Exhibit 99.1

CyrusOne Reports Fourth Quarter and Full Year 2016 Earnings

Year-over-Year Revenue Growth of 21% and Adjusted EBITDA Growth of 21%;

Announcing an 11% Increase in 1Q’17 Dividend per Share to $0.42

DALLAS (February 22, 2017) - CyrusOne Inc. (NASDAQ: CONE), a premiere global data center REIT, today announced fourth quarter and full year 2016 earnings.

Highlights

|

| | | | |

| Category | 4Q’16 | H/(L) vs. 4Q’15 | FY’16 | H/(L) vs. FY’15 |

| Net income | $0.8 million | n/m | $19.9 million | n/m |

| Revenue | $137.4 million | 21% | $529.1 million | 33% |

| Adjusted EBITDA | $73.0 million | 21% | $278.5 million | 32% |

| Normalized FFO | $56.4 million | 28% | $210.2 million | 39% |

| Net income per share | $0.01 | n/m | $0.24 | n/m |

| Normalized FFO per share | $0.68 | 11% | $2.66 | 23% |

| |

| • | Leased 9 megawatts ("MW") and 74,000 colocation square feet in the fourth quarter totaling $19 million in annualized GAAP revenue |

| |

| • | Backlog of $59 million in annualized GAAP revenue as of the end of the fourth quarter, representing nearly $470 million in total contract value |

| |

| • | Added two of the ten largest cloud companies as new customers in the fourth quarter, increasing our total to nine of the ten largest cloud companies |

| |

| • | For full year 2016, leased a record 92 MW and 642,000 colocation square feet totaling $148 million in annualized GAAP revenue and more than $1.2 billion in total contract value |

| |

| • | Announcing an 11% increase in the quarterly dividend for the first quarter of 2017 to $0.42 per share, up from $0.38 per share in 2016 |

| |

| • | Subsequent to quarter end, announced the acquisition of two data centers from Sentinel Data Centers ("Sentinel"), establishing a presence in the Southeast and enhancing the diversification of the portfolio, with expected immediate accretion to Normalized FFO per diluted share |

“CyrusOne had its strongest year since our IPO, including record revenue growth and bookings and high growth across all key metrics,” said Gary Wojtaszek, president and chief executive officer of CyrusOne. “We are well positioned for continued growth in 2017 with a revenue backlog of nearly $60 million, a robust sales funnel consisting of cloud and enterprise customers, and enhanced growth from our recently announced acquisition of the Sentinel data centers. Our balance sheet is strong, and our development pipeline is 72% pre-leased, significantly de-risking our capital spend.”

Fourth Quarter 2016 Financial Results

Net income was $0.8 million for the fourth quarter, compared to a net loss of $1.2 million in the same period in 2015. Normalized Funds From Operations (Normalized FFO)1 was $56.4 million for the fourth quarter, compared to $44.2 million in the same period in 2015, an increase of 28%. Net income per diluted common share2 was $0.01 in the fourth quarter of 2016, compared to a net loss of $0.02 per diluted common share or common share equivalent in the same period in 2015. Normalized FFO per diluted common share2 was $0.68 in the fourth quarter of 2016, an increase of 11% over fourth quarter 2015.

Revenue was $137.4 million for the fourth quarter, compared to $113.3 million for the same period in 2015, an increase of 21%. The increase in revenue was driven primarily by a 32% increase in leased colocation square feet and additional interconnection services. Net operating income (NOI)3 was $89.6 million for the fourth quarter, compared to $71.9 million in the same period in 2015, an increase of 25%. Adjusted EBITDA4 was $73.0 million for the fourth quarter, compared to $60.5 million in the same period in 2015, an increase of 21%.

Leasing Activity

CyrusOne leased approximately 9 MW of power and 74,000 colocation square feet (CSF) in the fourth quarter, representing $1.6 million in monthly recurring rent inclusive of the monthly impact of installation charges, or approximately $19 million in annualized contracted GAAP revenue5 excluding estimates for pass-through power. The weighted average lease term of the new leases based on square footage is 63 months (5.3 years), and the weighted average remaining lease term of CyrusOne’s portfolio is 56 months (taking into account the impact of the backlog and the Sentinel data center acquisition), double the weighted average remaining lease term of the portfolio at the time of the Company’s initial public offering. Recurring rent churn6 for the fourth quarter was 2.2%, compared to 0.4% for the same period in 2015.

Portfolio Utilization and Development

In the fourth quarter, the Company completed construction on approximately 41,000 CSF and 12 MW of power capacity in Northern Virginia and Phoenix, increasing total CSF across 35 data centers to approximately 2,080,000 CSF. This represents an increase of 506,000 CSF, or 32%, from December 31, 2015. CSF utilization7 as of the end of the fourth quarter was 92% for stabilized properties8 and 85% overall. The Company has development projects underway in Phoenix, Northern Virginia, San Antonio and Chicago that will add approximately 494,000 CSF and 88 MW of power capacity. The Company has 825,000 square feet of powered shell available for development as well as 239 acres of land across its markets.

Balance Sheet and Liquidity

As of December 31, 2016, the Company had gross assets totaling approximately $3.4 billion, an increase of approximately 30% over total gross assets as of December 31, 2015. CyrusOne had $1,262.3 million of long term debt9, cash and cash equivalents of $14.6 million, and $757.9 million available under its unsecured revolving credit facility as of December 31, 2016. Net debt9 was $1,258.5 million as of December 31, 2016, approximately 25% of the Company's total enterprise value of $5.0 billion, or 4.3x Adjusted EBITDA for the last quarter annualized. Available liquidity10 was $772.5 million as of December 31, 2016.

Dividend

On October 31, 2016, the Company announced a dividend of $0.38 per share of common stock for the fourth quarter of 2016. The dividend was paid on January 13, 2017, to stockholders of record at the close of business on December 30, 2016.

Additionally, today the Company is announcing a dividend of $0.42 per share of common stock for the first quarter of 2017, an 11% increase in the quarterly dividend compared to 2016. The dividend will be paid on April 14, 2017, to stockholders of record at the close of business on March 31, 2017.

Guidance

CyrusOne is issuing guidance for full year 2017. The annual guidance provided below represents forward-looking statements, which are based on current economic conditions, internal assumptions about the Company's existing customer base and the supply and demand dynamics of the markets in which CyrusOne operates.

CyrusOne does not provide reconciliations for the non-GAAP financial measures included in the annual guidance provided below due to the inherent difficulty in forecasting and quantifying certain amounts that are necessary for such reconciliations, including net income (loss) and adjustments that could be made for transaction and acquisition integration costs, legal claim costs, lease exit costs, asset impairments and loss on disposals and other charges in its reconciliation of historic numbers, the amount of which, based on historical experience, could be significant.

|

| | |

| Category | 2016 Results | 2017 Guidance(1) |

| Total Revenue | $529 million | $663 - 678 million |

| Base Revenue | $477 million | $588 - 598 million |

| Metered Power Reimbursements | $52 million | $75 - 80 million |

| Adjusted EBITDA | $279 million | $359 - 369 million |

| Normalized FFO per diluted common share | $2.66 million | $2.85 - 2.95 |

| Capital Expenditures | $600 million | $550 - 600 million |

| Development | $595 million | $545 - 590 million |

| Recurring | $5 million | $5 - 10 million |

(1)Full year 2017 guidance includes the Sentinel data center acquisition and assumes the transaction closes on February 28, 2017.

Acquisition of Two Data Centers from Sentinel

Subsequent to the end of the quarter, CyrusOne announced the execution of a definitive agreement to acquire two data centers (collectively, the “Facilities”) located in Raleigh-Durham, North Carolina and Somerset, New Jersey from Sentinel. The total purchase price is $490 million, excluding transaction-related expenses. This represents a multiple of approximately 14.4 times pro forma run-rate annualized EBITDA of approximately $34 million.

In 2016, the Facilities generated revenue of nearly $50 million. As of December 31, 2016, the two properties consisted of more than 160,000 colocation square feet and approximately 21 MW of power capacity, with nearly 85% of the power capacity leased. Taking into account the impact of this transaction, the NOI contribution from facilities fully owned by CyrusOne will increase to nearly 80%.

The transaction is expected to provide additional benefits to CyrusOne, including the following:

| |

| • | Enhanced Geographic Diversification: This transaction enhances CyrusOne’s geographic diversification, establishing a presence in the Southeast, a previously stated strategic goal for the Company. In addition, the Raleigh-Durham market will represent the lowest power cost in CyrusOne’s portfolio and one of the lowest in the United States. The Somerset, New Jersey data center further expands the Company’s Northeast footprint, providing additional options for the combined customer base to deploy disaster recovery facilities across New Jersey using the Company’s National IX product to link them together. |

| |

| • | Long-Term Leases with High Quality Customer Base: The weighted average remaining lease term of the Sentinel portfolio is more than 8 years, with only 3% of rent due for renewal through 2019. The Facilities consist of nearly 30 customers, more than two-thirds of which will be new to CyrusOne, including five new Fortune 1000 companies. Approximately 70% of the portfolio rent is generated from investment grade customers. |

| |

| • | Increased Penetration in Healthcare and Financial Services Verticals: Over 80% of rent from the Facilities is generated from customers in the Healthcare and Financial Services verticals. With respect to the Healthcare vertical, taking into account these new customers, the transaction is expected to more than double the contribution from this industry group to the combined CyrusOne portfolio. |

| |

| • | Growth Opportunity: There are approximately 34,000 colocation square feet and 8 MW of power capacity that are either currently available for lease or can be developed in the near term at a total cost of less than $15 million. CyrusOne also has the ability to add another 230,000 colocation square feet and 37 MW of power capacity at a cost expected to be in line with the Company’s current build cost per MW, more than doubling the footprint of the two data centers. This additional capacity will enhance the overall value of the transaction to CyrusOne as the Company fully develops the facilities over time to meet customer demand. |

The acquisition is expected to be immediately accretive to Normalized FFO per diluted share. CyrusOne also plans to develop additional capacity over time, which is expected to create incremental income accretion and long-term value creation.

CyrusOne intends to finance the acquisition with proceeds of approximately $211 million from early settlement of its forward equity sale entered last August 2016 and its recently expanded credit facility.

Upcoming Conferences and Events

| |

| • | Deutsche Bank Media & Telecom Conference on March 6-8 in Palm Beach, Florida |

| |

| • | Citi Global Property CEO Conference on March 5-8 in Hollywood, Florida |

| |

| • | CyrusOne Design and Build Teach-In on March 7 in Hollywood, Florida |

Conference Call Details

CyrusOne will host a conference call on February 23, 2017, at 11:00 AM Eastern Time (10:00 AM Central Time) to discuss its results for the fourth quarter of 2016. A live webcast of the conference call and the presentation to be made during the call will be available under the “Investor Relations” tab in the “Events and Presentations” section of the Company's website at http://investor.cyrusone.com/events.cfm. The U.S. conference call dial-in number is 1-844-492-3731, and the international dial-in number is 1-412-542-4121. A replay will be available one hour after the conclusion of the earnings call on February 23, 2017, through March 9, 2017. The U.S. toll-free replay dial-in number is 1-877-344-7529 and the international replay dial-in number is 1-412-317-0088. The replay access code is 10098910.

Safe Harbor

This release and the documents incorporated by reference herein contain forward-looking statements regarding future events and our future results that are subject to the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical facts, are statements that could be deemed forward-looking statements. These statements are based on current expectations, estimates, forecasts, and projections about the industries in which we operate and the beliefs and assumptions of our management. Words such as "expects," "anticipates," "predicts," "projects," "intends," "plans," "believes," "seeks," "estimates," "continues," "endeavors," "strives," "may," variations of such words and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to projections of our future financial performance, our anticipated growth and trends in our businesses, and other characterizations of future events or circumstances are forward-looking statements. Readers are cautioned these forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, which could cause our actual results to differ materially and adversely from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this release and those discussed in other documents we file with the Securities and Exchange Commission (SEC). More information on potential risks and uncertainties is available in our recent filings with the SEC, including CyrusOne's Form 10-K report, Form 10-Q reports, and Form 8-K reports. Actual results may differ materially and adversely from those expressed in any forward-looking statements. We undertake no obligation to revise or update any forward-looking statements for any reason.

Use of Non-GAAP Financial Measures

This press release contains certain non-GAAP financial measures that management believes are helpful in understanding the Company's business, as further discussed within this press release. These financial measures, which include Funds From Operations, Normalized Funds From Operations, Adjusted EBITDA, Net Operating Income, Adjusted Net Operating Income, and Net Debt should not be construed as being more important than comparable GAAP measures. Detailed reconciliations of these non-GAAP financial measures to comparable GAAP financial measures have been included in the tables that accompany this release and are available in the Investor Relations section of www.cyrusone.com.

Management uses FFO, Normalized FFO, Adjusted EBITDA, NOI, and Adjusted NOI as supplemental performance measures because they provide performance measures that, when compared year over year, capture trends in occupancy rates, rental rates and operating costs. The Company also believes that, as widely recognized measures of the performance of real estate investment trusts (REITs) and other companies, these measures will be used by investors as a basis to compare its operating performance with that of other companies. Other companies may not calculate these measures in the same manner, and, as presented, they may not be comparable to others. Therefore, FFO, Normalized FFO, NOI, Adjusted NOI, and Adjusted EBITDA should be considered only as supplements to net income as measures of our performance. FFO, Normalized FFO, NOI, Adjusted NOI, and Adjusted EBITDA should not be used as measures of liquidity or as indicative of funds available to fund the Company's cash needs, including the ability to pay dividends. These measures also should not be used as substitutes for cash flow from operating activities computed in accordance with U.S. GAAP.

1Normalized Funds From Operations (Normalized FFO) is defined as Funds From Operations (FFO) plus amortization of customer relationship intangibles, transaction and acquisition integration costs, legal claim costs and lease exit costs, and other special items including loss on extinguishment of debt and severance and management transition costs, as appropriate. FFO is net (loss) income computed in accordance with U.S. GAAP before real estate depreciation and amortization and Asset impairments and loss on disposal. Because the value of the customer relationship intangibles is inextricably connected to the real estate acquired, CyrusOne believes the amortization and impairments of such intangibles is analogous to real estate depreciation and impairments; therefore, the Company adds the customer relationship intangible amortization and impairments back for similar treatment with real estate depreciation and impairments. The Company believes its Normalized FFO calculation provides a comparable measure to that used by others in the industry. However, other REITs may not calculate Normalized FFO in the same manner. Accordingly, the Company’s Normalized FFO may not be comparable to others.

2Net income / (loss) per diluted common share and Normalized FFO per diluted common share are defined as net income / (loss) and Normalized FFO, respectively, divided by the weighted average common shares outstanding for the period, which were 82,881,867 for the fourth quarter of 2016 and 78,988,266 for full year 2016.

3Net Operating Income (NOI) is defined as revenue less property operating expenses. Amortization of deferred leasing costs is presented in depreciation and amortization, which is excluded from NOI. CyrusOne has not historically incurred any tenant improvement costs. Our sales and marketing costs consist of salaries and benefits for our internal sales staff, travel and entertainment, office supplies, marketing and advertising costs. General and administrative costs include salaries and benefits of our senior management and support functions, legal and consulting costs, and other administrative costs. Marketing and advertising costs are not property-specific, rather these costs support our entire portfolio. As a result, we have excluded these marketing and advertising costs from our NOI calculation, consistent with the treatment of general and administrative costs, which also support our entire portfolio. From time to time, there may be non-recurring costs in property operating expenses, and as a result the Company may present Adjusted Net Operating Income (Adjusted NOI) to exclude the impacts of those costs.

4Adjusted EBITDA is defined as net income (loss) as defined by U.S. GAAP plus interest expense, income tax (benefit) expense, depreciation and amortization, stock-based compensation, transaction and integration costs, severance and management transition costs, asset impairments and (gain) loss on disposals, lease exit costs, legal claim costs and other special items. Other companies may not calculate Adjusted EBITDA in the same manner. Accordingly, the Company's Adjusted EBITDA as presented may not be comparable to others.

5Annualized GAAP revenue is equal to monthly recurring rent, defined as average monthly contractual rent during the term of the lease plus the monthly impact of installation charges, multiplied by 12. It can be shown both inclusive and exclusive of the Company’s estimate of customer reimbursements for metered power.

6Recurring rent churn is calculated as any reduction in recurring rent due to customer terminations, service reductions or net pricing decreases as a percentage of rent at the beginning of the period, excluding any impact from metered power reimbursements or other usage-based billing.

7Utilization is calculated by dividing CSF under signed leases for available space (whether or not the contract has commenced billing) by total CSF. CSF Utilized differs from CSF Leased presented in the Data Center Portfolio table because the utilization rate includes CSF for signed leases that have not commenced billing.

8Stabilized properties include data halls that have been in service for at least 24 months or are at least 85% utilized.

9Long term debt and net debt exclude adjustments for deferred financing costs. Net debt provides a useful measure of liquidity and financial health. The Company defines net debt as long-term debt and capital lease obligations, offset by cash, cash equivalents, and temporary cash investments.

10Liquidity is calculated as cash, cash equivalents, and temporary cash investments on hand, plus the undrawn capacity on CyrusOne's revolving credit facility.

About CyrusOne

CyrusOne (NASDAQ: CONE) is a high-growth real estate investment trust (REIT) specializing in highly reliable enterprise-class, carrier-neutral data center properties. The Company provides mission-critical data center facilities that protect and ensure the continued operation of IT infrastructure for more than 945 customers, including 181 Fortune 1000 companies.

CyrusOne's data center offerings provide the flexibility, reliability, and security that enterprise and cloud customers require and are delivered through a tailored, customer service-focused platform designed to foster long-term relationships. CyrusOne is committed to full transparency in communication, management, and service delivery throughout its 35 data centers worldwide.

# # #

Investor Relations:

Michael Schafer

972-350-0060

investorrelations@cyrusone.com

Company Profile

CyrusOne (NASDAQ: CONE) specializes in highly reliable enterprise-class, carrier-neutral data center properties. The Company provides mission-critical data center facilities that protect and ensure the continued operation of IT infrastructure for more than 945 customers, including 181 Fortune 1000 companies. CyrusOne's data center offerings provide the flexibility, reliability, and security that enterprise customers require and are delivered through a tailored, customer service-focused platform designed to foster long-term relationships. CyrusOne is committed to full transparency in communication, management, and service delivery throughout its 35 data centers worldwide.

| |

| • | Best-in-Class Sales Force |

| |

| • | Flexible Solutions that Scale as Customers Grow |

| |

| • | Massively Modular® Engineering with Data Hall Builds in 12-16 Weeks |

| |

| • | Focus on Operational Excellence and Superior Customer Service |

| |

| • | Proven Leading-Edge Technology Delivering Power Densities up to 900 Watts per Square Foot |

| |

| • | National IX Replicates Enterprise Data Center Architecture |

|

| | |

| Corporate Headquarters | Senior Management | |

| 1649 West Frankford Road | Gary Wojtaszek, President and CEO | John Hatem, EVP Design, Construction & Operations |

| Carrollton, Texas 75007 | Diane Morefield, Chief Financial Officer | Blake Hankins, Chief Information Officer |

| Phone: (972) 350-0060 | Kevin Timmons, Chief Technology Officer | Scott Brueggeman, Chief Marketing Officer |

| Website: www.cyrusone.com | Tesh Durvasula, Chief Commercial Officer | John Gould, EVP Global Sales |

| | Kellie Teal-Guess, EVP & Chief People Officer | Brent Behrman, EVP Strategic Sales |

| | Robert Jackson, EVP General Counsel & Secretary | Amitabh Rai, Senior VP & Chief Accounting Officer |

Analyst Coverage

|

| | |

| Firm | Analyst | Phone Number |

| Bank of America Merrill Lynch | Michael J. Funk | (646) 855-5664 |

| Barclays | Amir Rozwadowski | (212) 526-4043 |

| Citi | Mike Rollins | (212) 816-1116 |

| Cowen and Company | Colby Synesael | (646) 562-1355 |

| Deutsche Bank | Vin Chao | (212) 250-6799 |

| Gabelli & Company | Sergey Dluzhevskiy | (914) 921-8355 |

| Guggenheim | Jonathan Schildkraut | (212) 518-5365 |

| Jefferies | Jonathan Petersen | (212) 284-1705 |

| J.P. Morgan | Richard Choe | (212) 622-6708 |

| KeyBanc Capital Markets | Jordan Sadler | (917) 368-2280 |

| Morgan Stanley | Simon Flannery | (212) 761-6432 |

| RBC Capital Markets | Jonathan Atkin | (415) 633-8589 |

| Raymond James | Frank G. Louthan IV | (404) 442-5867 |

| Stifel | Matthew S. Heinz, CFA | (443) 224-1382 |

SunTrust Robinson Humphrey

| Greg Miller

| (212) 303-4169

|

| UBS | John C. Hodulik, CFA | (212) 713-4226 |

| Wells Fargo | Eric Luebchow | (312) 630-2386 |

CyrusOne Inc.

Consolidated Statements of Operations

(Dollars in millions, except per share amounts)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | | | Twelve Months Ended

December 31, | | |

| | Change | Change |

| | 2016 | 2015 | $ | % | 2016 | 2015 | $ | % |

| Revenue | $ | 137.4 |

| $ | 113.3 |

| $ | 24.1 |

| 21 | % | $ | 529.1 |

| $ | 399.3 |

| $ | 129.8 |

| 33 | % |

| Costs and expenses: | | | |

|

| | | |

|

|

| Property operating expenses | 47.8 |

| 41.4 |

| 6.4 |

| 15 | % | 187.5 |

| 148.7 |

| 38.8 |

| 26 | % |

| Sales and marketing | 4.0 |

| 3.2 |

| 0.8 |

| 25 | % | 16.9 |

| 12.1 |

| 4.8 |

| 40 | % |

| General and administrative | 17.9 |

| 15.1 |

| 2.8 |

| 19 | % | 60.7 |

| 46.6 |

| 14.1 |

| 30 | % |

| Depreciation and amortization | 49.3 |

| 39.9 |

| 9.4 |

| 24 | % | 183.9 |

| 141.5 |

| 42.4 |

| 30 | % |

| Transaction and acquisition integration costs | 0.4 |

| 2.6 |

| (2.2 | ) | (85 | )% | 4.3 |

| 14.1 |

| (9.8 | ) | (70 | )% |

| Asset impairments and loss on disposal | 5.3 |

| — |

| 5.3 |

| n/m |

| 5.3 |

| 13.5 |

| (8.2 | ) | n/m |

|

| Total costs and expenses | 124.7 |

| 102.2 |

| 22.5 |

| 22 | % | 458.6 |

| 376.5 |

| 82.1 |

| 22 | % |

| Operating income | 12.7 |

| 11.1 |

| 1.6 |

| 14 | % | 70.5 |

| 22.8 |

| 47.7 |

| n/m |

|

| Interest expense | 11.4 |

| 12.0 |

| (0.6 | ) | (5 | )% | 48.8 |

| 41.2 |

| 7.6 |

| 18 | % |

| Income (loss) before income taxes | 1.3 |

| (0.9 | ) | 2.2 |

| n/m |

| 21.7 |

| (18.4 | ) | 40.1 |

| n/m |

|

| Income tax expense | (0.5 | ) | (0.3 | ) | (0.2 | ) | 67 | % | (1.8 | ) | (1.8 | ) | — |

| n/m |

|

| Net income (loss) | 0.8 |

| (1.2 | ) | 2.0 |

| n/m |

| 19.9 |

| (20.2 | ) | 40.1 |

| n/m |

|

| Noncontrolling interest in net income (loss) | — |

| (0.2 | ) | 0.2 |

| n/m |

| — |

| (4.8 | ) | 4.8 |

| n/m |

|

| Net income (loss) attributed to common stockholders | $ | 0.8 |

| $ | (1.0 | ) | $ | 1.8 |

| n/m |

| $ | 19.9 |

| $ | (15.4 | ) | $ | 35.3 |

| n/m |

|

| Income (loss) per common share - basic and diluted | $ | 0.01 |

| $ | (0.02 | ) | | | $ | 0.24 |

| $ | (0.30 | ) |

|

| |

CyrusOne Inc.

Consolidated Balance Sheets

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | |

| | December 31, | December 31, | Change |

| | 2016 | 2015 | $ | % |

| Assets | | | | |

| Investment in real estate: | | | | |

| Land | $ | 142.7 |

| $ | 93.0 |

| $ | 49.7 |

| 53 | % |

| Buildings and improvements | 1,008.9 |

| 905.3 |

| 103.6 |

| 11 | % |

| Equipment | 1,042.9 |

| 598.2 |

| 444.7 |

| 74 | % |

| Construction in progress | 407.1 |

| 231.1 |

| 176.0 |

| 76 | % |

| Subtotal | 2,601.6 |

| 1,827.6 |

| 774.0 |

| 42 | % |

| Accumulated depreciation | (578.5 | ) | (435.6 | ) | (142.9 | ) | 33 | % |

| Net investment in real estate | 2,023.1 |

| 1,392.0 |

| 631.1 |

| 45 | % |

| Cash and cash equivalents | 14.6 |

| 14.3 |

| 0.3 |

| 2 | % |

| Rent and other receivables, net | 83.3 |

| 76.1 |

| 7.2 |

| 9 | % |

| Restricted cash | — |

| 1.5 |

| (1.5 | ) | n/m |

|

| Goodwill | 455.1 |

| 453.4 |

| 1.7 |

| — | % |

| Intangible assets, net | 150.2 |

| 170.3 |

| (20.1 | ) | (12 | )% |

| Other assets | 126.1 |

| 88.0 |

| 38.1 |

| 43 | % |

| Total assets | $ | 2,852.4 |

| $ | 2,195.6 |

| $ | 656.8 |

| 30 | % |

| Liabilities and Equity | | |

|

|

| Accounts payable and accrued expenses | $ | 227.1 |

| $ | 136.6 |

| $ | 90.5 |

| 66 | % |

| Deferred revenue | 76.7 |

| 78.7 |

| (2.0 | ) | (3 | )% |

| Capital lease obligations | 10.8 |

| 12.2 |

| (1.4 | ) | (11 | )% |

| Long-term debt, net | 1,240.1 |

| 996.5 |

| 243.6 |

| 24 | % |

| Lease financing arrangements | 135.7 |

| 150.0 |

| (14.3 | ) | (10 | )% |

| Total liabilities | 1,690.4 |

| 1,374.0 |

| 316.4 |

| 23 | % |

| Equity: |

| |

|

|

| Preferred stock, $.01 par value, 100,000,000 authorized; no shares issued or outstanding | — |

| — |

| — |

| n/m |

|

| Common stock, $.01 par value, 500,000,000 shares authorized and 83,536,250 and 72,556,334 shares issued and outstanding at December 31, 2016 and December 31, 2015, respectively | 0.8 |

| 0.7 |

| 0.1 |

| 14 | % |

| Additional paid in capital | 1,412.3 |

| 967.2 |

| 445.1 |

| 46 | % |

| Accumulated deficit | (249.8 | ) | (145.9 | ) | (103.9 | ) | 71.2 | % |

| Accumulated other comprehensive loss | (1.3 | ) | (0.4 | ) | (0.9 | ) | n/m |

|

| Total stockholders’ equity | 1,162.0 |

| 821.6 |

| 340.4 |

| 41 | % |

| Total liabilities and stockholders’ equity | $ | 2,852.4 |

| $ | 2,195.6 |

| $ | 656.8 |

| 30 | % |

CyrusOne Inc.

Consolidated Statements of Operations

(Dollars in millions, except per share amounts)

(Unaudited)

|

| | | | | | | | | | | | | | | |

| For the three months ended: | December 31, | September 30, | June 30, | March 31, | December 31, |

| | 2016 | 2016 | 2016 | 2016 | 2015 |

| Revenue: | | | | |

|

|

| Base Revenue | $ | 123.2 |

| $ | 128.8 |

| $ | 118.2 |

| $ | 106.5 |

| $ | 101.2 |

|

| Metered Power Reimbursements | 14.2 |

| 15.0 |

| 11.9 |

| 11.3 |

| 12.1 |

|

| Total Revenue | 137.4 |

| 143.8 |

| 130.1 |

| 117.8 |

| 113.3 |

|

| Costs and expenses: | | | | | |

| Property operating expenses | 47.8 |

| 54.6 |

| 44.8 |

| 40.3 |

| 41.4 |

|

| Sales and marketing | 4.0 |

| 4.7 |

| 4.2 |

| 4.0 |

| 3.2 |

|

| General and administrative | 17.9 |

| 13.9 |

| 14.9 |

| 14.0 |

| 15.1 |

|

| Depreciation and amortization | 49.3 |

| 50.6 |

| 44.7 |

| 39.3 |

| 39.9 |

|

| Transaction and acquisition integration costs | 0.4 |

| 1.2 |

| 0.4 |

| 2.3 |

| 2.6 |

|

| Asset impairments and loss on disposal of assets | 5.3 |

| — |

| — |

| — |

| — |

|

| Total costs and expenses | 124.7 |

| 125.0 |

| 109.0 |

| 99.9 |

| 102.2 |

|

| Operating income | 12.7 |

| 18.8 |

| 21.1 |

| 17.9 |

| 11.1 |

|

| Interest expense | 11.4 |

| 13.8 |

| 11.5 |

| 12.1 |

| 12.0 |

|

| Income (loss) before income taxes | 1.3 |

| 5.0 |

| 9.6 |

| 5.8 |

| (0.9 | ) |

| Income tax expense | (0.5 | ) | (0.6 | ) | (0.5 | ) | (0.2 | ) | (0.3 | ) |

| Net income (loss) from continuing operations | 0.8 |

| 4.4 |

| 9.1 |

| 5.6 |

| (1.2 | ) |

| Noncontrolling interest in net income (loss) | — |

| — |

| — |

| — |

| (0.2 | ) |

| Net income (loss) attributed to common stockholders | $ | 0.8 |

| $ | 4.4 |

| $ | 9.1 |

| $ | 5.6 |

| $ | (1.0 | ) |

| Income (loss) per common share - basic and diluted | $ | 0.01 |

| $ | 0.05 |

| $ | 0.11 |

| $ | 0.07 |

| $ | (0.02 | ) |

CyrusOne Inc.

Consolidated Balance Sheets

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | | | | |

| | December 31, 2016 | September 30,

2016 | June 30, 2016 | March 31, 2016 | December 31,

2015 |

| Assets | | | | | |

| Investment in real estate: | | | | | |

| Land | $ | 142.7 |

| $ | 143.1 |

| $ | 122.9 |

| $ | 98.8 |

| $ | 93.0 |

|

| Buildings and improvements | 1,008.9 |

| 1,009.3 |

| 995.2 |

| 942.0 |

| 905.3 |

|

| Equipment | 1,042.9 |

| 976.9 |

| 917.8 |

| 715.6 |

| 598.2 |

|

| Construction in progress | 407.1 |

| 304.0 |

| 178.9 |

| 327.7 |

| 231.1 |

|

| Subtotal | 2,601.6 |

| 2,433.3 |

| 2,214.8 |

| 2,084.1 |

| 1,827.6 |

|

| Accumulated depreciation | (578.5 | ) | (546.4 | ) | (503.2 | ) | (467.2 | ) | (435.6 | ) |

| Net investment in real estate | 2,023.1 |

| 1,886.9 |

| 1,711.6 |

| 1,616.9 |

| 1,392.0 |

|

| Cash and cash equivalents | 14.6 |

| 11.0 |

| 13.2 |

| 87.7 |

| 14.3 |

|

| Rent and other receivables | 83.3 |

| 73.0 |

| 66.4 |

| 67.1 |

| 76.1 |

|

| Restricted cash | — |

| — |

| 0.3 |

| 0.7 |

| 1.5 |

|

| Goodwill | 455.1 |

| 455.1 |

| 453.4 |

| 453.4 |

| 453.4 |

|

| Intangible assets, net | 150.2 |

| 155.8 |

| 160.6 |

| 165.5 |

| 170.3 |

|

| Other assets | 126.1 |

| 114.5 |

| 105.8 |

| 92.2 |

| 88.0 |

|

| Total assets | $ | 2,852.4 |

| $ | 2,696.3 |

| $ | 2,511.3 |

| $ | 2,483.5 |

| $ | 2,195.6 |

|

| Liabilities and Equity | | | | | |

| Accounts payable and accrued expenses | $ | 227.1 |

| $ | 214.6 |

| $ | 163.7 |

| $ | 196.2 |

| $ | 136.6 |

|

| Deferred revenue | 76.7 |

| 72.5 |

| 71.7 |

| 76.4 |

| 78.7 |

|

| Capital lease obligations | 10.8 |

| 11.9 |

| 10.9 |

| 11.5 |

| 12.2 |

|

| Long-term debt | 1,240.1 |

| 1,065.7 |

| 1,096.2 |

| 1,010.3 |

| 996.5 |

|

| Lease financing arrangements | 135.7 |

| 141.9 |

| 144.3 |

| 147.0 |

| 150.0 |

|

| Total liabilities | 1,690.4 |

| 1,506.6 |

| 1,486.8 |

| 1,441.4 |

| 1,374.0 |

|

| Equity: | | | | | |

| Preferred stock, $.01 par value, 100,000,000 authorized; no shares issued or outstanding | — |

| — |

| — |

| — |

| — |

|

| Common stock, $.01 par value, 500,000,000 shares authorized and 83,536,250 and 72,556,334 shares issued and outstanding at December 31, 2016 and December 31, 2015, respectively | 0.8 |

| 0.8 |

| 0.8 |

| 0.8 |

| 0.7 |

|

| Additional paid in capital | 1,412.3 |

| 1,408.9 |

| 1,215.7 |

| 1,212.0 |

| 967.2 |

|

| Accumulated deficit | (249.8 | ) | (218.8 | ) | (191.5 | ) | (170.3 | ) | (145.9 | ) |

| Accumulated other comprehensive loss | (1.3 | ) | (1.2 | ) | (0.5 | ) | (0.4 | ) | (0.4 | ) |

| Total stockholders’ equity | 1,162.0 |

| 1,189.7 |

| 1,024.5 |

| 1,042.1 |

| 821.6 |

|

| Total liabilities and stockholders’ equity | $ | 2,852.4 |

| $ | 2,696.3 |

| $ | 2,511.3 |

| $ | 2,483.5 |

| $ | 2,195.6 |

|

CyrusOne Inc.

Consolidated Statements of Cash Flow

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | |

| | Three Months Ended December 31, 2016 | Three Months Ended December 31, 2015 | Year Ended

December 31, 2016 | December 31, 2015 |

| Cash flows from operating activities: | | | | |

| Net income (loss) | $ | 0.8 |

| $ | (1.2 | ) | $ | 19.9 |

| $ | (20.2 | ) |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | | |

| Depreciation and amortization | 49.3 |

| 39.9 |

| 183.9 |

| 141.5 |

|

| Provision for bad debt | 0.7 |

| (0.3 | ) | 1.6 |

| — |

|

| Asset impairments and loss on disposal | 5.3 |

| — |

| 5.3 |

| 13.5 |

|

| Non-cash interest expense | (6.3 | ) | 1.1 |

| 4.8 |

| 3.4 |

|

| Stock-based compensation expense | 3.8 |

| 3.9 |

| 12.3 |

| 14.4 |

|

| Changes in operating assets and liabilities: | | | | |

| Rent receivables and other assets | (22.7 | ) | (7.0 | ) | (51.7 | ) | (23.9 | ) |

| Accounts payable and accrued expenses | 4.4 |

| (2.9 | ) | 7.0 |

| 7.0 |

|

| Deferred revenues | 3.7 |

| 4.6 |

| (2.5 | ) | 5.4 |

|

| Due to affiliates | — |

| 0.6 |

| — |

| (0.9 | ) |

| Net cash provided by operating activities | 39.0 |

| 38.7 |

| 180.6 |

| 140.2 |

|

| Cash flows from investing activities: | | | | |

| Capital expenditures – purchase of fixed assets | — |

| — |

| (131.1 | ) | (17.3 | ) |

| Capital expenditures – other development | (174.6 | ) | (76.3 | ) | (600.0 | ) | (217.2 | ) |

| Business acquisition, net of cash acquired | — |

| — |

| — |

| (398.4 | ) |

| Changes in restricted cash | — |

| 7.3 |

| 1.5 |

| 7.3 |

|

| Net cash used in investing activities | (174.6 | ) | (69.0 | ) | (729.6 | ) | (625.6 | ) |

| Cash flows from financing activities: | | | | |

| Issuance of common stock | 0.1 |

| 0.2 |

| 448.7 |

| 799.5 |

|

| Stock issuance costs | — |

| — |

| (1.6 | ) | (0.8 | ) |

| Acquisition of operating partnership units | — |

| — |

| — |

| (596.4 | ) |

| Dividends paid | (31.5 | ) | (22.5 | ) | (114.3 | ) | (80.8 | ) |

| Borrowings from credit facility | 180.0 |

| 40.0 |

| 710.0 |

| 260.0 |

|

| Payments on credit facility | — |

| (10.0 | ) | (460.0 | ) | (10.0 | ) |

| Proceeds from issuance of debt | — |

| — |

| — |

| 103.8 |

|

| Payments on capital leases and lease financing arrangements | (2.3 | ) | (2.1 | ) | (9.1 | ) | (5.9 | ) |

| Payment of note payable | — |

| — |

| (1.5 | ) | — |

|

| Debt issuance costs | (6.6 | ) | — |

| (8.7 | ) | (5.4 | ) |

| Tax payments upon exercise of equity awards | (0.5 | ) | (0.8 | ) | (14.2 | ) | (0.8 | ) |

| Net cash provided by financing activities | 139.2 |

| 4.8 |

| 549.3 |

| 463.2 |

|

| Net increase (decrease) in cash and cash equivalents | 3.6 |

| (25.5 | ) | 0.3 |

| (22.2 | ) |

| Cash and cash equivalents at beginning of period | 11.0 |

| 39.8 |

| 14.3 |

| 36.5 |

|

| Cash and cash equivalents at end of period | $ | 14.6 |

| $ | 14.3 |

| $ | 14.6 |

| $ | 14.3 |

|

| | | | | |

|

| | | | | | | | | | | | |

| | Three Months Ended December 31, 2016 | Three Months Ended December 31, 2015 | Year Ended

December 31, 2016 | December 31, 2015 |

| Supplemental disclosures | | | | |

| Cash paid for interest, net of amount capitalized | $ | 21.6 |

| $ | 22.3 |

| $ | 55.0 |

| $ | 43.7 |

|

| Cash paid for income taxes | — |

| 0.9 |

| 1.2 |

| 3.4 |

|

| Capitalized interest | 3.8 |

| 1.9 |

| 10.6 |

| 6.1 |

|

| Non-cash investing and financing activities: | | | | |

| Acquisition and development of properties in accounts payable and other liabilities | | | 132.7 |

| 59.2 |

|

| Dividends payable | | | 33.9 |

| 23.6 |

|

CyrusOne Inc.

Net Operating Income and Reconciliation of Net Income (Loss) to Adjusted EBITDA

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended | | | Three Months Ended |

| | December 31, | Change | December 31, | September 30, | June 30, | March 31, | December 31, |

| | 2016 | 2015 | $ | % | 2016 | 2016 | 2016 | 2016 | 2015 |

| Net Operating Income | | | | | | | | | |

| Revenue | $ | 529.1 |

| $ | 399.3 |

| $ | 129.8 |

| 33% | $ | 137.4 |

| $ | 143.8 |

| $ | 130.1 |

| $ | 117.8 |

| $ | 113.3 |

|

| Property operating expenses | 187.5 |

| 148.7 |

| 38.8 |

| 26% | 47.8 |

| 54.6 |

| 44.8 |

| 40.3 |

| 41.4 |

|

| Net Operating Income (NOI) | 341.6 |

| 250.6 |

| 91.0 |

| 36% | 89.6 |

| 89.2 |

| 85.3 |

| 77.5 |

| 71.9 |

|

| Add Back: Lease exit costs | — |

| 1.4 |

| (1.4 | ) | n/m | — |

| — |

| — |

| — |

| 0.3 |

|

| Adjusted Net Operating Income (Adjusted NOI) | $ | 341.6 |

| $ | 252.0 |

| $ | 89.6 |

| 36% | $ | 89.6 |

| $ | 89.2 |

| $ | 85.3 |

| $ | 77.5 |

| $ | 72.2 |

|

| Adjusted NOI as a % of Revenue | 64.6 | % | 63.1 | % | | | 65.2 | % | 62.0 | % | 65.6 | % | 65.8 | % | 63.7 | % |

| | | | | | | | | | |

| Reconciliation of Net Income (Loss) to Adjusted EBITDA: | | | | | | | | | |

| Net income (loss) | $ | 19.9 |

| $ | (20.2 | ) | $ | 40.1 |

| n/m | 0.8 |

| $ | 4.4 |

| $ | 9.1 |

| $ | 5.6 |

| $ | (1.2 | ) |

| Interest expense | 48.8 |

| 41.2 |

| 7.6 |

| 18% | 11.4 |

| 13.8 |

| 11.5 |

| 12.1 |

| 12.0 |

|

| Income tax expense | 1.8 |

| 1.8 |

| — |

| n/m | 0.5 |

| 0.6 |

| 0.5 |

| 0.2 |

| 0.3 |

|

| Depreciation and amortization | 183.9 |

| 141.5 |

| 42.4 |

| 30% | 49.3 |

| 50.6 |

| 44.7 |

| 39.3 |

| 39.9 |

|

| Transaction and acquisition integration costs | 4.3 |

| 14.1 |

| (9.8 | ) | (70)% | 0.4 |

| 1.2 |

| 0.4 |

| 2.3 |

| 2.6 |

|

| Legal claim costs | 1.1 |

| 0.4 |

| 0.7 |

| n/m | 0.4 |

| 0.2 |

| 0.3 |

| 0.2 |

| 0.1 |

|

| Stock-based compensation | 11.5 |

| 12.0 |

| (0.5 | ) | (4)% | 3.0 |

| 2.3 |

| 3.2 |

| 3.0 |

| 2.4 |

|

| Severance and management transition costs | 1.9 |

| 6.0 |

| (4.1 | ) | (68)% | 1.9 |

| — |

| — |

| — |

| 4.1 |

|

| Lease exit costs | — |

| 1.4 |

| (1.4 | ) | n/m | — |

| — |

| — |

| — |

| 0.3 |

|

| Asset impairments and loss on disposals | 5.3 |

| 13.5 |

| (8.2 | ) | (61)% | 5.3 |

| — |

| — |

| — |

| — |

|

| Adjusted EBITDA | $ | 278.5 |

| $ | 211.7 |

| $ | 66.8 |

| 32% | $ | 73.0 |

| $ | 73.1 |

| $ | 69.7 |

| $ | 62.7 |

| $ | 60.5 |

|

| Adjusted EBITDA as a % of Revenue | 52.6 | % | 53.0 | % | | | 53.1 | % | 50.8 | % | 53.6 | % | 53.2 | % | 53.4 | % |

CyrusOne Inc.

Reconciliation of Revenue to Net Operating Income to Net Income (Loss)

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | | Twelve Months Ended | | |

| | December 31, | Change | December 31, | Change |

| 2016 | 2015 | $ | % | 2016 | 2015 | $ | % |

| Revenue | $ | 137.4 |

| $ | 113.3 |

| $ | 24.1 |

| 21 | % | $ | 529.1 |

| $ | 399.3 |

| $ | 129.8 |

| 33 | % |

| Property operating expenses | 47.8 |

| 41.4 |

| 6.4 |

| 15 | % | 187.5 |

| 148.7 |

| 38.8 |

| 26 | % |

| Net Operating Income | $ | 89.6 |

| $ | 71.9 |

| $ | 17.7 |

| 25 | % | $ | 341.6 |

| $ | 250.6 |

| $ | 91.0 |

| 36 | % |

| Sales and marketing | 4.0 |

| 3.2 |

| 0.8 |

| 25 | % | 16.9 |

| 12.1 |

| 4.8 |

| 40 | % |

| General and administrative | 17.9 |

| 15.1 |

| 2.8 |

| 19 | % | 60.7 |

| 46.6 |

| 14.1 |

| 30 | % |

| Depreciation and amortization | 49.3 |

| 39.9 |

| 9.4 |

| 24 | % | 183.9 |

| 141.5 |

| 42.4 |

| 30 | % |

| Transaction and acquisition integration costs | 0.4 |

| 2.6 |

| (2.2 | ) | (85 | )% | 4.3 |

| 14.1 |

| (9.8 | ) | (70 | )% |

| Asset impairments and loss on disposal | 5.3 |

| — |

| 5.3 |

| n/m |

| 5.3 |

| 13.5 |

| (8.2 | ) | n/m |

|

| Interest expense | 11.4 |

| 12.0 |

| (0.6 | ) | (5 | )% | 48.8 |

| 41.2 |

| 7.6 |

| 18 | % |

| Income tax expense | 0.5 |

| 0.3 |

| 0.2 |

| 67 | % | 1.8 |

| 1.8 |

| — |

| — | % |

| Net Income (Loss) | $ | 0.8 |

| $ | (1.2 | ) | $ | 2.0 |

| n/m |

| $ | 19.9 |

| $ | (20.2 | ) | $ | 40.1 |

| n/m |

|

CyrusOne Inc.

Reconciliation of Net Income (Loss) to FFO and Normalized FFO

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended | | | Three Months Ended |

| | December 31, | Change | December 31, 2016 | September 30, 2016 | June 30, 2016 | March 31, 2016 | December 31,

2015 |

| 2016 | 2015 | $ | % |

| Reconciliation of Net Income (Loss) to FFO and Normalized FFO: | | | | | | | | | |

| Net income (loss) | $ | 19.9 |

| $ | (20.2 | ) | $ | 40.1 |

| n/m |

| $ | 0.8 |

| $ | 4.4 |

| $ | 9.1 |

| $ | 5.6 |

| $ | (1.2 | ) |

| Real estate depreciation and amortization | 157.6 |

| 117.0 |

| 40.6 |

| 35 | % | 42.0 |

| 44.2 |

| 38.4 |

| 33.0 |

| 32.8 |

|

| Asset impairments and loss on disposal | 5.3 |

| 13.5 |

| (8.2 | ) | (61 | )% | 5.3 |

| — |

| — |

| — |

| — |

|

| Funds from Operations (FFO) | $ | 182.8 |

| $ | 110.3 |

| 72.5 |

| 66 | % | $ | 48.1 |

| $ | 48.6 |

| $ | 47.5 |

| $ | 38.6 |

| $ | 31.6 |

|

| | | | | | | | | | |

| Amortization of customer relationship intangibles | 20.1 |

| 18.5 |

| 1.6 |

| 9 | % | 5.6 |

| 4.8 |

| 4.9 |

| 4.8 |

| 5.6 |

|

| Transaction and acquisition integration costs | 4.3 |

| 14.1 |

| (9.8 | ) | (70 | )% | 0.4 |

| 1.2 |

| 0.4 |

| 2.3 |

| 2.5 |

|

| Severance and management transition costs | 1.9 |

| 6.0 |

| (4.1 | ) | (68 | )% | 1.9 |

| — |

| — |

| — |

| 4.1 |

|

| Legal claim costs | 1.1 |

| 0.4 |

| 0.7 |

| n/m |

| 0.4 |

| 0.2 |

| 0.3 |

| 0.2 |

| 0.1 |

|

| Lease exit costs | — |

| 1.4 |

| (1.4 | ) | n/m |

| — |

| — |

| — |

| — |

| 0.3 |

|

| Normalized Funds from Operations (Normalized FFO) | $ | 210.2 |

| $ | 150.7 |

| $ | 59.5 |

| 39 | % | $ | 56.4 |

| $ | 54.8 |

| $ | 53.1 |

| $ | 45.9 |

| $ | 44.2 |

|

| Normalized FFO per diluted common share or common share equivalent | $ | 2.66 |

| $ | 2.17 |

| $ | 0.49 |

| 23 | % | $ | 0.68 |

| $ | 0.67 |

| $ | 0.67 |

| $ | 0.63 |

| $ | 0.61 |

|

| Weighted average diluted common share and common share equivalent outstanding | 79.0 |

| 69.3 |

| 9.7 |

| 14 | % | 82.9 |

| 81.3 |

| 79.0 |

| 72.8 |

| 72.6 |

|

| | | | | | | | | | |

| Additional Information: | | | | | | | | | |

| Amortization of deferred financing costs | 4.1 |

| 3.4 |

| 0.7 |

| 21 | % | 1.1 |

| 1.0 |

| 1.1 |

| 0.9 |

| 1.1 |

|

| Stock-based compensation | 11.5 |

| 12.0 |

| (0.5 | ) | (4 | )% | 3.0 |

| 2.3 |

| 3.2 |

| 3.0 |

| 2.4 |

|

| Non-real estate depreciation and amortization | 6.2 |

| 6.0 |

| 0.2 |

| 3 | % | 1.7 |

| 1.6 |

| 1.4 |

| 1.5 |

| 1.5 |

|

| Deferred revenue and straight line rent adjustments | (20.2 | ) | (2.2 | ) | (18.0 | ) | n/m |

| (2.5 | ) | (10.7 | ) | (5.0 | ) | (2.0 | ) | 1.1 |

|

| Leasing commissions | (12.1 | ) | (6.9 | ) | (5.2 | ) | 75 | % | (3.8 | ) | (3.0 | ) | (3.4 | ) | (1.9 | ) | (3.3 | ) |

| Recurring capital expenditures | (5.4 | ) | (2.4 | ) | (3.0 | ) | 125 | % | (1.9 | ) | (1.7 | ) | (0.9 | ) | (0.9 | ) | (0.7 | ) |

CyrusOne Inc.

Market Capitalization Summary, Reconciliation of Net Debt, and Debt Schedule

(Unaudited)

Market Capitalization

|

| | | | | | | | |

| (dollars in millions) | Shares or Equivalents Outstanding | Market Price as of December 31, 2016 | Market Value Equivalents (in millions) |

| Common shares | 83,536,250 |

| $ | 44.73 |

| $ | 3,736.6 |

|

| Net debt |

|

| 1,258.5 |

|

| Total enterprise value (TEV) | |

| $ | 4,995.1 |

|

Reconciliation of Net Debt

|

| | | | | | |

| (dollars in millions) | December 31, | September 30, |

| | 2016 | 2016 |

Long-term debt(a) | $ | 1,262.3 |

| $ | 1,082.4 |

|

| Capital lease obligations | 10.8 |

| 11.9 |

|

| Less: | | |

| Cash and cash equivalents | (14.6 | ) | (11.0 | ) |

| Net debt | $ | 1,258.5 |

| $ | 1,083.3 |

|

| | | |

(a) Excludes adjustment for deferred financing costs.

| | |

Debt Schedule

|

| | | | | |

| (dollars in millions) | | | |

| Long-term debt: | Amount | Interest Rate | Maturity Date |

| 6.375% senior notes due 2022, including bond premium | 477.3 |

| 6.38 | % | November 2022 |

| Revolving credit facility | 235.0 |

| L + 155 bps |

| November 2021(a) |

| Term loan | 300.0 |

| 2.26 | % | January 2022 |

| Term loan | 250.0 |

| 2.26 | % | September 2021 |

Total long-term debt(b) | 1,262.3 |

| 3.81 | % | |

| | | | |

| Weighted average term of debt: | 5.3 |

| years | |

| |

| (a) | Assuming exercise of one-year extension option. |

| |

| (b) | Excludes adjustment for deferred financing costs. |

CyrusOne Inc.

Colocation Square Footage (CSF) and Utilization

(Unaudited)

|

| | | | | | | | |

| | As of December 31, 2016 | As of December 31, 2015 |

| Market | Colocation

Space (CSF)(a) | CSF

Utilized(b) | Colocation

Space (CSF)(a) | CSF

Utilized(b) |

| Dallas | 431,287 |

| 83 | % | 350,946 |

| 89 | % |

| Cincinnati | 386,508 |

| 92 | % | 419,589 |

| 91 | % |

| Houston | 308,074 |

| 73 | % | 255,094 |

| 88 | % |

| Northern Virginia | 277,629 |

| 100 | % | 74,653 |

| 73 | % |

| Phoenix | 215,892 |

| 94 | % | 149,620 |

| 100 | % |

| Austin | 105,610 |

| 50 | % | 121,833 |

| 51 | % |

| New York Metro | 121,530 |

| 79 | % | 121,434 |

| 87 | % |

| Chicago | 111,660 |

| 82 | % | 23,298 |

| 54 | % |

| San Antonio | 108,112 |

| 99 | % | 43,843 |

| 100 | % |

| International | 13,200 |

| 70 | % | 13,200 |

| 80 | % |

| Total | 2,079,502 |

| 85 | % | 1,573,510 |

| 86 | % |

| Stabilized Properties(c) | 1,895,867 |

| 92 | % | | |

| |

| (a) | CSF represents the NRSF at an operating facility that is currently leased or readily available for lease as colocation space, where customers locate their servers and other IT equipment. |

| |

| (b) | Utilization is calculated by dividing CSF under signed leases for colocation space (whether or not the lease has commenced billing) by total CSF. |

| |

| (c) | Stabilized properties include data halls that have been in service for at least 24 months or are at least 85% utilized. |

CyrusOne Inc.

2017 Guidance

(Unaudited)

|

| | |

| Category | 2016 Results | 2017 Guidance(1) |

| Total Revenue | $529 million | $663 - 678 million |

| Base Revenue | $477 million | $588 - 598 million |

| Metered Power Reimbursements | $52 million | $75 - 80 million |

| Adjusted EBITDA | $279 million | $359 - 369 million |

| Normalized FFO per diluted common share | $2.66 million | $2.85 - 2.95 |

| Capital Expenditures | $600 million | $550 - 600 million |

| Development | $595 million | $545 - 590 million |

| Recurring | $5 million | $5 - 10 million |

(1)Full year 2017 guidance includes the Sentinel data center acquisition and assumes the transaction closes on February 28, 2017.

The annual guidance provided above represents forward-looking statements, which are based on current economic conditions, internal assumptions about the Company's existing customer base and the supply and demand dynamics of the markets in which CyrusOne operates.

CyrusOne does not provide reconciliations for the non-GAAP financial measures included in the annual guidance provided above due to the inherent difficulty in forecasting and quantifying certain amounts that are necessary for such reconciliations, including net income (loss) and adjustments that could be made for transaction and acquisition integration costs, legal claim costs, lease exit costs, asset impairments and loss on disposals and other charges in its reconciliation of historic numbers, the amount of which, based on historical experience, could be significant.

CyrusOne Inc.

Data Center Portfolio

As of December 31, 2016

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | |

| | | | Operating Net Rentable Square Feet (NRSF)(a) | Powered

Shell

Available

for Future

Development

(NRSF)(k) | Available Critical Load Capacity

(MW)(l) |

Stabilized Properties(b) | Metro

Area | Annualized Rent(c) | Colocation Space (CSF)(d) | CSF Leased(e) | CSF

Utilized(f) | Office & Other(g) | Office & Other Leased (h) | Supporting

Infrastructure(i) | Total(j) |

| Dallas - Carrollton | Dallas | $ | 52,567,145 |

| 235,733 |

| 87 | % | 87 | % | 33,238 |

| 96 | % | 90,819 |

| 359,790 |

| 164,000 |

| 26 |

|

| Houston - Houston West I | Houston | 43,469,699 |

| 112,133 |

| 96 | % | 97 | % | 11,163 |

| 99 | % | 37,243 |

| 160,539 |

| 3,000 |

| 28 |

|

| Dallas - Lewisville* | Dallas | 35,957,070 |

| 114,054 |

| 96 | % | 96 | % | 11,374 |

| 89 | % | 54,122 |

| 179,550 |

| — |

| 21 |

|

| Cincinnati - 7th Street*** | Cincinnati | 35,262,055 |

| 178,949 |

| 93 | % | 93 | % | 5,744 |

| 100 | % | 167,241 |

| 351,934 |

| 74,000 |

| 13 |

|

| Northern Virginia - Sterling II | Northern Virginia | 29,582,564 |

| 158,998 |

| 100 | % | 100 | % | 8,651 |

| 100 | % | 55,306 |

| 222,955 |

| — |

| 30 |

|

| Totowa - Madison** | New York Metro | 26,215,274 |

| 51,290 |

| 86 | % | 86 | % | 22,477 |

| 100 | % | 58,964 |

| 132,731 |

| — |

| 6 |

|

| Wappingers Falls I** | New York Metro | 25,706,362 |

| 37,000 |

| 96 | % | 96 | % | 20,167 |

| 97 | % | 15,077 |

| 72,244 |

| — |

| 3 |

|

| Cincinnati - North Cincinnati | Cincinnati | 24,179,133 |

| 65,303 |

| 97 | % | 97 | % | 44,886 |

| 72 | % | 52,950 |

| 163,139 |

| 65,000 |

| 14 |

|

| Houston - Houston West II | Houston | 22,230,045 |

| 79,540 |

| 93 | % | 93 | % | 3,355 |

| 74 | % | 55,023 |

| 137,918 |

| 12,000 |

| 12 |

|

| San Antonio I | San Antonio | 21,531,649 |

| 43,891 |

| 99 | % | 99 | % | 5,989 |

| 83 | % | 45,650 |

| 95,530 |

| 11,000 |

| 12 |

|

| Chicago - Aurora I | Chicago | 21,137,317 |

| 88,362 |

| 92 | % | 92 | % | 34,008 |

| 100 | % | 220,109 |

| 342,479 |

| 27,000 |

| 65 |

|

| Phoenix - Chandler II | Phoenix | 19,896,927 |

| 74,058 |

| 100 | % | 100 | % | 5,639 |

| 38 | % | 25,519 |

| 105,216 |

| — |

| 12 |

|

| Houston - Galleria | Houston | 18,364,625 |

| 63,469 |

| 62 | % | 62 | % | 23,259 |

| 51 | % | 24,927 |

| 111,655 |

| — |

| 14 |

|

| Florence | Cincinnati | 15,689,642 |

| 52,698 |

| 100 | % | 100 | % | 46,848 |

| 87 | % | 40,374 |

| 139,920 |

| — |

| 9 |

|

| Austin II | Austin | 14,330,890 |

| 43,772 |

| 94 | % | 94 | % | 1,821 |

| 100 | % | 22,433 |

| 68,026 |

| — |

| 5 |

|

| San Antonio II | San Antonio | 13,997,234 |

| 64,221 |

| 100 | % | 100 | % | 11,255 |

| 100 | % | 41,127 |

| 116,603 |

| — |

| 12 |

|

| Northern Virginia - Sterling I | Northern Virginia | 13,564,435 |

| 77,961 |

| 98 | % | 99 | % | 5,618 |

| 77 | % | 48,598 |

| 132,177 |

| — |

| 12 |

|

| Phoenix - Chandler I | Phoenix | 12,996,911 |

| 73,921 |

| 92 | % | 92 | % | 34,582 |

| 12 | % | 38,572 |

| 147,075 |

| 31,000 |

| 16 |

|

| Cincinnati - Hamilton* | Cincinnati | 9,103,481 |

| 46,565 |

| 76 | % | 76 | % | 1,077 |

| 100 | % | 35,336 |

| 82,978 |

| — |

| 10 |

|

| Stamford - Riverbend** | New York Metro | 6,944,619 |

| 20,000 |

| 29 | % | 30 | % | — |

| — | % | 8,484 |

| 28,484 |

| — |

| 2 |

|

| Phoenix - Chandler III | Phoenix | 6,744,069 |

| 67,913 |

| 83 | % | 90 | % | 2,440 |

| — | % | 30,415 |

| 100,768 |

| — |

| 14 |

|

| London - Great Bridgewater** | International | 6,246,740 |

| 10,000 |

| 85 | % | 85 | % | — |

| — | % | 514 |

| 10,514 |

| — |

| 1 |

|

| Dallas - Midway** | Dallas | 5,353,920 |

| 8,390 |

| 100 | % | 100 | % | — |

| — | % | — |

| 8,390 |

| — |

| 1 |

|

| Cincinnati - Mason | Cincinnati | 5,284,274 |

| 34,072 |

| 100 | % | 100 | % | 26,458 |

| 98 | % | 17,193 |

| 77,723 |

| — |

| 4 |

|

| Norwalk I** | New York Metro | 3,225,171 |

| 13,240 |

| 79 | % | 79 | % | 4,085 |

| 72 | % | 40,610 |

| 57,935 |

| 87,000 |

| 2 |

|

| Dallas - Marsh** | Dallas | 2,490,522 |

| 4,245 |

| 100 | % | 100 | % | — |

| — | % | — |

| 4,245 |

| — |

| 1 |

|

| Chicago - Lombard | Chicago | 2,323,500 |

| 13,516 |

| 59 | % | 61 | % | 4,115 |

| 100 | % | 12,230 |

| 29,861 |

| 29,000 |

| 3 |

|

| Stamford - Omega** | New York Metro | 1,463,844 |

| — |

| — | % | — | % | 18,552 |

| 87 | % | 3,796 |

| 22,348 |

| — |

| — |

|

| Northern Virginia - Sterling IV | Northern Virginia | 1,296,000 |

| 40,670 |

| 100 | % | 100 | % | 5,523 |

| 100 | % | 32,433 |

| 78,626 |

| 14,000 |

| 6 |

|

| Cincinnati - Blue Ash* | Cincinnati | 560,116 |

| 6,193 |

| 36 | % | 36 | % | 6,821 |

| 100 | % | 2,165 |

| 15,179 |

| — |

| 1 |

|

| Totowa - Commerce** | New York Metro | 557,310 |

| — |

| — | % | — | % | 20,460 |

| 41 | % | 5,540 |

| 26,000 |

| — |

| — |

|

| South Bend - Crescent* | Chicago | 552,737 |

| 3,432 |

| 42 | % | 43 | % | — |

| — | % | 5,125 |

| 8,557 |

| 11,000 |

| 1 |

|

| Houston - Houston West III | Houston | 423,849 |

| — |

| — | % | — | % | 8,495 |

| 100 | % | 10,652 |

| 19,147 |

| 212,000 |

| — |

|

| Singapore - Inter Business Park** | International | 310,346 |

| 3,200 |

| 22 | % | 22 | % | — |

| — | % | — |

| 3,200 |

| — |

| 1 |

|

| South Bend - Monroe | Chicago | 174,907 |

| 6,350 |

| 22 | % | 22 | % | — |

| — | % | 6,478 |

| 12,828 |

| 4,000 |

| 1 |

|

| Cincinnati - Goldcoast | Cincinnati | 96,090 |

| 2,728 |

| — | % | — | % | 5,280 |

| 100 | % | 16,481 |

| 24,489 |

| 14,000 |

| 1 |

|

| Stabilized Properties - Total | | $ | 499,830,472 |

| 1,895,867 |

| 91 | % | 92 | % | 433,380 |

| 79 | % | 1,321,506 |

| 3,650,753 |

| 758,000 |

| 354 |

|

| | | | | | | | | | | | |

Pre-Stabilized Properties(b) | | | | | | | | | | | |

| Austin III | Austin | 5,331,140 |

| 61,838 |

| 17 | % | 20 | % | 15,055 |

| 44 | % | 20,629 |

| 97,522 |

| 67,000 |

| 3 |

|

| Houston - Houston West III (DH #1) | Houston | 894,690 |

| 52,932 |

| 5 | % | 6 | % | — |

| — | % | 23,358 |

| 76,290 |

| — |

| 6 |

|

| Dallas - Carrollton (DH #5) | Dallas | 3,634,126 |

| 68,865 |

| 29 | % | 44 | % | — |

| — | % | 10,539 |

| 79,404 |

| — |

| 6 |

|

| All Properties - Total | | $ | 509,690,428 |

| 2,079,502 |

| 84 | % | 85 | % | 448,435 |

| 74 | % | 1,376,032 |

| 3,903,969 |

| 825,000 |

| 369 |

|

| |

| * | Indicates properties in which we hold a leasehold interest in the building shell and land. All data center infrastructure has been constructed by us and owned by us. |

| |

| ** | Indicates properties in which we hold a leasehold interest in the building shell, land, and all data center infrastructure. |

*** The information provided for the West Seventh Street (7th St.) property includes data for two facilities, one of which we lease and one of which we own.

| |

| (a) | Represents the total square feet of a building under lease or available for lease based on engineers' drawings and estimates but does not include space held for development or space used by CyrusOne. |

| |

| (b) | Stabilized properties include data halls that have been in service for at least 24 months or are at least 85% utilized. Pre-stabilized properties include data halls that have been in service for less than 24 months and are less than 85% utilized. |

| |

| (c) | Represents monthly contractual rent (defined as cash rent including customer reimbursements for metered power) under existing customer leases as of December 31, 2016, multiplied by 12. For the month of December 2016, customer reimbursements were $56.4 million annualized and consisted of reimbursements by customers across all facilities with separately metered power. Customer reimbursements under leases with separately metered power vary from month-to-month based on factors such as our customers' utilization of power and the suppliers' pricing of power. From January 1, 2015 through December 31, 2016, customer reimbursements under leases with separately metered power constituted between 10.6% and 12.6% of annualized rent. After giving effect to abatements, free rent and other straight-line adjustments, our annualized effective rent as of December 31, 2016 was $519.9 million. Our annualized effective rent was greater than our annualized rent as of December 31, 2016 because our positive straight-line and other adjustments and amortization of deferred revenue exceeded our negative straight-line adjustments due to factors such as the timing of contractual rent escalations and customer prepayments for services. |

| |

| (d) | CSF represents the NRSF at an operating facility that is currently leased or readily available for lease as colocation space, where customers locate their servers and other IT equipment. |

| |

| (e) | Percent leased is determined based on CSF being billed to customers under signed leases as of December 31, 2016 divided by total CSF. Leases signed but not commenced as of December 31, 2016 are not included. |

| |

| (f) | Utilization is calculated by dividing CSF under signed leases for colocation space (whether or not the lease has commenced billing) by total CSF. |

| |

| (g) | Represents the NRSF at an operating facility that is currently leased or readily available for lease as space other than CSF, which is typically office and other space. |

| |

| (h) | Percent leased is determined based on Office & Other space being billed to customers under signed leases as of December 31, 2016 divided by total Office & Other space. Leases signed but not commenced as of December 31, 2016 are not included. |

| |

| (i) | Represents infrastructure support space, including mechanical, telecommunications and utility rooms, as well as building common areas. |

| |

| (j) | Represents the NRSF at an operating facility that is currently leased or readily available for lease. This excludes existing vacant space held for development. |

| |

| (k) | Represents space that is under roof that could be developed in the future for operating NRSF, rounded to the nearest 1,000. |

| |

| (l) | Critical load capacity represents the aggregate power available for lease and exclusive use by customers expressed in terms of megawatts. The capacity reported is for non-redundant megawatts, as we can develop flexible solutions to our customers at multiple resiliency levels. Does not sum to total due to rounding. |

CyrusOne Inc.

NRSF Under Development

As of December 31, 2016

(Dollars in millions)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| | | | NRSF Under Development (a) | | Under Development Costs(b) |

| Facilities | Metropolitan

Area | Estimated Completion Date | Colocation Space (CSF) | Office & Other | Supporting Infrastructure | Powered Shell(b) | Total | Critical Load MW Capacity(c) | Actual to Date(d) | Estimated Costs to

Completion(e) | Total |

| Northern Virginia - Sterling III | Northern Virginia | 1Q'17 | 79,000 |

| 7,000 |

| 34,000 |

| — |

| 120,000 |

| 15.0 |

| $ | 56 |

| $27-29 | $83-85 |

| San Antonio III | San Antonio | 1Q'17 | 132,000 |

| 9,000 |

| 43,000 |

| — |

| 184,000 |

| 24.0 |

| 82 |

| 42-46 | 124-128 |

| Chicago - Aurora I | Chicago | 1Q'17 | 25,000 |

| — |

| 3,000 |

| — |

| 28,000 |

| 6.0 |

| 3 |

| 9-10 | 12-13 |

| Phoenix - Chandler IV | Phoenix | 2Q'17 | 73,000 |

| 3,000 |

| 27,000 |

| — |

| 103,000 |

| 12.0 |

| 3 |

| 48-53 | 51-56 |

| Phoenix - Chandler V | Phoenix | 2Q'17 | — |

| — |

| — |

| 185,000 |

| 185,000 |

| — |

| 1 |

| 18-20 | 19-21 |

| Northern Virginia - Sterling IV | Northern Virginia | 2Q'17 | 27,000 |

| — |

| 2,000 |

| — |

| 29,000 |

| 9.0 |

| — |

| 38-41 | 38-41 |

| Northern Virginia - Sterling V | Northern Virginia | 2Q'17 | 81,000 |

| 40,000 |

| 55,000 |

| 459,000 |

| 635,000 |

| 12.0 |

| 5 |

| 113-125 | 118-130 |

| Chicago - Aurora II | Chicago | 2Q'17 | 77,000 |

| 10,000 |

| 14,000 |

| 272,000 |

| 373,000 |

| 10.0 |

| 3 |

| 69-76 | 72-79 |

| Total | | | 494,000 |

| 69,000 |

| 178,000 |

| 916,000 |

| 1,657,000 |

| 88.0 |

| $ | 153 |

| $364-400 | $517-553 |

| |

| (a) | Represents NRSF at a facility for which activities have commenced or are expected to commence in the next two quarters to prepare the space for its intended use. Estimates and timing are subject to change. |

| |

| (b) | Represents NRSF under construction that, upon completion, will be powered shell available for future development into operating NRSF. |

| |

| (c) | Critical load capacity represents the aggregate power available for lease and exclusive use by customers expressed in terms of megawatts. The capacity reported is for non-redundant megawatts, as we can develop flexible solutions to our customers at multiple resiliency levels. Does not sum to total due to rounding. |

| |

| (d) | Actual to date is the cash investment as of December 31, 2016. There may be accruals above this amount for work completed, for which cash has not yet been paid. |

| |

| (e) | Represents management’s estimate of the total costs required to complete the current NRSF under development. There may be an increase in costs if customers require greater power density. |

CyrusOne Inc.

Land Available for Future Development (Acres)

As of December 31, 2016

(Unaudited)

|

| | |

| | As of |

| Market | December 31, 2016 |

| Cincinnati | 98 |

|

| Dallas | — |

|

| Houston | 20 |

|

| Northern Virginia | 16 |

|

| Austin | 22 |

|

| Phoenix | 54 |

|

| San Antonio | 6 |

|

| Chicago | 23 |

|

| New York Metro | — |

|

| International | — |

|

| Total Available | 239 |

|

CyrusOne Inc.

Leasing Statistics - Lease Signings

As of December 31, 2016

(Dollars in thousands)

(Unaudited)

|

| | | | | |

| | | | | | Weighted |

| | Number | Total CSF | Total kW | Total MRR | Average |

| Period | of Leases(a)(f) | Signed(b)(f) | Signed(c)(f) | Signed ($000)(d)(f) | Lease Term(e)(f) |

| 4Q'16 | 358 | 74,000 | 9,038 | $1,590 | 63 |

| Prior 4Q Avg. | 363 | 193,250 | 28,171 | $3,589 | 107 |

| 3Q'16 | 389 | 105,000 | 16,930 | $2,250 | 63 |

| 2Q'16 | 363 | 282,000 | 40,272 | $4,866 | 112 |

| 1Q'16 | 375 | 181,000 | 25,468 | $3,610 | 144 |

| 4Q'15 | 326 | 205,000 | 30,012 | $3,630 | 107 |

| |

| (a) | Number of leases represents each agreement with a customer. A lease agreement could include multiple spaces, and a customer could have multiple leases. |

| |

| (b) | CSF represents the NRSF at an operating facility that is leased as colocation space, where customers locate their servers and other IT equipment. |

| |

| (c) | Represents maximum contracted kW that customers may draw during lease period. Additionally, we can develop flexible solutions for our customers at multiple resiliency levels, and the kW signed is unadjusted for this factor. |

| |

| (d) | Monthly recurring rent is defined as the average monthly contractual rent during the term of the lease. It includes the monthly impact of installation charges of approximately $0.1 million in each quarter. |

| |

| (e) | Calculated on a CSF-weighted basis. |

| |

| (f) | 1Q'16 includes the CME lease. Non-CME signings represent approximately 60% of total CSF, kW, and MRR signed. |

CyrusOne Inc.

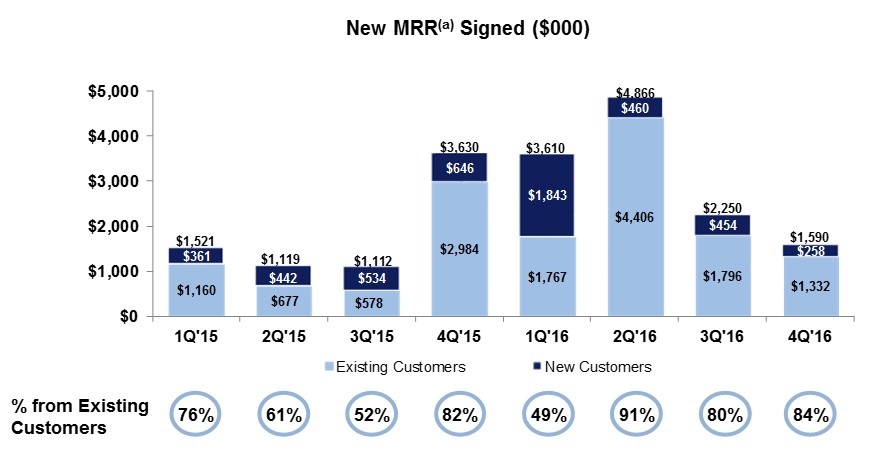

New MRR Signed - Existing vs. New Customers

As of December 31, 2016

(Dollars in thousands)

(Unaudited)

| |

| (a) | Monthly recurring rent is defined as the average monthly contractual rent during the term of the lease. It includes the monthly impact of installation charges of approximately $0.1 million in each of 1Q'15-4Q'16. 1Q'16 includes the CME lease, with non-CME signings representing approximately 60% of total MRR signed. |

CyrusOne Inc.

Customer Sector Diversification(a)

As of December 31, 2016

(Unaudited)

|

| | | | | | | | | |

| | Principal Customer Industry | Number of

Locations | Annualized

Rent(b) | Percentage of

Portfolio

Annualized

Rent(c) | Weighted

Average

Remaining

Lease Term in

Months(d) |

| 1 | Information Technology | 6 | $ | 67,426,116 |

| 13.2 | % | 90.4 |

|

| 2 | Financial Services | 1 | 19,982,174 |

| 3.9 | % | 171.0 |

|

| 3 | Information Technology | 2 | 18,754,830 |

| 3.7 | % | 98.2 |

|

| 4 | Telecommunication Services | 2 | 15,674,018 |

| 3.1 | % | 21.1 |

|

| 5 | Research and Consulting Services | 3 | 14,296,234 |

| 2.8 | % | 48.4 |

|

| 6 | Energy | 5 | 13,205,677 |

| 2.6 | % | 19.1 |

|

| 7 | Energy | 1 | 12,304,605 |

| 2.4 | % | 38.1 |

|

| 8 | Industrials | 4 | 11,412,753 |

| 2.2 | % | 15.8 |

|

| 9 | Telecommunication Services | 7 | 10,442,479 |

| 2.1 | % | 15.5 |

|

| 10 | Information Technology | 2 | 8,876,559 |

| 1.7 | % | 7.7 |

|

| 11 | Energy | 2 | 7,002,022 |

| 1.4 | % | 12.7 |

|

| 12 | Financial Services | 1 | 6,600,225 |

| 1.3 | % | 41.0 |

|

| 13 | Information Technology | 2 | 5,864,871 |

| 1.2 | % | 134.4 |

|

| 14 | Telecommunication Services | 5 | 5,623,136 |

| 1.1 | % | 28.1 |

|

| 15 | Financial Services | 3 | 5,439,249 |

| 1.1 | % | 6.2 |

|

| 16 | Financial Services | 1 | 5,006,844 |

| 1.0 | % | 59.0 |

|

| 17 | Financial Services | 6 | 4,830,345 |

| 0.9 | % | 52.7 |

|

| 18 | Consumer Staples | 2 | 4,820,878 |

| 0.9 | % | 63.6 |

|

| 19 | Consumer Staples | 4 | 4,567,939 |

| 0.9 | % | 49.3 |

|

| 20 | Information Technology | 1 | 4,455,726 |

| 0.9 | % | 101.8 |

|

| | | | $ | 246,586,680 |

| 48.4 | % | 66.4 |

|

| |

| (a) | Customers and their affiliates are consolidated. |

| |

| (b) | Represents monthly contractual rent (defined as cash rent including customer reimbursements for metered power) under existing customer leases as of December 31, 2016, multiplied by 12. For the month of December 2016, customer reimbursements were $56.4 million annualized and consisted of reimbursements by customers across all facilities with separately metered power. Customer reimbursements under leases with separately metered power vary from month-to-month based on factors such as our customers' utilization of power and the suppliers' pricing of power. From January 1, 2015 through December 31, 2016, customer reimbursements under leases with separately metered power constituted between 10.6% and 12.6% of annualized rent. After giving effect to abatements, free rent and other straight-line adjustments, our annualized effective rent as of December 31, 2016 was $519.9 million. Our annualized effective rent was greater than our annualized rent as of December 31, 2016 because our positive straight-line and other adjustments and amortization of deferred revenue exceeded our negative straight-line adjustments due to factors such as the timing of contractual rent escalations and customer prepayments for services. |

| |

| (c) | Represents the customer’s total annualized rent divided by the total annualized rent in the portfolio as of December 31, 2016, which was approximately $509.7 million. |

| |