UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811‑22774

| Name of Fund: | | BlackRock Multi-Sector Income Trust (BIT) |

| Fund Address: 100 | | Bellevue Parkway, Wilmington, DE 19809 |

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Multi-Sector Income Trust, 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882‑0052, Option 4

Date of fiscal year end: 10/31/2022

Date of reporting period: 10/31/2022

Item 1 – Report to Stockholders

(a) The Report to Shareholders is attached herewith.

BlackRock Multi-Sector Income Trust (BIT)

|

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

Supplemental Information (unaudited)

Section 19(a) Notices

BlackRock Multi-Sector Income Trust’s (BIT) (the “Trust”) amounts and sources of distributions reported are estimates and are being provided pursuant to regulatory requirements and are not being provided for tax reporting purposes. The actual amounts and sources for tax reporting purposes will depend upon the Trust’s investment experience during its fiscal year and may be subject to changes based on tax regulations. The Trust will provide a Form 1099-DIV each calendar year that will tell you how to report these distributions for U.S. federal income tax purposes.

October 31, 2022

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | | | Total Cumulative Distributions

for the Fiscal Period | | | % Breakdown of the Total Cumulative

Distributions for the Fiscal Period | | | | |

| | | | | | | | | | | | |

| | | Trust Name | |

| Net

Income |

| |

| Net Realized

Capital Gains

Short-Term |

| |

| Net Realized

Capital Gains

Long-Term |

| |

| Return of

Capital |

(a) | |

| Total Per

Common

Share |

| |

| Net

Income |

| |

| Net Realized

Capital Gains

Short-Term |

| |

| Net Realized

Capital Gains

Long-Term |

| |

| Return of

Capital |

| |

| Total Per

Common

Share |

| | | | |

| | | | | | | | | | | | |

| | BIT | | $ | 0.949678 | | | $ | — | | | $ | — | | | $ | 0.534722 | | | $ | 1.484400 | | | | 64 | % | | | — | % | | | — | % | | | 36 | % | | | 100 | % | | | | |

| | (a) | The Trust estimates that it has distributed more than its net income and net realized capital gains; therefore, a portion of the distribution may be a return of capital. A return of capital may occur, for example, when some or all of the shareholder’s investment in the Trust is returned to the shareholder. A return of capital does not necessarily reflect the Trust’s investment performance and should not be confused with “yield” or “income.” When distributions exceed total return performance, the difference will reduce the Trust’s net asset value per share. | |

Section 19(a) notices for the Trust, as applicable, are available on the BlackRock website at blackrock.com.

Section 19(b) Disclosure

The Trust, acting pursuant to a U.S. Securities and Exchange Commission (“SEC”) exemptive order and with the approval of the Trust’s Board of Trustees (the “Board”), has adopted a managed distribution plan, consistent with its investment objectives and policies to support a level distribution of income, capital gains and/or return of capital (the “Plan”). In accordance with the Plan, the Trust currently distributes the following fixed amounts per share on a monthly basis:

| | | | |

| | |

| Exchange Symbol | | Amount Per

Common Share | |

| |

| BIT | | $ | 0.1237 | |

The fixed amounts distributed per share are subject to change at the discretion of the Trust’s Board. Under its Plan, the Trust will distribute all available net income to its shareholders as required by the Internal Revenue Code of 1986, as amended (the “Code”). If sufficient income (inclusive of net income and short-term capital gains) is not earned on a monthly basis, the Trust will distribute long-term capital gains and/or return of capital to shareholders in order to maintain a level distribution. Each monthly distribution to shareholders is expected to be at the fixed amount established by the Board; however, the Trust may make additional distributions from time to time, including additional capital gain distributions at the end of the taxable year, if required to meet requirements imposed by the Code and/or the Investment Company Act of 1940, as amended (the “1940 Act”).

Shareholders should not draw any conclusions about the Trust’s investment performance from the amount of these distributions or from the terms of the Plan. The Trust’s total return performance is presented in its financial highlights table.

The Board may amend, suspend or terminate the Trust’s Plan at any time without prior notice to the Trust’s shareholders if it deems such actions to be in the best interests of the Trust or its shareholders. The suspension or termination of the Plan could have the effect of creating a trading discount (if the Trust’s stock is trading at or above net asset value) or widening an existing trading discount. The Trust is subject to risks that could have an adverse impact on its ability to maintain level distributions. Examples of potential risks include, but are not limited to, economic downturns impacting the markets, changes in interest rates, decreased market volatility, companies suspending or decreasing corporate dividend distributions and changes in the Code. Please refer to BIT’s prospectus for a more complete description of the Trust’s risks.

| | |

| 2 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

The Markets in Review

Dear Shareholder,

Significant economic headwinds emerged during the 12-month reporting period ended October 31, 2022, disrupting the economic recovery and strong financial markets of 2021. The U.S. economy shrank in the first half of 2022 before returning to moderate growth in the third quarter, marking a shift to a more challenging post-reopening economic environment. Changes in consumer spending patterns and a tight labor market led to elevated inflation, which reached a 40-year high. Moreover, while the foremost effect of Russia’s invasion of Ukraine has been a severe humanitarian crisis, the ongoing war continued to present challenges for both investors and policymakers.

Equity prices fell as interest rates rose, particularly weighing on relatively high-valuation growth stocks as inflation decreased the value of future cash flows and investors shifted focus to balance sheet resilience. Both large- and small-capitalization U.S. stocks fell, although declines for small-capitalization U.S. stocks were slightly steeper. Emerging market stocks and international equities from developed markets also declined significantly, pressured by rising interest rates and a strengthening U.S. dollar.

The 10-year U.S. Treasury yield rose notably during the reporting period, driving its price down, as investors reacted to higher inflation and attempted to anticipate its impact on future interest rate changes. The corporate bond market also faced inflationary headwinds, and increasing uncertainty led to higher corporate bond spreads (the difference in yield between U.S. Treasuries and similarly-dated corporate bonds).

The U.S. Federal Reserve (the “Fed”), acknowledging that inflation has been more persistent than expected, raised interest rates five times while indicating that additional rate hikes were likely. Furthermore, the Fed wound down its bond-buying programs and is accelerating the reduction of its balance sheet. As investors attempted to assess the Fed’s future trajectory, the Fed’s statements late in the reporting period led markets to believe that additional tightening is likely in the near term.

The pandemic’s restructuring of the economy brought an ongoing mismatch between supply and demand, contributing to the current inflationary regime. While growth has slowed in 2022, we believe that taming inflation requires a more dramatic economic decline to bring demand back to a lower level that is more in line with the economy’s capacity. The Fed has been raising interest rates at the fastest pace in decades, and seems set to overtighten in its effort to get inflation back to target. With this in mind, we believe the possibility of a U.S. recession in the near-term is high, and the outlook for Europe and the U.K. is also troubling. Investors should expect a period of higher volatility as markets adjust to the new economic reality and policymakers attempt to adapt to rapidly changing conditions.

In this environment, while we favor an overweight to equities in the long-term, the market’s concerns over excessive rate hikes from central banks moderate our outlook. Rising input costs and a deteriorating economic backdrop in China and Europe are likely to challenge corporate earnings, so we are underweight equities overall in the near term. However, we see better opportunities in credit, where higher spreads provide income opportunities and partially compensate for inflation risk. We believe that investment-grade corporates, local-currency emerging market debt, and inflation-protected bonds (particularly in Europe) offer strong opportunities for a six- to twelve-month horizon.

Overall, our view is that investors need to think globally, position themselves to be prepared for a decarbonizing economy, and be nimble as market conditions change. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| | | | |

Total Returns as of October 31, 2022 |

| | | 6-Month | | 12-Month |

| | |

U.S. large cap equities (S&P 500® Index) | | (5.50)% | | (14.61)% |

| | |

U.S. small cap equities (Russell 2000® Index) | | (0.20) | | (18.54) |

| | |

International equities (MSCI Europe, Australasia, Far East Index) | | (12.70) | | (23.00) |

| | |

Emerging market equities (MSCI Emerging Markets Index) | | (19.66) | | (31.03) |

| | |

| 3-month Treasury bills (ICE BofA 3-Month U.S. Treasury Bill Index) | | 0.72 | | 0.79 |

| | |

U.S. Treasury securities (ICE BofA 10-Year U.S. Treasury Index) | | (8.24) | | (17.68) |

| | |

| U.S. investment grade bonds (Bloomberg U.S. Aggregate Bond Index) | | (6.86) | | (15.68) |

| | |

| Tax-exempt municipal bonds (Bloomberg Municipal Bond Index) | | (4.43) | | (11.98) |

| | |

| U.S. high yield bonds (Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index) | | (4.71) | | (11.76) |

|

| Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. |

| | |

T H I S P A G E I S N O T P A R T O F Y O U R F U N D R E P O R T | | 3 |

Table of Contents

| | | | |

| | | Page | |

| |

| | | 2 | |

| | | 3 | |

| Annual Report: | | | | |

| | | 5 | |

| | | 5 | |

| | | 6 | |

| Financial Statements: | | | | |

| | | 9 | |

| | | 45 | |

| | | 47 | |

| | | 48 | |

| | | 49 | |

| | | 51 | |

| | | 52 | |

| | | 64 | |

| | | 65 | |

| | | 66 | |

| | | 69 | |

| | | 76 | |

| | | 78 | |

| | | 79 | |

| | | 82 | |

| | | 85 | |

| | |

| The Benefits and Risks of Leveraging | | BlackRock Multi-Sector Income Trust (BIT) |

The Trust may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, its common shares (“Common Shares”). However, there is no guarantee that these objectives can be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by the Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Trust (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Trust’s shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage (after paying the leverage costs) is paid to shareholders in the form of dividends, and the value of these portfolio holdings (less the leverage liability) is reflected in the per share NAV.

To illustrate these concepts, assume the Trust’s capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, the Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by the Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, the Trust’s financing cost of leverage is significantly lower than the income earned on the Trust’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed the Trust’s return on assets purchased with leverage proceeds, income to shareholders is lower than if the Trust had not used leverage. Furthermore, the value of the Trust’s portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast, the amount of the Trust’s obligations under its leverage arrangement generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Trust’s NAV positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that the Trust’s intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in the Trust’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of the Trust’s shares than if the Trust were not leveraged. In addition, the Trust may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trust to incur losses. The use of leverage may limit the Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. The Trust incurs expenses in connection with the use of leverage, all of which are borne by shareholders and may reduce income to the shareholders. Moreover, to the extent the calculation of the Trust’s investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Trust’s investment adviser will be higher than if the Trust did not use leverage.

The Trust may utilize leverage through reverse repurchase agreements and/or dollar rolls as described in the Notes to Financial Statements, if applicable.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), the Trust is permitted to borrow money (including through the use of TOB Trusts) or issue debt securities up to 33 1/3% of its total managed assets. The Trust may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act.

Derivative Financial Instruments

The Trust may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the instrument. Pursuant to Rule 18f-4 of the 1940 Act, among other things, the Trust must either use derivative financial instruments with embedded leverage in a limited manner or comply with an outer limit on fund leverage risk based on value-at-risk. The Trust’s successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation the Trust can realize on an investment and/or may result in lower distributions paid to shareholders. The Trust’s investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| | |

T H E B E N E F I T S A N D R I S K S O F L E V E R A G I N G / DE R I V A T I V E F I N A N C I A L I N S T R U M E N T S | | 5 |

| | |

| Trust Summary as of October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) |

Investment Objective

BlackRock Multi-Sector Income Trust’s (BIT) (the “Trust”) primary investment objective is to seek high current income, with a secondary objective of capital appreciation. The Trust seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its assets in loan and debt instruments and other investments with similar economic characteristics. The Trust may invest directly in such securities or synthetically through the use of derivatives. Additionally, as part of the Trust’s investments in loans, the Trust may make loans directly to borrowers either as a sole lender or by acting as a member of a syndicate of original lenders.

No assurance can be given that the Trust’s investment objective will be achieved.

Trust Information

| | |

| | |

| Symbol on New York Stock Exchange | | BIT |

| Initial Offering Date | | February 27, 2013 |

Current Distribution Rate on Closing Market Price as of October 31, 2022 ($14.43)(a) | | 10.29% |

Current Monthly Distribution per Common Share(b) | | $0.1237 |

Current Annualized Distribution per Common Share(b) | | $1.4844 |

Leverage as of October 31, 2022(c) | | 34% |

| | (a) | Current distribution rate on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. The current distribution rate may consist of income, net realized gains and/or a return of capital. Past performance is not an indication of future results. | |

| | (b) | The distribution rate is not constant and is subject to change. A portion of the distribution may be deemed a return of capital or net realized gain. | |

| | (c) | Represents reverse repurchase agreements as a percentage of total managed assets, which is the total assets of the Trust (including any assets attributable to any borrowings) minus the sum of its liabilities (other than borrowings representing financial leverage). Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments. | |

Market Price and Net Asset Value Per Share Summary

| | | | | | | | | | | | | | | | | | | | |

| | | 10/31/22 | | | 10/31/21 | | | Change | | | High | | | Low | |

| | | | | |

| Closing Market Price | | $ | 14.43 | | | $ | 18.90 | | | | (23.65 | )% | | | $ 18.95 | | | | $ 13.64 | |

| Net Asset Value | | | 14.66 | | | | 17.98 | | | | (18.46 | ) | | | 18.01 | | | | 14.38 | |

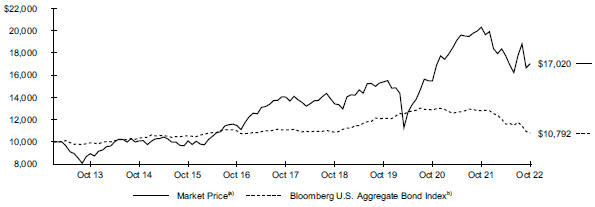

GROWTH OF $10,000 INVESTMENT

| | (a) | Represents the Trust’s closing market price on the NYSE and reflects the reinvestment of dividends and/or distributions at actual reinvestment prices. | |

| | (b) | A broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. | |

| | |

| 6 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

| Trust Summary as of October 31, 2022 (continued) | | BlackRock Multi-Sector Income Trust (BIT) |

Performance

Returns for the period ended October 31, 2022 were as follows:

| | | | | | | | | | | | |

| | | Average Annual Total Returns | |

| | | | |

| | | |

| | | | 1 Year | | | | 5 Years | | |

| Since

Inception |

(a) |

| | | |

Trust at NAV(b)(c) | | | (10.47 | )% | | | 2.66 | % | | | 6.33 | % |

Trust at Market Price(b)(c) | | | (16.16 | ) | | | 3.95 | | | | 5.65 | |

| | | |

| Bloomberg U.S. Aggregate Bond Index | | | (15.68 | ) | | | (0.54 | ) | | | 0.79 | |

| | (a) | BIT commenced operations on February 27, 2013. | |

| | (b) | All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results reflect the Trust’s use of leverage. | |

| | (c) | The Trust moved from a premium to NAV to a discount during the period, which accounts for the difference between performance based on market price and performance based on NAV. | |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles.

Past performance is not an indication of future results.

The Trust is presenting the performance of one or more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies, portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed End Funds” section of blackrock.com.

The following discussion relates to the Trust’s absolute performance based on NAV:

What factors influenced performance?

Against the backdrop of a sharp rise in interest rates, most of the Trust’s sector exposures weighed on performance. Allocations to both high yield and investment grade corporate bonds were among the leading detractors. Exposure to emerging market, sovereign plus and non-dollar developed international market bonds detracted as well. Holdings of a range of securitized asset categories were in negative territory, including residential mortgage-backed securities (“MBS”), non-agency adjustable-rate mortgage-backed securities (“ARMS”), commercial mortgage-backed securities (“CMBS”), asset-backed securities (“ABS”) and collateralized mortgage obligations (“CMOs”). Finally, exposure to municipal bonds detracted as well.

Positive contributions to performance were led by the use of derivatives. During the period, the Trust held derivatives including U.S. futures and interest rate swaps, primarily as hedging vehicles. The use of derivatives had a positive impact on performance over the period.

The Trust’s practice of maintaining a specified level of monthly distributions to shareholders did not have a material impact on the Fund’s investment strategy.

Describe recent portfolio activity.

Over the period, the Trust’s exposure to high yield corporate and emerging market bonds was trimmed in anticipation of an economic slowdown. The Trust’s exposure to agency MBS was increased based on a favorable view of valuation relative to credit-oriented sectors, with a focus on higher coupons and specified pools not subject to the Fed’s efforts to reduce its balance sheet. The Trust also purchased collateralized loan obligations which appeared attractively valued relative to corporate bonds.

Describe portfolio positioning at period end.

At period end, the Trust maintained a diverse exposure within non-government spread sectors, including U.S. high yield corporate bonds, non-agency MBS, investment grade corporate bonds, and ABS. The Trust also held allocations to foreign sovereign issues, emerging market debt and agency MBS.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

T R U S T S U M M A R Y | | 7 |

| | |

| Trust Summary as of October 31, 2022 (continued) | | BlackRock Multi-Sector Income Trust (BIT) |

Overview of the Trust’s Total Investments

| | | | |

| PORTFOLIO COMPOSITION | |

| | |

| Asset Type | | 10/31/22 | |

| |

| Corporate Bonds | | | 51.9 | % |

| U.S. Government Sponsored Agency Securities | | | 16.9 | |

| Non-Agency Mortgage-Backed Securities | | | 7.8 | |

| Asset-Backed Securities | | | 7.3 | |

| Preferred Securities | | | 5.6 | |

| Floating Rate Loan Interests | | | 4.8 | |

| Foreign Agency Obligations | | | 2.1 | |

| U.S. Treasury Obligations | | | 1.6 | |

| Short-Term Securities | | | 1.4 | |

| Other* | | | 0.6 | |

| | | | |

| CREDIT QUALITY ALLOCATION | |

| | |

| Credit Rating(a)(b) | | 10/31/22 | |

| |

AAA/Aaa(c) | | | 19.8 | % |

| AA/Aa | | | 0.7 | |

| A | | | 1.6 | |

| BBB/Baa | | | 14.7 | |

| BB/Ba | | | 26.3 | |

| B | | | 19.0 | |

| CCC/Caa | | | 6.6 | |

| CC | | | 2.6 | |

| C | | | 2.1 | |

N/R(d) | | | 6.6 | |

| (a) | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| (b) | Excludes common stocks, warrants, short-term securities, options purchased and options written. |

| (c) | Includes U.S. Government Sponsored Agency Securities which are deemed AAA/Aaa by the investment adviser. |

| (d) | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2022, the market value of unrated securities deemed by the investment adviser to be investment grade represents less than 1.0% of the Trust’s total investments. |

| * | Includes one or more investment categories that individually represents less than 1.0% of the Trust’s total investments. Please refer to the Schedule of Investments for details. | |

| | |

| 8 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

| Asset-Backed Securities | |

Ajax Mortgage Loan Trust, Series 2017-D, Class B, 0.00%, 12/25/57(a)(b)(c) | | USD | 20 | | | $ | 15,897 | |

ALM Ltd., Series 2020-1A, Class D, (3 mo. LIBOR US + 6.00%), 10.08%, 10/15/29(b)(c) | | | 287 | | | | 239,053 | |

American Homes 4 Rent Trust, Series 2014-SFR2, Class E, 6.23%, 10/17/36(c) | | | 2,000 | | | | 1,964,565 | |

AMMC CLO 19 Ltd., Series 2016-1A, Class E, (3 mo. LIBOR US + 7.00%),

11.08%, 10/15/28(b)(c) | | | 1,000 | | | | 948,452 | |

Anchorage Capital CLO 5-R Ltd., Series 2014-5RA, Class E,

(3 mo. LIBOR US + 5.40%),

9.48%, 01/15/30(b)(c) | | | 860 | | | | 758,654 | |

Anchorage Capital CLO 7 Ltd., Series 2015-7A, Class D1R2, (3 mo. LIBOR US + 3.50%),

7.87%, 01/28/31(b)(c) | | | 250 | | | | 220,020 | |

Apidos CLO XXVI, Series 2017-26A, Class A1AR, (3 mo. LIBOR US + 0.90%),

5.09%, 07/18/29(b)(c) | | | 460 | | | | 448,899 | |

Argent Securities Trust, Series 2006-W5, Class A1A, (1 mo. LIBOR US + 0.30%),

3.89%, 06/25/36(b) | | | 4,278 | | | | 2,859,373 | |

Bain Capital Credit CLO Ltd., Series 2020-2A, Class DR,

(3 mo. LIBOR US + 3.30%),

7.53%, 07/19/34(b)(c) | | | 250 | | | | 211,805 | |

Bear Stearns Asset-Backed Securities I Trust, Series 2006-HE9, Class 2A, (1 mo. LIBOR US + 0.14%), 3.73%, 11/25/36(b) | | | 1,177 | | | | 1,128,473 | |

Benefit Street Partners CLO XX Ltd., Series 2020-20A, Class CR, (3 mo. LIBOR US + 2.05%), 6.13%, 07/15/34(b)(c) | | | 250 | | | | 224,408 | |

Brookside Mill CLO Ltd., Series 2013-1A, Class DR, (3 mo. LIBOR US + 2.65%),

6.73%, 01/17/28(b)(c) | | | 250 | | | | 234,420 | |

Carlyle U.S. CLO Ltd., Series 2018-4A, Class A2, (3 mo. LIBOR US + 1.80%),

6.04%, 01/20/31(b)(c) | | | 250 | | | | 234,924 | |

Carrington Mortgage Loan Trust(b) | | | | | | | | |

| Series 2006-FRE2, Class A2, (1 mo. LIBOR US + 0.12%), 3.71%, 10/25/36 | | | 3,030 | | | | 2,436,047 | |

Series 2006-FRE2, Class A5, (1 mo. LIBOR US + 0.08%), 3.67%, 03/25/35(d) | | | 6,241 | | | | 5,020,085 | |

CarVal CLO III Ltd., Series 2019-2A, Class E, (3 mo. LIBOR US + 6.44%),

10.68%, 07/20/32(b)(c) | | | 500 | | | | 415,100 | |

C-BASS Trust, Series 2006-CB7, Class A4, (1 mo. LIBOR US + 0.32%),

3.91%, 10/25/36(b) | | | 4,346 | | | | 2,860,216 | |

CIFC Funding 2020-I Ltd., Series 2020-1A, Class DR, (3 mo. LIBOR US + 3.10%),

7.18%, 07/15/36(b)(c) | | | 500 | | | | 433,696 | |

CIFC Funding 2022-VII Ltd., 0.00%, 10/22/35(e) | | | 750 | | | | 737,500 | |

CIFC Funding Ltd., Class 1A, (3 mo. LIBOR US + 1.70%), 5.98%, 10/21/31(b)(c) | | | 750 | | | | 701,445 | |

| Citigroup Mortgage Loan Trust, Series 2006-FX1, Class A7, 5.78%, 10/25/36 | | | 346 | | | | 222,746 | |

Clear Creek CLO, Series 2015-1A, Class DR, (3 mo. LIBOR US + 2.95%),

7.19%, 10/20/30(b)(c) | | | 250 | | | | 219,191 | |

Countrywide Asset-Backed Certificates Trust, Series 2006-26, Class 1A, (1 mo. LIBOR US + 0.14%),

3.73%, 06/25/37(b) | | | 546 | | | | 494,457 | |

CWHEQ Revolving Home Equity Loan Trust, Series 2006-I, Class 1A, (1 mo. LIBOR US + 0.14%),

3.55%, 01/15/37(b) | | | 471 | | | | 428,490 | |

Dryden 106 CLO Ltd.,

5.78%, 10/15/35(a)(e) | | | 500 | | | | 480,000 | |

Elevation CLO Ltd., Series 2021-12A, Class E, (3 mo. LIBOR US + 7.27%),

11.51%, 04/20/32(b)(c) | | | 250 | | | | 203,882 | |

Elmwood CLO IV Ltd., Series 2020-1A, Class B, (3 mo. LIBOR US + 1.70%),

5.78%, 04/15/33(b)(c) | | | 250 | | | | 236,899 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

| Asset-Backed Securities (continued) | |

FirstKey Homes Trust, Series 2022-SFR1, Class E1,

5.00%, 05/17/39(c) | | USD | 3,800 | | | $ | 3,309,300 | |

Fremont Home Loan Trust(b) | | | | | | | | |

| Series 2006-A, Class 2A3, (1 mo. LIBOR US + 0.32%), 3.91%, 05/25/36 | | | 4,220 | | | | 2,418,603 | |

| Series 2006-D, Class 2A3, (1 mo. LIBOR US + 0.15%), 3.74%, 11/25/36 | | | 6,407 | | | | 2,334,505 | |

Galaxy XXI CLO Ltd., Series 2015-21A, Class ER, (3 mo. LIBOR US + 5.25%),

9.49%, 04/20/31(b)(c) | | | 500 | | | | 402,654 | |

Generate CLO 2 Ltd., Series 2015-1A, Class ER, (3 mo. LIBOR US + 5.65%),

9.97%, 01/22/31(b)(c) | | | 250 | | | | 211,522 | |

Goldentree Loan Management U.S. CLO 5 Ltd., Series 2019-5A, Class BR, (3 mo. LIBOR US + 1.55%),

5.79%, 10/20/32(b)(c) | | | 250 | | | | 234,541 | |

Gulf Stream Meridian 1 Ltd., Series 2020-IA, Class E, (3 mo. LIBOR US + 6.45%),

10.53%, 04/15/33(b)(c) | | | 500 | | | | 421,161 | |

Home Equity Mortgage Loan Asset-Backed Trust, Series 2006-E, Class 2A3, (1 mo. LIBOR US + 0.17%),

3.76%, 04/25/37(b) | | | 3,504 | | | | 2,381,167 | |

HPS Loan Management Ltd., Series 8A-2016, Class ER,

(3 mo. LIBOR US + 5.50%), 9.74%, 07/20/30(b)(c) | | | 1,000 | | | | 768,665 | |

Jay Park CLO Ltd., Series 2016-1A, Class CR, (3 mo. LIBOR US + 2.65%),

6.89%, 10/20/27(b)(c) | | | 250 | | | | 228,317 | |

LCM XXIV Ltd., Series 24A, Class AR, (3 mo. LIBOR US + 0.98%), 5.22%, 03/20/30(b)(c) | | | 243 | | | | 236,998 | |

Long Beach Mortgage Loan Trust, Series 2006-7, Class 2A3, (1 mo. LIBOR US + 0.32%),

3.91%, 08/25/36(b) | | | 5,173 | | | | 2,156,740 | |

Madison Park Funding XVII Ltd., Series 2015-17A, Class DR, (3 mo. LIBOR US + 3.60%),

7.88%, 07/21/30(b)(c) | | | 500 | | | | 453,633 | |

Madison Park Funding XXIX Ltd.(b)(c) | | | | | | | | |

Series 2018-29A, Class D, (3 mo. LIBOR US + 3.00%),

7.19%, 10/18/30 | | | 565 | | | | 497,339 | |

Series 2018-29A, Class E, (3 mo. LIBOR US + 5.70%),

9.89%, 10/18/30 | | | 500 | | | | 426,215 | |

Mastr Asset-Backed Securities Trust, Series 2006-HE2,

Class A3, (1 mo. LIBOR US + 0.30%), 3.89%, 06/25/36(b) | | | 7,252 | | | | 2,843,623 | |

Neuberger Berman CLO XX Ltd., Series 2015-20A, Class ERR,

(3 mo. LIBOR US + 6.50%), 10.58%, 07/15/34(b)(c) | | | 710 | | | | 598,274 | |

Neuberger Berman Loan Advisers CLO 37 Ltd., Series 2020-37A, Class CR, (3 mo. LIBOR US + 1.80%),

6.04%, 07/20/31(b)(c) | | | 400 | | | | 370,131 | |

Neuberger Berman Loan Advisers CLO Ltd., Series 2021-46A, Class B, (3 mo. LIBOR US + 1.65%),

5.89%, 01/20/36(b)(c) | | | 250 | | | | 237,113 | |

Octagon Investment Partners 31 Ltd., Series 2017-1A, Class E, (3 mo. LIBOR US + 6.30%),

10.54%, 07/20/30(b)(c) | | | 500 | | | | 406,924 | |

Octagon Investment Partners XVII Ltd., Series 2013-1A, Class BR2, (3 mo. LIBOR US + 1.40%),

5.76%, 01/25/31(b)(c) | | | 250 | | | | 237,129 | |

Octagon Investment Partners XXII Ltd., Series 2014-1A, Class DRR, (3 mo. LIBOR US + 2.75%),

7.07%, 01/22/30(b)(c) | | | 500 | | | | 425,998 | |

OZLM XXI Ltd., Series 2017-21A, Class D, (3 mo. LIBOR US + 5.54%),

9.78%, 01/20/31(b)(c) | | | 250 | | | | 197,543 | |

| | |

S C H E D U L E O F I N V E S T M E N T S | | 9 |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| |

| Asset-Backed Securities (continued) | | | | | |

Rad CLO 6 Ltd., Series 2019-6A,

Class E, (3 mo. LIBOR US + 7.53%), 11.77%, 01/20/33(b)(c) | | USD | 500 | | | $ | 434,268 | |

Rad CLO Ltd., Series 2022-17A,

Class E, (3 mo. SOFR + 8.30%), 12.26%, 10/20/35(a)(b)(c) | | | 250 | | | | 245,000 | |

Regional Management Issuance, 3.88%, 10/17/33(a) | | | 1,110 | | | | 943,500 | |

| Renaissance Home Equity Loan Trust, Series 2007-3, Class AF2, 7.00%, 09/25/37 | | | 3,603 | | | | 1,656,460 | |

Rockford Tower CLO Ltd., Series 2017-2A, Class DR,

(3 mo. LIBOR US + 2.85%), 6.93%, 10/15/29(b)(c) | | | 500 | | | | 446,254 | |

Saxon Asset Securities Trust, Series 2007-3, Class 2A3, (1 mo. LIBOR US + 0.40%), 3.99%, 09/25/47(b) | | | 3,798 | | | | 3,491,353 | |

Scholar Funding Trust, Series 2013-A, Class R, 0.00%, 01/30/45(a) | | | — | (f) | | | 922,662 | |

Stratus CLO Ltd., 0.00%, 10/20/31(e) | | | 500 | | | | 485,000 | |

TICP CLO VII Ltd., Series 2017-7A, Class ER,

(3 mo. LIBOR US + 7.05%), 11.13%, 04/15/33(b)(c) | | | 250 | | | | 223,052 | |

TICP CLO VIII Ltd., Series 2017-8A, Class A2R, (3 mo. LIBOR US + 1.70%),

5.94%, 10/20/34(b)(c) | | | 250 | | | | 235,130 | |

Trestles CLO IV Ltd., (3 mo. LIBOR US + 1.70%), 5.98%, 07/21/34(b)(c) | | | 1,000 | | | | 930,433 | |

Trestles CLO Ltd., Series 2017-1A, Class CR,

(3 mo. LIBOR US + 2.90%),

7.26%, 04/25/32(b)(c) | | | 250 | | | | 212,470 | |

Unique Pub Finance Co. PLC(g) | | | | | | | | |

| Series M, 7.40%, 03/28/24 | | GBP | 1,687 | | | | 1,913,970 | |

| Series N, 6.46%, 03/30/32 | | | 50 | | | | 58,205 | |

| Voya CLO Ltd., 7.23%, 07/15/34 | | USD | 250 | | | | 216,701 | |

WaMu Asset-Backed Certificates Trust, Series 2007- HE3, Class 2A3, (1 mo. LIBOR US + 0.24%),

3.83%, 05/25/37(b) | | | 5,867 | | | | 4,714,310 | |

Whetstone Park CLO Ltd., Classs 1A,

(3 mo. LIBOR US + 1.60%), 5.84%, 01/20/35(b)(c) | | | 275 | | | | 257,943 | |

York CLO 1 Ltd., Series 2014-1A, Class DRR,

(3 mo. LIBOR US + 3.01%),

7.33%, 10/22/29(b)(c) | | | 250 | | | | 229,294 | |

| | | | | | | | |

| |

Total Asset-Backed Securities — 11.5%

(Cost: $69,548,293) | | | | 63,792,797 | |

| | | | | | | | |

| | |

| | | Shares | | | | |

| | |

| Common Stocks | | | | | | | | |

| | |

| Aerospace & Defense — 0.4% | | | | | | |

| Raytheon Technologies Corp. | | | 25,650 | | | | 2,432,133 | |

| | | | | | | | |

| | |

| Building Products — 0.2% | | | | | | |

| Carrier Global Corp. | | | 25,650 | | | | 1,019,844 | |

| | | | | | | | |

| | |

| Machinery — 0.2% | | | | | | |

| Otis Worldwide Corp. | | | 12,825 | | | | 905,958 | |

| | | | | | | | |

| | |

Total Common Stocks — 0.8%

(Cost: $2,968,841) | | | | | | | 4,357,935 | |

| | | | | | | | |

| | |

| | | Par (000) | | | | |

| | |

| Corporate Bonds | | | | | | | | |

| | |

| Aerospace & Defense — 3.3% | | | | | | |

Amsted Industries, Inc., 5.63%, 07/01/27(c) | | USD | 185 | | | | 171,125 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

| Aerospace & Defense (continued) | |

| Boeing Co. | | | | | | | | |

5.15%, 05/01/30(d) | | USD | 1,583 | | | $ | 1,462,667 | |

| 3.63%, 02/01/31 | | | 127 | | | | 105,441 | |

Bombardier, Inc.(c) | | | | | | | | |

| 7.50%, 03/15/25 | | | 50 | | | | 49,144 | |

7.13%, 06/15/26(d) | | | 907 | | | | 858,537 | |

7.88%, 04/15/27(d) | | | 781 | | | | 741,739 | |

6.00%, 02/15/28(d) | | | 683 | | | | 607,802 | |

| 7.45%, 05/01/34 | | | 286 | | | | 267,353 | |

Embraer Netherlands Finance BV, 6.95%, 01/17/28(c) | | | 269 | | | | 253,216 | |

F-Brasile SpA/F-Brasile U.S. LLC, Series XR, 7.38%, 08/15/26(c) | | | 464 | | | | 366,560 | |

| Howmet Aerospace, Inc., 5.13%, 10/01/24 | | | 2 | | | | 1,975 | |

Lockheed Martin Corp., 4.09%, 09/15/52(d) | | | 451 | | | | 360,584 | |

Northrop Grumman Corp., 3.85%, 04/15/45(d) | | | 530 | | | | 401,515 | |

Raytheon Technologies Corp., 3.75%, 11/01/46(d) | | | 700 | | | | 512,406 | |

Rolls-Royce PLC, 5.75%, 10/15/27(c) | | | 1,545 | | | | 1,398,179 | |

Spirit AeroSystems, Inc.(c) | | | | | | | | |

| 5.50%, 01/15/25 | | | 236 | | | | 227,740 | |

| 7.50%, 04/15/25 | | | 40 | | | | 38,862 | |

| TransDigm, Inc. | | | | | | | | |

8.00%, 12/15/25(c) | | | 825 | | | | 839,437 | |

6.25%, 03/15/26(c)(d) | | | 7,356 | | | | 7,256,032 | |

| 6.38%, 06/15/26 | | | 58 | | | | 55,970 | |

| 7.50%, 03/15/27 | | | 134 | | | | 132,041 | |

| 4.63%, 01/15/29 | | | 715 | | | | 608,844 | |

4.88%, 05/01/29(d) | | | 382 | | | | 324,797 | |

Triumph Group, Inc., 8.88%, 06/01/24(c) | | | 1,055 | | | | 1,066,352 | |

| | | | | | | | |

| | |

| | | | | | | 18,108,318 | |

| | |

| Airlines — 2.0% | | | | | | |

Air Canada, 3.88%, 08/15/26(c) | | | 495 | | | | 437,986 | |

Allegiant Travel Co., 7.25%, 08/15/27(c) | | | 147 | | | | 138,186 | |

| American Airlines Pass-Through Trust, | | | | | | | | |

Series 2013-2, Class A, 4.95%, 07/15/24(d) | | | 403 | | | | 398,656 | |

American Airlines, Inc., 11.75%, 07/15/25(c) | | | 582 | | | | 636,488 | |

American Airlines, Inc./AAdvantage Loyalty IP Ltd.(c) | | | | | | | | |

| 5.50%, 04/20/26 | | | 219 | | | | 208,348 | |

| 5.75%, 04/20/29 | | | 1,343 | | | | 1,222,175 | |

Avianca Midco 2 PLC, 9.00%, 12/01/28(c) | | | 304 | | | | 226,617 | |

| Azul Investments LLP | | | | | | | | |

5.88%, 10/26/24(g) | | | 200 | | | | 149,500 | |

7.25%, 06/15/26(c) | | | 230 | | | | 144,584 | |

Delta Air Lines, Inc./SkyMiles IP Ltd., 4.75%, 10/20/28(c) | | | 12 | | | | 11,052 | |

Deutsche Lufthansa AG(g) | | | | | | | | |

| 3.75%, 02/11/28 | | EUR | 100 | | | | 82,424 | |

| 3.50%, 07/14/29 | | | 100 | | | | 78,150 | |

Gol Finance SA, 8.00%, 06/30/26(c) | | USD | 200 | | | | 116,000 | |

Hawaiian Brand Intellectual Property Ltd./HawaiianMiles Loyalty Ltd., 5.75%, 01/20/26(c) | | | 317 | | | | 291,852 | |

International Consolidated Airlines Group SA, 3.75%, 03/25/29(g) | | EUR | 100 | | | | 73,130 | |

Mileage Plus Holdings LLC/Mileage Plus Intellectual Property Assets Ltd., 6.50%, 06/20/27(c)(d) | | USD | 900 | | | | 889,868 | |

| United Airlines Pass-Through Trust | | | | | | | | |

Series 2015-1, Class A, 3.70%, 06/01/24(d) | | | 3,570 | | | | 3,560,683 | |

Series 2020-1, Class A, 5.88%, 04/15/29(d) | | | 713 | | | | 688,649 | |

| | |

| 10 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Airlines (continued) | | | | | | |

| United Airlines Pass-Through Trust (continued) | | | | | |

| Series 2020-1, Class B, 4.88%, 07/15/27 | | USD | 46 | | | $ | 42,432 | |

United Airlines, Inc.(c) | | | | | | | | |

4.38%, 04/15/26(d) | | | 747 | | | | 681,755 | |

| 4.63%, 04/15/29 | | | 824 | | | | 704,759 | |

| | | | | | | | |

| | |

| | | | | | | 10,783,294 | |

| | |

| Auto Components — 1.2% | | | | | | |

Aptiv PLC, 4.40%, 10/01/46(d) | | | 280 | | | | 197,166 | |

Clarios Global LP/Clarios U.S. Finance Co.(c) | | | | | |

| 6.25%, 05/15/26 | | | 1,673 | | | | 1,618,628 | |

8.50%, 05/15/27(d) | | | 3,592 | | | | 3,520,160 | |

Dealer Tire LLC/DT Issuer LLC, 8.00%, 02/01/28(c) | | | 408 | | | | 356,836 | |

Dornoch Debt Merger Sub, Inc., 6.63%, 10/15/29(c) | | | 131 | | | | 89,196 | |

Faurecia SE(g) | | | | | | | | |

| 2.75%, 02/15/27 | | EUR | 100 | | | | 84,482 | |

| 3.75%, 06/15/28 | | | 100 | | | | 83,256 | |

| Goodyear Tire & Rubber Co. | | | | | | | | |

| 5.00%, 07/15/29 | | USD | 132 | | | | 114,464 | |

| 5.63%, 04/30/33 | | | 137 | | | | 114,681 | |

IHO Verwaltungs GmbH, (4.63% PIK), 3.88%, 05/15/27(g)(h) | | EUR | 100 | | | | 78,532 | |

ZF Finance GmbH(g) | | | | | | | | |

| 3.00%, 09/21/25 | | | 100 | | | | 90,796 | |

| 2.00%, 05/06/27 | | | 100 | | | | 79,933 | |

| | | | | | | | |

| | |

| | | | | | | 6,428,130 | |

| | |

| Automobiles — 2.0% | | | | | | |

Allison Transmission, Inc., 5.88%, 06/01/29(c) | | USD | 160 | | | | 149,200 | |

| Asbury Automotive Group, Inc. | | | | | | | | |

| 4.50%, 03/01/28 | | | 168 | | | | 145,648 | |

| 4.75%, 03/01/30 | | | 164 | | | | 134,355 | |

5.00%, 02/15/32(c) | | | 201 | | | | 162,056 | |

Carvana Co.(c) | | | | | | | | |

5.50%, 04/15/27(d) | | | 32 | | | | 15,207 | |

4.88%, 09/01/29(d) | | | 185 | | | | 81,863 | |

| 10.25%, 05/01/30 | | | 42 | | | | 25,200 | |

Constellation Automotive Financing PLC, 4.88%, 07/15/27(g) | | GBP | 100 | | | | 73,395 | |

| Ford Motor Co. | | | | | | | | |

0.00%, 03/15/26(i)(j) | | USD | 526 | | | | 528,630 | |

3.25%, 02/12/32(d) | | | 797 | | | | 598,404 | |

| 6.10%, 08/19/32 | | | 232 | | | | 212,351 | |

| Ford Motor Credit Co. LLC | | | | | | | | |

| 5.13%, 06/16/25 | | | 397 | | | | 383,026 | |

| 3.38%, 11/13/25 | | | 200 | | | | 181,442 | |

4.39%, 01/08/26(d) | | | 1,250 | | | | 1,153,361 | |

| 2.70%, 08/10/26 | | | 376 | | | | 325,796 | |

4.95%, 05/28/27(d) | | | 519 | | | | 475,124 | |

| 4.13%, 08/17/27 | | | 320 | | | | 284,176 | |

| 3.82%, 11/02/27 | | | 400 | | | | 343,581 | |

| 2.90%, 02/16/28 | | | 376 | | | | 305,230 | |

| 5.11%, 05/03/29 | | | 214 | | | | 191,316 | |

4.00%, 11/13/30(d) | | | 937 | | | | 757,827 | |

| 3.63%, 06/17/31 | | | 617 | | | | 479,825 | |

| General Motors Co. | | | | | | | | |

| 5.40%, 10/15/29 | | | 213 | | | | 197,428 | |

| 5.60%, 10/15/32 | | | 127 | | | | 115,262 | |

6.25%, 10/02/43(d) | | | 2,194 | | | | 1,926,229 | |

General Motors Financial Co., Inc., 4.25%, 05/15/23(d) | | | 326 | | | | 323,930 | |

Group 1 Automotive, Inc., 4.00%, 08/15/28(c) | | | 59 | | | | 48,521 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Automobiles (continued) | | | | | | |

Jaguar Land Rover Automotive PLC, 4.50%, 07/15/28(g) | | EUR | 100 | | | $ | 70,954 | |

Ken Garff Automotive LLC, 4.88%, 09/15/28(c) | | USD | 156 | | | | 129,515 | |

LCM Investments Holdings II LLC, 4.88%, 05/01/29(c) | | | 373 | | | | 314,633 | |

Lithia Motors, Inc., 3.88%, 06/01/29(c) | | | 167 | | | | 134,552 | |

MajorDrive Holdings IV LLC, 6.38%, 06/01/29(c) | | | 228 | | | | 160,672 | |

| Penske Automotive Group, Inc. | | | | | | | | |

| 3.50%, 09/01/25 | | | 104 | | | | 96,676 | |

| 3.75%, 06/15/29 | | | 87 | | | | 71,423 | |

Renault SA, 2.38%, 05/25/26(g) | | EUR | 100 | | | | 87,535 | |

Sonic Automotive, Inc., 4.63%, 11/15/29(c) | | USD | 76 | | | | 59,502 | |

TML Holdings Pte. Ltd., 4.35%, 06/09/26(g) | | | 200 | | | | 160,288 | |

Wabash National Corp., 4.50%, 10/15/28(c) | | | 281 | | | | 236,221 | |

| | | | | | | | |

| | |

| | | | | | | 11,140,354 | |

| | |

| Banks — 1.4% | | | | | | |

Banco Bilbao Vizcaya Argentaria SA, (5 year USD Swap + 3.87%), 6.13%(b)(k) | | | 2,000 | | | | 1,535,831 | |

Banco BPM SpA, (5 year EUR Swap + 3.17%), 2.88%, 06/29/31(b)(g) | | EUR | 100 | | | | 78,094 | |

| Bangkok Bank PCL, (5 year CMT + 4.73%), 5.00% | | USD | 205 | | | | 180,554 | |

BBK BSC, 5.50%, 07/09/24(g) | | | 289 | | | | 278,849 | |

Chong Hing Bank Ltd., (5 year CMT + 3.86%), 5.70%(b)(g)(k) | | | 250 | | | | 225,281 | |

Commerzbank AG, (5 year EUR Swap + 6.36%), 6.13%(b)(g)(k) | | EUR | 200 | | | | 173,932 | |

Grupo Aval Ltd., 4.38%, 02/04/30(c) | | USD | 512 | | | | 353,376 | |

Intesa Sanpaolo SpA(c) | | | | | | | | |

| 5.02%, 06/26/24 | | | 2,888 | | | | 2,726,241 | |

| 5.71%, 01/15/26 | | | 200 | | | | 186,307 | |

NBK Tier 1 Ltd., (6 year USD Swap + 2.88%), 3.63%(b)(c)(k) | | | 556 | | | | 460,194 | |

Northern Trust Corp., 6.13%, 11/02/32(e) | | | 300 | | | | 300,245 | |

| PNC Financial Services Group, Inc., 6.04%, 10/28/33 | | | 245 | | | | 246,181 | |

Standard Chartered PLC, (5 year USD ICE Swap + 1.97%), 4.87%, 03/15/33(b)(c) | | | 500 | | | | 423,621 | |

Wells Fargo & Co., Series BB, (5 year CMT + 3.45%), 3.90%(b)(d)(k) | | | 465 | | | | 394,785 | |

| | | | | | | | |

| | |

| | | | | | | 7,563,491 | |

| | |

| Beverages — 1.8% | | | | | | |

Anheuser-Busch Cos. LLC/Anheuser-Busch InBev Worldwide, Inc., 4.90%, 02/01/46(d) | | | 2,160 | | | | 1,852,573 | |

ARD Finance SA, (6.50% Cash or 7.25% PIK), 6.50%, 06/30/27(c)(h) | | | 865 | | | | 620,316 | |

| Ardagh Metal Packaging Finance USA LLC/Ardagh | | | | | | | | |

Metal Packaging Finance PLC(c) | | | | | | | | |

| 6.00%, 06/15/27 | | | 736 | | | | 706,244 | |

| 3.25%, 09/01/28 | | | 200 | | | | 163,981 | |

4.00%, 09/01/29(d) | | | 2,668 | | | | 2,023,918 | |

| Ball Corp. | | | | | | | | |

| 5.25%, 07/01/25 | | | 44 | | | | 43,428 | |

| 2.88%, 08/15/30 | | | 46 | | | | 35,724 | |

3.13%, 09/15/31(d) | | | 481 | | | | 368,302 | |

Canpack SA/Canpack U.S. LLC, 3.13%, 11/01/25(c) | | | 211 | | | | 183,834 | |

| Crown Cork & Seal Co., Inc., 7.38%, 12/15/26 | | | 45 | | | | 45,487 | |

Mauser Packaging Solutions Holding Co., 5.50%, 04/15/24(c) | | | 1,030 | | | | 1,009,400 | |

OI European Group BV, 2.88%, 02/15/25(g) | | EUR | 100 | | | | 92,678 | |

| Silgan Holdings, Inc., 4.13%, 02/01/28 | | USD | 105 | | | | 96,075 | |

| | |

S C H E D U L E O F I N V E S T M E N T S | | 11 |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Beverages (continued) | | | | | | |

Trivium Packaging Finance BV(c) | | | | | | | | |

| 5.50%, 08/15/26 | | USD | 1,189 | | | $ | 1,093,523 | |

| 8.50%, 08/15/27 | | | 1,924 | | | | 1,808,966 | |

| | | | | | | | |

| | |

| | | | | | | 10,144,449 | |

| | |

| Biotechnology — 0.2% | | | | | | |

Amgen, Inc., 2.80%, 08/15/41(d) | | | 250 | | | | 167,291 | |

Cidron Aida Finco SARL, 5.00%, 04/01/28(g) | | EUR | 100 | | | | 77,376 | |

Gilead Sciences, Inc., 4.75%, 03/01/46(d) | | USD | 700 | | | | 601,322 | |

| | | | | | | | |

| | |

| | | | | | | 845,989 | |

| | |

| Building Materials(c) — 0.5% | | | | | | |

| Camelot Return Merger Sub, Inc., 8.75%, 08/01/28 | | | 269 | | | | 223,942 | |

| Jeld-Wen, Inc., 6.25%, 05/15/25 | | | 189 | | | | 176,715 | |

| Masonite International Corp. | | | | | | | | |

| Class C, 5.38%, 02/01/28 | | | 161 | | | | 147,389 | |

| Class C, 3.50%, 02/15/30 | | | 273 | | | | 216,953 | |

| New Enterprise Stone & Lime Co., Inc. | | | | | | | | |

| 5.25%, 07/15/28 | | | 103 | | | | 89,610 | |

| 9.75%, 07/15/28 | | | 48 | | | | 41,199 | |

| Smyrna Ready Mix Concrete LLC, 6.00%, 11/01/28 | | | 643 | | | | 540,120 | |

| Standard Industries, Inc. | | | | | | | | |

| 5.00%, 02/15/27 | | | 94 | | | | 85,070 | |

| 4.75%, 01/15/28 | | | 115 | | | | 100,769 | |

| 4.38%, 07/15/30 | | | 1,082 | | | | 874,851 | |

| 3.38%, 01/15/31 | | | 384 | | | | 287,309 | |

| Summit Materials LLC/Summit Materials Finance Corp., 5.25%, 01/15/29 | | | 227 | | | | 207,299 | |

| | | | | | | | |

| | |

| | | | | | | 2,991,226 | |

| | |

| Building Products — 0.8% | | | | | | |

Advanced Drainage Systems, Inc.(c) | | | | | | | | |

| 5.00%, 09/30/27 | | | 259 | | | | 240,155 | |

| 6.38%, 06/15/30 | | | 636 | | | | 614,624 | |

Beacon Roofing Supply, Inc., 4.13%, 05/15/29(c) | | | 159 | | | | 131,569 | |

Foundation Building Materials, Inc., 6.00%, 03/01/29(c) | | | 139 | | | | 96,029 | |

GYP Holdings III Corp., 4.63%, 05/01/29(c) | | | 300 | | | | 236,918 | |

LBM Acquisition LLC, 6.25%, 01/15/29(c) | | | 157 | | | | 109,818 | |

Lowe’s Cos., Inc., 4.65%, 04/15/42(d) | | | 400 | | | | 327,177 | |

Specialty Building Products Holdings LLC/SBP Finance Corp., 6.38%, 09/30/26(c) | | | 111 | | | | 89,166 | |

SRS Distribution, Inc.(c) | | | | | | | | |

| 4.63%, 07/01/28 | | | 661 | | | | 580,384 | |

| 6.13%, 07/01/29 | | | 606 | | | | 492,777 | |

6.00%, 12/01/29(d) | | | 503 | | | | 410,121 | |

White Cap Buyer LLC, 6.88%, 10/15/28(c)(d) | | | 1,067 | | | | 904,283 | |

White Cap Parent LLC, (8.25% PIK),

8.25%, 03/15/26(c)(h) | | | 324 | | | | 273,780 | |

| | | | | | | | |

| | |

| | | | | | | 4,506,801 | |

| | |

| Capital Markets — 1.4% | | | | | | |

| Blackstone Private Credit Fund, 3.25%, 03/15/27 | | | 97 | | | | 80,476 | |

Charles Schwab Corp., Series H, (10 year CMT + 3.08%), 4.00%(b)(d)(k) | | | 1,060 | | | | 787,315 | |

Compass Group Diversified Holdings LLC, 5.25%, 04/15/29(c) | | | 273 | | | | 234,780 | |

| GLP Capital LP/GLP Financing II, Inc., 3.25%, 01/15/32 | | | 355 | | | | 264,620 | |

Icahn Enterprises LP/Icahn Enterprises Finance Corp.

6.25%, 05/15/26 | | | 534 | | | | 512,907 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Capital Markets (continued) | | | | | | |

| Icahn Enterprises LP/Icahn Enterprises Finance Corp. (continued) | | | | | | | | |

| 5.25%, 05/15/27 | | USD | 842 | | | $ | 775,810 | |

| 4.38%, 02/01/29 | | | 378 | | | | 315,581 | |

Intercorp Peru Ltd., 3.88%, 08/15/29(c) | | | 270 | | | | 213,469 | |

Kane Bidco Ltd., 6.50%, 02/15/27(g) | | GBP | 100 | | | | 91,687 | |

NFP Corp.(c) | | | | | | | | |

4.88%, 08/15/28(d) | | USD | 1,027 | | | | 886,003 | |

6.88%, 08/15/28(d) | | | 2,267 | | | | 1,926,236 | |

| 7.50%, 10/01/30 | | | 136 | | | | 129,508 | |

| Owl Rock Capital Corp. | | | | | | | | |

| 3.75%, 07/22/25 | | | 238 | | | | 217,443 | |

| 4.25%, 01/15/26 | | | 22 | | | | 19,896 | |

| 3.40%, 07/15/26 | | | 83 | | | | 70,727 | |

| OWL Rock Core Income Corp. | | | | | | | | |

| 3.13%, 09/23/26 | | | 56 | | | | 46,801 | |

7.75%, 09/16/27(c)(d) | | | 395 | | | | 385,047 | |

Raymond James Financial, Inc., 4.95%, 07/15/46(d) | | | 400 | | | | 338,661 | |

SURAAsset Management SA, 4.88%, 04/17/24(g) | | | 376 | | | | 363,028 | |

| | | | | | | | |

| | |

| | | | | | | 7,659,995 | |

| | |

| Chemicals — 2.1% | | | | | | |

Alpek SAB de CV, 3.25%, 02/25/31(c) | | | 285 | | | | 217,277 | |

Ashland LLC, 3.38%, 09/01/31(c) | | | 373 | | | | 291,828 | |

Avient Corp., 7.13%, 08/01/30(c) | | | 214 | | | | 204,642 | |

Axalta Coating Systems LLC, 3.38%, 02/15/29(c) | | | 745 | | | | 612,297 | |

Axalta Coating Systems LLC/Axalta Coating Systems Dutch Holding B BV, 4.75%, 06/15/27(c) | | | 600 | | | | 546,734 | |

Braskem Idesa SAPI, 6.99%, 02/20/32(c) | | | 305 | | | | 202,102 | |

Celanese U.S. Holdings LLC, 6.17%, 07/15/27(d) | | | 355 | | | | 334,939 | |

| Chemours Co., 4.00%, 05/15/26 | | EUR | 100 | | | | 85,697 | |

Diamond BC BV, 4.63%, 10/01/29(c) | | USD | 712 | | | | 523,042 | |

Element Solutions, Inc.,

3.88%, 09/01/28(c)(d) | | | 1,917 | | | | 1,629,450 | |

Equate Petrochemical BV, 2.63%, 04/28/28(c) | | | 200 | | | | 165,230 | |

| HB Fuller Co., 4.25%, 10/15/28 | | | 141 | | | | 121,965 | |

Herens Holdco SARL, 4.75%, 05/15/28(c) | | | 671 | | | | 549,709 | |

Herens Midco SARL, 5.25%, 05/15/29(g) | | EUR | 100 | | | | 63,841 | |

Illuminate Buyer LLC/Illuminate Holdings IV, Inc., 9.00%, 07/01/28(c) | | USD | 443 | | | | 374,136 | |

Ingevity Corp., 3.88%, 11/01/28(c) | | | 105 | | | | 88,632 | |

Kobe U.S. Midco 2, Inc., (9.25% Cash or 10.00% PIK), 9.25%, 11/01/26(c)(h) | | | 332 | | | | 255,640 | |

LSF11 A5 HoldCo LLC, 6.63%, 10/15/29(c) | | | 144 | | | | 113,508 | |

Minerals Technologies, Inc., 5.00%, 07/01/28(c) | | | 218 | | | | 189,387 | |

Monitchem HoldCo 3 SA, 5.25%, 03/15/25(g) | | EUR | 100 | | | | 90,133 | |

NOVA Chemicals Corp., 4.88%, 06/01/24(c) | | USD | 80 | | | | 77,800 | |

| Sasol Financing USA LLC | | | | | | | | |

| 6.50%, 09/27/28 | | | 290 | | | | 255,798 | |

| 5.50%, 03/18/31 | | | 320 | | | | 239,060 | |

SCIL IV LLC/SCIL USA Holdings LLC, 5.38%, 11/01/26(c)(d) | | | 305 | | | | 242,454 | |

| Scotts Miracle-Gro Co. | | | | | | | | |

| 4.00%, 04/01/31 | | | 220 | | | | 168,542 | |

| 4.38%, 02/01/32 | | | 34 | | | | 25,732 | |

Sherwin-Williams Co., 4.50%, 06/01/47(d) | | | 310 | | | | 245,141 | |

SK Invictus Intermediate II Sarl, 5.00%, 10/30/29(c) | | | 703 | | | | 574,963 | |

WESCO Distribution, Inc.(c) | | | | | | | | |

| 7.13%, 06/15/25 | | | 830 | | | | 838,051 | |

7.25%, 06/15/28(d) | | | 573 | | | | 581,285 | |

WR Grace Holdings LLC(c) | | | | | | | | |

5.63%, 10/01/24(d) | | | 300 | | | | 294,060 | |

| | |

| 12 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Chemicals (continued) | | | | | | |

WR Grace Holdings LLC(c) (continued) | | | | | | | | |

| 4.88%, 06/15/27 | | USD | 62 | | | $ | 54,250 | |

5.63%, 08/15/29(d) | | | 1,508 | | | | 1,165,654 | |

| | | | | | | | |

| | |

| | | | | | | 11,422,979 | |

| |

| Commercial Services & Supplies — 0.8% | | | | |

| ADT Security Corp. | | | | | | | | |

| 4.13%, 06/15/23 | | | 16 | | | | 15,843 | |

4.13%, 08/01/29(c) | | | 35 | | | | 30,013 | |

4.88%, 07/15/32(c) | | | 57 | | | | 48,497 | |

Albion Financing 1 SARL/Aggreko Holdings, Inc., 6.13%, 10/15/26(c) | | | 222 | | | | 189,541 | |

APX Group, Inc., 5.75%, 07/15/29(c) | | | 342 | | | | 269,274 | |

Avis Budget Car Rental LLC/Avis Budget Finance, Inc., 5.38%, 03/01/29(c)(d) | | | 45 | | | | 38,982 | |

Fortress Transportation & Infrastructure Investors LLC(c) | | | | | | | | |

| 6.50%, 10/01/25 | | | 74 | | | | 71,013 | |

5.50%, 05/01/28(d) | | | 396 | | | | 331,110 | |

Herc Holdings, Inc., 5.50%, 07/15/27(c) | | | 428 | | | | 404,995 | |

Hertz Corp.(c) | | | | | | | | |

| 4.63%, 12/01/26 | | | 161 | | | | 137,253 | |

5.00%, 12/01/29(d) | | | 130 | | | | 102,980 | |

Loxam SAS, 4.50%, 02/15/27(g) | | EUR | 101 | | | | 88,548 | |

Metis Merger Sub LLC, 6.50%, 05/15/29(c) | | USD | 158 | | | | 126,798 | |

NESCO Holdings II, Inc.,

5.50%, 04/15/29(c) | | | 305 | | | | 267,354 | |

Prime Security Services Borrower LLC/Prime Finance, Inc.(c) | | | | | | | | |

| 5.25%, 04/15/24 | | | 178 | | | | 177,156 | |

| 5.75%, 04/15/26 | | | 626 | | | | 609,317 | |

6.25%, 01/15/28(d) | | | 201 | | | | 184,716 | |

Ritchie Bros Auctioneers, Inc., 5.38%, 01/15/25(c)(d) | | | 157 | | | | 154,645 | |

Sotheby’s/Bidfair Holdings, Inc., 5.88%, 06/01/29(c) | | | 690 | | | | 576,678 | |

| United Rentals North America, Inc. | | | | | | | | |

| 5.50%, 05/15/27 | | | 173 | | | | 168,795 | |

| 5.25%, 01/15/30 | | | 170 | | | | 157,675 | |

Verisure Holding AB, 3.25%, 02/15/27(g) | | EUR | 100 | | | | 83,937 | |

Williams Scotsman International, Inc.,

4.63%, 08/15/28(c) | | USD | 316 | | | | 285,395 | |

| | | | | | | | |

| | |

| | | | | | | 4,520,515 | |

| | |

| Communications Equipment — 0.5% | | | | | | |

Ciena Corp., 4.00%, 01/31/30(c) | | | 133 | | | | 112,385 | |

CommScope Technologies LLC,

6.00%, 06/15/25(c)(d) | | | 655 | | | | 610,788 | |

CommScope, Inc.(c) | | | | | | | | |

| 6.00%, 03/01/26 | | | 47 | | | | 45,334 | |

| 8.25%, 03/01/27 | | | 222 | | | | 197,092 | |

7.13%, 07/01/28(d) | | | 188 | | | | 159,222 | |

| 4.75%, 09/01/29 | | | 604 | | | | 510,884 | |

Nokia OYJ, 4.38%, 06/12/27(d) | | | 177 | | | | 162,775 | |

Viasat, Inc.(c) | | | | | | | | |

| 5.63%, 09/15/25 | | | 410 | | | | 378,143 | |

| 5.63%, 04/15/27 | | | 87 | | | | 80,438 | |

| 6.50%, 07/15/28 | | | 360 | | | | 300,825 | |

Viavi Solutions, Inc., 3.75%, 10/01/29(c) | | | 454 | | | | 379,040 | |

| | | | | | | | |

| | |

| | | | | | | 2,936,926 | |

| | |

| Construction Materials(c) — 0.2% | | | | | | |

| American Builders & Contractors Supply Co., Inc. | | | | | | | | |

4.00%, 01/15/28(d) | | | 340 | | | | 300,013 | |

| 3.88%, 11/15/29 | | | 76 | | | | 62,426 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Construction Materials (continued) | | | | | | |

| BCPE Empire Holdings, Inc., 7.63%, 05/01/27 | | USD | 166 | | | $ | 151,632 | |

| H&E Equipment Services, Inc., 3.88%, 12/15/28 | | | 76 | | | | 64,218 | |

| IAA, Inc., 5.50%, 06/15/27 | | | 443 | | | | 414,558 | |

| Resideo Funding, Inc., 4.00%, 09/01/29 | | | 77 | | | | 63,140 | |

| Winnebago Industries, Inc., 6.25%, 07/15/28 | | | 98 | | | | 91,194 | |

| | | | | | | | |

| | |

| | | | | | | 1,147,181 | |

| | |

| Consumer Discretionary — 1.2% | | | | | | |

APi Group DE, Inc.(c) | | | | | | | | |

| 4.13%, 07/15/29 | | | 168 | | | | 134,734 | |

| 4.75%, 10/15/29 | | | 128 | | | | 107,915 | |

| Carnival Corp. | | | | | | | | |

10.13%, 02/01/26(g) | | EUR | 100 | | | | 96,601 | |

10.50%, 02/01/26(c) | | USD | 614 | | | | 601,695 | |

7.63%, 03/01/26(c) | | | 91 | | | | 68,427 | |

5.75%, 03/01/27(c)(d) | | | 1,110 | | | | 769,213 | |

9.88%, 08/01/27(c) | | | 335 | | | | 312,388 | |

4.00%, 08/01/28(c) | | | 652 | | | | 525,300 | |

6.00%, 05/01/29(c) | | | 325 | | | | 215,562 | |

CoreLogic, Inc., 4.50%, 05/01/28(c) | | | 657 | | | | 441,959 | |

Legends Hospitality Holding Co. LLC/Legends Hospitality Co.-Issuer, Inc., 5.00%, 02/01/26(c) | | | 114 | | | | 99,750 | |

Life Time, Inc.(c) | | | | | | | | |

| 5.75%, 01/15/26 | | | 329 | | | | 305,970 | |

| 8.00%, 04/15/26 | | | 276 | | | | 240,632 | |

Lindblad Expeditions LLC, 6.75%, 02/15/27(c) | | | 389 | | | | 346,053 | |

NCL Corp. Ltd.(c) | | | | | | | | |

| 5.88%, 03/15/26 | | | 324 | | | | 265,275 | |

| 7.75%, 02/15/29 | | | 86 | | | | 68,510 | |

NCL Finance Ltd., 6.13%, 03/15/28(c) | | | 333 | | | | 258,908 | |

Royal Caribbean Cruises Ltd.(c) | | | | | | | | |

| 11.50%, 06/01/25 | | | 154 | | | | 165,853 | |

| 4.25%, 07/01/26 | | | 92 | | | | 73,145 | |

| 5.50%, 08/31/26 | | | 116 | | | | 94,842 | |

| 5.38%, 07/15/27 | | | 173 | | | | 134,476 | |

| 11.63%, 08/15/27 | | | 229 | | | | 219,597 | |

| 5.50%, 04/01/28 | | | 92 | | | | 70,840 | |

| 8.25%, 01/15/29 | | | 251 | | | | 250,178 | |

| 9.25%, 01/15/29 | | | 427 | | | | 433,405 | |

Viking Ocean Cruises Ship VII Ltd., 5.63%, 02/15/29(c) | | | 224 | | | | 174,615 | |

| | | | | | | | |

| | |

| | | | | | | 6,475,843 | |

| | |

| Consumer Finance — 1.7% | | | | | | |

American Express Co., (5 year CMT + 2.85%), 3.55%(b)(d)(k) | | | 940 | | | | 724,975 | |

Block, Inc., 3.50%, 06/01/31(d) | | | 2,304 | | | | 1,854,720 | |

| Global Payments, Inc. | | | | | | | | |

4.95%, 08/15/27(d) | | | 130 | | | | 123,522 | |

| 3.20%, 08/15/29 | | | 139 | | | | 115,536 | |

| 5.40%, 08/15/32 | | | 178 | | | | 164,300 | |

HealthEquity, Inc., 4.50%, 10/01/29(c) | | | 865 | | | | 755,794 | |

Iron Mountain U.K. PLC, 3.88%, 11/15/25(g) | | GBP | 100 | | | | 102,604 | |

MPH Acquisition Holdings LLC, 5.50%, 09/01/28(c) | | USD | 280 | | | | 241,710 | |

| Navient Corp. | | | | | | | | |

7.25%, 09/25/23(d) | | | 91 | | | | 91,268 | |

| 6.13%, 03/25/24 | | | 105 | | | | 103,054 | |

| 5.88%, 10/25/24 | | | 76 | | | | 73,497 | |

| 5.50%, 03/15/29 | | | 268 | | | | 212,626 | |

| OneMain Finance Corp. | | | | | | | | |

| 6.88%, 03/15/25 | | | 263 | | | | 255,110 | |

| 7.13%, 03/15/26 | | | 389 | | | | 374,607 | |

| | |

S C H E D U L E O F I N V E S T M E N T S | | 13 |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Consumer Finance (continued) | | | | | | |

| OneMain Finance Corp. (continued) | | | | | | | | |

| 3.50%, 01/15/27 | | USD | 389 | | | $ | 318,830 | |

| 6.63%, 01/15/28 | | | 285 | | | | 258,903 | |

| 5.38%, 11/15/29 | | | 131 | | | | 107,420 | |

| 4.00%, 09/15/30 | | | 141 | | | | 106,455 | |

Sabre Global, Inc.(c) | | | | | | | | |

| 9.25%, 04/15/25 | | | 229 | | | | 221,762 | |

| 7.38%, 09/01/25 | | | 336 | | | | 315,397 | |

Shift4 Payments LLC/Shift4 Payments Finance Sub, Inc., 4.63%, 11/01/26(c) | | | 666 | | | | 613,939 | |

Shift4 Payments, Inc., 0.00%, 12/15/25(i)(j) | | | 219 | | | | 197,511 | |

| SLM Corp., 3.13%, 11/02/26 | | | 221 | | | | 193,832 | |

Verscend Escrow Corp.,

9.75%, 08/15/26(c)(d) | | | 2,007 | | | | 2,013,101 | |

| | | | | | | | |

| | |

| | | | | | | 9,540,473 | |

| | |

| Containers & Packaging — 0.5% | | | | | | |

Clydesdale Acquisition Holdings, Inc.(c) | | | | | | | | |

| 6.63%, 04/15/29 | | | 718 | | | | 681,669 | |

| 8.75%, 04/15/30 | | | 483 | | | | 424,436 | |

| Crown Americas LLC/Crown Americas Capital Corp. V, 4.25%, 09/30/26 | | | 513 | | | | 473,910 | |

| Crown Americas LLC/Crown Americas Capital Corp. VI, 4.75%, 02/01/26 | | | 258 | | | | 246,934 | |

| Graphic Packaging International LLC | | | | | | | | |

4.75%, 07/15/27(c) | | | 104 | | | | 95,728 | |

3.50%, 03/15/28(c) | | | 22 | | | | 19,022 | |

2.63%, 02/01/29(g) | | EUR | 195 | | | | 156,228 | |

3.50%, 03/01/29(c) | | USD | 78 | | | | 65,879 | |

Klabin Austria GmbH, 3.20%, 01/12/31(c) | | | 315 | | | | 235,463 | |

LABL, Inc., 5.88%, 11/01/28(c) | | | 332 | | | | 288,395 | |

Sealed Air Corp.(c) | | | | | | | | |

| 5.13%, 12/01/24 | | | 54 | | | | 53,190 | |

| 4.00%, 12/01/27 | | | 92 | | | | 81,943 | |

| | | | | | | | |

| | |

| | | | | | | 2,822,797 | |

| | |

| Diversified Consumer Services — 1.8% | | | | | | |

Allied Universal Holdco LLC/Allied Universal Finance Corp.(c) | | | | | | | | |

| 6.63%, 07/15/26 | | | 2,652 | | | | 2,532,766 | |

9.75%, 07/15/27(d) | | | 812 | | | | 705,961 | |

6.00%, 06/01/29(d) | | | 1,655 | | | | 1,149,063 | |

Allied Universal Holdco LLC/Allied Universal Finance Corp./Atlas Luxco 4 SARL, 4.63%, 06/01/28(c) | | | 1,610 | | | | 1,333,420 | |

Clarivate Science Holdings Corp.(c) | | | | | | | | |

| 3.88%, 07/01/28 | | | 1,281 | | | | 1,098,559 | |

4.88%, 07/01/29(d) | | | 589 | | | | 491,079 | |

Garda World Security Corp., 4.63%, 02/15/27(c) | | | 183 | | | | 162,524 | |

Graham Holdings Co., 5.75%, 06/01/26(c) | | | 135 | | | | 131,625 | |

Rekeep SpA, 7.25%, 02/01/26(g) | | EUR | 100 | | | | 86,595 | |

| Service Corp. International | | | | | | | | |

| 5.13%, 06/01/29 | | USD | 107 | | | | 99,666 | |

| 3.38%, 08/15/30 | | | 341 | | | | 275,263 | |

4.00%, 05/15/31(d) | | | 454 | | | | 376,791 | |

Sotheby’s, 7.38%, 10/15/27(c) | | | 1,297 | | | | 1,254,848 | |

| | | | | | | | |

| | |

| | | | | | | 9,698,160 | |

| | |

| Diversified Financial Services — 1.8% | | | | | | |

Acuris Finance U.S., Inc./Acuris Finance SARL, 5.00%, 05/01/28(c) | | | 514 | | | | 416,340 | |

American Express Co., 5.85%, 11/05/27(e) | | | 155 | | | | 154,888 | |

ASG Finance Designated Activity Co.,

7.88%, 12/03/24(c) | | | 262 | | | | 248,900 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

| Diversified Financial Services (continued) | | | | | | |

| Barclays PLC, 5.20%, 05/12/26 | | USD | 200 | | | $ | 182,966 | |

Blackstone Holdings Finance Co. LLC,

5.90%, 11/03/27 | | | 375 | | | | 374,231 | |

BNP Paribas SA, (5 year CMT + 3.34%), 4.63%(b)(c)(k) | | | 1,750 | | | | 1,209,688 | |

| Central Garden & Pet Co. | | | | | | | | |

| 4.13%, 10/15/30 | | | 244 | | | | 201,683 | |

4.13%, 04/30/31(c) | | | 224 | | | | 185,920 | |

Citigroup, Inc.(b)(k) | | | | | | | | |

(5 year CMT + 3.42%), 3.88%(d) | | | 2,000 | | | | 1,642,000 | |

| Series W, (5 year CMT + 3.60%), 4.00% | | | 200 | | | | 168,700 | |

| Series Y, (5 year CMT + 3.00%), 4.15% | | | 630 | | | | 492,090 | |

Deutsche Bank AG, (5 year EURIBOR ICE Swap Rate + 3.30%), 4.00%, 06/24/32(b)(g) | | EUR | 100 | | | | 86,502 | |

Garfunkelux Holdco 3 SA, 7.75%, 11/01/25(g) | | GBP | 100 | | | | 81,609 | |

Global Aircraft Leasing Co. Ltd., (6.50% Cash or 7.25% PIK), 7.25%, 09/15/24(c)(h) | | USD | 285 | | | | 227,888 | |

Goldman Sachs Group, Inc., Series R, (5 year CMT + 3.22%), 4.95%(b)(k) | | | 900 | | | | 811,422 | |

| HSBC Holdings PLC | | | | | | | | |

4.38%, 11/23/26(d) | | | 370 | | | | 335,978 | |

(5 year CMT + 3.25%), 4.70%(b)(d)(k) | | | 465 | | | | 323,496 | |

(5 year CMT + 3.65%), 4.60%(b)(k) | | | 200 | | | | 131,940 | |

7.39%, 11/03/28(b) | | | 350 | | | | 350,298 | |

Intrum AB, 3.00%, 09/15/27(g) | | EUR | 100 | | | | 74,860 | |

ION Trading Technologies SARL, 5.75%, 05/15/28(c) . | | USD | 246 | | | | 197,927 | |

Jefferies Finance LLC/JFIN Co.-Issuer Corp., 5.00%, 08/15/28(c) | | | 415 | | | | 325,787 | |

JPMorgan Chase & Co., (1 day SOFR + 2.58%), 5.72%, 09/14/33(b)(d) | | | 254 | | | | 236,781 | |

Ladder Capital Finance Holdings LLLP/Ladder Capital Finance Corp.(c) | | | | | | | | |

| 4.25%, 02/01/27 | | | 220 | | | | 184,769 | |

| 4.75%, 06/15/29 | | | 85 | | | | 67,657 | |

Lloyds Banking Group PLC, (5 year CMT + 4.82%), 6.75%(b)(k) | | | 515 | | | | 468,998 | |

Operadora de Servicios Mega SA de CV Sofom ER, 8.25%, 02/11/25(c) | | | 501 | | | | 210,044 | |

Spectrum Brands, Inc.(c) | | | | | | | | |

| 5.00%, 10/01/29 | | | 106 | | | | 86,920 | |

| 5.50%, 07/15/30 | | | 198 | | | | 158,948 | |

UBS Group AG, (5 year CMT + 3.31%),

4.38%(b)(c)(k) | | | 210 | | | | 145,877 | |

| | | | | | | | |

| | |

| | | | | | | 9,785,107 | |

| |

| Diversified Telecommunication Services — 2.9% | | | | |

AT&T, Inc.(d) | | | | | | | | |

| 4.65%, 06/01/44 | | | 111 | | | | 88,529 | |

| 4.75%, 05/15/46 | | | 2,545 | | | | 2,075,607 | |

Consolidated Communications, Inc.,

6.50%, 10/01/28(c) | | | 861 | | | | 704,126 | |

Level 3 Financing, Inc.(c) | | | | | | | | |

| 3.40%, 03/01/27 | | | 488 | | | | 420,100 | |

| 4.63%, 09/15/27 | | | 233 | | | | 202,188 | |

4.25%, 07/01/28(d) | | | 941 | | | | 776,325 | |

| 3.63%, 01/15/29 | | | 198 | | | | 150,975 | |

| 3.75%, 07/15/29 | | | 487 | | | | 369,993 | |

| Lumen Technologies, Inc. | | | | | | | | |

4.00%, 02/15/27(c) | | | 1,249 | | | | 1,061,900 | |

4.50%, 01/15/29(c) | | | 833 | | | | 587,225 | |

| Series U, 7.65%, 03/15/42 | | | 149 | | | | 98,709 | |

| | |

| 14 | | 2 0 2 2 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2022 | | BlackRock Multi-Sector Income Trust (BIT) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

| Diversified Telecommunication Services (continued) | |

Oi SA, (10.00% Cash or 8.00% Cash + 4.00% PIK), 10.00%, 07/27/25(h) | | USD | 383 | | | $ | 98,455 | |

SoftBank Group Corp., 4.50%, 04/20/25(g) | | EUR | 100 | | | | 92,359 | |

Sprint Capital Corp.(d) | | | | | | | | |

| 6.88%, 11/15/28 | | USD | 1,778 | | | | 1,834,860 | |

| 8.75%, 03/15/32 | | | 1,090 | | | | 1,279,268 | |

Switch Ltd.(c) | | | | | | | | |

| 3.75%, 09/15/28 | | | 399 | | | | 402,990 | |

| 4.13%, 06/15/29 | | | 788 | | | | 788,394 | |

| Telecom Italia Capital SA | | | | | | | | |

| 6.38%, 11/15/33 | | | 191 | | | | 146,764 | |

6.00%, 09/30/34(d) | | | 569 | | | | 415,216 | |

| 7.20%, 07/18/36 | | | 137 | | | | 106,690 | |

| 7.72%, 06/04/38 | | | 71 | | | | 56,445 | |

| Telecom Italia SpA | | | | | | | | |

5.30%, 05/30/24(c)(d) | | | 202 | | | | 190,036 | |

2.75%, 04/15/25(g) | | EUR | 100 | | | | 90,229 | |

1.63%, 01/18/29(g) | | | 100 | | | | 71,161 | |

Uniti Group LP/Uniti Group Finance, Inc./CSL Capital LLC, 4.75%, 04/15/28(c) | | USD | 116 | | | | 94,824 | |

| Verizon Communications, Inc. | | | | | | | | |

| 4.50%, 08/10/33 | | | 500 | | | | 445,465 | |

3.70%, 03/22/61(d) | | | 1,250 | | | | 817,607 | |

Zayo Group Holdings, Inc.(c)(d) | | | | | | | | |

| 4.00%, 03/01/27 | | | 1,305 | | | | 1,008,112 | |

| 6.13%, 03/01/28 | | | 2,371 | | | | 1,576,715 | |

| | | | | | | | |

| | |

| | | | | | | 16,051,267 | |

| | |

| Education — 0.0% | | | | | | |

| Grand Canyon University, 5.13%, 10/01/28 | | | 249 | | | | 222,544 | |

| | | | | | | | |

| | |

| Electric Utilities — 0.9% | | | | | | |

| Comision Federal de Electricidad, 4.88%, 01/15/24 | | | 323 | | | | 317,347 | |

Duke Energy Corp., 4.80%, 12/15/45(d) | | | 1,500 | | | | 1,211,904 | |

Empresas Publicas de Medellin ESP,

4.25%, 07/18/29(c) | | | 309 | | | | 220,414 | |

Enel Finance International NV, 3.63%, 05/25/27(c)(d) | | | 1,250 | | | | 1,086,996 | |

| FirstEnergy Corp. | | | | | | | | |

| 2.65%, 03/01/30 | | | 110 | | | | 88,926 | |

| Series B, 2.25%, 09/01/30 | | | 27 | | | | 20,782 | |

| Series C, 3.40%, 03/01/50 | | | 777 | | | | 482,711 | |

FirstEnergy Transmission LLC(c) | | | | | | | | |

5.45%, 07/15/44(d) | | | 573 | | | | 496,027 | |

| 4.55%, 04/01/49 | | | 206 | | | | 155,688 | |

NextEra Energy Operating Partners LP(c) | | | | | | | | |

| 4.25%, 07/15/24 | | | 205 | | | | 198,752 | |

| 4.25%, 09/15/24 | | | 11 | | | | 10,352 | |

Virginia Electric and Power Co., Series A, 6.00%, 05/15/37(d) | | | 750 | | | | 742,141 | |

| | | | | | | | |

| | |

| | | | | | | 5,032,040 | |

| | |

| Electrical Equipment(c) — 0.1% | | | | | | |

| Gates Global LLC/Gates Corp., 6.25%, 01/15/26 | | | 572 | | | | 549,120 | |

| GrafTech Finance, Inc., 4.63%, 12/15/28 | | | 176 | | | | 142,560 | |

| | | | | | | | |

| | |

| | | | | | | 691,680 | |

|

| Electronic Equipment, Instruments & Components — 0.6% | |

BWX Technologies, Inc.(c) | | | | | | | | |

| 4.13%, 06/30/28 | | | 22 | | | | 19,250 | |

| 4.13%, 04/15/29 | | | 265 | | | | 229,119 | |

| CDW LLC/CDW Finance Corp. | | | | | | | | |

| 3.28%, 12/01/28 | | | 72 | | | | 58,479 | |

| 3.25%, 02/15/29 | | | 202 | | | | 165,137 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

| Electronic Equipment, Instruments & Components (continued) | |

Corning, Inc., 4.38%, 11/15/57(d) | | USD | 1,915 | | | $ | 1,364,328 | |

Imola Merger Corp., 4.75%, 05/15/29(c) | | | 683 | | | | 588,882 | |

Vertiv Group Corp., 4.13%, 11/15/28(c) | | | 776 | | | | 675,027 | |

| | | | | | | | |

| | |

| | | | | | | 3,100,222 | |

| | |

| Energy Equipment & Services — 0.5% | | | | | | |

Archrock Partners LP/Archrock Partners Finance Corp.(c) | | | | | | | | |

| 6.88%, 04/01/27 | | | 209 | | | | 199,073 | |

6.25%, 04/01/28(d) | | | 1,088 | | | | 1,011,731 | |

| USA Compression Partners LP/USA Compression Finance Corp. | | | | | | | | |

| 6.88%, 04/01/26 | | | 318 | | | | 305,239 | |

| 6.88%, 09/01/27 | | | 657 | | | | 627,435 | |

Vallourec SA, 8.50%, 06/30/26(g) | | EUR | 32 | | | | 30,196 | |

Weatherford International Ltd.(c) | | | | | | | | |

| 11.00%, 12/01/24 | | USD | 11 | | | | 11,306 | |

| 6.50%, 09/15/28 | | | 280 | | | | 267,400 | |

| 8.63%, 04/30/30 | | | 342 | | | | 322,335 | |

| | | | | | | | |

| | |

| | | | | | | 2,774,715 | |

|

| Environmental, Maintenance & Security Service — 0.7% | |

Clean Harbors, Inc.(c)(d) | | | | | | | | |

| 4.88%, 07/15/27 | | | 297 | | | | 279,489 | |

| 5.13%, 07/15/29 | | | 149 | | | | 138,147 | |

| Covanta Holding Corp. | | | | | | | | |

4.88%, 12/01/29(c) | | | 181 | | | | 154,112 | |

| 5.00%, 09/01/30 | | | 91 | | | | 75,787 | |

GFL Environmental, Inc.(c) | | | | | | | | |

| 3.75%, 08/01/25 | | | 176 | | | | 166,320 | |

| 5.13%, 12/15/26 | | | 496 | | | | 472,133 | |

| 4.00%, 08/01/28 | | | 567 | | | | 490,682 | |

| 3.50%, 09/01/28 | | | 259 | | | | 219,585 | |

| 4.75%, 06/15/29 | | | 483 | | | | 420,972 | |

| 4.38%, 08/15/29 | | | 403 | | | | 341,329 | |

Stericycle, Inc., 3.88%, 01/15/29(c) | | | 210 | | | | 182,404 | |

Tervita Corp., 11.00%, 12/01/25(c) | | | 147 | | | | 159,481 | |

Waste Pro USA, Inc., 5.50%, 02/15/26(c) | | | 939 | | | | 868,960 | |

| | | | | | | | |

| | |

| | | | | | | 3,969,401 | |

|

| Equity Real Estate Investment Trusts (REITs) — 1.1% | |

| American Tower Corp. | | | | | | | | |

| 2.70%, 04/15/31 | | | 116 | | | | 90,462 | |