Table of Contents

Filed pursuant to Rule 424(b)(3)

Registration No. 333-187766

PROSPECTUS

Chesapeake Oilfield Operating, L.L.C.

Chesapeake Oilfield Finance, Inc.

Offer to Exchange

Up to $650,000,000 Principal Amount of

6.625% Senior Notes due 2019

for

a Like Principal Amount of

6.625% Senior Notes due 2019

that have been registered under the Securities Act of 1933

This Exchange Offer will expire at 5:00 p.m.,

New York City time, on July 15, 2013, unless extended.

Chesapeake Oilfield Operating, L.L.C. is offering to exchange registered 6.625% Senior Notes due 2019, or the “exchange notes,” for any and all of its unregistered 6.625% Senior Notes due 2019, or the “original notes,” that were issued pursuant to a private placement on October 28, 2011. We refer to the original notes and the exchange notes together in this prospectus as the “Notes” or “notes.” We refer to this exchange as the “exchange offer.” The exchange notes are substantially identical to the original notes, except the exchange notes are registered under the Securities Act of 1933, as amended (the “Securities Act”), and the transfer restrictions and registration rights, and related special interest provisions, applicable to the original notes will not apply to the exchange notes. The exchange notes will represent the same debt as the original notes, and we will issue the exchange notes under the same indenture used in issuing the original notes.

Terms of the exchange offer:

| • | The exchange offer expires at 5:00 p.m., New York City time, on July 15, 2013, unless we extend it. |

| • | The exchange offer is subject to customary conditions, which we may waive. |

| • | We will exchange all outstanding original notes that are validly tendered and not withdrawn prior to the expiration of the exchange offer for an equal principal amount of exchange notes. All interest due and payable on the original notes will become due and payable on the same terms under the exchange notes. |

| • | You may withdraw your tender of original notes at any time prior to the expiration of the exchange offer. |

| • | The exchange of original notes for exchange notes will not be a taxable transaction for U.S. federal income tax purposes, but you should see the discussion under the caption “U.S. Federal Income Tax Considerations” on page 126 for more information. |

See “Risk Factors” beginning on page 13 for a discussion of risks you should consider in connection with the exchange offer and an investment in the exchange notes.

Each broker-dealer that receives exchange notes pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of exchange notes. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for original notes where such original notes were acquired as a

Table of Contents

result of market-making activities or other trading activities. We have agreed to make this prospectus available to such broker-dealers upon reasonable request for the period required by the Securities Act. See “The Exchange Offer — Purpose and Effects of the Exchange Offer” and “Plan of Distribution.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is June 13, 2013.

Table of Contents

| ii | ||||

| iii | ||||

| 1 | ||||

| 13 | ||||

| 28 | ||||

| 37 | ||||

| 38 | ||||

| 40 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 41 | |||

| 58 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 72 | ||||

| 80 | ||||

| 81 | ||||

| 82 | ||||

| 123 | ||||

| 126 | ||||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| F-1 |

i

Table of Contents

YOU SHOULD RELY ONLY ON THE INFORMATION CONTAINED IN THIS PROSPECTUS AND IN THE ACCOMPANYING LETTER OF TRANSMITTAL. WE HAVE NOT AUTHORIZED ANYONE TO PROVIDE YOU WITH ANY OTHER OR DIFFERENT INFORMATION. IF YOU RECEIVE ANY UNAUTHORIZED INFORMATION, YOU MUST NOT RELY ON IT. THIS PROSPECTUS MAY ONLY BE USED WHERE IT IS LEGAL TO EXCHANGE THE ORIGINAL NOTES FOR THE EXCHANGE NOTES, AND THIS PROSPECTUS IS NOT AN OFFER TO EXCHANGE OR A SOLICITATION TO EXCHANGE THE ORIGINAL NOTES FOR THE EXCHANGE NOTES IN ANY JURISDICTION WHERE AN OFFER OR EXCHANGE WOULD BE UNLAWFUL. YOU SHOULD ASSUME THAT THE INFORMATION CONTAINED IN THIS PROSPECTUS IS ACCURATE ONLY AS OF THE DATE OF THIS PROSPECTUS.

Certain statements contained in this prospectus constitute forward-looking statements. These statements relate to future events or our future performance. All statements other than statements of historical fact may be forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek,” “anticipate,” “plan,” “continue,” “estimate,” “expect,” “may,” “will,” “project,” “predict,” “potential,” “targeting,” “intend,” “could,” “might,” “should,” “believe” and similar expressions. These statements involve known and unknown risks, uncertainties and other facts that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. We believe the expectations reflected in these forward-looking statements are reasonable but we cannot assure you that these expectations will prove to be correct. You should not place undue reliance on forward-looking statements included in this prospectus.

Our actual results could differ materially from those anticipated in these forward-looking statements as a result of many factors, including the following factors and the factors discussed in “Risk Factors” and elsewhere in this prospectus:

| • | dependence on Chesapeake Energy Corporation (“Chesapeake”) for a substantial majority of our revenues; |

| • | Chesapeake’s expenditures for oilfield services; |

| • | the limitations that Chesapeake’s and our own level of indebtedness may have on our financial flexibility; |

| • | the cyclical nature of the oil and natural gas industry; |

| • | changes in supply and demand of drilling rigs, hydraulic fracturing fleets and other equipment; |

| • | the availability of capital resources to fund capital expenditures and other contractual obligations, and our ability to access those resources through the debt or equity capital markets; |

| • | hazards and operational risks that may not be fully covered by insurance; |

| • | increased labor costs or the unavailability of skilled workers; |

| • | competitive conditions; and |

| • | legislative or regulatory changes, including changes in environmental regulations, environmental risks and liability under federal and state environmental laws and regulations. |

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this prospectus, including the information presented under the heading “Risk Factors.” If one or more events related to these or other risks and uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may differ materially from what we anticipate. Except as may be required by law, we do not intend, and do not assume any obligation, to update any forward-looking statements.

ii

Table of Contents

The market data and certain other statistical information used throughout this prospectus, including statements as to our ranking, market position and market estimates, are based on independent industry publications, government publications or other published independent sources. Some data is also based on our good faith estimates. Prospective investors are cautioned not to place undue reliance on such data and information due to the fact that it may be based on our estimates or, if derived from a third party, such data may not have been independently verified.

iii

Table of Contents

This summary highlights selected information about us and the exchange offer contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that may be important to you or that you should consider before participating in the exchange offer or making an investment in the exchange notes. You should read carefully the entire prospectus.

On October 25, 2011, Chesapeake completed the process of reorganizing its oilfield services subsidiaries and operations (the “COS Reorganization”) as subsidiaries of COS Holdings, L.L.C. (“COS LLC”) and commenced providing all of its oilfield services through COS LLC and its wholly owned subsidiary, Chesapeake Oilfield Operating, L.L.C. (“COO”). As a result, the historical financial information presented in this prospectus for periods and as of dates prior to the COS Reorganization is the historical consolidated financial information of our “predecessor.” The historical financial information presented in this prospectus for periods and as of dates on or after the COS Reorganization is the historical consolidated financial information of COO.

In this prospectus, unless indicated otherwise or the context requires otherwise, references to the terms “we,” “our,” “us” and the “Company” generally refer to COS LLC and its consolidated subsidiaries, including COO and Chesapeake Oilfield Finance, Inc. (“COF”). However, with respect to rights and obligations under the notes, the related indenture and the registration rights agreement described in this prospectus, references to “we,” “our,” “us” and the “Company” refer to COO and not to any of its subsidiaries, other than COF. The financial information presented in this prospectus is that of COO and its consolidated subsidiaries, including COF and the subsidiary guarantors. References to “Chesapeake Energy Corporation” or “Chesapeake” refer to Chesapeake Energy Corporation and its wholly owned subsidiaries (excluding us), unless the context indicates otherwise.

Our Company

We are a diversified oilfield services company that provides a wide range of wellsite services primarily to Chesapeake, our founder and principal customer, and its working interest partners. We focus on providing services to Chesapeake that are strategic to its oil and natural gas operations, represent historical bottlenecks to those operations or provide relatively high margins to the service provider, including drilling, hydraulic fracturing, oilfield rentals, rig relocation, fluid transportation and disposal and manufacturing of natural gas compressor packages. Our operations are geographically diversified across most major basins in the U.S. Specifically, we provide Chesapeake and its working interest partners with services in the Eagle Ford, Utica, Granite Wash, Cleveland, Tonkawa, Mississippi Lime and Niobrara liquids-rich plays and the Barnett, Haynesville, Bossier and Marcellus natural gas shale plays.

Our business has grown rapidly since our first subsidiary was founded in 2001, both organically and through acquisitions. As of March 31, 2013, we owned or leased 116 land drilling rigs. As of March 31, 2013, we also operated (a) eight hydraulic fracturing fleets with an aggregate of 315,000 horsepower; (b) a diversified oilfield rentals business; (c) an oilfield trucking fleet consisting of 286 rig relocation trucks, 67 cranes and forklifts used in the movement of drilling rigs and other heavy equipment and 254 fluid hauling trucks; and (d) manufacturing capacity for up to 150 natural gas compressor packages per quarter, or approximately 85,000 horsepower in the aggregate per quarter. We continue to modernize our asset base and have received seven of our proprietary, fit-for-purpose PeakeRigs™ that utilize advanced electronic drilling technology. We are scheduled to receive three additional PeakeRigs™ by July 2013.

We are an indirect, wholly owned subsidiary of Chesapeake. During the three months ended March 31, 2013 and for the years ended December 31, 2012, 2011 and 2010, Chesapeake and its working interest partners accounted for approximately 94%, 94%, 94% and 96% of our revenues, respectively, and we expect to derive a substantial majority of our revenues from Chesapeake and its working interest partners for the foreseeable future. Please read “Risk Factors—Risks Relating to Our Business—We are dependent on Chesapeake for a substantial majority of our revenues. Therefore, we are indirectly subject to the business and financial risks of Chesapeake. We have no control over Chesapeake’s business decisions and operations, and Chesapeake is under no obligation to adopt a business strategy that favors us,” “Risk Factors—Risks Relating to Our Business—Demand for services in our industry is cyclical and depends on drilling and completion spending by Chesapeake and other E&P companies in the U.S., and the level of such activity is volatile” and “Risk Factors—Risks Relating to Our Relationship with Chesapeake.”

We conduct our business through five operating segments:

Drilling. Our drilling segment provides land drilling and drilling-related services, including directional drilling, geosteering and mudlogging, for oil and natural gas exploration and development activities. As of March 31, 2013, we owned or leased a fleet of 116 land drilling rigs.

Hydraulic Fracturing. Our hydraulic fracturing segment provides hydraulic fracturing and other well stimulation services. Hydraulic fracturing involves pumping fluid down a well casing or tubing under high pressure to cause the underground formation to crack, allowing the oil or natural gas to flow more freely. As of March 31, 2013, we owned eight hydraulic fracturing fleets with an aggregate of 315,000 horsepower.

1

Table of Contents

Oilfield Rentals. Our oilfield rentals segment provides premium rental tools for land-based oil and natural gas drilling, completion and workover activities. We offer a full line of rental tools, including drill pipe, drill collars, tubing, blowout preventers, frac tanks, mud tanks and environmental containment. We also provide air drilling, flowback services and services associated with the transfer of water to the wellsite for well completions.

Oilfield Trucking. Our oilfield trucking segment provides drilling rig relocation and logistics services as well as fluid handling services. Our trucks move drilling rigs, crude oil, other fluids and construction materials to and from the wellsite and also transport produced water from the wellsite. As of March 31, 2013, we owned a fleet of 286 rig relocation trucks, 67 cranes and forklifts and 254 fluid hauling trucks.

Other Operations. Our other operations primarily consist of our natural gas compressor manufacturing operations and corporate functions.

Industry Overview

Oilfield services companies provide services that are used by exploration and production companies, or E&P companies, in connection with the exploration for, and the development and production of, hydrocarbons. E&P companies operating in the U.S. include independent E&P companies, such as Chesapeake and ConocoPhillips, U.S.-based major integrated oil and gas companies, such as ExxonMobil and Chevron, and international major integrated oil and gas companies, such as Shell Oil Company, Total S.A., BP America, CNOOC Limited, Sinopec International Petroleum Exploration and Production Corporation and Statoil. Demand for domestic onshore oilfield services is a function of the willingness of E&P companies to make capital and operating expenditures to explore for, develop and produce hydrocarbons in the U.S. When oil or natural gas prices increase, E&P companies generally increase their capital expenditures, resulting in greater revenues and profits for oilfield services companies. Likewise, significant decreases in the prices of those commodities typically lead E&P companies to reduce their capital expenditures, which diminishes demand for oilfield services.

Oil and natural gas prices rose to record levels in 2008 and then began to decline in late 2008 in conjunction with the widespread economic recession. While the price of oil rebounded somewhat in 2009 and continued to rise throughout 2010 and 2011, the price of natural gas has remained relatively low since 2009, largely due to discoveries of vast new natural gas resources in the U.S. Oil prices were volatile in 2012 due to increased domestic supply and economic and political uncertainty. Low natural gas prices have resulted in increased drilling activity in liquids-rich plays as operators have reduced less economical natural gas drilling activities.

In response to low natural gas prices, a number of E&P companies, including Chesapeake, have reduced dry natural gas drilling and production and redirected their activities and capital toward currently more economical liquids-rich plays. Liquids-rich plays are those that are characterized by production of predominantly oil and natural gas liquids (NGL) such as ethane, propane, butane and iso-butane, which are used as energy sources and manufacturing feedstocks. NGL prices have historically been highly correlated with oil prices rather than natural gas prices, although they have decoupled recently due to increased production. The proportion of rigs in the U.S. drilling for oil versus natural gas has also increased steadily over the past few years and, in April 2011, for the first time since 1993, the number of rigs drilling for oil surpassed the number of rigs drilling for natural gas.

The number of drilling rigs under contract in the U.S. decreased in 2009 but rebounded in 2010 and has remained relatively high compared to historical levels, according to data compiled by Baker Hughes Incorporated. This has remained the case despite a dramatic decrease in the price of natural gas over the same period, suggesting a weakening in the traditional correlation between natural gas prices and U.S. onshore drilling rig counts. We believe this decrease in correlation is attributable to several factors, including the discovery of potentially large liquids-rich unconventional plays onshore in the U.S., the increasing presence in U.S. onshore plays of major U.S. and international integrated E&P companies that are typically less reactive to short-term pricing fluctuations than most independent E&P companies, the presence of term contracts for certain types of oilfield services, the need by operators to commence drilling activities in order to establish production and avoid the expiration of oil and natural gas leases, and the more regimented approach to developing unconventional plays characterized by

2

Table of Contents

continuous hydrocarbon accumulations. Additionally, we believe that the weakening correlation between natural gas prices and U.S. onshore rig counts is partially attributable to the prevalence of joint ventures for the development of U.S. unconventional plays, many of which include a drilling “carry” that is paid by the joint venture partner and used by the operator to pay for a portion of the cost of drilling and completing the well. Chesapeake, for example, has entered into several such joint ventures since 2008 with companies such as Total S.A., CNOOC Limited, Statoil, BP America and Plains Exploration & Production Company that have resulted in more than $9.0 billion of drilling carries to Chesapeake.

Our Relationship with Chesapeake

We are an indirect, wholly owned subsidiary of Chesapeake. We are party to several agreements with Chesapeake, including a master services agreement and services agreement pursuant to which we provide services and supply materials and equipment to Chesapeake and under which Chesapeake has agreed to operate a minimum number of our drilling rigs and to utilize our hydraulic fracturing equipment for a minimum number of fracturing stages per month. In addition, we and Chesapeake are parties to an administrative services agreement and a facilities lease agreement. These agreements were entered into in the context of an affiliated relationship and, consequently, may not be as favorable to us as they might have been if we had negotiated them with unaffiliated third parties. For a more comprehensive discussion of certain agreements that we have entered into with Chesapeake and its affiliates, please see “Certain Relationships and Related Party Transactions.” For a discussion of the risks related to our relationship with Chesapeake, please see “Risk Factors—Risks Relating to Our Relationship with Chesapeake.”

3

Table of Contents

Corporate Information

Our principal executive offices are located at 6100 North Western Avenue, Oklahoma City, Oklahoma 73118, and our telephone number is (405) 848-8000. Our website is located at www.chesapeakeoilfieldservices.com. Information on our website or any other website is not incorporated by reference herein and does not constitute a part of this prospectus.

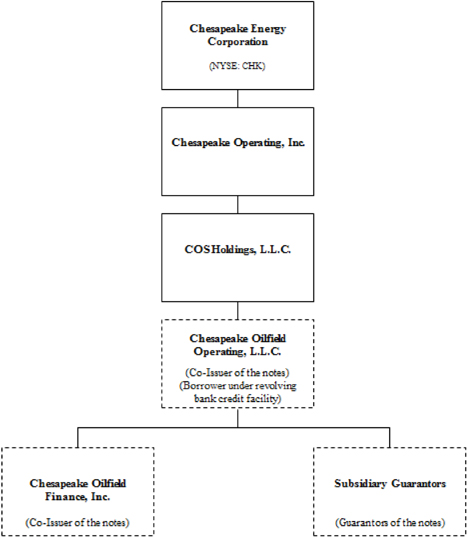

Summary Organizational Structure

The following chart sets forth a summary of our organizational structure as of the date of this prospectus.

4

Table of Contents

Summary of the Exchange Offer

On October 28, 2011, Chesapeake Oilfield Operating, L.L.C. and Chesapeake Oilfield Finance, Inc. completed an unregistered offering of the original notes. As part of that offering, we entered into a registration rights agreement with the initial purchasers of the original notes, which we refer to as the registration rights agreement, in which we agreed, among other things, to offer to exchange the original notes for the exchange notes. The following is a summary of the principal terms of the exchange offer. A more detailed description is contained in the section of this prospectus titled “The Exchange Offer.”

Original Notes | 6.625% Senior Notes due 2019, which were issued by Chesapeake Oilfield Operating, L.L.C. and Chesapeake Oilfield Finance, Inc. in a private placement on October 28, 2011. | |

Exchange Notes | 6.625% Senior Notes due 2019, issued by Chesapeake Oilfield Operating, L.L.C. and Chesapeake Oilfield Finance, Inc. The terms of the exchange notes are substantially identical to the terms of the original notes, except that the exchange notes are registered under the Securities Act, and the transfer restrictions and registration rights, and related special interest provisions, applicable to the original notes will not apply to the exchange notes. | |

Exchange Offer | Pursuant to the registration rights agreement, we are offering to exchange up to $650.0 million principal amount of our exchange notes that have been registered under the Securities Act for an equal principal amount of our original notes. | |

| The exchange notes will evidence the same debt as the original notes, including principal and interest, and will be issued under and be entitled to the benefits of the same indenture that governs the original notes. Holders of the original notes do not have any appraisal or dissenter’s rights in connection with the exchange offer. Because the exchange notes will be registered, the exchange notes will not be subject to transfer restrictions and holders of original notes that tender and have their original notes accepted in the exchange offer will no longer have registration rights or the right to receive the related special interest under the circumstances described in the registration rights agreement. Please see “The Exchange Offer” for more information regarding the registration rights agreement. | ||

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on July 15, 2013, which we refer to as the Expiration Date, unless we decide to extend it or terminate it early. We do not currently intend to extend the exchange offer. A tender of original notes pursuant to this exchange offer may be withdrawn at any time on or prior to the Expiration Date if we receive a valid written withdrawal request before the expiration of the exchange offer. | |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, which we may, but are not required to, waive. Please see “The Exchange Offer—Conditions to the Exchange Offer” for more information regarding the conditions to the exchange offer. | |

5

Table of Contents

Procedures for Tendering Original Notes | Unless you comply with the procedures described under “The Exchange Offer—Procedures for Tendering Original Notes—Guaranteed Delivery,” to participate in the exchange offer, on or prior to the Expiration Date you must tender your original notes by using the book-entry transfer procedures described in “The Exchange Offer—Procedures for Tendering Original Notes—Tenders of Original Notes; Book-Entry Delivery Procedure,” including transmission or delivery to the exchange agent of an agent’s message or a properly completed and duly executed letter of transmittal, with any required signature guarantee. In order for a book-entry transfer to constitute a valid tender of your original notes in the exchange offer, Wells Fargo Bank, National Association, as registrar and exchange agent, must receive a confirmation of book-entry transfer of your original notes into the exchange agent’s account at The Depository Trust Company prior to the Expiration Date. | |

By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things:

• you are acquiring exchange notes in the ordinary course of your business;

• you have no arrangement or understanding with any person or entity to participate in a distribution of the exchange notes;

• you are not our or any subsidiary guarantor’s “affiliate” as defined in Rule 405 of the Securities Act;

• if you are not a broker-dealer, that you are not engaged in, and do not intend to engage in, the distribution of the exchange notes; and

• if you are a broker-dealer that will receive exchange notes for your own account in exchange for original notes that were acquired by you as a result of market-making or other trading activities, that you will deliver a prospectus in connection with any resale of such exchange notes.

If you are a broker-dealer, you may not participate in the exchange offer as to any original notes you purchased directly from us. | ||

Guaranteed Delivery Procedures | If you wish to tender your original notes in the exchange offer, but such notes are not immediately available or if you cannot deliver your original notes and the other required documents prior to the expiration date, then you may tender original notes by following the procedures described below under “The Exchange Offer—Procedures for Tendering Original Notes—Guaranteed Delivery.” | |

Withdrawal; Non-Acceptance | You may withdraw any original notes tendered in the exchange offer by sending the exchange agent written notice of withdrawal at any time prior to 5:00 p.m., New York City time, on the Expiration Date. For further information regarding the withdrawal of tendered original notes, please see “The Exchange Offer—Withdrawal of Tenders.” If any tendered original notes are not accepted for exchange because they do not comply with the procedures set forth in this prospectus and the accompanying letter of transmittal, or because of our withdrawal of the exchange offer, the occurrence of certain other events set forth herein or otherwise, such unaccepted original notes will be returned, without expense, to the tendering holder promptly after the Expiration Date or our withdrawal of the exchange offer. For further information regarding conditions to the exchange offer, please see “The Exchange Offer—Conditions to the Exchange Offer.” | |

U.S. Federal Income Tax Considerations | The exchange of original notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. Please see “U.S. Federal Income Tax Considerations” for more information regarding the tax consequences to you of the exchange offer. | |

6

Table of Contents

Use of Proceeds | The issuance of the exchange notes will not provide us with any proceeds. We are making this exchange offer solely to satisfy our obligations under the registration rights agreement we entered into with the initial purchasers of the original notes. | |

Fees and Expenses | We will pay all expenses incident to the exchange offer. | |

Exchange Agent | We have appointed Wells Fargo Bank, National Association as our exchange agent for the exchange offer. You can find the address and telephone number of the exchange agent elsewhere in this prospectus under the caption “The Exchange Offer—Exchange Agent.” | |

Resales of Exchange Notes | Based on interpretations by the staff of the Securities and Exchange Commission (SEC), as set forth in no-action letters issued to third parties, we believe that the exchange notes you receive in the exchange offer may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act so long as certain conditions are met. See “The Exchange Offer—Purpose and Effects of the Exchange Offer” and “Plan of Distribution” for more information regarding resales. | |

Not Exchanging Your Original Notes | If you do not exchange your original notes in this exchange offer, you will continue to hold unregistered original notes and you will no longer be entitled to registration rights or the special interest provisions related thereto, except in the limited circumstances set forth in the registration rights agreement. See “The Exchange Offer—Consequences of Failure to Exchange.” In addition, you will not be able to resell, offer to resell or otherwise transfer your original notes unless you do so in a transaction exempt from the registration requirements of the Securities Act and applicable state securities laws or unless we register the offer and resale of your original notes under the Securities Act. Following the exchange offer, we will be under no obligation to, and we do not intend to, register your original notes, except under the limited circumstances set forth in the registration rights agreement. | |

Additional Documentation; Further Information; Assistance | Any questions or requests for assistance or additional documentation regarding the exchange offer may be directed to the exchange agent. Beneficial owners of original notes should contact their broker, dealer, commercial bank, trust company or other nominee for assistance in tendering their original notes in the exchange offer. | |

7

Table of Contents

The Exchange Notes

The terms of the exchange notes and those of the outstanding original notes are substantially identical, except that the exchange notes are registered under the Securities Act, and the transfer restrictions and registration rights, and related special interest provisions, applicable to the original notes will not apply to the exchange notes. The exchange notes represent the same debt as the original notes for which they are being exchanged. Both the original notes and the exchange notes are governed by the same indenture. The brief summary below describes the principal terms of the exchange notes. Some of the terms and conditions described below are subject to important limitations and exceptions. The “Description of Exchange Notes” section of this prospectus contains a more detailed description of the terms and conditions of the exchange notes.

Issuers | Chesapeake Oilfield Operating, L.L.C. and Chesapeake Oilfield Finance, Inc. | |

Exchange Notes Offered | $650.0 million aggregate principal amount of 6.625% Senior Notes due 2019. | |

Maturity | November 15, 2019. | |

Interest | 6.625% per annum payable semi-annually in arrears on May 15 and November 15 of each year. | |

Guarantees | The exchange notes initially will be guaranteed, jointly and severally, on a senior unsecured basis by all of Chesapeake Oilfield Operating, L.L.C.’s existing subsidiaries, other than certain immaterial subsidiaries, including Chesapeake Oilfield Finance, Inc. See “Description of Exchange Notes—Subsidiary Guarantees.” | |

Ranking | The exchange notes and guarantees will constitute senior unsecured debt of Chesapeake Oilfield Operating, L.L.C. and Chesapeake Oilfield Finance, Inc. and the guarantors. They will rank: | |

• equally in right of payment with all of our existing and future senior unsecured indebtedness;

• effectively junior in right of payment to all of our existing and future secured indebtedness and other obligations to the extent of the value of the assets securing such indebtedness or obligations, including indebtedness under our revolving bank credit facility;

• effectively junior in right of payment to all of the indebtedness and other liabilities of any of our subsidiaries that do not guarantee the exchange notes, to the extent of the assets of those subsidiaries; and

• senior to any of our future subordinated indebtedness.

As of March 31, 2013, Chesapeake Oilfield Operating, L.L.C.’s and Chesapeake Oilfield Finance, Inc.’s outstanding debt was approximately $1.1 billion, of which $650.0 million was the original notes and $407.6 million was secured indebtedness outstanding under the revolving bank credit facility. In addition, Chesapeake Oilfield Operating, L.L.C. had the ability to access an additional $92.4 million under the revolving bank credit facility. | ||

8

Table of Contents

Optional Redemption | We may redeem the exchange notes, in whole or in part, at any time on or after November 15, 2015 at the redemption prices set forth in this prospectus plus accrued and unpaid interest, if any. See “Description of Exchange Notes—Optional Redemption.”

At any time prior to November 15, 2014, subject to certain exceptions, we may on one or more occasions redeem up to 35% of the aggregate principal amount of the exchange notes with net cash proceeds of one or more qualified equity offerings at the redemption price set forth in this prospectus plus accrued and unpaid interest, if any. In addition, at any time prior to November 15, 2015, we may on one or more occasions redeem all or part of the exchange notes at a redemption price equal to 100% of the principal amount of the exchange notes redeemed, plus a “make-whole premium” described in this prospectus plus accrued and unpaid interest, if any. See “Description of Exchange Notes—Optional Redemption.” | |

Offer to Repurchase Following Change of Control | Upon a change of control, if we do not redeem the exchange notes, each holder of exchange notes will be entitled to require us to purchase all or a portion of its exchange notes at a purchase price equal to 101% of the principal amount thereof, plus accrued and unpaid interest, if any. Our ability to purchase the exchange notes upon a change of control will be limited by the terms of our then outstanding debt agreements. See “Description of Exchange Notes—Repurchase at the Option of Holders—Change of Control.” | |

Offer to Repurchase Following Certain Asset Sales | If we or our restricted subsidiaries engage in certain asset sales, we may either invest the net cash proceeds from such event in our business or prepay our senior debt, each within a certain period of time of such event, or we must make an offer to purchase a principal amount of the exchange notes equal to the excess net cash proceeds, with certain exceptions. The purchase price of the exchange notes will be 100% of their principal amount, plus accrued and unpaid interest, if any. See “Description of Exchange Notes— Repurchase at the Option of Holders—Asset Sales.” | |

Certain Covenants | The indenture governing the exchange notes, among other things, limits our ability and the ability of our restricted subsidiaries to: | |

• sell assets; | ||

• declare dividends or make distributions on our equity interests or purchase or redeem our equity interests; | ||

• make investments or other specified restricted payments; | ||

• incur or guarantee additional indebtedness and issue disqualified or preferred equity; | ||

• create liens; | ||

• enter into agreements that restrict the ability of our restricted subsidiaries to pay dividends, make intercompany loans or transfer assets to us; | ||

• effect a merger, consolidation or sale of all or substantially all of our assets; | ||

9

Table of Contents

• enter into transactions with affiliates; and | ||

• designate subsidiaries as unrestricted subsidiaries. | ||

| These and other covenants are subject to important exceptions and qualifications as described under “Description of Exchange Notes—Certain Covenants.” | ||

Covenant Suspension/Termination | If the exchange notes receive an investment grade rating by either Standard & Poor’s Ratings Services (S&P) or Moody’s Investors Service, Inc. (Moody’s), our obligation to comply with certain of the covenants in the indenture will be suspended, and if the exchange notes receive an investment grade rating by both S&P and Moody’s, then such obligations will terminate as described under “Description of Exchange Notes—Certain Covenants—Covenant Suspension and Termination.” | |

No Prior Market | The exchange notes will generally be freely transferable but are also new securities for which there initially will not be a market. We do not intend to apply for a listing of the exchange notes on any securities exchange or for their inclusion on any automated dealer quotation system. Accordingly, we cannot assure you as to the development or liquidity of any market for the exchange notes. | |

Book-Entry Form | The exchange notes will be issued in book-entry form and will be represented by one or more global securities registered in the name of Cede & Co., as nominee for The Depository Trust Company, or DTC. Beneficial interests in the exchange notes will be evidenced by, and transfers will be effected only through, records maintained by DTC participants. | |

Form and Denomination | Exchange notes will be issuable in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. | |

Risk Factors | See “Risk Factors” and the other information in this prospectus for a discussion of the factors you should carefully consider before deciding to participate in the exchange offer. | |

10

Table of Contents

SUMMARY HISTORICAL FINANCIAL DATA

The following tables set forth the summary historical financial data of COO and its predecessors. The summary historical financial data for each of the three-month periods ended March 31, 2013 and 2012 are derived from the unaudited condensed consolidated financial statements included elsewhere in this prospectus. The summary historical financial data for each of the years ended December 31, 2012, 2011 and 2010 are derived from the audited consolidated financial statements included elsewhere in this prospectus. Our historical consolidated financial statements for periods and as of dates prior to our October 25, 2011 reorganization were prepared on a “carve-out” basis from Chesapeake and are intended to represent the financial results of Chesapeake’s oilfield services operations for those periods. The summary historical financial data is not necessarily indicative of results to be expected in future periods. Our summary historical financial data should be read together with the historical consolidated financial statements and related notes thereto and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” each included elsewhere in this prospectus.

The financial statements of COF have not been presented in this prospectus as it has had no business transactions or activities to date and has no (or nominal) assets or liabilities.

| Three Months Ended March 31, | Years Ended December 31, | |||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | 2010 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Income Statement Data: | ||||||||||||||||||||

Revenues, including revenues from affiliates | $ | 543,887 | $ | 446,881 | $ | 1,920,022 | $ | 1,303,496 | $ | 815,756 | ||||||||||

Operating costs | 415,049 | 326,914 | 1,390,786 | 986,239 | 667,927 | |||||||||||||||

Depreciation and amortization | 70,112 | 53,673 | 231,322 | 175,790 | 103,339 | |||||||||||||||

General and administrative, including expenses from affiliates | 20,491 | 15,631 | 66,360 | 37,074 | 25,312 | |||||||||||||||

Losses (gains) on sales of property and equipment | 374 | (1,221 | ) | 2,025 | (3,571 | ) | (854 | ) | ||||||||||||

Impairments and other(1) | 24 | 1,038 | 60,710 | 2,729 | 9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating income | 37,837 | 50,846 | 168,819 | 105,235 | 20,023 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Interest expense, including expenses from affiliates | (14,010 | ) | (12,616 | ) | (53,548 | ) | (48,802 | ) | (38,795 | ) | ||||||||||

Losses from equity investees | (119 | ) | (163 | ) | (361 | ) | — | (2,243 | ) | |||||||||||

Other income (expense) | 524 | 184 | 1,543 | (2,464 | ) | 211 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total other expense | (13,605 | ) | (12,595 | ) | (52,366 | ) | (51,266 | ) | (40,827 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income (loss) before income taxes | 24,232 | 38,251 | 116,453 | 53,969 | (20,804 | ) | ||||||||||||||

Income tax expense (benefit) | 9,999 | 15,415 | 46,877 | 26,279 | (4,195 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | 14,233 | 22,836 | 69,576 | 27,690 | (16,609 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Less: Net Loss Attributable to Noncontrolling Interest | — | — | — | (154 | ) | (639 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net Income (Loss) Attributable to Chesapeake Oilfield Operating, L.L.C. | $ | 14,233 | $ | 22,836 | $ | 69,576 | $ | 27,844 | $ | (15,970 | ) | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Other Financial Data: | ||||||||||||||||||||

Adjusted EBITDA(2)(unaudited) | $ | 108,752 | $ | 104,357 | $ | 439,203 | $ | 277,719 | $ | 120,485 | ||||||||||

Capital expenditures (including acquisitions) | $ | 92,496 | $ | 155,184 | $ | 622,825 | $ | 752,715 | $ | 273,154 | ||||||||||

11

Table of Contents

| As of March 31, 2013 | ||||

| (in thousands) | ||||

| (unaudited) | ||||

Balance Sheet Data: | ||||

Cash | $ | 1,745 | ||

Total property and equipment, net | $ | 1,576,155 | ||

Total assets | $ | 2,196,597 | ||

Total long-term debt | $ | 1,057,600 | ||

Total equity | $ | 598,089 | ||

| (1) | We recorded impairments of long-lived assets and lease termination costs in the amount of $35.8 million and $24.9 million, respectively, for the year ended December 31, 2012. |

| (2) | “Adjusted EBITDA” is a non-GAAP financial measure that we define as net income before interest, taxes, depreciation and amortization, as further adjusted to add back gain or loss on sale of property and equipment and impairments. “Adjusted EBITDA,” as used and defined by us, may not be comparable to similarly titled measures employed by other companies and is not a measure of performance calculated in accordance with GAAP. Adjusted EBITDA should not be considered in isolation or as a substitute for operating income, net income or loss, cash flows provided by operating, investing and financing activities, or other income or cash flow statement data prepared in accordance with GAAP. However, our management believes Adjusted EBITDA may be useful to an investor in evaluating our operating performance because this measure: |

| • | is widely used by investors in the oilfield services industry to measure a company’s operating performance without regard to items excluded from the calculation of such measure, which can vary substantially from company to company depending upon accounting methods, book value of assets, capital structure and the method by which assets were acquired, among other factors; |

| • | is a financial measurement that is used by rating agencies, lenders and other parties to evaluate our creditworthiness; and |

| • | is used by our management for various purposes, including as a measure of performance of our operating entities and as a basis for strategic planning and forecasting. |

There are significant limitations to using Adjusted EBITDA as a measure of performance, including the inability to analyze the effect of certain recurring and non-recurring items that materially affect our net income or loss, and the lack of comparability of results of operations of different companies.

The following table presents a reconciliation of the non-GAAP financial measure of Adjusted EBITDA to the GAAP financial measure of net income (loss):

| Three Months Ended March 31, | Years Ended December 31, | |||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | 2010 | ||||||||||||||||

(Unaudited) | ||||||||||||||||||||

(in thousands) | ||||||||||||||||||||

Net income (loss) | $ | 14,233 | $ | 22,836 | $ | 69,576 | $ | 27,690 | $ | (16,609 | ) | |||||||||

Interest expense | 14,010 | 12,616 | 53,548 | 48,802 | 38,795 | |||||||||||||||

Income tax expense (benefit) | 9,999 | 15,415 | 46,877 | 26,279 | (4,195 | ) | ||||||||||||||

Depreciation and amortization | 70,112 | 53,673 | 231,322 | 175,790 | 103,339 | |||||||||||||||

Impairments | 24 | 1,038 | 35,855 | 2,729 | 9 | |||||||||||||||

Losses (gains) on sales of property and equipment | 374 | (1,221 | ) | 2,025 | (3,571 | ) | (854 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Adjusted EBITDA | $ | 108,752 | $ | 104,357 | $ | 439,203 | $ | 277,719 | $ | 120,485 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

12

Table of Contents

You should carefully consider the risk factors set forth below as well as the other information contained under “Forward-Looking Statements” and elsewhere in this prospectus before deciding to participate in the exchange offer. This prospectus contains forward-looking statements that involve risks and uncertainties. Any of the following risks could materially and adversely affect our business, financial condition, results of operations or cash flows. In such a case, you may lose all or part of your original investment.

Risks Relating to Our Business

We are dependent on Chesapeake for a substantial majority of our revenues. Therefore, we are indirectly subject to the business and financial risks of Chesapeake. We have no control over Chesapeake’s business decisions and operations, and Chesapeake is under no obligation to adopt a business strategy that favors us.

We have provided a substantial majority of all of our oilfield services to Chesapeake and its working interest partners. During the three months ended March 31, 2013 and for the years ended December 31, 2012, 2011 and 2010, Chesapeake and its working interest partners accounted for approximately 94%, 94%, 94% and 96% of our revenues, respectively, and we expect to derive a substantial majority of our revenues from Chesapeake and its working interest partners for the foreseeable future. If Chesapeake ceases to engage us on terms that are attractive to us, particularly after the expiration of our services agreement with it, our business, financial condition, results of operations and cash flows would be materially adversely affected. Accordingly, we are indirectly subject to the business and financial risks of Chesapeake, some of which are the following:

| • | the volatility of oil and natural gas prices, which could have a negative effect on the value of Chesapeake’s oil and natural gas properties, its drilling program, its ability to finance its operations and its willingness to allocate capital toward exploration and development activities; |

| • | the availability of capital on favorable terms to fund its exploration and development activities; |

| • | its discovery rate of new oil and natural gas reserves and the speed at which it develops such reserves; |

| • | its drilling and operating risks, including potential environmental liabilities; |

| • | pipeline, storage and other transportation capacity constraints and interruptions; and |

| • | adverse effects of governmental and environmental regulation. |

In particular, Chesapeake has historically pursued a strategy of making capital expenditures for land acquisition, drilling and completion of wells, and other activities in excess of its operating cash flows. To fund these expenditures, Chesapeake obtained capital from the debt and equity capital markets, oil and natural gas asset sales or joint ventures, counterparties in volumetric production payment transactions and other sources. Chesapeake has announced that it intends to fund 2013 capital expenditures from operating cash flows, borrowings under its bank credit facilities and, to the extent those sources are not sufficient, proceeds from asset sales and other financings. If Chesapeake is unable to consummate such asset sales or if they do not generate the proceeds that are anticipated, Chesapeake would be required to reduce its spending on drilling and completion activities, which would have a material adverse impact on our business, financial condition, results of operations and cash flows.

Our relationship with Chesapeake presents a number of additional risks to us. Please read “—Risks Relating to Our Relationship with Chesapeake.”

Demand for services in our industry is cyclical and depends on drilling and completion spending by Chesapeake and other E&P companies in the U.S., and the level of such activity is volatile.

Demand for services in our industry is cyclical, and we depend on Chesapeake’s and our other customers’ willingness to make capital and operating expenditures to explore for, develop and produce oil and natural gas in the U.S. Our customers’ willingness to undertake these activities depends largely upon prevailing industry conditions that are influenced by numerous factors over which we have no control, including:

| • | prices, and expectations about future prices, of oil and natural gas; |

13

Table of Contents

| • | domestic and foreign supply of and demand for oil and natural gas; |

| • | the cost of exploring for, developing, producing and delivering oil and natural gas; |

| • | available pipeline, storage and other transportation capacity; |

| • | lead times associated with acquiring equipment and products and availability of qualified personnel; |

| • | the expected rates of decline in production from existing and prospective wells; |

| • | the discovery rates of new oil and natural gas reserves; |

| • | federal, state and local regulation of hydraulic fracturing and other oilfield activities, including public pressure on governmental bodies and regulatory agencies to regulate our industry; |

| • | the availability of water resources and suitable proppants in sufficient quantities for use in hydraulic fracturing operations; |

| • | the availability, capacity and cost of disposal and recycling services for used hydraulic fracturing fluids; |

| • | political instability in oil and natural gas producing countries; |

| • | advances in exploration, development and production technologies or in technologies affecting energy consumption; |

| • | the price and availability of alternative fuels and energy sources; and |

| • | uncertainty in capital and commodities markets and the ability of oil and natural gas producers to raise equity capital and debt financing on favorable terms. |

Anticipated future prices for natural gas and crude oil are a primary factor affecting spending and drilling activity by E&P companies, including Chesapeake. Lower prices or volatility in prices for oil and natural gas typically decrease spending and drilling activity, which can cause rapid and material declines in demand for our services and in the prices we are able to charge for our services. Worldwide political, economic and military events as well as natural disasters and other factors beyond our control contribute to oil and natural gas price levels and volatility and are likely to continue to do so in the future.

Any prolonged substantial reduction in oil and natural gas prices would likely affect oil and natural gas production levels and, therefore, would affect demand for and prices of the services we provide. While we have a services agreement with Chesapeake providing for minimum utilization of certain of our services, that agreement provides that we will receive market rates for our services, and, consequently, the prices we are able to charge will fluctuate with market conditions. A material decline in oil and natural gas prices or drilling activity levels or sustained lower prices or activity levels could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Natural gas prices declined significantly in late 2011 and 2012 to the lowest level in recent years, and while prices have risen from their lows, they remain depressed. As a result of depressed natural gas prices, many E&P companies, including Chesapeake, have reduced drilling in plays characterized by higher concentrations of dry natural gas. Although many of these companies, including Chesapeake, have refocused their drilling activities on liquids-rich plays, an overall reduction in the demand for oilfield services could still occur, which would adversely affect the prices that we are able to charge, and the demand, for our services. Additionally, we may incur costs and have downtime as we redeploy equipment and personnel from dry natural gas plays to liquids-rich plays.

14

Table of Contents

Spending by E&P companies can also be impacted by conditions in the capital markets. Limitations on the availability of capital, or higher costs of capital, for financing expenditures may cause Chesapeake and other E&P companies to make additional reductions to capital budgets in the future even if oil prices remain at current levels or natural gas prices increase from current levels. Any such cuts in spending will curtail drilling and completion programs as well as discretionary spending on wellsite services, which may result in a reduction in the demand for our services, the rates we can charge and the utilization of our services. Moreover, reduced discovery rates of new oil and natural gas reserves, or a decrease in the development rate of reserves, in our market areas, whether due to increased governmental or environmental regulation, limitations on exploration and drilling activity or other factors, could also have a material adverse impact on our business, financial condition, results of operations and cash flows, even in a stronger oil and natural gas price environment.

Competition in our industry or increases in the supply of drilling rigs or hydraulic fracturing units could decrease the prices for our products and services and our revenues.

The market for oilfield services in which we operate is highly competitive. Contracts are traditionally awarded on the basis of competitive bids or direct negotiations with customers. The competitive environment has intensified as recent mergers among E&P companies have reduced the number of available customers. The fact that drilling rigs and other vehicles and pieces of oilfield services equipment are mobile and can be moved from one market to another in response to market conditions heightens the competition in the industry.

In addition, there has been a substantial increase in the supply of land drilling rigs and hydraulic fracturing fleets in the U.S. over the past several years. Such increase, whether through new construction or refurbishment of existing equipment, could have a material adverse impact on market prices and utilization rates of the service-provider. We do not have a fixed price contract with Chesapeake. Thus, if competition or other factors decrease market prices for the products and services we provide, Chesapeake could require us to lower the rates we charge to it. A reduction in the rates we charge would adversely affect our revenues and profitability. Such adverse effect on our revenues and profitability could be further aggravated by any downturn in oil and natural gas prices.

Shortages or increases in the costs of the equipment we use in our operations could adversely affect our operations in the future.

We generally do not have long term contracts in place that provide for the delivery of equipment, including, but not limited to, drill pipe, replacement parts and other equipment. We could experience delays in the delivery of the equipment that we have ordered and its placement into service due to factors that are beyond our control. New federal regulations regarding diesel engines, demand by other oilfield services companies and numerous other factors beyond our control could adversely affect our ability to procure equipment that we have not yet ordered or cause the prices of such equipment to increase. Price increases, delays in delivery and interruptions in supply may require us to increase capital and repair expenditures and incur higher operating costs. Each of these could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are dependent on a small number of suppliers for key raw materials and finished products.

We do not have long term contracts with third party suppliers of many of the raw materials and finished products that we use in large volumes in our operations, including, in the case of our hydraulic fracturing operations, proppants, acid, gels, including guar gum, chemicals and water, and fuels used in our equipment and vehicles. Especially during periods in which oilfield services are in high demand, the availability of raw materials and finished products used in our industry decreases and the price of such raw materials and finished products increases. We are dependent on a small number of suppliers for key raw materials and finished products. Our reliance on such suppliers could increase the difficulty of obtaining such raw materials and finished products in the event of shortage in our industry or cause us to pay higher prices to obtain such raw materials and finished products. Price increases, delays in delivery and interruptions in supply may require us to incur higher operating costs. Each of these could have a material adverse effect on our business, financial condition, results of operations and cash flows.

15

Table of Contents

The loss of key executives could adversely affect our ability to effectively operate and manage our business.

We are dependent upon the efforts and skills of our executives to operate and manage our business. We cannot assure you that we will be able to retain these employees, and the loss of the services of one or more of our key executives could increase our exposure to the other risks described in this “Risk Factors” section. We do not maintain key man insurance on any of our personnel.

Increased labor costs or the unavailability of skilled workers could hurt our operations.

We are dependent upon an available pool of skilled employees to maintain our business. We compete with other oilfield services businesses and other employers to attract and retain qualified personnel with the technical skills and experience required to provide the highest quality service. The demand for skilled workers is high and the supply is limited, and a shortage in the labor pool of skilled workers or other general inflationary pressures or changes in applicable laws and regulations could make it more difficult for us to attract and retain personnel and could require us to enhance our wage and benefits packages thereby increasing our operating costs.

Although our employees are not covered by a collective bargaining agreement, union organizational efforts could occur and, if successful, could increase our labor costs. A significant increase in the wages paid by competing employers or the unionization of groups of our employees could result in increases in the wage rates that we must pay. Likewise, laws and regulations to which we are subject, such as the Fair Labor Standards Act, which governs such matters as minimum wage, overtime and other working conditions, can increase our labor costs or subject us to liabilities to our employees. We cannot assure you that labor costs will not increase. Increases in our labor costs or unavailability of skilled workers could impair our capacity and diminish our profitability, having a material adverse effect on our business, financial condition, results of operations and cash flows.

Historically, our industry has experienced a high annual employee turnover rate. We believe that the high turnover rate is attributable to the nature of the work, which is physically demanding and performed outdoors, and to the volatility and cyclical nature of the oilfield services industry. As a result, workers may choose to pursue employment in fields that offer a more desirable work environment at wage rates that are competitive with ours. We cannot assure you that we will be able to recruit, train and retain an adequate number of workers to replace departing workers. The inability to maintain an adequate workforce could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We participate in a capital intensive industry. We may not be able to finance our operations or future acquisitions.

Our activities require substantial capital expenditures. In the past, we have relied on capital infusions by Chesapeake to meet our liquidity needs. We do not anticipate that Chesapeake will need to make these capital infusions to us in the future. However, if our cash flows from operating activities and borrowings under our revolving bank credit facility are not sufficient to fund our capital expenditures budget, we would be required to fund these expenditures through debt or equity or alternative financing plans, such as:

| • | refinancing or restructuring our debt; |

| • | selling assets; and/or |

| • | reducing or delaying acquisitions or capital investments, such as acquisitions of additional revenue-generating equipment and refurbishments of our rigs and related equipment. |

If debt and equity capital or alternative financing plans are not available on favorable terms or at all, we would be required to curtail our capital spending, and our ability to sustain or improve our profits may be adversely affected. Our ability to refinance or restructure our debt will depend on the condition of the capital markets and our and Chesapeake’s financial condition at such time, among other things. Any refinancing of our debt could be at higher interest rates and may require us to comply with more onerous covenants, which could further restrict our business operations. In addition, any failure to make payments of interest and principal on our outstanding indebtedness on a timely basis or to satisfy our liquidity needs would likely result in a reduction of our credit rating, which could harm our ability to incur additional indebtedness. Any failure to make payments under the operating subleases for our drilling rigs would result in a default under such sublease and could cause us to lose the use of the affected drilling rigs. The terms of existing or future debt instruments may restrict us from adopting some of these alternatives.

16

Table of Contents

Chesapeake has significant long-term indebtedness, and we could experience an increase in our borrowing costs or difficultly accessing, or an inability to access, the capital markets based on adverse developments affecting Chesapeake. See “—Risks Relating to Our Relationship with Chesapeake—Chesapeake’s level of indebtedness could adversely affect our business, as well as our credit ratings and profile.” Any of the foregoing could materially and adversely affect our business, financial condition, results of operations and cash flows.

Delays in obtaining permits by our customers for their operations could impair our business.

Our customers are required to obtain permits from one or more governmental agencies in order to perform drilling and/or completion activities. Such permits are typically required by state agencies but can also be required by federal and local governmental agencies. The requirements for such permits vary depending on the location where such drilling and completion activities will be conducted. As with all governmental permitting processes, there is a degree of uncertainty as to whether a permit will be granted, the time it will take for a permit to be issued and the conditions which may be imposed in connection with the granting of the permit. Certain regulatory authorities have delayed or suspended the issuance of permits while the potential environmental impacts associated with issuing such permits can be studied and appropriate mitigation measures evaluated. Permitting delays, an inability to obtain new permits or revocation of our or our customers’ current permits could cause a loss of revenue and could materially and adversely affect our business, financial condition, results of operations and cash flows.

Any future decreases in the rate at which oil or natural gas reserves are discovered or developed could decrease the demand for our services.

Reduced discovery rates of new oil and natural gas reserves, or a decrease in the development rate of reserves, in our market areas, whether due to increased governmental regulation, limitations on exploration and drilling activity or other factors, could have a material adverse impact on our business, financial condition, results of operations and cash flows even in a stronger oil and natural gas price environment.

Our business involves many hazards and operational risks, some of which may not be fully covered by insurance.

Our operations are subject to many hazards and risks, including the following:

| • | accidents resulting in serious bodily injury and the loss of life or property; |

| • | liabilities from accidents or damage by our fleet of trucks, rigs and other equipment; |

| • | pollution and other damage to the environment; |

| • | blow-outs, the uncontrolled flow of natural gas, oil or other well fluids into or through the environment, including onto the ground or into the atmosphere, surface waters or an underground formation; and |

| • | fires and explosions. |

If any of these hazards occur, they could result in suspension of operations, damage to or destruction of our equipment and the property of others, or injury or death to our personnel or third parties and could expose us to substantial liability or losses. The frequency and severity of such incidents will affect operating costs, insurability and relationships with customers, employees and regulators. In addition, these risks may be greater for us upon the acquisition of another company that has not allocated significant resources and management focus to safety and has a poor safety record.

We are not fully insured against all risks inherent in our business. For example, we do not have any business interruption/loss of income insurance that would provide coverage in the event of damage to any of our equipment or facilities. Although we are insured for environmental pollution resulting from environmental accidents that occur on a sudden and accidental basis, we may not be insured against all environmental accidents that might occur, some of which may result in toxic tort claims. If a significant accident or event occurs for which we are not adequately insured, it could adversely affect our business, financial condition, results of operations and cash flows. Furthermore, we may not be able to maintain or obtain insurance of the type and

17

Table of Contents

amount we desire at reasonable rates. As a result of market conditions, premiums and deductibles for certain of our insurance policies may substantially increase. In some instances, certain insurance could become unavailable or available only for reduced amounts of coverage. See “Business—Risk Management and Insurance.”

Federal and state legislative and regulatory initiatives relating to hydraulic fracturing could restrict or make our hydraulic fracturing operations more difficult and could increase our or Chesapeake’s operating costs.

Various federal legislative and regulatory initiatives have been undertaken which could result in additional requirements or restrictions being imposed on hydraulic fracturing operations. These regulations, if adopted, would establish additional levels of regulation at the federal level that could lead to operational delays and increased operating costs. At the same time, several states have adopted, and other states are considering adopting, regulations that could impose more stringent permitting, public disclosure, and/or well construction requirements on hydraulic fracturing operations. In addition to state laws, some local municipalities have adopted or are considering adopting land use restrictions, such as city ordinances, that may restrict or prohibit the performance of well drilling in general and/or hydraulic fracturing in particular. Additionally, the United States Environmental Protection Agency (EPA) has asserted federal regulatory authority over hydraulic fracturing activities involving diesel fuel (specifically, when diesel fuel is utilized in the stimulation fluid) under the Safe Drinking Water Act and is drafting guidance documents related to this newly asserted regulatory authority. There are also certain governmental reviews either underway or being proposed that focus on deep shale and other formation completion and production practices, including hydraulic fracturing. Depending on the outcome of these studies, federal and state legislatures and agencies may seek to further regulate such activities. In addition, certain environmental and other groups have suggested that additional federal, state and local laws and regulations may be needed to more closely regulate the hydraulic fracturing process. We are unable to predict whether the proposed changes in laws or regulations or any other governmental proposals or responses will ultimately occur, and accordingly, we are unable to assess the potential financial or operational impact they may have on our business.

The adoption of any future federal, state or local laws or implementing regulations imposing reporting obligations on, or limiting or banning, the hydraulic fracturing process could make it more difficult to complete natural gas and oil wells and could have a material adverse impact on our business, financial condition, results of operations and cash flows.

We are subject to federal, state and local laws and regulations regarding issues of health, safety, climate change and protection of the environment. Under these laws and regulations, we may become liable for penalties, damages or costs of remediation or other corrective measures. Any changes in laws or government regulations could increase our costs of doing business.

Our operations are subject to stringent federal, state and local laws and regulations relating to, among other things, protection of natural resources, wetlands, endangered species, the environment, health and safety, waste management, waste disposal and transportation of waste and other materials. Our operations pose risks of environmental liability, including leakage from our operations to surface or subsurface soils, surface water or groundwater. Some environmental laws and regulations may impose strict liability, joint and several liability, or both. Therefore, in some situations, we could be exposed to liability as a result of our conduct that was lawful at the time it occurred or the conduct of, or conditions caused by, third parties without regard to whether we caused or contributed to the conditions. Actions arising under these laws and regulations could result in the shutdown of our operations, fines and penalties, expenditures for remediation or other corrective measures, and claims for liability for property damage, exposure to hazardous materials, exposure to hazardous waste or personal injuries. Sanctions for noncompliance with applicable environmental laws and regulations also may include the assessment of administrative, civil or criminal penalties, revocation of permits, temporary or permanent cessation of operations in a particular location and issuance of corrective action orders. Such claims or sanctions and related costs could cause us to incur substantial costs or losses and could have a material adverse effect on our business, financial condition, results of operations and cash flows. Additionally, an increase in regulatory requirements on oil and gas exploration and completion activities could significantly delay or interrupt our operations.

Various state governments and regional organizations are considering enacting new legislation and promulgating new regulations governing or restricting the emission of greenhouse gases from stationary sources such as our equipment and operations.

18

Table of Contents

At the federal level, the EPA has already made findings and issued regulations that require us to establish and report an inventory of greenhouse gas emissions. Legislative and regulatory proposals for restricting greenhouse gas emissions or otherwise addressing climate change could require us to incur additional operating costs and could adversely affect demand for the oil and natural gas that we drill for and help produce. The potential increase in our operating costs could include new or increased costs to obtain permits, operate and maintain our equipment and facilities, install new emission controls on our equipment and facilities, acquire allowances to authorize our greenhouse gas emissions, pay taxes related to our greenhouse gas emissions and administer and manage a greenhouse gas emissions program. Even without federal legislation or regulation of greenhouse gas emissions, states may pursue the issue either directly or indirectly. Restrictions on emissions of methane or carbon dioxide that may be imposed in various states could adversely affect the oil and natural gas industry. Moreover, incentives to conserve energy or use alternative energy sources could reduce demand for oil and natural gas.

The EPA regulates air emissions from certain off-road diesel engines that are used by us to power equipment in the field. Under these Tier IV regulations, we are required to retrofit or retire certain engines, and we are limited in the number of non-compliant off-road diesel engines we can purchase. Tier IV engines are costlier and are not yet widely available. Until Tier IV-compliant engines that meet our needs are available, these regulations could limit our ability to acquire a sufficient number of engines to expand our fleet and to replace existing engines as they are taken out of service.

Laws protecting the environment generally have become more stringent over time and we expect them to continue to do so, which could lead to material increases in our costs for future environmental compliance and remediation.

Chesapeake has the option to terminate our services agreement if Chesapeake no longer controls us.

Chesapeake has the option to terminate our services agreement in the event it no longer controls us. Under our services agreement with Chesapeake, Chesapeake has guaranteed certain utilization levels for our drilling rigs and hydraulic fracturing fleets. If Chesapeake no longer controls us, it may no longer be required to utilize our services and it will have less incentive to do so, which could have a material adverse impact on our business, financial condition, results of operations and cash flows.

Severe weather could have a material adverse effect on our business.

Adverse weather can directly impede our operations. Repercussions of severe weather conditions may include:

| • | curtailment of services; |

| • | weather-related damage to facilities and equipment, resulting in suspension of operations; |

| • | inability to deliver equipment, personnel and products to job sites in accordance with contract schedules; and |

| • | loss of productivity. |

These constraints could delay our operations and materially increase our operating and capital costs. Unusually warm winters or cool summers may also adversely affect the demand for our services by decreasing the demand for natural gas. Our operations in semi-arid regions can be affected by droughts and other lack of access to water used in our operations, especially with respect to our hydraulic fracturing operations.

We may not be successful in identifying, making and integrating acquisitions.

A component of our business strategy is to make selective acquisitions that will strengthen our core services or presence in selected markets. The success of this strategy will depend, among other things, on our ability to identify suitable acquisition candidates, to negotiate acceptable financial and other terms, to timely and successfully integrate acquired businesses or assets and to retain the key personnel and the customer base of acquired businesses. Any future acquisitions could present a number of risks, including but not limited to:

19

Table of Contents

| • | incorrect assumptions regarding the future results of acquired operations or assets or expected cost reductions or other synergies expected to be realized as a result of acquiring operations or assets; |