Exhibit (d)

This description of FMS-WM and the Federal Republic is dated August 13, 2014 and appears as Exhibit (d) to the Annual Report on Form 18-K of FMS-WM for the fiscal year ended December 31, 2013.

TABLE OF CONTENTS

-1-

-2-

THIS DOCUMENT (OTHERWISE THAN AS PART OF A PROSPECTUS CONTAINED IN A REGISTRATION STATEMENT FILED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED) DOES NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES OF FMS-WM. THE DELIVERY OF THIS DOCUMENT AT ANY TIME DOES NOT IMPLY THAT THE INFORMATION HEREIN IS CORRECT AS OF ANY TIME SUBSEQUENT TO ITS DATE.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this description, references to “€”, “euro” or “EUR” are to the single European currency of the member states of the European Union participating in the euro and references to “U.S. dollars”, “$” or “USD” are to United States dollars. See “Exchange Rate Information” below for information regarding the rates of conversion of the euro into United States dollars and “The Federal Republic of Germany—General—The European Union and European Integration” for a discussion of the introduction of the euro.

FMS-WM’s accounts are kept, and the economic data on the Federal Republic is expressed, in euro.

Any discrepancies in the tables included in this prospectus between the amounts and the totals thereof are due to rounding.

In this document, references to the “Federal Republic” and “Germany” are to the Federal Republic of Germany and references to the “Federal Government” are to the government of the Federal Republic of Germany. The term “FMS-WM” refers to FMS Wertmanagement.

EXCHANGE RATE INFORMATION

FMS-WM files reports with the Securities and Exchange Commission giving financial and economic data expressed in euro.

The following table shows noon buying rates for euro, expressed as U.S. dollars per EUR 1.00, for the periods and dates indicated, as reported by the Federal Reserve Bank of New York. On January 1, 2009, the Federal Reserve Bank of New York discontinued daily publication of noon buying rates. As of this date, noon buying rates are as published on a weekly basis by the Federal Reserve Bank of New York.

| | | | | | | | | | | | | | | | |

Year ended December 31, | | Period End | | | Average(1) | | | High | | | Low | |

2009 | | | 1.4332 | | | | 1.3955 | | | | 1.5100 | | | | 1.2547 | |

2010 | | | 1.3269 | | | | 1.3216 | | | | 1.4536 | | | | 1.1959 | |

2011 | | | 1.2973 | | | | 1.4002 | | | | 1.4875 | | | | 1.2926 | |

2012 | | | 1.3186 | | | | 1.2909 | | | | 1.3463 | | | | 1.2062 | |

2013 | | | 1.3779 | | | | 1.3303 | | | | 1.3816 | | | | 1.2774 | |

| (1) | The average of the noon buying rates on the last business day of each month during the relevant period. |

The following table shows the high and low noon buying rates for euro, expressed as U.S. dollars per EUR 1.00, for each month from January 2014 through August 2014 (through August 8, 2014), as reported by the Federal Reserve Bank of New York.

| | | | | | | | |

2014 | | High | | | Low | |

January | | | 1.3682 | | | | 1.3500 | |

February | | | 1.3806 | | | | 1.3507 | |

March | | | 1.3927 | | | | 1.3731 | |

April | | | 1.3898 | | | | 1.3704 | |

May | | | 1.3924 | | | | 1.3596 | |

June | | | 1.3690 | | | | 1.3522 | |

July | | | 1.3681 | | | | 1.3378 | |

August (through August 8, 2014) | | | 1.3436 | | | | 1.3355 | |

-3-

No representation is made that the euro or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or euro, as the case may be, at any particular rate.

There are, except in limited embargo circumstances, no legal restrictions in the Federal Republic on international capital movements and foreign exchange transactions. However, for statistical purposes only, every individual or corporation residing in the Federal Republic must report to the Deutsche Bundesbank, the German Central Bank, subject to a number of exceptions, any payment received from or made to an individual or a corporation resident outside of the Federal Republic if such payment exceeds EUR 12,500 (or the equivalent in a foreign currency).

-4-

RECENT DEVELOPMENTS

FMS-WM

Partial Transfer of Operations to Rome Branch

FMS-WM acquired part of the operations of the Rome branch of Depfa Bank plc (“Depfa”) in a transaction (cessione di ramo d’azienda) effective February 3, 2014. These transferred operations, which will be continued by the Rome branch of FMS-WM established in 2013, almost exclusively comprise assets (as well as the funding of such assets) the risk positions of which were initially taken over from Depfa by way of guarantee as of October 1, 2010. As a result of the partial transfer of operations, contingent liabilities of FMS-WM were reduced by EUR 2.0 billion in the first quarter of 2014. Loans and advances to customers will increase by the same amount.

Termination of the Liquidity Facilities Granted to Depfa

On January 31, 2014, Depfa and FMS-WM agreed to terminate the liquidity facility of EUR 3.8 billion previously granted to Depfa by FMS-WM effective February 17, 2014. Under the terms of this agreement, draw-downs under the facility, which totaled EUR 2.3 billion as of December 31, 2013, were repaid in full in February 2014.

The second liquidity facility granted to Depfa by FMS-WM was a variable facility, which was used to fund certain risk positions transferred by way of guarantee from Depfa to FMS-WM as of October 1, 2010 and to finance the cash collateral that Depfa was required to provide in an amount equal to the negative fair value of derivatives serving to hedge the above-mentioned risk positions. The draw-downs under this facility, which totaled EUR 1.0 billion as of December 31, 2013, were repaid in full in February 2014.

Privatization of FMS Wertmanagement Service GmbH

On February 7, 2014, FMS-WM published a preliminary announcement regarding the privatization of FMS Wertmanagement Service GmbH (“FMS-WM Service”) in the online version of the Supplement to the Official Journal of the European Union. The privatization will take place as part of a European Union (“EU”)-wide competitive tendering procedure that is expected to be completed by the end of 2014.

Wind-down of Depfa by FMS-WM

On May 13, 2014, the German Federal Agency for Financial Market Stabilization’s (Bundesanstalt für Finanzmarktstabilisierung) inter-ministerial steering committee and an extraordinary general meeting of Hypo Real Estate Holding AG decided in favor of the preparation of a takeover and wind-down of Depfa by FMS-WM. Depfa will have to be wound down in accordance with an EU state aid decision of July 18, 2011. The transfer to, and wind down of Depfa under, FMS-WM is subject, inter alia, to the approvals of the Irish and Luxemboug Regulators. The takeover of Depfa as a regulated entity may have an impact on FMS-WM’s financial performance. As of December 31, 2013, Depfa’s consolidated total assets amounted to EUR 49 billion.

The Federal Republic of Germany

Overview of Key Economic Figures

The following economic information regarding the Federal Republic is derived from the public official documents cited below. Certain of the information is preliminary.

-5-

Gross Domestic Product (GDP)

GROSS DOMESTIC PRODUCT

(adjusted for price, seasonal and calendar effects)(1)

| | | | |

Reference period | | Percentage change on

previous quarter | | Percentage change on the same quarter in previous year |

1st quarter 2013 | | 0.0 | | -0.3 |

2nd quarter 2013 | | 0.7 | | 0.5 |

3rd quarter 2013 | | 0.3 | | 0.6 |

4th quarter 2013 | | 0.4 | | 1.4 |

1st quarter 2014 | | 0.8 | | 2.3 |

| (1) | Adjustment for seasonal and calendar effects according to the Census X-12-ARIMA method. |

Germany’s gross domestic product increased by 0.8% after price, seasonal and calendar adjustments in the first quarter of 2014 compared to the fourth quarter of 2013. One factor that contributed to the strong growth at the beginning of 2014 was the extremely mild weather. Positive contributions to this increase were made only by domestic demand. Final consumption expenditure for both households and government increased compared to the fourth quarter of 2013. A positive development was also recorded for fixed capital formation, which significantly increased both in construction and in machinery and equipment compared with the fourth quarter of 2013. Moreover, building inventories supported the GDP growth. Foreign trade, however, had a downward effect on economic growth.

In a year-on-year comparison, economic growth accelerated markedly. GDP in the first quarter of 2014 increased by 2.3% in price- and calendar-adjusted terms compared to the first quarter of 2013.

Source: Statistisches Bundesamt, Gross domestic product up 0.8% in 1st quarter of 2014, press release of May 15, 2014 (https://www.destatis.de/EN/PressServices/Press/pr/2014/05/PE14_167_811.html).

Inflation Rate

INFLATION RATE

(based on overall consumer price index)

| | | | |

Reference period | | Percentage change on previous month | | Percentage change on the same month in previous year |

July 2013 | | 0.5 | | 1.9 |

August 2013 | | 0.0 | | 1.5 |

September 2013 | | 0.0 | | 1.4 |

October 2013 | | -0.2 | | 1.2 |

November 2013 | | 0.2 | | 1.3 |

December 2013 | | 0.4 | | 1.4 |

January 2014 | | -0.6 | | 1.3 |

February 2014 | | 0.5 | | 1.2 |

March 2014 | | 0.3 | | 1.0 |

April 2014 | | -0.2 | | 1.3 |

May 2014 | | -0.1 | | 0.9 |

June 2014 | | 0.3 | | 1.0 |

July 2014 | | 0.3 | | 0.8 |

In July 2014, consumer prices in Germany rose by 0.8% compared to June 2013, marking the lowest year-on-year rate of price increase since February 2010.

Energy prices declined by 1.5% from July 2013 to July 2014, representing a larger decline in energy prices when compared to previous months. Most notably, prices for mineral oil products were down 3.8% compared to a year earlier. In addition, prices for solid fuels and charges for central and district heating decreased by 2.5% and 1.3%, respectively, while prices for electricity rose by 1.7%. Excluding energy prices, the inflation rate in July 2014 compared to July 2013 would have been 1.2%.

-6-

Food prices increased by 0.1% in July 2014 compared to July 2013. In particular, prices for vegetables fell 7.7%. Additionally, consumers paid 4.4% less for edible oils and fats and 4.8% less for fruit, while prices for dairy products rose by 8.7%.

Total goods prices also increased by 0.1% in July 2014 compared to July 2013. Service prices rose above-average by 1.5% in July 2014, due mainly to a 1.4% increase in net rents exclusive of heating expenses.

Compared with June 2014, consumer prices rose by 0.3% in July 2014. In particular, prices for package holidays and air tickets increased by 11.6% and 8.8%, respectively. Food prices and energy prices decreased by 0.2% and 0.3%, respectively, from June 2014 to July 2014.

Source: Statistisches Bundesamt, Consumer prices in July 2014: +0.8% on July 2013, press release of August 13, 2014 (https://www.destatis.de/EN/PressServices/Press/pr/2014/08/PE14_285_611.html).

Unemployment Rate

UNEMPLOYMENT RATE

(percent of unemployed persons in the total labor force according to the

International Labour Organization (ILO) definition)(1)

| | | | |

Reference period | | Original percentages | | Adjusted percentages(2) |

June 2013 | | 5.4 | | 5.3 |

July 2013 | | 5.3 | | 5.3 |

August 2013 | | 5.0 | | 5.3 |

September 2013 | | 5.1 | | 5.3 |

October 2013 | | 5.1 | | 5.2 |

November 2013 | | 5.0 | | 5.2 |

December 2013 | | 5.0 | | 5.2 |

January 2014 | | 5.6 | | 5.2 |

February 2014 | | 5.5 | | 5.2 |

March 2014 | | 5.5 | | 5.2 |

April 2014 | | 5.3 | | 5.2 |

May 2014 | | 5.0 | | 5.1 |

June 2014 | | 5.0 | | 5.1 |

| (1) | The time series on unemployment are based on the German Labour Force Survey. |

| (2) | Adjusted for seasonal and irregular effects (trend cycle component) using the X-12-ARIMA method. |

The number of employed persons increased by approximately 379,000 persons, or 0.9%, from June 2013 to June 2014. Compared to May 2014, the number of employed persons in June 2014 increased by approximately 16,000, after adjustment for seasonal fluctuations.

In June 2014, the number of unemployed persons decreased by approximately 166,000, or 7.4%, compared to June 2013. When adjusted for seasonal and irregular effects (trend cycle component), the number of unemployed persons in June 2014 decreased by 0.9% to 2.16 million compared to May 2014.

Sources: Statistisches Bundesamt, June 2014: labour market nearly unchanged on May, press release of July 31, 2014 (https://www.destatis.de/EN/PressServices/Press/pr/2014/07/PE14_270_132.html); Statistisches Bundesamt, Genesis-Online Datenbank, Tabelle 13231-0001, Erwerbslose, Erwerbstätige, Erwerbspersonen, Erwerbslosenquote: Deutschland, Monate, Original- und bereinigte Daten (https://www-genesis.destatis.de/genesis/online/logon?sequenz=tabelleErgebnis&selectionname=13231-0001&zeitscheiben=2&leerzeilen=false).

-7-

Current Account and Foreign Trade

CURRENT ACCOUNTAND FOREIGN TRADE(1)

| | | | | | | | |

| | | (balance in EUR billion)(2) | |

Item | | January to June 2014 | | | January to June 2013 | |

Trade in goods, including supplementary trade items | | | 106.2 | | | | 108.8 | |

Services | | | -15.8 | | | | -22.9 | |

Primary income | | | 24.8 | | | | 29.2 | |

Secondary income | | | -21.7 | | | | -22.6 | |

| | | | | | | | |

Current account | | | 93.5 | | | | 92.4 | |

| | | | | | | | |

| (1) | The table reflects an updated statistical framework for the German balance of payments, which, as of July 2014, has been brought into line with the revised standard of the International Monetary Fund. For more information, see Deutsche Bundesbank, Monthly Report June 2014, pp. 57-68 (http://www.bundesbank.de/Redaktion/EN/Downloads/Publications/Monthly_Report/2014/2014_06_monthly_report.pdf?__blob=publicationFile). |

| (2) | Figures may not add up due to rounding. |

Source: Statistisches Bundesamt, German exports in June 2014: +1.1% on June 2013, press release of August 8, 2014 (https://www.destatis.de/EN/PressServices/Press/pr/2014/08/PE14_280_51.html).

Other Recent Developments

Policy Responses to the Global Economic and Financial Crisis

On June 5, 2014, the European Central Bank (“ECB”) announced several measures designed to enhance the functioning of the monetary policy transmission mechanism by supporting lending to the real economy. In particular, the ECB decided to conduct a series of targeted longer-term refinancing operations (“TLTROs”). These TLTROs are aimed at improving bank lending to the euro area non-financial private sector (defined as euro area households and non-financial corporations), excluding loans to households for house purchase, for a period of two years.

Source: European Central Bank, ECB announces monetary policy measures to enhance the functioning of the monetary policy transmission mechanism, press release of June 5, 2014 (http://www.ecb.europa.eu/press/pr/date/2014/html/pr140605_2.en.html).

The European Union and European Integration

On July 23, 2014, the Council of the European Union formally approved the accession of Lithuania to the euro area as of January 1, 2015. The ECB will take over direct supervision of the biggest Lithuanian banks in January 2015, as the country is also joining the Single Supervisory Mechanism.

Source: European Central Bank, Lithuania to join euro area and single supervisory mechanism (SSM) on 1 January 2015, press release of July 23, 2014 (http://www.ecb.europa.eu/press/pr/date/2014/html/pr140723.en.html).

-8-

FMS WERTMANAGEMENT

Overview

FMS-WM is a wind-up institution (Abwicklungsanstalt) organized as a public law entity (Anstalt öffentlichen Rechts) under public law of the Federal Republic with partial legal capacity pursuant to Section 8a para 1 of the German Financial Market Stabilization Fund Act (Finanzmarktstabilisierungsfondsgesetz, “FMStFG”). Partial legal capacity, under German administrative law, means that FMS-WM does not have the right to bring an administrative proceeding against the German Federal Agency for Financial Market Stabilization (Bundesanstalt für Finanzmarktstabilisierung, “FMSA”) under its charter. FMS-WM has, however, full power and legal capacity to contract with third parties and sue and be sued in court. FMS-WM is fully owned by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds, “SoFFin”), which is a special pool of assets (Sondervermögen) of the Federal Republic. FMS-WM is charged with liquidating a portfolio of risk positions and non-strategic assets/businesses in an original amount of EUR 175.7 billion (nominal volume) that it assumed from Hypo Real Estate Holding AG and its subsidiaries and special purpose entities (referred to herein collectively as the “HRE Group”) on October 1, 2010. As of 2007, the HRE Group was one of the largest commercial property lenders, issuers of covered bonds and providers of public finance in Germany. It encountered severe financial difficulties in 2008/09 in the course of the global financial markets crisis. Given the systemic importance of the HRE Group and the resulting public interest in stabilizing the HRE Group, the Federal Republic initiated support measures for this financial institution, including the transfer of risk positions and non-strategic assets/businesses to FMS-WM.

FMS-WM pursues its objective of managing and winding up its portfolio according to a strategic management framework known as the winding-up plan (Abwicklungsplan), which is updated and adapted on a regular basis. FMS-WM aims to maximize the value of its portfolio by managing and liquidating it in a value-preserving manner over an extended period of time. For any given part of the portfolio, the plan requires an assessment of whether FMS-WM should sell, hold, or restructure its holdings. As of December 31, 2013, FMS-WM had liquidated approximately EUR 56.6 billion of its initial portfolio of EUR 175.7 billion.

FMS-WM engages in funding activities, including the issuance of debt securities and/or obtaining financing from financial institutions, in order to refinance funding instruments associated with the portfolio it has assumed as they expire. FMS-WM will have to engage in refinancing activities on the capital markets until its portfolio has been liquidated. As of December 31, 2013, FMS-WM had subscribed capital of EUR 200,000, the total amount of which had been paid in.

FMS-WM’s obligations are backed by the full faith and credit of the Federal Republic. Pursuant to the FMStFG, FMS-WM’s obligations benefit from a statutory guarantee of SoFFin and under FMS-WM’s charter, SoFFin is obligated to cover all losses sustained by FMS-WM and to ensure that FMS-WM is able to pay all its liabilities at any time when due and in full. According to Section 5 of the FMStFG, the Federal Republic, in turn, is directly liable for all of SoFFin’s obligations.

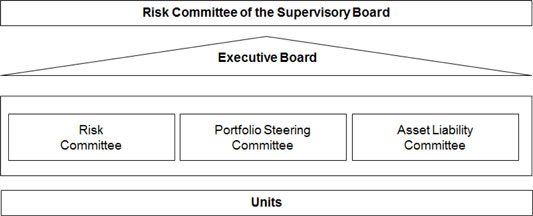

FMS-WM is governed by two corporate bodies: the Supervisory Board (Verwaltungsrat) and the Executive Board (Vorstand). The six-member Supervisory Board is appointed by SoFFin and is responsible for the composition and oversight of the Executive Board as well as for major strategic decisions of FMS-WM. The Executive Board has a minimum of two members (currently three) and is appointed by the Supervisory Board. It is responsible for representing FMS-WM externally and for managing its business. In addition, a General Manager (Generalbevollmächtigter) was appointed by the Executive Board, who functions as Chief Operating Officer. In February 2014, the Supervisory Board decided that the Executive Board would assume the responsibilities previously assigned to the Management Board (Geschäftsleitung).

FMS-WM is registered with the commercial register (Handelsregister) of the local court (Amtsgericht) of Munich under HRA 96076. Its registered office and business address is at Prinzregentenstraße 56, 80538 Munich, Federal Republic of Germany. Its telephone number is +49 89 9547627-0. FMS-WM maintains a branch in Rome, Italy. The Italian branch was registered with the company register (Registro delle Imprese) of Rome on May 7, 2013 under registration number 12372371000. As at the date hereof, the registered status of the Italian branch is inactive. As of August 13, 2014, FMS-WM does not intend to open any additional branches.

Creation and Legal Status

FMS-WM’s creation and legal status are a direct result of the German Federal Government’s response to the global financial markets crisis. In October 2008, the German Federal Government enacted a comprehensive package of measures to support key German strategic financial institutions, most notably the HRE Group. This comprehensive package included the FMStFG, which provided for the implementation of SoFFin and established the FMSA, a federal agency under public law with legal personality (rechtsfähige Anstalt öffentlichen Rechts) supervised by the German Federal Ministry of Finance (Bundesfinanzministerium). Section 8a of the FMStFG grants the FMSA the power to create wind-up institutions. The purpose of these institutions is to assume distressed and non-strategic assets from systemically important financial institutions and to eventually dispose of or liquidate the risk positions transferred to them.

-9-

As of 2007, the HRE Group was one of the largest commercial property lenders and providers of public finance in Germany. Most of the commercial property loans were refinanced by the issuance of covered bonds, making the HRE Group the leading German issuer of covered bonds. In the course of the liquidity crisis in September 2008, the HRE Group encountered financial difficulties primarily caused by the heavy debt burden held by one of its subsidiaries, Depfa Bank plc (“Depfa”). Depfa had borrowed short-term money to fund higher interest-bearing long-term positions in public sector finance on a large scale. When the interbank lending market collapsed in September 2008, Depfa faced substantial refinancing problems. Within a short period of time, the entire HRE Group faced solvency issues as well. Due to the HRE Group’s importance for the German financial system, the Federal Republic initiated various support measures, which led to the SoFFin becoming the sole owner of Hypo Real Estate Holding AG (“HRE”) in October 2009. The government support measures also included the extension of liquidity guarantees by SoFFin and the creation of FMS-WM as a wind-up institution under Section 8a of the FMStFG on July 8, 2010. Risk positions and non-strategic assets/businesses of the HRE Group were then transferred to FMS-WM on October 1, 2010.

FMS-WM is a public law institution with partial legal capacity (teilrechtsfähige Anstalt des öffentlichen Rechts) created pursuant to German administrative law. It is fully-owned by the SoFFin and is subject to the supervision and control of the FMSA. FMS-WM may act in its own name, and may be subject to court proceedings. In order to achieve its mandate of winding-up the portfolio of risk positions and non-strategic assets/businesses assumed from the HRE Group, FMS-WM may engage in all kinds of banking and financial services transactions and all other transactions that directly or indirectly serve its purposes. FMS-WM is, however, neither a financial institution nor a financial services institution within the meaning of the German Banking Act (Kreditwesengesetz, “KWG”), nor a financial service provider within the meaning of the German Securities Trading Act (Wertpapierhandelsgesetz, “WpHG”), nor an insurance company within the meaning of the German Insurance Supervision Act (Versicherungsaufsichtsgesetz, “VAG”) nor regulated as such. As a consequence, FMS-WM is prohibited from engaging in transactions that would require a license under the EU Banking Directive (2006/48/EC) or the EU Directive on markets for financial instruments (2004/39/EC). Nonetheless, pursuant to its charter and the FMStFG, FMS-WM is subject to certain provisions of the KWG and the WpHG. In particular, FMS-WM is subject to banking supervision by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht) and must comply with the organizational obligations and restrictions on certain activities imposed by the KWG applicable to banks and financial institutions. FMS-WM is, however, exempted from the regulatory capital and liquidity requirements and the licensing requirements under the KWG. FMS-WM is also deemed to be a financial institution for purposes of the German Money Laundering Act (Geldwäschegesetz), and is therefore subject to the provisions thereof.

-10-

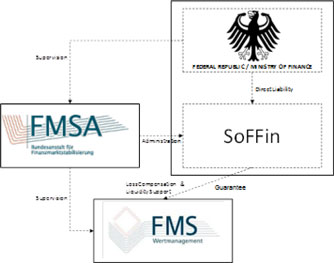

Relationship with the Federal Republic of Germany

The following chart provides an overview of the relationship between FMS-WM and the Federal Republic.

Relationship with SoFFin

SoFFin. FMS-WM is fully owned by SoFFin, which is established by law and designated to fulfill specific tasks of the German Federal Government assigned to it under the FMStFG. SoFFin is administered by FMSA. SoFFin is a special pool of assets (Sondervermögen) of the Federal Republic. The term special pool of assets (Sondervermögen) designates legally dependent assets of the Federal Republic. Accordingly, the FMStG provides that SoFFin shall have no legal capacity, although in legal relations SoFFin may act, sue and be sued in its own name. There shall be no attachment of, or other measures of compulsory execution against, SoFFin. Any debt incurred by SoFFin is accounted for as direct debt of the Federal Republic. In addition, Section 5 of the FMStFG provides that the Federal Republic is directly liable for the obligations of SoFFin. SoFFin’s obligations are thus effectively obligations of the Federal Republic.

SoFFin’s purpose is to stabilize the German financial sector by extending liquidity guarantees, providing equity capital, assuming risk positions, and setting up wind-up institutions. To this end, SoFFin has been authorized by the German legislature under Section 6 of the FMStFG to extend liquidity guarantees in a total aggregate amount of up to EUR 400 billion. In addition, Section 9 of the FMStFG authorizes the German Federal Ministry of Finance to incur debt in a total aggregate amount of up to EUR 80 billion to cover the cost of measures taken by SoFFin in connection with the provision of equity capital, the assumption of risk positions and the compensation of losses of wind-up institutions. Specifically, the authorization permits the German Federal Ministry of Finance to incur debt up to an amount of EUR 40 billion. Subject to the approval of the parliamentary control panel for financial market stabilization which is comprised of nine members of the budget committee of the German Bundestag, this amount can be increased by up to another EUR 30 billion and, subject to the approval of the budget committee of the German Bundestag, by up to another EUR 10 billion. Any financing required by SoFFin is obtained in the manner used by the Federal Republic to finance itself, i.e., through the issuance of debt instruments by the Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH). When the Federal Republic incurs debt for SoFFin, it results in an increase in the net borrowings and debt of the Federal Republic. Applications for stabilization measures extended by SoFFin could initially be made only until the end of 2010. As a consequence of developments in the euro area, however, the German Federal Government has re-opened the application period twice since then, initially until the end of 2012 and, subsequently, until the end of 2014.

Guarantee. With effect from January 1, 2014, Section 8a of the FMStFG, which deals with the establishment of wind-up institutions, was amended to provide that SoFFin guarantees all existing and future obligations of FMS-WM with respect to moneys, debt securities and derivative transactions as well as obligations of third parties that are expressly guaranteed by FMS-WM, which FMS-WM has borrowed, issued, entered into or incurred or which have been transferred to FMS-WM during the time period for which SoFFin is the sole obligor of the loss compensation obligation (alleiniger Verlustausgleichspflichtiger). For a description of SoFFin’s loss compensation obligation, see “–Loss Compensation and Liquidity Support Obligations” below. Accordingly, under the guarantee, if FMS-WM fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued by it when that payment is due and payable, SoFFin will be liable for that payment as and when it becomes due and payable, provided that the security was issued during the time period for which SoFFin was the sole obligor of the loss compensation

-11-

obligation. SoFFin’s obligation under the guarantee ranks equally, without any preference, with all of its other present and future unsecured and unsubordinated indebtedness. Holders of securities issued by FMS-WM may enforce this obligation directly against SoFFin without first having to take legal action against FMS-WM. If SoFFin fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued by FMS-WM when that payment is due and payable under the guarantee, the Federal Republic will be liable for that payment as and when it becomes due and payable pursuant to Section 5 of the FMStFG, as described above. The guarantee and the Federal Republic’s direct liability for SoFFin’s obligations pursuant to Section 5 of the FMStFG are strictly a matter of statutory law and are not evidenced by any contract or instrument. Potential claims based on the guarantee and on Section 5 of the FMStFG may be subject to defenses available to FMS-WM and SoFFin with respect to the obligations covered.

Loss Compensation and Liquidity Support Obligations. Under FMS-WM’s charter, which was enacted pursuant to Section 8a of the FMStFG, SoFFin is obligated to cover all losses sustained by FMS-WM and to ensure that FMS-WM is able to pay all its liabilities at all times when due and in full. As described above, pursuant to Section 5 of the FMStFG, the Federal Republic is directly liable for SoFFin’s obligations. Accordingly, SoFFin’s loss compensation and liquidity support obligations enable FMS-WM to pursue its operations and effectively mean that FMS-WM’s obligations, including the obligations to holders of debt securities issued by FMS-WM, are backed by the full faith and credit of the Federal Republic.

For the year ended December 31, 2013, SoFFin recorded a profit of EUR 23.0 million, largely due to valuation effects. As of December 31, 2013, the total outstanding stabilization measures provided by SoFFin amounted to EUR 17.1 billion, which related entirely to equity capital.

Relationship with FMSA

FMS-WM operates under the supervision and control of the Federal Republic, which is exercised through the FMSA. FMSA was established to manage SoFFin and to implement and monitor the stabilization measures extended by SoFFin. FMSA has the power to create wind-up institutions under Section 8a of FMStFG. FMSA is supervised by the German Federal Ministry of Finance (Bundesfinanzministerium), which ensures that FMSA acts in the public interest. In particular, the German Federal Ministry of Finance supervises FMSA’s activities and nominates the members of FMSA’s management committee (Leitungsausschuss). Certain decision-making powers have been delegated to the management committee by the FMStFG.

FMSA appoints the members of FMS-WM’s Supervisory Board. The Supervisory Board members, in turn, appoint the members of FMS-WM’s Executive Board. Both the Supervisory Board and FMSA may dismiss a member of the Executive Board for good cause.

FMSA is responsible for the legal supervision of FMS-WM. In particular, FMSA has to approve and supervise FMS-WM’s implementation of the winding-up plan as well as any deviations from, or amendments to, the winding-up plan. FMSA may give instructions to FMS-WM’s Executive Board and Supervisory Board in order to ensure that FMS-WM complies with applicable law and the requirements of its charter. Comprehensive reporting obligations by FMS-WM ensure that FMSA has a solid basis for exercising its control and instruction rights.

In keeping with its supervisory role, FMSA action is required for the dissolution of FMS-WM. While there is no set maximum duration for FMS-WM’s existence, FMS-WM’s charter provides that FMS-WM shall exist only until the transferred risk positions and non-strategic assets/businesses have been liquidated in full, at which point it is obligated to notify FMSA. FMSA may initiate the final dissolution process for FMS-WM if it has no remaining liabilities or if SoFFin has assumed any remaining liabilities. Any assets or profits remaining at the time of dissolution will be transferred to SoFFin.

Business and Operations

Introduction

FMS-WM is tasked with unwinding the portfolio of risk positions and non-strategic assets/businesses that it assumed on October 1, 2010 from the HRE Group in ways that maximize its value. As described in more detail under “—Outsourced Portfolio Administration,” the HRE Group ceased to provide asset management and financing services for FMS-WM as of September 30, 2013. As of October 1, 2013, FMS-WM Service has been tasked with administering the portfolio assumed by FMS-WM.

-12-

FMS-WM’s activities are characterized by the following strategic goals:

| | • | | Winding-up of the risk assets aimed at maximizing their value: FMS-WM aims to unwind the risk assets in a manner that maximizes their value, subject to defined wind-up and risk strategies that are adjusted on a continuous basis. The winding-up plan – which is the key strategic management tool of FMS-WM – serves as the basis for the implementation of its portfolio liquidation operations. Depending on the market situation and the asset category, the winding-up plan provides for the following strategies in connection with liquidating the portfolio assumed by FMS-WM: |

| | • | | Holding assets, which includes active management of loans and securities with a view to repaying outstanding amounts (e.g., where the risk/return profile is acceptable). |

| | • | | Selling assets to the extent it makes economic sense (e.g., to reduce positions with a higher risk profile and when market opportunities arise). |

| | • | | Restructuring, including workout, wind-up and reorganization measures, relating to both performing and non-performing financial instruments, particularly in the Infrastructure and Commercial Real Estate segments, with a view to maximizing the value of the liquidation measure related to the financial instrument (including by reducing risk). |

| | • | | Cost-effective servicing and management of the risk assets: The wind-up of the risk assets is carried out in part by FMS-WM itself and in part by FMS-WM Service (as of October 1, 2013; until September 30, 2013, the HRE Group functioned as the external service provider carrying out the wind-up of the risk assets in part) as portfolio servicer. FMS-WM remains solely responsible for the winding-up aimed at maximizing value and the cost-effective servicing and management of the portfolio. |

| | • | | Cost-effective funding and separate market access for FMS-WM: FMS-WM seeks to ensure cost-effective funding for the purpose of carrying out its mandate. Given its backing by the full faith and credit of the Federal Republic, FMS-WM is able to realize funding cost advantages that are not available to the HRE Group. |

In order to achieve its mandate of winding up the portfolio of risk positions and non-strategic assets/businesses assumed from the HRE Group, FMS-WM may engage in all kinds of banking and financial services transactions and all other transactions that directly or indirectly serve its purposes. FMS-WM is, however, neither a financial institution nor a financial services institution within the meaning of the KWG, nor a financial service provider within the meaning of the WpHG, nor an insurance company within the meaning of the VAG. FMS-WM is also prohibited from engaging in transactions that would require a license under the EU Banking Directive (2006/48/EC) or the EU Directive on markets for financial instruments (2004/39/EC).

The Portfolio

FMS-WM assumed a portfolio of risk positions and non-strategic assets/businesses in an original amount of EUR 175.7 billion (nominal volume) from the HRE Group on October 1, 2010. As of December 31, 2013, FMS-WM had liquidated approximately EUR 56.6 billion (December 31, 2012: EUR 38.8 billion) of its initial portfolio of EUR 175.7 billion. As of the same date, FMS-WM’s portfolio encompassed 3,855 individual exposures (December 31, 2012: 4,553) with 1,859 different counterparties (December 31, 2012: approximately 2,144) and a significant amount of derivatives. The individual exposures are located in 63 countries and denominated in 16 currencies. Geographically, the greatest concentrations are in Germany, the United States, the United Kingdom, Spain and Italy. About half (52%) of the exposures in the portfolio are denominated in euro, nearly a quarter (23%) in U.S. dollars, approximately 16% in GBP and approximately 4% in JPY. The portfolio is highly complex and diverse and consists of a particularly high proportion of illiquid exposures with extremely long maturities. To the extent that a legal transfer of risk assets could not be effected as of October 1, 2010 (for example, due to outstanding consent requirements), economic ownership of such risk positions was transferred synthetically to FMS-WM (for example, through subparticipations or guarantees). FMS-WM is currently working on the physical and legal transfer of these risk positions that to date have only been transferred synthetically from the HRE Group to FMS-WM, and exposures relating to synthetically transferred receivables and derivatives still awaiting novation were significantly reduced in 2013.

For purposes of risk management and the wind-up reports that FMS-WM submits to FMSA on a monthly basis in accordance with the winding-up plan, FMS-WM has classified the portfolio into four segments – Commercial Real Estate, Infrastructure, Public Sector and Structured Products. The Commercial Real Estate and Commercial Real Estate-Workout segments were merged to form the Commercial Real Estate segment in 2013. The segments in turn are broken down into 34 wind-up clusters. The assets of all four segments include syndicated loans.

-13-

Outsourced Portfolio Administration

Until September 30, 2013, the HRE Group served as an outside administrator of the portfolio transferred to FMS-WM. The work outsourced to the HRE Group pursuant to a cooperation agreement between FMS-WM and Deutsche Pfandbriefbank AG (“PBB”), the core financial institution of the HRE Group, included many of the administrative activities in connection with the portfolio assumed and, as of December 31, 2012, approximately 500 employees of the HRE Group were working for FMS-WM in connection with portfolio servicing at a cost of approximately EUR 21 million per month.

As the transfer of risk positions and non-strategic assets/businesses from the HRE Group to FMS-WM could be viewed as state aid, the transfer had to be approved by the European Commission. In this context, the Federal Republic committed to ensure that, after September 30, 2013, the HRE Group will provide neither asset management services nor refinancing services for FMS-WM and that, from an organizational point of view, those services can be assumed by third parties. Pursuant to this commitment, the cooperation agreement with PBB has been terminated with effect as of September 30, 2013.

Since October 1, 2013, FMS-WM Service, a service entity established by FMS-WM in April 2012, has been tasked with the full set of portfolio management services and operations services including collateral management, settlement functions and credit operations, while FMS-WM retains final decision-making powers and ultimate responsibility for the risk assets under management. The master agreement governing the outsourcing of business processes and services also grants FMS-WM extensive rights to obtain information and perform inspections, enabling it to monitor and control the servicing of the risk assets by FMS-WM Service. Further, IBM Deutschland GmbH, has assumed the provision of comprehensive information technology services as of October 1, 2013, and additional third-party service providers perform regulatory reporting and financial administration functions.

FMS-WM’s Segments

As described above, FMS-WM’s portfolio is grouped into four segments – Commercial Real Estate, Infrastructure, Public Sector and Structured Products.

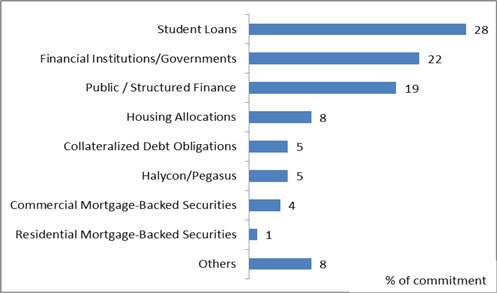

Structured Products

As of December 31, 2013, the Structured Products segment comprised assets with a nominal value of EUR 31.4 billion, which accounted for 26.4% of FMS-WM’s overall portfolio (December 31, 2012: EUR 36.3 billion). The Structured Products segment includes practically all types of structured credit instruments from asset-backed securities, commercial and residential mortgage-backed securities or collateralized debt obligations to exotic interest, inflation and credit derivatives. Many of the underlying assets of these structured products originated in the United States. The following chart reflects the proportion of the various asset classes in the segment.

-14-

The Structured Products segment succeeded in winding up exposures with a nominal value of approximately EUR 4.9 billion in 2013 (2012: EUR 5.9 billion). Forced sales of the exposures would have been possible only at substantial discounts, due to, among other reasons, changed market conditions, sharp cuts in external ratings and the poor quality of the assets that serve as collateral for these securities.

A hold strategy often is the best option for preventing losses on sales because most structured products are highly illiquid securities, i.e., they are rarely traded in the market. In some cases, restructuring the transactions increased their value or improved their tradability. Client derivatives in the acquired portfolio that were entered into with municipalities and cities in Europe and America present a particular challenge in this respect. Many of these derivatives must be restructured to maintain their value and minimize losses. The increase in the number of non-performing exposures in this category is also creating the need for additional workout efforts.

Infrastructure

As of December 31, 2013, the Infrastructure segment held 483 exposures with an aggregate nominal value of EUR 14.5 billion (12.1% of FMS-WM’s total portfolio) (December 31, 2012: EUR 16.4 billion). These exposures are spread across all five continents (with a focus on the United Kingdom, which makes up more than half of the segment’s total portfolio as of December 31, 2013) and encompass loans (approximately 46.7%) and securities (approximately 53.3%) which were used to finance regulated utilities (31%), social infrastructure (19%), roads (17%), non-roads (10%), airports and ports (8%), power/energy (7%), environmental water/waste (3%), telecommunications and others (3%) and asset finance (2%). Most of the loans in this segment have very long maturities and were closed at margins that are substantially below current market levels because many borrowers were either government or government-sponsored entities or are structures to which the public sector is a party in some other way, for instance as the entity that procures products and services. In view of the complexity of the portfolio held by this segment, activities of this segment focus on restructuring individual transactions to improve the chances of effecting a subsequent redemption, (partial) settlement by a third party or subsequent sale.

The portfolio held by this segment was reduced by approximately 61 exposures in 2013, corresponding to a reduction of approximately EUR 1.9 billion, or roughly 12% (December 31, 2012: EUR 0.7 billion), related to sales of ports and airports. It is very difficult to sell or prematurely repay individual exposures or entire sub-portfolios because the assumptions that were made at the time of entering into the exposures in many of these projects with respect to the degree of utilization or occupancy have in the meantime turned out to be too optimistic.

-15-

The economic success of infrastructure projects is generally dependent on external factors, including the growth of the gross domestic product (“GDP”), the unemployment rate and energy costs. Despite the uptake in infrastructure financing in 2013, the portfolio held by this segment continues to be adversely affected by the persistent financial and economic crisis.

Public Sector

As of December 31, 2013, the Public Sector segment held assets with an aggregate nominal value of EUR 59.8 billion, accounting for 50.3% of FMS-WM’s total portfolio (December 31, 2012: EUR 67.4 billion). The Public Sector segment accomplished a satisfactory unwinding result in 2013 with a share of around 68.2% in active sales (consisting of, in particular, Greek and Japanese bonds), accompanied by positive trends in the bond markets in the euro area, which led to higher securities prices. In particular, FMS-WM’s Greek exposures were further reduced to EUR 1.5 billion in fiscal year 2013, as FMS-WM effected targeted sales of small tranches of government bonds in the secondary market.

However, there was a deterioration in the ratings breakdown of the Public Sector segment’s portfolio. The year-on-year decline in the volume of financing with top ratings of “AAA”, “AA” and “A” by S&P was mainly due to sales of and exchange rate effects on Japanese government bonds, the repayment of loans and advances to the European Financial Stability Facility (“EFSF”) assumed in the course of restructuring the Greek bond position, and larger principal repayments from German states and regional state banks.

FMS-WM is working to improve its position in the medium and long term. To that end, FMS-WM negotiates directly with the issuers of the bonds or the counterparties of hedging transactions with the aim of unwinding, simplifying or untangling complex coupon or derivatives structures.

Commercial Real Estate

As of December 31, 2013, the Commercial Real Estate segment, which was merged with the former Commercial Real Estate-Workout segment during the course of 2013, held assets with a nominal value of EUR 13.4 billion, accounting for 11.3% of FMS-WM’s total portfolio (December 31, 2012: aggregate amount held by Commercial Real Estate and Commercial Real Estate-Workout segments was EUR 16.8 billion).

FMS-WM’s Commercial Real Estate segment is managed by FMS-WM’s Commercial Real Estate units. The portfolio of the segment had a volume of approximately EUR 27.2 billion when it was transferred in October 2010. It was reduced to approximately 727 counterparties and a volume of EUR 13.4 billion as of December 31, 2013 (December 31, 2012: EUR 16.8 billion), corresponding to a net reduction of approximately EUR 3.4 billion.

Loans secured by mortgages on commercial real estate account for the majority of the global portfolio managed by the Commercial Real Estate segment. On the one hand, the portfolio is composed of loans for office properties (39% of the nominal value) in European metropolitan areas, Asia and the United States; loans for shopping centers (13%), as well as hotels (7%) and hospitals; or residential properties (7%) in Europe, both in Germany and elsewhere.

The standard wind-up strategies of the segment are to “hold”, “restructure” and “sell”. The restructuring strategy approach is pursued when it becomes evident that a borrower cannot repay the loan upon maturity. The objective here is to stabilize the exposure and thus improve the outlook for later repayment or sale of the loan or collateral.

In some cases, FMS-WM carries out foreclosures to enforce claims. In very rare cases, rescue acquisitions are made in which FMS-WM takes over a financed property with the aim of selling it again as quickly as possible after further restructuring. The principle of maximizing value remains of the utmost importance in this case as well.

A major part of the unwinding of the Commercial Real estate segment’s portfolio is expected to be completed by 2020.

-16-

Winding-Up the Portfolio

The portfolio assumed by FMS-WM is managed and liquidated in accordance with a winding-up plan (Abwicklungsplan), which describes the wind-up measures FMS-WM intends to take and includes a timeline for liquidation measures relating to the risk positions and non-strategic assets/businesses. The winding-up plan is proposed by FMS-WM’s Executive Board and adopted by the Supervisory Board. In accordance with its charter, FMS-WM submits monthly reports to the FMSA, which include information on the process of recovery and liquidation under the winding-up plan. In its supervisory capacity, the FMSA has the right to request changes to the winding-up plan and approves and supervises FMS-WM’s implementation of the winding-up plan as well as any deviations from, or amendments to, the winding-up plan. FMS-WM monitors prevailing market conditions on an ongoing basis to determine whether the winding-up plan needs to be adapted.

The winding-up plan has been designed with a view to ensuring that FMS-WM at all times has sufficient liquidity to cover its three-month liquidity requirements under stress scenario assumptions over the entire wind-up period, independently of SoFFin’s duty to provide liquidity to FMS-WM and to offset losses incurred by it. It also provides that, in principle, FMS-WM may not engage in new business with the exception of refinancing and hedging transactions and selected new business that reduces portfolio risks in a cost efficient manner (e.g., prolongations as well as selective restructuring measures).

The process of selling individual assets follows detailed, fixed instructions. For instance, a sale has to be based on offers from several bidders and deviations from this process are only permitted under special circumstances. The sales process aims to ensure verification and documentation that bids reflect market prices.

In addition to actively reducing the portfolio volume, an important goal for the successful management of the portfolio is the improvement of the quality of the portfolio’s structure, which FMS-WM strives to achieve by restructuring loan exposures, securities holdings and derivative positions. In this way, FMS-WM substantially improved the medium- to long-term prospects for the realization of numerous exposures in 2013, for example through intensive negotiations with borrowers, consortium members and issuers. Such successfully implemented restructuring measures have the effect of reducing the portfolio’s complexity and risk.

Since taking over the portfolio from the HRE Group, the portfolio’s nominal value has been reduced from EUR 175.7 billion to EUR 119.1 billion by the end of 2013 (2012: EUR 136.9 billion). This corresponds to a reduction of 32.2%. Of the cumulative reduction in the portfolio by EUR 56.6 billion by December 31, 2013, active sales accounted for EUR 12.2 billion and contractual redemptions and amortizations accounted for the remainder of EUR 44.4 billion. The cumulative portfolio reduction of EUR 55.4 billion was positively impacted by currency effects of EUR 1.2 billion.

The following table shows the reconciliation of the nominal value of the portfolio excluding derivatives from the transfer date (October 1, 2010) to total assets as of December 31, 2013 and 2012 (translated at exchange rates as of December 31, 2013 and 2012, respectively):

| | | | | | | | |

| | | As of December 31, | |

| | | 2012 | | | 2013 | |

| | | (unaudited) | |

| | | (€ in billions) | |

Wind-up portfolio commitment as of October 1, 2010 | | | 175.7 | | | | 175.7 | |

– Cumulative portfolio wind-up | | | –41.3 | | | | –55.4 | |

+ Currency effects | | | +2.5 | | | | –1.2 | |

| | | | | | | | |

Wind-up portfolio commitment | | | 136.9 | | | | 119.1 | |

– Undrawn credit lines and guarantees | | | –6.4 | | | | –3.7 | |

+ Portfolio of own issues(1) | | | +65.2 | | | | +35.6 | |

+ Other receivables including portions thereof(2) | | | +50.7 | | | | +36.7 | |

| | | | | | | | |

Total assets | | | 246.4 | | | | 187.7 | |

| | | | | | | | |

| (1) | Nominal value before accrued interest. |

| (2) | Mainly contains the cash collateral for derivatives, amortized cost of derivatives taken over, receivables from liquidity facilities used, current credit balances, accrued interest and loss compensation claims against SoFFin. |

-17-

Based on nominal values broken down by segment, the portfolio was reduced as follows from October 1, 2010 to December 31, 2013 (translated at exchange rates as of December 31, 2013):

| | | | | | | | | | | | | | | | |

| | | October 1, 2010 | | | Portfolio wind-up | | | Currency effects | | | December 31, 2013 | |

| | | (unaudited) | |

| | | (€ in billions) | |

Structured Products | | | 43.9 | | | | –12.3 | | | | –0.2 | | | | 31.4 | |

Infrastructure | | | 18.0 | | | | –3.5 | | | | 0.0 | | | | 14.5 | |

Public Sector | | | 86.6 | | | | –25.8 | | | | –1.0 | | | | 59.8 | |

Commercial Real Estate | | | 27.2 | | | | –13.8 | | | | 0.0 | | | | 13.4 | |

| | | | | | | | | | | | | | | | |

Total | | | 175.7 | | | | –55.4 | | | | –1.2 | | | | 119.1 | |

| | | | | | | | | | | | | | | | |

The following table shows the remaining maturities of the assets broken down by segments as of December 31, 2013:

| | | | | | | | | | | | | | | | | | | | |

| | | 2013–2015 | | | 2016–2020 | | | 2021–2030 | | | 2031–2040 | | | After 2040 | |

| | | (unaudited) | |

| | | (€ in billions) | |

Structured Products | | | 6.0 | | | | 14.0 | | | | 11.1 | | | | 20.8 | | | | 7.9 | |

Infrastructure | | | 1,5 | | | | 1.1 | | | | 2.5 | | | | 3.0 | | | | 6.3 | |

Public Sector | | | 0.5 | | | | 4.5 | | | | 7.4 | | | | 8.6 | | | | 10.4 | |

Commercial Real Estate | | | 10.5 | | | | 2.3 | | | | 0.4 | | | | 0.0 | | | | 0.2 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | | 18.5 | | | | 21.9 | | | | 21.4 | | | | 32.4 | | | | 24.8 | |

| | | | | | | | | | | | | | | | | | | | |

Exposure to Troubled Sovereigns and Concentration Risks

The portfolio of FMS-WM contains several significant concentration risks, including those in sovereign debt exposures. As the example of Greece showed in 2011, such concentration risks, which are vulnerable to macroeconomic or systemic risks, can cause significant losses in FMS-WM’s portfolio. In addition to Greece, there are major concentrations in the portfolio related to the other “PIIGS” countries (i.e., Portugal, Ireland, Italy, Greece, Spain), particularly in the Public Sector segment. In fiscal 2013, Italy comprised an important part of FMS-WM’s exposure at default (“EaD”), accounting for EUR 31.0 billion, representing approximately 22.7% of FMS-WM’s total EaD (2012: EUR 32.1 billion). For more information on the breakdown of FMS-WM’s credit portfolio by countries and regions, see “—Risk Report—Credit Risks—Breakdown of Credit Portfolio by Countries and Regions.”

The following table shows a breakdown of FMS-WM’s EaD by sector for bonds and loans concerning the PIIGS countries, including information on related microhedges, as of December 31, 2013.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Exposure at Default – Bonds & Loans per Sector | | | | | | Microhedges(2) | |

Country(1) | | Gross

sovereign | | | Other

public

borrowers | | | Financial

institutions | | | Non-financial

corporations | | | Total EaD per

country | | | Additional (negative)

MtM of Microhedges | |

| | | (unaudited) | |

| | | (€ in millions) | |

Italy | | | 24,937 | | | | 3,050 | | | | 203 | | | | 2,761 | | | | 30,952 | | | | (2,277 | ) |

Spain | | | 1,132 | | | | 4,165 | | | | 1,305 | | | | 2,118 | | | | 8,720 | | | | (363 | ) |

Portugal | | | 1,206 | | | | 111 | | | | 201 | | | | 829 | | | | 2,347 | | | | (90 | ) |

Greece | | | 1,550 | | | | 0 | | | | 0 | | | | 5 | | | | 1,555 | | | | (53 | ) |

Ireland | | | 0 | | | | 346 | | | | 362 | | | | 609 | | | | 1,316 | | | | (28 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 28,825 | | | | 7,671 | | | | 2,072 | | | | 6,321 | | | | 44,889 | | | | (2,812 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | The allocation is based on the country of the economic risk (e.g., location of the collateral), which may be different from the legal domicile of the debtor/issuer in individual cases. |

| (2) | The exposure-at-default definition applied by FMS-WM already accounts for negative mark-to-market (MtM) values of microhedges as of the date of the asset transfer from the HRE Group in October 2010. In order to avoid redundancies, and different from the presentations in the prior year’s table, only the current negative mark-to-market values of microhedge instruments to the extent that they exceed their October 2010 values are included in this table. In 2013, market developments resulted in a MtM-increase, i.e., a decrease of negative MtM of PIIGS microhedge instruments of about EUR 3.5 billion. |

-18-

Treasury, Capital Markets Funding

FMS-WM engages in funding activities, including the issuing of debt securities and/or obtaining financing from financial institutions, in order to refinance funding instruments associated with the assumed portfolio as they expire. FMS-WM will have to engage in refinancing activities until its portfolio has been liquidated. In the first quarter of fiscal 2012, refinancing from the European Central Bank (“ECB”), which had amounted to EUR 35.2 billion as of December 31, 2011, was fully replaced by the inflow of funds from FMS-WM’s own money and capital markets issuances. In fiscal year 2013, the funding requirement saw a year-on-year decline of EUR 24 billion, as a loss compensation claim in respect of SoFFin amounting to EUR 7.3 billion was recognized as cash in the first quarter of 2013, complementing the accelerated portfolio wind-up. FMS-WM monitors its financing needs and liquidity requirements by means of a liquidity management system similar to the ones used by financial institutions. FMS-WM seeks to ensure that it has sufficient liquidity to cover its three-month liquidity requirements under stress scenario assumptions at all times.

Treasury

Treasury’s core tasks are short-term liquidity management and the management of interest rate and foreign exchange risks. In addition, FMS-WM’s treasury group is responsible for improving FMS-WM’s funding structure on an ongoing basis with the aim of generating positive contributions to FMS-WM’s earnings.

As part of its short-term liquidity management, FMS-WM utilizes instruments with maturities of up to one year. In fiscal year 2013, FMS-WM’s issuing activity under its existing money market program, namely the European Commercial Paper (“ECP”) / Certificates of Deposit (“CD”) program and the U.S. Asset-Backed Commercial Paper (“US ABCP”) program further contributed to a stable and sustainable funding structure for FMS-WM. As of December 31, 2013, the ECP/CD program had a volume of EUR 29.1 billion (December 31, 2012: EUR 30 billion), and the US ABCP program had a volume of EUR 15.3 billion (December 31, 2012: EUR 18.8 billion).

Interest rate and foreign exchange risks are managed in a centralized fashion on an income-oriented basis guided by a risk aversion policy within the limit system. The aim is to minimize the fluctuations in the fair value and profit / loss due to market risks. To this end, treasury enters into hedging transactions for individual exposures (micro hedges) or at the portfolio level (macro hedges).

Capital Markets Funding

Capital markets funding’s main task is to raise long-term funds in the international capital markets. Maturities generally range from one to ten years, with the majority of bonds having a tenor of three to five years. In fiscal year 2013, FMS-WM further optimized its funding base, as it successfully raised about EUR 11 billion via the capital markets. In this context, the share of funding with an initial maturity of more than one year was further increased as planned and, as of December 31, 2013, accounted for approximately 46% of the aggregate funding volume (December 31, 2012: 35%). As of December 31, 2013, FMS-WM reported a total outstanding capital market issues of approximately EUR 60 billion with an average remaining maturity of around 3.5 years.

FMS-WM’s bonds are being offered in a broad range of formats, including benchmark format, non-benchmark public format and private placements as well as different currencies, e.g. EUR, USD and GBP, in order to fund the wind-up portfolio at matching currencies. In fiscal year 2013, FMS-WM focused in particular on obtaining USD funding on the U.S. capital market through its issuance program in global format established in the United States, and it successfully raised a total of USD 5.5 billion through three USD benchmark issues with maturities of between three to five years.

-19-

Capitalization and Indebtedness

The following table sets forth FMS-WM’s actual capitalization and indebtedness as of December 31, 2013.

| | | | |

| | | As of

December 31, 2013 | |

| | | audited | |

| | | (in € millions) | |

Debt | | | | |

Short-term debt | | | 257 | |

Bonds and notes | | | 121,189 | |

Loans and advances to bank and loans and advances to customers (not payable on demand) | | | 47,947 | |

Other borrowings and other liabilities | | | 18,152 | |

Equity | | | | |

Total equity | | | 119 | |

| | | | |

Total capitalization | | | 187,664 | |

| | | | |

-20-

Economic Conditions and Market Developments

The following sections contain an overview of economic conditions and market developments, which affected the value of FMS-WM’s portfolio and its business in general in 2013.

Macroeconomic Developments

According to International Monetary Fund (“IMF”) estimates, the global economy grew at an average rate of 3.0% in 2013.

The euro area saw a 0.4% decline in economic output in 2013. However, the systemic risk of a wave of sovereign bankruptcies in the euro area and of a dissolution of the euro area has decreased considerably. This is attributable in particular to the ECB’s announcement in the summer of 2012 to launch a purchasing program for bonds issued by those Member States whose currency is the euro (“Euro Area Member States”) (so-called “outright monetary transactions”). The situation on the capital markets subsequently stabilized, a trend that continued throughout the remainder of 2013. The establishment of a banking union was further advanced and helped to mitigate systemic risks.

Due to declining inflation rates, the ECB sharply lowered the interest rate for securities and repo transactions to reach a new historical low of 0.25% during the course of 2013. In addition, it introduced forward guidance, reiterating its decision to keep key interest rates at or below current levels for an extended period of time. The secondary market spreads for government bonds issued by peripheral Euro Area Member States narrowed during the year, and yields on short term instruments hit new historical lows. The euro gained substantial ground against not only the Japanese yen, but also emerging market currencies.

Real Estate Markets

Developments in the real estate markets in which FMS-WM’s real estate collateral is located presented a varied picture in 2013. The same held true for investor interest in the acquisition of real estate and receivables in the relevant markets. In geographical terms, FMS-WM’s receivables portfolio focused on Germany, the United States and the United Kingdom.

In Germany, financing was focused on office, residential, commercial and retail properties. Vacancy rates were generally steady, while metropolitan areas generally saw more positive development than economically weaker regions. In the case of residential real estate, movement to cities continued and vacancy rates rose in rural regions.

The improved economic performance of the United Kingdom had positive effects on its real estate market in 2013. There were initial signs of the market overheating in London’s real estate sector, which led to a slight upturn even in some non-first rate locations. However, the real estate market remained stagnant outside of major urban areas.

In the United States, real estate market performance varied depending on the regional markets and segments in 2013. Due to improved purchasing power, the commercial and retail markets experienced a slight recovery, in particular in major metropolitan areas. A trend toward moving to larger urban centers was also evident in the United States, leading to imbalances in regional real estate markets. Major east and west coast cities benefited disproportionately from this development. These effects were particularly pronounced in the second half of 2013.

Infrastructure Markets

Led by the energy and infrastructure sectors, total worldwide project finance volume in 2013 marked a new all-time high with significant growth in the private finance initiative / public private partnership (“PFI/PPP”) segment, in particular. Infrastructure financing was the primary focus, accounting for nearly 80% of the total global project finance volume.

While banks remained reticent to provide financing in 2013, this was more than compensated for by financing through the capital markets. Driven by an improved outlook for returns and relatively low default rates, institutional investors such as insurance companies and pension funds increasingly sought project financing investments having good credit ratings as an alternative to conventional investments in government or corporate bonds.

-21-

For a large number of ongoing projects, however, the persistent financial and economic crisis, supplemented by weak macroeconomic data from many countries, continued to cause problems in achieving planned capacity utilization or meeting contractually agreed interest and principal payment deadlines.

Financial Institutions and Covered Bonds

In 2013, bonds issued by financial institutions benefited from the easing of the sovereign debt crisis. As a result of certain capitalization measures taken by some banks in peripheral Euro Area Member States, such as credit sales and capital increases, the ECB’s announcement to carry out stress tests for euro-area banks in 2014 did not have any adverse effects on the financial sector. Compared to 2012, the volatility of risk premiums was much lower in 2013.

Public Sector

At the end of 2013, the global economic environment was subdued, as a result of slowing growth rates in China and the currency crises in the emerging markets of India, Turkey, South Africa and Argentina.

Nevertheless, due to the continued relief experienced by the financial markets, resulting from the ECB’s introduction of outright monetary transactions and the implementation of various monetary policies, yields in the peripheral Euro Area Member States continued to decline steadily in 2013. Yields on ten-year German government bonds rose sharply from 1.3% at the start of 2013 to around 1.9% at the end of December 2013, whereas Spain’s ten-year bonds achieved a yield of 4% by the end of 2013 (start of 2013: 5%). Yields on Greek government bonds also declined during 2013, with the yield on ten-year bonds amounting to a little over 8% by the end of the year (end of 2012: 11%). In the case of the Italian ten-year government bonds, yields managed to settle at a lower level (below 4%) at the end of the year, after a difficult government formation process. Yields on ten-year UK government bonds rose sharply during the reporting period by 120 basis points to 3% against the backdrop of a strong upturn in UK growth.

On the income side, the financial situation of the public-sector in the United States tracked the performance of the U.S. economy as a whole. The increase in taxes collected by the states had dropped to a normal level by year-end after seeing rapid growth in previous quarters. The stabilizing real estate market and continued revival in United States’ economic growth resulted in a strong year-on-year upturn in yields of ten-year U.S. treasuries, rising 125 basis points to 3% at the end of 2013.

The situation on the U.S. municipal bond market was difficult in 2013, chiefly due to higher yield expectations, credit uncertainties and a significant outflow of funds.

ABS Markets

In 2013, ABS markets continued to recover worldwide. The performance of U.S. commercial mortgage-backed securities (CMBSs) paralleled the positive developments in the residential and commercial real estate markets. Accordingly, spreads tightened in the course of 2013 and the market for new issues in the United States also recovered. Securities backed by student loans delivered steady performance in 2013, although the high level of student debt remains a burdening factor.

-22-

Financial Report – Net Assets, Financial Position and Results of Operations

Net Assets

The asset transfer from the HRE Group as of October 1, 2010 continued to have a major impact on the net assets of FMS-WM as of December 31, 2012 and 2013. FMS-WM took over assets, liabilities, provisions, accrued and deferred items, derivative financial instruments as well as other executory contracts from the transferring legal entities for accounting purposes effective October 1, 2010.

In fiscal year 2013, asset swap packages with a nominal value of EUR 1.3 billion were transferred to FMS-WM, resulting in an asset upgrade. The risk positions underlying these asset swap packages had initially been transferred to FMS-WM by way of guarantee with effect from October 1, 2010. Consequently, the off-balance sheet items (contingent liabilities and other obligations) decreased by EUR 1.3 billion, and the balance sheet items affected by asset upgrades increased by the amount of the purchase price of the assets and related derivatives.

Taking contingent liabilities and other obligations into account, FMS-WM posted a transaction volume (total equity and liabilities plus contingent liabilities plus other obligations) of EUR 201,732 million as of December 31, 2013 compared to a transaction volume of EUR 262,479 million as of December 31, 2012. The table below provides an overview of the amount and composition of the transaction volume of FMS-WM as of December 31, 2012 and 2013 (numbers may not add up due to rounding differences):

| | | | | | | | |

| | | As of December 31, | |

| | | 2012 | | | 2013 | |

| | | (€ in millions) | |

Assets | | | | | | | | |

Cash reserve | | | — | | | | 383 | |

Loans and advances to banks | | | 39,667 | | | | 23,609 | |

Loans and advances to customers | | | 24,427 | | | | 28,359 | |

Debt instruments | | | 169,618 | | | | 130,918 | |

Other long-term equity investments | | | 7 | | | | 7 | |

Shares in affiliated companies | | | 381 | | | | 386 | |

Intangible and tangible fixed assets | | | 2 | | | | 11 | |

Other assets | | | 7,413 | | | | 51 | |

Prepaid expenses | | | 4,908 | | | | 3,940 | |

| | | | | | | | |

Total assets | | | 246,423 | | | | 187,664 | |

| | | | | | | | |

| |

| | | As of December 31, | |

| | | 2012 | | | 2013 | |

| | | (€ in millions) | |

Equity and liabilities | | | | | | | | |

Liabilities to banks | | | 42,109 | | | | 21,837 | |

Liabilities to customers | | | 37,427 | | | | 26,367 | |

Securitized liabilities | | | 147,234 | | | | 121,189 | |

Other liabilities | | | 751 | | | | 373 | |

Deferred income | | | 17,506 | | | | 16,559 | |

Provisions | | | 1,361 | | | | 1,220 | |

Equity | | | 35 | | | | 119 | |

| | | | | | | | |

Total equity and liabilities | | | 246,423 | | | | 187,664 | |

Contingent liabilities | | | 10,669 | | | | 8,115 | |

Other obligations | | | 5,387 | | | | 5,953 | |

| | | | | | | | |

Transaction volume | | | 262,479 | | | | 201,732 | |

| | | | | | | | |

-23-

Lending Business

The transferred risk positions that arise from the underlying lending business encompass receivables, disbursement obligations under irrevocable loan commitments and guarantees. Some of the contingent liabilities stem from guarantees granted by FMS-WM for certain assets that are being held by HRE Group companies and could not be transferred to FMS-WM.

The lending business had a volume of EUR 61,234 million as of December 31, 2013, compared to a volume of EUR 74,609 million as of December 31, 2012, and was broken down into the following balance sheet and below-the-line items:

| | | | | | | | |

| | | As of December 31, | |

| | | 2012 | | | 2013 | |

| | | (unaudited) | |

| | | (in € millions) | |

Loans and advances to banks | | | 39,667 | | | | 23,609 | |

Loans and advances to customers | | | 24,427 | | | | 28,359 | |

Contingent liabilities (excluding credit default swaps) | | | 5,128 | | | | 3,313 | |

Other obligations | | | 5,387 | | | | 5,953 | |

| | | | | | | | |

Lending business | | | 74,609 | | | | 61,234 | |

| | | | | | | | |

The decrease in loans and advances to banks is mainly attributable to an agreement reached with PBB in August 2013 on what is referred to as the “Ersatzdeckungslösung”, or the substitute cover solution. This concerns a portfolio of loans and advances that had been transferred to FMS-WM as of October 1, 2010 through limited cash subparticipations, as these items were still being used by the transferor at the transfer date in order to cover mortgage-backed Pfandbrief securities (covered bonds) the transferor had issued. On the basis of the agreement, this portfolio was removed from PBB’s mortgage cover register and, as with other subparticipations, passed into the beneficial ownership of FMS-WM. As of December 31, 2013, this portfolio of loans and advances is thus recognized under loans and advances to customers, whereas as of December 31, 2012 it was still recognized as a limited cash subparticipation under loans and advances to banks (to PBB) in the amount of EUR 6.9 billion. Accordingly, loans and advances to customers increased following the substitute cover solution.

In connection with the agreement on the substitute cover solution, FMS-WM has pledged to pay out up to EUR 2,994 million to PBB upon PBB’s request. Likewise, a disbursement would give rise to a claim of FMS-WM against PBB. In this respect, FMS-WM is exposed to a default risk vis-à-vis PBB, which is primarily offset by a reduction in irrevocable loan commitments to third parties of EUR 640 million, as well as the partial repayment of the liquidity facility with Depfa in the amount of EUR 1,628 million.

Securities Holdings

Holdings of securities in the amount of EUR 130,918 million were recognized as debt instruments as of December 31, 2013, compared to an amount of EUR 169,618 million as of December 31, 2012. As of December 31, 2013, the amount of securities holdings included debt instruments issued by FMS-WM of EUR 35,660 million that were repurchased, compared to EUR 65,250 million as of December 31, 2012. The repurchased debt instruments were allocated to the liquidity reserve and partly pledged as collateral. The holdings of debt instruments issued by FMS-WM solely concern marketable bonds and other fixed-income securities, which are classified as holdings of financial investments. The holdings of securities are hedged against interest rate and foreign exchange risks through the use of derivatives.

Shares in Affiliated Companies and Other Long-Term Equity Investments

As of December 31, 2013, a book value of EUR 393 million was recognized for shares in affiliated companies and other long-term equity investments (December 31, 2012: EUR 388 million). The changes in fiscal year 2013 resulted mainly from the additions with respect to the affiliated companies Awareness (EUR 18 million) and Airen (EUR 2 million), as well as from countervailing currency effects.

-24-

Liabilities

Issuing bonds and engaging in repos in accordance with FMS-WM’s funding strategy had a significant impact on the following balance sheet items: (i) liabilities to banks, (ii) liabilities to customers and (iii) securitized liabilities.

As of December 31, 2013, FMS-WM recognized liabilities to banks of EUR 21,837 million (December 31, 2012: EUR 42,109 million), which was primarily comprised of repo transactions in a nominal amount of EUR 16,764 million (December 31, 2012: EUR 35,479 million).

As of December 31, 2013, liabilities to customers amounted to EUR 26,367 million (December 31, 2012: EUR 37,427 million) and mainly included repo transactions in a nominal amount of EUR 21,747 million (December 31, 2012: EUR 33,205 million).

In addition, FMS-WM recognized securitized liabilities of EUR 121,189 million as of December 31, 2013 (December 31, 2012: EUR 147,234 million). In connection therewith, the holdings of FMS-WM’s own debt issues, including pro rata interest, as of December 31, 2013 were EUR 92,139 million (December 31, 2012: EUR 117,705 million). As of December 31, 2013, this item also included EUR 29,050 million in commercial paper from the ECP/CD Program launched in fiscal year 2011 (December 31, 2012: EUR 29,529 million). For further details, please see “Financial Position — Issuing Activity and Funding.”

Prepaid Expenses and Deferred Income