UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-22784 |

| |

| Dreyfus Municipal Bond Infrastructure, Inc. | |

| (Exact name of Registrant as specified in charter) | |

| | |

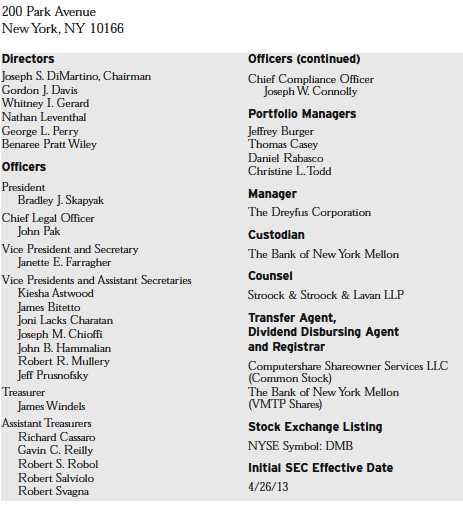

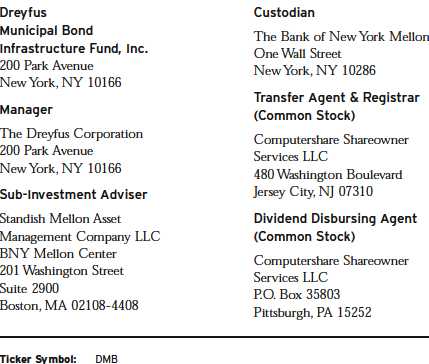

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| John Pak, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 2/28 | |

Date of reporting period: | 2/28/14 | |

| | | | | | | |

FORM N-CSR

Item 1. Reports to Stockholders.

|

| Dreyfus |

| Municipal Bond |

| Infrastructure Fund, Inc. |

ANNUAL REPORT February 28, 2014

Dreyfus Municipal Bond Infrastructure Fund, Inc.

Protecting Your Privacy

Our Pledge to You

THE FUND IS COMMITTED TO YOUR PRIVACY. On this page, you will find the Fund’s policies and practices for collecting, disclosing, and safeguarding “nonpublic personal information,” which may include financial or other customer information.These policies apply to individuals who purchase Fund shares for personal, family, or household purposes, or have done so in the past. This notification replaces all previous statements of the Fund’s consumer privacy policy, and may be amended at any time. We’ll keep you informed of changes as required by law.

YOUR ACCOUNT IS PROVIDED IN A SECURE ENVIRONMENT. The Fund maintains physical, electronic and procedural safeguards that comply with federal regulations to guard nonpublic personal information. The Fund’s agents and service providers have limited access to customer information based on their role in servicing your account.

THE FUND COLLECTS INFORMATION IN ORDER TO SERVICE AND ADMINISTER YOUR ACCOUNT.

The Fund collects a variety of nonpublic personal information, which may include:

Information we receive from you, such as your name, address, and social security number.

Information about your transactions with us, such as the purchase or sale of Fund shares.

Information we receive from agents and service providers, such as proxy voting information.

THE FUND DOES NOT SHARE NONPUBLIC

PERSONAL INFORMATION WITH ANYONE, EXCEPT

AS PERMITTED BY LAW.

Thank you for this opportunity to serve you.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily rep resent the views of Dreyfus or any other person in the Dreyfus organi zation. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

|

| Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

| | Contents |

| | THE FUND |

| 2 | A Letter from the President |

| 3 | Discussion of Fund Performance |

| 6 | Selected Information |

| 7 | Statement of Investments |

| 16 | Statement of Assets and Liabilities |

| 17 | Statement of Operations |

| 18 | Statement of Cash Flows |

| 19 | Statement of Changes in Net Assets |

| 20 | Financial Highlights |

| 21 | Notes to Financial Statements |

| 31 | Report of Independent Registered Public Accounting Firm |

| 32 | Additional Information |

| 36 | Important Tax Information |

| 37 | Board Members Information |

| 39 | Officers of the Fund |

| 45 | Officers and Directors |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus

Municipal Bond

Infrastructure Fund, Inc.

The Fund

A LETTER FROM THE PRESIDENT

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Municipal Bond Infrastructure Fund, Inc., covering the period from the fund’s inception on April 26, 2013, through February 28, 2014. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

The past year delivered mixed results for municipal bonds. Accelerating economic growth and anticipation of a more moderately accommodative monetary policy drove longer term interest rates higher and bond prices lower over the reporting period’s first half, and the negative effects of rising rates were exacerbated by selling pressure among investors seeking safer havens. Municipal bonds fared better over the second half as investors became acclimated to the Federal Reserve Board’s adjusted policy stance, investor demand rebounded, and most states and municipalities saw improved credit conditions in the recovering U.S. economy.

We remain cautiously optimistic regarding the municipal bond market’s prospects over the months ahead.We expect the domestic economy to continue to strengthen over the next year, which could support higher tax revenues for most states and municipalities.We also anticipate rising demand for a limited supply of securities as more income-oriented investors seek the tax advantages of municipal bonds. However, municipal bonds could remain sensitive to rising long-term interest rates as the economic recovery gains additional traction. As always, we encourage you to discuss our observations with your financial advisor to assess their potential impact on your investments.

Thank you for your continued confidence and support.

J. Charles Cardona

President

The Dreyfus Corporation

March 17, 2014

2

DISCUSSION OF FUND PERFORMANCE

For the period of April 26, 2013, through February 28, 2014, as provided by Daniel Rabasco and Jeffrey Burger, Primary Portfolio Managers

Fund and Market Performance Overview

From its inception on April 26, 2013, through the end of its annual reporting period on February 28, 2014, Dreyfus Municipal Bond Infrastructure Fund achieved a total return of –9.00% on a net-asset-value basis.1 Over the same period, the fund provided aggregate income dividends of $0.50 per share, which reflects a distribution rate of 5.23%.2

Selling pressure stemming from investors’ concerns about actual and anticipated interest rate changes sent municipal bond prices lower during much of 2013, and a mild rally over the first two months of 2014 only partly offset earlier weakness.

The Fund’s Investment Approach

The fund seeks to provide as high a level of current income exempt from regular federal income tax as is consistent with the preservation of capital.The fund’s portfolio is composed principally of investments that finance the development, support, or improvement of America’s infrastructure.

The fund pursues its investment objective normally by investing at least 80% of its Managed Assets 3 in municipal bonds issued to finance infrastructure projects in the United States.Also, under normal circumstances, the fund will invest at least 50% of its Managed Assets in investment grade municipal bonds, meaning that up to 50% of Managed Assets can be invested in below investment grade municipal bonds. Projects in which the fund may invest include (but are not limited to) those in the transportation, energy and utilities, social infrastructure, and water and environmental sectors.We focus on identifying undervalued sectors and securities and minimize the use of interest rate forecasting.We select municipal bonds using fundamental credit analysis to estimate the relative value and attractiveness of various sectors and securities and to exploit pricing inefficiencies.

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

The fund employs leverage by issuing preferred stock and participating in tender option bond programs. Leverage has the effect of “leveraging” the portfolio, which can magnify gain and loss potential depending on market conditions.

Selling Pressure Sparked Declines Among Municipal Bonds

Municipal bonds struggled in the weeks after the fund’s inception as rebounding labor and housing markets sent long-term interest rates higher. Market volatility spiked in late May when the Federal Reserve Board’s (the “Fed”) chairman indicated that the central bank would soon back away from quantitative easing.This development sent longer term interest rates sharply higher in June, and bond prices declined commensurately.

In July, a bankruptcy filing by the city of Detroit intensified selling pressure in the municipal bond market, and in September, municipal bonds issued by Puerto Rico lost value after media reports detailed the U.S. territory’s fiscal and economic problems. While municipal bonds generally rallied in September and October when the Fed delayed tapering its quantitative easing program, November and December saw renewed bouts of market weakness. Municipal bonds rebounded to a degree over the first two months of 2014 after the Fed resolved prevailing uncertainty by starting gradual reductions in its bond purchasing program, investor demand increased, and the supply of newly issued municipal bonds declined.

Despite the fiscal problems facing Detroit and Puerto Rico, the economic rebound resulted in better underlying credit conditions for most municipal issuers, as improving tax revenues and reduced spending enabled many state and local governments to balance their budgets and replenish reserves.

Puerto Rico Bonds Weighed on Total Return

The fund began operations just weeks before the Fed’s announcement roiled fixed-income markets, which exposed it to the full brunt of market volatility. While the fund experienced no credit defaults during the reporting period, Puerto Rico bonds weighed on its total return. Puerto Rico securities showed signs of recovery in early 2014, helping to offset some of their earlier weakness. Likewise, our leveraging strategy hurt results for the overall reporting period, but

4

it magnified gains over the first two months of 2014. Finally, the fund’s high-grade holdings generally lagged their lower rated counterparts.

The fund achieved better results from riskier parts of the municipal bond infrastructure market, including non-rated and high yield bonds, as investors resumed their reach for yield in a low interest rate environment.

Finding Income Opportunities in a Strengthening Market

We believe that recently improved market trends have been driven, in part, by investors returning their focus to market and issuer fundamentals now that the Fed has begun to taper its quantitative easing program. Over the longer term, improved credit conditions and restored demand from investors seeking relief from higher taxes may continue to benefit municipal bonds, in our view. In the meantime, we believe that relatively wide yield differences along the market’s maturity range portend well for the fund’s ability potentially to generate competitive levels of current income.We have established a relatively long average duration in an effort to take full advantage of these income opportunities.

March 17, 2014

Bond funds are subject generally to interest rate, credit, liquidity, and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

High yield bonds are subject to increased credit risk and are considered speculative in terms of the issuer’s perceived ability to continue making interest payments on a timely basis and to repay principal upon maturity.

The use of leverage may magnify the fund’s gains or losses. For derivatives with a leveraging component, adverse changes in the value or level of the underlying asset can result in a loss that is much greater than the original investment in the derivative.

| 1 | Total return includes reinvestment of dividends and any capital gains paid, based upon net asset value per share. Past performance is no guarantee of future results. Income may be subject to state and local taxes, and some income may be subject to the federal alternative minimum tax (AMT) for certain investors. Capital gains, if any, are fully taxable. |

| 2 | Annualized distribution rate per share is based upon dividends per share paid from net investment income during the period, annualized, divided by the market price per share at the end of the period, adjusted for any capital gain distributions. |

| 3 | “Managed Assets” of the fund means the fund’s total assets, including any assets attributable to effective leverage, minus certain defined accrued liabilities. |

The Fund 5

SELECTED INFORMATION

February 28, 2014 (Unaudited)

| | |

| Market Price per share February 28, 2014 | $ | 11.29 |

| Shares Outstanding February 28, 2014 | | 18,381,981 |

| New York Stock Exchange Ticker Symbol | | DMB |

| | | | | | | | |

| MARKET PRICE (NEW YORK STOCK EXCHANGE) | | |

| | | | | Fiscal Year Ended February 28, 2014 | | |

| | | Quarter | | Quarter | | Quarter | | Quarter |

| | | Ended | | Ended | | Ended | | Ended |

| | | May 31, 2013† | | August 31, 2013 | | November 30, 2013 | | February 28, 2014 |

| High | $ | 15.08 | $ | 15.00 | $ | 10.90 | $ | 11.29 |

| Low | | 15.00 | | 10.03 | | 10.01 | | 10.02 |

| Close | | 15.00 | | 10.15 | | 10.10 | | 11.29 |

| | | |

| PERCENTAGE GAIN (LOSS) based on change in Market Price†† | |

| April 26, 2013 (commencement of operations) | | | |

| through February 28, 2014 | | (21.13 | )% |

| June 1, 2013 through February 28, 2014 | | (21.13 | ) |

| September 1, 2013 through February 28, 2014 | | 15.20 | |

| December 1, 2013 through February 28, 2014 | | 13.72 | |

| |

| NET ASSET VALUE PER SHARE | | | |

| April 26, 2013 (commencement of operations) | | $14.295 | |

| May 31, 2013 | | 13.95 | |

| August 31, 2013 | | 11.02 | |

| November 30, 2013 | | 11.61 | |

| February 28, 2014 | | 12.42 | |

| | |

| PERCENTAGE GAIN (LOSS) based on change in Net Asset Value†† | |

| April 26, 2013 (commencement of operations) | | |

| through February 28, 2014 | (9.00 | )% |

| June 1, 2013 through February 28, 2014 | (6.76 | ) |

| September 1, 2013 through February 28, 2014 | 16.66 | |

| December 1, 2013 through February 28, 2014 | 8.77 | |

| |

| † | Since 4/26/2013 inception. |

| †† | With dividends reinvested. |

6

| | | | | |

| STATEMENT OF INVESTMENTS | | | | |

| February 28, 2014 | | | | | |

| |

| |

| |

| |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments—146.7% | Rate (%) | Date | Amount ($) | | Value ($) |

| Arizona—6.3% | | | | | |

| Pima County Industrial Development | | | | | |

| Authority, Education Revenue | | | | | |

| (American Charter Schools | | | | | |

| Foundation Project) | 5.63 | 7/1/38 | 5,585,000 | | 4,664,536 |

| Pima County Industrial Development | | | | | |

| Authority, Education Revenue | | | | | |

| (Arizona Charter Schools | | | | | |

| Refunding Project) | 5.38 | 7/1/31 | 4,465,000 | | 4,363,778 |

| Salt Verde Financial Corporation, | | | | | |

| Senior Gas Revenue | 5.00 | 12/1/37 | 5,000,000 | | 5,257,100 |

| California—11.2% | | | | | |

| California Statewide Communities | | | | | |

| Development Authority, Revenue | | | | | |

| (California Baptist University) | 6.38 | 11/1/43 | 2,035,000 | | 2,056,713 |

| Golden State Tobacco | | | | | |

| Securitization Corporation, | | | | | |

| Tobacco Settlement | | | | | |

| Asset-Backed Bonds | 5.75 | 6/1/47 | 8,000,000 | | 6,592,640 |

| Long Beach Bond Finance Authority, | | | | | |

| Natural Gas Purchase Revenue | 5.50 | 11/15/37 | 5,000,000 | | 5,514,600 |

| Riverside County Transportation | | | | | |

| Commission, Senior Lien | | | | | |

| Toll Revenue | 5.75 | 6/1/44 | 3,250,000 | a | 3,376,100 |

| San Buenaventura, | | | | | |

| Revenue (Community Memorial | | | | | |

| Health System) | 7.50 | 12/1/41 | 2,500,000 | | 2,822,975 |

| University of California Regents, | | | | | |

| Medical Center Pooled Revenue | 5.00 | 5/15/43 | 5,000,000 | | 5,253,900 |

| Colorado—4.3% | | | | | |

| City and County of Denver, | | | | | |

| Airport System | | | | | |

| Subordinate Revenue | 5.25 | 11/15/43 | 5,000,000 | a | 5,186,450 |

| Colorado Health Facilities | | | | | |

| Authority, Health Facilities | | | | | |

| Revenue (The Evangelical | | | | | |

| Lutheran Good Samaritan | | | | | |

| Society Project) | 5.63 | 6/1/43 | 2,000,000 | | 2,103,680 |

| Colorado Health Facilities | | | | | |

| Authority, Revenue | | | | | |

| (Sisters of Charity of | | | | | |

| Leavenworth Health System) | 5.00 | 1/1/44 | 2,500,000 | | 2,595,350 |

The Fund 7

STATEMENT OF INVESTMENTS (continued)

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| District of Columbia—.8% | | | | | |

| District of Columbia, | | | | | |

| Revenue (Knowledge is | | | | | |

| Power Program, | | | | | |

| District of Columbia Issue) | 6.00 | 7/1/43 | 1,700,000 | | 1,812,710 |

| Florida—3.9% | | | | | |

| Broward County, | | | | | |

| Airport System Revenue | 5.00 | 10/1/42 | 3,750,000 | a | 3,875,475 |

| Davie, | | | | | |

| Educational Facilities | | | | | |

| Revenue (Nova Southeastern | | | | | |

| University Project) | 5.63 | 4/1/43 | 4,805,000 | | 4,995,326 |

| Illinois—2.9% | | | | | |

| Chicago, | | | | | |

| Customer Facility Charge | | | | | |

| Senior Lien Revenue (Chicago | | | | | |

| O’Hare International Airport) | 5.75 | 1/1/43 | 3,750,000 | a | 3,895,763 |

| University of Illinois Board of | | | | | |

| Trustees, Auxiliary | | | | | |

| Facilities System Revenue | | | | | |

| (University of Illinois) | 5.00 | 4/1/44 | 2,500,000 | | 2,622,125 |

| Indiana—7.0% | | | | | |

| Indiana Finance Authority, | | | | | |

| HR (The King’s Daughters’ | | | | | |

| Hospital and Health Services) | 5.50 | 8/15/40 | 7,425,000 | | 7,458,338 |

| Indiana Finance Authority, | | | | | |

| Private Activity Bonds (Ohio | | | | | |

| River Bridges East End | | | | | |

| Crossing Project) | 5.00 | 7/1/40 | 5,000,000 | | 5,007,050 |

| Indiana Finance Authority, | | | | | |

| Revenue (Baptist Homes of | | | | | |

| Indiana Senior Living) | 6.00 | 11/15/41 | 3,500,000 | | 3,525,235 |

| Iowa—5.1% | | | | | |

| Iowa Finance Authority, | | | | | |

| Midwestern Disaster Area | | | | | |

| Revenue (Alcoa Inc. Project) | 4.75 | 8/1/42 | 5,495,000 | | 4,934,785 |

| Iowa Finance Authority, | | | | | |

| Midwestern Disaster Area | | | | | |

| Revenue (Iowa Fertilizer | | | | | |

| Company Project) | 5.25 | 12/1/25 | 7,000,000 | | 6,796,230 |

8

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | �� | Value ($) |

| Kentucky—1.1% | | | | | |

| Louisville/Jefferson County | | | | | |

| Metro Government, | | | | | |

| Health System Revenue | | | | | |

| (Norton Healthcare, Inc.) | 5.75 | 10/1/42 | 2,370,000 | | 2,522,581 |

| Louisiana—.9% | | | | | |

| Louisiana Public Facilities | | | | | |

| Authority, Dock and | | | | | |

| Wharf Revenue (Impala | | | | | |

| Warehousing LLC Project) | 6.50 | 7/1/36 | 2,000,000 | a,b | 1,987,420 |

| Massachusetts—4.3% | | | | | |

| Massachusetts Development Finance | | | | | |

| Agency, Revenue (North Hill | | | | | |

| Communities Issue) | 6.50 | 11/15/43 | 2,000,000 | | 1,971,280 |

| Massachusetts Port Authority, | | | | | |

| Special Facilities Revenue | | | | | |

| (Delta Air Lines, Inc. | | | | | |

| Project) (Insured; AMBAC) | 5.00 | 1/1/27 | 8,210,000 | | 7,842,192 |

| Michigan—8.9% | | | | | |

| Detroit, | | | | | |

| Water Supply System Senior | | | | | |

| Lien Revenue | 5.25 | 7/1/41 | 5,000,000 | | 4,854,850 |

| Kent Hospital Finance Authority, | | | | | |

| Revenue (Metropolitan | | | | | |

| Hospital Project) | 6.25 | 7/1/40 | 5,750,000 | | 6,008,405 |

| Michigan Finance Authority, | | | | | |

| HR (Trinity Health Credit Group) | 5.00 | 12/1/39 | 5,000,000 | | 5,143,700 |

| Michigan Tobacco Settlement | | | | | |

| Finance Authority, Tobacco | | | | | |

| Settlement Asset-Backed Bonds | 6.00 | 6/1/34 | 5,000,000 | | 4,270,450 |

| Missouri—2.4% | | | | | |

| Missouri Health and Educational | | | | | |

| Facilities Authority, Educational | | | | | |

| Facilities Revenue (Saint Louis | | | | | |

| College of Pharmacy) | 5.50 | 5/1/43 | 2,000,000 | | 2,085,420 |

| Saint Louis County Industrial | | | | | |

| Development Authority, Senior | | | | | |

| Living Facilities Revenue | | | | | |

| (Friendship Village Sunset Hills) | 5.00 | 9/1/42 | 3,500,000 | | 3,504,795 |

The Fund 9

STATEMENT OF INVESTMENTS (continued)

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| New Jersey—4.9% | | | | | |

| New Jersey Economic Development | | | | | |

| Authority, Private Activity | | | | | |

| Revenue (The Goethals Bridge | | | | | |

| Replacement Project) | 5.38 | 1/1/43 | 2,500,000 | | 2,561,650 |

| New Jersey Economic Development | | | | | |

| Authority, Special Facility | | | | | |

| Revenue (Continental | | | | | |

| Airlines, Inc. Project) | 5.13 | 9/15/23 | 2,500,000 | a | 2,467,475 |

| New Jersey Economic Development | | | | | |

| Authority, Special Facility | | | | | |

| Revenue (Continental | | | | | |

| Airlines, Inc. Project) | 5.25 | 9/15/29 | 4,500,000 | a | 4,409,550 |

| Tobacco Settlement Financing | | | | | |

| Corporation of New Jersey, | | | | | |

| Tobacco Settlement | | | | | |

| Asset-Backed Bonds | 5.00 | 6/1/41 | 2,330,000 | | 1,791,467 |

| New York—14.5% | | | | | |

| Deutsche Bank Spears/Lifers Trust | | | | | |

| (Series DBE-1177) Recourse | | | | | |

| (Metropolitan Transportation | | | | | |

| Authority, Transportation Revenue) | 5.00 | 11/15/38 | 15,000,000 | a,b,c | 15,890,400 |

| New York City Industrial | | | | | |

| Development Agency, | | | | | |

| PILOT Revenue (Queens | | | | | |

| Baseball Stadium Project) | | | | | |

| (Insured; AMBAC) | 5.00 | 1/1/36 | 8,000,000 | | 7,480,000 |

| New York State Dormitory | | | | | |

| Authority, Revenue (Saint | | | | | |

| John’s University) | 5.00 | 7/1/44 | 2,000,000 | | 2,082,440 |

| Niagara Area Development | | | | | |

| Corporation, Solid Waste | | | | | |

| Disposal Facility Revenue | | | | | |

| (Covanta Energy Project) | 5.25 | 11/1/42 | 7,870,000 | | 7,609,109 |

| Ohio—8.4% | | | | | |

| Buckeye Tobacco Settlement | | | | | |

| Financing Authority, Tobacco | | | | | |

| Settlement Asset-Backed Bonds | 6.25 | 6/1/37 | 7,000,000 | | 6,077,190 |

10

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Ohio (continued) | | | | | |

| Muskingum County, | | | | | |

| Hospital Facilities Revenue | | | | | |

| (Genesis HealthCare System | | | | | |

| Obligated Group Project) | 5.00 | 2/15/44 | 7,000,000 | | 5,692,540 |

| Rickenbacker Port Authority, | | | | | |

| Capital Funding Revenue (Ohio | | | | | |

| Association of School Business | | | | | |

| Officials Expanded Asset | | | | | |

| Pooled Financing Program) | 5.38 | 1/1/32 | 4,225,000 | | 4,446,136 |

| Southeastern Ohio Port Authority, | | | | | |

| Hospital Facilities Improvement | | | | | |

| Revenue (Memorial Health | | | | | |

| System Obligated Group Project) | 6.00 | 12/1/42 | 3,000,000 | | 2,865,480 |

| Pennsylvania—10.7% | | | | | |

| Clairton Municipal Authority, | | | | | |

| Sewer Revenue | 5.00 | 12/1/37 | 4,000,000 | | 4,009,560 |

| Clairton Municipal Authority, | | | | | |

| Sewer Revenue | 5.00 | 12/1/42 | 1,500,000 | | 1,494,405 |

| Deutsche Bank Spears/Lifers | | | | | |

| Trust (Series DBE-1179) Recourse | | | | | |

| (Pennsylvania Turnpike | | | | | |

| Commission, Motor License | | | | | |

| Fund-Enhanced Turnpike | | | | | |

| Subordinate Special Revenue) | 5.00 | 12/1/42 | 13,000,000 | a,b,c | 13,702,270 |

| Pennsylvania Turnpike Commission, | | | | | |

| Motor License Fund-Enhanced | | | | | |

| Turnpike Subordinate Special | | | | | |

| Revenue (Insured; Assured | | | | | |

| Guaranty Municipal Corp.) | 5.00 | 12/1/42 | 5,000,000 | a | 5,210,250 |

| South Carolina—3.0% | | | | | |

| South Carolina Jobs-Economic | | | | | |

| Development Authority, Health | | | | | |

| Facilities Revenue (The Lutheran | | | | | |

| Homes of South Carolina, Inc.) | 5.13 | 5/1/48 | 1,750,000 | | 1,493,223 |

| South Carolina Public Service | | | | | |

| Authority, Revenue Obligations | | | | | |

| (Santee Cooper) | 5.13 | 12/1/43 | 5,000,000 | | 5,247,700 |

The Fund 11

STATEMENT OF INVESTMENTS (continued)

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Texas—15.1% | | | | | |

| Austin Convention Enterprises, Inc., | | | | | |

| Convention Center Hotel First Tier | | | | | |

| Revenue (Insured; XLCA) | 5.00 | 1/1/34 | 5,000,000 | | 4,617,650 |

| Clifton Higher Education Finance | | | | | |

| Corporation, Education Revenue | | | | | |

| (IDEA Public Schools) | 6.00 | 8/15/43 | 1,500,000 | | 1,615,680 |

| Deutsche Bank Spears/Lifers Trust | | | | | |

| (Series DBE-1182) Recourse (Dallas | | | | | |

| and Fort Worth, Joint Improvement | | | | | |

| Revenue (Dallas/Fort Worth | | | | | |

| International Airport)) | 5.00 | 11/1/45 | 15,000,000 | a,b,c | 15,127,350 |

| JPMorgan Chase Putters/Drivers | | | | | |

| Trust (Series 4314) Non-recourse | | | | | |

| (Tarrant County Cultural Education | | | | | |

| Facilities Finance Corporation, | | | | | |

| HR (Baylor Health Care | | | | | |

| System Project)) | 5.00 | 11/15/20 | 7,410,000 | b,c | 7,763,378 |

| North Texas Education Finance | | | | | |

| Corporation, Education Revenue | | | | | |

| (Uplift Education) | 5.13 | 12/1/42 | 3,000,000 | | 2,993,040 |

| Texas Transportation Commission, | | | | | |

| Central Texas Turnpike System | | | | | |

| First Tier Revenue | 5.00 | 8/15/41 | 2,500,000 | a | 2,530,050 |

| Virginia—7.8% | | | | | |

| Lexington Industrial Development | | | | | |

| Authority, Residential Care | | | | | |

| Facilities Mortgage Revenue | | | | | |

| (Kendal at Lexington) | 5.50 | 1/1/37 | 5,400,000 | | 5,242,428 |

| Virginia Small Business Financing | | | | | |

| Authority, Senior Lien Revenue | | | | | |

| (95 Express Lanes LLC Project) | 5.00 | 1/1/40 | 7,640,000 | a | 7,460,766 |

| Virginia Small Business Financing | | | | | |

| Authority, Senior Lien Revenue | | | | | |

| (Elizabeth River Crossing | | | | | |

| Opco, LLC Project) | 5.50 | 1/1/42 | 5,000,000 | a | 5,147,850 |

| Washington—2.3% | | | | | |

| Washington Health Care Facilities | | | | | |

| Authority, Revenue (Providence | | | | | |

| Health and Services) | 5.00 | 10/1/42 | 5,000,000 | | 5,185,350 |

12

| | | | | |

| Long-Term Municipal | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Wisconsin—8.7% | | | | | |

| Public Finance Agency of | | | | | |

| Wisconsin, Senior Airport | | | | | |

| Facilities Revenue (Transportation | | | | | |

| Infrastructure Properties, LLC | | | | | |

| Obligated Group) | 5.00 | 7/1/42 | 5,000,000 | a | 4,459,100 |

| Wisconsin Health and Educational | | | | | |

| Facilities Authority, Revenue | | | | | |

| (Aurora Health Care, Inc.) | 5.25 | 4/15/35 | 5,000,000 | | 5,175,700 |

| Wisconsin Health and Educational | | | | | |

| Facilities Authority, Revenue | | | | | |

| (Beaver Dam Community | | | | | |

| Hospitals, Inc.) | 5.25 | 8/15/34 | 5,700,000 | | 5,759,166 |

| Wisconsin Health and Educational | | | | | |

| Facilities Authority, Revenue | | | | | |

| (Sauk-Prairie Memorial | | | | | |

| Hospital, Inc. Project) | 5.38 | 2/1/48 | 5,000,000 | | 4,559,050 |

| U.S. Related—12.2% | | | | | |

| Guam Waterworks Authority, | | | | | |

| Water and Wastewater | | | | | |

| System Revenue | 5.50 | 7/1/43 | 3,000,000 | | 3,079,110 |

| Puerto Rico Aqueduct and | | | | | |

| Sewer Authority, | | | | | |

| Senior Lien Revenue | 5.75 | 7/1/37 | 6,500,000 | | 4,892,550 |

| Puerto Rico Aqueduct and Sewer | | | | | |

| Authority, Senior Lien Revenue | 6.00 | 7/1/44 | 6,200,000 | | 4,719,564 |

| Puerto Rico Electric Power | | | | | |

| Authority, Power Revenue | 5.00 | 7/1/32 | 4,500,000 | | 3,055,365 |

| Puerto Rico Electric Power | | | | | |

| Authority, Power Revenue | 6.75 | 7/1/36 | 2,500,000 | | 1,834,425 |

| Puerto Rico Electric Power | | | | | |

| Authority, Power Revenue | 5.05 | 7/1/42 | 7,480,000 | | 4,825,348 |

| Puerto Rico Highways and | | | | | |

| Transportation Authority, | | | | | |

| Transportation Revenue | | | | | |

| (Insured; FGIC) | 5.25 | 7/1/39 | 9,120,000 | a | 5,467,531 |

| Total Long-Term | | | | | |

| Municipal Investments | | | | | |

| (cost $343,982,803) | | | | | 334,943,248 |

The Fund 13

STATEMENT OF INVESTMENTS (continued)

| | | | | | |

| Short-Term Municipal | Coupon | Maturity | Principal | | | |

| Investment—1.1% | Rate (%) | Date | Amount ($) | | Value ($) | |

| Pennsylvania; | | | | | | |

| Geisinger Authority, | | | | | | |

| Health System Revenue | | | | | | |

| (Geisinger Health System) | | | | | | |

| (Liquidity Facility; | | | | | | |

| JPMorgan Chase Bank) | | | | | | |

| (cost $2,500,000) | 0.03 | 3/3/14 | 2,500,000 | d | 2,500,000 | |

| |

| Total Investments (cost $346,482,803) | | | 147.8 | % | 337,443,248 | |

| Liabilities, Less Cash and Receivables | | | (15.0 | %) | (34,124,283 | ) |

| VMTPS, at liquidation value | | | (32.8 | %) | (75,000,000 | ) |

| Net Assets Applicable to Common Shareholders | | 100.0 | % | 228,318,965 | |

VMTPS—Variable Rate Municipal Term Preferred Shares

| a | At February 28, 2014, the fund had $100,193,800 or 43.9% of net assets applicable to Common Shareholders invested in securities whose payment of principal and interest is dependent upon revenues generated from transportation. |

| b | Securities exempt from registration pursuant to Rule 144A under the Securities Act of 1933.These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.At February 28, 2014, these securities were valued at $54,470,818 or 23.9% of net assets applicable to Common Shareholders. |

| c | Collateral for floating rate borrowings. |

| d | Variable rate demand note—rate shown is the interest rate in effect at February 28, 2014. Maturity date represents the next demand date, or the ultimate maturity date if earlier. |

| | | |

| Portfolio Summary (Unaudited)† | | |

| |

| | Value (%) | | Value (%) |

| Transportation Services | 43.9 | Tobacco | 7.4 |

| Health Care | 23.3 | Retirement | 5.3 |

| Education | 14.8 | Industrial Development | 3.3 |

| Industrial | 13.9 | Pollution Control | 3.3 |

| Hospital | 10.4 | Utility-Gas | 2.4 |

| Utility-Water and Sewer | 10.1 | Asset-Backed | .8 |

| Utility-Electric | 8.9 | | 147.8 |

| |

| † Based on net assets applicable to Common Shareholders. | | |

14

| | | |

| Summary of Abbreviations | | |

| |

| ABAG | Association of Bay Area | ACA | American Capital Access |

| | Governments | | |

| AGC | ACE Guaranty Corporation | AGIC | Asset Guaranty Insurance Company |

| AMBAC | American Municipal Bond | ARRN | Adjustable Rate |

| | Assurance Corporation | | Receipt Notes |

| BAN | Bond Anticipation Notes | BPA | Bond Purchase Agreement |

| CIFG | CDC Ixis Financial Guaranty | COP | Certificate of Participation |

| CP | Commercial Paper | DRIVERS | Derivative Inverse |

| | | | Tax-Exempt Receipts |

| EDR | Economic Development | EIR | Environmental Improvement |

| | Revenue | | Revenue |

| FGIC | Financial Guaranty | FHA | Federal Housing |

| | Insurance Company | | Administration |

| FHLB | Federal Home | FHLMC | Federal Home Loan Mortgage |

| | Loan Bank | | Corporation |

| FNMA | Federal National | GAN | Grant Anticipation Notes |

| | Mortgage Association | | |

| GIC | Guaranteed Investment | GNMA | Government National Mortgage |

| | Contract | | Association |

| GO | General Obligation | HR | Hospital Revenue |

| IDB | Industrial Development Board | IDC | Industrial Development Corporation |

| IDR | Industrial Development | LIFERS | Long Inverse Floating |

| | Revenue | | Exempt Receipts |

| LOC | Letter of Credit | LOR | Limited Obligation Revenue |

| LR | Lease Revenue | MERLOTS | Municipal Exempt Receipts |

| | | | Liquidity Option Tender |

| MFHR | Multi-Family Housing Revenue | MFMR | Multi-Family Mortgage Revenue |

| PCR | Pollution Control Revenue | PILOT | Payment in Lieu of Taxes |

| P-FLOATS | Puttable Floating Option | PUTTERS | Puttable Tax-Exempt Receipts |

| | Tax-Exempt Receipts | | |

| RAC | Revenue Anticipation Certificates | RAN | Revenue Anticipation Notes |

| RAW | Revenue Anticipation Warrants | RIB | Residual Interest Bonds |

| ROCS | Reset Options Certificates | RRR | Resources Recovery Revenue |

| SAAN | State Aid Anticipation Notes | SBPA | Standby Bond Purchase Agreement |

| SFHR | Single Family Housing Revenue | SFMR | Single Family Mortgage Revenue |

| SONYMA | State of New York | SPEARS | Short Puttable Exempt |

| | Mortgage Agency | | Adjustable Receipts |

| SWDR | Solid Waste Disposal Revenue | TAN | Tax Anticipation Notes |

| TAW | Tax Anticipation Warrants | TRAN | Tax and Revenue Anticipation Notes |

| XLCA | XL Capital Assurance | | |

| |

| See notes to financial statements. | | |

The Fund 15

|

| STATEMENT OF ASSETS AND LIABILITIES |

| February 28, 2014 |

| | | |

| | Cost | Value | |

| Assets ($): | | | |

| Investments in securities—See Statement of Investments | 346,482,803 | 337,443,248 | |

| Cash | | 725,445 | |

| Interest receivable | | 4,110,292 | |

| Receivable for investment securities sold | | 883,992 | |

| Deferred VMTPS offering costs—Note 1(f) | | 548,406 | |

| Prepaid expenses | | 55,885 | |

| | | 343,767,268 | |

| Liabilities ($): | | | |

| Due to The Dreyfus Corporation and affiliates—Note 2(b) | | 182,154 | |

| Payable for floating rate notes issued—Note 3 | | 36,805,000 | |

| Payable for investment securities purchased | | 2,035,000 | |

| Dividends payable to Common Shareholders | | 1,148,874 | |

| Interest and expense payble related to | | | |

| floating rate notes issued—Note 3 | | 94,051 | |

| Interest expense payable on VMTPS—Note 1(f) | | 73,891 | |

| Accrued expenses | | 109,333 | |

| | | 40,448,303 | |

| VMTPS, $.001 par value per share (750 shares issued | | | |

| and outstanding at $100,000 per share liquidation value )—Note 1 | 75,000,000 | |

| Net Assets Applicable to Common Shareholders ($) | | 228,318,965 | |

| Composition of Net Assets ($): | | | |

| Common Stock, par value, $.001 per share | | | |

| (18,381,981 shares issued and outstanding) | | 18,382 | |

| Paid-in capital | | 262,715,065 | |

| Accumulated undistributed investment income—net | | 1,655,413 | |

| Accumulated net realized gain (loss) on investments | | (27,030,340 | ) |

| Accumulated net unrealized appreciation | | | |

| (depreciation) on investments | | (9,039,555 | ) |

| Net Assets Applicable to Common Shareholders ($) | | 228,318,965 | |

| Shares Outstanding (250 million shares authorized) | | 18,381,981 | |

| Net Asset Value, per share of Common Stock ($) | | 12.42 | |

| |

| See notes to financial statements. | | | |

16

|

| STATEMENT OF OPERATIONS |

| From April 26, 2013 (commencement of operations) to February 28, 2014 |

| | |

| Investment Income ($): | | |

| Interest Income | 13,934,416 | |

| Expenses: | | |

| Management fee—Note 2(a) | 1,826,123 | |

| VMTPS interest expense and fees—Note 1(f) | 491,295 | |

| Interest and expense related to floating rate notes issued—Note 3 | 468,678 | |

| Professional fees | 74,055 | |

| Shareholders’ reports | 48,081 | |

| Custodian fees—Note 2(b) | 19,097 | |

| Directors’ fees and expenses—Note 2(c) | 17,727 | |

| Shareholder servicing costs | 13,146 | |

| Redemption and paying agent fees—Note 2(b) | 8,600 | |

| Registration fees | 7,365 | |

| Amortization of VMTPS offering costs—Note 1(f), 2(b) | 37,178 | |

| Miscellaneous | 61,282 | |

| Total Expenses | 3,072,627 | |

| Investment Income—Net | 10,861,789 | |

| Realized and Unrealized Gain (Loss) on Investments—Note 3 ($): | | |

| Net realized gain (loss) on investments | (27,082,904 | ) |

| Net unrealized appreciation (depreciation) on investments | (9,039,555 | ) |

| Net Realized and Unrealized Gain (Loss) on Investments | (36,122,459 | ) |

| Net (Decrease) in Net Assets Applicable to | | |

| Common Shareholders Resulting from Operations | (25,260,670 | ) |

| |

| See notes to financial statements. | | |

The Fund 17

|

| STATEMENT OF CASH FLOWS |

| From April 26, 2013 (commencement of operations) to February 28, 2014 |

| | | | |

| Cash Flows from Operating Activities ($): | | | | |

| Interest received | 10,367,129 | | | |

| Operating expenses paid | (1,839,874 | ) | | |

| Purchases of long-term portfolio securities | (504,112,855 | ) | | |

| Net purchases of short-term portfolio securities | (2,500,000 | ) | | |

| Proceeds from sales of long-term portfolio securities | 170,460,151 | | | |

| | | | (327,625,449 | ) |

| Cash Flows from Financing Activities ($): | | | | |

| Dividends paid to Common Shareholders | (8,042,116 | ) | | |

| Proceeds from issuance of Common Stock | 262,670,625 | | | |

| Offering costs paid on VMTPS | (585,584 | ) | | |

| Proceeds from issuance of VMTPS | 75,000,000 | | | |

| VMTPS interest expense paid | (417,404 | ) | | |

| Interest and expense related to floating rate notes issued paid | (374,627 | ) | 328,250,894 | |

| Increase in cash | | | 625,445 | |

| Cash at beginning of period | | | 100,000 | |

| Cash at end of period | | | 725,445 | |

| Reconciliation of Net Decrease in Net Assets Applicable to | | | | |

| Common Shareholders Resulting from Operations to | | | | |

| Net Cash Used in Operating Activities ($): | | | | |

| Net Decrease in Net Assets Applicable to Common | | | | |

| Shareholders Resulting From Operations | | | (25,260,670 | ) |

| Adjustments to reconcile net decrease in net assets applicable | | | |

| to common shareholders resulting from operations | | | | |

| to net cash used in operating activities ($): | | | | |

| Increase in investments in securities, at cost | | | (347,025,808 | ) |

| Increase in receivable for investment securites sold | | | (883,992 | ) |

| Increase in payable for investment securities purchased | | | 2,035,000 | |

| Increase in interest receivable | | | (4,110,292 | ) |

| Increase in accrued expenses | | | 109,333 | |

| Increase in prepaid expenses | | | (55,885 | ) |

| Increase in Due to The Dreyfus Corporation and affiliates | | | 182,154 | |

| Interest and expense related to floating rate notes issued | | | 468,678 | |

| VMTPS interest expense and fees | | | 491,295 | |

| Amortization of VMTPS offering costs | | | 37,178 | |

| Increase in payable for floating rate notes issued | | | 36,805,000 | |

| Net unrealized depreciation on investments | | | 9,039,555 | |

| Net amortization of premiums on investments | | | 543,005 | |

| Net Cash Used In Operating Activities | | | (327,625,449 | ) |

| |

| See notes to financial statements. | | | | |

18

|

| STATEMENT OF CHANGES IN NET ASSETS |

| From April 26, 2013 (commencement of operations) to February 28, 2014 |

| | |

| Operations ($): | | |

| Investment income—net | 10,861,789 | |

| Net realized gain (loss) on investments | (27,082,904 | ) |

| Net unrealized appreciation (depreciation) on investments | (9,039,555 | ) |

| Net Increase (Decrease) in Net Assets Applicable | | |

| to Common Shareholders Resulting from Operations | (25,260,670 | ) |

| Dividends to Common Shareholders from ($) | | |

| Investment income—net | (9,190,990 | ) |

| Capital Stock Transactions ($): | | |

| Net proceeds from shares of Common Stock sold | 263,221,875 | |

| Offering costs charged to paid-in capital—Note 1 | (551,250 | ) |

| Increase (Decrease) in Net Assets | | |

| from Capital Stock Transactions | 262,670,625 | |

| Total Increase (Decrease) in Net Assets | | |

| Applicable to Common Shareholders | 228,218,965 | |

| Net Assets ($): | | |

| Beginning of Period | 100,000 | |

| End of Period | 228,318,965 | |

| Undistributed investment income—net | 1,655,413 | |

| Capital Share Transactions (Common Shares): | | |

| Increase in Common Shares Outstanding | | |

| as a result of Shares sold | 18,381,981 | |

| |

| See notes to financial statements. | | |

The Fund 19

FINANCIAL HIGHLIGHTS

The following table describes the performance for the fiscal period from April 26, 2013 (commencement of operations) to February 28, 2014.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions. These figures have been derived from the fund’s financial statements, and with respect to common stock, market price data for the fund’s common shares.

| | |

| Per Share Data ($): | | |

| Net asset value, beginning of period | 14.33 | a |

| Investment Operations: | | |

| Investment income—netb | .60 | |

| Net realized and unrealized gain (loss) on investments | (1.98 | ) |

| Total from Investment Operations | (1.38 | ) |

| Distributions to Common Shareholders: | | |

| Dividends from investment income—net | (.50 | ) |

| Offering costs charged to paid-in capital | (.03 | ) |

| Net asset value, end of period | 12.42 | |

| Market value, end of period | 11.29 | |

| Total Return (%)c | (21.13 | )d |

| Ratios/Supplemental Data (%): | | |

| Ratio of total expenses to average net assets | 1.65 | e |

| Ratio of net expenses to average net assets | 1.65 | e |

| Ratio of interest and expense related to | | |

| floating rate notes issued and VMTPS | | |

| interest expense and fees to average net assets | .52 | e |

| Ratio of net investment income | | |

| to average net assets | 5.83 | e |

| Portfolio Turnover Rate | 70.72 | d |

| Asset coverage of VMTPS, end of period | 404 | |

| Net Assets, Applicable to Common Shareholders, | | |

| end of period ($ x 1,000) | 228,319 | |

| VMTPS outstanding, end of period ($ x 1,000) | 75,000 | |

| Floating Rate Notes outstanding ($ x 1000) | 36,805 | |

| a | Reflects a deduction of $.675 per share sales load from the initial offering price of $15.00 per share. |

| b | Based on average common shares outstanding at each month end. |

| c | Calculated based on market value. |

| d | Not annualized. |

| e | Annualized. |

See notes to financial statements.

20

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Municipal Bond Infrastructure Fund, Inc. (the “fund”) had no operations until April 26, 2013 (commencement of operations) other than matters relating to its organization and registration as a non-diversified closed-end management investment company under the Investment Company Act of 1940, as amended (the “Act”) and the issuance of 6,981 shares of Common Stock to MBC Investments, an affiliate of Dreyfus.The fund’s investment objective is to seek to provide as high a level of current income exempt from regular federal income tax as is consistent with the preservation of capital. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary ofThe Bank of NewYork Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. Standish Mellon Asset Management Company LLC (“Standish”), a subsidiary of BNY Mellon and an affiliate of Dreyfus, serves as the fund’s sub-investment adviser. The fund’s Common Stock trades on the NewYork Stock Exchange (the “NYSE”) under the ticker symbol DMB.

The fund sold 16,950,000 shares of Common Stock at $15.00 per share through an initial offering which settled on April 26, 2013. Subsequently, an additional 1,425,000 shares of Common Stock at $15.00 per share were also issued to cover over-allotments to the underwriters on June 10, 2013. Net proceeds amounted to $263,221,875 after deducting sales load of $12,403,125. Costs associated with the initial underwriting of $551,250 were charged to paid-in capital at the time of issuance.

The fund has outstanding 750 VMTPS, with a liquidation preference of $100,000 per share (plus an amount equal to accumulated but unpaid dividends upon liquidation) and a stated mandatory redemption date of July 29, 2018. The fund issued the VMTPS on July 29, 2013 and, subsequently, on November 1, 2013 in private placements and, accordingly, the VMTPS are not registered under the Act. The fund entered into a Redemption and Paying Agent Agreement with The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of the Manager, with respect to the VMTPS.

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

The fund is subject to certain restrictions relating to the VMTPS. Failure to comply with these restrictions could preclude the fund from declaring any distributions to Common Shareholders or repurchasing common shares and/or could trigger the mandatory redemption of VMTPS at liquidation value. Thus, redemptions of VMTPS may be deemed to be outside of the control of the fund. In addition, the VMTPS have a mandatory redemption date of July 29,2018.The fund will have the right to request that the Total Holders, in their sole and absolute discretion, extend the term of the Term Redemption Date for an additional 364 day period.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

22

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

Investments in securities are valued each business day by an independent pricing service (the “Service”) approved by the fund’s Board of Directors (the “Board”). Investments for which quoted bid prices are readily available and are representative of the bid side of the market in the judgment of the Service are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such securities) and asked prices (as calculated by the Service based upon its evaluation of the market for such securities). Other investments (which constitute a majority of the portfolio securities) are carried at fair value as determined by the Service, based on methods which include consideration of the following: yields or prices of municipal securities of comparable

The Fund 23

NOTES TO FINANCIAL STATEMENTS (continued)

quality, coupon, maturity and type; indications as to values from dealers; and general market conditions. All of the preceding securities are categorized within Level 2 of the fair value hierarchy.

The Service’s procedures are reviewed by Dreyfus under the general supervision of the Board.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Board. Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers.These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are categorized within Level 3 of the fair value hierarchy.

The following is a summary of the inputs used as of February 28, 2014 in valuing the fund’s investments:

| | | | | | |

| | | Level 2—Other | | Level 3— | | |

| | Level 1— | Significant | | Significant | | |

| | Unadjusted | Observable | | Unobservable | | |

| | Quoted Prices | Inputs | | Inputs | Total | |

| Assets ($) | | | | | | |

| Investments in Securities: | | | | | |

| Municipal Bonds | — | 337,443,248 | | — | 337,443,248 | |

| Liabilities ($) | | | | | | |

| Floating Rate Notes† | — | (36,805,000 | ) | — | (36,805,000 | ) |

| VMTPS† | — | (75,000,000 | ) | — | (75,000,000 | ) |

| |

| † | Certain of the fund’s liabilities are held at carrying amount, which approximates fair value for |

| | financial reporting purposes. |

24

At February 28, 2014, there were no transfers between Level 1 and Level 2 of the fair value hierarchy.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Interest income, adjusted for accretion of discount and amortization of premium on investments, is earned from settlement date and recognized on the accrual basis. Securities purchased or sold on a when issued or delayed delivery basis may be settled a month or more after the trade date.

(c) Dividends to shareholders of Common Stock (“Common Shareholders(s)”): Dividends are recorded on the ex-dividend date. Dividends from investment income-net are normally declared and paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

For Common Shareholders who elect to receive their distributions in additional shares of the fund, in lieu of cash, such distributions will be reinvested at the lower of the market price or net asset value per share (but not less than 95% of the market price) in additional shares of the fund unless they opt-out of the dividend reinvestment plan, in which case they will receive all distributions in cash. If market price is equal to or exceeds net asset value, shares will be issued at a per share rate equal to the greater of (i) the net asset value or (ii) 95% of the closing market price per share of Common Stock on the payment date. If net asset value exceeds market price or if a cash dividend only is declared, Computershare Shareowner Services LLC (“Computershare”), the fund’s transfer agent, will buy fund shares in the open market.

The Fund 25

NOTES TO FINANCIAL STATEMENTS (continued)

On February 4, 2014, the Board declared a cash dividend of $.0625 per share from investment income-net, payable on March 3, 2014 to Common Shareholders of record as of the close of business on February 20, 2014.

(d) Dividends to shareholders of VMTPS: Dividends onVMTPS are declared daily and paid monthly.The Applicable Rate is equal to the rate per annum that results from the sum of the (a) Applicable Base Rate and (b) Ratings Spread as determined pursuant to the Applicable Rate Determination for theVMTPS on the Rate Determination Date immediately preceding such Subsequent Rate Period.The Applicable Rate for the initial rate period of theVMTPS was equal to the sum of 1.25% per annum plus the Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index rate of .03% on February 27, 2014.The dividend rate as of February 28, 2014 for theVMTPS was 1.28%.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, which can distribute tax-exempt dividends, by complying with the applicable provisions of the Code, and to make distributions of income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended February 28, 2014, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended February 28, 2014, the fund did not incur any interest or penalties.

The tax year for the period ended February 28, 2014 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At February 28, 2014, the components of accumulated earnings on a tax basis were as follows: undistributed tax-exempt income $2,804,287, accumulated capital losses $27,080,552 and unrealized depreciation $8,989,343.

26

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net realized capital gains, if any, realized subsequent to February 28, 2014. The fund has $27,080,552 of short-term capital losses which can be carried forward for an unlimited period.

The tax character of distributions paid to shareholders during the fiscal period ended February 28, 2014 was as follows: tax-exempt income $9,190,990.

During the period ended February 28, 2014, as a result of permanent book to tax differences, primarily due to the tax treatment for amortization adjustments and nondeductible VMTPS offering costs, the fund decreased accumulated undistributed investment income-net by $15,386, increased accumulated net realized gain (loss) on investments by $52,564 and decreased paid-in capital by $37,178. Net assets and net asset value per share were not affected by this reclassification.

(f) VMTPS: In the fund’s Statement of Assets and Liabilities,VMTPS aggregate liquidation preference is shown as a liability since they have a stated mandatory redemption date of July 29, 2018. Dividends paid to VMTPS are treated as interest expense and recorded as incurred. For the period ended February 28, 2014, interest expense related to VMTPS amounted to $491,295 and is included in “VMTPS interest expense and fees” in the Statement of Operations. Costs directly related to the issuance of theVMTPS of $585,584 are considered debt issuance costs which have been deferred and are being amortized into expense over the life of the VMTPS.

NOTE 2—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement (the “Agreement”) with the Manager, the management fee is computed at the annual rate of .65% of the value of the fund’s daily total assets minus the sum of accrued

The Fund 27

NOTES TO FINANCIAL STATEMENTS (continued)

liabilities (other than the aggregate indebtedness constituting financial leverage) (the “Managed Assets”) and is payable monthly.

Pursuant to a sub-investment advisory agreement between Dreyfus and Standish, Dreyfus pays Standish a monthly fee at the annual rate of .27% of the value of the fund’s average daily Managed Assets.

(b) The fund compensates The Bank of New York Mellon, a wholly-owned subsidiary of the Manager, under a custody agreement for providing custodial services for the fund.These fees are determined based on net assets and transaction activity. During the period ended February 28, 2014, the fund was charged $19,097 pursuant to the custody agreement.

The fund has an arrangement with the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates The Bank of New York Mellon under a Redemption and Paying Agent Agreement for providing certain transfer agency and payment services with respect to the VMTPS for the fund. During the period ended February 28, 2014, the fund was charged $8,600 for the services provided by the Redemption and Paying Agent. These fees are included in Redemption and paying agent fees in the Statement of Operations.

During the period ended February 28, 2014, the fund was charged $9,134 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $166,591, custodian fees $9,665, Redemption and Paying Agent fees $4,375 and Chief Compliance Officer fees $1,523.

(c) Each Board member also serves as a board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

28

NOTE 3—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended February 28, 2014, amounted to $506,147,855 and $171,344,143, respectively.

Inverse Floater Securities: The fund participates in secondary inverse floater structures in which fixed-rate, tax-exempt municipal bonds are transferred to a trust (“Trust”). The Trust typically issues two variable rate securities that are collateralized by the cash flows of the fixed-rate, tax-exempt municipal bonds.These variable rate securities pay interest based on a short-term floating rate set by a remarketing agent at predetermined intervals (“Trust Certificates”).A residual interest tax-exempt security is also created by theTrust, which is transferred to the fund, and is paid interest based on the remaining cash flow of the Trust, after payment of interest on the other securities and various expenses of the Trust. An inverse floater security may also be collapsed without the consent of the fund due to certain termination events such as bankruptcy, default or other credit event.

The fund accounts for the transfer of bonds to the Trust as secured borrowings, with the securities transferred remaining in the fund’s investments, and the related floating rate certificate securities reflected as fund liabilities in the Statement of Assets and Liabilities.

The fund may invest in inverse floater securities on either a non-recourse or recourse basis.These securities are typically supported by a liquidity facility provided by a bank or other financial institution (the “Liquidity Provider”) that allows the holders of the Trust Certificates to tender their certificates in exchange for payment from the Liquidity Provider of par plus accrued interest on any business day prior to a termination event.When the fund invests in inverse floater securities on a non-recourse basis, the Liquidity Provider is required to make a payment under the liquidity facility due to a termination event.When this occurs, the Liquidity Provider typically liquidates all or a portion of the municipal securities held in the Trust and then in

The Fund 29

NOTES TO FINANCIAL STATEMENTS (continued)

the fund, on a net basis.The balance, if any, is the amount owed under the liquidity facility over the liquidation proceeds (the “Liquidation Shortfall”). When a fund invests in inverse floater securities on a recourse basis, the fund typically enters into a reimbursement agreement with the Liquidity Provider where the fund is required to repay the Liquidity Provider the amount of any Liquidation Shortfall. As a result, the fund investing in a recourse inverse floater security bears the risk of loss with respect to any Liquidation Shortfall.

The average amount of borrowings outstanding under the inverse floater structure during the period ended February 28, 2014, was $66,308,500, with a related weighted average annualized interest rate of .71%.

VMTPS: The average amount of borrowings outstanding for the VMTPS during the period ended February 28, 2014, was approximately $63,815,800, with a related weighted average annualized interest rate of 1.31%.

At February 28, 2014, the cost of investments for federal income tax purposes was $309,627,591; accordingly, accumulated net unrealized depreciation on investments was $8,989,343, consisting of $8,776,541 gross unrealized appreciation and $17,765,884 gross unrealized depreciation.

30

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Dreyfus Municipal Bond Infrastructure Fund, Inc.

We have audited the accompanying statement of assets and liabilities of Dreyfus Municipal Bond Infrastructure Fund, Inc., including the statement of investments, as of February 28, 2014, and the related statements of operations, cash flows and changes in net assets and the financial highlights for the period from April 26, 2013 (commencement of operations) to February 28, 2014.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of February 28, 2014 by correspondence with the custodian and others.We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Municipal Bond Infrastructure Fund, Inc. at February 28, 2014 and the results of its operations, its cash flows, the changes in its net assets and the financial highlights for the period from April 26, 2013 to February 28, 2014, in conformity with U.S. generally accepted accounting principles.

New York, New York

April 25, 2014

The Fund 31

ADDITIONAL INFORMATION (Unaudited)

Dividend Reinvestment Plan

The fund’s Dividend Reinvestment Plan (the “Plan”) is commonly referred to as an “opt-out” plan. Each Common Shareholder who participates in the Plan will have all distributions of dividends and capital gains automatically reinvested in additional Common Shares by Computershare Trust Company, N.A. as agent (the “Plan Agent”). Common Shareholders who elect not to participate in the Plan will receive all distributions in cash, which will be paid by check and mailed directly to the shareholder of record (or if the shares are held in street or other nominee name, then to the nominee) by the Plan Agent, as dividend disbursing agent. Common Shareholders whose shares are held in the name of a broker or nominee should contact the broker or nominee to determine whether and how they may participate in the Plan. The Plan Agent serves as agent for the Common Shareholders in administering the Plan.After the Fund declares a dividend or makes a capital gain distribution, the Plan Agent will, as agent for the shareholders, either (i) receive the cash payment and use it to buy Common Shares in the open market, on the NYSE or elsewhere, for the participants’ accounts or (ii) distribute newly issued Common Shares of the Fund on behalf of the participants.The Plan Agent will receive cash from the Fund with which to buy Common Shares in the open market if, on the distribution payment date, the net asset value per share exceeds the market price per Common Share plus estimated brokerage commissions on that date.The Plan Agent will receive the dividend or distribution in newly issued Common Shares of the Fund if, on the payment date, the market price per share plus estimated brokerage commissions equals or exceeds the net asset value per share of the Fund on that date.The number of shares to be issued will be computed at a per share rate equal to the greater of (i) the net asset value or (ii) 95% of the closing market price per Common Share on the payment date.

32

Participants in the Plan may withdraw from the Plan at any time upon written notice to the Plan Agent. Such withdrawal will be effective immediately if received not less than ten days prior to a distribution record date; otherwise, it will be effective for all subsequent distributions. When a participant withdraws from the Plan or the Plan is terminated, such participant will receive whole Common Shares in his or her account under the Plan and will receive a cash payment for any fraction of a Common Share credited to such account. If any participant elects to have the Plan Agent sell all or part of his or her Common Shares and remit the proceeds, the Plan Agent is authorized to deduct a $15.00 fee plus $0.10 per share in brokerage commissions.

In the case of shareholders, such as banks, brokers or nominees, which hold Common Shares for others who are the beneficial owners, the Plan Agent will administer the Plan on the basis of the number of Common Shares certified from time to time by the record shareholders as representing the total amount registered in the record shareholder’s name and held for the account of beneficial owners who are participants in the Plan.

The Plan Agent’s fees for the handling of reinvestment of dividends and other distributions will be paid by the Fund. Each participant will pay a pro rata share of brokerage commissions incurred with respect to the Plan Agent’s open market purchases in connection with the reinvestment of distributions.There are no other charges to participants for reinvesting dividends or capital gain distributions. Purchases and/or sales are usually made through a broker affiliated with the Plan Agent.

Experience under the Plan may indicate that changes are desirable. Accordingly, the Fund reserves the right to amend or terminate the Plan as applied to any distribution paid subsequent to written notice of the

The Fund 33

ADDITIONAL INFORMATION (Unaudited) (continued)

change sent to all shareholders of the Fund at least 90 days before the record date for the dividend or distribution. The Plan also may be amended or terminated by the Plan Agent by at least 90 days’ written notice to all shareholders of the Fund.All correspondence concerning the Plan should be directed to the Plan Agent by calling 1-855-866-0953, or writing P.O. Box 43006, Providence, RI 02940-3006.

The automatic reinvestment of dividends and other distributions will not relieve participants of any income tax that may be payable or required to be withheld on such dividends or distributions. See “Tax Matters.”

Level Distribution Policy

The fund’s dividend policy is to distribute substantially all of its net investment income to its shareholders on a monthly basis. In order to provide shareholders with a more consistent yield to the current trading price of shares of Common Stock of the fund, the fund may at times pay out more or less than the entire amount of net investment income earned in any particular month and may at times in any month pay out any accumulated but undistributed income in addition to net investment income earned in that month. As a result, the dividends paid by the fund for any particular month may be more or less than the amount of net investment income earned by the fund during such month.The fund’s current accumulated but undistributed net investment income, if any, is disclosed in the Statement of Assets and Liabilities, which comprises part of the Financial Information included in this report.

Benefits and Risks of Leveraging

The fund utilizes leverage to seek to enhance the yield and net asset value of its Common Stock.These objectives cannot be achieved in all interest rate environments. To leverage, the fund has issued VMTPS, which pays dividends at prevailing short-term interest rates, and invests

34

the proceeds in long-term municipal bonds. The interest earned on these investments is paid to Common Shareholders in the form of dividends, and the value of these portfolio holdings is reflected in the per share net asset value of the fund’s common stock. In order for either of these forms of leverage to benefit Common shareholders, the yield curve must be positively sloped: that is, short-term interest rates must be lower than long-term interest rates. At the same time, a period of generally declining interest rates will benefit Common Shareholders. If either of these conditions change along with other factors that may have an effect on preferred dividends or tender options bonds, then the risk of leveraging will begin to outweigh the benefits.

Supplemental Information

During the period ended February 28, 2014, there were: (i) no material changes in the fund’s investment objectives or fundamental investment policies, (ii) no changes in the fund’s charter or by-laws that would delay or prevent a change of control of the fund, (iii) no material changes in the principal risk factors associated with investment in the fund, and (iv) no change in the persons primarily responsible for the day-to-day management of the fund’s portfolio.

The Fund 35

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund hereby reports all the dividends paid from investment income-net during its fiscal year ended February 28, 2014 as “exempt-interest dividends” (not generally subject to regular federal income tax).Where required by federal tax law rules, shareholders will receive notification of their portion of the fund’s taxable ordinary dividends (if any), capital gains distributions (if any) and tax-exempt dividends paid for the 2014 calendar year on Form 1099-DIV, which will be mailed in early 2015.

36

|

| BOARD MEMBERS INFORMATION (Unaudited) |

| INDEPENDENT BOARD MEMBERS |

|

| Joseph S. DiMartino (70) |

| Chairman of the Board (2013) |

| Current term expires in 2016 |

| Principal Occupation During Past 5Years: |

| • Corporate Director and Trustee |

| Other Public Company Board Memberships During Past 5Years: |

| • CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small |

| and medium size companies, Director (1997-present) |

| • The Newark Group, a provider of a national market of paper recovery facilities, paperboard |

| mills and paperboard converting plants, Director (2000-2010) |

| • Sunair Services Corporation, a provider of certain outdoor-related services to homes and |

| businesses, Director (2005-2009) |

| No. of Portfolios for which Board Member Serves: 142 |

| ——————— |

| Whitney I. Gerard (79) |

| Board Member (2013) |

| Current term expires in 2016 |

| Principal Occupation During Past 5Years: |

| • Partner in the law firm of Chadbourne & Parke LLP |

| No. of Portfolios for which Board Member Serves: 35 |

| ——————— |

| Nathan Leventhal (71) |

| Board Member (2013) |

| Current term expires in 2016 |

| Principal Occupation During Past 5Years: |

| • Chairman of the Avery-Fisher Artist Program (1997-present) |

| • Commissioner, NYC Planning Commission (2007-2011) |

| Other Public Company Board Memberships During Past 5Years: |

| • Movado Group, Inc., Director (2003-present) |

| No. of Portfolios for which Board Member Serves: 49 |

| ——————— |

| Benaree Pratt Wiley (67) |

| Board Member (2013) |

| Current term expires in 2016 |

| Principal Occupation During Past 5Years: |

| • Principal,TheWiley Group, a firm specializing in strategy and business development (2005-present) |

| Other Public Company Board Memberships During Past 5Years: |

| • CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small |

| and medium size companies, Director (2008-present) |

| No. of Portfolios for which Board Member Serves: 62 |

Th eFund 37

|

| BOARD MEMBERS INFORMATION (Unaudited) (continued) |

| INTERESTED BOARD MEMBER |

|

| Gordon J. Davis (72) |

| Board Member (2013) |

| Principal Occupation During Past 5Years: |