Santander Mexico Financial Group, S.A.B. de C.V. Inactive

Filed: 29 Jan 16, 12:00am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of January, 2016

____________________

Commission File Number: 001-35658

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

(Exact Name of Registrant as Specified in Its Charter)

SANTANDER MEXICO FINANCIAL GROUP, S.A.B. de C.V.

(Translation of Registrant’s Name into English)

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Delegación Álvaro Obregón

01219 México, D.F.

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F | X | Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes | No | X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes | No | X |

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

TABLE OF CONTENTS

| ITEM | |

| 1. | Fourth quarter 2015 earnings report of Grupo Financiero Santander México, S.A.B. de C.V. |

| 2. | Fourth quarter and full-year 2015 earnings presentation of Grupo Financiero Santander México, S.A.B. de C.V. |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

GRUPO FINANCIERO SANTANDER MÉXICO,

S.A.B. de C.V.

| ||||

| By: | /s/ Gerardo Manuel Freire Alvarado | |||

| Name: | Gerardo Manuel Freire Alvarado | |||

| Title: | Executive Director of Investor Relations | |||

Date: January 29, 2016

Item 1

TABLE OF CONTENTS

| I. | CEO Message / Key Highlights for the Quarter |

| II. | Summary of 4Q15 Consolidated Results |

| III. | Analysis of 4Q15 Consolidated Results |

| IV. | Relevant Events & Representative Activities and Transactions |

| V. | Awards & Recognitions |

| VI. | Sustainability and Social Responsibility |

| VII. | Credit Ratings |

| VIII. | 4Q15 Earnings Call Dial-In Information |

| IX. | Analysts Coverage |

| X. | Definition of Ratios |

| XI. | Financial Statements |

| XII. | Notes to the Financial Statements |

2

Grupo Financiero Santander México Reports Fourth Quarter 2015 Loan Portfolio Up 17.7% YoY and Net Income of Ps.4,224 Million

-Net income growth mainly driven by core earnings

-Loan growth driven by above market YoY increases in both individual and commercial segments

-Strong loan growth achieved while maintaining focus on asset quality

Mexico City – January 29, 2016, Grupo Financiero Santander México, S.A.B. de C.V., (NYSE: BSMX; BMV:SANMEX), (“Santander México”), one of the leading financial groups in Mexico, today announced financial results for the three- and twelve-month periods ending December 31, 2015.

Santander México reported net income for 4Q15 of Ps.4,224 million, representing YoY and QoQ increases of 10.5% and 21.9%, respectively. For 12M15, net income amounted to Ps.14,141 million, reflecting a 0.9% increase from 12M14.

| HIGHLIGHTS | |||||

| Income Statement Data(Millions of pesos) | 4Q15 | 3Q15 | 4Q14 | % YoY | % QoQ |

| Net interest income | 11,431 | 10,810 | 9,799 | 16.7 | 5.7 |

| Fee and commission, net | 3,777 | 3,686 | 3,364 | 12.3 | 2.5 |

| Core revenues | 15,208 | 14,496 | 13,163 | 15.5 | 4.9 |

| Provisions for loan losses | 4,424 | 4,594 | 3,334 | 32.7 | (3.7) |

| Administrative and promotional expenses | 6,437 | 6,426 | 6,059 | 6.2 | 0.2 |

| Net income | 4,224 | 3,464 | 3,824 | 10.5 | 21.9 |

| Net income per share1 | 2.08 | 1.46 | 2.07 | 0.5 | 42.5 |

| Balance Sheet Data(Millions of pesos) | 4Q15 | 3Q15 | 4Q14 | % YoY | % QoQ |

| Total assets | 1,184,857 | 1,182,882 | 937,384 | 26.4 | 0.2 |

| Total loans | 547,745 | 526,037 | 465,541 | 17.7 | 4.1 |

| Deposits | 516,432 | 492,713 | 459,624 | 12.4 | 4.8 |

| Shareholders´s equity | 113,549 | 112,589 | 105,384 | 7.7 | 0.9 |

| Key Ratios | 4Q15 | 3Q15 | 4Q14 | bps YoY | bps QoQ |

| Net interest margin | 4.89% | 4.91% | 4.86% | 2.7 | (1.6) |

| Net loans to deposits ratio | 102.2% | 102.8% | 97.6% | 464.1 | (58.3) |

| ROAE | 12.9% | 12.1% | 14.0% | (109.0) | 78.6 |

| ROAA | 1.3% | 1.2% | 1.6% | (26.0) | 8.5 |

| Efficiency ratio | 42.0% | 42.9% | 43.0% | (100.2) | (87.8) |

| Capital ratio | 15.6% | 15.4% | 16.2% | (56.8) | 17.0 |

| NPLs ratio | 3.33% | 3.49% | 3.75% | (41.8) | (15.7) |

| Cost of Risk | 3.4% | 3.4% | 3.3% | 8.2 | (4.4) |

| Coverage ratio | 108.2% | 105.8% | 97.1% | 1,108.0 | 240.0 |

| Operating Data | 4Q15 | 3Q15 | 4Q14 | % YoY | % QoQ |

| Branches and offices2 | 1,377 | 1,374 | 1,346 | 2.3 | 0.2 |

| ATMs | 5,989 | 5,875 | 5,528 | 8.3 | 1.9 |

| Customers | 12,502,204 | 12,327,031 | 11,742,797 | 6.5 | 1.4 |

| Employees | 17,205 | 17,068 | 16,428 | 4.7 | 0.8 |

| 1) Accumulated EPS, net of treasury shares (compensation plan) and discontinued operations. Calculated by using weighted shares. |

2) As of 4Q15 includes: 1,079 branches (including 120 branches with Select service) + 18 SME offices + 7 SME branches + 119 cash desks (including 1 cash desk with Select service) + 11 Select offices + 45 Select units + 57 Select boxes + 18 Select corner + 23 brokerage house branches |

3

Héctor Grisi, Grupo Financiero Santander México’s Executive President and CEO, commented,“Our fourth quarter 2015 results reflect the many strengths and opportunities we see at Santander México. Total loans grew by 18% year-on-year, exceeding market growth, while we achieved even stronger performance in consumer loans, a clear reflection of the strength of our franchise. We hold leading market shares in core segments - SMEs, middle-market and mortgages, as well as solid positions in consumer banking and credit cards. Our heightened focus on individuals also allowed us to achieve a significant increase in retail deposit growth, although we maintain more ambitious targets for our long term share in this segment.”

“Despite our achievements, key profitability metrics remain below our desired levels. Since joining in December, I have been working closely with our leadership team on a thorough assessment of Santander México’s operations. The bank has identified its key challenges, and we are already implementing initiatives that will enable us to attract new clients and increase customer loyalty in our retail banking operations. Our goal is to be our customers’ primary bank and for this we need to become a client-centric franchise.”

“While Mexico has a growing economy and favorable market dynamics, like all banks, capital is becoming a scarce and increasingly costly resource. In this context, our mandate is clear: to improve profitability. At Santander México, we are uniquely positioned to better realize the strong potential of our investment and corporate banking business, creating additional synergies with our retail operation.”

“I am excited by the opportunities ahead, and confident that the operational transformation of our retail and corporate banking franchise, will ensure we achieve profitable, sustainable growth for customers and shareholders. I am fully committed to maintaining our focus on profitability, and look forward to updating you on our progress,” Mr. Grisi said.

4

SUMMARY OF FOURTH QUARTER 2015 CONSOLIDATED RESULTS

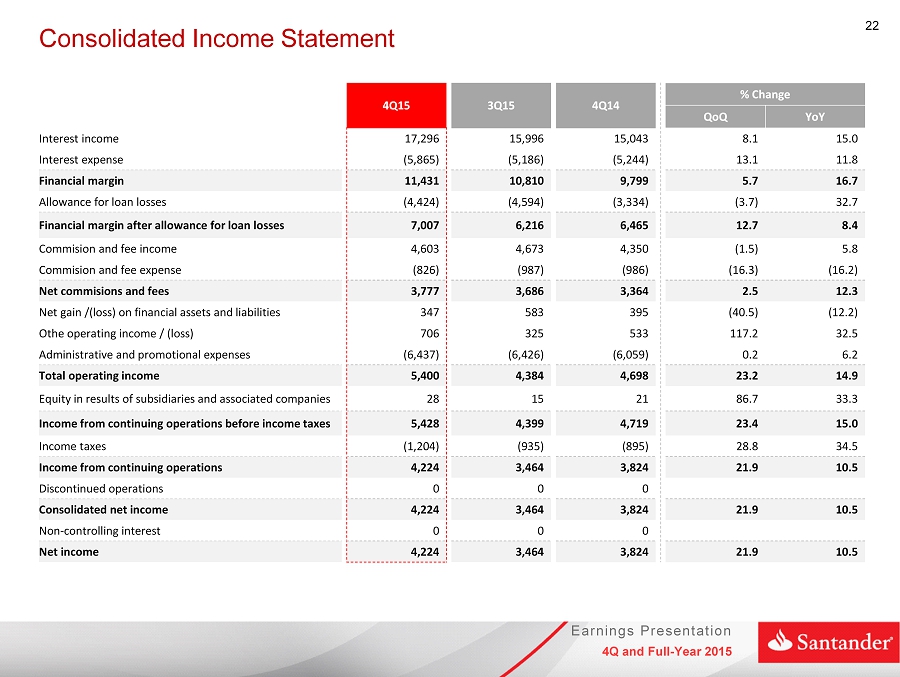

| Income statement |

| Millions of pesos | % Variation | % Variation | |||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Net interest income | 11,431 | 10,810 | 9,799 | 5.7 | 16.7 | 42,632 | 37,578 | 13.4 | |||

| Provisions for loan losses | (4,424) | (4,594) | (3,334) | (3.7) | 32.7 | (17,244) | (14,289) | 20.7 | |||

| Net interest income after provisions for loan losses | 7,007 | 6,216 | 6,465 | 12.7 | 8.4 | 25,388 | 23,289 | 9.0 | |||

| Commission and fee income, net | 3,777 | 3,686 | 3,364 | 2.5 | 12.3 | 14,772 | 13,417 | 10.1 | |||

| Net gain (loss) on financial assets and liabilities | 347 | 583 | 395 | (40.5) | (12.2) | 2,265 | 2,957 | (23.4) | |||

| Other operating income | 706 | 325 | 533 | 117.2 | 32.5 | 1,379 | 1,435 | (3.9) | |||

| Administrative and promotional expenses | (6,437) | (6,426) | (6,059) | 0.2 | 6.2 | (25,643) | (23,820) | 7.7 | |||

| Operating income | 5,400 | 4,384 | 4,698 | 23.2 | 14.9 | 18,161 | 17,278 | 5.1 | |||

| Equity in results of associated companies | 28 | 15 | 21 | 86.7 | 33.3 | 81 | 78 | 3.8 | |||

| Operating income before income taxes | 5,428 | 4,399 | 4,719 | 23.4 | 15.0 | 18,242 | 17,356 | 5.1 | |||

| Income taxes (net) | (1,204) | (935) | (895) | 28.8 | 34.5 | (4,100) | (3,341) | 22.7 | |||

| Income from continuing operations | 4,224 | 3,464 | 3,824 | 21.9 | 10.5 | 14,142 | 14,015 | 0.9 | |||

| Non-controlling interest | 0 | 0 | 0 | 0.0 | 0.0 | (1) | (1) | 0.0 | |||

| Net income | 4,224 | 3,464 | 3,824 | 21.9 | 10.5 | 14,141 | 14,014 | 0.9 | |||

Net income

Santander México reported net income for the quarter of Ps.4,224 million, representing YoY and QoQ increases of 10.5% and 21.9%, respectively. Net income for 12M15 increased by 0.9% to Ps.14,141 million.

4Q15 vs 4Q14

The 10.5% year-on-year increase in net income was principally driven by:

| i) | a 16.7%, or Ps.1,632 million, increase in net interest income, mainly reflecting interest income growth from the loan portfolio and a stable cost of deposits; |

| ii) | a 12.3%, or Ps.413 million, increase in net commissions and fees, principally due to the pick-up in debit and credit card fees in the quarter that resulted fromhigher card use and lower placement fees; higher fees from purchase-sale of securities and money market transactions, collections and payments, foreign trade and insurance. |

5

| iii) | a 32.5%, or Ps.173 million, increase in other operating income, mainly from higher recoveries of previously written-off loans. |

These contributions to net income were partially offset by:

| i) | a 32.7%, or Ps.1,090 million, increase in provisions for loan losses. This increase reflects: i) significant business volume growth across all segments; and ii) higher provisions resulting from the exposure to certain corporates; as well as a difficult comparable year-ago period, as 4Q14 benefitted from a reversal of provisions related to loans that were restructured in 3Q14 and became current in 4Q14; |

| ii) | a 6.2%, or Ps.378 million, increase in administrative and promotional expenses, mainly due to higher leaseholds, taxes and duties, as well as an increase in contributions to the bank savings protection system (IPAB) driven by the higher deposit base and other funding sources; |

| iii) | a 34.5%, or Ps.309 million, increase in expense taxes, that resulted in a 22.2% effective tax rate in the quarter compared to 19.0% in 4Q14; and |

| iv) | a 12.2%, or Ps.48 million, decrease in net gains on financial assets and liabilities, mainly due to lower customer activity as a result of market uncertainty. |

12M15 vs 12M14

Net income growth of 0.9% for 12M15, is mainly explained by the following increases:

| i) | a 13.4%, or Ps.5,054 million rise in net interest income, mainly reflecting higher interest income from the loan portfolio and a stable cost of deposits; and |

| ii) | a 10.1%, or Ps.1,355 million, in net commissions and fees, mainly resulting from growth in insurance, financial advisory, collections and payments and foreign trade, which more than offset lower debit and credit card fees. The decline in credit card fees during the year resulted from higher expenses incurred in connection with reward programs and placement fees in the open market. |

These contributions to net income were partially offset by:

| i) | a 20.7%, or Ps.2,955 million increase in provisions for loan losses. This reflects: i) significant business volume growth across all segments; ii) provisions required in connection with Pemex suppliers, homebuilders and the consumer loan portfolio acquired from Scotiabank and iii) provisions required in connection with the exposure to certain corporates; |

| ii) | a 7.7%, or Ps.1,823 million, increase in administrative and promotional expenses, mainly explained by higher salaries and employee benefits to support business growth; an increase in contributions to the IPAB resulting from a higher deposit base and other funding sources; followed by increases in leaseholds, depreciations and amortizations, and taxes and duties; |

| iii) | a 22.7%, or Ps.759 million, increase in tax expenses, that resulted in a 22.5% effective tax rate in the year which compares with 19.2% in 2014; |

| iv) | a 23.4%, or Ps.692 million, decrease in net gains on financial assets and liabilities, mainly due to lower customer activity as a result of market uncertainty, as well as a difficult comparable year-ago period which benefitted from the decrease in interest rates in 2Q14; and |

6

| v) | a 3.9%, or Ps.56 million, decrease in other operating income, which mainly resulted from an increase in portfolio recovery legal expenses and costs, as well as in write-offs and bankruptcies which more than offset higher recoveries of previously written-off loans and lower provisions for legal and tax contingencies. |

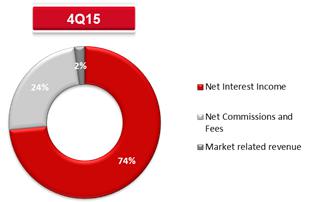

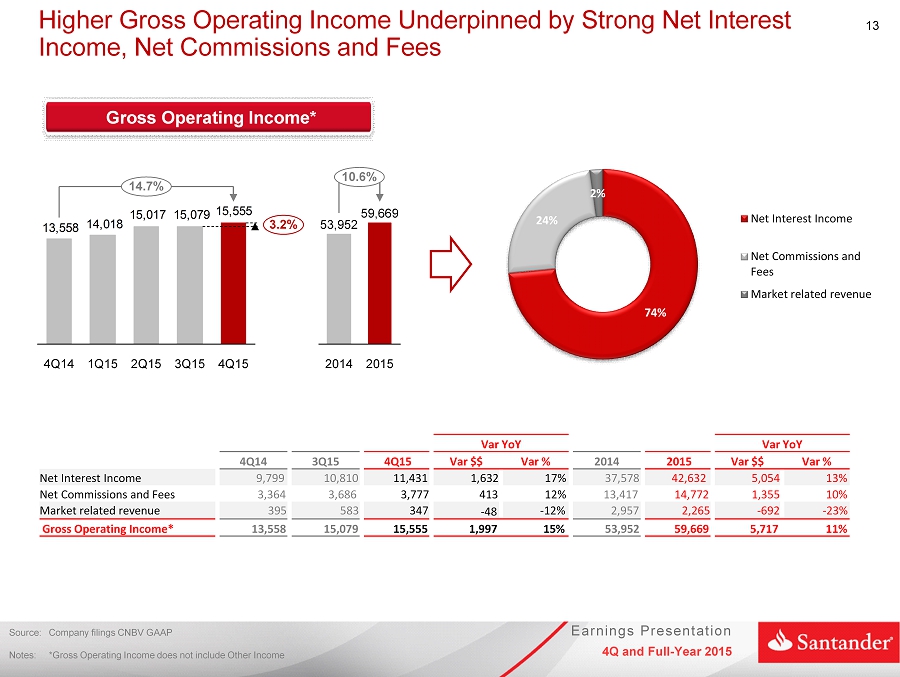

Gross Operating Income

Santander México’s gross operating income for 4Q15 totaled Ps.15,555 million, representing YoY and QoQ increases of 14.7% and 3.2%, respectively, and is broken down as follows.

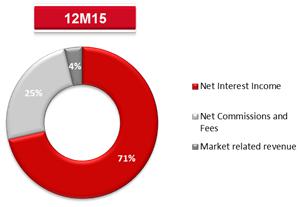

Gross operating income for 12M15 amounted to Ps.59,669 million, increasing 10.6% from 12M14, and is broken down as follows:

Profit Before Taxes

Profit before taxes in 4Q15 amounted to Ps.5,428 million, reflecting increases of 15.0% and 23.4% YoY and QoQ, respectively.

Profit before taxes for 12M15 amounted to Ps.18,242 million, and increased 5.1% YoY, mainly explained by higher net interest income and net commissions and fees, partially offset by lower income from trading gains and higher provisions for loan losses and expenses.

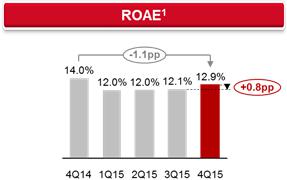

Return on Average Equity (ROAE)

Santander México´s ROAE in 4Q15 was 12.9%, which compares with 14.0% in 4Q14 and improved from 12.1% in 3Q15.

7

1Annualized net income divided by average equity (4Q14;4Q15)

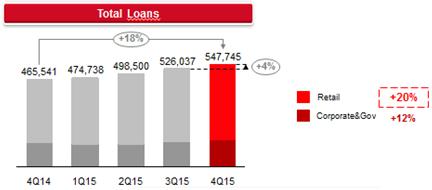

Loan portfolio growth

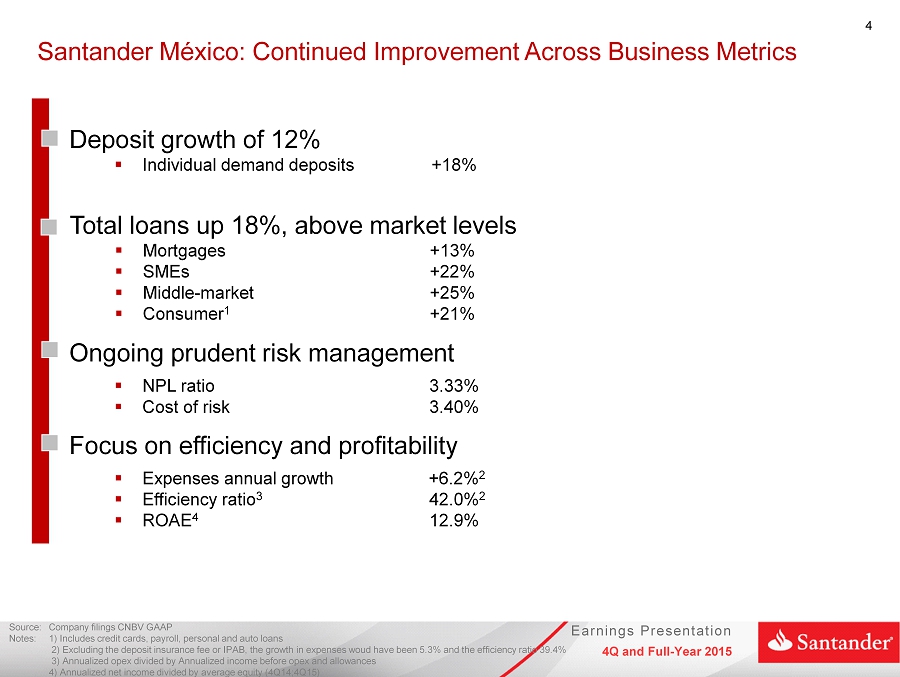

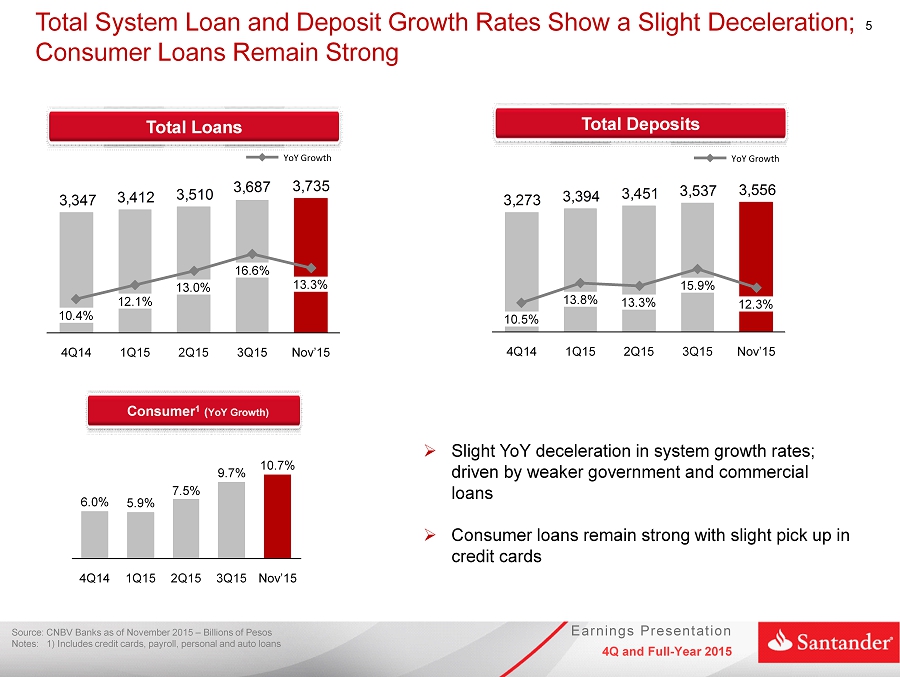

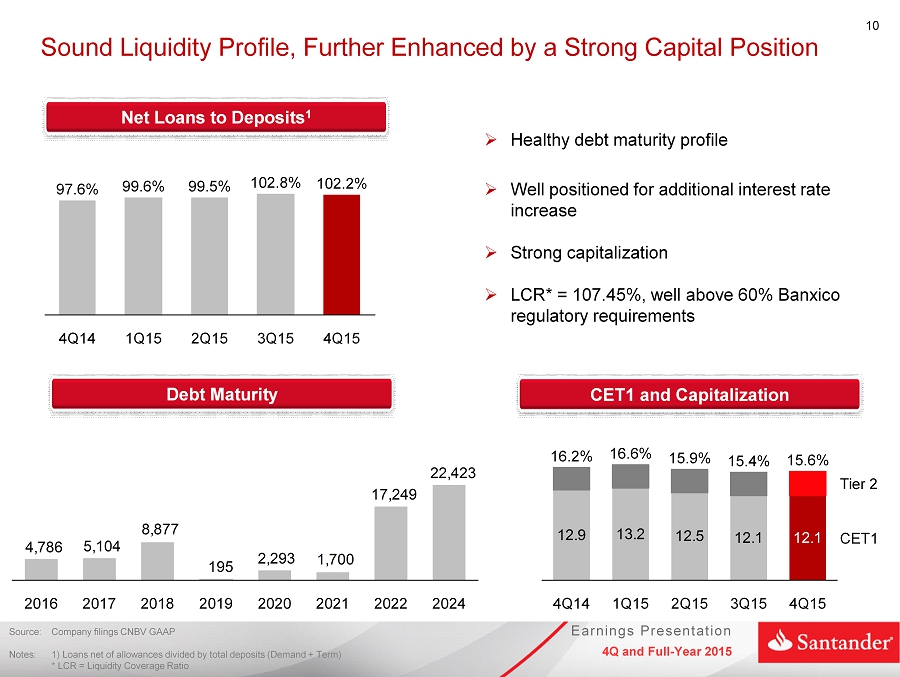

Santander México’s total loan portfolio as of 4Q15 increased YoY by 17.7%, or Ps.82,204 million, to Ps.547,745 million, and by 4.1%, or Ps.21,708 million, on a sequential basis.

In 4Q15, Santander México’s loan portfolio expanded YoY above market growth rates and showed positive trends across all core products, in both the individual and commercial loan segments.

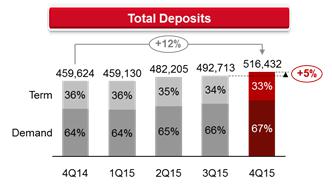

Deposits and loans to deposit ratio

In 4Q15, deposits increased 12.4% YoY and 4.8% sequentially; representing 48.2% of Santander México’s total funding sources. This deposit base provides stable, low-cost funding to support Santander México’s continued growth.

The net loan to deposit ratio was 102.2% in 4Q15, which compares with 97.6% in 4Q14 and 102.8% in 3Q15.

|  |

8

ANALYSIS OF FOURTH QUARTER 2015 CONSOLIDATED RESULTS

(Amounts expressed in millions of pesos, except where otherwise stated)

Net interest income

| Net interest income | ||||||||||

| Millions of pesos | % Variation | % Variation | ||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | |||

| Interest on funds available | 317 | 327 | 351 | (3.1) | (9.7) | 1,322 | 1,384 | (4.5) | ||

| Interest on margin accounts | 103 | 105 | 65 | (1.9) | 58.5 | 366 | 278 | 31.7 | ||

| Interest and yield on securities | 3,379 | 2,631 | 2,523 | 28.4 | 33.9 | 10,723 | 9,219 | 16.3 | ||

| Interest and yield on loan portfolio – excluding credit cards | 10,352 | 9,997 | 8,677 | 3.6 | 19.3 | 39,031 | 33,480 | 16.6 | ||

| Interest and yield on loan portfolio related to credit card transactions | 2,499 | 2,446 | 2,443 | 2.2 | 2.3 | 9,794 | 9,725 | 0.7 | ||

| Commissions collected on loan originations | 213 | 165 | 189 | 29.1 | 12.7 | 733 | 783 | (6.4) | ||

| Interest and premium on sale and repurchase agreements and securities loans | 433 | 325 | 795 | 33.2 | (45.5) | 1,804 | 2,988 | (39.6) | ||

| Interest income | 17,296 | 15,996 | 15,043 | 8.1 | 15.0 | 63,773 | 57,857 | 10.2 | ||

| Daily average interest earning assets* | 871,957 | 772,855 | 12.8 | |||||||

| Interest from customer deposits – demand deposits | (841) | (818) | (856) | 2.8 | (1.8) | (3,194) | (3,098) | 3.1 | ||

| Interest from customer deposits – time deposits | (1,099) | (1,153) | (1,064) | (4.7) | 3.3 | (4,361) | (4,324) | 0.9 | ||

| Interest from credit instruments issued | (373) | (354) | (293) | 5.4 | 27.3 | (1,361) | (1,152) | 18.1 | ||

| Interest on bank and other loans | (571) | (505) | (488) | 13.1 | 17.0 | (2,107) | (1,874) | 12.4 | ||

| Interest on subordinated capital notes | (424) | (419) | (475) | 1.2 | (10.7) | (1,737) | (1,783) | (2.6) | ||

| Interest and premium on sale and repurchase agreements and securities loans | (2,557) | (1,937) | (2,068) | 32.0 | 23.6 | (8,381) | (8,048) | 4.1 | ||

| Interest expense | (5,865) | (5,186) | (5,244) | 13.1 | 11.8 | (21,141) | (20,279) | 4.3 | ||

| Net interest income | 11,431 | 10,810 | 9,799 | 5.7 | 16.7 | 42,632 | 37,578 | 13.4 | ||

*Includes funds available, margin accounts, investments in securities, loan portfolio and sale and repurchase agreements

Net interest income in 4Q15 increased YoY by 16.7%, or Ps.1,632 million, to Ps.11,431 million and QoQ by 5.7%, or Ps.621 million.

The 16.7% YoY increase in net interest income resulted from the combined effect of:

| i) | A 15.0%, or Ps.2,253 million, increase in interest income, to Ps.17,296 million, explained by an increase of Ps.122,584 million, or 14.6%, in average interest-earning assets and a 3 basis points increase in the average interest income rate; and |

| ii) | An 11.8%, or Ps.621 million, increase in interest expense, to Ps.5,865 million, resulting from an increase of Ps.90,760 million, or 11.8%, in interest-bearing liabilities while the average interest rate paid remained unchanged. |

The net interest margin ratio (NIM) calculated with daily average interest-earning assets for 4Q15 improved to 4.74% from 4.66% in 4Q14.

9

NIM calculated with daily average interest-earning assets for 12M15 improved slightly to 4.89% from 4.86% in 12M14.

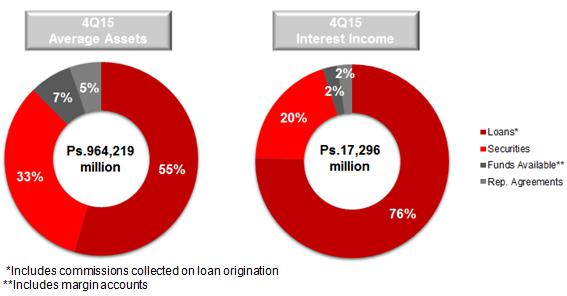

Interest Income

Santander México’s main source of recurring interest income comes from the loan portfolio, which in 4Q15 accounted for 75.5% of interest income and 54.5% of average interest earning assets. The sources of earnings in this line item are broken down as follows:

The average interest rate on interest-earning assets for 4Q15 stood at 7.02%, increasing 3 basis points from 6.99% in 4Q14.

Interest income for 4Q15 increased by 15.0%, or Ps.2,253 million, to Ps.17,296 million. On a sequential basis, interest income increased by 8.1%, or Ps.1,300 million.

The 15.0% YoY increase in interest income mainly reflects increases of:

| i) | 15.5%, or Ps.1,755 million, in interest income from our total loan portfolio and commissions on loan origination, which resulted from the combined effect of a Ps.79,031 million, or 17.7%, increase in the average loan portfolio volume, and a 18 basis points decrease in the average interest rate. |

The increase in the average loan portfolio volume is explained by increases across all segments and products, as follows:

| § | 18.7%, or Ps.50,031 million, in the commercial portfolio, mainly reflecting increases of Ps.22,960, or 21.5% million, and Ps.10,226 million, or 20.3%, in mid-market and SMEs, respectively; |

| § | 13.1%, or Ps.13,672 million, in mortgages; |

| § | 33.7%, or Ps.10,905 million, in consumer loans; and |

| § | 10.5%, or Ps.4,423 million, in credit card loans. |

The increase in the average loan portfolio volume more than offset the lower average interest rate earned.

10

The decrease in the average interest rate earned is mainly explained by the prevailing low reference rate in 2015 due to the cut from the Mexican Central Bank during 2014. Variation in the average interest rate earned is broken down as follows:

| § | A 2 basis points decrease in the commercial portfolio, from 5.93% in 4Q14 to 5.91% in 4Q15. This decrease partially resulted from the low reference rate and is also explained by higher competition in middle-market and SMEs; |

| § | A 18 basis points decrease in mortgages, from 9.64% to 9.46%; |

| § | A 39 basis points decrease in consumer loans (excluding credit cards), from 24.76% to 24.37%, explained by the cut in the reference rate during 2014; and |

| § | A 170 basis points decrease in credit cards, from 22.77% to 21.07%, which in addition to the lower reference rate, was further affected by a change in mix in the composition of our credit card portfolio, as we are seeing higher customers who pay their outstanding balances in full therefore not contributing to interest income. |

| ii) | 33.9%, or Ps.856 million, in interest income from our investment in securities portfolio, due to a Ps.86,468 million, or 37.2%, increase in average volume of this portfolio, partially offset by a 10 basis points decrease in the average interest rate earned; and |

| iii) | 58.5%, or Ps.38 million, in margin accounts, which resulted from a Ps.9,946 million, or 49.0%, increase the average volume together with an 8 basis point increase in the average interest rate earned. |

These increases in interest income were partially offset by decreases of:

| i) | 45.5%, or Ps.362 million, in sale and repurchase agreement transactions, which resulted from a Ps.49,230 million, or 49.1%, decrease in the average volume, partially offset by a 22 basis points increase in the average interest rate earned; and |

| ii) | 9.7%, or Ps.34 million, in funds available, which resulted from the combined effect of a Ps.3,631 million, or 8.6%, decrease in the average volume, together with a 4 basis points decrease in the average interest rate earned. |

11

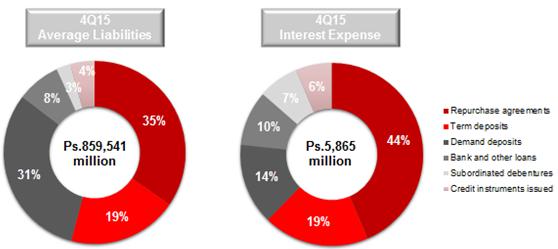

Interest Expense

Santander México’s main sources of funding are repurchase agreements and customer deposits. In 4Q15 these accounted for 43.6% and 33.1% of interest expense, respectively; and 34.7% and 50.7% of average interest liabilities, respectively. Santander México’s funding structure is broken down as follows:

The average interest rate on interest-bearing liabilities remained flat at 2.67% in 4Q15. This stable rate mainly reflects the decrease in reference rates enacted by the Mexican Central Bank during 2014 which resulted in lower interest paid on customer deposits, as well as a shift in the deposit mix towards demand deposits.

Interest expense for 4Q15 increased 11.8%, or Ps.621 million, to Ps.5,865 million. On a sequential basis, interest expense increased by 13.1%, or Ps.679 million.

The 11.8% YoY increase in interest expense mainly reflects increases of:

| i) | 23.6%, or Ps.489 million, in interest paid on sale and repurchase agreement transactions, which resulted from the combined effect of a Ps.26,616 million, or 9.8% increase in the average volume and a 38 basis points increase in the average interest rate paid; |

| ii) | 17.0%, or Ps.83 million, in bank and other loans, mainly due to a Ps.11,886 million, or 21.7% increase in the average volume, was partially offset by a 13 basis points decrease in the average interest rate paid; |

| iii) | 27.3%, or Ps.80 million, in credit instruments issued, which resulted from a Ps.10,800 million, or 41.4% increase in the average volume of credit instruments issued which was partially offset by a 44 basis points decrease in the average interest rate paid; and |

| iv) | 3.3%, or Ps.35 million, in term deposits, which resulted from a Ps.14,159 million, or 9.3% increase in the average volume, partially offset by a 15 basis points decrease in the average interest rate paid. |

These increases in interest expense were partially offset by the following declines:

| i) | 10.7%, or Ps.51 million, on interest paid on subordinated notes, due to a Ps.3,742 million, or 20.7% increase in the average volume together with a 268 basis point decrease in the average interest rate paid; and |

| ii) | 1.8%, or Ps.15 million, on interest paid on demand deposits, due to a Ps.23,557 million, or 9.6% increase in the average volume together with a 15 basis point decrease in the average interest rate paid. |

12

Commission and fee income, net

| Commission and fee income, net | |||||||||||

| Millions of pesos | % Variation | % Variation | |||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Commission and fee income | |||||||||||

| Debit and credit card | 1,424 | 1,307 | 1,257 | 9.0 | 13.3 | 5,196 | 4,756 | 9.3 | |||

| Account management | 220 | 240 | 237 | (8.3) | (7.2) | 896 | 816 | 9.8 | |||

| Collection services | 530 | 531 | 455 | (0.2) | 16.5 | 2,114 | 1,830 | 15.5 | |||

| Investment funds | 350 | 337 | 341 | 3.9 | 2.6 | 1,363 | 1,369 | (0.4) | |||

| Insurance | 1,004 | 1,047 | 1,028 | (4.1) | (2.3) | 4,106 | 3,896 | 5.4 | |||

| Purchase-sale of securities and money market transactions | 204 | 203 | 187 | 0.5 | 9.1 | 814 | 833 | (2.3) | |||

| Checks trading | 65 | 63 | 78 | 3.2 | (16.7) | 257 | 302 | (14.9) | |||

| Foreign trade | 233 | 224 | 175 | 4.0 | 33.1 | 866 | 701 | 23.5 | |||

| Financial advisory services | 365 | 511 | 386 | (28.6) | (5.4) | 1,745 | 1,505 | 15.9 | |||

| Other | 208 | 210 | 206 | (1.0) | 1.0 | 889 | 850 | 4.6 | |||

| Total | 4,603 | 4,673 | 4,350 | (1.5) | 5.8 | 18,246 | 16,858 | 8.2 | |||

| Commission and fee expense | |||||||||||

| Debit and credit card | (438) | (532) | (418) | (17.7) | 4.8 | (1,895) | (1,451) | 30.6 | |||

| Investment funds | (2) | (2) | (16) | 0.0 | (87.5) | (25) | (73) | (65.8) | |||

| Insurance | 25 | (25) | (34) | (200.0) | (173.5) | (18) | (103) | (82.5) | |||

| Purchase-sale of securities and money market transactions | (91) | (71) | (155) | 28.2 | (41.3) | (302) | (406) | (25.6) | |||

| Checks trading | (6) | (6) | (9) | 0.0 | (33.3) | (23) | (33) | (30.3) | |||

| Financial advisory services | (13) | (14) | (2) | (7.1) | 550.0 | (46) | (62) | (25.8) | |||

| Other | (301) | (337) | (352) | (10.7) | (14.5) | (1,165) | (1,313) | (11.3) | |||

| Total | (826) | (987) | (986) | (16.3) | (16.2) | (3,474) | (3,441) | 1.0 | |||

| Commission and fee income, net | |||||||||||

| Debit and credit card | 986 | 775 | 839 | 27.2 | 17.5 | 3,301 | 3,305 | (0.1) | |||

| Account management | 220 | 240 | 237 | (8.3) | (7.2) | 896 | 816 | 9.8 | |||

| Collection services | 530 | 531 | 455 | (0.2) | 16.5 | 2,114 | 1,830 | 15.5 | |||

| Investment funds | 348 | 335 | 325 | 3.9 | 7.1 | 1,338 | 1,296 | 3.2 | |||

| Insurance | 1,029 | 1,022 | 994 | 0.7 | 3.5 | 4,088 | 3,793 | 7.8 | |||

| Purchase-sale of securities and money market transactions | 113 | 132 | 32 | (14.4) | 253.1 | 512 | 427 | 19.9 | |||

| Checks trading | 59 | 57 | 69 | 3.5 | (14.5) | 234 | 269 | (13.0) | |||

| Foreign trade | 233 | 224 | 175 | 4.0 | 33.1 | 866 | 701 | 23.5 | |||

| Financial advisory services | 352 | 497 | 384 | (29.2) | (8.3) | 1,699 | 1,443 | 17.7 | |||

| Other | (93) | (127) | (146) | (26.8) | (36.3) | (276) | (463) | (40.4) | |||

| Total | 3,777 | 3,686 | 3,364 | 2.5 | 12.3 | 14,772 | 13,417 | 10.1 |

* Includes fees from: collections and payments, account management, checks, foreign trade and others

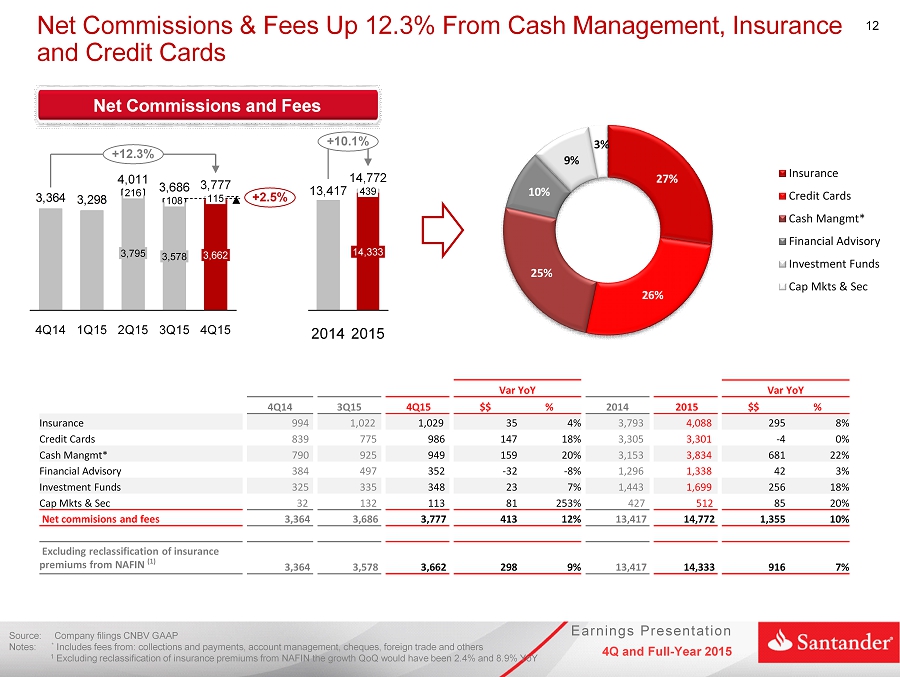

In 4Q15, net commission and fee income totaled Ps.3,777 million, increasing YoY by 12.3%, or Ps.413 million, and by 2.5%, or Ps.91 million, QoQ.

In 2Q15, the cost associated to the insurance premium paid to NAFIN in connection with the guarantee programs for SMEs was reclassified from commission and fee income to expenses for loan recoveries in the other operating income line. On a comparable basis, excluding the reclassification of the insurance premiums, net commissions and fees increased 8.9% YoY and 2.4% sequentially.

13

The main contributor to net commissions and fees in the quarter were insurance fees, which accounted for 27.2% of the total, followed by debit and credit card and cash management1 fees which accounted for 26.1% and 25.1% of total commissions and fees, respectively.

| Commission and fee income, net | |||||||||

| Breakdown (%) | |||||||||

| 4Q15 | 3Q15 | 4Q14 | 12M15 | 12M14 | |||||

| Debit and Credit card | 26.1 | 21.0 | 24.9 | 22.3 | 24.6 | ||||

| Account management | 5.8 | 6.5 | 7.0 | 6.1 | 6.1 | ||||

| Collection services | 14.0 | 14.4 | 13.5 | 14.3 | 13.6 | ||||

| Investment funds | 9.2 | 9.1 | 9.7 | 9.1 | 9.7 | ||||

| Insurance | 27.2 | 27.7 | 29.5 | 27.7 | 28.3 | ||||

| Purchase-sale of securities and money market transactions | 3.0 | 3.6 | 1.0 | 3.5 | 3.2 | ||||

| Checks trading | 1.6 | 1.5 | 2.1 | 1.6 | 2.0 | ||||

| Foreign trade | 6.2 | 6.1 | 5.2 | 5.9 | 5.2 | ||||

| Financial advisory services | 9.3 | 13.5 | 11.4 | 11.5 | 10.8 | ||||

| Other | (2.5) | (3.4) | (4.3) | (1.9) | (3.5) | ||||

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

The 12.3% YoY increase of net commissions and fees in 4Q15 mainly resulted from the following increases:

| i) | 17.5%, or Ps.147 million, in debit and credit cards, mainly reflecting a pick-up after three consecutive flat quarters which resulted from higher card use together with lower placement fees and reward costs in the quarter; |

| ii) | 253.1%, or Ps.81 million, in purchase-sale of securities and money market transactions; |

| iii) | 16.5%, or Ps.75 million, in collection and payment services, reflecting recurring customer activity and transaction activity; and |

| iv) | 33.1%, or Ps.58 million, in foreign trade, which resulted from our strong focus on growing this business and our wide product offering. |

These increases in net commissions and fees were partially offset by an 8.3%, or Ps.32 million, decline in financial advisory fees as this quarter Santander México executed a lower number of deals from its pipeline reflecting weaker market conditions in this segment.

1* Cash management fees include fees from: collections and payments, account management, checks, foreign trade and others

14

Net gain (loss) on financial assets and liabilities

Net gain (loss) on financial assets and liabilities | |||||||||||

| Millions of pesos | % Variation | % Variation | |||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Valuation | |||||||||||

| Foreign exchange | 608 | 116 | (101) | 424.1 | (702.0) | 719 | (101) | (811.9) | |||

| Derivatives | (489) | 2,075 | 3,331 | (123.6) | (114.7) | 8,225 | 3,909 | 110.4 | |||

| Shares | (361) | 235 | (71) | (253.6) | 408.5 | (90) | (118) | (23.7) | |||

| Debt instruments | (76) | (533) | (238) | (85.7) | (68.1) | (967) | 471 | (305.3) | |||

| Valuation result | (318) | 1,893 | 2,921 | (116.8) | (110.9) | 7,887 | 4,161 | 89.5 | |||

| Purchase / sale of securities | |||||||||||

| Foreign exchange | (572) | (212) | (566) | 169.8 | 1.1 | (1,407) | (689) | 104.2 | |||

| Derivatives | 1,415 | (1,606) | (2,044) | (188.1) | (169.2) | (5,134) | (938) | 447.3 | |||

| Shares | (47) | 140 | (90) | (133.6) | (47.8) | 65 | 50 | 30.0 | |||

| Debt instruments | (131) | 368 | 174 | (135.6) | (175.3) | 854 | 373 | 129.0 | |||

| Purchase -sale result | 665 | (1,310) | (2,526) | (150.8) | (126.3) | (5,622) | (1,204) | 366.9 | |||

| Total | 347 | 583 | 395 | (40.5) | (12.2) | 2,265 | 2,957 | (23.4) | |||

In 4Q15, Santander México reported a Ps.347 million net gain from financial assets and liabilities, which compares with gains of Ps.395 million in 4Q14 and Ps.583 million in 3Q15.

The Ps.347 million net gain from financial assets and liabilities in the quarter is mainly explained by:

| i) | A Ps.665 million purchase-sale gain principally related to gains of Ps.1,415 million in derivatives, which were partially offset by purchase-sale losses of Ps.572 million, Ps.131 million and Ps.47 million in foreign exchange instruments, debt instruments and share instruments. |

This gain was partially offset by:

| i) | A Ps.318 million valuation loss which resulted from losses of Ps.489 million, Ps.361 million and Ps.76 million in derivatives, share instruments and in debt instruments, respectively. These valuation losses were partially offset by gains of Ps.608 million in foreign exchange instruments. |

15

Other operating income

| Other operating income |

| Millions of pesos | % Variation | % Variation | |||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Recovery of previously written-off loans | 860 | 601 | 733 | 43.1 | 17.3 | 2,443 | 2,164 | 12.9 | |||

| Cancellation of liabilities and reserves | 77 | 85 | 60 | (9.4) | 28.3 | 329 | 239 | 37.7 | |||

| Interest on personnel loans | 30 | 29 | 27 | 3.4 | 11.1 | 114 | 111 | 2.7 | |||

| Allowance for losses on foreclosed assets | (24) | (36) | (7) | (33.3) | 242.9 | (88) | (40) | 120.0 | |||

| Profit from sale of foreclosed assets | 43 | 55 | 72 | (21.8) | (40.3) | 237 | 478 | (50.4) | |||

| Technical advisory services | 3 | 6 | 7 | (50.0) | (57.1) | 16 | 19 | (15.8) | |||

| Portfolio recovery legal expenses and costs | (321) | (333) | (220) | (3.6) | 45.9 | (1,215) | (728) | 66.9 | |||

| Write-offs and bankruptcies | (72) | (316) | (146) | (77.2) | (50.7) | (828) | (654) | 26.6 | |||

| Provision for legal and tax contingencies | 59 | 40 | (62) | 47.5 | (195.2) | 15 | (227) | (106.6) | |||

| IPAB ("Indemnity") provisions and payments | (2) | (1) | (1) | 100.0 | 100.0 | (6) | (6) | 0.0 | |||

| Result on sale of loan portfolio | 0 | 0 | 6 | 0.0 | (100.0) | 52 | (100) | (152.0) | |||

| Income from acquisition of Scotiabank portfolio | 177 | 0 | (100.0) | 0.0 | 177 | 0 | 0.0 | ||||

| Others | 53 | 18 | 64 | 194.4 | (17.2) | 133 | 179 | (25.7) | |||

| Total | 706 | 325 | 533 | 117.2 | 32.5 | 1,379 | 1,435 | (3.9) | |||

Other income in 4Q15 totaled Ps.706 million, up from Ps.533 million in 4Q14 and Ps.325 million in 3Q15, representing increases of 32.5% YoY and 117.2% QoQ. These comparisons however, are affected by the reclassification made in 2Q15 where the cost associated with the insurance premium paid to NAFIN in connection with the guarantee programs for SMEs was reclassified from commission and fee expense to expenses for loan recoveries in the other operating income line. Excluding this effect, on a comparable basis, other income increased Ps.288 million, or 54.0%, YoY and Ps.388 million, or 89.6%, QoQ.

The 32.5% YoY increase in other income was mainly driven by the following;

| i) | A Ps.127 million, or 17.3%, increase in recoveries from previously written off loans, mainly explained by the sale of Ps.242 million written-off loans; |

| ii) | A Ps.121 million, or 195.2%, decrease in provision for legal and tax contingencies; and |

| iii) | A Ps.74 million, or 50.7%, decrease in expenses in connection with write-offs and bankruptcies. |

These contributions to other income were partially offset by a Ps.101 million, or 45.9%, increase in portfolio recovery costs and legal expenses. On a comparable basis, excluding the cost associated with the insurance premium paid to NAFIN, these expenses would have decreased 6.3% or Ps.14 million.

16

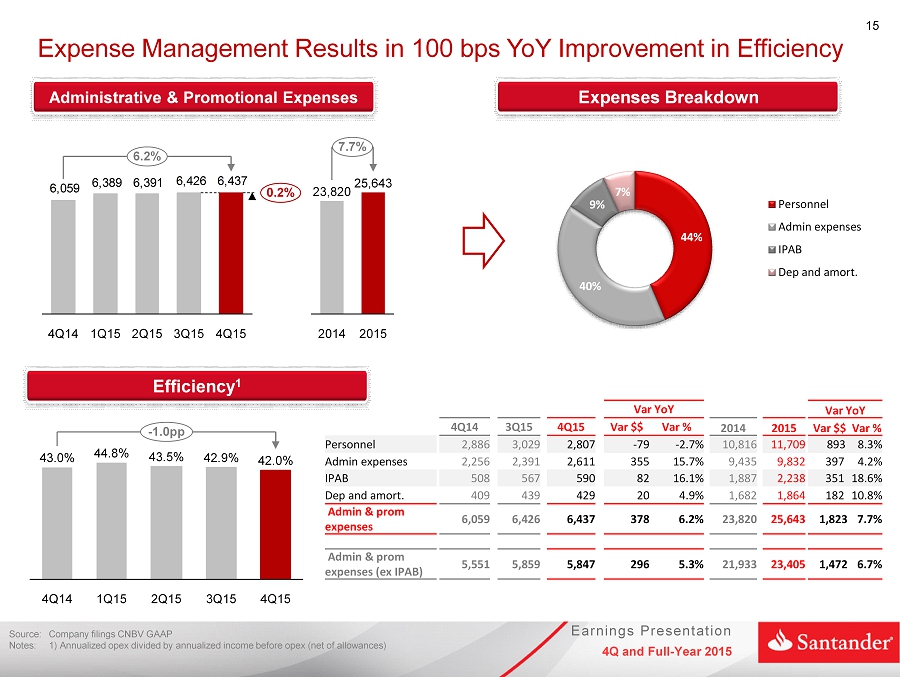

Administrative and promotional expenses

Administrative and promotional expenses consist of personnel costs such as payroll and benefits, promotion and advertising expenses, and other general expenses. Personnel expenses consist mainly of salaries, social security contributions, bonuses and our long-term incentive plan for our executives. Other general expenses mainly consist of: expenses related to technology and systems, administrative services, which are mainly services outsourced in the areas of information technology, taxes and duties, professional fees, contributions to bank savings protection system (IPAB), rental of properties and hardware, advertising and communication, surveillance and cash courier services and expenses related to maintenance, conservation and repair, among others.

| Administrative and promotional expenses | |||||||||||

| Millions of pesos | % Variation | % Variation | |||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Salaries and employee benefits | 2,807 | 3,029 | 2,886 | (7.3) | (2.7) | 11,709 | 10,816 | 8.3 | |||

| Credit card operation | 55 | 72 | 77 | (23.6) | (28.6) | 314 | 285 | 10.2 | |||

| Professional fees | 168 | 92 | 166 | 82.6 | 1.2 | 458 | 437 | 4.8 | |||

| Leasehold | 555 | 427 | 393 | 30.0 | 41.2 | 1,844 | 1,622 | 13.7 | |||

| Promotional and advertising expenses | 243 | 88 | 162 | 176.1 | 50.0 | 659 | 564 | 16.8 | |||

| Taxes and duties | 320 | 358 | 167 | (10.6) | 91.6 | 1,366 | 1,184 | 15.4 | |||

| Technology services (IT) | 527 | 688 | 578 | (23.4) | (8.8) | 2,400 | 2,404 | (0.2) | |||

| Depreciation and amortization | 429 | 439 | 409 | (2.3) | 4.9 | 1,864 | 1,682 | 10.8 | |||

| Contributions to bank savings protection system (IPAB) | 590 | 567 | 508 | 4.1 | 16.1 | 2,238 | 1,887 | 18.6 | |||

| Cash protection | 146 | 154 | 109 | (5.2) | 33.9 | 611 | 589 | 3.7 | |||

| Others | 597 | 512 | 604 | 16.6 | (1.2) | 2,180 | 2,350 | (7.2) | |||

| Total | 6,437 | 6,426 | 6,059 | 0.2 | 6.2 | 25,643 | 23,820 | 7.7 | |||

Santander México’s administrative and promotional expenses are broken down as follows:

| Administrative and promotional expenses | |||||||||

| Breakdown (%) | |||||||||

| 4Q15 | 3Q15 | 4Q14 | 12M15 | 12M14 | |||||

| Salaries and employee benefits | 43.6 | 47.1 | 47.6 | 45.7 | 45.4 | ||||

| Credit card operation | 0.9 | 1.1 | 1.3 | 1.2 | 1.2 | ||||

| Professional fees | 2.6 | 1.4 | 2.7 | 1.8 | 1.8 | ||||

| Leasehold | 8.6 | 6.6 | 6.5 | 7.2 | 6.8 | ||||

| Promotional and advertising expenses | 3.8 | 1.4 | 2.7 | 2.6 | 2.4 | ||||

| Taxes and duties | 5.0 | 5.6 | 2.8 | 5.3 | 5.0 | ||||

| Technology services (IT) | 8.2 | 10.7 | 9.5 | 9.4 | 10.1 | ||||

| Depreciation and amortization | 6.7 | 6.8 | 6.8 | 7.3 | 7.1 | ||||

| Contributions to bank savings protection system (IPAB) | 9.2 | 8.8 | 8.4 | 8.7 | 7.9 | ||||

| Cash protection | 2.3 | 2.4 | 1.8 | 2.4 | 2.5 | ||||

| Others | 9.3 | 8.0 | 10.0 | 8.5 | 9.9 | ||||

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | ||||

Administrative and promotional expenses in 4Q15 amounted to Ps.6,437 million which compare with Ps.6,059 million in 4Q14 and Ps.6,426 million in 3Q15, increasing 6.2% YoY and remaining flat QoQ.

17

The 6.2% YoY rise in administrative and promotional expenses was mainly due to the following increases:

| i) | A 41.2%, or Ps.162 million, in leaseholds, mainly reflecting a larger number of branches which resulted from the branch expansion plan executed in the past two years; |

| ii) | A 91.6%, or Ps.153 million, in taxes and duties; |

| iii) | A 50.0%, or Ps.81 million, in promotional and advertising expenses, reflecting the investment in positioning “Santander’s” brand during the last quarter at events such as Formula 1 in Mexico during November 2015; and |

| iv) | A 16.1%, or Ps.82 million, in contributions to the bank savings protection system (IPAB), reflecting growth in funding sources. |

Expenses continue to reflect cost management initiatives that translate into an optimized operating structure, mitigating costs resulting from the investment in strategic businesses, technology and a larger branch network.

Expenses include the deposit insurance fee or IPAB, which increased YoY by 16.1%, or Ps.82 million, reflecting growth in funding sources. Excluding the deposit insurance fee, expenses would have increased by 5.3%.

The implementation of tight cost controls across the organization combined with strong core earnings allowed us to improve the efficiency ratio by 100 basis points YoY to 42.0% from 43.0% and by 90 basis points sequentially.

The recurrence ratio was 62.1%, which compares to 60.6% reported in 4Q14 and 61.9% in 3Q15.

Income Taxes

In 4Q15 Santander México reported a tax expense of Ps.1,204 million compared to tax expenses of Ps.895 million in 4Q14 and Ps.935 million in 3Q15.

The effective tax rate for the quarter was 22.2%, 320 basis points and 90 basis points higher compared to 19.0% reported in 4Q14 and 21.3% paid in 3Q15. The effective tax rate for the twelve-month period ending 31 December, 2015 was 22.5%.

Contribution to net income by subsidiary

Reported net income in 4Q15 was Ps.4,224 million, representing increases of 10.5% YoY and 21.9% QoQ.

Casa de Bolsa Santander, the brokerage business, reported net profit of Ps.8 million in 4Q15, compared with net loss of Ps.2 million in 4Q14 and net profit of Ps.3 million in 3Q15.

The Holding (Grupo Financiero) reported a net loss of Ps.20 million in 4Q15, compared with net losses of Ps.16 million in 4Q14 and Ps.14 million in 3Q15.

| Earnings contribution by subsidiary |

| Millions of pesos | |||||||||||

| % Variation | % Variation | ||||||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | 12M15 | 12M14 | 15/14 | ||||

| Banking business 1/ | 4,236 | 3,475 | 3,842 | 21.9 | 10.3 | 14,186 | 14,053 | 0.9 | |||

| Brokerage | 8 | 3 | (2) | 166.7 | 500.0 | 12 | 11 | 9.1 | |||

| Holding | (20) | (14) | (16) | 42.9 | 25.0 | (57) | (50) | 14.0 | |||

| Net income attributable to Grupo Financiero Santander México | 4,224 | 3,464 | 3,824 | 21.9 | 10.5 | 14,141 | 14,014 | 0.9 | |||

| 1/Includes sofomes | |||||||||||

18

LOAN PORTFOLIO AND ASSET QUALITY

Loan portfolio

The evolution of the loan portfolio continues to show a positive trend, with diversification in all segments and growth across all core businesses.

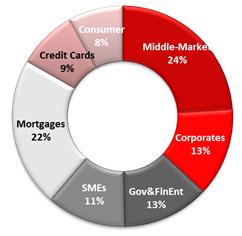

| Portfolio Breakdown | |||||||

| Millions of pesos | % Variation | ||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | |||

| Commercial | 335,575 | 320,963 | 283,329 | 4.6 | 18.4 | ||

| Middle- market | 131,503 | 128,805 | 105,552 | 2.1 | 24.6 | ||

| Corporates | 70,865 | 67,132 | 64,435 | 5.6 | 10.0 | ||

| SME´s | 63,493 | 62,020 | 51,835 | 2.4 | 22.5 | ||

| Government & Financial Entities | 69,714 | 63,006 | 61,507 | 10.6 | 13.3 | ||

| Individuals | 212,170 | 205,074 | 182,212 | 3.5 | 16.4 | ||

| Consumer | 91,693 | 88,273 | 75,624 | 3.9 | 21.2 | ||

| Credit Cards | 47,775 | 45,515 | 42,104 | 5.0 | 13.5 | ||

| Other Consumer | 43,918 | 42,758 | 33,520 | 2.7 | 31.0 | ||

| Mortgages | 120,477 | 116,801 | 106,588 | 3.1 | 13.0 | ||

| Total | 547,745 | 526,037 | 465,541 | 4.1 | 17.7 | ||

The total loan portfolio rose YoY by 17.7%, or Ps.82,204 million, to Ps.547,745 million in 4Q15. On a sequential basis, the total loan portfolio increased 4.1%, or Ps.21,708 million. All core segments grew above market rates, with SMEs, middle-market, mortgages and consumer showing the strongest performance, followed by corporates and government entities, and financial institutions that also posted healthy growth. Meanwhile, credit cards continued to recover, growing above market rates.

19

| Loan portfolio breakdown | ||||||||

| Millions of pesos | ||||||||

| 4Q15 | % | 3Q15 | % | 4Q14 | % | |||

| Performing loans | ||||||||

| Commercial | 326,979 | 59.7 | 311,781 | 59.3 | 274,438 | 59.0 | ||

| Individuals | 202,518 | 37.0 | 195,904 | 37.2 | 173,648 | 37.3 | ||

| Consumer | 88,029 | 16.1 | 85,010 | 16.2 | 72,459 | 15.6 | ||

| Credit cards | 45,690 | 8.3 | 43,713 | 8.3 | 40,371 | 8.7 | ||

| Other consumer | 42,339 | 7.7 | 41,297 | 7.9 | 32,088 | 6.9 | ||

| Mortgages | 114,489 | 20.9 | 110,894 | 21.1 | 101,189 | 21.7 | ||

| Total performing loans | 529,497 | 96.7 | 507,685 | 96.5 | 448,086 | 96.3 | ||

| Non-performing loans | ||||||||

| Commercial | 8,596 | 1.6 | 9,182 | 1.7 | 8,891 | 1.9 | ||

| Individuals | 9,652 | 1.8 | 9,170 | 1.7 | 8,564 | 1.8 | ||

| Consumer | 3,664 | 0.7 | 3,263 | 0.6 | 3,165 | 0.7 | ||

| Credit cards | 2,084 | 0.4 | 1,802 | 0.3 | 1,733 | 0.4 | ||

| Other consumer | 1,580 | 0.3 | 1,461 | 0.3 | 1,432 | 0.3 | ||

| Mortgages | 5,988 | 1.1 | 5,907 | 1.1 | 5,399 | 1.2 | ||

| Total non-performing loans | 18,248 | 3.3 | 18,352 | 3.5 | 17,455 | 3.7 | ||

| Total loan portfolio | ||||||||

| Commercial | 335,575 | 61.3 | 320,963 | 61.0 | 283,329 | 60.9 | ||

| Individuals | 212,170 | 38.7 | 205,074 | 39.0 | 182,212 | 39.1 | ||

| Consumer | 91,693 | 16.7 | 88,273 | 16.8 | 75,624 | 16.2 | ||

| Credit cards | 47,775 | 8.7 | 45,515 | 8.7 | 42,104 | 9.0 | ||

| Other consumer | 43,918 | 8.0 | 42,758 | 8.1 | 33,520 | 7.2 | ||

| Mortgages | 120,477 | 22.0 | 116,801 | 22.2 | 106,588 | 22.9 | ||

| Total loan portfolio | 547,745 | 100.0 | 526,037 | 100.0 | 465,541 | 100.0 |

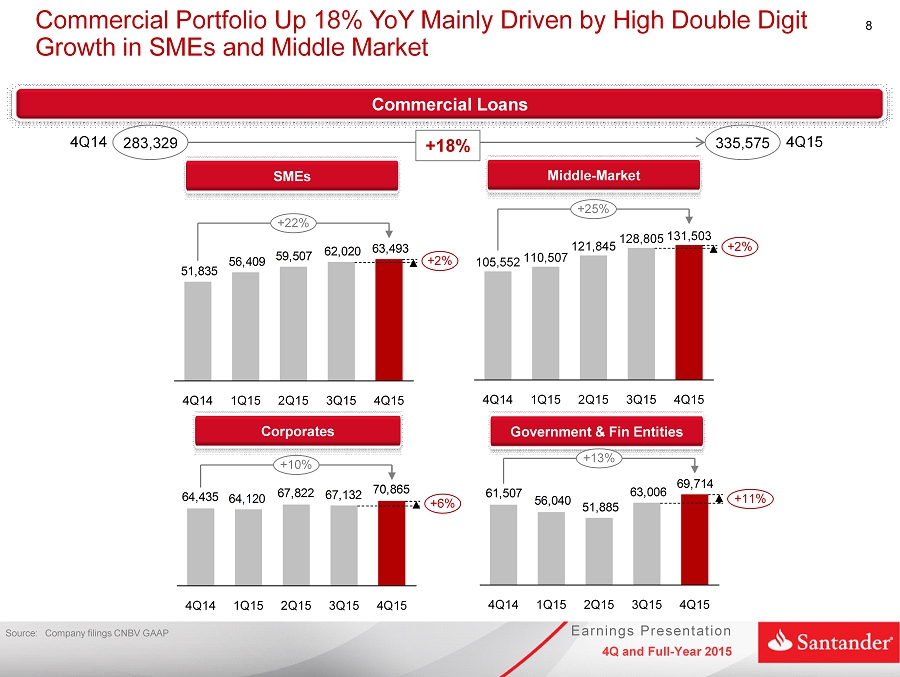

The Commercial loan portfolio is comprised of loans to business and commercial entities, as well as loans togovernment entities and financial institutions, and represented 61.3% of the total loan portfolio. Excluding loans to government entities, the commercial loan portfolio accounted for 50.3% of the total loan portfolio. As of 4Q15, commercial loans increased 18.4% YoY, principally reflecting increases of 24.6%, 22.5% and 10.0% in the middle market, SMEs and corporate segments, respectively. Loans to government and financial entities increased 13.3% YoY, reflecting loans to the federal government, and a couple of states and financial entities, but mostly composed by loans to the two state-owned energy companies in Mexico.

On a sequential basis, the commercial loan portfolio increased 4.6%, principally reflecting strong growth in both government and financial entities, and corporates, which grew 10.6% and 5.6%, respectively. Meanwhile, SMEs and middle-markets were up 2.4% and 2.1%, respectively, maintaining a solid performance and a continued positive trend.

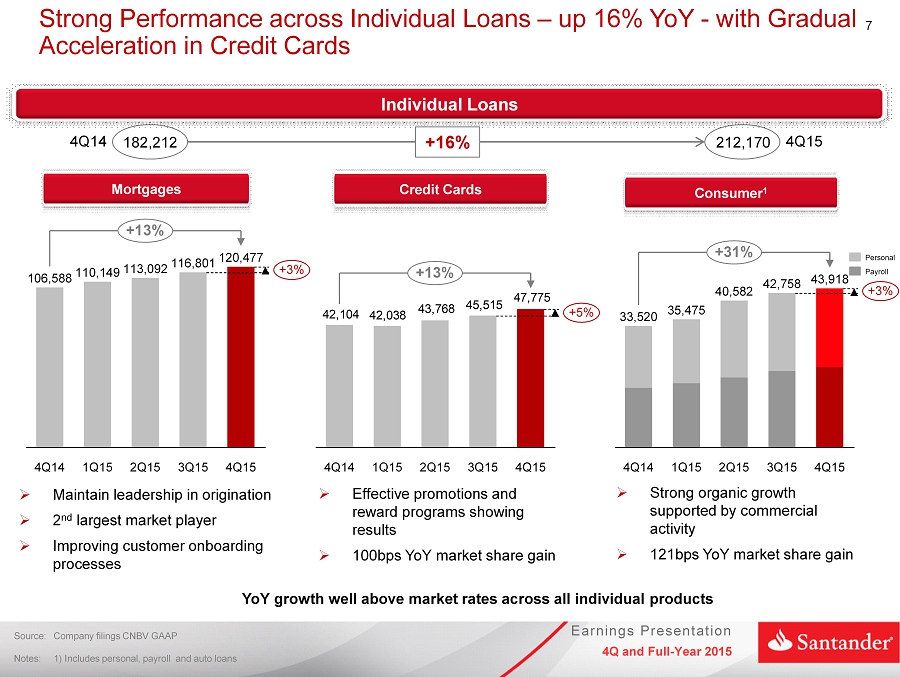

The Individual loan portfoliocomprised of mortgages, consumer and credit card loans, represented 38.7% of the total loan portfolio and increased 16.4% YoY. Credit cards, consumer and mortgage loans represented 8.7%, 8.0%, and 22.0% of the total loan portfolio, respectively, and increased YoY by 13.5%, 31.0%, and 13.0%, respectively.

On a sequential basis, consumer loans and credit cards increased 2.7% and 5.0%, respectively, reflecting a sustained pick-up in personal and payroll loans, while credit card growth continued to accelerate and gradually recover. Santander México has maintained above-market growth rates, principally reflecting its focus on innovation and strong commercial activity. We continue to penetrate the open market focusing on medium- and high-income individuals.

20

Asset quality

| Asset quality | ||||||

| Millions of pesos | ||||||

| % Variation | ||||||

| 4Q15 | 3Q15 | 4Q14 | QoQ | YoY | ||

| Total loans | 547,745 | 526,037 | 465,541 | 4.13 | 17.66 | |

| Performing loans | 529,497 | 507,685 | 448,086 | 4.30 | 18.17 | |

| Non-performing loans | 18,248 | 18,352 | 17,455 | (0.57) | 4.54 | |

| Allowance for loan losses | (19,743) | (19,415) | (16,951) | 1.69 | 16.47 | |

| Charge-offs & Debit Relieves | (4,126) | (3,734) | (3,100) | 10.5 | 33.1 | |

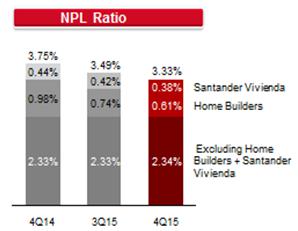

| Non-performing loan ratio | 3.33% | 3.49% | 3.75% | (16bps) | (42bps) | |

| Coverage ratio | 108.2% | 105.8% | 97.1% | 240bps | 1110bps | |

| Cost of Risk* | 3.40% | 3.45% | 3.32% | (5bps) | 8bps | |

*Cost of risk is calculated using annualized cumulative provisions for loan losses for the period

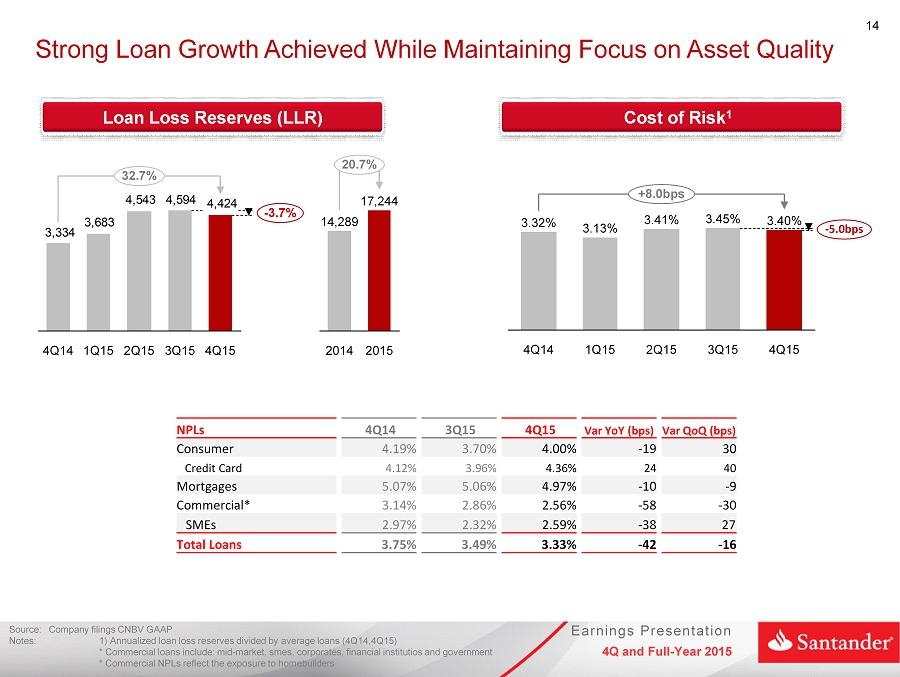

Non-performing loans at the end of 4Q15 increased YoY by Ps.793 million, or 4.5%, to Ps.18,248 million, and decreased 0.6%, or Ps.104 million QoQ.

On a YoY basis, increases of Ps.589 million, or 10.9%, in mortgages and Ps.499 million, or 15.6% in consumer loans (including credit cards) were partly offset by a decrease of Ps.295 million, or 3.3%, in commercial loans. The YoY 10.9% increase in non-performing mortgage loans, mainly resulted from an internal change in the charge-off policy which was extended from 12 months to 36 months for those mortgages originated at the bank, which represent 84% of total mortgages. The charge-of policy for the remaining mortgages which were originated at Santander Hipotecario and Santander Vivienda was reduced from 48 months to 36 months, thus unifying the overall charge-off criteria in this segment.

On a sequential basis, Santander México reported increases of Ps.81 million, or 1.4%, in mortgages and Ps.401 million, or 12.3% in consumer loans (including credit cards). The increase in non-performing credit card loans mainly reflects lower charge-offs in the quarter. The increases in non-performing mortgage and credit card loans were more than offset by a decrease of Ps.586 million, or 6.4%, in commercial loans, which mainly resulted from further progress by the homebuilders.

The breakdown of the non-performing loan portfolio is as follows: commercial loans 47.1%, mortgage loans 32.8% and consumer loans (including credit cards) 20.1%.

| Non-Performing Loan Ratios | |||||

| % | 4Q15 | 3Q15 | 4Q14 | ||

| Commercial | 2.56 | 2.86 | 3.14 | ||

| Individuals | |||||

| Consumer | 4.00 | 3.70 | 4.00 | ||

| Credit Card | 4.36 | 3.96 | 4.12 | ||

| Other consumer | 4.07 | 3.35 | 2.43 | ||

| Mortgages | 4.97 | 5.06 | 5.07 | ||

| Total | 3.33 | 3.49 | 3.75 |

The above mentioned variations to non-performing loans led to an improvement in the NPL ratio, down to 3.33% in 4Q15, decreasing by 42 basis points from 3.75% in 4Q14 and 16 basis points lower than the 3.49% reported in 3Q15.

The NPL ratio for 4Q15 continues to reflect Santander México’s exposure to homebuilders, with non-performing loans of Ps.3,479 million, as well as the impact of Santander Vivienda’s non-performing portfolio, which as of 4Q15 amounted to Ps.2,289 million.

21

Our total exposure to homebuilders as of 4Q15 decreased further QoQ by Ps.560 million to Ps.4,233 million, while non-performing loans declined by the same amount to Ps.3,479 million; driven by additional progress in the situation with the homebuilders, resulting in a write-off of the unsecured exposure in connection with one of the homebuilders´ after receiving shares in payment.

Excluding the impact of the homebuilders and Santander Vivienda’s portfolio, the NPL ratio for 4Q15 would have been 2.34%. The current NPL ratio continues to reflect loan portfolio growth combined with Santander México’s stringent credit scoring model and ongoing monitoring of loan portfolio quality.

*Cost of risk is calculated using annualized cumulative provisions for loan losses for the period

During 4Q15, provisions for loan losses amounted to Ps.4,424 million, which represented an increase of Ps.1,090 million, or 32.7%, YoY and a decrease of Ps.170 million, or 3.7%, on a sequential basis.

The 32.7% YoY increase in provisions mainly reflect: i) significant business volume growth across all segments; and ii) provisions in connection with our exposure to certain corporates, respectively; as well as difficult comps from lower provisions in 4Q14 resulting from the reversal of some provisions related to loans that were restructured in 3Q14 and became current in 4Q14.

Cost of risk in 4Q15 stood at 3.40%, which compares to 3.32% and 3.45% reported in 4Q14 and 3Q15, respectively.

22

The coverage ratio for the quarter was 108.2%, increasing from 97.1% in 4Q14 and 105.8% in 3Q15. The improvement in the coverage ratio was mainly due to lower non-performing loans in the commercial segment reflecting improvements in negotiations with homebuilders.

TOTAL DEPOSITS

Total deposits at the end of 4Q15 amounted to Ps.516,432 million, representing increases of 12.4% YoY and 4.8% sequentially. Demand deposits reached Ps.347,786 million, increasing 18.3% YoY and 6.7% sequentially, partly reflecting system seasonality. Term deposits, in turn, reached Ps.168,646 million, showing an increase of 1.9% YoY and 1.1% QoQ.

Santander México continues to implement its strategy of further enhancing customer service to meet the needs of each segment. Campaigns targeting the SMEs and middle-market segments, together with products offered to middle- and high-income clients have resulted in increases of 17.5%, 19.9% and 12.9% in demand deposits from individuals, SMEs and middle-market, respectively. This performance in deposits has led to an improved mix which supports a stable cost of deposits and contributes to funding.

LIQUIDITY COVERAGE RATIO

Pursuant Banxico’s and CNBV regulatory requirements, the average Liquidity Coverage Ratio (LCR or CCL by its Spanish acronym) for 4Q15 was 107.45%, which compares to 106.60% in 3Q15. (Please refer to note 25 of this report).

23

CAPITALIZATION AND ROAE

| Capitalization | ||||||

| Millions of pesos | 4Q15 | 3Q15 | 4Q14 | |||

| Fundamental | 80,328 | 81,344 | 76,697 | |||

| Non-fundamental | 23,311 | 22,456 | 19,820 | |||

| Total Capital | 103,639 | 103,800 | 96,517 | |||

| Risk-weighted assets | ||||||

| Credit risk | 487,440 | 447,044 | 406,832 | |||

| Credit, market and operational risk | 664,122 | 672,566 | 596,952 | |||

| Credit risk ratios: | ||||||

| Fundamental (%) | 16.5 | 18.2 | 18.8 | |||

| Non-fundamental (%) | 4.8 | 5.0 | 4.9 | |||

| Capitalization ratio (%) | 21.3 | 23.2 | 23.7 | |||

| Total capital ratios: | ||||||

| Fundamental (%) | 12.1 | 12.1 | 12.9 | |||

| Non-fundamental (%) | 3.5 | 3.3 | 3.3 | |||

| Capitalization ratio (%) | 15.6 | 15.4 | 16.2 |

Banco Santander México’s preliminary capital ratio at period end 4Q15 was 15.6%, compared to 16.2% and 15.4% at 4Q14 and 3Q15, respectively. The 15.6% capital ratio was comprised of 12.1% fundamental (CET1) and 3.5% non-fundamental (Tier 2).

As of November 2015, Banco Santander México is classified within Category 1 in accordance with Article 134bis of the Mexican Banking Law, and remains in this category as per the preliminary results dated December 2015, which is the most recent available analysis.

ROAE in 4Q15 was 12.9%, which compares with 14.0% in 4Q14 and improved from 12.1% in 3Q15.

24

RELEVANT EVENTS & REPRESENTATIVE ACTIVITIES AND TRANSACTIONS

Relevant Events

Banco Santander México published Pilar III pursuant CNBV requirements

On January 29, 2016 Banco Santander México published its Pilar III report on risk and capital issues, pursuant to CNBV requirements.

Please refer to the following link to access the complete document:

http://www.santander.com.mx/ir/english/financial/annual.html

Banco Santander México completed an equity swap derivative financial instrument with underlying shares of OMA

On January 8, 2016 Banco Santander México announced that upon request of a holding company of Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. (OMA), it completed an equity swap derivative financial instrument with underlying shares of OMA prior to its termination date, thereby eliminating its shareholding in the company.

Banco Santander México issued debt in the local market

On December 10, 2015 Banco Santander México issued a three-year, Ps.3,000 million bond at a variable rate of TIIE + 18 basis points.

Santander México’s changes in its Board of Directors and CEO positions became effective

On January 1st, 2016, the appointment of Ing. Marcos Martínez Gavica as Chairman of the Board of Directors, became effective.

On December 1st, 2015, the appointment of Lic. Héctor B. Grisi Checa as Executive President and CEO of the Group became effective.

General Ordinary and Extraordinary Shareholders’ Meeting

On November 25, 2015, Santander México held its General Ordinary and Extraordinary Shareholders’ Meeting and approved among other items:

| · | To decree payment of a cash dividend to the Company’s Shareholders for the amount of Ps.3,226 million, which was paid on December 22, 2015. |

| · | To amend the Chapter X of the Corporate By-Laws in order to incorporate the measures to avoid Conflict of Interests, as provided by the General Rules of Financial Groups published in the Official Journal of the Federation on December 31, 2014, such resolution is subjected to a suspensive condition that the Corporation attains the corresponding approval by the Ministry of Finance and Public Credit, as well as others required and necessary. |

| · | The resignation of Messrs. Carlos Gómez y Gómez, José Doncel Razola and Carlos Fernández González from the position of Non-Independent Director of Series “F” shares |

| · | The appointment of Messrs. Héctor B. Grisi Checa and Ángel Rivera Congosto as Non Independent Directors of Series “F” shares. |

| · | That the changes to the members of the Board of Directors would become effective on January 1st, 2016. |

| · | Finally, the approval of the composition of the Board of Directors as indicated below: |

25

| Series “F” Non Independent Directors | |

| D. Marcos Alejandro Martínez Gavica | Chairman |

| D. Héctor B. Grisi Checa | Director |

| D. Rodrigo Echenique Gordillo | Director |

| D. Ángel Rivera Congosto | Director |

| D. Rodrigo Brand de Lara | Director |

| D. Vittorio Corbo Lioi | Alternate Director |

| D. Francisco Javier Hidalgo Blazquez | Alternate Director |

| D. Pedro José Moreno Cantalejo | Alternate Director |

| D. Fernando Borja Mujica | Alternate Director |

| Series “F” Independent Directors | |

| D. Guillermo Güemez García | Director |

| D. Joaquín Vargas Guajardo | Director |

| D. Juan Gallardo Thurlow | Director |

| D. Eduardo Carredano Fernández | Alternate Director |

| D. Jesús Federico Reyes Heroles González Garza | Alternate Director |

| Series “B” Independent Directors | |

| D. Fernando Solana Morales | Director |

| D. Fernando Ruíz Sahagún | Director |

| D. Alberto Torrado Martínez | Director |

| D. Gina Lorenza Diez Barroso Azcárraga | Director |

| D. Enrique Krauze Kleinbort | Alternate Director |

| D. Antonio Purón Mier y Terán | Alternate Director |

Santander México selected PricewaterhouseCoopers, S.C. (“PWC”) as external auditors

Santander México selected PWC as external auditors, to audit its financial statements starting in 2016. Such resolution has been adopted in accordance with corporate governance recommendations related to the rotation of the external auditor, following a proposal by the audit committee and the results of a fully transparent selection process.

Representative Transactions

Santander México acted as joint placement agent of Banco Santander México’s debt issuance

Santander México acted as joint placement agent of a three-year, Ps.3,000 million bond at a variable rate of TIIE + 18 basis points.

Santander México acted as joint placement agent of CFE’s debt issuance

Santander México acted as joint placement agent in a combined three-part issuance which totaled Ps.8,000 million, which was broken down as follows: Ps.2,500 million at fix rate, Ps.500 million at variable rate and Ps.5,000 million at an UDI denominated rate.

Santander México participated in a Club Deal with Consorcio Ara

Santander México participated along with 3 other Banks in a 5-year Club Deal with Consorcio Ara for Ps.1,850 million.

Santander México acted as structuring agent and bookrunner of a financing facility for Elementia

Santander México acted as structuring agent and bookrunner of a 5-year, US$500 million financing facility for Elementia.

Santander México acted as manager in a syndicated loan for Minera Frisco

Santander México acted as manager in a 5-year, US$1,100 million syndicated loan for Minera Frisco.

Santander México acted as senior mandated lead arranger for the financing of the new Mexico City’s airport

Santander México acted as senior mandated lead arranger for a U$3,000 million credit facility for the new Mexico City’s airport. Grupo Aeroportuario de la Ciudad de México acted as sponsor.

26

Santander México participated in financing public works (Pidiregas) for CFE

Santander México participated in a 10-year, Ps.5,000 million financing for public works (Pidiregas) for CFE.

AWARDS & RECOGNITIONS

“Best Investment Bank in Mexico” by International Finance Magazine

On November 19, 2015, the prestigious magazineInternational Finance Magazine recognized Banco Santander México as the “Best Investment Bank in Mexico”.

These financial awards recognize organizations that make a difference through the highest standards of innovation and performance.

“Best Infrastructure Bank in Mexico” by LatinFinance

On October 13, 2015, Banco Santander México was awarded for the second consecutive year as "Best Bank in infrastructure in Mexico" by the prestigious magazine LatinFinance, which also recognized the bank's participation in the pipeline“Los Ramones II” with three awards: best project, best funding and best infrastructure financing.

These awards underscore Santander México’s leadership position supporting the energy and infrastructure sectors, where over 14 projects with a total value of Ps.88 billion have been funded over the last year.

SUSTAINABILITY AND SOCIAL RESPONSIBILITY

Santander México recognized “The Most Socially Responsible Bank in Mexico” by International Finance Magazine

On November 19, 2015, the prestigious magazineInternational Finance Magazine recognized Banco Santander México as the “The Most Socially Responsible Bank in Mexico”.

This award recognizes Banco Santander México’s strong track record of social and environmental commitment. Santander México also provides the strongest financial support to higher education and socially disadvantaged children in Mexico.

Santander México will provide financial support to 66 organizations in 2016

During 2016, Santander México will provide financial support to 66 organizations in Mexico which are working on behalf of socially disadvantaged children in various areas such as: health, education and nutrition.

Study by CLARES confirms favorable impact of Santander México’s trust in favor of children in Mexico

The Latin American Center for Social Responsibility (“CLARES” - Centro Latinoamericano de Responsabilidad Social) of the Universidad Anahuac, conducted a study that revealed the favorable impact this trust has had with children in Mexico. After 20 years of work, this initiative has become one Santander México’s most significant socially responsible actions, achieved through the combined effort and commitment of employees, managers, volunteers and strategic partners.

For more information on Santander México – Sustainability and Social Responsibility, please refer to:

https://servicios.santander.com.mx/comprometidos/images/archivos/Reporte2014.pdf

27

CREDIT RATINGS

| Banco Santander México | Moody’s | Fitch Ratings | |

| Global scale | |||

| Foreign currency | |||

| Long term | A3 | BBB+ | |

| Short Term | P-2 | F2 | |

| Local currency | |||

| Long term | A3 | BBB+ | |

| Short Term | P-2 | F2 | |

| National scale | |||

| Long term | Aaa.mx | AAA(mex) | |

| Short Term | Mx-1 | F1+(mex) | |

| Rating viability (VR) | ---- | bbb+ | |

| Support | ---- | 2 | |

| Counterparty risk Assessments (CR) | |||

| Long Term | A2 (cr) | ---- | |

| Short Term | P-1 (cr) | ---- | |

| Standalone BCA | baa1 | ---- | |

| Outlook | Stable | Stable | |

| International Issuances | |||

| Tier 2 Subordinated Capital Notes due 2024 | Baa3 | BB+ | |

| Long-term senior unsecured global notes due 2022 | A3 | BBB+ | |

| Last publication: | Dec-18-2015 | June-25-2015 | |

| Santander Vivienda | Moody´s | Fitch Ratings | |

| National scale | |||

| Long Term | ---- | AAA (mex) | |

| Short Term | ---- | F1+ (mex) | |

| Notes HICOAM 07 | |||

| Global Scale | |||

| Local currency | |||

| Long Term | A3 | ---- | |

| National scale | |||

| Long Term | Aaa.mx | AAA(mex) | |

| Standalone BCA | b1 | ---- | |

| Outlook | Stable | Stable | |

| Last publication: | Nov-11-2015 | June-9-2015 | |

| RMBS Primary Servicer | ---- | AAFC1(mex) | |

| Outlook | ---- | Stable | |

| Last publication: | ---- | Nov-10-2015 | |

28

| Santander Consumo | Moody´s | Fitch Ratings | |

| National Scale | |||

| Long term | ---- | AAA (mex) | |

| Short Term | ---- | F1+ (mex) | |

| Unsecured bonds Issuance Program | |||

| Global Scale | |||

| Local currency | |||

| Short term | P-2 | ---- | |

| National Scale | |||

| Short Term | MX-1 | F1+ (mex) | |

| Standalone Credit Profile (SCP) | ba3 | ---- | |

| Outlook | Stable | Stable | |

| Last publication: | Nov-13-2015 | Dec-18-2015 | |

Brokerage - Casa de Bolsa Santander | Moody´s | Fitch Ratings | |

| Global scale | |||

| Local currency | |||

| Long term | Baa1 | ---- | |

| Short term | P-2 | ---- | |

| National scale | |||

| Local currency | |||

| Long term | Aaa.mx | AAA(mex) | |

| Short term | Mx-1 | F1+(mex) | |

| Standalone BCA | b1 | ---- | |

| Outlook | Stable | Stable | |

| Last publication: | Dec-18-2015 | Sep-01-2015 |

Notes:

| § | BCA = Baseline Credit Assessment |

| § | SR = Support Rating |

| § | VR = Viability Rating |

| § | SCP = Standalone Credit Profile |

| § | CR= Counterparty Risk Assessments |

29

4Q15 EARNINGS CALL DIAL-IN INFORMATION

| Date: | Friday, January 29, 2016 |

| Time: | 8:00 AM (MCT); 9:00 AM (US ET) |

| Dial-in Numbers: | 1-888-215-6982 US & Canada; 1-913-312-0845 International & Mexico |

| Access Code: | 4402274 |

| Webcast: | http://public.viavid.com/index.php?id=117826 |

| Replay: | Friday, January 29, 2016 at 12:00 pm US ET, and Friday, February 5, 2016 at 11:59 pm US ET |

| Dial-in number: | 1-877-870-5176 US & Canada; 1-858-384-5517 International & Mexico Access Code: 4402274 |

ANALYST COVERAGE

Actinver, Bank of America Merrill Lynch, Barclays, Brasil Plural, BTG Pactual, Citi, Credit Suisse, Deutsche Bank, EVA Dimensions, GBM, Goldman Sachs, HSBC, Itaú, JP Morgan, Morgan Stanley, Nau Securities, UBS and Vector.

Santander México is covered by the aforementioned analysts. Please note that any opinions, estimates or forecasts regarding the performance of Santander México issued by these analysts reflect their own views, and therefore do not represent the opinions, estimates or forecasts of Santander México or its management. Although Santander México may refer to or distribute such statements, this does not imply that Santander México agrees with or endorses any information, conclusions or recommendations included therein.

DEFINITION OF RATIOS

ROAE:Annualized net income divided by average equity

EFFICIENCY:Annualized administrative and promotional expenses divided by annualized gross operating income (before administrative and promotional expenses and allowances).

RECURRENCY:Annualized net fees divided by annualized administrative and promotional expenses (net of amortizations and depreciations).

NIM:Financial margin divided by daily average interest earnings assets.

COST OF RISK:Annualized provisions for loan losses divided by average loan portfolio

Note:

·Annualized figures consider (12M15) cumulative results

·Average figures are calculated using 4Q14 and 4Q15

30

ABOUT GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. DE C.V. (NYSE: BSMX; BMV: SANMEX)

Grupo Financiero Santander México, S.A.B. de C.V. (Santander México), one of Mexico’s leading financial services holding companies, provides a wide range of financial and related services, including retail and commercial banking, securities brokerage, financial advisory and other related investment activities. Santander México offers a multichannel financial services platform focused on mid- to high-income individuals and small- to medium-sized enterprises, while also providing integrated financial services to larger multinational companies in Mexico. As of December 31, 2015, Santander México had total assets of Ps.1,185 billion under Mexican Banking GAAP and more than 12 million customers. Headquartered in Mexico City, the Company operates 1,079 branches and 298 offices nationwide and has a total of 17,205 employees.

We, the undersigned under oath to tell the truth declare that, in the area of our corresponding functions, we prepared the information on Grupo Financiero Santander México contained in this quarterly report, which to the best of our knowledge reasonably reflects its situation.

| HÉCTOR B. GRISI CHECA | PEDRO JOSÉ MORENO CANTALEJO | |

| Executive President and Chief Executive Officer | Vice President of Administration and Finance | |

| EMILIO DE EUSEBIO SAIZ | JUAN CARLOS GARCÍA CONTRERAS | JUAN RAMÓN JIMÉNEZ LORENZO |

| Deputy General Director of Intervention and Control Management | Executive Director Controller Finance | Executive Director of Internal Audit |

The financial information presented in this report has been obtained from the non-audited financial statements prepared in accordance with the General Nature Provisions applicable to Holding Corporations of Financial Groups which are subject to the supervision of the National Banking and Securities Commission on accounting procedures, published in the Federal Official Gazette on January 31, 2011. The exchange rate used to convert foreign currency transactions to pesos is Ps.17.2487

INVESTOR RELATIONS CONTACT

Héctor Chávez Lopez – Managing Director - IRO

+ 52 (55) 5269-1925

hchavez@santander.com.mx

Gerardo Freire Alvarado – Executive Director of Investor Relations

+ 52 (55) 5269-1827/+ 52 (55) 5269-1828

gfreire@santander.com.mx

Investor Relations Team

investor@santander.com.mx

www.santander.com.mx

31

LEGAL DISCLAIMER

Grupo Financiero Santander México cautions that this report may contain forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements may be found in various places throughout this report and include, without limitation, statements regarding our intent, belief, targets or current expectations in connection with: asset growth and sources of funding; growth of our fee-based business; expansion of our distribution network; our focus on strategic businesses; our compound annual growth rate; our risk, efficiency and profitability targets; financing plans; competition; impact of regulation; exposure to market risks including interest rate risk, foreign exchange risk and equity price risk; exposure to credit risks including credit default risk and settlement risk; projected capital expenditures; capitalization requirements and level of reserves; liquidity; trends affecting the economy generally; and trends affecting our financial condition and our results of operations. While these forward-looking statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: changes in capital markets in general that may affect policies or attitudes towards lending to Mexico or Mexican companies; changes in economic conditions, in Mexico in particular, in the United States or globally; the monetary, foreign exchange and interest rate policies of the Mexican Central Bank (Banco de Mexico); inflation; deflation; unemployment; unanticipated turbulence in interest rates; movements in foreign exchange rates; movements in equity prices or other rates or prices; changes in Mexican and foreign policies, legislation and regulations; changes in requirements to make contributions to, for the receipt of support from programs organized by or requiring deposits to be made or assessments observed or imposed by, the Mexican government; changes in taxes; competition, changes in competition and pricing environments; our inability to hedge certain risks economically; economic conditions that affect consumer spending and the ability of customers to comply with obligations; the adequacy of allowances for loans and other losses; increased default by borrowers; technological changes; changes in consumer spending and saving habits; increased costs; unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; changes in, or failure to comply with, banking regulations; and certain other factors indicated in our annual report20F. The risk factors and other key factors that we have indicated in our past and future filings and reports, including those with the U.S. Securities and Exchange Commission, could adversely affect our business and financial performance.

Note: The information contained in this report is not audited. Nevertheless, the consolidated accounts are prepared on the basis of the accounting principles and regulations prescribed by the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) for credit institutions, as amended (Mexican Banking GAAP). All figures presented are in nominal terms. Historical figures are not adjusted for inflation.

32

Grupo Financiero Santander México

| § | Consolidated Balance Sheet |

| § | Consolidated Statement of Income |

| § | Consolidated Statement of Changes in Stockholders’ Equity |

| § | Consolidated Statement of Cash Flows |

The information contained in this report and the financial statements of the Group’s subsidiaries may be consulted on the Internet website: www.santander.com.mx or through the following direct access:

http://www.santander.com.mx/ir/english/financial/quarterly.html

There is also information on Santander México on the CNBV website: www.cnbv.gob.mx

33

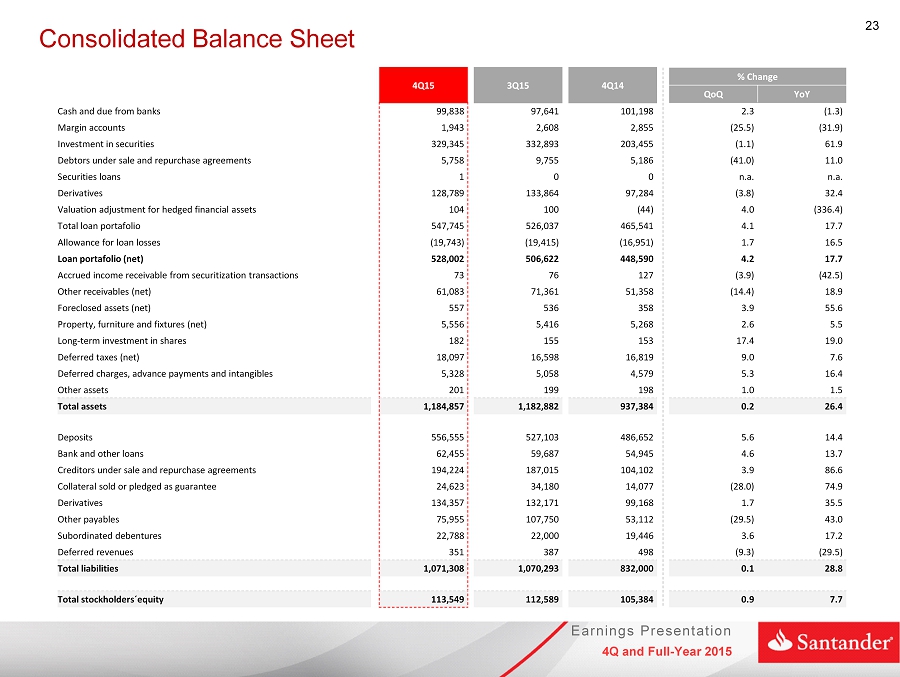

| Consolidated balance sheet | ||||||||||

| Millions of pesos | ||||||||||

| 2015 | 2014 | |||||||||

| Dec | Sep | Jun | Mar | Dec | Sep | Jun | Mar | |||

| Assets | ||||||||||

| Funds Available | 99,838 | 97,641 | 102,323 | 105,370 | 101,198 | 97,474 | 91,384 | 94,408 | ||

| Margin accounts | 1,943 | 2,608 | 3,181 | 2,844 | 2,855 | 3,203 | 3,392 | 2,894 | ||

| Investment in securities | 329,345 | 332,893 | 269,782 | 271,576 | 203,455 | 231,705 | 219,044 | 218,047 | ||

| Trading securities | 210,158 | 233,074 | 194,057 | 198,638 | 114,936 | 156,247 | 143,491 | 149,772 | ||

| Securities available for sale | 113,549 | 94,227 | 70,178 | 67,436 | 83,057 | 70,038 | 70,175 | 62,944 | ||

| Securities held to maturity | 5,638 | 5,592 | 5,547 | 5,502 | 5,462 | 5,420 | 5,378 | 5,331 | ||

| Debtors under sale and repurchase agreements | 5,758 | 9,755 | 19,303 | 7,331 | 5,186 | 10,689 | 10,471 | 8,413 | ||

| Securities Lending | 1 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | ||

| Derivatives | 128,789 | 133,864 | 99,783 | 100,357 | 97,284 | 73,888 | 88,209 | 73,878 | ||

| Trading purposes | 116,668 | 116,898 | 90,763 | 89,721 | 92,544 | 72,891 | 87,566 | 73,422 | ||

| Hedging purposes | 12,121 | 16,966 | 9,020 | 10,636 | 4,740 | 997 | 643 | 456 | ||

| Valuation adjustment for hedged financial assets | 104 | 100 | 106 | 49 | (44) | (65) | 85 | 29 | ||

| Performing loan portfolio | ||||||||||

| Commercial loans | 326,979 | 311,781 | 291,182 | 277,921 | 274,438 | 256,496 | 261,976 | 236,610 | ||

| Commercial or business activity | 257,268 | 248,778 | 239,301 | 221,884 | 212,933 | 204,255 | 205,210 | 189,995 | ||

| Financial entities loans | 9,841 | 5,883 | 5,745 | 5,444 | 5,580 | 5,226 | 5,901 | 3,859 | ||

| Government entities loans | 59,870 | 57,120 | 46,136 | 50,593 | 55,925 | 47,015 | 50,865 | 42,756 | ||

| Consumer loans | 88,029 | 85,010 | 81,139 | 74,714 | 72,459 | 70,917 | 69,372 | 67,069 | ||

| Mortgage loans | 114,489 | 110,894 | 107,371 | 104,645 | 101,189 | 97,698 | 94,655 | 91,739 | ||

| Total performing loan portfolio | 529,497 | 507,685 | 479,692 | 457,280 | 448,086 | 425,111 | 426,003 | 395,418 | ||

| Non-performing loan portfolio | ||||||||||

| Commercial loans | 8,596 | 9,182 | 9,876 | 9,155 | 8,891 | 8,709 | 7,152 | 6,910 | ||

| Commercial or business activity | 8,593 | 9,179 | 9,872 | 9,152 | 8,889 | 8,709 | 7,152 | 6,909 | ||

| Financial entities loans | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | ||

| Government entities loans | 3 | 3 | 4 | 3 | 2 | 0 | 0 | 0 | ||

| Consumer loans | 3,664 | 3,263 | 3,211 | 2,799 | 3,165 | 2,755 | 2,933 | 2,895 | ||

| Mortgage loans | 5,988 | 5,907 | 5,721 | 5,504 | 5,399 | 4,900 | 4,587 | 4,126 | ||

| Total non-performing portfolio | 18,248 | 18,352 | 18,808 | 17,458 | 17,455 | 16,364 | 14,672 | 13,931 | ||

| Total loan portfolio | 547,745 | 526,037 | 498,500 | 474,738 | 465,541 | 441,475 | 440,675 | 409,349 | ||

| Allowance for loan losses | (19,743) | (19,415) | (18,643) | (17,382) | (16,951) | (16,631) | (16,397) | (16,081) | ||