Use these links to rapidly review the document

Table of Contents

TABLE OF CONTENTS

Exhibit 99.2

Annual Report

2018

GRANITE REIT

Table of Contents

Table of Contents

| | |

Letter to Unitholders | | 1 |

Management's Discussion and Analysis of Results of Operations and Financial Position | | 3 |

Management's Responsibility for Financial Reporting | | 64 |

Reports of Independent Registered Public Accounting Firm | | 65 |

Combined Balance Sheets | | 68 |

Combined Statements of Net Income | | 69 |

Combined Statements of Comprehensive Income | | 70 |

Combined Statements of Unitholders' Equity | | 71 |

Combined Statements of Cash Flows | | 72 |

Notes to Combined Financial Statements | | 73 |

Corporate Information | | Inside Back Cover |

| | |

| | 77 King St. W., Suite 4010

P.O. Box 159, TD Centre

Toronto, ON, M5K 1H1 Canada

|

LETTER TO UNITHOLDERS

Dear Unitholders:

2018 was another active and successful year for Granite, underpinned by strong financial results, approval of a new strategic plan, significant progress made towards achieving our strategic objectives and a transition to new leadership.

Granite acquired over $540 million in modern e-commerce and distribution assets, which when combined with the gains generated from the sale of non-core assets, significantly increased net asset value and improved the quality and diversification of the portfolio. As a result of this activity, Granite increased FFO per unit while maintaining overall debt levels and liquidity with which to fund future acquisitions and development.

Organizationally, I was appointed as President and CEO on August 1st, replacing Michael Forsayeth, who retired that same month. Following the annual general meeting in June, the Board also welcomed the election of Jennifer Warren as a trustee. Finally, a new strategic plan was approved by the Board in November, setting the course for Granite over the next five years.

As highlighted below, the initiatives taken in 2018 have strategically positioned Granite to execute on its priorities and continue to deliver strong financial performance for unitholders.

HIGHLIGHTS FOR 2018

Unitholder Return and Increased Distribution

- •

- Granite delivered a total return in 2018 of approximately 13.5% for our unitholders (vs 1.0% for the S&P TSX Capped REIT Index and -12.2% for the S&P TSX) and a 2.9% year-over-year increase in the annual amount distributed to unitholders to $2.80 per unit for 2019, marking our seventh consecutive annual distribution increase.

Strategic Allocation of Capital

- •

- $730 million generated from the sale of 16 non-core assets at an average capitalization rate of 6.7%, contributing to the overall fair value gains on investment properties of approximately $355 million or $7.75 per unit in net asset value;

- •

- $544 million invested in modern assets in key e-commerce and distribution markets in the United States and Germany at an average in-going yield of 5.8%;

- •

- $500 million 5-year unsecured revolving facility, available in Canadian dollars, US dollars or Euros;

- •

- $550 million in unsecured committed term facilities were obtained at a weighted average term of 5.6 years and bearing a weighted average fixed interest rate of 1.76%;

- •

- $63.5 million to repurchase 1.28 million of Granite's stapled units at an average price of $49.55; and

- •

- $628 million of additional commitments made to acquire, construct or develop properties in 2019.

Portfolio Enhancement & Tenant Diversification

- •

- Reduced Magna concentration from 61% to 47% as a percentage of gross leasable area and 71% to 54% as a percentage of annualized revenue.

Financial & Operational Performance

- •

- FFO per unit year-over-year growth of 13.2%, despite the loss of approximately $49 million in annualized revenue from the $730 million in dispositions. AFFO per unit decreased by 2.6% year-over-year;

- •

- Net leverage ratio of 19% providing in excess of $1.2 billion in debt capacity and approximately $1.2 billion in available liquidity;

- •

- 3.2 million square feet of lease expiries renewed or re-leased at an average increase in base rent of 4.6%; and

- •

- Occupancy rate at year end of 99.1%.

Focused Strategy

- •

- A new strategic plan, which sets the course for Granite for the next five years, was approved in November; and

- •

- All employee compensation to be aligned with the achievement of targets and objectives of the strategic plan.

OUTLOOK

As noted above, the actions taken by management and the Board over the past few years have resulted in a strong foundation upon which we can continue to build. With over $1.0 billion in liquidity, Granite is uniquely positioned to capitalize on an active pipeline of development and acquisition opportunities, and continue to make progress towards achieving its strategic objectives.

For the remainder of 2019, Granite will focus on the following priorities:

- •

- Increase scale in target markets;

- •

- Dispose of select non-core assets and exit non-core markets;

- •

- Drive net asset value, FFO and AFFO per unit growth;

- •

- Enhance platform capabilities in Europe and the United States;

- •

- Execute on development projects in Plainfield, IN and Altbach, Germany; and

- •

- Reduce Magna concentration to below 50% as a percentage of revenue.

As we execute on the initiatives above for 2019, we will adhere to our core principle of delivering maximum long-term value for Granite's unitholders. In pursuit of this, we will continue to prioritize total return, net asset value, portfolio quality, platform capability and the maintenance of a conservative capital structure.

On a personal note, this is my first of what I hope to be many letters to Granite's unitholders. It is a privilege to join the Granite team, and I would like to thank the Board of Trustees for providing me with this tremendous opportunity. I would also like to acknowledge Michael Forsayeth and the team for their assistance and support during and after the transition.

Looking forward, all of us at Granite are truly excited about meeting the challenges in front of us and fulfilling our potential.

To our unitholders, I want to thank you for investing in Granite and for your continued support and trust.

Sincerely,

Kevan Gorrie,

President and Chief Executive Officer

FFO, AFFO and related per unit amounts as well as net leverage ratio are not International Financial Reporting Standards ("IFRS") measures. Please refer to the Basis of Presentation and Non-IFRS Measures sections in the attached MD&A for definitions and reconciliations to IFRS measures.

Table of Contents

MANAGEMENT'S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL POSITION |

| | |

Basis of Presentation | |

3 |

Financial and Operating Highlights | |

4 |

Business Overview and Strategic Outlook | |

5 |

Significant Matters | |

7 |

Results of Operations | |

11 |

Investment Properties | |

27 |

Liquidity and Capital Resources | |

36 |

Commitments, Contractual Obligations, Contingencies and Off-Balance Sheet Arrangements | |

44 |

Related Party Transactions | |

45 |

Non-IFRS Measures | |

46 |

Significant Accounting Estimates | |

49 |

New Accounting Pronouncements and Developments | |

51 |

Internal Controls over Financial Reporting | |

54 |

Risks and Uncertainties | |

55 |

Selected Annual and Quarterly Data | |

56 |

Forward-Looking Statements | |

61 |

Management's Discussion and Analysis of Results of Operations and Financial Position ("MD&A") of Granite Real Estate Investment Trust ("Granite REIT") and Granite REIT Inc. ("Granite GP") summarizes the significant factors affecting the combined operating results, financial condition, liquidity and cash flows of Granite REIT, Granite GP and their subsidiaries (collectively "Granite" or the "Trust") for the three month period and year ended December 31, 2018. Unless otherwise noted, all amounts are in millions of Canadian dollars. This MD&A should be read in conjunction with the accompanying audited combined financial statements for the year ended December 31, 2018 prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board. The MD&A was prepared as at March 6, 2019 and its contents were approved by the Board of Trustees of Granite REIT and Board of Directors of Granite GP on this date. Additional information relating to Granite, including the 2018 Annual Information Form ("AIF") dated March 6, 2019, can be obtained from the Trust's website atwww.granitereit.com, on SEDAR atwww.sedar.comand on EDGAR at www.sec.gov.

In addition to using financial measures determined in accordance with IFRS, Granite also uses certain non-IFRS measures in managing its business to measure financial and operating performance as well as for capital allocation decisions and valuation purposes. Granite believes that providing these measures on a supplemental basis to the IFRS results is helpful to investors in assessing the overall performance of Granite's business. These non-IFRS measures include net operating income before lease termination and close-out fees, straight-line rent and tenant incentive amortization ("NOI — cash basis"), same property NOI — cash basis, funds from operations ("FFO"), adjusted funds from operations ("AFFO"), FFO payout ratio, AFFO payout ratio, leverage ratio, interest coverage ratio, net leverage ratio, indebtedness ratio, unencumbered asset coverage ratio and any related per unit amounts. Readers are cautioned that these measures do not have standardized meanings prescribed under IFRS and, therefore, should not be construed as alternatives to net income, cash provided by operating activities or any other measure calculated in accordance with IFRS. Additionally, because these terms do not have standardized meanings prescribed by IFRS, they may not be comparable to similarly titled measures presented by other reporting issuers. Refer to "NON-IFRS MEASURES" for definitions and reconciliations of non-IFRS measures to IFRS financial measures.

Table of Contents

FINANCIAL AND OPERATING HIGHLIGHTS |

| | | | | | | | | | | | | |

| | | | | | | | | | |

| | Three Months Ended

December 31, | | Years Ended

December 31, | |

|---|

(in millions, except as noted)

| | 2018

| | 2017

| | 2018

| | 2017

| |

|---|

| | | | | | | | | | |

Operating highlights | | | | | | | | | |

Revenue(1) | | $ | 59.9 | | $ | 62.6 | | $ | 247.5 | | $ | 244.7 | |

NOI — cash basis(2) | | 52.9 | | 56.2 | | 216.7 | | 218.2 | |

Net income attributable to stapled unitholders | | 85.9 | | 233.6 | | 465.2 | | 357.7 | |

FFO(2)(3) | | 40.9 | | 41.6 | | 168.9 | | 153.2 | |

AFFO(2)(3) | | 39.8 | | 32.6 | | 138.1 | | 145.4 | |

Cash flows provided from operating activities | | 34.7 | | 38.2 | | 157.9 | | 158.7 | |

Monthly distributions paid | | 31.1 | | 30.6 | | 125.1 | | 122.6 | |

FFO payout ratio(2)(4) | | 77% | | 75% | | 78% | | 78% | |

AFFO payout ratio(2)(4) | | 79% | | 95% | | 91% | | 82% | |

Per unit amounts | |

| |

| |

| |

| |

Diluted FFO(2)(3) | | $ | 0.90 | | $ | 0.89 | | $ | 3.68 | | $ | 3.25 | |

Diluted AFFO(2)(3) | | $ | 0.87 | | $ | 0.69 | | $ | 3.01 | | $ | 3.09 | |

Monthly distributions paid | | $ | 0.68 | | $ | 0.65 | | $ | 2.72 | | $ | 2.60 | |

Diluted weighted average number of units | | 45.7 | | 47.0 | | 45.9 | | 47.1 | |

| | | | | | | | | |

As at December 31,

| | 2018

| | 2017

| |

|---|

| | | | | | |

Financial highlights | | | | | | | |

Investment properties — fair value(5) | | | $ | 3,425.0 | | | $ | 2,733.6 | |

Assets held for sale(5) | | | 44.2 | | | 391.4 | |

Cash and cash equivalents | | | 658.2 | | | 69.0 | |

Total debt | | | 1,303.2 | | | 741.4 | |

Trading price per unit (TSX: GRT.UN) | | | $ | 53.21 | | | $ | 49.25 | |

Debt metrics, ratings and outlook | | |

| | |

| |

Net leverage ratio(2) | | | 19% | | | 25% | |

Interest coverage ratio(2) | | | 9.4x | | | 9.5x | |

Weighted average cost of debt | | | 2.17% | | | 2.54% | |

Weighted average debt term-to-maturity, in years | | | 4.7 | | | 4.8 | |

DBRS rating and outlook | | BBB stable | | BBB stable | |

Moody's rating and outlook | | Baa2 stable | | Baa2 stable | |

Property metrics(5) | | |

| | |

| |

Number of investment properties | | | 84 | | | 87 | |

Income-producing properties | | | 80 | | | 84 | |

Properties under development | | | 2 | | | — | |

Land held for development | | | 2 | | | 3 | |

Gross leasable area ("GLA"), square feet | | | 32.2 | | | 29.1 | |

Occupancy, by GLA | | | 99.1% | | | 98.4% | |

Magna as a percentage of annualized revenue(6) | | | 54% | | | 71% | |

Magna as a percentage of GLA | | | 47% | | | 61% | |

Weighted average lease term, in years by GLA | | | 6.0 | | | 5.9 | |

Overall capitalization rate(7) | | | 6.7% | | | 7.6% | |

| | | | | | |

Table of Contents

- (1)

- Granite has retrospectively applied IFRS 15,Revenue from Contracts with Customers (see "NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS") and all historical periods herein have been restated to reflect such treatment.

- (2)

- For definitions of Granite's non-IFRS measures, refer to the section "NON-IFRS MEASURES".

- (3)

- For the year ended December 31, 2018, Granite recognized $1.0 million ($0.02 per unit) in revenue related to a lease termination and close-out fee and a net $8.5 million ($0.19 per unit) foreign exchange gain on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018. For the year ended December 31, 2017, Granite incurred $5.9 million ($0.12 per unit) of expenses in connection with a proxy contest that preceded the June 2017 annual general meeting and recognized $1.6 million ($0.03 per unit) related to lease termination and close-out fees in revenue. FFO, AFFO and the per unit amounts include the aforementioned items.

In the first quarter of 2018, Granite also paid $9.1 million ($0.19 per unit) related to a tenant incentive allowance for a 2014 lease extension at the Eurostar facility in Graz, Austria. AFFO and AFFO per unit amounts have been reduced by this $9.1 million tenant allowance payment. - (4)

- For comparative purposes, the FFO payout ratio and AFFO payout ratio exclude the lease termination and close-out fee of $1.0 million and the net $8.5 million foreign exchange gain on the remeasurement of US dollar cash proceeds from the sale of properties for the year ended December 31, 2018 as well as the lease termination and close-out fees of $1.6 million and the $5.9 million of proxy contest expenses in the prior year. AFFO payout ratio further excludes the $9.1 million tenant incentive payment made in 2018 in connection with the 2014 lease extension at the Eurostar facility.

- (5)

- Assets held for sale are excluded from investment properties and related property metrics. Accordingly, six such assets that were held for sale at December 31, 2018 and 10 such assets that were held for sale at December 31, 2017 were excluded from investment properties and related property metrics at December 31, 2018 and December 31, 2017, respectively, throughout this MD&A.

- (6)

- Annualized revenue for each period presented is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month of December multiplied by twelve months.

- (7)

- Refer to "Valuation Metrics by Investment Property Asset Category" in "Investment Properties" section.

BUSINESS OVERVIEW AND STRATEGIC OUTLOOK |

Business Overview

Granite is a Canadian-based real estate investment trust ("REIT") engaged in the acquisition, development, ownership and management of industrial, warehouse and logistics properties in North America and Europe. As at March 6, 2019, Granite owns 86 investment properties in nine countries having approximately 33.6 million square feet of gross leasable area. The tenant base includes Magna International Inc. and its operating subsidiaries (collectively "Magna") as the largest tenant, in addition to tenants from various other industries. Properties leased to Magna are generally leased to operating subsidiaries of Magna International Inc. and the terms of the leases are not guaranteed by the parent company except for certain leases wherein the parent is the tenant.

Granite's investment properties consist of income-producing properties, properties under development and land held for development (see "INVESTMENT PROPERTIES"). The income-producing properties consist of light industrial properties, heavy industrial manufacturing facilities, warehouse and logistics properties, corporate offices, product development and engineering centres and test facilities. The lease payments are primarily denominated in three currencies: the Canadian dollar ("$"), the Euro ("€") and the US dollar ("US$").

Table of Contents

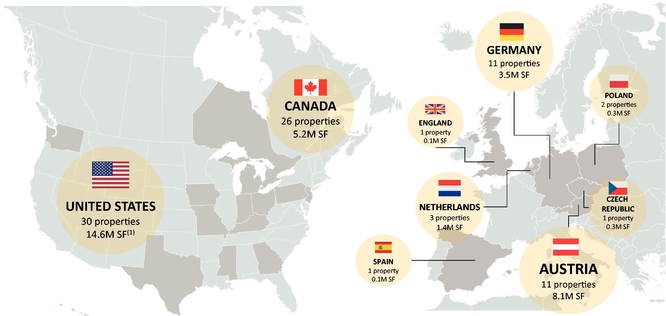

Granite's investment properties (excluding the six assets held for sale) by geographic location, property count and square footage as at March 6, 2019 are summarized below:

Investment Properties Summary

Nine countries/86 properties/33.6(1) million square feet

- (1)

- Includes a 0.3 million square foot expansion completed in West Jefferson, OH and two income-producing properties representing 1.0 million of GLA acquired subsequent to December 31, 2018.

Strategic Outlook

Management continues to identify and pursue value creation opportunities that will build on Granite's current foundation, leverage the balance sheet and invest to grow and diversify the asset base.

Granite's long-term strategy is to continue to build an institutional quality and globally diversified industrial real estate business; to grow and diversify its asset base through acquisitions, development, re-development and dispositions; to optimize its balance sheet; and to reduce its exposure to Magna and the special purpose properties (see "INVESTMENT PROPERTIES") over the long-term.

Following the sale of 16 non-core properties in 2018 (see "SIGNIFICANT MATTERS"), Granite has positioned itself to capitalize on market opportunities within its geographic footprint and execute on its strategy as well as benefit from a net leverage ratio of 19%, liquidity of approximately $1.2 billion and a strong pipeline of acquisition and development opportunities.

As Granite looks to the remainder of 2019, its priorities are as follows:

- •

- Strategically redeploy the proceeds from the recently sold properties and financing initiatives;

- •

- Accelerate growth in its target markets in North America and Europe primarily through property, portfolio and corporate acquisitions as well as through joint venture arrangements and development of modern logistics and e-commerce assets in e-commerce markets;

- •

- Continue to dispose of select non-core assets;

- •

- Maintain a target occupancy in excess of 98%;

- •

- Enhance Granite's global platform;

- •

- Grow net asset value as well as FFO and AFFO per unit; and

- •

- Pursue development opportunities within the existing portfolio.

Executing on these near-term priorities will accelerate the ongoing transformation of Granite into an institutional quality e-commerce and distribution real estate business.

Table of Contents

Property Acquisitions

During the year ended December 31, 2018, Granite acquired seven income-producing modern properties in the United States and one in Germany as well as one property comprised of development land in the United States. Property acquisitions consisted of the following:

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | |

2018 Acquisitions

(in millions, except as noted)

Property Address

| | Location

| | Sq ft(1)

| | Weighted Average

Lease Term,

in years by

sq ft(1)

| | Date Acquired

| | Property

Purchase

Price

| | In-going

Stabilized

Yield(1)

|

|---|

| | | | | | | | | | | | | |

Income-producing properties: | | | | | | | | | | |

3870 Ronald Reagan Parkway | | Plainfield, IN | | | 0.6 | | | 5.8 | | Mar 23, 2018 | | | $ | 50.8 | | 5.3% |

181 Antrim Commons Drive | | Greencastle, PA | | | 0.4 | | | 14.6 | | Apr 4, 2018 | | | 44.3 | | 5.7% |

Ohio portfolio (four properties): | |

| | |

| | |

| |

| | |

| |

|

10, 100 and 115 Enterprise Parkway and 15 Commerce Parkway | | West Jefferson, OH | | | 3.8 | | | 7.0 | | May 23, 2018 | | | 299.3 | | 6.0% |

Joseph-Meyer-Straße 3 | | Erfurt, Germany | | | 0.7 | | | 4.7 | | Jul 12, 2018 | | | 82.7 | | 5.4% |

120 Velocity Way | | Shepherdsville, KY | | | 0.7 | | | 4.8 | | Dec 3, 2018 | | | 65.9 | | 5.7% |

Development land: | | |

| | |

| |

| | |

| |

|

12.9 acres of development land, Lot 18, Park 70 | | West Jefferson, OH | | | N/A | | | N/A | | Nov 1, 2018 | | | 1.2 | | N/A |

| | | | | | | | | | | | | |

Total | | | | | 6.2 | | | 6.8 | | | | | $ | 544.2 | | 5.8% |

| | | | | | | | | | | | | |

- (1)

- As at the date of acquisition

Acquisition, Construction and Development Commitments

Granite had the following property expansion and purchase commitments as well as construction and development commitments:

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

Commitments

(in millions, except as noted)

Property Location

| | Additional

sq ft

| | Payments/

Deposits

Made(1)

| | Future

Commitments

| | Total

Cost

| | Year-One

Stabilized

Yield

|

|---|

| | | | | | | | | | | |

As at December 31, 2018: | | | | | | | |

Expansion at West Jefferson, OH | | 0.3 | | | $ | 20.6 | | | $ | 3.5 | | $ | 24.1 | | 6.1% |

Leasehold interest in two properties in Mississauga, ON | | 0.9 | | | 7.0 | | | 147.0 | | 154.0 | | 4.5% |

Properties under development in Texas and Indiana as well as other construction commitments | | 1.4 | | | 34.5 | | | 306.5 | | 341.0 | | 6.0% |

| | | | | | | | | | | |

| | 2.6 | | | $ | 62.1 | | | $ | 457.0 | | $ | 519.1 | | 5.4% |

Commitments between January 1, 2019 and March 6, 2019: | |

| | |

| | |

| |

| |

|

Two property purchases in Wilmer and Hutchins, TX(2) | |

1.0 | | |

— | | |

168.8 | |

168.8 | |

6.2% |

Demolition phase of property under development in Germany | | — | | | — | | | 1.7 | | 1.7 | | N/A |

| | | | | | | | | | | |

| | 3.6 | | | $ | 62.1 | | | $ | 627.5 | | $ | 689.6 | | 5.6% |

| | | | | | | | | | | |

- (1)

- As at December 31, 2018

- (2)

- Subsequent to December 31, 2018, Granite committed to acquire these properties. On March 1, 2019, Granite purchased the properties for total consideration of $168.8 million.

Table of Contents

Commitments as at December 31, 2018

In January 2019, Granite completed a building expansion at a West Jefferson, Ohio property for $24.1 million (US$17.7 million) that added 0.3 million square feet and is expected to contribute approximately $1.4 million in additional annual revenue upon rent commencement in the first quarter of 2020 subsequent to a rent-free period of approximately one year. Construction of the expansion commenced during the third quarter of 2018 and was substantially completed in January 2019.

A deposit of $7.0 million was made during 2018 to acquire the leasehold interest in two income-producing properties located in Mississauga, Ontario for total consideration of $154.0 million. This commitment to purchase the leasehold interest is subject to customary closing conditions and the consent of the ground lessor. The purchase is expected to close in the second quarter of 2019.

A deposit of $27.3 million (US$20.0 million) was also made during 2018 in connection with a contractual commitment to acquire a property under development in the state of Texas. This commitment to purchase the property under development is subject to specific confidentiality provisions and customary closing conditions including certain purchase rights in favour of the tenant and is expected to close concurrently with the lease commencement in the third quarter of 2019 following construction of the building.

As at December 31, 2018, Granite's commitment to purchase these aforementioned properties and expansion together with additional contractual commitments related to construction and development projects, including the development of a property in Plainfield, Indiana, amounted to approximately $457 million.

Commitments subsequent to December 31, 2018

On March 1, 2019, Granite acquired two properties in the United States for $168.8 million (US$123.7 million). The first property, 201 Sunridge Boulevard, Wilmer, Texas, is a 0.8 million square feet, 30-foot clear height distribution centre situated on 53.4 acres of land. Constructed in 2008, the property is 100% leased to a subsidiary of Unilever for a remaining lease term of 9.5 years. The excess land on the property can support a building expansion of up to 0.3 million square feet, providing attractive site flexibility and the potential for additional income in the future. The second property, 3501 North Lancaster Hutchins Road, Hutchins, Texas, is a 174.6 acre site, containing three buildings totaling 0.2 million square feet. The property is 100% leased to a leading wholesale automotive auction company for a remaining lease term of 10.4 years. The gross leasable area of the existing buildings represents a site coverage ratio of only 2.6%, providing significant potential for future development. Both properties are located within the southeast Dallas-Fort Worth industrial market.

During the first quarter of 2019, Granite entered into an agreement for approximately $1.7 million (€1.1 million) to demolish an existing building on a 15 acre site in Altbach, Germany. As at March 6, 2019, the demolition of the property is almost complete and construction of a 0.3 million square foot distribution/light industrial facility is expected to commence later in 2019.

Table of Contents

2018 Property Dispositions

During the year ended December 31, 2018, 16 properties previously classified as assets held for sale were disposed of for approximately $730 million and an overall capitalization rate of 6.7%. The properties consisted of the following:

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

2018 Dispositions

(in millions, except as noted)

Property Address

| | Location

| | Sq ft

| | Date Disposed

| | Sale Price

| | Annualized

Revenue(1)

| |

|---|

| | | | | | | | | | | | |

111 Cosma Drive | | Bowling Green, KY | | 1.2 | | Jan 30, 2018 | | | $ | 170.0 | | | $ | 12.0 | |

1 Cosma Court and 170 Edward Street | | St. Thomas, ON | | 1.5 | | Jan 30, 2018 | | | 154.6 | | | 10.8 | |

Newpark campus (seven properties): | |

| |

| |

| | |

| | |

| |

521, 550, 561, 564, 581, 594 and 630 Newpark Boulevard | | Newmarket, ON | | 0.6 | | Jan 31, 2018 | | | 63.0 | | | 2.8 | |

1 Clearview Drive | | Tillsonburg, ON | | 0.3 | | Jul 18, 2018 | | | 7.2 | | | 0.6 | |

120 Moon Acres Road | | Piedmont, SC | | 1.1 | | Sep 13, 2018 | | | 216.4 | | | 14.2 | |

1000 JD Yarnell Industrial Parkway | | Clinton, TN | | 0.5 | | Sep 13, 2018 | | | 54.8 | | | 4.1 | |

337 and 375 Magna Drive | | Aurora, ON | | 0.1 | | Sep 27, 2018 | | | 60.0 | | | 3.7 | |

Industriestrasse 11 | | Schleiz, Germany | | 0.1 | | Oct 4, 2018 | | | 3.6 | | | 0.4 | |

| | | | | | | | | | | | |

| | | | 5.4 | | | | | $ | 729.6 | | | $ | 48.6 | |

| | | | | | | | | | | | |

- (1)

- Annualized revenue is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month the property was first classified as an asset held for sale multiplied by twelve months.

During the year ended December 31, 2018, Granite completed the sale of its two remaining special purpose properties in the United States located in Piedmont, South Carolina and Clinton, Tennessee. The gross proceeds for these two properties of $216.4 million and $54.8 million included amounts that are expected to be received in the first quarters of 2020 and 2019, respectively, and were based on an estimated consumer price index inflation factor at the date of disposition. At December 31, 2018, the expected remaining proceeds receivable was $11.8 million (US$8.7 million) for the property disposed of in South Carolina and $0.2 million (US$0.2 million) for the Tennessee property disposal. The proceeds receivable are subject to change and will be dependent upon the actual inflation factors.

Assets Held for Sale

At December 31, 2018, six investment properties located in Canada and the United States were classified as assets held for sale. The six properties, having an aggregate fair value of $44.2 million, consisted of the following:

| | | | | | | | | | | | | | |

| | | | | | | | | | |

Held for Sale

(in millions, except as noted)

Property Address

| | Location

| | Sq ft

| | Fair

Value

| | Annualized

Revenue(1)

| |

|---|

| | | | | | | | | | |

3 Walker Drive (nine acre parcel of land) | | Brampton, ON | | N/A | | | $ | 13.4 | | | $ | — | |

375 Edward Street | | Richmond Hill, ON | | 0.1 | | | 7.8 | | | — | |

403 S 8th Street | | Montezuma, IA | | 0.2 | | | 7.1 | | | 0.8 | |

1951 A Avenue | | Victor, IA | | 0.1 | | | 5.5 | | | 0.6 | |

408 N Maplewood Avenue | | Williamsburg, IA | | 0.2 | | | 7.2 | | | 0.6 | |

411 N Maplewood Avenue | | Williamsburg, IA | | 0.1 | | | 3.2 | | | 0.2 | |

| | | | | | | | | | |

| | | | 0.7 | | | $ | 44.2 | | | $ | 2.2 | |

| | | | | | | | | | |

- (1)

- Annualized revenue is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month the property was first classified as an asset held for sale multiplied by twelve months.

Table of Contents

These aforementioned properties were classified as assets held for sale on the combined balance sheets at December 31, 2018 and were excluded from the value of investment properties. These properties are also excluded from references to investment properties and related property metrics on the date thereof throughout this MD&A. During January and February 2019, all six properties classified as assets held for sale were sold for aggregate gross proceeds of $43.7 million.

Unsecured Term Loans

On December 12, 2018, Granite entered into and fully drew down a $300.0 million seven-year senior unsecured non-revolving term facility (the "2025 Term Loan"). Through a cross currency interest rate swap, Granite has exchanged the variable rate interest payments (Canadian Dollar Offered Rate "CDOR" plus margin) from the 2025 Term Loan for Euro denominated payments at a 2.202% fixed interest rate.

On December 19, 2018, Granite entered into and fully drew down a US$185.0 million four-year senior unsecured non-revolving term facility (the "2022 Term Loan"). Through a cross currency interest rate swap, Granite has exchanged the variable rate interest payments (LIBOR plus margin) from the 2022 Term Loan for Euro denominated payments at a 1.225% fixed interest rate.

Granite intends to use the net proceeds from both term loans for general corporate purposes, including to fund development and property acquisitions.

Officer and Board Appointments

Effective August 1, 2018, Kevan Gorrie became Granite's President and Chief Executive Officer, a trustee of Granite REIT and a director of Granite GP, replacing Michael Forsayeth.

Special Distribution to Unitholders

As a result of the increase in taxable income generated primarily by the sale transactions in 2018, Granite's Board of Trustees declared a special distribution in December 2018 of $1.20 per stapled unit which comprised 30.0 cents per unit payable in cash and 90.0 cents per unit payable by the issuance of stapled units. The cash portion of the special distribution was intended to provide liquidity to unitholders to cover all or part of any non-resident withholding taxes or other income tax obligations that may arise from the additional taxable income being distributed via the special distribution. On January 15, 2019, immediately following the issuance of the stapled units related to the portion of the special distribution payable in stapled units of 90.0 cents per unit, the stapled units were consolidated such that each unitholder held the same number of stapled units after the consolidation as each unitholder held prior to the special distribution.

Increase in Monthly Distributions

The 2019 targeted annualized distribution increased by 2.9% to $2.80 (23.3 cents per month) per stapled unit commencing with the monthly distribution paid in January 2019.

Table of Contents

Foreign Currency Translation

The majority of Granite's investment properties are located in Europe and the United States and the cash flows derived from such properties are primarily denominated in Euros and US dollars. Accordingly, fluctuations in the Canadian dollar, Granite's reporting currency, relative to the Euro and US dollar will result in fluctuations in the reported values of revenues, expenses, cash flows, assets and liabilities. The most significant foreign currency exchange rates that impact Granite's business are summarized in the following table:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | Average Exchange Rates | | Period End Exchange Rates | |

|---|

| | Three Months Ended

December 31, | |

| | Years Ended

December 31, | |

| |

| |

| |

| |

|---|

| |

| |

| | December 31,

2018

| | December 31,

2017

| |

| |

|---|

| | 2018

| | 2017

| | Change

| | 2018

| | 2017

| | Change

| | Change

| |

|---|

| | | | | | | | | | | | | | | | | | | | |

$ per €1.00 | | | 1.508 | | 1.497 | | | 1% | | | 1.530 | | 1.465 | | | 4% | | | 1.563 | | | 1.505 | | | 4% | |

$ per US$1.00 | | | 1.322 | | 1.271 | | | 4% | | | 1.296 | | 1.298 | | | —% | | | 1.364 | | | 1.252 | | | 9% | |

| | | | | | | | | | | | | | | | | | | | |

The average exchange rates for the three months ended December 31, 2018 were higher when compared to those for the three months ended December 31, 2017 as a result of the relative weakening of the Canadian dollar vis-à-vis the Euro and US dollar, which, on a comparative basis, increased the Canadian dollar equivalent of revenue and expenses from Granite's European and U.S. operations.

For the year ended December 31, 2018 compared to the prior year, the average exchange rates of the Canadian dollar to the Euro and US dollar were higher and slightly lower, respectively, which on a comparative basis, increased the Canadian dollar equivalent of revenue and expenses from Granite's European operations and marginally decreased the Canadian dollar equivalent of revenue and expenses from Granite's U.S. operations.

The period end exchange rates of the Canadian dollar to the Euro and US dollar on December 31, 2018 were higher when compared to the December 31, 2017 exchange rates. As a result, the Canadian dollar equivalent of assets and liabilities from Granite's European and U.S. subsidiaries were higher when compared to December 31, 2017.

On a net basis, the effect of the changes in exchange rates on Granite's operating results for the three month period and year ended December 31, 2018 was as follows:

Effects of Changes in Exchange Rates on Operating Results

| | | | | | | | | |

| | | | | | |

| | Three Months Ended

December 31, | | Years Ended

December 31, | |

|---|

(in millions, except per unit information)

| | 2018 vs 2017

| | 2018 vs 2017

| |

|---|

| | | | | | |

Increase in revenue | | | $ | 0.9 | | | $ | 4.5 | |

Increase in NOI — cash basis | | | 0.8 | | | 4.4 | |

Increase in net income | | | 1.2 | | | 5.0 | |

Increase in FFO | | | 0.9 | | | 2.8 | |

Increase in AFFO | | | 0.8 | | | 2.8 | |

Increase in FFO per unit | | | $ | 0.02 | | | $ | 0.06 | |

Increase in AFFO per unit | | | $ | 0.02 | | | $ | 0.06 | |

| | | | | | |

Table of Contents

Operating Results

Revenue

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | |

| | Years Ended

December 31, | |

| |

|---|

| | 2018

| | 2017(1)

| | $ change

| | 2018

| | 2017(1)

| | $ change

| |

|---|

| | | | | | | | | | | | | | |

Rental revenue | | | $ | 53.5 | | | $ | 55.7 | | (2.2 | ) | $ | 220.0 | | | $ | 216.1 | | 3.9 | |

Tenant recoveries | | | 6.4 | | | 6.9 | | (0.5 | ) | 26.5 | | | 27.0 | | (0.5 | ) |

Lease termination and close-out fees | | | — | | | — | | — | | 1.0 | | | 1.6 | | (0.6 | ) |

| | | | | | | | | | | | | | |

Revenue | | | $ | 59.9 | | | $ | 62.6 | | (2.7 | ) | $ | 247.5 | | | $ | 244.7 | | 2.8 | |

| | | | | | | | | | | | | | |

- (1)

- Granite has retrospectively applied IFRS 15,Revenue from Contracts with Customers (see "NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS") and all historical periods herein have been restated to reflect such treatment.

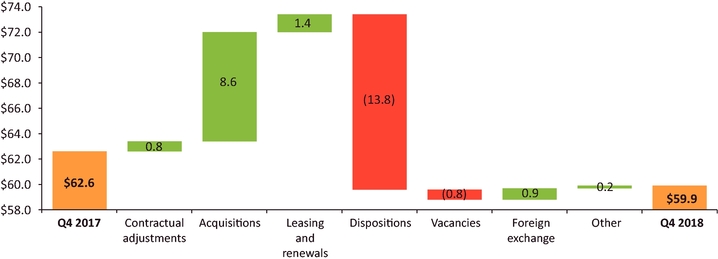

Revenue for the three month period ended December 31, 2018 decreased $2.7 million to $59.9 million from $62.6 million in the prior year period. The components contributing to the change in revenue are detailed below:

Q4 2018 vs Q4 2017 Change in Revenue

Additional details pertaining to the components of the change in revenue are as follows:

- •

- contractual rent adjustments included $0.7 million from consumer price index based increases and $0.1 million from fixed contractual adjustments related to rent escalations;

- •

- the acquisitions of properties located in the United States and Germany in 2018 increased revenue by $8.6 million, which included $0.7 million of tenant recoveries;

- •

- revenue increased by $1.4 million primarily due to the partial lease-up of a property in Novi, Michigan;

Table of Contents

- •

- the sale of 16 investment properties in Canada, the United States and Germany in 2018 decreased revenue by $13.8 million of which $1.6 million related to a reduction in property tax and insurance tenant recoveries;

- •

- vacancies arising from a lease expiry for a property in the Netherlands and three lease expiries for properties in Canada decreased revenue by $0.4 million each. The property in the Netherlands was re-leased in December 2018; and

- •

- foreign exchange had a $0.9 million positive impact as the weakening of the Canadian dollar against the Euro and US dollar increased revenue by $0.1 million and $0.8 million, respectively.

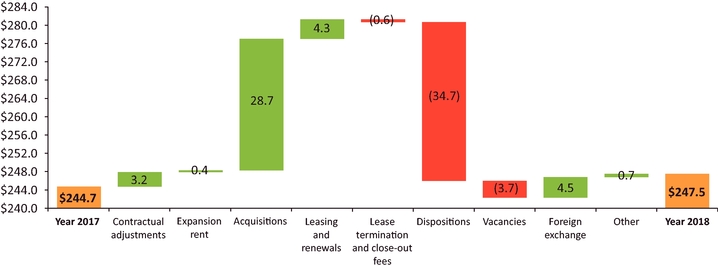

Revenue for the year ended December 31, 2018 increased $2.8 million to $247.5 million from $244.7 million in the prior year. The components contributing to the change in revenue are detailed below:

Year 2018 vs Year 2017 Change in Revenue

Additional details pertaining to the components of the change in revenue are as follows:

- •

- contractual rent adjustments included $2.8 million from consumer price index based increases and $0.4 million from fixed contractual adjustments related to rent escalations;

- •

- revenue increased by $0.4 million primarily due to the purchase of two building expansions in the United States in the prior year;

- •

- the acquisitions of properties located in the United States and Germany from October 2017 to December 2018 increased revenue by $28.7 million, which included $2.8 million of tenant recoveries;

- •

- revenue increased by $4.3 million primarily due to the partial lease-up of a property in Novi, Michigan;

- •

- revenue decreased by $1.6 million as a result of the lease termination and close-out fees received in the prior year, partially offset by a $1.0 million lease termination fee in 2018 for an acquired property in the United States for which the leasable area was re-leased to a new tenant;

- •

- the sale of 16 properties in Canada, the United States and Germany in 2018 decreased revenue by $34.7 million of which $4.4 million related to a reduction in property tax and insurance tenant recoveries;

Table of Contents

- •

- lease expiries for five properties in North America and two properties in Europe resulted in vacancies that decreased revenue by $1.5 million and $2.2 million, respectively; and

- •

- foreign exchange had a net $4.5 million positive impact largely from the weakening of the Canadian dollar against the Euro.

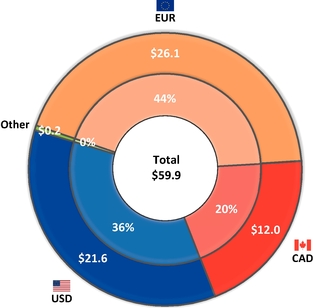

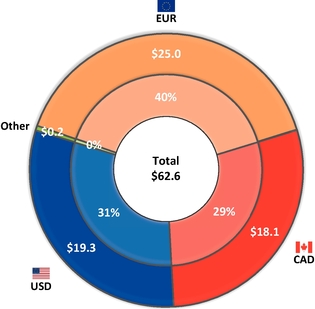

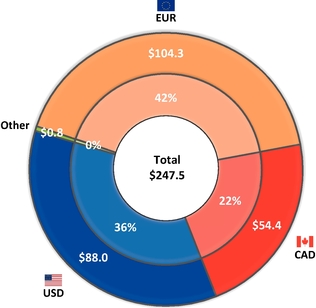

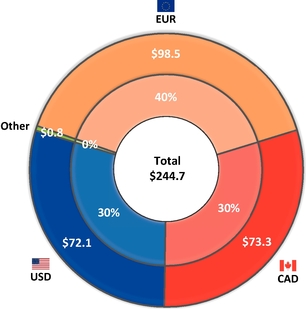

Revenue by major currency for the three month periods and years ended December 31, 2018 and 2017 was as follows:

| | |

Fourth Quarter 2018

| | Fourth Quarter 2017

|

|---|

|

|

|

| | |

Year 2018

| | Year 2017

|

|---|

|

|

|

The mix in revenue for the three months and year ended December 31, 2018 compared to the prior year periods has changed primarily with revenue denominated in US dollars increasing and revenue

Table of Contents

denominated in Canadian dollars decreasing as a result of the recent U.S. acquisitions and Canadian property dispositions.

As a majority of the Trust's revenue is denominated in currencies other than the Canadian dollar, Granite uses derivative financial instruments, including cross currency interest rate swaps and forward currency contracts, to partially hedge its exposure to foreign currencies and reduce the potential impact that foreign currency rate changes may have on Granite's operating results, cash flows and distributions.

Net Operating Income

Net operating income ("NOI") in the three months ended December 31, 2018 was $52.4 million compared to $54.5 million in the three months ended December 31, 2017. NOI in the year ended December 31, 2018 was $216.6 million compared to $213.3 million in the year ended December 31, 2017. NOI — cash basis excludes the impact of lease termination and close-out fees, and straight-line rent and tenant incentive amortization and reflects the cash generated by the income-producing properties excluding lease termination and close-out fees on a period-over-period basis. NOI — cash basis was $52.9 million in the three months ended December 31, 2018 compared with $56.2 million in the prior year period. NOI — cash basis was $216.7 million in the year ended December 31, 2018 compared with $218.2 million in the year ended December 31, 2017.

Same property NOI — cash basis refers to the NOI — cash basis for those properties owned by Granite throughout the entire current and prior year periods under comparison. Same property NOI — cash basis excludes properties that were acquired, disposed of, classified as properties under or held for development or assets held for sale during the periods under comparison. Same property NOI — cash basis in the three months ended December 31, 2018 was $42.9 million compared to $41.3 million in the three months ended December 31, 2017. Same property NOI — cash basis in the year ended December 31, 2018 was $170.9 million compared to $164.6 million in the year ended December 31, 2017. The changes in NOI, NOI — cash basis and same property NOI — cash basis are detailed below:

Changes in NOI(3), NOI — Cash Basis and Same Property NOI — Cash Basis

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| |

| | Three Months Ended

December 31, | |

| | Years Ended

December 31, | |

|---|

| | Sq ft(1)

(in millions)

| | Sq ft(1)

(in millions)

| |

|---|

| | 2018

| | 2017(2)

| | $ change

| | 2018

| | 2017(2)

| | $ change

| |

|---|

| | | | | | | | | | | | | | | | | | |

Revenue | | | | $ | 59.9 | | | $ | 62.6 | | (2.7 | ) | | | $ | 247.5 | | | $ | 244.7 | | 2.8 | |

Less: Property operating costs | | | | 7.5 | | | 8.1 | | (0.6 | ) | | | 30.9 | | | 31.4 | | (0.5 | ) |

| | | | | | | | | | | | | | | | | | |

NOI(3) | | | | $ | 52.4 | | | $ | 54.5 | | (2.1 | ) | | | $ | 216.6 | | | $ | 213.3 | | 3.3 | |

Add (deduct): | | | | | | | | | | | | | | | | | | | |

Lease termination and close-out fees | | | | — | | | — | | — | | | | (1.0 | ) | | (1.6 | ) | 0.6 | |

Straight-line rent amortization | | | | (0.8 | ) | | 0.3 | | (1.1 | ) | | | (4.3 | ) | | 1.1 | | (5.4 | ) |

Tenant incentive amortization | | | | 1.3 | | | 1.4 | | (0.1 | ) | | | 5.4 | | | 5.4 | | — | |

| | | | | | | | | | | | | | | | | | |

NOI — cash basis | | 32.2 | | $ | 52.9 | | | $ | 56.2 | | (3.3 | ) | 32.2 | | $ | 216.7 | | | $ | 218.2 | | (1.5 | ) |

Less NOI — cash basis for: | | | | | | | | | | | | | | | | | | | |

Acquisitions | | 8.4 | | 9.5 | | | 2.3 | | 7.2 | | 8.4 | | 26.0 | | | 2.3 | | 23.7 | |

Dispositions, assets held for sale and developments | | 0.7 | | 0.5 | | | 12.6 | | (12.1 | ) | 6.0 | | 19.8 | | | 51.3 | | (31.5 | ) |

| | | | | | | | | | | | | | | | | | |

Same property NOI — cash basis | | 23.8 | | $ | 42.9 | | | $ | 41.3 | | 1.6 | | 23.8 | | $ | 170.9 | | | $ | 164.6 | | 6.3 | |

| | | | | | | | | | | | | | | | | | |

- (1)

- The square footage relating to the NOI — cash basis represents GLA of 32.2 million square feet as at December 31, 2018. The square footage relating to the same property NOI — cash basis represents Granite's GLA of 23.8 million square feet as at

Table of Contents

December 31, 2018, which excludes the impact from the acquisitions, dispositions, assets held for sale and developments during the relevant periods.

- (2)

- The Trust has retrospectively applied IFRS 15,Revenue from Contracts with Customers (see "NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS") and all historical periods herein have been restated to reflect such treatment.

- (3)

- NOI is calculated in accordance with IFRS and is included in the audited combined financial statements as at and for the year ended December 31, 2018. Previously, Granite reported NOI as a non-IFRS financial measure, calculated as set forth above but excluding lease termination and close-out fee revenue. NOI for the year ended December 31, 2017 as calculated under the prior method was previously reported as $211.7 million, and for the quarter ended December 31, 2017 was previously reported as $54.5 million.

Property operating costs include recoverable and non-recoverable costs from tenants and consist of property taxes, utilities, insurance, repairs and maintenance, legal and other property-related expenses. None of Granite's employee compensation expenses are included in property operating costs.

Straight-line rent amortization represents the scheduled fixed rent changes or rent-free periods in leases that are recognized in revenue evenly on a straight-line basis over the term of the lease. Tenant incentive amortization mainly represents allowances provided to tenants that are recognized in revenue evenly on a straight-line basis over the term of the lease and primarily comprises the amortization associated with the cash allowance incentives paid to Magna in respect of the 10-year lease extensions exercised during the 2014 year at the Thondorf and Eurostar properties in Graz, Austria.

NOI — cash basis for the three month period ended December 31, 2018 decreased $3.3 million to $52.9 million from $56.2 million in the prior year period due to the decrease in rental revenue as noted previously and the straight-line rent amortization associated with the recent acquisitions in the United States and rent-free period for the re-leasing of a property in the Netherlands.

NOI — cash basis for the year ended December 31, 2018 decreased $1.5 million to $216.7 million from $218.2 million in the prior year as a result of the straight-line rent amortization for the properties mentioned above and rent-free periods associated with the partial lease-up of vacant space in Novi, Michigan and the early renewals and extensions of three leases in North America and Germany, partially offset by the increase in rental revenue as noted previously.

Same property NOI — cash basis for the three month period ended December 31, 2018 increased $1.6 million (3.9%) to $42.9 million primarily due to the increase in contractual rents, partial lease-up of the property in Novi, Michigan and the favourable foreign exchange impact from the weakening of the Canadian dollar against the US dollar, partially offset by vacancies for properties in Canada and the Netherlands. Excluding the impact of foreign exchange, same property NOI — cash basis for the three month period ended December 31, 2018 would have increased by 1.9%.

Same property NOI — cash basis for the year ended December 31, 2018 increased $6.3 million (3.8%) to $170.9 million largely resulting from the increase in contractual rents, the partial lease-up of the vacant space in Novi, Michigan and the property in Poland, and the favourable foreign exchange impact from the weakening of the Canadian dollar against the Euro, partially offset by vacancies for properties in North America and the Netherlands and rent-free periods for certain lease renewals in Europe. Excluding the impact of foreign exchange, same property NOI — cash basis for the year ended December 31, 2018 would have increased by 0.3%.

Table of Contents

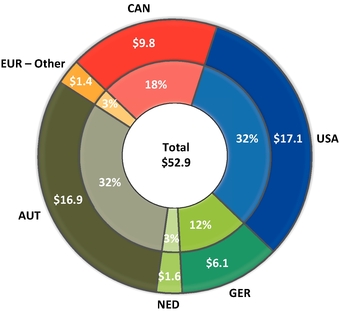

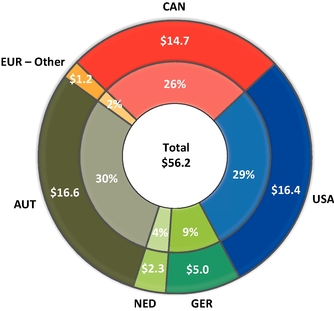

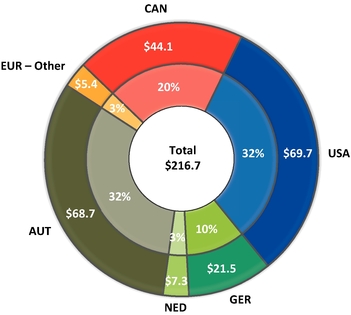

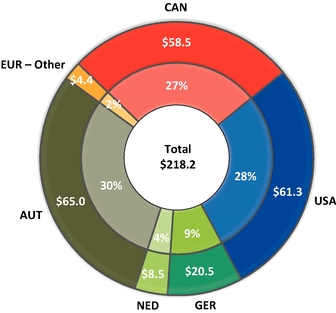

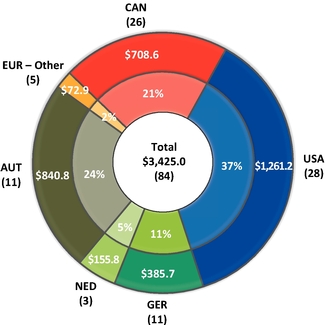

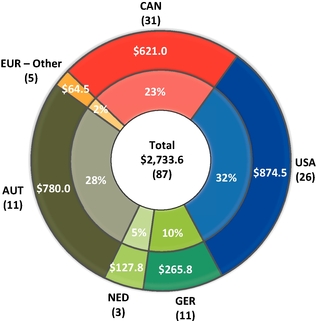

NOI — cash basis for the three month periods and years ended December 31, 2018 and 2017 by geography was as follows:

NOI — Cash Basis by Geography

| | |

Fourth Quarter 2018

| | Fourth Quarter 2017

|

|---|

|

|

|

| | |

Year 2018

| | Year 2017

|

|---|

|

|

|

Table of Contents

The mix in NOI — cash basis for the three months and year ended December 31, 2018 compared to the prior year periods has changed primarily with the percentage attributable to the United States increasing and Canada decreasing as a result of the recent U.S. acquisitions and Canadian property dispositions.

Granite's property portfolio and NOI — cash basis are geographically diversified, which reduces the risk to Granite's operating results of any particular country's economic downturn.

General and Administrative Expenses

General and administrative expenses consisted of the following:

General and Administrative Expenses

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | |

| | Years Ended

December 31, | |

| |

|---|

| | 2018

| | 2017

| | $ change

| | 2018

| | 2017

| | $ change

| |

|---|

| | | | | | | | | | | | | | |

Salaries and benefits | | | $ | 4.2 | | | $ | 3.1 | | | 1.1 | | $ | 16.0 | | $ | 12.1 | | | 3.9 | |

Audit, legal and consulting | | | 1.0 | | | 0.9 | | | 0.1 | | 4.0 | | 3.4 | | | 0.6 | |

Trustee/director fees and related expenses | | | 0.2 | | | 0.4 | | | (0.2 | ) | 1.1 | | 1.4 | | | (0.3 | ) |

Unit-based compensation including distributions and revaluations | | | 0.6 | | | 0.7 | | | (0.1 | ) | 3.2 | | 4.0 | | | (0.8 | ) |

Other public entity costs | | | 0.4 | | | 0.4 | | | — | | 1.6 | | 1.7 | | | (0.1 | ) |

Office rents | | | 0.2 | | | 0.2 | | | — | | 0.9 | | 0.9 | | | — | |

Other | | | 0.6 | | | 0.9 | | | (0.3 | ) | 2.6 | | 2.5 | | | 0.1 | |

| | | | | | | | | | | | | | |

General and administrative expenses | | | $ | 7.2 | | | $ | 6.6 | | | 0.6 | | $ | 29.4 | | $ | 26.0 | | | 3.4 | |

| | | | | | | | | | | | | | |

General and administrative expenses were $7.2 million for the three month period ended December 31, 2018 and increased $0.6 million in comparison to the prior year period primarily as a result of the following:

- •

- an increase in salaries and benefits expense mainly due to higher incentive pay expense, partially offset by;

- •

- a decrease in trustee/director fees as a result of a reduction in board fees starting in 2017; and

- •

- a decrease in other general and administrative expenses primarily due to fees for various administrative matters, such as staff replacements and travel, incurred in the prior year period.

General and administrative expenses were $29.4 million for the year ended December 31, 2018 and increased $3.4 million in comparison to the prior year primarily as a result of the following:

- •

- an increase in salaries and benefits expense mainly due to compensation costs associated with departing employees including Granite's former Chief Executive Officer and Chief Operating Officer as well as higher incentive pay expense in the 2018 year; and

- •

- an increase in audit, legal and consulting costs due to corporate advisory matters including internal reorganizations and administrative matters, such as temporary staff replacements. These increases were partially offset by:

- •

- the reduction in unit-based compensation costs mainly due to the decrease in fair value remeasurement expense resulting from fluctuations in the market price of the Trust's stapled units. For the years ended December 31, 2018 and 2017, general and administrative expenses included a

Table of Contents

Proxy Contest Expenses

In the year ended December 31, 2017, Granite incurred expenses of $5.9 million in connection with the proxy contest leading up to Granite's June 2017 annual general meeting. Included in the proxy contest expenses are legal, advisory and proxy solicitation costs incurred directly by Granite and a $2.0 million reimbursement of out-of-pocket fees and expenses incurred by Front Four Capital Group and Sandpiper Group regarding matters relating to the annual general meeting. Sandpiper Group received $0.7 million of the reimbursement. An individual affiliated with Sandpiper Group is a related party of Granite by virtue of becoming a director of Granite GP and a trustee of Granite REIT.

Interest Income

Interest income for the three month periods ended December 31, 2018 and 2017 was $0.8 million and $0.1 million, respectively. The $0.7 million increase is primarily due to interest income earned from higher cash balances resulting from property dispositions and the drawdowns from the term loans.

Interest income for the years ended December 31, 2018 and 2017 was $2.6 million and $0.5 million, respectively. The $2.1 million increase is primarily due to interest income earned from higher cash balances as noted above and a vendor take-back mortgage receivable associated with a property disposition. The mortgage receivable bore interest at an annual rate of 6.0% and was repaid on April 16, 2018.

Interest Expense and Other Financing Costs

Interest expense and other financing costs for the three month periods ended December 31, 2018 and 2017 remained consistent at $5.5 million. The fourth quarter of 2018 included interest expense associated with the term loan drawdowns in December 2018 while the prior year period included interest expense for the outstanding credit facility draws.

Interest expense and other financing costs for the years ended December 31, 2018 and 2017 were $22.4 million and $20.0 million, respectively. The $2.4 million increase is primarily related to:

- •

- the higher interest expense associated with the credit facility draws and term loans indebtedness during 2018;

- •

- the foreign exchange impact resulting from the relative weakening of the Canadian dollar against the Euro on the cross currency interest rate swaps; and

- •

- the higher standby fees relating to the increased borrowing capacity under the credit facility.

As at December 31, 2018, Granite's weighted average cost of interest-bearing debt was 2.17% (2017 — 2.54%) and the weighted average debt term-to-maturity was 4.7 years (2017 — 4.8 years).

Foreign Exchange Gains/Losses, Net

Granite recognized net foreign exchange gains of $1.4 million and $0.8 million in the three month periods ended December 31, 2018 and 2017, respectively. The $0.6 million increase in net foreign exchange gains is primarily due to the settlement of two cross currency interest rate swaps entered into to fund the property acquisition in Germany.

Granite recognized net foreign exchange gains of $9.4 million in the year ended December 31, 2018 which included an $8.5 million foreign exchange gain related to the remeasurement of the US dollar cash proceeds received from the sale of three investment properties in January 2018. In comparison, Granite recognized net foreign exchange losses of $0.6 million in the year ended December 31, 2017. The $10.0 million increase

Table of Contents

in net foreign exchange gains is substantially due to the remeasurement of the US dollar cash proceeds and, to a lesser extent, the settlement of two cross currency interest rate swaps as noted above, partially offset by the net remeasurement of certain monetary assets and liabilities of the Trust that are denominated in US dollars or Euros.

Fair Value Gains/Losses on Investment Properties, Net

Net fair value gains on investment properties were $52.9 million and $185.2 million in the three month periods ended December 31, 2018 and 2017, respectively. In the three month period ended December 31, 2018, net fair value gains of $52.9 million were largely attributable to a compression in discount and terminal capitalization rates for properties located in Canada, the United States and the Netherlands that resulted from a greater market demand for industrial real estate properties and, to a lesser extent, the increase in fair value to the expected sale price for the multi-purpose properties sold in the first quarter of 2019 and the positive changes in leasing assumptions associated with new leases and lease renewals.

The net fair value gains on investment properties in the three month period ended December 31, 2017 of $185.2 million were primarily attributable to i) the increase in fair value to the sale price for the 10 properties (three special purpose properties and seven multi-purpose facilities) sold in January 2018 and the higher valuation implied on certain remaining special purpose properties (see "INVESTMENT PROPERTIES") from the pricing realized and the liquidity potential demonstrated from the sale and ii) a compression in discount and terminal capitalization rates for certain multi-purpose properties located in Canada resulting from market demand which led to improved asset pricing.

Net fair value gains on investment properties were $354.7 million and $212.1 million in the years ended December 31, 2018 and 2017, respectively. In the year ended December 31, 2018, net fair value gains of $354.7 million were largely attributable to i) an increase in fair value to the sale price for the multi-purpose and special purpose properties sold in 2018 and 2019, ii) a compression in discount and terminal capitalization rates and an increase in market rents for properties located in Canada, the United States, Germany and the Netherlands resulting from a greater market demand and, to a lesser extent, iii) positive changes in leasing assumptions primarily from contractual rent increases, new leases and lease renewals.

The net fair value gains on investment properties in the year ended December 31, 2017 of $212.1 million were attributable to several factors, and, in particular, to i) the increase in fair value to the sale price for the 10 properties sold in January 2018 and the higher valuation implied on certain remaining special purpose properties, as noted above, ii) a compression in discount and terminal capitalization rates for certain modern warehouse and multi-purpose properties located in Canada, the United States and Europe resulting from market demand which led to improved asset pricing and iii) favourable changes in leasing assumptions from new leases or renewals executed at multi-purpose properties located in Canada and the United States and modern warehouse properties in Europe.

Acquisition Transaction Costs

Acquisition transaction costs for the three month period and year ended December 31, 2018 were $0.4 million and $8.0 million compared to $0.4 million and $0.7 million for the prior year periods, respectively. Acquisition transaction costs primarily include land transfer tax, legal and advisory costs associated with completed acquisitions and, to a lesser extent, legal and advisory costs associated with pursuing acquisition opportunities that were not completed. The increase in acquisition transaction costs for the current year is due to greater overall acquisition activity and a $5.4 million land transfer tax for the property acquired in Germany.

Table of Contents

Loss on Sale of Investment Properties

The loss on sale of investment properties for the three month period and year ended December 31, 2018 was $1.5 million and $6.9 million, respectively, compared to $0.4 million for both prior year periods. Loss on sale of investment properties is related to broker commissions and legal and advisory costs associated with the dispositions or planned dispositions of assets held for sale.

Other Income

Other income of $2.3 million for the year ended December 31, 2018 is attributable to a settlement amount related to a land use matter for a property in Ontario, Canada. Granite received $1.4 million of the settlement during 2018 and the remaining balance was collected in January 2019.

Income Tax Expense

Income tax expense comprised the following:

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | |

| | Years Ended

December 31, | |

| |

|---|

| | 2018

| | 2017

| | $ change

| | 2018

| | 2017

| | $ change

| |

|---|

| | | | | | | | | | | | | | |

Foreign operations | | $ | 1.3 | | $ | 1.4 | | | (0.1 | ) | $ | 5.9 | | $ | 5.2 | | | 0.7 | |

Withholding taxes | | — | | — | | | — | | 0.7 | | 1.0 | | | (0.3 | ) |

Related to sale of an investment property | | — | | — | | | — | | 0.2 | | — | | | 0.2 | |

Other | | (0.5 | ) | 0.1 | | | (0.6 | ) | 0.8 | | 1.5 | | | (0.7 | ) |

| | | | | | | | | | | | | | |

Current tax expense | | 0.8 | | 1.5 | | | (0.7 | ) | 7.6 | | 7.7 | | | (0.1 | ) |

Deferred tax expense | | 4.6 | | (8.0 | ) | | 12.6 | | 45.0 | | 5.7 | | | 39.3 | |

| | | | | | | | | | | | | | |

Income tax expense | | $ | 5.4 | | $ | (6.5 | ) | | 11.9 | | $ | 52.6 | | $ | 13.4 | | | 39.2 | |

| | | | | | | | | | | | | | |

For the three months ended December 31, 2018, the current tax expense decreased compared to the prior year period primarily due to the favourable settlement of an Austrian tax matter in the fourth quarter of 2018.

For the year ended December 31, 2018, the current tax expense decreased compared to the prior year primarily due to the favourable settlement of an Austrian tax matter and lower withholding taxes incurred on inter-company dividends, partially offset by higher taxable income generated in taxable European jurisdictions, the foreign exchange impact resulting from the relative weakening of the Canadian dollar on Euro denominated tax expense and the tax expense associated with the disposition of a property located in Germany.

The increase in deferred tax expense for the three months and year ended December 31, 2018 compared to the prior year periods was primarily due to an increase in fair value gains in jurisdictions in which deferred taxes are recorded and the reduction in the US tax rate enacted in December 2017 that resulted in a deferred tax recovery in the prior year.

Table of Contents

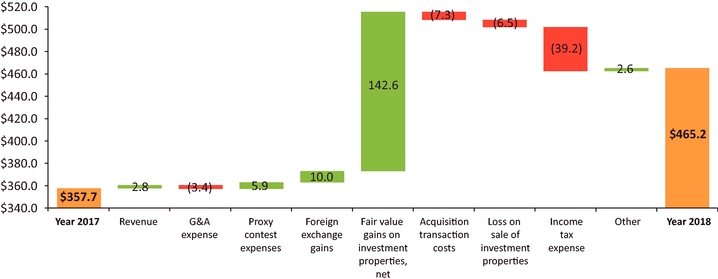

Net Income Attributable to Stapled Unitholders

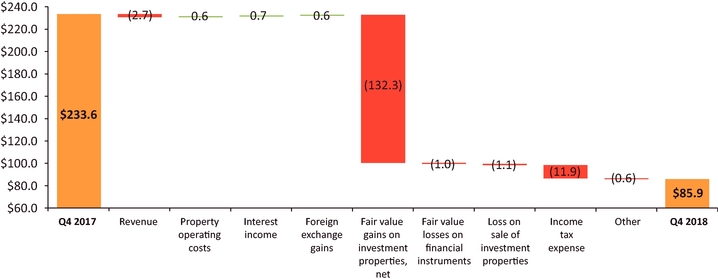

For the three month period ended December 31, 2018, net income attributable to stapled unitholders was $85.9 million compared to $233.6 million in the prior year period. The $147.7 million net decrease was primarily due to a $132.3 million decrease in net fair value gains on investment properties and an $11.9 million increase in income tax expense. The $147.7 million decrease in net income attributable to stapled unitholders is summarized below:

Q4 2018 vs Q4 2017 Change in Net Income Attributable to Stapled Unitholders

For the year ended December 31, 2018, net income attributable to stapled unitholders was $465.2 million compared to $357.7 million in the prior year. The $107.5 million net increase was primarily due to a $142.6 million increase in net fair value gains on investment properties, partially offset by a corresponding $39.3 million increase in deferred income tax expense. The $107.5 million increase in net income attributable to stapled unitholders is summarized below:

Year 2018 vs Year 2017 Change in Net Income Attributable to Stapled Unitholders

Table of Contents

Funds From Operations and Adjusted Funds From Operations

The reconciliation of net income attributable to stapled unitholders to FFO and AFFO for the three months and years ended December 31, 2018 and 2017 is presented below:

FFO AND AFFO RECONCILIATION

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

| |

| | Three Months Ended

December 31, | | Years Ended

December 31, | |

|---|

(in millions, except per unit information)

| |

| |

|---|

| |

| | 2018

| | 2017

| | 2018

| | 2017

| |

|---|

| | | | | | | | | | | | |

Net income attributable to stapled unitholders | | | | $ | 85.9 | | $ | 233.6 | | $ | 465.2 | | $ | 357.7 | |

Add (deduct): | | | | | | | | | | | |

Fair value gains on investment properties, net | | | | (52.9 | ) | (185.2 | ) | (354.7 | ) | (212.1 | ) |

Fair value losses on financial instruments | | | | 1.4 | | 0.4 | | 0.5 | | 0.8 | |

Acquisition transaction costs | | | | 0.4 | | 0.4 | | 8.0 | | 0.7 | |

Loss on sale of investment properties | | | | 1.5 | | 0.4 | | 6.9 | | 0.4 | |

Other income — settlement award | | | | — | | — | | (2.3 | ) | — | |

Current income tax expense associated with the sale of an investment property | | | | — | | — | | 0.2 | | — | |

Deferred income tax expense | | | | 4.6 | | (8.0 | ) | 45.0 | | 5.7 | |

Non-controlling interests relating to the above | | | | — | | — | | 0.1 | | — | |

| | | | | | | | | | | | |

FFO | | [A] | | $ | 40.9 | | $ | 41.6 | | $ | 168.9 | | $ | 153.2 | |

Add (deduct): | | | | | | | | | | | |

Maintenance or improvement capital expenditures paid | | | | (1.2 | ) | (9.3 | ) | (17.8 | ) | (10.7 | ) |

Leasing commissions paid | | | | (0.2 | ) | (1.2 | ) | (4.2 | ) | (2.6 | ) |

Tenant incentives paid | | | | (0.2 | ) | (0.2 | ) | (9.9 | ) | (1.0 | ) |

Tenant incentive amortization | | | | 1.3 | | 1.4 | | 5.4 | | 5.4 | |

Straight-line rent amortization | | | | (0.8 | ) | 0.3 | | (4.3 | ) | 1.1 | |

| | | | | | | | | | | | |

AFFO | | [B] | | $ | 39.8 | | $ | 32.6 | | $ | 138.1 | | $ | 145.4 | |

| | | | | | | | | | | | |

Per unit amounts: | | | |

| |

| |

| |

| |

Basic and Diluted FFO per stapled unit | | [A]/[C] and [A]/[D] | | $ | 0.90 | | $ | 0.89 | | $ | 3.68 | | $ | 3.25 | |

Basic and Diluted AFFO per stapled unit | | [B]/[C] and [B]/[D] | | $ | 0.87 | | $ | 0.69 | | $ | 3.01 | | $ | 3.09 | |

Basic weighted average number of stapled units | | [C] | |

45.7 | |

46.9 | |

45.9 | |

47.1 | |

Diluted weighted average number of stapled units | | [D] | | 45.7 | | 47.0 | | 45.9 | | 47.1 | |

| | | | | | | | | | | | |

Table of Contents

Funds From Operations

FFO for the three month period ended December 31, 2018 was $40.9 million ($0.90 per unit) compared to $41.6 million ($0.89 per unit) in the prior year period. The $0.7 million decrease in FFO is summarized below:

Q4 2018 vs Q4 2017 Change in FFO

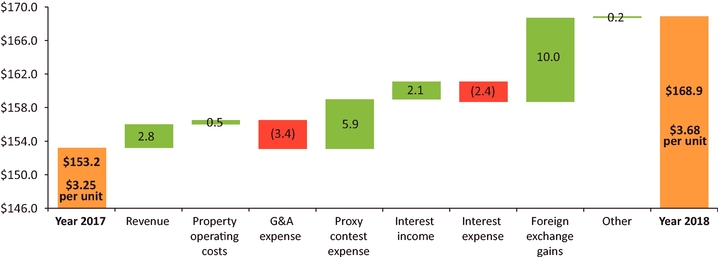

FFO for the year ended December 31, 2018 was $168.9 million ($3.68 per unit) compared to $153.2 million ($3.25 per unit) in the prior year. The $15.7 million ($0.43 per unit) increase in FFO is summarized below:

Year 2018 vs Year 2017 Change in FFO

Excluding the following items which can be a source of variance between periods: the lease termination and close-out fee of $1.0 million ($0.02 per unit) and the net foreign exchange gain on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018 of $8.5 million ($0.19 per unit), FFO would have been $159.4 million ($3.47 per unit) in the year ended December 31, 2018. In comparison, excluding the proxy contest expense of $5.9 million ($0.12 per unit) and the lease termination and close-out fees of $1.6 million ($0.03 per unit), FFO would have been $157.5 million ($3.34 per unit) in the prior year.

Table of Contents

Adjusted Funds From Operations

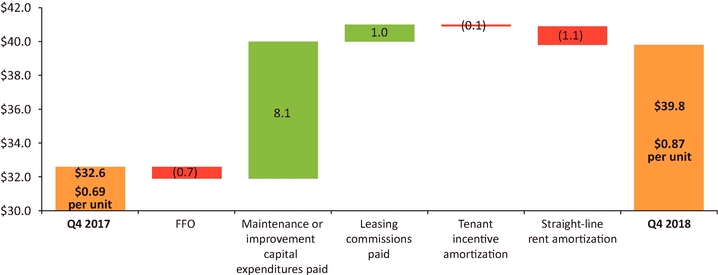

As previously detailed in the FFO and AFFO reconciliation table, AFFO for the three month period ended December 31, 2018 was $39.8 million ($0.87 per unit) compared to $32.6 million ($0.69 per unit) in the prior year period. The $7.2 million ($0.18 per unit) increase in AFFO is summarized below:

Q4 2018 vs Q4 2017 Change in AFFO

Additional details pertaining to the components of the change in AFFO are as follows:

- •

- the $0.7 million decrease in FFO, as noted previously;

- •

- an $8.1 million decrease in capital expenditures paid largely relating to an improvement project at the partially leased-up property in Novi, Michigan in the prior year period; and

- •

- a $1.0 million decrease in leasing commissions paid largely relating to the property in Novi, Michigan in the prior year period, as noted above, partially offset by;

- •

- a $0.1 million decrease in AFFO from tenant incentive amortization; and

- •

- a $1.1 million decrease in AFFO from straight-line rent amortization associated with the recent acquisitions in the United States and rent-free period for the re-leasing of a property in the Netherlands.

Table of Contents

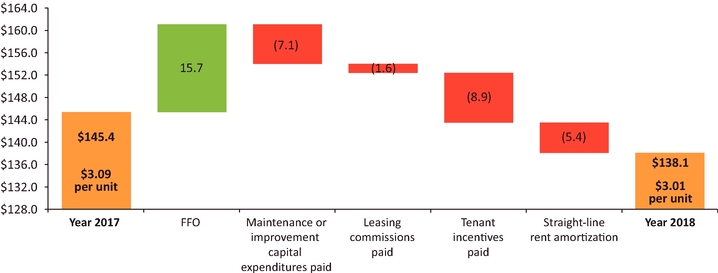

AFFO for the year ended December 31, 2018 was $138.1 million ($3.01 per unit) compared to $145.4 million ($3.09 per unit) in the prior year. The $7.3 million ($0.08 per unit) decrease in AFFO is summarized below:

Year 2018 vs Year 2017 Change in AFFO

Additional details pertaining to the components of the change in AFFO are as follows:

- •

- the $15.7 million increase in FFO, as noted above, partially offset by;

- •

- a $7.1 million increase in capital expenditures paid largely relating to improvement projects at properties in Novi, Michigan and Olive Branch, Mississippi;

- •

- a $1.6 million increase in leasing commissions paid primarily relating to the re-leasing of the property in Olive Branch, Mississippi, the developed property in Poland, as well as lease renewals and extensions for two properties in the United States and Germany, partially offset by leasing commissions paid for the partially leased-up property in Novi, Michigan in the prior year;

- •

- a $8.9 million increase in tenant incentives paid in 2018 largely relating to a tenant allowance for a 2014 lease extension at the Eurostar facility in Graz, Austria; and

- •

- a $5.4 million decrease in AFFO from straight-line rent amortization, primarily from newly acquired properties in the United States and rent-free periods associated with the partial lease-up of vacant space in Novi, Michigan, the re-leasing of a property in the Netherlands and the early renewals and extensions of three leases in North America and Germany.

Excluding the following items which can be a source of variance between periods: lease termination and close-out fee of $1.0 million ($0.02 per unit) recognized in revenue, the net foreign exchange gain on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018 of $8.5 million ($0.19 per unit) and the payment of the tenant incentive allowance made in connection with a 2014 lease extension at the Eurostar facility in Graz, Austria of $9.1 million ($0.19 per unit), AFFO would have been $137.7 million ($2.99 per unit) in the year ended December 31, 2018. In comparison, excluding the proxy contest expense of $5.9 million ($0.12 per unit) and lease termination and close-out fees of $1.6 million ($0.03 per unit), AFFO would have been $149.7 million ($3.18 per unit) in the prior year.

Table of Contents

Granite's investment properties consist of income-producing properties, properties under development and land held for development. Substantially all of the income-producing properties are for industrial use and can be categorized as (i) modern logistics/distribution warehouse facilities ("modern warehouse facilities"), which were recently acquired or newly developed/redeveloped, (ii) multi-purpose facilities, which are tenantable by a wide variety of potential users or (iii) special purpose properties designed and built with specialized features and leased to Magna. The attributes of the income-producing properties are versatile and are based on the needs of the tenant such that an industrial property used by a certain tenant for light or heavy manufacturing can be used by another tenant for other industrial uses after some retrofitting if necessary. Accordingly, the investment property portfolio is substantially for industrial use and, as such, Granite determined that its asset class comprises industrial properties for purposes of financial reporting. The fair value of the industrial properties, as noted below, is based upon the current tenanting, existing use and attributes of such properties.

Properties under development comprise a 29 acre site located in Indiana, United States where Granite is planning to construct a 0.5 million square foot logistics-industrial property in 2019 and a 15 acre site in Altbach, Germany where Granite is demolishing the existing building and expects to begin construction of a 0.3 million square foot Class A distribution/light industrial facility later in 2019. Land held for development comprise a 16 acre parcel of land located in Wroclaw, Poland that could provide for approximately 0.3 million square feet of logistics-warehouse space as well as 12.9 acres of development land in Ohio, United States which was recently acquired.

Summary attributes of the investment properties at December 31, 2018 and 2017 were as follows:

Investment Properties Summary(1)

| | | | | | | |

| | | | | | |

As at December 31,

|

|

2018

|

|

2017

|

|

|---|

| | | | | | |

(in millions, except as noted) | | | | | |

Investment properties — fair value | | $ | 3,425.0 | | $ | 2,733.6 | |

Income-producing properties | | 3,404.0 | | 2,714.7 | |

Properties under development | | 17.0 | | — | |

Land held for development | | 4.0 | | 18.9 | |

Overall capitalization rate | | 6.7% | | 7.6% | |

Number of investment properties | |

84 | |

87 | |

Income-producing properties | | 80 | | 84 | |

Properties under development | | 2 | | — | |

Land held for development | | 2 | | 3 | |

Property metrics | |

| |

| |

GLA, square feet | | 32.2 | | 29.1 | |

Occupancy, by GLA | | 99.1% | | 98.4% | |

Weighted average lease term, in years by square footage | | 6.0 | | 5.9 | |

Total number of tenants | | 48 | | 40 | |

Magna as a percentage of annualized revenue(2) | | 54% | | 71% | |

Magna as a percentage of GLA | | 47% | | 61% | |

| | | | | | |

Table of Contents

| | | | | | | |

| | | | | | |

As at December 31,

|

|

2018

|

|

2017

|

|

|---|

| | | | | | |

(in millions, except as noted) | | | | | |

Assets held for sale | | | | | |

Fair value | | $ | 44.2 | | $ | 391.4 | |

Number of properties | | 6 | | 10 | |

GLA, square feet | | 0.7 | | 3.2 | |

Magna as a percentage of GLA | | 94% | | 95% | |

Annualized revenue(2) | | $ | 2.2 | | $ | 25.6 | |

| | | | | | |

- (1)

- Assets held for sale are excluded from investment properties and related property metrics. Accordingly, six such assets that were held for sale at December 31, 2018 (subsequently sold) and 10 such assets that were held for sale at December 31, 2017 were excluded from investment properties and related property metrics at December 31, 2018 and December 31, 2017, respectively, throughout this MD&A.

- (2)

- Annualized revenue for each period presented is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month of December multiplied by twelve months.

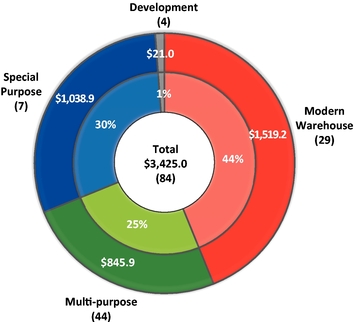

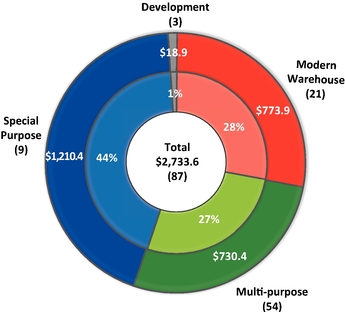

The fair value of the investment properties by asset category as at December 31, 2018 and 2017 was as follows:

Fair Value of Investment Properties by Asset Category(1)

| | |

December 31, 2018

| | December 31, 2017

|