Exhibit 99.1

PATAGONIA GOLD CORP.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the three and nine months ended September 30, 2021

November 29, 2021

The following management’s discussion and analysis (“MD&A”) of Patagonia Gold Corp. (hereinafter referred to as the “Company” or “Patagonia”), formerly Hunt Mining Corp. (“Hunt”) and its subsidiaries provides an analysis of the operating and financial results for the three and nine months ended September 30, 2021 and a comparison of the material changes in our results of operations and financial condition between the year ended December 31, 2020 and the three and nine months ended September 30, 2021. This MD&A should be read in conjunction with the Company’s unaudited condensed interim consolidated financial statements (“interim financial statements”) for the three and nine months ended September 30, 2021, annual audited consolidated financial statements for the year ended December 31, 2020 and the related MD&A.

These statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). Upon the reverse acquisition with Patagonia Gold Corp, Patagonia Gold Limited became the ongoing entity for accounting purposes and Patagonia Gold Limited had to switch to reporting under accounting principles generally accepted in the United States of America (“US GAAP”) as Patagonia Gold Corp. is a registrant with the U.S. Securities and Exchange Commission (“SEC”). Effective June 30, 2020, the Company obtained “foreign private issuer” status in accordance with SEC guidelines and became eligible to satisfy its reporting requirements using IFRS.

This MD&A includes certain non-IFRS financial performance measures. For a detailed description of these measures, please see “Non-IFRS Financial Performance Measures” section. The amounts presented in this MD&A are in thousands ($’000) of U.S. dollars, except share, per share, per unit amounts and unless otherwise noted.

The Company’s head office and principal business address is Av. Libertador 498 Piso 26, Buenos Aires, Argentina, C1001ABR and the registered office address is 2200 HSBC Building, 885 West Georgia Street, Vancouver, British Columbia, V6C 3E8. The Company’s common shares trade on the TSX Venture Exchange (the “Exchange”), under the symbol PGDC. Additional information relevant to the Company’s activities can be found on their website at http://patagoniagold.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Management’s Responsibility for Financial Reporting

The interim financial statements have been prepared by management in accordance with IFRS and have been approved by the Company’s board of directors (the “Board”). The integrity and objectivity of the interim financial statements are the responsibility of management. In addition, management is responsible for ensuring that the information contained in the MD&A is consistent where appropriate, with the information contained in the interim financial Statements.

The financial statements may contain certain amounts based on estimates and judgments. Management has determined such amounts on a reasonable basis to ensure that the financial statements are presented fairly in all material respects.

As the Company is a Venture Issuer (as defined under under National Instrument 52-109 Certification of Disclosure in Issuers’ Annual and Interim Filings) (“NI 52-109”), the Company and management are not required to include representations relating to the evaluation, design, establishment and/or maintenance of disclosure controls and procedures (“DC&P”) and/or Internal Controls over Financial Reporting (“ICFR”), as defined in NI 52-109, nor has it completed such an evaluation. Inherent limitations on the ability of the certifying officers to design and implement on a cost-effective bases DC&P and ICFR for the issuer may result in additional risks of quality, reliability, transparency and timeliness of interim and annual filings and other reports provided under securities legislation.

Cautionary Note on Forward-Looking Information

This MD&A contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws of Canada and the United States of America (collectively referred to as “forward-looking information”) which relate to future events or the Company’s future performance and may include, but are not limited to, statements about strategic plans, spending commitments, future operations, results of exploration, anticipated financial results, future work programs, capital expenditures and expected working capital requirements. Often, but not always, forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “continues”, “forecasts”, “projects”, “predicts”, “intends”, “anticipates” or “believes”, or variations of, or the negatives of, such words and phrases, or state that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved.

| - 1 - |

Readers are cautioned not to place undue reliance on forward looking information and there can be no assurance that forward looking information will prove to be accurate as the Company’s actual results, performance or achievements may differ materially from any future results, performance or achievements expressed or implied by such forward-looking information if known or unknown risks, uncertainties or other factors affect the Company’s business, or if the Company’s estimates or assumptions prove inaccurate. Therefore, the Company cannot provide any assurance that forward-looking information will materialize. Factors that could cause results or events to differ materially from current expectations expressed or implied by the forward-looking information, include, but are not limited to: fluctuations in the currency markets (such as the Canadian Dollar, Chilean Peso, Great Britain Pound and the United States Dollar); changes in national and local government, legislation, taxation, controls, regulations and political or economic developments in Canada and Argentina or other countries in which the Company may carry on business in the future; operating or technical difficulties in connection with exploration and development activities; risks and hazards associated with the business of mineral exploration and development (including environmental hazards or industrial accidents); risks relating to the credit worthiness or financial condition of suppliers and other parties with whom the Company does business; the presence of laws and regulations that may impose restrictions on mining, including those currently enacted in Argentina; employee relations; relationships with and claims by local communities; availability and increasing costs associated with operational inputs and labour; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses, permits and approvals from government authorities; business opportunities that may be presented to, or pursued by, the Company; challenges to, or difficulty in maintaining, the Company’s title to properties; risks relating to the Company’s ability to raise funds; and the factors identified under “Risk Factors” in this MD&A.

The forward looking information contained in this MD&A are based upon assumptions management believes to be reasonable including, without limitation: financing will be available for future exploration, development and operating activities; the actual results of the Company’s development and exploration activities will be favourable or at least consistent with management’s expectations; operating, development and exploration costs will not exceed management’s expectations; all requisite regulatory and governmental approvals for development projects and other operations will be received on a timely basis upon terms acceptable to the Company, and applicable political and economic conditions will be favourable to the Company such as the continuing support for mining by local governments in Argentina; the price of gold and/or other applicable metals and applicable interest and exchange rates will be favourable to the Company or at least consistent with management’s expectations; no title disputes will exist with respect to the Company’s properties; debt and equity markets and other applicable economic conditions will be favourable to the Company; the availability of equipment and qualified personnel to advance exploration projects and; the execution of the Company’s existing plans and further exploration and development programs for its projects, which may change due to changes in the views of the Company or if new information arises which makes it prudent to change such plans or programs.

All forward-looking-information contained in this MD&A is given as of the date hereof and is based upon the opinions and estimates of management and information available to management as at the date hereof. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by law.

Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates

Unless otherwise indicated, all reserve and resource estimates used by the Company have been prepared in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum Definition Standards for Mineral Resources and Mineral Reserves (“CIM Definition Standards”). NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Accordingly, information contained in this MD&A providing descriptions of the Company’s mineral deposits in accordance with NI 43-101 may not be comparable to similar information made public by other U.S. companies subject to the United States federal securities laws and the rules and regulations thereunder.

Pursuant to CIM Definition Standards, “Inferred mineral resources” are that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Such geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. However, it is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource is economically or legally mineable. Effective February 25, 2019, the SEC adopted new mining disclosure rules under subpart 1300 of Regulation S-K of the United States Securities Act of 1933, as amended (the “SEC Modernization Rules”), with compliance required for the first fiscal year beginning on or after January 1, 2021. The SEC Modernization Rules replace the historical property disclosure requirements included in SEC Industry Guide 7. As a result of the adoption of the SEC Modernization Rules, the SEC now recognizes estimates of “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources”. In addition, the SEC has amended its definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” to be substantially similar to corresponding definitions under the CIM Definition Standards. While the SEC Modernization Rules are purported to be “substantially similar” to the CIM Definition Standards, readers are cautioned that there are differences between the SEC Modernization Rules and the CIM Definition Standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as “proven mineral reserves”, “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same had the Company prepared the reserve or resource estimates under the standards adopted under the SEC Modernization Rules.

| - 2 - |

The Company

On July 24, 2019, the Company and Patagonia Gold Limited (“PGL”) [formerly Patagonia Gold PLC (“PGP”)] completed a reverse acquisition (or reverse takeover, the “RTO”) resulting in Hunt acquiring all issued shares of common stock of PGP in exchange for common shares of Hunt on the basis of 10.76 Hunt shares for each PGP share. Hunt issued 254,355,192 common shares to the shareholders of PGP representing an ownership interest of approximately 80%. The operating name of Hunt Mining Corp. was changed to Patagonia Gold Corp. For more information, see note 25 of the December 31, 2020 audited financial statements.

Patagonia is a mineral exploration and production Company incorporated on January 10, 2006 under the laws of Alberta, Canada and, together with its subsidiaries, is engaged in the exploration of mineral properties and exploitation of mineral resources and mineral reserves in the Santa Cruz, Rio Negro and Chubut Provinces of Argentina.

The interim financial statements are presented on a consolidated basis and include the accounts of the Company, its wholly owned and majority owned subsidiary:

Corporation |

Incorporation | Percentage ownership | Functional currency | Business purpose | ||||

Patagonia Gold S.A. (“PGSA”) | Argentina | 95.3 | US$ | Production and Exploration Stage | ||||

| Minera Minamalu S.A. | Argentina | 100 | US$ | Exploration Stage | ||||

| Huemules S.A. | Argentina | 100 | US$ | Exploration Stage | ||||

| Leleque Exploración S.A. | Argentina | 100 | US$ | Exploration Stage | ||||

| Patagonia Gold Limited (formerly Patagonia Gold PLC) | UK | 100 | GBP$ | Holding | ||||

| Minera Aquiline S.A.U. | Argentina | 100 | US$ | Exploration Stage | ||||

| Patagonia Gold Canada Inc. | Canada | 100 | CAD$ | Holding | ||||

| Patagonia Gold Chile S.C.M. | Chile | 100 | CH$ | Exploration Stage | ||||

| Ganadera Patagonia S.R.L. | Argentina | 100 | US$ | Land Holding | ||||

| 1272680 B.C. Ltd (formerly 1494716 Alberta Ltd.) | Canada | 100 | CAD$ | Nominee Shareholder |

The Company’s activities include the exploration for and production of minerals from properties in Argentina. On the basis of information to date, properties where it has not yet been determined if economically recoverable reserves exist are classified as exploration-stage. Properties where economically recoverable reserves exist and are being exploited are classified as production-stage. The underlying value of the mineral properties is entirely dependent upon the existence of reserves, the ability of the Company to obtain the necessary financing to complete development and upon future profitable production or a sale of these properties.

On some properties, ongoing production and sales of gold and silver are being undertaken without established mineral resources or reserves and the Company has not established the economic viability of the operations. As a result, there is increased uncertainty and economic risks of failure associated with these production activities. Despite the sale of gold and silver, these projects remain in the exploration stage because management has not established proven or probable reserves required to be classified in either the development or production stage.

| - 3 - |

Summary of Consolidated Results of Operations ($’000’s)

| Three months ended September 30, | Nine months ended September 30, | |||||||||||||||||||||||||||||||

| (in $000’s, except ounces and per share amounts) | 2021 | 2020 | Change | %Change | 2021 | 2020 | Change | %Change | ||||||||||||||||||||||||

| Operational results | ||||||||||||||||||||||||||||||||

| Total gold equivalent ounces – produced (1) | 2,175 | 2,020 | 155 | 8 | % | 6,865 | 7,382 | (517 | ) | (7 | )% | |||||||||||||||||||||

| Total gold equivalent ounces – sold (1) | �� | 3,223 | 3,277 | (54 | ) | (2 | )% | 7,878 | 9,279 | (1,401 | ) | (15 | )% | |||||||||||||||||||

| Financial results | ||||||||||||||||||||||||||||||||

| Revenue | $ | 5,758 | $ | 6,549 | $ | (791 | ) | (12 | )% | $ | 14,233 | $ | 16,469 | $ | (2,236 | ) | (14 | )% | ||||||||||||||

| Cost of sales | $ | 4,278 | $ | 4,213 | $ | 65 | 2 | % | $ | 10,061 | $ | 10,880 | $ | (819 | ) | (8 | )% | |||||||||||||||

| Exploration expenses | $ | 1,432 | $ | 678 | $ | 754 | 111 | % | $ | 3,204 | $ | 1,792 | $ | 1,412 | 79 | % | ||||||||||||||||

| Repair and maintenance | $ | 126 | $ | - | $ | 126 | N/A | $ | 514 | $ | - | $ | 514 | N/A | ||||||||||||||||||

| Administrative expenses | $ | 1,227 | $ | 1,315 | $ | (88 | ) | (7 | )% | $ | 4,188 | $ | 3,810 | $ | 378 | 10 | % | |||||||||||||||

| Interest expense | $ | 377 | $ | 615 | $ | (238 | ) | (39 | )% | $ | 959 | $ | 1,957 | $ | (998 | ) | (51 | )% | ||||||||||||||

| Net loss | $ | (1,712 | ) | $ | (1,041 | ) | $ | (671 | ) | (64 | )% | $ | (4,575 | ) | $ | (1,775 | ) | $ | (2,800 | ) | (158 | )% | ||||||||||

| Net loss per share – basic and diluted | $ | (0.004 | ) | $ | (0.003 | ) | $ | (0.001 | ) | (33 | %) | $ | (0.010 | ) | $ | (0.006 | ) | $ | (0.004 | ) | (73 | )% | ||||||||||

| (1) | Gold equivalent ounces include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market price for the commodities each period. The ratio for three months ended September 30, 2021 was 76.10:1 (2020 – 80.97:1). The ratio for the nine months ended September 30, 2021 was 72.51:1 (2020 – 87.80:1). |

Three months ended September 30, 2021 and 2020

Total production increased during the three months ended September 30, 2021 due to the re-handling of the material on the Cap-Oeste’s leach pad to regenerate the solution percolation and generate new channels of circulation of solution and improve the recovery. Additionally, improved leach kinetics were achieved following some chemical changes to the chemistry of the recovery process.

The Company earned total revenue of $5,758 during the three months ended September 30, 2021 compared to $6,549 during the same period in 2020. Revenue decreased mainly due to decreased in gold prices during the period compared to the same period in 2020.

Cost of sales were $4,278 during the three months ended September 30, 2021 compared to $4,213 during the same period in 2020. Cost of sales was consistent as the sale of gold equivalent ounces remained consistent during the period compared to the same period in 2020.

The Company incurred exploration expenses of $1,432 during the three months ended September 30, 2021 compared to $678 during the same period in 2020. The increase in exploration expenses was due to the Company’s increased exploration program for 2021.

The Company incurred repair and maintenance expense of $126 during the three months ended September 30, 2021 compared to $Nil during the same period in 2020. The repair and maintenance expense during the period related to maintenance work at the Mina Martha Plant.

The Company incurred administrative expenses of $1,227 during the three months ended September 30, 2021 compared to $1,315 during the same period in 2020. The decrease in administrative expenses was due to lower professional fees and depreciation of property, plant and equipment.

The Company incurred interest expense of $377 during the three months ended September 30, 2021 compared to $615 during the same period in 2020. The decrease in interest expense was due to debt settled by issuing shares in October 2020.

Net loss for the three months ended September 30, 2021 was $1,712 compared to $1,041 during the same period in 2020. Net loss increased due to decrease in gross profits and increase in exploration expenses during the current period compared to the same prior period. The increase in net loss was partially offset by foreign exchange gain and other income, which consists of gain on disposition of securities. See note 22 of the interim financial statements for more information.

Nine months ended September 30, 2021 and 2020

Total production decreased during the nine months ended September 30, 2021 as the Company had residual heap leach operations at Lomada de Leiva (“Lomada”) and Cap-Oeste since February 2019, which has been declining due to the depletion in the pads from ongoing leaching. In November 2020 the Company restarted the mining operation at Lomada and started placing new material on the leach pad. Despite production decreasing quarter over quarter from the residual leach pads, the Company expects that production will stabilize and start showing the benefit from placing new material on the leach pad at Lomada. Production was also lower as the Company has not produced concentrate from Mina Martha since April 2020.

| - 4 - |

The Company earned total revenue of $14,233 during the nine months ended September 30, 2021 compared to $16,469 during the same period in 2020. Revenue decreased due to decrease in gold equivalent ounces sold during the period compared to the same period in 2020. Gold prices remained consistent during the nine months ended September 30, 2021 compared to the same period in 2020.

Cost of sales were $10,061 during the nine months ended September 30, 2021 compared to $10,880 during the same period in 2020. Cost of sales stayed consistent due to higher cost of production during the period compared to the same period in 2020.

The Company incurred exploration expenses of $3,204 during the nine months ended September 30, 2021 compared to $1,792 during the same period in 2020. The increase in exploration expenses was due to the Company’s increased exploration program for 2021.

The Company incurred repair and maintenance expense of $514 during the nine months ended September 30, 2021 compared to $Nil during the same period in 2020. The repair and maintenance expense during the period related to maintenance work at the Mina Martha Plant.

The Company incurred administrative expenses of $4,188 during the nine months ended September 30, 2021 compared to $3,810 during the same period in 2020. The increase in administrative expenses was due to the increase in Argentine statutory taxes related to the interest paid overseas to Patagonia Gold Limited and increase in depreciation of mineral properties.

The Company incurred interest expense of $959 during the nine months ended September 30, 2021 compared to $1,957 during the same period in 2020. The decrease in interest expense was due to debt settled by issuing shares in October 2020.

Net loss for the nine months ended September 30, 2021 was $4,575 compared to $1,775 during the same period in 2020. Net loss increased due to decrease in gross profits, increase in exploration and administrative expenses and decrease in other income during the current period compared to the same prior period. Other income consists of gain on disposition of securities. See note 22 of the interim financial statements for more information.

Cash flows for the nine months ended September 30, 2021 and 2020 ($’000’s)

The Company generated cash of $1,812 from operating activities for the nine months ended September 30, 2021 compared to cash generated of $389 during the same period in 2020. The increase in cash generated from operating activities during 2021 was primarily due to higher accounts payable and accrued liabilities at period end.

Cash used in investing activities for the nine months ended September 30, 2021 was $3,972 compared to $1,506 for the same period in 2020. The increase in cash used in investing activities was a result of higher additions to the mineral properties as the Company restarted mining operations at Lomada in November 2020, following receipt of a preliminary permit on October 7, 2020. Mining operations at Lomada had been closed since February 2019. The costs related to the development of the new pit were capitalized as mineral properties.

Cash generated from financing activities for the nine months ended September 30, 2021 was $1,840 compared to $778 used in financing activities during the same period in 2020. The increase in cash generated from financing activities was primarily due to the private placement completed in March 2021.

Financial Position ($’000’s)

Cash

The Company has cash on hand of $592 as of September 30, 2021 compared to $819 as of December 31, 2020.

Receivables

Current receivables are $1,964 as of September 30, 2021 compared to $2,041 as of December 31, 2020. The decrease in current receivables is a result of the decrease in trade and other receivables. The decrease in receivables was partially offset by increase in VAT recoverable during the nine months ended September 30, 2021.

Non-current receivables are $3,970 as of September 30, 2021 compared to $3,544 as of December 31, 2020. The increase in non-current receivables is a result of the increase in VAT recoverable and other recoverable costs during the nine months ended September 30, 2021.

| - 5 - |

Inventories

The Company has inventories of $3,369 as of September 30, 2021 compared to $3,289 as of December 31, 2020. The increase in inventories was mainly due to higher materials and supplies which was offset by lower gold held on carbon due to the inventory write down of $670 during the nine months ended September 30, 2021.

Property, plant and equipment (“PPE”)

The Company has PPE of $12,410 as of September 30, 2021 compared to $13,233 as of December 31, 2020. The decrease in PPE was a result of the depreciation charge which was partially offset by capital additions.

Bank indebtedness

The Company has bank indebtedness of $4,644 as of September 30, 2021 compared to $9,636 as of December 31, 2020. The decrease in bank indebtedness was a result paying down the existing lines of credit using the funds raised from the March 2021 private placement.

Accounts payable and accrued liabilities

The Company has accounts payable and accrued liabilities of $6,655 as of September 30, 2021 compared to $4,384 as of December 31, 2020. The increase in accounts payable and accrued liabilities was a result of the restart of mining operations at Lomada.

Accounts payable with related parties

The Company has accounts payable with related parties of $197 as of September 30, 2021 compared to $144 as of December 31, 2020. The increase in accounts payable with related parties is a result of remuneration, fees and interest expenses incurred during the period.

Loan payable and current portion of long-term debt

The Company has loan payable and current portion of long-term debt of $222 as of September 30, 2021 compared to $363 as of December 31, 2020.

Long term debt

The Company has non-current portion of total long-term debt of $15,330 as of September 30, 2021 compared to $14,917 as of December 31, 2020. This includes $15,330 payable to related parties as of September 30, 2021 compared to $14,808 as of December 31, 2020.

In February 2019, the Company announced that Cantomi Uruguay S.A., a company owned and controlled by the Company’s Non-Executive Chairman, Carlos J. Miguens, had provided a two-year $15,000 loan facility that will be utilized to fund the Company’s activities going forward, while the review of the Cap-Oeste underground option is ongoing together with the Feasibility Study of its flagship Calcatreu project. On November 16, 2020, the maturity of the loan was extended to December 31, 2022. All other terms of the loan remain unchanged. As of September 30, 2021, there was $15,330 of principal and interest owing under this loan facility compared to $14,808 as of December 31, 2020.

As of February 2021, Cantomi Uruguay S.A. is no longer a related party as Carlos Miguens no longer has control of the company.

Summary of Segmented Results of Operations ($’000’s)

Cap-Oeste

Cap-Oeste produced a total of 5,266 gold equivalent ounces (3,159 ounces of gold and 148,781 ounces of silver) during the nine months ended September 30, 2021 compared to 4,807 gold equivalent ounces (3,581 ounces of gold and 111,209 ounces of silver) during the same period in 2020. Production increased due to the re-handling of the material on the leach pad to regenerate the solution percolation and generate new channels of circulation of solution and improve the recovery. Additionally, improved leach kinetics were achieved following some chemical changes to the chemistry of the recovery process.

The cash costs of production for nine months ended September 30, 2021 were $679 per ounce1 and $713 per ounce1 including depreciation and amortization compared to $695 per ounce1 and $756 per ounce1 during the same period in 2020. The decrease in cash cost of production per ounce was due to the increase in production.

1 See Non-IFRS Financial Performance Measures

| - 6 - |

A total of 6,132 gold equivalent ounces (3,832 ounces of gold and 166,805 ounces of silver) were sold during the nine months ended September 30, 2021 at an average gross price of $1,807 per ounce1. During the same period in 2020, a total of 5,668 gold equivalent ounces (4,194 ounces of gold and 131,338 ounces of silver) were sold at an average gross price of $1,766 per ounce1.

Cap-Oeste generated revenues of $11,081 during the nine months ended September 30, 2021 compared to $10,008 during the same period in 2020. The increase in revenues was due to the higher gold prices and higher gold equivalent ounces produced and sold during the nine months ended September 30, 2021 compared to the same period in 2020.

Cost of sales were $5,643 during the nine months ended September 30, 2021 compared to $5,510 during the same period in 2020. The increase in cost of sales was due to higher gold equivalent ounces sold during the nine months ended September 30, 2021 compared to the same period in 2020.

Administration expenses of $301 were incurred during the nine months ended September 30, 2021 compared to $394 during the same period in 2020. Administrative expenses consisted of depreciation of the mineral properties.

Lomada de Leiva Project (“Lomada”)

Lomada produced a total of 1,599 ounces of gold during the nine months ended September 30, 2021 compared to 2,219 ounces of gold during the same period in 2020. Production decreased as the Company had residual heap leach operations at Lomada since February 2019, which has been declining due to the depletion in the pads from ongoing leaching. Following receipt of a preliminary permit on October 7, 2020, in November 2020 the Company restarted the mining operation at Lomada which had been previously closed since in February 2019 and started placing new material on the leach pad. Despite production decreasing quarter over quarter from the residual leach pads, the Company expects that production will stabilize and start showing the benefit from placing new material on the leach pad at Lomada.

The cash costs of production for the nine months ended September 30, 2021 were $2,384 per ounce1 and $2,532 per ounce1 including depreciation and amortization compared to $650 per ounce1 and $757 per ounce1 during the same period in 2020. The increase in cash costs is due to the decrease in production and the increase in costs due to the restart of mining operations.

A total of 1,746 gold equivalent ounces were sold during the nine months ended September 30, 2021 at an average gross price of $1,805 per ounce1. During the same period in 2020, 3,225 gold equivalent ounces were sold at an average gross price of $1,709 per ounce1.

Lomada generated revenues of $3,152 during the nine months ended September 30, 2021 compared to $5,511 during the same period in 2020. The decrease in revenue was due to lower amounts of gold equivalent ounces sold, partially offset by the increase in gold price during 2021.

Cost of sales were $4,418 during the nine months ended September 30, 2021 compared to $3,370 during the same period in 2020. The increase in cost of sales was due to the increase in costs due to the restart of mining operations. During the nine months ended September 30, 2021, the net realizable value of the inventory was less than the costs incurred in establishing the gold held on carbon and the Company recorded an inventory write down of $670 (2020 - $Nil) under cost of sales.

Administrative expenses of $383 were incurred during the nine months ended September 30, 2021 compared to $102 during the same period in 2020. Administrative expenses consisted of depreciation of the mineral properties.

Martha and La Josefina Projects

There was no production at Martha during the nine months ended September 30, 2021 as the Company did not produce concentrate from Martha after April 2020. During the nine months ended September 30, 2020, Martha produced a total of 356 gold equivalent ounces (49 ounces of gold and 29,838 ounces of silver). Operations at Martha remain on care and maintenance while the Company continues to explore the property.

The cash costs of production for the nine months ended September 30, 2020 were $1,421 per ounce1 and $1,601 per ounce1 including depreciation and amortization.

1 See Non-IFRS Financial Performance Measures

| - 7 - |

Martha generated revenues of $Nil during the nine months ended September 30, 2021 compared to $950 during the same period in 2020.

Cost of sales were $Nil during the nine months ended September 30, 2021 compared to $2,000 during the same period in 2020.

Exploration expenses of $70 were incurred during the nine months ended September 30, 2021 compared to $64 during the same period in 2020.

The Company incurred repair and maintenance expense of $514 during the nine months ended September 30, 2021 compared to $Nil during the same period in 2020. The repair and maintenance during the period related to maintenance work at the Mina Martha Plant.

Calcatreu Project

Exploration expenses of $1,256 were incurred during the nine months ended September 30, 2021 compared to $671 during the same period in 2020. The increase in exploration expenses was due to work on the Baseline Study and continued field work, which includes drilling, surface exploration, geophysics and hydrologic studies.

Administration expenses of $192 were incurred during the nine months ended September 30, 2021 compared to $175 during the same period in 2020.

Argentina, Uruguay and Chile

This segment includes the results from the Company’s work on the La Manchuria and La Sarita projects in Argentina, the San José Project in Uruguay and general corporate activities. This segment does not generate revenues and includes costs that are not directly related to other mining properties that are reported as separate segments.

Exploration expenses of $1,878 were incurred during the nine months ended September 30, 2021 compared to $1,057 during the same period in 2020. Exploration expenses increased due to the drilling program in Monte Leon and Tornado y Huracán projects, geological mapping and sampling related to projects included in this segment.

Administration expenses of $2,110 were incurred during the nine months ended September 30, 2021 compared to $1,873 during the same period in 2020. The increase in administrative expenses was mainly due to the increase in Argentine statutory taxes related to the interest paid overseas to Patagonia Gold Limited.

Interest expense of $360 was incurred during the nine months ended September 30, 2021 compared to $377 during the same period in 2020. The decrease in interest expense was due to the decrease in loans with Argentinian banks and bank indebtedness.

United Kingdom

This segment includes the results of Patagonia Gold Limited (“PGL”) (formerly Patagonia Gold PLC) which is a holding company and does not generate any revenues.

Administration expenses of $146 were incurred during the nine months ended September 30, 2021 compared to $106 during the same period in 2020. Administrative expenses increased as an increase in professional fees.

Interest expense of $359 was incurred during the nine months ended September 30, 2021 compared to $479 during the same period in 2020. The decrease in interest expense was due to the repayment of bank indebtedness.

North America

This segment includes the results of Patagonia Gold Corp (“PGC”), Patagonia Gold Canada Inc and 1272680 B.C. Ltd (“BC”) (formerly 1494716 Alberta Ltd.).

These entities are holding companies and do not generate any revenues. PGC and BC were acquired as part of the reverse acquisition during 2019 and their results of operations prior to the reverse acquisition are not incorporated in the financial statements.

Administration expenses of $673 were incurred during the nine months ended September 30, 2021 compared to $817 during the same period in 2020. The decrease in administration expenses was primarily due to lower accounting and legal fees during the period.

| - 8 - |

Interest expense of $231 was incurred during the nine months ended September 30, 2021 compared to $1,100 during the same period in 2020. The decrease in interest expense was a result of the Company repaying its debts.

Mineral Properties

The following is a summary of the Company’s operations, together with an update on exploration activities for the year to date. Except as otherwise noted, Donald J. Birak, independent geologist and Registered Member of the Society for Mining, Metallurgy and Exploration (“SME”) and Fellow of the Australasian Institute for Mining and Metallurgy (“AusIMM”), is the Qualified Person who has reviewed and approved the scientific and technical information contained herein.

Calcatreu Project

The Company’s principal project is Calcatreu located in south-central Rio Negro province approximately 80 kilometers (“km”) southwest of the town of Jacobacci. Calcatreu is located in the Jurassic-aged, Somuncura Massif along the NW- to SE-oriented, regional-scale Gastre Fault System; a highly prospective belt of Mesozoic-aged rocks and structures and base and precious metal mineral deposits occurring in both the provinces of Chubut and Rio Negro. The massif is similar in geologic character to the larger Deseado Massif in the province of Santa Cruz to the south. Patagonia has also recently acquired new concessions, bringing its holdings to more than 100,000 ha along this belt in Rio Negro province, bordering Chubut on the north. Calcatreu is a gold and silver project acquired in January 2018 through the acquisition of Minera Aquiline Argentina SA, a subsidiary of Pan American Silver and the Company’s immediate aim is to increase the existing mineral resources and advance the project to feasibility study stage. Precious metal mineralization in the Somuncura Massif, like that on the Company’s Calcatreu property, is largely epithermal in character within quartz-rich veins, vein clusters, stockworks and as disseminations. Sulfide minerals are ubiquitous in the mineral deposits as well as a suite of temporally- and spatially-related gangue minerals typical of epithermal deposits in the massif and elsewhere.

The Calcatreu Deposit is a low sulfidation, epithermal gold and silver system with outcropping mineralization. An independent mineral resource estimate (“MRE”) was completed by Micon International Limited of Toronto in 2004 for the Calcatreu Deposit and disclosed in an NI 43-101 technical report for Aquiline Resources Inc. Mineral resources were estimated for two vein systems on the property: Veta 49 and Nelson and consisted of 6.2 M tonnes of indicated resources grading 3.04 g/t Au and 28.1 g/t Ag and 1.9 M tonnes of inferred resources grading 2.1 g/t Au and 19.4 g/t Ag. In 2018, Cube Consulting Ltd. (“CUBE”) of Australia prepared an updated mineral resource estimate for the Calcatreu project, effective December 31, 2018, which consists of an indicated resource of 9.8 M tonnes grading 2.11 g/t Au and 19.83 g/t Ag (2.36 g/t gold equivalent – “AuEq”) and 8.1 M tonnes of inferred grading 1.34 g/t Au and 13.09 g/t Ag (1.5 g/t AuEq); all contained within Veta 49, Nelson, Belen and Castro Sur veins. Gold equivalent values were calculated by CUBE using a metal price at a ratio of 81:25:1 Ag/Au. The changes from the previous estimate were due to a revised interpretation of prior and new data collected by the Company. The 2018 exploration work at Calcatreu consisted of project-scale geological mapping along with a pole-dipole, induced polarization and resistivity (IP/Res) geophysical survey, followed by a diamond drill program of 6,495 meters (please see the table of the Company’s mineral resources herein and the respective, supporting NI 43-101 technical reports on file at www.sedar.com). The updated mineral resource estimate, completed by CUBE, is tabulated below.

In 2019, an exploration program was conducted consisting of surface work, a total of 41.28 line kilometers of pole-dipole induced polarization and resistivity (“IP/Res”) geophysical survey conducted over the main Nelson targets and Castro Norte, Fiero, Sabrina and Viuda de Castro areas, and 121.5 line kilometers of gradient array IP/Res geophysics over Nelson, Sabrina and Mariano. Subsequently, 1,687.2 linear kilometers of ground magnetics surveying, covering 55.44 square kilometers, was completed in the project covering several targets including the main V49 and Nelson. The objective of the surveys was to identify hidden, non-outcropping mineralization in dilatational jogs, blind structures and other geologic settings. Geologic mapping and sampling were completed over several targets of interest, notably Viuda de Castro, Trinidad, La Cruz, subcrops of the Nelson extension, Piche, La Olvidada and Epu-Peni. The sampling yielded 254 rock chips and 81 new, sawn channels. Overall, approximately 50% of the core from the project was relogged, though totalling up to 80% in some areas such as Veta 49 and Belen.

A rotary air blast (“RAB”) drilling campaign and channel (sawn) sampling was in progress in early 2020 when all the activities were paused due to the COVID-19 pandemic. The activities restarted in September 2020. A total of 36 RAB holes were drilled over the main V49 vein and 6 over Piche totaling 740 and 116 meters of drilling respectively and a total of 856 samples. Trenches and saw channel: a total of 1,308.7 m and 447 samples were taken over the Epu Peñi, Fiero, La Olvidada, Nelson Sur, Piche and Viuda de Castro targets. Geophysics: A total of 1,111.57 km of ground magnetic geophysical surveying was completed over the extension of the main targets and the new Amancay area, and 18.4 km of pole-diploe IP/Res over Trinidad and Nelson Targets. In December 2020, the Baseline (environmental) Study began by choosing the contractors and reviewing the information generated in the past. The Baseline Study aims to contextualize the environmental state before the construction and production of the project begins.

In 2021, the Baseline Study continues with field work, along with drilling, surface exploration and geophysics. The RAB drilling to obtain information from near surface of the main structures (Veta 49 and Nelson) is in progress. A total of 156 holes have been drilled so far, for a total of 1,708 meters (“m”); 15 holes in the Belen prospect (156 m), 51 holes at Nelson (528 m), 21 holes in Nelson Oeste (241 m) and 69 holes in the Vein 49 target (783 m). A total of 613.3 m of trenches have been cut in Nelson (1 trench), Nelson Central (7), Nelson Oeste (4), Nelson Sur (4) and 1 in Veta 49 for a total of 17 new trenches. ground geophysical surveying, in the southern portion of the project, and a total of 200 line kilometers have been completed. The Baseline Study is in progress under the supervision of GT Ingenieria, A draft of the study, provided to the Company, is under review.

| - 9 - |

During the third quarter of 2021, work at Calcatreu continued with the Baseline Study and condemnation sampling collected from trenches, and rock chips in areas of future waste dump and the leach pad. A total of 827 m of trenches were dug and 58 samples taken from them. In addition, a total of 950.1 m and 572 samples from trenches and 187 samples over 135.1 m of sawn channel, plus mapping, core re-logging and were also completed. In addition, a total of 319 line kilometers of ground magnetic and 2.6 line km of pole-dipole IP/Res surveying was completed at the project.

Additional work is planned to follow-up on the initial geochemical results to include new trenching and sampling. New ground magnetic survey is in progress in the southern part of the project.

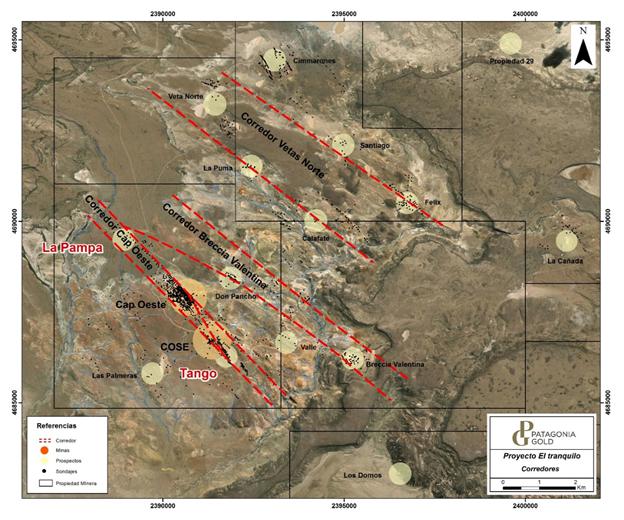

Cap-Oeste Project

The Company’s Cap-Oeste project, in the province of Santa Cruz, is located within a six kilometer long, northwest-trending, structural corridor extending six kilometers from the La Pampa prospect in the northwest to the Tango prospect in the southeast. The Cap-Oeste deposit has an identified and delineated strike extent of 1.2 kilometers. Cap-Oeste has been on care and maintenance since February 2019 though residual leaching continues.

The Company has initiated studies to assess the potential technical and economic extraction of a higher-grade portion of the current mineral resources as defined in the December 2019 CUBE NI 43-101 technical report on file on www.sedar.com. The Company is now focused on evaluating the development of this portion, termed “COSE-Style” mineralization, of the total mineral resources by underground mining. The Company is expecting quotations with respect to potential construction of an underground mine in Cap-Oeste. Material processing options are being considered and may include utilizing the Company’s flotation facilities at Martha, about 100 kilometers to the southeast of Cap-Oeste. The Company has successfully carried out bulk metallurgical tests in the Martha process plant, obtaining favorable precious metal recoveries.

| - 10 - |

On November 23, 2020, the Company announced that it had received a provisional permit to proceed with the development of the Cap-Oeste gold/silver underground project (the “Project”). Development of the Project will focus on a high-grade portion of the current mineral resources, which lies under and peripheral to the depleted surface mine. The intention is to mine the Cap-Oeste underground resource and truck the mineralized material approximately 100 kilometers to the Martha plant where it will be processed to produce a concentrate.

In the second half of 2020, a general exploration review of the Project identified the Monte Leon Target, located 10 km to the south of the mine, led to metallurgical studies using samples from prior diamond holes. This led to planning a diamond drilling program that will be carried out during the second half of 2021. Five km of core drilling is planned. The Company believes this target also has the potential for the development of near-surface, oxidized mineralization. New mapping and interpretation of the Monte Leon area including core re-logging have been completed in January/February 2021 and a total of 2.5 km of pole dipole IP/Res have been surveyed and 12 other surveys are in progress. 133 line kilometers of ground magnetics have also been completed.

On March 9, 2021, the Company announced that it had received a definitive, environmental permit for the development of the Cap-Oeste Project. The Cap-Oeste project has been put on hold pending evaluation of results from the planned exploration program at Monte Leon; favorable results from which the Company believes may be synergistic with the main Cap-Oeste project.

During the third quarter of 2021, efforts continue focused mainly in the near surface – oxide – mineral potential at Monte Leon about 12 km to the south of the Cap-Oeste Pit. A total of 2,215 m of RAB drilling was completed in the area based on new geological interpretation and have been sampled meter by meter. With these, the phase 1, of 7413 mts was completed. In August the Monte Leon mineral inventory have been estimated in 42,766 Oz Au @ 0,8gr/tn Au, using 0.5 gr/Tn Au Cut Off, from surface and up to 20mts depth with plus 90% Au recovery in historical standard roll bottle test. New roll bottle test are in progress and result are expected to return at the end of November and the RAB drilling continues, aimed to extend resources.

In addition, a total of 237.5 km of ground magnetics have been surveyed at La Marciana and Monte Leon prospects, plus 18,2 km of pole-dipole IP/Res, in lines of approximately 2 kilometers length at Monte Leon. The purpose of this work was to further define the size potential and, thus, new core drilling targets, of the epithermal mineralization identified with prior Company work. Geological mapping and sampling over other targets are also in progress.

The Company has reclamation and remediation obligations for Cap-Oeste Project of $0.63 million as of September 30, 2021.

Lomada de Leiva Project (“Lomada”)

The Lomada mine, located in the western part of the province of Santa Cruz, was closed in May 2016 while production from the ongoing leaching continues, though at a reduced output. Given that the mineralized material from the Lomada open pit mine was originally placed on the heap leach pad without crushing, the Company decided to return to Lomada to reprocess this mineralized material. However, in mid-February 2019 the Company took the decision to cease operations and proceed with the closure of Lomada. During the year ended December 31, 2020, the Company was working on re-handling material of leach pad to regenerate the solution percolation and generate new channels of circulation of solution.

The Company has prepared an update to the closure plan presented to and approved by the provincial authorities in 2017. The Company received the final approval in November 2019 and started with the work of remediation at the end of 2019. The work on the remediation had been halted due to the COVID-19 pandemic. On October 8, 2020, the Company announced that it had received a preliminary Environmental Permit (“Permit”) for a restart of mining and new leaching operations at Lomada. Patagonia applied for the Permit in August 2020.

Following receipt of a preliminary permit in October 2020, the Company restarted operations at Lomada. In addition to production from this restart, the Company continues to recover precious metals from residual leaching of material already placed on the heap leach pad. On March 9, 2021, the Company announced that it had received a definitive environmental permit for Lomada. The mine is currently operating at a rate of 120,000 tonnes/month of total material. In the leach pad area, road construction has been completed and new mineralized material is being placed on the pad to be leached.

No exploration activities were undertaken at Lomada during the nine months ended September 30, 2021. Exploration work to reinterpret targets, Brecha La Emilia and Cerro Vasco, both in the north part of the project, is expected to start at the end of 2021.

The Company has reclamation and remediation obligations for Lomada of $3.35 million as of September 30, 2021.

| - 11 - |

Mineral Resources

| Cap-Oeste (Santa Cruz, AR) – Cube Consulting Dec 2018; Notes ¹ and 2 | ||||||||||||||||||||||||||||

| Classification | Tonnes (K) | Average Grades (g/t) | Contained Ounces (K) | |||||||||||||||||||||||||

| Gold | Silver | Gold Equivalent | Gold | Silver | Gold Equivalent | |||||||||||||||||||||||

| Measured Indicated | 3.4 10,554.0 | 2.92 2.07 | 46.7 63.2 | 3.59 2.99 | 0.3 704.0 | 5.3 21,448.0 | 0.4 1,013.0 | |||||||||||||||||||||

| Meas+Ind | 10,557.4 | 2.07 | 63.2 | 2.99 | 704.3 | 21,453.3 | 1,013.4 | |||||||||||||||||||||

| Inferred | 4,895.0 | 1.37 | 34.7 | 1.87 | 215.0 | 5,467.0 | 294.0 | |||||||||||||||||||||

| Calcatreu (Rio Negro, AR) – Cube Consulting Dec 2018; Notes 3 and 4 | ||||||||||||||||||||||||||||

| Classification | Tonnes (K) | Average Grades (g/t) | Contained Ounces (K) | |||||||||||||||||||||||||

| Gold | Silver | Gold Equivalent | Gold | Silver | Gold Equivalent | |||||||||||||||||||||||

| Measured Indicated | 9,841.0 | 2.11 | 19.8 | 2.36 | 669.0 | 6,275.0 | 746.0 | |||||||||||||||||||||

| Meas+Ind | 9,841.0 | 2.11 | 19.8 | 2.36 | 669.0 | 6,275.0 | 746.0 | |||||||||||||||||||||

| Inferred | 8,078.0 | 1.34 | 13.1 | 1.50 | 348.0 | 3,399.0 | 390.0 | |||||||||||||||||||||

| La Manchuria (Santa Cruz, AR) – Micon 2019; Notes 5 and 6 | ||||||||||||||||||||||||||||

| Classification | Tonnes (K) | Average Grades (g/t) | Contained Ounces (K) | |||||||||||||||||||||||||

| Gold | Silver | Gold Equivalent | Gold | Silver | Gold Equivalent | |||||||||||||||||||||||

| Measured Indicated | 474.0 | 2.59 | 129.0 | 3.53 | 39.5 | 1,969.0 | 53.9 | |||||||||||||||||||||

| Meas+Ind | 474.0 | 2.59 | 129.0 | 3.53 | 39.5 | 1,969.0 | 53.9 | |||||||||||||||||||||

| Inferred | 1,836.0 | 1.30 | 40.0 | 1.56 | 76.5 | 2,375.0 | 92.4 | |||||||||||||||||||||

Notes

“K” = Thousands, “g/t” = grams per tonne

Rounding may affect sums and weighted averages

Mineral resources that are not mineral reserves have not demonstrated economic viability

100% basis; Fomicruz has a 5% interest in all Santa Cruz mineral interests.

| 1. | Cap-Oeste | 0.5 g/t AuEq cutoff | |

| 2. | Cap-Oeste | AuEq = Au + (Ag*69.4) | |

| 3. | Calcatreu | 0.5 g/t AuEq cutoff | |

| 4. | Calcatreu | AuEq = Au + (Ag*81.25) | |

| 5. | La Manchuria | 0.55 AuEq cutoff | |

| 6. | La Manchuria | AuEq = (Au + Ag)/(Au price*0.32151) |

Exploration Update

In Rio Negro Province, at Calcatreu project, the RAB drill program to extend mineralization from the upper-most drill intercepts, up to the surface, was conducted the first quarter of 2021. In this program, a total of 156 holes were drilled (totalling 1,708 m) over the main Veta 49 and Nelson veins, and 358mts in 17 trenches have been excavated. 200 km of ground magnetics have been surveyed over the southern extension of the Veta 49-Nelson corridor.

In Santa Cruz province, at the El Tranquilo project, which encompasses the Company’s Cap-Oeste mine, preparation of a new geological base map is in progress. During the second quarter of 2021, a total of 5,173.5 m of RAB drilling was completed in the northern part of Monte Leon target based a new geological interpretation, plus 400 m in the Felix and Don Pancho prospect - located about 1.5 and 8 km, respectively, to the west of the Cap-Oeste Pit and Monte Leon, about 12 km to the south - also aimed to identify oxide mineralization near surface. Also, at El Tranquilo, ground magnetic and pole-dipole surveys are in progress.

| - 12 - |

A review of La Esperanza and Las Mellizas prospects, including work to obtain environmental and landowners access permits, are in progress. Geologically, the area hosts a large, underexplored epithermal vein field.

Finally, a total of 3,600 m of RC drilling was planned for mid-2021 at the Tornado and Huracán (“Tornado”) properties, located approximately 85 kilometers southeast of the town of Perito Moreno in Santa Cruz province. Tornado is located in a prospective area in the northwestern portion of the Deseado Massif. The area lies within cluster of epithermal, low sulfidation volcanic hosted gold and silver deposits, including the San Jose (Hochschild-McEwen) and the Cerro Negro (Newmont-Goldcorp) mines. The RC drill program commenced at Tornado but, because of adverse winter condition and poor rock conditions encountered during drilling, the campaign was put on hold until later in the year.

Homenaje and Nico Projects

In 2021, the Company entered into definitive agreements to acquire two projects in Argentina. A definitive option agreement, dated April 15, 2021 (the “Option Agreement”), was executed with Mirasol Resources Ltd. (“Mirasol”) and Mirasol’s wholly owned subsidiary Australis S.A. (“Australis” and together with Mirasol, the “Vendors”), which grants Patagonia an option to acquire a 75% undivided, managing? interest in and to Australis’ rights and interest in the Homenaje project (the “Homenaje Project”) located in Santa Cruz Province, Argentina. The Company also entered into a definitive transfer agreement dated April 15, 2021 (the “Transfer Agreement”) with the Vendors, which grants Patagonia a 100% undivided interest in and to Australis’ rights and interest in the Nico project (the “Nico Project”) located in Santa Cruz Province, Argentina. The Nico Project was previously explored by Mirasol, while the Homenaje Project, which is adjacent to two mining operations, holds targets that have yet to be drilled.

Pursuant to the Option Agreement, Patagonia has an option to earn a 75% interest in the Homenaje Project over six years upon achievement of the following (collectively, the “Earn-In Obligations”):

| ● | an initial work program over six years of $2.55 million in exploration expenditures, including 2,500 meters of drilling, on the Homenaje Project; | |

| ● | expenditures on exploration activities with respect to the Homenaje Project (the “Exploration Expenditures”) of a minimum of $0.4 million over the first 18-months; | |

| ● | following completion of the initial Exploration Expenditures and drilling obligations due within the first 30 months, Patagonia must complete a minimum of $0.4 million of Exploration Expenditures in any 12-month period, and a minimum of $0.2 million of Exploration Expenditures in any six-month period; and | |

| ● | a pre-feasibility study, prepared in accordance with NI 43-101 and CIM standards, for a mineral resource of not less than 300,000 ounces of gold equivalent. |

Upon Patagonia completing the Earn-In Obligations, Patagonia and the Vendors will hold 75% and 25%, respectively, in a joint venture company holding the Homenaje Project. If either party’s equity interest is diluted below 10%, it will convert to a 2% NSR royalty.

Pursuant to the terms of the Transfer Agreement, Patagonia has acquired the Vendors’ interest in the Nico Project in exchange for a 1.5% NSR royalty. If, by the end of third-year, the Nico Project has not been operated as a producing mine, or Patagonia has not produced and shipped minerals in commercial quantities (excluding bulk sampling or pilot plant operations, if any) from the Nico Project for a period of 30 consecutive days, Mirasol will have the right to regain full ownership of the Nico Project at no cost.

No exploration activities were undertaken at Homenaje as of September 30, 2021, although environmental permitting commenced.

Mina Angela

On August 13, 2019, the Company announced an offer letter agreement with Latin Metals Inc. to acquire its Mina Angela property. Mina Angela is situated in the Somuncura Massif of southern Argentina and is comprised of 44 individual claims located approximately 50 kilometers east-southeast of Patagonia’s 100% owned Calcatreu gold project. Pan American Silver’s Navidad silver and base metal deposit is located 45 kilometers further to the south-southeast of Mina Angela. In March 2020, Patagonia extended the period by which it must enter into the definitive agreement with a $100 thousand payment to Latin Metals; $50 thousand of which was applied to extend the period to enter into the definitive agreement and $50 thousand of which was a partial prepayment of the first earn-in payment to be made under the definitive agreement.

| - 13 - |

On September 15, 2020, the Company entered into the definitive option agreement with Latin Metals Inc., which grants the Company an irrevocable option to acquire a 100% interest in the Mina Angela property. Upon signing of the definitive agreement, the Company paid $250 thousand representing the balance of the first earn-in payment. It is expected that the Company will pay the second earn-in payment of $250 thousand within the next six months if it exercises the option to acquire the Mina Angela property. A further and final payment of $500 thousand is expected to be paid within 30 days of verification that the legal restrictions preventing development of mining activity in the Chubut Province and at the Mina Angela property have been lifted in such a manner that the Company thereafter has the ability to perform exploration and exploitation activities on the Mina Angela property. In addition, Latin Metals will be entitled to receive a 1.25% Net Smelter Return royalty from future productions, half of which can be repurchased by the Company for $1 million.

On March 12, 2021, the Company exercised the option to acquire 100% interest in the Mina Angela property and paid the second earn-in payment of $250 thousand.

La Manchuria Project

In addition to its current mineral resources, the Company’s La Manchuria Project is believed to be prospective for the discovery of new gold and silver mineralization. Exploration work continued with mapping and rock chip sampling over an area of approximately 2,000 hectares (“ha”). Veinlets and narrow breccia zones, indicative of hydrothermal activity, were found at the Magali zone. Anomalous gold values were reported from the Cecilia zone. As a result of these favorable results, a new drill program for La Manchuria, of 2,000 m in 14 holes is planned to test geophysical anomalies and to test gold anomalies generated from surface rock chip sampling. An updated NI 43-101 report for this project was completed on September 27, 2019 by Micon International and is on file at www.sedar.com.

Sarita Project

The Sarita Project, located in the SW part of the Deseado Massif approximately 10 kilometers northwest of the Company’s Martha mine and mill, hosts a widespread system of banded, low sulfidation, gold- and silver-bearing veins, within a rhyolitic dome complex. Geologically, the area displays very similar structural and stratigraphic characteristics to Martha with Ag-rich, polymetallic, vein-hosted, intermediate sulfidation mineralization. The banded, silver- and gold-bearing quartz veins and quartz vein breccias occur within a set of NNW-SSE striking normal faults and constitute an extensive mineralized vein system, with more than 12 kilometers in total length. Precious and base metal mineralization has been recognized in quartz veins and vein breccias up to 3 meters wide at surface, composed of quartz and sulphides. Rock chips from discrete vein structures or aligned float contained anomalous gold values ranging from 0.1 to 83.4 g/t Au and from 100 to 15,444 g/t Ag, in separate samples. To date, 16 diamond drill holes have been drilled for a total of 1,754 m targeting the vein mineralization. Geochemical results from drilling show gold and silver anomalies. Due to poor ground conditions encountered during drilling, core recovery in some of the veins was poor and Au and Ag mineralization may have not been recovered. Other exploration activities at Sarita included 7.1 line kilometers of IP/Res geophysical surveys and ground magnetics (220 hectares of grids) over different target areas.

During May 2019, a total of 82 RAB holes completing 1,818.4 m, were drilled in the area yielding a total of 1,257 samples for geochemical analysis. In September and October 2019, a second phase of drilling was undertaken, for a total of 2,409 m in 116 holes and 1,361 samples assayed. The RAB drilling defined several shallow, NW-oriented zones of vein-hosted mineralization; notably Veta Maria and Virginia. The Company has plans to follow-up the RAB results with core drilling.

No exploration activities have been undertaken at Sarita during the nine months ended September 30, 2021.

Martha Project

The Martha Project (“Martha” or “Mina Martha”) is located in the Province of Santa Cruz, Argentina. The closest community is the town of Gobernador Gregores, situated approximately 50 road kilometers to the west-southwest. The property is the site of past exploration for, and surface and underground mining and recovery of, silver and gold from epithermal veins and vein breccias, previously operated by Coeur Mining Inc. (formerly, Coeur d’Alene Mine Corp.) and Yamana Inc.

The Company acquired Martha as part of its RTO of Hunt in 2019. The land package at Martha consists of approximately 7,850 ha of concessions, various buildings and facilities, surface and underground mining and support equipment, a 480 tonne per day (maximum) crushing, grinding and flotation plant, tailings facility, various stockpiles and waste dumps, employee living and cafeteria quarters, and miscellaneous physical materials. In addition, the Company has access to surface ranch (“estancia”) lands surrounding the mine and mill site that are approximately 35,700 ha in size.

The property was purchased in 2016 by Cerro Cazador SA (CCSA), an Argentine subsidiary of Hunt, from an Argentine subsidiary of Coeur Mining Inc. The intent to purchase was announced February 10, 2016 and closed May 11, 2016 as disclosed by the Company on its website (www.patagoniagold.com). The processing plant at the Martha Project is anticipated to be used to process material from the future Cap-Oeste underground project, from new mining at the greater Martha Project and from the La Josefina Project. Royal Gold Inc. holds a 2% Net Smelter Return (NSR) royalty on all production from the Martha property; the obligation for which transferred from Coeur to the Company (www.royalgold.com). In addition, the provincial government holds a 3% pit-head royalty from future production.

| - 14 - |

During the first quarter of 2020, a plan for reviewing near-mine targets (less than 5 kilometers away from the mill) was defined. Those remaining targets consist of outcropping veins-veinlets and included Veta del Medio System, Noroeste, Ivana, Martha Oeste, Martha Norte, Futuro and Sugar Hill, among others. A total 77 sawn channels were cut, and after encouraging results at Veta del Medio System, a RAB drill program was carried out to test mineralization at shallow depths. A total of 80 RAB drill holes (1,622.4 m of drilling, ranging from 6 to 25 m in depth) tested several targets.

Highly anomalous drill intercepts, ranging from 1 m grading 180 g/t Ag up to 3 m grading 2,566 g/t Ag (and 3.5 g/t Au), were returned from the Veta del Medio Norte. No exploration activities were undertaken at Martha Project during the first half of 2021.

The operations at the Martha plant continue to be on care and maintenance pending the discovery of new material to put through the plant.

The Company has reclamation and remediation obligations for the Mina Martha Project of $1.59 million as of September 30, 2021.

La Josefina Project

La Josefina is situated about 450 kilometers northwest of the city of Rio Gallegos, in the Santa Cruz province of Argentina within a scarcely populated steppe-like region. The La Josefina property is large, covered by 52,800 hectares of concessions. The La Josefina Project consists of mineral rights composed by an area of 528 square kilometers established in 1994 as a Mineral Reserve held by Fomento Minero de Santa Cruz Sociedad del Estado (“Fomicruz”), the Santa Cruz Provincial mining company.

In March 2007, the Company (via a subsidiary of Hunt) acquired the exploration and development rights to the La Josefina project from Fomicruz. In July 2007, the Company entered into an agreement (subsequently amended) with Fomicruz which provides that, in the event that a positive feasibility study is completed on the La Josefina property, a Joint Venture Corporation (“JV Corporation”) would be formed by the Company and Fomicruz. The Company would own 81% of the joint venture company and Fomicruz would own the remaining 19%. Fomicruz has the option to earn up to a 49% participating interest in the JV Corporation by reimbursing the Company an equivalent amount, up to 49%, of the exploration investment made by the Company. The Company has the right to buy back any increase in Fomicruz’s ownership interest in the JV Corporation at a purchase price of $200 thousand per each percentage interest owned by Fomicruz down to its initial ownership interest of 19%. The Company can also purchase 10% of the Fomicruz’s initial 19% JV Corporation ownership interest by negotiating a purchase price with Fomicruz. Under the agreement, the Company had until the end of 2019 to complete cumulative exploration expenditures of $18 million and determine if it will enter into production on the property. In October 2019, the agreement was extended until April 30, 2021 which period may be extended for an additional one-year term. At December 31, 2019, the Company had incurred approximately $20 million and is currently in discussions with Fomicruz to develop a plan for production.

An NI 43-101 compliant technical report on La Josefina, dated September 29, 2010 and prepared by UAKO Geological Consulting, is on file on www.sedar.com.

During 2020, a total of 1,098 line kilometers of ground geophysics and sampling were surveyed covering the Flaca, Cecilia, Amanda, Pequeña and Cruzada veins. And a total of 124 rock chip samples were taken.

The Company has renegotiated the terms of the La Josefina and Valenciana properties held by Cerro Cazador and is expecting the new terms to be adjudicated at the end of 2021. In the meantime, the exploration program on these properties has been put on hold.

La Valenciana Project

La Valenciana is located in the central-north portion of the Santa Cruz Province, Argentina. The project encompasses an area of approximately 29,600 ha and is contiguous with the Company’s La Josefina property to the east. The La Valenciana project is comprised of 11 Manifestations of Discovery (“MDs”) covering segments of Estancia Cañadón Grande, Estancia Flecha Negra, Estancia Las Vallas, Estancia La Florentina, Estancia La Valenciana and Estancia La Modesta (inactive ranches). In La Valenciana, exploration has been limited, with more than half of the surface without systematic exploration. Fomicruz carried out preliminary works defining a main vein system of low sulfidation, epithermal style, with gold and silver values and base metals. Exploration and subsequent reconnaissance sampling by CCSA added other secondary targets and structures combining a total of 5.70 kilometers mapped veins and stockworks. The limited exploration to date, alteration features and associated structures, and partial coverage by probable post-mineral units suggests that there is still a high degree of discovery potential in the mining block. A new exploration program to define mineralization includes geophysical surveys and shallow drilling in new and known target areas and an intensive prospecting and reconnaissance sampling over the Company’s entire land position, is being considered. Mineral resources have not yet been defined on the La Valenciana property.

| - 15 - |

The Company has renegotiated the terms of the La Josefina and Valenciana properties held by Cerro Cazador and is expecting the new terms to be adjudicated at the end of 2021. In the meantime, the exploration program on these properties has been put on hold.

Bajo Pobre Property

The Bajo Pobre property covers 3,190 hectares and is mainly on the Estancia Bajo Pobre. The property is located 90 kilometers south of the town of Las Heras. No exploration activity has taken place on the Bajo Pobre Property and no exploration activity is planned for the immediate future. Mineral resources have not yet been defined on the Bajo Pobre property.

Short visits have been carried out to the area during 2020 and a total of 16 samples have been taken. A new review of the project will commence at the end of 2021.

El Gateado Property

In March 2006, CCSA acquired the right to conduct exploration on the El Gateado property through a claim staking process for a period of at least 1,000 days, commencing after the Government issues a formal claim notice, and retain 100% ownership of any mineral deposit found within. El Gateado is a 10,000-hectare exploration concession filed with the Santa Cruz Provincial mining authority. The El Gateado property is located in the north-central part of Santa Cruz province, contiguous to La Josefina on the east.

The Company has not yet received a formal claim notice pertaining to the El Gateado property. Should a mineral deposit be discovered, the Company has the exclusive option to file for mining rights on the property. The surface rights of the El Gateado claim are held by the following ranches (“estancias”):, Estancia Los Ventisqueros, Estancia La Primavera, Estancia La Virginia and Estancia Piedra Labrada. The El Gateado claims are filed with the government under file #406.776/DPS/06.

Mineral resources have not yet been defined on the El Gateado property. No recent exploration activity has taken place on El Gateado Property and no exploration activity is planned for the immediate future.

Las Mellizas – La Esperanza Block

The Company acquired Newmont’s interest in the Las Mellizas and La Esperanza Block in early 2019 in exchange for a 1.5% net smelter return royalty, which grants the Company a 100% undivided right and interest in these properties. This 30,000 ha area project is located north and west of La Valenciana in the central part of the Deseado Massif, in Santa Cruz Province, Argentina. These early exploration projects have been granted the environmental exploration permit and land owners access agreements have been negotiated, allowing the development of the exploration plan which consist in conducting a new interpretation of the data provided by the former owner of these projects. Trenches and drill holes have been carried out in this epithermal vein field. Results from surface sampling are very encouraging and several structures have never been tested or mapped.

Tornado – Huracán

The Tornado and Huracán (“Tornado”) properties are located approximately 85 kilometers southeast from the town of Perito Moreno and 250 kilometers west of the city of Pico Truncado, the main population center that serve the oil industry in the region. Tornado is located in a prospective area in the northwestern portion of the Deseado Massif. The area lies within cluster of epithermal low sulfidation volcanic hosted gold and silver deposits, including the San Jose (Hochschild-McEwen) and the Cerro Negro (Newmont-Goldcorp) mines to the northwest and southeast of Tornado, respectivley.

No activities have been undertaken during the third quarter of 2021, The drill program is expected to resume in November 2021. The remaining plan is approximately 3,300m and will be drilled with diamond.

| - 16 - |

Selected Annual Information

The following selected financial data for the Company’s most recently completed financial periods are derived from the audited financial statements of the Company.

| As at and for the Year Ended December 31, 2020 ($’000) | As at and for the Year Ended December 31, 2019 ($’000) | As at and for the Year Ended December 31, 2018 ($’000) | ||||||||||

| Revenue | 19,849 | 21,938 | 48,089 | |||||||||

| Net income (loss) for the year | (4,381 | ) | (12,354 | ) | (17,590 | ) | ||||||

| Comprehensive income (loss) for the year | (3,023 | ) | (12,008 | ) | (10,591 | ) | ||||||

| Current Assets | 6,149 | 5,407 | 11,482 | |||||||||

| Non-current assets | 53,919 | 59,087 | 44,428 | |||||||||

| Current Liabilities | 14,527 | 28,032 | 29,425 | |||||||||

| Non-current liabilities | 24,136 | 22,674 | 3,103 | |||||||||

| Working Capital (Deficit) | (8,378 | ) | (22,625 | ) | (17,943 | ) | ||||||

| Share Capital | 7,320 | 2,588 | 301 | |||||||||

| Shareholders’ Equity | 21,405 | 13,788 | 23,382 | |||||||||

Selected Quarterly Information

The following table shows selected financial information related to the results of the Company´s most recent periods.

| Fiscal Year | 2021 | 2020 | 2019 | |||||||||||||||||||||||||||||

| For the quarters | Sep | Jun | Mar | Dec | Sep | Jun | Mar | Dec | ||||||||||||||||||||||||

| ended | $’000 | |||||||||||||||||||||||||||||||

| Revenues | 5,758 | 2,728 | 5,747 | 3,380 | 6,549 | 4,705 | 5,215 | 5,016 | ||||||||||||||||||||||||

| Net income (loss) for the period | (1,712 | ) | (2,738 | ) | (125 | ) | (2,606 | ) | (1,041 | ) | (177 | ) | (557 | ) | (7,066 | ) | ||||||||||||||||

| Comprehensive Income (Loss) for the period | (2,372 | ) | (2,556 | ) | 484 | (875 | ) | (877 | ) | 252 | (1,523 | ) | (5,897 | ) | ||||||||||||||||||

| Income (Loss) per share, basic and diluted | (0.004 | ) | (0.006 | ) | (0.000 | ) | (0.007 | ) | (0.003 | ) | (0.001 | ) | (0.002 | ) | (0.022 | ) | ||||||||||||||||

The Company’s results over the past several quarters have been driven primarily by fluctuations in the gold price, input costs and changes in gold equivalent ounces produced. In addition, the Company is also affected by fluctuations in the price of silver and foreign exchange rates.

Liquidity and Capital Resources

As of September 30, 2021, the Company had a working capital deficiency of $5,793 (December 31, 2020 - $8,378). The improvement in the working capital deficiency is a result of the repayment of bank indebtedness and the settlement of debts with related parties. For more information, see “Transactions Between Related Parties” section of the MD&A.

| - 17 - |

The Company’s capital management objectives are:

| ● | to ensure the Company’s ability to continue as a going concern; |

| ● | to fund projects from raising capital from equity placements rather than long-term borrowings; |

| ● | to increase the value of the assets of the business; and |

| ● | to provide an adequate return to shareholders in the future when new or existing exploration assets are taken into production. |

These objectives will be achieved by maintaining and adding value to existing extraction projects and identifying new exploration projects, adding value to these projects and ultimately taking them through to production and cash flow, either with partners or by the Company’s means.