Exhibit 4.5

MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL POSITION

| TABLE OF CONTENTS |

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 5 | ||||

| 8 | ||||

| 24 | ||||

| 34 | ||||

Commitments, Contractual Obligations, Contingencies andOff-Balance Sheet Arrangements | 41 | |||

| 41 | ||||

| 45 | ||||

| 46 | ||||

| 50 | ||||

| 50 | ||||

| 51 | ||||

| 52 | ||||

| BASIS OF PRESENTATION |

Management’s Discussion and Analysis of Results of Operations and Financial Position (“MD&A”) of Granite Real Estate Investment Trust (“Granite REIT”) and Granite REIT Inc. (“Granite GP”) summarizes the significant factors affecting the combined operating results, financial condition, liquidity and cash flows of Granite REIT, Granite GP and their subsidiaries (collectively “Granite” or the “Trust”) for the three and six month periods ended June 30, 2019. Unless otherwise noted, all amounts are in millions of Canadian dollars. This MD&A should be read in conjunction with the accompanying unaudited condensed combined financial statements for the three and six month periods ended June 30, 2019 and the audited combined financial statements for the year ended December 31, 2018 prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. The MD&A was prepared as at July 31, 2019 and its contents were approved by the Board of Trustees of Granite REIT and Board of Directors of Granite GP on this date. Additional information relating to Granite, including the Annual Report and Annual Information Form (“AIF”) for fiscal 2018, can be obtained from the Trust’s website atwww.granitereit.com, on SEDAR atwww.sedar.comand on EDGAR atwww.sec.gov.

In addition to using financial measures determined in accordance with IFRS, Granite also uses certainnon-IFRS measures in managing its business to measure financial and operating performance as well as for capital allocation decisions and valuation purposes. Granite believes that providing these measures on a supplemental basis to the IFRS results is helpful to investors in assessing the overall performance of Granite’s business. Thesenon-IFRS measures include net operating income before lease termination andclose-out fees, straight-line rent and tenant incentive amortization (“NOI — cash basis”), same property NOI — cash basis, funds from operations (“FFO”), adjusted funds from operations (“AFFO”), FFO payout ratio, AFFO payout ratio, leverage ratio, interest coverage ratio, net leverage ratio, indebtedness ratio, unencumbered asset coverage ratio and any related per unit amounts. Readers are cautioned that these measures do not have standardized meanings prescribed under IFRS and, therefore, should not be construed as alternatives to net income, cash provided by operating activities or any other measure calculated in accordance with IFRS. Additionally, because these terms do not have standardized meanings prescribed by IFRS, they may not be comparable to similarly titled measures presented by other reporting issuers. Refer to “NON-IFRS MEASURES” for definitions and reconciliations ofnon-IFRS measures to IFRS financial measures.

Granite REIT 2019 Second Quarter Report 1

| FINANCIAL AND OPERATING HIGHLIGHTS |

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| (in millions, except as noted) | 2019 | 2018 | 2019 | 2018 | ||||||||||||

Operating highlights | ||||||||||||||||

Revenue | $ | 67.9 | $ | 62.1 | $ | 131.3 | $ | 123.8 | ||||||||

NOI — cash basis(1) | 58.3 | 55.2 | 113.3 | 107.5 | ||||||||||||

Net income attributable to stapled unitholders | 98.7 | 149.2 | 176.9 | 221.5 | ||||||||||||

FFO(1)(2) | 43.1 | 37.6 | 83.8 | 88.7 | ||||||||||||

AFFO(1)(2) | 42.3 | 29.4 | 81.5 | 60.5 | ||||||||||||

Cash flows provided from operating activities | 50.1 | 45.0 | 90.5 | 82.5 | ||||||||||||

Monthly distributions paid | 33.7 | 31.2 | 65.6 | 62.8 | ||||||||||||

Special distribution paid | — | — | 13.7 | — | ||||||||||||

FFO payout ratio(1)(3) | 81% | 79% | 80% | 79% | ||||||||||||

AFFO payout ratio(1)(3) | 83% | 99% | 83% | 104% | ||||||||||||

Per unit amounts | ||||||||||||||||

Diluted FFO(1)(2) | $ | 0.89 | $ | 0.82 | $ | 1.78 | $ | 1.93 | ||||||||

Diluted AFFO(1)(2) | $ | 0.88 | $ | 0.64 | $ | 1.73 | $ | 1.32 | ||||||||

Monthly distributions paid | $ | 0.70 | $ | 0.68 | $ | 1.40 | $ | 1.36 | ||||||||

Special distribution paid | — | — | $ | 0.30 | — | |||||||||||

Diluted weighted average number of units | 48.3 | 45.8 | 47.0 | 46.1 | ||||||||||||

| As at June 30, 2019 and December 31, 2018 | 2019 | 2018 | ||||||||||||||

Financial highlights | ||||||||||||||||

Investment properties — fair value(4) | $ | 3,799.1 | $ | 3,425.0 | ||||||||||||

Assets held for sale(4) | 50.5 | 44.2 | ||||||||||||||

Cash and cash equivalents | 496.9 | 658.2 | ||||||||||||||

Total debt(5) | 1,285.6 | 1,303.2 | ||||||||||||||

Trading price per unit (TSX: GRT.UN) | $ | 60.29 | $ | 53.21 | ||||||||||||

Debt metrics, ratings and outlook | ||||||||||||||||

Net leverage ratio(1) | 21% | 19% | ||||||||||||||

Interest coverage ratio(1) | 9.3x | 9.4x | ||||||||||||||

Indebtedness ratio (total debt to adjusted EBITDA)(1) | 6.8x | 7.0x | ||||||||||||||

Weighted average cost of debt(6) | 2.17% | 2.17% | ||||||||||||||

Weighted average debtterm-to-maturity, in years(6) | 4.2 | 4.7 | ||||||||||||||

DBRS rating and outlook | BBB stable | BBB stable | ||||||||||||||

Moody’s rating and outlook | Baa2 stable | Baa2 stable | ||||||||||||||

Property metrics(4) | ||||||||||||||||

Number of investment properties | 83 | 84 | ||||||||||||||

Income-producing properties | 79 | 80 | ||||||||||||||

Properties under development | 2 | 2 | ||||||||||||||

Land held for development | 2 | 2 | ||||||||||||||

Gross leasable area (“GLA”), square feet | 34.5 | 32.2 | ||||||||||||||

Occupancy, by GLA | 98.9% | 99.1% | ||||||||||||||

Magna as a percentage of annualized revenue(7) | 48% | 54% | ||||||||||||||

Magna as a percentage of GLA | 41% | 47% | ||||||||||||||

Weighted average lease term in years, by GLA | 6.0 | 6.0 | ||||||||||||||

Overall capitalization rate(8) | 6.3% | 6.7% | ||||||||||||||

| (1) | For definitions of Granite’snon-IFRS measures, refer to the section “NON-IFRS MEASURES”. |

2 Granite REIT 2019 Second Quarter Report

| (2) | For the three and six months ended June 30, 2019, Granite recognized $0.6 million ($0.01 per unit) and $0.9 million ($0.02 per unit), respectively, in revenue related to lease termination andclose-out fees. For the three months ended June 30, 2018, Granite recognized a $1.9 million ($0.04 per unit) realized foreign exchange loss in the period relating to the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018. For the six months ended June 30, 2018, Granite recognized $1.0 million ($0.02 per unit) in revenue related to a lease termination andclose-out fee and a net $8.5 million ($0.19 per unit) realized foreign exchange gain during the period on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018. FFO, AFFO and the per unit amounts include the aforementioned items. |

In the first quarter of 2018, Granite also paid $9.1 million ($0.19 per unit) related to a tenant incentive allowance for a 2014 lease extension at the Eurostar facility in Graz, Austria. AFFO and AFFO per unit amounts have been reduced by this $9.1 million tenant allowance payment. |

| (3) | The FFO and AFFO payout ratios are calculated as monthly distributions, which exclude the special distribution, declared to unitholders divided by FFO and AFFO, respectively, in a period. For comparative purposes, the FFO payout ratio and AFFO payout ratio for the three months ended June 30, 2019 and 2018 exclude the lease termination andclose-out fees of $0.6 million and the $1.9 million realized foreign exchange loss relating to the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018, respectively. |

For comparative purposes, the FFO payout ratio and AFFO payout ratio for the six months ended June 30, 2019 and 2018 exclude the lease termination andclose-out fees of $0.9 million and $1.0 million, respectively, as well as the net $8.5 million realized foreign exchange gain relating to the remeasurement of US dollar cash proceeds from the sale of properties during the six months ended June 30, 2018. |

AFFO payout ratio further excludes the $9.1 million tenant incentive payment made in 2018 in connection with the 2014 lease extension at the Eurostar facility. |

| (4) | Assets held for sale are excluded from investment properties and related property metrics. Accordingly, six such assets that were held for sale at June 30, 2019 and six such assets that were held for sale at December 31, 2018 were excluded from investment properties and related property metrics at June 30, 2019 and December 31, 2018, respectively, throughout this MD&A. |

| (5) | The Trust has adopted IFRS 16,Leases effective January 1, 2019 resulting in the recognition of lease obligations on the combined balance sheet and, thereby, included in total debt (see “NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS”). |

| (6) | Excludes lease obligations noted above. |

| (7) | Annualized revenue for each period presented is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the reported month multiplied by 12 months. |

| (8) | Refer to “Valuation Metrics by Investment Property Asset Category” in the“Investment Properties”section. |

| BUSINESS OVERVIEW AND STRATEGIC OUTLOOK |

Business Overview

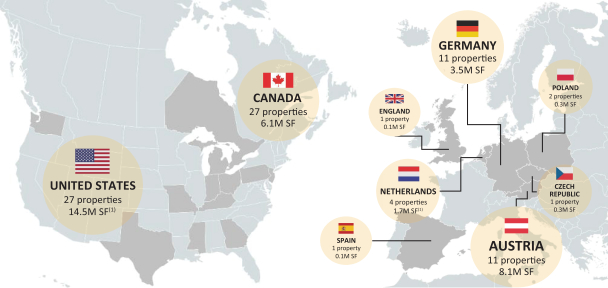

Granite is a Canadian-based real estate investment trust (“REIT”) engaged in the acquisition, development, ownership and management of industrial, warehouse and logistics properties in North America and Europe. As at July 31, 2019, Granite owns 85 investment properties in nine countries having approximately 34.7 million square feetof gross leasable area. The tenant base includes Magna International Inc. and its operating subsidiaries (collectively, “Magna”) as the largest tenant, in addition to tenants from various other industries. Properties leased to Magna are generally leased to operating subsidiaries of Magna International Inc. and the terms of the leases are not guaranteed by the parent company except for certain leases wherein the parent is the tenant.

Granite’s investment properties consist of income-producing properties, properties under development and land held for development (see“INVESTMENT PROPERTIES”). The income-producing properties consist of light industrial properties, heavy industrial manufacturing facilities, distribution/warehouse and logistics properties, corporate offices, product development and engineering centres and test facilities. The lease

Granite REIT 2019 Second Quarter Report 3

payments are primarily denominated in three currencies: the Canadian dollar (“$”), the Euro (“€”) and the US dollar (“US$”). Granite’s investment properties (excluding six assets held for sale) by geographic location, property count and square footage as at July 31, 2019 are summarized below:

Investment Properties Summary(1)

Nine countries/85 properties/34.7 million square feet |

| (1) | Includes an income-producing property in the Netherlands representing 0.3 million square feet of GLA and one property in the United States comprised of 190.6 acres of development land acquired subsequent to June 30, 2019. |

Strategic Outlook

Management continues to identify and pursue value creation and investment opportunities that will generate superior long-term total return for unitholders.

Granite’s strategy is to continue to build an institutional quality and globally diversified industrial real estate business; to grow and diversify its asset base through acquisitions, development,re-development and dispositions; to optimize its balance sheet; and to reduce its exposure to Magna and the special purpose properties (see“INVESTMENT PROPERTIES”) over the long-term.

Following the sale of 22non-core properties in 2018 and 2019 and the recent equity offering, Granite has positioned itself financially to capitalize on a strong pipeline of acquisition and development opportunities within its geographic footprint and execute on its strategic plan.

As Granite looks to the remainder of 2019, its priorities are as follows:

| • | Strategically deploy the proceeds from the recent equity offering and property dispositions; |

| • | Accelerate growth in its target markets in North America and Europe primarily through property, portfolio and corporate acquisitions as well as through joint venture arrangements and development of modern logistics ande-commerce assets; |

| • | Continue to dispose of selectnon-core assets; |

| • | Maintain a target occupancy in excess of 98%; |

| • | Enhance Granite’s global platform; |

4 Granite REIT 2019 Second Quarter Report

| • | Grow net asset value as well as FFO and AFFO per unit through intensive asset management; |

| • | Maintain lower leverage providing balance sheet flexibility and liquidity; and |

| • | Pursue development opportunities within the existing portfolio. |

| SIGNIFICANT MATTERS |

Property Acquisitions

During the six months ended June 30, 2019, Granite acquired three income-producing modern industrial properties in the United States and the leasehold interest in two properties in Mississauga, Ontario. Subsequent to thequarter-end, Granite acquired two properties consisting of development land in the United States and an income-producing property in Born, Netherlands. Property acquisitions consisted of the following:

Acquisitions (in millions, except as noted)

Property Address | Location | Sq ft(1) | Weighted sq ft(1) | Date Acquired | Property Purchase Price(2) | In-going Yield(1) | ||||||||||||||||||

Acquired during the six months ended June 30, 2019: |

| |||||||||||||||||||||||

201 Sunridge Boulevard | Wilmer, TX | 0.8 | 9.5 | Mar 1, 2019 | $ | 58.1 | 5.1% | |||||||||||||||||

3501 North Lancaster Hutchins Road | Lancaster, TX | 0.2 | 10.4 | Mar 1, 2019 | 106.1 | 6.8% | ||||||||||||||||||

Leasehold interest in two properties: 2020 and 2095 Logistics Drive | Mississauga, ON | 0.9 | 8.7 | Apr 9, 2019 | 153.6 | (3) | 4.5% | |||||||||||||||||

1901 Beggrow Street | Columbus, OH | 0.8 | 4.7 | May 23, 2019 | 71.6 | 5.7% | ||||||||||||||||||

Acquired between July 1, 2019 and July 31, 2019: |

| |||||||||||||||||||||||

190.6 acres of development land | Harris County, Texas | N/A | N/A | July 1, 2019 | 33.4 | N/A | ||||||||||||||||||

Heirweg 3 | Born, Netherlands | 0.3 | 7.6 | July 8, 2019 | 25.7 | 6.1% | ||||||||||||||||||

| 3.0 | 7.9 | $ | 448.5 | 5.4% | ||||||||||||||||||||

| (1) | As at the date of acquisition. |

| (2) | Purchase price does not include transaction costs associated with property acquisitions. |

| (3) | Excludesright-of-use asset of $20.5 million associated with ground lease (see “NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS”). |

On April 9, 2019, Granite acquired the leasehold interest in two distribution/warehouse properties located in Mississauga, Ontario for total consideration of $153.6 million. The contractual rent at 2020 Logistics Drive is significantly below market, providing expected net operating income growth upon lease rollover. The property located at 2095 Logistics Drive is expected to be expanded by approximately 0.1 million square feet by the second quarter of 2020, generating additional net operating income at an estimated yield of 8.9%.

On May 23, 2019, Granite acquired 1901 Beggrow Street, a 36 foot clear height distribution centre situated on 51.1 acres of land in Columbus, Ohio for consideration of $71.6 million (US$53.2 million). This state of the art facility was completed in 2018 and is 100% leased to a subsidiary of Pepsico, Inc. The property is well-located within the major southeast Columbus industrial market and within two miles of the Rickenbacker International Airport, one of the only cargo-dedicated airports in the world. The building can be expanded by approximately 0.2 million square feet, providing attractive site flexibility and growth potential.

On July 1, 2019, Granite, in partnership with NorthPoint Development, acquired a greenfield site in Houston, Texas for $33.4 million (US$25.4 million) for the future development of up to a 2.5 million square foot multi-phased business park capable of accommodating buildings ranging from 0.3 million to 1.2 million square feet. Speculative construction of the initial phase, consisting of two buildings totaling 0.6 million square feet, is anticipated to begin in the third quarter of 2019. The project is expected to generate a development yield spread of greater than 200 basis points. Granite’s partner, NorthPoint Development, will

Granite REIT 2019 Second Quarter Report 5

act as development manager for the project. The site is strategically located within Houston’s northeast submarket and located directly on US Highway 90, benefiting from exceptional access to Houston’s extensive interstate system, the city’s railroads and the Houston International Airport.

On July 8, 2019, Granite acquired Heirweg 3, a distribution centre situated on 7.4 acres of land in Born, Netherlands for $25.7 million (€17.5 million). Constructed in 2008, the property is 100% leased to Broekman Logistics and is well-located in an established business park. Its strategic location and close proximity to an inland port, rail and the A2 motorway provide excellent distribution access serving the local Dutch market as well as broader European markets.

Acquisition, Construction and Development Commitments

As at the date of this MD&A, Granite had the following property purchase and construction and development commitments:

Commitments (in millions, except as noted)

Property Location | Additional sq ft | Accruals/ Payments/ Deposits | Future Commitments | Total Cost | Year-One Stabilized Yield | |||||||||||||||

As at June 30, 2019: | ||||||||||||||||||||

Demolition phase of property under development in Altbach, Germany | — | $ | 1.2 | $ | 0.4 | $ | 1.6 | N/A | ||||||||||||

Expansion of 2095 Logistics Drive, Mississauga, ON | 0.1 | — | 9.0 | 9.0 | 8.9% | |||||||||||||||

Properties under development in Texas and Indiana as well as other construction commitments | 2.8 | 29.7 | 290.9 | 320.6 | 5.6% | |||||||||||||||

| 2.9 | $ | 30.9 | $ | 300.3 | $ | 331.2 | 5.7% | |||||||||||||

Commitments between July 1, 2019 and July 31, 2019: |

| |||||||||||||||||||

Property purchase in Horn Lake, Mississippi | 0.3 | — | 24.0 | 24.0 | 5.7% | |||||||||||||||

| 3.2 | $ | 30.9 | $ | 324.3 | $ | 355.2 | 5.7% | |||||||||||||

| (1) | As at June 30, 2019. |

A deposit of $26.2 million (US$20.0 million) was made during 2018 in connection with a contractual commitment to acquire a property under development in the state of Texas. This commitment to purchase the property under development is subject to specific confidentiality provisions and customary closing conditions including certain purchase rights in favour of the tenant and is expected to close in the fourth quarter of 2019 following construction of the building and commencement of the lease.

During the first quarter of 2019, Granite entered into an agreement for approximately $1.6 million (€1.1 million) to demolish an existing building on a13-acre site in Altbach, Germany. As at July 31, 2019, the demolition of the property is substantially complete and construction of a 0.3 million square foot distribution/light industrial facility is expected to commence in the first quarter of 2020, subject to receipt of all required permits and state approval.

On July 17, 2019, Granite agreed to acquire 1222 Commerce Parkway, a 32 foot clear height distribution centre situated on 20.9 acres of land in Horn Lake, Mississippi for total consideration of $24.0 million (US$18.5 million). The property was constructed in 2018 and is 100% leased to DSV Solutions and EPE Industries for a remaining weighted average lease term of 4.8 years. The acquisition is subject to customary closing conditions and is expected to close in the third quarter of 2019. The property is located within the DeSoto County submarket, less than 15 miles from downtown Memphis, Tennessee. The property offers exceptional access to Interstate 55 and proximity to the Memphis International Airport, which is home to the FedEx World Hub, the busiest air cargo airport in the United States.

6 Granite REIT 2019 Second Quarter Report

Property Dispositions

During the six months ended June 30, 2019, six properties previously classified as assets held for sale were disposed of for approximately $43.8 million. The properties consisted of the following:

Dispositions (in millions, except as noted)

Property Address | Location | Sq ft | Date Disposed | Sale Price | Annualized Revenue(1) | |||||||||||||

3 Walker Drive (a nine-acre parcel of land) | Brampton, ON | N/A | Jan 15, 2019 | $ | 13.4 | $ | — | |||||||||||

Iowa properties(four properties): | ||||||||||||||||||

403 S 8th Street | Montezuma, IA | |||||||||||||||||

1951 A Avenue | Victor, IA | |||||||||||||||||

408 N Maplewood Avenue | Williamsburg, IA | |||||||||||||||||

411 N Maplewood Avenue | Williamsburg, IA | 0.6 | Feb 25, 2019 | 22.3 | 2.2 | |||||||||||||

375 Edward Street | Richmond Hill, ON | 0.1 | Feb 27, 2019 | 8.1 | — | |||||||||||||

| 0.7 | $ | 43.8 | $ | 2.2 | ||||||||||||||

| (1) | Annualized revenue is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month the property was first classified as an asset held for sale multiplied by 12 months. |

Assets Held for Sale

As at June 30, 2019, six investment properties located in Canada and the United States were classified as assets held for sale. The six properties, having an aggregate fair value of $50.5 million, consisted of the following:

Held for Sale (in millions, except as noted)

Property Address | Location | Sq ft | Fair Value | Annualized Revenue(1) | ||||||||||

Michigan properties (five properties): | ||||||||||||||

6151 Bancroft Avenue | Alto, MI | |||||||||||||

3501 John F Donnelly Drive | Holland, MI | |||||||||||||

3575 128th Avenue | Holland, MI | |||||||||||||

3601 John F Donnelly Drive | Holland, MI | |||||||||||||

1800 Hayes Street | Grand Haven, MI | 0.7 | $ | 38.0 | $ | 3.6 | ||||||||

330 Finchdene Square | Toronto, ON | 0.1 | 12.5 | — | ||||||||||

| 0.8 | $ | 50.5 | $ | 3.6 | ||||||||||

| (1) | Annualized revenue is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the month the property was first classified as an asset held for sale multiplied by 12 months. |

These aforementioned properties were classified as assets held for sale on the combined balance sheets at June 30, 2019 and were excluded from the value of investment properties. These properties are also excluded from references to investment properties and related property metrics as at June 30, 2019 throughout this MD&A.

Officer and Board Changes and Appointments

On June 3, 2019, Granite announced the departure of its Chief Financial Officer (“CFO”), Ilias Konstantopoulos. Subsequently, effective July 8, 2019, Teresa Neto was appointed Granite’s CFO. Ms. Neto has over 13 years of real estate experience and has held previous CFO positions at publicly traded real estate investment trusts in Canada, most recently at Pure Industrial Real Estate Trust and prior to that at Northwest Healthcare Properties REIT. Ms. Neto has a chartered professional accounting designation (CPA, CA) and is a member of the Institute of Corporate Directors.

Granite REIT 2019 Second Quarter Report 7

On June 13, 2019, at the Trust’s annual general meeting, Fern Grodner and Sheila Murray were elected as new trustees of Granite REIT and directors of Granite GP. Donald Clow and Samir Manji did not stand forre-election. Ms. Grodner has over 25 years of corporate real estate experience which includes her roles at Amazon.com, Inc. as Senior Manager, Global Real Estate and Facilities and JDS Uniphase Corporation overseeing all real estate aspects of office and manufacturing sites. Ms. Murray was most recently the President and prior to that, the Executive Vice-President, General Counsel and Secretary of CI Financial Corp., following a25-year career at Blake, Cassels & Graydon LLP. Ms. Murray is also a member of the Board of Directors of Teck Resources Limited, Lendified Holdings Inc., and the SickKids Foundation, a trustee of the Toronto Symphony Foundation, and has been a director of a number of other private and public companies.

Bought Deal Equity Offering

On April 30, 2019, Granite completed an offering of 3,749,000 stapled units at a price of $61.50 per unit for gross proceeds of $230.6 million, including 489,000 stapled units issued pursuant to the exercise of the over-allotment option granted to the underwriters. Total costs related to the offering totaled $10.2 million.

Normal Course Issuer Bid

On May 14, 2019, Granite renewed its normal course issuer bid for an additional year.

| RESULTS OF OPERATIONS |

Foreign Currency Translation

The majority of Granite’s investment properties are located in Europe and the United States and the cash flows derived from such properties are primarily denominated in Euros and US dollars. Accordingly, fluctuations in the Canadian dollar, Granite’s reporting currency, relative to the Euro and US dollar will result in fluctuations in the reported values of revenues, expenses, cash flows, assets and liabilities. The most significant foreign currency exchange rates that impact Granite’s business are summarized in the following table:

Average Exchange Rates | Period End Exchange Rates | |||||||||||||||||||||||||||||||||||||||||||

Three Months Ended June 30, | Six Months Ended | June 30, 2019 | December 31, 2018 | |||||||||||||||||||||||||||||||||||||||||

| 2019 | 2018 | Change | 2019 | 2018 | Change | Change | ||||||||||||||||||||||||||||||||||||||

$ per€1.00 | 1.503 | 1.539 | (2% | ) | 1.506 | 1.547 | (3% | ) | 1.489 | 1.563 | (5% | ) | ||||||||||||||||||||||||||||||||

$ per US$1.00 | 1.338 | 1.291 | 4% | 1.333 | 1.278 | 4% | 1.309 | 1.364 | (4% | ) | ||||||||||||||||||||||||||||||||||

For the three and six months ended June 30, 2019 compared to the prior year periods, the average exchange rates of the Canadian dollar relative to the Euro and US dollar were lower and higher, respectively, which on a comparative basis, decreased the Canadian dollar equivalent of revenue and expenses from Granite’s European operations and increased the Canadian dollar equivalent of revenue and expenses from Granite’s US operations.

The period end exchange rates of the Canadian dollar relative to the Euro and US dollar on June 30, 2019 were lower when compared to the December 31, 2018 exchange rates. As a result, the Canadian dollar equivalent of assets and liabilities from Granite’s European and US subsidiaries were lower when compared to December 31, 2018.

8 Granite REIT 2019 Second Quarter Report

On a net basis, the effect of the changes in exchange rates on Granite’s operating results for the three and six months ended June 30, 2019 was as follows:

Effects of Changes in Exchange Rates on Operating Results |

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||

| (in millions, except per unit information) | 2019 vs 2018 | 2019 vs 2018 | ||||||

Increase in revenue | $ | 0.2 | $ | 0.3 | ||||

Increase in NOI — cash basis | — | 0.1 | ||||||

Increase in net income | 0.3 | 0.7 | ||||||

Increase in FFO | 0.5 | 1.4 | ||||||

Increase in AFFO | 0.4 | 1.1 | ||||||

Increase in FFO per unit | $ | 0.01 | $ | 0.03 | ||||

Increase in AFFO per unit | $ | 0.01 | $ | 0.02 | ||||

Operating Results

Revenue

Revenue |

Three Months Ended | Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2019 | 2018 | $ change | 2019 | 2018 | $ change | |||||||||||||||||||||||

Rental revenue | $ | 59.6 | $ | 55.3 | 4.3 | $ | 115.4 | $ | 109.3 | 6.1 | ||||||||||||||||||

Tenant recoveries | 7.7 | 6.8 | 0.9 | 15.0 | 13.5 | 1.5 | ||||||||||||||||||||||

Lease termination andclose-out fees | 0.6 | — | 0.6 | 0.9 | 1.0 | (0.1 | ) | |||||||||||||||||||||

Revenue | $ | 67.9 | $ | 62.1 | 5.8 | $ | 131.3 | $ | 123.8 | 7.5 | ||||||||||||||||||

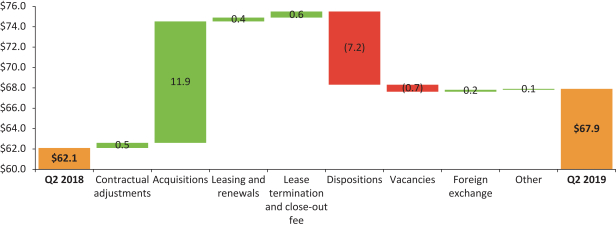

Revenue for the three month period ended June 30, 2019 increased $5.8 million to $67.9 million from $62.1 million in the prior year period. The components contributing to the change in revenue are detailed below:

Q2 2019 vs Q2 2018 Change in Revenue |

Granite REIT 2019 Second Quarter Report 9

Additional details pertaining to the components of the change in revenue are as follows:

| • | contractual rent adjustments included $0.3 million from consumer price index based increases and $0.2 million from fixed contractual adjustments related to rent escalations; |

| • | the acquisitions of properties located in the United States, Canada and Germany beginning in the second quarter of 2018 increased revenue by $11.9 million, which included $1.6 million of tenant recoveries; |

| • | revenue increased by $0.4 million due to various renewal andre-leasing activities for properties primarily in Canada, the United States and Austria; |

| • | revenue increased by $0.6 million as a result of a leaseclose-out fee received in 2019 for a property in Canada that was vacated and classified as asset held for sale; |

| • | the sale of 11 properties in Canada, the United States and Germany beginning in the second quarter of 2018 decreased revenue by $7.2 million of which $0.6 million related to a reduction in property tax and insurance tenant recoveries; |

| • | two lease expiries and one lease termination for properties in Canada and the United States resulted in vacancies that decreased revenue by $0.3 million and $0.4 million, respectively; and |

| • | foreign exchange had a net $0.2 million positive impact as the weakening of the Canadian dollar against the US dollar increased revenue by $0.8 million while the relative strengthening of the Canadian dollar against the Euro decreased revenue by $0.6 million. |

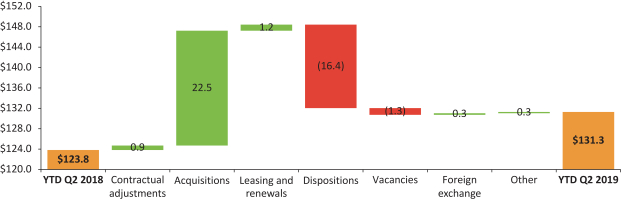

Revenue for the six month period ended June 30, 2019 increased $7.5 million to $131.3 million from $123.8 million in the prior year period. The components contributing to the change in revenue are detailed below:

Q2 2019 YTD vs Q2 2018 YTD Change in Revenue |

Additional details pertaining to the components of the change in revenue are as follows:

| • | contractual rent adjustments included $0.6 million from consumer price index based increases and $0.3 million from fixed contractual adjustments related to rent escalations; |

| • | the acquisitions of properties located in the United States, Canada and Germany during 2018 and 2019 increased revenue by $22.5 million, which included $2.7 million of tenant recoveries; |

| • | revenue increased by $1.2 million due to various renewal andre-leasing activities for properties primarily in Canada and the United States; |

| • | the sale of 21 properties in Canada, the United States and Germany in 2018 and 2019 decreased revenue by $16.4 million of which $1.7 million related to a reduction in property tax and insurance tenant recoveries; |

10 Granite REIT 2019 Second Quarter Report

| • | three vacancies noted above for properties in Canada and the United States decreased revenue by $0.6 million and $0.7 million, respectively; and |

| • | foreign exchange had a net $0.3 million positive impact as the weakening of the Canadian dollar against the US dollar increased revenue by $1.7 million while the relative strengthening of the Canadian dollar against the Euro decreased revenue by $1.4 million. |

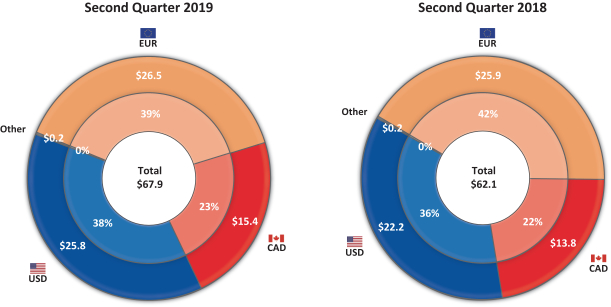

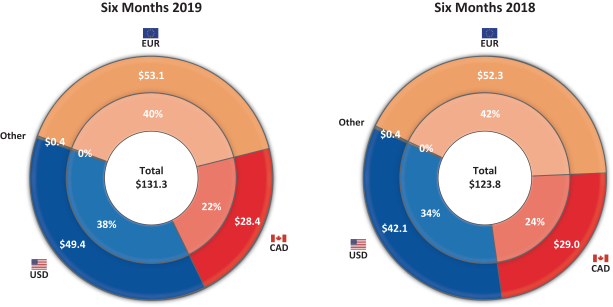

Revenue by major currency for the three and six months ended June 30, 2019 and 2018 was as follows:

Revenue by Currency |

As a majority of the Trust’s revenue is denominated in currencies other than the Canadian dollar, Granite uses derivative financial instruments, including cross currency interest rate swaps and forward currency contracts,

Granite REIT 2019 Second Quarter Report 11

to partially hedge its exposure to foreign currencies and reduce the potential impact that foreign currency rate changes may have on Granite’s operating results, cash flows and distributions (see “DEBT STRUCTURE”).

Net Operating Income

Net operating income (“NOI”) in the three months ended June 30, 2019 was $59.1 million compared to $54.7 million in the three months ended June 30, 2018. NOI in the six months ended June 30, 2019 was $114.3 million compared to $108.5 million in the six months ended June 30, 2018. NOI — cash basis excludes the impact of lease termination andclose-out fees, and straight-line rent and tenant incentive amortization and reflects the cash generated by the income-producing properties excluding lease termination andclose-out fees on a period-over-period basis. NOI — cash basis was $58.3 million in the three months ended June 30, 2019 compared with $55.2 million in the prior year period. NOI — cash basis was $113.3 million in the six months ended June 30, 2019 compared with $107.5 million in the six months ended June 30, 2018.

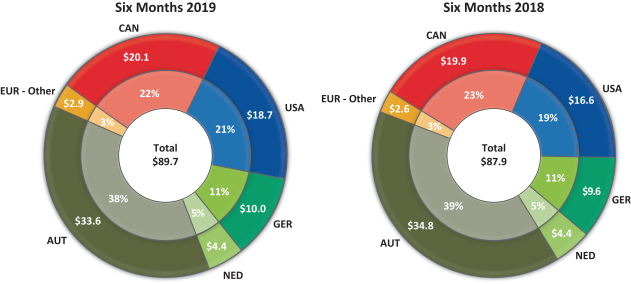

Same property NOI — cash basis refers to the NOI — cash basis for those properties owned by Granite throughout the entire current and prior year periods under comparison. Same property NOI — cash basis excludes properties that were acquired, disposed of, classified as properties under or held for development or assets held for sale during the periods under comparison. Same property NOI — cash basis in the three months ended June 30, 2019 and 2018 were both $45.5 million. Same property NOI — cash basis in the six months ended June 30, 2019 was $89.7 million compared to $87.9 million in the six months ended June 30, 2018. The changes in NOI, NOI — cash basis and same property NOI — cash basis are detailed below:

Changes in NOI(2), NOI — Cash Basis and Same Property NOI — Cash Basis |

Sq ft(1) (in millions) | Three Months Ended June 30, | $ change | Sq ft(1) (in millions) | Six Months Ended June 30, | $ change | |||||||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||||||||||

Revenue | $ | 67.9 | $ | 62.1 | 5.8 | $ | 131.3 | $ | 123.8 | 7.5 | ||||||||||||||||||||||

Less: Property operating costs | (8.8 | ) | (7.4 | ) | (1.4 | ) | (17.0 | ) | (15.3 | ) | (1.7 | ) | ||||||||||||||||||||

NOI(2) | $ | 59.1 | $ | 54.7 | 4.4 | $ | 114.3 | $ | 108.5 | 5.8 | ||||||||||||||||||||||

Add (deduct): | ||||||||||||||||||||||||||||||||

Lease termination andclose-out fees | (0.6 | ) | — | (0.6 | ) | (0.9 | ) | (1.0 | ) | 0.1 | ||||||||||||||||||||||

Straight-line rent amortization | (1.5 | ) | (0.8 | ) | (0.7 | ) | (2.7 | ) | (2.7 | ) | — | |||||||||||||||||||||

Tenant incentive amortization | 1.3 | 1.3 | — | 2.6 | 2.7 | (0.1 | ) | |||||||||||||||||||||||||

NOI — cash basis | 34.5 | $ | 58.3 | $ | 55.2 | 3.1 | 34.5 | $ | 113.3 | $ | 107.5 | 5.8 | ||||||||||||||||||||

Less NOI — cash basis for: | ||||||||||||||||||||||||||||||||

Acquisitions | 8.4 | (11.7 | ) | (2.7 | ) | (9.0 | ) | 9.0 | (21.3 | ) | (3.4 | ) | (17.9 | ) | ||||||||||||||||||

Dispositions, assets held for sale and developments | 0.8 | (1.1 | ) | (7.0 | ) | 5.9 | 1.6 | (2.3 | ) | (16.2 | ) | 13.9 | ||||||||||||||||||||

Same property NOI — cash basis | 26.1 | $ | 45.5 | $ | 45.5 | — | 25.5 | $ | 89.7 | $ | 87.9 | 1.8 | ||||||||||||||||||||

| (1) | The square footage relating to the NOI — cash basis represents GLA of 34.5 million square feet as at June 30, 2019. The square footage relating to the same property NOI — cash basis represents the aforementioned GLA excluding the impact from the acquisitions during the relevant periods. |

| (2) | NOI is calculated in accordance with IFRS and is included in the unaudited condensed combined financial statements as at and for the three and six months ended June 30, 2019. In the prior year periods, Granite reported NOI as anon-IFRS financial measure, calculated as set forth above but excluding lease termination andclose-out fee revenue. NOI for the six months ended June 30, 2018 was previously reported as $107.5 million, and for the quarter ended June 30, 2018 remained the same as previously reported. |

12 Granite REIT 2019 Second Quarter Report

Property operating costs include recoverable andnon-recoverable costs from tenants and consist of property taxes, utilities, insurance, repairs and maintenance, legal and other property-related expenses. None of Granite’s employee compensation expenses are included in property operating costs.

Straight-line rent amortization represents the scheduled fixed rent changes or rent-free periods in leases that are recognized in revenue evenly on a straight-line basis over the term of the lease. Tenant incentive amortization mainly represents allowances provided to tenants that are recognized in revenue evenly on a straight-line basis over the term of the lease and primarily comprises the amortization associated with the cash allowance incentives paid to Magna in respect of the10-year lease extensions exercised during the 2014 year at the Thondorf and Eurostar properties in Graz, Austria.

NOI — cash basis for the three month period ended June 30, 2019 increased $3.1 million to $58.3 million from $55.2 million in the prior year period largely as a result of the increase in rental revenue as noted previously, partially offset by an increase in property operating costs primarily relating to the properties acquired in 2018 and 2019 and a decrease from straight-line rent amortization, primarily from rent-free periods associated with the building expansion completed in January 2019 at the West Jefferson, Ohio property and the recently acquired property in Mississauga, Ontario.

NOI — cash basis for the six month period ended June 30, 2019 increased $5.8 million to $113.3 million from $107.5 million in the prior year period largely as a result of the increase in rental revenue as noted previously.

Same property NOI — cash basis for the three month periods ended June 30, 2019 and 2018 remained consistent at $45.5 million. Same property NOI — cash basis for the six month period ended June 30, 2019 increased $1.8 million (2.0%) to $89.7 million primarily due to the increase in contractual rents, partiallease-up of the property in Novi, Michigan, andre-leasing and renewals of various leases for properties located in Canada, the United States and Germany, partially offset by vacancies for properties in Canada and the United States and the unfavourable foreign exchange impact from the strengthening of the Canadian dollar against the Euro. Excluding the impact of foreign exchange, same property NOI — cash basis for the three and six month periods ended June 30, 2019 would have increased by 0.6% and 2.8%, respectively.

Granite REIT 2019 Second Quarter Report 13

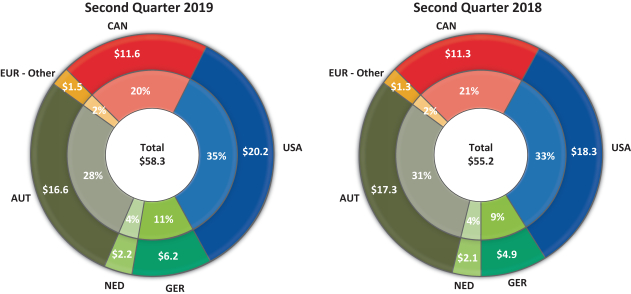

NOI — cash basis for the three and six month periods ended June 30, 2019 and 2018 by geography was as follows:

NOI — Cash Basis by Geography |

Granite’s property portfolio and NOI — cash basis are geographically diversified, which reduces the risk to Granite’s operating results from any particular country’s economic downturn.

14 Granite REIT 2019 Second Quarter Report

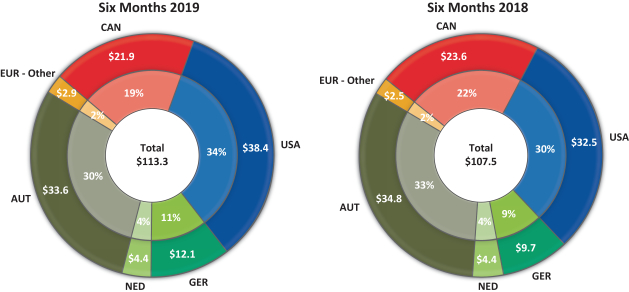

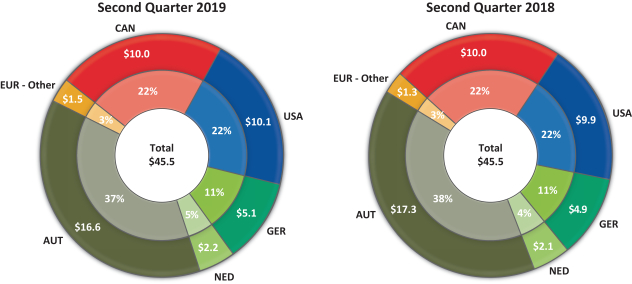

Same property NOI — cash basis for the three and six month periods ended June 30, 2019 and 2018 by geography was as follows:

Same Property NOI — Cash Basis by Geography |

Granite REIT 2019 Second Quarter Report 15

General and Administrative Expenses

General and administrative expenses consisted of the following:

General and Administrative Expenses |

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2019 | 2018 | $ change | 2019 | 2018 | $ change | |||||||||||||||||||||||

Salaries and benefits | $ | 4.4 | $ | 3.6 | 0.8 | $ | 7.4 | $ | 8.1 | (0.7 | ) | |||||||||||||||||

Audit, legal and consulting | 1.1 | 1.1 | — | 2.5 | 1.9 | 0.6 | ||||||||||||||||||||||

Trustee/director fees and related expenses | 0.3 | 0.3 | — | 0.6 | 0.6 | — | ||||||||||||||||||||||

Unit-based compensation including distributions and revaluations | 1.3 | 0.6 | 0.7 | 3.2 | 1.6 | 1.6 | ||||||||||||||||||||||

Other public entity costs | 0.7 | 0.6 | 0.1 | 1.2 | 0.9 | 0.3 | ||||||||||||||||||||||

Office rents including property taxes and common area maintenance costs | 0.1 | 0.2 | (0.1 | ) | 0.2 | 0.4 | (0.2 | ) | ||||||||||||||||||||

Other | 0.7 | 0.8 | (0.1 | ) | 1.4 | 1.1 | 0.3 | |||||||||||||||||||||

General and administrative expenses | $ | 8.6 | $ | 7.2 | 1.4 | $ | 16.5 | $ | 14.6 | 1.9 | ||||||||||||||||||

General and administrative expenses were $8.6 million for the three month period ended June 30, 2019 and increased $1.4 million in comparison to the prior year period primarily as a result of the following:

| • | an increase in salaries and benefits expense mainly due to higher compensation costs of $0.6 million in the current year period compared to the prior year period associated with departed executives. The compensation costs related to the former CFO were $1.6 million for the current year period; and |

| • | an increase in unit-based compensation costs mainly due to the accelerated vesting of awards related to the former CFO of $0.5 million, partially offset by the increase in fair value remeasurement recovery resulting from fluctuations in the market price of the Trust’s stapled units. For the three months ended June 30, 2019 and 2018, general and administrative expenses included a fair value remeasurement recovery of $0.2 million and expense of $0.2 million, respectively, associated with the unit-based compensation plans. |

General and administrative expenses were $16.5 million for the six months ended June 30, 2019 and increased $1.9 million in comparison to the prior year period primarily as a result of the following:

| • | an increase in unit-based compensation costs due to the increase in fair value remeasurement expense resulting from fluctuations in the market price of the Trust’s stapled units, greater awards outstanding under the plans and the accelerated vesting of awards noted above. For the six months ended June 30, 2019 and 2018, general and administrative expenses included a fair value remeasurement expense of $1.0 million and $0.5 million, respectively, associated with the unit-based compensation plans; and |

| • | an increase in audit, legal and consulting costs due to corporate advisory matters including internal reorganizations and administrative matters. These increases were partially offset by: |

| • | a decrease in salaries and benefits expense mainly due to a $0.5 million decrease in compensation costs in the current year period (including compensation related to the former CFO) compared to the prior year period associated with departed executives. |

16 Granite REIT 2019 Second Quarter Report

Interest Income

Interest income for the three month period ended June 30, 2019 increased $2.1 million to $2.7 million from $0.6 million in the prior year period. Interest income for the six month period ended June 30, 2019 increased $3.9 million to $5.6 million from $1.7 million in the prior year period. Both increases were primarily due to interest income earned from higher cash balances resulting from the proceeds from the April 2019 equity offering and drawdowns from the term loans in December 2018.

Interest Expense and Other Financing Costs

Interest expense and other financing costs for the three month period ended June 30, 2019 increased $2.4 million to $7.8 million from $5.4 million in the prior year period. Interest expense and other financing costs for the six months ended June 30, 2019 increased $4.4 million to $15.4 million from $11.0 million in the prior year period. Both increases were primarily related to:

| • | interest expense associated with the term loan drawdowns in December 2018; and |

| • | the accretion of interest related to lease obligations as a result of the adoption of IFRS 16,Leasesin 2019(see“NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS”). These increases were partially offset by: |

| • | the higher interest expense associated with the credit facility draws in the prior year period. |

As at June 30, 2019, Granite’s weighted average cost of interest-bearing debt was 2.17% (June 30, 2018 — 2.65%) and the weighted average debtterm-to-maturity was 4.2 years (June 30, 2018 — 4.0 years).

Foreign Exchange Gains/Losses, Net

Granite recognized net foreign exchange losses of $0.3 million and $2.3 million in the three month periods ended June 30, 2019 and 2018, respectively. The $2.0 million decrease in net foreign exchange losses is substantially due to the realized foreign exchange loss of $1.9 million recognized in the prior year period relating to the remeasurement of the US dollar cash proceeds from the sale of three investment properties in January 2018.

Granite recognized net foreign exchange losses of $0.8 million and foreign exchange gains of $9.1 million in the six month periods ended June 30, 2019 and 2018, respectively. The $9.9 million increase in net foreign exchange losses is substantially due to the realized net foreign exchange gain of $8.5 million in the prior year period relating to the remeasurement of the US dollar cash proceeds from the sale of three investment properties in January 2018 and, to a lesser extent, the remeasurement of certain monetary assets and liabilities of the Trust that are denominated in US dollars or Euros.

Acquisition Transaction Costs

There were no amounts recorded in acquisition transaction costs for the three and six month periods ended June 30, 2019 as Granite has early adopted, effective January 1, 2019, the amendments to IFRS 3,Business Combinations (see “NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS”). Accordingly, transaction costs relating to asset acquisitions are initially recorded to investment properties and, when subsequently measured at fair value, are expensed to net fair value gains/losses on investment properties. For the three and six month periods ended June 30, 2019, transaction costs of $0.9 million and $1.3 million, respectively, were recorded to net fair value gains/losses on investment properties. Acquisition transaction costs for the three and six month periods ended June 30, 2018 were $1.6 million and $1.7 million, respectively. Acquisition transaction costs primarily include land transfer tax and legal and advisory costs.

Granite REIT 2019 Second Quarter Report 17

Fair Value Gains/Losses on Investment Properties, Net

Net fair value gains on investment properties were $69.6 million and $127.9 million in the three month periods ended June 30, 2019 and 2018, respectively. In the three month period ended June 30, 2019, net fair value gains of $69.6 million were primarily attributable to (i) the favourable changes in leasing assumptions associated with fair market rent increases for properties located in Canada and the United States and (ii) a compression in discount and terminal capitalization rates for certain European properties, both resulting from the continued market demand for industrial real estate properties.

Net fair value gains on investment properties in the three month period ended June 30, 2018 of $127.9 million were largely attributable to (i) the increase in fair value to the expected sale price of the six multi-purpose and special purpose propertiesclassified as assets held for sale in the second quarter of 2018 and (ii) for certain properties across Granite’s portfolio, positive changes in leasing assumptions primarily from fair market rent increases and a compression in discount and terminal capitalization rates resulting from market demand.

Net fair value gains on investment properties were $119.7 million and $160.2 million in the six month periods ended June 30, 2019 and 2018, respectively. In the six month period ended June 30, 2019, net fair value gains of $119.7 million were attributable to various factors including (i) the positive changes in leasing assumptions associated with lease renewals and fair market rent increases for properties located in Canada and the United States and (ii) a compression in discount and terminal capitalization rates for certain European properties resulting from the continued market demand for industrial real estate properties.

Net fair value gains on investment properties in the six month period ended June 30, 2018 of $160.2 million were primarily attributable to (i) the increase in fair value to the expected sale price of six multi-purpose and special purpose properties as noted above and(ii) for certain properties across Granite’s portfolio, positive changes in leasing assumptions primarily from contractual and fair market rent increases as well as lease renewals and a compression in discount and terminal capitalization rates resulting from market demand.

Loss on Sale of Investment Properties

The loss on sale of investment properties for the three and six month periods ended June 30, 2019 was $0.6 million and $1.4 million compared to $0.1 million and $1.2 million for the prior year periods, respectively. Loss on sale of investment properties is related to broker commissions and legal and advisory costs associated with the dispositions or planned dispositions of assets held for sale.

18 Granite REIT 2019 Second Quarter Report

Income Tax Expense

Income tax expense comprised the following:

Income Tax Expense |

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2019 | 2018 | $ change | 2019 | 2018 | $ change | |||||||||||||||||||||||

Foreign operations | $ | 1.2 | $ | 1.4 | (0.2 | ) | $ | 2.7 | $ | 3.0 | (0.3 | ) | ||||||||||||||||

Withholding taxes | — | 0.7 | (0.7 | ) | — | 0.7 | (0.7 | ) | ||||||||||||||||||||

Related to sale of an investment property | — | 0.2 | (0.2 | ) | — | 0.2 | (0.2 | ) | ||||||||||||||||||||

Other | 0.5 | 0.5 | — | 0.9 | 0.9 | — | ||||||||||||||||||||||

Current tax expense | 1.7 | 2.8 | (1.1 | ) | 3.6 | 4.8 | (1.2 | ) | ||||||||||||||||||||

Deferred tax expense | 11.8 | 18.1 | (6.3 | ) | 22.7 | 26.1 | (3.4 | ) | ||||||||||||||||||||

Income tax expense | $ | 13.5 | $ | 20.9 | (7.4 | ) | $ | 26.3 | $ | 30.9 | (4.6 | ) | ||||||||||||||||

For the three and six months ended June 30, 2019, the current tax expense decreased compared to the prior year periods primarily due to withholding taxes on inter-company dividends paid in the prior year periods, the foreign exchange impact resulting from the relative strengthening of the Canadian dollar on Euro denominated tax expense, and the payment of taxes in the prior year periods on the disposition of a property located in Germany.

The decrease in deferred tax expense for the three and six months ended June 30, 2019 compared to the prior year periods was primarily due to a decrease in fair value gains in jurisdictions in which deferred taxes are recorded.

Granite REIT 2019 Second Quarter Report 19

Net Income Attributable to Stapled Unitholders

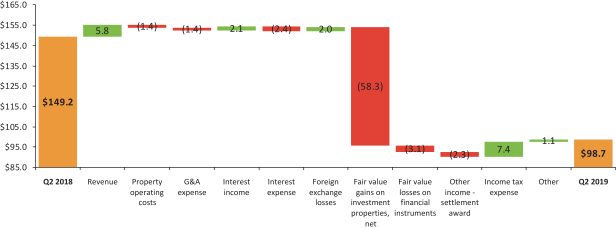

For the three month period ended June 30, 2019, net income attributable to stapled unitholders was $98.7 million compared to $149.2 million in the prior year period. The $50.5 million net decrease was primarily due to a $58.3 million decrease in net fair value gains on investment properties, partially offset by a $5.8 million increase in revenue. The $50.5 million decrease in net income attributable to stapled unitholders is summarized below:

Q2 2019 vs Q2 2018 Change in Net Income Attributable to Stapled Unitholders |

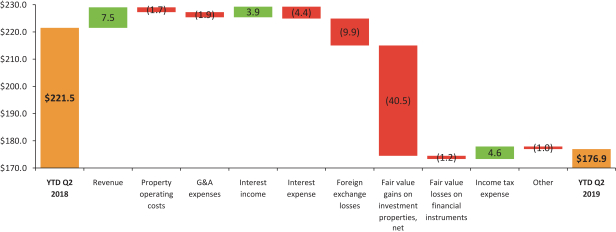

For the six month period ended June 30, 2019, net income attributable to stapled unitholders was $176.9 million compared to $221.5 million in the prior year period. The $44.6 million net decrease was primarily due to a $40.5 million decrease in net fair value gains on investment properties. The $44.6 million decrease in net income attributable to stapled unitholders is summarized below:

Q2 2019 YTD vs Q2 2018 YTD Change in Net Income Attributable to Stapled Unitholders |

20 Granite REIT 2019 Second Quarter Report

Funds From Operations and Adjusted Funds From Operations

The reconciliation of net income attributable to stapled unitholders to FFO and AFFO for the three and six months ended June 30, 2019 and 2018 is presented below:

FFO AND AFFO RECONCILIATION |

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||

| (in millions, except per unit information) | 2019 | 2018 | 2019 | 2018 | ||||||||||||||

Net income attributable to stapled unitholders | $ | 98.7 | $ | 149.2 | $ | 176.9 | $ | 221.5 | ||||||||||

Add (deduct): | ||||||||||||||||||

Fair value gains on investment | (69.6 | ) | (127.9 | ) | (119.7 | ) | (160.2 | ) | ||||||||||

Fair value losses (gains) on financial instruments | 1.7 | (1.4 | ) | 1.8 | 0.5 | |||||||||||||

Acquisition transaction costs | — | 1.6 | — | 1.7 | ||||||||||||||

Loss on sale of investment properties | 0.6 | 0.1 | 1.4 | 1.2 | ||||||||||||||

Other income — settlement award | — | (2.3 | ) | — | (2.3 | ) | ||||||||||||

Current income tax expense associated with the sale of an investment property | — | 0.2 | — | 0.2 | ||||||||||||||

Deferred income tax expense | 11.8 | 18.1 | 22.7 | 26.1 | ||||||||||||||

Fair value remeasurement expense relating to the Executive Deferred Stapled Unit Plan(1) | — | — | 0.7 | — | ||||||||||||||

Non-controlling interests relating to the above | (0.1 | ) | — | — | — | |||||||||||||

FFO | [A] | $ | 43.1 | $ | 37.6 | $ | 83.8 | $ | 88.7 | |||||||||

Add (deduct): | ||||||||||||||||||

Maintenance or improvement | (0.6 | ) | (6.2 | ) | (1.8 | ) | (15.0 | ) | ||||||||||

Leasing commissions paid | — | (2.3 | ) | (0.2 | ) | (4.0 | ) | |||||||||||

Tenant incentives paid | — | (0.2 | ) | (0.2 | ) | (9.2 | ) | |||||||||||

Tenant incentive amortization | 1.3 | 1.3 | 2.6 | 2.7 | ||||||||||||||

Straight-line rent amortization | (1.5 | ) | (0.8 | ) | (2.7 | ) | (2.7 | ) | ||||||||||

AFFO | [B] | $ | 42.3 | $ | 29.4 | $ | 81.5 | $ | 60.5 | |||||||||

Per unit amounts: | ||||||||||||||||||

Basic and diluted FFO per stapled unit | [A]/[C] and [A]/[D] | $ | 0.89 | $ | 0.82 | $ | 1.78 | $ | 1.93 | |||||||||

Basic and diluted AFFO per stapled unit | [B]/[C] and [B]/[D] | $ | 0.88 | $ | 0.64 | $ | 1.73 | $ | 1.32 | |||||||||

Basic weighted average number of | [C] | 48.2 | 45.8 | 47.0 | 46.0 | |||||||||||||

Diluted weighted average number of stapled units | [D] | 48.3 | 45.8 | 47.0 | 46.1 | |||||||||||||

| (1) | The Executive Deferred Stapled Unit Plan provides equity-based compensation in the form of stapled units to executives and other employees. It is anticipated that the fair value remeasurement relating to the Executive Deferred Stapled Unit Plan will fluctuate and have a greater impact on FFO and AFFO going forward and has, therefore, been adjusted in FFO and AFFO in accordance with the REALPAC White Paper. The comparative amount was not adjusted as it was not significant in the prior year periods and the year 2018. |

Granite REIT 2019 Second Quarter Report 21

Funds From Operations

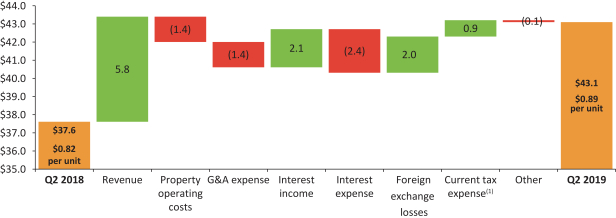

FFO for the three month period ended June 30, 2019 was $43.1 million ($0.89 per unit) compared to $37.6 million ($0.82 per unit) in the prior year period. The $5.5 million ($0.07 per unit) increase in FFO is summarized below:

Q2 2019 vs Q2 2018 Change in FFO |

| (1) | Excludes current tax expense of $0.2 million associated with the sale of an investment property in 2018. |

Excluding the compensation costs of $2.1 million ($0.04 per unit) associated with the departure of the former CFO, which include the accelerated vesting of unit-based awards, FFO would have been $45.2 million ($0.93 per unit) in the three month period ended June 30, 2019. Excluding the foreign exchange loss of $1.9 million ($0.04 per unit) realized during the second quarter of 2018 on US dollar cash proceeds from the sale of investment properties in January 2018 and the compensation costs relating to departed executives of $1.0 million ($0.02 per unit), FFO would have been $40.5 million ($0.88 per unit) in the three month period ended June 30, 2018.

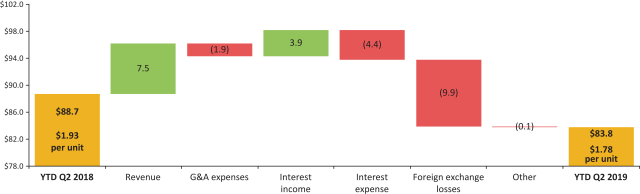

FFO for the six months ended June 30, 2019 was $83.8 million ($1.78 per unit) compared to $88.7 million ($1.93 per unit) in the prior year period. The $4.9 million ($0.15 per unit) decrease in FFO is summarized below:

Q2 2019 YTD vs Q2 2018 YTD Change in FFO |

Excluding the compensation costs of $2.1 million ($0.04 per unit) associated with the departure of the former CFO, which include the accelerated vesting of unit-based awards, FFO would have been $85.9 million ($1.82 per unit) for the six months ended June 30, 2019. In comparison, excluding the net

22 Granite REIT 2019 Second Quarter Report

foreign exchange gain of $8.5 million ($0.19 per unit) realized during the period on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018 and the compensation costs associated with departed executives of $2.4 million ($0.05 per unit), FFO would have been $82.6 million ($1.79 per unit) in the prior year period.

Adjusted Funds From Operations

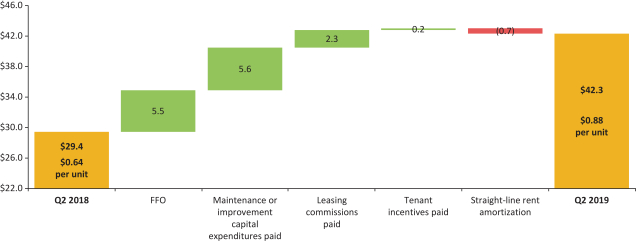

As previously detailed in the FFO and AFFO reconciliation table, AFFO for the three month period ended June 30, 2019 was $42.3 million ($0.88 per unit) compared to $29.4 million ($0.64 per unit) in the prior year period. The $12.9 million ($0.24 per unit) increase in AFFO is summarized below:

Q2 2019 vs Q2 2018 Change in AFFO |

Additional details pertaining to the components of the change in AFFO are as follows:

| • | the $5.5 million increase in FFO, as noted previously; |

| • | a $5.6 million decrease in capital expenditures paid largely due to higher payments made in the prior year period relating to improvement projects arising fromre-leasing activities at a property in Novi, Michigan and a property located in Olive Branch, Mississippi acquired in 2017; and |

| • | a $2.3 million decrease in leasing commissions paid due to payments made in the prior year period relating to there-leasing of the property located in Olive Branch, Mississippi, partially offset by; |

| • | a $0.7 million decrease in AFFO from straight-line rent amortization, primarily from rent-free periods associated with the building expansion completed in January 2019 at the West Jefferson, Ohio property and the recently acquired property in Mississauga, Ontario. |

Excluding the compensation costs of $2.1 million ($0.04 per unit) associated with the departure of the former CFO, which include the accelerated vesting of unit-based awards, AFFO would have been $44.4 million ($0.92 per unit) in the three month period ended June 30, 2019. In comparison, excluding the foreign exchange loss of $1.9 million ($0.04 per unit) realized during the second quarter of 2018 on US dollar cash proceeds from the sale of investment properties in January 2018 and the compensation costs associated with departed executives of $1.0 million ($0.02 per unit), AFFO would have been $32.3 million ($0.70 per unit) in the prior year period.

Granite REIT 2019 Second Quarter Report 23

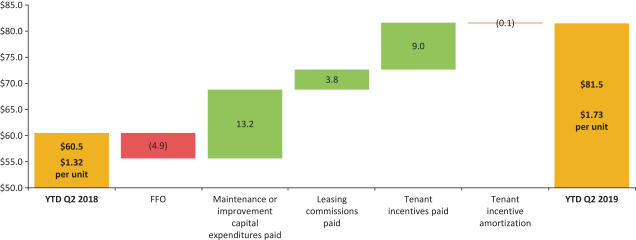

AFFO for the six months ended June 30, 2019 was $81.5 million ($1.73 per unit) compared to $60.5 million ($1.32 per unit) in the prior year period. The $21.0 million ($0.41 per unit) increase in AFFO is summarized below:

Q2 2019 YTD vs Q2 YTD 2018 Change in AFFO |

Additional details pertaining to the components of the change in AFFO are as follows:

| • | the $4.9 million decrease in FFO, as noted previously, partially offset by; |

| • | a $13.2 million decrease in capital expenditures paid largely due to higher payments made in the prior year period relating to improvement projects arising fromre-leasing activities at the properties in Novi, Michigan and Olive Branch, Mississippi as noted above; |

| • | a $3.8 million decrease in leasing commissions paid primarily due to payments made in the prior year period relating to there-leasing of the property located in Olive Branch, Mississippi, the developed property in Poland, the partiallyleased-up property in Novi, Michigan, as well as lease renewals and extensions for two properties in the United States and Germany; and |

| • | a $9.0 million decrease in tenant incentives paid largely due to a 2018 payment relating to a tenant allowance for a 2014 lease extension at the Eurostar facility in Graz, Austria. |

Excluding the compensation costs of $2.1 million ($0.04 per unit) associated with the departure of the former CFO, which include the accelerated vesting of unit-based awards, AFFO would have been $83.6 million ($1.77 per unit) for the six months ended June 30, 2019. In comparison, excluding the net foreign exchange gain of $8.5 million ($0.19 per unit) realized during the period on the remeasurement of US dollar cash proceeds from the sale of investment properties in January 2018, compensation costs associated with departed executives of $2.4 million ($0.05 per unit) and the payment of the tenant incentive allowance made in connection with a 2014 lease extension at the Eurostar facility in Graz, Austria of $9.1 million ($0.19 per unit), AFFO would have been $63.5 million ($1.37 per unit) in the six months ended June 30, 2018.

| INVESTMENT PROPERTIES |

Granite’s investment properties consist of income-producing properties, properties under development and land held for development. Substantially all of the income-producing properties are for industrial use and can be categorized as (i) modern logistics/distribution warehouse facilities (“modern warehouse facilities”), which were recently acquired or newly developed/redeveloped, (ii) multi-purpose facilities, which are tenantable by a wide variety of potential users or (iii) special purpose properties designed and built with specialized features and leased to Magna. The attributes of the income-producing properties are versatile and are based on the needs of the tenant such that an industrial property used by a certain tenant

24 Granite REIT 2019 Second Quarter Report

for light or heavy manufacturing can be used by another tenant for other industrial uses after some retrofitting if necessary. Accordingly, the investment property portfolio is substantially for industrial use and, as such, Granite determined that its asset class comprises industrial properties for purposes of financial reporting. The fair value of the industrial properties, as noted below, is based upon the current tenanting, existing use and attributes of such properties.

Properties under development comprise a site in Altbach, Germany where the demolition of the property is substantially complete and construction of a distribution/light industrial facility is subject to receipt of all required permits and state approval, and a parcel of development land in Plainfield, Indiana where construction of a class A distribution/warehouse commenced in the second quarter of 2019 and the total expected costs are approximately $32 million.

Land held for development comprise a16-acre parcel of land located in Wroclaw, Poland that could provide for approximately 0.3 million square feet of logistics-warehouse space as well as 12.9 acres of development land in Ohio, United States that was acquired in 2018.

Summary attributes of the investment properties as at June 30, 2019 and December 31, 2018 were as follows:

Investment Properties Summary(1) |

| As at June 30, 2019 and December 31, 2018 | 2019 | 2018 | ||||||

(in millions, except as noted) | ||||||||

Investment properties — fair value | $ | 3,799.1 | $ | 3,425.0 | ||||

Income-producing properties | 3,776.0 | 3,404.0 | ||||||

Properties under development | 18.4 | 17.0 | ||||||

Land held for development | 4.7 | 4.0 | ||||||

Overall capitalization rate(2) | 6.3% | 6.7% | ||||||

Number of investment properties | 83 | 84 | ||||||

Income-producing properties | 79 | 80 | ||||||

Properties under development | 2 | 2 | ||||||

Land held for development | 2 | 2 | ||||||

Property metrics | ||||||||

GLA, square feet | 34.5 | 32.2 | ||||||

Occupancy, by GLA | 98.9% | 99.1% | ||||||

Weighted average lease term in years, by square footage | 6.0 | 6.0 | ||||||

Total number of tenants | 51 | 48 | ||||||

Magna as a percentage of annualized revenue(3) | 48% | 54% | ||||||

Magna as a percentage of GLA | 41% | 47% | ||||||

Granite REIT 2019 Second Quarter Report 25

Assets Held for Sale(1) | ||||

| As at June 30, 2019 and December 31, 2018 | 2019 | 2018 | ||||||

(in millions, except as noted) | ||||||||

Assets held for sale | ||||||||

Fair value | $ | 50.5 | $ | 44.2 | ||||

Number of properties | 6 | 6 | ||||||

GLA, square feet | 0.8 | 0.7 | ||||||

Magna as a percentage of GLA | 90% | 94% | ||||||

Annualized revenue(3) | $ | 3.6 | $ | 2.2 | ||||

| (1) | Assets held for sale are excluded from investment properties and related property metrics. Accordingly, six such assets that were held for sale as at June 30, 2019 and six such assets that were held for sale as at December 31, 2018 were excluded from investment properties and related property metrics as at June 30, 2019 and December 31, 2018, respectively, throughout this MD&A. |

| (2) | Overall capitalization rate pertains only to income-producing properties. |

| (3) | Annualized revenue for each period presented is calculated as rental revenue excluding tenant recoveries, recognized in accordance with IFRS, in the reported month multiplied by 12 months. |

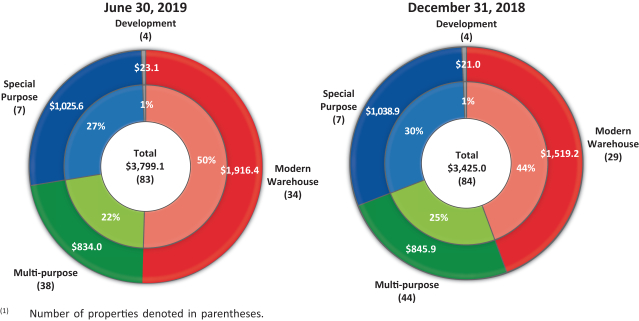

The fair value of the investment properties by asset category as at June 30, 2019 and December 31, 2018 was as follows:

Fair Value of Investment Properties by Asset Category(1) |

26 Granite REIT 2019 Second Quarter Report

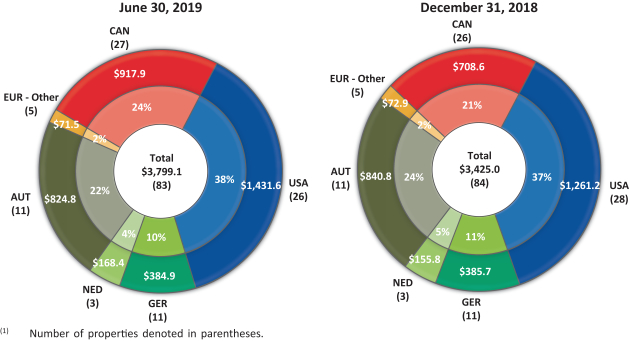

Granite has a specialized and high quality global portfolio of large scale properties strategically located in Canada, the United States and Europe. The fair value of the investment properties by country as at June 30, 2019 and December 31, 2018 was as follows:

Fair Value of Investment Properties by Geography(1) |

The change in the fair value of investment properties by asset category during the six months ended June 30, 2019 was as follows:

Change in Fair Value of Investment Properties by Asset Category |

| January 1, 2019 | June 30, 2019 | |||||||||||||||||||||||||||||||||||

| Investment properties | Ground leases | Fair value gains | Acquisitions | Capital expenditures | Foreign exchange losses | Other changes | Classified as assets held for sale | Investment properties | ||||||||||||||||||||||||||||

Modern | $ | 1,519.2 | 11.8 | 36.3 | 411.2 | 3.8 | (68.9 | ) | 3.0 | — | $ | 1,916.4 | ||||||||||||||||||||||||

Multi-purpose facilities | 845.9 | — | 55.9 | — | 0.7 | (17.4 | ) | 0.1 | (51.2 | ) | 834.0 | |||||||||||||||||||||||||

Special purpose properties | 1,038.9 | — | 26.3 | — | — | (37.3 | ) | (2.3 | ) | — | 1,025.6 | |||||||||||||||||||||||||

Income-Producing Properties | 3,404.0 | 11.8 | 118.5 | 411.2 | 4.5 | (123.6 | ) | 0.8 | (51.2 | ) | 3,776.0 | |||||||||||||||||||||||||

Properties Under Development | 17.0 | — | — | — | 2.2 | (0.8 | ) | — | — | 18.4 | ||||||||||||||||||||||||||

Land Held For Development | 4.0 | — | 0.9 | — | — | (0.2 | ) | — | — | 4.7 | ||||||||||||||||||||||||||

| $ | 3,425.0 | $ | 11.8 | $ | 119.4 | $ | 411.2 | $ | 6.7 | $ | (124.6 | ) | $ | 0.8 | $ | (51.2 | ) | $ | 3,799.1 | |||||||||||||||||

Granite REIT 2019 Second Quarter Report 27

During the six months ended June 30, 2019, the fair value of investment properties increased by $374.1 million, primarily due to:

| • | the recognition of ground leases effective January 1, 2019 under IFRS 16,Leases has increased the fair value of investment properties by $11.8 million, consisting of $9.1 million in Botlek, Netherlands and $2.7 million in Soest, Germany (see“NEW ACCOUNTING PRONOUNCEMENTS AND DEVELOPMENTS”). The obligations for these two land leases have been recorded on the combined balance sheet with theright-of-use assets recorded in investment properties; |

| • | net fair value gains of $119.4 million which were attributable to various factors including (i) the positive changes in leasing assumptions associated with lease renewals and fair market rent increases for certain properties located in Canada and the United States and (ii) a compression in discount and terminal capitalization rates for certain European properties resulting from the continued market demand for industrial real estate properties; |

| • | the acquisitions of three income-producing properties in the United States and the leasehold interest in two properties in Canada for $411.2 million consisting of two properties in Texas for $164.2 million, one property in Columbus, Ohio for $71.6 million, the leasehold interest in two properties in Mississauga, Ontario for $174.1 million and the associated transaction costs of $1.3 million (see “SIGNIFICANT MATTERS”); and |

| • | capital expenditures of $6.7 million, of which $3.4 million related to the construction of a 0.3 million square foot recently completed expansion at an acquired property near Columbus, Ohio and $2.2 million related to development capital expenditures for two properties under construction in Altbach, Germany and Indiana, United States. Capital expenditures can include expansion or development expenditures and maintenance or improvement expenditures. Expansion or development capital expenditures are discretionary in nature and are incurred to generate new revenue streams and/or increase the productivity of a property. Maintenance or improvement capital expenditures relate to sustaining the existing earnings capacity of a property. |

These increases are partially offset by:

| • | foreign exchange losses of $124.6 million, which primarily include foreign exchange losses of $57.5 million and $65.5 million resulting from the relative strengthening of the Canadian dollar against the US dollar and the Euro, respectively; and |

| • | the classification of six properties valued at $51.2 million as assets held for sale. These properties are classified as assets held for sale on the combined balance sheet and excluded from the investment properties categorization (see “SIGNIFICANT MATTERS”). |

Fair values were primarily determined by discounting the expected future cash flows, generally over a term of 10 years, plus a terminal value based on the application of a capitalization rate to estimated year 11 cash flows. Granite measures its investment properties using valuations prepared by management. Granite does not measure its investment properties based on valuations prepared by external appraisers but uses such external appraisals as data points, together with other external market information accumulated by management, in arriving at its own conclusions on values. Management uses valuation assumptions such as discount rates, terminal capitalization rates and market rental rates applied in external appraisals or sourced from valuation experts; however, the Trust also uses its historical renewal experience with tenants, its direct knowledge of the specialized nature of Granite’s portfolio and tenant profile and its knowledge of the actual condition of the properties in making business judgments about lease renewal probabilities, renewal rents and capital expenditures. There has been no change in the valuation methodology used during the six month period ended June 30, 2019. The key valuation metrics for Granite’s investment properties including the discount and terminal capitalization rates by jurisdiction are summarized in note 4 to the unaudited condensed combined financial statements for the three and six month periods ended

28 Granite REIT 2019 Second Quarter Report

June 30, 2019. In addition, valuation metrics for Granite’s income-producing properties (excluding assets held for sale) by asset category as at June 30, 2019 and December 31, 2018 were as follows:

Valuation Metrics by Income-Producing Property Asset Category |

As at June 30, 2019 and | Modern warehouse facilities | Multi-purpose facilities | Special purpose properties | Total | ||||||||||||||||||||||||||||||||||||||||

| 2019 | 2018 | 2019 | 2018 | 2019 | 2018 | 2019 | 2018 | |||||||||||||||||||||||||||||||||||||

Overall capitalization rate(1)(2) | 5.50% | 5.66% | 6.58% | 7.06% | 7.58% | 7.77% | 6.30% | 6.65% | ||||||||||||||||||||||||||||||||||||

Terminal capitalization rate(1) | 6.17% | 6.25% | 6.72% | 6.95% | 7.13% | 7.50% | 6.56% | 6.81% | ||||||||||||||||||||||||||||||||||||

Discount rate(1) | 6.24% | 6.34% | 6.79% | 7.02% | 7.48% | 7.63% | 6.70% | 6.90% | ||||||||||||||||||||||||||||||||||||

| (1) | Weighted based on income-producing property fair value. |

| (2) | Overall capitalization rate is calculated as stabilized net operating income (property revenue less property expenses) divided by the fair value of the property. |

A sensitivity analysis of the fair value of income-producing properties to changes in the overall capitalization rate, terminal capitalization rate and discount rate at June 30, 2019 is presented below:

Sensitivity Analysis of Fair Value of Income-Producing Properties |

| Rate sensitivity | Overall capitalization rate | Terminal capitalization rate | Discount rate | |||||||||

+50 bps | 3,485.7 | 3,627.2 | 3,637.2 | |||||||||

+25 bps | 3,624.7 | 3,698.7 | 3,705.7 | |||||||||

Base rate | $ | 3,776.0 | $ | 3,776.0 | $ | 3,776.0 | ||||||

-25 bps | 3,941.2 | 3,859.6 | 3,847.9 | |||||||||

-50 bps | 4,122.5 | 3,950.5 | 3,921.7 | |||||||||

Maintenance or Improvement Capital Expenditures and Leasing Costs

Maintenance or improvement capital expenditures relate to sustaining the existing earnings capacity of the property portfolio. Leasing costs include direct leasing costs and lease incentives. Direct leasing costs include broker commissions incurred in negotiating and arranging tenant leases. Lease incentives include the cost of leasehold improvements to tenant spaces and/or cash allowances provided to tenants for leasehold improvement costs.

Maintenance or Improvement Capital Expenditures and Leasing Costs Paid

The maintenance or improvement capital expenditures and leasing costs paid by quarter for the trailing eight quarters were as follows:

Maintenance or Improvement Capital Expenditures and Leasing Costs Paid |

| Q2’19 | Q1’19 | Q4’18 | Q3’18 | Q2’18 | Q1’18 | Q4’17 | Q3’17 | |||||||||||||||||||||||||||

Maintenance or improvement capital expenditures paid | $ | 0.6 | $ | 1.2 | $ | 1.2 | $ | 1.6 | $ | 6.2 | $ | 8.8 | $ | 9.3 | $ | 0.6 | ||||||||||||||||||

Leasing costs paid | — | 0.4 | 0.4 | 0.5 | 2.4 | 10.8 | 1.4 | 1.6 | ||||||||||||||||||||||||||

Total paid | [A] | $ | 0.6 | $ | 1.6 | $ | 1.6 | $ | 2.1 | $ | 8.6 | $ | 19.6 | $ | 10.7 | $ | 2.2 | |||||||||||||||||

GLA, square feet | [B] | 34.5 | 32.8 | 32.2 | 32.5 | 31.8 | 29.7 | 29.1 | 30.2 | |||||||||||||||||||||||||

$ paid per square feet | [A]/[B] | $ | 0.02 | $ | 0.05 | $ | 0.05 | $ | 0.06 | $ | 0.27 | $ | 0.66 | $ | 0.37 | $ | 0.07 | |||||||||||||||||

Granite REIT 2019 Second Quarter Report 29

In the first quarter of 2018, Granite paid $9.1 million related to a tenant incentive allowance for a 2014 lease extension at the 1.1 million square foot Eurostar facility in Graz, Austria.

Commencing with the third quarter of 2017, Granite undertook tore-develop its Novi, MI property, which was vacated by Magna in March 2017. Granite leased 71% of the space to Hanon Systems for a minimum lease term of 15 years commencing in January 2018. The 0.3 million square foot facility is one of the very few office properties in Granite’s portfolio.

Granite has invested a total of $23.6 million in capital commencing 2017 to reposition and lease the Novi, MI flex office property. The following is a summary of the capital expenditures and leasing costs paid by quarter in connection with the Novi, MI property:

Novi, MI Property: Maintenance or Improvement Capital Expenditures and Leasing Costs Paid |

| Q2’19 | Q1’19 | Q4’18 | Q3’18 | Q2’18 | Q1’18 | Q4’17 | Q3’17 | |||||||||||||||||||||||||

Maintenance or improvement capital expenditures paid | $ | 0.3 | $ | 0.6 | $ | 0.5 | $ | 0.1 | $ | 3.2 | $ | 8.4 | $ | 8.0 | $ | 0.1 | ||||||||||||||||

Leasing costs paid | — | — | — | — | — | 0.2 | 1.0 | 1.2 | ||||||||||||||||||||||||

Total paid | $ | 0.3 | $ | 0.6 | $ | 0.5 | $ | 0.1 | $ | 3.2 | $ | 8.6 | $ | 9.0 | $ | 1.3 | ||||||||||||||||

Granite is actively marketing the remaining 0.1 million square feet of available space and anticipates incurring additional cash outflows totaling approximately $5.6 million in capital expenditures and leasing costs over the next year to complete the Novi, MI facility andlease-up of the remaining available space.

Excluding thenon-recurring or unusual items noted above for the Graz, Austria and Novi, MI properties, the maintenance or improvement capital expenditures and leasing costs paid by quarter for the trailing eight quarters were as follows:

Maintenance or Improvement Capital Expenditures and Leasing Costs Paid — |

| Q2’19 | Q1’19 | Q4’18 | Q3’18 | Q2’18 | Q1’18 | Q4’17 | Q3’17 | |||||||||||||||||||||||||||

Maintenance or improvement capital expenditures paid | $ | 0.3 | $ | 0.6 | $ | 0.7 | $ | 1.5 | $ | 3.0 | $ | 0.4 | $ | 1.3 | $ | 0.5 | ||||||||||||||||||