Exhibit 99.3

PRO FORMA VALUATION REPORT

MALVERN BANCORP, INC.

Paoli, Pennsylvania

PROPOSED HOLDING COMPANY FOR:

MALVERN FEDERAL SAVINGS BANK

Paoli, Pennsylvania

Dated As Of:

May 4, 2012

Prepared By:

RP® Financial, LC.

1100 North Glebe Road

Suite 600

Arlington, Virginia 22201

| May 4, 2012 |

Boards of Directors

Malvern Federal Mutual Holding Company

Malvern Federal Bancorp, Inc.

Malvern Federal Savings Bank

42 East Lancaster Avenue

Paoli, Pennsylvania 19301

Members of the Boards of Directors:

At your request, we have completed and hereby provide an independent appraisal (“Appraisal”) of the estimated pro forma market value of the common stock which is to be issued in connection with the mutual-to-stock conversion transaction described below.

This Appraisal is furnished pursuant to the requirements of the Code of Federal Regulations 563b.7 and has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the Office of Thrift Supervision (“OTS”) and reissued by the Office of the Comptroller of the Currency (“OCC”), and applicable regulatory interpretations thereof. Such Valuation Guidelines are relied upon by the Federal Reserve Board (“FRB”) in the absence of separate written valuation guidelines.

Description of Plan of Conversion and Reorganization

On January 17 2012, the respective Boards of Directors of Malvern Federal Mutual Holding Company (the “MHC”), Malvern Federal Bancorp, Inc. (“MLVF”) and Malvern Federal Savings Bank, Paoli, Pennsylvania (the “Bank”) adopted a Plan of Conversion and Reorganization (the “Plan of Conversion”) whereby the MHC will convert to stock form. As a result of the conversion, MLVF, which currently owns all of the issued and outstanding common stock of the Bank, will be succeed by a Pennsylvania corporation with the name of Malvern Bancorp, Inc. (“Malvern Bancorp” or the “Company”). Following the conversion, the MHC and MLVF will no longer exist. For purposes of this document, the existing consolidated entity will hereinafter be referred to as Malvern Bancorp or the Company. As of March 31, 2012, the MHC had a majority ownership interest in, and its principal asset consisted of, approximately 55.45% of the common stock (the “MHC Shares”) of MLVF. The remaining 44.55% of MLVF’s common stock is owned by public stockholders.

It is our understanding that Malvern Bancorp will offer its stock, representing the majority ownership interest held by the MHC, in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Other Members, as such terms are defined for purposes of applicable federal regulatory requirements governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions

| Washington Headquarters | |

| Three Ballston Plaza | Telephone: (703) 528-1700 |

| 1100 North Glebe Road, Suite 600 | Fax No.: (703) 528-1788 |

| Arlington, VA 22201 | Toll-Free No.: (866) 723-0594 |

| www.rpfinancial.com | E-Mail: mail@rpfinancial.com |

Boards of Directors

May 4, 2012

Page 2

received in the subscription offering, the shares may be offered for sale to the public at large in a community offering and/or a syndicated community offering. Upon completing the mutual-to-stock conversion and stock offering (the “second-step conversion”), the Company will be 100% owned by public shareholders, the publicly-held shares of MLVF will be exchanged for shares in the Company at a ratio that retains their ownership interest at the time the conversion is completed and the MHC assets will be consolidated with the Company.

RP® Financial, LC.

RP® Financial, LC. (“RP Financial”) is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. The background and experience of RP Financial is detailed in Exhibit V-1. For its appraisal services, RP Financial is being compensated on a fixed fee basis for the original appraisal and for any subsequent updates, and such fees are payable regardless of the valuation conclusion or the completion of the conversion offering transaction. We believe that we are independent of the Company, the Bank, the MHC and the other parties engaged by the Bank or the Company to assist in the stock conversion process.

Valuation Methodology

In preparing our Appraisal, we have reviewed the regulatory applications of the Company, the Bank and the MHC, including the prospectus as filed with the FRB, the OCC and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of the Company, the Bank and the MHC that has included a review of audited financial information for the fiscal years ended September 30, 2007 through September 30, 2011 and a review of various unaudited information and internal financial reports through March 31, 2012, and due diligence related discussions with the Company’s management; ParenteBeard LLC, the Company’s independent auditor; Elias, Matz, Tiernan & Herrick L.L.P., the Company’s conversion counsel; and Stifel Nicolaus Weisel, the Company’s marketing advisor in connection with the stock offering. All assumptions and conclusions set forth in the Appraisal were reached independently from such discussions. In addition, where appropriate, we have considered information based on other available published sources that we believe are reliable. While we believe the information and data gathered from all these sources are reliable, we cannot guarantee the accuracy and completeness of such information.

We have investigated the competitive environment within which Malvern Bancorp operates and have assessed Malvern Bancorp’s relative strengths and weaknesses. We have kept abreast of the changing regulatory and legislative environment for financial institutions and analyzed the potential impact on Malvern Bancorp and the industry as a whole. We have analyzed the potential effects of the stock conversion on Malvern Bancorp’s operating characteristics and financial performance as they relate to the pro forma market value of Malvern Bancorp. We have analyzed the assets held by the MHC, which will be consolidated with Malvern Bancorp’s assets and equity pursuant to the completion of the second-step conversion. We have reviewed the economic and demographic characteristics of the Company’s primary market area. We have compared Malvern Bancorp’s financial performance

Boards of Directors

May 4, 2012

Page 3

and condition with selected publicly-traded thrifts in accordance with the Valuation Guidelines, as well as all publicly-traded thrifts and thrift holding companies. We have reviewed the current conditions in the securities markets in general and the market for thrift stocks in particular, including the market for existing thrift issues, initial public offerings by thrifts and thrift holding companies, and second-step conversion offerings. We have excluded from such analyses thrifts subject to announced or rumored acquisition, and/or institutions that exhibit other unusual characteristics.

The Appraisal is based on Malvern Bancorp’s representation that the information contained in the regulatory applications and additional information furnished to us by Malvern Bancorp and its independent auditor, legal counsel and other authorized agents are truthful, accurate and complete. We did not independently verify the financial statements and other information provided by Malvern Bancorp, or its independent auditor, legal counsel and other authorized agents nor did we independently value the assets or liabilities of Malvern Bancorp. The valuation considers Malvern Bancorp only as a going concern and should not be considered as an indication of Malvern Bancorp’s liquidation value.

Our appraised value is predicated on a continuation of the current operating environment for Malvern Bancorp and for all thrifts and their holding companies. Changes in the local, state and national economy, the legislative and regulatory environment for financial institutions and mutual holding companies, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability and may materially impact the value of thrift stocks as a whole or the value of Malvern Bancorp’s stock alone. It is our understanding that there are no current plans for selling control of Malvern Bancorp following completion of the second-step conversion. To the extent that such factors can be foreseen, they have been factored into our analysis.

The estimated pro forma market value is defined as the price at which Malvern Bancorp’s common stock, immediately upon completion of the second-step stock offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Valuation Conclusion

It is our opinion that, as of May 4, 2012, the estimated aggregate pro forma valuation of the shares of the Company to be issued and outstanding at the end of the conversion offering – including (1) newly-issued shares representing the MHC’s current ownership interest in the Company and (2) exchange shares issued to existing public shareholders of MLVF – was $49,593,660 at the midpoint, equal to 4,959,366 shares at $10.00 per share. The resulting range of value and pro forma shares, all based on $10.00 per share, are as follows: $42,154,610 or 4,215,461 shares at the minimum; $57,032,710 or 5,703,271 shares at the maximum; and $65,587,620 or 6,558,762 shares at the super maximum (also known as “maximum, as adjusted”).

Based on this valuation and taking into account the ownership interest represented by the shares owned by the MHC, the midpoint of the offering range is $27,500,000, equal to 2,750,000 shares at $10.00 per share. The resulting offering range and offering shares, all based on $10.00 per share, are as follows: $23,375,000 or 2,337,500 shares at the minimum;

Boards of Directors

May 4, 2012

Page 4

$31,625,000 or 3,162,500 shares at the maximum; and $36,368,750 or 3,636,875 shares at the super maximum.

Establishment of the Exchange Ratio

OCC regulations provide that in a conversion of a mutual holding company, the minority stockholders are entitled to exchange the public shares for newly issued shares in the fully converted company. The Boards of Directors of the MHC, MLVF and the Bank have independently determined the exchange ratio, which has been designed to preserve the current aggregate percentage ownership in the Company held by the public shareholders. The exchange ratio to be received by the existing minority shareholders of the Company will be determined at the end of the offering, based on the total number of shares sold in the offering and the final appraisal. Based on the valuation conclusion herein, the resulting offering value and the $10.00 per share offering price, the indicated exchange ratio at the midpoint is 0.8127 shares of the Company for every one share held by public shareholders. Furthermore, based on the offering range of value, the indicated exchange ratio is 0.6908 at the minimum, 0.9346 at the maximum and 1.0748 at the super maximum. RP Financial expresses no opinion on the proposed exchange of newly issued Company shares for the shares held by the public stockholders or on the proposed exchange ratio.

Limiting Factors and Considerations

The valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is determined in accordance with applicable OCC regulatory guidelines and is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion offering, or prior to that time, will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The appraisal reflects only a valuation range as of this date for the pro forma market value of Malvern Bancorp immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market on the date of issuance of such securities or at anytime thereafter following the completion of the second-step conversion.

RP Financial’s valuation was based on the financial condition, operations and shares outstanding of Malvern Bancorp as of March 31, 2012, the date of the financial data included in the prospectus. The proposed exchange ratio to be received by the current public stockholders of MLVF and the exchange of the public shares for newly issued shares of Malvern Bancorp’s common stock as a full public company was determined independently by the Boards of Directors of the MHC, MLVF and the Bank. RP Financial expresses no opinion on the proposed exchange ratio to public stockholders or the exchange of public shares for newly issued shares.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its client institutions.

Boards of Directors

May 4, 2012

Page 5

This valuation will be updated as provided for in the conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of Malvern Bancorp, management policies, and current conditions in the equity markets for thrift shares, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including, but not limited to: various changes in the legislative and regulatory environment for financial institutions, the stock market and the market for thrift stocks, and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update. The valuation will also be updated at the completion of Malvern Bancorp’s stock offering.

| Respectfully submitted, | |

| RP® FINANCIAL, LC. | |

| |

| Ronald S. Riggins | |

| President and Managing Director | |

| |

| Gregory E. Dunn | |

| Director |

| RP® Financial, LC. | TABLE OF CONTENTS |

| i |

TABLE OF CONTENTS

MALVERN BANCORP, INC.

MALVERN FEDERAL SAVINGS BANK

Paoli, Pennsylvania

| DESCRIPTION | PAGE NUMBER | |||

| CHAPTER ONE | OVERVIEW AND FINANCIAL ANALYSIS | |||

| Introduction | I.1 | |||

| Plan of Conversion and Reorganization | I.1 | |||

| Strategic Overview | I.2 | |||

| Balance Sheet Trends | I.5 | |||

| Income and Expense Trends | I.9 | |||

| Interest Rate Risk Management | I.13 | |||

| Lending Activities and Strategy | I.13 | |||

| Asset Quality | I.17 | |||

| Funding Composition and Strategy | I.18 | |||

| Subsidiaries | I.18 | |||

| Legal Proceedings | I.19 | |||

| CHAPTER TWO | MARKET AREA | |||

| Introduction | II.1 | |||

| National Economic Factors | II.1 | |||

| Market Area Demographics | II.5 | |||

| Local Economy | II.7 | |||

| Unemployment Trends | II.10 | |||

| Market Area Deposit Characteristics and Competition | II.10 | |||

| CHAPTER THREE | PEER GROUP ANALYSIS | |||

| Peer Group Selection | III.1 | |||

| Financial Condition | III.5 | |||

| Income and Expense Components | III.8 | |||

| Loan Composition | III.11 | |||

| Interest Rate Risk | III.13 | |||

| Credit Risk | III.13 | |||

| Summary | III.16 | |||

| RP® Financial, LC. | TABLE OF CONTENTS |

| ii |

TABLE OF CONTENTS

MALVERN BANCORP, INC.

MALVERN FEDERAL SAVINGS BANK

Paoli, Pennsylvania

(continued)

| DESCRIPTION | PAGE NUMBER | |||||

| CHAPTER FOUR | VALUATION ANALYSIS | |||||

| Introduction | IV.1 | |||||

| Appraisal Guidelines | IV.1 | |||||

| RP Financial Approach to the Valuation | IV.1 | |||||

| Valuation Analysis | IV.2 | |||||

| 1. | Financial Condition | IV.2 | ||||

| 2. | Profitability, Growth and Viability of Earnings | IV.4 | ||||

| 3. | Asset Growth | IV.6 | ||||

| 4. | Primary Market Area | IV.6 | ||||

| 5. | Dividends | IV.7 | ||||

| 6. | Liquidity of the Shares | IV.8 | ||||

| 7. | Marketing of the Issue | IV.8 | ||||

| A. | The Public Market | IV.9 | ||||

| B. | The New Issue Market | IV.12 | ||||

| C. | The Acquisition Market | IV.13 | ||||

| D. | Trading in Malvern Bancorp’s Stock | IV.13 | ||||

| 8. | Management | IV.15 | ||||

| 9. | Effect of Government Regulation and Regulatory Reform | IV.16 | ||||

| Summary of Adjustments | IV.16 | |||||

| Valuation Approaches: | IV.16 | |||||

| 1. | Price-to-Earnings (“P/E”) | IV.18 | ||||

| 2. | Price-to-Book (“P/B”) | IV.19 | ||||

| 3. | Price-to-Assets (“P/A”) | IV.19 | ||||

| Comparison to Recent Offerings | IV.21 | |||||

| Valuation Conclusion | IV.21 | |||||

| Establishment of the Exchange Ratio | IV.22 | |||||

| RP® Financial, LC. | LIST OF TABLES |

| iii |

LIST OF TABLES

MALVERN BANCORP, INC.

MALVERN FEDERAL SAVINGS BANK

Paoli, Pennsylvania

| TABLE NUMBER | DESCRIPTION | PAGE | ||

| 1.1 | Historical Balance Sheet Data | I.6 | ||

| 1.2 | Historical Income Statements | I.10 | ||

| 2.1 | Summary Demographic Data | II.6 | ||

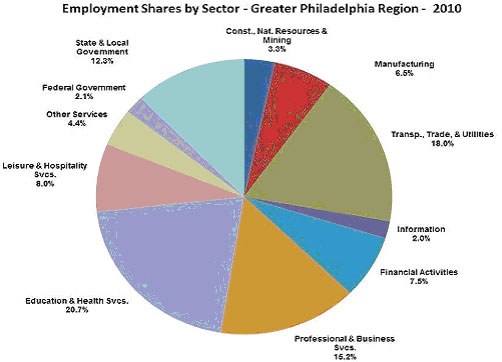

| 2.2 | Employment by Sector | II.7 | ||

| 2.3 | Market Area Largest Employers | II.9 | ||

| 2.4 | Unemployment Trends | II.10 | ||

| 2.5 | Deposit Summary | II.11 | ||

| 2.6 | Market Area Deposit Competitors | II.12 | ||

| 3.1 | Peer Group of Publicly-Traded Thrifts | III.3 | ||

| 3.2 | Balance Sheet Composition and Growth Rates | III.6 | ||

| 3.3 | Income as a Percent of Average Assets and Yields, Costs, Spreads | III.9 | ||

| 3.4 | Loan Portfolio Composition and Related Information | III.12 | ||

| 3.5 | Interest Rate Risk Measures and Net Interest Income Volatility | III.14 | ||

| 3.6 | Credit Risk Measures and Related Information | III.15 | ||

| 4.1 | Market Area Unemployment Rates | IV.7 | ||

| 4.2 | Pricing Characteristics and After-Market Trends | IV.14 | ||

| 4.3 | Public Market Pricing | IV.20 |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.1 |

I. Overview and Financial Analysis

Introduction

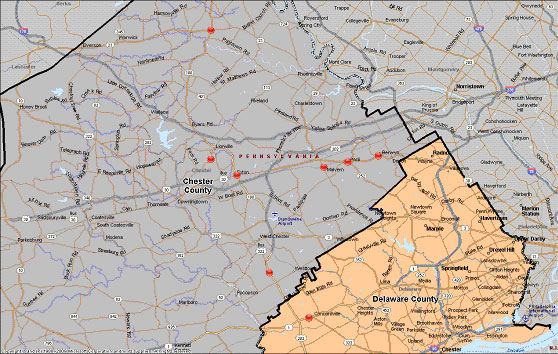

Malvern Federal Savings Bank (the “Bank”), chartered in 1887, is a federally chartered stock savings bank headquartered in Paoli, Pennsylvania. The Bank serves the Philadelphia metropolitan area through the headquarters office and eight branch offices. The headquarters and seven branches are located in Chester County and one branch is located in Delaware County. A map of the Bank’s branch office locations is provided in Exhibit I-1. The Bank is a member of the Federal Home Loan Bank (“FHLB”) system and its deposits are insured up to the maximum allowable amount by the Federal Deposit Insurance Corporation (“FDIC”).

Malvern Federal Bancorp, Inc. (“MLVF”) is the federally-chartered mid-tier holding company of the Bank. MLVF owns 100% of the outstanding common stock of the Bank. Since being formed in 2008, MLVF has engaged primarily in the business of holding the common stock of the Bank. MLVF completed its initial public offering in May 2008, pursuant to which it sold 2,645,575 shares or 43% of its outstanding common stock to the public at a purchase price of $10.00 per share, issued 3,383,875 shares or 55% of its common stock outstanding to Malvern Federal Mutual Holding Company (the “MHC”), the mutual holding company parent of MLVF and contributed 123,050 shares or 2% of the common stock outstanding to the Malvern Federal Charitable Foundation. The Bank is supervised and examined by the Office of the Comptroller of the Currency (“OCC”). The MHC and MLVF are subject to supervision and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board” or the “FRB”). At March 31, 2012, MLVF had total assets of $651.6 million, deposits of $537.0 million and equity of $61.9 million or 9.5% of total assets. MLVF’s audited financial statements for the most recent period are included by reference as Exhibit I-2.

Plan of Conversion and Reorganization

On January 17, 2012, the respective Boards of Directors of the MHC, MLVF and the Bank adopted a Plan of Conversion and Reorganization (the “Plan of Conversion”) whereby the MHC will convert to stock form. As a result of the conversion, MLVF, which currently owns all of the issued and outstanding common stock of the Bank, will be succeed by a Pennsylvania corporation with the name of Malvern Bancorp, Inc. (“Malvern Bancorp” or the “Company”). Following the conversion, the MHC will no longer exist. For purposes of this document, the

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.2 |

existing consolidated entity will hereinafter be referred to as Malvern Bancorp or the Company. As of March 31, 2012, the MHC’s ownership interest in MLVF approximated 55.45% and the public stockholders’ ownership interest in MLVF approximated 44.55%.

It is our understanding that Malvern Bancorp will offer its stock, representing the majority ownership interest held by the MHC, in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Other Members, as such terms are defined for purposes of applicable federal regulatory requirements governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to members of the general public in a community offering and/or a syndicated community offering. Upon completing the mutual-to-stock conversion and stock offering (the “second-step conversion”), the Company will be 100% owned by public shareholders, the publicly-held shares of MLVF will be exchanged for shares in the Company at a ratio that retains their ownership interest at the time the conversion is completed and the MHC assets will be consolidated with the Company.

Strategic Overview

Malvern Bancorp maintains a local community banking emphasis, with a primary strategic objective of meeting the borrowing and savings needs of its local customer base. Historically, Malvern Bancorp’s operating strategy has been fairly reflective of a traditional thrift operating strategy in which 1-4 family residential mortgage loans and retail deposits have constituted the principal components of the Company’s assets and liabilities, respectively. Beyond 1-4 family permanent mortgage loans, the Company’s lending activities include diversification into commercial real estate loans, construction and land loans, commercial business, and consumer loans. Pursuant to the Company’s diversification into higher risk types of lending followed by a downturn in real estate market conditions, the Company experienced deterioration in credit quality. Non-performing assets increased from $2.5 million or 0.45% of assets at September 30, 2007 to $25.2 million or 3.49% of assets at September 30, 2010. Residential mortgage loans (both first and second mortgages) and commercial real estate/multi-family loans comprised the largest concentrations of the Company’s non-performing assets balance at September 30, 2010. Since fiscal year end 2010, the non-performing assets balance has trended lower and equaled $16.5 million or 2.53% of assets at March 31, 2012. In light of the Company’s deterioration in credit quality, less favorable real estate market conditions for higher risk commercial real estate loans and construction and development loans and due to

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.3 |

regulatory constraints imposed by the Office of Thrift Supervision (“OTS”) during fiscal 2010, the Company has generally stopped originating new commercial real estate loans and construction and development loans. Accordingly, the Company’s current lending activities emphasize the origination of 1-4 family permanent mortgage loans and consumer loans.

In October 2010, the Company, the Bank and the MHC entered into Supervisory Agreements with the OTS, which have been transferred to the OCC in the case of the Bank and to the FRB in the case of the Company and the MHC. Exhibit I-3 provides a summary of the requirements and restrictions set forth in the Supervisory Agreements. As of March 31, 2012, the Bank, the Company and the MHC were in compliance with the terms of their respective Supervisory Agreements.

Investments serve as a supplement to the Company’s lending activities, with recent trends showing an increase in investment securities. The Company has experienced an increase in liquidity in connection with the loan portfolio shrinkage that has occurred over the past two and one-half fiscal years, which in part has been deployed into investment securities. The Company’s investment activities have emphasized investment in mortgage-backed securities and U.S. Government and agency securities. Other investments maintained by the Company include trust preferred securities, municipal bonds, corporate debt securities and FHLB stock.

Retail deposits have consistently served as the primary interest-bearing funding source for the Company. The deposit base is concentrated in time deposits, which are locally generated deposits. Malvern Federal does not maintain any brokered certificates of deposit (“CDs”) and under the terms of the Bank’s Supervisory Agreement, the Bank may not engage in the use of brokered deposits without the prior written non-objection of the OCC. In recent years, the concentration of CDs has declined as a percent of total deposits, as the result of a decline in CD balances and growth of transaction and saving account deposits. The Company utilizes borrowings as a supplemental funding source to facilitate management of funding costs and interest rate risk. FHLB advances currently account for all of the Company’s borrowings and consist substantially of long-term advances with initial terms of more than five years.

Malvern Bancorp’s earnings base is largely dependent upon net interest income and operating expense levels. The Company’s net interest margin has increased since fiscal 2009, as the decline in short-term interest rates and resulting steeper yield curve has facilitated higher interest rate spreads for the Company. In particular, the Company’s balance sheet is liability-sensitive in the short-term and, therefore, funding costs have decreased more rapidly relative to

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.4 |

yields earned on less rate sensitive interest-earning assets. Operating expenses have increased in recent years as well, which combined with asset shrinkage has inflated the Company’s operating expense ratio as a percent of average assets. The increase in operating expenses has been mostly related to professional fees incurred to facilitate the work out of problem assets and expenses related to holding higher balances of Other Real Estate Owned (“OREO”). Revenues derived from sources of non-interest operating income have been a relatively limited contributor to the Company’s earnings.

The post-offering business plan of the Company is expected to remain consistent with current strategic objectives. Malvern Bancorp will continue to be an independent community-oriented financial institution with a commitment to local real estate financing with operations funded primarily by retail deposits. Growth strategies will continue to be implemented within the context of managing the Company’s exposure to credit risk and interest rate risk and adhering to the requirements of the Supervisory Agreements. ..Accordingly, the Company’s business strategies will continue to focus on reducing the level of non-performing assets, managing the existing loan portfolio and emphasizing retail lending growth going forward, increasing market share in Chester and Delaware Counties and growing core deposits. Pursuant to the modification of the lending restrictions set forth in the Supervisory Agreements, the Company will seek to implement a more diversified lending strategy that will emphasize growth of commercial real estate loans and construction loans.

The Company’s Board of Directors has elected to complete a second-step conversion to improve the competitive position of Malvern Bancorp. The capital realized from the stock offering will increase the operating flexibility and overall financial strength of Malvern Bancorp. The additional capital realized from stock proceeds will increase liquidity to support funding of future loan growth and other interest-earning assets. The Company’s strengthened capital position will also provide more of a cushion against potential credit quality related losses, as the Company continues to implement workout strategies to reduce the balance of non-performing assets. Malvern Bancorp’s higher capital position resulting from the infusion of stock proceeds will also serve to reduce interest rate risk, particularly through enhancing the Company’s interest-earning-assets-to-interest-bearing-liabilities (“IEA/IBL”) ratio. The additional funds realized from the stock offering will provide an alternative funding source to deposits and borrowings in meeting the Company’s future funding needs, which may facilitate a reduction in Malvern Bancorp’s funding costs. The projected uses of proceeds are highlighted below.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.5 |

| o | Malvern Bancorp. The Company is expected to retain up to 30% of the net offering proceeds. At present, funds at the Company level are expected to be primarily invested initially into short-term investments. Over time, the funds may be utilized for various corporate purposes, possibly including infusing additional equity into the Bank, repurchases of common stock, and the payment of cash dividends pursuant to regulatory limitations and guidelines and the requirements of the Supervisory Agreements. | |

| o | Malvern Federal Savings Bank. Approximately 70% of the net stock proceeds will be infused into the Bank in exchange for all of the Bank’s newly issued stock. Cash proceeds (i.e., net proceeds less deposits withdrawn to fund stock purchases) infused into the Bank are anticipated to become part of general operating funds, and are expected to be primarily utilized to fund retail loan growth over time. |

Overall, it is the Company’s objective to pursue growth that will serve to increase returns, while, at the same time, growth will not be pursued that could potentially compromise the overall risk associated with Malvern Bancorp’s operations.

Balance Sheet Trends

Table 1.1 shows the Company’s historical balance sheet data for the past five and one-half years. From fiscal year end 2007 through March 31, 2012, Malvern Bancorp’s assets increased at a 3.8% annual rate. Asset growth was sustained through fiscal year end 2010 and then declined through March 31, 2012, as the Company curtailed its lending activities and focused on resolution of problem of assets. Asset growth was primarily funded by deposit growth, which paralleled asset growth trends for the period covered in Table 1.1. A summary of Malvern Bancorp’s key operating ratios for the past five and one-half fiscal years is presented in Exhibit I-4.

Malvern Bancorp’s loans receivable balance at March 31, 2012 was only nominally higher compared to the balance at fiscal year end 2007, as loan growth sustained from year fiscal end 2007 through fiscal year end 2009 was substantially offset by a steady downward trend in the loans receivable balance from fiscal year end 2009 through March 31, 2012. The Company’s lower loan growth rate compared to its asset growth rate provided for a decrease in the loans-to-assets ratio from 84.5% at fiscal year end 2007 to 71.7% at March 31, 2012. Trends in the Company’s loan portfolio composition over the past five and one-half fiscal years show that the concentration of 1-4 family permanent mortgage loans comprising total loans increased from 40.4% at fiscal year end 2007 to 46.6% at March 31, 2012. Over the past five and one-half years lending diversification by the Company has emphasized commercial real estate/multi-family loans, with the concentration of commercial real estate/multi-family loans

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.6 |

Table 1.1

Malvern Bancorp, Inc.

Historical Balance Sheet Data

| 09/30/07- 03/31/12 | ||||||||||||||||||||||||||||||||||

| At Fiscal Year Ended September 30, | At March 31, | Annual. | ||||||||||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | Growth Rate | ||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct | ||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | ||||||||||||||||||||||

| Total Amount of: | ||||||||||||||||||||||||||||||||||

| Assets | $ | 551,932 | 100.00 | % | $ | 639,509 | 100.00 | % | $ | 691,639 | 100.00 | % | $ | 720,506 | 100.00 | % | $ | 666,568 | 100.00 | % | $ | 651,604 | 100.00 | % | 3.76 | % | ||||||||

| Cash and cash equivalents | 18,967 | 3.44 | % | 12,922 | 2.02 | % | 25,325 | 3.66 | % | 81,395 | 11.30 | % | 33,496 | 5.03 | % | 58,625 | 9.00 | % | 28.50 | % | ||||||||||||||

| Investment securities | 30,577 | 5.54 | % | 24,839 | 3.88 | % | 31,940 | 4.62 | % | 45,435 | 6.31 | % | 78,186 | 11.73 | % | 82,397 | 12.65 | % | 24.64 | % | ||||||||||||||

| Loans receivable, net | 466,192 | 84.47 | % | 571,536 | 89.37 | % | 593,565 | 85.82 | % | 547,323 | 75.96 | % | 506,019 | 75.91 | % | 467,028 | 71.67 | % | 0.04 | % | ||||||||||||||

| Loans held for sale | 9,258 | 1.68 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | -100.00 | % | ||||||||||||||

| FHLB stock | 4,560 | 0.83 | % | 6,896 | 1.08 | % | 6,567 | 0.95 | % | 6,567 | 0.91 | % | 5,349 | 0.80 | % | 4,827 | 0.74 | % | 1.27 | % | ||||||||||||||

| Bank-owned life insurance | 7,787 | 1.41 | % | 8,136 | 1.27 | % | 13,650 | 1.97 | % | 14,213 | 1.97 | % | 14,760 | 2.21 | % | 15,026 | 2.31 | % | 15.73 | % | ||||||||||||||

| Other real estate owned | 227 | 0.04 | % | 230 | 0.04 | % | 5,875 | 0.85 | % | 5,315 | 0.74 | % | 8,321 | 1.25 | % | 4,743 | 0.73 | % | 96.49 | % | ||||||||||||||

| Deposits | $ | 433,488 | 78.54 | % | $ | 453,493 | 70.91 | % | $ | 516,511 | 74.68 | % | $ | 596,858 | 82.84 | % | $ | 554,455 | 83.18 | % | $ | 537,029 | 82.42 | % | 4.87 | % | ||||||||

| Borrowings | 71,387 | 12.93 | % | 113,798 | 17.79 | % | 99,621 | 14.40 | % | 55,334 | 7.68 | % | 49,098 | 7.37 | % | 48,593 | 7.46 | % | -8.19 | % | ||||||||||||||

| Equity | $ | 44,039 | 7.98 | % | $ | 68,836 | 10.76 | % | $ | 69,842 | 10.10 | % | $ | 66,207 | 9.19 | % | $ | 60,284 | 9.04 | % | $ | 61,903 | 9.50 | % | 7.86 | % | ||||||||

| Loans/Deposits | 105.19 | % | 152.06 | % | 127.14 | % | 110.03 | % | 96.47 | % | 89.88 | % | ||||||||||||||||||||||

| Full Service Offices | 7 | 7 | 7 | 8 | 8 | 8 | ||||||||||||||||||||||||||||

(1) Ratios are as a percent of ending assets.

Sources: Malvern Bancorp’s prospectus, audited and unaudited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.7 |

comprising total loans increasing from 23.2% at fiscal year end 2007 to 27.0% at March 31, 2012. Consumer loans constitute the second largest area of lending diversification for the Company and increased from 19.3% of total loans at fiscal year end 2007 to 19.9% of total loans at March 31, 2012. Other areas of lending diversification for the Company include construction and land loans, which declined from 13.8% of total loans at fiscal year end 2007 to 4.7% of total loans at March 31, 2012, and commercial business loans, which declined from 3.3% of total loans at fiscal year end 2007 to 1.8% of total loans at March 31, 2012. Loan balances for 1-4 family permanent mortgage loans, commercial real estate/multi-family loans and consumer loans have been declining since fiscal year end 2009, while the balance of construction and land loans has been declining since fiscal year end 2007 and the balance of commercial business loans has been declining since fiscal year end 2008.

The intent of the Company’s investment policy is to provide adequate liquidity and to generate a favorable return within the context of supporting Malvern Bancorp’s overall credit and interest rate risk objectives. It is anticipated that proceeds retained at the holding company level will primarily be invested into short-term funds. The Company has maintained a higher level of cash and investments in recent years for purposes of managing credit risk and interest rate exposure, during a period when the Company has experienced credit quality deterioration in its loans portfolio and interest rates are at historical lows. Over the past five and one half fiscal years, the Company’s level of cash and investment securities (inclusive of FHLB stock) ranged from a low of 7.2% of assets at fiscal year end 2008 to a high of 22.4% of assets at March 31, 2012. The Company maintained total cash and investments of $145.8 million at March 31, 2012.

Mortgage-backed securities have generally comprised the largest portion of the Company’s investment holdings over the past five and one-half years and are generally purchased as a means to deploy excess liquidity at more favorable yields than other investment alternatives that are consistent with Malvern Bancorp’s investment philosophy. Mortgage-backed securities held by Malvern Bancorp consist of securities that are guaranteed or insured by GSEs. As of March 31, 2012, the mortgage-backed securities portfolio totaled $47.8 million. Mortgage-backed securities maintained as available for sale totaled $47.1 million at March 31, 2012, with the remaining $696,000 of the portfolio maintained as held to maturity. As of March 31, 2012, the net unrealized gain on the available for sale mortgage-backed securities portfolio equaled $803,000. Beyond the mortgage-backed securities portfolio, investment securities held by the Company at March 31, 2012 consisted of $28.0 million of U.S. Government and agency

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.8 |

debt securities, $1.5 million of corporate debt securities, $2.6 million of municipal bonds and $758,000 of trust preferred securities and were all maintained as available for sale. As of March 31, 2012, the net unrealized loss on the available for sale portfolio of investment securities equaled $114.000. Exhibit I-5 provides historical detail of the Company’s investment portfolio. As of March 31, 2012, the Company also held FHLB stock of $4.8 million or 0.7% of assets and cash and cash equivalents amounting to $58.6 million or 9.0% of assets.

The Company also maintains an investment in bank-owned life insurance (“BOLI”) policies, which cover the lives of some of the Company’s employees and directors. The purpose of the investment is to provide funding for the benefit plans of the covered individuals. The life insurance policies earn tax-exempt income through cash value accumulation and death proceeds. As of March 31, 2012, the cash surrender value of the Company’s BOLI equaled $15.0 million or 2.3% of assets.

Over the past five and one-half fiscal years, Malvern Bancorp’s funding needs have been addressed through a combination of deposits, borrowings and internal cash flows. From fiscal year end 2007 through March 31, 2012, the Company’s deposits increased at a 4.9% annual rate. Deposit growth was sustained from fiscal year end 2007 through fiscal year end 2010, which was followed by a decline in deposits during the past one and one-half fiscal years. Most of decline in deposits consisted of CDs, as the Company elected not to match higher rates offered in the marketplace to facilitate deposit run-off that could be funded by asset shrinkage. Overall, total deposits increased from $433.5 million or 78.5% of assets at fiscal year end 2007 to $537.0 million or 82.4% of assets at March 31, 2012. CDs accounted for 54.8% of total deposits at March 31, 2012, versus 62.3% of total deposits at fiscal year end 2010.

Borrowings serve as an alternative funding source for the Company to address funding needs for growth and to support management of deposit costs and interest rate risk. From year end 2007 through March 31, 2012, borrowings decreased at an annual rate of 8.2%. Borrowings increased from $71.4 million or 12.9% of assets at fiscal year end 2007 to a peak balance of $113.8 million or 17.8% of assets at fiscal year end 2008 and then declined to a low of $48.6 million or 7.5% of assets at March 31, 2012. The Company’s utilization of borrowings has generally been limited to FHLB advances and borrowings held by the Company at March 31, 2012 consisted entirely of FHLB advances.

The Company’s equity increased at a 7.9% annual rate from year fiscal year end 2007 through March 31, 2012, which was mostly attributable to the minority stock offering completed during fiscal 2008. Retention of earnings during fiscal years 2008 and 2009 and the first six

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS |

| I.9 |

months of fiscal 2012 also contributed to the Company’s capital growth, but was more than offset by net losses recorded during fiscal years 2010 and 2011. Capital growth outpaced the Company’s asset growth rate, which provided for an increase in the Company’s equity-to-assets ratio from 8.0% at fiscal year end 2007 to 9.5% at March 31, 2012. All of the Company’s capital is tangible capital. Malvern Bancorp maintained capital surpluses relative to all of its regulatory capital requirements at March 31, 2012. The addition of stock proceeds will serve to strengthen the Company’s capital position, as well as support growth opportunities. At the same time, Malvern Bancorp’s ROE will initially be depressed following its stock conversion as the result of the significant increase that will be realized in the Company’s pro forma capital position.

Income and Expense Trends

Table 1.2 shows the Company’s historical income statements for the past five and one-half fiscal years. The Company’s reported earnings over the past five and one-half fiscal years ranged from a net loss of $6.1 million or 0.90% of average assets in fiscal 2011 to net income of $2.4 million or 0.45% of average assets during fiscal 2007. For the twelve months ended March 31, 2012, the Company reported net income of $801,000 or 0.12% of average assets. The net losses recorded during fiscal years 2010 and 2011 were largely related to significantly higher loan loss provisions established to address deterioration in the credit quality of the Company’s loan portfolio. Net interest income and operating expenses represent the primary components of the Company’s recurring earnings. Revenues derived from sources of non-interest operating income have been a relatively limited contributor to the Company’s earnings. Non-operating gains and losses have been a relatively minor factor in the Company’s earnings over the past five and one-half fiscal years.

Over the past five and one-half fiscal years, the Company’s net interest income to average assets ratio ranged from a low of 2.36% during fiscal 2009 to a high of 2.86% during fiscal 2011. For the twelve months ended March 31, 2012, the Company’s net interest income to average assets ratio equaled 2.82%. The comparatively higher net interest income ratios reported since fiscal 2009 have been facilitated by wider yield-cost spreads, as the decline in short-term interest rates and resulting steeper yield curve has provided for a more significant decline in the Company’s funding costs relative to less rate sensitive interest-earning asset yields. Deposit run-off, consisting primarily of relatively higher costing CDs, and the pay down of borrowings also contributed to lowering the Company’s funding costs. A reduction in the concentration of non-interest earning comprising assets further contributed to the increase in the

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.10 |

Table 1.2

Malvern Bancorp, Inc.

Historical Income Statements

| For the Fiscal Year Ended September 30, | For the 12 months | ||||||||||||||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | Ended 03/31/12 | ||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | ||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ||||||||||||||||||||||||||

| Interest income | $ | 32,769 | 6.18 | % | $ | 33,592 | 5.85 | % | $ | 34,701 | 5.10 | % | $ | 33,148 | 4.80 | % | $ | 29,726 | 4.36 | % | $ | 27,954 | 4.20 | % | |||||||||||||

| Interest expense | (19,235 | ) | -3.63 | % | (19,105 | ) | -3.33 | % | (18,681 | ) | -2.75 | % | (13,641 | ) | -1.97 | % | (10,198 | ) | -1.50 | % | (9,191 | ) | -1.38 | % | |||||||||||||

| Net interest income | $ | 13,534 | 2.55 | % | $ | 14,487 | 2.52 | % | $ | 16,020 | 2.36 | % | $ | 19,507 | 2.82 | % | $ | 19,528 | 2.86 | % | $ | 18,763 | 2.82 | % | |||||||||||||

| Provision for loan losses | (1,298 | ) | -0.24 | % | (1,609 | ) | -0.28 | % | (2,280 | ) | -0.34 | % | (9,367 | ) | -1.36 | % | (12,392 | ) | -1.82 | % | (2,375 | ) | -0.36 | % | |||||||||||||

| Net interest income after provisions | $ | 12,236 | 2.31 | % | $ | 12,878 | 2.24 | % | $ | 13,740 | 2.02 | % | $ | 10,140 | 1.47 | % | $ | 7,136 | 1.05 | % | $ | 16,388 | 2.46 | % | |||||||||||||

| Other operating income | $ | 1,461 | 0.28 | % | $ | 1,846 | 0.32 | % | $ | 2,201 | 0.32 | % | $ | 2,096 | 0.30 | % | $ | 1,706 | 0.25 | % | $ | 2,094 | 0.31 | % | |||||||||||||

| Operating expense | (10,154 | ) | -1.91 | % | (12,642 | ) | -2.20 | % | (14,501 | ) | -2.13 | % | (17,105 | ) | -2.48 | % | (18,556 | ) | -2.72 | % | (18,325 | ) | -2.75 | % | |||||||||||||

| Net operating income | $ | 3,543 | 0.67 | % | $ | 2,082 | 0.36 | % | $ | 1,440 | 0.21 | % | ($ | 4,869 | ) | -0.70 | % | ($ | 9,714 | ) | -1.43 | % | $ | 157 | 0.02 | % | |||||||||||

| Non-Operating Income(Loss) | |||||||||||||||||||||||||||||||||||||

| Investment securities gains (losses), net | ($ | 8 | ) | 0.00 | % | — | 0.00 | % | 29 | 0.00 | % | $ | (13 | ) | 0.00 | % | — | 0.00 | % | $ | 623 | 0.09 | % | ||||||||||||||

| Gain (Loss)on sale of OREO | — | 0.00 | % | — | 0.00 | % | (225 | ) | -0.03 | % | (142 | ) | -0.02 | % | 23 | 0.00 | % | 9 | 0.00 | % | |||||||||||||||||

| Gain on disposal of fixed assets | — | 0.00 | % | — | 0.00 | % | 8 | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | |||||||||||||||||||

| Net non-operating income | ($ | 8 | ) | 0.00 | % | $ | 0 | 0.00 | % | ($ | 188 | ) | -0.03 | % | ($ | 155 | ) | -0.02 | % | $ | 23 | 0.00 | % | $ | 632 | 0.09 | % | ||||||||||

| Net income before tax | $ | 3,535 | 0.67 | % | $ | 2,082 | 0.36 | % | $ | 1,252 | 0.18 | % | ($ | 5,024 | ) | -0.73 | % | ($ | 9,691 | ) | -1.42 | % | $ | 789 | 0.12 | % | |||||||||||

| Income tax (expense) benefit | (1,123 | ) | -0.21 | % | (630 | ) | -0.11 | % | (242 | ) | -0.04 | % | 1,895 | 0.27 | % | 3,579 | 0.53 | % | 12 | 0.00 | % | ||||||||||||||||

| Net income (loss) | $ | 2,412 | 0.45 | % | $ | 1,452 | 0.25 | % | $ | 1,010 | 0.15 | % | ($ | 3,129 | ) | -0.45 | % | ($ | 6,112 | ) | -0.90 | % | $ | 801 | 0.12 | % | |||||||||||

| Adjusted Earnings | |||||||||||||||||||||||||||||||||||||

| Net income | $ | 2,412 | 0.45 | % | $ | 1,452 | 0.25 | % | $ | 1,010 | 0.15 | % | ($ | 3,129 | ) | -0.45 | % | ($ | 6,112 | ) | -0.90 | % | $ | 801 | 0.12 | % | |||||||||||

| Add(Deduct): Net gain/(loss) on sale | 8 | 0.00 | % | 0 | 0.00 | % | 188 | 0.03 | % | 155 | 0.02 | % | (23 | ) | 0.00 | % | (632 | ) | -0.09 | % | |||||||||||||||||

| Tax effect (2) | (3 | ) | 0.00 | % | — | 0.00 | % | (75 | ) | -0.01 | % | (62 | ) | -0.01 | % | 9 | 0.00 | % | 253 | 0.04 | % | ||||||||||||||||

| Adjusted earnings | $ | 2,417 | 0.46 | % | $ | 1,452 | 0.25 | % | $ | 1,123 | 0.17 | % | ($ | 3,036 | ) | -0.44 | % | ($ | 6,126 | ) | -0.90 | % | $ | 422 | 0.06 | % | |||||||||||

| Expense Coverage Ratio (3) | 1.34 | 1.15 | 1.10 | 1.14 | 1.05 | 1.03 | |||||||||||||||||||||||||||||||

| Efficiency Ratio (4) | 67.5 | % | 77.4 | % | 79.6 | % | 79.2 | % | 87.5 | % | 87.9 | % | |||||||||||||||||||||||||

| (1) | Ratios are as a percent of average assets. |

| (2) | Assumes a 40.0% effective tax rate. |

| (3) | Expense coverage ratio calculated as net interest income before provisions for loan losses divided by operating expenses. |

| (4) | Efficiency ratio calculated as operating expenses divided by the sum of net interest income before provisions for loan losses plus other income (excluding net gains). |

Sources: Malvern Bancorp’s prospectus, audited & unaudited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.11 |

net interest income ratio during the most recent twelve month period. The slight decline in the net interest income ratio during the most twelve month period reflects some compression in the interest rate spread since fiscal 2011, as yields declined more significantly relative to funding costs. The more significant decrease in interest-earning assets yields was related to a shift in the Company’s interest-earning asset composition towards a higher concentration of relatively lower yielding cash and investments, as well as the lag in less interest-rate sensitive interest-earning assets repricing lower relatively to interest-bearing deposits and borrowings. The Company’s interest rate spread equaled 2.78% during the six months ended March 31, 2012, versus interest rate spreads of 2.17% and 2.93% during fiscal years 2009 and 2011, respectively. The Company’s net interest rate spreads and yields and costs for the period covered in Table 1.1 are set forth in Exhibits I-3 and I-6.

Non-interest operating income has been a fairly stable and somewhat of a limited contributor to the Company’s earnings, reflecting the Company’s limited diversification into products and services that generate sources of non-interest operating income. Throughout the period shown in Table 1.2, sources of non-interest operating income ranged from a low of 0.25% of average assets during fiscal 2011 to a high of 0.32% of average assets during fiscal 2009. For the twelve month ended March 31, 2012, the Company reported non-interest operating income of $2.1 million or 0.31% of average assets. Service charges and fees, rental income and earnings on BOLI constitute the largest sources of non-interest operating income for the Company.

Operating expenses represent the other major component of the Company’s earnings, ranging from a low of 1.91% of average assets during fiscal 2007 to a high of 2.75% of average assets during the twelve months ended March 31, 2012. The comparatively higher operating expense ratios reflected for the past two fiscal years and the most recent twelve month period were largely attributable to higher operating expenses resulting from increases in professional fees incurred to facilitate the work out of problem assets and OREO expenses incurred to maintain and dispose of OREO. Asset shrinkage has also placed upward pressure on the Company’s operating expense ratio over the past one and one-half fiscal years. The increase in capital realized from the stock offering will increase the Company’s capacity to leverage operating expenses through growth of the balance sheet.

Overall, the general trends in the Company’s net interest margin and operating expense ratio since fiscal 2007 reflect a decrease in core earnings, as indicated by the Company’s expense coverage ratio (net interest income divided by operating expenses). Malvern

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.12 |

Bancorp’s expense coverage ratio equaled 1.34 times during fiscal 2007 versus a ratio of 1.03 times during the twelve months ended March 31, 2012. The decrease in the expense coverage ratio resulted from a comparatively larger increase in the operating expense ratio relative to the net interest income ratio. Similarly, Malvern Bancorp’s efficiency ratio (operating expenses, net of amortization of intangibles, as a percent of the sum of net interest income and other operating income) of 67.5% for fiscal 2007 was more favorable than its efficiency ratio of 87.9% for the twelve months ended March 31, 2012.

During the period covered in Table 1.2, loan loss provisions had a varied impact on the Company earnings which was largely related to credit quality trends. Over the past five and one-half fiscal years, loan loss provisions established by the Company ranged from 0.24% of average assets during fiscal 2007 to 1.82% of average asset during fiscal 2011. For the twelve months ended March 31, 2012, provisions for loan losses were $2.4 million or 0.36% of average assets. The lower loan loss provisions established during the most recent twelve month period was supported by a downward trend in non-performing loans since peaking at fiscal year end 2010, as well as the decline in loans outstanding that has been occurring since fiscal year end 2009. As of March 31, 2012, the Company maintained valuation allowances of $8.1 million, equal to 1.73% of net loans receivable and 68.84% of total non-accruing loans. Exhibit I-7 sets forth the Company’s loan loss allowance activity during the past five and one-half fiscal years.

Non-operating income over the past five and one-half years has primarily consisted of gains and losses on the sale of investment securities and OREO. Overall, non-operating income ranged from a net loss of 0.03% of average assets during fiscal 2009 to net gains equal to 0.09% of average assets during the twelve months ended March 31, 2012. Net gains recorded for the most recent twelve month period included gains on the sale of investment securities of $623,000 and gains on the sale of OREO of $9,000. The gain on sale of investment securities was realized from the securitization and sale of $10.7 million of long-term, fixed rate residential loans and $7.6 million of investment securities. The gains and losses realized from the sale of investment securities and OREO are viewed as non-recurring income items and, therefore, are not considered to be part of the Company’s core earnings.

The Company’s effective tax rate ranged from a low of 1.52% during the twelve months ended March 31, 2012 to a high of 37.72% during fiscal 210. As set forth in the prospectus, the Company’s marginal effective statutory tax rate is 40.0%.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.13 |

Interest Rate Risk Management

The Company’s balance sheet is liability-sensitive in the short-term (less than one year) and, thus, the net interest margin will typically be adversely affected during periods of rising and higher interest rates, as well as in the interest rate environment that generally prevailed during 2007, in which the yield curve was flat or inverted. Comparatively, the Company’s interest rate spreads will tend to benefit when short-term interest rates decline and the yield curve steepens. As of March 31, 2012 the Company’s Net Portfolio Value (“NPV”) analysis indicated that a 2.0% instantaneous and sustained increase in interest rates would result in a 2% decline in the Company’s NPV (see Exhibit I-8).

The Company pursues a number of strategies to manage interest rate risk, particularly with respect to seeking to limit the repricing mismatch between interest rate sensitive assets and liabilities. The Company manages interest rate risk from the asset side of the balance sheet through underwriting residential mortgages that will allow for their sale to the secondary market when such a strategy is appropriate, originating 1-4 family ARM loans, diversifying into other types of lending beyond 1-4 family permanent mortgage loans which consist primarily of shorter term and adjustable rate loans, emphasizing investing in securities with maturities of less five than years or with floating rates, maintaining most investments as available for sale and building up liquidity in the prevailing low interest rate environment. As of March 31, 2012, ARM loans comprised 31.5% of total loans (see Exhibit I-9). On the liability side of the balance sheet, management of interest rate risk has been pursued through emphasizing growth of lower cost and less interest rate sensitive transaction and savings account deposits, extending CD maturities through offering attractive rates on certain CDs with maturities of more than one year and utilizing fixed rate FHLB advances with terms out to ten years.

The infusion of stock proceeds will serve to further limit the Company’s interest rate risk exposure, as most of the net proceeds will be redeployed into interest-earning assets and the increase in the Company’s capital position will lessen the proportion of interest rate sensitive liabilities funding assets.

Lending Activities and Strategy

Malvern Bancorp’s lending activities have traditionally emphasized 1-4 family permanent mortgage loans and such loans continue to comprise the major portion of the Company’s loan portfolio. Beyond 1-4 family loans, lending diversification by the Company has emphasized

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.14 |

commercial real estate/multi-family loans followed by consumer loans. Other areas of lending diversification for the Company included construction and land development loans and commercial business loans. During fiscal 2010, the Company discontinued, with certain exceptions, the origination of any new commercial real estate loans, construction loans and land development loans. Pursuant to the terms of the Supervisory Agreements, the Company may not make, invest in or purchase any new commercial real estate loans and/or commercial business loans without the prior written non-objection of the OCC, other than with respect to any refinancing, extension or modification of an existing commercial real estate loan or commercial business loan where no new funds are advanced. Accordingly, the Company’s current lending strategy is to remain primarily a 1-4 family lender, with lending diversification emphasizing consumer loan products. Exhibit I-10 provides historical detail of Malvern Bancorp’s loan portfolio composition over the past five and one-half fiscal years and Exhibit I-11 provides the contractual maturity of the Company’s loan portfolio by loan type as of March 31, 2012.

Malvern Bancorp offers fixed rate and adjustable rate loans for 1-4 family permanent mortgage loans, with terms of up to 30 years. Loans are generally underwritten to secondary market guidelines and the Company’s current philosophy is to retain most originations for investment. In the prevailing interest rate environment, the substantial portion of 1-4 family loans originated by the Company consists of fixed rate loans. ARM loans offered by the Company include loans with repricing terms of one, three or five years and are indexed to U.S. Treasury notes of comparable maturities as the repricing term. After the initial repricing period, ARM loans convert to a one-year ARM loan for the balance of the mortgage term. Fixed rate loans are offered for terms of 10 to 30 years. The Company also offers balloon loans, which are amortized over thirty years and have a five or seven year balloon provision and bi-weekly mortgage loans. As of March 31, 2012, the Company’s outstanding balance of 1-4 family loans equaled $220.2 million or 46.6% of total loans outstanding.

During 2010, the Company generally stopped originating any new construction and land development loans. Previously, construction loans originated by the Company consisted of loans to finance the construction of 1-4 family residences, as well as multi-family and commercial real estate properties. The Company’s 1-4 family construction lending activities consisted of construction financing for construction/permanent loans, as well as financing for speculative loans that are extended to builders. Generally, the Company limited a builder on the number of homes built on speculative basis to two unsold homes (one model home and one speculative home) per development project. Construction loans for the construction of

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.15 |

commercial properties were originated as construction/permanent loans. Construction loans were generally originated as prime rate based loans and required payment of interest only during the construction period. Construction loans were extended up to a loan-to-value (“LTV”) ratio of 80.0%.

The Company also made construction loans for the acquisition and development of land for sale (i.e. roads, sewer and water lines). Acquisition and development construction loans were generally only made in conjunction with a commitment for a construction loan for the units to be built on the site. Acquisition and development construction loans were generally originated as prime rate based loans and required payment of interest only during the construction period. Acquisition and development construction loans were extended up to a LTV ratio of 80.0%. At March 31, 2012, the Company’s largest commercial construction or development loan had an outstanding balance of $3.4 million and was performing in accordance with its terms at March 31, 2012. Malvern Bancorp’s outstanding balance of construction and development loans equaled $21.8 million or 4.6% of total loans outstanding.

Land loans consist substantially of properties that will be used for residential and commercial development. Land loans are typically prime rate based loans that require payment of interest only for terms of up to three years and are extended up to a LTV ratio of 80.0%. As of March 31, 2012, Malvern Bancorp’s outstanding balance of land loans equaled $632,000 or 0.1% of total loans outstanding.

The balance of the mortgage loan portfolio consists of commercial real estate and multi-family loans, which are substantially collateralized by properties in the Philadelphia MSA. During 2010, the Company generally stopped originating any new commercial real estate/multi-family loans. Previously, Malvern Bancorp originated commercial real estate and multi-family loans up to a LTV ratio of 75.0% and required a minimum debt-coverage ratio of 1.2 times. Commercial real estate and multi-family loans were generally extended as ten year notes, with a five year repricing term indexed to the prime rate as published inThe Wall Street Journal. Commercial real estate and multi-family loans generally have amortization terms of up to 25 years. Properties securing the commercial real estate and multi-family loan portfolio include office buildings, retail and industrial use buildings, strip shopping centers, mixed-use properties, medical and professional buildings, churches and apartment buildings. As of March 31, 2012, the Company’s largest commercial real estate/multi-family loan on one property had an outstanding balance of $7.6 million and was performing in accordance with its terms at March

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.16 |

31, 2012. As of March 31, 2012, the Company’s outstanding balance of commercial real estate and multi-family loans totaled $127.5 million or 27.0% of total loans outstanding.

Malvern Bancorp’s diversification into non-mortgage loans consists primarily of consumer loans, with second mortgage loans and home equity lines of credit constituting the major portion of the consumer loan portfolio. Most of the Company’s second mortgage loans are generated through loan brokers operating in southeastern Pennsylvania. Second mortgage loans are offered as fixed or adjustable rate amortizing loans for terms of up to 20 years, while home equity lines of credit have a floating rate tied to the prime rate for terms of up to 20 years. The Bank will originate second mortgage loans and home equity lines of credit up to a LTV ratio of 85.0% when combined with a first mortgage held by the Company and up to an 80.0% LTV ratio when combined with a first mortgage held by any other financial institution. Other than second mortgage loans and home equity lines of credit, consumer lending has been a relatively minor area of lending diversification for the Company, with the balance of the portfolio consisting of various types of installment loans, unsecured personal loans and loans secured by deposits. As of March 31, 2012, the Company’s outstanding balance of consumer loans equaled $93.7 million or 19.9% of total loans outstanding. Second mortgage loans and home equity lines of credit accounted for $72.2 million and $20.7 million of the consumer loan balance, respectively, at March 31, 2012.

During 2010, the Company generally stopped originating any new commercial business loans. Previously, the Company offered commercial business loans and lines of credit to small- and medium-sized companies in its market area. Commercial business loans offered by the Company consisted of fixed rate term loans for terms of up to ten years and floating rate lines of credit indexed to the prime rate as published inThe Wall Street Journal. As of March 31, 2012, the Company’s outstanding balance of commercial business loans equaled $8.7 million or 1.8% of total loans outstanding.

Exhibit I-12 provides a summary of the Company’s lending activities over the past three and one-half fiscal years. Over the past three and one-half fiscal years, total loans originated declined significantly, which was mostly related to decreases in originations of commercial/real estate/multi-family loans and construction and development loans. Total originations declined from $128.5 million during fiscal 2009 to $65.0 million during fiscal 2011 and for the six months ended March 31, 2012 totaled $29.3 million. Originations of 1-4 family permanent mortgage loans accounted for the largest source of originations during the past three and one-half fiscal years ($117.5 million or 38.1% of total loans originated), followed by commercial real

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.17 |

estate/multi-family loans ($75.8 million or 24.6% of total loans originated) and consumer loans ($70.3 million or 22.8% of total loans originated). Loan originations were supplemented with loan purchases totaling $127.4 million during the past three and one-half fiscal years, which consisted substantially of purchases of 1-4 family permanent mortgage loans (total purchases of $77.3 million) and second mortgage loans (total purchases of $49.7 million). Loan purchases reflect loans obtained from the Company’s network of loan brokers, which are classified as “purchased” loans when the broker provides the loan funds at closing and closes the loan in its name. The Company did not sell any loans during the past three and one-half fiscal years. After recording loan growth during fiscal 2009, the Company’s loan portfolio trended lower during the past two and one-half fiscal years as loan originations and purchases were more than offset by loan repayments, transfers of loans to OREO and net loan charge-offs.

Asset Quality

The Company’s historical 1-4 family lending emphasis and lending emphasis on lending in local and familiar markets generally supported maintenance of relatively favorable credit quality measures. However, with the onset of the recession in the Company’s lending markets, the Company experienced credit quality deterioration in its loan portfolio. Over the past five and one-half fiscal years, Malvern Bancorp’s balance of non-performing assets ranged from a low of 0.45% of assets at fiscal year end 2007 to a high of 3.49% of assets at fiscal year end 2010. The Company held $16.5 million of non-performing assets at March 31, 2012, equal to 2.53% of assets. As shown in Exhibit I-13, non-performing assets at March 31, 2012 consisted of $11.7 million of non-accruing loans and $4.7 million of OREO and other foreclosed assets. As of March 31, 2012, non-accruing 1-4 family loans totaling $4.4 million accounted for the largest concentration of the non-accruing loan balance and commercial real estate properties totaling $3.2 million accounted for the largest portion of the OREO and other foreclosed assets balance. The decrease in non-performing assets since fiscal year end 2010 was the result of an $8.1 million reduction in the non-accruing loan balance and a $572,000 reduction in OREO and other foreclosed assets.

To track the Company’s asset quality and the adequacy of valuation allowances, Malvern Bancorp has established detailed asset classification policies and procedures which are consistent with regulatory guidelines. Classified assets are reviewed monthly by senior management and the Board. Pursuant to these procedures, when needed, the Company establishes additional valuation allowances to cover anticipated losses in classified or non-

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.18 |

classified assets. As of March 31, 2012, the Company maintained allowance for loan losses of $8.1 million, equal to 1.73% of net loans receivable and 68.85% of non-accruing loans.

Funding Composition and Strategy

Deposits have consistently served as the Company’s primary funding source and at March 31, 2012 deposits accounted for 91.7% of Malvern Bancorp’s interest-bearing funding composition. Exhibit I-14 sets forth the Company’s deposit composition for the past three and one-half fiscal years. CDs constitute the largest concentration of the Company’s deposit composition, with the concentration of CDs comprising total deposits trending lower since fiscal year end 2010. As of March 31, 2012, the CD portfolio totaled $294.3 million or 54.8% of total deposits, versus comparable measures of $371.6 million and 62.3% of total deposits at year fiscal end 2010. CDs with scheduled maturities of one year or less comprised 38.4% of the Company’s CDs at March 31, 2012. Exhibit I-15 sets forth the maturity schedule of the Company’s CDs as of March 31, 2012. As of March 31, 2012, jumbo CDs (CD accounts with balances of $100,000 or more) amounted to $135.2 million or 46.0% of total CDs. Historically, the Company has not utilized brokered CDs as a funding source.

The Company maintained $242.7 million of savings and transaction account deposits at March 31, 2012, which equaled 45.2% of total deposits. Comparatively, core deposits equaled $225.2 million or 37.7% of total deposits at fiscal year end 2010. Since fiscal year end 2010, interest-bearing demand deposits have been the primary source of the Company’s core deposit growth and comprised the largest concentration of the Company’s core deposits at March 31, 2012, amounting to $95.1 million or 39.2% of core deposits.

Borrowings serve as an alternative funding source for the Company to facilitate management of funding costs and interest rate risk. The Company maintained $48.6 million of borrowings at March 31, 2012 with a weighted average rate of 1.76%. Borrowings held by the Company at March 31, 2012 consisted entirely of FHLB advances, most of which had remaining terms of more than five years.

Subsidiaries

In addition to the Bank, Malvern Bancorp has one subsidiary, Malvern Federal Holdings, Inc., a Delaware corporation organized to hold and manage certain investment securities. The Bank has two subsidiaries, Malvern Federal Investments, Inc., a Delaware corporation

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS I.19 |

organized as an operating subsidiary of the Bank to hold and manage certain investment securities, and Strategic Asset Management Group, Inc. (“SAMG”), a Pennsylvania corporation and insurance brokerage engaged in sales of property and casualty insurance, commercial insurance and life and health insurance. SAMG currently is inactive.

Legal Proceedings

On January 12, 2012, Stilwell Value Partners VI, L.P., withdrew the lawsuit it had previously filed against MLVF, the MHC and each of their directors pursuant to a Praecipe to Discontinue filed in the Court of Common Pleas of Chester County, Pennsylvania.Stilwell Value Partners VI, L.P. v. Hughes, et al. The Company is not presently involved in any legal proceedings of a material nature. From time to time, the Company is a party to legal proceedings incidental to its business, such as suits to enforce its security interest in collateral pledged to secure loans made by the Bank.

| RP® Financial, LC. | MARKET AREA II.1 |

II. MARKET AREA

Introduction

Malvern Bancorp conducts operations out of the headquarters office and eight branch offices in the Pennsylvania counties of Chester and Delaware Counties, which are in located southeastern Pennsylvania, approximately 25 miles west of downtown Philadelphia. The headquarters office and seven branch locations are in Chester County and during 2010 the Company opened its first branch location in Delaware County. Exhibit II-1 provides information on the Company’s office properties.

The Philadelphia MSA is the nation’s sixth largest metropolitan area in terms of total population, with a 2011 population of approximately 6.0 million. The two counties served by the Company’s branches had a total population of approximately 1.1 million in 2011. The Greater Philadelphia area economy is typical of the cities in the northeast corridor, where the traditional manufacturing-based economy has diminished and the service sector has been the primary source of growth. Overall, the Philadelphia MSA maintains a fairly diversified economic base, as traditional employers in the manufacturing and financial services industry have been bolstered by growth in the life sciences and healthcare industries as well as the information technology and communication sectors.

Future growth opportunities for Malvern Bancorp depend on the future growth and stability of the local and regional economy, demographic growth trends, and the nature and intensity of the competitive environment. These factors have been briefly examined to help determine the growth potential that exists for the Company, the relative economic health of the Company’s market area, and the resultant impact on value.

National Economic Factors

The future success of the Company’s operations is partially dependent upon various national and local economic trends. In assessing national economic trends over the past few quarters, manufacturing and non-manufacturing activity continued to expand in October 2011, but at a slower pace compared to September. Jobs data for October continued to imply a slow recovery, with 80,000 jobs added and the unemployment rate ticking down to 9.0%. Economists’ had forecasted a gain of 95,000 jobs for October. Retail sales and the index of leading economic indicators both increased in October. Sales of existing homes were also

| RP® Financial, LC. | MARKET AREA II.2 |

higher in October, but prices continued to decline as a glut of foreclosures kept pressure on home prices. An increase in manufacturing activity during November and a brighter jobs report for November provided further evidence that the recovery was gaining momentum. November employment data showed 120,000 jobs were added and the unemployment rate declined to 8.6%. However, the pace of growth in the service sector was slower in November and November retail sales showed only a modest increase from October. Housing starts surged 9.3% in November, which was fueled by construction of apartments, townhouses and other multi-family properties. Increases in November durable-goods orders and single-family home sales also suggested that the economy was improving. Manufacturing activity expanded at a slightly higher rate in December, as the index which measures manufacturing activity reached a six month high. The pace of non-manufacturing activity picked up as well in December. Employers added 200,000 jobs in December, which pushed the December unemployment rate down to 8.5%. December was the third consecutive month of retail sales showing slower growth and new home construction declined in December. Declining home prices and attractive mortgage rates supported a gain in existing home sales for December. Comparatively, sales of new homes declined in December and for all of 2011 new home sales were the lowest since the Census Bureau began tracking such sales in 1963. A more positive economic outlook was indicated by the 3% increase in December durable-goods orders and fourth quarter GDP increased at a 2.8% annual rate (subsequently revised up to 3.0%), the fastest pace since the second quarter of 2010.