Michael J. Swidler mswidler@velaw.com

Tel +1.212.237.0020 Fax +1.917.849.5367

January 3, 2012

Via EDGAR and Federal Express

Erin Jaskot

Staff Attorney

Division of Corporation Finance

United States Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | SunCoke Energy Partners, L.P. | |

| Amendment No. 9 to Registration Statement on Form S-1 | ||

| File No. 333-183162 |

Dear Ms. Jaskot:

Pursuant to discussions with the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”), we hereby submit on behalf of SunCoke Energy Partners, L.P. (the “Partnership”) the proposed offering terms of its initial public offering (the “IPO”), including the bona fide price range pursuant to Item 501(b)(3) of Regulation S-K. These pricing terms shall be included in Amendment No. 9 to Registration Statement on Form S-1, File No. 333-183162 (the “IPO Registration Statement”), to be filed with the Commission on or about January 8, 2013. The provided terms are a bona fide estimate of the range of the maximum offering price and the maximum number of securities offered as of January 3, 2012. Should the bona fide estimates of these terms change between today and January 8, 2013, the figures presented in Amendment No. 9 may increase or decrease accordingly.

The Partnership proposes to price the IPO with a bona fide price range of $19.00 to $21.00, with a midpoint of $20.00. The IPO will include the offering of 13,500,000 common units representing limited partner interests in the Partnership. As discussed with members of the Staff, this range is initially being provided for your consideration by correspondence given the Partnership’s and the underwriters’ concern regarding providing such information significantly in advance of the launch of the offering given recent market volatility as well as our desire to provide all information necessary for the Staff to complete its review on a timely basis.

Vinson & Elkins LLP Attorneys at Law Abu Dhabi Austin Beijing Dallas Dubai Hong Kong Houston London Moscow New York Palo Alto Riyadh San Francisco Shanghai Tokyo Washington | 666 Fifth Avenue, 26th Floor New York, NY 10103-0040 Tel +1.212.237.0000Fax +1.212.237.0100www.velaw.com |

| Securities and Exchange Commission January 3, 2013 Page 2 |

Additionally, the Partnership is enclosing its proposed marked copy of those pages of the IPO Registration Statement that will be affected by the offering terms set forth herein. These marked changes will be incorporated into Amendment No. 9 to be filed with the Commission on or about January 8, 2013.

The Partnership seeks confirmation from the Staff that it may launch its IPO with the price range specified herein and include such price range in Amendment No. 9, to be filed with the Commission on or about January 8, 2013.

Please direct any questions that you have with respect to the foregoing to the undersigned at (212) 237-0020 or to Mike Rosenwasser at (212) 237-0019 or Rachel Packer at (212) 237-0187.

(The remainder of this page is intentionally left blank.)

Very truly yours,

/s/ Michael Swidler

Michael Swidler

| cc: | Tracey Smith (Commission) |

| Al Pavot (Commission) |

| Craig E. Slivka (Commission) |

| Pamela A. Long (Commission) |

| Denise R. Cade (Registrant) |

| Sean T. Wheeler (Latham & Watkins LLP) |

| Divakar Gupta (Latham & Watkins LLP) |

As filed with the Securities and Exchange Commission on January , 2013

Registration No. 333-183162

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 9

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

SunCoke Energy Partners, L.P.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 3312 | 35-2451470 | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

1011 Warrenville Road, Suite 600 Lisle, Illinois 60532

(630) 824-1000

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Denise R. Cade, Esq.

Senior Vice President, General Counsel and Corporate Secretary

1011 Warrenville Road, Suite 600 Lisle, Illinois 60532

(630) 824-1000

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

Mike Rosenwasser Michael Swidler Tel: (212) 237-0000 Fax: (212) 237-0100 | Sean T. Wheeler Divakar Gupta |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ¨ | |||

Non-accelerated filer x | (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated , 2013

| PR | OSPECTUS |

SunCoke Energy Partners, L.P.

13,500,000 Common Units

Representing Limited Partner Interests

This is the initial public offering of our common units representing limited partner interests. We are offering 13,500,000 common units. Prior to this offering, there has been no public market for our common units. We currently expect the initial public offering price to be between $19.00 and $21.00 per common unit. We have been approved to list our common units on the New York Stock Exchange under the symbol “SXCP.”

Investing in our common units involves risks.Please read “Risk Factors” beginning on page 20.

These risks include the following:

| • | We may not generate sufficient earnings from operations to enable us to pay the minimum quarterly distribution to our unitholders. We would not have generated sufficient earnings on a pro forma basis to have paid any distribution on our units for the year ended December 31, 2011 or the twelve months ended September 30, 2012. |

| • | All of our sales are generated at two facilities. Any adverse developments at either facility could have a material adverse effect on our results of operations and therefore our ability to distribute cash to unitholders. |

| • | All of our coke sales are made under long-term contracts with two customers. Any adverse developments with either of these customers could have a material adverse effect on our cash flows, financial position and results of operations. |

| • | Excess capacity in the global steel industry, including in China, may weaken demand for steel produced by our customers, which, in turn, may reduce demand for our coke. |

| • | SunCoke Energy, Inc. owns and controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including SunCoke Energy, Inc., have conflicts of interest with us and limited duties, and they may favor their own interests to the detriment of us and our unitholders. |

| • | Unitholders will experience immediate and substantial dilution of $2.12 per common unit. |

| • | Our tax treatment depends on our status as a partnership for U.S. federal income tax purposes, as well as our not being subject to a material amount of entity-level taxation by individual states. If the IRS were to treat us as a corporation for federal income tax purposes or we were to become subject to material additional amounts of entity-level taxation for state tax purposes, then our results of operations and therefore our ability to distribute cash to unitholders could be substantially reduced. |

| • | There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may not develop. The price of our common units may fluctuate significantly, and unitholders could lose all or part of their investment. |

In addition, we qualify as an “emerging growth company” as defined in Section 2(a)(19) of the Securities Act of 1933 and, as such, are allowed to provide in this prospectus more limited disclosures than an issuer that would not so qualify. Furthermore, for so long as we remain an emerging growth company, we will qualify for certain limited exceptions from investor protection laws such as the Sarbanes Oxley Act of 2002 and the Investor Protection and Securities Reform Act of 2010. Please read “Risk Factors” and “Summary—Emerging Growth Company Status.”

| Per Common Unit | Total | |||||||

Public Offering Price | $ | $ | ||||||

Underwriting Discount(1) | $ | $ | ||||||

Proceeds to SunCoke Energy Partners, L.P. (before expenses) | $ | $ | ||||||

| (1) | Excludes a structuring fee of 0.6250% of the gross proceeds of this offering payable to Barclays Capital Inc. and Evercore Group L.L.C. Please read “Underwriting.” |

The underwriters may purchase up to an additional 2,025,000 common units from us at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover over-allotments.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Barclays expects to deliver the common units to purchasers on or about , 2013 through the book-entry facilities of The Depository Trust Company.

| Barclays | BofA Merrill Lynch | Citigroup |

| Credit Suisse | J.P. Morgan |

| Evercore Partners | Goldman, Sachs & Co. | RBC Capital Markets | UBS Investment Bank |

Prospectus dated , 2013

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical and pro forma financial statements and the notes to those financial statements, before investing in our common units. The information presented in this prospectus assumes an initial public offering price of $20.00 per common unit (the mid-point of the price range set forth on the cover page of this prospectus) and, unless otherwise indicated, that the underwriters’ option to purchase additional common units is not exercised and that the common units otherwise issuable upon the exercise of such option are instead issued to our sponsor, SunCoke Energy, Inc. You should read “Risk Factors” for information about important risks that you should consider before buying our common units.

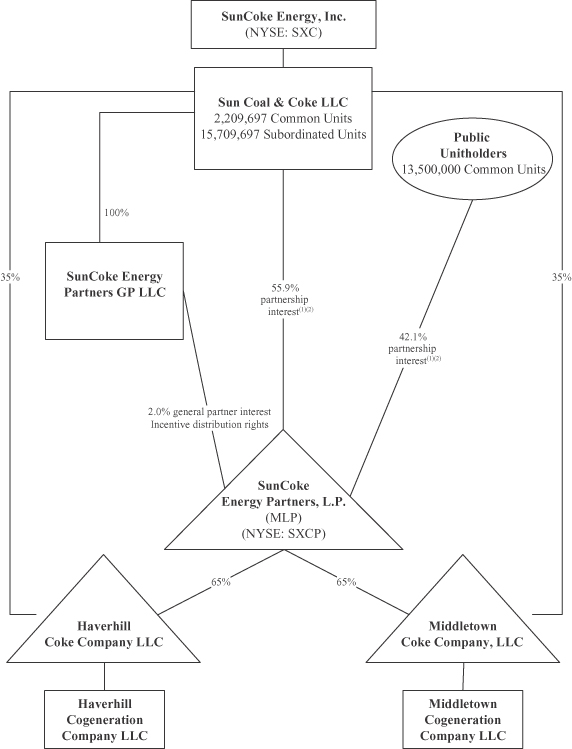

SunCoke Energy Partners, L.P. has been recently formed to acquire, at the closing of this offering, an interest in each of two entities that own two cokemaking facilities and related assets from SunCoke Energy, Inc., who we refer to as “our sponsor”, which will result in us owning a 65% interest in each of these entities. Throughout this document we often refer to ourselves as if we currently operate these two facilities. Following this offering, our sponsor will control our operations and will own our general partner and approximately 57.0% of our limited partner interests and all of our incentive distribution rights. Our financial statements have been prepared by carving out the financial statements relating to these two cokemaking facilities and related assets from the financial statements of our sponsor. As a result, a number of allocations and estimates were required in preparing our financial statements which may not be reflective of our actual operations following completion of this offering.

Unless the context otherwise requires, references in this prospectus to “the Predecessor,” “we,” “our,” “us,” or like terms, when used in a historical context refer to the cokemaking operations and related assets of our sponsor’s Haverhill Coke Company LLC facility located in Franklin Furnace, Ohio, or Haverhill, and Middletown Coke Company, LLC facility located in Middletown, Ohio, or Middletown. We refer to Haverhill Coke Company LLC and Middletown Coke Company, LLC as our “operating subsidiaries.” SunCoke Energy Partners, L.P. does not have any employees, and we are managed by our general partner, the executive officers of which are employees of our sponsor. Unless the context otherwise requires, references in this prospectus to “our employees” refer to employees of our sponsor, and references to “our officers” and “our directors” refer to the officers and directors of our general partner. We have included a glossary of industry terms in Appendix A and a glossary of limited partnership agreement terms in Appendix B.

We have been recently formed to acquire, at the closing of this offering, an interest in each of two entities that own our sponsor’s Haverhill and Middletown cokemaking facilities and related assets, which will result in us owning a 65% interest in each of these entities. The Haverhill and Middletown facilities have a combined 300 cokemaking ovens with an aggregate capacity of approximately 1.7 million tons per year and an average age of four years. We currently operate at full capacity and expect to sell an aggregate of approximately 1.7 million tons of coke per year to two primary customers: AK Steel Corporation, or AK Steel, and ArcelorMittal USA, Inc., or ArcelorMittal. All of our coke sales are made pursuant to long-term take-or-pay agreements. These coke sales agreements have an average remaining term of approximately 13 years and contain pass-through provisions for costs we incur in the cokemaking process, including coal procurement costs, subject to meeting contractual coal-to-coke yields, operating and maintenance expenses, costs related to the transportation of coke to our customers, taxes (other than income taxes) and costs associated with changes in regulation.

Coke is a principal raw material in the blast furnace steelmaking process. Coke is generally produced by heating metallurgical coals in a refractory oven to approximately 2,000 degrees Fahrenheit, which releases certain volatile components from the coal, thus transforming the coal into coke. Our cokemaking ovens utilize

1

3.7 million tons of coke per year in 2010 to approximately 4.2 million tons of coke per year in 2011 due to the addition of the Middletown facility. The cokemaking facility that our sponsor operates in Brazil has cokemaking capacity of approximately 1.7 million tons of coke per year.

Our sponsor also owns and operates coal mining operations in Virginia and West Virginia which sold approximately 1.4 million tons of metallurgical coal in 2011.

Incorporated in Delaware in 2010 and headquartered in Lisle, Illinois, our sponsor became a publicly-traded company in 2011, and completed its two-step separation from Sunoco, Inc., or Sunoco, in 2012. Our sponsor’s stock is listed on the NYSE under the symbol “SXC.”

After this offering, our sponsor will own 14.1% of our common units (1.2% if the underwriters exercise their option to purchase additional common units in full), all of our subordinated units, all of our incentive distribution rights and our general partner. Our sponsor will appoint all of our directors and officers and manage our day-to-day operations. We will reimburse our sponsor for all of the costs it and its affiliates incur on our behalf. Our sponsor has agreed to share with us its cokemaking technology and to provide us preferential rights with respect to growth opportunities in the United States and Canada.

Summary of Conflicts of Interest and Fiduciary Duties

Our general partner has a legal duty to manage us in a manner it believes is in our best interest. However, the officers and directors of our general partner also have fiduciary duties to manage our general partner in a manner beneficial to our sponsor, the owner of our general partner. As a result, conflicts of interest may arise in the future between us or our unitholders, on the one hand, and our sponsor and our general partner, on the other hand.

Our partnership agreement limits the liability of and replaces the duties owed by our general partner to our unitholders. Our partnership agreement also restricts the remedies available to our unitholders for actions that might otherwise constitute a breach of our general partner’s duties. By purchasing a common unit, the purchaser agrees to be bound by the terms of our partnership agreement, and each unitholder is treated as having consented to various actions and potential conflicts of interest contemplated in the partnership agreement that might otherwise be considered a breach of fiduciary or other duties under Delaware law.

For a more detailed description of the conflicts of interest and duties of our general partner, please read “Conflicts of Interest and Fiduciary Duties.” For a description of other relationships with our affiliates, please read “Certain Relationships and Related Party Transactions.”

Our principal executive offices are located at 1011 Warrenville Road, Suite 600, Lisle, Illinois 60532 and our telephone number is (630) 824-1000. Our website address will be www.sxcpartners.com. We intend to make our periodic reports and other information filed with or furnished to the U.S. Securities and Exchange Commission, or SEC, available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

5

Emerging Growth Company Status

We are an emerging growth company as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we are an emerging growth company, unlike other public companies, we will not be required to:

| • | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; |

| • | comply with certain new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB; |

| • | comply with any new audit rules adopted by the PCAOB after April 5, 2012, unless the SEC determines otherwise; |

| • | provide certain disclosure regarding executive compensation required of larger public companies; or |

| • | obtain unitholder approval of any golden parachute payments not previously approved. |

We will cease to be an emerging growth company upon the earliest of:

| • | when we have $1.0 billion or more in annual revenues; |

| • | when we have at least $700 million in market value of our common units held by non-affiliates; |

| • | when we issue more than $1.0 billion of non-convertible debt over a three-year period; or |

| • | the last day of the fiscal year following the fifth anniversary of our initial public offering. |

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Proposed Concurrent Financing Transactions

Concurrent with the closing of this offering, we expect to enter into a new $100.0 million revolving credit facility, or the new revolving credit facility, which we anticipate will be undrawn at the closing of this offering. We also expect to issue $150.0 million aggregate principal amount of senior notes, or the senior notes. Completion of this offering is contingent upon the issuance of the senior notes and the entry into the revolving credit facility. Information regarding our offering of senior notes in this prospectus is neither an offer to sell nor a solicitation of an offer to buy senior notes. The senior notes will not be registered under the Securities Act, and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements. Please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

Formation Transactions and Partnership Structure

We are a Delaware limited partnership formed in July 2012 by our sponsor to own interests in certain entities and to operate certain of the businesses that have historically been conducted by our sponsor. In addition, prior to the closing of this offering, we will cause Haverhill Coke Company LLC and Middletown Coke Company, LLC to contribute their energy producing assets to their respective wholly-owned subsidiaries.

6

In connection with the closing of this offering, the following will occur:

| • | our sponsor will contribute to us an interest in each of Haverhill Coke Company LLC and Middletown Coke Company, LLC, the entities that own its Haverhill and Middletown cokemaking facilities and related assets, which will result in us owning a 65% interest in each of these entities; |

| • | SunCoke Energy Partners GP LLC, our general partner and a wholly-owned subsidiary of our sponsor, will receive a 2.0% general partner interest in us; |

| • | we will issue to our general partner the incentive distribution rights, which entitle the holder to increasing percentages, up to a maximum of 48.0%, of the cash we distribute in excess of our minimum quarterly distribution of $0.4125 per unit per quarter, as described under “Cash Distribution Policy and Restrictions on Distributions”; |

| • | we will issue 13,500,000 common units to the public and will use the net proceeds from this offering, together with the net proceeds from our expected concurrent offering of senior notes, as described under “Use of Proceeds”; |

| • | we will issue to our sponsor an aggregate of 2,209,697 common units (184,697 common units if the underwriters exercise their option to purchase additional common units in full) and 15,709,697 subordinated units; |

| • | we will enter into an omnibus agreement with our sponsor and our general partner, as described in “Certain Relationships and Related Party Transactions—Agreements with Affiliates in Connection with the Transactions”; |

| • | we will assume and promptly repay, with the net proceeds of this offering and our concurrent senior notes offering, $225.0 million of debt under our sponsor’s term loan; |

| • | as partial consideration for the interest in Haverhill Coke Company LLC and Middletown Coke Company, LLC conveyed to us by our sponsor, we will retain $128.7 million of the net proceeds of this offering and will pay from such retained proceeds, 100% (i.e., not merely our 65% proportionate share) of the following requirements of our 65% owned subsidiaries: (a) $67.0 million for identified environmental capital expenditures, (b) approximately $12.4 million to pay sales discounts related to tax credits owed to our customers and (c) $49.3 million to replenish our working capital; |

| • | we will enter into a new $100.0 million revolving credit facility which we anticipate will be undrawn at the closing of this offering; and |

| • | we expect to issue approximately $150.0 million aggregate principal amount of senior notes. |

Completion of this offering is contingent upon the issuance of the senior notes and the entry into the revolving credit facility.

Please read “Certain Relationships and Related Party Transactions—Agreements with Affiliates in Connection with the Transactions.”

Recent Developments

Although final results for the fourth quarter of 2012 are not yet available, based on the information currently available, we expect that our operating results and financial performance for the fourth quarter of 2012 will be slightly lower than results for the third quarter of 2012 but consistent with the forecast for the twelve months ending December 31, 2013. Results in the third quarter of 2012 were favorably impacted by timing of shipments, as well as by increased production reflecting higher coal-to-coke yields due to favorable weather in the summer months. We estimate that coke production for the fourth quarter of 2012 will be approximately 443,000 tons, including 153,000 tons at Middletown and 290,000 tons at Haverhill, reflecting capacity utilization of 107.0%, versus approximately 452,000 tons in the third quarter of 2012 including 154,000 tons at Middletown and 298,000 tons at Haverhill, reflecting capacity utilization of 109.0%. In addition, results in the fourth quarter of 2012 will include a charge of approximately $1.2 million associated with accelerated depreciation for capital replacements completed in the fourth quarter. We are not aware of any material events that occurred in the fourth quarter of 2012 that we believe will have an adverse impact on fourth quarter financial results or that we believe will change our forecast for the twelve months ending December 31, 2013.

7

8

| (1) | Assumes the underwriters do not exercise their option to purchase additional common units, which would instead be issued to Sun Coal & Coke LLC upon the option’s expiration. If and to the extent the underwriters exercise their option to purchase additional common units, the units purchased pursuant to such exercise will be issued to the public and the remainder, if any, will be issued to Sun Coal & Coke LLC. Accordingly, the exercise of the underwriters’ option will not affect the total number of units outstanding. If the underwriters’ option is exercised in full, then Sun Coal & Coke LLC would own 50.6% of the outstanding units and the public would own 49.4% of the outstanding units. |

| (2) | Sun Coal & Coke LLC will own 2,209,697 common units and 15,709,697 subordinated units, representing a 57.0% limited partner interest (which equates to a 55.9% partnership interest). The public will own 13,500,000 common units, representing a 43.0% limited partnership interest (which equates to a 42.1% partnership interest). |

9

Common units offered to the public | 13,500,000 common units. |

| 15,525,000 common units if the underwriters exercise their option to purchase additional common units in full. |

Units outstanding after this offering | 15,709,697 common units and 15,709,697 subordinated units for a total of 31,419,394 limited partner units. If and to the extent the underwriters exercise their option to purchase up to 2,025,000 additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be issued to the underwriters and the remainder, if any, will be issued to our sponsor. Any such units issued to our sponsor will be issued for no additional consideration. If the underwriters do not exercise their option to purchase additional 2,025,000 common units, we will issue common units to our sponsor upon the option’s expiration for no additional consideration. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding. In addition, our general partner will own a 2.0% general partner interest in us. |

Use of proceeds | We expect to receive estimated net proceeds of approximately $245.7 million from this offering (based on an assumed initial offering price of $20.00 per common unit, the mid-point of the price range set forth on the cover page of this prospectus), after deducting the estimated underwriting discount and offering expenses. We expect to receive estimated net proceeds of approximately $146.4 million from our offering of $150.0 million aggregate principal amount of senior notes concurrently with the closing of this offering. We intend to use approximately $36.0 million of the proceeds received to make a distribution to our sponsor which will in effect reimburse our sponsor for expenditures made by our sponsor during the two-year period prior to this offering for the expansion and improvement of the Haverhill and Middletown facilities; for federal income tax purposes, our sponsor is treated as having been the party that made such expenditures. We also intend to use approximately $225.0 million to repay term loan debt bearing a floating rate of interest based on LIBOR plus 3.00% per annum and maturing in June 2018 assumed from our sponsor and approximately $2.4 million to pay expenses related to our new revolving credit facility. As partial consideration for the interest in our operating subsidiaries conveyed to us by our sponsor, we will retain $128.7 million of net proceeds of this offering and will pay from such retained proceeds, 100% (i.e., not merely our 65% proportionate share) of the following requirements of our operating subsidiaries: (a) $67.0 million for identified environmental capital expenditures, (b) approximately $12.4 million to pay sales discounts related to tax credits owed to our customers and (c) $49.3 million to replenish our working capital. |

10

| If the underwriters exercise their option to purchase additional common units in full, the additional net proceeds to us would be approximately $37.8 million (and the total net proceeds to us from this offering would be approximately $283.6 million), in each case assuming an initial public offering price per common unit of $20.00 (based upon the mid-point of the price range set forth on the cover page of this prospectus). The net proceeds from any exercise of such option will be paid as a special distribution to our sponsor. If the underwriters do not exercise their option to purchase additional common units, we will issue 2,025,000 common units to our sponsor upon the expiration of the option for no additional consideration. Affiliates of certain of the underwriters are lenders under our sponsor’s term loan and, accordingly, will receive a portion of the proceeds from this offering in the form of repayment of the debt assumed by us. Please read “Use of Proceeds.” |

Cash distributions | We expect to make a minimum quarterly distribution of $0.4125 per common unit and subordinated unit ($1.65 per common unit and subordinated unit on an annualized basis). However, since it will be our policy to set our distributions based on the level of success of our operations, the actual amount of cash we will distribute on our common and subordinated units will depend principally on the amount of earnings we can generate from our operations. Our ability to pay the distributions is also subject to various restrictions and other factors described in more detail under the caption “Cash Distribution Policy and Restrictions on Distributions.” |

| For the first quarter that we are publicly-traded, we will pay a prorated distribution covering the period from the completion of this offering through March 31, 2013, based on the actual length of that period. |

| Our partnership agreement generally provides that we will make our distribution, if any, each quarter in the following manner: |

| • | first, 98.0% to the holders of common units and 2.0% to our general partner, until each common unit has received the minimum quarterly distribution of $0.4125 plus any arrearages from prior quarters; |

| • | second, 98.0% to the holders of subordinated units and 2.0% to our general partner, until each subordinated unit has received the minimum quarterly distribution of $0.4125 ; and |

| • | third, 98.0% to all unitholders, pro rata, and 2.0% to our general partner, until each unit has received a distribution of $0.4744. |

If cash distributions to our unitholders exceed $0.4744 per unit in any quarter, our general partner will receive, in addition to distributions on its 2.0% general partner interest, increasing percentages, up to 48.0%, of the cash we distribute in excess of that amount. The |

11

additional increasing distributions to our general partner are referred to herein as incentive distributions. In certain circumstances, our general partner, as the initial holder of our incentive distribution rights, will have the right to reset the minimum quarterly distribution and the target distribution levels at which the incentive distributions receive increasing percentages of the cash we distribute to higher levels based on our cash distributions at the time of the exercise of this reset election. Please read “How We Make Distributions To Our Partners—General Partner Interest and Incentive Distribution Rights.” |

| We may not generate sufficient earnings from operations to pay the minimum quarterly distribution on our common units. We would not have generated sufficient earnings on a pro forma basis to have paid any distributions on our common or subordinated units for the year ended December 31, 2011 or the twelve months ended September 30, 2012. |

| We believe, based on our financial forecast and related assumptions included in “Cash Distribution Policy and Restrictions on Distributions,” that we will generate sufficient earnings to pay the minimum quarterly distribution of $0.4125 per unit on all of our common units and subordinated units and the corresponding distributions on our general partner’s 2.0% interest for each quarter for the twelve months ending December 31, 2013. However, we do not have a legal or contractual obligation to pay quarterly distributions at our minimum quarterly distribution rate or at any other rate, and there is no guarantee that we will pay distributions to our unitholders in any quarter. Please read “Cash Distribution Policy and Restrictions on Distributions.” |

Subordinated units | Our sponsor will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period, holders of the subordinated units are not entitled to receive any distribution until the common units have received the minimum quarterly distribution plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. |

Conversion of subordinated units | The subordination period will end on the first business day after we have earned and paid at least (1) $1.65 (the minimum quarterly distribution on an annualized basis) on each outstanding common unit and subordinated unit and the corresponding distribution on our general partner’s 2.0% interest for each of three consecutive, non-overlapping four quarter periods ending on or after December 31, 2015 or (2) $2.48 (150.0% of the annualized minimum quarterly distribution) on each outstanding common unit and subordinated unit and the corresponding distributions on our general partner’s 2.0% interest and the related distribution on the incentive distribution rights for a four-quarter period ending on or after December 31, 2013, in each case provided there are no arrearages on our common units at that time. |

12

and its affiliates, voting together as a single class. Upon consummation of this offering, our sponsor will own an aggregate of 57.0% of our outstanding units (or 50.6% of our outstanding units, if the underwriters exercise their option to purchase additional common units in full). This will give our sponsor the ability to prevent the removal of our general partner. Please read “The Partnership Agreement—Voting Rights.” |

Limited call right | If at any time our general partner and its affiliates own more than 80% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price equal to the greater of (1) the average of the daily closing price of the common units over the 20 trading days preceding the date three days before notice of exercise of the call right is first mailed and (2) the highest per-unit price paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. Please read “The Partnership Agreement—Limited Call Right.” |

Estimated ratio of taxable income to distributions | We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2015, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be less than 30% of the cash distributed to you with respect to that period. Thereafter, the ratio of allocable taxable income to cash distributions to you could substantially increase. Please read “Material U.S. Federal Income Tax Consequences—Tax Consequences of Unit Ownership.” |

Material federal income tax consequences | Subject to the discussion under “Material U.S. Federal Income Tax Consequences—Taxation of the Partnership—Partnership Status” and the limitations set forth therein, it is the opinion of Vinson & Elkins L.L.P. that we will be treated as a partnership for U.S. federal income tax purposes. As a result, we generally will not be liable for U.S. federal income taxes. Instead, each of our unitholders will take into account its share of our income, gains, losses and deductions in computing its U.S. federal income tax liability as if it had earned such income directly, even if we do not make cash distributions to that unitholder. Consequently, a unitholder may be liable for U.S. federal income taxes as a result of ownership of our units even if that unitholder has not received a cash distribution from us. Cash distributions by us to a unitholder generally will not give rise to income or gain. |

| For a discussion of the material U.S. federal income tax consequences that may be relevant to prospective unitholders, you should read “Material U.S. Federal Income Tax Consequences.” |

14

Directed Unit Program | The underwriters have reserved for sale at the initial public offering price up to 5% of the common units being offered by this prospectus for sale to the directors and executive officers of our general partner and certain other employees of our sponsor who have expressed an interest in purchasing common units in the offering. We do not know if these persons will choose to purchase all or any portion of these reserved common units, but any purchases they do make will reduce the number of common units available to the general public. Please read “Underwriting—Directed Unit Program.” |

Exchange listing | We have been approved to list our common units on the NYSE, under the symbol “SXCP.” |

Summary Historical and Pro Forma Financial and Operating Data

The following table sets forth certain of our summary historical and pro forma financial and operating data. We derived our summary historical financial data as of December 31, 2011 and 2010, and for the years ended December 31, 2011, 2010 and 2009 from our audited historical Combined Financial Statements included elsewhere in this prospectus. We derived our summary historical financial data as of September 30, 2012 and for the nine months ended September 30, 2012 and 2011 from our unaudited historical Combined Financial Statements included elsewhere in this prospectus. We derived our summary historical financial data as of September 30, 2011 and December 31, 2009 from our unaudited historical Combined Financial Statements not included in this prospectus.

Our Combined Financial Statements include amounts allocated from our sponsor for general corporate overhead costs attributable to our operations. The general corporate overhead expenses incurred by our sponsor include costs from certain corporate and shared services functions provided by our sponsor.The amounts reflected include (i) charges that were incurred by our sponsor that were specifically identified as being attributable to us and (ii) an allocation of all of our sponsor’s remaining general corporate overhead costs based on the proportional level of effort attributable to the operation of our facilities. These costs include legal, accounting, tax, treasury, engineering, information technology, insurance, employee benefit costs, communications, human resources, and procurement. All corporate costs that were specifically identifiable to a particular operating facility of our sponsor have been allocated to that facility, including our operating facilities. Where specific identification of charges to a particular operating facility was not practicable, a reasonable method of allocation was applied to all remaining general corporate overhead costs. The allocation methodology for all remaining corporate overhead costs is based on management’s estimate of the proportional level of effort devoted by corporate resources that is attributable to each of our sponsor’s operating facilities, including our operating facilities.

The Combined Financial Statements included in this prospectus may not necessarily reflect our financial position, results of operations and cash flows as if we had operated as a stand-alone public company during the periods presented. Accordingly, our historical results should not be relied upon as an indicator of our future performance.

At the closing of this offering we will own a 65% interest in the entity that owns the Haverhill cokemaking facility and related assets and a 65% interest in the entity that owns the Middletown cokemaking facility and related assets. The unaudited pro forma Combined Financial Statements reflect the acquisition of our interests in these entities. Our unaudited pro forma Combined Financial Statements will show these entities as consolidated and, as a result, our sponsor’s remaining 35% interest in each of these entities will be reflected as a noncontrolling equity interest.

15

The summary pro forma combined financial data for the year ended December 31, 2011 and as of and for the nine months ended September 30, 2012 are derived from our unaudited pro forma Combined Financial Statements included elsewhere in this prospectus.

The unaudited pro forma Combined Financial Statements have been prepared as if certain transactions to be effected at the completion of this offering had taken place on September 30, 2012 in the case of the pro forma Combined Balance Sheet, or as of January 1, 2011 in the case of the pro forma Combined Statement of Operations for the year ended December 31, 2011 and the nine months ended September 30, 2012. Our unaudited pro forma Combined Financial Statements give effect to the following:

| • | the issuance (i) to our general partner of a 2.0% general partner interest in us and all of our incentive distribution rights and (ii) to our sponsor of2,209,697 common units and15,709,697 subordinated units, representing an aggregate57.0% limited partner interest in us; |

| • | the issuance of13,500,000 common units to the public in this offering, representing a43.0% limited partner interest in us at an initial public offering price of $20.00 per unit; |

| • | $100.0 million of available undrawn borrowing capacity under the new revolving credit facility, as described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources”; |

| • | the issuance of $150.0 million aggregate principal amount of senior notes, as described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources”; |

| • | the payment of expenses related to this offering of $24.3 million and debt financing fees related to the new revolving credit facility and the senior notes offering of $6.0 million; |

| • | the application of the net proceeds of this offering, together with the net proceeds from the senior notes offering, as described in “Use of Proceeds”; |

| • | a reduction in the parent net equity for tax credits and net operating loss carryforwards generated by the Predecessor which were used by Sunoco; and |

| • | the change in tax status of the Predecessor to a non-taxable entity. |

The unaudited pro forma Combined Financial Statements do not necessarily reflect what our financial position and results of operations would have been if we had operated as an independent, publicly-traded partnership during the periods shown. In addition, the unaudited pro forma Combined Financial Statements are not necessarily indicative of our future results of operations or financial condition. The assumptions and adjustments give effect to pro forma events that are (i) directly attributable to the offering, (ii) factually supportable and (iii) with respect to the pro forma combined statements of operations, expected to have a continuing impact on the partnership. The pro forma combined financial data do not give effect to the estimated $2.5 million in incremental annual general and administrative expenses we expect to incur as a result of being a separate publicly-traded partnership. Additionally, if the omnibus agreement had been in effect during the year ended December 31, 2011 and the nine months ended September 30, 2012, then the corporate overhead allocated to us would have been lower by approximately $6.4 million and $5.1 million in such periods, respectively.

The following table includes the non-GAAP financial measures, EBITDA and Adjusted EBITDA, which we use to evaluate our operating performance. EBITDA and Adjusted EBITDA do not represent and should not be considered as alternatives to net income as determined by GAAP, and our calculations thereof may not be comparable to those reported by other companies. We believe Adjusted EBITDA is an important measure of operating performance and provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance. Adjusted EBITDA, as presented herein, is a supplemental

16

The information below should be read in conjunction with “Use of Proceeds,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Certain Relationships and Related Party Transactions,” our audited historical Combined Financial Statements and related notes and our unaudited pro forma Combined Financial Statements and related notes included elsewhere in this prospectus.

| Historical | Pro Forma | |||||||||||||||||||||||||||

| Years Ended December 31, | Nine Months Ended September 30, | Year Ended December 31, 2011 | Nine Months Ended September 30, 2012 | |||||||||||||||||||||||||

| 2011 | 2010 | 2009 | 2012 | 2011 | ||||||||||||||||||||||||

| (Dollars in millions, except per unit and per ton data) | ||||||||||||||||||||||||||||

Income Statement Data: | ||||||||||||||||||||||||||||

Revenues | ||||||||||||||||||||||||||||

Sales and other operating revenue | $ | 449.8 | $ | 360.7 | $ | 308.7 | $ | 554.0 | $ | 309.7 | $ | 449.8 | $ | 554.0 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Costs and operating expenses | ||||||||||||||||||||||||||||

Cost of products sold and operating expenses | 367.2 | 308.9 | 317.5 | 446.4 | 249.7 | 367.2 | 446.4 | |||||||||||||||||||||

Selling, general and administrative expenses | 25.7 | 11.7 | 8.4 | 16.5 | 17.6 | 25.7 | 16.5 | |||||||||||||||||||||

Depreciation expense | 18.6 | 17.2 | 13.7 | 24.4 | 12.7 | 18.6 | 24.4 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total costs and operating expenses | 411.5 | 337.8 | 339.6 | 487.3 | 280.0 | 411.5 | 487.3 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Operating income (loss) | 38.3 | 22.9 | (30.9 | ) | 66.7 | 29.7 | 38.3 | 66.7 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Interest expense | 4.7 | — | — | 7.8 | 2.1 | 13.0 | 9.7 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Income (loss) before income tax expense (benefit) | 33.6 | 22.9 | (30.9 | ) | 58.9 | 27.6 | 25.3 | 57.0 | ||||||||||||||||||||

Income tax expense (benefit) | 2.8 | (1.1 | ) | (24.4 | ) | 17.4 | 4.1 | — | — | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Net income (loss) | $ | 30.8 | $ | 24.0 | $ | (6.5 | ) | $ | 41.5 | $ | 23.5 | 25.3 | 57.0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Less: Net income attributable to noncontrolling interests | 13.4 | 23.3 | ||||||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||

Net income attributable to SunCoke Energy Partners, L.P. | $ | 11.9 | $ | 33.7 | ||||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||

General partner’s interest in net income | $ | 0.2 | $ | 0.7 | ||||||||||||||||||||||||

Common unitholders’ interest in net income | $ | 11.7 | $ | 33.0 | ||||||||||||||||||||||||

Subordinated unitholders’ interest in net income | $ | — | $ | — | ||||||||||||||||||||||||

Pro forma net income (loss) per common unit | $ | 0.74 | $ | 2.10 | ||||||||||||||||||||||||

Pro forma net income (loss) per subordinated unit | $ | — | $ | — | ||||||||||||||||||||||||

Cash Flow Data: | ||||||||||||||||||||||||||||

Net cash provided by (used in) operating activities | $ | 23.5 | $ | 77.7 | $ | (34.9 | ) | $ | 30.7 | $ | 3.0 | |||||||||||||||||

Net cash used in investing activities | $ | (175.7 | ) | $ | (180.9 | ) | $ | (46.9 | ) | $ | (8.1 | ) | $ | (149.0 | ) | |||||||||||||

Net cash provided by (used in) financing activities | $ | 152.2 | $ | 103.2 | $ | 81.8 | $ | (22.6 | ) | $ | 146.0 | |||||||||||||||||

Capital expenditures: | ||||||||||||||||||||||||||||

Ongoing capital | 6.3 | 12.9 | 6.1 | 8.1 | 3.6 | |||||||||||||||||||||||

Expansion capital | 169.4 | 169.7 | 40.8 | — | 145.4 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 175.7 | $ | 182.6 | $ | 46.9 | $ | 8.1 | $ | 149.0 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||||||||||

Properties, plants and equipment, net | $ | 783.8 | $ | 626.2 | $ | 460.7 | $ | 768.0 | $ | 762.7 | $ | 768.0 | ||||||||||||||||

Total assets | $ | 928.7 | $ | 728.4 | $ | 567.2 | $ | 922.1 | $ | 891.9 | $ | 974.2 | ||||||||||||||||

Total liabilities | $ | 305.5 | $ | 63.2 | $ | 29.2 | $ | 280.0 | $ | 282.2 | $ | 205.0 | ||||||||||||||||

Total parent net equity/ partners’ capital attributable to SunCoke Energy Partners, L.P. | $ | 623.2 | $ | 665.2 | $ | 538.0 | $ | 642.1 | $ | 609.7 | $ | 573.4 | ||||||||||||||||

Coke Operating Data: | ||||||||||||||||||||||||||||

Capacity utilization (%)(1) | 102 | 100 | 84 | 107 | 101 | |||||||||||||||||||||||

Coke production volume (thousands of tons)(2) | 1,192 | 1,103 | 928 | 1,323 | 834 | |||||||||||||||||||||||

Coke sales volumes (thousands of tons)(3) | 1,203 | 1,130 | 894 | 1,318 | 843 | 1,203 | 1,318 | |||||||||||||||||||||

Other Financial Data: | ||||||||||||||||||||||||||||

Adjusted EBITDA(4) | $ | 61.9 | $ | 44.8 | $ | (10.1 | ) | $ | 93.8 | $ | 46.1 | $ | 40.2 | $ | 61.0 | |||||||||||||

Adjusted EBITDA/ton(5) | $ | 51.45 | $ | 39.65 | $ | (11.30 | ) | $ | 71.17 | $ | 54.69 | $ | 51.41 | $ | 71.20 | |||||||||||||

18

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were to occur, our business, financial condition, results of operations and therefore our ability to distribute cash could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline, and you could lose all or part of your investment.

Risks Inherent in Our Business and Industry

We may not generate sufficient earnings from operations to enable us to pay the minimum quarterly distribution to unitholders.

We may not have sufficient earnings each quarter to support a decision to pay the full amount of our minimum quarterly distribution of $0.4125 per unit, or $1.65 per unit per year, which will require us to generate from earnings amounts available for distribution of approximately $13.2 million per quarter, or $52.9 million per year, based on the number of common units, subordinated units and the 2.0% general partner interest that will be outstanding after the completion of this offering. The amount we decide to distribute on our common and subordinated units also depends upon our liquidity and other considerations, which will fluctuate from quarter to quarter based on the following factors, some of which are beyond our control:

| • | severe financial hardship or bankruptcy of one or more of our major customers, or the occurrence of other events affecting our ability to collect payments from our customers, including our customers’ default; |

| • | volatility and cyclical downturns in the steel industry and other industries in which our customers operate; |

| • | the exercise by AK Steel of its early termination rights under its coke sales agreement and its energy sales agreement at our Haverhill facility; |

| • | our sponsor’s inability to perform under the omnibus agreement; |

| • | age of, and changes in the reliability, efficiency and capacity of the various equipment and operating facilities used in our cokemaking operations, and in the operations of our major customers, business partners and/or suppliers; |

| • | the cost of environmental remediation at our cokemaking facilities; |

| • | changes in the expected operating levels of our assets; |

| • | our ability to meet minimum volume requirements, coal-to-coke yield standards and coke quality requirements in our coke sales agreements; |

| • | our ability to enter into new, or renew existing, long-term agreements for the supply of coke to domestic steel producers under terms similar or more favorable than those currently in place; |

| • | our ability to enter into new, or renew existing, agreements for the sale of steam and electricity generated by our facilities under terms similar or more favorable than those currently in place; |

| • | changes in the marketplace that may affect supply and demand for our coke, including increased exports of coke from China related to reduced export duties and export quotas and increasing competition from alternative steelmaking and cokemaking technologies that have the potential to reduce or eliminate the use of coke; |

20

| • | our relationships with, and other conditions affecting, our customers; |

| • | changes in levels of production, production capacity, pricing and/or margins for coke; |

| • | our ability to secure new coal supply agreements or to renew existing coal supply agreements; |

| • | variation in availability, quality and supply of metallurgical coal used in the cokemaking process, including as a result of nonperformance by our suppliers; |

| • | effects of railroad, barge, truck and other transportation performance and costs, including any transportation disruptions; |

| • | cost of labor; |

| • | risks related to employees and workplace safety; |

| • | effects of adverse events relating to the operation of our facilities and to the transportation and storage of hazardous materials (including equipment malfunction, explosions, fires, spills, and the effects of severe weather conditions); |

| • | changes in product specifications for the coke that we produce; |

| • | changes in credit terms required by our suppliers; |

| • | changes in insurance markets and the level, types and costs of coverage available, and the financial ability of our insurers to meet their obligations; |

| • | changes in, or new, statutes, regulations or governmental policies by federal, state and local authorities with respect to protection of the environment; |

| • | changes in accounting rules and/or tax laws or their interpretations, including the method of accounting for inventories and leases; |

| • | nonperformance or force majeure by, or disputes with or changes in contract terms with, major customers, suppliers, dealers, distributors or other business partners; and |

| • | changes in, or new, statutes, regulations, governmental policies and taxes, or their interpretations. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

| • | the level of capital expenditures we make; |

| • | the cost of acquisitions; |

| • | our debt service requirements and other liabilities; |

| • | fluctuations in our working capital needs; |

| • | our ability to borrow funds and access capital markets; |

| • | restrictions contained in debt agreements to which we are a party; and |

| • | the amount of cash reserves established by our general partner. |

For a description of additional restrictions and factors that may affect our ability to pay cash distributions, please read “Cash Distribution Policy and Restrictions on Distributions.”

On a pro forma basis we would not have generated sufficient earnings to pay the full minimum quarterly distribution on all units for the twelve months ended September 30, 2012.

The amount of cash we need to pay the minimum quarterly distribution for four quarters on the common units, subordinated units and 2.0% general partner interest to be outstanding immediately after this offering is approximately $52.9 million. Our pro forma earnings generated during the twelve months ended September 30, 2012 would have

21

Limitations on the availability and reliability of transportation, and increases in transportation costs, particularly rail systems, could materially and adversely affect our ability to obtain a supply of coal and deliver coke to our customers.

Our ability to obtain coal depends primarily on third-party rail systems and to a lesser extent river barges. If we are unable to obtain rail or other transportation services, or are unable to do so on a cost-effective basis, our results of operations could be adversely affected. Alternative transportation and delivery systems are generally inadequate and not suitable to handle the quantity of our shipments or to ensure timely delivery. The loss of access to rail capacity could create temporary disruption until the access is restored, significantly impairing our ability to receive coal and resulting in materially decreased revenues. Our ability to open new cokemaking facilities may also be affected by the availability and cost of rail or other transportation systems available for servicing these facilities.

Our arrangements with ArcelorMittal at our Haverhill cokemaking facility require us to deliver coke to ArcelorMittal via railcar. We have entered into a long-term rail transportation agreement to meet this obligation. Disruption of these transportation services because of weather-related problems, mechanical difficulties, train derailments, infrastructure damage, strikes, lock-outs, lack of fuel or maintenance items, fuel costs, transportation delays, accidents, terrorism, domestic catastrophe or other events could temporarily or over the long term impair our ability to produce coke, and therefore, could materially and adversely affect our results of operations. In addition, if our rail transportation agreement is terminated, we may have to pay higher rates to access rail lines or make alternative transportation arrangements.

Labor disputes with the unionized portion of our workforce could adversely affect us.

As of September 30, 2012, we have approximately 252 employees. Approximately 120, or 48% of our employees are currently represented by the United Steelworkers under various contracts. When these agreements expire or terminate, we may not be able to negotiate the agreements on the same or more favorable terms as the current agreements, or at all, and without production interruptions, including labor stoppages. The collective bargaining agreement with respect to our Haverhill cokemaking facility was set to expire on November 1, 2012 but has been extended through January 29, 2013 while we continue discussions regarding the terms of a new agreement. We may unilaterally exercise up to two additional thirty day extensions and the union may unilaterally exercise one additional thirty day extension. If we are unable to negotiate a new collective bargaining agreement before the expiration date, our operations and our profitability could be adversely affected. A prolonged labor dispute, which could include a work stoppage, could adversely affect our ability to satisfy our customers’ orders and, as a result, adversely affect our production and results of operations.

If we fail to maintain satisfactory labor relations, we may be adversely affected. Union represented labor creates an increased risk of work stoppages and higher labor costs.

We rely, at one or more of our facilities, on unionized labor, and there is always the possibility that the employing entity will be unable to reach agreement on terms and conditions of employment or renewal of a collective bargaining agreement. Any labor disputes, work stoppages, or increased labor costs could adversely affect operations, the stability of production and reduce our future revenues, profitability, or our ability to pay cash distributions to our unitholders. It is also possible that, in the future, additional employee groups may choose to be represented by a labor union.

We expect to enter into a new revolving credit facility and an indenture in connection with this offering, each of which will likely contain restrictions and financial covenants that may restrict our business and financing activities.

The new revolving credit facility that we expect to enter into and the indenture that will govern the senior notes that we expect to issue in connection with this offering, and any other future financing agreements that we

30

Risks Inherent in an Investment in Us

Our sponsor owns and controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including our sponsor, have conflicts of interest with us and limited duties, and they may favor their own interests to the detriment of us and our unitholders.

Following the offering, our sponsor will own and control our general partner and will appoint all of the directors of our general partner. Although our general partner has a duty to manage us in a manner it believes to be in our best interests, the executive officers and directors of our general partner have a fiduciary duty to manage our general partner in a manner beneficial to our sponsor. Therefore, conflicts of interest may arise between our sponsor or any of its affiliates, including our general partner, on the one hand, and us or any of our unitholders, on the other hand. In resolving these conflicts of interest, our general partner may favor its own interests and the interests of its affiliates over the interests of our common unitholders. These conflicts include the following situations, among others:

| • | our general partner is allowed to take into account the interests of parties other than us, such as our sponsor, in exercising certain rights under our partnership agreement, which has the effect of limiting its duty to our unitholders; |

| • | neither our partnership agreement nor any other agreement requires our sponsor to pursue a business strategy that favors us; |

| • | our partnership agreement replaces the fiduciary duties that would otherwise be owed by our general partner with contractual standards governing its duties, limits our general partner’s liabilities and restricts the remedies available to our unitholders for actions that, without such limitations, might constitute breaches of fiduciary duty; |

| • | except in limited circumstances, our general partner has the power and authority to conduct our business without unitholder approval; |

| • | our general partner determines the amount and timing of asset purchases and sales, borrowings, issuances of additional partnership securities and the level of reserves, each of which can affect the amount of cash that is distributed to our unitholders; |

| • | our general partner determines the amount and timing of any capital expenditure and whether a capital expenditure is classified as an ongoing capital expenditure, which reduces operating surplus, or a replacement capital expenditure, which does not reduce operating surplus. Please read “How We Make Distributions to Our Partners—Capital Expenditures” for a discussion on when a capital expenditure constitutes an ongoing capital expenditure or a replacement capital expenditure. This determination can affect the amount of cash that is distributed to our unitholders which, in turn, may affect the ability of the subordinated units to convert. Please read “How We Make Distributions to Our Partners—Subordination Period”; |

| • | our general partner may cause us to borrow funds in order to permit the payment of cash distributions, even if the purpose or effect of the borrowing is to make a distribution on the subordinated units, to make incentive distributions or to accelerate the expiration of the subordination period; |

| • | our partnership agreement permits us to distribute up to $26.5 million as operating surplus, even if it is generated from asset sales, non-working capital borrowings or other sources that would otherwise constitute capital surplus. This cash may be used to fund distributions on our subordinated units or the incentive distribution rights; |

| • | our general partner determines which costs incurred by it and its affiliates are reimbursable by us; |

| • | our partnership agreement does not restrict our general partner from causing us to pay it or its affiliates for any services rendered to us or entering into additional contractual arrangements with its affiliates on our behalf; |

32

While our partnership agreement requires us to distribute all of our available cash, our partnership agreement, including provisions requiring us to make cash distributions contained therein, may be amended.

While our partnership agreement requires us to distribute all of our available cash, our partnership agreement, including provisions requiring us to make cash distributions contained therein, may be amended. Our partnership agreement generally may not be amended during the subordination period without the approval of our public common unitholders. However, our partnership agreement can be amended with the consent of our general partner and the approval of a majority of the outstanding common units (including common units held by affiliates of our general partner) after the subordination period has ended. At the closing of this offering, affiliates of our general partner will own, directly or indirectly, approximately 14.1% of the outstanding common units and all of our outstanding subordinated units. Please read “The Partnership Agreement—Amendment of Our Partnership Agreement.”

Our partnership agreement replaces our general partner’s fiduciary duties to holders of our units.

Our partnership agreement contains provisions that eliminate and replace the fiduciary standards to which our general partner would otherwise be held by state fiduciary duty law. For example, our partnership agreement permits our general partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our general partner, or otherwise free of fiduciary duties to us and our unitholders. This entitles our general partner to consider only the interests and factors that it desires and relieves it of any duty or obligation to give any consideration to any interest of, or factors affecting, us, our affiliates or our limited partners. Examples of decisions that our general partner may make in its individual capacity include:

| • | how to allocate business opportunities among us and its affiliates; |

| • | whether to exercise its call right; |

| • | how to exercise its voting rights with respect to the units it owns; |

| • | whether to exercise its registration rights; |

| • | whether to elect to reset target distribution levels; and |

| • | whether or not to consent to any merger or consolidation of the partnership or amendment to the partnership agreement. |

By purchasing a common unit, a unitholder is treated as having consented to the provisions in the partnership agreement, including the provisions discussed above. Please read “Conflicts of Interest and Fiduciary Duties—Fiduciary Duties.”

Our partnership agreement restricts the remedies available to holders of our units for actions taken by our general partner that might otherwise constitute breaches of fiduciary duty.

Our partnership agreement contains provisions that restrict the remedies available to unitholders for actions taken by our general partner that might otherwise constitute breaches of fiduciary duty under state fiduciary duty law. For example, our partnership agreement provides that:

| • | whenever our general partner makes a determination or takes, or declines to take, any other action in its capacity as our general partner, our general partner is required to make such determination, or take or decline to take such other action, in good faith, and will not be subject to any other or different standard imposed by our partnership agreement, Delaware law, or any other law, rule or regulation, or at equity; |

| • | our general partner will not have any liability to us or our unitholders for decisions made in its capacity as a general partner so long as it acted in good faith, meaning that it believed that the decision was in the best interest of our partnership; |

| • | our general partner and its officers and directors will not be liable for monetary damages to us or our limited partners resulting from any act or omission unless there has been a final and non-appealable |

34

exercise this reset right in order to facilitate acquisitions or internal growth projects that would not be sufficiently accretive to cash distributions per common unit without such conversion. It is possible, however, that our general partner could exercise this reset election at a time when it is experiencing, or expects to experience, declines in the cash distributions it receives related to its incentive distribution rights and may, therefore, desire to be issued common units rather than retain the right to receive incentive distributions based on the initial target distribution levels. This risk could be elevated if our incentive distribution rights have been transferred to a third-party. As a result, a reset election may cause our common unitholders to experience a reduction in the amount of cash distributions that our common unitholders would have otherwise received had we not issued new common units to our general partner in connection with resetting the target distribution levels. Please read “How We Make Distributions to Our Partners—General Partner’s Right to Reset Incentive Distribution Levels.”

Holders of our common units have limited voting rights and are not entitled to appoint our general partner or its directors, which could reduce the price at which our common units will trade.

Unlike the holders of common stock in a corporation, unitholders have only limited voting rights on matters affecting our business and, therefore, limited ability to influence management’s decisions regarding our business. Unitholders will have no right on an annual or ongoing basis to appoint our general partner or its board of directors. The board of directors of our general partner, including the independent directors, is chosen entirely by our sponsor, as a result of it owning our general partner, and not by our unitholders. Please read “Management—Management of SunCoke Energy Partners, L.P.” and “Certain Relationships and Related Party Transactions.” Unlike publicly-traded corporations, we will not conduct annual meetings of our unitholders to appoint directors or conduct other matters routinely conducted at annual meetings of stockholders of corporations.

Even if holders of our common units are dissatisfied, they cannot initially remove our general partner without its consent.

If our unitholders are dissatisfied with the performance of our general partner, they will have limited ability to remove our general partner. Unitholders initially will be unable to remove our general partner without its consent because our general partner and its affiliates will own sufficient units upon the completion of this offering to be able to prevent its removal. The vote of the holders of at least 66 2/3% of all outstanding common and subordinated units voting together as a single class is required to remove our general partner. Following the closing of this offering, our sponsor will own an aggregate of 57.0% of our outstanding units (or 50.6% of our outstanding units, if the underwriters exercise their option to purchase additional common units in full). Also, if our general partner is removed without cause during the subordination period and no units held by the holders of the subordinated units or their affiliates are voted in favor of that removal, all remaining subordinated units will automatically be converted into common units and any existing arrearages on the common units will be extinguished. Cause is narrowly defined in our partnership agreement to mean that a court of competent jurisdiction has entered a final, non-appealable judgment finding our general partner liable for actual fraud or willful or wanton misconduct in its capacity as our general partner. Cause does not include most cases of charges of poor management of the business.

Unitholders will experience immediate and substantial dilution of $2.12 per common unit.

The assumed initial public offering price of $20.00 per common unit (the mid-point of the price range set forth on the cover page of this prospectus) exceeds our pro forma net tangible book value of $17.88 per common unit. Based on the assumed initial public offering price of $20.00 per common unit, unitholders will incur immediate and substantial dilution of $2.12 per common unit. This dilution results primarily because the assets contributed to us by affiliates of our general partner are recorded at their historical cost in accordance with GAAP, and not their fair value. Please read “Dilution.”

36

Our general partner interest or the control of our general partner may be transferred to a third-party without unitholder consent.