Steel Success Strategies XXVIII Supporting Steel Industry Competitiveness June 19, 2013 Exhibit 99.1 |

TM About SunCoke Largest independent producer of metallurgical coke in the Americas 2 • More than 6 million tons of capacity – Facilities in U.S., Brazil and joint venture in India • Reliable, long-term supplier to leading steelmakers – ArcelorMittal, U.S. Steel, AK Steel • Industry-leading cokemaking technology and know-how – 50+ years of cokemaking experience – State-of-the-art heat recovery design – Meets U.S. EPA Maximum Achievable Control Technology (MACT) Standards |

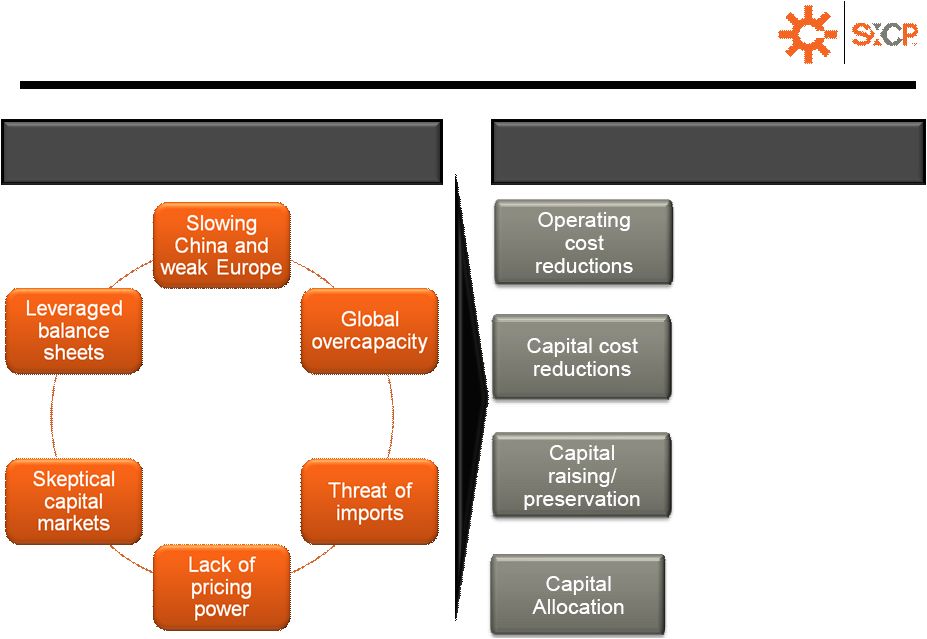

TM Steel Industry Dynamics Challenging Steel Industry Environment Steelmakers’ and Raw Material Suppliers’ Strategic Choices • Lower raw material costs • Implement operating efficiencies • Reduce ongoing capital needs • Unlock value of captive assets • Focus capital on targeted growth 3 • Allocate capital in highest value add manner |

TM The SunCoke Advantage Implement best practices Improve technology • Compiled comprehensive database of U.S. coals • Developed model to optimize coal blend for cost and targeted quality • Enhanced oven controls and process automation • Improved coal/coke handling practices/equipment • Maximize power recovery • Maximize natural gas/injectant capability for customers • Blast furnaces using 100% our coke achieve some of best fuel rates in industry • Simple operation; no by-product or waste water treatment plants • Less operating and maintenance manpower requirements • Gross operating cost ~ ½ that of typical by-product batteries 1 Master coal science 2 3 4 The SunCoke Way Blend optimization Yield improvement Larger and stronger coke Lower operating cost • Standardize operating and maintenance practices to achieve reliable, predictable operations • Use advanced prediction models to optimize coal blend and maximize yield • Increase production flexibility • Decrease equipment cost and lengthen asset life |

TM Capital Cost Reductions 5 SXC reengineering its next facility to reduce capital intensity of cokemaking and meet increasingly stringent environmental requirements |

TM Capital Cost Reductions (cont’d) • Next plant up to 30% smaller in footprint • Modular design enables staged installation • Increased power and/or steam output • Capital costs per ton decrease with footprint (~20% reduction in capital cost/ton, including next generation NAAQS requirements) New plant design 6 |

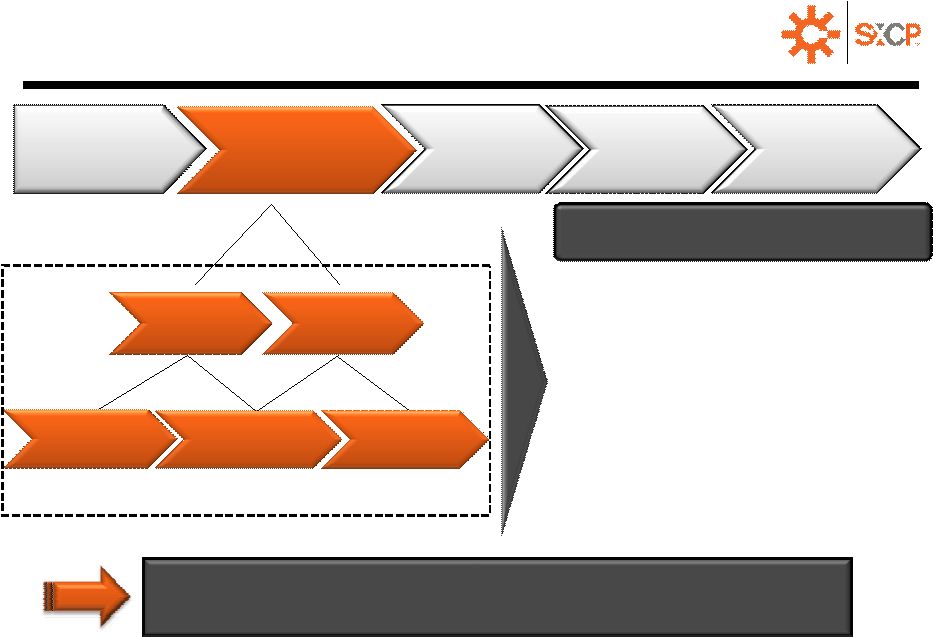

TM Steel Value Chain Raw materials mining Crude steel Finished steel End customer Raw material processing/ transportation Carbon Ferrous Transport Processing Handling Disaggregation Opportunity • Elements of steel value chain can be disaggregated to create value • Maintain strategic control/use of assets on long-term, competitive and reliable basis • Free up and redeploy proceeds • Fund construction of new assets 7 Requires trusted counterparty to own/operate and valuation/cost of capital advantage |

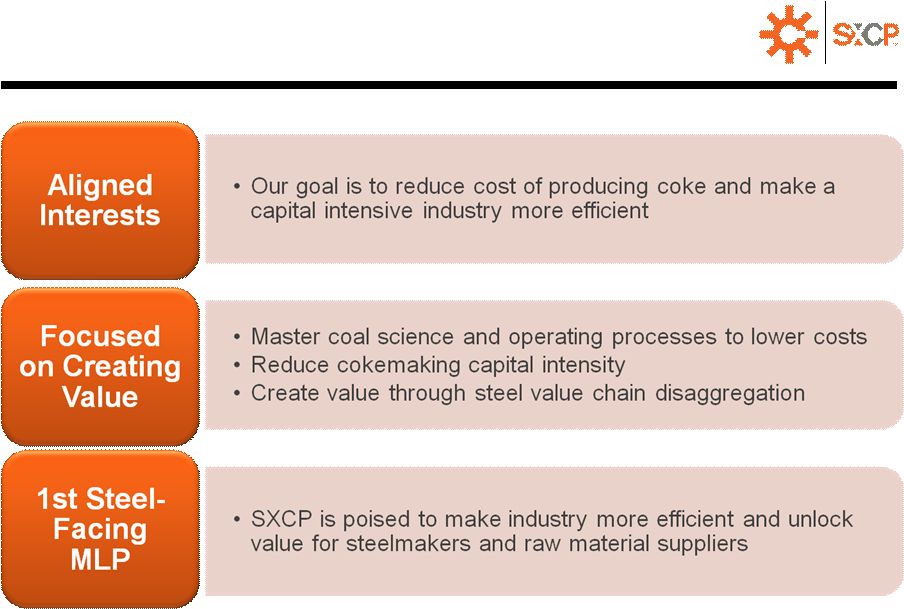

TM SunCoke’s Strategic Role SXCP 1 st steel-facing MLP Advantaged cost of capital Experienced constructor and operator Trusted, reliable long- term supplier SXC/SXCP can create value for steelmakers and raw material suppliers through strategic disaggregation 8 |

TM Conclusion 9 |