Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration Statement No. 333-215186

The information in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement does not constitute an offer to sell, and does not seek an offer to buy, those securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS SUPPLEMENT

(To prospectus dated January 13, 2017)

SUBJECT TO COMPLETION DATED JANUARY 23, 2019

FMS WERTMANAGEMENT

$

% Notes due

FMS Wertmanagement (“FMS-WM”), will pay interest on the % Notes due (the “Notes”) in two semi-annual installments on and of each year. Interest will accrue on the Notes from and including , and the first interest payment date will be . The Notes will mature on . The Notes will not be redeemable at any time prior to maturity. There is no sinking fund for the Notes.

FMS-WM has applied for the Notes to be admitted for listing and trading on the Euro MTF Market of the Luxembourg Stock Exchange.

Pursuant to the German Financial Market Stabilization Fund Act (Finanzmarktstabilisierungsfondsgesetz, “FMStFG”), the Notes issued by FMS-WM will benefit from a statutory guarantee by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds, “SoFFin”). The Federal Republic of Germany (the “Federal Republic”) is, in turn, directly liable for all of SoFFin’s obligations. See “Responsibility of the Federal Republic for FMS-WM” in the accompanying prospectus.

PRICE % AND ACCRUED INTEREST

| Price to Public(1) | Underwriting Discounts And Commissions(2) | Proceeds to FMS-WM(1)(3) | ||||||||||

Per Note | % | % | % | |||||||||

Total | $ | $ | $ | |||||||||

| (1) | Plus accrued interest, if any, from , if settlement occurs after that date. |

| (2) | FMS-WM has agreed to indemnify the Underwriters (as defined herein) against certain liabilities, including liabilities under the Securities Act of 1933, as amended. |

| (3) | Before deducting expenses related to the offering. |

Neither the Securities and Exchange Commission, any state securities commission, the Luxembourg Stock Exchange nor any foreign governmental agency has approved or disapproved of these securities or determined whether this prospectus supplement or the accompanying prospectus is accurate and complete. Any representation to the contrary is a criminal offense.

The Underwriters expect to deliver the Notes to purchasers in book-entry form only through The Depository Trust Company (“DTC”) and through the facilities of other clearing systems that participate in DTC, including Clearstream Banking, société anonyme, Luxembourg and Euroclear Bank SA/NV on .

This prospectus supplement may only be used for the purposes for which it has been published.

| BofA Merrill Lynch | Citigroup | Commerzbank | Crédit Agricole CIB | TD Securities | ||||

Prospectus Supplement dated .

Table of Contents

Prospectus Supplement | ||||

| S-4 | ||||

| S-5 | ||||

| S-9 | ||||

| S-11 | ||||

| S-12 | ||||

| S-16 | ||||

| S-17 | ||||

| S-18 | ||||

| S-22 | ||||

| S-23 | ||||

Prospectus | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 7 | ||||

| 8 | ||||

| 8 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 14 | ||||

| 16 | ||||

| 16 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 29 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

S-2

Table of Contents

This prospectus supplement should be read together with the accompanying prospectus dated January 13, 2017, and the documents incorporated herein by reference (see “Where You Can Find More Information” in this prospectus supplement). These documents taken together are herein referred to as the “disclosure document.” The documents incorporated herein by reference contain information regarding FMS-WM and other matters. Further information concerning FMS-WM and the Notes offered hereby may be found in the registration statement (Registration No. 333-215186) filed with the U.S. Securities and Exchange Commission under the Securities Act of 1933 relating to our debt securities described in the prospectus.

If the information in this prospectus supplement differs from the information contained in the accompanying prospectus, you should rely on the information in this prospectus supplement. If a capitalized term is used in this prospectus supplement and not defined, it is defined in the accompanying prospectus and has the same meaning herein.

You should rely only on the information provided in the disclosure document. We have not, and the Underwriters have not, authorized anyone else to provide you with different information. We are not, and the Underwriters are not, making an offer of these securities in any jurisdiction where the offer is not permitted.

The distribution of this disclosure document, and the offering of the Notes in certain jurisdictions may be restricted by law. Persons into whose possession this disclosure document comes should inform themselves about and observe any such restrictions. This disclosure document does not constitute, and may not be used in connection with, an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such offer or solicitation. See “Underwriting.”

FMS-WM accepts full responsibility for the accuracy of the information contained in the disclosure document and confirms, having made all reasonable inquiries, that to the best of its knowledge and belief there are no other facts the omission of which would make any statement herein misleading in any material respect. FMS-WM has not, and the Underwriters have not, authorized anyone to give you any other information, and FMS-WM takes, and the Underwriters take, no responsibility for any other information that others may give you. You should not assume that the information contained in this disclosure document is accurate as of any date other than the date on the front of each document forming part of the disclosure document, or, with respect to information incorporated by reference, as of the date of such information.

This disclosure document constitutes a single prospectus for purposes of Luxembourg law on prospectus securities dated July 10, 2005, as amended. Inquiries regarding our listing status on the Luxembourg Stock Exchange should be directed to our Luxembourg listing agent and Luxembourg local agent, The Bank of New York Mellon SA/NV, Luxembourg Branch, Vertigo Building – Polaris,2-4 rue Eugène Ruppert, L-2453 Luxembourg, Luxembourg.

This prospectus supplement and the accompanying prospectus will be published on the website of the Luxembourg Stock Exchange at http://www.bourse.lu.

References herein to “euro”, “EUR” or “€” are to the single European currency adopted by certain participating member countries of the European Union, as of January 1, 1999. References to “U.S. dollars,” “USD” or “$” are to United States dollars.

References herein to “we” or “us” or similar expressions are to FMS-WM.

S-3

Table of Contents

WHERE YOU CAN FIND MORE INFORMATION

The registration statement on Schedule B filed by FMS-WM (Registration No. 333-215186), including the attached exhibits and schedules, contains additional relevant information about the Notes. The rules and regulations of the Securities and Exchange Commission (the “SEC”) allow FMS-WM to omit certain information included in the registration statement from this prospectus supplement and the accompanying prospectus. The registration statement, including its various exhibits, is available to the public over the internet at the SEC’s website: http://www.sec.gov. You may also read and copy these documents at the SEC’s Conventional Reading Room, located at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SECat 1-800-SEC-0330 for further information on the Conventional Reading Room.

FMS-WM files annual reports and other information with the SEC, which are available to the public over the internet at http://www.sec.gov or may be read and copied at the SEC’s public reference room. The SEC allows FMS-WM to “incorporate by reference” the documents that FMS-WM files with the SEC, which means that FMS-WM can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be part of this prospectus supplement and the accompanying prospectus, and later information that FMS-WM files with the SEC will automatically update and supersede this information, as well as the information included in this prospectus supplement and the accompanying prospectus. We incorporate by reference the annual report on Form 18-K for FMS-WM for the fiscal year ended December 31, 2017, as filed with the SEC on August 24, 2018 (File No. 333-184318) (the “Annual Report”), as subsequently amended by Amendment No. 1 on Form 18-K/A filed with the SEC on September 28, 2018, and any future filings made with the SEC to the extent such filings indicate that they are intended to be incorporated by reference. FMS-WM’s Form 18-K and amendments on Form 18-K/A, if any, contain or will contain, among other information, its most recently published annual report and financial statements, from time to time.

You can obtain any of the documents incorporated by reference in this document through us, from the SEC as described above or, with respect to the Annual Report and so long as any of the Notes are listed on the Luxembourg Stock Exchange, on the website of the Luxembourg Stock Exchange at http://www.bourse.lu. Documents incorporated by reference are available from FMS-WM free of charge by requesting them in writing or by telephone from FMS-WM at the following address and telephone number:

FMS Wertmanagement

Prinzregentenstrasse 56

80538 Munich, Federal Republic of Germany

+49 89 9547627-0

S-4

Table of Contents

Federal Republic of Germany

Overview of Key Economic Figures

The following economic information regarding the Federal Republic is derived from the public official documents cited below. Certain of the information is preliminary.

Gross Domestic Product (GDP)

GROSS DOMESTIC PRODUCT

(adjusted for price, seasonal and calendar effects)(1)

Reference period | Percentage change on previous quarter | Percentage change on the same quarter in previous year | ||||||

3rd quarter 2017 | 0.6 | 2.6 | ||||||

4th quarter 2017 | 0.5 | 2.8 | ||||||

1st quarter 2018 | 0.4 | 2.1 | ||||||

2nd quarter 2018 | 0.5 | 2.0 | ||||||

3rd quarter 2018 | -0.2 | 1.1 | ||||||

| (1) | Adjustment for seasonal and calendar effects according to the CensusX-12-ARIMA method. |

In the third quarter of 2018, Germany’s gross domestic product (“GDP”) decreased by 0.2% after price, seasonal and calendar adjustments compared to the second quarter of 2018. The slightquarter-on-quarter decrease in GDP was mainly due to the development of foreign trade in the third quarter of 2018 compared to the second quarter of 2018. According to provisional calculations, exports of goods and services decreased by 0.9% in the third quarter of 2018 compared to the second quarter of 2018, while imports increased by 1.3% in the third quarter of 2018 compared to the second quarter of 2018.

With respect to domestic demand, household final consumption expenditure decreased by 0.3%, while government final consumption expenditure slightly increased by 0.2% in the third quarter of 2018, in each case compared to the second quarter of 2018. Gross fixed capital formation in machinery and equipment increased by 0.8% and gross fixed capital formation in construction by 0.9% in the third quarter of 2018, in each case compared to the second quarter of 2018.

In ayear-on-year comparison, in price and calendar-adjusted terms, the German economy decelerated and grew by 1.1% in the third quarter of 2018, following increases by 2.0% in the second quarter of 2018 and 2.1% in the first quarter of 2018, in each case compared to the corresponding periods in 2017.

Source: Statistisches Bundesamt, Detailed gross domestic product results for the 3rd quarter of 2018, press release of November 23, 2018 (https://www.destatis.de/EN/PressServices/Press/pr/2018/11/PE18_454_811.html).

In 2018 as a whole, the economic situation in Germany was characterized by economic growth, although growth has lost momentum. According to preliminary calculations of the Federal Statistical Office, the price-adjusted GDP was 1.5% higher in 2018 than in 2017. The German economy thus has grown for the ninth consecutive year. Compared to 2017 and 2016, however, the growth rate decreased as German GDP increased by 2.2% each year. From a longer term perspective, German economic growth in 2018 exceeded the average growth rate of the last ten years (+1.2%).

Positive contributions to growth in 2018 came primarily from domestic demand. Household final consumption expenditure increased by a price-adjusted 1.0% compared to 2017, while government final consumption expenditure increased by 1.1%. Price-adjusted gross fixed capital formation increased by 4.8% in

S-5

Table of Contents

2018 compared to 2017, reflecting increases in gross fixed capital formation in construction (+3.0%) and other fixed assets (including expenditure on research and development) (+0.4%) in 2018 compared to 2017.

German exports continued to increase in 2018 on an annual average, though at a lower pace than in previous years. Price-adjusted exports of goods and services increased by 2.4% in 2018 compared to 2017. The increase in imports was larger (+3.4%) in 2018 compared to 2017. Arithmetically, the resulting balance of exports and imports had a slight downward effect of 0.2 percentage points on GDP growth in 2018.

Source: Statistisches Bundesamt, German economy grew 1.5% in 2018, press release of January 15, 2019 (https://www.destatis.de/EN/PressServices/Press/pr/2019/01/PE19_018_811.html).

Inflation Rate

INFLATION RATE

(based on overall consumer price index)

Reference period | Percentage change on previous month | Percentage change on the same month in previous year | ||||||

December 2017 | 0.6 | 1.7 | ||||||

January 2018 | -0.7 | 1.6 | ||||||

February 2018 | 0.5 | 1.4 | ||||||

March 2018 | 0.4 | 1.6 | ||||||

April 2018 | 0.0 | 1.6 | ||||||

May 2018 | 0.5 | 2.2 | ||||||

June 2018 | 0.1 | 2.1 | ||||||

July 2018 | 0.3 | 2.0 | ||||||

August 2018 | 0.1 | 2.0 | ||||||

September 2018 | 0.4 | 2.3 | ||||||

October 2018 | 0.2 | 2.5 | ||||||

November 2018 | 0.1 | 2.3 | ||||||

December 2018 | 0.1 | 1.7 | ||||||

In December 2018, consumer prices in Germany increased by 1.7% compared to December 2017. The inflation rate thus decreased markedly at the end of the year (November 2018: +2.3%). As in the preceding months, the increase of energy product prices had a considerable effect on the inflation rate in December 2018. Energy prices increased by 4.8% in December 2018 compared to December 2017. The price increase slowed markedly on the previous month especially for heating oil (+16.1%) and motor fuels (+8.6%). Excluding energy prices, the inflation rate would have been 1.4% in December 2018.

Compared to December 2017, food prices rose by 1.0% in December 2018. While a substantialyear-on-year price increase was recorded for vegetables (+8.1%), fruit prices decreased markedly in the same period(-5.1%). The prices of goods overall increased by 2.0% in December 2018 compared to December 2017, the main reason being the increase in energy prices. Significantyear-on-year price increases were also recorded for other goods such as newspapers and periodicals (+4.3%) and beer (+3.1%). Theyear-on-year increase in prices of services overall (+1.5%) was smaller in December 2018 than the increase in prices of goods.

Compared to November 2018, the consumer price index increased by 0.1% in December 2018. The prices of services overall increased by 1.3% in December 2018 compared to November 2018. Among other things, rail fares increased towards the end of 2018 as a result of the annual adjustments of railway fares (+1.4%). The main

S-6

Table of Contents

reason for the decrease of prices in goods(-1.1%) was the development of energy prices(-4.2%). Furthermore, a favorable development for consumers was price reductions for clothing and footwear(-2.0%) at the end of the year.

Source: Statistisches Bundesamt, Consumer prices in 2018: +1.9% on the previous year, press release of January 16, 2019 (https://www.destatis.de/EN/PressServices/Press/pr/2019/01/PE19_019_611.html).

Unemployment Rate

UNEMPLOYMENT RATE

(percent of unemployed persons in the total labor force according to the

International Labour Organization (ILO) definition)(1)

Reference period | Original percentages | Adjusted percentages(2) | ||||||

November 2017 | 3.4 | 3.6 | ||||||

December 2017 | 3.5 | 3.6 | ||||||

January 2018 | 3.6 | 3.5 | ||||||

February 2018 | 3.8 | 3.5 | ||||||

March 2018 | 3.5 | 3.5 | ||||||

April 2018 | 3.5 | 3.5 | ||||||

May 2018 | 3.4 | 3.4 | ||||||

June 2018 | 3.5 | 3.4 | ||||||

July 2018 | 3.3 | 3.4 | ||||||

August 2018 | 3.4 | 3.4 | ||||||

September 2018 | 3.3 | 3.4 | ||||||

October 2018 | 3.2 | 3.3 | ||||||

November 2018 | 3.2 | 3.3 | ||||||

| (1) | The time series on unemployment are based on the German Labour Force Survey. |

| (2) | Adjusted for seasonal and irregular effects (trend cycle component) using theX-12-ARIMA method. |

Compared to November 2017, the number of employed persons increased by approximately 485,000 persons, or 1.1%, in November 2018. Compared to October 2018, the number of employed persons in November 2018 increased by approximately 34,000, or 0.1%, after adjustment for seasonal fluctuations.

In November 2018, the number of unemployed persons decreased by approximately 45,000, or 3.4%, compared to November 2017. Adjusted for seasonal and irregular effects (trend cycle component), the number of unemployed persons in November 2018 stood at 1.44 million, which was a decrease of roughly 9,200 compared to October 2018.

Source: Statistisches Bundesamt, 45.1 million persons in employment in November 2018, press release of January 4, 2019 (https://www.destatis.de/EN/PressServices/Press/pr/2019/01/PE19_003_132.html); Statistisches Bundesamt, Genesis-Online Datenbank, Result 13231-0001, Unemployed persons, persons in employment, economically active population, unemployment rate: Germany, months, original and adjusted data(https://www-genesis.destatis.de/genesis/online/logon?sequenz=tabelleErgebnis&selectionname=13231-0001&zeitscheiben=2&leerzeilen=false).

S-7

Table of Contents

Current Account and Foreign Trade

CURRENT ACCOUNTAND FOREIGN TRADE

| (balance in EUR billion)(1) | ||||||||

Item | January to November 2018 | January to November 2017 | ||||||

Trade in goods, including supplementary trade items | 230.4 | 250.1 | ||||||

Services | -19.4 | -23.9 | ||||||

Primary income | 58.9 | 55.7 | ||||||

Secondary income | -41.9 | -49.1 | ||||||

|

|

|

| |||||

Current account | 228.0 | 232.8 | ||||||

|

|

|

| |||||

| (1) | Figures may not add up due to rounding. |

Source: Statistisches Bundesamt, German exports in November 2018 at the same level as in November 2017, press release of January 9, 2019 (https://www.destatis.de/EN/PressServices/Press/pr/2019/01/PE19_008_51.html).

Germany’s General Government Deficit/Surplus and General Government Gross Debt

The Federal Government has forecast that the German general government surplus for the full year 2018 will be 1.6% of GDP compared to a surplus of 1.0% of GDP for the full year 2017. The general government gross debt ratio is forecast to be 60.6% in 2018 compared to a gross debt ratio of 63.9% in 2017.

Source: Eurostat, EDP Notification Tables, October 2018, Germany (https://ec.europa.eu/eurostat/documents/1015035/9306962/DE-2018-10.pdf/ff631c93-81e8-4713-b029-7c11b20ead4d).

Other Recent Developments

British Parliament Rejects Prime Minister May’s Brexit Deal

On January 15, 2019, the British Parliament rejected Prime Minister May’s Brexit deal. A total of 432 Members of Parliament (MPs) voted against, 202 voted for the deal. On January 21, 2019, Prime Minister May returned to the British Parliament with an alternative plan. In her statement, the Prime Minister stated that she would not support a second referendum and that she remained committed to delivering a deal in advance of Article 50’s expiration on March 29, 2019.

Sources: The Federal Government, Following vote in British Parliament – Finding a way to secure an orderly Brexit, dated January 16, 2019(https://www.bundesregierung.de/breg-en/news/finding-a-way-to-secure-an-orderly-brexit-1569342); Statement of Prime Minister Theresa May, “We can make Progress,” Prime Minister sets out Brexit next steps, dated January 21, 2019(https://www.parliament.uk/business/news/2019/parliamentary-news-2019/prime-minister-announces-next-steps-for-eu-withdrawal/).

S-8

Table of Contents

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus supplement and the accompanying prospectus.

Issuer | FMS Wertmanagement |

Securities Offered | $ principal amount of % Notes due . |

Issue Date | . |

Maturity Date | . |

Interest Payment Dates | and of each year, commencing . |

Interest Rate | % per annum, from . Interest will be calculated on the basis of a 360-day year consisting of twelve 30-day months unadjusted. |

Redemption | The Notes are not subject to redemption prior to maturity. |

The Federal Republic of Germany | The Notes will benefit from a statutory guarantee by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds, “SoFFin”). The Federal Republic is, in turn, directly liable for all of SoFFin’s obligations. See “Responsibility of the Federal Republic for FMS-WM” in the accompanying prospectus. |

Settlement Cycle | T+ |

Listing and Admission to Trading | FMS-WM has applied for the Notes to be admitted for listing and trading on the Euro MTF Market of the Luxembourg Stock Exchange. |

Form, Registration and Settlement | The Notes will be represented by one or more Global Notes registered in the name of Cede & Co. as nominee for DTC. The Global Notes will be deposited with a custodian for DTC. Except as described in the accompanying prospectus, beneficial interests in the Global Notes will be represented through accounts of financial institutions acting on behalf of the beneficial owners as direct and indirect participants in DTC. Investors may elect to hold interests in the Global Notes through DTC, if they are participants in DTC, or indirectly through organizations that are participants in DTC. Owners of beneficial interests in the Global Notes will not be entitled to have Notes registered in their names and will not receive or be entitled to receive physical delivery of definitive Notes. Initial settlement for the Notes will be made in immediately available funds in dollars. See “Clearing and Settlement” in the accompanying prospectus. |

No Additional Amounts | FMS-WM will have no obligation to pay holders any additional amounts in respect of the Notes as a result of possible withholding or deduction for taxes pursuant to any fiscal or other laws and regulations applicable to the Notes. |

S-9

Table of Contents

Collective Action Clause | The Notes will contain a collective action clause. The holders of the Notes may agree with FMS-WM to amend the terms or conditions contained in the Notes or the Fiscal Agency Agreement with the affirmative vote by holders of Notes representing not less than 50% of the principal amount of the Notes then outstanding. Certain material amendments of the terms and conditions of the Notes or the Fiscal Agency Agreement, including changes in the due date for the payment of interest or principal or the reduction or elimination of the interest rate on the Notes, reduction of the principal amount on the Notes and changes in the currency of the Notes will require the affirmative vote by holders of not less than 75% of the principal amount of the Notes then outstanding. |

Fiscal Agent | The Bank of New York Mellon will be acting in its capacity as Fiscal Agent through its corporate trust office located at 101 Barclay Street, New York, NY 10286. |

Securities Codes | CUSIP: |

ISIN:

Common Code:

S-10

Table of Contents

We estimate that the net proceeds from the sale of the Notes will be approximately $ (after deducting underwriting commissions). The net proceeds from the sale of the Notes will be primarily used to refinance existing liabilities in order to replace maturing, short-term money market instruments with long-term funding. Any remaining proceeds will be used for general corporate purposes.

S-11

Table of Contents

The following is a brief description of the terms and conditions of the Notes offered by FMS-WM and the fiscal agency agreement with respect thereto. The description does not purport to be complete and is qualified in their entirety by reference to the fiscal agency agreement and to the form of global note filed by FMS-WM with the SEC as exhibits to the registration statement of which this prospectus supplement and the accompanying prospectus are a part. For a complete description of the Notes, you should also read the fiscal agency agreement and the form of global note, a copy of which has been filed as an exhibit to FMS-WM’s registration statement and will be available for inspection as described below under “General Information.”

General

The % Notes due offered hereby will be issued under a fiscal agency agreement as amended (the “Fiscal Agency Agreement”), between FMS-WM and The Bank of New York Mellon, as fiscal agent, principal paying agent, transfer agent and registrar (collectively, the “Fiscal Agent”). The Notes constitute direct and unsecured obligations of FMS-WM.

Interest

Interest will be paid on the Notes at the rate set forth on the cover page of this prospectus supplement and will be payable on and of each year (each, an “Interest Payment Date”), subject to the Business Day Convention as defined below. The Notes will bear interest from and the initial interest payment will be made on . Interest will be calculated on the basis of a 360-day year consisting of twelve 30-day months unadjusted. The Notes will mature on (the “Maturity Date”). The Notes are not subject to any sinking fund.

If an Interest Payment Date or the Maturity Date is a day on which banking institutions are authorized or obligated by law to close in New York or in a place of payment, then payment of principal or interest need not be made on such Interest Payment Date or Maturity Date, as applicable. FMS-WM may make the required payment on the next succeeding day that is not a day on which banking institutions are authorized or obligated by law to close in New York or in the place of payment. The payment will be made with the same force and effect as if made on the Interest Payment Date or Maturity Date and no additional interest shall accrue for the period from the Interest Payment Date or Maturity Date to the date of actual payment. Such adjustments of the Interest Payment Date or Maturity Date are referred to as the “Business Day Convention.”

Fiscal Agent

The duties of the Fiscal Agent will be governed by the Fiscal Agency Agreement. FMS-WM may replace the Fiscal Agent. FMS-WM may maintain deposit accounts and conduct other banking transactions in the ordinary course of business with the Fiscal Agent. The Fiscal Agent is an agent of FMS-WM, is not a trustee for the holders of the Notes and does not have the same responsibilities or duties to act for such holders as would a trustee.

The Fiscal Agent will be responsible for:

| • | maintaining a record of the aggregate holdings of Notes; |

| • | ensuring that payments of principal and interest in respect of the notes received by the Fiscal Agent from FMS-WM are duly credited to the holders of the Notes; and |

| • | transmitting to FMS-WM any notices from the holders of the Notes, or, as described below under “—Notices,” transmitting notices from FMS-WM to holders of the Notes. |

The Bank of New York Mellon will be acting in its capacity as Fiscal Agent through its corporate trust office located at 101 Barclay Street, New York, New York 10286.

S-12

Table of Contents

Payment of Principal and Interest

Interest will be payable to the persons in whose names the Notes are registered at the close of business on the date that is 15 calendar days prior to each Interest Payment Date (the “Record Date”). The Record Date may be changed by agreement among FMS-WM, the Fiscal Agent and all applicable securities clearing systems. The principal of and interest on the Notes will be paid in such coin or currency of the United States as of the time of payment is legal tender for the payment of public and private debts. FMS-WM may change or terminate the designation of paying agents from time to time. Payments of principal and interest at such agencies will be subject to applicable laws and regulations, including any withholding or other taxes, and will be effected by wire transfer to the person entitled to such payment at the person’s address appearing on the register of Notes maintained by the security registrar.

FMS-WM will redeem the Notes on the Maturity Date at 100% of the principal amount plus accrued but unpaid interest to date.

The Notes will be sold in denominations of $200,000 and integral multiples of $1,000 in excess thereof.

Any monies paid by FMS-WM to the Fiscal Agent or any paying agent for the payment of the principal of (or premium, if any, on) or interest, respectively, on any Notes that remain unclaimed at the end of ten years or five years, respectively, after such principal (or premium, if any) or interest shall have become due and payable (whether at maturity or otherwise) shall then be repaid to FMS-WM upon its written request. Upon such repayment all liability of the Fiscal Agent and any paying agent with respect to such monies shall cease. Any obligation FMS-WM may have to pay the principal of (or premium, if any, on) the Notes shall terminate at the end of ten years after such principal or premium shall have become due and payable. Any obligation FMS-WM may have to pay any interest on the Notes shall terminate at the end of five years after such interest shall have become due and payable.

Redemption

The Notes shall not be redeemed prior to maturity.

No Payment of Additional Amounts

All payments of principal and interest on the Notes will be subject to any fiscal or other laws and regulations applicable thereto. FMS-WM has no obligation to pay you any additional amounts in respect of the Notes as a result of possible withholding or deduction for taxes pursuant to any such law and/or regulations. Accordingly, the holder will, in the event of any such withholding or deduction, receive less than he or she would have received without such withholding or deduction.

Ranking

The obligations under the Notes constitute unsecured and unsubordinated obligations of FMS-WM rankingpari passu among themselves andpari passu with all other unsecured and unsubordinated obligations ofFMS-WM, unless such obligations are given priority under mandatory provisions of statutory law.

Negative Pledge

The Notes will not contain a negative pledge provision.

Termination for Default

Each holder will be entitled to declare its securities due and demand immediate redemption of the principal amount of its securities together with accrued but unpaid interest (if any) to the date of repayment, in the event that FMS-WM fails to pay principal or interest within 30 days from the relevant due date. The right to declare securities due shall terminate if the situation giving rise to it has been cured before the right is exercised.

S-13

Table of Contents

Notice

Any notice, including any notice declaring Notes due, in connection with events of default shall be made by means of a written declaration in the German or English language delivered to the specified office of the Fiscal Agent together with proof that such holder at the time of such notice is a holder of the relevant Notes.

Amendments (Collective Action Clause)

The holders of the Notes may agree with FMS-WM to amend the terms or conditions contained in the Notes or the Fiscal Agency Agreement with the affirmative vote by the holders of the Notes representing not less than 50% of the principal amount of the Notes then outstanding. However, amendments of the terms and conditions of the Notes or the Fiscal Agency Agreement which relate to the following matters require the affirmative vote by the holders of not less than 75% of the principal amount of the Notes then outstanding:

| (1) | changes in the due date for the payment of interest or the reduction or elimination of the interest rate on the Notes; |

| (2) | changes in the due date for the payment of the principal on the Notes; |

| (3) | reduction of the principal amount on the Notes; |

| (4) | subordination of outstanding amounts payable under the Notes in insolvency proceedings ofFMS-WM; |

| (5) | conversion or exchange of the Notes into equity securities or other types of securities of FMS-WM; |

| (6) | exchange and release of collateral on the Notes, if any; |

| (7) | change in the currency of the Notes; |

| (8) | waiver of or limitations on termination rights of the holders of Notes; and |

| (9) | substitution of FMS-WM as payment obligor on the Notes. |

Such resolutions voted by the applicable majority of the holders of notes of a series shall be binding on all holders of Notes. Amendments made to the terms or conditions contained in the notes or the Fiscal Agency Agreement which do not provide for identical conditions for all holders of Notes shall be void, unless the disadvantaged holders of Notes have given an express consent to such unequal conditions.

FMS-WM may, in agreement with the Fiscal Agent but without the vote or consent of the holders of the Notes, modify any of the terms and conditions of the Fiscal Agency Agreement and the Notes for the purpose of:

| (1) | adding to FMS-WM’s covenants for the benefit of the holders of the Notes; |

| (2) | surrendering any right or power conferred on FMS-WM; |

| (3) | securing the Notes; |

| (4) | curing any ambiguity or correcting or supplementing any defective provision of the Fiscal Agency Agreement or the Notes; or |

| (5) | amending the Fiscal Agency Agreement or the Notes for any purpose that FMS-WM may consider necessary or desirable that does not adversely affect the interests of the holders of the Notes in any material respect. |

Jurisdiction

FMS-WM will accept the jurisdiction of any state or federal court in the City of New York, in respect of any action arising out of or based on the Notes that may be maintained by any holder of those Notes. FMS-WM will appoint Corporation Service Company, 1180 Avenue of the Americas, Suite 210, New York, NY 10036 as its

S-14

Table of Contents

authorized agent upon which process in any such action may be served. FMS-WM will irrevocably waive any immunity to which it might otherwise be entitled in any action arising out of or based upon the Notes brought in any state or federal court in the City of New York.

FMS-WM is also subject to suit in competent courts in the Federal Republic to the extent permitted by German Law.

Governing Law

The Fiscal Agency Agreement and the Notes will be governed by, and interpreted in accordance with, the internal laws of the State of New York, except that all matters governing FMS-WM’s authorization of issuance of any notes shall be governed by the laws of the Federal Republic.

Further Issues

FMS-WM may from time to time, without notice to or the consent of the holders of the Notes, create and issue further notes having the same terms and conditions as the Notes in all respects (or in all respects except for the issue date, issue price and, if applicable, the first interest payment thereon) and such further notes shall be consolidated and form a single series with the Notes outstanding.

Repurchase

FMS-WM may repurchase Notes at any time and price in the open market or otherwise. Notes repurchased by FMS-WM may, at FMS-WM’s discretion, be held, resold (subject to compliance with applicable securities and tax laws) or surrendered to the Fiscal Agent for cancellation.

Notices

All notices will be published in a daily English language newspaper of general circulation in London (expected to be theFinancial Times) and in New York (expected to beThe Wall Street Journal), provided that for so long as any Notes are represented by global notes, notices may be given by delivery of the relevant notice to DTC by FMS-WM or the Fiscal Agent for communication by DTC to its participants in substitution for publication in any such newspaper. If at any time publication in any such newspaper is not practicable, notices will be valid if published in an English language newspaper selected by FMS-WM with general circulation in the relevant market regions. In addition, so long as any of the Notes are listed on the Luxembourg Stock Exchange and the rules of that exchange so require, such notices will be published on the website of the Luxembourg Stock Exchange at http://www.bourse.lu. Any such notice shall be deemed to have been given on the date of such publication or, if published more than once on different dates, on the first date on which publication is made.

S-15

Table of Contents

ADDITIONAL INFORMATION ON UNITED STATES TAXATION

The following supplements the discussion under the “United States Taxation” section of the accompanying prospectus regarding the United States federal income tax consequences of owning the Notes, and is subject to the limitations and exceptions set forth therein.

The Notes may be issued with a de minimis amount of original issue discount (“OID”). While a United States holder is generally not required to include de minimis OID in income prior to the sale or maturity of the Notes, United States holders that maintain certain types of financial statements and that are subject to the accrual method of tax accounting may be required to include de minimis OID on the Notes in income no later than the time upon which they include such amounts in income on their financial statements. United States holders that maintain financial statements should consult their tax advisors regarding the tax consequences to them of this requirement.

The second paragraph of “—Payments of Interest” under the “United States Taxation” section of the prospectus should be updated to read as follows: “Interest paid byFMS-WM on the debt securities and original issue discount, if any, accrued with respect to the debt securities (as described below under “Original Issue Discount”) is income from sources outside the United States and will generally be “passive” income for purposes of the rules regarding the foreign tax credit allowable to a United States holder.”

S-16

Table of Contents

CAPITALIZATION AND INDEBTEDNESS

The following table sets forth FMS-WM’s actual capitalization and indebtedness as of December 31, 2017, and its capitalization and indebtedness as of December 31, 2017 as adjusted for the receipt of the net proceeds of the offering. It does not otherwise give effect to any transaction since that date.

Since December 31, 2017, there has been no material change in the capitalization ofFMS-WM, except for (1) the issuance in benchmark format of USD 1.5 billion (approximately EUR 1.220 billion) 2.75% Notes due 2023 underFMS-WM’s SEC registration statement under Schedule B, the issuance in benchmark format of GBP 450 million (approximately EUR 512 million) 0.875% Notes due 2021, GBP 500 million (approximately EUR 553 million) 1.125% Notes due 2021, GBP 500 million (approximately EUR 557 million) SONIA+28 bps Notes 2021, GBP 325 million (approximately EUR 371 million) 0.875% Notes due 2022, GBP 1.250 billion (approximately EUR 1.414 billion) 1.000% Notes due 2022, GBP 900 million (approximately EUR 1.016 billion) 1.125% Notes due 2023, GBP 250 million (approximately EUR 276 million) 1.375% Notes due 2025 each underFMS-WM’s Debt Issuance Programme as well as (2) issuances in other public and private placement format in different currencies of approximately EUR 1.923 billion underFMS-WM’s Debt Issuance Programme as well as standalone documentation. EUR equivalent amounts have been determined on the basis of the exchange rates as of the relevant trade date.

| As of December 31, 2017 | As adjusted for the offering | |||||||

(unaudited) (in € millions) | ||||||||

Debt | ||||||||

Short-term debt | 5,632 | 5,632 | ||||||

Bonds and notes | 107,719 | (1) | ||||||

Loans and advances to bank and loans and advances to customers (not payable on demand) | 23,282 | 23,282 | ||||||

Other borrowings and other liabilities | 19,255 | 19,255 | ||||||

Equity | ||||||||

Total equity | 1,400 | 1,400 | ||||||

|

|

|

| |||||

Total Capitalization | 157,288 | |||||||

|

|

|

| |||||

| (1) | The adjustment of EUR million reflects the euro equivalent of the $ million principal amount of the Notes based on a EUR/U.S. dollar exchange rate of €1.00 = $ on . This value may differ from the liability that will be recorded on FMS-WM’s balance sheet under German GAAP. |

S-17

Table of Contents

FMS-WM intends to offer the Notes through Citigroup Global Markets Limited, Commerzbank Aktiengesellschaft, Crédit Agricole Corporate and Investment Bank, Merrill Lynch International and The Toronto-Dominion Bank (the “Underwriters”). Subject to the terms and conditions of the underwriting agreement with FMS-WM, dated , the Underwriters have agreed to purchase, and FMS-WM has agreed to sell to the Underwriters, $ in principal amount of Notes, as indicated in the table below:

Underwriter | Principal Amount of the Notes | |||

Citigroup Global Markets Limited | $ | |||

Commerzbank Aktiengesellschaft | $ | |||

Crédit Agricole Corporate and Investment Bank | $ | |||

Merrill Lynch International | $ | |||

The Toronto-Dominion Bank | $ | |||

|

| |||

Total | $ | |||

The underwriting agreement provides that the Underwriters are obligated to purchase all of the Notes if any are purchased.

The Underwriters propose to offer the Notes initially at the price to public on the cover page of this prospectus supplement.

The Underwriters may offer such Notes to certain dealers at the price to public minus a selling concession of up to % of the principal amount of the Notes. After the initial offering, the Underwriters may change the price to public and other selling terms.

FMS-WM has agreed to indemnify the Underwriters against certain liabilities, including liabilities under the Securities Act of 1933, as amended, or to contribute to payments the Underwriters may be required to make in respect of those liabilities.

The total expenses of the offering, excluding underwriting discounts and commissions, are estimated to amount to approximately $ .

The Notes are a new issue of securities with no established trading market. FMS-WM has been advised by the Underwriters that they presently intend to make a market in the Notes after completion of the offering. However, they are under no obligation to do so and may discontinue any market-making activities at any time without any notice. No assurance can be given with respect to the liquidity of the trading market for the Notes or that an active public market for the Notes will develop. If an active public trading market for the Notes does not develop, the market price and liquidity of the Notes may be adversely affected.

In connection with this offering, the Underwriters may, subject to applicable laws and regulations, purchase and sell the Notes in the open market. These transactions may include short sales, stabilizing transactions and purchases to cover positions created by short sales. Short sales involve the sale by the Underwriters of a greater number of Notes than they are required to purchase in this offering. Stabilizing transactions consist of certain bids or purchases made for the purpose of preventing or retarding a decline in the market price of the Notes while the offering is in progress.

These activities by the Underwriters may stabilize, maintain or otherwise affect the market price of the Notes. As a result, the price of the Notes may be higher than the price that otherwise might exist in the open market. If these activities are commenced, they may be discontinued by the Underwriters at any time.

Certain offers and sales in the United States are expected to be made through affiliates of the Underwriters that are registered as broker-dealers, acting as U.S. selling agents.

S-18

Table of Contents

Settlement

FMS-WM expects that delivery of the Notes will be made to purchasers of the Notes on or about , , which will be the business day following the date of pricing of the Notes (such settlement being referred to as “T+ ”). Under Rule 15c6-1 under the U.S. Securities Exchange Act of 1934, as amended, trades in the secondary market are required to settle in two business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes prior to the delivery of the Notes hereunder may be required, by virtue of the fact that the Notes will initially settle in T+ , to specify an alternate settlement arrangement at the time of any such trade to prevent a failed settlement. Purchasers of the Notes who wish to trade the Notes prior to their date of delivery hereunder should consult their advisors.

Other relationships

The Underwriters and their affiliates from time to time may have provided certain investment banking, commercial banking and financial advisory services to FMS-WM, for which they have received customary fees, commissions and other payments, and they may provide such services to us in the future, for which they would receive customary fees, commissions and other payments.

In addition, in the ordinary course of their business activities, the Underwriters and their affiliates may make or hold a broad array of investments and actively trade debt and equity securities (or related derivative securities) and financial instruments (including bank loans) for their own account and for the accounts of their customers. Such investments and securities activities may involve securities and/or instruments of ours or our affiliates. Certain of the Underwriters or their affiliates that have a lending relationship with us routinely hedge their credit exposure to us consistent with their customary risk management policies. Typically, such Underwriters and their affiliates would hedge such exposure by entering into transactions which consist of either the purchase of credit default swaps or the creation of short positions in our securities, including potentially the Notes offered hereby. Any such short positions could adversely affect future trading prices of the Notes offered hereby. The Underwriters and their affiliates may also make investment recommendations and/or publish or express independent research views in respect of such securities or financial instruments and may hold, or recommend to clients that they acquire, long and/or short positions in such securities and instruments.

Selling Restrictions

General

Each Underwriter has represented and agreed that it will comply to the best of its knowledge and belief, with all applicable laws and regulations in force in any jurisdiction in which it purchases, offers, sells or delivers Notes or possesses or distributes the prospectus supplement and/or the prospectus and will obtain any consent, approval or permission required by it for the purchase, offer, sale or delivery by it of the Notes under the laws and regulations in force in any jurisdiction to which it is subject or in which it makes such purchases, offers, sales or deliveries and that neither FMS-WM nor any other Underwriter shall have any responsibility therefor.

Each Underwriter has represented and agreed that it will offer, sell and deliver or otherwise convey the Notes only to the ECB, any other central bank or to institutional investors such as banks, insurers or other entities or persons which are regularly engaged in or established for the purposes of making, purchasing or investing in loans, securities or other financial assets, and not to non-institutional investors.

United Kingdom of Great Britain and Northern Ireland (“United Kingdom”)

Each Underwriter has represented and agreed that:

| (i) | in relation to Notes which have a maturity of less than one year, (a) it is a person whose ordinary activities involve it in acquiring, holding, managing or disposing of investments (as principal or agent) for the purposes of its business and (b) it has not offered or sold and will not offer or sell any such |

S-19

Table of Contents

| Notes other than to persons whose ordinary activities involve them in acquiring, holding, managing or disposing of investments (as principal or agent) for the purposes of their businesses or who it is reasonable to expect will acquire, hold, manage or dispose of investments (as principal or agent) for the purposes of their businesses where the issue of the Notes would otherwise constitute a contravention of Section 19 of the Financial Services and Markets Act 2000 (the “FSMA”) by FMS-WM; |

| (ii) | it has only communicated or caused to be communicated and will only communicate or cause to be communicated any invitation or inducement to engage in investment activity (within the meaning of Section 21 of the FSMA) received by it in connection with the issue or sale of any Notes in circumstances in which Section 21(1) of the FSMA does not apply to FMS-WM; and |

| (iii) | it has complied and will comply with all applicable provisions of the FSMA with respect to anything done by it in relation to any Notes in, from or otherwise involving the United Kingdom. |

Japan

Each Underwriter has acknowledged that the Notes have not been and will not be registered under the Financial Instrument and Exchange Law of Japan (Law No. 25 of 1948, as amended) (the “Financial Instrument and Exchange Law”). Each Underwriter has represented and agreed that it will not offer or sell any Notes, directly or indirectly, in Japan or to, or for the benefit of, any resident of Japan (which term as used herein means any person resident in Japan, including any corporation or other entity organized under the laws of Japan), or to others for re-offering or resale, directly or indirectly, in Japan or to a resident of Japan except only pursuant to an exemption from the registration requirements of, and otherwise in compliance with, the Financial Instrument and Exchange Law and any applicable laws, regulations and guidelines of Japan.

Singapore

This prospectus supplement and the accompanying prospectus have not been registered as a prospectus with the Monetary Authority of Singapore under the Securities and Futures Act, Chapter 289 of Singapore (as modified or amended from time to time including by any subsidiary legislation as may be applicable at the relevant time, the “SFA”). Accordingly, each Underwriter has represented, warranted and agreed that it has not offered or sold any Notes or caused the Notes to be made the subject of an invitation for subscription or purchase and will not offer or sell any Notes or cause the Notes to be made the subject of an invitation for subscription or purchase, and has not circulated or distributed, nor will it circulate or distribute, the prospectus supplement and the accompanying prospectus or any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of the Notes, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor (as defined in Section 4A of the SFA) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1) of the SFA, or any person pursuant to Section 275(1A) of the SFA, and in accordance with the conditions, specified in Section 275 of the SFA or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where the Notes are subscribed or purchased under Section 275 of the SFA by a relevant person which is: a) a corporation (which is not an accredited investor) (as defined in Section 4A of the SFA) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within 6 months after that corporation or that trust has acquired the Notes pursuant to an offer made under Section 275 of the SFA except: i) to an institutional investor or to a relevant person defined in Section 275(2) of the SFA, or to any person arising from an offer referred to in Section 276(4)(i)(B) of the SFA; ii) where no consideration is given for the transfer; or iii) where the transfer is by operation of law; or iv) pursuant to Section 276(7) of the SFA.

S-20

Table of Contents

Notification under Section 309B(1)(c) of the SFA — In connection with Section 309B of the SFA and the Securities and Futures (Capital Markets Products) Regulations 2018 of Singapore (the “CMP Regulations 2018”), the Issuer has determined, and hereby notifies all relevant persons (as defined in Section 309(A)(1) of the SFA), that the Notes are “prescribed capital markets products” (as defined in the CMP Regulations 2018) and Excluded Investment Products (as defined in MAS Notice SFA 04-N12: Notice on the Sale of Investment Products and MAS Notice FAA-N16: Notice on Recommendations on Investment Products).

Notice to Distributors regarding MIFID II Product Governance

Solely for the purposes of each manufacturer’s product approval process, the target market assessment in respect of the Notes has led the Underwriters to the conclusion that: (i) the target market for the Notes is eligible counterparties and professional clients only, each as defined in Directive 2014/65/EU (as amended, “MiFID II”); and (ii) all channels for distribution of the Notes to eligible counterparties and professional clients are appropriate. Any person subsequently offering, selling or recommending the Notes (a “distributor”) should take into consideration the manufacturers’ target market assessment; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessment in respect of the Notes (by either adopting or refining the manufacturers’ target market assessment) and determining appropriate distribution channels.

S-21

Table of Contents

The validity of the securities will be passed upon on behalf of FMS-WM by Sullivan & Cromwell LLP, and on behalf of the underwriters by Hogan Lovells US LLP. Sullivan & Cromwell LLP and Hogan Lovells US LLP may rely as to certain matters on the opinions of FMS-WM’s in-house counsel.

All statements in this prospectus supplement and the accompanying prospectus with respect to the statutory guarantee by the SoFFin have been passed upon by FMS-WM’s in-house counsel, and are included upon their authority.

S-22

Table of Contents

The following information is required by the rules of the Luxembourg Stock Exchange:

| 1. | The issuance of the Notes was duly authorized by FMS-WM’s Management Board pursuant to a resolution dated January 22, 2019. |

| 2. | The Notes have been accepted for clearance through DTC. The Global Note has been assigned ISIN No. , CUSIP No. and Common Code No. . |

| 3. | FMS-WM will appoint The Bank of New York Mellon as paying agent and transfer agent with respect to the Notes. A copy of the Fiscal Agency Agreement, dated as of November 14, 2012, and amended as of August 13, 2014, will be available for inspection at the office of The Bank of New York Mellon, 101 Barclay Street, New York, NY 10286, USA. In addition, a copy of the current, and any future, published annual and interim report of FMS-WM may be obtained free of charge at the office of The Bank of New York Mellon SA/NV, Luxembourg Branch, Vertigo Building – Polaris, 2-4 rue Eugène Ruppert, L-2453 Luxembourg, Luxembourg. |

| 4. | The independent auditors of FMS-WM are PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft. |

S-23

Table of Contents

PROSPECTUS

FMS WERTMANAGEMENT

Debt Securities

FMS Wertmanagement(“FMS-WM”), awind-up institution (Abwicklungsanstalt) organized as a public law entity (Anstalt öffentlichen Rechts) under public law of the Federal Republic of Germany (the “Federal Republic”), may from time to time offer debt securities. The securities will be offered from time to time in amounts, at prices and on terms to be determined at the time of sale and to be set forth in supplements to this prospectus. You should read this prospectus and the prospectus supplement carefully.

FMS-WM intends to apply for the securities to be admitted to the Euro MTF Market of the Luxembourg Stock Exchange.

Pursuant to the German Financial Market Stabilization Fund Act (Finanzmarktstabilisierungsfondsgesetz, “FMStFG”), the securities issued byFMS-WM will benefit from a statutory guarantee by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds (FMS), herein referred to as “SoFFin”). The Federal Republic is, in turn, directly liable for all of SoFFin’s obligations. See “Responsibility ofthe Federal Republic forFMS-WM”.

Neither the U.S. Securities and Exchange Commission (the “SEC”), any state securities commission, the Luxembourg Stock Exchange or any foreign governmental agencies has approved or disapproved of these securities or determined whether this prospectus is accurate and complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is January 13, 2017

Table of Contents

| Page | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 7 | ||||

| 8 | ||||

| 8 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 14 | ||||

| 16 | ||||

| 16 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 29 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

i

Table of Contents

This prospectus is part of a registration statement thatFMS-WM filed with the SEC under the U.S. Securities Act of 1933, as amended, utilizing a “shelf” registration process. Under this shelf registration process,FMS-WM may sell any combination of the securities described in this prospectus in one or more offerings up to the total dollar amount registered with the SEC (or the equivalent in other currencies).

This prospectus provides a general description of the securitiesFMS-WM may offer. Each timeFMS-WM sells securities, it will provide a prospectus supplement that will contain specific information about the terms of that offering. The prospectus supplement may also add, update or change information contained in this prospectus. You should read both this prospectus and any prospectus supplement together with additional information described under the heading “Where You Can Find More Information” below before you purchaseFMS-WM’s securities.

You should rely only on the information provided in this prospectus and in any prospectus supplement including the information incorporated by reference.FMS-WM has not authorized anyone to provide you with different or additional information.FMS-WM is not offering securities in any state where the offer is not permitted by law. You should not assume that the information in this prospectus, or any prospectus supplement, is accurate or complete at any date other than the date indicated on the cover page of those documents.FMS-WM’s activities, financial condition, results of operations and prospects may have changed since that date.

A portion of the securities offered hereby may be offered and sold outside of the United States in transactions not subject to the registration requirements of the U.S. Securities Act of 1933, as amended.

This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any of the securities offered hereby by any person in any jurisdiction in which it is unlawful for such person to make such an offering or solicitation. The offer or sale of the securities and the distribution of this prospectus may be restricted by law in certain jurisdictions, and you should inform yourself about, and observe, any such restrictions.

This prospectus may only be used for the purposes stated herein.

This prospectus and any prospectus supplement and documents incorporated by reference in this prospectus and any prospectus supplement may contain forward-looking statements. Statements that are not historical facts, including statements aboutFMS-WM’s beliefs and expectations, are forward-looking statements.Forward-looking statements speak only as of the date they are made, andFMS-WM undertakes no obligation to update publicly any of them in light of new information or future events. Forward-looking statements involve inherent risks and uncertainties and actual results may differ materially from those contained in anyforward-looking statements.

WHERE YOU CAN FIND MORE INFORMATION

FMS-WM files an annual report on Form18-K with the SEC. The annual report includes financial, statistical and other information concerningFMS-WM and the Federal Republic. You can inspect and copy this report at the SEC’s Conventional Reading Room, located at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at1-800-SEC-0330 for further information on the Conventional Reading Room. The report is also available to the public over the internet at the SEC’s website: http://www.sec.gov.

1

Table of Contents

The SEC allowsFMS-WM to “incorporate by reference” the documents thatFMS-WM files with the SEC, which means thatFMS-WM can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be part of this prospectus, and later information thatFMS-WM files with the SEC will automatically update and supersede this information, as well as the information included in this prospectus.FMS-WM incorporates by referenceFMS-WM’s annual report on Form18-K for the year ended December 31, 2015 (filed on June 6, 2016), as subsequently amended by amendment number one thereto (filed on October 11, 2016) and any future filings made with the SEC to the extent such filings indicate that they are intended to be incorporated by reference.

You can obtain any of the documents incorporated by reference in this prospectus fromFMS-WM, or from the SEC. These documents (excluding any exhibits thereto) are available fromFMS-WM free of charge by requesting them in writing or by telephone fromFMS-WM at the following address and telephone number:

FMS Wertmanagement

Prinzregentenstrasse 56

80538 Munich, Federal Republic of Germany

+49 899547627-0

PRESENTATION OF FINANCIAL INFORMATION

FMS-WM’s accounts are kept, and the economic data on the Federal Republic is expressed, in euro.

As used herein, the terms “euro,” “EUR” and the euro sign (€) refer to euro, and the terms “dollars,” “U.S. dollars,” “USD” and the dollar sign ($) refer to United States dollars.

Any discrepancies in the tables included in this prospectus between the amounts and the totals thereof are due to rounding.

2

Table of Contents

The following summary information should be read in conjunction with the more complete information included inFMS-WM’s annual report on Form18-K for the year ended December 31, 2015, as amended, and any future periodic reports and amendments filed byFMS-WM with the SEC.

FMS-WM is awind-up institution (Abwicklungsanstalt) organized as a public law entity (Anstalt öffentlichen Rechts) under public law of the Federal Republic and is wholly owned by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds). The German Financial Market Stabilization Fund, which is abbreviated as FMS in German and referred to in this prospectus as SoFFin, is a special pool of assets (Sondervermögen) of the Federal Republic.FMS-WM is charged with liquidating a portfolio of risk positions andnon-strategic assets/businesses in an original amount of EUR 175.7 billion (nominal volume) that it assumed from Hypo Real Estate Holding AG and its subsidiaries and special purpose entities (referred to herein collectively as the “HRE Group”) on October 1, 2010. As of 2007, the HRE Group was one of the largest commercial property lenders, issuers of covered bonds and providers of public finance in Germany. It encountered severe financial difficulties in 2008/09 in the course of the global financial markets crisis. Given the systemic importance of the HRE Group and the resulting public interest in stabilizing the HRE Group, the Federal Republic initiated support measures for this financial institution, including the transfer of risk positions andnon-strategic assets/businesses toFMS-WM.

FMS-WM pursues its objective of managing and unwinding its portfolio according to a strategic management framework known as the“winding-up plan” (Abwicklungsplan), which is updated and adapted on a regular basis.FMS-WM aims to maximize the value of its portfolio by managing and liquidating it in a value-preserving manner over an extended period of time. For any given part of the portfolio, the plan requires an assessment of whetherFMS-WM should sell, hold, or restructure its holdings.

FMS-WM engages in funding activities, including the issuance of debt securities and/or obtaining financing from financial institutions, in order to refinance funding instruments associated with the portfolio it has assumed as they expire.FMS-WM will have to engage in refinancing activities on the capital markets until its portfolio has been liquidated.

FMS-WM is registered with the commercial register (Handelsregister) of the local court (Amtsgericht) of Munich under HRA 96076. Its registered office and business address is at Prinzregentenstrasse 56, 80538 Munich, Federal Republic of Germany. Its telephone number is +49 899547627-0.

FMS-WM’s creation and legal status are a direct result of the German Federal Government’s response to the global financial markets crisis. In October 2008, the German Federal Government enacted a comprehensive package of measures to support key German strategic financial institutions, most notably the HRE Group. This comprehensive package included the FMStFG, which provided for the implementation of SoFFin and established the German Federal Agency for Financial Market Stabilization (Bundesanstalt für Finanzmarktstabilisierung, “FMSA”), a federal agency under public law with legal personality (rechtsfähige Anstalt öffentlichen Rechts) supervised by the German Federal Ministry of Finance (Bundesfinanzministerium). Section 8a of the FMStFG grants FMSA the power to createwind-up institutions. The purpose of these institutions is to assume distressed andnon-strategic assets from systemically important financial institutions and to eventually dispose of or liquidate the risk positions transferred to them.

Following the financial difficulties encountered by Depfa Bank plc and the solvency issues affecting the HRE Group that ensued in September 2008, various government support measures were instituted by the Federal

3

Table of Contents

Republic. These support measures, which were taken in consideration of the HRE Group’s importance for the German financial system, led to the SoFFin becoming the sole owner of the HRE Group in October 2009. They also included the extension of liquidity guarantees by SoFFin and the creation ofFMS-WM as awind-up institution under Section 8a of the FMStFG on July 8, 2010. Risk positions andnon-strategic assets/businesses of the HRE Group were then transferred toFMS-WM on October 1, 2010.

FMS-WM is a public law institution with partial legal capacity (teilrechtsfähige Anstalt des öffentlichen Rechts) created pursuant to German administrative law. It is fully-owned by the SoFFin and is subject to the supervision and control of FMSA.FMS-WM may act in its own name, and may be subject to court proceedings. In order to achieve its mandate of unwinding the portfolio of risk positions andnon-strategic assets/businesses assumed from the HRE Group,FMS-WM may engage in all kinds of banking and financial services transactions and all other transactions that directly or indirectly serve its purposes.FMS-WM is, however, neither a financial institution nor a financial services institution within the meaning of the German Banking Act (Kreditwesengesetz, “KWG”), nor a financial service provider within the meaning of the German Securities Trading Act (Wertpapierhandelsgesetz, “WpHG”), nor an insurance company within the meaning of the German Insurance Supervision Act (Versicherungsaufsichtsgesetz) nor regulated as such. As a consequence,FMS-WM is prohibited from engaging in transactions that would require a license under the European Union Banking Directive (2006/48/EC) or the European Union Directive on markets for financial instruments (2004/39/EC). Nonetheless, pursuant to its charter and the FMStFG,FMS-WM is subject to certain provisions of the KWG and the WpHG. In particular,FMS-WM is subject to banking supervision by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht) and must comply with the organizational obligations and restrictions on certain activities imposed by the KWG applicable to banks and financial institutions.FMS-WM is, however, exempted from the regulatory capital and liquidity requirements and the licensing requirements under the KWG.FMS-WM is also deemed to be a financial institution for purposes of the German Money Laundering Act (Geldwäschegesetz), and is therefore subject to the provisions thereof.

Relationship with the Federal Republic of Germany

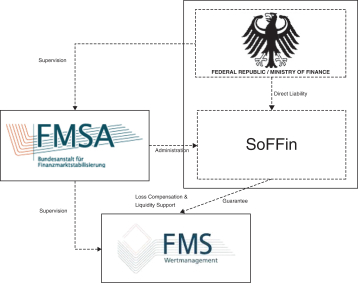

The following chart provides an overview of the current relationship betweenFMS-WM and the Federal Republic:

For information on certain changes to the supervision of FMSA and the administration of SoFFin as a result of a pending reorganization of FMSA, see “—Reorganization of FMSA” below.

4

Table of Contents

Relationship with SoFFin

SoFFin.FMS-WM is fully-owned by SoFFin, which is established by law and designated to fulfill specific tasks of the German Federal Government assigned to it under the FMStFG. SoFFin is currently administered by FMSA and, following the pending reorganization of FMSA, is expected to be administered and managed by Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH) (see “—Reorganization of FMSA”). SoFFin is a special pool of assets (Sondervermögen) of the Federal Republic. The term special pool of assets (Sondervermögen) designates legally dependent assets of the Federal Republic. Accordingly, the FMStFG provides that SoFFin shall have no legal capacity, although in legal relations SoFFin may act, sue and be sued in its own name. There shall be no attachment of, or other measures of compulsory execution against, SoFFin. Any debt incurred by SoFFin is accounted for as direct debt of the Federal Republic. In addition, Section 5 of the FMStFG provides that the Federal Republic is directly liable for the obligations of SoFFin. SoFFin’s obligations are thus effectively obligations of the Federal Republic.

SoFFin’s purpose is to stabilize the German financial sector by extending liquidity guarantees, providing equity capital, assuming risk positions, and setting upwind-up institutions. To this end, SoFFin has been authorized by the German legislature under Section 6 of the FMStFG to extend liquidity guarantees in a total aggregate amount of up to EUR 400 billion. In addition, Section 9 of the FMStFG authorizes the German Federal Ministry of Finance to incur debt in a total aggregate amount of up to EUR 80 billion to cover the cost of measures taken by SoFFin in connection with the provision of equity capital, the assumption of risk positions and the compensation of losses ofwind-up institutions. Any financing required by SoFFin is obtained in the manner used by the Federal Republic to finance itself, i.e., through the issuance of debt instruments by the Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH). When the Federal Republic incurs debt for SoFFin it results in an increase in the net borrowings and debt of the Federal Republic. Applications for stabilization measures extended by SoFFin could initially be made only until the end of 2010. As a consequence of developments in the euro area, however, the German Federal Government subsequentlyre-opened the application period, which finally expired at the end of 2015. The timing of the expiration of SoFFin’s mandate to accept new applications for support measures coincided with the assumption by the European Single Resolution Board at the beginning of 2016 of responsibility for resolving and restructuringnon-viable systemically important banks.

Guarantee. With effect from January 1, 2014, Section 8a of the FMStFG, which deals with the establishment ofwind-up institutions, was amended to provide that SoFFin guarantees all existing and future obligations ofFMS-WM with respect to moneys, debt securities and derivative transactions as well as obligations of third parties that are expressly guaranteed byFMS-WM, whichFMS-WM has borrowed, issued, entered into or incurred or which have been transferred toFMS-WM during the time period for which SoFFin is the sole obligor of the loss compensation obligation (alleiniger Verlustausgleichspflichtiger). For a description of SoFFin’s loss compensation obligation, see “—Loss Compensation and Liquidity Support Obligations” below. Accordingly, under the guarantee, ifFMS-WM fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued by it when that payment is due and payable, SoFFin will be liable for that payment as and when it becomes due and payable, provided that the security was issued during the time period for which SoFFin was the sole obligor of the loss compensation obligation. SoFFin’s obligation under the guarantee ranks equally, without any preference, with all of its other present and future unsecured and unsubordinated indebtedness. Holders of securities issued byFMS-WM may enforce this obligation directly against SoFFin without first having to take legal action againstFMS-WM. If SoFFin fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued byFMS-WM when that payment is due and payable under the guarantee, the Federal Republic will be liable for that payment as and when it becomes due and payable pursuant to Section 5 of the FMStFG, as described above. The guarantee and the Federal Republic’s direct liability for SoFFin’s obligations pursuant to Section 5 of the FMStFG are strictly a matter of statutory law and are not evidenced by any contract or instrument. Potential claims based on the guarantee and on Section 5 of the FMStFG may be subject to defenses

5

Table of Contents

available toFMS-WM and SoFFin with respect to the obligations covered. For additional information on the guarantee and the Federal Republic’s direct liability for SoFFin’s obligations, see “Responsibility ofthe Federal Republic forFMS-WM—Guarantee.”

Loss Compensation and Liquidity Support Obligations.UnderFMS-WM’s charter, which was enacted pursuant to Section 8a of the FMStFG, SoFFin is obligated to cover all losses sustained byFMS-WM and to ensure thatFMS-WM is able to pay all its liabilities at all times when due and in full. As described above, pursuant to Section 5 of the FMStFG, the Federal Republic is directly liable for SoFFin’s obligations. Accordingly, SoFFin’s loss compensation and liquidity support obligations enableFMS-WM to pursue its operations and effectively mean thatFMS-WM’s obligations, including the obligations to holders of debt securities issued byFMS-WM, are backed by the full faith and credit of the Federal Republic. For additional information on the loss compensation and liquidity support obligations, see “Responsibility ofthe Federal Republic forFMS-WM—Liquidity Support and Loss Compensation Obligations.”

Relationship with FMSA