January 8, 2013

VIA EDGAR AND OVERNIGHT DELIVERY

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, DC 20549

Attention: Ms. Amanda Ravitz

| Re: | The ExOne Company (formerly The Ex One Company, LLC) |

Registration Statement on Form S-1

Filed November 13, 2012

CIK No. 0001561627

Dear Ms. Ravitz:

This letter is being furnished on behalf of The ExOne Company (formerly The Ex One Company, LLC) (the “Company”) in response to comments received from the staff of the Division of Corporation Finance (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) by letter dated January 4, 2013 to Mr. John Irvin, Chief Financial Officer of the Company, with respect to Amendment No. 1 to the Company’s Registration Statement on Form S-1 (CIK No. 0001561627) which was filed confidentially with the Commission pursuant to the Jumpstart Our Business Startups Act initially on November 13, 2012 ( the “Amendment”).

The text of the Staff’s comments has been included in this letter in bold and italics for your convenience, and we have numbered the paragraphs to correspond to the numbers in the Staff’s letter. For your convenience, we have also set forth the Company’s response to each of the numbered comments immediately below each numbered comment.

In addition, on behalf of the Company, we are today filing publicly on the EDGAR system a Registration Statement on Form S-1 (the “Registration Statement”). The Registration Statement has been drafted to reflect both the Company’s responses to the comments from the Staff and certain updating and conforming changes. All page numbers in the responses below refer to the Registration Statement, except as otherwise noted. We are delivering by messenger a courtesy package, which includes four copies of the Registration Statement, two of which are marked to show changes from the Amendment.

Cover Page

| 1. | With a view toward revised disclosure, please tell us the percentage of your revenue you generate from each of the industries identified on the bottom of your gatefold graphics following the cover page. |

Response:Revenues for 2012 derived from the industries identified were as follows: aerospace—17%; automotive—34%; heavy equipment—21%; and energy/oil/gas—7%. Refer to page 15 of the Registration Statement for our revised risk factor disclosure.

Prospectus Summary, page 1

| 2. | Please revise your summary to disclose (1) that you will use $9.6 million of the proceeds to repay indebtedness to an entity controlled by your CEO and (2) the recent covenant breach regarding your bank line of credit. |

Response: The Company has revised the summary as requested. Please see pages 8, 10 and 11 of the Registration Statement.

| 3. | Please expand your response to prior comment 4 to address the additional time required for producing metal parts discussed on page 71 of the Wohlers Report that you cite. Also, revise your summary to clarify the extent to which other companies can currently print using the materials you identify on page 1, as indicated in your response. In this regard, we note the list of competitors on page 2 of the Science and Technology Policy Institute report that you cite. Further, please reconcile your disclosure regarding your ability to print in stainless steel with page 95 of the Wohlers Report, which indicates that you are currently printing in a steel-bronze composite. Refer to prior comment 7. |

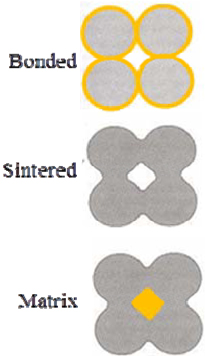

Response: In 3D printing, materials are printed as bonded materials. ExOne uses subsequent thermal processing steps for some materials to produce either sintered or sintered/matrix materials. See the figure below for a visual reference for combining particles in this way. If ExOne is seeking full density, it uses an infiltrant to create a matrix material. It is anticipated that the industrial market for bonded or sintered materials is relatively low. The matrix material has a material skeleton, composed of the primary matrix and then another material as an infiltrant.

Within the field of competitors, we have tried to make distinctions between the various processes in the additive manufacturing (“AM”) world. The fact that a company participates in AM, even with a common set of material capabilities, does not make it a competitor. There are no other binder jetting companies that we are aware of that produce metal parts, and certainly not for industrial application. The only partially competitive process, although much slower than binder jetting, is powder bed fusion. There we compete with EOS and Arcam, both of whom have a full range of materials available, including the metal material suite delivered by ExOne. Our specific statement in prior response 4 is that“The 3D printing process or technology it uses (printing utilizing chemical binding agent as opposed to other applications) and the printing materials in which it prints (industrial qualified materials for printing including silica sand, ceramics, stainless steel bronze and glass) distinguishes the Company from its competitors.” We believe that it is the combination of materials and speed which creates our competitive advantage.

Relative to the question of “printing in stainless,” the print media that we use for stainless applications is pure stainless powder. The resultant printed piece is, in fact, stainless steel. As noted above, in the process of sintering we often create matrix materials to raise the material density properties for some applications. In those cases, we may infiltrate with bronze, thus creating a stainless/bronze composite. As such, the printing is done in stainless steel with some parts finished as stainless steel only, depending on the application. Others are infiltrated with bronze during heat treatment, creating the steel/bronze composite noted in the Wohlers Report.

| 4. | Please expand your response to prior comment 5 to tell us the specific “business volume” you have with each of the customers identified and whether there are other customers not identified with whom you have similar business volume. Please note that you should not identify customers because they are “recognizable to potential investors.” Accordingly, please revise your list to identify only those customers with whom you have a significant business volume, quantifying the volume, or tell us why you continue to believe your present list should be retained. |

Response: The Company has developed a quantitative list of significant customers using historical revenues. The list is comprised of customers that have purchased a machine and/or experienced significant volume using our Production Service Centers (PSCs) for 3D printed product. Each of the customers listed share three common characteristics:

| 1. | They are active customers and are part of our top 30 industrial customers in terms of historical revenues since 2010; |

| 2. | They are in our top 10 customers associated with our target industries (aerospace, automotive, heavy equipment and energy/oil/gas); |

| 3. | The Company has explicit permission from the customer to use their name publicly. |

The Company notes that it has certain customers meeting the criteria above that are not listed in the Registration Statement. For these customers, the Company does not have explicit permission to use their name publicly. Based on the criteria noted above, the Company has revised its customer listing on page 75 of the Registration Statement.

We have modified the list of customers to some extent in response to your comment. However, we believe that the list of our customers serves a valid disclosure purpose beyond being a listing of our historical sources of revenue. Because 3D printing is a new technology and there are several other companies participating in the industry, we are making the point to investors that we are focused on selling into the industrial products market. We want to provide some way for investors to judge that the industrial products market has shown a willingness to adopt our technology and products. We believe that investors will be interested to know not only which customers are our most significant in terms of historical revenues, but also whether any sophisticated industrial companies have purchased our products.

The customers we named are sophisticated companies with well-known, experienced engineering departments which are fully capable of evaluating the usefulness of our products to their business. We believe investors, who are not usually in a position to independently evaluate new industrial technology, would like to know whether or not several industrial companies with sophisticated engineering departments have accepted our technology sufficiently to purchase our products.

Liquidity and Capital Resources, page 46

| 5. | Please disclose the steps you are taking to cure the lack of compliance with the covenant discussed in Note (A) on page 46 and the impact of the breach, if any, on (1) your current loan arrangements and (2) your ability to obtain additional financing. In addition, tell us what consideration you have given to adding risk factor disclosure. |

Response: Based on the Staff’s comment, we have revised pages 54 and 57 of the Registration Statement to disclose our expected remedy regarding lack of compliance with a covenant governing our German line of credit facility. Consistent with the expanded disclosure included on the aforementioned pages, we wish to inform the Staff that the German line of credit facility does not have any cross default or other related impacts on other existing lending agreements, and we do not expect the noncompliance to impact our future financing capabilities. We further note that our principal sources of liquidity are existing cash and loans from our majority stockholder, neither of which has been impacted by our noncompliance.

With respect to our risk factor disclosure considerations, we respectfully direct the Staff to our revised disclosure on page 15 of the Registration Statement.

Business, page 52

| 6. | Please reconcile your response to prior comment 23 regarding the lack of quality issues with the discussion of additive manufacturing part strength in Part V of the Atlantic Council Strategic Foresight Report you cite in your response to prior comment 4. Also, please address the manufacturing speed issues discussed in the same section of the report. |

Response: We have re-examined the response letter, including the response to prior comment 23, prior comment 4 and Part V of the Atlantic Council Strategic Foresight Report (ACSFR). We believe that the distinction that is important is between the notion of “quality issues,” as opposed to the notion of “fitness for use”. Industrial products, by nature, have explicit specifications embedded within them. A quality issue occurs when the material or product fails to meet the express specification. A product can meet specification, and therefore, be a quality product, yet not be fit for use in some applications.

The reference in the ACSFR generally discusses AM as a field of manufacturing, and specifically cites polymers as materials that are not well characterized and are weaker than their traditionally manufactured counterparts. We understand this general statement and agree that it may be true as a broad statement across AM. Many companies that

struggle with this issue do not sell in industrial markets. We do not print in polymers. A specific strength of ExOne is the investment that we have made to ensure that we do not face the problems cited in ACSFR. Through EXMAL, we actively certify materials for use. We gather the specifications required by our customers, and we examine our ability to meet those specifications. If we cannot meet the material specification required by a customer, we do not quote or sell for that application. Thus, we do not have quality problems, in the sense that we understand the specification required by our customer and we have confidence in meeting that specification. If our product is not “fit for use,” we do not quote or sell for that application.

Relative to print speeds, the ACSFR specifically states that, on average, AM processes are capable of creating a 1.5 inch cube in an hour, and this is cited as a limitation in competing with traditional manufacturing methods. ExOne, unlike many AM processes, intends to compete with traditional processes. In our newest entry into metal printing, the FLEX platform, we are printing 111 cubic inches per hour, a factor of 74 times faster than the average cited. In sand printing, on our MAX platform, we are printing an average output of 2,582 cubic inches per hour, a factor of more than 1,700 times faster than the average cited.

Customers, page 66

| 7. | Please expand your response to prior comment 24 to clarify your dependence on a limited number of customers implied by your disclosure in Note 17 on page F-55. |

Response: The Company has expanded its response to prior comment 24 as follows:

During the nine months ended September 30, 2011 and 2012 and the twelve months ended December 31, 2010 and 2011, the Company conducted a significant portion of its business with a limited number of customers. The Company’s top five customers represented approximately 46% and 42% of total revenue for the nine months ended September 30, 2011 and 2012, respectively, and approximately 43% and 47% of total revenue in 2010 and 2011, respectively. These customers primarily purchased 3D printing machines. Sales of 3D printed parts and consumables tend to be from repeat customers that may utilize the capability of our PSCs for three months or longer. Sales of 3D printing machines are low volume and generate significant revenue but the same customers do not necessarily buy machines in each period. Timing of customer purchases is dependent on the customer’s capital budgeting cycle, which may vary from period to period. The nature of the revenue from 3D printing machines, as described above does not leave us dependent upon a single or a limited number of customers. Rather, the timing of the sales can have a material effect on period to period financial results.

In addition, the Company has made revisions to its disclosure on pages 2, 62 and 80 of the Registration Statement.

Certain Relationships and Related Party Transactions, page 75

| 8. | Please provide us your analysis of how you determined the equipment purchaser identified on page F-32 is not a related party as defined in Regulation S-K Item 404, citing the relevant facts. |

Response: For financial reporting purposes, the equipment purchaser (a limited partnership) is identified as a related party because members of such limited partnership also participate in entities that have some non-voting, equity ownership. The equipment purchaser to which this Comment refers is not a related party as defined in the Instruction to Item 404(a) of Regulation S-K. That Instruction states that Item 404(a) applies to any person who is a director or executive officer of the Company, a nominee for director, or an individual who is an immediate family member of a director, executive officer or a nominee for directors; or any person who should be named pursuant to Item 403(a) of Regulation S-K, i.e., a person who owns equity securities with more than 5% or more of the voting power of the Company’s equity securities, or an immediate family member of such a person. The equipment purchaser is a limited partnership which is ultimately owned by two individuals neither of whom is a director or executive officer of the Company or a nominee for director or an immediate family member of any of those people or the owner of equity securities of the Company holding 5% or more of the voting power or an immediate family member of such a person.

Schedule

As a separate matter, we wish to confirm to the Staff that we still plan to commence our road show in late January 2013. We would appreciate it if the Staff would keep this schedule in mind when reviewing the Company’s filings. Thank you.

Very truly yours,

Warren J. Archer

| cc: | Mr. Louis Rambo |

Ms. Julie Sherman

Mr. Gary Todd

Mr. John Irvin