UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

----------------------

FORM 10-Q/A-1

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2017

Commission File Number: 333-182072

--------------------------

Hunt Mining Corp.

(Exact name of Registrant as specified in its charter)

| British Columbia, Canada | 1041 | |

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) |

23800 East Appleway Ave.

Liberty Lake, WA 99019

(509) 290-5659

(Address of principal executive offices)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Check whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer | ☐ | Accelerated Filer | ☐ |

| Non-accelerated Filer | ☐ | Smaller Reporting Company | ☒ |

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date: As of August 11, 2017, the registrant's outstanding common stock consisted of 63,588,798 shares.

REASON FOR AMENDMENT

The sole purpose of this Amendment to the Registrant's Quarterly Report on Form 10-Q for the period ended June 30, 2017 is to furnish the Interactive Data File exhibits pursuant to Rule 405 of Regulation S-T. No other changes have been made to this Form 10-Q and this Amendment has not been updated to reflect events occurring subsequent to the filing of this Form 10-Q.

PART I

ITEM 1. FINANCIAL STATEMENTS

Hunt Mining Corp.

Interim Consolidated Financial Statements

Six months ended June 30, 2017 and 2016 | Page |

| Interim Consolidated Balance Sheets | 3 |

| Interim Consolidated Statements of Operations and Comprehensive Loss | 4 |

| Interim Consolidated Statement of Changes in Stockholders' Deficiency | 5 |

| Interim Consolidated Statements of Cash Flows | 6 |

| Notes to the Interim Consolidated Financial Statements | 7 - 23 |

2

| Hunt Mining Corp. | ||||||||||||

| Expressed in U.S. Dollars (Unaudited) | ||||||||||||

| Interim Consolidated Balance Sheets | ||||||||||||

| NOTE | June 30, 2017 | December 31, 2016 Restated | ||||||||||

| CURRENT ASSETS: | ||||||||||||

| Cash | 16 | $ | 667,125 | $ | 108,272 | |||||||

| Accounts receivable | 16,19 | 901,686 | 126,453 | |||||||||

| Prepaid expenses | 8,423 | 17,593 | ||||||||||

| Inventory | 7 | 581,324 | - | |||||||||

| Total Current Assets | 2,158,558 | 252,318 | ||||||||||

| NON-CURRENT ASSETS: | ||||||||||||

| Mineral Properties | 8 | 438,062 | 438,062 | |||||||||

| Property, plant and equipment | 10 | 4,382,212 | 4,934,783 | |||||||||

| Performance bond | 12,16 | 410,716 | 381,355 | |||||||||

| Other deposit | 18a | 63,891 | 64,610 | |||||||||

| Total Non-Current Assets: | 5,294,881 | 5,818,810 | ||||||||||

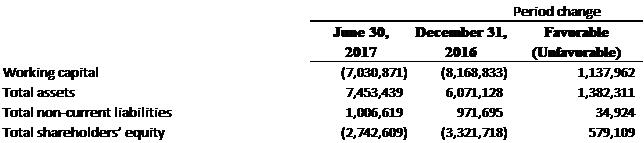

| TOTAL ASSETS: | $ | 7,453,439 | $ | 6,071,128 | ||||||||

| CURRENT LIABILITIES: | ||||||||||||

| Bank indebtedness | 14,16 | $ | 50,000 | $ | - | |||||||

| Accounts payable and accrued liabilities | 15,16 | 5,564,071 | 3,087,611 | |||||||||

| Purchase price payable | 8 | - | 1,500,000 | |||||||||

| Deferred advances | - | 190,269 | ||||||||||

| Interest payable | 15,16 | 72,243 | 53,293 | |||||||||

| Transaction taxes payable | 16 | 129,155 | 118,667 | |||||||||

| Loan payable | 13,15,16 | 3,373,960 | 3,471,311 | |||||||||

| Total Current Liabilities: | 9,189,429 | 8,421,151 | ||||||||||

| NON-CURRENT LIABILITIES: | ||||||||||||

| Asset retirement obligation | 9 | 756,619 | 721,695 | |||||||||

| Contingent liability | 18a | 250,000 | 250,000 | |||||||||

| Total Non-Current Liabilities: | 1,006,619 | 971,695 | ||||||||||

| TOTAL LIABILITIES: | $ | 10,196,048 | $ | 9,392,846 | ||||||||

| STOCKHOLDERS' DEFICIENCY: | ||||||||||||

Capital stock: Authorized- Unlimited No Par Value Issued and outstanding - 63,588,798 common shares (December 31, 2016 - 63,588,798 common shares) | 11 | $ | 24,695,186 | $ | 24,695,186 | |||||||

| Additional paid in capital | 9,661,992 | 9,661,992 | ||||||||||

| Deficit | (37,038,513 | ) | (37,649,570 | ) | ||||||||

| Accumulated other comprehensive loss | (61,274 | ) | (29,326 | ) | ||||||||

| Total Stockholders' Deficiency: | (2,742,609 | ) | (3,321,718 | ) | ||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIENCY: | $ | 7,453,439 | $ | 6,071,128 | ||||||||

| Going Concern (Note 3) | ||||||||||||

| Commitments and Provision (Note 18) | ||||||||||||

| Subsequent Events (Note 20) | ||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

| Hunt Mining Corp. | ||||||||||||||||||||

| Expressed in U.S. Dollars (Unaudited) | ||||||||||||||||||||

| Interim Consolidated Statements of Operations and Comprehensive Loss | ||||||||||||||||||||

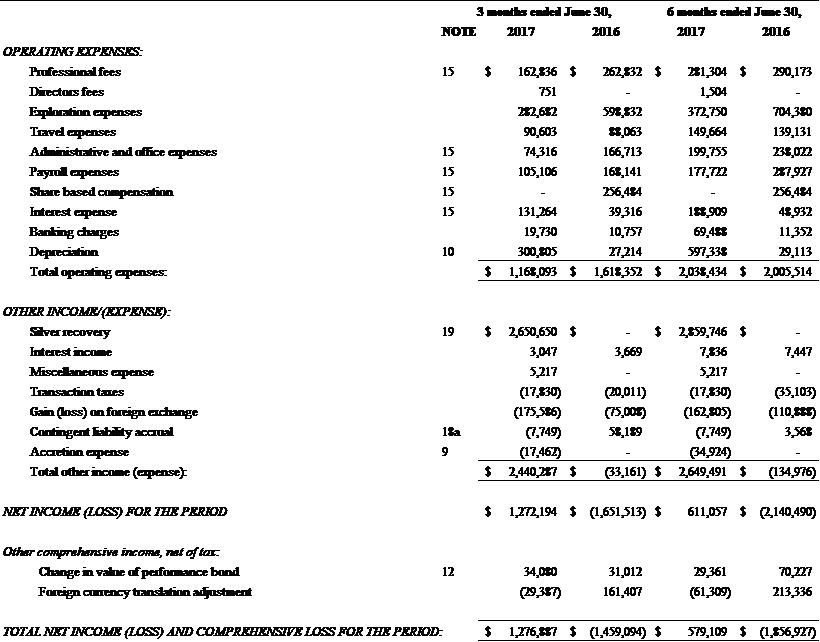

| 3 months ended June 30, | 6 months ended June 30, | |||||||||||||||||||

| NOTE | 2017 | 2016 | 2017 | 2016 | ||||||||||||||||

| OPERATING EXPENSES: | ||||||||||||||||||||

| Professional fees | 15 | $ | 162,836 | $ | 262,832 | $ | 281,304 | $ | 290,173 | |||||||||||

| Directors fees | 751 | - | 1,504 | - | ||||||||||||||||

| Exploration expenses | 282,682 | 598,832 | 372,750 | 704,380 | ||||||||||||||||

| Travel expenses | 90,603 | 88,063 | 149,664 | 139,131 | ||||||||||||||||

| Administrative and office expenses | 15 | 74,316 | 166,713 | 199,755 | 238,022 | |||||||||||||||

| Payroll expenses | 15 | 105,106 | 168,141 | 177,722 | 287,927 | |||||||||||||||

| Share based compensation | 15 | - | 256,484 | - | 256,484 | |||||||||||||||

| Interest expense | 15 | 131,264 | 39,316 | 188,909 | 48,932 | |||||||||||||||

| Banking charges | 19,730 | 10,757 | 69,488 | 11,352 | ||||||||||||||||

| Depreciation | 10 | 300,805 | 27,214 | 597,338 | 29,113 | |||||||||||||||

| Total operating expenses: | $ | 1,168,093 | $ | 1,618,352 | $ | 2,038,434 | $ | 2,005,514 | ||||||||||||

| OTHER INCOME/(EXPENSE): | ||||||||||||||||||||

| Silver recovery | 19 | $ | 2,650,650 | $ | - | $ | 2,859,746 | $ | - | |||||||||||

| Interest income | 3,047 | 3,669 | 7,836 | 7,447 | ||||||||||||||||

| Miscellaneous expense | 5,217 | - | 5,217 | - | ||||||||||||||||

| Transaction taxes | (17,830 | ) | (20,011 | ) | (17,830 | ) | (35,103 | ) | ||||||||||||

| Gain (loss) on foreign exchange | (175,586 | ) | (75,008 | ) | (162,805 | ) | (110,888 | ) | ||||||||||||

| Contingent liability accrual | 18a | (7,749 | ) | 58,189 | (7,749 | ) | 3,568 | |||||||||||||

| Accretion expense | 9 | (17,462 | ) | - | (34,924 | ) | - | |||||||||||||

| Total other income (expense): | $ | 2,440,287 | $ | (33,161 | ) | $ | 2,649,491 | $ | (134,976 | ) | ||||||||||

| NET INCOME (LOSS) FOR THE PERIOD | $ | 1,272,194 | $ | (1,651,513 | ) | $ | 611,057 | $ | (2,140,490 | ) | ||||||||||

| Other comprehensive income, net of tax: | ||||||||||||||||||||

| Change in value of performance bond | 12 | 34,080 | 31,012 | 29,361 | 70,227 | |||||||||||||||

| Foreign currency translation adjustment | (29,387 | ) | 161,407 | (61,309 | ) | 213,336 | ||||||||||||||

| TOTAL NET INCOME (LOSS) AND COMPREHENSIVE LOSS FOR THE PERIOD: | $ | 1,276,887 | $ | (1,459,094 | ) | $ | 579,109 | $ | (1,856,927 | ) | ||||||||||

| Weighted average shares outstanding - basic | 63,588,798 | 62,150,298 | 63,588,798 | 63,027,776 | ||||||||||||||||

| Weighted average shares outstanding - diluted | 114,963,798 | 62,150,298 | 114,963,798 | 63,027,776 | ||||||||||||||||

| NET INCOME (LOSS) PER SHARE - BASIC: | $ | 0.02 | $ | (0.02 | ) | $ | 0.01 | $ | (0.03 | ) | ||||||||||

| NET INCOME (LOSS) PER SHARE - DILUTED: | $ | 0.01 | $ | (0.02 | ) | $ | 0.01 | $ | (0.03 | ) | ||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

| Hunt Mining Corp. | ||||||||||||||||||||

| Expressed in U.S. Dollars (Unaudited) | ||||||||||||||||||||

| Interim Consolidated Statement of Changes in Stockholders' Deficiency | ||||||||||||||||||||

Share Capital | Deficit | Accumulated Other Comprehensive Income (Loss) | Additional Paid in Capital | Total | ||||||||||||||||

| Balance -January 1, 2016 | $ | 24,560,711 | $ | (34,540,496 | ) | $ | 89,200 | $ | 9,296,239 | $ | (594,346 | ) | ||||||||

| Net Loss | - | (3,109,074 | ) | - | - | (3,109,074 | ) | |||||||||||||

| Other comprehensive loss | - | - | (118,526 | ) | - | (118,526 | ) | |||||||||||||

| Capital stock issued, net | 243,744 | - | - | - | 243,744 | |||||||||||||||

| Portion of units attributable to warrants issued | (109,269 | ) | - | - | 109,269 | - | ||||||||||||||

| Share based compensation | - | - | - | 256,484 | 256,484 | |||||||||||||||

| Balance - December 31, 2016 | $ | 24,695,186 | $ | (37,649,570 | ) | $ | (29,326 | ) | $ | 9,661,992 | $ | (3,321,718 | ) | |||||||

| Balance - January 1, 2017 | $ | 24,695,186 | $ | (37,649,570 | ) | $ | (29,326 | ) | $ | 9,661,992 | $ | (3,321,718 | ) | |||||||

| Net Income | - | 611,057 | - | - | 611,057 | |||||||||||||||

| Other comprehensive loss | - | - | (31,948 | ) | - | (31,948 | ) | |||||||||||||

| Balance - June 30, 2017 | $ | 24,695,186 | $ | (37,038,513 | ) | $ | (61,274 | ) | $ | 9,661,992 | $ | (2,742,609 | ) | |||||||

The accompanying notes are an integral part of these consolidated financial statements.

5

| Hunt Mining Corp. | ||||||||||||

| Expressed in U.S. Dollars (Unaudited) | ||||||||||||

| Interim Consolidated Statements of Cash Flows | ||||||||||||

| 6 months ended June 30, | ||||||||||||

| NOTE | 2017 | 2016 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||

| Net income (loss) | $ | 611,057 | $ | (2,140,490 | ) | |||||||

| Items not affecting cash | ||||||||||||

| Depreciation | 10 | 597,338 | 29,113 | |||||||||

| Gain on foreign exchange | 719 | - | ||||||||||

| Share based compensation | 11 | - | 256,484 | |||||||||

| Accretion | 8 | 34,924 | - | |||||||||

| Net change in non-cash working capital items | ||||||||||||

| Increase (decrease) in accounts receivable | (775,233 | ) | 6,648 | |||||||||

| Decrease (increase) in prepaid expenses | 9,468 | (2,445 | ) | |||||||||

| Increase in inventory | (581,324 | ) | - | |||||||||

| Increase in accounts payable and accrued liabilities | 2,201,129 | 1,293,178 | ||||||||||

| Increase in interest payable | 18,950 | - | ||||||||||

| Increase in transaction taxes payable | 10,488 | 23,574 | ||||||||||

| 2,127,516 | (533,938 | ) | ||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||||||

| Purchases of property and equipment | 10 | (1,544,767 | ) | (1,069,288 | ) | |||||||

| Purchases of mineral property | - | (438,062 | ) | |||||||||

| (1,544,767 | ) | (1,507,350 | ) | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||

| Proceeds from bank indebtedness | 14,16 | 50,000 | 19,558 | |||||||||

| Proceeds from loan | 15 | 2,500,000 | 2,000,000 | |||||||||

| Repayment of loan | 13,15 | (2,597,351 | ) | - | ||||||||

| (47,351 | ) | 2,019,558 | ||||||||||

| NET INCREASE (DECREASE) IN CASH: | 535,398 | (21,730 | ) | |||||||||

| EFFECT OF FOREIGN EXCHANGE ON CASH | 23,455 | 214,386 | ||||||||||

| CASH, BEGINNING OF PERIOD: | 108,272 | 32,683 | ||||||||||

| CASH, END OF PERIOD: | $ | 667,125 | $ | 225,339 | ||||||||

| SUPPLEMENTAL CASH FLOW INFORMATION | ||||||||||||

| Taxes paid | - | - | ||||||||||

| Interest paid | (62,602 | ) | (11,806 | ) | ||||||||

The accompanying notes are an integral part of these consolidated financial statements.

6

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

1. Nature of Business

Hunt Mining Corp. (the "Company" or "Hunt"), is a mineral exploration company incorporated on January 10, 2006 under the laws of Alberta, Canada and, together with its subsidiaries, is engaged in the exploration of mineral properties in Santa Cruz Province, Argentina.

Effective November 6, 2013, the Company continued from the Province of Alberta to the Province of British Columbia. The Company's registered office is located at 25th Floor, 700 West Georgia Street, Vancouver, B.C. V7Y 1B3. The Company's head office is located at 23800 E Appleway Avenue, Liberty Lake, Washington, 99019 USA.

The consolidated interim financial statements include the accounts of the following subsidiaries after elimination of intercompany transactions and balances:

| Corporation | Incorporation | Percentage ownership | Business Purpose |

| Cerro Cazador S.A. | Argentina | 100% | Holder of Assets and Exploration Company |

| Ganadera Patagonia SRL | Argentina | 40% | Land Holding Company |

| 1494716 Alberta Ltd. | Alberta, Canada | 100% | Nominee Shareholder |

| Hunt Gold USA LLC | Washington, USA | 100% | Management Company |

(1) The Company has determined that the subsidiary is a variable interest entity because the Company is the primary beneficiary of the land the subsidiary holds, and therefore consolidates the subsidiary in its interim financial statements.

The Company's activities include the exploration of mineral properties in Argentina and the Mina Martha project (Note 8). On the basis of information to date, the Company has not yet determined whether the Exploration properties contain economically recoverable ore reserves. The underlying value of the mineral properties is entirely dependent upon the existence of economically recoverable reserves, the ability of the Company to obtain the necessary financing to complete development and upon future profitable production or a sale of these properties. The Mina Martha project was purchased in the second quarter of 2016 and refurbishing activities began in late 2016. The Company finished all refurbishments to the Mina Martha project in the first quarter of 2017 and began operations and selling concentrate in the second quarter of 2017.

2. Basis of presentation

These consolidated interim financial statements have been prepared in conformity with generally accepted accounting principles of the United States of America ("US GAAP").

These consolidated interim financial statements have been prepared on a historical cost basis except for certain financial instruments measured at fair value. In addition, these consolidated interim financial statements have been prepared using the accrual basis of accounting, except for cash flow information.

The Company's presentation currency is the US Dollar.

The preparation of the consolidated interim financial statements requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates.

Judgments made by management in the application of US GAAP that have a significant effect on the consolidated interim financial statements and estimates with significant risk of material adjustment in the current and following years are discussed in Note 6.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

3. Going Concern

The accompanying consolidated interim financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates the realization of assets and the liquidation of liabilities in the normal course of business. During the six months ended June 30, 2017, the Company had net income of $611,057. As at June 30, 2017, the Company had an accumulated deficit of $37,038,513. The Company intends to continue funding operations through operation of the Martha Mine and equity financing arrangements, which may be insufficient to fund its capital expenditures, working capital and other cash requirements for the year ending December 31, 2017.

These factors, among others, raise substantial doubt about the Company's ability to continue as a going concern. The accompanying interim financial statements do not include any adjustments that might result from the outcome of this uncertainty.

4. Significant Accounting Policies

The significant accounting policies used in the preparation of these consolidated interim financial statements are described below.

(a) Basis of measurement

The consolidated interim financial statements have been prepared under the historical cost convention, except for the revaluation of certain financial assets and financial liabilities to fair value.

(b) Consolidation

The Company's consolidated interim financial statements consolidate the accounts of the Company and its subsidiaries. All intercompany transactions, balances and unrealized gains or losses from intercompany transactions are eliminated on consolidation.

(c) Foreign currency translation

Monetary assets and liabilities, denominated in foreign currencies are translated into the functional currency at the rates of exchange prevailing at the reporting date. Non-monetary assets and liabilities are translated at the exchange rate prevailing at the transaction date. Revenues and expenses are translated at average exchange rates throughout the reporting period. Gains and losses on translation of foreign currencies are included in the consolidated statement of operations.

The Company's functional currency is the Canadian dollar. All of the Company's subsidiaries have a US dollar functional currency. Interim financial statements are translated to their US dollar equivalents using the current rate method. Under this method, the statements of operations and comprehensive loss and cash flows for each period have been translated using the average exchange rates prevailing during each period. All assets and liabilities have been translated using the exchange rate prevailing at the balance sheet date. Translation adjustments are recorded as income or losses in other comprehensive income or loss. Transaction gains and losses resulting from fluctuations in currency exchange rates on transactions denominated in currencies other than the functional currency are recognized as incurred in the accompanying consolidated statement of loss and comprehensive loss.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

(d) Financial instruments

The Company measures the fair value of financial assets and liabilities based on US GAAP guidance, which defines fair value, establishes a framework for measuring fair value, and expands disclosures about fair value measurements.

The Company classifies financial assets and liabilities as held-for-trading, available-for-sale, held-to-maturity, loans and receivables or other financial liabilities depending on their nature. Financial assets and financial liabilities are recognized at fair value on their initial recognition, except for those arising from certain related party transactions, which are accounted for at the transferor's carrying amount or exchange amount.

Financial assets and liabilities classified as held-for-trading are measured at fair value, with gains and losses recognized in net income. Financial assets classified as held-to-maturity, loans and receivables, and financial liabilities other than those classified as held-for-trading are measured at amortized cost, using the effective interest method of amortization. Financial assets classified as available-for-sale are measured at fair value, with unrealized gains and losses being recognized as other comprehensive income until realized, or if an unrealized loss is considered other than temporary, the unrealized loss is recorded in income.

See Note 16 to the Consolidated Interim financial statements for fair value disclosures.

(e) Cash and equivalents

Cash and equivalents include cash on hand, deposits held with banks and other liquid short-term investments with original maturities of three months or less. The Company has no cash equivalents for all years presented.

(f) Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses. Cost includes expenditures that are directly attributable to the acquisition of an asset.

Repairs and maintenance costs are charged to the consolidated statement of operations and comprehensive loss during the period in which they are incurred.

Depreciation is calculated to amortize the cost of the property, plant and equipment over their estimated useful lives using the straight-line method. Plant, buildings, equipment and vehicles are stated at cost and depreciated straight line over an estimated useful life of three to eight years. Depreciation begins once the asset is in the state intended for use by management.

The Company allocates the amount initially recognized in respect of an item of property and equipment to its significant parts and depreciates separately each such part. Residual values, method of depreciation and useful lives of the assets are reviewed annually and adjusted if appropriate.

Gains and losses on disposals of property, plant and equipment are determined by comparing the proceeds with the carrying amount of the asset and are included as part of other gains or losses in the consolidated statement of operations and comprehensive loss.

(g) Mineral properties and exploration and evaluation expenditures

All exploration expenditures are expensed as incurred. Expenditures to acquire mineral rights, to develop new mines, to define further mineralization in mineral properties which are in the development or operating stage, and to expand the capacity of operating mines, are capitalized and amortized on a straight-line basis over the estimated life of the mine.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Should a property be abandoned, its capitalized costs are charged to the consolidated statement of loss and comprehensive loss. The Company charges to the consolidated statement of loss and comprehensive loss the allocable portion of capitalized costs attributable to properties sold. Capitalized costs are allocated to properties sold based on the proportion of claims sold to the claims remaining within the project area.

(h) Long-lived assets

Long-lived assets held and used by the Company are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. For purposes of evaluating the recoverability of long-lived assets, the recoverability test is performed using undiscounted net cash flows related to the long-lived assets. If such assets are considered to be impaired, the impairment recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets. Assets to be disposed of are reported at the lower of their carrying amount or fair value less costs to sell.

(i) Asset retirement obligations

The Company records the fair value of an asset retirement obligation as a liability in the period in which it incurs a legal obligation associated with the retirement of tangible long-lived assets that result from the acquisition, construction, development, and/or normal use of the long-lived assets. The Company also records a corresponding asset, which is amortized over the life of the asset. Subsequent to the initial measurement of the asset retirement obligation, the obligation is adjusted at the end of each period to reflect the passage of time (accretion expense) and changes in the estimated future cash flows underlying the obligation (asset retirement cost).

(j) Income taxes

The Company accounts for income taxes under the asset and liability method. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Under the asset and liability method, the effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. A valuation allowance is recognized if it is more likely than not that some portion or all of the deferred tax asset will not be recognized.

(k) Share-based compensation

The Company offers a share option plan for its directors, officers, employees and consultants. ASC 718 "Compensation – Stock Compensation" prescribes accounting and reporting standards for all share-based payment transactions in which employee services are acquired. Transactions include incurring liabilities, or issuing or offering to issue shares, options, and other equity instruments such as employee stock ownership plans and stock appreciation rights. Share-based payments to employees, including grants of employee stock options, are recognized as compensation expense in the interim financial statements based on their fair values. That expense is recognized over the period during which an employee is required to provide services in exchange for the award, known as the requisite service period (usually the vesting period).

The Company accounts for stock-based compensation issued to non-employees and consultants in accordance with the provisions of ASC 505-50, "Equity Based Payments to Non-Employees." Measurement of share-based payment transactions with non-employees is based on the fair value of whichever is more reliably measurable: (a) the goods or services received; or (b) the equity instruments issued. The fair value of the share-based payment transaction is determined at the earlier of performance commitment date or performance completion date.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

(l) Earnings (loss) per share

The calculation of earnings (loss) per share ("EPS") is based on the weighted average number of shares outstanding for each year. The basic EPS is calculated by dividing the earnings or loss attributable to the equity owners of the Company by the weighted average number of common shares outstanding during the year.

The computation of diluted EPS assumes the conversion, exercise or contingent issuance of securities only when such conversion, exercise or issuance would have a dilutive effect on the earnings per share. The treasury stock method is used to determine the dilutive effect of the warrants and share options. When the Company reports a loss, the diluted net loss per common share is equal to the basic net loss per common share due to the anti-dilutive effect of the outstanding warrants and share options.

(m) Silver Recovery

Recovery of concentrate and other income is recognized when title and the risks and rewards of ownership to delivered concentrate and commodities pass to the buyer and collection is reasonably assured.

(n) Inventories

Mineral concentrate and ore stockpiles are physically measured or estimated and valued at the lower of cost or net realizable value. Net realizable value is the estimated future sales price of the product the entity expects to realize when the product is processed and sold, less estimated costs to complete production and bring the product to sale. Where the time value of money is material, these future prices and costs to complete are discounted.

If the ore stockpile is not expected to be processed in 12 months after the reporting date, it is included in noncurrent assets and the net realizable value is calculated on a discounted cash flow basis.

Cost of silver concentrate and ore stockpiles is determined by using the first in first out method and comprises direct costs and a portion of fixed and variable overhead costs, including depreciation and amortization, incurred in converting materials into concentrate, based on the normal production capacity.

Materials and supplies are valued at the lower of cost or net realizable value. Any provision for obsolescence is determined by reference to specific items of stock. A regular review is undertaken to determine the extent of any provision for obsolescence.

5. Recently Issued Accounting Pronouncements

Restricted Cash

In November 2016, ASU No. 2016-18 was issued related to the inclusion of restricted cash in the statement of cash flows. This new guidance requires that a statement of cash flows explain the change during the period in the total of cash, cash equivalents and amounts generally described as restricted cash or restricted cash equivalents. This update is effective in fiscal years, including interim periods, beginning after December 15, 2017 and early adoption is permitted. The adoption of this guidance will result in the inclusion of the restricted cash balances within the overall cash balance and removal of the changes in restricted cash activities, which are currently recognized in other financing activities, on the Statements of Consolidated Cash Flows. Furthermore, an additional reconciliation will be required to reconcile Cash and cash equivalents and restricted cash reported within the Consolidated Balance Sheets to sum to the total shown in the Statements of Consolidated Cash Flows. The Company anticipates adopting this new guidance effective January 1, 2018.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Intra-Entity Transfers

In October 2016, ASU No. 2016-16 was issued related to the intra-entity transfers of assets other than inventory. This new guidance requires entities to recognize the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs. This update is effective in fiscal years, including interim periods, beginning after December 15, 2017 and early adoption is permitted. The Company is currently evaluating this guidance and the impact it will have on the Consolidated Interim financial statements and disclosures.

Statement of Cash Flows

In August 2016, ASU No. 2016-15 was issued related to the statement of cash flows. This new guidance addresses eight specific cash flow issues with the objective of reducing the existing diversity in practice in how certain cash receipts and cash payments are presented and classified in the statement of cash flows. This update is effective in fiscal years, including interim periods, beginning after December 15, 2017 and early adoption is permitted. The Company is currently evaluating this guidance and the impact it will have on the Consolidated Interim financial statements and disclosures.

Stock-based compensation

In March 2016, ASU No. 2016-09 was issued related to stock-based compensation. The new guidance simplifies the accounting for stock-based compensation transactions, including income tax consequences, classification of awards as either equity or liabilities and classification on the statement of cash flows. This update is effective in fiscal years, including interim periods, beginning after December 15, 2016 and early adoption is permitted. The adoption of this ASU had no material impact on the Company's interim consolidated financial statements.

Leases

In February 2016, ASU No. 2016-02 was issued related to leases. The new guidance modifies the classification criteria and requires lessees to recognize the assets and liabilities arising from most leases on the balance sheet. This update is effective in fiscal years, including interim periods, beginning after December 15, 2018 and early adoption is permitted. The Company is currently evaluating the updated guidance.

Investments

In January 2016, ASU No. 2016-01 was issued related to financial instruments. The new guidance requires entities to measure equity investments that do not result in consolidation and are not accounted for under the equity method at fair value and recognize any changes in fair value in net income. This new guidance also updates certain disclosure requirements for these investments. This update is effective in fiscal years, including interim periods, beginning after December 15, 2017 and early adoption is not permitted. The Company is currently evaluating the updated guidance.

Inventory

In July 2015, ASU No. 2015-11 was issued related to inventory, simplifying the subsequent measurement of inventories by replacing the lower of cost or market test with a lower of cost and net realizable value test. The update is effective in fiscal years, including interim periods, beginning after December 15, 2016 and early adoption is permitted. The adoption of this ASU had no material impact on the Company's interim consolidated financial statements.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Revenue recognition

In May 2014, ASU No. 2014-09 was issued related to revenue from contracts with customers. This ASU was further amended in August 2015, March 2016, April 2016, May 2016 and December 2016 by ASU No. 2015-14, No. 2016-08, No. 2016-10, No. 2016-12 and No. 2016-20, respectively. The new standard provides a five-step approach to be applied to all contracts with customers and also requires expanded disclosures about revenue recognition. In August 2015, the effective date was deferred to reporting periods, including interim periods, beginning after December 15, 2017 and will be applied retrospectively. Early adoption is not permitted. The Company is currently evaluating the updated guidance.

6. Critical accounting judgments and estimates

(a) Significant judgments

Preparation of the consolidated interim financial statements requires management to make judgments in applying the Company's accounting policies. Judgments that have the most significant effect on the amounts recognized in these consolidated interim financial statements relate to functional currency; income taxes; provisions and reclamation and closure cost obligations. These judgments have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year.

Functional Currency

Management determines the functional currency for each entity. This requires that management assess the primary economic environment in which each of these entities operates. Management's determination of functional currencies affects how the Company translates foreign currency balances and transactions. Determination includes an assessment of various indicators. In determining the functional currency of the Company's operations in Canada (Canadian dollar) and Argentina (U.S. dollar), management considered the indicators of ASC 830.

Income Taxes

Significant judgment is required in determining the provision for income taxes. There are many transactions and calculations undertaken during the ordinary course of business for which the ultimate tax determination is uncertain and subject to judgment. The Company recognizes liabilities and contingencies for anticipated tax audit issues based on the Company's current understanding of the tax law in the various jurisdictions in which it operates. For matters where it is probable that an adjustment will be made, the Company records its best estimate of the tax liability including the related interest and penalties in the current tax provision. Management believes they have adequately provided for the probable outcome of these matters; however, the final outcome may result in a materially different outcome than the amount included in the tax liabilities.

Provisions

Management makes judgments as to whether an obligation exists and whether an outflow of resources embodying economic benefits of a liability of uncertain timing or amount is probable, not probable or remote. Management considers all available information relevant to each specific matter.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Reclamation and closure costs obligations

The Argentine mining regulations require that mine property be restored in accordance with specified standards and an approved reclamation plan. Significant reclamation activities include reclaiming refuse and slurry ponds, reclaiming the pit and support acreage at surface mines, and sealing portals at deep mines. The Company accrues for the cost of final mine closure reclamation over the estimated useful mining life of the property. At each period, the Company reviews the entire reclamation liability and makes necessary adjustments for revisions to cost estimates to reflect current experience.

The Company has adopted ASC 410, Asset Retirement and Environmental Obligations, which requires legal obligations associated with the retirement of long-lived assets to be recognized at their fair value at the time that the obligations are incurred. Upon initial recognition of a liability, that cost is capitalized as part of the related long-lived asset and allocated to expense over the useful life of the asset.

(b) Estimation uncertainty

The preparation of the consolidated interim financial statements in conformity with US GAAP requires the Company to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated interim financial statements and the reported amounts of revenues and expenses during the reporting period. The Company also makes estimates and assumptions concerning the future. The determination of estimates requires the exercise of judgment based on various assumptions and other factors such as historical experience and current and expected economic conditions. Actual results could differ from those estimates.

The more significant areas requiring the use of management estimates and assumptions relate to title to mineral property interests; share-based payments, asset retirement obligations and inventories. These estimates have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year.

The Company is also exposed to legal risk. The outcome of currently pending and future proceedings cannot be predicted with certainty. Thus, an adverse decision in a lawsuit could result in additional costs that are not covered, either wholly or partly, under insurance policies and that could significantly influence the business and results of operations.

Estimates and assumptions are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

Title to Mineral Property Interests

Although the Company has taken steps to verify title to mineral properties in which it has an interest, these procedures do not guarantee the Company's title. Such properties may be subject to prior agreements or transfers and title may be affected by undetected defects.

Share-based Payment Transactions

The Company measures the cost of equity-settled transactions with employees by reference to the fair value of the equity instruments at the date at which they are granted. Estimating fair value for share-based payment transactions is done by application of the Black-Scholes option-pricing model, which is dependent on the terms and conditions of the grant. This estimate also requires determining the most appropriate inputs to the Black-Scholes option-pricing model, including the expected life of the stock option, forfeiture rate, and volatility based on historical share prices and dividend yield and making assumptions about them.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Legal Proceedings

In the normal course of business, legal proceedings and other claims brought against the Company expose us to potential losses. Given the nature of these events, in most cases the amounts involved are not reasonably estimable due to uncertainty about the final outcome. In estimating the final outcome of litigation, management makes assumptions about factors including experience with similar matters, past history, precedents, relevant financial, scientific and other evidence, and facts specific to the matter. This determines whether management requires a provision or disclosure in the consolidated interim financial statements.

Asset retirement obligation

Upon retirement of the Company's mineral properties, retirement costs will be incurred by the Company. Estimates of these costs are subject to uncertainty associated with the method, timing and extent of future decommissioning activities. The liability, the related asset and the expense are affected by estimates with respect to the costs and timing of retiring the assets.

Inventories

Net realizable value tests are performed at each reporting date and represent the estimated future sales price of the product the Company expects to realize when the product is processed and sold, less estimated costs to complete production and bring the product to sale. Where the time value of money is material, these future prices and costs to complete are discounted.

Stockpiles are measured by estimating the number of tones added and removed from the stockpile, the number of contained ore ounces is based on assay data, and the estimated recovery percentage is based on the expected processing method.

Stockpile tonnages are verified by periodic surveys.

7. Inventories

| June 30, 2017 | December 31, 2016 | |||||||

| Silver concentrate | $ | 162,847 | $ | - | ||||

| Ore stockpiles | 373,443 | - | ||||||

| Materials and supplies | 45,034 | - | ||||||

| $ | 581,324 | $ | - | |||||

8. Mineral properties

(a) Acquisition of Mina Martha project

On May 6, 2016, the Company acquired the assets of the Mina Martha project from Coeur Mining Inc. ("Coeur"). The Mina Martha project consists of land, mineral rights, a mine camp, offices, a warehouse, maintenance shop, mining facilities including a flotation mill and a tailings retention facility. The transaction has been accounted for as acquisition of assets. The consideration of $3,000,000 paid by Hunt Mining Corp., and the transaction costs of $129,360 have been allocated to the assets and liabilities acquired based on their relative fair value on the date of acquisition. During the six-month period ended June 30, 2017, the Company paid the remaining purchase price of $1,500,000 outstanding as at December 31, 2016.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

The following table summarizes the allocation of the purchase price and the related acquisition costs to the fair value of the assets acquired at the date of acquisition.

| Consideration Paid: | ||||

| Cash consideration paid: | $ | 3,000,000 | ||

| Transaction costs incurred: | 129,360 | |||

| $ | 3,129,360 | |||

| Net identifiable assets acquired: | ||||

| Vehicles and Equipment | $ | 1,155,000 | ||

| Buildings | 117,500 | |||

| Plant | 1,775,536 | |||

| Land | 321,294 | |||

| Mineral properties | 438,062 | |||

| Asset retirement obligation | (678,032 | ) | ||

| $ | 3,129,360 | |||

(b) Acquisition of La Josefina project

In March 2007, the Company acquired the exploration and development rights to the La Josefina project from Fomento Minero de Santa Cruz Sociedad del Estado ("Fomicruz").

In July 2007, the Company entered into an agreement (subsequently amended) with Fomicruz which provides that, in the event that a positive feasibility study is completed on the La Josefina property, a Joint Venture Corporation ("JV Corporation") would be formed by the Company and Fomicruz. The Company would own 81% of the joint venture company and Fomicruz would own the remaining 19%. Fomicruz has the option to earn up to a 49% participating interest in JV Corporation by reimbursing the Company an equivalent amount, up to 49%, of the exploration investment made by the Company. The Company has the right to buy back any increase in Fomicruz's ownership interest in the JV Corporation at a purchase price of USD$200,000 per each percentage interest owned by Fomicruz down to its initial ownership interest of 19%; the Company can also purchase 10% of the Fomicruz's initial 19% JV Corporation ownership interest by negotiating a purchase price with Fomicruz. Under the agreement, the Company has until the end of 2019 to complete cumulative exploration expenditures of $18 million and determine if it will enter into production on the property.

(c) Acquisition of La Valenciana project

On November 1, 2012, the Company entered into an agreement for the exploration of the La Valenciana project in Santa Cruz province, Argentina. The agreement is for a total of 7 years, expiring on October 31, 2019. The agreement requires the Company to spend $5,000,000 in exploration on the project over 7 years. If the Company elects to exercise its option to bring the La Valenciana project into production it must grant Fomicruz a 9% ownership in a new JV Corporation to be created by the Company to manage the project and the Company will have a 91% ownership interest in the JV Corporation.

9. Asset retirement obligation

On May 6, 2016, the Company purchased the Mina Martha project (Note 8) that has an estimated life of 8 years. The Company is legally required to perform reclamation on the site to restore it to its original condition at the end of its useful life. In accordance with FASB ASC 410-20, Asset Retirement Obligations, the Company recognized the fair value of a liability for an asset retirement obligation in the amount of $678,032. The total amount of undiscounted cash flows required to settle the estimated obligation is $1,226,817 which has been discounted using a credit-adjusted rate of 10% and an inflation rate of 2%.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

The Company capitalized that cost as part of the carrying amount of the flotation plant acquired as part of the Mina Martha project, which is depreciated on a straight-line basis over 8 years.

The following table describes all of the changes to the Company's asset retirement obligation liability:

June 30, 2017 | December 31, 2016 | |||||||

| Asset retirement obligation at beginning of period | $ | 721,695 | $ | - | ||||

| Additions | - | 678,032 | ||||||

| Accretion expense | 34,924 | 43,663 | ||||||

| Asset retirement obligation at end of period | $ | 756,619 | $ | 721,695 | ||||

10. Property, Plant and Equipment

| Land | Plant | Buildings | Vehicles and Equipment | Total | ||||||||||||||||

| Cost | ||||||||||||||||||||

| Balance at December 31, 2015 | $ | 714,103 | $ | - | $ | - | $ | 1,132,837 | $ | 1,846,940 | ||||||||||

| Additions | 321,294 | 2,631,646 | 117,500 | 1,219,385 | 4,289,825 | |||||||||||||||

| Balance at December 31, 2016 | 1,035,397 | 2,631,646 | 117,500 | 2,352,222 | 6,136,765 | |||||||||||||||

| Additions | - | - | - | 44,767 | 44,767 | |||||||||||||||

| Balance at June 30, 2017 | $ | 1,035,397 | $ | 2,631,646 | $ | 117,500 | $ | 2,396,989 | $ | 6,181,532 | ||||||||||

| Accumulated amortization | ||||||||||||||||||||

| Balance at December 31, 2015 | $ | - | $ | - | $ | - | $ | 1,118,442 | $ | 1,118,442 | ||||||||||

| Depreciation for the year | - | - | - | 83,540 | 83,540 | |||||||||||||||

| Balance at December 31, 2016 | - | - | - | 1,201,982 | 1,201,982 | |||||||||||||||

| Depreciation for the period | - | 370,252 | 19,583 | 207,503 | 597,338 | |||||||||||||||

| Balance at June 30, 2017 | $ | - | $ | 370,252 | $ | 19,583 | $ | 1,409,485 | $ | 1,799,320 | ||||||||||

| Net book value | ||||||||||||||||||||

| At December 31, 2016 | $ | 1,035,397 | $ | 2,631,646 | $ | 117,500 | $ | 1,150,240 | $ | 4,934,783 | ||||||||||

| At June 30, 2017 | $ | 1,035,397 | $ | 2,261,394 | $ | 97,917 | $ | 987,504 | $ | 4,382,212 | ||||||||||

11. Capital Stock

Authorized:

Unlimited number of common shares without par value

Unlimited number of preferred shares without par value

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Issued:

| Common Shares | Six months ended | Year ended | ||||||||||||||

| June 30, 2017 | December 31, 2016 | |||||||||||||||

| Number | Amount | Number | Amount | |||||||||||||

| Balance, beginning of period | 63,588,798 | $ | 24,695,186 | 62,150,298 | $ | 24,560,711 | ||||||||||

| Non-brokered private placements | - | - | 1,313,500 | 229,433 | ||||||||||||

| Exercise of stock options | - | - | 125,000 | 14,311 | ||||||||||||

| Portion of units attributable to warrants issued | - | - | - | (109,269 | ) | |||||||||||

| Balance, end of period | 63,588,798 | $ | 24,695,186 | 63,588,798 | $ | 24,695,186 | ||||||||||

| Warrants | Six months ended | Year ended | ||||||||||||||

| June 30, 2017 | December 31, 2016 | |||||||||||||||

| Number | Amount | Number | Amount | |||||||||||||

| Balance, beginning of period | 48,862,500 | $ | 735,152 | 47,500,000 | $ | 625,883 | ||||||||||

| Portion of units attributable to warrants issued | - | - | 1,362,500 | 109,269 | ||||||||||||

| Balance, end of period | 48,862,500 | $ | 735,152 | 48,862,500 | $ | 735,152 | ||||||||||

Common share issuances:

On November 25, 2016, the Company announced the closing of the non-brokered private placement. The Company issued 1,313,500 units at an issue price of CAD $0.25 per unit. Each unit consists of one common share and one common share purchase warrant. Each common share purchase warrant entitles the holder to acquire common shares at an exercise price of CAD $0.40 per common share until November 25, 2018. The non-brokered private placement raised $229,433, net of cash share issuance costs of $14,604 and the issuance of 49,000 broker warrants on the same terms as the warrants included within the units. The fair value of the warrants attached in the units was determined to be $109,269.

The $109,269 fair value of the 1,313,500 warrants granted as part of the units was calculated using the Black-Scholes option pricing model and using the following assumptions:

| November 25, 2016 | |||

| Risk free interest rate | 0.75% | ||

| Expected volatility | 252.66% | ||

| Expected life (years) | 2 | ||

| Expected dividend yield | 0% | ||

| Forfeiture rate | 0% | ||

| Stock price | CAD $0.26 | ||

Stock options

Under the Company's share option plan, and in accordance with TSX Venture Exchange requirements, the number of common shares reserved for issuance under the option plan shall not exceed 10% of the issued and outstanding common shares of the Company, have a maximum term of 5 years and vest at the discretion of the Board of Directors. In connection with the foregoing, the number of common shares reserved for issuance to: (a) any individual director or officer will not exceed 5% of the issued and outstanding common shares; and (b) all consultants will not exceed 2% of the issued and outstanding common shares.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Range of Exercise prices (CAD) | Number outstanding | Weighted average life (years) | Weighted average exercise price (CAD) | Number exercisable on June 30, 2017 | ||||||||||||||||

| Stock options | $0.15 - $1.00 | 4,180,000 | 3.73 | $ | 0.21 | 4,180,000 | ||||||||||||||

| June 30, 2017 | December 31, 2016 | |||||||||||||||

| Number of options | Weighted Average Price (CAD) | Number of options | Weighted Average Price (CAD) | |||||||||||||

| Balance, beginning of period | 4,225,000 | $ | 0.24 | 434,753 | $ | 1.59 | ||||||||||

| Granted | - | $ | 0.00 | 4,000,000 | $ | 0.15 | ||||||||||

| Forfeiture of stock options | - | $ | 0.00 | (35,000 | ) | $ | 1.00 | |||||||||

| Expiration of stock options | (45,000 | ) | $ | 3.00 | (49,753 | ) | $ | 3.34 | ||||||||

| Exercise of stock options | - | $ | 0.00 | (125,000 | ) | $ | 0.15 | |||||||||

| Balance, end of period | 4,180,000 | $ | 0.21 | 4,225,000 | $ | 0.24 | ||||||||||

On February 27, 2017, 45,000 options with an exercise price of CAD $3.00 expired.

As at June 30, 2017, the Company's outstanding and exercisable stock options have an aggregate intrinsic value of $164,172 (December 31, 2016 - $374,898)

Warrants:

Range of Exercise prices (CAD) | Number outstanding | Weighted average life (years) | Weighted average exercise price (CAD) | |||||||||||||

| Warrants | $0.05 - $0.40 | 48,862,500 | 3.13 | $ | 0.07 | |||||||||||

| June 30, 2017 | December 31, 2016 | |||||||||||||||

| Number of warrants | Weighted Average Price (CAD) | Number of warrants | Weighted Average Price (CAD) | |||||||||||||

| Balance, beginning of period | 48,862,500 | $ | 0.07 | 47,500,000 | $ | 0.06 | ||||||||||

| Warrants | - | - | 1,362,500 | $ | 0.40 | |||||||||||

| Balance, end of period | 48,862,500 | $ | 0.07 | 48,862,500 | $ | 0.07 | ||||||||||

12. Performance bond

The performance bond, originally required to secure the Company's rights to explore the La Josefina property, is a step-up US dollar denominated 2.5% coupon bond, paying quarterly, issued by the Government of Argentina with a face value of $600,000 and a maturity date of 2035. The bond trades in the secondary market in Argentina. The bond was originally purchased for $247,487. As of the six months ended June 30, 2017, the value of the bond increased to $410,716 (December 31, 2016-$381,355). The change in the face value of the performance bond of $29,361 for the period ended June 30, 2017 (June 30, 2016- $70,227) is recorded as other comprehensive income (loss) in the Company's consolidated statement of loss and comprehensive loss.

Since Cerro Cazador S.A. ("CCSA") fulfilled its exploration expenditure requirement mandated by the agreement with Fomento Minero de Santa Cruz Sociedad del Estado ("Fomicruz"), the performance bond was no longer required to secure the La Josefina project. Therefore, in June 2010 the Company used the bond to secure the La Valenciana project, an additional Fomicruz exploration project.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

13. Loan Payable

The Following is a summary of all notes payable.

June 30, 2017 | December 31, 2016 | |||||||

| Unsecured loan payable to Timothy Hunt, at 8% interest per annum, due on demand | $ | 1,873,960 | $ | 1,972,092 | ||||

Loan payable to Ocean Partners, repayable in monthly installments of $15,000 per dry metric ton of concentrate, at 6% per annum, secured by concentrate, due 2017 (1) | 1,500,000 | - | ||||||

| Loan payable to Ocean Partners, repayable in monthly installments of $15,000 per dry metric ton of concentrate, at 6% per annum, secured by concentrate, due 2017 | - | 1,499,219 | ||||||

| $ | 3,373,960 | $ | 3,471,311 | |||||

(1) Subsequent to June 30, 2017, the Company made principal repayment of $511,605 on the loan from the sale of concentrate (Note 20).

14. Bank indebtedness

During the three months ended March 31, 2017, the Company drew the maximum of $50,000 against its secured variable rate line of credit due December 31, 2017. The Company makes monthly interest only payments. Interest is charged at the lender's Index Rate plus 1.0%, with a floor of 4.25%.

15. Related Party Transactions

During the six months ended June 30, 2017, the Company incurred $102,229 (2016- $38,751) in professional fees expense relating to the services of the President of CCSA. Included in accounts payable and accrued liabilities as at June 30, 2017 was $212,255 (December 31, 2016- $180,359) owing to the President of CCSA for professional geological fees.

During the six months ended June 30, 2017, the Company incurred $31,692 (December 31, 2016- $10,800) in professional fees expense relating to the accounting services of a director of CCSA. Included in accounts payable and accrued liabilities as at June 30, 2017, the Company had a payable owing to the director of CCSA of $40,603 (December 31, 2016-$39,403).

During the six months ended June 30, 2017, the Company incurred $192,493 (December 31, 2016- $10,915) in administrative and office expenses relating to the rental of office space and various administrative services and expenses payable to Hunt Family Limited Partnership, LLC, ("HFLP") an entity controlled by the Company's President, CEO and Executive Chairman. HFLP also advanced $1,586,991 to the Company for general administrative purposes. At June 30, 2017, the Company had a payable owing to HFLP of $3,413,710 (December 31, 2016- $1,576,506). The advances accrue interest at 7% per annum, are unsecured and due on demand.

The Company has a loan balance payable to its President, CEO and Executive Chairman of $1,873,960 (December 31, 2016- $1,972,092). During the six months ended June 30, 2017 the Company made payments of $98,132 on the loan principle. During the six months ended June 30, 2017, the President, CEO and Executive Chairman loaned an additional $1,000,000 to the Company which was repaid in full prior to June 30, 2017. The Company incurred interest expense of $65,593 and has $25,916 included in interest payable at June 30, 2017 (December 31, 2016- $53,293).

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

Included in accounts payable and accrued liabilities as at June 30, 2017, are amounts owing to the Company's Chief Financial Officer for consulting fees of $94,957 (December 31, 2016- $50,956).

Included in accounts payable and accrued liabilities as at June 30, 2017, are amounts owing to the Company's President for wages of $84,000 (December 31, 2016– $84,000).

All related party transactions are in the normal course of business, and were measured at the exchange amount which is the amount of consideration established and agreed to by the related party.

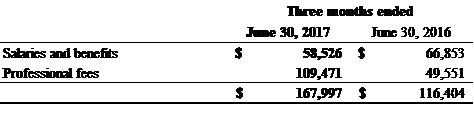

Remuneration of directors and key management of the Company

The remuneration awarded to directors and to senior key management, including the Executive Chairman and Chief Executive Officer, the Chief Financial Officer, a Director of the Company, the President of CCSA and a Director of CCSA, is as follows:

| Three months ended | ||||||||

| June 30, 2017 | June 30, 2016 | |||||||

| Salaries and benefits | $ | 58,526 | $ | 66,853 | ||||

| Professional fees | 109,471 | 49,551 | ||||||

| $ | 167,997 | $ | 116,404 | |||||

16. Financial Instruments

The Company's financial instruments consist of cash, accounts receivable, performance bond, bank indebtedness and accounts payable and accrued liabilities, purchase price payable, transaction taxes payable, loan payable and interest payable.

The Company characterizes inputs used in determining fair value using a hierarchy that prioritizes inputs depending on the degree to which they are observable. The fair value hierarchy establishes three levels to classify the inputs to valuation techniques used to measure fair value. The three levels of the fair value hierarchy are as follows:

· Level 1: inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. Active markets are those in which transactions occur in sufficient frequency and volume to provide pricing information on an ongoing basis.

· Level 2: inputs, other than quoted prices, that are observable, either directly or indirectly. Level 2 valuations are based on inputs, including quoted forward prices for commodities, market interest rates, and volatility factors, which can be observed or corroborated in the market place.

· Level 3: inputs are less observable, unavoidable or where the observable data does not support the majority of the instruments' fair value.

Fair value

As at June 30, 2017, there were no changes in the levels in comparison to December 31, 2016. The fair values of financial instruments are summarized as follows:

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

| June 30, 2017 | June 30, 2016 | |||||||||||||||

Carrying amount $ | Fair value $ | Carrying amount $ | Fair value $ | |||||||||||||

| Financial Assets | ||||||||||||||||

| FVTPL | ||||||||||||||||

| Cash (Level 1) | 667,125 | 667,125 | 225,339 | 225,339 | ||||||||||||

| Available for sale | ||||||||||||||||

| Performance bond (Level 1) | 410,716 | 410,716 | 450,143 | 450,143 | ||||||||||||

| Loans and receivables | ||||||||||||||||

| Accounts receivable | 901,686 | 901,686 | 79,334 | 79,334 | ||||||||||||

| Financial Liabilities | ||||||||||||||||

| Other financial liabilities | ||||||||||||||||

| Bank indebtedness | 50,000 | 50,000 | 48,920 | 48,920 | ||||||||||||

| Accounts payable and accrued liabilities | 5,564,071 | 5,564,071 | 2,833,559 | 2,833,559 | ||||||||||||

| Purchase price payable | - | - | 1,500,000 | 1,500,000 | ||||||||||||

| Transaction taxes payable | 129,155 | 129,155 | 105,207 | 105,207 | ||||||||||||

| Interest payable | 72,243 | 72,243 | - | - | ||||||||||||

| Loan payable | 3,373,960 | 3,373,960 | 2,000,000 | 2,000,000 | ||||||||||||

Cash and performance bond are measured based on Level 1 inputs of the fair value hierarchy on a recurring basis.

The carrying value of accounts receivable, bank indebtedness and accounts payable and accrued liabilities, purchase price payable, transaction taxes payable, loan payable and interest payable approximate their fair value because of the short-term nature of these instruments. The Company assessed that there were no indicators of impairment for these financial instruments.

Financial instruments that potentially subject the Company to concentrations of credit risk consist primarily of cash and accounts receivable. The Company places its cash with high quality financial institutions and limits the amount of credit exposure with any one institution. Accounts receivable consist of input tax credits receivable and are not considered subject to significant risk.

The Company currently maintains a substantial portion of its day-to-day operating cash balances at financial institutions. At June 30, 2017, the Company had total cash balances of $667,125 (December 31, 2016- $108,272) at financial institutions, where $0 (zero) (December 31, 2016- $0 (zero)) is in excess of federally insured limits.

17. Segmented Information

All of the Company's operations are in the mineral properties exploration industry with its principal business activity in mineral exploration. The Company conducts its activities primarily in Argentina. All of the Company's long-lived assets are located in Argentina.

Hunt Mining Corp.

Notes to the Consolidated Interim Financial Statements (Unaudited)

(Expressed in US Dollars)

Six month period ended June 30, 2017 and 2016

18. Commitments and Provision

| a) | On March 18, 2011, a lawsuit was filed against the Company and its subsidiaries by a former director and consultant "the Consultant". The lawsuit claimed that the Consultant was an employee of the Company, not a consultant, since 2006. The total value of the claim was US$249,041, including wages, alleged bonus payments, interest and penalties. The consolidated interim financial statements include a provision of $250,000 at June 30, 2017 (December 31, 2016- $250,000). Management intends to defend the Company and its subsidiaries to the fullest extent possible. |

As of June 30, 2017, the Company has been notified that amounts totaling 1,026,704 pesos ($63,891) ($64,610 as at December 31, 2016) was withheld from its Argentine bank account and placed in escrow with the Court pending the outcome of the lawsuit filed on March 18, 2011 against the Company.

| b) | On October 31, 2011, the Company signed an agreement with the owners of the Piedra Labrada Ranch for the use and lease of facilities on the same premises as the Company's La Josefina facilities. The initial term was for three years beginning November 1, 2011 and ended on October 31, 2014, including annual commitments of $60,000. The Company extended this agreement on April 30, 2015 for three years. |

19. Silver Recovery

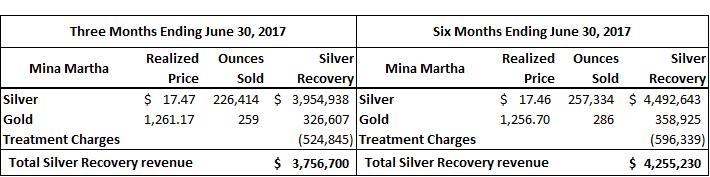

Silver recovery includes the sales from concentrate sold during the three months ended June 30, 2017 and the six months ended June 30, 2017 from the Martha Mine project. Sales were $3,756,700 and $4,255,230 respectively. It also includes $190,269 from deferred advances for tailing sales from the Martha Mine project. Silver recovery revenues have been reported net of direct operating expenses of $1,106,050 and $1,585,753 for the three and six months ended June 30, 2017. Accounts receivable include $427,230 for the sales of concentrate.

20. Subsequent Events

Subsequent to June 30, 2017, the Company had sales of concentrate in the amount of $1,025,869 and made principle repayment on the Ocean Partner loan of $511,605.

Subsequent to June 30, 2017, the President, CEO and Executive Chairman loaned an additional $500,000 to the Company. The loan is unsecured with interest at 8% per annum and is due on demand.

| ITEM 2. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion of the operating results, corporate activities and financial condition of Hunt Mining Corp. (hereinafter referred to as "we", "us", "Hunt Mining", "HMX", or the "Company") and its subsidiaries provides an analysis of the operating and financial results between December 31, 2016 and June 30, 2017 and a comparison of the material changes in our results of operations and financial condition between the six-month period ended June 30, 2016 and the six-month period ended June 30, 2017. This discussion should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations included in our Annual Report on Form 10-K for the year ended December 31, 2016.

This discussion and analysis contains forward-looking statements that involve risks, uncertainties and assumptions. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of many factors, including, but not limited to, those set forth under the heading "Risk Factors and Uncertainties" in our Annual Report on Form 10-K for the year ended December 31, 2016, and elsewhere in this Quarterly Report on Form 10-Q.

The interim statements have been prepared in accordance with US Generally Accepted Accounting Principles ("US GAAP") as required under U.S. federal securities laws applicable to the Company, and as permitted under applicable Canadian securities laws. The Company is a reporting company under applicable securities laws in Canada and the United States. The reporting currency used in our financial statements is the United States Dollar.

The information contained within this report is current as of August 11, 2017 unless otherwise noted. Additional information relevant to the Company's activities can be found on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates

The Company uses Canadian Institute of Mining, Metallurgy and Petroleum definitions for the terms "proven reserves", "probable reserves", "measured resources", "indicated resources" and inferred resources. U.S. investors are cautioned that while these terms are recognized and required by Canadian regulations, including National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"), the U.S. Securities and Exchange Commission ("SEC") does not recognize them. Canadian mining disclosure standards differ from the requirements of the SEC under SEC Industry Guide 7, and reserve and resource information referenced in this Form 10-Q may not be comparable to similar information disclosed by companies reporting under U.S. standards. In particular, and without limiting the generality of the foregoing, the term "resource" does not equate to the term "reserve". Under United States standards, mineralization may not be classified as a "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. The SEC's disclosure standards normally do not permit the inclusion of information concerning "measured mineral resources" or "indicated mineral resources" or other descriptions of the amount of mineralization in mineral deposits that do not constitute "reserves" by U.S. standards in documents filed with the SEC. Disclosure of "contained ounces" in a resource estimate is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute "reserves" by SEC standards as tonnage and grade without reference to unit measures. The requirements of NI 43- 101 for identification of "reserves" are also not the same as those of the SEC, and reserves in compliance with NI 43-101 may not qualify as "reserves" under SEC standards.

Cautionary Note Regarding Forward-Looking Statements

Certain statements made in this Quarterly Report on Form 10-Q may constitute "forward-looking statements about the Company and its business. Forward looking statements are statements that are not historical facts and include, but are not limited to, reserve and resource estimates, estimated value of the project, projected investment returns, anticipated mining and processing methods for the project, the estimated economics of the project, anticipated Hunt Mining recoveries, production rates, grades, estimated capital costs, operating cash costs and total production costs, planned additional processing work and environmental permitting. The forward-looking statements in this report are subject to various risks, uncertainties and other factors that could cause the Company's actual results or achievements to differ materially from those expressed in or implied by forward looking statements. These risks, uncertainties and other factors include, without limitation risks related to uncertainty of Hunt Mining property valuation assumptions; uncertainties related to raising sufficient financing to fund the project in a timely manner and on acceptable terms; changes in planned work resulting from logistical, technical or other factors; the possibility that results of work will not fulfill expectations and realize the perceived potential of the Company's properties; uncertainties involved in the estimation of Hunt Mining reserves and resources; the possibility that required permits may not be obtained on a timely manner or at all; the possibility that capital and operating costs may be higher than currently estimated and may preclude commercial development or render operations uneconomic; the possibility that the estimated recovery rates may not be achieved; risk of accidents, equipment breakdowns and labor disputes or other unanticipated difficulties or interruptions; the possibility of cost overruns or unanticipated expenses in the work program; risks related to projected project economics, recovery rates, and estimated NPV and anticipated IRR and other factors identified in the Company's SEC filings and its filings with Canadian securities regulatory authorities. Forward-looking statements are based on the beliefs, opinions and expectations of the Company's management at the time they are made, and other than as required by applicable securities laws, the Company does not assume any obligation to update its forward-looking statements if those beliefs, opinions or expectations, or other circumstances, should change.

Hunt Mining Corporation – Corporate Overview

Hunt Mining Corp. (the "Company" or "Hunt"), is a mineral mining and exploration company incorporated on January 10, 2006 under the laws of Alberta, Canada and, together with its subsidiaries, is engaged in the exploration and development of mineral properties in Santa Cruz Province, Argentina.

Effective November 6, 2013, the Company continued from the Province of Alberta to the Province of British Columbia. The Company's registered office is located at 25th Floor, 700 West Georgia Street, Vancouver, B.C. V7Y 1B3. The Company's head office is located at 23800 E Appleway Avenue, Liberty Lake, Washington, 99019 USA.

The interim consolidated financial statements include the accounts of the following subsidiaries after elimination of intercompany transactions and balances:

| Corporation | Incorporation | Percentage ownership | Business Purpose |

| Cerro Cazador S.A. | Argentina | 100% | Holder of Assets and Exploration Company |

| Ganadera Patagonia SRL | Argentina | 40% | Land Holding Company |

| 1494716 Alberta Ltd. | Alberta, Canada | 100% | Nominee Shareholder |

| Hunt Gold USA LLC | Washington, USA | 100% | Management Company |

The Company's activities include the exploration, development and mining of mineral properties in Argentina. On the basis of information to date, the Company has not yet determined whether the exploration properties contain economically recoverable ore reserves. The underlying value of the mineral properties is entirely dependent upon the existence of economically recoverable reserves, the ability of the Company to obtain the necessary financing to complete development and upon future profitable production or a sale of these properties.

During the second quarter of 2017 our focus has been on continued development of the Mina Martha property and mining selected remnants for shipments of concentrate.

Principal Property Review La Josefina Property

The La Josefina property was our primary exploration property because it occupies 52,800 hectares and approximately 90% of the nearly 65,000 meters drilled by us. It is located in North-Central Santa Cruz province in southern Argentina, within the region known as Patagonia.

The Company purchased the Mina Martha property in May 2016 and has focused our efforts on restoring the mill and property and mining selected mineralized remnants. The La Josefina property has been put on a care and maintenance mode and minimal activity has taken place and minimal exploration activity is planned in the immediate future.

La Valenciana Property

La Valenciana is the Company's second most advanced exploration project. The property is located on the central- north area of the Santa Cruz Province, Argentina, and is located 25 kilometers to the west of the Company's main Piedra Labrada base camp. The project encompasses an area of approximately 29,600 hectares, and is contiguous to the Company's La Josefina property to the east. The La Valenciana project is comprised of 11 Manifestations of Discovery covering segments of Estancia Canodon Grande, Estancia Flecha Negra, Estancia Las Vallas, Estancia La Florentina, Estancia La Valenciana and Estancia La Modesta (inactive ranches). The La Valenciana property has been put on a care and maintenance mode and minimal activity has taken place and minimal exploration activity is planned in the immediate future.

Bajo Pobré Property

The Bajo Pobré property covers 3,190 hectares and is mainly on the Estancia Bajo Pobré. The property is located 90 kilometers south of the town of Las Heras.