EXHIBIT 99.1

I NVESTOR P RESENTATION N OVEMBER 2014 M ERGE W ORTH R X C ORP . B USINESS C OMBINATION WITH A ERO C ARE H OLDINGS , I NC .

2 Disclaimer ▪ The sole purpose of the presentation is to assist persons in deciding whether they wish to proceed with a further review of the proposed transaction discussed herein and is not intended to be all - inclusive or to contain all the information that a person may desire in considering the proposed transaction discussed herein . It is not intended to form the basis of any investment decision or any other decision in respect of the proposed transaction . ▪ This presentation shall not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed transactions . This presentation shall also not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . No offering of securities shall be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933 , as amended . ▪ This presentation includes “forward - looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995 . MWRX’s actual results may differ from its expectations, estimates and projections and consequently, you should not rely on these forward looking statements as predictions of future events . Words such as “expect,” “estimate,” “project,” “budget,” “forecast,” “anticipate,” “intend,” “plan,” “may,” “will,” “could,” “should,” “believes,” “predicts,” “potential,” “continue,” and similar expressions are intended to identify such forward - looking statements . These forward - looking statements include, without limitation, the expectations of MergeWorthRX Corp . (“ MWRX ”) with respect to future performance and anticipated financial impacts of the proposed transaction, the satisfaction of the closing conditions to the proposed transaction, and the timing of the completion of the proposed transaction . ▪ These forward - looking statements involve significant risks and uncertainties that could cause the actual results to differ materially from the expected results . Most of these factors are outside MWRX’s control and are difficult to predict . Factors that may cause such differences include, but are not limited to, those described under the heading “Risk Factors” in MWRX’s final prospectus, dated June 26 , 2013 . ▪ Other factors include the possibility that the transactions contemplated by a potential transaction agreement do not close, including due to the failure of certain closing conditions . ▪ MWRX cautions that the foregoing list of factors is not exclusive . Additional information concerning these and other risk factors is contained in MWRX’s most recent filings with the Securities and Exchange Commission . All subsequent written and oral forward - looking statements concerning MWRX, a potential transaction agreement, the related transactions, or other matters and attributable to MWRX or any person acting on its behalf, are expressly qualified in their entirety by the cautionary statements above . MWRX cautions readers not to place undue reliance upon any forward - looking statements, which speak only as of the date made . MWRX does not undertake or accept any obligation or undertaking to release publicly any updates or revisions to any forward - looking statements to reflect any change in its expectations or any change in events, conditions or circumstances on which any such statement is based . ▪ AeroCare reports its financial results in accordance with U . S . generally accepted accounting principles, or GAAP . To supplement this information, AeroCare also presents several other metrics including : Adjusted EBITDA and Pro Forma Adjusted EBITDA, which are non - GAAP financial measures under Section 101 of Regulation G under the Securities Exchange Act of 1934 , as amended . ▪ Adjusted EBITDA is a non - GAAP measure and consists of GAAP net income (loss) as reported and adjusts for : tax provision (benefit) ; interest expense and other income, net ; stock - based compensation expense ; depreciation and amortization ; non - recurring and transaction - related costs ; and non - cash asset impairment charges . ▪ Pro Forma Adjusted EBITDA is a non - GAAP measure and consists of the same items as Adjusted EBITDA and is pro forma to reflect annualized contribution from completed acquisitions as if they occurred on the first day of the stated year . With respect to the year ending December 31 , 2014 , Pro Forma Adjusted EBITDA includes annual EBITDA from three ( 3 ) acquisitions that are under Letter of Intent (LOI), which are anticipated, although there can be no assurance of same, to close in Q 4 ’ 14 .

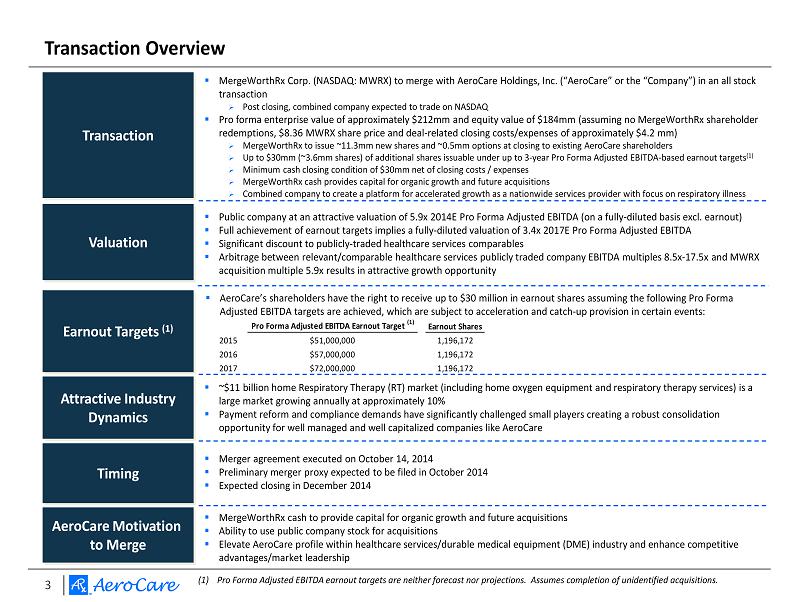

3 Transaction Overview Transaction ▪ MergeWorthRx Corp. (NASDAQ: MWRX) to merge with AeroCare Holdings, Inc . (“AeroCare” or the “Company”) in an all stock transaction » Post closing, combined company expected to trade on NASDAQ ▪ Pro forma enterprise value of approximately $212mm and equity value of $184mm (assuming no MergeWorthRx shareholder redemptions, $8.36 MWRX share price and deal - related closing costs/expenses of approximately $4.2 mm) » MergeWorthRx to issue ~ 11.3mm new shares and ~0.5mm options at closing to existing AeroCare shareholders » Up to $30mm (~ 3.6mm shares) of additional shares issuable under up to 3 - year Pro Forma Adjusted EBITDA - based earnout targets (1) » Minimum cash closing condition of $ 30mm net of closing costs / expenses » MergeWorthRx cash provides capital for organic growth and future acquisitions » Combined company to create a platform for accelerated growth as a nationwide services provider with focus on respiratory illness Valuation ▪ Public company at an attractive valuation of 5.9x 2014E Pro Forma Adjusted EBITDA (on a fully - diluted basis excl. earnout) ▪ Full achievement of earnout targets implies a fully - diluted valuation of 3.4x 2017E Pro Forma Adjusted EBITDA ▪ Significant discount to publicly - traded healthcare services comparables ▪ Arbitrage between relevant/comparable healthcare services publicly traded company EBITDA multiples 8.5x - 17.5x and MWRX acquisition multiple 5.9x results in attractive growth opportunity ▪ MergeWorthRx cash to provide capital for organic growth and future acquisitions ▪ Ability to use public company stock for acquisitions ▪ Elevate AeroCare profile within healthcare services/durable medical equipment (DME) industry and enhance competitive advantages/market leadership AeroCare Motivation to Merge Timing ▪ Merger agreement executed on October 14, 2014 ▪ Preliminary merger proxy expected to be filed in October 2014 ▪ Expected closing in December 2014 Attractive Industry Dynamics ▪ ~$11 billion home R espiratory Therapy (RT) market (including home oxygen equipment and respiratory therapy services) is a large market growing annually at approximately 10 % ▪ Payment reform and compliance demands have significantly challenged small players creating a robust consolidation opportunity for well managed and well capitalized companies like AeroCare Earnout Targets (1) ▪ AeroCare’s shareholders have the right to receive up to $30 million in earnout shares assuming the following P ro Forma Adjusted EBITDA targets are achieved, which are subject to acceleration and catch - up provision in certain events: Pro Forma Adjusted EBITDA Earnout Target (1) Earnout Shares 2015 $51,000,000 1,196,172 2016 $57,000,000 1,196,172 2017 $72,000,000 1,196,172 (1) Pro Forma Adjusted EBITDA earnout targets are neither forecast nor projections . Assumes completion of unidentified acquisitions .

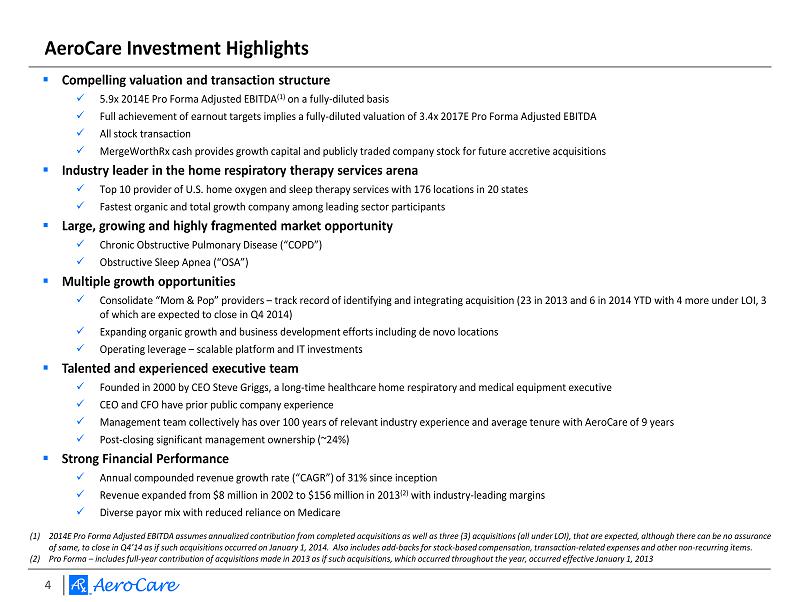

4 AeroCare Investment Highlights ▪ Compelling valuation and transaction structure x 5.9x 2014E Pro Forma Adjusted EBITDA (1) on a fully - diluted basis x Full achievement of earnout targets implies a fully - diluted valuation of 3.4x 2017E Pro Forma Adjusted EBITDA x All stock transaction x MergeWorthRx cash provides growth capital and publicly traded company stock for future accretive acquisitions ▪ Industry leader in the home respiratory therapy services arena x Top 10 provider of U.S. home oxygen and sleep therapy services with 176 locations in 20 states x Fastest organic and total growth company among leading sector participants ▪ Large, growing and highly fragmented market opportunity x Chronic Obstructive Pulmonary Disease (“COPD”) x Obstructive Sleep Apnea (“OSA”) ▪ Multiple growth opportunities x Consolidate “Mom & Pop” providers – track record of identifying and integrating acquisition (23 in 2013 and 6 in 2014 YTD with 4 more under LOI, 3 of which are expected to close in Q4 2014) x Expanding organic growth and business development efforts including de novo locations x Operating leverage – scalable platform and IT investments ▪ Talented and experienced executive team x Founded in 2000 by CEO Steve Griggs, a long - time healthcare home respiratory and medical equipment executive x CEO and CFO have prior public company experience x Management team collectively has over 100 years of relevant industry experience and average tenure with AeroCare of 9 years x Post - closing s ignificant management ownership (~24%) ▪ Strong Financial Performance x Annual compounded revenue growth rate (“CAGR”) of 31% since inception x Revenue expanded from $8 million in 2002 to $156 million in 2013 (2) with industry - leading margins x Diverse payor mix with reduced reliance on Medicare (1) 2014E Pro Forma Adjusted EBITDA assumes annualized contribution from completed acquisitions as well as three (3) acquisitions (all under LOI), that are expected, although there can be no assurance of same, to close in Q4’14 as if such acquisitions occurred on January 1, 2014. Also includes add - backs for stock - based compens ation, transaction - related expenses and other non - recurring items. (2) Pro Forma – includes full - year contribution of acquisitions made in 2013 as if such acquisitions, which occurred throughout the year, occurred effective January 1, 2013

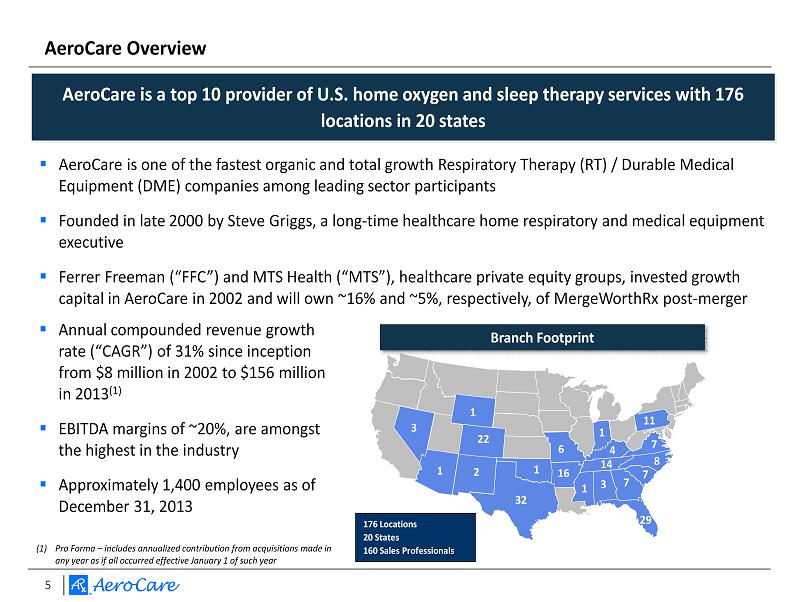

5 ▪ AeroCare is one of the fastest organic and total growth Respiratory Therapy (RT) / Durable Medical Equipment (DME) companies among leading sector participants ▪ Founded in late 2000 by Steve Griggs, a long - time healthcare home respiratory and medical equipment executive ▪ Ferrer Freeman (“FFC”) and MTS Health (“MTS”), healthcare private equity groups, invested growth capital in AeroCare in 2002 and will own ~16% and ~5%, respectively, of MergeWorthRx post - merger AeroCare Overview 16 22 29 7 14 6 3 8 11 32 7 7 1 1 3 176 Locations 20 States 160 Sales Professionals Branch Footprint 2 4 1 1 1 ▪ Annual compounded revenue growth rate (“CAGR”) of 31% since inception from $8 million in 2002 to $156 million in 2013 (1 ) ▪ EBITDA margins of ~20%, are amongst the highest in the industry ▪ Approximately 1,400 employees as of December 31, 2013 AeroCare is a top 10 provider of U.S. home oxygen and sleep therapy services with 176 locations in 20 states (1) Pro Forma – includes annualized contribution from acquisitions made in any year as if all occurred effective January 1 of such year

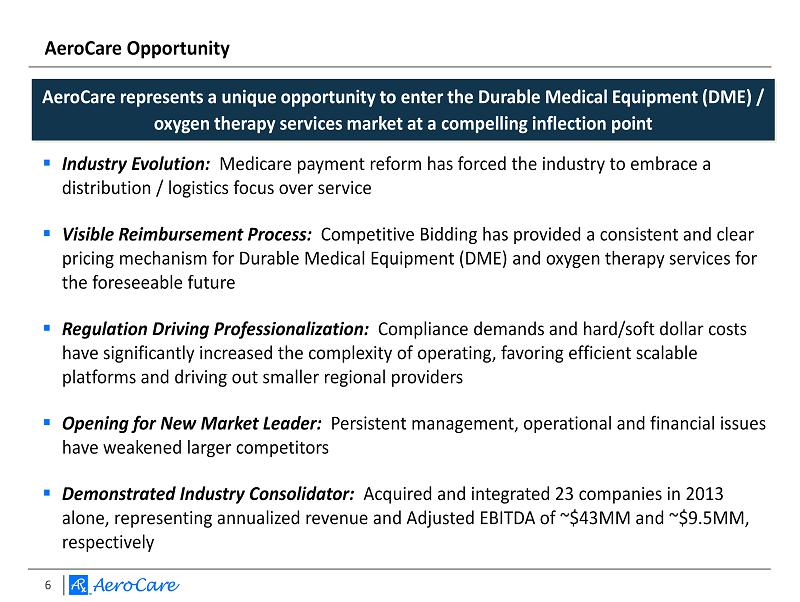

6 ▪ Industry Evolution: Medicare payment reform has forced the industry to embrace a distribution / logistics focus over service ▪ Visible Reimbursement Process: Competitive Bidding has provided a consistent and clear pricing mechanism for Durable Medical Equipment (DME) and oxygen therapy services for the foreseeable future ▪ Regulation Driving Professionalization: Compliance demands and hard/soft dollar costs have significantly increased the complexity of operating, favoring efficient scalable platforms and driving out smaller regional providers ▪ Opening for New Market Leader: Persistent management, operational and financial issues have weakened larger competitors ▪ Demonstrated Industry Consolidator: Acquired and integrated 23 companies in 2013 alone, representing annualized revenue and Adjusted EBITDA of ~$43MM and ~$9.5MM, respectively AeroCare Opportunity AeroCare represents a unique opportunity to enter the Durable Medical Equipment (DME) / oxygen therapy services market at a compelling inflection point

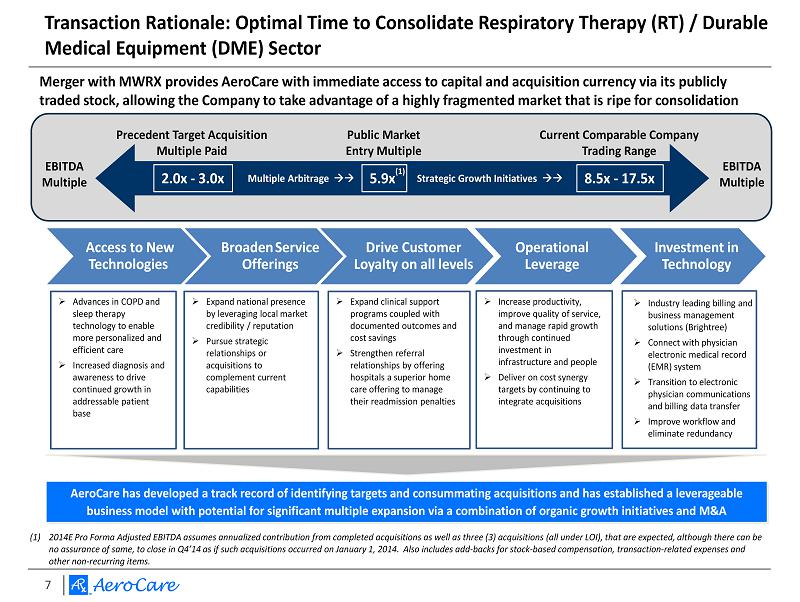

7 Transaction Rationale: Optimal Time to Consolidate Respiratory Therapy (RT) / Durable Medical Equipment (DME) Sector » Advances in COPD and sleep therapy technology to enable more personalized and efficient care » Increased diagnosis and awareness to drive continued growth in addressable patient base Access to New Technologies Broaden Service Offerings Drive Customer Loyalty on all levels Operational Leverage Investment in Technology » Expand national presence by leveraging local market credibility / reputation » Pursue strategic relationships or acquisitions to complement current capabilities » Expand clinical support programs coupled with documented outcomes and cost savings » Strengthen referral relationships by offering hospitals a superior home care offering to manage their readmission penalties AeroCare has developed a track record of identifying targets and consummating acquisitions and has established a leverageable business model with potential for significant multiple expansion via a combination of organic growth initiatives and M&A » Increase productivity, improve quality of service, and manage rapid growth through continued investment in infrastructure and people » Deliver on cost synergy targets by continuing to integrate acquisitions EBITDA Multiple 2.0x - 3.0x 5.9x 8.5x - 17.5x EBITDA Multiple Public Market Entry Multiple Current Comparable Company Trading Range Precedent Target Acquisition Multiple Paid Multiple Arbitrage Strategic Growth Initiatives » Industry leading billing and business management solutions (Brightree) » Connect with physician electronic medical record (EMR) system » Transition to electronic physician communications and billing data transfer » Improve workflow and eliminate redundancy Merger with MWRX provides AeroCare with immediate access to capital and acquisition currency via its publicly traded stock, allowing the Company to take advantage of a highly fragmented market that is ripe for consolidation (1) (1) 2014E Pro Forma Adjusted EBITDA assumes annualized contribution from completed acquisitions as well as three (3) acquisitions (all under LOI), that are expected, although there can be no assurance of same, to close in Q4’14 as if such acquisitions occurred on January 1, 2014. Also includes add - backs for stock - based compensation, transaction - related expenses and other non - recurring items.

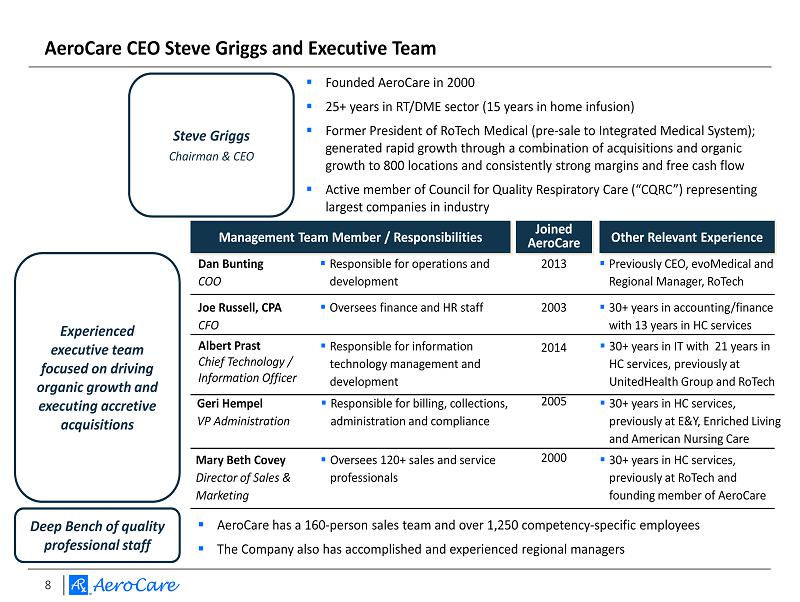

8 AeroCare CEO Steve Griggs and Executive Team ▪ Founded AeroCare in 2000 ▪ 25+ years in RT/DME sector (15 years in home infusion) ▪ Former President of RoTech Medical (pre - sale to Integrated Medical System); generated rapid growth through a combination of acquisitions and organic growth to 800 locations and consistently strong margins and free cash flow ▪ Active member of Council for Quality Respiratory Care (“CQRC”) representing largest companies in industry Steve Griggs Chairman & CEO Experienced executive team focused on driving organic growth and executing accretive acquisitions Management Team Member / Responsibilities Other Relevant Experience Joe Russell, CPA CFO ▪ Oversees finance and HR staff ▪ 30+ years in accounting/finance with 13 years in HC services ▪ Responsible for billing, collections, administration and compliance Geri Hempel VP Administration ▪ 30+ years in HC services, p reviously at E&Y, Enriched Living and American Nursing Care ▪ Oversees 120+ sales and service professionals Mary Beth Covey Director of Sales & Marketing ▪ Responsible for information technology management and development Albert Prast Chief Technology / Information Officer Dan Bunting COO ▪ Responsible for operations and development Joined AeroCare 2003 2013 2005 2000 2014 ▪ AeroCare has a 160 - person sales team and over 1,250 competency - specific employees ▪ The Company also has accomplished and experienced regional managers Deep Bench of quality professional staff ▪ Previously CEO, evoMedical and Regional Manager, RoTech ▪ 30+ years in HC services, previously at RoTech and founding member of AeroCare ▪ 30+ years in IT with 21 years in HC services, previously at UnitedHealth Group and RoTech

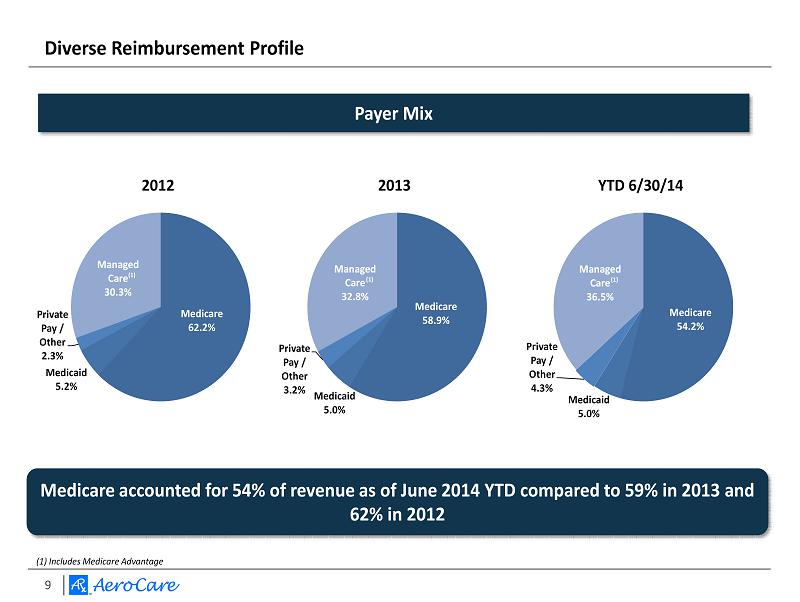

9 Medicare 62.2% Medicaid 5.2% Private Pay / Other 2.3% Managed Care 30.3% 2012 Medicare 58.9% Medicaid 5.0% Private Pay / Other 3.2% Managed Care 32.8% 2013 Medicare 54.2% Medicaid 5.0% Private Pay / Other 4.3% Managed Care 36.5% YTD 6/30/14 Diverse Reimbursement Profile Payer Mix Medicare accounted for 54% of revenue as of June 2014 YTD compared to 59% in 2013 and 62% in 2012 (1) (1) (1) (1) Includes Medicare Advantage

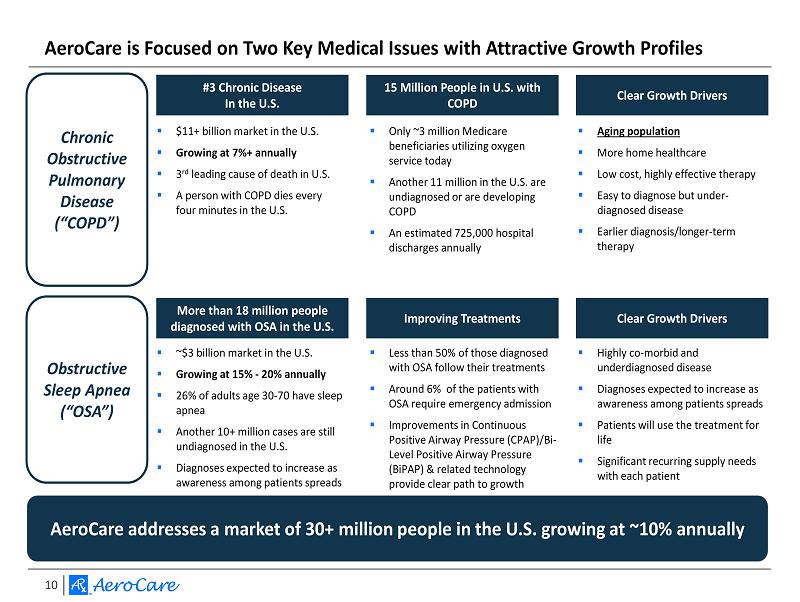

10 AeroCare is Focused on Two Key Medical Issues with Attractive Growth Profiles Chronic Obstructive Pulmonary Disease (“COPD”) Obstructive Sleep Apnea (“OSA”) #3 Chronic Disease In the U.S. 15 Million People in U.S. with COPD Clear Growth Drivers ▪ $11+ billion market in the U.S. ▪ Growing at 7%+ annually ▪ 3 rd leading cause of death in U.S . ▪ A person with COPD dies every four minutes in the U.S . ▪ Only ~3 million Medicare beneficiaries utilizing oxygen service today ▪ Another 11 million in the U.S. are undiagnosed or are developing COPD ▪ An estimated 725,000 hospital discharges annually ▪ Aging population ▪ More home healthcare ▪ Low cost, highly effective therapy ▪ Easy to diagnose but under - diagnosed disease ▪ Earlier diagnosis/longer - term therapy More than 18 million people diagnosed with OSA in the U.S. Clear Growth Drivers ▪ ~ $3 billion market in the U.S. ▪ Growing at 15% - 20% annually ▪ 26% of adults age 30 - 70 have sleep apnea ▪ Another 10+ million cases are still undiagnosed in the U.S. ▪ Diagnoses expected to increase as awareness among patients spreads ▪ Less than 50% of those diagnosed with OSA follow their treatments ▪ Around 6% of the patients with OSA require emergency admission ▪ Improvements in Continuous Positive Airway Pressure ( CPAP )/Bi - Level Positive Airway P ressure (BiPAP) & related technology provide clear path to growth ▪ Highly co - morbid and underdiagnosed disease ▪ Diagnoses expected to increase as awareness among patients spreads ▪ Patients will use the treatment for life ▪ Significant recurring supply needs with each patient Improving Treatments AeroCare addresses a market of 30+ million people in the U.S. growing at ~10% annually

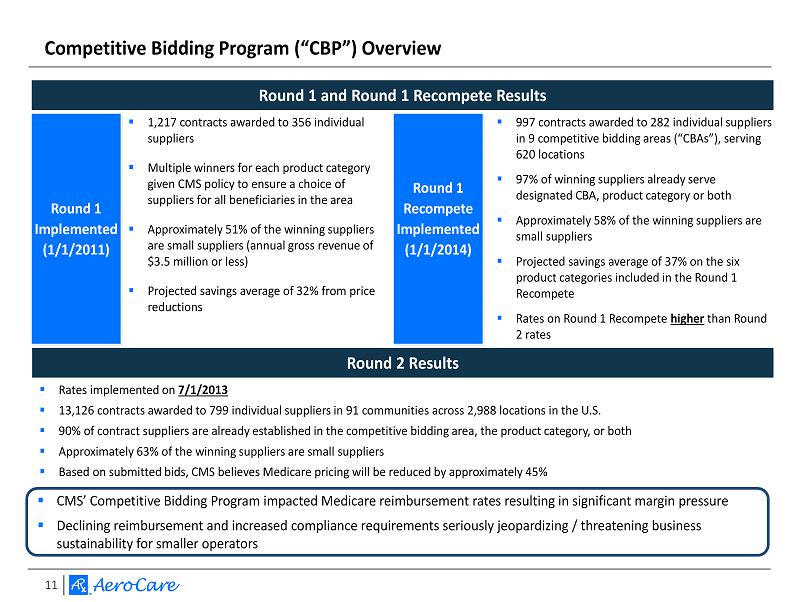

11 Competitive Bidding Program (“CBP”) Overview Round 1 and Round 1 Recompete Results ▪ 1,217 contracts awarded to 356 individual suppliers ▪ Multiple winners for each product category given CMS policy to ensure a choice of suppliers for all beneficiaries in the area ▪ Approximately 51% of the winning suppliers are small suppliers (annual gross revenue of $3.5 million or less) ▪ Projected savings average of 32% from price reductions Round 2 Results ▪ Rates implemented on 7/1/2013 ▪ 13,126 contracts awarded to 799 individual suppliers in 91 communities across 2,988 locations in the U.S. ▪ 90% of contract suppliers are already established in the competitive bidding area, the product category, or both ▪ Approximately 63% of the winning suppliers are small suppliers ▪ Based on submitted bids, CMS believes Medicare pricing will be reduced by approximately 45% Round 1 Implemented (1/1/2011) Round 1 Recompete Implemented (1/1/2014) ▪ 997 contracts awarded to 282 individual suppliers in 9 competitive bidding areas (“CBAs”), serving 620 locations ▪ 97% of winning suppliers already serve designated CBA, product category or both ▪ Approximately 58% of the winning suppliers are small suppliers ▪ Projected savings average of 37% on the six product categories included in the Round 1 Recompete ▪ Rates on Round 1 Recompete higher than Round 2 rates ▪ CMS’ Competitive Bidding Program impacted Medicare reimbursement rates resulting in significant margin pressure ▪ Declining reimbursement and increased compliance requirements seriously jeopardizing / threatening business sustainability for smaller operators

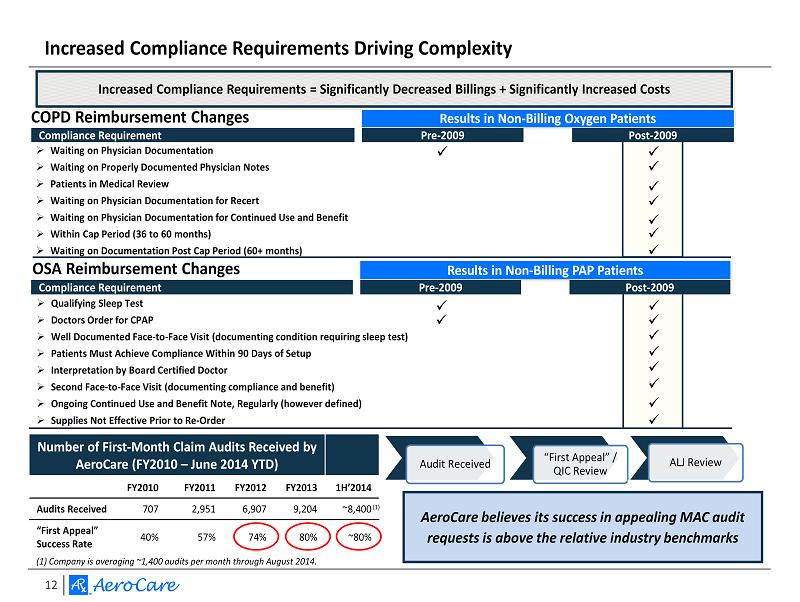

12 » Qualifying Sleep Test » Doctors Order for CPAP » Well Documented Face - to - Face Visit (documenting condition requiring sleep test) » Patients Must Achieve Compliance Within 90 Days of Setup » Interpretation by Board Certified Doctor » Second Face - to - Face Visit (documenting compliance and benefit) » Ongoing Continued Use and Benefit Note, Regularly (however defined) » Supplies Not Effective Prior to Re - Order Increased Compliance Requirements Driving Complexity Results in Non - Billing Oxygen Patients Pre - 2009 Post - 2009 Compliance Requirement x x x x x x x COPD Reimbursement Changes Increased Compliance Requirements = Significantly Decreased Billings + Significantly Increased Costs OSA Reimbursement Changes x x x x x x x x x x Results in Non - Billing PAP Patients Pre - 2009 Post - 2009 Compliance Requirement Number of First - Month Claim Audits Received by AeroCare (FY2010 – June 2014 YTD) FY2010 FY2011 FY2012 FY2013 1H’2014 Audits Received 707 2,951 6,907 9,204 ~8,400 “First Appeal” Success Rate 40% 57% 74% 80% ~80% Audit Received “First Appeal” / QIC Review ALJ Review AeroCare believes its success in appealing MAC audit requests is above the relative industry benchmarks » Waiting on Physician Documentation » Waiting on Properly Documented Physician Notes » Patients in Medical Review » Waiting on Physician Documentation for Recert » Waiting on Physician Documentation for Continued Use and Benefit » Within Cap Period (36 to 60 months) » Waiting on Documentation Post Cap Period (60+ months) x (1) Company is averaging ~1,400 audits per month through August 2014. (1)

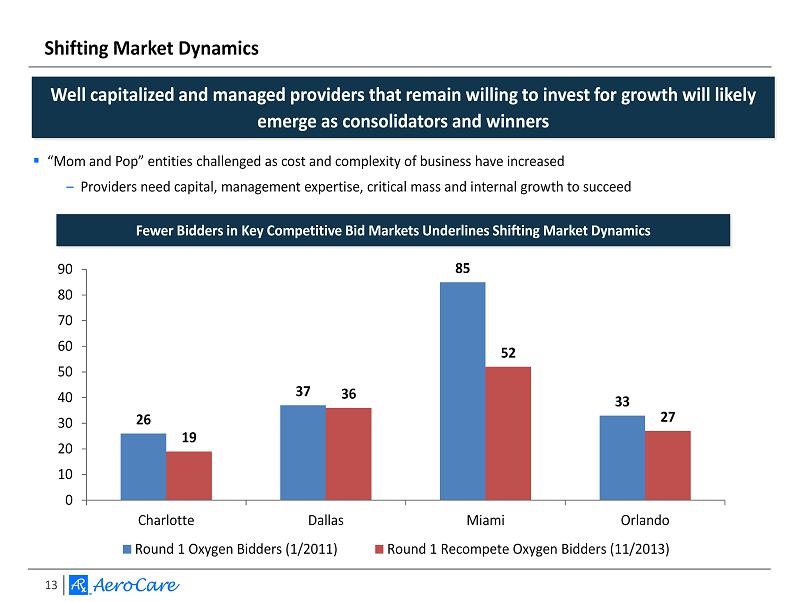

13 Shifting Market Dynamics ▪ “Mom and Pop” entities challenged as cost and complexity of business have increased – Providers need capital, management expertise, critical mass and internal growth to succeed 26 37 85 33 19 36 52 27 0 10 20 30 40 50 60 70 80 90 Charlotte Dallas Miami Orlando Round 1 Oxygen Bidders (1/2011) Round 1 Recompete Oxygen Bidders (11/2013) Fewer Bidders in Key Competitive Bid Markets Underlines Shifting Market Dynamics Well capitalized and managed providers that remain willing to invest for growth will likely emerge as consolidators and winners

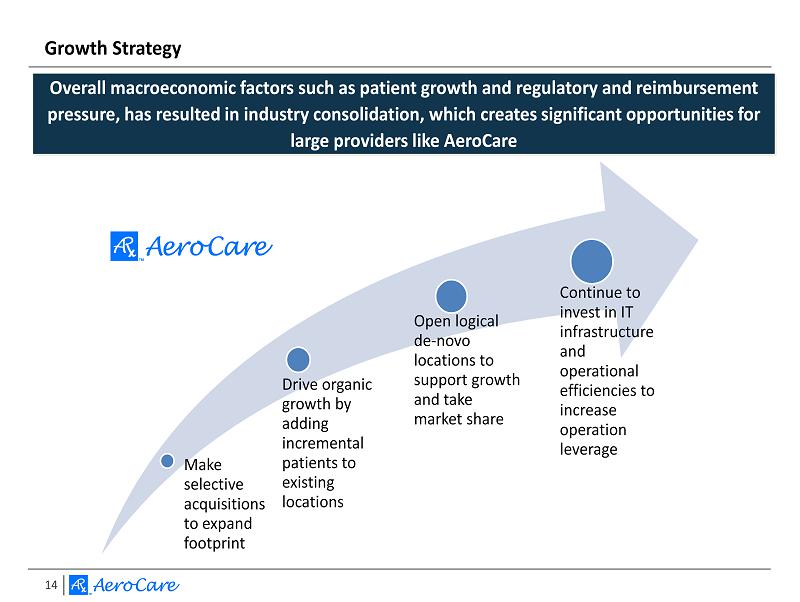

14 Make selective acquisitions to expand footprint Drive organic growth by adding incremental patients to existing locations Open logical de - novo locations to support growth and take market share Continue to invest in IT infrastructure and operational efficiencies to increase operation leverage Growth Strategy Overall macroeconomic factors such as patient growth and regulatory and reimbursement pressure, has resulted in industry consolidation , which creates significant opportunities for large providers like AeroCare 14

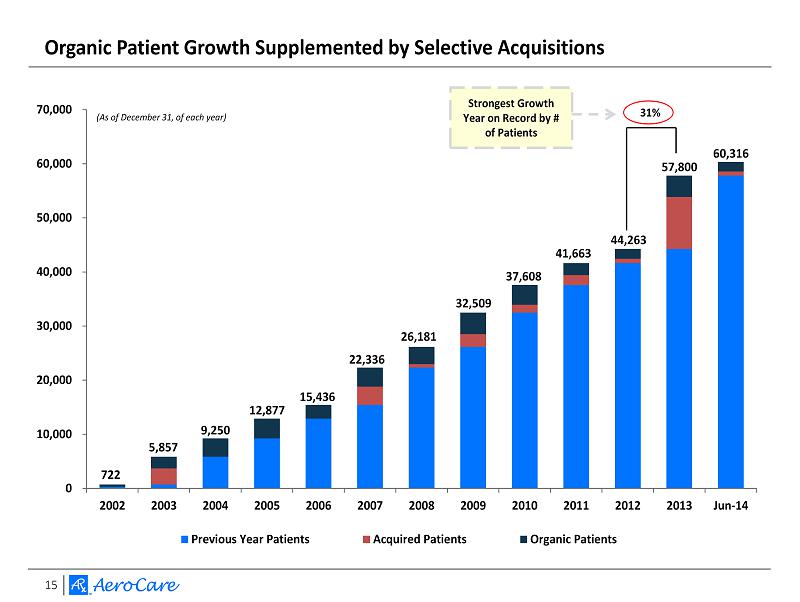

15 Organic Patient Growth Supplemented by Selective Acquisitions 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Jun-14 Previous Year Patients Acquired Patients Organic Patients 722 15,436 44,263 22,336 26,181 32,509 37,608 41,663 57,800 12,877 9,250 5,857 Strongest Growth Year on Record by # of Patients 60,316 31% (As of December 31, of each year)

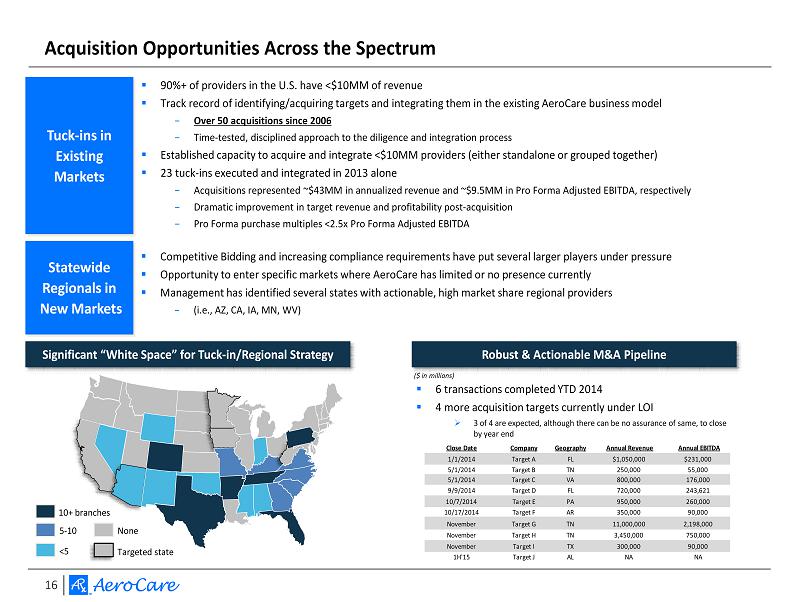

16 ▪ 90%+ of providers in the U.S. have <$10MM of revenue ▪ Track record of identifying/acquiring targets and integrating them in the existing AeroCare business model − Over 50 acquisitions since 2006 − Time - tested, disciplined approach to the diligence and integration process ▪ Established capacity to acquire and integrate <$10MM providers (either standalone or grouped together) ▪ 23 tuck - ins executed and integrated in 2013 alone − Acquisitions represented ~$43MM in annualized revenue and ~$9.5MM in Pro Forma Adjusted EBITDA, respectively − Dramatic improvement in target revenue and profitability post - acquisition − Pro Forma purchase multiples <2.5x Pro Forma Adjusted EBITDA Acquisition Opportunities Across the Spectrum Tuck - ins in Existing Markets Statewide Regionals in New Markets ▪ Competitive Bidding and increasing compliance requirements have put several larger players under pressure ▪ Opportunity to enter specific markets where AeroCare has limited or no presence currently ▪ Management has identified several states with actionable, high market share regional providers − (i.e ., AZ, CA, IA, MN, WV) Significant “White Space” for Tuck - in/Regional Strategy 10+ branches 5 - 10 <5 None Targeted state Robust & Actionable M&A Pipeline ▪ 6 transactions completed YTD 2014 ▪ 4 more acquisition targets currently under LOI » 3 of 4 are expected, although there can be no assurance of same, to close by year end ($ in millions) Close Date Company Geography Annual Revenue Annual EBITDA 1/1/2014 Target A FL $1,050,000 $231,000 5/1/2014 Target B TN 250,000 55,000 5/1/2014 Target C VA 800,000 176,000 9/9/2014 Target D FL 720,000 243,621 10/7/2014 Target E PA 950,000 260,000 10/17/2014 Target F AR 350,000 90,000 November Target G TN 11,000,000 2,198,000 November Target H TN 3,450,000 750,000 November Target I TX 300,000 90,000 1H'15 Target J AL NA NA

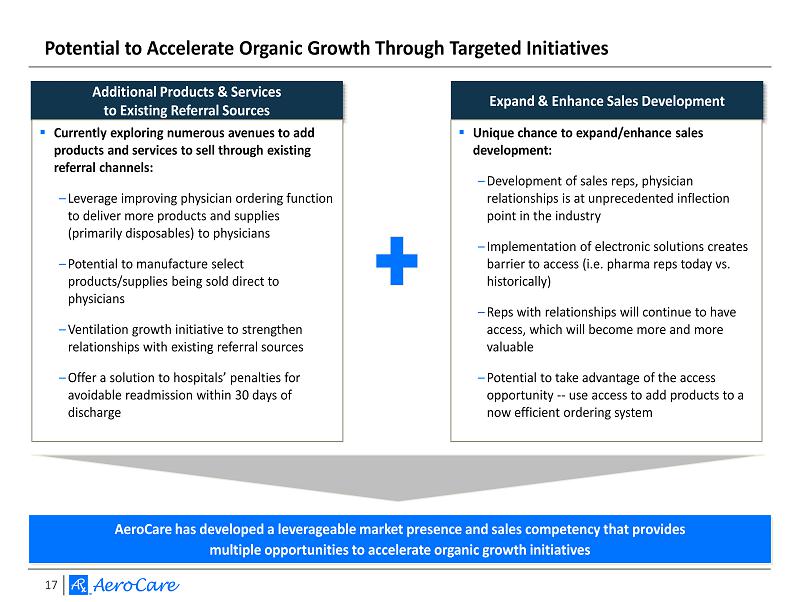

17 Potential to Accelerate Organic Growth Through Targeted Initiatives Additional Products & Services to Existing Referral Sources ▪ Currently exploring numerous avenues to add products and services to sell through existing referral channels: – Leverage improving physician ordering function to deliver more products and supplies (primarily disposables) to physicians – Potential to manufacture select products/supplies being sold direct to physicians – V entilation growth initiative to strengthen relationships with existing referral sources – Offer a solution to hospitals’ penalties for avoidable readmission within 30 days of discharge Expand & Enhance Sales Development ▪ Unique chance to expand/enhance sales development: – Development of sales reps, physician relationships is at unprecedented inflection point in the industry – Implementation of electronic solutions creates barrier to access (i.e. pharma reps today vs. historically) – Reps with relationships will continue to have access, which will become more and more valuable – Potential to take advantage of the access opportunity -- use access to add products to a now efficient ordering system AeroCare has developed a leverageable market presence and sales competency that provides multiple opportunities to accelerate organic growth initiatives

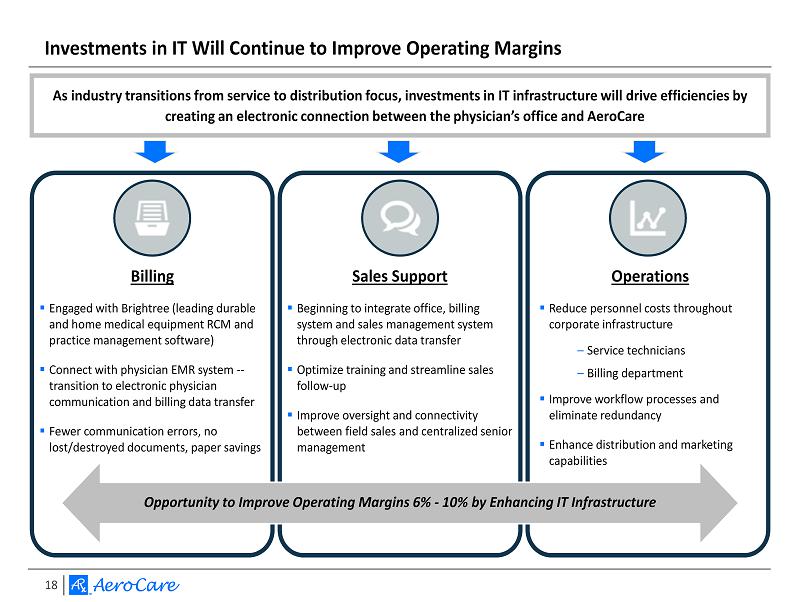

18 Investments in IT Will Continue to Improve Operating Margins Billing ▪ Engaged with Brightree (leading durable and home medical equipment RCM and practice management software) ▪ Connect with physician EMR system -- transition to electronic physician communication and billing data transfer ▪ Fewer communication errors, no lost/destroyed documents, paper savings Sales Support ▪ Beginning to integrate office, billing system and sales management system through electronic data transfer ▪ Optimize training and streamline sales follow - up ▪ Improve oversight and connectivity between field sales and centralized senior management Operations ▪ Reduce personnel costs throughout corporate infrastructure – Service technicians – Billing department ▪ Improve workflow processes and eliminate redundancy ▪ Enhance distribution and marketing capabilities As industry transitions from service to distribution focus, investments in IT infrastructure will drive efficiencies by creating an electronic connection between the physician’s office and AeroCare Opportunity to Improve Operating Margins 6% - 10% by Enhancing IT Infrastructure

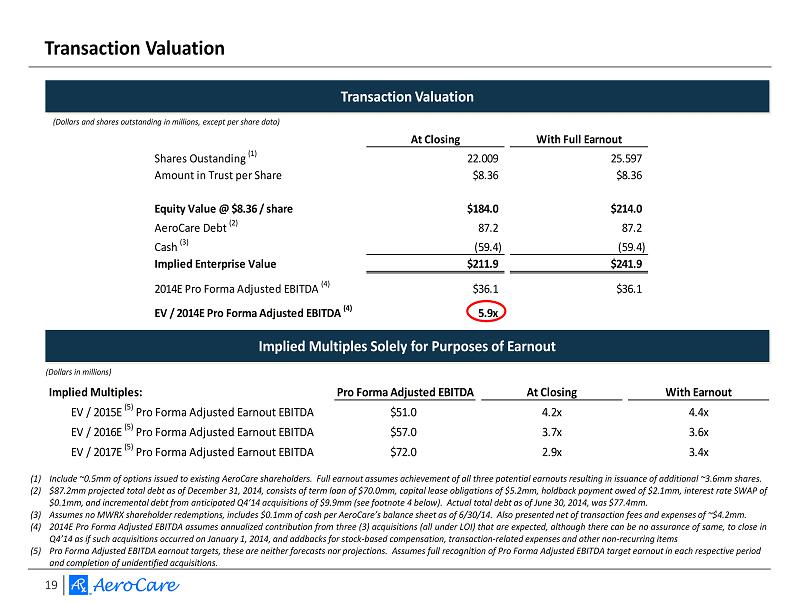

19 At Closing With Full Earnout Shares Oustanding (1) 22.009 25.597 Amount in Trust per Share $8.36 $8.36 Equity Value @ $8.36 / share $184.0 $214.0 AeroCare Debt (2) 87.2 87.2 Cash (3) (59.4) (59.4) Implied Enterprise Value $211.9 $241.9 2014E Pro Forma Adjusted EBITDA (4) $36.1 $36.1 EV / 2014E Pro Forma Adjusted EBITDA (4) 5.9x 6.7x Transaction Valuation Transaction Valuation Implied Multiples Solely for Purposes of Earnout (1) I nclude ~ 0 . 5 mm of options issued to existing AeroCare shareholders . Full earnout assumes achievement of all three potential earnouts resulting in issuance of additional ~ 3 . 6 mm shares . (2) $ 87 . 2 mm projected total debt as of December 31 , 2014 , consists of term loan of $ 70 . 0 mm, capital lease obligations of $ 5 . 2 mm, holdback payment owed of $ 2 . 1 mm, interest rate SWAP of $ 0 . 1 mm, and incremental debt from anticipated Q 4 ’ 14 acquisitions of $ 9 . 9 mm (see footnote 4 below) . Actual total debt as of June 30 , 2014 , was $ 77 . 4 mm . (3) Assumes no MWRX shareholder redemptions, includes $ 0 . 1 mm of cash per AeroCare’s balance sheet as of 6 / 30 / 14 . Also presented net of transaction fees and expenses of ~ $ 4 . 2 mm . (4) 2014 E Pro Forma Adjusted EBITDA assumes annualized contribution from three ( 3 ) acquisitions (all under LOI) that are expected, although there can be no assurance of same , to close in Q 4 ’ 14 as if such acquisitions occurred on January 1 , 2014 , and addbacks for stock - based compensation, transaction - related expenses and other non - recurring items ( 5 ) Pro Forma Adjusted EBITDA earnout targets, these are neither forecasts nor projections . Assumes full recognition of Pro Forma Adjusted EBITDA target earnout in each respective period and completion of unidentified acquisitions . (Dollars and shares outstanding in millions, except per share data) (Dollars in millions) Implied Multiples: Pro Forma Adjusted EBITDA At Closing With Earnout EV / 2015E (5) Pro Forma Adjusted Earnout EBITDA $51.0 4.2x 4.4x EV / 2016E (5) Pro Forma Adjusted Earnout EBITDA $57.0 3.7x 3.6x EV / 2017E (5) Pro Forma Adjusted Earnout EBITDA $72.0 2.9x 3.4x

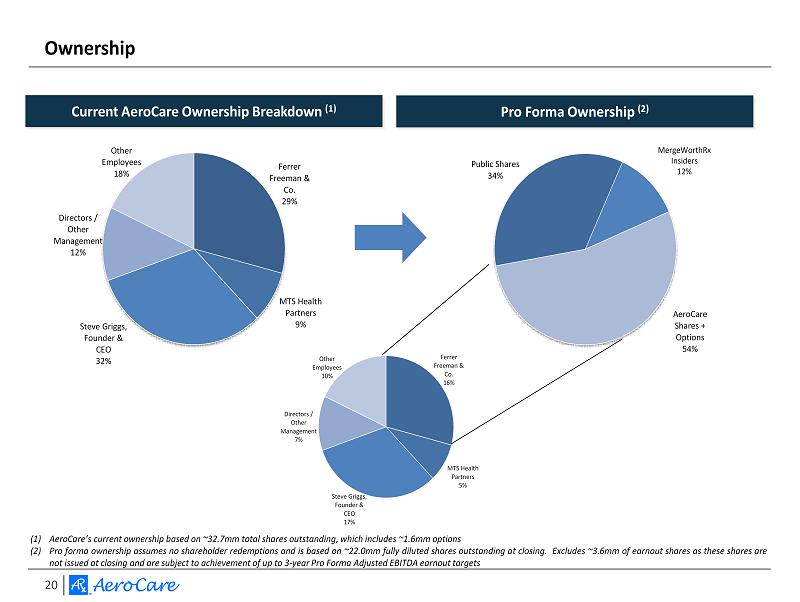

20 Ferrer Freeman & Co. 29% MTS Health Partners 9% Steve Griggs, Founder & CEO 32% Directors / Other Management 12% Other Employees 18% Public Shares 34% MergeWorth Rx Insiders 12% AeroCare Shares + Options 54% Ferrer Freeman & Co. 16% MTS Health Partners 5% Steve Griggs, Founder & CEO 17% Directors / Other Management 7% Other Employees 10% Ownership Current AeroCare Ownership Breakdown (1) Pro Forma Ownership (2) (1) AeroCare’s current ownership based on ~ 32 . 7 mm total shares outstanding, which includes ~ 1 . 6 mm options (2) Pro forma ownership assumes no shareholder redemptions and is based on ~ 22 . 0 mm fully diluted shares outstanding at closing . Excludes ~ 3 . 6 mm of earnout shares as these shares are not issued at closing and are subject to achievement of up to 3 - year Pro Forma Adjusted EBITDA earnout targets MergeWorthRx Insiders 12%

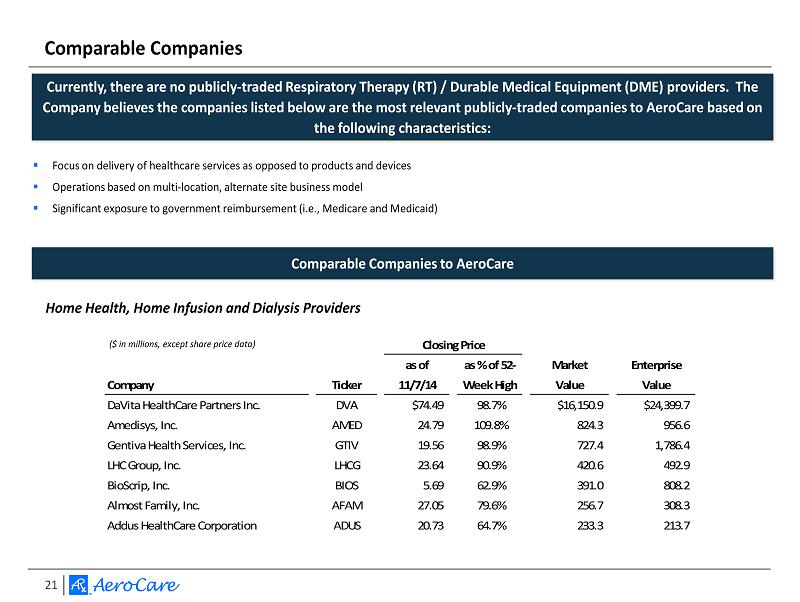

21 Closing Price as of as % of 52- Market Enterprise Company Ticker 11/7/14 Week High Value Value DaVita HealthCare Partners Inc. DVA $74.49 98.7% $16,150.9 $24,399.7 Amedisys, Inc. AMED 24.79 109.8% 824.3 956.6 Gentiva Health Services, Inc. GTIV 19.56 98.9% 727.4 1,786.4 LHC Group, Inc. LHCG 23.64 90.9% 420.6 492.9 BioScrip, Inc. BIOS 5.69 62.9% 391.0 808.2 Almost Family, Inc. AFAM 27.05 79.6% 256.7 308.3 Addus HealthCare Corporation ADUS 20.73 64.7% 233.3 213.7 Comparable Companies Comparable Companies to AeroCare Home Health, Home Infusion and Dialysis Providers ▪ Focus on delivery of healthcare services as opposed to products and devices ▪ Operations based on multi - location, alternate site business model ▪ Significant exposure to government reimbursement (i.e., Medicare and M edicaid) ($ in millions, except share price data) Currently , there are no publicly - traded Respiratory Therapy (RT) / Durable Medical Equipment (DME) providers. The Company believes the companies listed below are the most relevant publicly - traded companies to AeroCare based on the following characteristics :

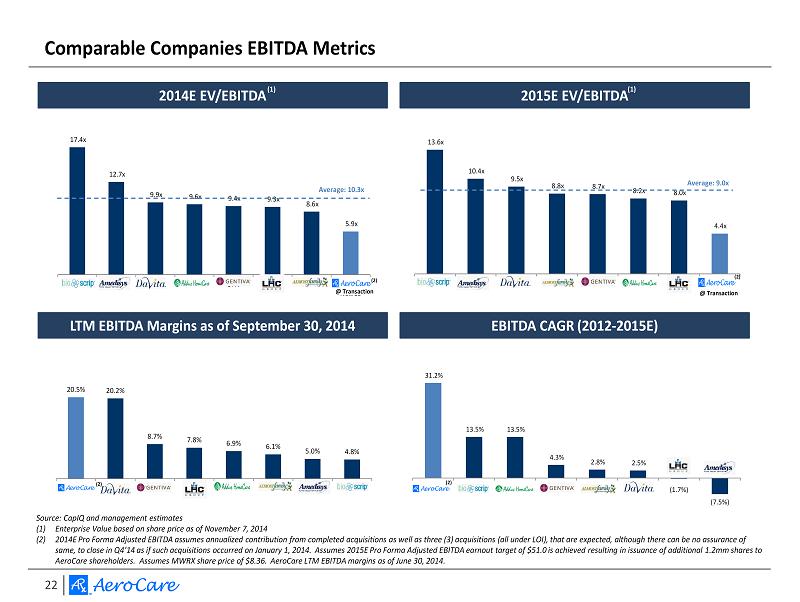

22 17.4x 12.7x 9.9x 9.6x 9.4x 9.3x 8.6x 5.9x BIOS AMED DVA ADUS GTIV LHCG AFAM AeroCare NewCo 31.2% 13.5% 13.5% 4.3% 2.8% 2.5% (1.7%) (7.5%) 20.5% 20.2% 8.7% 7.8% 6.9% 6.1% 5.0% 4.8% AeroCare DVA GTIV LHCG ADUS AFAM AMED BIOS 13.6x 10.4x 9.5x 8.8x 8.7x 8.2x 8.0x 4.4x BIOS AMED DVA AFAM GTIV ADUS LHCG AeroCare NewCo Comparable Companies EBITDA Metrics Source: CapIQ and management estimates (1) Enterprise Value based on share price as of November 7, 2014 (2) 2014E Pro Forma Adjusted EBITDA assumes annualized contribution from completed acquisitions as well as three (3) acquisitions (all under LOI), that are expected, although there can be no assurance of same, to close in Q4’14 as if such acquisitions occurred on January 1, 2014. Assumes 2015E Pro Forma Adjusted EBITDA earnout target of $51.0 is achieved resulting in issuance of additional 1.2mm shares to AeroCare shareholders. Assumes MWRX share price of $8.36. AeroCare LTM EBITDA margins as of June 30, 2014. 2014E EV/EBITDA 2015E EV/EBITDA LTM EBITDA Margins as of September 30, 2014 EBITDA CAGR (2012 - 2015E) (1) (1) (2) (2) Average: 9.0x (2) @ Transaction Average: 10.3x @ Transaction (2)

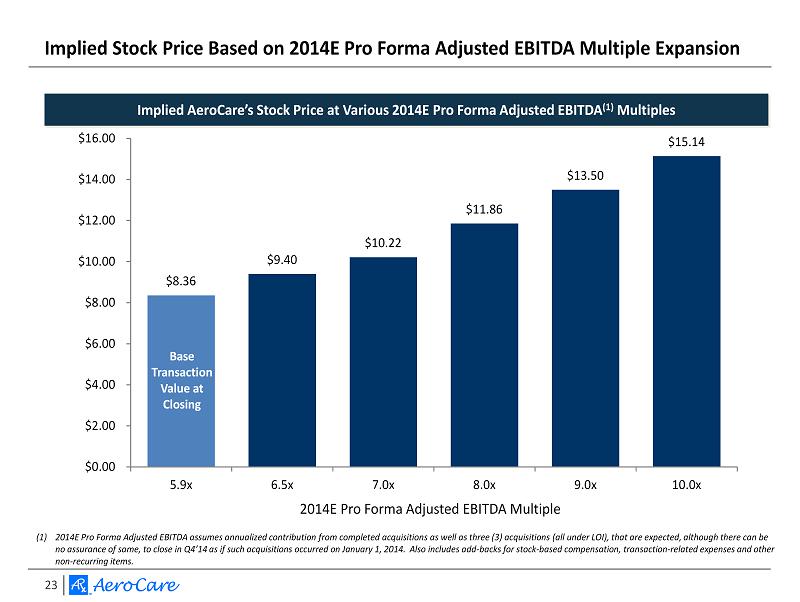

23 $8.36 $9.40 $10.22 $11.86 $13.50 $15.14 $0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 5.9x 6.5x 7.0x 8.0x 9.0x 10.0x (1) 2014E Pro Forma Adjusted EBITDA assumes annualized contribution from completed acquisitions as well as three (3) acquisitions (all under LOI), that are expected, although there can be no assurance of same, to close in Q4’14 as if such acquisitions occurred on January 1, 2014. Also includes add - backs for stock - based compensation, transaction - related expenses and other non - recurring items. Implied Stock Price Based on 2014E Pro Forma Adjusted EBITDA Multiple Expansion Implied AeroCare’s Stock Price at Various 2014E Pro Forma Adjusted EBITDA (1) Multiples Base Transaction Value at Closing 2014E Pro Forma Adjusted EBITDA Multiple

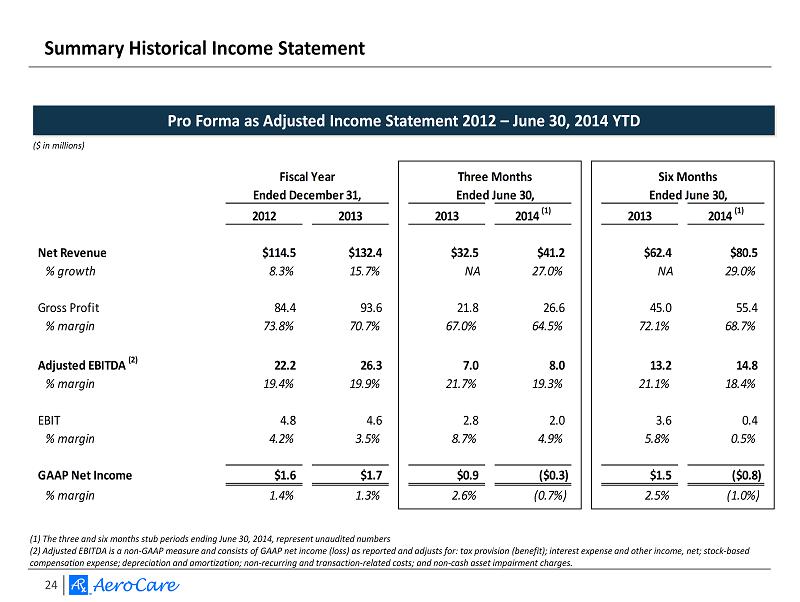

24 Summary Historical Income Statement Pro Forma as Adjusted Income Statement 2012 – June 30, 2014 YTD ($ in millions) (1) The three and six months stub periods ending June 30, 2014, represent unaudited numbers (2) Adjusted EBITDA is a non - GAAP measure and consists of GAAP net income (loss) as reported and adjusts for: tax provision (benefit ); interest expense and other income, net; stock - based compensation expense; depreciation and amortization; non - recurring and transaction - related costs; and non - cash asset impairment charges. Fiscal Year Three Months Six Months Ended December 31, Ended June 30, Ended June 30, 2012 2013 2013 2014 (1) 2013 2014 (1) Net Revenue $114.5 $132.4 $32.5 $41.2 $62.4 $80.5 % growth 8.3% 15.7% NA 27.0% NA 29.0% Gross Profit 84.4 93.6 21.8 26.6 45.0 55.4 % margin 73.8% 70.7% 67.0% 64.5% 72.1% 68.7% Adjusted EBITDA (2) 22.2 26.3 7.0 8.0 13.2 14.8 % margin 19.4% 19.9% 21.7% 19.3% 21.1% 18.4% EBIT 4.8 4.6 2.8 2.0 3.6 0.4 % margin 4.2% 3.5% 8.7% 4.9% 5.8% 0.5% GAAP Net Income $1.6 $1.7 $0.9 ($0.3) $1.5 ($0.8) % margin 1.4% 1.3% 2.6% (0.7%) 2.5% (1.0%)

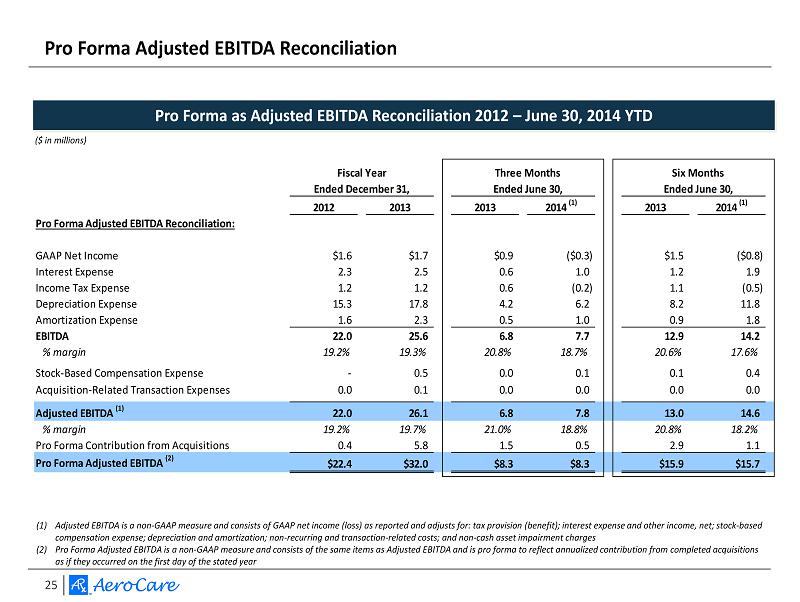

25 Pro Forma Adjusted EBITDA Reconciliation Pro Forma as Adjusted EBITDA Reconciliation 2012 – June 30, 2014 YTD ($ in millions) (1) Adjusted EBITDA is a non - GAAP measure and consists of GAAP net income (loss) as reported and adjusts for: tax provision (benefit); intere st expense and other income, net; stock - based compensation expense; depreciation and amortization; non - recurring and transaction - related costs; and non - cash asset impairment charges (2) Pro Forma Adjusted EBITDA is a non - GAAP measure and consists of the same items as Adjusted EBITDA and is pro forma to reflect an nualized contribution from completed acquisitions as if they occurred on the first day of the stated year Fiscal Year Three Months Six Months Ended December 31, Ended June 30, Ended June 30, 2012 2013 2013 2014 (1) 2013 2014 (1) Pro Forma Adjusted EBITDA Reconciliation: GAAP Net Income $1.6 $1.7 $0.9 ($0.3) $1.5 ($0.8) Interest Expense 2.3 2.5 0.6 1.0 1.2 1.9 Income Tax Expense 1.2 1.2 0.6 (0.2) 1.1 (0.5) Depreciation Expense 15.3 17.8 4.2 6.2 8.2 11.8 Amortization Expense 1.6 2.3 0.5 1.0 0.9 1.8 EBITDA 22.0 25.6 6.8 7.7 12.9 14.2 % margin 19.2% 19.3% 20.8% 18.7% 20.6% 17.6% Stock-Based Compensation Expense - 0.5 0.0 0.1 0.1 0.4 Acquisition-Related Transaction Expenses 0.0 0.1 0.0 0.0 0.0 0.0 Adjusted EBITDA (1) 22.0 26.1 6.8 7.8 13.0 14.6 % margin 19.2% 19.7% 21.0% 18.8% 20.8% 18.2% Pro Forma Contribution from Acquisitions 0.4 5.8 1.5 0.5 2.9 1.1 Pro Forma Adjusted EBITDA (2) $22.4 $32.0 $8.3 $8.3 $15.9 $15.7

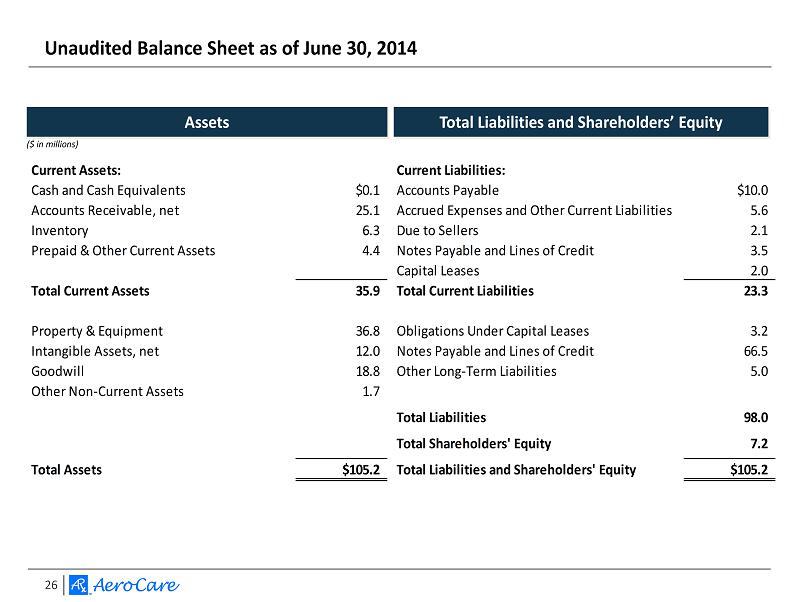

26 Assets Total Liabilities and Shareholders’ Equity Unaudited Balance Sheet as of June 30, 2014 Current Assets: Cash and Cash Equivalents $0.1 Accounts Receivable, net 25.1 Inventory 6.3 Prepaid & Other Current Assets 4.4 Total Current Assets 35.9 Property & Equipment 36.8 Intangible Assets, net 12.0 Goodwill 18.8 Other Non-Current Assets 1.7 Total Assets $105.2 Current Liabilities: Accounts Payable $10.0 Accrued Expenses and Other Current Liabilities 5.6 Due to Sellers 2.1 Notes Payable and Lines of Credit 3.5 Capital Leases 2.0 Total Current Liabilities 23.3 Obligations Under Capital Leases 3.2 Notes Payable and Lines of Credit 66.5 Other Long-Term Liabilities 5.0 Total Liabilities 98.0 Total Shareholders' Equity 7.2 Total Liabilities and Shareholders' Equity $105.2 ($ in millions)