STL MARKETING GROUP, INC.

10 BOULDER CRESCENT, SUITE 102

COLORADO SPRINGS, CO 80903

March 28, 2014

VIA ELECTRONIC MAIL

Mara L. Ransom

Assistant Director

U.S. Securities & Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549

| Re: | STL Marketing Group, Inc. | |

| Second Amended Registration Statement on Form 10 | ||

| Filed December 9, 2013 | ||

| File No. 000-55013 |

Dear Ms. Ransom:

By letter dated January 3, 2014, the staff (the “Staff,” “you” or “your”) of the U.S. Securities & Exchange Commission (the “Commission”) provided STL Marketing Group, Inc. (the “Company,” “we,” “us” or “our”) with its comments to the Company’s Amended Registration Statement on Form 10, filed on December 9, 2010 (the “Registration Statement”). We are in receipt of your letter and set forth below are the Company’s responses to the Staff’s comments. For your convenience, the comments are listed below, followed by the Company’s responses.

General

| 1. | We note your response to comment 2 in our letter dated August 26, 2013. Please disclose whether the following statements are based upon management’s belief, industry data, reports/articles or any other source. If the statement is based upon management’s belief, please indicate that this is the case and include an explanation for the basis of such belief. Alternatively, if the information is based upon reports or articles, please disclose the source of the information in your filing and provide us copies of these documents, appropriately marked to highlight the sections relied upon. |

| ● | “[Costa Rica] already uses hydroelectric and geo thermal methods and, in 2007, set 2021 as the year it becomes carbon neutral,” on page 5. |

RESPONSE:We have revised our disclosure to cite our source for the statement above. Additionally, we have provided the article appropriately marked to highlight the sections relied upon and have attached it hereto asExhibit A.

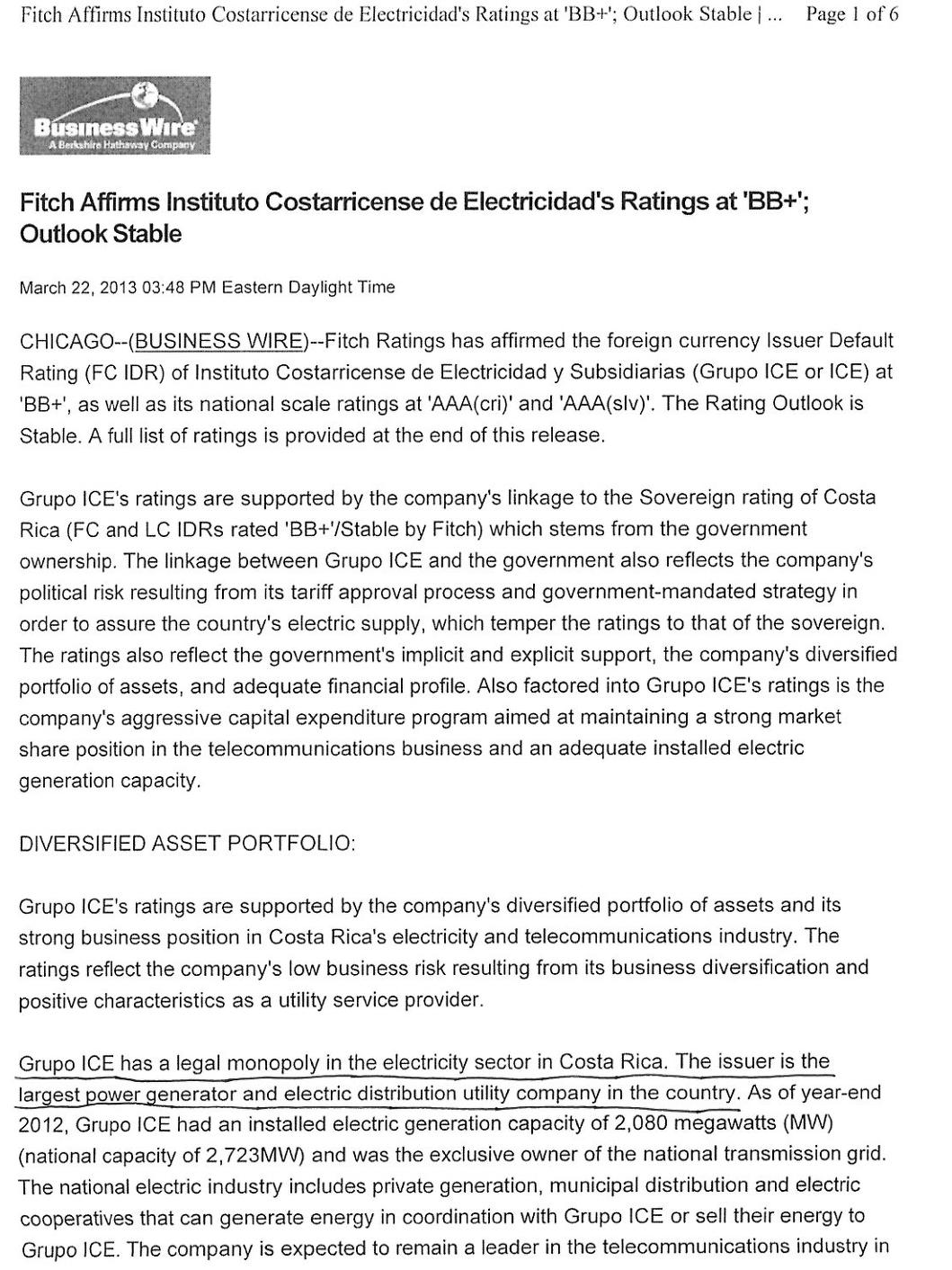

| ● | “The largest, and most recognized, entity is the Instituto Costarricense de Electricidad (“ICE”),” on page 5. |

RESPONSE:We have revised our disclosureaccordingly andwe have provided the source material appropriately marked to highlight the section relied upon asExhibit B hereto.

| ● | “ICE’s latest hydroelectric project was put into operation almost 6 years behind schedule and at a cost of more than $4.3 mm per MW. Its two largest projects- Diquis and Reventazon- are unfunded and already behind schedule. These delays mean that about 900 MW will not come on-line in the next 10 years, further straining the need for electrical infrastructure,” on page 5. |

RESPONSE:The foregoing statement was made by the former Chairman and Chief Executive Officer of Grupo ICE, Mr. Pedro Quiros. Mr. Pedro Quiros held this position with Grupo ICE from 2006-2010. Currently, Mr. Pedro Quiros is the current Chairman of the Board of the Company. The Company believes this statement is true and factual according to the direct knowledge of the Chairman of the Company, Mr. Pedro Quiros.

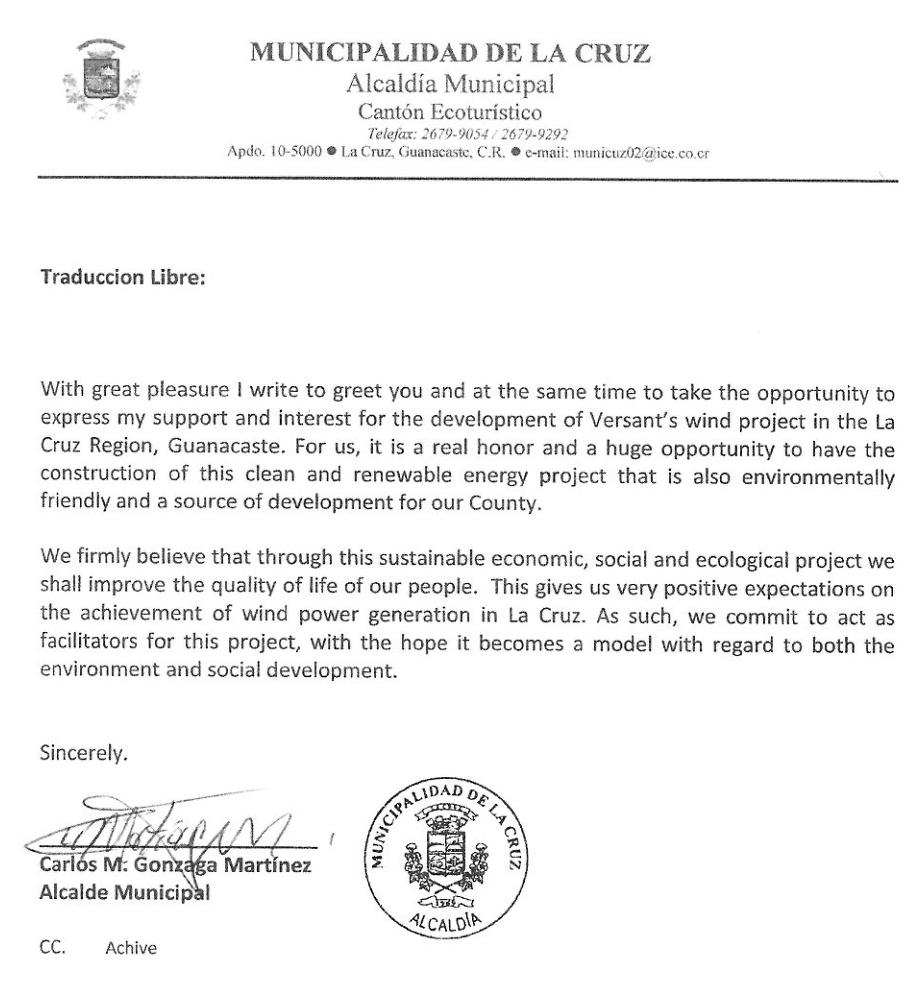

| 2. | We further note your response to comment 2 in our letter dated August 26, 2013, in which you state that “[t]e statement that “Mayor Matias Gonzaga is a supporter of the project and assisting the Company fully” is supported by letters from the Mayor, copies of which are attached hereto. Additionally, the lease has been filed as an exhibit as well as a report related to the potential wind resources of the land.” We note that neither the letters nor the lease has been filed as an exhibit or otherwise provided to us. Please advise or revise. |

RESPONSE:We have sent the Lease Agreement to the offices of the Commission as the Lease Agreement is confidential with certain confidentiality practices. See Section 10 of the Lease Agreement. We have provided the letter from Mayor Matias Gonzaga asExhibit C hereto.

| 3. | We note your response to comment 3 in our letter dated August 26, 2013. While we note that you have provided quotations of some source materials to us, please provide copies of such source materials, appropriately mark such materials to highlight the sections relied upon and cross-referenced to your prospectus and provide the remainder of such materials. For example, we still do not see support for your statement on page 5 that “[a]ccording to The Economist Intelligence Unit, October 2, 2012, “In 2004, 46.7% of Costa Rica’s primary energy came from renewable sources, while 94% of its electricity was generated from hydroelectric power, wind farms and geothermal energy in 2006. A 3.5% tax on gasoline in the country is used for payments to compensate landowners for growing trees and protecting forests and its government is making further plans for reducing emissions from transport, farming and industry.” If you funded or were otherwise affiliated with any of the studies or reports you cite, other than with regard to the AEP Report generated by Garrad Hassan, please disclose this. Please also tell us whether these reports and articles are publicly available without cost or at a nominal expense to investors. |

RESPONSE:We have revised our disclosure and provided the source material appropriately marked to highlight the sections relied upon and cross-referenced to our prospectus attached asExhibit D hereto. We did not fund or were not otherwise affiliated with any of the studies or reports cited herein, except for the AEP Report generated by Garrad Hassan as disclosed. To the best of our knowledge, these reports and articles are publicly available without cost or at a nominal expense to investors.

| 4. | We note that you have provided us with a portion of the AEP Report generated by Garrad Hassan. Please provide the entirety of such report, appropriately marked to highlight the sections relied upon and cross-referenced to your prospectus. |

RESPONSE: We have provided the AEP Report in full via regular mail to the Commission as the contents of this report are confidential and we do not want our competitors to have access to this information.

| 5. | We note your response to comment 4 in our letter dated August 26, 2013. However, we continue to note that you have not begun operations, generated any revenues, or developed your wind turbine business. As applicable, please further revise your registration statement to remove statements that imply you have operations, revenue or assets that you do not have. As examples only, we note the following disclosure: |

| ● | “The Company and SIEPAC do not have any contractual relationship, however, if the Company is successful in building its wind farm, SIEPAC, as an interconnection, will provide power generated by our wind farm to customers across Costa Rica,” on page 6. |

RESPONSE:We have revised our disclosure to remove any implications that we have operations, revenue or assets that we do not have and made the above statement more clear. The Company and SIEPAC have entered into a non-binding letter of intent whereby SIEPAC intends to serve as an interconnection and will provide power generated by our wind farm to customers across Costa Rica. Please see the Letter of Intent filed on December 9, 2013 as Exhibit 10.3 to the amended Form 10 registration statement.

| ● | Your reference to “selected vendors” on page 14. |

RESPONSE:We have revised our disclosure to remove the above quoted statement.

| ● | “The lease costs 4% of the energy generated and sold from the facility,” on page 17. |

RESPONSE:We have revised our disclosure in this section for clarity and to remove any implications that we have operations, revenue or assets that we do not have. Please see the Lease Agreement sent via regular mail to the offices of the Commission at your attention.

Explanatory Note, page 3

| 6. | We note your response to comment 6 in our letter dated August 26, 2013; however, we do not believe that any clarifications have been made to the statement in the third sentence of the first paragraph. Please advise or revise. |

RESPONSE:We have revised our disclosure by removing the third sentence of the first paragraph.

Item 1. Business, page 4

| 7. | Please update your statement here and in Item 2. Financial Information that you expect to execute the PPA in 2013. |

RESPONSE:We have updated our disclosure in accordance with this comment.

Wind Studies, page 7

| 8. | Please confirm whether you have paid or plan to pay Garrad Hassan an additional amount for the new AEP Report disclosed on page 7. |

RESPONSE:We have made a payment of $20,000 to Garrad Hassan for a new AEP Report and plan to pay the remaining balance of $18,120 upon completion of certain amendments.

Competition, page 7

| 9. | Please describe the competition you face in signing the PPA. In this regard, we note your statement on page 10 that “[d]epending on the regulatory framework and market dynamics of a region, we may also compete with other wind energy companies, as well other renewable energy generators, when we bid on or negotiate for a long-term power purchase agreement (“PPA”).” We also note your statement that you “compete with traditional energy companies,” also on page 10. Please also describe the competition you anticipate facing if the PPA is canceled or otherwise terminated. |

RESPONSE:We have revised our disclosure in accordance with this comment to discuss the competition we face in signing the PPA.

Additionally, the PPA, if cancelled, terminates the Company’s potential sales and ability to continue its business operations. Alternatively, if the PPA is executed the Company believes it will have no competition as the PPA constitutes a supply contract to the government. The Off-Taker or Buyer is the government of Costa Rica which has certain concessions that provide it with its territory to service end users and business customers. We only sell to the Off-Taker, and the PPA is the supply “sales contract” for this energy to the government.

Item 2. Financial Information, page 14

Plan & Operations, page 14

| 10. | Please provide further disclosure regarding the process of negotiating and signing the PPA, including your plans if you are not able to sign the PPA as intended. |

RESPONSE:We have provided further disclosure in this section regarding the process of negotiating and signing the PPA as well as the possibility that we may have to cease our business operations in the event we are unable to sign the PPA.

Liquidity and Capital Resources, page 16

| 11. | We note your changes to the first risk factor on page 7, in which you estimate that you have “sufficient capital for operations through the first quarter of the 2014 fiscal year.” We also note your disclosure on page 16 that you have “sufficient capital for operations through fiscal year ended 2013.” Please advise or revise. |

RESPONSE:We have revised our disclosure to remove the statement that we have “sufficient capital for operations through fiscal year ended 2013.”

Item 3. Properties, page 17

| 12. | Please clarify the start date of the lease agreement in Guanacaste, Costa Rica. |

RESPONSE:The start date of the lease agreement in Guanacaste, Costa Rica is the moment when the Company starts generating electricity as described in the second amended registration statement on Form 10. This can be viewed in the Lease Agreement on page 2.

Item 4. Security Ownership of Certain Beneficial Holders and Management, page 17

| 13. | Please disclose the name and address of the natural persons who have voting and dispositive control over the shares held by each of Versant I, Inc., Full Moon Night Corp., Red Canyon Investments Corp., Grupos Unídos Tres Ele, S.A., Almunidos S.A. and Portafolio de Inversiones Lulu S.A. |

RESPONSE:We have revised our disclosure to provide the name and address of the natural persons who have voting and dispositive control over the shares held by the entities named in this comment.

Item 7. Certain Relationships and Related Transactions, and Director Independence, page 21

| 14. | Please revise your disclosure regarding the related party notes payable such that disclosure of the amount involved in the transaction includes the largest aggregate amount of principal outstanding during the period for which disclosure is provided, the amount thereof outstanding as of the latest practicable date, the amount of principal paid during the periods for which disclosure is provided, the amount of interest paid during the period for which disclosure is provided, and the rate or amount of interest payable on the indebtedness. In particular, we note that many of the amounts outstanding as of September 30, 2013 do not include accrued interest. Please see Item 404(a)(5) of Regulation S-K. |

RESPONSE:We have revised our disclosure in the related party notes payable section in accordance with Item 404(a)(5) of Regulation S-K.

Item 10. Recent Sales of Unregistered Securities, page 22

| 15. | We note your disclosure on page 17 that a number of your shareholders “were brought over in the merger.” Please confirm whether the issuance of shares to such shareholders should be included in your disclosure under Item 10, as recent sales of unregistered securities, and revise your disclosure, as appropriate. |

RESPONSE:We have revised this section to include the shares issued in the merger as recent sales of unregistered securities.

Item 13. Financial Statements and Supplementary Data, page 25

General

| 16. | We reviewed your response to comment 22 in our letter dated August 26, 2013. We are unable to locate any pro forma statements of operations data showing the effect of the reverse merger for the latest fiscal year. Please provide the pro forma financial information required by Rule 8-05 of Regulation S-X or tell us why you believe pro forma financial information is not required. |

RESPONSE:We have revised our disclosure to include pro forma financial information in accordance with Rule 8-05 of Regulation S-X.

STL Marketing Group, Inc. and Subsidiaries Financial Statements, page 25

Consolidated Changes in Stockholders’ Deficit, page F-3

| 17. | Please tell us why a portion of the net equity deficit acquired in the reverse merger is recognized as a reduction in additional paid-in capital, common stock. |

RESPONSE:We have revised our disclosure accordingly.

| 18. | Please tell us the consideration transferred to purchase treasury shares during the nine months ended September 30, 2013. Please also tell us why the transaction is not reflected in the condensed consolidated statements of cash flows or disclosed in the notes to financial statements. |

RESPONSE:Consideration consists of $200,000 of convertible notes issued for stock. We have revised the cash flow to include the disclosure in the supplemental disclosure of the non-cash investing and financing activities.

Condensed Consolidated Statements of Cash Flows, page F-4

| 19. | We reviewed the revisions to your disclosure in response to comment 27 in our letter dated August 26, 2013. It appears that the net amount of the assets and liabilities acquired in the reverse merger presented in the supplemental disclosure of non-cash investing and financing activities differs from the amount of the net equity deficit acquired as presented in the consolidated statement of stockholders’ deficit. Please revise or advise. |

RESPONSE:We have revised our disclosure for consistency in accordance with this comment.

| 20. | We note that the proceeds from convertible notes for the nine months ended September 30, 2013 differs from the amount of borrowings presented in the table at the top of page F-14. Please revise or advise. |

RESPONSE:We haverevised disclosure on page F-14 to breakout convertible notes issued for common stock.

| 21. | We reviewed your response to comment 24 in our letter dated August 26, 2013. Please tell us how the loan to related party at September 30, 2013 is classified in the condensed consolidated balance sheets. Please also tell us how stock based compensation for the nine months ended September 30, 2013 is presented in the condensed consolidated statements of changes in stockholders’ deficit. |

RESPONSE:There is no longer a loan to related parties at September 30, 2013. The $13,675 included in the statement of cash flows represents loans to Versant Corporation and were eliminated at the consummation of the merger with Versant.

The stock based compensation for the nine months ended September 30, 2013 is included in the $103,333 liabilities to be settled in stock. The equity instrument for this stock based compensation has not yet been issued. There were $98,333 of liabilities to be settled in stock due to the reverse merger.

Notes to the Condensed Consolidated Financial Statements, page F-5

Note 1 – Nature of Operations and Summary of Significant Accounting Policies, page F-5 Nature of Operations, page F-5

| 22. | We reviewed the revisions to your disclosure in response to comment 28 in our letter dated August 26, 2013. Please revise your disclosure in the first paragraph to clarify that you issued 1.8 million shares of Class A preferred stock in exchange for 1.8 million shares of Class A preferred stock held by the shareholders of Versant, 1.4 billion shares of Class B preferred stock in exchange for 1,000 shares of Class X common stock held by the shareholders of Versant, and 100.2 million shares of Class B common stock in exchange for the Class B common stock held by the shareholders of Versant. In addition, please explain to us your basis for allocating the 100.2 million shares of Class B common stock to the Class B common stock equity transactions of Versant during 2010 and 2011. Furthermore, please file a copy of the acquisition agreement as an exhibit to the filing as previously requested. |

RESPONSE:We have revised our disclosure accordingly to include the above requested information. With regard to the basis for allocating 100 million shares of STLK Class B Common Stock for the Versant Corporation Common Stock, the shares had a dollar value in Versant Corporation of $219,000. Versant agreed to assuming STLK, a Caveat Emptor rated OTC firm, and assigned a price for the issuance that was twice the market price prior to the merger. As such, we allocated a $0.00219 price to the STLK stock for conversion, as that was the price agreed to in order to complete the Share Exchange Plan since there were no guarantees the price of the shares would appreciate and the debt on STLK was significant. Prior to the announcement of the merger in October 2012, the shares had a cost of $0.001 per share. For the purposes of the merger, the shares were valued at $0.00219 for the issuance, the stock has a low volume and was highly volatile. At current prices this block of shares could not be sold in less than 18 months. The shares are restricted and have not been sold, registered or otherwise used.

| 23. | Please tell us how you computed the ownership percentages disclosed in the next to last sentence in the first paragraph. |

RESPONSE:The ownership percentages are calculated based upon the overall outstanding share amount at time of merger of 1,528,423,524. The accounting acquirer held 1,501,800,000 of the 1,528,423,524 outstanding shares or 98.26%. The same calculation is used for the legal acquirer, which held 26,623,524 of the 1,528,423,524 outstanding shares or 1.74%.

STL Marketing Group, Inc. Financial Statements, page 26

General

| 24. | We reviewed your response to comment 21 in our letter dated August 26, 2013. Please tell why you believe STL Marketing Group, Inc. does not meet the definition of development stage enterprise. Since STL Marketing Group, Inc. is a shell company, it appears that the financial statements should comply with ASC 915. |

RESPONSE:STL Marketing Group, Inc. prior to 2010 was an operating company, with significant asset and revenues and was not in the development stage. On December 1, 2009, the company sold the majority of its assets, leaving the company with limited assets and no operations. From that time, through the merger with Versant Corporation, the company was a shell company looking for a business purpose. There were no revenues and limited expenses to keep the company alive. The company merged with Versant Corporation, which is a development stage enterprise. Versant Corporation is the accounting acquirer and the financial statements from date of merger are those of Versant Corporation and include the required disclosures. STL Marketing Group, Inc. is not a shell company as of February 6th, 2014. The merger announced in October 2012, was finalized on February 6, 2013.

Note 7 – Convertible Notes Payable, page F-14

(A) Convertible Notes Payable, page F-14

| 25. | We reviewed your response to comment 30 in our letter dated August 26, 2013 and the revisions to your disclosure. As previously requested, please revise to disclose the payment terms and/or maturity dates of the convertible notes. Please refer to ASC 505- 10-50-3. |

RESPONSE: We have revised this section to disclose the payment terms and/or maturity dates of the convertible notes.

Note 8 – Derivative Liabilities, page F-15

| 26. | We reviewed your response to comment 31 in our letter dated August 26, 2013 and the revisions to your disclosure. As previously requested, please revise to disclose the valuation technique used to measure the fair value of the embedded conversion options classified as derivative liabilities. Please refer to ASC820-10-50-2(e). |

RESPONSE:We have revised our disclosure to include the valuation technique used to measure the fair value of the embedded conversion options classified as derivative liabilities.

Form 10-Q for Fiscal Quarter Ended September 30, 2013

| 27. | Please address the above comments in regard to STL Marketing Group, Inc. and Subsidiaries as applicable. |

RESPONSE:We will address the above comments in regard to STL Marketing Group, Inc. and Subsidiaries as applicable.

Exhibits 31.1 and 31.2

| 28. | Please revise paragraphs 4 and 5 to conform exactly to the certifications as set forth in Item 601(b)(31)(i) of Regulation S-K. |

RESPONSE: We will revise paragraphs 4 and 5 to conform exactly to the certifications as set forth in Item 601(b)(31)(i) of Regulation S-K.

Very Truly Yours,

| /s/ Jose P. Quiros | |

| Jose P. Quiros | |

| Chief Executive Officer | |

| STL Marketing Group |

Exhibit A

Exhibit B

Exhibit C

Exhibit D