UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2013

or

| ☐ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number: 001-35629

TILE SHOP HOLDINGS,INC.

(Exact name of registrant as specified in its charter)

Delaware | 45-5538095 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

14000 Carlson Parkway, Plymouth, Minnesota 55441

(Address of principal executive offices, including zip code)

(763) 852-2901

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, $0.0001 par value | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form -10K or any amendment to this Form 10K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12-b2 of the Exchange Act.

Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately: $1,118,716,430

At February 21, 2014, the registrant had 51,230,600 shares of Common Stock outstanding.

TILE SHOP HOLDINGS, INC.

FORM 10-K

TABLE OF CONTENTS

PART��I | | | |

| | ITEM 1. | BUSINESS | 3 |

| | ITEM 1A. | RISK FACTORS | 6 |

| | ITEM 1B. | UNRESOLVED STAFF COMMENTS | 14 |

| | ITEM 2. | PROPERTIES | 14 |

| | ITEM 3. | LEGAL PROCEEDINGS | 15 |

| | ITEM 4. | MINE SAFETY DISCLOSURES | 15 |

| | | | |

PART II | | | |

| | ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERSAND ISSUER PURCHASES OF EQUITY SECURITIES | 16 |

| | ITEM 6. | SELECTED FINANCIAL DATA | 18 |

| | ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OFOPERATIONS | 19 |

| | ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 27 |

| | ITEM 8. | CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 28 |

| | ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING ANDFINANCIAL DISCLOSURE | 28 |

| | ITEM 9A. | CONTROLS AND PROCEDURES | 28 |

| | ITEM 9B. | OTHER INFORMATION | 29 |

| | | | |

PART III | | | |

| | ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 30 |

| | ITEM 11. | EXECUTIVE COMPENSATION | 34 |

| | ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT ANDRELATED STOCKHOLDER MATTERS | 43 |

| | ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 45 |

| | ITEM 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 49 |

| | | | |

PART IV | | | |

| ITEM 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 51 |

| | | |

SIGNATURES | 76 |

| | | |

POWER OF ATTORNEY | 77 |

PART I

ITEM 1. BUSINESS

Overview

We are a specialty retailer of manufactured and natural stone tiles, setting and maintenance materials, and related accessories in the United States. We offer a wide selection of products, attractive prices, and exceptional customer service in an extensive showroom setting. We sell over 4,500 products from around the world, including ceramic, porcelain, glass, and stainless steel manufactured tiles and, marble, granite, quartz, sandstone, travertine, slate, and onyx natural tiles, primarily under our proprietary Rush River and Fired Earth brands. We purchase our tile products and accessories directly from producers. We manufacture our own setting and maintenance materials, such as thinset, grout, and sealers under our Superior brand name. As of December 31, 2013, we operated 88 stores in 28 states, with an average size of 23,000 square feet. We also sell our products on our website.

We believe that our long-term producer relationships, together with our design, manufacturing and distribution capabilities, enable us to offer a broad assortment of high-quality products to our customers, who are primarily homeowners, at competitive prices. We have invested significant resources to develop our proprietary brands and product sources and believe that we are a leading retailer of stone tiles, accessories, and related materials in the United States.

In 2013, we reported net sales and income from operations of $229.6 million and $33.1 million, respectively. We opened 20 new stores in 2013 and intend to open 20 stores in 2014. As of fiscal year end 2013, 2012 and 2011, we had total assets of $242.8 million, $176.1 million and $119.0 million, respectively.

Organizational History

Tile Shop Holdings, Inc. (“Holdings”, and together with its wholly owned subsidiaries, the “Company”) was incorporated in Delaware in June 2012. On August 21, 2012, Holdings consummated the transactions contemplated pursuant to that certain Contribution and Merger Agreement dated as of June 27, 2012, among Holdings, JWC Acquisition Corp., a publicly-held Delaware corporation (“JWCAC”), The Tile Shop, LLC, a privately-held Delaware limited liability company (“The Tile Shop”), and certain other parties. Through a series of transactions, The Tile Shop was contributed to and became a subsidiary of Holdings and Holdings effected a business combination with and became a successor issuer to JWCAC. These transactions are referred to herein as the “Business Combination.”

Competitive Strengths

We believe that the following factors differentiate us from our competitors and position us to continue to grow our specialty tile business.

Inspiring Customer ExperienceOur showrooms bring our products to life. Each showroom features up to 70 different mockups, or vignettes, of bathrooms, kitchens, fireplaces, foyers, and other settings that showcase our broad array of products. Each store also features over 1,400 hand- crafted display boards showing tile that we offer for sale. Our stores are spacious, well-lit, and organized by product type to make our customers’ shopping experience easy.

Broad Product Assortment at Attractive PricesWe offer over 4,500 manufactured and natural tile products, setting and maintenance materials, and accessories. We are able to maintain every-day low prices by purchasing tile and accessories directly from producers and manufacturing our own setting and maintenance materials.

Customer Service and SatisfactionOur sales personnel are highly-trained and knowledgeable about the technical and design aspects of our products. We offer weekly do-it-yourself classes in all of our showrooms. In addition, we provide one-on-one installation training as required to meet customer needs. We offer a liberal return policy, with no restocking fees.

Worldwide Sourcing CapabilitiesWe have long-standing relationships with producers of our tiles throughout the world and work with them to design products exclusively for us. We believe that these direct relationships differentiate us from our competitors, who generally purchase commodity products through distributors. We are often the largest or exclusive customer for many of our producers.

Proprietary BrandingWe sell the majority of our products under our proprietary brand names, which help us to differentiate our products from those of our competitors. We offer products across a range of price points and quality levels that allow us to target discrete market segments and to appeal to diverse groups of customers.

Centralized Distribution SystemWe service our retail locations from four distribution centers. Our distribution centers can cost-effectively service stores within a 700-mile radius, providing us with the ability to open new locations in markets where we believe that we have a competitive advantage or see attractive demographics.

Growth Strategy

We intend to increase our net sales and profitability through a combination of new store openings, store re-models and same store sales growth. In the five years ended December 31, 2013, we grew through a combination of opening 47 new retail locations and increases in same store sales. We expect to continue to gain market share. Specific elements of our strategy for continued growth include the following:

Open New StoresWe believe that the highly-fragmented U.S. retail tile market provides us with a significant opportunity to expand our store base. During 2013, we opened 20 new stores. We intend to open 20 new stores in 2014, in new markets and our existing markets, northeast, southeast, midwest, and mid-Atlantic regions of the United States. We believe that there will continue to be additional expansion opportunities in the United States. We expect our store base growth to increase operational efficiencies.

Increase Sales and Profitability of Existing StoresWe believe that our ongoing investment in new products, store re-models and training program for our sales associates, together with our associate incentive compensation structure, will result in continued same store sales growth.

Sales Model

We appeal to customers who desire high-quality products at an attractive value. We principally sell our products directly to homeowners. We also sell products to contractors, who are primarily small businesses that have been hired by homeowners to complete tile projects. We believe that due to the average cost and relative infrequency of a tile purchase, many of our customers conduct extensive research using multiple channels before making a purchase decision. Our sales strategy emphasizes customer service by providing comprehensive and convenient education tools on our website and in our stores for our customers to learn about our products and the tile installation process. Our website contains a broad range of information regarding our tile products, setting and maintenance materials, and accessories. Customers can order samples, view catalogs, or purchase products from either our stores or website. Customers can choose to have their purchases delivered or picked up at one of our stores. We strive to make our customers’ transactions easy and efficient.

Our stores are designed to emphasize our products in a visually appealing showroom format. Our typical store is approximately 23,000 square feet, with approximately 19,000 square feet devoted to the showroom and the balance being warehouse space, which is used primarily to hold customer orders waiting to be picked up or delivered. Our stores are typically accessible from major roadways and have significant visibility to passing traffic. We can adapt to a range of existing buildings, whether free-standing or in shopping centers.

Unlike many of our competitors, we devote a substantial portion of our retail store space to showrooms, including samples of our over 4,500 products and up to 70 different vignettes of bathrooms, kitchens, fireplaces, foyers, outdoor living, and other settings that showcase our products. Our showrooms are designed to provide our customers with a better understanding of how to integrate various types of tile in order to create an attractive presentation in their homes. Each store is also equipped with a consumer training center designed to teach customers how to properly install tile.

A typical store staff consists of a manager and 6 to 15 sales and warehouse associates. Our store managers are responsible for store operations and for overseeing our customers’ shopping experience. Our store associates have flexibility to meet or beat competitor pricing.

We offer financing to customers through a branded credit card provided by a third-party consumer finance company. These credit cards, which can only be used in our stores and on our website, provide customers with a 10% discount on all purchases. In 2013, approximately 6.3% of our sales were made using our branded credit card.

Marketing

We utilize a variety of methods to market to our customer base and attract new customers to our retail locations and website. We establish and maintain our market presence through strong execution of our in-store branding and execution, best-in-class and unique product assortment, personalized customer service, and attractive and competitive pricing. In addition, we are very active in social media and employ a dynamic, data-driven marketing approach that focuses on the most qualified customers that are actively researching our products. We also partner extensively with local and national designers as well as sponsoring nationally recognized home improvement shows. Our advertising expenditures largely fall into the above mentioned categories.

Our website is designed to educate consumers and to generate in-store and online sales. Visitors to our website can purchase our products directly as well as search a comprehensive knowledge base on tile, including frequently asked questions, installation guides, detailed product information, catalogs, and how-to videos that explain the installation process. Our website and social media efforts have also been devoted to building brand awareness, connecting with potential customers, and building relationships with satisfied customers.

Products

We offer a complete assortment of tile products, generally sourced directly from producers, including ceramic, porcelain, glass, and stainless steel manufactured tiles, marble, granite, quartz, sandstone, travertine, slate, and onyx natural tiles. We also offer a broad range of setting and maintenance materials, such as thinset, grout and sealers, and accessories, including installation tools, shower and bath caddies, drains, and similar products. We sell most of our products under our proprietary brand names. In total, we offer over 4,500 different tile, setting and maintenance materials, and accessory products. In 2013, our net sales were 52% from stone products, 32% from ceramic products, and 16% from setting and maintenance products. These amounts compare to 53% from stone products, 30% from ceramic products, and 17% from setting and maintenance products in 2012.

Manufacturers

We have long-standing relationships with manufacturers of our tiles throughout the world and work with them to design products exclusively for us. We believe that these direct relationships differentiate us from our competitors, who generally purchase commodity products through distributors. We are often the largest or exclusive customer for many of our suppliers, which we believe enables us to obtain better prices in some circumstances.

We currently purchase tile products from approximately 130 different producers. Our top 10 tile suppliers accounted for approximately 52% of our tile purchases in 2013. We believe that alternative and competitive suppliers are available for most of our products. In 2013, approximately 60% of our purchased product was sourced from Asia, 33% from Europe, 4% from North America and 3% from South America. Our foreign purchases are negotiated and paid for in U.S. dollars.

Distribution and Order Fulfillment

We take possession of our products in the country of origin and arrange for transportation to our distribution centers located in Wisconsin, Michigan, Virginia and Oklahoma. We maintain a large inventory of products in order to fulfill customer orders and minimize delays in delivery. We manufacture our setting and maintenance materials at our Wisconsin, Michigan, Virginia and Oklahoma locations.

We fulfill customer orders primarily by shipping our products to our stores where customers can either pick them up or arrange for home delivery. Orders placed on our website are shipped directly to customers’ homes from our distribution centers. We continue to evaluate logistics alternatives to best service our retail store base and our customers. We believe that our existing distribution facilities will continue to play an integral role in our growth strategy, and we expect to establish one or more additional distribution centers in the next five years to support geographic expansion of our retail store base.

Competition

The retail tile market is highly-fragmented. We compete directly with large national home centers that offer a wide range of home improvement products in addition to tile, such as Home Depot and Lowe’s; regional and local specialty retailers of tile, such as Tile America, World of Tile, Arizona Tile, Century Tile, and Floor and Décor; factory-direct stores, such as Dal-Tile and Florida Tile; and a large number of privately-owned, single-site stores. We also compete indirectly with companies that sell other types of floor coverings, including wood floors, carpet, and vinyl sheet. The barriers to entry into the retail tile industry are relatively low and new or existing tile retailers could enter our markets and increase the competition that we face. Many of our competitors enjoy competitive advantages over us, such as greater name recognition, longer operating histories, more varied product offerings, and greater financial, technical, and other resources.

We believe that the key competitive factors in the retail tile industry include:

| | • | immediacy of inventory; and |

We believe that we compete favorably with respect to each of these factors by providing a highly diverse selection of products to our customers, at an attractive value, in appealing and convenient retail store locations, with exceptional customer service and on-site instructional opportunities. Further, while some larger factory-direct competitors manufacture their own products, most of our competitors purchase their tile from domestic manufacturers or distributors when they receive an order from a customer. As a result, we believe that it takes these retailers longer than us to deliver products to customers and that their prices tend to be higher than our prices. We also believe that we offer a broader range of products and stronger in-store customer support than these competitors.

Employees

As of December 31, 2013, we had 1,214 employees, 1,200 of whom were full-time and none of whom were represented by a union. Of these employees, 834 work in our stores, 72 work in corporate, store support, infrastructure or similar functions, and 308 work in distribution and manufacturing facilities. We believe that we have good relations with our employees.

Property and Trademarks

We have registered and unregistered trademarks for all of our brands, including 15 registered marks and 2 pending trademark applications marks in the United States. We regard our intellectual property as having significant value and our brands are an important factor in the marketing of our products. Accordingly, we have taken, and continue to take, appropriate steps to protect our intellectual property.

Government Regulation

We are subject to extensive and varied federal, state and local government regulation in the jurisdictions in which we operate, including laws and regulations relating to our relationships with our employees, public health and safety, zoning, and fire codes. We operate each of our stores, offices, and distribution and manufacturing facilities in accordance with standards and procedures designed to comply with applicable laws, codes, and regulations.

Our operations and properties are also subject to federal, state and local laws and regulations relating to the use, storage, handling, generation, transportation, treatment, emission, release, discharge and disposal of hazardous materials, substances and wastes and relating to the investigation and cleanup of contaminated properties, including off-site disposal locations. We do not incur significant costs complying with environmental laws and regulations. However, we could be subject to material costs, liabilities, or claims relating to environmental compliance in the future, especially in the event of changes in existing laws and regulations or in their interpretation.

Products that we import into the United States are subject to laws and regulations imposed in conjunction with such importation, including those issued and/or enforced by U.S. Customs and Border Protection. We work closely with our suppliers to ensure compliance with the applicable laws and regulations in these areas.

Financial Information about Geographic Areas

All of our revenues are generated within the United States and all of our long-lived assets are located within the United States as well.

Available Information

We are subject to the reporting requirements of the Securities Exchange Act of 1934 and its rules and regulations (the “1934 Act”). The 1934 Act requires us to file periodic reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Copies of these reports, proxy statements and other information can be read and copied at the SEC Public Reference Room, 100 F Street, N.E., Washington D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a Web site that contains reports, proxy statements, and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s Web site at http://www.sec.gov.

We maintain a Web site atwww.tileshop.com, the contents of which are not part of or incorporated by reference into this Annual Report on Form 10-K. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and amendments to those reports available on our Web site, free of charge, as soon as reasonably practicable after such reports have been filed with or furnished to the SEC. Our Code of Business Conduct and Ethics, as well as any waivers from and amendments to the Code of Business Conduct and Ethics, are also posted on our Web site.

ITEM 1A. RISK FACTORS

The following are significant factors known to us that could adversely affect our business, financial condition, or operating results, as well as adversely affect the value of an investment in our common stock. These risks could cause our actual results to differ materially from our historical experience and from results predicted by forward-looking statements. All forward-looking statements made by us are qualified by the risks described below. There may be additional risks that are not presently material or known. You should carefully consider each of the following risks and all other information set forth in this Annual Report on Form 10-K.

Our business is dependent on general economic conditions in our markets.

Our revenues depend, in part, on discretionary spending by our customers. Pressure on discretionary income brought on by economic downturns and slow recoveries, including housing market declines, rising energy prices, and weak labor markets, may cause consumers to reduce the amount that they spend on discretionary items. If recovery from the current economic downturn continues to be slow or prolonged, our growth, prospects, results of operations, cash flows, and financial condition could be adversely impacted. General economic conditions and discretionary spending are beyond our control and are affected by, among other things:

| | • | consumer confidence in the economy; |

| | • | consumer credit availability; |

| | • | data security and privacy concerns; |

| | • | gasoline and fuel prices; |

| | • | interest rates and inflation; |

| | • | price deflation, including due to low-cost imports; |

| | • | slower rates of growth in real disposable personal income; |

| | • | natural disasters and unpredictable weather; |

| | • | national security concerns; |

| | • | tax rates and tax policy; and |

| | • | other matters that influence consumer confidence and spending. |

Increasing volatility in financial markets may cause some of the above factors to change with an even greater degree of frequency and magnitude than in the past.

Our ability to grow and remain profitable may be limited by direct or indirect competition in the retail tile industry, which is highly competitive.

The retail tile industry in the United States is highly competitive. Participants in the tile industry compete primarily based on product variety, customer service, store location, and price. There can be no assurance that we will be able to continue to compete favorably with our competitors in these areas. Our store competitors include large national home centers (such as Home Depot and Lowe’s), regional and local specialty retailers of tile (such as Tile America, World of Tile, Century Tile, and Floor and Décor), factory direct stores (such as Dal-Tile and Florida Tile) and privately-owned, single-site stores. We also compete indirectly with companies that sell other types of floor coverings, including wood floors, carpet, and vinyl sheet. In the past, we have faced periods of heightened competition that materially affected our results of operations. Certain of our competitors have greater name recognition, longer operating histories, more varied product offerings, and substantially greater financial and other resources than us. Accordingly, we may face periods of intense competition in the future that could have a material adverse effect on our planned growth and future results of operations. Moreover, the barriers to entry into the retail tile industry are relatively low. New or existing retailers could enter our markets and increase the competition that we face. In addition, manufacturers and vendors of tile and related products, including those whose products we currently sell, could enter the U.S. retail tile market and start directly competing with us. Competition in existing and new markets may also prevent or delay our ability to gain relative market share. Any of the developments described above could have a material adverse effect on our planned growth and future results of operations.

If we fail to successfully manage the challenges that our planned growth poses or encounter unexpected difficulties during our expansion, our revenues and profitability could be materially adversely affected.

One of our long term objectives is to increase revenues and profitability through market share leadership. Our ability to achieve market share leadership, however, is contingent upon our ability to open new stores and achieve operating results in new stores at the same level as our similarly situated current stores. There can be no assurance that we will be able to open stores in new markets at the rate required to achieve market leadership in such markets, identify and obtain favorable store sites, arrange favorable leases for stores, or obtain governmental and other third- party consents, permits, and licenses needed to open or operate stores in a timely manner, train and hire a sufficient number of qualified managers for new stores, attract a strong customer base and brand familiarity in new markets, or successfully compete with established retail tile stores in the new markets that we enter. Failure to open new stores in an effective and cost-efficient manner could place us at a competitive disadvantage as compared to retailers who are more adept than us at managing these challenges, which, in turn, could negatively affect our overall operating results.

Our same store sales fluctuate due to a variety of economic, operating, industry and environmental factors and may not be a fair indicator of our overall performance.

Our same store sales have experienced fluctuations, which can be expected to continue. Numerous factors affect our same store sales results, including among others, the timing of new and relocated store openings, the relative proportion of new and relocated stores to mature stores, cannibalization resulting from the opening of new stores in existing markets, changes in advertising and other operating costs, the timing and level of markdowns, changes in our product mix, weather conditions, retail trends, the retail sales environment, economic conditions, inflation, the impact of competition, and our ability to execute our business strategy efficiently. As a result, same store sales or operating results may fluctuate, and may cause the price of our securities to fluctuate significantly. Therefore, we believe that period-to-period comparisons of our same store sales may not be a reliable indicator of our future overall operating performance.

We intend to open additional stores in both our existing markets and new markets, which poses both the possibility of diminishing sales by existing stores in our existing markets and the risk of a slow ramp-up period for stores in new markets.

Our expansion strategy includes plans to open 20 additional stores in existing markets and new markets in 2014. Because our stores typically draw customers from their local areas, additional stores may draw customers away from nearby existing stores and may cause same store sales performance at those existing stores to decline, which may adversely affect our overall operating results. Additionally, stores in new markets typically have a ramp-up period before sales become steady enough for such stores to be profitable. Our ability to open additional stores will be dependent on our ability to promote and/or recruit enough qualified field managers, store managers, assistant store managers, and sales associates. The time and effort required to train and supervise a large number of new managers and associates and integrate them into our culture may divert resources from our existing stores. If we are unable to profitably open additional stores in both new and existing markets and limit the adverse impact of those new stores on existing stores, it may reduce our same store sales and overall operating results during the implementation of our expansion strategy.

Our expansion strategy will be dependent upon, and limited by, the availability of adequate capital.

Our expansion strategy will require additional capital for, among other purposes, opening new stores, distribution centers, and manufacturing facilities as well as entering new markets. Such capital expenditures will include researching real estate and consumer markets, lease, inventory, property and equipment costs, integration of new stores and markets into company-wide systems and programs, and other costs associated with new stores and market entry expenses and growth. If cash generated internally is insufficient to fund capital requirements, we will require additional debt or equity financing. Adequate financing may not be available or, if available, may not be available on terms satisfactory to us. In addition, our credit facility may limit the amount of capital expenditures that we may make annually, depending on our leverage ratio. If we fail to obtain sufficient additional capital in the future or we are unable to make capital expenditures under our credit facility, we could be forced to curtail our expansion strategies by reducing or delaying capital expenditures relating to new stores and new market entry. As a result, there can be no assurance that we will be able to fund our current plans for the opening of new stores or entry into new markets.

We depend on a number of suppliers, and any failure by any of them to supply us with products may impair our inventory and adversely affect our ability to meet customer demands, which could result in a decrease in revenues and/or gross margin.

Our current suppliers may not continue to sell products to us on acceptable terms or at all, and we may not be able to establish relationships with new suppliers to ensure delivery of products in a timely manner or on terms acceptable to us. We do not have long-term contractual supply agreements with our suppliers which obligate them to supply us with products at specified quantities or prices. We may not be able to acquire desired merchandise in sufficient quantities on terms acceptable to us in the future. We are also dependent on suppliers for assuring the quality of merchandise supplied to us. Our inability to acquire suitable merchandise in the future or the loss of one or more of our suppliers and our failure to replace them may harm our relationship with our customers and our ability to attract new customers, resulting in a decrease in net sales.

We source the approximately 4,500 products that we stock and sell from over 130 domestic and international vendors. We source a large number of those products from foreign manufacturers, including approximately 52% of our products from a group of 10 suppliers located in Asia and Europe. We generally take title to these products overseas and are responsible for arranging shipment to our distribution centers. Financial instability among key vendors, political instability, trade restrictions, tariffs, currency exchange rates, and transport capacity and costs are beyond our control and could negatively impact our business if they seriously disrupt the movement of products through our supply chain or increased the costs of our products.

If our suppliers do not use ethical business practices or comply with applicable laws and regulations, our reputation could be harmed due to negative publicity and we could be subject to legal risk.

We do not control the operations of our suppliers. Accordingly, we cannot guarantee that our suppliers will comply with applicable environmental and labor laws and regulations or operate in a legal, ethical, and responsible manner. Violation of environmental, labor or other laws by our suppliers or their failure to operate in a legal, ethical, or responsible manner, could reduce demand for our products if, as a result of such violation or failure, we attract negative publicity. Further, such conduct could expose us to legal risks as a result of the purchase of products from non-compliant suppliers.

If customers are unable to obtain third-party financing at satisfactory rates, sales of our products could be materially adversely affected.

Our business, financial condition, and results of operations have been, and may continue to be affected, by various economic factors. Deterioration in the current economic environment could lead to reduced consumer and business spending, including by our customers. It may also cause customers to shift their spending to products that we either do not sell or that generate lower profitably for us. Further, reduced access to credit may adversely affect the ability of consumers to purchase our products. This potential reduction in access to credit may adversely impact our ability to offer customers credit card financing through third party credit providers on terms similar to those offered currently, or at all. In addition, economic conditions, including decreases in access to credit, may result in financial difficulties leading to restructuring, bankruptcies, liquidations and other unfavorable events for our customers, which may adversely impact our industry, business, and results of operations.

Any failure by us to successfully anticipate consumer trends may lead to loss of consumer acceptance of our products, resulting in reduced revenues.

Our success depends on our ability to anticipate and respond to changing trends and consumer demands in a timely manner. If we fail to identify and respond to emerging trends, consumer acceptance of our merchandise and our image with current or potential customers may be harmed, which could reduce our revenues. Additionally, if we misjudge market trends, we may significantly overstock unpopular products and be forced to reduce the sales price of such products, which would have a negative impact on our gross profit and cash flow. Conversely, shortages of products that prove popular could also reduce our revenues.

We depend on a few key employees, and if we lose the services of certain of our executive officers, we may not be able to run our business effectively.

Our future success depends in part on our ability to attract and retain key executive, merchandising, marketing, and sales personnel. Our executive officers include Robert Rucker, president and chief executive officer; Chris Homeister, chief operating officer; Timothy Clayton, chief financial officer; Carl Randazzo, senior vice president — retail; and Joseph Kinder, senior vice president — operations. We have employment and non-compete arrangements with each of Messrs. Rucker, Homeister, Clayton, Randazzo, and Kinder. If any of these executive officers ceases to be employed by us, we would have to hire additional qualified personnel. Our ability to successfully hire other experienced and qualified executive officers cannot be assured, and may be difficult because we face competition for these professionals from our competitors, our suppliers and other companies operating in our industry. As a result, the loss or unavailability of any of our executive officers could have a material adverse effect on us.

We have entered into a $120 million credit facility. The burden of this additional debt could adversely affect us, make us more vulnerable to adverse economic or industry conditions, and prevent us from fulfilling our debt obligations or from funding our expansion strategy.

In connection with the Business Combination, we issued promissory notes in an aggregate principal amount of approximately $70 million, which we fully repaid as of December 31, 2013. We have entered into a credit facility with Bank of America, N.A., as administrative agent and The Huntington National Bank, as syndication agent, for $120 million, including a term loan of $25 million and a revolving credit facility of $95 million, which we have used, in part, to repay the promissory notes issued in connection with the Business Combination. The terms of our credit facility and the burden of the indebtedness incurred thereunder could have serious consequences for us, such as:

| | • | limiting our ability to obtain additional financing to fund our working capital, capital expenditures, debt service requirements, expansion strategy, or other needs; |

| | • | placing us at a competitive disadvantage compared to competitors with less debt; |

| | • | increasing our vulnerability to, and reducing our flexibility in planning for, adverse changes in economic, industry, and competitive conditions; and |

| | • | increasing our vulnerability to increases in interest rates if borrowings under the credit facility are subject to variable interest rates. |

Our credit facility also contains negative covenants that limit our ability to engage in specified types of transactions. These covenants limit our ability to, among other things:

| | • | engage in mergers or consolidations; |

| | • | sell assets (including pursuant to sale and leaseback transactions); |

| | • | pay dividends and distributions or repurchase our capital stock; |

| | • | make investments, acquisitions, loans, or advances; |

| | • | make capital expenditures; |

| | • | repay, prepay, or redeem certain indebtedness; |

| | • | engage in certain transactions with affiliates; |

| | • | enter into agreements limiting subsidiary distributions; |

| | • | enter into agreements limiting the ability to create liens; |

| | • | amend our organizational document in a way that has a material effect on the lenders or administrative agent under our credit facility; and |

| | • | change our lines of business. |

A breach of any of these covenants could result in an event of default under our credit facility. Upon the occurrence of an event of default, the lender could elect to declare all amounts outstanding under such facility to be immediately due and payable and terminate all commitments to extend further credit, or seek amendments to our debt agreements that would provide for terms more favorable to such lender and that we may have to accept under the circumstances. If we were unable to repay those amounts, the lender under our credit facility could proceed against the collateral granted to them to secure that indebtedness.

If we fail to hire, train, and retain qualified store managers, sales associates, and other employees, our enhanced customer service could be compromised and we could lose sales to our competitors.

A key element of our competitive strategy is to provide product expertise to our customers through our extensively trained, commissioned sales associates. If we are unable to attract and retain qualified personnel and managers as needed in the future, including qualified sales personnel, our level of customer service may decline, which may decrease our revenues and profitability.

If we are unable to renew or replace current store leases or if we are unable to enter into leases for additional stores on favorable terms, or if one or more of our current leases is terminated prior to expiration of its stated term and we cannot find suitable alternate locations, our growth and profitability could be negatively impacted.

We currently lease all of our store locations. Many of our current leases provide us with the unilateral option to renew for several additional rental periods at specific rental rates. Our ability to re-negotiate favorable terms on an expiring lease or to negotiate favorable terms for a suitable alternate location, and our ability to negotiate favorable lease terms for additional store locations, could depend on conditions in the real estate market, competition for desirable properties, our relationships with current and prospective landlords, or on other factors that are not within our control. Any or all of these factors and conditions could negatively impact our growth and profitability.

Compliance with laws or changes in existing or new laws and regulations or regulatory enforcement priorities could adversely affect our business.

We must comply with various laws and regulations at the local, regional, state, federal, and international levels. These laws and regulations change frequently and such changes can impose significant costs and other burdens of compliance on our business and vendors. Any changes in regulations, the imposition of additional regulations, or the enactment of any new legislation that affect employment/labor, trade, product safety, transportation/logistics, energy costs, health care, tax, or environmental issues, or compliance with the Foreign Corrupt Practices Act, could have an adverse impact on our financial condition and results of operations. Changes in enforcement priorities by governmental agencies charged with enforcing existing laws and regulations can increase our cost of doing business.

We may also be subject to audits by various taxing authorities. Changes in tax laws in any of the multiple jurisdictions in which we operate, or adverse outcomes from tax audits that we may be subject to in any of the jurisdictions in which we operate, could result in an unfavorable change in our effective tax rate, which could have an adverse effect on our business and results of operations.

As our stores are generally concentrated in the midwestern, mid-Atlantic and northeast regions of the United States, we are subject to regional risks.

We have a high concentration of stores in the midwestern, mid-Atlantic and northeast regions. If these markets individually or collectively suffer an economic downturn or other significant adverse event, there could be an adverse impact on same store sales, revenues, and profitability, and the ability to implement our planned expansion program. Any natural disaster, extended adverse weather or other serious disruption in these markets due to fire, tornado, hurricane, or any other calamity could damage inventory and could result in decreased revenues.

Our results may be adversely affected by fluctuations in material and energy costs.

Our results may be affected by the prices of the materials used in the manufacture of tile, setting and maintenance materials, and related accessories that we sell. These prices may fluctuate based on a number of factors beyond our control, including: oil prices, changes in supply and demand, general economic conditions, labor costs, competition, import duties, tariffs, currency exchange rates, and government regulation. In addition, energy costs have fluctuated dramatically in the past and may fluctuate in the future. These fluctuations may result in an increase in our transportation costs for distribution from the manufacturer to our distribution center and from our regional distribution centers to our retail stores, utility costs for our distribution and manufacturing centers and retail stores, and overall costs to purchase products from our vendors.

We may not be able to adjust the prices of our products, especially in the short-term, to recover these cost increases in materials and energy. A continual rise in material and energy costs could adversely affect consumer spending and demand for our products and increase our operating costs, both of which could have a material adverse effect on our financial condition and results of operations.

Our success is highly dependent on our ability to provide timely delivery to our customers, and any disruption in our delivery capabilities or our related planning and control processes may adversely affect our operating results.

Our success is due in part to our ability to deliver products quickly to our customers, which relies on successful planning and distribution infrastructure, including ordering, transportation and receipt processing, and the ability of suppliers to meet distribution requirements. Our ability to maintain this success depends on the continued identification and implementation of improvements to our planning processes, distribution infrastructure, and supply chain. We also need to ensure that our distribution infrastructure and supply chain keep pace with our anticipated growth and increased number of stores. The cost of these enhanced processes could be significant and any failure to maintain, grow, or improve them could adversely affect our operating results. Our business could also be adversely affected if there are delays in product shipments due to freight difficulties, strikes, or other difficulties at our suppliers’ principal transport providers, or otherwise.

Damage, destruction, or disruption of our distribution and manufacturing centers could significantly impact our operations and impede our ability to produce and distribute our products.

We rely on four regional distribution centers to supply products to all of our retail stores. In addition, we rely on our manufacturing centers, located at our distribution centers, to manufacture our setting and maintenance materials. If any of these facilities, or the inventory stored in these facilities, were damaged or destroyed by fire or other causes, our distribution or manufacturing processes would be disrupted, which could cause significant delays in delivery. This could negatively impact our ability to stock our stores and deliver products to our customers, and cause our revenues and operating results to deteriorate.

Our ability to control labor costs is limited, which may negatively affect our business.

Our ability to control labor costs is subject to numerous external factors, including prevailing wage rates, the impact of legislation or regulations governing healthcare benefits or labor relations, such as the Employee Free Choice Act, and health and other insurance costs. If our labor and/or benefit costs increase, we may not be able to hire or maintain qualified personnel to the extent necessary to execute our competitive strategy, which could adversely affect our results of operations.

Our business exposes us to personal injury and product liability claims, which could result in adverse publicity and harm to our brands and our results of operations.

We are from time to time subject to claims due to the injury of an individual in our stores or on our property. In addition, we may be subject to product liability claims for the products that we sell. Our purchase orders generally do not require the manufacturer to indemnify us against any product liability claims arising from products purchased by us. Any personal injury or product liability claim made against us, whether or not it has merit, could be time-consuming and costly to defend, resulting in adverse publicity or damage to our reputation, and have an adverse effect on our results of operations. In addition, any negative publicity involving our vendors, employees, and other parties who are not within our control could negatively impact us.

Our business operations could be disrupted if our information technology systems fail to perform adequately or we are unable to protect the integrity and security of our customers’ information.

We depend upon our information technology systems in the conduct of all aspects of our operations. If our information technology systems fail to perform as anticipated, we could experience difficulties in virtually any area of our operations, including but not limited to replenishing inventories or delivering products to store locations in response to consumer demands. It is also possible that our competitors could develop better online platforms than us, which could negatively impact our internet sales. Any of these or other systems-related problems could, in turn, adversely affect our revenues and profitability.

In addition, in the ordinary course of our business, we collect and store certain personal information from individuals, such as our customers and suppliers, and we process customer payment card and check information. We are continually evaluating our systems associated with the collection, security, and handling of personal information and intend to make any required changes or enhancements in our systems and policies in response to this assessment. Our failure to properly comply with relevant laws, a breach of our network security and systems, or other events that cause the loss or public disclosure of, or access by third parties to, our customers’ personal information could have serious negative consequences for our business, including possible fines, penalties and damages, an unwillingness of customers to provide us with their credit card or payment information, harm to our reputation and brand, loss of our ability to accept and process customer credit card orders, and time-consuming and expensive litigation.

Computer hackers may attempt to penetrate our computer systems and, if successful, misappropriate personal information, payment card or check information, or confidential business information. In addition, an employee, contractor, or other third party with whom we do business may attempt to circumvent our security measures in order to obtain such information. The techniques used to obtain unauthorized access or sabotage systems change frequently and may originate from less regulated or remote areas around the world. As a result, we may be unable to proactively address these techniques or to implement adequate preventative measures.

Many states have enacted laws requiring companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach often lead to widespread negative publicity, which may cause our customers to lose confidence in the effectiveness of our data security measures. Any security breach, whether successful or not, would harm our reputation and could cause the loss of customers.

Concentration of ownership may have the effect of delaying or preventing a change in control.

Our directors, executive officers, and holders of more than 5% of our common stock, together with their affiliates, beneficially hold approximately 45% of our outstanding shares of common stock. As a result, these stockholders, if acting together, have the ability to influence the outcome of corporate actions requiring stockholder approval. This concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of our securities.

Future sales of our common stock may cause the market price of our securities to drop significantly, even if our business is doing well.

In connection with the Business Combination and the underwritten public offerings of our common stock by certain of our stockholders in December 2012 and June 2013, our officers, directors and certain stockholders, who, immediately following the Business Combination, collectively held an aggregate of 34,305,233 shares of our common stock, agreed to refrain from selling such shares for periods of time that have now passed. As a result, our directors, officers and the selling stockholders in the December 2012 and June 2013 underwritten public offerings may sell their shares at any time, subject to compliance with applicable securities laws. The presence of these additional securities trading in the public market may have an adverse effect on the market price of our common stock.

In addition, the former direct and indirect holders of equity interests in The Tile Shop and the JWCAC founders hold registration rights, subject to certain limitations, with respect to our common stock that they received in the Business Combination pursuant to a registration rights agreement. The holders of a majority in interest of our common stock held by the former direct and indirect holders of equity interests in The Tile Shop will be entitled to require us, on up to four occasions, to register under the Securities Act of 1933, as amended, or the Securities Act, the shares of common stock that they received in the Business Combination. The holders of a majority in interest of our common stock held by the JWCAC founders will be entitled to require us, on up to two occasions, to register under the Securities Act the shares of common stock that they received in the Business Combination, and any shares that may be issued pursuant to the exercise of certain warrants held by them. As of the date of this report, we have effected two registrations pursuant to such agreements. The presence of these additional securities trading in the public market may have an adverse effect on the market price of our common stock.

Although our common stock is currently listed on The NASDAQ Global Market, there can be no assurance that we will be able to comply with the continued listing standards.

The NASDAQ Global Market may delist our common stock from trading on its exchange for failure to meet the continued listing standards. If our common stock were delisted from The NASDAQ Global Market, we and our stockholders could face significant material adverse consequences including:

| | • | a limited availability of market quotations for our common stock; |

| | • | a determination that our common stock is a “penny stock” would require brokers trading in our common stock to adhere to more stringent rules, possibly resulting in a reduced level of trading activity in the secondary trading market for our common stock; |

| | • | a limited amount of analyst coverage; and |

| | • | a decreased ability to issue additional securities or obtain additional financing in the future. |

The market price of our securities may decline and/or be volatile.

Fluctuations in the price of our securities could contribute to the loss of all or part of your investment. Prior to the Business Combination, there had not been a public market for our securities or The Tile Shop’s securities, and trading in JWCAC’s securities had not been active. An active, liquid, and orderly market for our securities may not be sustained and the trading price of our securities could be volatile and subject to wide fluctuations in response to various factors, some of which are beyond our control. Any of the factors listed below could have a material adverse effect on your investment in our securities and our securities may trade at prices significantly below the price that you paid for them. In such circumstances, the trading price of our securities may not recover and may experience a further decline.

Factors affecting the trading price of our securities may include:

| | • | actual or anticipated fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to us; |

| | • | changes in the market’s expectations about our operating results; |

| | • | the effects of seasonality on our business cycle; |

| | • | success of competitive retailers; |

| | • | our operating results failing to meet the expectation of securities analysts or investors in a particular period; |

| | • | research reports published regarding our business; |

| | • | changes in financial estimates and recommendations by securities analysts concerning us, the housing market, the retail specialty tile market, or the retail market in general; |

| | • | operating and stock price performance of other companies that investors deem comparable to us; |

| | • | our ability to market new and enhanced products on a timely basis; |

| | • | changes in laws and regulations affecting our business; |

| | • | commencement of, or involvement in, litigation involving us; |

| | • | changes in our capital structure, such as future issuances of securities or the incurrence of additional debt; |

| | • | the volume of shares of our common stock available for public sale; |

| | • | any major change in our board of directors or management; |

| | • | sales of substantial amounts of common stock by our directors, executive officers, or significant stockholders or the perception that such sales could occur; and |

| | • | general economic and political conditions such as recessions, interest rates, fuel prices, international currency fluctuations, and acts of war or terrorism. |

Broad market and industry factors may materially harm the market price of our securities irrespective of our operating performance. The NASDAQ Global Market and the stock market in general have experienced price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of the particular companies affected. The trading prices and valuations of these securities, and of our securities, may not be predictable. A loss of investor confidence in the market for retail securities or the securities of other companies that investors perceive to be similar to us could depress the price of our securities regardless of our business, prospects, financial conditions, or results of operations. A decline in the market price of our securities also could adversely affect our ability to issue additional securities and our ability to obtain additional financing in the future.

If securities or industry analysts do not publish or cease publishing research or reports about us, our business, or our market, or if they change their recommendations regarding our common stock adversely, the price and trading volume of our common stock could decline.

The trading market for our common stock will be influenced by the research and reports that industry or securities analysts may publish about us, our business, our market, or our competitors. If any of the analysts who cover us change their recommendation regarding our common stock adversely, or provide more favorable relative recommendations about our competitors, the price of our common stock would likely decline. If any analyst who covers us were to cease coverage of us or fail to regularly publish reports on us, we could lose visibility in the financial markets, which in turn could cause our common stock price or trading volume to decline.

We are a holding company with no business operations of our own and depend on cash flow from The Tile Shop to meet our obligations.

We are a holding company with no business operations of our own or material assets other than the equity of our subsidiaries. All of our operations are conducted by our subsidiary, The Tile Shop. As a holding company, we will require dividends and other payments from our subsidiaries to meet cash requirements. The terms of any future credit facility may restrict our subsidiaries from paying dividends and otherwise transferring cash or other assets to us, although our current facility does not restrict this action. If there is an insolvency, liquidation, or other reorganization of any of our subsidiaries, our stockholders likely will have no right to proceed against their assets. Creditors of those subsidiaries will be entitled to payment in full from the sale or other disposal of the assets of those subsidiaries before us, as an equity holder, would be entitled to receive any distribution from that sale or disposal. If The Tile Shop is unable to pay dividends or make other payments to us when needed, we will be unable to satisfy our obligations.

Anti-takeover provisions contained in our certificate of incorporation and bylaws, as well as provisions of Delaware law, could impair a takeover attempt.

Our certificate of incorporation and bylaws contain provisions that could have the effect of delaying or preventing changes in control or changes in our management without the consent of our board of directors. These provisions include:

| | • | a classified board of directors with three-year staggered terms, which may delay the ability of stockholders to change the membership of a majority of our board of directors; |

| | • | no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates; |

| | • | the exclusive right of our board of directors to elect a director to fill a vacancy created by the expansion of the board of directors or the resignation, death, or removal of a director, which prevents stockholders from being able to fill vacancies on our board of directors; |

| | • | the ability of our board of directors to determine to issue shares of preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquirer; |

| | • | a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or special meeting of our stockholders; |

| | • | the requirement that a special meeting of stockholders may be called only by the chairman of the board of directors, the chief executive officer, or the board of directors, which may delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors; |

| | • | limiting the liability of, and providing indemnification to, our directors and officers; |

| | • | controlling the procedures for the conduct and scheduling of stockholder meetings; |

| | • | providing the board of directors with the express power to postpone previously scheduled annual meetings of stockholders and to cancel previously scheduled special meetings of stockholders; |

| | • | providing that directors may be removed prior to the expiration of their terms by stockholders only for cause; and |

| | • | advance notice procedures that stockholders must comply with in order to nominate candidates to our board of directors or to propose matters to be acted upon at a stockholders’ meeting, which may discourage or deter a potential acquiror from conducting a solicitation of proxies to elect the acquiror’s own slate of directors or otherwise attempting to obtain control of us. |

These provisions, alone or together, could delay hostile takeovers and changes in control of us or changes in our management.

As a Delaware corporation, we are also subject to provisions of Delaware law, including Section 203 of the Delaware General Corporation Law, which prevents some stockholders holding more than 15% of our outstanding common stock from engaging in certain business combinations without approval of the holders of substantially all of our outstanding common stock. Any provision of our certificate of incorporation or bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their shares of our common stock, and could also affect the price that some investors are willing to pay for our common stock.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

As of December 31, 2013, we operated 88 stores located in 28 states with an average square footage of approximately 23,000 square feet.

We lease all of our stores. Our 15,000 square foot headquarters in Plymouth, Minnesota is attached to our flagship retail store. We own four regional facilities used for distribution of purchased product and manufacturing of maintenance and setting materials, located in Spring Valley, Wisconsin; Ottawa Lake, Michigan; Ridgeway, Virginia; and Durant, Oklahoma, which consist of 51,000, 271,000, 134,000, and 150,000 square feet, respectively.

We believe that our material property holdings are suitable for our current operations and purposes. In order to continue executing our growth strategy, we intend to open 20 new retail locations in 2014.

ITEM 3. LEGAL PROCEEDINGS

From time to time, we have been and may become involved in legal proceedings arising in the ordinary course of our business. Although the results of litigation and claims cannot be predicted with certainty, we are not presently involved in any legal proceeding which we expect to have a material adverse effect on our business, operating results, or financial condition. Regardless of the outcome, litigation can have an adverse impact on us because of defense and settlement costs, diversion of management resources, and other factors.

ITEM 4. MINE SAFETY DISCLOSURES

None.

Part II

ITEM 5.MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock has been traded on The NASDAQ Global Market under the symbol “TTS” since the consummation of the Business Combination on August 21, 2012. Prior to this time, there was no public market for our common stock. Our Public Warrants (as defined in Item 13. “Certain Relationships and Related Transactions-Warrant Agreement,”) were previously on the Over- the-Counter Bulletin Board under the symbol “TTSAW.” The following table shows the high and low sale prices per share of our common stock and Public Warrants as reported on The NASDAQ Global Market and the Over-the-Counter Bulletin Board for the periods indicated:

| | | | Common Stock | | | Public Warrants(1) | |

| | Quarter | | High | | | Low | | | High | | | Low | |

Fiscal 2012 | Third (beginning August 21, 2012) | | $ | 16.99 | | | $ | 11.75 | | | $ | 3.60 | | | $ | 1.05 | |

| | Fourth | | $ | 17.56 | | | $ | 12.00 | | | $ | 6.85 | | | $ | 3.05 | |

| | | | | | | | | | | | | | | | | | |

Fiscal 2013 | First | | $ | 22.39 | | | $ | 16.41 | | | $ | 5.21 | | | $ | 10.48 | |

| | Second | | $ | 30.33 | | | $ | 19.69 | | | $ | 9.57 | | | $ | 9.82 | |

| | Third | | $ | 30.88 | | | $ | 24.72 | | | $ | - | | | $ | - | |

| | Fourth | | $ | 29.90 | | | $ | 10.05 | | | $ | - | | | $ | - | |

| | (1) | Following the second quarter of fiscal 2013, no warrants remain outstanding. |

As of February 21, 2014, we had approximately 33 holders of record of our common stock. All our Public Warrants were either exercised or redeemed during the year ended December 31, 2013. This figure does not include the number of persons whose securities are held in nominee or “street” name accounts through brokers.

As of February 21, 2014, we had outstanding a total of 51,230,600 shares of common stock and no warrants.

Dividends

We have never declared or paid, and do not anticipate declaring or paying, any cash dividends on our common stock in the foreseeable future. While our board of directors may consider whether or not to institute a dividend policy, it is our present intention to retain any earnings for use in our business operations. In addition, our credit facility restricts our ability to pay dividends.

Securities Authorized for Issuance Under Equity Compensation Plans

For information on our equity compensation plans, refer to Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Recent Sales of Unregistered Securities

None.

Issuer Purchases of Equity Securities

None.

Stock Performance Graph

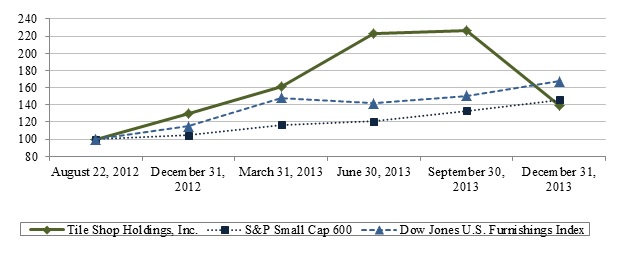

The graph and table below present the Company’s cumulative total stockholder returns relative to the performance of the S&P SmallCap 600 and the Dow Jones U.S. Furnishings Index for the period commencing August 22, 2012, the date of the Business Combination, and ending December 31, 2013, the last trading day of fiscal 2013. The comparison assumes $100 invested at the close of trading on August 22, 2012 in (i) the Company’s common stock, (ii) the stocks comprising the S&P SmallCap 600, and (iii) the stocks comprising the Dow Jones U.S. Furnishings Index. All values assume that all dividends were reinvested on the date paid. The points on the graph represent fiscal quarter-end amounts based on the last trading day in each fiscal quarter. The stock price performance included in the line graph below is not necessarily indicative of future stock price performance.

| | | August 22, 2012 | | | December 31, 2012 | | | March 31, 2013 | | | June 30, 2013 | | | September 30, 2013 | | | December 31, 2013 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Tile Shop Holdings, Inc. | | $ | 100.00 | | | $ | 129.46 | | | $ | 161.62 | | | $ | 222.77 | | | $ | 226.85 | | | $ | 139.00 | |

S&P Small Cap 600 | | $ | 100.00 | | | $ | 104.18 | | | $ | 116.44 | | | $ | 120.57 | | | $ | 133.11 | | | $ | 145.76 | |

Dow Jones U.S. Furnishings Index | | $ | 100.00 | | | $ | 114.95 | | | $ | 148.24 | | | $ | 141.74 | | | $ | 150.66 | | | $ | 167.14 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Source: Market Watch | | | | | | | | | | | | | | | | | | | | | | | | |

ITEM 6. SELECTED FINANCIAL DATA

The following table sets forth selected historical financial information derived from (i) our audited financial statements included elsewhere in this report as of December 31, 2013 and for the year ended December 31, 2013, (ii) The Tile Shop’s audited financial statements included elsewhere in this report as of December 31, 2012 and for the years ended December 31, 2012 and 2011 and (iii) The Tile Shop’s audited financial statements not included in this report as of December 31, 2011 and 2010 and for the years ended December 31, 2010 and 2009. The following selected financial data should be read in conjunction with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and the related notes appearing elsewhere in this report.

| | | As of December 31, or for the year ended December 31, | |

| | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| | | (in thousands, except per share) | |

Statement of Income Data | | | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 229,564 | | | $ | 182,650 | | | $ | 152,717 | | | $ | 135,340 | | | $ | 116,247 | |

Cost of sales | | | 68,755 | | | | 49,626 | | | | 40,321 | | | | 36,124 | | | | 31,706 | |

Gross profit | | | 160,809 | | | | 133,024 | | | | 112,396 | | | | 99,216 | | | | 84,541 | |

Selling, general and administrative expenses | | | 127,731 | | | | 94,716 | | | | 78,368 | | | | 68,105 | | | | 60,051 | |

Deferred compensation expense | | | - | | | | 3,897 | | | | 1,415 | | | | 450 | | | | 120 | |

Income from operations | | | 33,078 | | | | 34,411 | | | | 32,613 | | | | 30,661 | | | | 24,370 | |

Interest expense | | | 2,581 | | | | 1,252 | | | | 443 | | | | 467 | | | | 545 | |

Change in fair value of warrants | | | 54,219 | | | | 82,063 | | | | - | | | | - | | | | - | |

Other income (expense) | | | 4 | | | | 15 | | | | (77 | ) | | | 124 | | | | 73 | |

(Loss) income before income taxes | | | (23,718 | ) | | | (48,889 | ) | | | 32,093 | | | | 30,318 | | | | 23,898 | |

(Provision for) benefit from income taxes(1) | | | (11,942 | ) | | | 2,002 | | | | (733 | ) | | | (609 | ) | | | (675 | ) |

Net (loss) income | | $ | (35,660 | ) | | $ | (46,887 | ) | | $ | 31,360 | | | $ | 29,709 | | | $ | 23,223 | |

Earnings per share(1) | | | (0.72 | ) | | $ | (1.31 | ) | | $ | 0.97 | | | $ | 0.92 | | | $ | 0.72 | |

Weighted average shares outstanding | | | 49,600 | | | | 35,838 | | | | 32,261 | | | | 32,330 | | | | 32,330 | |

Balance Sheet Data | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 1,761 | | | $ | 2,987 | | | $ | 6,283 | | | $ | 14,117 | | | $ | 17,850 | |

Inventories | | | 67,756 | | | | 46,890 | | | | 43,744 | | | | 35,358 | | | | 26,342 | |

Total assets | | | 242,769 | | | | 176,074 | | | | 119,005 | | | | 108,890 | | | | 95,632 | |

Warrant liability | | | - | | | | 95,645 | | | | - | | | | - | | | | - | |

Total debt and capital lease obligations, including current maturities | | | 96,396 | | | | 74,824 | | | | 4,853 | | | | 5,582 | | | | 4,574 | |

Total stockholders' equity | | | 79,863 | | | | (44,763 | ) | | | 75,147 | | | | 69,437 | | | | 62,000 | |

Working capital | | | 51,719 | | | | 35,934 | | | | 34,852 | | | | 34,895 | | | | 31,851 | |

Cash Flow Data | | | | | | | | | | | | | | | | | | | | |

Net cash provided by operating activities | | $ | 21,211 | | | $ | 47,222 | | | $ | 34,722 | | | $ | 32,461 | | | $ | 34,729 | |

Net cash used in investing activities | | | (52,955 | ) | | | (29,064 | ) | | | (18,561 | ) | | | (14,376 | ) | | | (8,267 | ) |

Net cash used in financing activities | | | 30,518 | | | | (21,454 | ) | | | (23,995 | ) | | | (21,818 | ) | | | (12,243 | ) |

Other Selected Financial Data (unaudited) | | | | | | | | | | | | | | | | | | | | |

Adjusted EBITDA(2) | | $ | 54,294 | | | $ | 50,634 | | | $ | 42,602 | | | $ | 38,472 | | | $ | 31,576 | |

Adjusted EBITDA margin(2) | | | 23.7 | % | | | 27.7 | % | | | 27.9 | % | | | 28.4 | % | | | 27.2 | % |

Gross margin(3) | | | 70.0 | % | | | 72.8 | % | | | 73.6 | % | | | 73.3 | % | | | 72.7 | % |

Operating income margin(4) | | | 14.4 | % | | | 18.8 | % | | | 21.4 | % | | | 22.7 | % | | | 21.0 | % |

Same stores sales growth(5) | | | 12.4 | % | | | 7.1 | % | | | 6.4 | % | | | 11.4 | % | | | (4.6 | %) |

Stores open - end of period | | | 88 | | | | 68 | | | | 53 | | | | 48 | | | | 41 | |

| | (1) | Historical amounts do not include pro forma adjustments for income taxes as a result of our change in tax status, which was effective on August 21, 2012 upon consummation of the Business Combination. |

| | (2) | We calculate Adjusted EBITDA by taking net income calculated in accordance with accounting principles generally accepted in the United States, or GAAP, and adjusting interest expense, income taxes, depreciation and amortization, non-cash change in fair value of warrants, non-recurring items including equity related transaction costs, other items (including special investigation costs), deferred compensation expense, and stock based compensation expense. Adjusted EBITDA margin is equal to Adjusted EBITDA divided by net sales. We believe that these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to our financial condition and results of operations. Our management uses these non-GAAP measures to compare our performance to that of prior periods for trend analyses, for purposes of determining management incentive compensation, and for budgeting and planning purposes. These measures are used in financial reports prepared for management and our board of directors. We believe that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends and in comparing our financial measures with other specialty retailers, many of which present similar non-GAAP financial measures to investors. |

| | (3) | Gross margin is gross profit divided by net sales. |