Table of Contents

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON JANUARY 9, 2014

REGISTRATION NO. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TRI POINTE HOMES, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 1531 | 27-3201111 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

19520 Jamboree Road, Suite 200

Irvine, California 92612

(949) 478-8600

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Douglas F. Bauer

Chief Executive Officer

TRI Pointe Homes, Inc.

19520 Jamboree Road, Suite 200

Irvine, California 92612

(949) 478-8600

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Andrew J. Pitts, Esq. D. Scott Bennett, Esq. Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, New York 10019 (212) 474-1000 | Keith P. Bishop, Esq. Allen Matkins Leck Gamble Mallory & Natsis LLP 1900 Main Street, Fifth Floor Irvine, California 92614 (949) 553-1313 | Michael E. Flynn, Esq. Brian J. Lane, Esq. Gibson, Dunn & Crutcher LLP 3161 Michelson Drive Irvine, California 92612 (949) 451-4054 |

Approximate date of commencement of proposed sale to the public: As soon as practicable on or after the effective date of this registration statement and after all other conditions to the completion of the exchange offer and merger described herein have been satisfied or waived.

If the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

| ||||||||

| ||||||||

Title of each class of securities to be registered | Amount to be registered(1)(2) | Proposed maximum offering price per unit(3) | Proposed maximum aggregate offering price(3) | Amount of registration fee(3) | ||||

Common stock, $0.01 par value per share | 129,700,000 | $18.65 | $2,418,905,000.00 | $311,554.96 | ||||

| ||||||||

| ||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, as amended, this registration statement also covers an indeterminate number of additional shares common stock of TRI Pointe Homes, Inc., par value $0.01 per share, as may be issuable as a result of stock splits, stock dividends or similar transactions. |

| (2) | Represents the estimated total number of shares of common stock of TRI Pointe Homes, Inc. which will be issuable in connection with the transactions contemplated by the Transaction Agreement, dated as of November 3, 2013, by and among TRI Pointe Homes, Inc., Weyerhaeuser Company, Weyerhaeuser Real Estate Company and Topaz Acquisition, Inc., as described in the Prospectus-Offer to Exchange filed as part of this registration statement. |

| (3) | Calculated pursuant to Rule 457(c) and Rule 457(f) under the Securities Act of 1933, as amended, based on the average of the high and low prices of shares of common stock of TRI Pointe Homes, Inc. as reported on the New York Stock Exchange on January 8, 2014. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

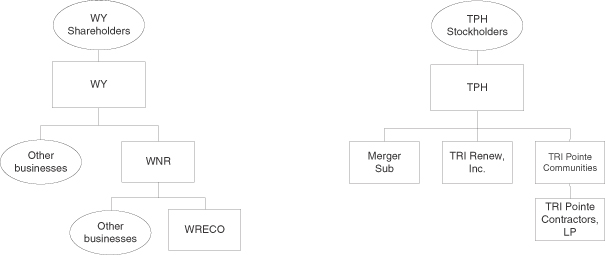

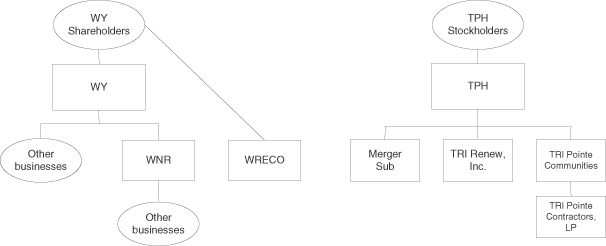

TRI Pointe Homes, Inc. (“TRI Pointe”) is filing this registration statement on Form S-4 (Reg. No. 333- ) to register shares of its common stock, par value $0.01 per share, which will be issued in connection with the merger (the “Merger”) of Topaz Acquisition, Inc. (“Merger Sub”), which is a wholly owned subsidiary of TRI Pointe, with and into Weyerhaeuser Real Estate Company (“WRECO”), which is an indirect, wholly owned subsidiary of Weyerhaeuser Company (“Weyerhaeuser”), with WRECO surviving the Merger and becoming a wholly owned subsidiary of TRI Pointe. In the Merger, the WRECO common shares will be immediately converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share. Prior to the consummation of the Merger, Weyerhaeuser will cause certain assets relating to Weyerhaeuser’s real estate business to be transferred to, and certain liabilities relating to Weyerhaeuser’s real estate business to be assumed by, WRECO and its subsidiaries. Weyerhaeuser will also cause certain assets of WRECO and its subsidiaries that will be excluded from the Transactions (as defined herein) to be transferred to, and certain liabilities of WRECO and its subsidiaries that will be excluded from the Transactions to be assumed by, Weyerhaeuser and its subsidiaries (other than WRECO and its subsidiaries). Weyerhaeuser NR Company (“WNR”), a wholly owned subsidiary of Weyerhaeuser, will receive cash proceeds of approximately $739 million from new debt financing to be incurred by WRECO upon consummation of the Transactions, which cash will be retained by Weyerhaeuser and its subsidiaries (other than WRECO and its subsidiaries). WNR may also receive a cash payment of the Adjustment Amount (as defined herein), if the Adjustment Amount is payable by TRI Pointe, as described in this registration statement. TRI Pointe will file a proxy statement that relates to the annual meeting of TRI Pointe stockholders to approve, among other proposals, the issuance of shares of TRI Pointe common stock in the Merger. In addition, WRECO will file a registration statement on Form S-4 and Form S-1 (Reg. No. 333- ) to register its common shares (which will have a par value of $0.04 per share after the consummation of the WRECO Stock Split described in this registration statement), which common shares will be distributed to Weyerhaeuser shareholders pursuant to a spin-off or a split-off in connection with the Merger.

Based on market conditions prior to the consummation of the Transactions, Weyerhaeuser will determine whether the WRECO common shares will be distributed to Weyerhaeuser’s shareholders in a spin-off or a split-off. Weyerhaeuser will determine which approach it will take prior to the consummation of the Transactions and no decision has been made at this time.In a spin-off, all Weyerhaeuser shareholders would receive a pro rata number of WRECO common shares. In a split-off, Weyerhaeuser would offer its shareholders the option to exchange their Weyerhaeuser common shares for WRECO common shares in an exchange offer, which WRECO common shares would immediately be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share in the Merger, resulting in a reduction in Weyerhaeuser’s outstanding common shares. If the exchange offer is consummated but fewer than all of the issued and outstanding WRECO common shares are exchanged because this exchange offer is not fully subscribed, the remaining WRECO common shares owned by Weyerhaeuser will be distributed on a pro rata basis to Weyerhaeuser shareholders whose Weyerhaeuser common shares remain outstanding after the consummation of the exchange offer. WRECO is filing its registration statement under the assumption that the WRECO common shares will be distributed to Weyerhaeuser shareholders pursuant to a split-off. This registration statement also assumes, and TRI Pointe’s proxy statement will assume, that the WRECO common shares will be distributed to Weyerhaeuser shareholders pursuant to a split-off. Once a final decision is made regarding the manner of distribution of the shares, this registration statement on Form S-4, TRI Pointe’s proxy statement and WRECO’s registration statement on Form S-4 and Form S-1will be amended to reflect that decision, if necessary.As TRI Pointe is not yet eligible to incorporate by reference, “Appendix A: Description of TRI Pointe” is included in this registration statement. TRI Pointe expects to incorporate the information in Appendix A by reference in subsequent amendments.

Table of Contents

The information in this document may change. The exchange offer and issuance of securities being registered pursuant to the registration statement of which this document forms a part may not be completed until the registration statement is effective. This document is not an offer to sell these securities, and it is not soliciting an offer to buy these securities, in any state where such offer or sale is not permitted.

SUBJECT TO COMPLETION DATED JANUARY 9, 2014

PRELIMINARY PROSPECTUS—OFFER TO EXCHANGE

WEYERHAEUSER COMPANY

Offer to Exchange All Common Shares of

WEYERHAEUSER REAL ESTATE COMPANY

Which Are Owned by Weyerhaeuser Company

and Will Be Converted into the Right to Receive Shares of Common Stock of

TRI POINTE HOMES, INC.

for

Common Shares of Weyerhaeuser Company

Weyerhaeuser Company, a Washington corporation (“Weyerhaeuser”), is offering to exchange all issued and outstanding common shares (“WRECO common shares”) of Weyerhaeuser Real Estate Company, a Washington corporation (“WRECO”), for common shares of Weyerhaeuser (“Weyerhaeuser common shares”) that are validly tendered and not properly withdrawn. The number of Weyerhaeuser common shares that will be accepted if this exchange offer is completed will depend on the final exchange ratio and the number of Weyerhaeuser common shares tendered. The terms and conditions of this exchange offer are described in this document, which you should read carefully. None of Weyerhaeuser, WRECO, any of their respective directors or officers or any of their respective representatives makes any recommendation as to whether you should participate in this exchange offer. You must make your own decision after reading this document and consulting with your advisors.

Immediately following the consummation of this exchange offer, a special purpose merger subsidiary of TRI Pointe Homes, Inc., a Delaware corporation (“TRI Pointe”), named Topaz Acquisition, Inc., a Washington corporation (“Merger Sub”), will be merged with and into WRECO, with WRECO surviving the merger and becoming a wholly owned subsidiary of TRI Pointe (the “Merger”). In the Merger, each issued and outstanding WRECO common share will be converted into the right to receive 1.297 fully paid and non-assessable shares of common stock of TRI Pointe (“TRI Pointe common stock”). Accordingly, WRECO common shares will not be transferred to participants in this exchange offer; participants will instead receive shares of TRI Pointe common stock in the Merger. No trading market currently exists or will ever exist for WRECO common shares. You will not be able to trade the WRECO common shares before or after they are converted into the right to receive shares of TRI Pointe common stock in the Merger. There can be no assurance that shares of TRI Pointe common stock issued in the Merger will trade at the same prices at which shares of TRI Pointe common stock are traded prior to the Merger.

Weyerhaeuser will calculate the value of Weyerhaeuser common shares, WRECO common shares and shares of TRI Pointe common stock based on the simple arithmetic averages of the daily volume-weighted average prices (“VWAP”) of Weyerhaeuser common shares and TRI Pointe common stock on the New York Stock Exchange (“NYSE”) on each of the last three trading days (“Valuation Dates”) of the exchange offer period (not including the expiration date), as it may be voluntarily extended, but not including the last two trading days that are part of any Mandatory Extension (as described below) or any voluntary extension following a Mandatory Extension. Based on an expiration date of , 2014, the Valuation Dates are expected to be , 2014, , 2014 and , 2014. See “This Exchange Offer—Terms of this Exchange Offer”.

This exchange offer is designed to permit you to exchange your Weyerhaeuser common shares for a number of WRECO common shares that corresponds to a % discount to the equivalent amount of TRI Pointe common stock, calculated as set forth in this document. However, the exchange ratio is subject to an upper limit, as discussed in “This Exchange Offer—Upper Limit”. Subject to the upper limit, for each $1.00 of Weyerhaeuser common shares accepted in this exchange offer, you will ultimately receive $ of fully paid and non-assessable shares of TRI Pointe common stock as a result of this exchange offer and the Merger. This exchange offer does not provide for a minimum exchange ratio. See “This Exchange Offer—Terms of this Exchange Offer”. If the upper limit is in effect, then the exchange ratio will be fixed at the upper limit and this exchange offer will be automatically extended (a “Mandatory Extension”) until 8:00 a.m., New York City time, on the day after the second trading day following the last trading day prior to the originally contemplated expiration date to permit shareholders to tender or withdraw their Weyerhaeuser common shares during that period. IF THE UPPER LIMIT IS IN EFFECT, AND UNLESS YOU PROPERLY WITHDRAW YOUR SHARES, YOU WILL RECEIVE LESS THAN $ OF WRECO COMMON SHARES FOR EACH $1.00 OF WEYERHAEUSER COMMON SHARES THAT YOU TENDER, AND YOU COULD RECEIVE MUCH LESS.

The indicative exchange ratio that would have been in effect following the official close of trading on the NYSE on , (the last trading day before the date of this document), based on the daily VWAPs of Weyerhaeuser common shares and TRI Pointe common stock on , 2014, , 2014 and , 2014, would have provided for WRECO common shares (which will be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock per WRECO common share in the Merger) to be exchanged for every Weyerhaeuser common share accepted. The value of WRECO common shares received and, following the consummation of the Merger, the value of TRI Pointe common stock received may not remain above the value of Weyerhaeuser common shares tendered following the expiration date of this exchange offer.

THIS EXCHANGE OFFER AND WITHDRAWAL RIGHTS WILL EXPIRE AT 12:00 MIDNIGHT, NEW YORK CITY TIME, ON , 2014, UNLESS THE OFFER IS EXTENDED OR TERMINATED. WEYERHAEUSER COMMON SHARES TENDERED PURSUANT TO THIS EXCHANGE OFFER MAY BE WITHDRAWN AT ANY TIME PRIOR TO THE EXPIRATION OF THIS EXCHANGE OFFER.

In reviewing this document, you should carefully consider therisk factors discussed beginning on page 44 of this document.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this Prospectus—Offer to Exchange is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this Prospectus—Offer to Exchange is , 2014.

Table of Contents

Unless there is a Mandatory Extension, the final exchange ratio used to determine the number of WRECO common shares that you will receive for each Weyerhaeuser common share accepted in this exchange offer will be announced by press release no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date. At that time, the final exchange ratio will be available at http://www. .com/ / and from the information agent at the toll-free number provided on the back cover of this document. Weyerhaeuser will announce whether the upper limit on the number of WRECO common shares (which will be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock per WRECO common share in the Merger) that can be received for each Weyerhaeuser common share tendered will be in effect at the expiration of the exchange offer period, at http://www. .com/ / and by press release, no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date. Throughout this exchange offer, indicative exchange ratios (calculated in the manner described in this document) will also be available on that website and from the information agent at the toll-free number provided on the back cover of this document.

This document provides information regarding Weyerhaeuser, WRECO, TRI Pointe and the Transactions (as defined below), in which Weyerhaeuser common shares may be exchanged for WRECO common shares, which will then be immediately converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share in the Merger, which shares of TRI Pointe common stock will then be distributed to participating Weyerhaeuser shareholders. Weyerhaeuser common shares are listed on the NYSE under the symbol “WY”. TRI Pointe common stock is listed on the NYSE under the symbol “TPH”. On , 2014, the last reported sale price of Weyerhaeuser common shares on the NYSE was $ , and the last reported sale price of TRI Pointe common stock on the NYSE was $ . The market prices of Weyerhaeuser common shares and of TRI Pointe common stock will fluctuate prior to the completion of this exchange offer and thereafter and may be higher or lower at the expiration date than the prices set forth above. No trading market currently exists for WRECO common shares, and no such market will exist in the future. WRECO has not applied for listing of its common shares on any exchange.

TRI Pointe has prepared this document under the assumption that the WRECO common shares will be distributed to Weyerhaeuser shareholders pursuant to a split-off.Based on market conditions prior to the consummation of the Transactions, Weyerhaeuser will determine whether the WRECO common shares will be distributed to Weyerhaeuser shareholders in a spin-off or a split-off and, once a final decision is made, this document will be amended to reflect that decision, if necessary.

If this exchange offer is consummated but fewer than all of the issued and outstanding WRECO common shares are exchanged because this exchange offer is not fully subscribed, the remaining WRECO common shares owned by Weyerhaeuser will be distributed pursuant to a pro rata distribution (a spin-off) also consummated on the closing date of the Merger. Any Weyerhaeuser shareholder who validly tenders (and does not properly withdraw) Weyerhaeuser common shares for WRECO common shares in this exchange offer will waive its rights with respect to those tendered Weyerhaeuser common shares to receive, and will forfeit any rights to, WRECO common shares distributed on a pro rata basis to Weyerhaeuser shareholders in the event this exchange offer is not fully subscribed. If this exchange offer is terminated by Weyerhaeuser without the exchange of shares, but the conditions for consummation of the Transactions have otherwise been satisfied, Weyerhaeuser intends to distribute all of the issued and outstanding WRECO common shares on a pro rata basis to Weyerhaeuser shareholders, with a record date to be announced by Weyerhaeuser. See “This Exchange Offer—Distribution of Any WRECO Common Shares Remaining after this Exchange Offer”.

Immediately following the consummation of this exchange offer, Merger Sub will be merged with and into WRECO, with WRECO surviving the Merger and becoming a wholly owned subsidiary of TRI Pointe. Each issued and outstanding WRECO common share will be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock. Immediately after the consummation of the Merger, the

i

Table of Contents

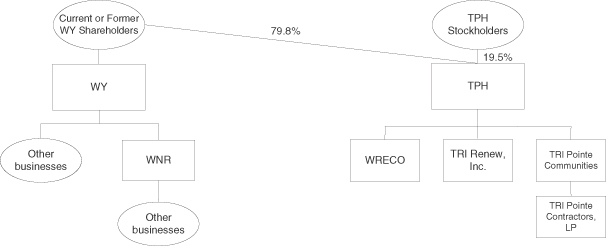

ownership of TRI Pointe common stock on a fully diluted basis is expected to be as follows: (i) WRECO common shares will have been converted into the right to receive, in the aggregate, approximately 79.8% of the then outstanding TRI Pointe common stock, (ii) the TRI Pointe common stock outstanding immediately prior to the consummation of the Merger will represent approximately 19.5% of the then outstanding TRI Pointe common stock and (iii) outstanding equity awards of WRECO and TRI Pointe employees will represent the remaining 0.7% of the then outstanding TRI Pointe common stock.

Weyerhaeuser’s obligation to exchange WRECO common shares for Weyerhaeuser common shares is subject to the conditions described in “This Exchange Offer—Conditions for Consummation of this Exchange Offer”, including the satisfaction of conditions to the Transactions, which include TRI Pointe stockholder approval of the issuance of TRI Pointe common stock in the Merger and other conditions.

ii

Table of Contents

| 1 | ||||

QUESTIONS AND ANSWERS ABOUT THIS EXCHANGE OFFER AND THE TRANSACTIONS | 5 | |||

| 20 | ||||

| 35 | ||||

| 44 | ||||

| 81 | ||||

| 83 | ||||

| 106 | ||||

| 113 | ||||

| 114 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR WRECO | 127 | |||

SELECTED HISTORICAL AND PRO FORMA FINANCIAL AND OPERATING DATA | 161 | |||

| 178 | ||||

| 181 | ||||

| 206 | ||||

| 229 | ||||

| 233 | ||||

| 236 | ||||

| 241 | ||||

COMPARISON OF RIGHTS OF WEYERHAEUSER SHAREHOLDERS AND TRI POINTE STOCKHOLDERS | 244 | |||

| 253 | ||||

| 253 | ||||

| 253 | ||||

WHERE YOU CAN FIND MORE INFORMATION; INCORPORATION BY REFERENCE | 254 | |||

| F-1 | ||||

| A-1 |

iii

Table of Contents

This document incorporates by reference important business and financial information about Weyerhaeuser from documents filed with the U.S. Securities and Exchange Commission (“SEC”) that have not been included in or delivered with this document. This information is available at the website that the SEC maintains athttp://www.sec.gov, as well as from other sources. See “Where You Can Find More Information; Incorporation By Reference”. You also may ask any questions about this exchange offer or request copies of the exchange offer documents from Weyerhaeuser, without charge, upon written or oral request to Weyerhaeuser’s information agent, , located at or at telephone number . In order to receive timely delivery of the documents, you must make your requests no later than , 2014.

Weyerhaeuser has provided all information contained or incorporated by reference in this document with respect to Weyerhaeuser and WRECO and their respective subsidiaries, the Real Estate Business and the terms and conditions of this exchange offer. TRI Pointe has provided all information contained in this document with respect to TRI Pointe and Merger Sub and their respective subsidiaries, as well as information with respect to TRI Pointe after the consummation of the Transactions. This document contains references to trademarks, trade names and service marks, including “Avanti”, “Camberley Homes”, “Everson Homes”, “Evoke”, “Maracay Homes”, “Pardee Homes”, “Quadrant Homes”, “Texas Casual Cottages”, “Trendmaker Homes”, “Urban Innovations” and “Winchester Homes”, that are owned by WRECO and its related entities.

This document is not an offer to sell or exchange and it is not a solicitation of an offer to buy any Weyerhaeuser common shares, WRECO common shares or TRI Pointe common stock in any jurisdiction in which the offer, sale or exchange is not permitted. Non-U.S. shareholders should consult their advisors in considering whether they may participate in this exchange offer in accordance with the laws of their home countries and, if they do participate, whether there are any restrictions or limitations on transactions in Weyerhaeuser common shares, WRECO common shares or TRI Pointe common stock that may apply in their home countries. None of Weyerhaeuser, WRECO or TRI Pointe can provide any assurance about whether such limitations may exist. See “This Exchange Offer—Certain Matters Relating to Non-U.S. Jurisdictions” for additional information about limitations on this exchange offer outside the United States.

iv

Table of Contents

In this document:

| • | “Adjustment Amount” means the Adjustment Amount payable in cash by TRI Pointe or WNR, as applicable, to the other party in connection with the consummation of the Transactions, as described in “The Transaction Agreement—Payment of Adjustment Amount”; |

| • | “business day” means, for purposes of this exchange offer, any day other than a Saturday, Sunday, or U.S. federal holiday and consists of the time period from 12:01 a.m. through 12:00 midnight, New York City time; |

| • | “CIP Shares” means Weyerhaeuser common shares in uncertificated form held through the Computershare CIP, a direct stock purchase and dividend reinvestment plan for Weyerhaeuser, maintained by Computershare Trust Company, N.A., as transfer agent; |

| • | “Citigroup” means Citigroup Global Markets Inc.; |

| • | “Closing Date” means the closing date of the Transactions; |

| • | “Code” means the Internal Revenue Code of 1986, as amended; |

| • | “Commitment Letter” means the commitment letter, dated as of November 3, 2013, of DB Cayman, Deutsche Bank and Citigroup to WRECO; |

| • | “Covington & Burling Tax Opinion” means a written opinion received by Weyerhaeuser from Covington & Burling LLP to the effect that (i) the WRECO Spin will qualify as a tax-free transaction described in Section 355 of the Code, (ii) the Distribution will qualify as a tax-free transaction described in Section 355 of the Code and (iii) the Merger will qualify as a tax-free reorganization described in Section 368 of the Code; |

| • | “Coyote Springs” means the portions of a mixed use master planned community under development located in Clark and Lincoln Counties, Nevada, which are owned by Pardee through its wholly owned subsidiary, Pardee Homes of Nevada (“Pardee Nevada”). The Coyote Springs project is approximately 50 miles north of Las Vegas, Nevada and consists of approximately 42,000 acres, of which approximately 30,000 acres can be developed. As of September 30, 2013, Pardee Nevada owned 10,686 lots and controlled 56,413 lots in Coyote Springs. Within Coyote Springs, Pardee Nevada owns land in Clark County zoned or designated for both single-family home development and multi-family development. Pardee Nevada holds an option to acquire additional land and lots in Clark and Lincoln Counties. Pardee Nevada also owns property in Clark County occupied by a golf course, which is leased to and operated by a third party, as well as land dedicated to commercial and retail development; |

| • | “DB Cayman” means Deutsche Bank AG Cayman Islands Branch; |

| • | “Debt Securities” means the debt securities, in the aggregate principal amount of up to the full amount of the New Debt, which may be issued and sold by WRECO upon consummation of the Transactions; |

| • | “Delayed Transfer Assets” means (i) those assets relating to the Real Estate Business to be transferred to WRECO and its subsidiaries and (ii) those assets of WRECO that will be excluded from the Transactions and transferred to Weyerhaeuser and its subsidiaries (other than WRECO and its subsidiaries), in each case the transfer of which would constitute a violation of applicable law or require a consent or governmental approval not obtained prior to the time such assets should be transferred pursuant to the terms of the Transaction Agreement; |

| • | “Delayed Transfer Liabilities” means (i) those liabilities relating to the Real Estate Business to be assumed by WRECO and its subsidiaries and (ii) those liabilities that will be excluded from the Transactions and assumed by Weyerhaeuser and its subsidiaries (other than WRECO and its subsidiaries), in each case the assumption of which would constitute a violation of applicable law or require a consent or governmental approval not obtained prior to the time such liabilities should be transferred pursuant to the terms of the Transaction Agreement; |

| • | “Deutsche Bank” means Deutsche Bank Securities Inc.; |

| • | “DGCL” means the Delaware General Corporation Law; |

| • | “DRS” means the Direct Registration System maintained by Computershare Trust Company, N.A.; |

1

Table of Contents

| • | “Distribution” means the distribution by Weyerhaeuser of the issued and outstanding WRECO common shares to Weyerhaeuser shareholders by way of this exchange offer and, with respect to any WRECO common shares that are not subscribed for in this exchange offer, a pro rata distribution to Weyerhaeuser shareholders whose Weyerhaeuser common shares remain outstanding after consummation of this exchange offer; |

| • | “Exchange Act” means the Securities Exchange Act of 1934, as amended; |

| • | “Financing Letters” means the Commitment Letter and the related engagement letter and fee letter executed in connection therewith; |

| • | “GAAP” means generally accepted accounting principles in the United States; |

| • | “Gibson Dunn Tax Opinion” means a written opinion received by TRI Pointe from Gibson, Dunn & Crutcher LLP to the effect that the Merger will qualify as a tax-free reorganization described in Section 368 of the Code; |

| • | “HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended; |

| • | “Incentive Unit Holder” means a holder of incentive units in TPH LLC; |

| • | “Intra-Day VWAP” means, at a specific time in a day, the VWAP for the period beginning at the official open of trading on the NYSE and ending as of the specific time in such day; |

| • | “IRS” means the U.S. Internal Revenue Service; |

| • | “Merger” means the combination of TRI Pointe’s business and the Real Estate Business through the merger of Merger Sub with and into WRECO, with WRECO surviving the merger and becoming a wholly owned subsidiary of TRI Pointe, as contemplated by the Transaction Agreement; |

| • | “Merger Sub” means Topaz Acquisition, Inc., a Washington corporation and a wholly owned subsidiary of TRI Pointe; |

| • | “New Debt” means the $800 million or more in aggregate principal amount of debt financing to be incurred by WRECO upon consummation of the Transactions in the form of (i) the Debt Securities, (ii) the Senior Unsecured Bridge Facility or (iii) a combination thereof, which debt will be an obligation of WRECO and will be guaranteed by WRECO’s material wholly owned subsidiaries (and after the consummation of the Merger, TRI Pointe and its material wholly owned subsidiaries), subject to certain exceptions; |

| • | “NYSE” means the New York Stock Exchange; |

| • | “Real Estate Business” means the real estate business of Weyerhaeuser, which business is currently conducted by WRECO and its subsidiaries and set forth in certain financial statements of WRECO, other than the operations of certain excluded assets; |

| • | “REB Transfers” means (i) the transfer of certain assets of Weyerhaeuser and its subsidiaries relating to the Real Estate Business to, and the assumption of certain liabilities of Weyerhaeuser and its subsidiaries relating to the Real Estate Business by, WRECO and its subsidiaries and (ii) the transfer of certain assets of WRECO and its subsidiaries that will be excluded from the Transactions to, and the assumption of certain liabilities of WRECO and its subsidiaries that will be excluded from the Transactions by, Weyerhaeuser and its subsidiaries (other than WRECO and its subsidiaries), including the assets and liabilities relating to Coyote Springs; |

| • | “Revolving Credit Agreement” means the Revolving Credit Agreement, dated as of July 18, 2013, by and between TRI Pointe and U.S. Bank National Association d/b/a Housing Capital Company, as amended on December 26, 2013; |

| • | “SEC” means the U.S. Securities and Exchange Commission; |

| • | “Securities Act” means the Securities Act of 1933, as amended; |

2

Table of Contents

| • | “Senior Unsecured Bridge Facility” means the senior unsecured bridge loans that may be incurred by WRECO upon consummation of the Transactions in the event that WRECO does not issue Debt Securities in aggregate principal amount of at least $800 million and in an aggregate principal amount equal to $800 million less the aggregate principal amount of the Debt Securities issued by WRECO; |

| • | “Starwood Capital” means Starwood Capital Group LLC, an affiliate of TRI Pointe; |

| • | “Starwood Capital Group” means Starwood Capital Group Global, L.P., its predecessors and owned affiliates; |

| • | “Starwood Fund” means VIII/TPC Holdings, L.L.C., a private equity fund managed by an affiliate of Starwood Capital Group; |

| • | “Starwood Property Trust” means Starwood Property Trust, Inc., an NYSE-listed public mortgage REIT managed by an affiliate of Starwood Capital Group; |

| • | “Tax Sharing Agreement” means the tax sharing agreement to be entered into by Weyerhaeuser, TRI Pointe and WRECO on or prior to the date on which validly tendered Weyerhaeuser common shares are accepted for payment pursuant to the Distribution; |

| • | “TPH LLC” means TRI Pointe Homes, LLC, the entity that was reorganized from a Delaware limited liability company into a Delaware corporation and renamed TRI Pointe Homes, Inc. in connection with its initial public offering; |

| • | “Transaction Agreement” means the Transaction Agreement, dated as of November 3, 2013, by and among Weyerhaeuser, WRECO, TRI Pointe and Merger Sub, which is incorporated by reference into this document; |

| • | “Transaction Documents” has the meaning ascribed to it in the Transaction Agreement; |

| • | “Transactions” means the transactions contemplated by the Transaction Agreement and the other Transaction Documents, which provide for, among other things, the New Debt, the REB Transfers, the Distribution, the WRECO Spin, the WRECO Stock Split and the Merger, as described in “The Transactions”; |

| • | “TRI Pointe” means TRI Pointe Homes, Inc., a Delaware corporation, and, unless the context otherwise requires, its subsidiaries. For periods prior to September 24, 2010, “TRI Pointe” refers to the entities through which it conducted its business during those periods. For periods from and after September 24, 2010 and prior to January 30, 2013, “TRI Pointe” refers to TPH LLC and, unless the context otherwise requires, its subsidiaries and affiliates; |

| • | “TRI Pointe Bylaws” means the Amended and Restated Bylaws of TRI Pointe Homes, Inc.; |

| • | “TRI Pointe Charter” means the Amended and Restated Certificate of Incorporation of TRI Pointe Homes, Inc.; |

| • | “TRI Pointe common stock” means the common stock, par value $0.01 per share, of TRI Pointe; |

| • | “TRI Pointe Stockholder Approval” means the approval of the TRI Pointe stockholders of the issuance of shares of TRI Pointe common stock in the Merger; |

| • | “TRI Pointe stockholders” means the holders of TRI Pointe common stock; |

| • | “Valuation Dates” means each of the last three trading days of the exchange offer period (not including the expiration date), as it may be voluntarily extended, but not including the last two trading days that are part of any Mandatory Extension or any voluntary extension following a Mandatory Extension. Based on an expiration date of , 2014, the Valuation Dates are expected to be , 2014, , 2014 and , 2014; |

| • | “VWAP” means volume-weighted average price; |

| • | “Voting Agreements” means the Voting Agreements filed as Exhibits 9.1, 9.2, 9.3 and 9.4 to this document; |

3

Table of Contents

| • | “Weyerhaeuser” means Weyerhaeuser Company, a Washington corporation, and, unless the context otherwise requires, its subsidiaries, other than WRECO and any of its subsidiaries; |

| • | “Weyerhaeuser common shares” means the common shares, par value $1.25 per share, of Weyerhaeuser; |

| • | “Weyerhaeuser shareholders” means the holders of Weyerhaeuser common shares; |

| • | “WNR” means Weyerhaeuser NR Company, a Washington corporation and a wholly owned subsidiary of Weyerhaeuser; |

| • | “WRECO” means Weyerhaeuser Real Estate Company, a Washington corporation, and, prior to the consummation of the Transactions, an indirect wholly owned subsidiary of Weyerhaeuser, and, unless the context otherwise requires, its subsidiaries; |

| • | “WRECO common shares” means the common shares of WRECO, which will have a par value of $0.04 per share after the consummation of the WRECO Stock Split; |

| • | “WRECO Spin” means the distribution by WNR of all of the issued and outstanding WRECO common shares to Weyerhaeuser; and |

| • | “WRECO Stock Split” means the stock split to be effected by WRECO pursuant to which the number of WRECO common shares issued and outstanding will be increased to 100,000,000 shares and the par value of each WRECO common share will be reduced to $0.04 per share. |

4

Table of Contents

QUESTIONS AND ANSWERS ABOUT THIS EXCHANGE OFFER AND THE TRANSACTIONS

The following are some of the questions that Weyerhaeuser shareholders may have and answers to those questions. These questions and answers, as well as the summary that follows them, are not meant to be a substitute for the information contained in the remainder of this document, and this information is qualified in its entirety by the more detailed descriptions and explanations contained elsewhere in this document. You are urged to read this document in its entirety prior to making any investment decision.

Questions and Answers About This Exchange Offer

| Q: | Who may participate in this Exchange Offer? |

| A: | Any U.S. holder of Weyerhaeuser common shares during the exchange offer period may participate in this exchange offer. Holders of Weyerhaeuser’s 6.375% Mandatory Convertible Preference Shares, Series A, may participate in this exchange offer only to the extent that they convert their preference shares into Weyerhaeuser common shares and validly tender those Weyerhaeuser common shares prior to the expiration of this exchange offer. Although Weyerhaeuser has mailed this document to its shareholders to the extent required by U.S. law, including shareholders located outside the United States, this document is not an offer to buy, sell or exchange and it is not a solicitation of an offer to buy or sell any Weyerhaeuser common shares, TRI Pointe common stock or WRECO common shares in any jurisdiction in which such offer, sale or exchange is not permitted. |

Countries outside the United States generally have their own legal requirements that govern securities offerings made to persons resident in those countries and often impose stringent requirements about the form and content of offers made to the general public. None of Weyerhaeuser, WRECO or TRI Pointe has taken any action under non-U.S. regulations to facilitate a public offer to exchange Weyerhaeuser common shares, WRECO common shares or TRI Pointe common stock outside the United States. Accordingly, the ability of any non-U.S. person to tender Weyerhaeuser common shares in this exchange offer will depend on whether there is an exemption available under the laws of such person’s home country that would permit the person to participate in this exchange offer without the need for Weyerhaeuser, WRECO or TRI Pointe to take any action to facilitate a public offering in that country or otherwise. For example, some countries exempt transactions from the rules governing public offerings if they involve persons who meet certain eligibility requirements relating to their status as sophisticated or professional investors.

Non-U.S. shareholders should consult their advisors in considering whether they may participate in this exchange offer in accordance with the laws of their home countries and, if they do participate, whether there are any restrictions or limitations on transactions in Weyerhaeuser common shares, WRECO common shares or TRI Pointe common stock that may apply in their home countries. None of Weyerhaeuser, WRECO or TRI Pointe can provide any assurance about whether such limitations may exist. See “This Exchange Offer—Certain Matters Relating to Non-U.S. Jurisdictions” for additional information about limitations on this exchange offer outside the United States.

| Q: | How many WRECO common shares will I receive for each Weyerhaeuser common share that I tender? |

| A: | This exchange offer is designed to permit you to exchange your Weyerhaeuser common shares for a number of WRECO common shares that corresponds to a % discount to the equivalent amount of TRI Pointe common stock, calculated as set forth in this document. However, the exchange ratio is subject to an upper limit, as discussed in “This Exchange Offer—Upper Limit”. If the upper limit is in effect, Weyerhaeuser common shares will be exchanged for a number of WRECO common shares that corresponds to less, and possibly much less, than a % discount to the equivalent amount of TRI Pointe common stock, calculated as set forth in this document. Subject to the upper limit, for each $1.00 of Weyerhaeuser common shares accepted in this exchange offer, you will ultimately receive $ of fully paid and non-assessable shares of TRI Pointe common stock as a result of this exchange offer and the Merger. If the upper limit is in effect, |

5

Table of Contents

| you will ultimately receive less than $ of TRI Pointe common stock for each $1.00 of Weyerhaeuser common shares that is accepted in this exchange offer, and you could receive much less. The calculated per-share value of Weyerhaeuser common shares for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of Weyerhaeuser common shares on the NYSE on each of the Valuation Dates. The calculated per-share value of WRECO common shares for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of TRI Pointe common stock on the NYSE on each of the Valuation Dates, multiplied by 1.297 (which is the number of shares of TRI Pointe common stock to be received per WRECO common share as a result of the Merger). The calculated per-share value of TRI Pointe common stock for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of shares of TRI Pointe common stock on the NYSE on each of the Valuation Dates. Weyerhaeuser will determine the calculations of the per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock and its determination will be final. |

Please note, however, that:

| • | The number of shares you can receive is subject to an upper limit of WRECO common shares for each Weyerhaeuser common share accepted in this exchange offer. The next question and answer below describe how this limit may impact the value you receive. |

| • | This exchange offer does not provide for a minimum exchange ratio. See “This Exchange Offer—Terms of this Exchange Offer”. |

| • | Because this exchange offer is subject to proration in the event of oversubscription, Weyerhaeuser may accept for exchange only a portion of the Weyerhaeuser common shares tendered by you. |

| Q: | Is there a limit on the number of WRECO common shares that I can receive for each Weyerhaeuser common share that I tender? |

| A: | The number of shares you can receive is subject to an upper limit of WRECO common shares for each Weyerhaeuser common share accepted in this exchange offer. If the upper limit is in effect, Weyerhaeuser common shares will be exchanged for a number of WRECO common shares that corresponds to less, and possibly much less, than a % discount to the equivalent amount of TRI Pointe common stock, calculated as set forth in this document. If the upper limit is in effect, you will ultimately receive less than $ of TRI Pointe common stock for each $1.00 of Weyerhaeuser common shares that is accepted in this exchange offer, and you could receive much less. For example, if the calculated per-share value of Weyerhaeuser common shares was $ (the highest closing price for Weyerhaeuser common shares on the NYSE during the three-month period prior to commencement of this exchange offer) and the calculated per-share value of WRECO common shares was $ (based on the lowest closing price for TRI Pointe common stock on the NYSE during that three-month period multiplied by 1.297 (which is the number of shares of TRI Pointe common stock to be received per WRECO common share as a result of the Merger)), the value of WRECO common shares, based on the TRI Pointe common stock price multiplied by 1.297 (which is the number of shares of TRI Pointe common stock to be received per WRECO common share as a result of the Merger), received for Weyerhaeuser common shares accepted for exchange would be approximately $ for each $1.00 of Weyerhaeuser common shares accepted for exchange. |

The upper limit was calculated to correspond to a % discount in the value of TRI Pointe common stock, relative to Weyerhaeuser common shares, based on the averages of the daily VWAPs of Weyerhaeuser common shares and TRI Pointe common stock on the NYSE on , 2014, , 2014 and , 2014 (the last three trading days before the commencement of this exchange offer). Weyerhaeuser set this upper limit to ensure that an unusual or unexpected drop in the trading price of TRI Pointe common stock, relative to the trading price of Weyerhaeuser common shares, would not result in an unduly high number of WRECO common shares being exchanged for each Weyerhaeuser common share accepted in this exchange offer.

6

Table of Contents

| Q: | What will happen if the upper limit is in effect? |

| A: | Weyerhaeuser will announce whether the upper limit on the number of shares that can be received for each Weyerhaeuser common share tendered is in effect athttp://www. .com/ / and separately by press release, no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date of this exchange offer. If the upper limit is in effect at that time, then the exchange ratio will be fixed at the upper limit and a Mandatory Extension of this exchange offer will be made until 8:00 a.m., New York City time, on the day after the second trading day following the last trading day prior to the originally contemplated expiration date to permit shareholders to tender or withdraw their Weyerhaeuser common shares during those days. The daily VWAP and trading prices of Weyerhaeuser common shares and TRI Pointe common stock during the Mandatory Extension will not affect the exchange ratio, which will be fixed at . See “This Exchange Offer—Terms of this Exchange Offer—Extension; Termination; Amendment—Mandatory Extension”. |

| Q: | How are the calculated per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock determined for purposes of calculating the number of WRECO common shares to be received in this exchange offer? |

| A: | The calculated per-share value of Weyerhaeuser common shares for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of Weyerhaeuser common shares on the NYSE on each of the Valuation Dates. The calculated per-share value of WRECO common shares for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of TRI Pointe common stock on the NYSE on each of the Valuation Dates, multiplied by 1.297 (which is the number of shares of TRI Pointe common stock to be received per WRECO common share as a result of the Merger). The calculated per-share value of TRI Pointe common stock for purposes of this exchange offer will equal the simple arithmetic average of the daily VWAP of shares of TRI Pointe common stock on the NYSE on each of the Valuation Dates. Weyerhaeuser will determine the calculations of the per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock and its determination will be final. |

| Q: | What is the “daily volume-weighted average price” or “daily VWAP”? |

| A: | The “daily volume-weighted average price” for Weyerhaeuser common shares and TRI Pointe common stock will be the volume-weighted average price of Weyerhaeuser common shares and TRI Pointe common stock on the NYSE during the period beginning at 9:30 a.m., New York City time (or such other time as is the official open of trading on the NYSE), and ending at 4:00 p.m., New York City time (or such other time as is the official close of trading on the NYSE and in no event later than 4:10 p.m., New York City time), as reported to Weyerhaeuser by Bloomberg L.P. for the equity ticker pages WY.N, in the case of Weyerhaeuser common shares, and TPH.N, in the case of TRI Pointe common stock. The daily VWAPs provided by Bloomberg L.P. may be different from other sources of volume-weighted average prices or investors’ or security holders’ own calculations of volume-weighted average prices. |

| Q: | Where can I find the daily VWAP of Weyerhaeuser common shares and TRI Pointe common stock during the exchange offer period? |

| A: | Weyerhaeuser will maintain a website athttp://www. .com/ / that provides the daily VWAP of both Weyerhaeuser common shares and TRI Pointe common stock, together with indicative exchange ratios, for each day during this exchange offer. The indicative exchange ratios will reflect whether the upper limit on the exchange ratio, described above, would have been in effect. You may also contact the information agent at the toll-free number provided on the back cover of this document to obtain the indicative exchange ratios. During the period of the Valuation Dates, when the values of Weyerhaeuser common shares, WRECO common shares and shares of TRI Pointe common stock are calculated for the purposes of this exchange offer, the website will show the indicative exchange ratios based on indicative per-share values |

7

Table of Contents

| calculated by Weyerhaeuser. The indicative per-share value of Weyerhaeuser common shares will equal (i) on the first Valuation Date, the Intra-Day VWAP for Weyerhaeuser common shares on the NYSE during the elapsed portion of that day, (ii) on the second Valuation Date, the Intra-Day VWAP for Weyerhaeuser common shares on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date and (iii) on the third Valuation Date, theIntra-Day VWAP for Weyerhaeuser common shares on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date and with the actual daily VWAP on the second Valuation Date. The indicative per-share value of WRECO common shares will equal (x) on the first Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day, multiplied by 1.297 (which is the number of shares of TRI Pointe common stock to be received per WRECO common share as a result of the Merger), (y) on the second Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date, multiplied by 1.297, and (z) on the third Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date and with the actual daily VWAP on the second Valuation Date, multiplied by 1.297. The indicative per-share value of TRI Pointe common stock will equal (i) on the first Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day, (ii) on the second Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date and (iii) on the third Valuation Date, the Intra-Day VWAP for TRI Pointe common stock on the NYSE during the elapsed portion of that day averaged with the actual daily VWAP on the first Valuation Date and with the actual daily VWAP on the second Valuation Date. Weyerhaeuser will determine the calculations of the per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock and its determination will be final. During the period of the Valuation Dates, the indicative exchange ratios and calculated per-share values will be updated at 10:30 a.m., 1:30 p.m. and no later than 4:30 p.m., New York City time. |

| Q: | Why is the calculated per-share value for WRECO common shares based on the trading prices for TRI Pointe common stock? |

| A: | There is currently no trading market for WRECO common shares and no trading market will be established in the future. Weyerhaeuser believes, however, that the trading prices for TRI Pointe common stock are an appropriate proxy for the trading prices of WRECO common shares because (i) in the Merger each issued and outstanding WRECO common share will be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock and (ii) at the Valuation Dates, it is expected that all the major conditions to the consummation of the Merger will have been satisfied and the Merger will be expected to be consummated shortly thereafter, such that investors should be expected to be valuing TRI Pointe common stock based on the expected value of the TRI Pointe common stock after the consummation of the Merger. There can be no assurance, however, that TRI Pointe common stock after the consummation of the Merger will trade at the same prices at which TRI Pointe common stock trades prior to the consummation of the Merger. See “Risk Factors—Risks Related to the Transactions—The trading prices of TRI Pointe common stock may not be an appropriate proxy for the prices of WRECO common shares”. |

| Q: | How and when will I know the final exchange ratio? |

| A: | Subject to the possible Mandatory Extension of this exchange offer described below, the final exchange ratio showing the number of WRECO common shares that you will receive for each Weyerhaeuser common share accepted in this exchange offer will be available athttp://www. .com/ / and separately by press release no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date. In addition, as described below, you may also contact the information agent to obtain the final exchange ratio at its toll-free number provided on the back cover of this document. |

8

Table of Contents

Weyerhaeuser will announce whether the upper limit on the number of shares that can be received for each Weyerhaeuser common share tendered is in effect athttp://www. .com/ / and separately by press release no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date. If the upper limit is in effect at that time, then the exchange ratio will be fixed at the upper limit and a Mandatory Extension of this exchange offer will be made until 8:00 a.m., New York City time, on the day after the second trading day following the last trading day prior to the originally contemplated expiration date to permit shareholders to tender or withdraw their Weyerhaeuser common shares during those days.

| Q: | Will indicative exchange ratios be provided during the tender offer period? |

| A: | Yes. You will be able to review indicative exchange ratios and calculated per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock and the final exchange ratio used to determine the number of WRECO common shares to be exchanged per Weyerhaeuser common share. Weyerhaeuser will maintain a website athttp://www. .com/ / that provides the indicative exchange ratios and calculated per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock. The indicative exchange ratios will also reflect whether the upper limit on the exchange ratio, described above, would have been in effect. You may also contact the information agent at the toll-free number provided on the back cover of this document to obtain these indicative exchange ratios. |

In addition, for purposes of illustration, a table that indicates the number of WRECO common shares that you would receive per Weyerhaeuser common share, calculated on the basis described above and taking into account the upper limit, assuming a range of averages of the daily VWAP of Weyerhaeuser common shares and TRI Pointe common stock on the Valuation Dates, is provided under “This Exchange Offer—Terms of this Exchange Offer”.

| Q: | What if Weyerhaeuser common shares or shares of TRI Pointe common stock do not trade on any of the Valuation Dates? |

| A: | If a market disruption event occurs with respect to Weyerhaeuser common shares or TRI Pointe common stock on any of the Valuation Dates, the calculated per-share value of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock will be determined using the daily VWAP of Weyerhaeuser common shares and TRI Pointe common stock on the preceding trading day or days, as the case may be, on which no market disruption event occurred with respect to both Weyerhaeuser common shares and TRI Pointe common stock. If, however, a market disruption event occurs as specified above, Weyerhaeuser may terminate this exchange offer if, in its reasonable judgment, the market disruption event has impaired the benefits of this exchange offer. For specific information as to what would constitute a market disruption event, see “This Exchange Offer—Conditions for Consummation of this Exchange Offer”. |

| Q: | Are there circumstances under which I would receive fewer WRECO common shares than I would have received if the exchange ratio were determined using the closing prices of Weyerhaeuser common shares and TRI Pointe common stock on the expiration date of this exchange offer? |

| A: | Yes. For example, if the trading price of Weyerhaeuser common shares were to increase during the period of the Valuation Dates, the average Weyerhaeuser common share price used to calculate the exchange ratio would likely be lower than the closing price of Weyerhaeuser common shares on the expiration date of this exchange offer. As a result, you may receive fewer WRECO common shares, and therefore effectively fewer shares of TRI Pointe common stock, for each $1.00 of Weyerhaeuser common shares than you would have if that per-share value were calculated on the basis of the closing price of Weyerhaeuser common shares on the expiration date of this exchange offer. Similarly, if the trading price of TRI Pointe common stock were to decrease during the period of the Valuation Dates, the average TRI Pointe common stock price used to calculate the exchange ratio would likely be higher than the closing price of TRI Pointe |

9

Table of Contents

| common stock on the expiration date of this exchange offer. This could also result in you receiving fewer WRECO common shares, and therefore effectively fewer shares of TRI Pointe common stock, for each $1.00 of Weyerhaeuser common shares than you would otherwise receive if that per-share value were calculated on the basis of the closing price of TRI Pointe common stock on the expiration date of this exchange offer. See “This Exchange Offer—Terms of this Exchange Offer”. |

| Q: | Will Weyerhaeuser distribute fractional shares? |

| A: | Immediately following the consummation of this exchange offer, Merger Sub will be merged with and into WRECO, with WRECO surviving the Merger and becoming a wholly owned subsidiary of TRI Pointe. Each issued and outstanding WRECO common share will be converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock. In this conversion of WRECO common shares into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share, no fractional shares of TRI Pointe common stock will be delivered to holders of WRECO common shares. TRI Pointe’s transfer agent will aggregate all fractional shares of TRI Pointe common stock that holders of WRECO common shares would otherwise be entitled to receive as a result of the Merger. The transfer agent will cause the whole shares obtained thereby to be sold on behalf of those holders in the open market or otherwise as reasonably directed by TRI Pointe, in no case later than five business days after the consummation of the Merger. The transfer agent will make available the net proceeds thereof, after deducting any required withholding taxes and brokerage charges, commissions and transfer taxes, on a pro rata basis, without interest, as soon as practicable to the holders of WRECO common shares who would otherwise be entitled to receive those fractional shares of TRI Pointe common stock in the Merger. |

| Q: | What is the aggregate number of WRECO common shares being offered in this exchange offer? |

| A: | In this exchange offer, Weyerhaeuser is offering 100,000,000 WRECO common shares. Weyerhaeuser is offering all of the WRECO common shares that will be issued and outstanding on the date of consummation of this exchange offer. |

| Q: | What happens if not enough Weyerhaeuser common shares are tendered to allow Weyerhaeuser to exchange all of the issued and outstanding WRECO common shares? |

| A: | If this exchange offer is consummated but fewer than all of the issued and outstanding WRECO common shares are exchanged because this exchange offer is not fully subscribed, the remaining WRECO common shares owned by Weyerhaeuser will be distributed on a pro rata basis to Weyerhaeuser shareholders whose Weyerhaeuser common shares remain outstanding after the consummation of this exchange offer. Any Weyerhaeuser shareholder who validly tenders (and does not properly withdraw) Weyerhaeuser common shares for WRECO common shares in this exchange offer will waive its rights with respect to those tendered Weyerhaeuser common shares to receive, and will forfeit any rights to, WRECO common shares distributed on a pro rata basis to Weyerhaeuser shareholders in the event this exchange offer is not fully subscribed. |

Regardless of whether this exchange offer is fully subscribed, the exchange agent will hold all issued and outstanding WRECO common shares (including any shares distributed on a pro rata basis) in trust until the WRECO common shares are converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share in the Merger. You will not be able to trade WRECO common shares during this period or at any time before or after the consummation of the Merger. See “This Exchange Offer—Distribution of Any WRECO Common Shares Remaining after This Exchange Offer”.

10

Table of Contents

| Q: | Will all Weyerhaeuser common shares that I tender be accepted in this exchange offer? |

| A: | Not necessarily. Depending on the number of Weyerhaeuser common shares validly tendered in this exchange offer and not properly withdrawn, and the calculated per-share values of Weyerhaeuser common shares, WRECO common shares and TRI Pointe common stock determined as described above, Weyerhaeuser may have to limit the number of Weyerhaeuser common shares that it accepts in this exchange offer through a proration process. Any proration of the number of shares accepted in this exchange offer will be determined on the basis of the proration mechanics described in “This Exchange Offer—Terms of this Exchange Offer—Proration; Tenders for Exchange by Holders of Fewer than 100 Weyerhaeuser Common Shares”. |

An exception to proration can apply to shareholders who beneficially own “odd-lots”, that is, fewer than 100 Weyerhaeuser common shares. Beneficial holders of fewer than 100 Weyerhaeuser common shares who validly tender all of their shares and request preferential treatment as described in “This Exchange Offer—Terms of this Exchange Offer—Proration; Tenders for Exchange by Holders of Fewer than 100 Weyerhaeuser Common Shares” will not be subject to proration.

In all other cases, proration for each tendering shareholder will be based on (i) the proportion that the total number of Weyerhaeuser common shares to be accepted bears to the total number of Weyerhaeuser common shares validly tendered and not properly withdrawn and (ii) the number of Weyerhaeuser common shares validly tendered and not properly withdrawn by that shareholder (and not on that shareholder’s aggregate ownership of Weyerhaeuser common shares). Any Weyerhaeuser common shares not accepted for exchange in this exchange offer as a result of proration or otherwise will be returned to tendering shareholders promptly after the final proration factor is determined.

| Q: | Will I be able to sell my WRECO common shares after this exchange offer is completed? |

| A: | No. There currently is no trading market for WRECO common shares and no trading market will be established in the future. The exchange agent will hold all issued and outstanding WRECO common shares in trust until the WRECO common shares are converted into the right to receive 1.297 fully paid and non-assessable shares of TRI Pointe common stock for each WRECO common share in the Merger. You will not be able to trade WRECO common shares during this period or at any time before or after the consummation of the Merger. See “This Exchange Offer—Distribution of Any WRECO Common Shares Remaining after this Exchange Offer”. |

| Q: | How many Weyerhaeuser common shares will Weyerhaeuser accept if this exchange offer is completed? |

| A: | The number of Weyerhaeuser common shares that will be accepted if this exchange offer is completed will depend on the final exchange ratio and the number of Weyerhaeuser common shares tendered. Because Weyerhaeuser will offer 100,000,000 WRECO common shares in this exchange offer, the number of Weyerhaeuser common shares that will be accepted will equal 100,000,000 divided by the final exchange ratio. For example, assuming that the final exchange ratio is (the maximum number of WRECO common shares that could be exchanged for one Weyerhaeuser common share), then Weyerhaeuser would accept up to a total of approximately Weyerhaeuser common shares. |

| Q: | Are there any conditions to Weyerhaeuser’s obligation to complete this exchange offer? |

| A: | Yes. This exchange offer is subject to various conditions listed under “This Exchange Offer—Conditions for Consummation of this Exchange Offer”. If any of these conditions is not satisfied or waived prior to the expiration of this exchange offer, Weyerhaeuser will not be required to accept shares for exchange and may extend or terminate this exchange offer. |

| Q: | When does this exchange offer expire? |

| A: | The period during which you are permitted to tender your Weyerhaeuser common shares in this exchange offer will expire at 12:00 midnight, New York City time, on , 2014, unless Weyerhaeuser extends this exchange offer. See “This Exchange Offer—Terms of this Exchange Offer—Extension; Termination; Amendment”. |

11

Table of Contents

| Q: | Can this exchange offer be extended and under what circumstances? |

| A: | Yes. Weyerhaeuser expressly reserves the right, in its sole discretion, at any time and from time to time, to extend the period of time during which this exchange offer is open and thereby delay acceptance for payment of, and the payment for, any Weyerhaeuser common shares validly tendered and not properly withdrawn in this exchange offer. For example, this exchange offer can be extended (i) if any of the conditions for consummation of this exchange offer described in the next section entitled “This Exchange Offer—Conditions for Consummation of this Exchange Offer” are not satisfied or waived prior to the expiration of this exchange offer, (ii) to comply with any applicable law or to obtain any governmental, regulatory or other approvals or (iii) for any period required by any rule, regulation, interpretation or position of the SEC or the staff thereof applicable to this exchange offer, including as required in connection with any material changes to the terms of or information concerning this exchange offer as described below. In addition, if the upper limit on the number of WRECO common shares that can be exchanged for each Weyerhaeuser common share tendered is in effect at the expiration of the exchange offer period, then the exchange ratio will be fixed at the upper limit and a Mandatory Extension of this exchange offer will be made until 8:00 a.m., New York City time, on the day after the second trading day following the last trading day prior to the originally scheduled expiration date. Weyerhaeuser will publicly announce any extension (mandatory or otherwise) athttp://www. .com/ / and separately by press release no later than 9:00 a.m., New York City time, on the next business day following the previously scheduled expiration date. |

| Q: | How do I participate in this exchange offer? |

| A: | The procedures you must follow to participate in this exchange offer depend on whether you hold your Weyerhaeuser common shares in certificated form, through a broker, dealer, commercial bank, trust company or similar institution, in book-entry form via DRS or in uncertificated form as CIP Shares. For specific instructions about how to participate, see “This Exchange Offer—Terms of this Exchange Offer—Procedures for Tendering”. |

| Q: | How do I tender my Weyerhaeuser common shares after the final exchange ratio has been determined? |

| A: | If you wish to tender your shares after the final exchange ratio has been determined, you will generally need to do so by means of delivering a notice of guaranteed delivery and complying with the guaranteed delivery procedures described in the section entitled “This Exchange Offer—Terms of this Exchange Offer—Procedures for Tendering—Guaranteed Delivery Procedures”. If you hold Weyerhaeuser common shares through a broker, dealer, commercial bank, trust company or similar institution, that institution must tender your shares on your behalf. |

If your Weyerhaeuser common shares are held through an institution and you wish to tender your Weyerhaeuser common shares after The Depository Trust Company has closed, the institution must deliver a notice of guaranteed delivery to the exchange agent via facsimile prior to 12:00 midnight, New York City time, on the expiration date.

| Q: | Can I tender only a portion of my Weyerhaeuser common shares in this exchange offer? |

| A: | Yes. You may tender all, some or none of your Weyerhaeuser common shares. |

| Q: | What do I do if I want to retain all of my Weyerhaeuser common shares? |

| A: | If you want to retain all of your Weyerhaeuser common shares, you do not need to take any action. However, after the consummation of the Transactions, the Real Estate Business will no longer be owned by Weyerhaeuser, and as a holder of Weyerhaeuser common shares you will no longer hold shares in a company that owns the Real Estate Business (unless this exchange offer is consummated but is not fully subscribed and the remaining WRECO common shares are distributed on a pro rata basis to Weyerhaeuser shareholders whose Weyerhaeuser common shares remain outstanding after consummation of this exchange offer). |

12

Table of Contents

| Q: | Can I change my mind after I tender my Weyerhaeuser common shares? |

| A: | Yes. You may withdraw your tendered shares at any time before this exchange offer expires. See “This Exchange Offer—Terms of this Exchange Offer—Withdrawal Rights”. If you change your mind again, you can re-tender your Weyerhaeuser common shares by following the tender procedures again prior to the expiration of this exchange offer. |

| Q: | Will I be able to withdraw the Weyerhaeuser common shares I tender after the final exchange ratio has been determined? |

| A: | Yes. The final exchange ratio used to determine the number of WRECO common shares that you will receive for each Weyerhaeuser common share accepted in this exchange offer will be announced no later than 4:30 p.m., New York City time, on the last trading day prior to the expiration date of this exchange offer, which is , 2014, unless this exchange offer is extended or terminated. You have the right to withdraw Weyerhaeuser common shares you have tendered at any time before 12:00 midnight, New York City time, on the expiration date, which is , 2014. See “This Exchange Offer—Terms of this Exchange Offer”. |

If the upper limit on the number of WRECO common shares that can be exchanged for each Weyerhaeuser common share tendered is in effect at the expiration of this exchange offer period, then the exchange ratio will be fixed at the upper limit and a Mandatory Extension of this exchange offer will be made until 8:00 a.m., New York City time, on the day after the second trading day following the last trading day prior to the originally contemplated expiration date, which will permit you to tender or properly withdraw your Weyerhaeuser common shares during those days, either directly or by acting through a broker, dealer, commercial bank, trust company or similar institution on your behalf.

| Q: | How do I withdraw my tendered Weyerhaeuser common shares after the final exchange ratio has been determined? |

| A: | If you are a registered holder of Weyerhaeuser common shares (which includes persons holding certificated shares, book-entry shares held through DRS or CIP Shares and you wish to withdraw your shares after the final exchange ratio has been determined, then you must deliver a written notice of withdrawal or a facsimile transmission notice of withdrawal to the exchange agent prior to 12:00 midnight, New York City time, on the expiration date, subject to a Mandatory Extension. The information that must be included in that notice is specified under “This Exchange Offer—Terms of this Exchange Offer—Withdrawal Rights”. |

If you hold your shares through a broker, dealer, commercial bank, trust company or similar institution, you should consult that institution on the procedures you must comply with and the time by which such procedures must be completed in order for that institution to provide a written notice of withdrawal or facsimile notice of withdrawal to the exchange agent on your behalf before 12:00 midnight, New York City time, on the expiration date. If you hold your shares through such an institution, that institution must deliver the notice of withdrawal with respect to any shares you wish to withdraw. In such a case, as a beneficial owner and not a registered shareholder, you will not be able to provide a notice of withdrawal for those shares directly to the exchange agent.

If your Weyerhaeuser common shares are held through an institution and you wish to withdraw Weyerhaeuser common shares after The Depository Trust Company has closed, the institution must deliver a written notice of withdrawal to the exchange agent prior to 12:00 midnight, New York City time, on the expiration date, subject to a Mandatory Extension. Such notice of withdrawal must be in the form of The Depository Trust Company’s notice of withdrawal, must specify the name and number of the account at The Depository Trust Company to be credited with the withdrawn shares and must otherwise comply with The Depository Trust Company’s procedures. Shares can be properly withdrawn only if the exchange agent receives a withdrawal notice directly from the relevant institution that tendered the shares through The Depository Trust Company. See “This Exchange Offer—Terms of this Exchange Offer—Withdrawal Rights—Withdrawing Your Shares after the Final Exchange Ratio Has Been Determined”.

13

Table of Contents

| Q: | Will I be subject to U.S. federal income tax on the WRECO common shares that I receive in this exchange offer or on the shares of TRI Pointe common stock that I receive in the Merger? |

| A: | Weyerhaeuser shareholders generally will not recognize any gain or loss for U.S. federal income tax purposes as a result of this exchange offer or the Merger, except for any gain or loss attributable to the receipt of cash in lieu of fractional shares of TRI Pointe common stock received in the Merger. |

The material U.S. federal income tax consequences of this exchange offer and the Merger are described in more detail under “This Exchange Offer—Material U.S. Federal Income Tax Consequences of the Distribution and the Merger”.

| Q: | Are there any material differences between the rights of Weyerhaeuser shareholders and TRI Pointe stockholders? |