UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22725

Priority Income Fund, Inc.

(Exact name of registrant as specified in charter)

10 East 40th Street, 42nd Floor

New York, NY 10016

(Address of principal executive offices)

M. Grier Eliasek

Chief Executive Officer

Priority Income Fund, Inc.

10 East 40th Street, 42nd Floor

New York, NY 10016

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 448-0702

Date of fiscal year end: June 30

Date of reporting period: June 30, 2017

Item 1. Report to Stockholders.

The year end report to stockholders for the year ended June 30, 2017 is filed herewith pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended.

Annual Report

June 30, 2017

priority-incomefund.com

Priority Income Fund, Inc. (the “Company”) is an externally managed, non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended. The Company has elected to be treated for tax purposes as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended.

INVESTMENT OBJECTIVE

The Company’s investment objective is to generate current income and, as a secondary objective, long-term capital appreciation. We expect to seek to achieve our investment objective by investing, under normal circumstances, in senior secured loans made to companies whose debt is rated below investment grade or, in limited circumstances, unrated, which we collectively refer to as “Senior Secured Loans,” with an emphasis on current income. Our investments may take the form of the purchase of Senior Secured Loans (either in the primary or secondary markets) or through investments in the equity and junior debt tranches of collateralized loan obligation (“CLO”) vehicles that in turn own pools of Senior Secured Loans. The Company intends to invest in both the primary and secondary markets.

TABLE OF CONTENTS

|

| |

| |

| | |

| Index to Financial Statements | |

| |

| |

| |

| |

| |

| |

| | |

| |

| |

| |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 4

Letter to Stockholders

Dear Stockholders,

We are pleased to present this annual report of Priority Income Fund, Inc. (“we,” “us,” “our,” the “Company” or “Priority”) for the fiscal year ended June 30, 2017. Priority has made regular monthly distributions for each month of the past fourteen quarters and declared bonus distributions for each of the past fourteen quarters. We maintain our optimism about the Company’s performance and investment opportunities that we believe will continue to provide stockholders with current income.

Dividend Policy

As a regulated investment company, the Company is required to pay out distributions as determined in accordance with federal income tax regulations (distributable income), rather than accounting income. In certain periods, we expect our annual distributable income to be higher or lower than our reportable accounting income. Our dividend policy factors in our estimate of our distributable income, which includes interest income from our underlying collateralized loan obligation (“CLO”) equity investments as well as the recognition of certain mark-to-market gains or losses to the extent that the fair market value of our CLO investments is determined to deviate from its adjusted tax basis. As a result, distributions may differ from accounting income, as expressed by net investment income.

Market Commentary

In this annual report, we refer to “Senior Secured Loans” collectively as senior secured loans made to primarily U.S. companies whose debt is rated below investment grade or, in some circumstances, unrated. These investments, which are often referred to as “junk” or “high yield,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be difficult to value and illiquid.

Fiscal year 2017 represented a year where we continued to implement our strategy of making attractive risk-adjusted CLO equity investments allowing us to meet our primary objective of providing our stockholders with current income. Priority accomplished the following in fiscal year 2017: (i) making 29 CLO equity investments totaling $162 million in par value and (ii) continuing to pay a base dividend and bonus dividend totaling 10% based on our original gross offering price. Since our last semi-annual report as of December 31, 2016, Priority made 13 CLO equity investments totaling $86 million.

The first six calendar months of 2017 was the first period when CLO collateral managers were required to comply with risk retention requirements. Risk retention has been a prominent industry topic since October 2014, when the U.S. government published the final regulations and implementation of the Dodd Frank Wall Street Reform and Consumer Protection Act for U.S. CLOs. As mentioned in our last Letter to Stockholders, the new rules apply to all new CLOs issued after December 24, 2016 and require that collateral managers own a minimum of 5% of the assets of each CLO they manage. We have historically sought out collateral managers with substantive stakes in the CLO funds managed by them. We believe our portfolio is well positioned with historically strongly performing collateral managers who we believe are more likely to thrive in a post-risk retention environment.

Despite the implementation of risk retention, U.S. CLO issuance in the first six calendar months of 2017 totaled $51.2 billion, including $33.8 billion in the second quarter of 2017, the highest quarterly amount since the second quarter of 2014.1 The $51.2 billion of issuance was 95% higher than the $26.2 billion of issuance in the first six calendar months of 2016.1 The surge in CLO volume in the first half of 2017 was driven by a combination of the strength in fixed income markets, CLO managers implementing solutions to satisfy risk retention requirements faster than CLO research analysts were expecting, and anemic issuance in the first six calendar months of 2016 due to volatility in fixed income markets. CLO research analysts were expecting $50 to $70 billion of issuance for the calendar year of 2017.2 Given issuance in the first six calendar months of 2017 totaled $51.2 billion, several research analysts have increased their CLO projections for 2017 to range from $80 to $95 billion.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 5

| |

| • | Deutsche Bank: increased from $65 billion to $95 billion3 |

| |

| • | JP Morgan: increased from $50 - $60 billion to $85 - $95 billion4 |

| |

| • | Morgan Stanley; $70 billion to $80 billion5 |

| |

| • | Nomura: $50 - $55 billion to $80 - $85 billion6 |

While issuance in the first six calendar months of 2017 was almost double the amount issued in the first six calendar months of 2016, it still lagged the amount issued in the first six calendar months of 2014 ($61.0 billion) and 2015 ($59.9 billion).1

In addition to the increase in CLO issuance witnessed in the first half of 2017, there was also record amount of CLO refinancings and CLO resets (also known as extensions). A CLO refinancing is an occurrence where all or part of the CLO liabilities are refinanced at a lower spread. The CLO refinancing directly benefits the equity investors in CLOs given such refinancing reduces the spread cost of CLO financing. Given the tightening in spreads across fixed income markets including the CLO liability market, CLO equity investors took advantage of this and refinanced $79 billion of CLOs in 2017 through June 29, 2017, exceeding the $51.2 billion in new issuance.6 Priority refinanced the liabilities in 31 different CLOs in the first six calendar months of 2017, reducing the liability spread by an average of 37.0 basis points. A CLO reset is an occurrence where all of the CLO liabilities are refinanced and the CLO reinvestment period is extended typically by 2 to 5 years. $18 billion of CLOs were reset in 2017 through June 29, 2017.6 In total, $97 billion of CLOs were refinanced and reset through June 29, 2017, easily dwarfing the $41.6 billion total in 2016 and $9.6 billion total in 2015.2

Issuance in the Senior Secured Loan market (including refinancings) got off to a rapid pace in the first quarter of 2017 with $171 billion of issuance, an all-time high.7 The record issuance was primarily driven by $75 billion of refinancings, but also significant increases in issuance for leveraged buyouts, mergers & acquisitions, dividends, and other uses.7 The $171 billion of issuance in the first quarter excludes an additional $169 billion of repricings where corporate borrowers were able to reduce the spread over Libor via an amendment.7 The record new issuance and repricings were largely a function of the supply / demand imbalance in the first quarter as demand for Senior Secured Loans outpaced supply by $31.7 billion.7 This imbalance was driven by $11.4 billion of inflows to retail Senior Secured Loan open-ended mutual funds, $17.4 billion of CLO issuance, and the loan market declining $4.2 billion in size to $876 billion despite the record issuance.8,9

The Senior Secured Loan market slowed down in the second quarter of 2017 from the record-setting pace of the first quarter with $125 billion of issuance, which was still the sixth-highest quarterly total on record.7 In addition, there was still $93 billion of repricings via amendments, but significantly less than the $170 billion of repricings in the first quarter.7 The market cooled down in the second quarter of 2017 as Senior Secured Loan supply exceeded demand by $7.8 billion including $20 billion of excess supply in June 2017.7,10 This excess supply was driven by a $47 billion increase in the outstanding balance of Senior Secured Loans in the second quarter to $925 billion as of June 30, 2017, a record amount.9

Despite the record issuance in the first six calendar months of 2017, the S&P / LSTA Leveraged Loan Index remained relatively flat with a change in value from 98.08% on December 31, 2016 to 98.02% on June 30, 2017.9 The index provided a 1.91% return in the first half of 2017.10

For CLO equity investors, the asset spreads of Senior Secured Loans are an important factor for performance. Short-term CLO equity performance can decline due to periods of downward movement in loan spreads. With the combination of refinancings and repricings, the median weighted average spread of the underlying Senior Secured Loan portfolio in CLOs declined 17 basis points from 3.83% at 12/31/2016 to 3.66% at 6/30/2017.11

Despite the decline in the weighted average spread of the underlying Senior Secured Loan portfolio in CLOs, we continue to believe fundamentals in the CLO market remain solid:

| |

| • | The equity tranches of U.S. cash flow CLOs have delivered over 22.0% annual cash average yields from January 2003 through December 2016.12 |

| |

| • | Default rates for senior secured loans continue to remain below the historical average in the U.S. of 2.27% from January 1, 2003 to June 30, 2017. The market trailing 12-month (“TTM”) default rate on June 30, 2017 was 1.54%, a slight decline from 1.58% on December 31, 2016.7 The TTM default rate of the Senior Secured Loans underlying the CLOs held by Priority at June 30, 2017 stood at 0.60%, substantially below and outperforming the market trailing 12-month default rate of 1.54% as of June 30, 2017. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 6

| |

| • | We believe the continued moderate default environment provides a favorable backdrop to the historically strong cash flow performance of CLO equity tranches. While low current defaults are a positive indicator of credit performance, we are vigilant with respect to market developments in terms of extensions of credit terms and structures at the individual loan level. We believe credit quality has remained acceptable on an absolute and historically relative basis. Market leverage has increased, but generally not to the levels seen in the large private equity leveraged buyouts of 2006-2007 before the last economic recession.1 Overall we believe the health of corporations continued to improve in 2017. According to FACTSET, the S&P 500 is on target to report double-digit earnings growth for the second consecutive quarter.14 Cash flow coverage continues to be solid, as the average ratio of EBITDA less capital expenditures to cash interest increased to 3.05x in the first half of 2017 compared to 2.92x in 2016.1 |

| |

| • | While oil and gas industry concentration in the U.S. high-yield bond market at year end stood at 13.5%, exposure in the Senior Secured Loan market was 3.7%.1,15 Furthermore, Priority’s exposure to the S&P designated oil and gas sector stood at 2.16% in June 2107, down from 2.68% in December 2016, 3.43% in December 2015, and 4.32% in December 2014. We have evaluated in a detailed fashion our oil and gas exposures with our collateral managers, and we continue to actively monitor our positions in this sector. |

Priority’s Net Asset Value per share ("NAV") increased 1.3% from $14.24 at June 30, 2016 to $14.43 at June 30, 2017, representing a 1.6% decline from December 31, 2016. The decline in NAV since December 31, 2016 is primarily a function of the decline in the median weighted average spread of the underlying Senior Secured Loan portfolio in CLOs partially offset by a decline in default rates in the underlying Senior Secured Loan portfolios and decline in CLO liability costs from the 31 refinancings completed in the Priority portfolio.

We believe fundamentals for the investments held by Priority remain strong given (1) Priority’s exposure to the oil and gas sector at year end stood at 2.2% compared to 13.5% in the high-yield bond market, (2) Priority’s portfolio TTM default rate at June 30, 2017 stood at 0.60% (significantly less than the market TTM default rate of 1.54%), and (3) Priority continues to pay a base plus bonus dividend that annualizes to 10% of our original gross offering price.

We believe that the Senior Secured Loan market is well supported by the recovering U.S. economy, solid corporate fundamentals, increased demand for yield in a low interest rate environment, and the continued health of the credit markets.

M. Grier Eliasek

Chief Executive Officer

This letter may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the future performance of Priority Income Fund, Inc. Words such as “believes,” “expects,” and “future” or similar expressions are intended to identify forward-looking statements. Any such statements, other than statements of historical fact, are highly likely to be affected by unknowable future events and conditions, including elements of the future that are or are not under the control of Priority Income Fund, Inc., and that Priority Income Fund, Inc. may or may not have considered. Accordingly, such statements cannot be guarantees or assurances of any aspect of future performance. Actual developments and results may vary materially from any forward-looking statements. Such statements speak only as of the time when made. Priority Income Fund, Inc. undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. We caution investors that the past performance described above is not indicative of future returns. Index and asset class performance quoted above does not reflect the fees, expenses or taxes that a stockholder may incur. The results described above may not be representative of our portfolio.

1 S&P Capital IQ - Leveraged Lending Review 2Q’16.

2 S&P Capital IQ - 2017 CLO Outlook: Regime change in the post risk retention world, December 27, 2016.

3 Deutsche Bank MBS and Securitized Products Outlook, June 28, 2017.

4 J.P. Morgan CLO Midyear 2017 Outlook: Steady as she goes, June 16, 2017.

5 Morgan Stanley 2017 Global Securitized Products Mid-Year Outlook: Diverging Paths, June 16, 2017.

6 Nomura Review of 2017 H1 trends, June 29, 2017.

7 S&P Capital IQ - Wrap Charts 2017 2Q.

8 S&P Capital IQ - LCD Quarterly Review 1Q’17.

9 S&P Capital IQ - S&P LSTA Leveraged Loan Index charts.

10 S&P Capital IQ - U.S. leveraged loans lose 0.04% in June, snapping 15-month win streak, July 5, 2017.

11 Citigroup Global Markets Research, U.S. CLO Scorecard, June 27, 2017.

12 Citigroup Global Markets Research, CLO Equity - Performing as Marketed (January 26, 2011); 2012 Equity Study; Global Structured Credit.

13 S&P Capital IQ - Default Rates.

14 FACTSET Earnings Insight, August 4, 2017.

15 Bank of America Merrill Lynch.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 7

|

| | | | | | | | | | | |

| Portfolio Composition - At a Glance |

| | | | | | | | | |

| Top Ten Holdings | | | | | | | | |

| As of June 30, 2017 | | | | | | | | |

| | | | | | | | | |

| Portfolio Investment | | Investment | | Legal Maturity | | Fair Value | | % of Net Assets |

| OZLM V, Ltd. | | Subordinated Notes | | 1/20/2026 | | $ | 14,351,567 |

| | 5.0 | % |

| Carlyle Global Market Strategies CLO 2014-3, Ltd. | | Subordinated Notes | | 7/27/2026 | | 12,063,963 |

| | 4.2 | % |

| OZLM IX, Ltd. | | Subordinated Notes | | 1/20/2027 | | 11,546,175 |

| | 4.1 | % |

| Madison Park Funding XIV, Ltd. | | Subordinated Notes | | 7/20/2026 | | 11,252,325 |

| | 3.9 | % |

| Madison Park Funding XIII, Ltd. | | Subordinated Notes | | 1/19/2025 | | 10,373,484 |

| | 3.6 | % |

| Octagon Investment Partners XXIII, Ltd. | | Subordinated Notes | | 7/15/2027 | | 9,363,654 |

| | 3.3 | % |

| OZLM VI, Ltd. | | Subordinated Notes | | 4/17/2026 | | 9,044,082 |

| | 3.2 | % |

| OZLM XII, Ltd. | | Subordinated Notes | | 4/30/2027 | | 9,040,505 |

| | 3.2 | % |

| Carlyle Global Market Strategies CLO 2014-1, Ltd. | | Income Notes | | 4/17/2025 | | 8,964,186 |

| | 3.1 | % |

| Cedar Funding IV CLO, Ltd. | | Subordinated Notes | | 10/23/2026 | | 8,834,269 |

| | 3.1 | % |

Portfolio Composition

|

| | |

| Number of Loans Underlying the Company’s CLO Investments | 2,885 |

|

| Dollar Amount of Loans Underlying the Company’s CLO Investments | $42.8 billion |

|

| Percentage of Collateral Underlying the Company’s CLO Investments that are in Default | 0.68% |

|

| Last Twelve Months Default Rate of Collateral Underlying the Company’s CLO Investments | 0.60% |

|

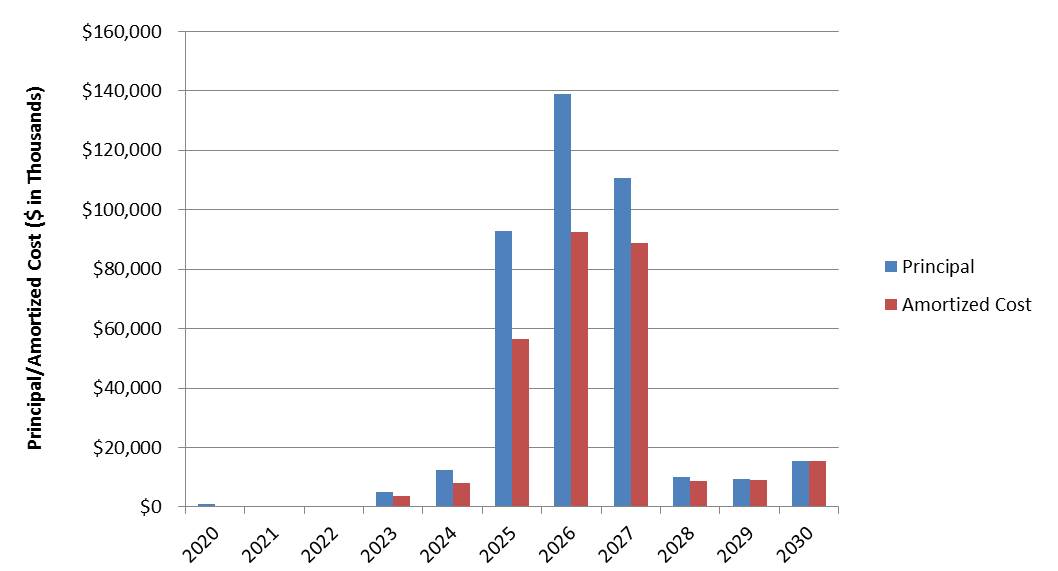

Legal Maturity of Portfolio Securities

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 8

Collateral Summary

|

| | |

| Number of loans underlying the Company’s CLO investments | 2,885 |

|

| Largest exposure to any individual borrower | 0.89 | % |

| Average individual borrower exposure | 0.08 | % |

| Aggregate exposure to 10 largest borrowers | 6.40 | % |

| Aggregate exposure to senior secured loans | 96.47 | % |

| Weighted average stated spread | 3.63 | % |

| Weighted average LIBOR floor | 0.95 | % |

| Weighted average percentage of floating rate loans with LIBOR floors | 77.63 | % |

| Weighted average credit rating of underlying collateral based on average Moody’s rating | B2/B3 |

|

| Weighted average maturity of underlying collateral | 5.0 |

|

| U.S. dollar currency exposure | 100 | % |

|

| | | | | | | |

Underlying Secured Loan Ratings Distribution (Moody’s / S&P)(1) |

| Quarter-End | Aaa/AAA | A/A | Baa/BBB | Ba/BB | B/B | Caa/CCC and Lower | Unrated |

| 6/30/2017 | 0.00% / 0.00% | 0.00% / 0.00% | 2.79% / 1.42% | 29.26% / 23.95% | 58.59% / 64.56% | 5.11% / 4.48% | 1.71% / 3.06% |

(1)Excludes structured product assets and newly issued transactions for which collateral data is not yet available. |

| Cash is included within the denominator of the above calculations, but is not rated by Moody’s/S&P. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 9

Report of Independent Registered Public Accounting Firm

To the Stockholders and Board of Directors of

Priority Income Fund, Inc.

New York, New York

We have audited the accompanying statement of assets and liabilities of Priority Income Fund, Inc. (the “Company”), including the schedule of investments, as of June 30, 2017, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the three years in the period then ended and the period from January 6, 2014 (the date non-affiliate stockholders were admitted into the Company) to June 30, 2014. These financial statements and financial highlights are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of June 30, 2017, by correspondence with the custodian and broker. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Priority Income Fund, Inc. as of June 30, 2017, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the three years in the period then ended and the period from January 6, 2014 (the date non-affiliate stockholders were admitted into the Company) to June 30, 2014, in conformity with accounting principles generally accepted in the United States of America.

/s/ BDO USA, LLP

New York, New York

August 29, 2017

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 10

|

| | | | | | | | |

| Statement of Assets and Liabilities |

| As of June 30, 2017 |

| | | | | | | |

| Assets | |

| Investments, at fair value (amortized cost $282,641,613) | $ | 283,611,208 |

|

| Cash | 13,121,238 |

|

| Receivable for capital shares sold | 1,487,101 |

|

| Interest Receivable | 435,080 |

|

| Deferred offering costs (Note 5) | 299,936 |

|

| Prepaid expenses | 171,649 |

|

| Due from affiliate (Note 5) | 43,377 |

|

| | | | | Total assets | 299,169,589 |

|

| Liabilities | |

| Payable for investment securities purchased | 5,750,000 |

|

| Dividends payable | 3,896,948 |

|

| Due to Adviser (Note 5) | 3,694,251 |

|

| Accrued expenses | 753,830 |

|

| Due to Administrator (Note 5) | 34,059 |

|

| Due to affiliate (Note 5) | 7,155 |

|

| | | | | Total liabilities | 14,136,243 |

|

| Commitments and contingencies (Note 9) | |

| Net assets | $ | 285,033,346 |

|

| | |

| Components of net assets: | |

| Common stock, $0.01 par value; 200,000,000 shares authorized; 18,672,346, 460,788 and 619,951 of | |

| | Class R shares, Class RIA shares and Class I shares issued and outstanding, respectively (Note 4) | $ | 197,531 |

|

| Paid-in capital in excess of par | 264,665,208 |

|

| Accumulated undistributed net investment income | 19,788,883 |

|

| Accumulated net realized loss | (587,871 | ) |

| Net unrealized gain on investments | 969,595 |

|

| Net assets | $ | 285,033,346 |

|

| | | | | | | |

Net asset value per share(1) | $ | 14.43 |

|

| |

(1)Net asset value per share disclosed is the net asset value per share for Class R, Class RIA and Class I shares. |

| |

| See accompanying notes to financial statements. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 11

|

| | | | | | | | |

| Statement of Operations |

| For the year ended June 30, 2017 |

| | |

| Investment income | |

| Interest income from investments | $ | 46,621,367 |

|

| | | | | Total investment income | 46,621,367 |

|

| Expenses | |

| Base management fee (Note 5) | 4,821,337 |

|

| Incentive fee (Note 5) | 7,668,329 |

|

| Total investment advisory fees | 12,489,666 |

|

| | |

| Transfer agent fees and expenses | 795,076 |

|

| Administrator costs (Note 5) | 674,683 |

|

| Audit and tax expense | 576,500 |

|

| Valuation services | 380,445 |

|

| Amortization of offering costs (Note 5) | 375,847 |

|

| Adviser shared service expense (Note 5) | 325,802 |

|

| Legal expense | 205,717 |

|

| General and administrative | 205,558 |

|

| Insurance expense | 202,811 |

|

| Report and notice to shareholders | 189,036 |

|

| Director fees | 105,000 |

|

| Excise tax expense | (202,244 | ) |

| Total expenses | 16,323,897 |

|

| Expense support repayment (Note 5) | 1,441,093 |

|

| Total expenses and expense support repayment | 17,764,990 |

|

| Net investment income | 28,856,377 |

|

| Net realized and unrealized loss on investments | |

| Net realized loss on investments | (849,656 | ) |

| Net decrease in unrealized gain on investments | (2,715,945 | ) |

| Net realized and unrealized loss on investments | (3,565,601 | ) |

| Net increase in net assets resulting from operations | $ | 25,290,776 |

|

| |

| See accompanying notes to financial statements. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 12

|

| | | | | | | | | | | | |

| Statements of Changes in Net Assets |

| | | | | | | | | |

| | | | | | | Year Ended | | Year Ended |

| | | | | | | June 30, 2017 | | June 30, 2016 |

| | | | | | | | | |

| Net increase in net assets resulting from operations: | | | |

| Net investment income | $ | 28,856,377 |

| | $ | 19,238,747 |

|

| Net realized (loss) gain on investments | (849,656 | ) | | 281,673 |

|

| Net (decrease) increase in unrealized gain on investments | (2,715,945 | ) | | 2,279,140 |

|

| | | | | Net increase in net assets resulting from operations | 25,290,776 |

| | 21,799,560 |

|

| Distributions to stockholders: | | | |

| Dividends from net investment income (Note 6) | (14,692,360 | ) | | (14,126,013 | ) |

| Return of capital (Note 6) | (10,126,869 | ) | | — |

|

| | | | | Total distributions to stockholders | (24,819,229 | ) | | (14,126,013 | ) |

| Capital transactions: | | | |

| Gross proceeds from shares sold (Note 4) | 105,828,605 |

| | 108,925,832 |

|

| Commissions and fees on shares sold (Note 5) | (8,169,939 | ) | | (7,930,650 | ) |

| Reinvestment of dividends (Note 4) | 10,211,783 |

| | 7,120,484 |

|

| Repurchase of common shares (Note 4) | (5,588,980 | ) | | (2,544,520 | ) |

| Offering costs (Note 5) | — |

| | (202,011 | ) |

| | | | | Net increase in net assets from capital transactions | 102,281,469 |

| | 105,369,135 |

|

| | | | | Total increase in net assets | 102,753,016 |

| | 113,042,682 |

|

| Net assets: | | | |

| Beginning of year | 182,280,330 |

| | 69,237,648 |

|

End of year (a) | $ | 285,033,346 |

| | $ | 182,280,330 |

|

| | | | | | | | | |

(a)Includes accumulated undistributed net investment income of: | $ | 19,788,883 |

| | $ | 5,457,278 |

|

| |

| See accompanying notes to financial statements. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 13

|

| | | | | | | | |

| Statement of Cash Flows |

| For the year ended June 30, 2017 |

| | | | | | | |

| Cash flows used in operating activities: | |

| Net increase in net assets resulting from operations | $ | 25,290,776 |

|

| Adjustments to reconcile net increase in net assets resulting from operations to | |

| net cash used in operating activities: | |

| Amortization of offering costs | 375,847 |

|

| Purchase of investments | (116,435,679 | ) |

| Sale of distributions received from investments | 2,195,499 |

|

| Net realized loss on investments | 849,656 |

|

| Net decrease in unrealized gain on investments | 2,715,945 |

|

| Amortization of purchase discount, net | 8,906,641 |

|

| (Increase) Decrease in operating assets: | |

| Deferred offering costs | (456,146 | ) |

| Interest receivable | (435,080 | ) |

| Due from affiliate | (43,377 | ) |

| Prepaid expenses | 4,266 |

|

| Increase (Decrease) in operating liabilities: | |

| Payable for investment securities purchased | 5,750,000 |

|

| Due to Adviser | 1,902,276 |

|

| Tax payable | (252,429 | ) |

| Accrued expenses | 363,231 |

|

| Due to Administrator | (17,395 | ) |

| Due to affiliate | 7,155 |

|

| Net cash used in operating activities | (69,278,814 | ) |

| Cash flows provided by financing activities: | |

| Gross proceeds from shares sold | 104,225,250 |

|

| Commissions and fees on shares sold | (8,053,683 | ) |

| Distributions paid to stockholders | (10,710,499 | ) |

| Repurchase of common shares | (5,588,981 | ) |

| Net cash provided by financing activities | 79,872,087 |

|

| Net increase in cash | 10,593,273 |

|

| Cash, beginning of year | 2,527,965 |

|

| Cash, end of year | $ | 13,121,238 |

|

| | |

| Supplemental information | |

| Value of shares issued through reinvestment of dividends | $ | 10,211,783 |

|

| Taxes paid during the year | $ | 50,185 |

|

| |

| See accompanying notes to financial statements. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 14

|

| | | | | | | | | | | | | | |

| Schedule of Investments |

| As of June 30, 2017 |

|

| | | | | | | | | | | | | | | | | | | | | | |

Portfolio Investments(1) | | Investment | | Estimated Yield(2) | | Legal Maturity | | Principal Amount | | Amortized Cost | | Fair Value(3) | | % of Net Assets |

| Collateralized Loan Obligation - Equity Class (Cayman Islands) |

| Adams Mill CLO Ltd. | | Subordinated Notes | | 7.56 | % | | 7/15/2026 | | $ | 500,000 |

| | $ | 376,642 |

| | $ | 299,332 |

| | 0.1 | % |

| Apidos CLO XVIII | | Subordinated Notes | | 11.68 | % | | 7/22/2026 | | 750,000 |

| | 626,207 |

| | 566,378 |

| | 0.2 | % |

| Apidos CLO XXI | | Subordinated Notes | | 15.44 | % | | 7/18/2027 | | 5,000,000 |

| | 4,154,333 |

| | 3,887,879 |

| | 1.4 | % |

Apidos CLO XXII(4) | | Subordinated Notes | | 14.51 | % | | 10/20/2027 | | 3,000,000 |

| | 2,582,864 |

| | 2,433,718 |

| | 0.9 | % |

| Babson CLO Ltd. 2014-II | | Subordinated Notes | | 19.75 | % | | 10/17/2026 | | 1,000,000 |

| | 737,731 |

| | 734,180 |

| | 0.3 | % |

Babson CLO Ltd. 2014-III(4) | | Subordinated Notes | | 15.01 | % | | 1/15/2026 | | 250,000 |

| | 201,435 |

| | 186,609 |

| | 0.1 | % |

| Babson CLO Ltd. 2015-I | | Subordinated Notes | | 14.72 | % | | 4/20/2027 | | 3,000,000 |

| | 2,340,364 |

| | 2,171,502 |

| | 0.8 | % |

| BlueMountain CLO 2012-1 Ltd. | | Subordinated Notes | | 12.20 | % | | 7/20/2023 | | 5,000,000 |

| | 3,680,079 |

| | 3,647,362 |

| | 1.3 | % |

| BlueMountain CLO 2012-2 Ltd. | | Subordinated Notes | | 14.31 | % | | 11/20/2028 | | 3,000,000 |

| | 2,504,260 |

| | 2,056,556 |

| | 0.7 | % |

| BlueMountain CLO 2013-2 Ltd. | | Subordinated Notes | | 21.02 | % | | 1/22/2025 | | 1,900,000 |

| | 1,406,863 |

| | 1,456,796 |

| | 0.5 | % |

| BlueMountain CLO 2014-1 Ltd. | | Subordinated Notes | | 15.61 | % | | 4/30/2026 | | 250,000 |

| | 195,981 |

| | 177,144 |

| | 0.1 | % |

California Street CLO XI Limited Partnership(5) | | LP Certificates | | 24.90 | % | | 1/17/2025 | | 18,330,000 |

| | 7,555,834 |

| | 7,754,555 |

| | 2.7 | % |

| California Street CLO XII, Ltd. | | Subordinated Notes | | 20.25 | % | | 10/15/2025 | | 14,500,000 |

| | 9,157,475 |

| | 8,646,949 |

| | 3.0 | % |

| Carlyle Global Market Strategies CLO 2013-1, Ltd. | | Subordinated Notes | | 27.80 | % | | 2/14/2025 | | 10,000,000 |

| | 7,527,249 |

| | 7,583,134 |

| | 2.7 | % |

| Carlyle Global Market Strategies CLO 2013-4, Ltd. | | Income Notes | | 20.82 | % | | 10/15/2025 | | 8,000,000 |

| | 5,172,402 |

| | 5,008,530 |

| | 1.8 | % |

| Carlyle Global Market Strategies CLO 2014-1, Ltd. | | Income Notes | | 33.49 | % | | 4/17/2025 | | 12,870,000 |

| | 7,131,542 |

| | 8,964,186 |

| | 3.1 | % |

| Carlyle Global Market Strategies CLO 2014-3, Ltd. | | Subordinated Notes | | 21.89 | % | | 7/27/2026 | | 15,000,000 |

| | 11,552,851 |

| | 12,063,963 |

| | 4.2 | % |

| Carlyle Global Market Strategies CLO 2016-1, Ltd. | | Subordinated Notes | | 20.41 | % | | 4/20/2027 | | 6,500,000 |

| | 5,163,896 |

| | 5,863,917 |

| | 2.1 | % |

Carlyle Global Market Strategies CLO 2016-3, Ltd.(4) | | Subordinated Notes | | 15.04 | % | | 10/20/2029 | | 1,400,000 |

| | 1,367,339 |

| | 1,162,813 |

| | 0.4 | % |

| Cedar Funding IV CLO, Ltd. | | Subordinated Notes | | 14.63 | % | | 10/23/2026 | | 9,592,857 |

| | 9,471,225 |

| | 8,834,269 |

| | 3.1 | % |

Cent CLO 21 Limited(4) | | Subordinated Notes | | 15.47 | % | | 7/27/2026 | | 500,000 |

| | 377,686 |

| | 372,757 |

| | 0.1 | % |

CIFC Funding 2006-II, Ltd.(5) | | Preferred Notes | | — | % | | 3/1/2021 | | 406,629 |

| | — |

| | 1,924 |

| | — | % |

| CIFC Funding 2012-II, Ltd. | | Subordinated Notes | | — | % | | 12/5/2024 | | 6,000,000 |

| | 3,804,120 |

| | 3,194,283 |

| | 1.1 | % |

| CIFC Funding 2013-II, Ltd. | | Income Notes | | 10.44 | % | | 4/21/2025 | | 250,000 |

| | 172,952 |

| | 158,131 |

| | 0.1 | % |

| CIFC Funding 2014, Ltd. | | Income Notes | | 20.89 | % | | 4/18/2025 | | 2,250,000 |

| | 1,484,313 |

| | 1,662,725 |

| | 0.6 | % |

| CIFC Funding 2014-III, Ltd. | | Income Notes | | 19.11 | % | | 7/22/2026 | | 11,700,000 |

| | 7,441,261 |

| | 6,681,183 |

| | 2.3 | % |

CIFC Funding 2014-IV, Ltd.(4) | | Income Notes | | 20.94 | % | | 10/17/2026 | | 4,000,000 |

| | 2,440,132 |

| | 2,808,531 |

| | 1.0 | % |

| CIFC Funding 2015-I, Ltd. | | Subordinated Notes | | 21.19 | % | | 1/22/2027 | | 7,500,000 |

| | 5,635,458 |

| | 5,935,731 |

| | 2.1 | % |

| CIFC Funding 2015-IV, Ltd. | | Subordinated Notes | | 17.00 | % | | 10/20/2027 | | 9,100,000 |

| | 7,377,459 |

| | 8,211,819 |

| | 2.9 | % |

CIFC Funding 2016-I, Ltd.(4) | | Subordinated Notes | | 16.33 | % | | 10/21/2028 | | 2,000,000 |

| | 1,869,031 |

| | 1,736,049 |

| | 0.6 | % |

| CIFC Funding 2017-I, Ltd. | | Subordinated Notes | | 15.90 | % | | 4/21/2029 | | 8,000,000 |

| | 7,700,924 |

| | 7,803,982 |

| | 2.7 | % |

Covenant Credit Partners CLO II, Ltd.(6) | | Subordinated Notes | | 15.47 | % | | 10/17/2026 | | 4,392,156 |

| | 3,005,453 |

| | 2,925,579 |

| | 1.0 | % |

Galaxy XVII CLO, Ltd.(4) | | Subordinated Notes | | 10.16 | % | | 7/15/2026 | | 250,000 |

| | 184,710 |

| | 168,108 |

| | 0.1 | % |

| Galaxy XVIII CLO, Ltd. | | Subordinated Notes | | 18.62 | % | | 10/15/2026 | | 1,250,000 |

| | 762,014 |

| | 780,929 |

| | 0.3 | % |

Galaxy XIX CLO, Ltd.(4) | | Subordinated Notes | | 17.89 | % | | 1/24/2027 | | 2,750,000 |

| | 1,827,950 |

| | 1,581,994 |

| | 0.6 | % |

GoldenTree 2013-7A(4) | | Subordinated Notes | | 21.10 | % | | 4/25/2025 | | 4,250,000 |

| | 2,705,927 |

| | 2,353,137 |

| | 0.8 | % |

Halcyon Loan Advisors Funding 2014-2 Ltd.(4) | | Subordinated Notes | | 14.48 | % | | 4/28/2025 | | 400,000 |

| | 267,911 |

| | 270,806 |

| | 0.1 | % |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 15

|

| | | | | | | | | | | | | | | | | | | | | | |

Portfolio Investments(1) | | Investment | | Estimated Yield(2) | | Legal Maturity | | Principal Amount | | Amortized Cost | | Fair Value(3) | | % of Net Assets |

| Collateralized Loan Obligation - Equity Class (Cayman Islands) |

| Halcyon Loan Advisors Funding 2014-3 Ltd. | | Subordinated Notes | | 16.24 | % | | 10/22/2025 | | $ | 500,000 |

| | $ | 358,973 |

| | $ | 314,164 |

| | 0.1 | % |

| Halcyon Loan Advisors Funding 2015-1 Ltd. | | Subordinated Notes | | 15.70 | % | | 4/20/2027 | | 3,000,000 |

| | 2,167,152 |

| | 2,051,182 |

| | 0.7 | % |

| Halcyon Loan Advisors Funding 2015-2 Ltd. | | Subordinated Notes | | 17.02 | % | | 7/25/2027 | | 3,000,000 |

| | 2,341,512 |

| | 2,369,192 |

| | 0.8 | % |

Halcyon Loan Advisors Funding 2015-3 Ltd.(4) | | Subordinated Notes | | 15.09 | % | | 10/18/2027 | | 7,000,000 |

| | 6,046,688 |

| | 6,176,300 |

| | 2.2 | % |

Halcyon Loan Investors CLO I, Ltd.(5) | | Income Notes | | — | % | | 11/20/2020 | | 504,000 |

| | 27,571 |

| | 47,375 |

| | — | % |

HarbourView CLO VII, Ltd.(4) | | Subordinated Notes | | 19.27 | % | | 11/18/2026 | | 275,000 |

| | 216,117 |

| | 203,040 |

| | 0.1 | % |

Jefferson Mill CLO Ltd.(4) | | Subordinated Notes | | 10.46 | % | | 7/20/2027 | | 5,000,000 |

| | 4,230,680 |

| | 3,463,262 |

| | 1.2 | % |

| LCM XV Limited Partnership | | Income Notes | | 11.23 | % | | 7/20/2030 | | 250,000 |

| | 185,617 |

| | 151,985 |

| | 0.1 | % |

| LCM XVI Limited Partnership | | Income Notes | | 13.84 | % | | 7/15/2026 | | 5,000,000 |

| | 3,690,407 |

| | 3,305,382 |

| | 1.2 | % |

| LCM XVII Limited Partnership | | Income Notes | | 12.09 | % | | 10/15/2026 | | 500,000 |

| | 420,160 |

| | 365,307 |

| | 0.1 | % |

Madison Park Funding XIII, Ltd.(4) | | Subordinated Notes | | 26.86 | % | | 1/19/2025 | | 13,000,000 |

| | 9,090,530 |

| | 10,373,484 |

| | 3.6 | % |

Madison Park Funding XIV, Ltd.(4) | | Subordinated Notes | | 22.54 | % | | 7/20/2026 | | 12,500,000 |

| | 9,804,121 |

| | 11,252,325 |

| | 3.9 | % |

| Madison Park Funding XV, Ltd. | | Subordinated Notes | | 25.18 | % | | 1/27/2026 | | 3,000,000 |

| | 2,181,844 |

| | 2,548,080 |

| | 0.9 | % |

MC Funding Ltd.(5) | | Preferred Notes | | — | % | | 12/20/2020 | | 387,965 |

| | 24,541 |

| | 43,637 |

| | — | % |

| Mountain View CLO 2014-1 Ltd. | | Income Notes | | 10.58 | % | | 10/15/2026 | | 1,000,000 |

| | 678,852 |

| | 557,456 |

| | 0.2 | % |

Mountain View CLO IX Ltd.(4) | | Subordinated Notes | | 14.70 | % | | 7/15/2027 | | 5,000,000 |

| | 4,268,415 |

| | 4,166,567 |

| | 1.5 | % |

Ocean Trails CLO II(5) | | Subordinated Notes | | — | % | | 6/27/2022 | | 367,064 |

| | 25,940 |

| | 32,268 |

| | — | % |

Octagon Investment Partners XVIII, Ltd.(4) | | Subordinated Notes | | 15.05 | % | | 12/16/2024 | | 2,800,000 |

| | 1,844,441 |

| | 1,729,187 |

| | 0.6 | % |

| Octagon Investment Partners XX, Ltd. | | Subordinated Notes | | 9.14 | % | | 8/12/2026 | | 500,000 |

| | 390,210 |

| | 298,306 |

| | 0.1 | % |

Octagon Investment Partners XXI, Ltd.(4) | | Subordinated Notes | | 29.93 | % | | 11/14/2026 | | 10,700,000 |

| | 6,376,045 |

| | 7,533,030 |

| | 2.6 | % |

| Octagon Investment Partners XXII, Ltd. | | Subordinated Notes | | 20.77 | % | | 11/25/2025 | | 6,500,000 |

| | 4,554,921 |

| | 4,338,582 |

| | 1.5 | % |

| Octagon Investment Partners XXIII, Ltd. | | Subordinated Notes | | 24.31 | % | | 7/15/2027 | | 12,000,000 |

| | 9,038,747 |

| | 9,363,654 |

| | 3.3 | % |

| Octagon Loan Funding, Ltd. | | Subordinated Notes | | 14.92 | % | | 11/18/2026 | | 2,550,000 |

| | 1,946,263 |

| | 1,729,898 |

| | 0.6 | % |

| OZLM V, Ltd. | | Subordinated Notes | | 26.94 | % | | 1/20/2026 | | 25,000,000 |

| | 13,887,152 |

| | 14,351,567 |

| | 5.0 | % |

| OZLM VI, Ltd. | | Subordinated Notes | | 22.06 | % | | 4/17/2026 | | 15,688,991 |

| | 9,843,881 |

| | 9,044,082 |

| | 3.2 | % |

| OZLM VII, Ltd. | | Subordinated Notes | | 23.52 | % | | 7/17/2026 | | 2,450,000 |

| | 1,583,859 |

| | 1,588,113 |

| | 0.6 | % |

| OZLM VIII, Ltd. | | Subordinated Notes | | 16.95 | % | | 10/17/2026 | | 750,000 |

| | 541,238 |

| | 583,120 |

| | 0.2 | % |

| OZLM IX, Ltd. | | Subordinated Notes | | 19.76 | % | | 1/20/2027 | | 15,000,000 |

| | 11,758,074 |

| | 11,546,175 |

| | 4.1 | % |

OZLM XII, Ltd.(4) | | Subordinated Notes | | 14.53 | % | | 4/30/2027 | | 12,122,952 |

| | 9,598,416 |

| | 9,040,505 |

| | 3.2 | % |

| Regatta IV Funding Ltd. | | Subordinated Notes | | 12.14 | % | | 7/25/2026 | | 250,000 |

| | 175,990 |

| | 171,921 |

| | 0.1 | % |

Symphony CLO XIV, Ltd.(4) | | Subordinated Notes | | 10.46 | % | | 7/14/2026 | | 750,000 |

| | 557,738 |

| | 513,873 |

| | 0.2 | % |

| Symphony CLO XVI, Ltd. | | Subordinated Notes | | 13.45 | % | | 7/15/2028 | | 5,000,000 |

| | 4,363,193 |

| | 4,108,597 |

| | 1.4 | % |

Voya IM CLO 2013-1, Ltd.(4) | | Income Notes | | 19.17 | % | | 4/15/2024 | | 3,750,000 |

| | 2,318,387 |

| | 2,176,678 |

| | 0.8 | % |

| Voya IM CLO 2013-3, Ltd. | | Subordinated Notes | | 20.01 | % | | 1/18/2026 | | 4,000,000 |

| | 2,632,139 |

| | 2,543,436 |

| | 0.9 | % |

Voya IM CLO 2014-1, Ltd.(4) | | Subordinated Notes | | 15.96 | % | | 4/18/2026 | | 250,000 |

| | 190,013 |

| | 202,094 |

| | 0.1 | % |

| Voya CLO 2014-3, Ltd. | | Subordinated Notes | | 17.77 | % | | 7/25/2026 | | 7,000,000 |

| | 4,192,603 |

| | 3,935,714 |

| | 1.4 | % |

| Voya CLO 2014-4, Ltd. | | Subordinated Notes | | 19.25 | % | | 10/14/2026 | | 1,000,000 |

| | 809,012 |

| | 765,271 |

| | 0.3 | % |

| Voya CLO 2015-2, Ltd. | | Subordinated Notes | | 13.49 | % | | 7/23/2027 | | 500,000 |

| | 414,063 |

| | 383,234 |

| | 0.1 | % |

Voya CLO 2016-1, Ltd.(4) | | Subordinated Notes | | 17.33 | % | | 1/20/2027 | | 6,250,000 |

| | 4,987,007 |

| | 5,464,953 |

| | 1.9 | % |

Voya CLO 2016-3, Ltd.(4) | | Subordinated Notes | | 12.55 | % | | 10/18/2027 | | 5,000,000 |

| | 4,826,379 |

| | 4,180,895 |

| | 1.5 | % |

Voya CLO 2017-3, Ltd.(4) | | Subordinated Notes | | 14.79 | % | | 7/20/2030 | | 5,750,000 |

| | 5,750,000 |

| | 5,722,477 |

| | 2.0 | % |

Washington Mill CLO Ltd.(4) | | Subordinated Notes | | 8.54 | % | | 4/20/2026 | | 400,000 |

| | 295,755 |

| | 251,019 |

| | 0.1 | % |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 16

|

| | | | | | | | | | | | | | | | | | | | | | |

Portfolio Investments(1) | | Investment | | Estimated Yield(2) | | Legal Maturity | | Principal Amount | | Amortized Cost | | Fair Value(3) | | % of Net Assets |

| Collateralized Loan Obligation - Equity Class (Cayman Islands) |

| West CLO 2014-1 Ltd. | | Subordinated Notes | | 19.37 | % | | 7/18/2026 | | $ | 5,375,000 |

| | $ | 4,043,094 |

| | $ | 4,476,381 |

| | 1.6 | % |

| Total Portfolio Investments | | | | | | $ | 282,641,613 |

| | $ | 283,611,208 |

| | 99.5 | % |

| Other assets in excess of liabilities | | | | | | | | 1,422,138 |

| | 0.5 | % |

| Net Assets | | | | | | | | $ | 285,033,346 |

| | 100.0 | % |

|

| | | | | | | | | | | | | | |

(1) The Company does not "control" and is not an "affiliate" of any of the portfolio investments, each term as defined in the Investment Company Act of 1940, as amended (the "1940 Act"). In general, under the 1940 Act, the Company would be presumed to "control" a portfolio company if the Company owned 25% or more of its voting securities and would be an "affiliate" of a portfolio company if the Company owned 5% or more of its voting securities. |

(2) The CLO subordinated notes/securities/fee notes, income notes and preferred shares are considered equity positions in the CLOs. The CLO equity investments are entitled to recurring distributions, which are generally equal to the excess cash flow generated from the underlying investments after payment of the contractual payments to senior debt holders and fund expenses. The current estimated yield indicated is based on the current projections of this excess cash flow taking into account assumptions which have been made regarding expected prepayments, losses and reinvestment rates. These assumptions are periodically reviewed and adjusted. Ultimately, the actual yield may be higher or lower than the estimated yield if actual results differ from those used for the assumptions. |

(3) Fair value is determined by or under the direction of the Company’s Board of Directors. As of June 30, 2017, all of the Company’s investments were classified as Level 3. ASC 820 classifies such unobservable inputs used to measure fair value as Level 3 within the valuation hierarchy. See Notes 2 and 3 within the accompanying notes to financial statements for further discussion. |

(4) Co-investment with other funds managed by an affiliate of the Company’s investment adviser, Priority Senior Secured Management, LLC, which is registered as an investment adviser under the Investment Advisers Act of 1940, as amended. See Note 5. |

(5) Security was called for redemption and the liquidation of the underlying loan portfolio is ongoing. |

(6) Principal amount of subordinated notes and subordinated fee note is $4,000,000 and $392,156, respectively. |

| | | | | | | | | | | | | | | |

| See accompanying notes to financial statements. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 17

Notes to Financial Statements

June 30, 2017

Note 1. Principal Business and Organization

Priority Income Fund, Inc., (the “Company,” “us,” “our,” or “we”) was incorporated under the general corporation laws of the State of Maryland on July 19, 2012 as an externally managed, nondiversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”), and commenced operations on May 9, 2013. In addition, the Company has elected to be treated for tax purposes as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). The Company’s investment objective is to generate current income, and as a secondary objective, long-term capital appreciation. We seek to achieve our investment objective by investing, under normal circumstances, in senior secured loans made to companies whose debt is rated below investment grade or, in limited circumstances, unrated (“Senior Secured Loans”) with an emphasis on current income. Our investments may take the form of the purchase of Senior Secured Loans (either in the primary or secondary markets) or through investments in the equity and junior debt tranches of collateralized loan obligation (“CLO”) vehicles that in turn own pools of Senior Secured Loans. The Company intends to invest in both the primary and secondary markets.

The Company is managed by Priority Senior Secured Income Management, LLC (the “Adviser”), which is registered as an investment adviser under the Investment Advisers Act of 1940, as amended. The Adviser is 50% owned by Prospect Capital Management, L.P. (“PCM”) and 50% by Stratera Holdings, LLC (“Stratera Holdings”).

The Company is offering up to 100,000,000 shares of its common stock, on a best efforts basis. The Company commenced the offering on May 9, 2013, at an initial offering price of $15.00 per share, for an initial offering period of 36 months from the date of the commencement of the offering. On January 6, 2014, the Company satisfied its minimum offering requirement by raising over $2.5 million from selling shares to persons not affiliated with the Company or the Adviser (the “Minimum Offering Requirement”), and as a result, broke escrow and commenced making investments.

On February 9, 2016 the Company’s Board of Directors approved an 18-month extension to the offering period for the sale of shares through November 9, 2017. Subsequently, on May 30, 2017, our Board of Directors approved a continuation of this offering for an additional two years, extending this offering until the earlier of (i) November 2, 2019, or (ii) the date upon which 150,000,000 shares have been sold in the course of the offering of the Company's shares, unless further extended by our Board of Directors.

Note 2. Summary of Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Company in the preparation of its financial statements.

Basis of Presentation

The accompanying financial statements have been prepared in accordance with U.S. generally accepted accounting principles(“U.S. GAAP”) pursuant to the requirements of ASC 946, Financial Services - Investment Companies (“ASC 946”), and Articles 6 and 12 of Regulation S-X.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income, expenses and gains (losses) during the reporting period. Actual results could differ from those estimates and those differences could be material.

Cash

Cash are funds deposited with financial institutions.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 18

Investment Valuation

The Company follows guidance under U.S. GAAP, which classifies the inputs used to measure fair values into the following hierarchy:

Level 1. Unadjusted quoted prices in active markets for identical assets or liabilities that the Company has the ability to access at the measurement date.

Level 2. Quoted prices for similar assets or liabilities in active markets, or quoted prices for identical or similar assets or liabilities on an inactive market, or other observable inputs other than quoted prices.

Level 3. Unobservable inputs for the asset or liability.

In all cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers factors specific to each investment.

Investments for which market quotations are readily available are valued at such market quotations and are classified in Level 1 of the fair value hierarchy.

U.S. government securities for which market quotations are available are valued at a price provided by an independent pricing agent or primary dealer. The pricing agent or primary dealer provides these prices usually after evaluating inputs including yield curves, credit rating, yield spreads, default rates, cash flows, broker quotes and reported trades. U.S. government securities are categorized in Level 2 of the fair value hierarchy.

With respect to investments for which market quotations are not readily available, or when such market quotations are deemed not to represent fair value, the board of directors (the “Board”) has approved a multi-step valuation process for each quarter, as described below, and such investments are classified in Level 3 of the fair value hierarchy:

| |

| 1. | Each portfolio investment is reviewed by investment professionals of the Adviser with the independent valuation firms engaged by the Board. |

| |

| 2. | The independent valuation firms prepare independent valuations based on their own independent assessments and issue their report. |

| |

| 3. | The Audit Committee of the Board (the “Audit Committee”) reviews and discusses with the independent valuation firms the valuation reports, and then makes a recommendation to the Board of the value for each investment. |

| |

| 4. | The Board discusses valuations and determines the fair value of such investments in the Company’s portfolio in good faith based on the input of the Adviser, the respective independent valuation firm and the Audit Committee. |

The Company's investments in CLOs are classified as Level 3 fair value measured securities under ASC 820 and are valued primarily using a discounted multi-path cash flow model. The CLO structures are analyzed to identify the risk exposures and appropriate call date (i.e., expected maturity). These risk factors are sensitized using Monte Carlo simulations to generate probability-weighted (i.e., multi-path) cash flows for the underlying assets and liabilities. These cash flows are discounted using appropriate market discount rates, and relevant data in the CLO market and certain benchmark credit indices are considered, to determine the value of each CLO investment. In addition, the Company generates a single-path cash flow utilizing our best estimate of expected cash receipts, and assesses the reasonableness of the discount rate that would be effective for the corresponding multi-path estimate of value. The Company is not responsible for and has no influence over the asset management of the portfolios underlying the CLO investments the Company holds as those portfolios are managed by non-affiliated third party CLO collateral managers. The main risk factors are: default risk, interest rate risk, downgrade risk, and credit spread risk.

The types of factors that are taken into account in fair value determination include, as relevant, market changes in expected returns for similar investments, performance improvement or deterioration, the nature and realizable value of any collateral, the issuer’s ability to make payments and its earnings and cash flows, the markets in which the issuer does business, comparisons to traded securities, and other relevant factors.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 19

Securities Transactions

Securities transactions are recorded on trade date. Realized gains or losses on investments are calculated by using the specific identification method. In accordance with ASC 325-40, Beneficial Interest in Securitized Financial Assets, investments in CLOs are periodically assessed for other-than-temporary impairment (“OTTI”). When the Company determines that a CLO has OTTI, the amortized cost basis of the CLO is written down to it’s fair value as of the date of the determination based on events and information evaluated and that write-down is recognized as a realized loss.

Revenue Recognition

Interest income from investments in the “equity” positions of CLOs (typically income notes, subordinated notes or preferred shares) is recorded based on an estimation of an effective yield to expected maturity utilizing assumed future cash flows. The Company monitors the expected cash inflows from CLO equity investments, including the expected residual payments, and the estimated effective yield is updated periodically.

Offering Costs

Offering costs prior to the commencement of operations were capitalized on the Company’s Statement of Assets and Liabilities as deferred charges until operations began. Thereafter, deferred offering costs were amortized as an expense over a twelve month period on a straight-line basis. The Company charged all offering costs incurred after the commencement of operations and through December 31, 2015 against paid-in capital in excess of par on the Statement of Assets and Liabilities. After discussions with the Staff of the Division of Investment Management of the SEC, the Company decided to change its accounting treatment of offering costs, effective January 1, 2016, and capitalize such costs on the Statement of Assets and Liabilities and amortize them to expense over the 12 month period following such capitalization on a straight line basis. The Company evaluated this change in accounting treatment of offering costs and determined that it did not have a material impact on the Company’s financial statements.

Offering expenses consist of costs for the registration, certain marketing and distribution of the Company’s shares. These expenses include, but are not limited to, expenses for legal, accounting, printing and certain marketing, and include salaries and direct expenses of the Adviser’s employees, employees of its affiliates and others for providing these services.

Due to Adviser

Amounts due to our Adviser consist of expense support reimbursement, base management fees, incentive fees, routine non-compensation overhead, operating expenses paid on behalf of the Company and offering and organization expenses paid on behalf of the Company. All balances due to the Adviser are settled quarterly.

Dividends and Distributions

Dividends and distributions to stockholders, which are determined in accordance with federal income tax regulations, are recorded on the record date. The amount to be paid out as a dividend or distribution is approved by the Board. Net realized capital gains, if any, are generally distributed or deemed distributed at least annually.

Income Taxes

The Company has elected to be treated as a RIC for U.S. federal income tax purposes and intends to comply with the requirement of the Code applicable to RICs. The Company is required to distribute at least 90% of its investment company taxable income and intends to distribute (or retain through a deemed distribution) all of the Company’s investment company taxable income and net capital gain to stockholders; therefore, the Company has made no provision for income taxes. The character of income and gains that the Company will distribute is determined in accordance with income tax regulations that may differ from U.S. GAAP. Book and tax basis differences relating to stockholder dividends and distributions and other permanent book and tax differences are reclassified to paid-in capital.

As of June 30, 2017, the cost basis of investments for tax purposes was $262,393,056 resulting in estimated gross unrealized appreciation and depreciation of $27,864,253 and $6,648,023 respectively.

If the Company does not distribute (or are not deemed to have distributed) at least 98% of its calendar year ordinary income and 98.2% of its capital gains in the calendar year earned, the Company will generally be required to pay an excise tax equal to 4% of the amount by which 98% of its calendar year ordinary income and 98.2% of its capital gains exceed the distributions from such taxable income for the year. To the extent that the Company determines that its estimated current calendar year taxable income will be in excess of estimated current calendar year dividend distributions from such taxable income, the Company accrues excise taxes, if any, on estimated excess taxable income. As of and for the calendar year ended December 31, 2016, we determined that the Company met the distribution requirements and therefore was not required to pay excise tax. As of June 30, 2017, we do not expect to have any excise tax due for 2017 calendar year. Thus, we have not accrued any excise tax for this period. For the year ended June 30, 2017, we reversed our previous excise tax accrual of $202,244.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 20

If the Company fails to satisfy the annual distribution requirement or otherwise fails to qualify as a RIC in any taxable year, the

Company would be subject to tax on all of its taxable income at regular corporate rates. The Company would not be able to deduct distributions to stockholders, nor would the Company be required to make distributions. Distributions would generally be taxable to the Company’s individual and other non-corporate taxable stockholders as ordinary dividend income to the extent of the Company’s current and accumulated earnings and profits, provided certain holding period and other requirements are met. However, such ordinary dividends would not be eligible for the reduced tax rate applicable to qualified dividend income. Subject to certain limitations under the Code, corporate distributions would be eligible for the dividends-received deduction. To qualify again to be taxed as a RIC in a subsequent year, the Company would be required to distribute to its stockholders the Company’s accumulated earnings and profits attributable to non-RIC years reduced by an interest charge of 50% of such earnings and profits payable by us as an additional tax. In addition, if the Company failed to qualify as a RIC for a period greater than two taxable years, then, in order to qualify as a RIC in a subsequent year, the Company would be required to elect to recognize and pay tax on any net built-in gain (the excess of aggregate gain, including items of income, over aggregate loss that would have been realized if the Company had been liquidated) or, alternatively, be subject to taxation on such built-in gain recognized for a period of ten years.

In September 2016, the IRS and U.S. Treasury Department issued proposed regulations that, if finalized, would provide that the income inclusions from a Passive Foreign Investment Company (“PFIC”) with a Qualified Electing Fund (“QEF”) or a Controlled Foreign Corporation (“CFC”) would not be good income for purposes of the 90% Income Test unless the Company receives a cash distribution from such entity in the same year attributable to the included income. If such income were not considered “good income” for purposes of the 90% income test, the Company may fail to qualify as a RIC.

It is unclear whether or in what form these regulations will be adopted or, if adopted, whether such regulations would have a significant impact on the income that could be generated by the Company. If adopted, the proposed regulations would apply to taxable years of the Company beginning on or after 90 days after the regulations are published as final. The Company is monitoring the status of the proposed regulations and is assessing the potential impact of the proposed tax regulation on its operations.

The Company follows ASC 740, Income Taxes (“ASC 740”). ASC 740 provides guidance for how uncertain tax positions should be recognized, measured, presented, and disclosed in the financial statements. ASC 740 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Company’s tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than not threshold are recorded as a tax benefit or expense in the current year. As of June 30, 2017 and for the year then ended, the Company did not have a liability for any unrecognized tax benefits, respectively. Management has analyzed the Company’s positions taken and expected to be taken on its income tax returns for all open tax years and for the year ended June 30, 2017 and has concluded that as of June 30, 2017 no provision for uncertain tax position is required in the Company’s financial statements. Our determinations regarding ASC 740 may be subject to review and adjustment at a later date based upon factors including, but not limited to, an on-going analysis of tax laws, regulations and interpretations thereof. All federal and state income tax returns for each tax year in the three-year period ended June 30, 2017 remain subject to examination by the Internal Revenue Service and state departments of revenue.

Recent Accounting Pronouncement

In August 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update 2014-15, Disclosure

of Uncertainties about an Entity’s Ability to Continue as a Going Concern (“ASU 2014-15”). ASU 2014-15 will explicitly require management to assess an entity’s ability to continue as a going concern, and to provide related footnote disclosure in certain circumstances. ASU 2014-15 is effective for annual and interim periods ending after December 15, 2016. Early application is permitted. The adoption of the amended guidance in ASU 2014-15 is not expected to have a significant effect on the Company’s financial statements and disclosures.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”), which amends the financial instruments impairment guidance so that an entity is required to measure expected credit losses for financial assets based on historical experience, current conditions and reasonable and supportable forecasts. As such, an entity will use forward-looking information to estimate credit losses. ASU 2016-13 also amends the guidance in FASB ASC Subtopic No. 325-40, Investments-Other, Beneficial Interests in Securitized Financial Assets, related to the subsequent measurement of accretable yield recognized as interest income over the life of a beneficial interest in securitized financial assets under the effective yield method. ASU 2016-13 is effective for financial statements issued for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. Early adoption is permitted as of the fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. We are currently evaluating the impact, if any, of adopting this ASU on our financial statements.

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 21

In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments (“ASU 2016-15”), which addresses certain aspects of cash flow statement classification. One such amendment requires cash payments for debt prepayment or debt extinguishment costs to be classified as cash outflows for financing activities. ASU 2016-15 is effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. Early adoption is permitted, including adoption in an interim period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period. An entity that elects early adoption must adopt all of the amendments in the same period. The adoption of the amended guidance in ASU 2016-15 is not expected to have a significant effect on our financial statements and disclosures.

In October 2016, the SEC adopted significant reforms under the 1940 Act that impose extensive new disclosure and reporting obligations on most 1940 Act funds (collectively, the “Reporting Rules”). The Reporting Rules greatly expand the volume of information regarding fund portfolio holdings and investment practices that must be disclosed. The adopted amendments to Regulation S-X for 1940 Act funds require quarterly filings of Form N-Q and additional information to be disclosed in the semi-annual Form N-CEN filing (among other changes). The amendments to Regulation S-X are effective for reporting periods ending after August 1, 2017, and adoption of the amended reform is not expected to have a significant effect on our consolidated financial statements and disclosures.

Note 3. Portfolio Investments

Purchases of investment securities (excluding short-term securities) for year ended June 30, 2017 were $116,435,679. Six investments were called for redemption during the year ended June 30, 2017 and the liquidation of the underlying portfolios is ongoing. During the year ended June 30, 2017, the Company recorded OTTI on four of these investments and two investments called in the prior year, resulting in realized losses of $1,273,540. The Company received $565 from a liquidating payment on an investment that was written-off for tax purposes prior to the year ended June 30, 2017, which resulted in a realized gain.

The following table summarizes the inputs used to value the Company’s investments measured at fair value as of June 30, 2017:

|

| | | | | | | | | | | | | | | |

| | Level 1 | | Level 2 | | Level 3 | | Total |

| Assets | | | | | | | |

| Collateralized Loan Obligations - Equity Class | $ | — |

| | $ | — |

| | $ | 283,611,208 |

| | $ | 283,611,208 |

|

The following is a reconciliation of investments for which Level 3 inputs were used in determining fair value:

|

| | | |

| | Collateralized Loan Obligation - Equity Class |

| Fair value at June 30, 2016 | $ | 181,843,270 |

|

| Net realized loss on investments | (849,656 | ) |

| Net decrease in unrealized gain on investments | (2,715,945 | ) |

| Purchases of investments | 116,435,679 |

|

| Sales of and distributions received from investments | (2,195,499 | ) |

| Amortization of purchase discount, net | (8,906,641 | ) |

Transfers into Level 3(1) | — |

|

Transfers out of Level 3(1) | — |

|

| Fair value at June 30, 2017 | $ | 283,611,208 |

|

| | |

| Net decrease in unrealized gain attributable to Level 3 investments still held at the end of the period | $ | (2,851,062 | ) |

| | |

(1) There were no transfers between Level 1 and Level 2 during the year. |

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 22

The following table provides quantitative information about significant unobservable inputs used in the fair value measurement of Level 3 investments as of June 30, 2017:

|

| | | | | | | | | | | | |

| | | | | | | Unobservable Input |

| Asset Category | | Fair Value | | Primary Valuation Technique | | Input | | Range(1) | | Weighted Average(1) |

| Collateral Loan Obligations - Equity Class | | $ | 283,611,208 |

| | Discounted Cash Flow | | Discount Rate | | 13.09% - 29.75% | | 19.44% |

(1) Excludes investments that have been called for redemption.

In determining the range of values for the Company's investments in CLOs, management and the independent valuation firm use primarily a discounted multi-path cash flow model. The valuations were accomplished through the analysis of the CLO deal structures to identify the risk exposures from the modeling point of view as well as to determine an appropriate call date (i.e., expected maturity). These risk factors are sensitized using Monte Carlo simulations to generate probability-weighted (i.e., multipath) cash flows for the underlying assets and liabilities. These cash flows are discounted using appropriate market discount rates, and relevant data in the CLO market and certain benchmark credit indices are considered, to determine the value of each CLO investment. In addition, we generate a single-path cash flow utilizing our best estimate of expected cash receipts, and assess the reasonableness of the implied discount rate that would be effective for the value derived from the corresponding multi-path cash flow model.

The significant unobservable input used to value the CLOs is the discount rate applied to the estimated future cash flows expected to be received from the underlying investment, which includes both future principal and interest payments. Included in the consideration and selection of the discount rate are the following factors: risk of default, comparable investments, and call provisions. An increase or decrease in the discount rate applied to projected cash flows, where all other inputs remain constant, would result in a decrease or increase, respectively, in the fair value measurement.

The Company is not responsible for and have no influence over the management of the portfolios underlying the CLO investments the Company holds as those portfolios are managed by non-affiliated third party CLO collateral managers. CLO investments may be riskier and less transparent to the Company than direct investments in underlying companies. CLOs typically will have no significant assets other than their underlying senior secured loans. Therefore, payments on CLO investments are and will be payable solely from the cash flows from such senior secured loans.

The Company’s portfolio consists of residual interests investments in CLOs, which involve a number of significant risks. CLOs are typically very highly levered (10 - 14 times), and therefore the residual interest tranches that the Company invests in are subject to a higher degree of risk of total loss. In particular, investors in CLO residual interests indirectly bear risks of the underlying loan investments held by such CLOs. The Company generally have the right to receive payments only from the CLOs, and generally do not have direct rights against the underlying borrowers or the entity that sponsored the CLO. While the CLOs the Company targets generally enable the investor to acquire interests in a pool of senior loans without the expenses associated with directly holding the same investments, the Company’s prices of indices and securities underlying CLOs will rise or fall. These prices (and, therefore, the values of the CLOs) will be influenced by the same types of political and economic events that affect issuers of securities and capital markets generally. The failure by a CLO investment in which the Company invest to satisfy financial covenants, including with respect to adequate collateralization and/or interest coverage tests, could lead to a reduction in its payments to the Company. In the event that a CLO fails certain tests, holders of debt senior to the Company may be entitled to additional payments that would, in turn, reduce the payments the Company would otherwise be entitled to receive. Separately, the Company may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting CLO or any other investment the Company may make. If any of these occur, it could materially and adversely affect the Company’s operating results and cash flows.

The interests the Company have acquired in CLOs are generally thinly traded or have only a limited trading market. CLOs are typically privately offered and sold, even in the secondary market. As a result, investments in CLOs may be characterized as illiquid securities. In addition to the general risks associated with investing in debt securities, CLO residual interests carry additional risks, including, but not limited to: (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) the fact that the Company’s investments in CLO tranches will likely be subordinate to other senior classes of note tranches thereof; and (iv) the complex structure of the security may not be fully understood at the time of investment and may produce disputes with the CLO investment or unexpected investment results. The Company’s net asset value may also decline over time if the Company’s principal recovery with respect to CLO residual interests is less than the price that the Company paid for those investments. The Company’s CLO

2017 ANNUAL REPORT

PRIORITY INCOME FUND, INC. 23

investments and/or the underlying senior secured loans may prepay more quickly than expected, which could have an adverse impact on its value.

An increase in LIBOR would materially increase the CLO’s financing costs. Since most of the collateral positions within the CLOs have LIBOR floors, there may not be corresponding increases in investment income (if LIBOR increases but stays below the LIBOR floor rate of such investments) resulting in materially smaller distribution payments to the residual interest investors.