MacKenzie Realty Capital, Inc.

Up to an aggregate of $56,613,094.88 of shares of Series A Preferred Stock

and shares of Series B Preferred Stock

$25.00 Per Share

MacKenzie Realty Capital, Inc. (the “Company”, “us”, “we”, “our” and other similar terms), a Maryland corporation, was formed to generate both current income and capital appreciation through real estate related investments, primarily in debt and equity real estate related securities. As of December 31, 2020, however, we have elected to withdraw our election to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Following withdrawal of the election to be regulated as a BDC, our underlying investment strategy remains very similar to the strategy we have historically followed. We intend to increase our control over our private investments, and to eventually consolidate those investments for financial reporting purposes. We conduct many of our operations through MacKenzie Realty Operating Partnership, LP, a Delaware limited partnership (the “Operating Partnership”). The withdrawal also allows us to expand our investment pool to include real, physical assets, as opposed to only investment securities. We believe that this expanded pool of potential investments will allow access to risk-adjusted returns consistent with our investment objective, while allowing us to maintain our REIT status.

We commenced offering our Series A Preferred Stock, $0.0001 par value per share (the “Series A Preferred Stock”), on November 2, 2021, upon qualification of the offering by the SEC. As of October 31, 2023, we had sold 735,476.21 in shares of our Series A Preferred Stock and were currently offering $56,613,094.88 in shares of our Series A Preferred Stock at $25 per share, which represents the value of shares remaining available to be offered as of October 31, 2023, out of the initial $75 million offered for sale. This Offering Circular is modifying the offering to offer two classes of preferred stock. We are offering to sell up to 3,000,000 shares in the aggregate (less the 735,476.21 shares that had been sold as of October 31, 2023) of either Series A Preferred Stock or Series B Preferred Stock, $0.0001 par value per share (the “Series B Preferred Stock”), of the Company. The minimum purchase requirement per investor is $5,000 in preferred shares; however, we can waive the minimum purchase requirement in our sole discretion. The primary difference between the two series is that the Series A Preferred Stock is entitled to receive dividends at the rate of 6% per annum, whereas the Series B Preferred Stock is entitled to receive dividends at the rate of 12% per annum, with 3% expected to be paid quarterly on the applicable dividend payment date and 9% to accrue for payment at the same time and in the same amounts per share with distributions paid on the Common Stock, beginning once holders of Common Stock have initially received distributions equal to 10% per annum from and after December 31, 2022 on the $7.38 per share net asset value (“NAV”) of the common stock as of such date, and the remainder of which will be paid no later than at redemption, liquidation or conversion. The sale of shares pursuant to this offering is expected to continue until we raise the maximum amount being offered, unless terminated by us at an earlier time in the discretion of our Board of Directors. Of the total, 2,700,000 shares are being sold through the primary offering and 300,000 shares are being sold through our dividend reinvestment program.

We are externally managed by MacKenzie Capital Management, LP, a California limited partnership, or the “Manager”. We are advised, as to our real estate investments, by an affiliate of the Adviser, MacKenzie Real Estate Advisers, LP (the “Real Estate Adviser”), and as to our securities portfolio, by MCM Advisers, LP (the “Investment Adviser”; together with the Real Estate Adviser, the “Advisers” or “Adviser”). These Advisers will make all investment decisions for us. Our Advisers intend to employ a variety of acquisition strategies in building our portfolio of investments, with a particular focus on obtaining properties in off-market transactions, work-out deals, Real Estate Owned (“REO”) properties, “creeping acquisitions” of controlling interests in securities, and similar transactions. We have elected to be taxed, and currently, as of calendar year end December 31, 2022, qualify, as a REIT for U.S. federal income tax purposes.

We do not intend to list our preferred shares for trading on a stock exchange or other trading market, however, the Board intends to apply for listing of our common stock sometime after October 2024.

Investing in our preferred shares involves a high degree of risk. See “Risk Factors” beginning on page 12 of this Offering Circular for a discussion of the risks that should be considered in connection with your investment in our shares. These risks include, but are not limited to, the following:

| • | There is no assurance that we will be able to successfully achieve our investment objectives. |

| • | Investors will not have the opportunity to evaluate or approve any Investments prior to our acquisition or financing thereof. |

| • | Investors will rely solely on the Adviser to manage us and our Investments. The Adviser will have broad discretion to invest our capital and make decisions regarding Investments. |

| • | We may not be able to invest the net proceeds of this offering on terms acceptable to investors, or at all. |

| • | Investors will have limited control over changes in our policies and day-to-day operations, which increases the uncertainty and risks you face as an investor. In addition, our Board of Directors may approve changes to our policies, including our policies with respect to distributions and redemption of shares without prior notice or your approval. |

| • | An investor could lose all or a substantial portion of any investment made in us. |

| • | There is no public trading market for our preferred shares, and we are not obligated to effectuate a liquidity event or a listing of our preferred shares on any nationally recognized stock exchange by a certain date or at all. It will thus be difficult for an investor to sell shares purchased from us. |

| • | We may fail to maintain our qualification as a REIT for federal income tax purposes. We would then be subject to corporate level taxation and regulation as an investment company and we would not be required to pay any distributions to our stockholders. |

| • | The offering price of our shares was not established based upon any appraisals of assets we own or may own. Thus, the initial offering price may not accurately reflect the value of our assets at the time an investor’s investment is made. |

| • | Substantial actual and potential conflicts of interest exist between our investors and our interests or the interests of our Adviser, and our respective affiliates, including conflicts arising out of (a) allocation of personnel to our activities, (b) allocation of investment opportunities between us, and (c) potential conflicts arising out of transactions between us, on the one hand, and our Adviser and its affiliates, on the other hand, involving compensation and incentive fees payable to our Adviser or dealings in real estate transactions between us and the Adviser and its affiliates. |

| • | There are substantial risks associated with owning, financing, operating, leasing, and managing real estate. |

| • | The amount of distributions we make is uncertain. We may fund distributions from offering proceeds, borrowings, and the sale of assets, to the extent distributions exceed our earnings or cash flows from our operations if we are unable to make distributions from our cash flows from operations. There is no limit on the amount of offering proceeds we may use to fund distributions. Distributions paid from sources other than cash flow or funds from operations may constitute a return of capital to our stockholders. Rates of distributions may not be indicative of our actual operating results. For example, on March 31, 2020, after assessing the impacts of the COVID-19 pandemic, our Board of Directors unanimously approved the suspension of regular quarterly dividends to our common stockholders. On May 10, 2021, the Board of Directors reinstated the quarterly dividend at the rate of $0.05 per common share, which was increased to $0.06, $0.07, $0.08, $0.09, $0.10, $0.11, $0.115, $0.12, and $0.125 cents per common share in the nine quarters thereafter, respectively. While the Series A Preferred Stock will accrue a 6% dividend, payment of this dividend is not guaranteed, only that it will be paid before any cash dividend may be paid to the holders of common shares. While the Series B Preferred Stock will accrue a 3% dividend, payment of this dividend is not guaranteed, only that it will be paid before any cash dividend may be paid to the holders of common shares, and the additional accrued 9% dividends on the Series B Preferred Stock will start being paid at the same time and in the same amount per share with distributions paid on the Common Stock once the holders of common stock have initially received distributions equal to 10% per annum from and after December 31, 2022 on the $7.38 per share net asset value per share for the common stock as of such date, and the remaining amounts (if any) will be paid no later than at redemption, liquidation or conversion. |

ii

The SEC does not pass upon the merits of or give its approval to any securities offered or the terms of the offering, nor does it pass upon the accuracy or completeness of any offering circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the SEC; however, the SEC has not made an independent determination that the securities offered are exempt from registration.

The use of projections or forecasts in this offering is prohibited. No one is permitted to make any oral or written predictions about the cash benefits or tax consequences you will receive from your investment in shares of our common stock.

| Per Share | Total Maximum | |

Offering Price (1) | $25.00 | $56,613,094.88(2) |

Underwriting Discounts and Commissions (3) | $2.50 | $5,661,309.49 |

Proceeds to Us from this Offering (Before Expenses) (4) | $22.50 | $50,951,785.39 |

1. The price per share has been arbitrarily determined by our Adviser to be $25.00 per share.

2. This is a “best efforts” offering of an aggregate of $67,500,000 of shares of preferred stock in the primary offering and $7,500,000 of shares of preferred stock through the dividend reinvestment program. See “Plan of Distribution” and “Series A and B Preferred Stock Dividend Reinvestment Program.”

3. We will pay selected brokers (the “Selling Agents”) a sales load of 7.0% of the offering price, which load is reduced based on the number of shares purchased from a Selling Agent, and we will also pay our dealer manager, Arete Wealth Management, LLC (“Arete”), a dealer manager fee of up to 1.9% of the offering price (the “Dealer Adviser Fee”). If shares are purchased through investment advisers, we will only pay the Dealer Adviser Fee to Arete, and no commissions will be payable. For purposes of the table, we have assumed a sales charge of 7.0%. To the extent purchasers qualify for the volume discounts or purchase through certain investment advisory accounts, the sales load amount shown in the table would be less. Selling Agents will also receive a marketing support fee of 1.1% of the offering price from us (the “Marketing Support Fee”) to assist the Selling Agents in covering their costs for the marketing of the preferred shares. For purchases through certain investment advisory accounts, Arete will only receive the 1.9% Dealer Adviser Fee in lieu of commissions and no Marketing Support Fee will be paid. The total amount of all items of compensation from any source, payable to underwriters, broker-dealers or affiliates thereof will not exceed an amount that equals 10.0% of the gross proceeds of the offering. See “Arrangements with Dealer Adviser and Selected Broker Dealers.”

4. We estimate that we will incur approximately $1,500,000 in costs in connection with this offering (not including any costs or expenses incurred in connection with the prior offerings of common stock and not including legal fees). We have already paid or accrued $1,185,305 for the offering through the date hereof (not including any costs or expenses incurred in connection with the prior offering of common stock.) All amounts over $825,000 (not including legal fees), however, will be reimbursed by our Advisers, except to the extent the full 10.0% in broker fees described above are not incurred. In such case, the difference will be available to be paid or reimbursed by us to brokers for marketing expenses or other non-cash compensation.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

This Offering Circular uses the SEC Registration Statement on Form S-11 disclosure format.

The mailing address of our principal executive offices is:

MacKenzie Realty Capital, Inc.

89 Davis Road, Suite 100

Orinda, CA 94563

Attn: Investor Relations

Our telephone number is 1.800.854.8357 and our website address is www.mackenzierealty.com. You may direct inquiries to: investors@mackenziecapital.com.

This Offering Circular is dated November 14, 2023.

iii

IMPORTANT INFORMATION ABOUT THIS OFFERING CIRCULAR

Please carefully read the information in this Offering Circular and any accompanying Offering Circular supplements, which we refer to collectively as the Offering Circular. You should rely only on the information contained in this Offering Circular. We have not authorized anyone to provide you with different information. This Offering Circular may only be used where it is legal to sell these securities. You should not assume that the information contained in this Offering Circular is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This Offering Circular is part of an offering statement that we filed with the SEC, using a continuous offering process. Periodically, as we make material investments, update our NAV per share amount, or have other material developments, we will provide an Offering Circular Supplement that may add, update or change information contained in this Offering Circular. Any statement that we make in this Offering Circular will be modified or superseded by any inconsistent statement made by us in a subsequent Offering Circular Supplement. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this Offering Circular. You should read this Offering Circular and the related exhibits filed with the SEC and any Offering Circular Supplement, together with additional information contained in our annual reports, quarterly reports and other reports and information statements that we will file periodically with the SEC. See the section entitled “Additional Information” below for more details.

The offering statement and all supplements and reports that we have filed or will file in the future can be read at the SEC website, www.sec.gov, or on our website, www.mackenzierealty.com. The contents of our website (other than the offering statement, this Offering Circular and the appendices and exhibits thereto) are not incorporated by reference in or otherwise a part of this Offering Circular.

Our Adviser and those selling shares on our behalf in this offering will be permitted to make a determination that the purchasers of shares in this offering are “qualified purchasers” in reliance on the information and representations provided by the shareholder regarding the shareholder’s financial situation. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

STATE LAW EXEMPTION AND INVESTOR REQUIREMENTS

Our preferred shares will be offered and sold only to purchasers who meet the Company’s Suitability Standards (as defined below) and are “qualified purchasers” (as defined in Regulation A). As a Tier 2 offering pursuant to Regulation A, this offering will be exempt from state law “Blue Sky” review, subject to meeting certain state filing requirements and complying with certain anti-fraud provisions, to the extent that our preferred shares offered hereby are offered and sold only to “qualified purchasers” or at a time when our shares are listed on a national securities exchange.

The preferred shares are offered only to purchasers who meet the requirements set forth in Section 10.5 of the Company’s Charter (the “Company’s Suitability Standard”), which require that the purchaser have, at the time of acquisition of the preferred shares, either at least an annual gross income of $70,000 and a net worth of at least $70,000, or a minimum net worth of $250,000. (For these purposes, “net worth” is determined exclusive of the purchaser’s home, home furnishings and automobiles.)

The preferred shares are offered only to “Qualified Purchasers”, which include: (i) “accredited investors” under Rule 501(a) of Regulation D and (ii) all other investors so long as their investment in our preferred shares does not represent more than 10% of the greater of their annual income or net worth (for natural persons), or 10% of the greater of annual revenue or net assets at fiscal year-end (for non-natural persons). We reserve the right to reject any investor’s subscription in whole or in part for any reason, including if we determine in our sole and absolute discretion that such investor is not a “qualified purchaser” for purposes of Regulation A.

Generally, no sale may be made to you in this offering if (a) excluding the value of your home, furnishings and automobiles, you do not have either (i) a net worth of more than $250,000 or (ii) a gross annual income of at least $70,000 and a net worth of at least $70,000, and (b) the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply for purposes of the Regulation A investor qualification requirement to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to investor.gov.

For more detailed information regarding investor requirements see “Investment Limitations” on page 36 of this Offering Circular.

Please carefully read the information in this Offering Circular and any accompanying Offering Circular supplements, which we refer to collectively as the Offering Circular. You should rely only on the information contained in this Offering Circular. We have not authorized anyone to provide you with different information. This Offering Circular may only be used where it is legal to sell these securities. You should not assume that the information contained in this Offering Circular is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This Offering Circular is part of an offering statement that we filed with the SEC, using a continuous offering process. Periodically, as we make material investments, update our NAV per share amount, or have other material developments, we will provide an Offering Circular Supplement that may add, update or change information contained in this Offering Circular. Any statement that we make in this Offering Circular will be modified or superseded by any inconsistent statement made by us in a subsequent Offering Circular Supplement. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this Offering Circular. You should read this Offering Circular and the related exhibits filed with the SEC and any Offering Circular Supplement, together with additional information contained in our annual reports, quarterly reports and other reports and information statements that we will file periodically with the SEC. See the section entitled “Additional Information” below for more details.

The offering statement and all supplements and reports that we have filed or will file in the future can be read at the SEC website, www.sec.gov, or on our website, www.mackenzierealty.com. The contents of our website (other than the offering statement, this Offering Circular and the appendices and exhibits thereto) are not incorporated by reference in or otherwise a part of this Offering Circular.

Our Adviser and those selling shares on our behalf in this offering will be permitted to make a determination that the purchasers of shares in this offering are “qualified purchasers” in reliance on the information and representations provided by the shareholder regarding the shareholder’s financial situation. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

STATE LAW EXEMPTION AND INVESTOR REQUIREMENTS

Our preferred shares will be offered and sold only to purchasers who meet the Company’s Suitability Standards (as defined below) and are “qualified purchasers” (as defined in Regulation A). As a Tier 2 offering pursuant to Regulation A, this offering will be exempt from state law “Blue Sky” review, subject to meeting certain state filing requirements and complying with certain anti-fraud provisions, to the extent that our preferred shares offered hereby are offered and sold only to “qualified purchasers” or at a time when our shares are listed on a national securities exchange.

The preferred shares are offered only to purchasers who meet the requirements set forth in Section 10.5 of the Company’s Charter (the “Company’s Suitability Standard”), which require that the purchaser have, at the time of acquisition of the preferred shares, either at least an annual gross income of $70,000 and a net worth of at least $70,000, or a minimum net worth of $250,000. (For these purposes, “net worth” is determined exclusive of the purchaser’s home, home furnishings and automobiles.)

The preferred shares are offered only to “Qualified Purchasers”, which include: (i) “accredited investors” under Rule 501(a) of Regulation D and (ii) all other investors so long as their investment in our preferred shares does not represent more than 10% of the greater of their annual income or net worth (for natural persons), or 10% of the greater of annual revenue or net assets at fiscal year-end (for non-natural persons). We reserve the right to reject any investor’s subscription in whole or in part for any reason, including if we determine in our sole and absolute discretion that such investor is not a “qualified purchaser” for purposes of Regulation A.

Generally, no sale may be made to you in this offering if (a) excluding the value of your home, furnishings and automobiles, you do not have either (i) a net worth of more than $250,000 or (ii) a gross annual income of at least $70,000 and a net worth of at least $70,000, and (b) the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply for purposes of the Regulation A investor qualification requirement to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to investor.gov.

For more detailed information regarding investor requirements see “Investment Limitations” on page 36 of this Offering Circular.

iv

This offering summary highlights the information contained elsewhere in this Offering Circular. Because it is a summary, it may not contain all the information that you should consider before investing in our shares. To fully understand this offering (the “Offering”), you should carefully read this entire Offering Circular, including the more detailed information set forth under the caption “Risk Factors.” Unless the context otherwise requires or indicates, references in this Offering Circular to “us,” “we,” “our” or “our company” refer to MacKenzie Realty Capital, Inc., a Maryland corporation.

MacKenzie Realty Capital, Inc.

MacKenzie Realty Capital, Inc. was formed as of January 27, 2012, as a Maryland corporation, and we are taxed as a REIT for federal income tax purposes. Our objective is to acquire and develop a portfolio of mainly institutional-quality apartment communities and office properties across the United States.

We were formed to generate both current income and capital appreciation through real estate related investments, primarily in debt and equity real estate related securities. As of December 31, 2020, however, we elected to withdraw our election to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Following withdrawal of the election to be regulated as a BDC, we have and intend to continue to invest in private companies that directly or indirectly own real property, and increase our control over our private investments, and to eventually consolidate those investments for financial reporting purposes. We conduct many of our operations through MacKenzie Realty Operating Partnership, LP, a Delaware limited partnership (the “Operating Partnership”). The withdrawal of our BDC election has also allowed us to expand our investment pool to include real, physical assets, as opposed to only investment securities. We believe that this expanded pool of potential investments allows access to risk-adjusted returns consistent with our investment objective, while allowing us to maintain our REIT status.

We utilize three key investment strategies — Value-Add, Opportunistic, and Invest-to-Own — to drive growth in funds from operations and net asset value at our properties, in order to maximize returns to our investors.

We invest primarily through controlling positions (generally 90%) in joint ventures with our network of some of the leading private regional apartment owner/operators across the nation, which we believe enhances our ability to access proprietary off-market transactions, and to deliver best-in-class execution of multiple investment strategies across a substantial number of markets. Upon execution of the initial business plan for the property, we will often seek to increase our ownership to 100%, so that the property will be wholly owned by us.

As of the date of this Offering Circular, our portfolio consisted of (a) 5 commercial real estate properties: First & Main, LP, 1300 Main, LP, Main Street West, LP, all in Napa, CA, Woodland Corporate Center Two, LP, in Woodland, CA, and MacKenzie Satellite Place in Duluth, GA, and (b) 4 residential apartment properties: Commodore Apartments and The Park View (Formerly known as Pon De Leo Apartments), located in Oakland, CA, the Hollywood Property located in Los Angeles, CA, and the Shoreline Apartments in Concord, CA.

First & Main, 1300 Main, Main Street West, Woodland Corporate Center Two, and the Hollywood Property are owned through our subsidiary, the Operating Partnership, the Commodore Apartments are owned through our subsidiary Madison, the The Park View (f/k/a Pon De Leo Apartments) is owned through our subsidiary PVT, the Shoreline Apartments are owned through our subsidiary BAA-Shoreline, and MacKenzie Satellite Place is owned through our subsidiary MacKenzie Satellite Place, Inc. We also own 6 minority interests in non-traded REITs, 4 general partnership interests in commercial properties, and 4 other real estate investments.

Our primary intent is to purchase real estate interests, whether direct investments, joint ventures, minority interests, or loans secured by real estate. We refer to our investments in real property as “Investments”.

REIT Status

We are currently treated as a REIT for federal income tax purposes. As long as we maintain our qualification as a REIT, we generally will not be subject to federal income or excise tax on income that we distribute to our shareholders.

Under the Internal Revenue Code of 1986, as amended (the “Code”), a REIT is subject to numerous organizational and operational requirements, including a requirement that it annually distribute at least 90% of its REIT taxable income (determined without regard to the deduction for dividends paid and excluding net capital gain) to its shareholders.

If we fail to maintain our qualification as a REIT in any year, our income will be subject to federal income tax at regular corporate rates, regardless of our distributions to shareholders, and we may be precluded from qualifying for treatment as a REIT for the four-year period immediately following the taxable year in which such failure occurs.

Even if we qualify for treatment as a REIT, we may still be subject to state and local taxes on our income and property and to federal income and excise taxes on our undistributed income.

Investment Company Act Considerations

We intend to conduct our operations so that we will not be required to register as an investment company under the Investment Company Act.

Management

Company is Externally Managed

We are externally managed by MacKenzie Capital Management, LP, a California limited partnership or the “Manager” and advised as to our real estate investments by its affiliate MacKenzie Real Estate Advisers, LP (“Real Estate Adviser”) and as to any securities by MCM Advisers, LP (“Investment Adviser”) (together, the “Advisers” or “Adviser”). The Advisers will make all investment decisions for us. The Advisers’ principals and their respective affiliates specialize in acquiring, repositioning (where applicable) and managing commercial real estate and related securities.

The Advisers intend to apply this experience to identify suitable Investments and to present an opportunity for outside investors to take advantage of the principals’ experience through a pooled investment vehicle.

The Advisers will oversee our overall business and affairs and will have broad discretion to make operating decisions on our behalf and to make Investments. Our shareholders will not be involved in our day-to-day affairs.

Experienced Management Team

Our management team has significant real estate experience, which includes experience in acquisition, management, leasing, sales, development, and financing of multiple properties. Overall, our management team has 100+ years combined experience in the real estate business as portfolio managers, owners, lessors, and Realtors. Our management team has relevant experience in managing private and public investment funds which invested in real estate securities, but not directly in real estate. Our management team manages and advises one other real estate fund with similar investment objectives and strategies to us: MacKenzie REIT, Inc. (“MREIT”), which is a private REIT that owns an office building, a grocery-anchored shopping mall, and an office and research and development park, along with various other real estate assets. MREIT is an entity that resulted from the merger of two older limited partnerships sponsored by unaffiliated sponsors (including Concord Milestone Plus, LP which raised funds in 1987, which became CMP Old Orchard, LP, and New Orleans Associates Limited Partnership which raised funds in 1987). However, that entity is not currently public, is not currently raising capital to make new investments, and generally focuses on income-producing properties rather than growth opportunities. Further, the Advisers and the management team do not have any experience raising and investing other people’s money into direct ownership of real estate, but have extensive experience investing on behalf of affiliates and themselves. We will not compensate our management team; they will receive renumeration through their employment by and ownership in our Advisers.

Management Compensation

Our Advisers and their affiliates will receive fees and expense reimbursements for services relating to this Offering and the investment and management of our assets. The items of compensation are summarized in the following table. Neither of our Advisers nor their affiliates will receive any selling commissions or dealer manager fees in connection with the offer and sale of our preferred shares.

We do not have an agreement to limit any losses suffered by our Advisers or the Manager.

The projected compensation laid out below relates to all stages of our company, including offering stage, organizational stage, acquisition stage, and liquidation stage.

Asset Management Fee: | The asset management fee is calculated based on our “Invested Capital.” The asset management fee is payable monthly at an annual rate of 3% of the first $20 million in Invested Capital, 2% of the next $80 million in Invested Capital and 1.5% of Invested Capital over $100 million. “Invested Capital” is calculated by multiplying the total net number of Shares, Preferred Shares, and Partnership Units (units in our operating partnership issued by persons other than us) by the price paid for each or the value ascribed to each in connection with their issuance and is not derived from the value of our assets from time to time. There are currently 85,243.43 common Partnership Units outstanding not owned by us and 473,570.94 Series A Preferred Partnership Units not owned by us. The Asset Management Fee compensates our Adviser for managing all of our assets. The Real Estate Adviser and the Investment Adviser will allocate this fee between themselves. In the fiscal year ending June 30, 2024, we expect to pay our Adviser approximately $3,300,000 in Asset Management Fees. |

Acquisition Fees: | The Acquisition Fees are equal to 2.5% of the cost of the asset acquired. These are paid on acquisition of non-securities to our Adviser. Purchases of securities do not incur this fee. However, to the extent that such asset is not held for at least 5 years, any acquisition fee for subsequent purchases using proceeds from the sale of such asset will be reduced proportionally. These fees compensate our Adviser for traveling to and researching properties that are suitable for investment. In the fiscal year ending June 30, 2024, we expect to pay our Adviser approximately $2,000,000 in Acquisition Fees. |

Debt Financing Fee, Disposition Fee, Property Management Fee | We do not pay any such fees to our Adviser, but do anticipate paying debt financing and property management fees to unaffiliated third parties. We expect to pay property management fees based upon prevailing market rates, but most such fees will be paid by the entities that own a property. PVT-Madison Partners, LLC and Madison-PVT Partners, LLC pay their third-party property management firm a fee equal to 6% of gross collected revenue from such properties. Hillview Hollywood pays its third-party property manager 4% of gross revenue, subject to a minimum $2,500 monthly fee. MacKenzie Shoreline pays its third-party property management firm 4% of gross collected revenue. We pay an affiliate of our adviser, Wiseman Commercial, Inc., property management fees equal to 5% of gross collected revenue for the Wiseman Properties (as defined below). We have not yet paid any debt financing fees, but our understanding of the market rates for such services lead us to believe that such fees would usually be in the range of 0.5% to 1% of the amount of the loan, depending upon the size of the loan. |

Incentive Management Fee: | Once common stockholders have received distributions equal to 6% per annum on their Invested Capital, from and after January 1, 2021, the Real Estate Adviser will be entitled to receive an incentive management fee equal to an amount that would result in the Adviser having received 15% of all distributions not attributable to the securities we own or to any return of capital. Because common stockholders will not receive distributions before certain distributions are paid on preferred shares, no such fee can be paid to the Adviser unless all required distributions have been paid on the preferred shares. The Incentive Management Fee compensates our Adviser based upon the performance of the assets in which we invest. It is impracticable to determine the amount of Incentive Management Fees that will be paid in the next year, although we estimate than none will be paid. |

Expense Reimbursements | In addition to the compensation paid to the Adviser above, we shall reimburse the Adviser and/or its Affiliates for all of the costs and expenses paid or incurred by the Adviser that are in any way related to our operations or our business or the services the Adviser provides to us pursuant to the Advisory Agreement, including, but not limited to: organization and offering expenses; expenses of managing and operating Assets owned by us, whether payable to an Affiliate of us or a non-Affiliated Person; expenses connected with payments of distributions in cash or otherwise made or caused to be made by us to the stockholders; expenses of organizing, reorganizing, liquidating, or dissolving us and the expenses of filing or amending the Articles of Incorporation or Articles Supplementary establishing the terms of any preferred stock; transfer agent expenses, and related software development costs, for the shares and of maintaining communications with stockholders, including the cost of preparation, printing, and mailing annual reports and other stockholder reports, proxy statements and other reports required by governmental entities; administrative service expenses (including salary, benefits, and overhead costs of Affiliates and certain of the executive officers of us, based upon the amount of time they spend on Company business other than providing investment advice, as approved by Board); and audit, accounting, and legal fees. |

Conflicts of Interest

Our officers and directors, and the owners and officers of our Adviser and its affiliates are involved in, and will continue to be involved in, the ownership and advising of over 100 other real estate entities and programs, the vast majority of which are low-income housing projects. Only one other such entity has investment objectives similar to us—MREIT, a private real estate investment trust advised by the Adviser. Our Board, however, is independent from MREIT, and only Mr. Patterson is a director of both us and MREIT. Two of our 3 directors are independent. MREIT owns an office building, a grocery-anchored shopping mall, and an office and research and development park, along with various other real estate assets. However, it is not currently public, is not currently raising capital to make new investments, and generally focuses on income-producing properties rather than growth opportunities. Our sponsor and advisers have committed to providing us with the first chance at any investment opportunities so long as we have new capital to invest.

These pre-existing interests, and similar additional interests as may arise in the future, may give rise to conflicts of interest with respect to our business, our investments, and our investment opportunities. It is possible that investment opportunities may arise that would be appropriate for both us and one of the other real estate funds that is managed or advised by our Adviser. In such a case, it will be the responsibility of the Board and the Adviser to resolve that potential conflict.

We are subject to various conflicts of interest arising out of our relationship with our advisers and affiliates, including conflicts related to the arrangements pursuant to which our advisers and affiliates will be compensated by us. The agreements and compensation arrangements between us and our advisers and affiliates were not determined by arm’s-length negotiations. See the “Management Compensation” section of this Offering Circular above. Some of the conflicts of interest in our transactions with our advisers and affiliates, and the limitations on our advisers adopted to address these conflicts, are described below.

Our advisers and affiliates try to balance our interests with their duties to other programs sponsored by our sponsor and its affiliates. However, to the extent that our advisers or their affiliates take actions that are more favorable to other entities than to us, these actions could have a negative impact on our financial performance and, consequently, on distributions to our stockholders and the value of our stock. In addition, our directors, officers and certain of our stockholders may engage for their own account in business activities of the types conducted or to be conducted by us and our subsidiaries. For a description of some of the risks related to these conflicts of interest, see the section of this Offering Circular captioned “Risk Factors — Risks Related to Conflicts of Interest.”

Our independent directors have an obligation to serve on our behalf in all situations in which a conflict of interest may arise, and all of our directors have a fiduciary obligation to act on behalf of our stockholders.

Interests in Other Real Estate Programs

Affiliates of our advisers have sponsored numerous private real estate programs, but none with similar investment objectives to us other than MREIT because no other such programs raise capital from investors to invest in commercial real estate properties (all other programs that have raised capital from investors have invested in real estate securities or low-income housing projects). MREIT employs a similar investment strategy and has acquired or plans to acquire assets similar to ours and non-traded REIT shares. The common investment strategy used by MREIT would permit it to purchase certain properties that may also be suitable for our portfolio.

MREIT’s primary investment strategy is to invest in stabilized, income-producing properties but may also invest in opportunistic growth opportunities and non-traded REITs, similar to properties in which we invest. Other private funds advised by our advisers may purchase non-traded REITs and other fractionalized real property interests. Our advisers do not advise any other real estate programs which target the purchase of properties, however.

Affiliates of our officers and entities owned or managed by such affiliates also may acquire or develop real estate for their own accounts, and have done so in the past. Furthermore, affiliates of our officers and entities owned or managed by such affiliates intend to form additional real estate investment entities in the future, whether public or private, which can be expected to have the same investment objectives and policies as we do and which may be involved in the same geographic area, and such persons may be engaged in sponsoring one or more of such entities at approximately the same time as our shares of common or preferred stock are being offered. Our Advisers and affiliates of our officers are not obligated to present to us any particular investment opportunity that comes to their attention, even if such opportunity is of a character that might be suitable for investment by us. Our Advisers and affiliates likely will experience conflicts of interest as they simultaneously perform services for us and other affiliated real estate programs.

Any affiliated entity, whether or not currently existing, could compete with us in the sale or operation of our properties. We will seek to achieve any operating efficiency or similar savings that may result from affiliated management of competitive properties. However, to the extent that affiliates own or acquire a property that is adjacent, or in close proximity, to a property we own, our property may compete with the affiliate’s property for tenants or purchasers.

Every transaction that we enter into with our Advisers or their affiliates is subject to an inherent conflict of interest. Our board of directors may encounter conflicts of interest in enforcing our rights against any affiliate in the event of a default by or disagreement with an affiliate or in invoking powers, rights or options pursuant to any agreement between us and our Advisers or any of their affiliates.

Other Activities of Our Advisers and affiliates

We rely on our Advisers for the day-to-day operation of our business pursuant to our advisory agreements. As a result of the interests of members of our Advisers’ management in other programs and the fact that they have also engaged and will continue to engage in other business activities, our Advisers and affiliates will have conflicts of interest in allocating their time between us and other programs and other activities in which they are involved. However, our Advisers believe that they and their affiliates have sufficient personnel to discharge fully their responsibilities to all of such programs and other ventures in which they are involved.

In addition, a majority of our executive officers also serve as an officer of our Advisers or other affiliated entities. As a result, these individuals owe fiduciary duties to these other entities, which may conflict with the fiduciary duties that they owe to us and our stockholders.

We may purchase properties or interests in properties from affiliates of our Advisers. The prices we pay to affiliates of our Advisers for these properties will not be the subject of arm’s-length negotiations, which could mean that the acquisitions may be on terms less favorable to us than those negotiated with unaffiliated parties. However, the price must be approved by a majority of our directors, including a majority of our independent directors, who have no financial interest in the transaction. If the price to us exceeds the cost paid by our affiliate, our board of directors must determine that there is substantial justification for the excess cost. Additionally, we may sell properties or interests in properties to affiliates of our Advisers. The prices we receive from affiliates of our Adviser for these properties will not be the subject of arm’s-length negotiations, which could mean that the dispositions may be on terms less favorable to us than those negotiated with unaffiliated parties.

Competition in Acquiring, Leasing and Operating Properties

Conflicts of interest will exist to the extent that we may acquire properties in the same geographic areas where properties owned by other programs, including those sponsored by our sponsor’s affiliates are located. In such a case, a conflict could arise in the leasing of properties in the event that we and another program, including another program sponsored by our sponsor or its affiliates were to compete for the same tenants, or a conflict could arise in connection with the resale of properties in the event that we and another program, including another program sponsored by our sponsor or its affiliates were to attempt to sell similar properties at the same time. Conflicts of interest may also exist at such time as we or our affiliates managing a property on our behalf seek to employ developers, contractors or building managers, as well as under other circumstances.

Affiliated Property Manager

When we acquired the “Wiseman Portfolio,” consisting of the general partnership interests in 8 limited partnerships owning Class A or B office buildings in Napa, Woodland, Fairfield, and Suisun City, CA, our Adviser agreed to purchase the assets of the property management firm that managed the properties, which is now known as Wiseman Commercial, Inc. (“Wiseman”). Wiseman continues to manage the leasing, construction, and property for each of the Wiseman Portfolio properties under the same terms as they were previously managed. The Board has reviewed the terms of the management contracts and will continue to review the terms of such agreements to attempt to ensure that we are paying market rates for appropriate services.

Affiliated Transfer Agent

Our officers are also officers and indirect owners of our transfer agent, which is a registered transfer agent with the SEC. The services our transfer agent provides are substantially similar to what a third-party transfer agent would provide in the ordinary course of performing its functions as a transfer agent, including, but not limited to: providing customer service to our stockholders, processing the distributions and any servicing fees with respect to our shares and issuing regular reports to our stockholders. Our transfer agent may retain and supervise third-party vendors in its efforts to administer certain services. We believe that our transfer agent, through its knowledge and understanding of the direct participation program industry which includes non-traded REITs, is particularly suited to provide us with transfer agent and registrar services. Our transfer agent also conducts transfer agent and registrar services for MREIT, as well as other programs sponsored by our sponsor. Our Board of Directors has approved the terms of the transfer agent agreement, which provides for no compensation to be paid to the transfer agent, but only a reimbursement of software development costs.

It is the duty of our board of directors to evaluate the performance of our transfer agent. In addition, we will reimburse our transfer agent for all reasonable expenses or other changes incurred by it in connection with the provision of its services to us. Upon the request of our transfer agent, we may also advance payment for substantial reasonable out-of-pocket expenditures to be incurred by it.

Receipt of Fees and Other Compensation by Our Advisers and Affiliates

Our Advisers and affiliates receive substantial fees from us. See “Management Compensation.” Some of these fees are paid to our Advisers and affiliates regardless of the success or profitability of the property. Specifically, our Advisers and affiliates receive:

| • | acquisition fees upon any acquisition, regardless of whether the property will be profitable in the future; |

| • | asset management fees based on the Invested Capital, and not based on performance of our properties; and |

| • | subordinated incentive management fee equal to 15% of profits, payable only after the 6% return to stockholders. |

Although the acquisition and asset management fees are paid regardless of success or profitability of a property, our independent directors must approve all significant acquisitions or affiliated transactions as being in the best interests of us and our stockholders. Further, if our independent directors determine that the performance of our Advisers is unsatisfactory or that the compensation to be paid to our Advisers is unreasonable, the independent directors may take such actions as they deem to be in the best interests of us and our stockholders under the circumstances, including potentially terminating the advisory agreement and retaining a new Adviser.

The compensation arrangements between us and our Advisers and affiliates could influence our Advisers’ advice to us, as well as the judgment of the affiliates of our Advisers who may serve as our officers or directors. Among other matters, the compensation arrangements could affect their judgment with respect to:

| • | the continuation, renewal or enforcement of our agreements with our Advisers and affiliates, including the advisory agreement; |

| • | subsequent offerings of equity securities by us, which may entitle our Advisers to additional asset management fees; |

| • | property sales, which may entitle our Advisers to possible success-based share of net sale proceeds; |

| • | property acquisitions from other programs sponsored by affiliates of our Advisers which may entitle such affiliates to disposition fees and possible success-based sale fees in connection with its services for the seller, as well as acquisition fees for our Advisers; |

| • | property sales to other programs sponsored by affiliates of our Advisers which may entitle such affiliates to acquisition fees and expenses for its services to the buyer, as well as subordinated share of net sale proceeds to our Advisers; |

| • | whether and when we seek to sell our assets and liquidate, which sale may entitle our Advisers to a success-based distribution but could also adversely affect its sales efforts for other programs depending upon the sales price. |

Certain Conflict Resolution Procedures

Every transaction that we enter into with our sponsor, our Advisers, or their affiliates will be subject to an inherent conflict of interest. Our board of directors may encounter conflicts of interest in enforcing our rights against any affiliate in the event of a default by or disagreement with an affiliate or in invoking powers, rights, or options pursuant to any agreement between us and our sponsor, our Advisers, or any of their affiliates. In order to reduce or eliminate certain potential conflicts of interest, we will address any conflicts of interest in two distinct ways.

First, the nominating and corporate governance committee of the Board will consider and act on any conflicts-related matter required by our Charter or otherwise permitted by the Maryland General Corporation Law (“MGCL”) where the exercise of independent judgment by any of our directors (who is not an independent director) could reasonably be compromised, including approval of any transaction involving our Advisers and their affiliates.

Second, our advisory agreements with our Advisers contain a number of restrictions relating to (1) transactions we enter into with our sponsor, our Advisers and their affiliates, (2) certain future offerings, and (3) allocation of investment opportunities among affiliated entities. These restrictions include, among others, the following:

| • | We will not purchase or lease properties in which our sponsor, our Advisers, any of our directors or any of their respective affiliates has an interest without a determination by a majority of our directors, including a majority of the independent directors, not otherwise interested in such transaction that such transaction is fair and reasonable to us and at a price to us no greater than the cost of the property to the seller or lessor, unless there is substantial justification for any amount that exceeds such cost and such excess amount is determined to be reasonable. In no event will we acquire any such property at an amount in excess of its appraised value. We will not sell or lease properties to our sponsor, our Advisers, any of our directors or any of their respective affiliates unless a majority of our directors, including a majority of our independent directors, not otherwise interested in the transaction determines that the transaction is fair and reasonable to us. |

| • | We will not make any loans to our sponsor, our Advisers, any of our directors or any of their respective affiliates. In addition, our sponsor, our Advisers, any of our directors and any of their respective affiliates will not make loans to us or to joint ventures in which we are a joint venture partner unless approved by a majority of our directors, including a majority of the independent directors, not otherwise interested in the transaction as fair, competitive and commercially reasonable, and no less favorable to us than comparable loans between unaffiliated parties. |

| • | Our Advisers and affiliates will be entitled to reimbursement, at cost, for actual expenses incurred by them on behalf of us or joint ventures in which we are a joint venture partner. |

| • | Our directors, including our independent directors, have a duty to ensure that the method used by our Advisers for the allocation of the acquisition of properties by two or more affiliated programs seeking to acquire similar types of properties (summarized below) is applied fairly to us. |

Our sponsor has adopted an investment allocation policy with respect to real estate assets, which governs the allocation of such investment opportunities among the programs sponsored by our sponsor, and which provides as follows:

In the event that an investment opportunity becomes available, our sponsor will first allocate such investment opportunity to us. If we decline the investment opportunity, our adviser will allocate such investment opportunity to another program sponsored by our sponsor based on the following factors:

| • | the investment objectives of each program; |

| • | the amount of funds available to each program; |

| • | the financial and investment characteristics of each program, including investment size, potential leverage, transaction structure and anticipated cash flows; |

| • | the strategic location of the investment in relationship to existing properties owned by each program; |

| • | the effect of the investment on the diversification of each program’s investments; and |

| • | the impact of the financial metrics of the investment on each program. |

If, after consideration of the foregoing factors, our sponsor determines that an investment opportunity is suitable for two or more entities affiliated with our Advisers, then our sponsor will allocate such investment opportunity among the entities in its sole and absolute discretion, but generally will allocate such investment opportunity to whichever entity has gone the longest since purchasing such an investment opportunity.

If a subsequent development, such as a delay in the closing of a property or a delay in the construction of a property, causes any such investment, in the opinion of our Advisers, to be more appropriate for a program other than the program that committed to make the investment, our Advisers may determine that another program affiliated with our Advisers or their affiliates will make the investment. Our directors, including our independent directors, have a duty to ensure that the method used by our Advisers for the allocation of the acquisition of properties by two or more affiliated programs seeking to acquire similar types of properties is applied fairly to us.

As a result of the foregoing, our Advisers and affiliates could direct attractive investment opportunities to other entities or even purchase them for their own account. Our advisory agreement disclaims any interest in an investment opportunity known to our Advisers or their affiliates that our advisers has not recommended to us.

We will not accept goods or services from our sponsor, Advisers, or any affiliate thereof or enter into any other transaction with our sponsor, advisers, or any affiliate thereof unless a majority of our directors, including a majority of our independent directors not otherwise interested in the transaction, approve such transaction as fair and reasonable to us and on terms and conditions not less favorable to us than those available from unaffiliated third parties.

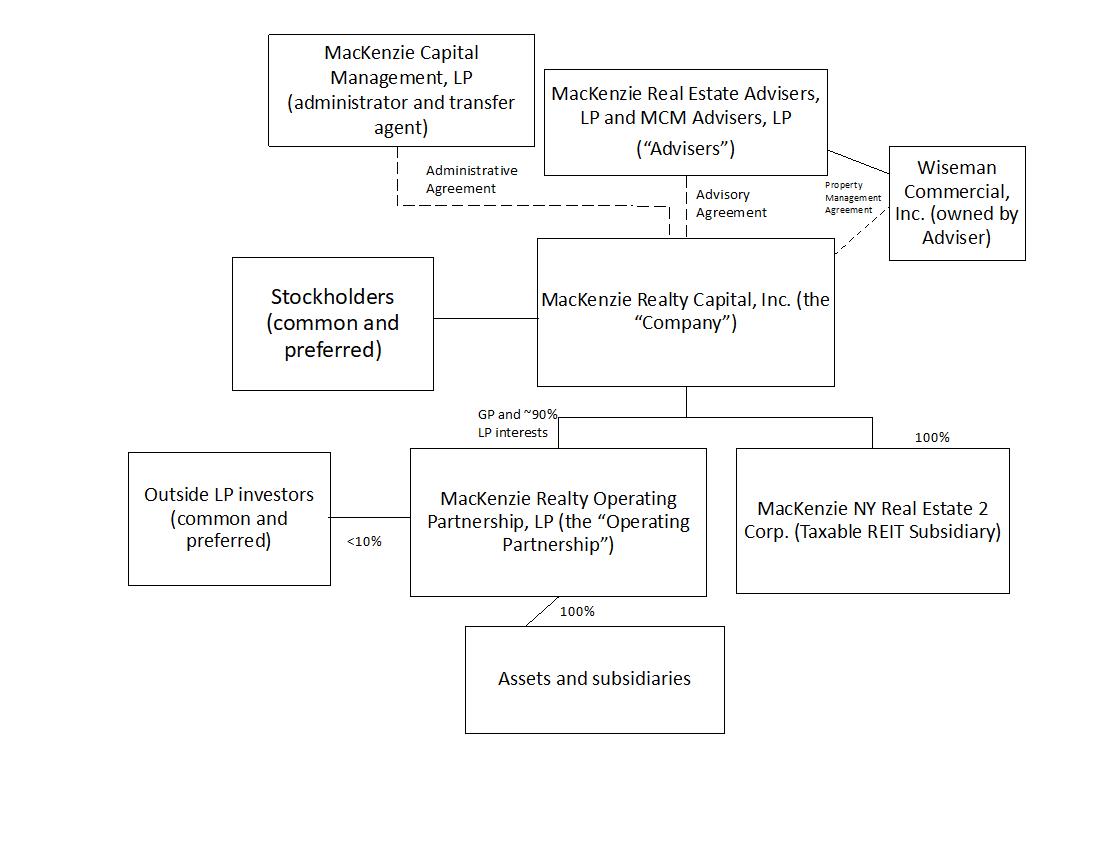

The following chart shows our ownership structure and entities that are affiliated with our Advisers and sponsor.

* | The address of all of these entities is 89 Davis Road, Suite 100, Orinda, CA 94563. |

Investment Objectives

Our primary investment objectives are:

| • | To acquire real estate assets at substantial discounts to fair market value; |

| • | To grow net cash from operations so that an increasing amount of cash flow is available for distributions to investors over the long term; |

| • | To pay attractive and consistent cash distributions; |

| • | To preserve and protect shareholder value; and |

| • | To realize growth in the value of our investment by timing their sale to maximize value. |

There is no assurance that any of our investment objectives will be met.

Investment Strategy

We intend to use substantially all of the proceeds of this Offering to acquire, manage, renovate or reposition, operate, selectively leverage, and lease properties throughout the United States.

We acquire primarily institutional-quality apartment and office properties where we believe we can create long-term value for our stockholders, utilizing the following investment strategies:

| • | Value-Add. We invest in well-located institutional-quality properties with strong and stable cash flows in demographically attractive knowledge economy growth markets where we believe there exists significant potential for medium-term capital appreciation through renovation or redevelopment, to reposition the asset and drive future rental growth. |

| • | Opportunistic. We invest in properties available at opportunistic prices (i.e., at prices we believe are below those available in an otherwise efficient market) that exhibit some characteristics of distress, such as operational inefficiencies, significant deferred capital maintenance, or broken capital structures providing an opportunity for a substantial portion of total return attributable to appreciation in value. |

| • | Invest-to-Own. We selectively invest in development of quality properties in target markets where we believe we can capture significant premiums upon completion. We intend to use either tender offers, a convertible loan, or convertible preferred equity structure to provide income during the early stage and/or the ability to capture premiums at completion by either acquiring controlling positions or exercising our conversion rights to take ownership. |

Please see the Risk Factors Section beginning on page 12 of this Offering Circular for the risks involved with this offering.

Distribution Policy

In order to qualify as a REIT, we must distribute to our stockholders at least 90% of our annual taxable income. We intend to make regular cash distributions to our stockholders out of our cash available for distribution, typically on a quarterly or annual basis for holders of our common and preferred stock.

Our Board of Directors will determine the amount of distributions to be distributed to our stockholders on a quarterly basis. The board’s determination will be based on a number of factors, including funds available from operations, our capital expenditure requirements, and the annual distribution requirements necessary to maintain our REIT qualification under the Code.

Our distribution rate and payment frequency may vary from time to time. Generally, our policy will be to pay distributions from cash flow from operations. However, our distributions may be paid from sources other than cash flows from operations, such as from the proceeds of this Offering, borrowings, advances from our Adviser or from our Adviser’s deferral of its fees and expense reimbursements, as necessary.

Limited Prospects for Future Liquidity; Potential Proxy to Liquidate

We currently do not plan to list either the Series A Preferred Stock or the Series B Preferred Stock on any securities exchange. Pursuant to our Charter, if the Company’s common stock is not listed on any national securities exchange registered under Section 6 of the Exchange Act after the eighth anniversary of the completion of our initial public offering (which will occur in October 2024) or in the process of being so listed or the Company is not in the process of making an orderly liquidation and sale of the Company’s assets, and unless such date is extended by the majority vote of the Board of Directors, the Company will be required to formally proxy the stockholders of the Company entitled to vote to determine whether the Company should be liquidated (the “Proxy to Liquidate”) as soon as reasonably practicable following the receipt of independent appraisals of the Company’s assets, which the Company shall obtain as part of this proxy process, and the filing with and review of such Proxy to Liquidate by the SEC. There can be no assurance that our Board of Directors will not extend the timeframe for a liquidity event, that a suitable transaction will be available or that related market conditions will be favorable during that timeframe. Examples of a potential liquidity event could include, among other possibilities (1) the sale of all or substantially all of our assets either on a complete portfolio basis or individually followed by a liquidation, (2) a listing of our shares on a national securities exchange, or (3) a merger or another transaction approved by our Board in which our stockholders would receive cash or shares of another publicly traded company. Apart from the above-described provision in our Charter, we do not have any present plans or proposals, and are not engaged in any negotiations, that relate to or would result in any such event. In making a determination of whether any future potential liquidity event is in our best interest, our Board, including our independent directors, may consider a variety of criteria, including, but not limited to, portfolio diversification, portfolio performance, our financial condition, potential access to capital as a listed company, market conditions for the sale of our assets or listing of our securities, internal management considerations and the potential for stockholder liquidity.

Overview of Significant Risk Factors

Investing in our preferred shares involves a high degree of risk. You should carefully review the “Risk Factors” section of this Offering Circular, beginning on page 12, which contains a detailed discussion of the material risks that you should consider before you invest in our preferred shares. Some of the more significant risks are those summarized below:

| • | Investors will not have the opportunity to evaluate or approve any Investments prior to our acquisition or financing thereof. |

| • | Investors will rely solely on the Adviser to manage us and our Investments. The Adviser will have broad discretion to invest our capital and make decisions regarding Investments. |

| • | We may not be able to invest the net proceeds of this Offering on terms acceptable to investors, or at all. |

| • | We may change our targeted investment and operational policies, including our policies with respect to distributions and redemption of shares, without prior notice or your approval. |

| • | An investor could lose all or a substantial portion of the investment in us. |

| • | There is no public trading market for our preferred shares, and we are not obligated to effectuate a liquidity event or a listing of our preferred shares on any nationally recognized stock exchange by a certain date or at all. It will thus be difficult for an investor to sell shares owned by the investor in us. |

| • | We may fail to qualify or maintain our qualification as a REIT for federal income tax purposes. We would then be subject to corporate level taxation and regulation as an investment company and we would not be required to pay any distributions to our stockholders. |

| • | The offering price of our shares was not established based upon any appraisals of assets we own or may own. Thus, the initial offering price may not accurately reflect the value of our assets at the time an investor’s investment is made. |

| • | Substantial actual and potential conflicts of interest exist between our investors and our interests or the interests of our Adviser, and our respective affiliates, including conflicts arising out of (a) allocation of personnel to our activities, (b) allocation of investment opportunities between us, and (c) potential conflicts arising out of transactions between us, on the one hand, and our Adviser and its affiliates, on the other hand, involving compensation and incentive fees payable to our Adviser or dealings in real estate transactions between us and the Adviser and its affiliates. |

| • | There are substantial risks associated with owning, financing, operating, leasing and managing real estate. |

| • | The amount of distributions we make is uncertain. We may fund distributions from offering proceeds, borrowings, and the sale of assets, to the extent distributions exceed our earnings or cash flows from our operations if we are unable to make distributions from our cash flows from operations. There is no limit on the amount of offering proceeds we may use to fund distributions. Distributions paid from sources other than cash flow or funds from operations may constitute a return of capital to our stockholders. Rates of distributions may not be indicative of our actual operating results. |

| • | Accrued dividends with respect to the Series B Preferred Stock might be treated as taxable dividends even though holders do not receive any current cash. |

We will pay substantial fees and reimburse expenses to the Adviser. These fees and expenses will increase investors’ risk of loss and will reduce the amount available for Investments.

Preferred stock offered by us | 3,000,000 shares of either Series A or Series B preferred stock, referred to herein as the “preferred shares.” |

| Preferred stock to be outstanding after this Offering (assuming the maximum offering amount is sold) | 3,000,000 preferred shares, in a combination of Series A and Series B. |

Ranking | The preferred shares will rank, with respect to dividend rights and rights upon liquidation, winding-up, or dissolution (i) senior to all classes of our common stock, and to any other class or series of our capital stock issued in the future unless the terms of that capital stock expressly provide that it ranks senior to, or on parity with, the preferred shares, and (ii) junior to any other class or series of our capital stock, the terms of which expressly provide that it will rank senior to the preferred shares. |

Stated Value | Each share of Series A Preferred Stock or Series B Preferred Stock will have an initial “Stated Value” of $25.00, subject to appropriate adjustment in relation to certain events as set forth in the Articles Supplementary for each such Series. |

Liquidation Preference | Upon any voluntary or involuntary liquidation, dissolution or winding up of the Company, the holders of shares of our preferred stock will be entitled to receive the following payments (in each case, the “Liquidation Preference” applicable to such series): Holders of Series A Preferred Stock will be entitled to be paid, as the Liquidation Preference applicable to such shares, an amount equal to the Stated Value of $25 per share, plus an amount equal to any accrued and unpaid dividends thereon. Holders of Series B Preferred Stock will be entitled to be paid the Liquidation Preference applicable to the Series B Preferred Stock, which is dependent on the Accrued Preference Value for each share of such stock. The “Accrued Preference Value” for each outstanding share of Series B Preferred Stock is equal to (i) the Stated Value of $25.00 per share of Series B Preferred Stock plus (ii) an amount equal to any accrued and unpaid dividends (whether or not authorized or declared) thereon to and including the date of payment of such amount, but without interest. The Liquidation Preference for each outstanding share of Series B Preferred Stock will be calculated as follows: (i) from the Acquisition Date applicable to such share until the third anniversary of such date, the dollar value of the Accrued Preference Value applicable to such share as of the date such Liquidation Preference is calculated and (ii) from and after the third anniversary of the Acquisition Date applicable to such share, an amount equal to the greater of (A) the dollar value of the Accrued Preference Value applicable to such share as of the date the Liquidation Preference is calculated or (B) an amount equal to the dollar value of the amount of common stock the holder of such share of Series B Preferred Stock would be entitled to receive as of the date the Liquidation Preference is calculated, pursuant to the provisions described below in this summary under the heading “Series B Preferred Repurchase/Additional Conversion Rights.” |

Dividend rights | Holders of our preferred shares are entitled to receive, when and as authorized by our Board of Directors and declared by us out of legally available funds, cumulative cash dividends on each preferred share at an annual rate of 6% for Series A Preferred Stock and at an annual rate of 3% for Series B Preferred Stock. This is a preference, not a guarantee, but is a term contained in the Company’s Charter; however, the Board could suspend the dividend at any time, although it would continue to accrue. The dividend must be paid before the common shares can be paid a dividend, and before the Adviser can receive any incentive management fee. Further, the Series B Preferred Stock will also accrue dividends at the rate of 9% per annum on the Stated Value, which will begin to be paid at the same time and in the same amounts per share with distributions paid to the holders of common stock, once holders of common stock have initially received distributions from and after December 31, 2022 equal to 10% per annum on the $7.38 per share NAV of the common stock as of such date, and the remainder of which will be paid no later than at redemption, liquidation or conversion. For additional information, see “Description of Securities – Preferred Stock – Preferred Dividend” herein. |

Company Special Redemption Right | If at any time the Company’s shares of common stock are traded on a national securities exchange with at least three market makers or a New York Stock Exchange Specialist, the Company will have the right to redeem the preferred shares at any time at a redemption price equal to (i) the Liquidation Preference for each share of Series A Preferred Stock and (ii) the Accrued Preference Value for each share of Series B Preferred Stock, in each case as of the Special Redemption Date selected by the Company. For additional information, see “Description of Securities – Preferred Stock – Special Redemption Rights” herein. |

| Company Optional Early Redemption Right | In addition to the Special Redemption Right described above, we also may redeem preferred shares for cash, in whole or in part from time to time, during an Early Redemption Period which began January 1, 2023 for the Series A Preferred Stock and will begin January 1, 2025 for the Series B Preferred Stock. The price per preferred share applicable to any such Optional Early Redemption will be equal to (i) the Liquidation Preference for each share of Series A Preferred Stock and (ii) the Accrued Preference Value for each share of Series B Preferred Stock, in each case as of the applicable Early Redemption Date selected by the Company. For additional information, see “Description of Securities – Preferred Stock – Optional Early Redemption” herein. |

Holders’ Conversion Right | Upon receipt of notice from us that we intend to redeem the preferred shares pursuant to the Optional Early Redemption Right, any holder thereof is entitled to elect instead to receive shares of our common stock as follows with respect to either the Series A Preferred shares or Series B Preferred shares, and holders of the Series B Preferred shares also will have the conversion election in the event we exercise the Company’s Special Redemption Right: (i) Series A Preferred Conversion Right: Each holder of Series A Preferred shares shall be entitled to elect to receive, in lieu of the aggregate Liquidation Preference for the applicable number of preferred shares, the number of shares of common stock equal to the value of such aggregate Liquidation Preference divided by $10.25. (ii) Series B Preferred Conversion Right: Each holder of Series B Preferred shares shall be entitled to elect to receive, in lieu of the aggregate Accrued Preference Value for the applicable number of preferred shares, the number of shares of common stock equal to such aggregate Accrued Liquidation Preference divided by (i) the lower of $10.25 or the Board’s most recent estimated net asset value per share of common stock, if the common stock is not then listed on a national securities exchange or an over-the-counter market as reported by OTC Markets Group, Inc. or another similar organization or (ii) if the common stock is then listed on a national securities exchange or an over-the-counter market as described above, the lower of $10.25 or the volume weighted average of the Last Reported Sale Price per share of common stock as reported on such market for the twenty (20) trading days prior to the Conversion Date (defined as the date of the giving of notice of an exercise of conversion rights and surrender of the underlying shares of Series B Preferred Stock to be converted). For purposes of this calculation, the “Last Reported Sale Price” for the common stock means, at any time that the common stock is listed on a national securities exchange or an over-the-counter market as described above, the closing sale price per share (or if no closing sale price is reported, the average of the bid and ask prices or, if more than one in either case, the average of the average bid and the average ask prices) on that date as reported in composite transactions for the principal U.S. national or regional securities exchange on which the common stock is traded. For additional information, see “Description of Securities – Preferred Stock – Conversion Right” herein. |