revenue hedges | Fair value gains and losses are recognised in the Income Statement on economic and revenue hedges used to manage interest rate and foreign exchange risk. The mark to market adjustments on these derivatives, not designated in an accounting hedge, are removed from cash profit as the fair value gains or losses will reverse over time to match the profit or loss on the hedged item. Included in economic hedges are funding related swaps, select structured finance and specialised leasing transactions. | |

Structured credit intermediation trades | ANZ entered into a series of structured credit intermediation trades with US financial guarantors from 2004 to 2007. The underlying structures involve credit default swaps (CDSs) over synthetic collateralised debt obligations (CDOs), portfolios of external collateralised loan obligations (CLOs) or specific bonds/floating rate notes (FRNs). ANZ sold protection using CDSs over these structures and then to mitigate risk, purchased protection via CDSs over the same structures from eight US financial guarantors. Being derivatives, both the sold protection and the purchased protection are measured at fair value and marked to model. The gains or losses on structured intermediation trades is an adjustment to cash profit as it relates to a legacy business and, unless terminated early, fair value movements are expected to reverse to zero in future periods. | |

Reclassification of SRCB to held for sale | Represents the impact of reclassifying Shanghai Rural Commercial Bank (SRCB) to an asset held for sale in 2017. This will be materially offset by a release of the foreign currency translation andavailable-for-sale reserves upon transaction completion in late 2017. | |

Credit risk on impaired derivatives | Nil profit after tax impact. The charge to income for derivative credit valuation adjustments on defaulted and impaired derivative exposures has been reclassified to cash credit impairment charges to reflect the manner in which the defaulted and impaired derivatives are managed. | |

Policyholders tax gross up | Nil profit after tax impact. For statutory reporting purposes, policyholder income tax and other related taxes paid on behalf of policyholders are included in net funds management and insurance income and income tax expense. The gross up has been excluded from cash profit as it does not reflect the underlying performance of the business which is assessed net of policyholder tax. | |

| ||

15

ANZ 2017 ANNUAL REPORT

OUR PERFORMANCE (continued)

CASH PROFIT PERFORMANCE

| 2017 | 2016 | |||||||||||

Income Statement | $m | $m | Movt | |||||||||

Net interest income | 14,872 | 15,095 | -1% | |||||||||

Other operating income | 5,617 | 5,499 | 2% | |||||||||

Operating income | 20,489 | 20,594 | -1% | |||||||||

Operating expenses | (9,448 | ) | (10,439 | ) | -9% | |||||||

Profit before credit impairment and income tax | 11,041 | 10,155 | 9% | |||||||||

Credit impairment charge | (1,199 | ) | (1,956 | ) | �� | -39% | ||||||

Profit before income tax | 9,842 | 8,199 | 20% | |||||||||

Income tax expense andnon-controlling interests | (2,904 | ) | (2,310 | ) | 26% | |||||||

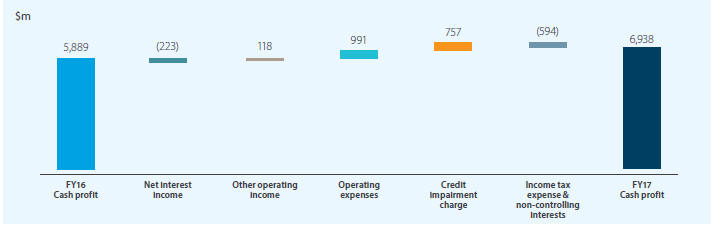

Cash profit | 6,938 | 5,889 | 18% | |||||||||

Cash profit increased 18% partly reflecting the impact of a number of large/notable items taken in 2016 and rigorous cost management in 2017.

Net interest income decreased $223 million(-1%) largely due to a 8 basis point decrease in the net interest margin, partially offset by 2% growth in average interest earning assets. The growth in average interest earning assets reflects ANZ’s strategic focus on home loans, in particular owner occupier, partially offset by reductions from Institutional portfolio rebalancing and the partial completion of the Asia Retail and Wealth sale. The lower net interest margin reflects the combined impact of deposit competition, growth in the liquidity portfolio and lower earnings on capital. This was partially offset by differentiated repricing in home loans across investor and owner occupier, principal and interest and interest only loans which on a net basis benefited margins. The major bank levy was introduced on 1 July 2017 which also reduced net interest income by $86 million.

Other operating income increased $118 million (+2%) benefiting from a net year on year change in derivative valuation adjustments of $331 million (2017: $229 million gain; 2016: $102 million loss), an improvement in Markets income of $102 million, and the $114 million gain on sale of 100 Queen Street, Melbourne. Prior year comparatives include the adverse impact of Asian minority valuation adjustments of $231 million and the $237 million derivative CVA methodology change. Partly offsetting this, a number of sales related transactions had unfavourable impacts including a $310 million net charge related to the Asia Retail and Wealth sale, and $365 million loss of income from SRCB, Bank of Tianjin (BoT) and Esanda Dealer Finance. There was a $186 million reduction in funds management and insurance income, and a $75 million decrease in net fee and commission income.

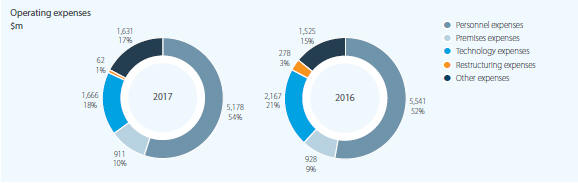

Operating expenses decreased $991 million(-9%) primarily due to the $556 million charge for software capitalisation policy changes and the $278 million charge for restructuring taken in 2016. Personnel expenses reduced by $363 million reflecting a 5% reduction in average Full Time Equivalent Staff (FTE). Partly offsetting this are increases in underlying technology expenses of $55 million and increases in other expenses of $106 million as the result ofnon-lending losses and higher technology related consulting expenses.

Credit impairment charges decreased $757 million(-39%). Individual credit impairment charges decreased by $598 million(-31%) primarily the result of a benign credit environment. Collective impairment charges decreased by $159 million due to an improvement in the Group’s overall risk profile and portfolio rebalancing in Institutional, partially offset by economic overlay adjustments.

16

OUR PERFORMANCE

DIVIDENDS

This performance allowed us to propose that a final dividend of 80 cents be paid on each eligible fully paid ANZ ordinary share, bringing the total dividend for the year ended 30 September 2017 to $1.60 per share. This represents a dividend payout ratio (cash basis) of 67.7%.

The proposed 2017 final dividend will be fully franked for Australian taxation purposes, and New Zealand (NZ) imputation credits of NZ 10 cents per ordinary share will also be attached. It will be paid on 18 December 2017 to owners of ordinary shares at close of business on 14 November 2017 (record date).

ANZ has a Dividend Reinvestment Plan (DRP) and a Bonus Option Plan (BOP) that will operate in respect of the proposed 2017 final dividend. For the 2017 final dividend, ANZ intends to provide shares under the DRP through anon-market purchase (as approved by APRA) and BOP through the issue of new shares.

Further details on dividends provided for or paid during the year ended 30 September 2017 are set out in Note 5 in the Financial Report.

ANALYSIS OF CASH PROFIT PERFORMANCE

NET INTEREST INCOME

2017

| 2016

| Movt

| ||||||||||

Net interest income ($m) | 14,872 | 15,095 | -1% | |||||||||

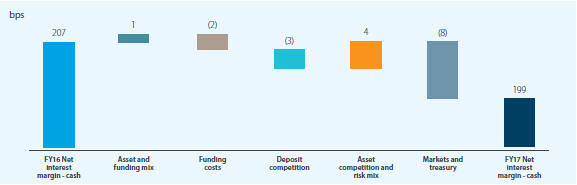

Net interest margin (%) | 1.99% | 2.07% | -8 bps | |||||||||

Average interest earnings assets ($m) | 748,000 | 730,835 | 2% | |||||||||

Average deposits and other borrowings ($m) | 600,186 | 586,453 | 2% | |||||||||

Net interest income decreased $223 million(-1%) largely due to a 8 basis point decrease in the net interest margin, partially offset by 2% growth in average interest earning assets.

Net interest margin decreased reflecting the combined impact of deposit competition, growth in the liquidity portfolio and lower earnings on capital. This was partially offset by differentiated repricing in home loans across investor and owner occupier, principal and interest and interest only loans which on a net basis benefited margins. The major bank levy was introduced on 1 July 2017 which also reduced net interest margin.

Average interest earning assets increased $17.2 billion (+2%) reflecting ANZ’s strategic focus on home loans, in particular owner occupier, partially offset by reductions from Institutional portfolio rebalancing, and the partial completion of the Asia Retail and Wealth sale.

Average deposits and other borrowings increased $13.7 billion (+2%) from growth in customer deposits across Australia, New Zealand and Institutional divisions, partially offset by a decline in deposits and other borrowings, as well as the partial completion of the Asia Retail and Wealth sale.

17

ANZ 2017 ANNUAL REPORT

OUR PERFORMANCE (continued)

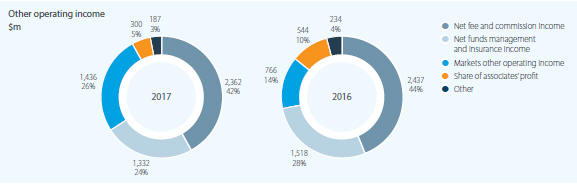

OTHER OPERATING INCOME

2017 $m

| 2016 $m

| Movt

| ||||||||||

Other operating income |

|

5,617

|

|

|

5,499

|

|

|

2%

|

| |||

Total increase/ (decrease) $m

| Movt

| Explanation

| ||||

| Net fee and commission income1 | (75) | -3% | Decrease of $70 million in Asia Retail and Pacific from lower performance and the transition of China, Singapore and Hong Kong businesses to DBS Bank. In addition, lower performance in Institutional of $56 million primarily driven by portfolio rebalancing. This is partially offset by an increase in the Australia division of $40 million driven by growth in Small Business and Deposits.

| |||

| Net funds management and insurance income1 | (186) | -12% | Decrease in Wealth Australia of $163 million due to adverse retail life claims, reduced fee income as expected from ongoing rationalisation of legacy investment platforms to SmartChoice, lower income on invested capital, partially offset by favourable Lenders Mortgage Insurance experience. The remaining decrease relates to the Asia Retail and Pacific division.

| |||

| Markets other operating income | 670 | 87% | Excluding the impact of the $237 million charge from the derivative credit valuation adjustment (CVA) methodology change recognised in 2016, Markets other operating income increased $433 million. This was driven by an increase Balance Sheet Trading due to tighter credit spreads which generated mark to market gains and increased income from higher average liquidity portfolio holdings. Franchise Trading increased as the result of derivative credit and funding valuation adjustments, net of associated hedges which benefited from decreasing credit spreads and increasing yield curves. This was offset by a decrease in Franchise Sales as the result of business transformational initiatives and market conditions limiting client activity particularly for longer tenor hedging as a result of low foreign exchange volatility and the low interest rate environment.

| |||

| Share of associates’ profit1 | (244) | -45% | Decrease primarily as the result of ceasing equity accounting for BoT from March 2016 of $86 million and SRCB from January 2017 of $201 million. This was partially offset by a net increase of $44 million in profits from other associates.

| |||

| Other1 | (47) | -20% | Driven by a $310 million net charge as a result of reclassifying Asia Retail and Wealth to held for sale and partial sale completion. A net $165 million increase due to the year on year impact of the Asian minority valuations adjustments and the Esanda Dealer finance gain recognised in 2016. In addition, the current year includes a $114 million gain on sale of 100 Queen Street, Melbourne.

| |||

| Total

| 118

| 2%

|

| 1. | Excluding Markets. |

18

OUR PERFORMANCE

OPERATING EXPENSES

| 2017 | 2016 | |||||||||||

| Movt | ||||||||||||

Operating expenses ($m)

|

| 9,448

|

|

| 10,439

|

|

| -9%

|

| |||

Expensed investment spend ($m) | 548 | 526 | 4% | |||||||||

Capitalised investment spend ($m) | 387 | 400 | -3% | |||||||||

Total technology infrastructure spend ($m) | 935 | 926 | 1% | |||||||||

Operating expenses to operating income % | 46.1% | 50.7% | -4.6% | |||||||||

Full time equivalent staff (FTE) | 44,896 | 46,554 | -4% | |||||||||

Average full time equivalent staff (FTE) | 46,068 | 48,633 | -5% | |||||||||

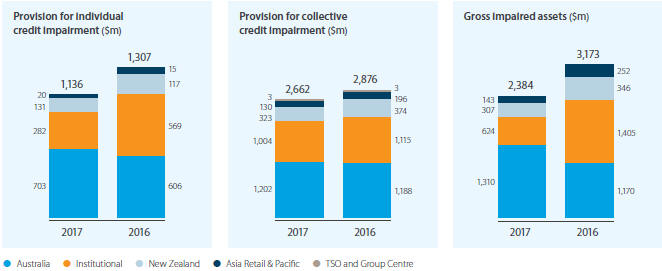

CREDIT IMPAIRMENT CHARGE

| 2017 | 2016 | |||||||||||

Individual credit impairment charge ($m) | 1,341 | 1,939 | -31% | |||||||||

Collective credit impairment charge/(release) ($m) | (142 | ) | 17 | large | ||||||||

Credit impairment charge ($m) | 1,199 | 1,956 | -39% | |||||||||

Gross impaired assets ($m) | 2,384 | 3,173 | -25% | |||||||||

Credit risk weighted assets ($b) | 336.8 | 352.0 | -4% | |||||||||

Total provision for credit impairment ($m) | 3,798 | 4,183 | -9% | |||||||||

Individual provision as % of gross impaired assets | 47.7% | 41.2% | 6.5% | |||||||||

Collective provision as % of credit risk weighted assets | 0.79% | 0.82% | -0.3% | |||||||||

Credit impairment charges decreased $757 million(-39%).

Individual credit impairment charge decreased $598 million(-31%) driven by a $402 million(-16%) decrease in new and existing provisions predominantly in Institutional largely arising from portfolio rebalancing, combined with a $196 million (+37%) increase in recoveries and write-backs in Australia and Institutional divisions from better than expected outcomes in impaired asset workouts.

Collective credit impairment charge decreased $159 million driven by a reduction in Institutional due to portfolio rebalancing, and further improvement in the Institutional and New Zealand divisional risk profile. This was partially offset by an economic overlay adjustment of $75 million.

Gross impaired assets decreased $789 million(-25%) driven by Institutional (-$781 million) and New Zealand (-$39 million) divisions due to higher repayments and upgrades on a small number of large exposures, and Asia Retail and Pacific division (-$109 million) due to the partial completion of the Asia Retail and Wealth sale. This was partially offset by an increase in the Australia division (+$140 million) driven by Corporate Banking, Small Business Banking and home loan portfolios. The Group’s individual provision coverage ratio on impaired assets was 47.7% at 30 September 2017 (2016: 41.2%).

19

ANZ 2017 ANNUAL REPORT

OUR PERFORMANCE (continued)

CREDIT IMPAIRMENT CHARGE

DIVISIONAL PERFORMANCE

| 2017 | Australia | Institutional | New Zealand | Wealth Australia | Asia Retail & Pacific | TSO and Group Centre | Group | |||||||||||||||||||||

Net interest margin | 2.68% | 1.01% | 2.31% | n/a | 3.03% | n/a | 1.99% | |||||||||||||||||||||

Operating expenses to operating income | 35.6% | 50.5% | 37.6% | 68.4% | 101.2% | n/a | 46.1% | |||||||||||||||||||||

Cash profit ($m) | 3,695 | 1,836 | 1,369 | 238 | (148 | ) | (52 | ) | 6,938 | |||||||||||||||||||

Net loans and advances ($b) | 345.4 | 119.6 | 107.9 | 1.7 | 5.7 | - | 580.3 | |||||||||||||||||||||

Customer deposits ($b) | 201.4 | 186.8 | 75.3 | - | 9.1 | (5.0 | ) | 467.6 | ||||||||||||||||||||

Number of employees | 11,387 | 4,754 | 6,207 | 2,110 | 3,981 | 16,457 | 44,896 | |||||||||||||||||||||

| 2016 | Australia | Institutional | New Zealand | Wealth Australia | Asia Retail & Pacific | TSO and Group Centre | Group | |||||||||||||||||||||

Net interest margin | 2.75% | 1.13% | 2.37% | n/a | 2.96% | n/a | 2.07% | |||||||||||||||||||||

Operating expenses to operating income | 36.4% | 57.1% | 39.6% | 63.8% | 68.7% | n/a | 50.7% | |||||||||||||||||||||

Cash profit ($m) | 3,547 | 1,041 | 1,268 | 324 | 159 | (450 | ) | 5,889 | ||||||||||||||||||||

Net loans and advances ($b) | 327.1 | 125.9 | 107.9 | 2.0 | 13.4 | (0.4 | ) | 575.9 | ||||||||||||||||||||

Customer deposits ($b) | 187.7 | 171.1 | 72.8 | 0.3 | 22.8 | (5.1 | ) | 449.6 | ||||||||||||||||||||

Number of employees | 11,563 | 5,112 | 6,317 | 2,174 | 4,894 | 16,494 | 46,554 | |||||||||||||||||||||

20

OUR PERFORMANCE

DIVISIONAL PERFORMANCE

Australia

Net interest margin declined as the result of higher average funding costs, lower earnings on deposits due to the lower interest rate environment and the introduction of the major bank levy. Net loans and advances grew in home loans particularly in New South Wales, and Corporate Banking. Customer deposits grew across all portfolios. Operating expenses were broadly flat due to a reduction in FTE driven by productivity efforts focused on simplifying the business, partially offset by inflation and increased investment in the business. Credit impairment charges decreased primarily due to lower single name charges in Corporate and Commercial Banking, partially offset by volume growth and higher delinquency rates for home loans in Western Australia. This led to a $148 million (+4%) increase in cash profit from prior year.

Institutional

Net interest marginex-Markets decreased due to asset pricing competition, the introduction of the major bank levy and the mix impact of lower lending volumes and higher deposit volumes, partially offset by margin improvements in Payments and Cash Management. Net loans and advances were down due to portfolio rebalancing mainly in Loans & Specialised Finance and Transaction Banking. Customer deposits grew in Markets and Transaction Banking. Other operating income increased significantly due to positive derivative valuation adjustments and higher Markets Balance Sheet income as a result of tightening credit spreads. Operating expenses decreased due to a reduction in FTE as a result of ongoing simplification of the business, partially offset by highernon-lending losses, regulatory and compliance spend. Credit impairment charges decreased significantly due to a benign credit environment, higher write-backs and an overall reduction in lending assets driven by portfolio rebalancing. This led to a $795 million (+76%) increase in cash profit from prior year.

New Zealand

Net interest margin declined as the result of a higher proportion of lower margin fixed rate lending and term deposits, pricing competition and higher average funding costs. Net loans and advances grew in home loans (excluding foreign currency impacts) in addition to higher balances in funds under management. Customer deposits grew across all portfolios. Other operating income decreased, more than offset by an increase in net funds management and insurance income as the result of higher funds under management balances. Operating expenses decreased from a reduction in FTE driven by automation and transaction migration to lower cost channels, partially offset by inflation. Credit impairment charges decreased due to an increase in write-backs and credit quality improvements across the Retail and Commercial and Agri portfolios, partially offset by increases in new and existing provisions. This led to a $101 million (+8%) increase in cash profit from prior year.

Wealth Australia

Insurance income decreased as the result of adverse retail life claims experience, aone-off experience loss due to the exit of a Group Life insurance plan, partially offset by reinsurance profit share and favourable claims experience in Lenders Mortgage Insurance. Funds Management income decreased in line with the planned strategy to rationalise the legacy portfolio to SmartChoice, a simpler and lower risk model, which is now complete. Corporate and Other income decreased due to realised gains in 2016 which was not repeated and investment market volatility on the guaranteed business. Operating expenses decreased due to productivity initiatives that resulted in a reduction in FTE, partially offset by inflation and higher regulatory compliance and remediation spend. This led to an $86 million(-27%) decrease in cash profit from prior year.

Asia Retail & Pacific

Asia Retail and Pacific results for 2017 were impacted by the reclassification of Asia Retail and Wealth business to held for sale and the transition of China, Singapore and Hong Kong businesses to DBS Bank, which resulted in a $310 million net charge(pre-tax). This led to a $307 million decrease in cash profit from prior year.

TSO and Group Centre

TSO and Group Centre divisional results for 2016 and 2017 were impacted by a number of large/notable items outlined on page 22. This includes Asian minority valuation adjustments in 2016, loss of equity accounted earnings in 2016 and 2017, Esanda Dealer Finance divestment gain on sale in 2016, software capitalisation changes in 2016, and the gain on sale of 100 Queen Street, Melbourne in 2017. This led to a $398 million (+88%) increase in cash profit from prior year.

21

ANZ 2017 ANNUAL REPORT

OUR PERFORMANCE (continued)

LARGE/NOTABLE ITEMS INCLUDED IN CASH PROFIT

Within cash profit, the Group has recognised some large and/or notable items. The impact of these items to cash profit on apre-tax basis is as follows:

Sale and investment related adjustments

| 2017

| 2016

| ||||||

Asian minority valuation adjustments | - | (231 | ) | |||||

Equity accounted earnings | 58 | 345 | ||||||

Sale of Asia Retail and Wealth businesses | (310 | ) | - | |||||

Esanda Dealer Finance divestment | - | 69 | ||||||

Derivative valuation adjustments | ||||||||

Market valuation adjustments | 229 | (102 | ) | |||||

Derivative CVA methodology change | - | (237 | ) | |||||

Other large/notable items | ||||||||

Gain on sale of 100 Queen Street, Melbourne | 114 | - | ||||||

Software capitalisation changes | - | (556 | ) | |||||

Restructuring | - | (278 | ) | |||||

Description of large/notable items:

| Item | Description | |

Asian minority valuation adjustments | Impairment of our investment in AMMB Holdings Berhad (Ambank) partially offset by a gain recognised on our investment in BoT upon cessation of equity accounting. | |

Equity accounted earnings | Earnings from BoT and SRCB prior to ceasing equity accounting on 30 March 2016 and 3 January 2017 respectively, that will no longer form part of future cash profit results. | |

Sale of Asia Retail and Wealth businesses | A charge to impair software, goodwill and fixed assets as well as providing for costs associated with the sale, partially offset by a gain relating to the transition of completed businesses to DBS Bank. | |

Esanda Dealer Finance divestment | Earnings from the Esanda Dealer Finance portfolio prior to divestment that will no longer form part of future cash profit results, and the gain on sale recognised on transaction completion. | |

Markets valuation adjustments | Gains or losses associated with the fair value of derivative positions, arising from adjustments to include factors such as the impact of credit and funding. | |

Derivative CVA methodology change | A charge associated with the fair value of derivative positions, arising from a revision to our methodology for determining derivative credit valuation adjustments to make greater use of market information and enhanced modelling, and to align with market leading practice. | |

Gain on sale of 100 Queen Street, Melbourne | Gain on sale of our premises at 100 Queen Street, Melbourne. | |

Software capitalisation changes | Aone-off charge as the result of the Group amending the application of its software capitalisation policy, reflecting the shorter useful life of smaller items of software. This resulted in an accelerated amortisation charge for software assets below the revised threshold. | |

Restructuring | Charges tore-shape our workforce and simplify our business at the reset of the Group’s strategy in 2016. | |

22

OUR PERFORMANCE

FIVE YEAR SUMMARY

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

$m

| $m

| $m

| $m

| $m

| ||||||||||||||||

Financial performance1 | ||||||||||||||||||||

Net interest income | 14,872 | 15,095 | 14,616 | 13,797 | 12,772 | |||||||||||||||

Other operating income | 5,617 | 5,499 | 5,921 | 5,781 | 5,619 | |||||||||||||||

Operating expenses

|

| (9,448)

|

|

| (10,439

| )

|

| (9,378

| )

|

| (8,760

| )

|

| (8,257

| )

| |||||

Profit before credit impairment and income tax | 11,041 | 10,155 | 11,159 | 10,818 | 10,134 | |||||||||||||||

Credit impairment charge | (1,199) | (1,956 | ) | (1,205 | ) | (989 | ) | (1,197 | ) | |||||||||||

Income tax expense | (2,889) | (2,299 | ) | (2,724 | ) | (2,700 | ) | (2,435 | ) | |||||||||||

Non-controlling interests

|

| (15)

|

|

| (11

| )

|

| (14

| )

|

| (12

| )

|

| (10

| )

| |||||

Cash profit1

|

| 6,938

|

|

| 5,889

|

|

| 7,216

|

|

| 7,117

|

|

| 6,492

|

| |||||

Adjustments to arrive at statutory profit1 | (532) | (180 | ) | 277 | 154 | (182 | ) | |||||||||||||

Profit attributable to shareholders of the Company

|

| 6,406

|

|

| 5,709

|

|

| 7,493

|

|

| 7,271

|

|

| 6,310

|

| |||||

Financial position | ||||||||||||||||||||

Assets | 897,326 | 914,869 | 889,900 | 772,092 | 702,995 | |||||||||||||||

Net assets | 59,075 | 57,927 | 57,353 | 49,284 | 45,603 | |||||||||||||||

Common Equity Tier 1 | 10.6% | 9.6% | 9.6% | 8.8% | 8.5% | |||||||||||||||

Common Equity Tier 1 – Internationally | 15.8% | 14.5% | 13.2% | 12.5% | 12.7% | |||||||||||||||

Comparable Basel lll2 | ||||||||||||||||||||

Return on average ordinary equity3 | 11.0% | 10.0% | 14.5% | 15.8% | 15.0% | |||||||||||||||

Return on average assets | 0.7% | 0.6% | 0.9% | 1.0% | 0.9% | |||||||||||||||

Cost to income ratio (cash)1

|

| 46.1%

|

|

| 50.7%

|

|

| 45.7%

|

|

| 44.7%

|

|

| 44.9%

|

| |||||

Shareholder value – ordinary shares | ||||||||||||||||||||

Total return to shareholders (share price movement plus dividends) | 13.1% | 9.2% | (7.5% | ) | 5.9% | 31.5% | ||||||||||||||

Market capitalisation | 86,948 | 80,886 | 78,606 | 85,235 | 84,450 | |||||||||||||||

Dividend | 160c | 160c | 181c | 178c | 164c | |||||||||||||||

Franked portion – interim | 100% | 100% | 100% | 100% | 100% | |||||||||||||||

| – final | 100% | 100% | 100% | 100% | 100% | |||||||||||||||

Share price – high | $32.95 | $29.17 | $37.25 | $35.07 | $32.09 | |||||||||||||||

| – low | $25.78 | $21.86 | $26.38 | $28.84 | $23.42 | |||||||||||||||

– closing

|

| $29.60

|

|

| $27.63

|

|

| $27.08

|

|

| $30.92

|

|

| $30.78

|

| |||||

Share information | ||||||||||||||||||||

(per fully paid ordinary share) | ||||||||||||||||||||

Earnings per share (cents) | 220.1 | 197.4 | 271.5 | 267.1 | 232.7 | |||||||||||||||

Dividend payout ratio | 73.4% | 81.9% | 68.6% | 67.4% | 71.4% | �� | ||||||||||||||

Net tangible assets per ordinary share4 | $17.66 | $17.13 | $16.86 | $14.65 | $13.48 | |||||||||||||||

No. of fully paid ordinary shares issued (millions) | 2,937 | 2,927 | 2,903 | 2,757 | 2,744 | |||||||||||||||

Dividend reinvestment plan (DRP) issue price | ||||||||||||||||||||

| – interim | $28.80 | $24.82 | $31.93 | $33.30 | $28.96 | |||||||||||||||

– final

|

| -

|

|

| $28.16

|

|

| $27.08

|

|

| $32.02

|

|

| $31.83

|

| |||||

Other information | ||||||||||||||||||||

No. of employees (full time equivalents) | 44,896 | 46,554 | 50,152 | 50,328 | 49,866 | |||||||||||||||

No. of shareholders5

|

| 522,425

|

|

| 545,256

|

|

| 546,558

|

|

| 498,309

|

|

| 468,343

|

| |||||

| 1. | Cash profit excludesnon-core items included in statutory profit and is provided to assist readers in understanding the result of the ongoing business activities of the Group. Cash profit is not audited; however, the external auditor has informed the Audit Committee that the adjustments have been determined on a consistent basis across each period presented. |

| 2. | Internationally Comparable Methodology applied for 2015–2017 aligns with APRA’s information paper entitled ‘International Capital Comparison Study’ (13 July 2015). Basel Internationally Comparable ratios do not include an estimate of the Basel l capital floor requirement. |

| 3. | Average ordinary equity excludesnon-controlling interests and preference shares. |

| 4. | Equals shareholders’ equity less preference share capital, goodwill, software and other intangible assets divided by the number of ordinary shares. |

| 5. | Excludes employees whose only ANZ shares are held in trust under ANZ employee share schemes. |

23

ANZ 2017 ANNUAL REPORT GOVERNANCE BOARD OF DIRECTORS B A D C A David Gonski, AC C John Macfarlane E Ilana Atlas G Jane Halton, AO, PSM Chairman, Independent Independent Independent Independent Non-Executive Director Non-Executive Director Non-Executive Director Non-Executive Director B Graeme Liebelt D Paula Dwyer F Shayne Elliott H Lee Hsien Yang Independent Independent Chief Executive Officer, Independent Non-Executive Director Non-Executive Director Executive Director Non-Executive Director24

The Board comprises seven Non-Executive, Independent Directors and one Executive Director — the Chief Executive Officer. Details of each Director’s qualifications, experience and special responsibilities are set out on the following pages. In addition, ANZ’s Board skills matrix (available on anz.com/corporategovernance) sets out the skills that ANZ considers each Director brings to the Board. 25

ANZ 2017 ANNUAL REPORT

GOVERNANCE (continued)

CORPORATE GOVERNANCE FRAMEWORK

26

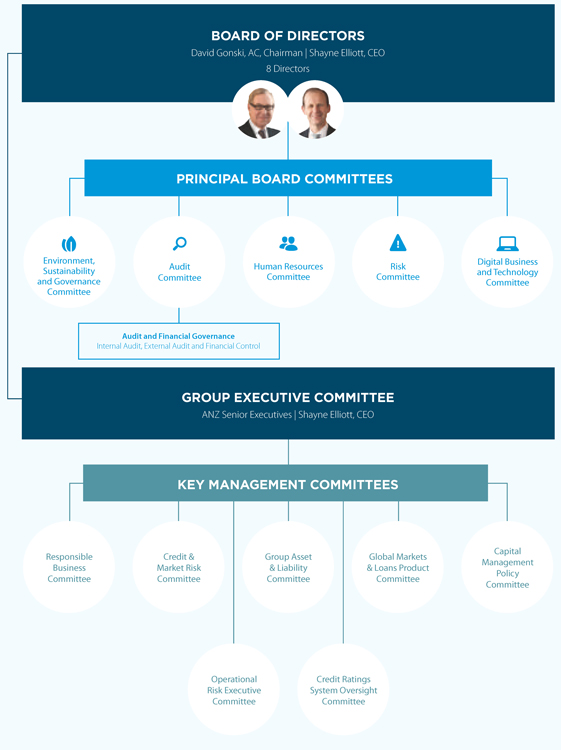

ANZ 2017 ANNUAL REPORT GOVERNANCE (continued) CORPORATE GOVERNANCE FRAMEWORK BOARD OF DIRECTORS David Gonski, AC, Chairman | Shayne Elliott, CEO 8 Directors PRINCIPAL BOARD COMMITTEES Environment, Digital Business Audit Human Resources Risk Sustainability and Technology Committee Committee Committee and Governance Committee Committee Audit and Financial Governance Internal Audit, External Audit and Financial Control GROUP EXECUTIVE COMMITTEE ANZ Senior Executives | Shayne Elliott, CEO KEY MANAGEMENT COMMITTEES Capital Responsible Credit & Group Asset Global Markets Management Business Market Risk & Liability & Loans Product Policy Committee Committee Committee Committee Committee Operational Credit Ratings Risk Executive System Oversight Committee Committee 26 26

GOVERNANCE

BOARD FOCUS AREAS

The work of the Board and its Committees during the year has been focused on providing oversight of the delivery of the Group’s strategy and ensuring that ANZ’s culture is aligned to ANZ’s purpose to shape a world where people and communities thrive.

|

During the year, the Board and its Committees undertook key governance activities supporting ANZ’s purpose. These included:

• Developing and implementing the charter of the ESG Committee.

• Embarking on a program to provide management with Board level advice on ANZ’s core sustainability issues.

• Adding a standing item to Board meeting agendas to provide insight into, and to review, ANZ’s culture.

• Endorsing and promoting a program to streamline ANZ’s annual reporting suite, with a focus on simplifying and improving the utility of the 2017 Annual Report.

• Overseeing the creation of a new Annual Review, which integrates the former Shareholder Review with strategic elements of the 2017 ANZ Corporate Sustainability Review to provide more comprehensive reporting to shareholders.

• Endorsing ANZ’s revised Code of Conduct, with a focus on clarity, simplicity, being action oriented, and being more aligned with ANZ’s values and purpose.

• Recognising the contribution of directors of ANZ’s subsidiary boards by increasing engagement between the ANZ Board and the Directors serving on ANZ subsidiary boards. Promoting and encouraging a focus on subsidiary board composition, renewal and diversity. As at 30 September 2017, females were appointed to 48.5% of all employee directorships on subsidiary boards.

|

DIRECTORS’ MEETINGS

The number of Board meetings and meetings of Committees during the year the Director was eligible to attend, and the number of meetings attended by each Director were:

| Board | Risk Committee | Audit Committee | Human Resources Committee | Environment, Sustainability and Governance Committee | Digital Business and Technology Committee | Special Committee | Committee of the Board1 | Shares Committee1 | ||||||||||||||||||||||||||||

A

| B

| A

| B

| A

| B

| A

| B

| A

| B

| A

| B

| A

| B

| A

| B

| A

| B

| |||||||||||||||||||

| Ilana Atlas | 12 | 11 | 5 | 5 | 4 | 4 | 4 | 4 | ||||||||||||||||||||||||||||

| Paula Dwyer | 12 | 12 | 6 | 6 | 5 | 5 | 4 | 4 | 2 | 2 | ||||||||||||||||||||||||||

| Shayne Elliott | 12 | 12 | 3 | 3 | 1 | 1 | ||||||||||||||||||||||||||||||

| David Gonski, AC | 12 | 12 | 6 | 6 | 5 | 5 | 4 | 4 | 4 | 4 | 3 | 3 | 5 | 5 | 1 | 1 | ||||||||||||||||||||

| Jane Halton, AO, PSM | 11 | 11 | 3 | 3 | 3 | 3 | ||||||||||||||||||||||||||||||

| Lee Hsien Yang | 12 | 12 | 6 | 6 | 4 | 4 | 3 | 3 | 1 | 1 | ||||||||||||||||||||||||||

| Graeme Liebelt | 12 | 12 | 6 | 6 | 4 | 4 | 1 | 1 | 4 | 4 | 3 | 3 | 2 | 2 | ||||||||||||||||||||||

| Ian Macfarlane2 | 4 | 4 | 2 | 2 | 1 | 1 | 1 | 1 | ||||||||||||||||||||||||||||

John Macfarlane

| 12

| 12

| 6

| 6

| 5

| 5

| 3

| 3

| ||||||||||||||||||||||||||||

Columns marked A indicate the number of meetings the Director was eligible to attend.

Columns marked B indicate the number of meetings attended. The Chairman is anex-officio member of the Audit, Environment, Sustainability and Governance, Human Resources, Risk and Digital Business and Technology Committees.

Any Director is entitled to attend any Committee meetings. Directors sometimes attend meetings of Committees of which they are not a member.

| 1. | The meetings of the Committee of the Board and Shares Committee referred to in the table include those conducted by written resolution. |

| 2. | Ian Macfarlane retired as a Director on 16 December 2016. |

27

ANZ 2017 ANNUAL REPORT

GOVERNANCE (continued)

DIRECTORS’ QUALIFICATIONS, EXPERIENCE AND SPECIAL RESPONSIBILITIES

DAVID GONSKI, AC

Chairman, IndependentNon-Executive Director and Chair

of the Environment, Sustainability and Governance Committee

BCom, LLB, FAICD(Life), FCPA

Chairman since 1 May 2014 and aNon-Executive Director since February 2014. David is anex-officio member of all Board Committees including Chair of the Environment, Sustainability and Governance Committee.

SHAYNE ELLIOTT

Chief Executive Officer and Executive Director

BCom

Chief Executive Officer and Executive Director since 1 January 2016.

Chair: Member:

Member:

Career

David started his career as a lawyer at Herbert Smith Freehills, and is now one of Australia’s most respected business leaders and company directors. He has business experience in Australia and internationally, and is involved in a broad range of organisations in the government and education sectors. He is a leading philanthropist and provides strong community leadership, particularly in relation to education in Australia.

Relevant Other Directorships

| • | Chairman: The University of New South Wales Foundation Limited (from 2005, Director from 1999). |

| • | Director/Member: Lowy Institute for International Policy (from 2012), Australian Philanthropic Services Limited (from 2012), ASIC External Advisory Panel (from 2013) and Advisory Committee for Optus Limited (from 2013). |

| • | Chancellor: University of New South Wales Council (from 2005). |

| • | President: Art Gallery of NSW Trust (from 2016). |

| • | Chair: Review to Achieve Education Excellence in Australian Schools for the Commonwealth of Australia. |

Relevant Former Directorships held

in last three years, include

| • | Former Chairman: Coca-Cola Amatil Limited (2001-2017, Director from 1997), Sydney Theatre Company Ltd (2010-2016), Guardians of the Future Fund of Australia (2012-2014), Swiss Re Life & Health Australia Limited (2011-2014), Investec Bank (Australia) Limited (2002-2014), Investec Holdings Australia Limited (2002-2014), Ingeus Limited (2009-2014) and NationalE-Health Transition Authority Ltd (2008-2014). |

| • | Former Director: Singapore Telecommunications Limited (2013-2015), Investec Property Limited (2005-2014) and Infrastructure NSW (2011-2014). |

Age64 years | ResidenceSydney, Australia

Career

Shayne has over 30 years’ experience in banking in Australia and overseas, in all aspects of the industry. Shayne joined ANZ as CEO Institutional in June 2009, and was appointed Chief Financial Officer in 2012.

Prior to joining ANZ, Shayne held senior executive roles at EFG Hermes, the largest investment bank in the Middle East, which included Chief Operating Officer. He started his career with Citibank New Zealand and worked with Citibank/Citigroup for 20 years, holding various senior positions across the UK, USA, Egypt, Australia and Hong Kong.

As a Director of the Financial Markets Foundation for Children, Shayne contributes to the promotion of health and welfare of Australian children. He actively engages in the promotion of Australian economic growth, social progress and public policy development through membership of the Australian Bankers’ Association and Business Council of Australia. Shayne will chair the Australian Bankers’ Association from December 2017.

Relevant Other Directorships

| • | Director: ANZ Bank New Zealand Limited (from 2009), ANZ Holdings (New Zealand) Limited (from 2012) and the Financial Markets Foundation for Children (from 2016). |

| • | Member: Australian Bankers’ Association (from 2016) and Business Council of Australia (from 2016). |

Age53 years | ResidenceMelbourne, Australia

28

GOVERNANCE

ILANA ATLAS

IndependentNon-Executive Director

and Chair of the Human Resources Committee

BJuris (Hons), LLB (Hons), LLM

Non-Executive Director since September 2014. Ilana is a member of the Audit Committee and Environment, Sustainability and Governance Committee.

Chair: Member:

PAULA DWYER

IndependentNon-Executive Director

and Chair of the Audit Committee

BCom, FCA, SF Fin, FAICD

Non-Executive Director since April 2012. Paula is a member of the Risk Committee and Human Resources Committee.

Chair: Member:

Career

Ilana brings a strong financial services background and legal experience to the Board. Ilana was a partner at law firm Mallesons Stephen Jaques (now King & Wood Mallesons), where in addition to her practice in corporate law, she held a number of management roles in the firm including Executive Partner, People and Information, and Managing Partner. She also worked at Westpac for 10 years, where her roles included Group Secretary and General Counsel and Group Executive, People, where she was responsible for human resources, corporate affairs and sustainability. Ilana has a strong commitment to the community, in particular the arts and education.

Relevant Other Directorships

| • | Chairman: Coca-Cola Amatil Limited (from 2017, Director from 2011) and Jawun (from 2017, Director from 2014). |

| • | Director: Westfield Corporation Limited (from 2014) and Human Rights Law Centre Ltd (from 2012). |

| • | Member: Panel of Adara Partners (from 2015). |

| • | Fellow: Senate of the University of Sydney (from 2015). |

Relevant Former Directorships held

in last three years, include

| • | Former Chairman: The Bell Shakespeare Company Limited (2010-2016, Director 2004-2016). |

| • | Former Director: Treasury Corporation of New South Wales (2013-2017), Suncorp Group Limited (2011-2014), Suncorp-Metway Limited (2011-2014), AAI Limited (2011-2014) and Scentre Group Limited (previously known as Westfield Holdings Limited) (2011-2014). |

Age63 years | ResidenceSydney, Australia

Career

Paula has extensive experience in financial markets, corporate finance, risk management and investments, having held senior executive roles at Calibre Asset Management, Ord Minnett (now J P Morgan) and at Price Waterhouse (now PricewaterhouseCoopers). Her career as a company director spans financial services, investment, insurance, healthcare, gambling and entertainment, fast moving consumer goods, property and construction and retailing sectors. Paula is a former member of the Takeovers Panel. Paula has a strong interest in education and medical research, having served as a member of the Geelong Grammar School Council and the Business and Economics Faculty at the University of Melbourne and as Deputy Chairman of Baker IDI.

Relevant Other Directorships

| • | Chairman: Tabcorp Holdings Limited (from 2011, Director from 2005), Healthscope Limited (from 2014) and Kin Group Advisory Board (from 2014). |

| • | Director: Lion Pty Ltd (from 2012). |

| • | Member: Kirin International Advisory Board (from 2012). |

Relevant Former Directorships held

in last three years, include

| • | Former Deputy Chairman: Leighton Holdings Limited (2013-2014, Director 2012). |

| • | Former Member: John Holland Group Advisory Board (2012-2014), Australian Government Takeovers Panel (2008-2014) and ASIC External Advisory Panel (2012-2015). |

Age57 years | ResidenceMelbourne, Australia

29

ANZ 2017 ANNUAL REPORT

GOVERNANCE (continued)

DIRECTORS’ QUALIFICATIONS, EXPERIENCE AND SPECIAL RESPONSIBILITIES(continued)

JANE HALTON, AO, PSM

IndependentNon-Executive Director

BA (Hons) Psychology, FIML, FIPAA, NAM, Hon. FAAHMS,

Hon. FACHSE, Hon. DLitt (UNSWA)

Non-Executive Director since October 2016. Jane is a member of the Human Resources Committee, Environment, Sustainability and Governance Committee and Digital Business and Technology Committee.

Member:

LEE HSIEN YANG

IndependentNon-Executive Director and Chair

of the Digital Business and Technology Committee

MSc, BA

Non-Executive Director since February 2009. Hsien Yang is a member of the Risk Committee and Human Resources Committee.

Chair: Member:

Career

Jane’s 33 year career in the public service includes the positions of Secretary of the Australian Department of Finance, Secretary of the Australian Department of Health, Secretary for the Department of Health and Ageing, and ExecutiveCo-ordinator (Deputy Secretary) of the Department of the Prime Minister and Cabinet. She brings to the Board extensive experience in finance, insurance, risk management, information technology, human resources, health and ageing and public policy. She also has significant international experience.

Jane has contributed extensively to community health through local and international organisations including the World Health Organisation and National Aboriginal and Torres Strait Islander Health Council.

Relevant Other Directorships

| • | Director: Clayton Utz (from 2017). |

| • | Member: Executive Board of the Institute of Health Metrics and Evaluation at the University of Washington (from 2007). |

| • | Board Member: Coalition for Epidemic Preparedness Innovations (Norway) (from 2016). |

| • | Public Policy Fellow: ANU Crawford School of Public Policy (from 2012). |

| • | Adjunct Professor: University of Sydney and University of Canberra. |

| • | Council Member: Australian Strategic Policy Institute (from 2016). |

Relevant Former Directorships held

in last three years, include

| • | Former Chairman: OECD Asian Senior Budget Officials Network (2014–2016) and World Health Organisation Executive Board (2013–2014, Member 2012-2015). |

| • | Former Executive Board Member: World Health Organisation (2012–2015). |

| • | Former Member: Melbourne Institute Advisory Board (2007–2015), the NationalE-Health Transition Authority (2005–2014) and Australian Institute of Health and Welfare (2002–2014). |

| • | Former Commissioner: Australian Sports Commission (2013–2014). |

Age57 years | ResidenceCanberra, Australia

Career

Hsien Yang is an experienced business executive with considerable knowledge of and operating experience in Asia. He has a background in engineering and brings to the Board his international business and management experience across a wide range of sectors including telecommunications, food and beverages, property, publishing and printing, financial services, education, civil aviation and land transport. His contribution to community education activities includes membership of the Governing Board of Lee Kuan Yew School of Public Policy.

Relevant Other Directorships

| • | Chairman: The Islamic Bank of Asia Limited (from 2012, Director from 2007), Civil Aviation Authority of Singapore (from 2009) and General Atlantic Singapore Fund Pte Ltd (from 2013). |

| • | Director: Rolls-Royce Holdings plc (from 2014), General Atlantic Singapore Fund FII Pte Ltd (from 2014), Cluny Lodge Pte Ltd (from 1979) and Caldecott Inc. (from 2013). |

| • | Member: Governing Board of Lee Kuan Yew School of Public Policy (from 2005). |

| • | Special Adviser: General Atlantic (from 2013). |

| • | President: INSEAD South East Asia Council (from 2013). |

Relevant Former Directorships held

in last three years, include

| • | Former Director: Singapore Exchange Limited (2004-2016). |

| • | Former Consultant: Capital International Inc Advisory Board (2007-2016) |

Age60 years | ResidenceSingapore

30

GOVERNANCE

GRAEME LIEBELT

IndependentNon-Executive Director

and Chair of the Risk Committee

BEc (Hons), FAICD, FTSE, FIML

Non-Executive Director since July 2013. Graeme is a member of the Audit Committee and Human Resources Committee.

Chair: Member:

JOHN MACFARLANE

IndependentNon-Executive Director

BCom, MCom (Hons)

Non-Executive Director since May 2014. John is a member of the Audit Committee, Risk Committee and Digital Business and Technology Committee.

Member:

Career

Graeme brings to the Board his experience of a 23 year executive career with Orica Limited (including a period as Chief Executive Officer), a global mining services company with operations in more than 50 countries. He has extensive international experience and a strong record of achievement as a senior executive including in strategy development and implementation.

Graeme is committed to global trade andco-operation, as well as community education.

Relevant Other Directorships

| • | Chairman: Amcor Limited (from 2013, Director from 2012). |

| • | Director: Australian Foundation Investment Company Limited (from 2012), Carey Baptist Grammar School (from 2012) and DuluxGroup Limited (from 2016). |

Relevant Former Directorships held

in last three years, include

| • | Former Deputy Chairman: Melbourne Business School (2012-2015, Director from 2008). |

| • | Former Chairman: The Global Foundation (2014-2015, Director from 2006). |

Age63 years | ResidenceMelbourne, Australia

Career