UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-22714

Eaton Vance Series Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

One Post Office Square, Boston, Massachusetts 02109

(Address of Principal Executive Offices)

Deidre E. Walsh

One Post Office Square, Boston, Massachusetts 02109

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

July 31

Date of Fiscal Year End

July 31, 2024

Date of Reporting Period

Item 1. Reports to Stockholders

(a)

Eaton Vance Emerging Markets Debt Opportunities Fund

Annual Shareholder Report July 31, 2024

This annual shareholder report contains important information about the Eaton Vance Emerging Markets Debt Opportunities Fund for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at www.eatonvance.com/open-end-mutual-fund-documents.php. You can also request this information by contacting us at 1-800-262-1122.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Class A | $122 | 1.15% |

How did the Fund perform last year and what affected its performance?

Key contributors to (↑) and detractors from (↓) performance, relative to the J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index (the Index):

↑ An overweight position in Surinamese government bonds -- boosted by debt restructuring in late 2023 -- helped Index-relative returns during the period

↑ An out-of-Index allocation to Egyptian local-currency bonds aided returns as actions by Egypt’s central bank led to support by the IMF and other groups

↑ An overweight exposure to Brazilian corporate bonds -- including sugar and ethanol producer Usina Coruripe, and mining firm Samarco -- helped returns

↑ The use of derivatives -- including foreign exchange forwards to manage currency exposures and interest-rate swaps to manage interest-rate exposures -- helped Index-relative performance

↓ The Fund’s lack of exposure to U.S. interest rates hurt performance as short-term interest-rate declines led to multiple bond rallies during the period

↓ An underweight exposure to the South African rand, which rallied after the ANC Party lost its majority in a national election, detracted from returns

↓ An out-of-Index exposure to the South Korean won hurt returns as the currency weakened amid rising concerns over political and economic risks

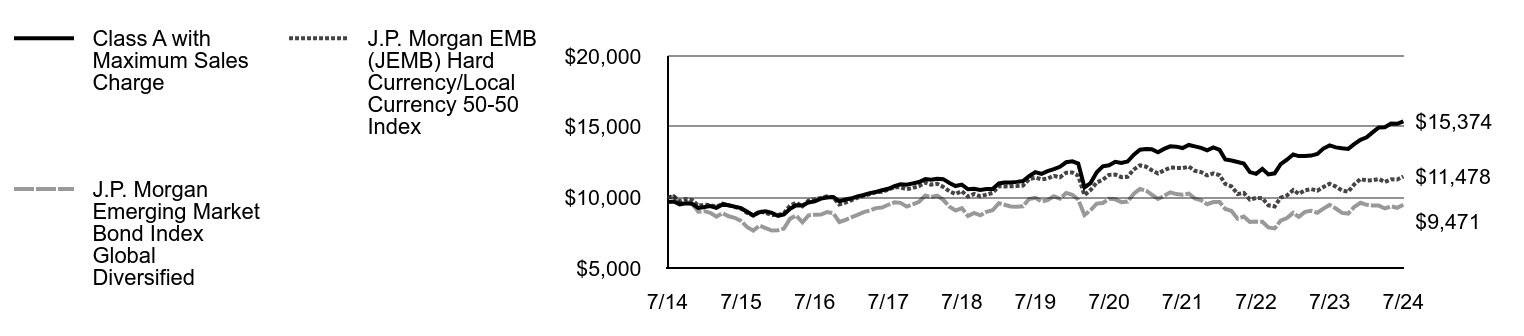

Comparison of the change in value of a $10,000 investment for the period indicated.

| Class A with Maximum Sales Charge | J.P. Morgan Emerging Market Bond Index Global Diversified | J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index |

|---|

| 7/14 | $9,675 | $10,000 | $10,000 |

| 8/14 | $9,704 | $10,048 | $10,065 |

| 9/14 | $9,499 | $9,535 | $9,741 |

| 10/14 | $9,577 | $9,684 | $9,881 |

| 11/14 | $9,538 | $9,557 | $9,814 |

| 12/14 | $9,255 | $8,990 | $9,419 |

| 1/15 | $9,316 | $9,021 | $9,473 |

| 2/15 | $9,387 | $8,899 | $9,456 |

| 3/15 | $9,255 | $8,634 | $9,333 |

| 4/15 | $9,499 | $8,886 | $9,547 |

| 5/15 | $9,438 | $8,657 | $9,427 |

| 6/15 | $9,346 | $8,552 | $9,312 |

| 7/15 | $9,234 | $8,332 | $9,203 |

| 8/15 | $8,979 | $7,884 | $8,899 |

| 9/15 | $8,725 | $7,650 | $8,711 |

| 10/15 | $8,949 | $7,996 | $9,017 |

| 11/15 | $9,010 | $7,823 | $8,906 |

| 12/15 | $8,907 | $7,649 | $8,749 |

| 1/16 | $8,690 | $7,676 | $8,752 |

| 2/16 | $8,793 | $7,787 | $8,880 |

| 3/16 | $9,196 | $8,492 | $9,425 |

| 4/16 | $9,434 | $8,710 | $9,629 |

| 5/16 | $9,423 | $8,237 | $9,368 |

| 6/16 | $9,640 | $8,722 | $9,764 |

| 7/16 | $9,713 | $8,774 | $9,876 |

| 8/16 | $9,909 | $8,778 | $9,955 |

| 9/16 | $9,992 | $8,955 | $10,070 |

| 10/16 | $10,018 | $8,879 | $9,996 |

| 11/16 | $9,723 | $8,255 | $9,490 |

| 12/16 | $9,847 | $8,410 | $9,629 |

| 1/17 | $9,929 | $8,599 | $9,802 |

| 2/17 | $10,065 | $8,754 | $9,973 |

| 3/17 | $10,169 | $8,956 | $10,106 |

| 4/17 | $10,296 | $9,061 | $10,231 |

| 5/17 | $10,380 | $9,239 | $10,370 |

| 6/17 | $10,497 | $9,281 | $10,396 |

| 7/17 | $10,604 | $9,473 | $10,546 |

| 8/17 | $10,790 | $9,643 | $10,712 |

| 9/17 | $10,921 | $9,610 | $10,704 |

| 10/17 | $10,893 | $9,340 | $10,572 |

| 11/17 | $10,991 | $9,497 | $10,663 |

| 12/17 | $11,085 | $9,689 | $10,799 |

| 1/18 | $11,289 | $10,123 | $11,041 |

| 2/18 | $11,249 | $10,017 | $10,901 |

| 3/18 | $11,315 | $10,119 | $10,960 |

| 4/18 | $11,286 | $9,820 | $10,740 |

| 5/18 | $11,020 | $9,331 | $10,428 |

| 6/18 | $10,800 | $9,065 | $10,237 |

| 7/18 | $10,903 | $9,237 | $10,437 |

| 8/18 | $10,572 | $8,674 | $10,046 |

| 9/18 | $10,603 | $8,899 | $10,238 |

| 10/18 | $10,525 | $8,725 | $10,067 |

| 11/18 | $10,594 | $8,970 | $10,194 |

| 12/18 | $10,592 | $9,087 | $10,313 |

| 1/19 | $10,980 | $9,583 | $10,778 |

| 2/19 | $11,055 | $9,478 | $10,775 |

| 3/19 | $11,055 | $9,353 | $10,777 |

| 4/19 | $11,093 | $9,336 | $10,795 |

| 5/19 | $11,157 | $9,364 | $10,835 |

| 6/19 | $11,493 | $9,880 | $11,285 |

| 7/19 | $11,779 | $9,971 | $11,397 |

| 8/19 | $11,663 | $9,708 | $11,271 |

| 9/19 | $11,848 | $9,801 | $11,330 |

| 10/19 | $11,995 | $10,085 | $11,526 |

| 11/19 | $12,157 | $9,902 | $11,419 |

| 12/19 | $12,481 | $10,311 | $11,740 |

| 1/20 | $12,550 | $10,179 | $11,755 |

| 2/20 | $12,388 | $9,832 | $11,525 |

| 3/20 | $10,707 | $8,743 | $10,156 |

| 4/20 | $11,013 | $9,086 | $10,516 |

| 5/20 | $11,770 | $9,556 | $11,051 |

| 6/20 | $12,196 | $9,601 | $11,250 |

| 7/20 | $12,272 | $9,891 | $11,590 |

| 8/20 | $12,519 | $9,858 | $11,612 |

| 9/20 | $12,440 | $9,660 | $11,427 |

| 10/20 | $12,532 | $9,701 | $11,458 |

| 11/20 | $13,000 | $10,233 | $11,959 |

| 12/20 | $13,370 | $10,589 | $12,267 |

| 1/21 | $13,419 | $10,476 | $12,166 |

| 2/21 | $13,410 | $10,195 | $11,923 |

| 3/21 | $13,195 | $9,882 | $11,692 |

| 4/21 | $13,425 | $10,105 | $11,906 |

| 5/21 | $13,611 | $10,357 | $12,106 |

| 6/21 | $13,587 | $10,232 | $12,080 |

| 7/21 | $13,487 | $10,188 | $12,073 |

| 8/21 | $13,707 | $10,266 | $12,170 |

| 9/21 | $13,606 | $9,914 | $11,878 |

| 10/21 | $13,505 | $9,782 | $11,786 |

| 11/21 | $13,325 | $9,515 | $11,555 |

| 12/21 | $13,535 | $9,663 | $11,697 |

| 1/22 | $13,353 | $9,662 | $11,564 |

| 2/22 | $12,679 | $9,179 | $10,946 |

| 3/22 | $12,606 | $9,039 | $10,768 |

| 4/22 | $12,501 | $8,494 | $10,237 |

| 5/22 | $12,395 | $8,644 | $10,313 |

| 6/22 | $11,784 | $8,259 | $9,844 |

| 7/22 | $11,661 | $8,283 | $9,956 |

| 8/22 | $12,016 | $8,271 | $9,930 |

| 9/22 | $11,624 | $7,869 | $9,435 |

| 10/22 | $11,699 | $7,799 | $9,349 |

| 11/22 | $12,350 | $8,353 | $9,982 |

| 12/22 | $12,664 | $8,534 | $10,136 |

| 1/23 | $13,032 | $8,900 | $10,511 |

| 2/23 | $12,919 | $8,618 | $10,245 |

| 3/23 | $12,927 | $8,974 | $10,502 |

| 4/23 | $12,952 | $9,051 | $10,584 |

| 5/23 | $13,066 | $8,908 | $10,470 |

| 6/23 | $13,449 | $9,199 | $10,727 |

| 7/23 | $13,672 | $9,463 | $10,959 |

| 8/23 | $13,536 | $9,209 | $10,759 |

| 9/23 | $13,471 | $8,899 | $10,487 |

| 10/23 | $13,425 | $8,852 | $10,392 |

| 11/23 | $13,766 | $9,319 | $10,907 |

| 12/23 | $14,072 | $9,618 | $11,295 |

| 1/24 | $14,249 | $9,471 | $11,196 |

| 2/24 | $14,597 | $9,417 | $11,212 |

| 3/24 | $14,948 | $9,414 | $11,297 |

| 4/24 | $14,957 | $9,213 | $11,092 |

| 5/24 | $15,216 | $9,362 | $11,272 |

| 6/24 | $15,205 | $9,261 | $11,255 |

| 7/24 | $15,374 | $9,471 | $11,478 |

Average Annual Total Returns (%)Footnote Reference*

| 1 Year | 5 Years | 10 Years |

|---|

| Class A | 12.42% | 5.46% | 4.73% |

| Class A with 3.25% Maximum Sales Charge | 8.83% | 4.78% | 4.39% |

J.P. Morgan Emerging Market Bond Index Global Diversified Footnote Reference†Footnote Referencea | 0.08% | (1.02%) | (0.54%) |

J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 IndexFootnote Referencea | 4.73% | 0.14% | 1.39% |

| Footnote | Description |

Footnote† | In accordance with regulatory changes requiring the Fund’s primary benchmark to represent the overall applicable market, the Fund’s primary prospectus benchmark changed to the indicated benchmark effective May 1, 2024. |

Footnotea | Index is used with permission. Copyright 2021, J.P. Morgan Chase & Co. All rights reserved. See Fund prospectus for full description. |

Footnote* | Class A performance prior to 9/3/15 is linked to Class R6. This linked performance is adjusted for any applicable sales charge, but is not adjusted for class expense differences. If adjusted for such differences, the performance would be different. Performance presented in the Financial Highlights included in the financial statements is not linked. |

Performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance assumes that all dividends and distributions, if any, were reinvested. For more recent performance information, visit www.eatonvance.com/performance.php.

THE FUND'S PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

| Total Net Assets | $2,357,927,839 |

| # of Portfolio Holdings (including derivatives) | 699 |

| Portfolio Turnover Rate | 173% |

| Total Advisory Fees Paid | $11,163,451 |

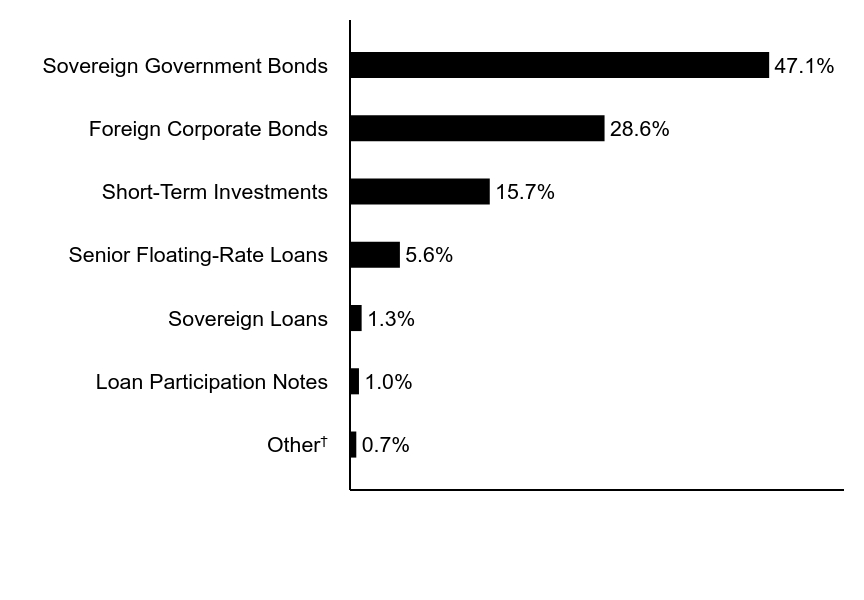

What did the Fund invest in?

The following tables reflect what the Fund invested in as of the report date.

Asset Allocation (% of total investments)

| Value | Value |

|---|

OtherFootnote Reference† | 0.7% |

| Loan Participation Notes | 1.0% |

| Sovereign Loans | 1.3% |

| Senior Floating-Rate Loans | 5.6% |

| Short-Term Investments | 15.7% |

| Foreign Corporate Bonds | 28.6% |

| Sovereign Government Bonds | 47.1% |

| Footnote | Description |

Footnote† | Investment types less than 1% each |

Foreign Currency Exposure (% of net assets)Footnote Reference*

| Egypt | 9.7% |

| Uzbekistan | 9.3% |

| Dominican Republic | 4.4% |

| Nigeria | 3.6% |

| Serbia | 3.2% |

| Turkey | 2.7% |

| Taiwan | 1.9% |

| Kazakhstan | 1.9% |

| Malaysia | 1.6% |

| Other | 9.3% |

| Total Long Exposure | 47.7% |

| Euro | (3.0%) |

| Total Short Exposure | (3.0%) |

| Footnote | Description |

Footnote* | Currency exposures include all foreign exchange denominated assets and currency derivatives. |

If you wish to view additional information about the Fund, including the prospectus, statement of additional information, financial statements and holdings, please scan the QR code or visit www.eatonvance.com/open-end-mutual-fund-documents.php. For proxy information, please visit www.eatonvance.com/proxyvoting.

The Funds may deliver a single copy of certain required shareholder documents (including prospectuses, shareholder reports, and proxy materials) to investors with the same last name and the same address. Your participation will continue indefinitely unless you instruct otherwise by calling 1-800-262-1122 or by contacting your financial intermediary. Your instruction will typically be effective within 30 days of receipt.

Not FDIC Insured | May Lose Value | No Bank Guarantee

Annual Shareholder Report July 31, 2024

Eaton Vance Emerging Markets Debt Opportunities Fund

Annual Shareholder Report July 31, 2024

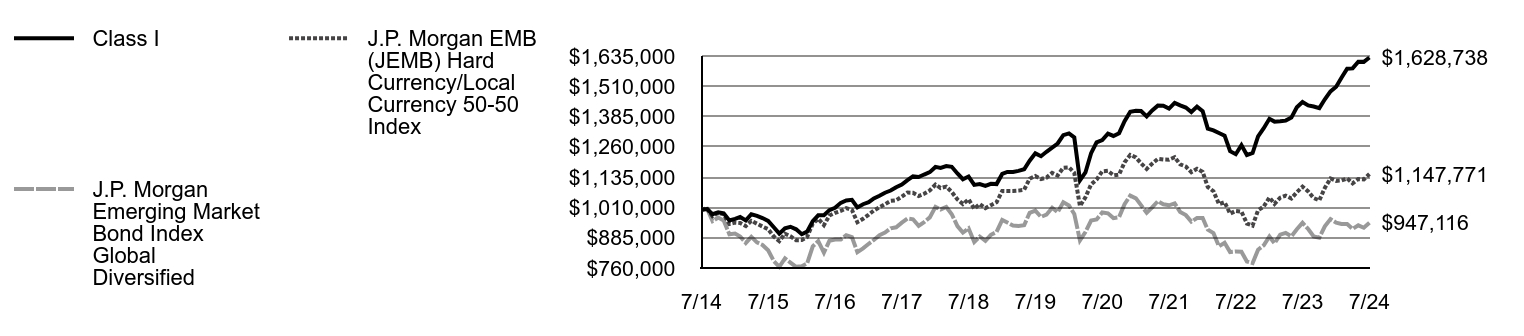

This annual shareholder report contains important information about the Eaton Vance Emerging Markets Debt Opportunities Fund for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at www.eatonvance.com/open-end-mutual-fund-documents.php. You can also request this information by contacting us at 1-800-262-1122.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Class I | $97 | 0.91% |

How did the Fund perform last year and what affected its performance?

Key contributors to (↑) and detractors from (↓) performance, relative to the J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index (the Index):

↑ An overweight position in Surinamese government bonds -- boosted by debt restructuring in late 2023 -- helped Index-relative returns during the period

↑ An out-of-Index allocation to Egyptian local-currency bonds aided returns as actions by Egypt’s central bank led to support by the IMF and other groups

↑ An overweight exposure to Brazilian corporate bonds -- including sugar and ethanol producer Usina Coruripe, and mining firm Samarco -- helped returns

↑ The use of derivatives -- including foreign exchange forwards to manage currency exposures and interest-rate swaps to manage interest-rate exposures -- helped Index-relative performance

↓ The Fund’s lack of exposure to U.S. interest rates hurt performance as short-term interest-rate declines led to multiple bond rallies during the period

↓ An underweight exposure to the South African rand, which rallied after the ANC Party lost its majority in a national election, detracted from returns

↓ An out-of-Index exposure to the South Korean won hurt returns as the currency weakened amid rising concerns over political and economic risks

Comparison of the change in value of a $1,000,000 investment for the period indicated.

| Class I | J.P. Morgan Emerging Market Bond Index Global Diversified | J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index |

|---|

| 7/14 | $1,000,000 | $1,000,000 | $1,000,000 |

| 8/14 | $1,003,041 | $1,004,800 | $1,006,507 |

| 9/14 | $981,784 | $953,471 | $974,074 |

| 10/14 | $989,883 | $968,373 | $988,062 |

| 11/14 | $985,830 | $955,682 | $981,372 |

| 12/14 | $956,557 | $899,035 | $941,886 |

| 1/15 | $962,877 | $902,050 | $947,255 |

| 2/15 | $970,250 | $889,941 | $945,646 |

| 3/15 | $956,558 | $863,416 | $933,273 |

| 4/15 | $981,840 | $888,615 | $954,692 |

| 5/15 | $975,518 | $865,700 | $942,688 |

| 6/15 | $966,033 | $855,160 | $931,157 |

| 7/15 | $954,443 | $833,234 | $920,259 |

| 8/15 | $928,104 | $788,415 | $889,850 |

| 9/15 | $901,764 | $765,008 | $871,146 |

| 10/15 | $923,883 | $799,639 | $901,690 |

| 11/15 | $930,203 | $782,348 | $890,640 |

| 12/15 | $919,700 | $764,915 | $874,876 |

| 1/16 | $899,354 | $767,573 | $875,214 |

| 2/16 | $910,064 | $778,654 | $887,954 |

| 3/16 | $952,890 | $849,173 | $942,511 |

| 4/16 | $977,519 | $871,017 | $962,878 |

| 5/16 | $977,519 | $823,660 | $936,784 |

| 6/16 | $998,932 | $872,154 | $976,446 |

| 7/16 | $1,008,567 | $877,403 | $987,650 |

| 8/16 | $1,028,908 | $877,755 | $995,515 |

| 9/16 | $1,038,542 | $895,514 | $1,006,957 |

| 10/16 | $1,041,538 | $887,943 | $999,554 |

| 11/16 | $1,010,115 | $825,506 | $949,007 |

| 12/16 | $1,023,157 | $840,957 | $962,902 |

| 1/17 | $1,031,840 | $859,894 | $980,190 |

| 2/17 | $1,047,327 | $875,389 | $997,346 |

| 3/17 | $1,058,394 | $895,633 | $1,010,614 |

| 4/17 | $1,070,676 | $906,094 | $1,023,115 |

| 5/17 | $1,079,601 | $923,858 | $1,037,039 |

| 6/17 | $1,093,169 | $928,086 | $1,039,570 |

| 7/17 | $1,104,507 | $947,334 | $1,054,582 |

| 8/17 | $1,122,892 | $964,321 | $1,071,243 |

| 9/17 | $1,137,897 | $961,047 | $1,070,380 |

| 10/17 | $1,135,312 | $933,956 | $1,057,194 |

| 11/17 | $1,145,750 | $949,692 | $1,066,304 |

| 12/17 | $1,155,781 | $968,892 | $1,079,881 |

| 1/18 | $1,177,264 | $1,012,287 | $1,104,140 |

| 2/18 | $1,173,381 | $1,001,718 | $1,090,103 |

| 3/18 | $1,180,470 | $1,011,947 | $1,095,952 |

| 4/18 | $1,177,773 | $982,024 | $1,073,956 |

| 5/18 | $1,150,328 | $933,148 | $1,042,833 |

| 6/18 | $1,126,453 | $906,484 | $1,023,732 |

| 7/18 | $1,137,449 | $923,663 | $1,043,675 |

| 8/18 | $1,103,175 | $867,447 | $1,004,594 |

| 9/18 | $1,106,721 | $889,940 | $1,023,789 |

| 10/18 | $1,098,800 | $872,504 | $1,006,718 |

| 11/18 | $1,107,544 | $897,000 | $1,019,386 |

| 12/18 | $1,106,329 | $908,713 | $1,031,304 |

| 1/19 | $1,148,243 | $958,304 | $1,077,821 |

| 2/19 | $1,156,376 | $947,830 | $1,077,530 |

| 3/19 | $1,156,623 | $935,253 | $1,077,652 |

| 4/19 | $1,160,839 | $933,613 | $1,079,460 |

| 5/19 | $1,167,749 | $936,372 | $1,083,484 |

| 6/19 | $1,203,068 | $987,961 | $1,128,503 |

| 7/19 | $1,233,222 | $997,124 | $1,139,683 |

| 8/19 | $1,221,445 | $970,800 | $1,127,123 |

| 9/19 | $1,239,687 | $980,133 | $1,133,036 |

| 10/19 | $1,256,715 | $1,008,532 | $1,152,649 |

| 11/19 | $1,273,848 | $990,202 | $1,141,893 |

| 12/19 | $1,308,047 | $1,031,138 | $1,174,018 |

| 1/20 | $1,315,565 | $1,017,869 | $1,175,454 |

| 2/20 | $1,298,887 | $983,163 | $1,152,535 |

| 3/20 | $1,122,037 | $874,279 | $1,015,617 |

| 4/20 | $1,154,291 | $908,555 | $1,051,624 |

| 5/20 | $1,233,732 | $955,600 | $1,105,094 |

| 6/20 | $1,278,566 | $960,097 | $1,125,007 |

| 7/20 | $1,288,335 | $989,087 | $1,158,962 |

| 8/20 | $1,314,481 | $985,841 | $1,161,152 |

| 9/20 | $1,304,991 | $965,965 | $1,142,679 |

| 10/20 | $1,316,454 | $970,079 | $1,145,759 |

| 11/20 | $1,365,779 | $1,023,317 | $1,195,879 |

| 12/20 | $1,404,778 | $1,058,914 | $1,226,736 |

| 1/21 | $1,408,794 | $1,047,562 | $1,216,627 |

| 2/21 | $1,408,166 | $1,019,493 | $1,192,265 |

| 3/21 | $1,385,909 | $988,197 | $1,169,194 |

| 4/21 | $1,410,271 | $1,010,525 | $1,190,632 |

| 5/21 | $1,430,110 | $1,035,737 | $1,210,564 |

| 6/21 | $1,429,516 | $1,023,155 | $1,207,964 |

| 7/21 | $1,417,793 | $1,018,783 | $1,207,296 |

| 8/21 | $1,441,198 | $1,026,635 | $1,217,041 |

| 9/21 | $1,430,952 | $991,407 | $1,187,819 |

| 10/21 | $1,422,238 | $978,240 | $1,178,629 |

| 11/21 | $1,403,726 | $951,483 | $1,155,466 |

| 12/21 | $1,426,077 | $966,287 | $1,169,664 |

| 1/22 | $1,407,343 | $966,237 | $1,156,419 |

| 2/22 | $1,335,154 | $917,920 | $1,094,583 |

| 3/22 | $1,327,843 | $903,861 | $1,076,770 |

| 4/22 | $1,317,109 | $849,392 | $1,023,728 |

| 5/22 | $1,306,284 | $864,367 | $1,031,310 |

| 6/22 | $1,242,323 | $825,879 | $984,437 |

| 7/22 | $1,229,707 | $828,297 | $995,576 |

| 8/22 | $1,267,262 | $827,134 | $992,974 |

| 9/22 | $1,226,356 | $786,851 | $943,501 |

| 10/22 | $1,234,540 | $779,909 | $934,857 |

| 11/22 | $1,303,300 | $835,334 | $998,175 |

| 12/22 | $1,336,712 | $853,375 | $1,013,615 |

| 1/23 | $1,375,757 | $890,009 | $1,051,109 |

| 2/23 | $1,364,151 | $861,845 | $1,024,475 |

| 3/23 | $1,365,320 | $897,396 | $1,050,200 |

| 4/23 | $1,368,331 | $905,133 | $1,058,435 |

| 5/23 | $1,380,674 | $890,841 | $1,047,018 |

| 6/23 | $1,423,140 | $919,882 | $1,072,750 |

| 7/23 | $1,445,149 | $946,350 | $1,095,932 |

| 8/23 | $1,431,102 | $920,923 | $1,075,869 |

| 9/23 | $1,426,570 | $889,918 | $1,048,662 |

| 10/23 | $1,420,071 | $885,233 | $1,039,164 |

| 11/23 | $1,456,361 | $931,876 | $1,090,708 |

| 12/23 | $1,489,002 | $961,763 | $1,129,469 |

| 1/24 | $1,508,030 | $947,116 | $1,119,643 |

| 2/24 | $1,545,143 | $941,683 | $1,121,165 |

| 3/24 | $1,582,527 | $941,417 | $1,129,667 |

| 4/24 | $1,583,801 | $921,300 | $1,109,241 |

| 5/24 | $1,611,548 | $936,163 | $1,127,225 |

| 6/24 | $1,610,804 | $926,051 | $1,125,490 |

| 7/24 | $1,628,738 | $947,116 | $1,147,771 |

Average Annual Total Returns (%)Footnote Reference*

| 1 Year | 5 Years | 10 Years |

|---|

| Class I | 12.70% | 5.71% | 4.99% |

J.P. Morgan Emerging Market Bond Index Global Diversified Footnote Reference†Footnote Referencea | 0.08% | (1.02%) | (0.54%) |

J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 IndexFootnote Referencea | 4.73% | 0.14% | 1.39% |

| Footnote | Description |

Footnote† | In accordance with regulatory changes requiring the Fund’s primary benchmark to represent the overall applicable market, the Fund’s primary prospectus benchmark changed to the indicated benchmark effective May 1, 2024. |

Footnotea | Index is used with permission. Copyright 2021, J.P. Morgan Chase & Co. All rights reserved. See Fund prospectus for full description. |

Footnote* | Class I performance prior to 9/3/15 is linked to Class R6. This linked performance is adjusted for any applicable sales charge, but is not adjusted for class expense differences. If adjusted for such differences, the performance would be different. Performance presented in the Financial Highlights included in the financial statements is not linked. |

Performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance assumes that all dividends and distributions, if any, were reinvested. For more recent performance information, visit www.eatonvance.com/performance.php.

THE FUND'S PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

| Total Net Assets | $2,357,927,839 |

| # of Portfolio Holdings (including derivatives) | 699 |

| Portfolio Turnover Rate | 173% |

| Total Advisory Fees Paid | $11,163,451 |

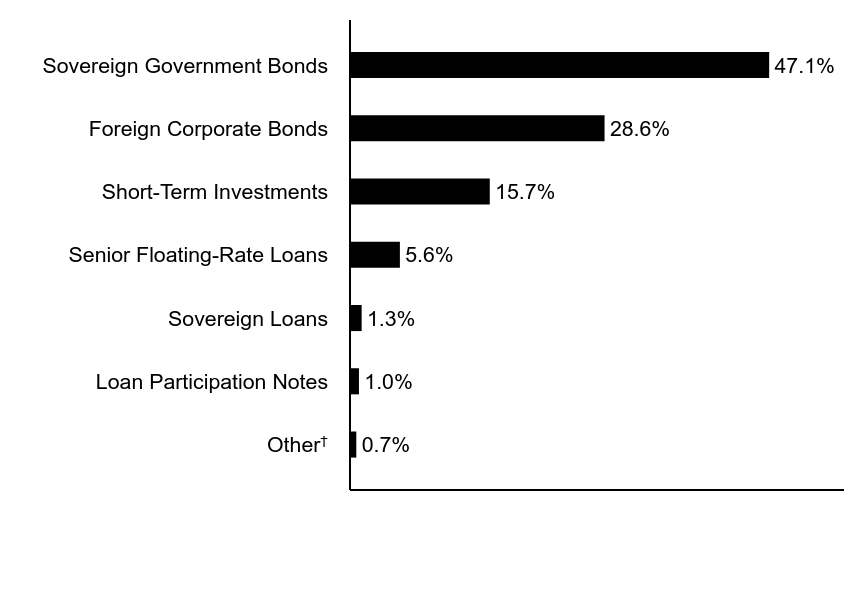

What did the Fund invest in?

The following tables reflect what the Fund invested in as of the report date.

Asset Allocation (% of total investments)

| Value | Value |

|---|

OtherFootnote Reference† | 0.7% |

| Loan Participation Notes | 1.0% |

| Sovereign Loans | 1.3% |

| Senior Floating-Rate Loans | 5.6% |

| Short-Term Investments | 15.7% |

| Foreign Corporate Bonds | 28.6% |

| Sovereign Government Bonds | 47.1% |

| Footnote | Description |

Footnote† | Investment types less than 1% each |

Foreign Currency Exposure (% of net assets)Footnote Reference*

| Egypt | 9.7% |

| Uzbekistan | 9.3% |

| Dominican Republic | 4.4% |

| Nigeria | 3.6% |

| Serbia | 3.2% |

| Turkey | 2.7% |

| Taiwan | 1.9% |

| Kazakhstan | 1.9% |

| Malaysia | 1.6% |

| Other | 9.3% |

| Total Long Exposure | 47.7% |

| Euro | (3.0%) |

| Total Short Exposure | (3.0%) |

| Footnote | Description |

Footnote* | Currency exposures include all foreign exchange denominated assets and currency derivatives. |

If you wish to view additional information about the Fund, including the prospectus, statement of additional information, financial statements and holdings, please scan the QR code or visit www.eatonvance.com/open-end-mutual-fund-documents.php. For proxy information, please visit www.eatonvance.com/proxyvoting.

The Funds may deliver a single copy of certain required shareholder documents (including prospectuses, shareholder reports, and proxy materials) to investors with the same last name and the same address. Your participation will continue indefinitely unless you instruct otherwise by calling 1-800-262-1122 or by contacting your financial intermediary. Your instruction will typically be effective within 30 days of receipt.

Not FDIC Insured | May Lose Value | No Bank Guarantee

Annual Shareholder Report July 31, 2024

Eaton Vance Emerging Markets Debt Opportunities Fund

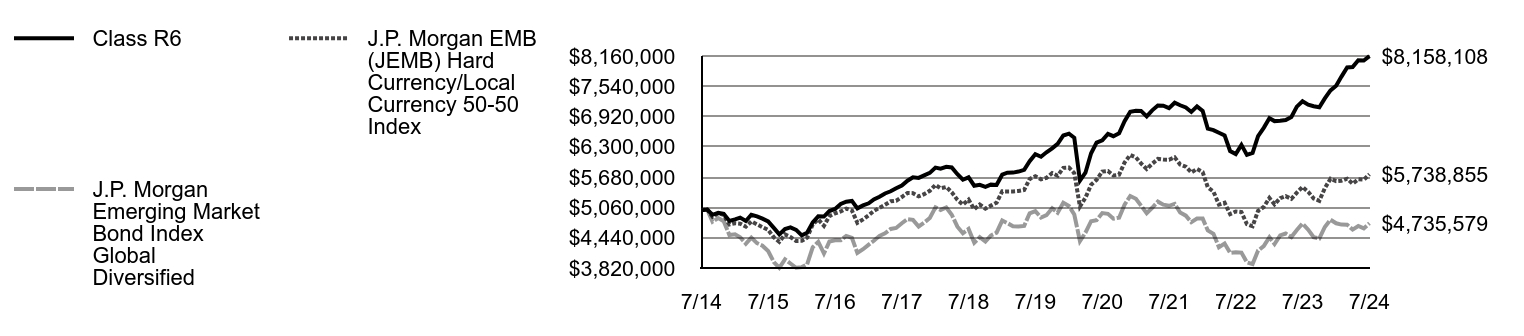

Annual Shareholder Report July 31, 2024

This annual shareholder report contains important information about the Eaton Vance Emerging Markets Debt Opportunities Fund for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at www.eatonvance.com/open-end-mutual-fund-documents.php. You can also request this information by contacting us at 1-800-262-1122.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Class R6 | $87 | 0.82% |

How did the Fund perform last year and what affected its performance?

Key contributors to (↑) and detractors from (↓) performance, relative to the J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index (the Index):

↑ An overweight position in Surinamese government bonds -- boosted by debt restructuring in late 2023 -- helped Index-relative returns during the period

↑ An out-of-Index allocation to Egyptian local-currency bonds aided returns as actions by Egypt’s central bank led to support by the IMF and other groups

↑ An overweight exposure to Brazilian corporate bonds -- including sugar and ethanol producer Usina Coruripe, and mining firm Samarco -- helped returns

↑ The use of derivatives -- including foreign exchange forwards to manage currency exposures and interest-rate swaps to manage interest-rate exposures -- helped Index-relative performance

↓ The Fund’s lack of exposure to U.S. interest rates hurt performance as short-term interest-rate declines led to multiple bond rallies during the period

↓ An underweight exposure to the South African rand, which rallied after the ANC Party lost its majority in a national election, detracted from returns

↓ An out-of-Index exposure to the South Korean won hurt returns as the currency weakened amid rising concerns over political and economic risks

Comparison of the change in value of a $5,000,000 investment for the period indicated.

| Class R6 | J.P. Morgan Emerging Market Bond Index Global Diversified | J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 Index |

|---|

| 7/14 | $5,000,000 | $5,000,000 | $5,000,000 |

| 8/14 | $5,015,203 | $5,024,002 | $5,032,537 |

| 9/14 | $4,908,919 | $4,767,355 | $4,870,371 |

| 10/14 | $4,949,415 | $4,841,866 | $4,940,309 |

| 11/14 | $4,929,149 | $4,778,409 | $4,906,861 |

| 12/14 | $4,782,787 | $4,495,175 | $4,709,428 |

| 1/15 | $4,814,385 | $4,510,250 | $4,736,274 |

| 2/15 | $4,851,248 | $4,449,703 | $4,728,229 |

| 3/15 | $4,782,788 | $4,317,082 | $4,666,366 |

| 4/15 | $4,909,199 | $4,443,075 | $4,773,459 |

| 5/15 | $4,877,588 | $4,328,502 | $4,713,441 |

| 6/15 | $4,830,166 | $4,275,799 | $4,655,783 |

| 7/15 | $4,772,214 | $4,166,168 | $4,601,297 |

| 8/15 | $4,640,518 | $3,942,077 | $4,449,251 |

| 9/15 | $4,508,820 | $3,825,042 | $4,355,731 |

| 10/15 | $4,619,417 | $3,998,197 | $4,508,449 |

| 11/15 | $4,651,017 | $3,911,742 | $4,453,202 |

| 12/15 | $4,599,861 | $3,824,575 | $4,374,380 |

| 1/16 | $4,487,391 | $3,837,863 | $4,376,072 |

| 2/16 | $4,540,950 | $3,893,271 | $4,439,770 |

| 3/16 | $4,755,164 | $4,245,863 | $4,712,555 |

| 4/16 | $4,878,344 | $4,355,086 | $4,814,391 |

| 5/16 | $4,872,968 | $4,118,301 | $4,683,919 |

| 6/16 | $4,985,416 | $4,360,769 | $4,882,229 |

| 7/16 | $5,028,237 | $4,387,014 | $4,938,249 |

| 8/16 | $5,129,967 | $4,388,776 | $4,977,577 |

| 9/16 | $5,178,154 | $4,477,572 | $5,034,786 |

| 10/16 | $5,193,257 | $4,439,714 | $4,997,769 |

| 11/16 | $5,041,561 | $4,127,530 | $4,745,035 |

| 12/16 | $5,101,502 | $4,204,785 | $4,814,511 |

| 1/17 | $5,145,136 | $4,299,469 | $4,900,949 |

| 2/17 | $5,222,755 | $4,376,943 | $4,986,730 |

| 3/17 | $5,278,230 | $4,478,167 | $5,053,071 |

| 4/17 | $5,345,453 | $4,530,472 | $5,115,575 |

| 5/17 | $5,390,252 | $4,619,289 | $5,185,196 |

| 6/17 | $5,452,599 | $4,640,431 | $5,197,852 |

| 7/17 | $5,509,481 | $4,736,670 | $5,272,912 |

| 8/17 | $5,607,487 | $4,821,606 | $5,356,214 |

| 9/17 | $5,676,815 | $4,805,234 | $5,351,902 |

| 10/17 | $5,663,964 | $4,669,781 | $5,285,970 |

| 11/17 | $5,716,318 | $4,748,459 | $5,331,519 |

| 12/17 | $5,766,594 | $4,844,458 | $5,399,404 |

| 1/18 | $5,874,294 | $5,061,436 | $5,520,702 |

| 2/18 | $5,854,984 | $5,008,589 | $5,450,513 |

| 3/18 | $5,890,594 | $5,059,737 | $5,479,761 |

| 4/18 | $5,877,210 | $4,910,119 | $5,369,778 |

| 5/18 | $5,739,960 | $4,665,741 | $5,214,164 |

| 6/18 | $5,626,841 | $4,532,422 | $5,118,661 |

| 7/18 | $5,675,805 | $4,618,315 | $5,218,375 |

| 8/18 | $5,504,348 | $4,337,237 | $5,022,970 |

| 9/18 | $5,522,194 | $4,449,700 | $5,118,944 |

| 10/18 | $5,482,678 | $4,362,518 | $5,033,589 |

| 11/18 | $5,526,626 | $4,484,999 | $5,096,930 |

| 12/18 | $5,520,692 | $4,543,564 | $5,156,521 |

| 1/19 | $5,730,753 | $4,791,521 | $5,389,104 |

| 2/19 | $5,771,585 | $4,739,148 | $5,387,648 |

| 3/19 | $5,773,015 | $4,676,264 | $5,388,259 |

| 4/19 | $5,794,293 | $4,668,064 | $5,397,301 |

| 5/19 | $5,828,977 | $4,681,862 | $5,417,422 |

| 6/19 | $6,006,021 | $4,939,807 | $5,642,513 |

| 7/19 | $6,150,394 | $4,985,619 | $5,698,414 |

| 8/19 | $6,098,345 | $4,853,998 | $5,635,617 |

| 9/19 | $6,189,861 | $4,900,664 | $5,665,180 |

| 10/19 | $6,268,342 | $5,042,661 | $5,763,247 |

| 11/19 | $6,361,278 | $4,951,011 | $5,709,463 |

| 12/19 | $6,532,845 | $5,155,688 | $5,870,090 |

| 1/20 | $6,570,690 | $5,089,345 | $5,877,271 |

| 2/20 | $6,487,247 | $4,915,813 | $5,762,676 |

| 3/20 | $5,608,344 | $4,371,397 | $5,078,083 |

| 4/20 | $5,770,087 | $4,542,775 | $5,258,122 |

| 5/20 | $6,168,340 | $4,777,998 | $5,525,471 |

| 6/20 | $6,385,877 | $4,800,485 | $5,625,033 |

| 7/20 | $6,434,960 | $4,945,434 | $5,794,812 |

| 8/20 | $6,566,082 | $4,929,205 | $5,805,760 |

| 9/20 | $6,518,577 | $4,829,825 | $5,713,396 |

| 10/20 | $6,576,042 | $4,850,395 | $5,728,793 |

| 11/20 | $6,823,363 | $5,116,586 | $5,979,397 |

| 12/20 | $7,018,992 | $5,294,570 | $6,133,682 |

| 1/21 | $7,039,276 | $5,237,808 | $6,083,134 |

| 2/21 | $7,036,261 | $5,097,467 | $5,961,326 |

| 3/21 | $6,924,868 | $4,940,984 | $5,845,970 |

| 4/21 | $7,047,216 | $5,052,623 | $5,953,158 |

| 5/21 | $7,146,809 | $5,178,687 | $6,052,820 |

| 6/21 | $7,144,070 | $5,115,777 | $6,039,821 |

| 7/21 | $7,093,404 | $5,093,916 | $6,036,482 |

| 8/21 | $7,202,913 | $5,133,173 | $6,085,206 |

| 9/21 | $7,151,613 | $4,957,034 | $5,939,094 |

| 10/21 | $7,107,998 | $4,891,201 | $5,893,146 |

| 11/21 | $7,015,240 | $4,757,413 | $5,777,331 |

| 12/21 | $7,127,500 | $4,831,435 | $5,848,321 |

| 1/22 | $7,033,571 | $4,831,183 | $5,782,097 |

| 2/22 | $6,671,666 | $4,589,600 | $5,472,917 |

| 3/22 | $6,643,553 | $4,519,304 | $5,383,851 |

| 4/22 | $6,589,857 | $4,246,960 | $5,118,639 |

| 5/22 | $6,535,708 | $4,321,836 | $5,156,550 |

| 6/22 | $6,214,917 | $4,129,393 | $4,922,185 |

| 7/22 | $6,151,716 | $4,141,484 | $4,977,879 |

| 8/22 | $6,340,208 | $4,135,670 | $4,964,870 |

| 9/22 | $6,135,073 | $3,934,253 | $4,717,504 |

| 10/22 | $6,176,223 | $3,899,543 | $4,674,284 |

| 11/22 | $6,521,301 | $4,176,670 | $4,990,873 |

| 12/22 | $6,689,125 | $4,266,877 | $5,068,074 |

| 1/23 | $6,885,131 | $4,450,043 | $5,255,546 |

| 2/23 | $6,827,077 | $4,309,226 | $5,122,374 |

| 3/23 | $6,833,128 | $4,486,979 | $5,251,001 |

| 4/23 | $6,848,426 | $4,525,663 | $5,292,174 |

| 5/23 | $6,910,464 | $4,454,205 | $5,235,088 |

| 6/23 | $7,123,851 | $4,599,409 | $5,363,749 |

| 7/23 | $7,234,574 | $4,731,749 | $5,479,659 |

| 8/23 | $7,164,163 | $4,604,613 | $5,379,344 |

| 9/23 | $7,131,979 | $4,449,588 | $5,243,311 |

| 10/23 | $7,109,252 | $4,426,164 | $5,195,821 |

| 11/23 | $7,291,628 | $4,659,381 | $5,453,540 |

| 12/23 | $7,455,690 | $4,808,815 | $5,647,345 |

| 1/24 | $7,551,418 | $4,735,581 | $5,598,214 |

| 2/24 | $7,737,953 | $4,708,415 | $5,605,823 |

| 3/24 | $7,925,860 | $4,707,084 | $5,648,334 |

| 4/24 | $7,932,456 | $4,606,501 | $5,546,204 |

| 5/24 | $8,071,888 | $4,680,817 | $5,636,124 |

| 6/24 | $8,068,359 | $4,630,256 | $5,627,452 |

| 7/24 | $8,158,108 | $4,735,579 | $5,738,855 |

Average Annual Total Returns (%)

| 1 Year | 5 Years | 10 Years |

|---|

| Class R6 | 12.76% | 5.81% | 5.01% |

J.P. Morgan Emerging Market Bond Index Global Diversified Footnote Reference†Footnote Referencea | 0.08% | (1.02%) | (0.54%) |

J.P. Morgan EMB (JEMB) Hard Currency/Local Currency 50-50 IndexFootnote Referencea | 4.73% | 0.14% | 1.39% |

| Footnote | Description |

Footnote† | In accordance with regulatory changes requiring the Fund’s primary benchmark to represent the overall applicable market, the Fund’s primary prospectus benchmark changed to the indicated benchmark effective May 1, 2024. |

Footnotea | Index is used with permission. Copyright 2021, J.P. Morgan Chase & Co. All rights reserved. See Fund prospectus for full description. |

Performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance assumes that all dividends and distributions, if any, were reinvested. For more recent performance information, visit www.eatonvance.com/performance.php.

THE FUND'S PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

| Total Net Assets | $2,357,927,839 |

| # of Portfolio Holdings (including derivatives) | 699 |

| Portfolio Turnover Rate | 173% |

| Total Advisory Fees Paid | $11,163,451 |

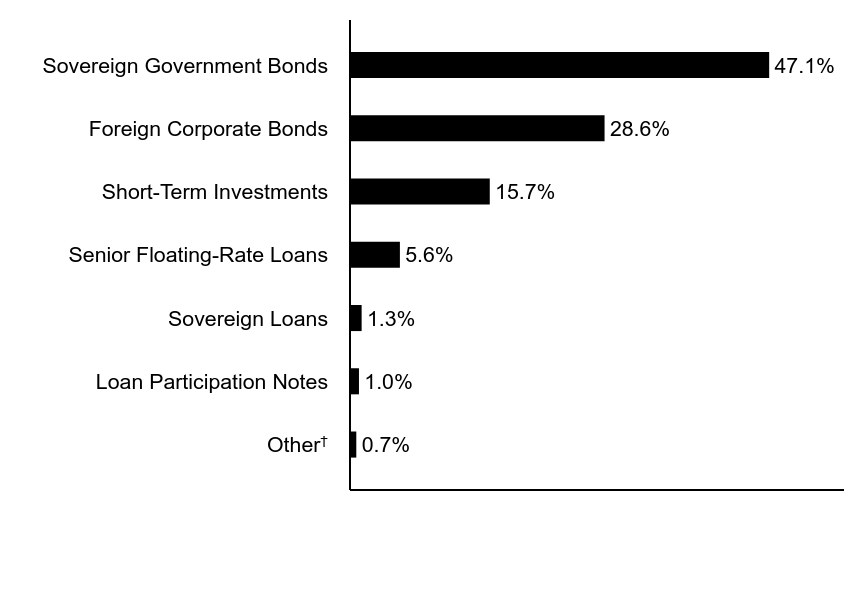

What did the Fund invest in?

The following tables reflect what the Fund invested in as of the report date.

Asset Allocation (% of total investments)

| Value | Value |

|---|

OtherFootnote Reference† | 0.7% |

| Loan Participation Notes | 1.0% |

| Sovereign Loans | 1.3% |

| Senior Floating-Rate Loans | 5.6% |

| Short-Term Investments | 15.7% |

| Foreign Corporate Bonds | 28.6% |

| Sovereign Government Bonds | 47.1% |

| Footnote | Description |

Footnote† | Investment types less than 1% each |

Foreign Currency Exposure (% of net assets)Footnote Reference*

| Egypt | 9.7% |

| Uzbekistan | 9.3% |

| Dominican Republic | 4.4% |

| Nigeria | 3.6% |

| Serbia | 3.2% |

| Turkey | 2.7% |

| Taiwan | 1.9% |

| Kazakhstan | 1.9% |

| Malaysia | 1.6% |

| Other | 9.3% |

| Total Long Exposure | 47.7% |

| Euro | (3.0%) |

| Total Short Exposure | (3.0%) |

| Footnote | Description |

Footnote* | Currency exposures include all foreign exchange denominated assets and currency derivatives. |

If you wish to view additional information about the Fund, including the prospectus, statement of additional information, financial statements and holdings, please scan the QR code or visit www.eatonvance.com/open-end-mutual-fund-documents.php. For proxy information, please visit www.eatonvance.com/proxyvoting.

The Funds may deliver a single copy of certain required shareholder documents (including prospectuses, shareholder reports, and proxy materials) to investors with the same last name and the same address. Your participation will continue indefinitely unless you instruct otherwise by calling 1-800-262-1122 or by contacting your financial intermediary. Your instruction will typically be effective within 30 days of receipt.

Not FDIC Insured | May Lose Value | No Bank Guarantee

Annual Shareholder Report July 31, 2024

(b) Not applicable.

Item 2. Code of Ethics

The registrant (sometimes referred to as the “Fund”) has adopted a code of ethics applicable to its Principal Executive Officer, Principal Financial Officer and Principal Accounting Officer. The registrant undertakes to provide a copy of such code of ethics to any person upon request, without charge, by calling 1-800-262-1122. The registrant has not amended the code of ethics as described in Form N-CSR during the period covered by this report. The registrant has not granted any waiver, including an implicit waiver, from a provision of the code of ethics as described in Form N-CSR during the period covered by this report.

Item 3. Audit Committee Financial Expert

The registrant’s Board of Trustees (the “Board”) has designated George J. Gorman and Scott E. Wennerholm, each an independent trustee, as audit committee financial experts. Mr. Gorman is a certified public accountant who is the Principal at George J. Gorman LLC (a consulting firm). Previously, Mr. Gorman served in various capacities at Ernst & Young LLP (a registered public accounting firm), including as Senior Partner. Mr. Gorman also has experience serving as an independent trustee and audit committee financial expert of other mutual fund complexes. Mr. Wennerholm is a private investor. Previously, Mr. Wennerholm served as a Trustee at Wheelock College (postsecondary institution), as a Consultant at GF Parish Group (executive recruiting firm), Chief Operating Officer and Executive Vice President at BNY Mellon Asset Management (investment management firm), Chief Operating Officer and Chief Financial Officer at Natixis Global Asset Management (investment management firm), and Vice President at Fidelity Investments Institutional Services (investment management firm).

Item 4. Principal Accountant Fees and Services

Eaton Vance Emerging Markets Debt Opportunities Fund (the “Fund”) is the only series of Eaton Vance Series Fund, Inc. (the “Corporation”), a Maryland corporation. The Corporation is registered under the Investment Company Act of 1940 as an open-end management investment company. This Form N-CSR relates to the Fund’s annual report.

(a)-(d)

The following table presents the aggregate fees billed to the registrant for the registrant’s fiscal years ended July 31, 2023 and July 31, 2024 by the registrant’s principal accountant, Deloitte & Touche LLP (“D&T”), for professional services rendered for the audit of the registrant’s annual financial statements and fees billed for other services rendered by D&T during those periods.

Eaton Vance Emerging Markets Debt Opportunities Fund

| | | | | | | | |

Fiscal Years Ended | | 7/31/23 | | | 7/31/24 | |

Audit Fees | | $ | 109,100 | | | $ | 108,900 | |

Audit-Related Fees(1) | | $ | 0 | | | $ | 0 | |

Tax Fees(2) | | $ | 7,481 | | | $ | 0 | |

All Other Fees(3) | | $ | 0 | | | $ | 0 | |

| | | | | | | | |

Total | | $ | 116,581 | | | $ | 108,900 | |

| | | | | | | | |

| (1) | Audit-related fees consist of the aggregate fees billed for assurance and related services that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under the category of audit fees. |

| (2) | Tax fees consist of the aggregate fees billed for professional services rendered by the principal accountant relating to tax compliance, tax advice, and tax planning and specifically include fees for tax return preparation and other related tax compliance/planning matters. |

| (3) | All other fees consist of the aggregate fees billed for products and services provided by the registrant’s principal accountant other than audit, audit-related, and tax services. |

(e)(1) The registrant’s audit committee has adopted policies and procedures relating to the pre-approval of services provided by the registrant’s principal accountant (the “Pre-Approval Policies”). The Pre-Approval Policies establish a framework intended to assist the audit committee in the proper discharge of its pre-approval responsibilities. As a general matter, the Pre-Approval Policies (i) specify certain types of audit, audit-related, tax, and other services determined to be pre-approved by the audit committee; and (ii) delineate specific procedures governing the mechanics of the pre-approval process, including the approval and monitoring of audit and non-audit service fees. Unless a service is specifically pre-approved under the Pre-Approval Policies, it must be separately pre-approved by the Audit Committee.

The Pre-Approval Policies and the types of audit and non-audit services pre-approved therein must be reviewed and ratified by the registrant’s audit committee at least annually. The registrant’s audit committee maintains full responsibility for the appointment, compensation, and oversight of the work of the registrant’s principal accountant.

(e)(2) No services described in paragraphs (b)-(d) above were approved by the registrant’s audit committee pursuant to the “de minimis exception” set forth in Rule 2-01 (c)(7)(i)(C) of Regulation S-X.

(f) Not applicable.

(g) The following table presents (i) the aggregate non-audit fees (i.e., fees for audit-related, tax, and other services) billed to the registrant by D&T for the registrant’s fiscal years ended July 31, 2023 and July 31, 2024; and (ii) the aggregate non-audit fees (i.e., fees for audit-related, tax, and other services) billed to the Eaton Vance organization by D&T for the same time periods.

| | | | | | | | |

Fiscal Years Ended | | 7/31/23 | | | 7/31/24 | |

Registrant | | $ | 7,481 | | | $ | 0 | |

Eaton Vance(1) | | $ | 0 | | | $ | 18,490 | |

| (1) | The investment adviser to the registrant, as well as any of its affiliates that provide ongoing services to the registrant, are subsidiaries of Morgan Stanley. |

(h) The registrant’s audit committee has considered whether the provision by the registrant’s principal accountant of non-audit services to the registrant’s investment adviser and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant that were not pre-approved pursuant to Rule 2-01(c)(7)(ii) of Regulation S-X is compatible with maintaining the principal accountant’s independence.

(i) Not applicable.

(j) Not applicable.

Item 5. Audit Committee of Listed Registrants

Not applicable.

Item 6. Schedule of Investments

(a) Please see schedule of investments contained in the Financial Statements and Financial Highlights included under Item 7 of this Form N-CSR.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies

Eaton Vance

Emerging Markets Debt Opportunities Fund

Annual Financial Statements and Additional Information

July 31, 2024

This report must be preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of a mutual fund. This and other important information is contained in the prospectus and/or statement of additional information, which can be obtained by calling 1-800-262-1122 or from a financial intermediary. Prospective investors should read the prospectus carefully before investing.

Annual Financial Statements and Additional Information July 31, 2024

Eaton Vance

Emerging Markets Debt Opportunities Fund

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

| Security | Principal

Amount

(000's omitted) | Value |

| China — 0.3% |

| Alibaba Group Holding Ltd., 0.50%, 6/1/31(1) | USD | 2,082 | $ 2,095,872 |

| H World Group Ltd., 3.00%, 5/1/26 | USD | 2,023 | 2,071,016 |

| PDD Holdings, Inc., 0.00%, 12/1/25 | USD | 2,067 | 2,008,883 |

| Sunac China Holdings Ltd., 1.00% PIK, 9/30/32(2) | USD | 1,231 | 80,650 |

| | | | $ 6,256,421 |

| India — 0.2% |

| Sammaan Capital Ltd., 4.50%, 9/28/26(2) | USD | 4,965 | $ 4,893,901 |

| | | | $ 4,893,901 |

| Tanzania — 0.1% |

| HTA Group Ltd., 2.875%, 3/18/27(2) | USD | 3,400 | $ 3,188,725 |

| | | | $ 3,188,725 |

Total Convertible Bonds

(identified cost $15,023,032) | | | $ 14,339,047 |

| Foreign Corporate Bonds — 26.5% |

| Security | Principal

Amount

(000's omitted) | Value |

| Argentina — 1.0% |

| Generacion Mediterranea SA/Central Termica Roca SA, 12.50%, 5/28/27(1) | USD | 7,712 | $ 7,712,000 |

| Pan American Energy LLC, 8.50%, 4/30/32(1) | USD | 7,784 | 8,124,706 |

| Telecom Argentina SA, 9.50%, 7/18/31(1) | USD | 4,640 | 4,603,496 |

| Transportadora de Gas del Sur SA, 8.50%, 7/24/31(1) | USD | 3,981 | 4,019,381 |

| | | | $ 24,459,583 |

| Brazil — 4.5% |

| Braskem Netherlands Finance BV, 8.50% to 10/24/25, 1/23/81(2)(3) | USD | 11,571 | $ 11,678,279 |

| Coruripe Netherlands BV, 10.00%, 2/10/27(2) | USD | 10,856 | 9,744,926 |

| Gol Finance SA, 15.844%, (1 mo. SOFR + 10.50%), 1/29/25(1)(4) | USD | 2,517 | 2,712,278 |

| Itau BBA International PLC, 9.03%, 2/19/30 | PYG | 55,450,500 | 8,045,146 |

| MC Brazil Downstream Trading SARL: | | | |

| 7.25%, 6/30/31(2) | USD | 589 | 545,111 |

| 7.25%, 6/30/31(1) | USD | 700 | 648,240 |

| MV24 Capital BV, 6.748%, 6/1/34(2) | USD | 6,071 | 5,758,776 |

| OHI Group SA, 13.00%, 7/22/29(1) | USD | 28,420 | 28,660,149 |

| Security | Principal

Amount

(000's omitted) | Value |

| Brazil (continued) |

| Samarco Mineracao SA, 9.00%, 6/30/31(2)(5) | USD | 23,861 | $ 22,121,320 |

| Vale SA, Series A6, 1.378%(6)(7) | BRL | 55,335 | 3,561,043 |

| Yinson Boronia Production BV, 8.947%, 7/31/42(1) | USD | 12,581 | 12,790,914 |

| | | | $ 106,266,182 |

| Chile — 0.1% |

| AES Andes SA, 6.35% to 1/7/25, 10/7/79(2)(3) | USD | 1,592 | $ 1,573,412 |

| | | | $ 1,573,412 |

| China — 1.2% |

| China Oil & Gas Group Ltd., 4.70%, 6/30/26(2) | USD | 12,060 | $ 11,288,160 |

| Greentown China Holdings Ltd., 4.70%, 4/29/25(2) | USD | 11,940 | 11,584,039 |

| KWG Group Holdings Ltd., 7.875%, 8/30/24(8) | USD | 5,749 | 376,766 |

| Shimao Group Holdings Ltd., 5.60%, 7/15/26(2)(8) | USD | 15,682 | 877,878 |

| Sunac China Holdings Ltd.: | | | |

| 6.00%, (5.00% cash or 6.00% PIK), 9/30/26(2)(5) | USD | 1,021 | 130,161 |

| 6.25%, (5.25% cash or 6.25% PIK), 9/30/27(2)(5) | USD | 1,022 | 117,257 |

| 6.50%, (5.50% cash or 6.50% PIK), 9/30/27(2)(5) | USD | 2,047 | 214,903 |

| 6.75%, (5.75% cash or 6.75% PIK), 9/30/28(2)(5) | USD | 3,074 | 306,608 |

| 7.00%, (6.00% cash or 7.00% PIK), 9/30/29(2)(5) | USD | 3,077 | 274,511 |

| 7.25%, (6.25% cash or 7.25% PIK), 9/30/30(2)(5) | USD | 1,447 | 121,804 |

| Times China Holdings Ltd.: | | | |

| 5.55%, 6/4/24(2)(8) | USD | 17,720 | 498,464 |

| 6.75%, 7/16/23(2)(8) | USD | 3,803 | 109,336 |

| West China Cement Ltd., 4.95%, 7/8/26(2) | USD | 1,324 | 1,090,202 |

| | | | $ 26,990,089 |

| Colombia — 1.8% |

| ABRA Global Finance, 11.50%, (6.00% cash and 5.50% PIK), 3/2/28(1) | USD | 129 | $ 123,853 |

| Banco Davivienda SA, 6.65% to 4/22/31(2)(3)(6) | USD | 3,051 | 2,361,706 |

| Banco de Occidente SA, 10.875% to 5/13/29, 8/13/34(2)(3) | USD | 15,700 | 16,815,877 |

| Bancolombia SA, 8.625% to 6/24/29, 12/24/34(3) | USD | 14,724 | 15,260,582 |

| Canacol Energy Ltd., 5.75%, 11/24/28(2) | USD | 15,150 | 7,505,436 |

| | | | $ 42,067,454 |

| Cyprus — 0.0%(9) |

| Bank of Cyprus PLC, 11.875% to 12/21/28(2)(3)(6) | EUR | 359 | $ 440,056 |

| | | | $ 440,056 |

1

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Georgia — 1.4% |

| Bank of Georgia JSC: | | | |

| 9.50% to 7/16/29(1)(3)(6) | USD | 205 | $ 200,336 |

| 9.50% to 7/16/29(2)(3)(6) | USD | 13,175 | 12,864,597 |

| TBC Bank JSC: | | | |

| 8.894% to 11/6/26(2)(3)(6) | USD | 7,668 | 7,368,948 |

| 10.25% to 7/30/29(2)(3)(6) | USD | 13,150 | 12,933,979 |

| | | | $ 33,367,860 |

| Ghana — 0.4% |

| Kosmos Energy Ltd., 7.50%, 3/1/28(2) | USD | 3,505 | $ 3,385,358 |

| Tullow Oil PLC, 10.25%, 5/15/26(2) | USD | 6,207 | 5,998,591 |

| | | | $ 9,383,949 |

| Greece — 0.9% |

| Piraeus Financial Holdings SA: | | | |

| 7.25% to 1/17/29, 4/17/34(2)(3) | EUR | 6,153 | $ 7,160,679 |

| 8.75% to 6/16/26(2)(3)(6) | EUR | 13,671 | 15,093,382 |

| | | | $ 22,254,061 |

| Hong Kong — 0.8% |

| CAS Capital No. 1 Ltd., 4.00% to 7/12/26(2)(3)(6) | USD | 5,900 | $ 5,595,118 |

| Yuexiu REIT MTN Co. Ltd., 2.65%, 2/2/26(2) | USD | 13,542 | 12,530,673 |

| | | | $ 18,125,791 |

| Hungary — 0.5% |

| MBH Bank Nyrt, 8.625% to 10/19/26, 10/19/27(2)(3) | EUR | 6,343 | $ 7,263,894 |

| OTP Bank Nyrt, 8.75% to 2/15/28, 5/15/33(2)(3) | USD | 4,622 | 4,863,158 |

| | | | $ 12,127,052 |

| India — 0.9% |

| Piramal Capital & Housing Finance Ltd., 7.80%, 1/29/28(2) | USD | 6,940 | $ 6,987,396 |

| Vedanta Resources Finance II PLC, 13.875%, 12/9/28(2) | USD | 14,591 | 14,585,778 |

| | | | $ 21,573,174 |

| Indonesia — 0.9% |

| Indika Energy Tbk. PT, 8.75%, 5/7/29(1) | USD | 13,060 | $ 13,273,936 |

| LLPL Capital Pte. Ltd., 6.875%, 2/4/39(2) | USD | 8,075 | 8,216,847 |

| | | | $ 21,490,783 |

| Security | Principal

Amount

(000's omitted) | Value |

| Jamaica — 0.8% |

| Digicel Intermediate Holdings Ltd./Digicel International Finance Ltd./DIFL U.S., 12.00%, (9.00% cash and 3.00% PIK), 5/25/27 | USD | 18,553 | $ 18,436,263 |

| | | | $ 18,436,263 |

| Kazakhstan — 0.7% |

| Development Bank of Kazakhstan JSC, 13.00%, 4/15/27(1) | KZT | 7,365,500 | $ 15,515,496 |

| | | | $ 15,515,496 |

| Latvia — 0.1% |

| Air Baltic Corp. AS, 14.50%, 8/14/29(1) | EUR | 2,030 | $ 2,330,864 |

| | | | $ 2,330,864 |

| Luxembourg — 0.6% |

| FORESEA Holding SA, 7.50%, 6/15/30(2) | USD | 15,793 | $ 14,718,259 |

| | | | $ 14,718,259 |

| Mexico — 1.2% |

| Alpha Holding SA de CV: | | | |

| 9.00%, 2/10/25(2)(8) | USD | 8,785 | $ 48,056 |

| 10.00%, 12/19/22(2)(8) | USD | 5,495 | 82,418 |

| BBVA Bancomer SA: | | | |

| 5.125% to 1/17/28, 1/18/33(2)(3) | USD | 9,044 | 8,432,359 |

| 8.45% to 6/29/33, 6/29/38(1)(3) | USD | 1,046 | 1,105,178 |

| Grupo Kaltex SA de CV, 14.50%, (13.00% cash and 1.50% PIK), 9/30/25(1) | USD | 7,480 | 5,910,771 |

| Petroleos Mexicanos, 7.19%, 9/12/24(1) | MXN | 1,420 | 75,780 |

| Total Play Telecomunicaciones SA de CV: | | | |

| 6.375%, 9/20/28(2) | USD | 7,037 | 4,315,591 |

| 10.50%, 12/31/28(1) | USD | 9,099 | 7,651,986 |

| | | | $ 27,622,139 |

| Moldova — 0.2% |

| Aragvi Finance International DAC, 8.45%, 4/29/26(2) | USD | 6,297 | $ 5,652,691 |

| | | | $ 5,652,691 |

| Nigeria — 0.3% |

| Access Bank PLC, 6.125%, 9/21/26(2) | USD | 6,321 | $ 6,020,752 |

| | | | $ 6,020,752 |

2

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Panama — 0.4% |

| AES Panama Generation Holdings SRL, 4.375%, 5/31/30(2) | USD | 11,053 | $ 9,763,551 |

| | | | $ 9,763,551 |

| Paraguay — 0.4% |

| Frigorifico Concepcion SA: | | | |

| 7.70%, 7/21/28(2) | USD | 5,798 | $ 3,536,466 |

| 7.70%, 7/21/28(1) | USD | 7,960 | 4,855,170 |

| | | | $ 8,391,636 |

| Peru — 1.2% |

| Auna SA, 10.00%, 12/15/29(1) | USD | 15,398 | $ 15,865,778 |

| Peru LNG SRL, 5.375%, 3/22/30(2) | USD | 7,489 | 6,597,851 |

| Telefonica del Peru SAA, 7.375%, 4/10/27(2) | PEN | 26,000 | 5,362,567 |

| | | | $ 27,826,196 |

| Russia — 0.0% |

| Tinkoff Bank JSC Via TCS Finance Ltd., 6.00% to 12/20/26(2)(3)(6)(8)(10) | USD | 4,509 | $ 0 |

| | | | $ 0 |

| Singapore — 0.3% |

| Puma International Financing SA, 7.75%, 4/25/29(1) | USD | 6,673 | $ 6,770,125 |

| | | | $ 6,770,125 |

| Supranational — 0.4% |

| European Bank for Reconstruction & Development: | | | |

| 17.20%, 4/9/26(2) | USD | 6,300 | $ 6,348,183 |

| 17.35%, 3/1/27(2) | USD | 2,300 | 2,278,628 |

| International Finance Corp., 16.00%, 2/21/25 | UZS | 19,000,000 | 1,487,382 |

| | | | $ 10,114,193 |

| Trinidad and Tobago — 0.1% |

| Telecommunications Services of Trinidad & Tobago Ltd., 8.875%, 10/18/29(2) | USD | 1,412 | $ 1,409,960 |

| | | | $ 1,409,960 |

| Tunisia — 0.0%(9) |

| Tunisian Republic, 3.28%, 8/9/27 | JPY | 200,000 | $ 1,016,771 |

| | | | $ 1,016,771 |

| Turkey — 1.1% |

| Eregli Demir ve Celik Fabrikalari TAS, 8.375%, 7/23/29(2) | USD | 8,783 | $ 8,873,219 |

| Security | Principal

Amount

(000's omitted) | Value |

| Turkey (continued) |

| Limak Iskenderun Uluslararasi Liman Isletmeciligi AS, 9.50%, 7/10/36(2) | USD | 7,891 | $ 7,328,638 |

| WE Soda Investments Holding PLC, 9.50%, 10/6/28(2) | USD | 9,325 | 9,602,195 |

| | | | $ 25,804,052 |

| United Arab Emirates — 0.5% |

| Ittihad International Ltd., 9.75%, 11/9/28(2) | USD | 11,130 | $ 11,456,944 |

| | | | $ 11,456,944 |

| United Kingdom — 0.7% |

| Avianca Midco 2 PLC: | | | |

| 9.00%, 12/1/28(2) | USD | 4,220 | $ 4,134,679 |

| 9.00%, 12/1/28(2) | USD | 11,851 | 11,613,050 |

| | | | $ 15,747,729 |

| Uzbekistan — 2.1% |

| Ipoteka-Bank ATIB: | | | |

| 5.50%, 11/19/25(2) | USD | 576 | $ 560,115 |

| 20.50%, 4/25/27(2) | UZS | 256,750,000 | 20,232,394 |

| Uzbek Industrial & Construction Bank ATB, 21.00%, 7/24/27(2) | UZS | 370,880,000 | 29,566,067 |

| | | | $ 50,358,576 |

| Venezuela — 0.8% |

| Petroleos de Venezuela SA: | | | |

| 5.375%, 4/12/27(2)(8) | USD | 35,423 | $ 4,028,884 |

| 5.50%, 4/12/37(2)(8) | USD | 12,934 | 1,455,019 |

| 6.00%, 10/28/22(2)(8) | USD | 9,482 | 948,196 |

| 6.00%, 5/16/24(2)(8) | USD | 35,278 | 4,162,812 |

| 6.00%, 11/15/26(2)(8) | USD | 15,098 | 1,736,300 |

| 8.50%, 10/27/20(2)(8) | USD | 2,128 | 1,936,480 |

| 9.00%, 11/17/21(2)(8) | USD | 16,078 | 1,937,399 |

| 9.75%, 5/17/35(2)(8) | USD | 18,355 | 2,294,354 |

| 12.75%, 2/17/22(2)(8) | USD | 10,019 | 1,377,640 |

| | | | $ 19,877,084 |

| Vietnam — 0.2% |

| Mong Duong Finance Holdings BV, 5.125%, 5/7/29(2) | USD | 5,591 | $ 5,375,501 |

| | | | $ 5,375,501 |

Total Foreign Corporate Bonds

(identified cost $649,778,912) | | | $ 624,328,228 |

3

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Loan Participation Notes — 0.9% |

| Security | Principal

Amount

(000's omitted) | Value |

| Uzbekistan — 0.9% |

| Daryo Finance BV (borrower - Uzbek Industrial and Construction Bank ATB), 18.75%, 6/15/25(2)(10)(11) | UZS | 86,016,955 | $ 6,898,940 |

| Europe Asia Investment Finance BV (borrower - Joint Stock Commercial Bank “Asaka”), 18.70%, 7/21/26(2)(10)(11) | UZS | 197,697,150 | 15,718,251 |

Total Loan Participation Notes

(identified cost $23,724,315) | | | $ 22,617,191 |

| Senior Floating-Rate Loans — 5.2%(12) |

| Borrower/Description | Principal

Amount

(000's omitted) | Value |

| Argentina — 0.5% |

| Provincia De Neuquen: | | | |

| Term Loan, 11/1/27(13) | $ | 3,282 | $ 3,347,257 |

| Term Loan, 11/1/27(13) | | 3,926 | 4,004,753 |

| Term Loan, 11/28/27(13) | | 3,548 | 3,583,871 |

| | | | $ 10,935,881 |

| Bahamas — 1.0% |

| Commonwealth of the Bahamas, Term Loan, 10.512%, (3 mo. EURIBOR + 6.85%), 11/24/28 | EUR | 21,080 | $ 22,813,828 |

| | | | $ 22,813,828 |

| Luxembourg — 0.1% |

| Zacapa SARL, Term Loan, 9.335%, (SOFR + 4.00%), 3/22/29 | $ | 2,346 | $ 2,348,058 |

| | | | $ 2,348,058 |

| Paraguay — 0.6% |

| Frigorifico Concepcion SA, Term Loan, 10.834%, (SOFR + 5.50%), 12/8/26 | $ | 14,610 | $ 14,756,100 |

| | | | $ 14,756,100 |

| Saint Lucia — 0.4% |

| Digicel International Finance Ltd., Term Loan, 12.002%, (SOFR + 6.75%), 5/25/27 | $ | 8,959 | $ 8,696,285 |

| | | | $ 8,696,285 |

| Borrower/Description | Principal

Amount

(000's omitted) | Value |

| Tanzania — 2.2% |

| HTA Group Ltd.: | | | |

| Term Loan, 9/13/28(13) | $ | 1,740 | $ 1,735,650 |

| Term Loan, 9/13/28(13) | | 10,645 | 10,618,387 |

| Tanzania, Term Loan, 10.696%, (SOFR + 5.45%), 2/27/31 | | 40,200 | 39,948,750 |

| | | | $ 52,302,787 |

| Uzbekistan — 0.4% |

| Navoi Mining & Metallurgical Co., Term Loan, 10.065%, (SOFR + 4.76%), 4/23/27 | $ | 10,575 | $ 10,564,650 |

| | | | $ 10,564,650 |

Total Senior Floating-Rate Loans

(identified cost $122,524,210) | | | $ 122,417,589 |

| Sovereign Government Bonds — 43.6% |

| Security | Principal

Amount

(000's omitted) | Value |

| Albania — 1.3% |

| Albania Government International Bonds: | | | |

| 3.50%, 6/16/27(2) | EUR | 154 | $ 161,890 |

| 3.50%, 11/23/31(2) | EUR | 447 | 440,182 |

| 5.90%, 6/9/28(2) | EUR | 10,009 | 11,172,296 |

| Albanian Government Bonds: | | | |

| 4.30%, 7/10/27 | ALL | 289,500 | 3,167,928 |

| 4.70%, 2/23/27 | ALL | 141,600 | 1,566,093 |

| 4.95%, 7/22/29 | ALL | 393,800 | 4,317,643 |

| 5.25%, 1/26/29 | ALL | 883,700 | 9,829,963 |

| | | | $ 30,655,995 |

| Angola — 2.3% |

| Angola Government International Bonds: | | | |

| 8.75%, 4/14/32(2) | USD | 12,575 | $ 11,274,292 |

| 9.125%, 11/26/49(2) | USD | 30,596 | 25,304,972 |

| 9.375%, 5/8/48(2) | USD | 20,368 | 17,172,363 |

| | | | $ 53,751,627 |

| Argentina — 0.2% |

| Bonos Para La Reconstruccion De Una Argentina Libre, 3.00%, 5/31/26 | USD | 7,343 | $ 5,445,072 |

| | | | $ 5,445,072 |

4

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Armenia — 1.6% |

| Republic of Armenia Treasury Bonds: | | | |

| 9.00%, 4/29/26 | AMD | 376,680 | $ 971,340 |

| 9.25%, 4/29/28 | AMD | 3,206,460 | 8,219,491 |

| 9.60%, 10/29/33 | AMD | 9,310,190 | 24,114,213 |

| 9.75%, 10/29/50 | AMD | 884,427 | 2,307,373 |

| 9.75%, 10/29/52 | AMD | 953,900 | 2,480,185 |

| | | | $ 38,092,602 |

| Bahamas — 0.4% |

| Bahamas Government International Bonds: | | | |

| 6.00%, 11/21/28(2) | USD | 5,831 | $ 5,393,673 |

| 8.95%, 10/15/32(2) | USD | 4,571 | 4,536,362 |

| | | | $ 9,930,035 |

| Benin — 2.7% |

| Benin Government International Bonds: | | | |

| 4.875%, 1/19/32(2) | EUR | 15,252 | $ 14,084,357 |

| 4.95%, 1/22/35(2) | EUR | 27,686 | 23,973,758 |

| 6.875%, 1/19/52(2) | EUR | 25,541 | 21,991,979 |

| 7.96%, 2/13/38(2) | USD | 4,190 | 3,915,686 |

| | | | $ 63,965,780 |

| Bosnia and Herzegovina — 0.0%(9) |

| Republic of Srpska Treasury Bonds: | | | |

| 1.50%, 6/9/25 | BAM | 10 | $ 5,357 |

| 1.50%, 9/25/26 | BAM | 126 | 69,934 |

| | | | $ 75,291 |

| Cameroon — 2.9% |

| Republic of Cameroon International Bonds: | | | |

| 5.95%, 7/7/32(2) | EUR | 13,391 | $ 11,415,362 |

| 9.50%, 7/31/31(2) | USD | 58,254 | 55,851,023 |

| | | | $ 67,266,385 |

| Colombia — 1.3% |

| Titulos De Tesoreria B: | | | |

| 2.25%, 4/18/29 | COP | 14,605,906 | $ 3,157,105 |

| 3.00%, 3/25/33 | COP | 31,398,577 | 6,451,233 |

| 3.75%, 2/25/37 | COP | 79,999,916 | 16,321,663 |

| 4.75%, 4/4/35 | COP | 23,100,176 | 5,278,402 |

| | | | $ 31,208,403 |

| Security | Principal

Amount

(000's omitted) | Value |

| Dominican Republic — 4.3% |

| Dominican Republic Bonds: | | | |

| 8.00%, 1/15/27(2) | DOP | 50,040 | $ 786,322 |

| 8.00%, 2/12/27(2) | DOP | 255,750 | 4,023,829 |

| 10.75%, 6/1/36(1) | DOP | 2,449,050 | 42,400,079 |

| 11.25%, 9/15/35(1) | DOP | 176,600 | 3,143,782 |

| 11.25%, 9/15/35(2) | DOP | 164,200 | 2,923,041 |

| 12.00%, 8/8/25(1) | DOP | 209,200 | 3,569,508 |

| 12.75%, 9/23/29(1) | DOP | 494,600 | 9,253,738 |

| 13.00%, 6/10/34(2) | DOP | 421,100 | 8,366,211 |

| 13.625%, 2/3/33(2) | DOP | 63,350 | 1,262,592 |

| 13.625%, 2/3/33(1) | DOP | 461,150 | 9,190,912 |

| Dominican Republic Central Bank Notes: | | | |

| 8.00%, 3/12/27(2) | DOP | 17,280 | 274,392 |

| 12.00%, 10/3/25(1) | DOP | 634,070 | 10,836,304 |

| 13.00%, 12/5/25(1) | DOP | 53,380 | 914,351 |

| 13.00%, 1/30/26(1) | DOP | 209,070 | 3,589,287 |

| | | | $ 100,534,348 |

| Ecuador — 1.8% |

| Ecuador Government International Bonds: | | | |

| 0.00%, 7/31/30(2) | USD | 33,230 | $ 17,090,236 |

| 2.50%, 7/31/40(2) | USD | 800 | 324,449 |

| 2.50%, 7/31/40(2) | USD | 2,515 | 1,019,909 |

| 2.50%, 7/31/40(2) | USD | 1,538 | 623,770 |

| 2.50%, 7/31/40(2) | USD | 3,451 | 1,399,418 |

| 2.50%, 7/31/40(2) | USD | 1,640 | 665,158 |

| 5.00%, 7/31/40(2) | USD | 410 | 166,290 |

| 5.00%, 7/31/40(2) | USD | 182 | 73,906 |

| 6.90%, 7/31/30(2) | USD | 29,308 | 19,904,679 |

| | | | $ 41,267,815 |

| Ethiopia — 1.6% |

| Ethiopia International Bonds, 6.625%, 12/11/24(2)(8) | USD | 47,270 | $ 37,328,055 |

| | | | $ 37,328,055 |

| Ghana — 1.8% |

| Ghana Government International Bonds: | | | |

| 6.375%, 2/11/27(2)(8) | USD | 4,711 | $ 2,372,990 |

| 7.625%, 5/16/29(2)(8) | USD | 14,034 | 7,112,080 |

| 7.75%, 4/7/29(2)(8) | USD | 6,711 | 3,411,285 |

| 7.875%, 3/26/27(2)(8) | USD | 1,893 | 962,283 |

| 7.875%, 2/11/35(2)(8) | USD | 7,357 | 3,768,715 |

| 8.125%, 1/18/26(2)(8) | USD | 4,030 | 2,085,557 |

| 8.125%, 3/26/32(2)(8) | USD | 7,573 | 3,890,629 |

5

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Ghana (continued) |

| Ghana Government International Bonds: (continued) | | | |

| 8.625%, 4/7/34(2)(8) | USD | 10,300 | $ 5,295,410 |

| 8.627%, 6/16/49(2)(8) | USD | 5,115 | 2,584,482 |

| 8.75%, 3/11/61(2)(8) | USD | 9,282 | 4,791,788 |

| 8.875%, 5/7/42(2)(8) | USD | 4,509 | 2,306,849 |

| 8.95%, 3/26/51(2)(8) | USD | 9,392 | 4,849,794 |

| | | | $ 43,431,862 |

| Indonesia — 2.3% |

| Indonesia Treasury Bonds: | | | |

| 6.625%, 2/15/34 | IDR | 246,872,000 | $ 14,881,174 |

| 7.125%, 6/15/43 | IDR | 541,600,000 | 33,540,229 |

| 7.375%, 5/15/48 | IDR | 86,457,000 | 5,451,417 |

| | | | $ 53,872,820 |

| Ivory Coast — 0.8% |

| Ivory Coast Government International Bonds: | | | |

| 6.625%, 3/22/48(2) | EUR | 10,967 | $ 9,272,500 |

| 6.875%, 10/17/40(2) | EUR | 4,106 | 3,736,139 |

| 8.25%, 1/30/37(2) | USD | 5,338 | 5,175,266 |

| | | | $ 18,183,905 |

| Jordan — 0.1% |

| Jordan Government International Bonds, 7.50%, 1/13/29(2) | USD | 2,747 | $ 2,735,220 |

| | | | $ 2,735,220 |

| Kenya — 1.3% |

| Republic of Kenya Government International Bonds: | | | |

| 8.25%, 2/28/48(2) | USD | 4,448 | $ 3,438,838 |

| 9.75%, 2/16/31(2) | USD | 28,061 | 26,769,955 |

| | | | $ 30,208,793 |

| Mexico — 0.2% |

| Mexican Bonos, 4.50%, 11/22/35 | MXN | 105,140 | $ 5,322,444 |

| | | | $ 5,322,444 |

| Paraguay — 0.7% |

| Paraguay Government Bonds, 7.90%, 2/9/31(1) | PYG | 113,186,000 | $ 15,538,420 |

| | | | $ 15,538,420 |

| Peru — 3.3% |

| Peru Government Bonds: | | | |

| 5.40%, 8/12/34 | PEN | 95,245 | $ 22,731,109 |

| Security | Principal

Amount

(000's omitted) | Value |

| Peru (continued) |

| Peru Government Bonds: (continued) | | | |

| 6.15%, 8/12/32 | PEN | 47,974 | $ 12,479,485 |

| 6.90%, 8/12/37 | PEN | 66,253 | 17,258,744 |

| 7.60%, 8/12/39(1)(2) | PEN | 94,299 | 25,836,662 |

| | | | $ 78,306,000 |

| Serbia — 3.1% |

| Serbia Treasury Bonds: | | | |

| 4.50%, 8/20/32 | RSD | 1,479,890 | $ 13,099,113 |

| 7.00%, 10/26/31 | RSD | 5,859,780 | 60,045,325 |

| | | | $ 73,144,438 |

| Seychelles — 0.0%(9) |

| Seychelles International Bonds, 8.00%, 1/1/26(2) | USD | 53 | $ 53,634 |

| | | | $ 53,634 |

| Sri Lanka — 2.2% |

| Sri Lanka Government International Bonds: | | | |

| 5.75%, 4/18/23(2)(8) | USD | 7,778 | $ 4,335,722 |

| 5.875%, 7/25/22(2)(8) | USD | 1,400 | 778,318 |

| 6.20%, 5/11/27(2)(8) | USD | 11,393 | 6,373,293 |

| 6.35%, 6/28/24(2)(8) | USD | 6,574 | 3,689,582 |

| 6.75%, 4/18/28(2)(8) | USD | 6,800 | 3,875,983 |

| 6.825%, 7/18/26(2)(8) | USD | 24,753 | 13,978,235 |

| 6.85%, 3/14/24(2)(8) | USD | 5,889 | 3,296,509 |

| 6.85%, 11/3/25(2)(8) | USD | 21,313 | 12,145,545 |

| 7.55%, 3/28/30(2)(8) | USD | 3,815 | 2,142,549 |

| | | | $ 50,615,736 |

| Suriname — 1.9% |

| Suriname Government International Bonds: | | | |

| 0.00%, Oil-Linked, 12/31/50(1) | USD | 17,170 | $ 15,109,600 |

| 7.95%, (4.95% cash and 3.00% PIK), 7/15/33(1) | USD | 31,253 | 30,315,853 |

| | | | $ 45,425,453 |

| Tajikistan — 0.0%(9) |

| Republic of Tajikistan International Bonds, 7.125%, 9/14/27(2) | USD | 565 | $ 545,258 |

| | | | $ 545,258 |

| Tunisia — 0.6% |

| Tunisian Republic: | | | |

| 3.50%, 2/3/33 | JPY | 600,000 | $ 2,510,603 |

| 4.20%, 3/17/31 | JPY | 30,000 | 138,505 |

6

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| Tunisia (continued) |

| Tunisian Republic: (continued) | | | |

| 5.75%, 1/30/25(2) | USD | 3,968 | $ 3,823,852 |

| 6.375%, 7/15/26(2) | EUR | 8,931 | 8,609,610 |

| | | | $ 15,082,570 |

| Turkey — 0.4% |

| Turkiye Government Bonds, 50.00% (TLREF), 5/17/28(4) | TRY | 329,380 | $ 9,886,120 |

| | | | $ 9,886,120 |

| Ukraine — 1.0% |

| Ukraine Government Bonds: | | | |

| 9.79%, 5/26/27 | UAH | 213,080 | $ 3,545,567 |

| 15.84%, 2/26/25 | UAH | 15,254 | 277,948 |

| 17.80%, 10/15/25 | UAH | 53,942 | 1,014,982 |

| 19.19%, 9/30/26 | UAH | 26,729 | 522,380 |

| Ukraine Government International Bonds: | | | |

| 4.375%, 1/27/32(2)(8) | EUR | 532 | 163,191 |

| 6.876%, 5/21/31(2)(8) | USD | 3,329 | 1,027,829 |

| 7.253%, 3/15/35(2)(8) | USD | 15,281 | 4,713,711 |

| 7.375%, 9/25/34(2)(8) | USD | 7,158 | 2,211,106 |

| 7.75%, 9/1/25(2)(8) | USD | 2,813 | 1,030,894 |

| 7.75%, 9/1/26(2)(8) | USD | 501 | 170,888 |

| 7.75%, 9/1/28(2)(8) | USD | 1,355 | 435,886 |

| 7.75%, 9/1/29(2)(8) | USD | 9,686 | 3,133,058 |

| 9.75%, 11/1/30(2)(8) | USD | 13,273 | 4,456,277 |

| | | | $ 22,703,717 |

| Uruguay — 1.1% |

| Uruguay Government Bonds: | | | |

| 3.40%, 5/16/45 | UYU | 287,812 | $ 7,070,327 |

| 3.875%, 7/2/40(14) | UYU | 399,396 | 10,421,739 |

| 9.75%, 7/20/33 | UYU | 350,216 | 8,768,429 |

| | | | $ 26,260,495 |

| Uzbekistan — 1.7% |

| National Bank of Uzbekistan, 19.875%, 7/5/27(2) | UZS | 175,670,000 | $ 13,909,940 |

| Republic of Uzbekistan Bonds: | | | |

| 16.25%, 10/12/26(2) | UZS | 181,050,000 | 14,680,607 |

| 16.625%, 5/29/27(2) | UZS | 90,000,000 | 7,171,469 |

| Republic of Uzbekistan International Bonds: | | | |

| 5.375%, 5/29/27(2) | EUR | 2,162 | 2,345,171 |

| 6.90%, 2/28/32(2) | USD | 3,005 | 2,948,420 |

| | | | $ 41,055,607 |

| Security | Principal

Amount

(000's omitted) | Value |

| Venezuela — 0.7% |

| Venezuela Government International Bonds: | | | |

| 6.00%, 12/9/20(2)(8) | USD | 13,632 | $ 1,832,704 |

| 7.00%, 3/31/38(2)(8) | USD | 4,210 | 613,641 |

| 7.65%, 4/21/25(2)(8) | USD | 8,539 | 1,336,123 |

| 7.75%, 10/13/19(2)(8) | USD | 15,543 | 2,256,114 |

| 8.25%, 10/13/24(2)(8) | USD | 12,954 | 2,026,057 |

| 9.00%, 5/7/23(2)(8) | USD | 2,387 | 375,139 |

| 9.25%, 9/15/27(8) | USD | 12,824 | 2,349,900 |

| 9.25%, 5/7/28(2)(8) | USD | 14,255 | 2,468,859 |

| 9.375%, 1/13/34(8) | USD | 976 | 190,234 |

| 11.75%, 10/21/26(2)(8) | USD | 5,305 | 980,222 |

| 11.95%, 8/5/31(2)(8) | USD | 5,917 | 1,078,414 |

| 12.75%, 8/23/22(2)(8) | USD | 6,018 | 1,082,919 |

| | | | $ 16,590,326 |

| Zambia — 0.0%(9) |

| Zambia Government International Bonds, 5.75% to 6/30/31, 6/30/33(2)(15) | USD | 15 | $ 13,155 |

| | | | $ 13,155 |

Total Sovereign Government Bonds

(identified cost $993,966,018) | | | $1,028,497,381 |

| Borrower/Description | Principal

Amount

(000's omitted) | Value |

| Ivory Coast — 0.1% |

| Republic of Ivory Coast, Term Loan, 9.426%, (6 mo. EURIBOR + 5.75%), 1/6/28(4) | EUR | 735 | $ 849,870 |

| | | | $ 849,870 |

| Kenya — 0.0%(9) |

| Government of Kenya, Term Loan, 12.142%, (6 mo. SOFR + 6.45%), 6/29/25(4) | USD | 391 | $ 394,725 |

| | | | $ 394,725 |

7

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Borrower/Description | Principal

Amount

(000's omitted) | Value |

| Tanzania — 1.1% |

| Government of the United Republic of Tanzania, Term Loan, 12.022%, (6 mo. SOFR + 6.30%), 4/28/31(4) | USD | 25,748 | $ 26,159,764 |

| | | | $ 26,159,764 |

Total Sovereign Loans

(identified cost $27,000,180) | | | $ 27,404,359 |

| Security | Shares | Value |

| Financial Intermediaries — 0.0%(9) |

| Alpha Holding SA, Escrow Certificates(10)(16) | | 9,319,000 | $ 0 |

Total Miscellaneous

(identified cost $0) | | | $ 0 |

| Short-Term Investments — 14.6% |

| Security | Shares | Value |

| Morgan Stanley Institutional Liquidity Funds - Government Portfolio, Institutional Class, 5.21%(17) | | 86,614,587 | $ 86,614,587 |

Total Affiliated Fund

(identified cost $86,614,587) | | | $ 86,614,587 |

| Sovereign Government Securities — 8.9% |

| Security | Principal

Amount

(000's omitted) | Value |

| Egypt — 4.9% |

| Egypt Treasury Bills: | | | |

| 0.00%, 8/6/24 | EGP | 137,100 | $ 2,822,602 |

| 0.00%, 8/6/24 | EGP | 614,000 | 12,640,977 |

| 0.00%, 9/10/24 | EGP | 1,814,725 | 36,436,752 |

| 0.00%, 12/3/24 | EGP | 261,300 | 4,955,154 |

| 0.00%, 12/10/24 | EGP | 1,004,725 | 18,964,406 |

| 0.00%, 12/17/24 | EGP | 1,244,375 | 23,379,254 |

| 0.00%, 3/11/25 | EGP | 817,525 | 14,555,896 |

| 0.00%, 3/18/25 | EGP | 158,350 | 2,807,172 |

| | | | $ 116,562,213 |

| Security | Principal

Amount

(000's omitted) | Value |

| Nigeria — 3.4% |

| Nigeria OMO Bills: | | | |

| 0.00%, 1/28/25 | NGN | 1,676,448 | $ 918,515 |

| 0.00%, 2/25/25 | NGN | 2,798,096 | 1,500,547 |

| 0.00%, 4/1/25 | NGN | 8,326,542 | 4,438,667 |

| 0.00%, 5/20/25 | NGN | 27,576,817 | 13,872,319 |

| 0.00%, 5/27/25 | NGN | 32,731,995 | 16,377,554 |

| 0.00%, 6/10/25 | NGN | 1,121,950 | 554,242 |

| 0.00%, 6/17/25 | NGN | 15,822,539 | 7,790,380 |

| Nigeria Treasury Bills: | | | |

| 0.00%, 2/6/25 | NGN | 3,549,468 | 1,931,003 |

| 0.00%, 2/20/25 | NGN | 15,581,382 | 8,387,553 |

| 0.00%, 3/6/25 | NGN | 8,658,262 | 4,611,665 |

| 0.00%, 3/27/25 | NGN | 22,042,230 | 11,554,702 |

| 0.00%, 4/10/25 | NGN | 14,161,750 | 7,345,001 |

| | | | $ 79,282,148 |

| Pakistan — 0.6% |

| Pakistan Treasury Bills: | | | |

| 0.00%, 8/8/24 | PKR | 304,000 | $ 1,085,997 |

| 0.00%, 8/8/24 | PKR | 304,000 | 1,085,997 |

| 0.00%, 8/8/24 | PKR | 151,800 | 542,284 |

| 0.00%, 8/8/24 | PKR | 911,000 | 3,254,419 |

| 0.00%, 8/8/24 | PKR | 227,800 | 813,783 |

| 0.00%, 8/22/24 | PKR | 595,000 | 2,109,756 |

| 0.00%, 8/22/24 | PKR | 525,100 | 1,861,904 |

| 0.00%, 11/14/24 | PKR | 607,700 | 2,064,244 |

| 0.00%, 11/14/24 | PKR | 212,000 | 720,125 |

| | | | $ 13,538,509 |

Total Sovereign Government Securities

(identified cost $223,382,460) | | | $ 209,382,870 |

| U.S. Treasury Obligations — 2.0% |

| Security | Principal

Amount

(000's omitted) | Value |

| U.S. Treasury Bills: | | | |

| 0.00%, 8/1/24 | $ | 10,000 | $ 10,000,000 |

| 0.00%, 8/22/24 | | 2,680 | 2,671,761 |

| 0.00%, 9/5/24(18) | | 2,622 | 2,608,561 |

| 0.00%, 10/10/24(18) | | 22,698 | 22,470,263 |

8

See Notes to Financial Statements.

Eaton Vance

Emerging Markets Debt Opportunities Fund

July 31, 2024

Portfolio of Investments — continued

| Security | Principal

Amount

(000's omitted) | Value |

| U.S. Treasury Bills: (continued) | | | |

| 0.00%, 10/24/24 | $ | 10,000 | $ 9,880,207 |

Total U.S. Treasury Obligations

(identified cost $47,629,175) | | | $ 47,630,792 |

Total Short-Term Investments

(identified cost $357,626,222) | | | $ 343,628,249 |

| | | |

Total Purchased Options — 0.0%(9)

(identified cost $721,745) | | | $ 459,352 |

Total Investments — 92.6%

(identified cost $2,190,364,634) | | | $2,183,691,396 |

| Other Assets, Less Liabilities — 7.4% | | | $ 174,236,443 |

| Net Assets — 100.0% | | | $2,357,927,839 |

| The percentage shown for each investment category in the Portfolio of Investments is based on net assets. |

| (1) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in certain transactions in reliance on an exemption from registration (normally to qualified institutional buyers). At July 31, 2024, the aggregate value of these securities is $314,744,805 or 13.3% of the Fund's net assets. |

| (2) | Security exempt from registration under Regulation S of the Securities Act of 1933, as amended, which exempts from registration securities offered and sold outside the United States. Security may not be offered or sold in the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933, as amended. At July 31, 2024, the aggregate value of these securities is $1,023,401,083 or 43.4% of the Fund's net assets. |

| (3) | Security converts to variable rate after the indicated fixed-rate coupon period. |

| (4) | Variable rate security. The stated interest rate represents the rate in effect at July 31, 2024. |

| (5) | Represents a payment-in-kind security which may pay interest in additional principal at the issuer’s discretion. |

| (6) | Perpetual security with no stated maturity date but may be subject to calls by the issuer. |

| (7) | Variable rate security whose coupon rate is linked to the issuer’s mining activity revenue. The coupon rate shown represents the rate in effect at July 31, 2024. |

| (8) | Issuer is in default with respect to interest and/or principal payments and is non-income producing. |

| (9) | Amount is less than 0.05%. |

| (10) | For fair value measurement disclosure purposes, security is categorized as Level 3 (see Note 11). |

| (11) | Limited recourse note whose payments by the issuer are limited to amounts received by the issuer from the borrower pursuant to a loan agreement with the borrower. |

| (12) | Senior floating-rate loans (Senior Loans) often require prepayments from excess cash flows or permit the borrowers to repay at their election. The degree to which borrowers repay, whether as a contractual requirement or at their election, cannot be predicted with accuracy. As a result, the actual remaining maturity may be substantially less than the stated maturities shown. However, Senior Loans will typically have an expected average life of approximately two to four years. Senior Loans typically have rates of interest which are redetermined periodically by reference to a base lending rate, plus a spread. These base lending rates are primarily the Secured Overnight Financing Rate (“SOFR”) and secondarily, the prime rate offered by one or more major United States banks (the “Prime Rate”). Base lending rates may be subject to a floor, or minimum rate. Rates for SOFR are generally 1 or 3-month tenors and may also be subject to a credit spread adjustment. Senior Loans are generally subject to contractual restrictions that must be satisfied before they can be bought or sold. |

| (13) | This Senior Loan will settle after July 31, 2024, at which time the interest rate will be determined. |