UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K/A

Amendment No. 2

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): September 24, 2013

NANOFLEX POWER CORPORATION |

| (Exact name of registrant as specified in its charter) |

| Florida | | 333-187308 | | 46-1904002 |

(State or other jurisdiction of incorporation) | | (Commission File Number) | | (IRS Employer Identification No.) |

| | 17207 N. Perimeter Dr., Suite 210 Scottsdale, AZ 85255 | |

| | (Address of Principal Executive Offices) | |

(former name or former address, if changed since last report)

Registrant’s telephone number, including area code: 609-654-8839

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Forward Looking Statements

This Current Report on Form 8-K/A and other reports filed by registrant from time to time with the Securities and Exchange Commission (collectively, the “Filings”) contain or may contain forward-looking statements and information that is based upon beliefs of, and information currently available to, registrant’s management, as well as estimates and assumptions made by registrant’s management. When used in the Filings, the words “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “plan” or the negative of these terms and similar expressions as they relate to registrant or registrant’s management identify forward-looking statements. Such statements reflect the current view of registrant with respect to future events and are subject to risks, uncertainties, assumptions and other factors relating to the Company’s industry, operations and results of operations. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this Current Report on Form 8-K. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this Current Report on Form 8-K/A to conform our statements to actual results or changed expectations, or the results of any revision to these forward-looking statements.

Except as otherwise indicated by the context, references in this Report to:

| | ● | The “Company,” “we,” “us,” or “our,” are references to the combined business of (i) NanoFlex Power Corporation (formerly, Universal Technology Systems Corp., a Florida corporation (“UTCH”)) and (ii) Global Photonic Energy Corporation, a Pennsylvania corporation (“GPEC”); |

| | | |

| | ● | “Common Stock” refers to the common stock, par value $.0001, of the Company; |

| | | |

| | ● | “U.S. dollar,” “$” and “US$” refer to the legal currency of the United States; |

| | | |

| | ● | “Securities Act” refers to the Securities Act of 1933, as amended; and |

| | | |

| | ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

Item 1.01 Entry Into A Material Definitive Agreement

Share Exchange Agreement

On September 24, 2013, the Company, Global Photonic Energy Corporation, a Pennsylvania corporation (“GPEC”) and GPEC Holdings, Inc., which owns 100% of the total outstanding equity interests of GPEC (the “GPEC Stockholder”) entered into and consummated transactions pursuant to a Share Exchange Agreement (the “Share Exchange Agreement,” such transaction referred to as the “Share Exchange Transaction”), whereby the Company issued to the GPEC Stockholder an aggregate of 15,500,640 shares of its common stock, par value $.0001 (“Common Stock”), in exchange for 100% of the equity interests of GPEC held by the GPEC Stockholder.

In addition, the Company agreed under the Share Exchange Agreement to issue the following securities as a result of the Share Exchange Transaction:

(i) a total of 5,780,500 shares of Common Stock and warrants to purchase a total of 5,780,500 shares of Common Stock to holders of the Series A Convertible Preferred Stock of GPEC (the “GPEC Series A Preferred”) as a result of the automatic conversion of the GPEC Series A Preferred;

(ii) a total of 11,433,200 shares of Common Stock and warrants to purchase a total of 11,433,200 shares of Common Stock to holders of the Convertible Promissory Notes of GPEC (the “GPEC Bridge Notes”) issued in July 2013 by GPEC in a bridge financing (the “Bridge Financing”) as a result of the automatic conversion of the GPEC Bridge Notes;

(iii) warrants to purchase 1,875,783 shares of Common Stock to holders of all of the issued and outstanding warrants of GPEC (“GPEC Warrants”) in consideration of the cancellation of such GPEC Warrants pursuant to the terms and conditions thereof; and

(iv) options to purchase 105,000 shares of Common Stock to holders of all of the issued and outstanding options of GPEC (“GPEC Options”) in consideration of the cancellation of such GPEC Options pursuant to the terms and conditions thereof.

As a result of the Share Exchange Transaction, GPEC became a wholly-owned subsidiary of the Company.

The Share Exchange Agreement contains representations and warranties by us, GPEC and the GPEC Stockholder which are customary for transactions of this type such as, with respect to the Company: organization, good standing and qualification to do business; capitalization; subsidiaries; authorization and validity of the transaction and transaction documents; consents being obtained or not required to consummate the transaction; no conflict or violation of Articles of Incorporations and By-laws, with respect to GPEC: authorization; capitalization; and title to GPEC’s common stock being exchanged and other equity interests being cancelled, and with respect to GPEC Stockholder: authorization; no conflict or violation of law; investment purpose; accredited investor status; reliance on exemption on the Company’s Common Stock to be exchanged; and transfer or resale pursuant to the Securities Act.

Our acquisition of GPEC pursuant to the Share Exchange Agreement was accounted for as a reverse merger and recapitalization effected by a share exchange. GPEC is considered the acquirer for accounting and financial reporting purposes. The assets and liabilities of the acquired entity have been brought forward at their book value and no goodwill has been recognized.

Private Placement of Common Stock

On September 22, 2013 the Company accepted subscriptions to purchase from, and issued an aggregate of 5,049,113 shares of its Common Stock (or 6,058,936 shares of Common Stock after given effect to the Forward Split, as defined below) to seven accredited investors. The shares were issued pursuant to separate Subscription Agreements between the Company and each purchaser. The Company made certain representations to the subscribers in the Subscription Agreements regarding the capitalization of the Company and the authorization and enforceability of the agreement and the subscribers made certain representations to the Company regarding the suitability of the sale of the Common Stock to the subscribers.

Forward Split and Name Change

On October 30, 2013, the board of directors of the Company as well as shareholders of the Company holding a majority of votes approved and ratified: (i) a 1.2-for-1 forward split of the Company’s Common Stock effective as of September 23, 2013 (the “Forward Split”), and (ii) change of the Company’s corporate name to “NanoFlex Power Corporation” (the “Name Change”). Financial Industry Regulatory Authority (“FINRA”) approved the Forward Split and the Name Change to be effective as of November 25, 2013. Unless otherwise indicated, all references to numbers of shares of Common Stock in this Current Report have given effect to the Forward Split.

Item 2.01 Completion of Acquisition or Disposition of Assets

OUR CORPORATE STRUCTURE

UTCH is a Florida corporation incorporated on January 28, 2013. Following the acquisition of GPEC, GPEC became our direct wholly-owned subsidiary effective on September 24, 2013.

The following diagram sets forth the structure of the Company as of the date of this Report:

Organizational History of GPEC

GPEC was incorporated on February 7, 1994 in the State of Pennsylvania to fund, develop and commercialize photonic energy conversion and storage technologies utilizing organic semiconductors for the production of electricity (i.e., converting incident light energy into electric current) based on the research of Dr. Mark E. Thompson, then a professor at Princeton University.

On September 10, 2013, GPEC incorporated in Pennsylvania a wholly-owned subsidiary, GPEC Holdings, Inc., which later formed GPEC Sub, Inc. (“GPEC Sub”). In September 2013, GPEC consummated a short-form merger, in which GPEC Sub was merged into GPEC, GPEC Sub ceased to exist and GPEC became a wholly-owned subsidiary of GPEC Holdings, Inc. The purpose of this restructuring was to prepare GPEC to be acquired by the Company.

On September 24, 2013, as a result of the Share Exchange Transaction discussed in Item 1.01, GPEC became a wholly-owned subsidiary of the Company.

OUR BUSINESS

General

GPEC was founded and incorporated in February 1994 and is engaged in the development, commercialization, and licensing of advanced thin film solar technologies and intellectual property. Since then, GPEC’s sponsored research programs at Princeton University, University of Southern California (“USC”) and the University of Michigan (“Michigan”) have resulted in more than 600 issued or pending patents worldwide covering materials, architectures, and fabrication processes for organic and inorganic flexible, thin-film photovoltaic technologies. The technology is targeted at, but not limited to, certain broad applications, including (a) mobile electronic device power, (b) electric vehicle charging or “power paint,” (c) semi-transparent solar power generating windows or glazing and (d) traditional off-grid and grid-connected solar power generation. Laboratory feasibility prototypes have been developed that successfully demonstrate key building block principles for these technology application areas.

Research and License Agreements

On October 22, 1993, American Biomimetics Corporation (“ABC”) entered into a Sponsored Research Agreement and License Agreement with Princeton University for work being done in the laboratory of Dr. Mark E. Thompson. In August 1995, this original sponsored research agreement with Princeton University was assigned to USC when Dr. Thompson accepted a position at USC. In August of 1996, ABC assigned to GPEC its rights to various research inventions under the foregoing agreements. On May 1, 1998, GPEC, Princeton University and USC entered into a new Sponsored Research Agreement (“1998 Sponsored Research Agreement”), which continued without interruption the research of Dr. Thompson (at USC) and added to it the research being done by Dr. Stephen R. Forrest (at Princeton University). At the same time, the parties entered into a License Agreement (the “1998 License Agreement”) which they considered an amendment of the earlier license agreement. This 1998 Sponsored Research Agreement formed the basis for future renewals of this agreement in 2004, 2006 and 2009 (together with such amendments, extensions and renewals referred to as the “Research Agreement”). From May 1, 2009 through June 30, 2013 GPEC paid and expensed $3,233,341 under the Research Agreement.

In 2006, the Company’s remaining principal researcher at Princeton University, Dr. Stephen R. Forrest, accepted a tenured position at the University of Michigan and became its Vice President of Research. The University of Southern California Research Agreement, dated January 1, 2006 (the “2006 Research Agreement”) is the renewal of the 1998 Sponsored Research Agreement and it retained the Company’s relationship with Dr. Thompson and his team, and established USC as the lead researcher and Michigan as the subcontractor. In addition, the 1998 License Agreement was also amended in 2006 (the “License Agreement 2006 Amendment”) to include University of Michigan, where Dr. Forrest has been conducting research for GPEC.

Currently, research and development of GPEC’s flexible, thin-film organic photovoltaic (“OPV”) and inorganic Gallium Arsenide (“GaAs”) technologies is being conducted at USC and the University of Michigan under the five year Sponsored Research Agreement dated May 1, 2009. Under the Sponsored Research Agreement, GPEC has agreed to pay USC up to $6,338,341 for work to be performed. From May 1, 2009 through December 31, 2012 GPEC paid and expensed $2,689,570 under this agreement. During the years ended December 31, 2010, December 31, 2011 and December 31, 2012, GPEC incurred research and development costs of $463,211, $887,097 and $998,127, respectively, and patent application expenses and prosecution fees of $1,352,072, $1,587,642 and $1,345,743, respectively.

Under the currently effective License Agreement, as amended, with USC, Princeton and the University of Michigan, wherein GPEC has obtained the exclusive worldwide license and right to sublicense any and all intellectual property resulting from GPEC’s sponsored research agreements, GPEC has agreed to pay for all reasonable and necessary out of pocket expenses incurred in the preparation, filing, maintenance, renewal and continuation of patent applications designated by GPEC. In addition, GPEC is required to pay to USC 5% of net sales of licensed products or licensed processes used, leased or sold by GPEC, 3% of revenues received by GPEC from the sublicensing of patent rights and 23% of revenues (net of costs and expenses, including legal fees) received by GPEC from final judgments in infringement actions respecting the patent rights licensed under the agreement.

GPEC has an exclusive worldwide license and rights to sublicense any and all intellectual property conceived or developed under its sponsorship at USC, Princeton University and the University of Michigan. There is currently no ongoing research activity at Princeton University related to GPEC, although the Company maintains licensing rights to technology previously developed there.

The foregoing description of the 1998 Sponsored Research Agreement, the 1998 License Agreement, the 2006 Research Agreement and the License Agreement 2006 Amendment is qualified in entirety by the respective agreements that are annexed hereto.

Founding Researchers

Dr. Stephen R. Forrest (University of Michigan)

Professor Stephen R. Forrest has been working with GPEC since 1998 under the Company's Sponsored Research Program with Princeton University, USC, and Michigan. Professor Forrest is one of the Company's Founding Research Scientists; his focus is on organic and GaAs photovoltaics. In 2006, he rejoined the University of Michigan as Vice President for Research, and as the William Gould Dow Collegiate Professor in Electrical Engineering, Materials Science and Engineering, and Physics. A Fellow of the APS, IEEE and OSA and a member of the National Academy of Engineering, he received the IEEE/LEOS Distinguished Lecturer Award in 1996-97, and in 1998 he was co-recipient of the IPO National Distinguished Inventor Award as well as the Thomas Alva Edison Award for innovations in organic LEDs. In 1999, Professor Forrest received the MRS Medal for work on organic thin films. In 2001, he was awarded the IEEE/LEOS William Streifer Scientific Achievement Award for advances made on photodetectors for optical communications systems. In 2006 he received the Jan Rajchman Prize from the Society for Information Display for invention of phosphorescent OLEDs, and is the recipient of the 2007 IEEE Daniel Nobel Award for innovations in OLEDs. Professor Forrest has been honored by Princeton University establishing the Stephen R. Forrest Faculty Chair in Electrical Engineering in 2012. Professor Forrest has authored 525 papers in refereed journals, and has 247 patents. He is co-founder or founding participant in several companies and is on the Board of Directors of Applied Materials and PD-LD, Inc. He has also served from 2009-2012 as Chairman of the Board of Ann Arbor SPARK, the regional economic development organization, and serves on the Board of Governors of the Technion – Israel Institute of Technology, as well as the Vanderbilt University School of Engineering Board of Visitors. From 1979 to 1985, Professor Forrest worked at Bell Labs investigating photodetectors for optical communications. In 1992, Professor Forrest became the James S. McDonnell Distinguished University Professor of Electrical Engineering at Princeton University. He served as director of the National Center for Integrated Photonic Technology, and as Director of Princeton's Center for Photonics and Optoelectronic Materials (POEM). From 1997-2001, he served as the Chair of the Princeton’s Electrical Engineering Department. He was appointed the CSM Visiting Professor of Electrical Engineering at the National University of Singapore from 2004-2009. In 2011, Professor Forrest was named number 13 of the top 100 most influential material scientists in the world by Thomson-Reuters, based largely on his work with organic electronics. Professor Forrest is a graduate of the University of Michigan (MSc Physics, 1974 and PhD Physics, 1979) and the University of California at Berkeley (B.A. Physics, 1972).

Dr. Mark E. Thompson (University of Southern California)

Professor Mark E. Thompson has been working with GPEC since 1994 under the Company's Sponsored Research Program with Princeton University, USC and Michigan. Professor Thompson is a professor of Chemistry at USC. Professor Thompson, in conjunction with Professor Stephen R. Forrest, was instrumental in the discovery of phosphorescent materials central to the highly efficient OLED technology marketed by Universal Display Corporation (NASDAQ: PANL). In 2013, Professor Thompson was named a Fellow of the American Association for the Advancement of Science. In 2012, Professor Thompson received the prestigious Alexander von Humboldt Research Award. In 2011, Professor Thompson was named number 12 of the top 100 most influential chemists in the world by Thomson-Reuters, based largely on his work with organic electronics. In 2007, Professor Thompson was awarded USC’s Associate’s Award for Excellence in Research (given to one faculty member per year). In 2006, he was awarded the MRS Medal by the Materials Research Society, and in the same year, Professors Forrest and Thompson were the co-recipients of the Jan Rajchman Prize from the Society for Information Display. Both the MRS medal and the Rajchman Prize were based on the invention of phosphorescent OLEDs. In 1998, Professor Thompson was co-recipient of The Intellectual Property Owners Association National Distinguished Inventor Award as well as the Thomas Alva Edison Award for innovations in organic LEDs. Professor Thompson joined The University of Southern California in 1995, and from 2005 through 2008, he served as the Department of Chemistry Chairman at USC. From 1987 to 1995, Professor Thompson worked at Princeton University. From 1985 to 1987, Professor Thompson worked at Oxford University and was an S.E.R.C. Research Fellow. From 1983 to 1985, Professor Thompson worked at E.I. duPont de Nemours & Company as a Visiting Scientist. Professor Thompson has authored over 200 papers in refereed journals, and has 75 patents. Professor Thompson is a graduate of the California Institute of Technology (Ph.D. Inorganic Chemistry, 1985) and the University of California Berkley (B.S. Chemistry with honors, 1980).

Summary Business Description

GPEC is engaged in the development, commercialization, and licensing of advanced photovoltaic technologies and intellectual property. GPEC’s sponsored research programs have resulted in intellectual property portfolio consisting of more than 600 issued or pending patents worldwide covering materials, architectures, and fabrication processes for organic and inorganic flexible, thin-film photovoltaic technologies.We also believe its proprietary technologies can fundamentally change the traditional paradigm of solar energy conversion – from applications defined by the conventional constraints of fixed, heavy, rigid and expensive to applications that are highly mobile, lightweight, flexible and inexpensive. Since its inception, GPEC has invested more than $52 million in capital for operations and development activities. GPEC’s sponsored research activities have generated a patent portfolio of more than 600 issued or pending patents worldwide to which the Company has exclusive commercial rights. The patents cover architecture, processes and materials for flexible, thin-film OPV technologies and inorganic GaAs technologies. As of December 13, 2013, the Company had 61 issued patents, 45 pending non-provisional applications and 17 pending provisional applications in the U.S. In addition, the Company had a total of 165 issued patents, 385 pending patent applications and 20 pending PCT applications in countries and regions outside the U.S, including but not limited to Australia, Canada, China, European Patent Convention, Hong Kong, India, Japan, Korea and Taiwan. The duration of all the issued U.S. and foreign patents is 20 years from their respective first effective filing dates. Currently, the Company is preparing to enter the applied research and pre-commercialization stage for both of these technology platforms with the near-term goal of establishing a technology development center in Ann Arbor, Michigan, that will enable:

| | ● | The development and commercialization of advanced organic and inorganic thin film solar cell technologies, including proprietary materials, architectures, and fabrication processes, that have the potential to transform the industry. |

| | | |

| | ● | GPEC to enter partnerships with manufacturers. |

| | | |

| | ● | GPEC to generate early revenue from government grants in an accelerated two-year program. |

GPEC is currently at development stage and has not licensed any of its technologies. GPEC has incurred losses and has no revenue to date. GPEC’s auditors’ opinion stated that there is substantial doubt about the Company’s ability to continue as a going concern.

Philosophy and Approach

Today, the solar industry is at an inflection point. The cost of solar energy generation is now within reach of those costs incurred through use of fossil fuels. Yet, while the solar industry is showing significant year-on-year growth, the value proposition for solar has yet to achieve wide-spread adoption in the absence of significant government incentives.

We believe the value proposition for solar will become much more attractive as new technologies remove the traditional constraints of silicon-based solar solutions.

GPEC is focusing on two parallel technology efforts: (a) its inorganic GaAs manufacturing technologies aim to provide solar cell manufacturers with the capability of producing GaAs solar cells with ultra-high efficiencies at a cost per watt well below grid parity of $1 per watt; and (b) through its portfolio of OPV thin film solar technologies, it is committed to further developing and delivering highly efficient, low-cost solar energy solutions via a host of new applications to worldwide markets. These include extending and/or replacing batteries for mobile devices, solar paint for electric cars to extend battery life, building integrated photovoltaic (“BIPV”) products that include glass, roofing materials and siding, off-grid applications, and solar textiles that generate power. GPEC further believes that its technologies could eventually be able to provide utility-scale power, augmenting and/or replacing fossil fuels.

GPEC is not, and does not plan to be, a direct manufacturer of its technologies. Rather, it plans to license or sublicense its intellectual property to industry partners and customers. This business model is oriented around licensing and sublicensing processes and technologies to large, well-positioned commercial partners who can provide manufacturing and marketing capabilities to enable rapid commercial growth. This model is also intended to quickly establish GPEC as an important player in the solar industry with rapid, high-margin revenue growth. Potential partners include current manufacturers of solar technology and manufacturers of semiconductors or electronics that recognize GPEC’s solar technologies as a significant emerging opportunity.

In addition, GPEC believes that there are several avenues for early revenue generation that become possible with the establishment of its technology development center in Ann Arbor, Michigan, utilizing cost-effective leased facilities near the University of Michigan. First among these avenues is government funding. The National Aeronautic and Space Administration (“NASA”), the Department of Defense, and the Department of Energy all have interests in businesses that can deliver ultra-lightweight, high-efficiency technologies for space, mobile warfighter, and grid-deployment applications. GPEC believes that its technology development center can make GPEC highly competitive for both GaAs and organic solar cell grants.

GPEC also anticipates that advancements at the technology development center can attract other industry players to acquire early licenses to use GPEC intellectual property. Finally, new licenses and agreements will be made possible by ongoing technology development, especially that related to perfecting and broadening of GPEC’s intellectual property in high-efficiency, lightweight organic solar cells. The principal function of the facility will be to demonstrate GPEC’s ability to prototype its inorganic and organic solar cells utilizing its proprietary technologies.

Technologies

Although GPEC has two complementary technology platforms, their development is synergistic and we believe that progress within each platform leads to success in the other.

The first technology is our inorganic platform that is based on the inorganic GaAs semiconductor, which is currently in an advanced development stage. GaAs is the mainstay of many ultra-high performance electronic technologies used in cellular telephones and military applications. While the very highest single and multi-junction solar cell efficiencies (approximately 29% and 44%, respectively) are based on GaAs, they remain prohibitively expensive for mass markets and hence are only considered for specialty applications where performance and weight requirements outweigh cost considerations, such as space-borne applications. Broader market acceptance of GaAs-based solar technologies requires enormous cost reductions before widespread applications are realized. GPEC’s patented technology has the potential to enable these cost reductions.

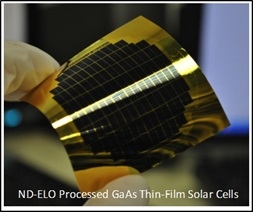

| | The primary cost in fabricating GaAs solar cells is the very high cost of the substrates on which the thin active region (called the epitaxial layers) is grown. These substrates, or “wafers,” cost approximately $20,000 per square meter. During the fabrication process that is currently in use, these expensive wafers are destroyed. For decades people have sought methods to eliminate the destruction or use of the wafer, using only the ultrathin solar cell active region. GPEC has developed a process for removing the active solar cell layer (approximately 2 micrometers thick, or around 1% of the thickness of a human hair) from the parent wafer on which it is grown in a completely non-destructive manner, thereby allowing for the re-use of the wafer an indefinite number of times without loss of performance on each growth and removal cycle. This process, called non-destructive epitaxial lift-off (“ND-ELOTM”), revolutionizes the cost structure of GaAs solar cell technology, converting the prohibitively expensive wafer cost from a recurring materials cost into a capital expenditure that is depreciated along with other equipment in the manufacturing facility. Furthermore, as part of the process, the ultrathin semiconductor is bonded to a flexible and thin secondary substrate such as plastic or metal foil using our adhesive-free, lightweight, ultra-strong and flexile process called cold-weld bonding. (See the solar cell production cycle shown in the figure on the left). |

The processes of ND-ELO™ and cold-weld bonding result in ultra-high efficiency solar cells—GPEC has achieved 23% in its researcher’s laboratories, and we believe that 29% is achievable. Moreover, the processes can be applied to multijunction cells with efficiencies of 42% or even higher if integrated with other electronic and optical device technologies. GPEC believes that its relatively simple processes can lead to dramatic improvements in the cost structure of solar energy conversion. The market for manufacturers which utilize GaAs technology is currently limited, but GPEC believes that it will expand as its Epitaxial Protection Layers (“EPL”), ND-ELO™, and Cold Weld processes allow cost reductions for manufacturers in their cost per watt that will permit these manufacturers to expand into areas and uses that were traditionally cost prohibitive. With the combination of GaAs’s high conversion efficiencies and the production cost reductions associated with utilizing our proprietary EPL, ND-ELO™, and Cold Weld processes, the costs of GaAs solar cells can approach cost-per-watt metrics associated with silicon-based solar cells. Moreover, GaAs cells provide functional and aesthetic advantages since they can be placed on flexible plastic, paper and other items that the current manufacturers using their technology are unable to incorporate today, as they are limited to rigid materials.

GPEC’s second, synergistic technology platform is based on flexible, thin-film OPV technologies that GPEC has researched and developed over the last two decades. Like GPEC’s GaAs technology, OPVs are extremely lightweight and, when deposited on flexible substrates, can be bent around small-radius cylinders for deployment in any number of applications, including in the generation of commodity power. These thin film technologies will allow power to be generated at the device level. A particular advantage of OPV technologies is the low cost of the materials used for the solar energy generating layers. Furthermore, the growth of the thin film layers can be accomplished directly onto the plastic or metal foils and therefore is no need for energy-intensive and expensive epitaxial growth required by inorganic semiconductors such as silicon or GaAs. Rather, there is the opportunity to “print” organic solar cells onto continuous rolls of plastic in an ultra-high-speed manufacturing process. The potential for printed electronics - making solar cells “by the kilometer” rather than on one substrate at a time - makes OPV a potentially revolutionary step in the widespread acceptance and deployment of solar energy. Since the organic films are lightweight and extremely thin (in this case the entire structure is only 0.1% the thickness of a human hair), they can be made semitransparent and adjusted to any desirable color. As a result, there are significant opportunities to achieve heretofore unrealizable applications such as car paint that allows vehicle coating to act as a source of power for an electric car; windows that can be coated with a clear semi-transparent film that captures photons from the sun to provide power for inside of the building, and fabric that can be made coated in order to make clothes, tents, flags, or lightweight roll-out power mats. One added advantage of OPVs over traditional semiconductor technologies is the very low energy intensity of their production. All of the fabrication temperatures are low and environmentally “green,” greatly reducing the ancillary costs required in conventional solar cell production.

GPEC’s approach has been to advance all dimensions of OPV technology, including the development of new materials (some of which are now being sold in small quantities by materials suppliers), new high efficiency device architectures, and ultra-high-speed, low-energy-cost production processes such as organic vapor phase deposition developed in GPEC’s researcher’s laboratories, and solar cell modulization. An example of an organic solar cell module is shown in the below photograph of an array of 24 OPVs on glass substrate.

In summary, GPEC is pursuing two solar cell technologies that break completely from traditional approaches in both cost and profile, allowing it to address established application spaces of commodity and spot energy generation, while opening up new opportunities that allow for migration of solar power generation into entirely new applications where flexible, lightweight form factors and low costs are demanded. GPEC holds extensive foundational intellectual property in both technologies with more than 600 issued or pending patents worldwide.

Intellectual Property

As of December 13, 2013, the Company had 61 issued patents, 45 pending non-provisional applications and 17 pending provisional applications in the U.S. In addition, the Company had a total of 165 issued patents, 385 pending patent applications and 20 pending PCT applications in countries and regions outside the U.S as set forth in the following table. The duration of all the issued U.S. and foreign patents is 20 years from their respective first effective filing dates.

| Country | Issued | Pending |

| Argentina | 1 | 0 |

| Australia | 23 | 28 |

| Canada | 2 | 41 |

| China | 39 | 25 |

| Germany | 7 | 0 |

| European Patent Convention | 17 | 54 |

| Spain | 6 | 0 |

| France | 5 | 0 |

| Great Britain | 5 | 0 |

| Hong Kong | 23 | 29 |

| India | 6 | 49 |

| Japan | 9 | 56 |

| Korea | 9 | 42 |

| Mexico | 3 | 0 |

| Taiwan | 10 | 61 |

| Total | 165 | 385 |

In addition, it has several hundred additional patent applications in process. Some of GPEC’s technology holdings include foundational concepts in the following areas (many of which are being validated in other labs as indicated by the asterisks).

| | ● | Tandem organic solar cell*. Individual conventional solar cells have limited spectral coverage, voltage output, and tradeoff between absorption length and charge collection length. By stacking multiple solar cells with complementary absorption profiles, voltages of the cells can be added (at a constant current). This can make a more efficient cell; the record organic solar cell efficiency to date is reported to be a tandem architecture. |

| | ● | Fullerene acceptors*. Fullerenes include molecules such as C60, C70, C84 and derivatives that are designed to dissolve in solvents (such as PCBM made with either C60 or C70) are the most prevalent acceptor in organic photovoltaics. Fullerenes offer better efficiency than any other acceptor molecule to date. |

| | ● | Blocking layers*. In most solar cell designs, excitons must be blocked and reflected away from the metallic (or transparent) contact so that they can be dissociated at the donor-acceptor junction. Additionally, it is desired that these layers block the wrong carrier from contacting the electrode. |

| | ● | New materials for visible and infrared sensitivity*. Current OPV materials absorb light in the visible and deep red part of the solar spectrum, but do not collect light in the near infrared (NIR). Extending efficient light collection into the NIR has the potential to increase photocurrent generation by 40%, markedly improving OPV performance. |

| | ● | Scalable growth technologies*. A number of growth technologies have been developed for organic materials. These include vacuum thermal evaporation and organic vapor phase deposition for materials that can be sublimed or evaporated directly and gravure or ink-jet printing of dissolved materials. All of these processes are compatible with rigid planar substrates, but more importantly can be applied to flexible plastic or metal foil substrates, for roll-to-roll fabrication of OPVs. |

| | ● | Inverted solar cells*. One of the most air sensitive parts of the OPV is the region between the anode and electron acceptor. This region is degraded by oxygen and water in the dark and even more so under illumination. This interfacial region in a “conventional” OPV is exposed to the atmosphere directly, requiring that the OPV be kept in a hermetic package. If the OPV is prepared as an inverted cell, the air sensitive anode/organic interfacial region is placed below the donor, buffer layer and cathode. Thus, the device itself provides a level of “packaging,” markedly slowing environmental degradation of the device, minimizing packaging requirements for long term deployment in the field. |

| | ● | Materials for enhanced light collection via multi-exciton generation. The Shockley-Queisser limit for solar cell efficiency is 29% for silicon based cells and 31% for cells made with GaAs. In order to prepare solar cells with efficiencies higher than the Shockley-Queisser, researchers have turned to multi-junction cells, however, these cells are very expensive. An alternate approach is to collect the high energy part of the spectrum, i.e. UV-to-green, and double the energy collected from this part of the solar spectrum using singlet fission (“SF”). SF materials absorb high energy light and generate two excitons for every photon absorbed, thus doubling the light collection efficiency. The SF approach has the potential to give a single solar cell a 45% efficiency, well over the Shockley-Queisser limit, without increasing the cost to produce the cell. |

| | ● | Mixed layer and nano-crystalline cells. In planar (e.g., bilayer) cells the thickness of a layer is limited by the distance an exciton is expected to travel before it recombines. If the layer is too thick, photons absorbed may never result in collected charge. If the layers are too thin, there is insufficient material available for absorption of the light. By mixing the donor and acceptor throughout a thicker layer, an additional donor-acceptor interface is created throughout the layer, improving photocurrent generation capability. Nano-crystalline cells have a higher degree of phase separation between the donor and acceptor with nano-crystalline domains, with high purity and domain sizes in the nanometer scale. |

| | ● | Solar paints. GPEC plans to paint solar cells onto any substrate (needs to be smooth, but not flat). The idea is to create solar paints that can be applied quickly and easily to any surface, including, for example, mobile communications devices, electric cars, roofing materials, building siding and glass). |

| | ● | Transparent/semi-transparent cells. In certain applications it may be desirable to have a partially transparent solar cell. These applications include tinted windows. Instead of just absorbing or reflecting the light, the light would be absorbed and converted into energy. The unique nature of organics allows GPEC to tune the wavelengths absorbed to those that it does not want transmitted or that are not useful for vision, such as in the infrared region of the spectrum. |

| | ● | Ultralow cost, ultrahigh efficiency, flexible thin film inorganic cells. |

| | ● | Accelerated and recyclable liftoff process. |

| | ● | Cold-weld bonding of inorganic solar cells to plastic substrates and metal foils. |

Development Goals

During the next two years GPEC plans to demonstrate ND-ELO™ technology on 4” diameter GaAs wafers (currently it is using 2” wafers), with 20 non-destructive growth, removal, cold-weld bonding cycles onto flexible substrates without a decrease in performance between cycles, and an approximately 1% efficiency variation over all 20 cycles. The performance objectives are power conversion efficiencies of 23%. GPEC also plans to extend the technology to multi-junction solar cells with efficiencies greater than 32% efficiency under un-concentrated illumination. Further, GPEC plans to integrate “mini-concentrators” with the ND-ELO+cold weld bonded cells to effect cost reductions compared to the non-concentrated cells, expected to achieve cost targets of less than $0.50/Watt (peak).

With respect to its OPV technology, within the next three years GPEC plans to achieve greater than 15% power conversion efficiencies on organic solar cells with operational lifetimes of 20 years on barrier-coated plastic or metal foil substrates, and to demonstrate roll-to-roll “printing” of solar cells on plastic or metal foil substrates.

In order to accomplish these tasks and to give confidence to our manufacturing partners, GPEC plans to build a technology development center in Ann Arbor, Michigan. We plan to obtain cost-effective leased facilities and will equip the facility with required equipment and obtain required engineering personnel. This infrastructure will support our objective of producing 6 inch square GaAs and OPV module prototypes to demonstrate the efficacy of our technology platforms and to substantially reduce the risk to large-scale market entry by our licensed partners. We believe that the costs of establishing the facility will be approximately $5,500,000 and expect that it can be in place by the first quarter of 2014. The Plan of Operation that is in place is dependent upon the Company’s ability to raise additional capital to support its research and development operations. Since its inception, GPEC has raised over $60,000,000 from various investors, which has been invested primarily in research and development activities and maintaining GPEC’s patent portfolio. GPEC anticipates that it will need to raise approximately $18,000,000 over the next 24 months until it earns sufficient revenue to support its operations, including its continuing research and development goals and patent prosecutions and to maintain its intellectual property portfolio. The following is a breakdown of the $18,000,000 budget:

| R&D Payroll (technology development center) | | $ | 2,275,000 | |

| R&D Sponsored Research | | $ | 2,856,000 | |

| R&D Operating Expenses (technology development center) | | $ | 948,000 | |

| R&D Equipment Purchases (technology development center) | | $ | 1,950,000 | |

| Patent Prosecution and App Fees | | $ | 3,045,000 | |

| General and Administrative | | $ | 6,926,000 | |

GPEC has made contact with major solar cell and electronics manufacturers world-wide. It is finding commercial interest in both its GaAs and OPV technologies. GPEC plans to work closely with those companies interested in its technology solutions, both in its own technology development center, as well as within partner facilities, to develop proof-of-concept prototypes and processes to mitigate commercialization risks and gain early market entry and acceptance. Currently, GPEC is aware of several laboratories and commercial suppliers that are exploring and positively validating technologies that it has developed.

A key to reducing the risk to market entry by our partners is for GPEC to qualify its technologies at the manufacturing scale. This task will be conducted in GPEC’s technology development center, which will include a pilot manufacturing line. Furthermore, we believe it is essential for GPEC to maintain its technology leadership through a continuing relationship with its world-class research partners at USC and Michigan. GPEC will also seek other opportunities with the best researchers worldwide as opportunities present themselves.

Market Opportunity

Worldwide demand for electricity is expected to expand by more than 70% from 21.4 trillion kilowatt hours (kWh) in 2010 to 36.6 trillion kWh in 2035, representing annual growth of approximately 2.2%, according to the International Energy Agency (the “IEA”). The growth of the world energy market is spurred by continued worldwide industrialization, population growth, and economic expansion. The world’s energy needs are met by fossil fuels, nuclear energy and other technologies, including renewable energy sources such as geothermal, hydropower, wind and solar power. The IEA estimates that approximately two-thirds of worldwide electricity is currently produced from fossil fuels which are environmentally damaging and depleting resources.

However, there are several key trends that are reshaping the future of the global energy mix, including continued rapid growth in the use of solar and wind technologies, a retreat from nuclear power in some countries, and the emergence of unconventional natural gas production, according to the IEA. These trends are driving a pronounced shift away from oil, coal, and nuclear towards renewables and natural gas.

Worldwide electricity generation from renewable energy is projected to increase 170% from 4.2 trillion kWh in 2010 to 11.3 trillion kWh in 2030, representing 3.4% annual growth, according to the IEA. The renewable share of total electricity generation is projected to increase from 20% to 31% during this period. Renewable energy adoption continues to largely be driven by support from governments in the form of quotas (renewable portfolio standards), net metering systems, and feed-in-tariffs (FiTs) along with financial support such as tax incentives, grants, loans, rebates, and production incentives.

Electricity generated from solar power is projected to experience more rapid growth globally, increasing from 34 billion kWh in 2010 to 1,124 billion kWh in 2030, representing 12.4% annual growth. By 2030, solar power is expected to comprise approximately 3% of total global electricity generation, compared to only a fraction of 1% today. This growth projection is based on expected solar capacity additions of more than 600 GW during this period, according to the IEA. Within the United States, 2013 is expected to be a record year for solar power, projecting 4,400 MW of solar PV installations, according to Solar Energy Industries Association (“SEIA”) and GTM Research, a division of Greentech Media which provides market analysis in research reports, data services, and advisory services (“GTM Research”). Demand for solar power is expected to continue to be driven largely by renewable energy incentives. Meanwhile, cost reductions in solar technology (largely due to silicon oversupply) have narrowed the gap between solar power and fossil power. SEIA and GTM Research forecast continued growth within the U.S., projecting installations will exceed 9,000 MW in 2016.

OPV is an early stage industry segment and market forecasts are limited. As traditional solar technologies become increasingly commoditized, we expect increased demand with new applications, which require advanced technologies, such as those that GPEC is developing. IDTechEx, an independent market research firm focused on emerging technologies, estimates that the organic photovoltaic market will grow by over 1,300% by 2022, from a value of $4.6 million today up to over $630 million during that period, primarily representing new end-markets such as small mobile applications and BIPV. SNE Research, a market research and consulting company focused on the renewable energy sector, projects that OPVs will enter production during 2014, with shipments of 28 MW in 2014, 94 MW in 2015, and more than 1 GW in 2020.

Competition

GPEC is focused on commercializing and licensing advanced solar technologies that will enable entry of solar PV into new applications and also compete with established solar technologies in traditional solar markets. As an IP licensor, we believe our competitive exposure is insulated from industry dynamics, since we aim to partner with key industry participants and license our technology. Additionally, our licensing business model does not require us to establish high-volume manufacturing, which is a key competitive factor for product-based companies.

The solar photovoltaic sector is highly competitive, characterized by intense price competition among commercialized technologies and aggressive investment in emerging technologies as companies attempt to compete within the solar markets as well as within the overall electric power industry. The current solar market is dominated by crystalline silicon (“c-Si”) technology, with some penetration by Cadmium Telluride (“CdTe”) thin film technology. Advanced solar technology development efforts encompass various technology platforms as various stages of development, and consist of several large players and a number of small and medium companies. Advanced inorganic technologies, such as GaAs, have been limited to specialty, niche applications due to their high costs; although numerous research efforts are focused on reducing manufacturing costs. Other technologies, based on advanced inorganic chemistries have been slow to achieve market adoption due to their heretofore inability to achieve the required cost and performance thresholds to stimulate market adoption. OPV technologies remain in the development stage, with numerous activities ongoing among government laboratories, universities, and private enterprises. Currently, we are not aware of any commercialized OPV technologies, but there are a limited number of developers planning introduction within the next two years, using polymer-based materials.

For traditional solar applications such as rooftop projects, our technologies compete with established technologies as well as advanced technologies under development by other organizations primarily on a basis of cost and performance, which is typically measured as cost per watt, largely a function of production costs and cell conversion efficiency. Within emerging applications, our technologies compete primarily with advanced technologies on a basis of cost and performance, but also functionality and aesthetics as we attempt to open new markets to solar power. Additionally, we compete with other research and development organizations for funding from government agencies, laboratories, research institutions, and universities. Some of our existing or future competitors may be part of larger corporations that have greater financial resources than we do and, as a result, may be better positioned to adapt to changes in the industry or the economy as a whole.

Among GaAs-based solar developers, there are several companies, including Boeing’s subsidiary SpectroLab, Emcore Corporation, and Alta Devices, which produce commercial solar cells for highly specialized applications such as military and space-borne systems, which are inelastic to the high prices associated with the technology. Other companies such as Sol Voltaic are in the early stages of commercializing technology to couple GaAs components with traditional c-Si modules to improve conversion efficiency. Some of these companies are attempting to reduce manufacturing costs to enable entry of GaAs-based solar technologies into commercial markets. We believe GPEC’s patented GaAs ND-ELO™ and Cold Weld technologies present the opportunity to significantly reduce the production cost for GaAs solutions and believe that we could potentially license our technology to these companies.

OPV technologies have yet to be commercialized, but there are numerous development efforts on going. Ongoing research and development is being performed by Mitsubishi Chemical Holdings Corporation, LG Chemical, and BELECTRIC OPV (Kolitzheim, Germany), along with Heliatek (Dresden, Germany), Plextronics (Pittsburgh, Pennsylvania), and Solarmer Energy (El Monte, California), among others. We believe GPEC’s patented technologies for small molecule OPVs present a formidable obstacle for competing development efforts and would seek to partner with other developers or attempt to protect our IP.

Employees

Currently, GPEC employees consist of five full-time personnel – our Executive Chairman; Chief Executive Officer, President and Chief Operating Officer; Executive Vice President, General Counsel and Secretary; Chief Financial Officer and Treasurer; and Senior Vice President of Corporate Development. GPEC plans to hire a Chief Technology Officer and in-house patent attorney prior to the end of 2013. GPEC anticipates that its technology development center in Ann Arbor, Michigan will initially employ seven technical personnel and expand to 20 at full deployment. This is in addition to approximately 15 post-doctoral fellows and PhD candidates that are employed in our sponsored university research programs at USC and University of Michigan.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND PLAN OF OPERATIONS

This Current Report on Form 8-K/A contains forward-looking statements within the meaning of the federal securities laws. These include statements about our expectations, beliefs, intentions or strategies for the future, which we indicate by words or phrases such as “anticipate,” “expect,” “intend,” “plan,” “will,” “we believe,” “management believes” and similar language. Except for the historical information contained herein, the matters discussed in this “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere in this Current Report are forward-looking statements that involve risks and uncertainties. Any cautionary language in this Current Report, provides examples of risk uncertainties and events that may cause our actual results to differ materially from those projected. Except as may be required by law, we undertake no obligation to update any forward-looking statement to reflect events after the date of this Current Report on Form 8-K.

Overview

GPEC is engaged in the development, commercialization, and licensing of advanced photovoltaic technologies and intellectual property. GPEC has agreements with Princeton University which were assigned to University of Southern California and the University of Michigan, pursuant to which it has developed certain technologies and prosecuted and paid for more than 600 issued or pending patents covering materials, architectures, and fabrication processes for organic and inorganic flexible, thin-film photovoltaic technologies. While each patent is issued in the names of the respective university that developed the subject technology, GPEC has exclusive commercial license rights to all of the patents and their attendant technologies and the patents are referred to herein as being GPEC’s patents.

Unlike conventional thin film solar, the materials platforms that we have developed and are developing for solar cells are capable of ultrahigh efficiency accessible only by single crystalline inorganic materials such as silicon and gallium arsenide. The technologies we are developing allow the solar energy generating surfaces to be sufficiently flexible to be wrapped around 1 centimeter diameter cylinders without damage or loss of performance. Their ultra-light weight impacts other traditional costs associated with solar such as eliminating the need for costly, complex and robust panel mounts. We believe that these solar energy generating “films” can be used on architectural surfaces, on windows as attractive semi-transparent energy-generating coatings and even paints. Their flexibility allows their application to surfaces such as tents, clothing and other oddly shaped or “mobile” surfaces, including space-borne applications. Finally, the ability to be rolled around cylinders permits compact and low cost transport for deployment at remote sites.

GPEC currently holds exclusive rights to more than 600 issued or pending patents worldwide which cover architecture, processes and materials for flexible, thin-film OPV and GaAs technologies. In addition, we have several hundred more patents in process. Some of our technology holdings include foundational concepts in the following areas (many of which are being validated in other labs as indicated by the asterisks).

● Tandem organic solar cell*

● Fullerene acceptors*

● Blocking layers*

● New materials for visible and infrared sensitivity*

● Scalable growth technologies*

● Inverted solar cells*

● Materials for enhanced light collection via multi-exciton generation

● Mixed layer and nano-crystalline cells

● Solar paints

● Transparent/semi-transparent cells

● Ultralow cost, ultrahigh efficiency, flexible thin film inorganic cells

● Accelerated and recyclable liftoff process

● Cold-weld bonding of inorganic solar cells to plastic substrates and metal foils

Plan of Operation and Liquidity and Capital Resources

GPEC has made contact with major solar cell and electronics manufacturers world-wide. It is finding commercial interest in both its GaAs and OPV technologies. GPEC plans to work closely with those companies interested in its technology solutions, both in its own technology development center, as well as within partner facilities, to develop proof-of-concept prototypes and processes to mitigate commercialization risks and gain early market entry and acceptance.

Although we currently do not have any commitments from third parties to license our technologies or otherwise provide revenue to us, we are aware of several laboratories and commercial suppliers who are exploring and positively validating technologies that we have developed and which are protected by our intellectual property portfolio. These interested parties potentially represent some of GPEC’s first partners for joint technology development and acceptance into manufacturing production.

A key to reducing the risk to market entry by our partners is for GPEC to qualify its technologies at a manufacturing scale. We believe that the best manner to do this is to develop our own technology development center in Ann Arbor, Michigan. The principal function of the facility will be to demonstrate our ability to prototype our inorganic and organic solar cells utilizing our proprietary technologies. In addition, we anticipate that advancements at the facility can attract other industry players to acquire early licenses to use GPEC intellectual property. Finally, we believe that having a technology development center will allow us to obtain government funding from the National Aeronautics and Space Administration, the Department of Defense and the Department of Energy, each of which have interests in businesses that can deliver ultra lightweight, high-efficiency technologies for space, mobile warfighter, and grid-deployment applications.

The technology development center can also make GPEC highly competitive to receive government grants to support GaAs and OPV research and development. A second revenue source is in joint development projects with existing solar cell manufacturers. The largest near-term opportunity will be in partnerships exploiting GaAs solar technology with existing GaAs cell manufactures in the space programs, military operations and other suitable end use. We anticipate that partnerships with one or more of these companies will be supported by the facility, and will result in early revenue opportunities.

We believe that the costs of establishing the facility will be approximately $5,500,000 and that it can be in place by first quarter 2014.

GPEC’s Plan of Operation is dependent upon its ability to raise additional capital to support its research and development operations. Since its inception, GPEC has raised over $60,000,000 from various investors, which has been invested primarily in research and development activities and maintaining GPEC’s patent portfolio. GPEC anticipates that it will need to raise approximately $18,000,000 over the next 24 months until it earns sufficient revenue to support its operations, including its continuing research and development activities and patent prosecutions and to maintain its intellectual property portfolio. The following is a breakdown of the $18,000,000 budget:

| R&D Payroll (technology development center) | | $ | 2,275,000 | |

| R&D Sponsored Research | | $ | 2,856,000 | |

| R&D Operating Expenses (technology development center) | | $ | 948,000 | |

| R&D Equipment Purchases (technology development center) | | $ | 1,950,000 | |

| Patent Prosecution and App Fees | | $ | 3,045,000 | |

| General and Administrative | | $ | 6,926,000 | |

There can be no assurance that financing will be available to GPEC to fund its $18,000,000 budget, or, if available, that it will be on terms acceptable to GPEC.

Results of Operations

For the three months ended June 30, 2013 and June 30, 2012

Research and Development Expenses

Research and development expenses for the three months ended June 30, 2013 were $321,896, a 49.7% increase from $215,024 for the for the three months ended June 30, 2012. The increase is attributable to additional funding we provided to the Universities pursuant to our research agreement.

Patent Application and Prosecution Fees

Patent application and prosecution fees consist of the fees due for prosecuting and maintaining GPEC’s patents and were $246,944 for the three months ended June 30, 2013, a 29.8% increase from $190,308 for the three months ended June 30, 2012. The increase is attributable to an increase in the number of GPEC patents and number of applications being researched for GPEC technologies.

Salaries and Related Expenses

Salaries and related expenses consist of salaries and fringe benefits paid to GPEC were $412,037 for the three months ended June 30, 2013, a 21.5 % increase from $339,023 for the three months ended June 30, 2012. The increase is attributable to the payout of deferred salaries during the three months ended June 20, 2013 and the costs associated with those salaries.

Selling, General and Administrative Expenses

Selling, general and administrative expenses consist primarily of office supplies, workers compensation insurance, medical insurance, postage and shipping, traveling expenses and consulting fees and were $128,612 for the three months ended June 30, 2013, a 43.5% decrease from $227,572 for the three months ended June 30, 2012. The decrease is primarily attributable to a decrease in traveling and consulting fees when compared to the prior period.

Net Loss

The net loss for the three months ended June 30, 2013 was ($24,498,925), a 1,134.8% increase from ($1,984,081) for the three months ended June 30, 2012. The increased net loss is primarily attributable to an increase in stock based compensation from zero for the three months ended June 30, 2012 to $19,210,470 for the six months ended June 30, 2013 which resulted from stock awards granted to officers.

For the six months ended June 30, 2013 and June 30, 2012

Research and Development Expenses

Research and development expenses for the six months ended June 30, 2013 were $543,771, a 6.6% increase from $510,258 for the for the six months ended June 30, 2012. The increase is attributable to the fluctuations in amounts spent on research contracts with the Universities.

Patent Application and Prosecution Fees

Patent application and prosecution fees consist of the fees due for prosecuting and maintaining GPEC’s patents and were $572,421 for the six months ended June 30, 2013, a 43.2% increase from $399,828 for the six months ended June 30, 2012. The increase is attributable to the increase in patents and filings as compared to the prior period.

Salaries and Related Expenses

Salaries and related expenses consist of salaries and fringe benefits paid to GPEC were $537,296 for the six months ended June 30, 2013, a 21.0 % decrease from $679,885 for the six months ended June 30, 2012. The decrease is attributable to a decrease in personnel.

Selling, General and Administrative Expenses

Selling, general and administrative expenses which consist primarily of office supplies, workers compensation insurance, medical insurance, postage and shipping, and traveling expenses were $310,001 for the six months ended June 30, 2013, a 14.2% decrease from $361,224 for the six months ended June 30, 2012. The decrease is primarily attributable to a reduction in traveling.

Net Loss

The net loss for the six months ended June 30, 2013 was ($27,628,017), a 180.8% increase from ($9,838,012) for the six months ended June 30, 2012. The increased net loss is primarily attributable to an increase in stock based compensation from $4,818,525 for the six months ended June 30, 2012 to $19,406,501 for the six months ended June 30, 2013 which resulted from stock awards granted to officers.

For the fiscal years ended December 31, 2012 and December 31, 2011

Research and Development Expenses

Research and development expenses for the fiscal year ended December 31, 2012 were $998,127, a 12.5% increase from $887,097 for the prior year. The increase is due to additional funding to the Universities pursuant to the research agreement.

Patent Application and Prosecution Fees

Patent application and prosecution fees consist of the fees due for prosecuting and maintaining GPEC’s patents and were $1,345,743 for the fiscal year ended December 31, 2012, a 15.8% decrease from $1,597,642 for the prior year. The decrease is attributable to the patent filings made a broad and their billing systems.

Salaries and Related Expenses

Salaries and related expenses consist of salaries and fringe benefits paid to GPEC and were $951,411 for the fiscal year ended December 31, 2012, a 45.1 % decrease from $1,731,634 in the prior year. The decrease is attributable to the forgiveness of salaries as agreed upon in the separation agreement of two former employees.

Selling, General and Administrative Expenses

Selling, general and administrative expenses consist primarily of office supplies, workers compensation insurance, medical insurance, postage and shipping, traveling expenses and consulting fees and were $622,451 for the fiscal year ended December 31, 2012, a 52.0% decrease from $1,297,954 in the prior year. The decrease is primarily attributable to a decrease in legal expenses of approximately $400,000 and travel expenses of approximately $275,000 when compared to the prior year.

Net Loss

The net loss for the fiscal year ended December 31, 2012 was ($20,862,200), a 113.0% increase from ($9,795,116) in the prior year. The increased net loss is primarily attributable to an increase in stock based compensation from $1,111,571 to $9,950,226 which resulted from stock awards granted to officers.

Recent Accounting Pronouncements

Critical Accounting Policies

The following critical accounting policies are important to the portrayal of the Company’s combined financial condition and results.

Basis of accounting

The Company’ policy is to maintain its books and prepare its combined financial statements on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America.

Use of estimates

The preparation of combined financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the combined financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and cash equivalents

Cash and cash equivalents include all cash and liquid investments with an initial maturity of three months or less.

Stock-based compensation

We account for stock based compensation in accordance with FASB ASC 718 which requires companies to measure the cost of employee services received in exchange for an award of an equity instrument based on the grant-date fair value of the award. For stock-based awards granted on or after January 1, 2006, stock-based compensation expense is recognized on a straight-line basis over the requisite service period. In prior years, we accounted for stock-based awards under APB No. 25, “Accounting for Stock Issued to Employees.” We account for non-employee share-based awards in accordance with FASB ASC 505-50.

DESCRIPTION OF PROPERTY

The Company’s executive offices are currently located at 17207 N. Perimeter Dr., Suite 210, Scottsdale, AZ 85255 and it started leasing it offices from DTR10, LLC on November 15, 2013. The office space is approximately 3,077 square feet. Its monthly rental is $6,410 during the first year of the lease and will be subject to 3% increase in the following years. The Company’s headquarter was formerly at 20 Trading Post Way, Medford Lakes, New Jersey 08055 in a 500 square foot space which was provided to GPEC free of charge by a spouse of GPEC’s officer.

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

Directors and Executive Officers

The following table sets forth the name and position of each of our current executive officers and directors. All directors hold office until the next annual meeting of stockholders or until their respective successors are elected, except in the case of death, resignation or removal:

| Name | | Age | | Position |

| | | | | |

| John D. Kuhns | | 63 | | Executive Chairman of the Board |

| | | | | |

| Dean L. Ledger | | 65 | | Chief Executive Officer, Director |

| | | | | |

| Robert J. Fasnacht | | 56 | | President, Director, Chief Operating Officer |

| | | | | |

| Amy B. Kornafel | | 42 | | Chief Financial Officer and Secretary |

| | | | | |

| Joey S. Stone | | 50 | | Senior Vice President of Corporate Development |

John D. Kuhns, age 63, is the Executive Chairman of the Board of the Company and of GPEC. Mr. Kuhns became an investor in GPEC in 1999, and has served as a Director of GPEC since April of 2000. He was appointed to serve as Director of the Company on September 24, 2013. In the last 30 years, Mr. Kuhns has founded and completed five initial public offerings for renewable energy companies. Most recently in 2006 he founded China Hydroelectric Corporation (NYSE: CHC), China’s largest foreign-owned hydroelectric power company. China Hydro listed its shares on the New York Stock Exchange in January of 2010. Mr. Kuhns served as Chairman of the Board of China Hydro from 2006 until 2012. In 1988, Mr. Kuhns founded The New World Power Corporation (NASDAQ: NWPC), where he served as Chairman of the Board of directors. This company was the first wind farm company to go public. In 1981, Mr. Kuhns was also the founder of Catalyst Energy Corporation (NYSE: CE), one of the country’s most successful hydroelectric developers and recognized by Inc. Magazine as the nation's fastest growing public company in the five years from 1982 to 1987. Mr. Kuhns is the Chairman and CEO of Kuhns Brothers, an investment banking boutique and one of the oldest continually operating investment firms in the United States, tracing its origins to 1842. Mr. Kuhns is a graduate of the Harvard Business School (M.B.A., 1977), the University of Chicago (M.F.A. in Fine Arts, 1975) and Georgetown University (A.B., in Sociology and in Fine Arts, 1972), where he was captain of the varsity football team and is a member of the University's Athletic Hall of Fame. Mr. Kuhns was selected to serve originally as a Director of GPEC and now as a Director of the Company due in part to his comprehensive knowledge gained over the last 30 years in all aspects of the Green Energy field. He also has accumulated vast experience and understanding of all business aspects and competitive worldwide environment for solar power.

Dean L. Ledger, age 65, has served as a Director and senior executive of GPEC since its inception in 1994 and was instrumental in its founding. Mr. Ledger is GPEC’s Chief Executive Officer, and was elected as the Chief Executive Officer of the Company on September 24, 2013. Mr. Ledger has significant experience in capital formation and business building as he played instrumental roles in both Universal Display Corporation (NASDAQ: OLED) and InterDigital Corporation (NASDAQ: IDCC) from their inception. From 1994 to 2012, Mr. Ledger served as Executive Vice President-Corporate Development of Universal Display Corporation. From July 1994 to January 2001, Mr. Ledger served as a member of the Board of Directors of Universal Display Corporation. From December 2001 to July 2003, Mr. Ledger served as a member of the Board of Directors of North American Technologies, Inc. (NASDAQ: NATK). From May 1991 until October 1992, Mr. Ledger was a consultant to the IntelCom Group. Mr. Ledger served as a consultant to InterDigital Communications Corporation from October 1989 to April 1991. Prior to October 1989, Mr. Ledger spent 12 years as a financial consultant with E.F. Hutton, Shearson Lehman Brothers and Paine Webber. He is a graduate of Colorado College (B.A., Business Administration, 1972).

The Board concluded that Mr. Ledger should serve as a Director of the Company based on his extensive experience and knowledge of the history of our Company and of all of its related technologies. Furthermore, he has a proven track record in leveraging information technology to capture new commercial opportunities and to increase operational efficiencies in various industries.

Robert J. Fasnacht, age 56, is a director, President and Chief Operating Officer of GPEC and he was elected as a director, President and Chief Operating Officer of the Company on September 24, 2013. He first joined GPEC in 2011 as its Executive Vice President, General Counsel and corporate Secretary. Prior to that, he was engaged in a private legal practice emphasizing both corporate transactions and complex civil litigation. He also served for a number of years as a Board Member of various U.S. companies, including a U.S. based privately held restaurant Franchisor. He is admitted to practice in the 9th Circuit Court of Appeals, along with several state and federal courts, including the U.S. Tax Court. Mr. Fasnacht is a graduate of the University of Idaho (B.S., Chemistry, 1983 and J.D., 1985). Mr. Fasnacht was selected as a Director due to his extensive knowledge both from his scientific education and his legal training on all aspects of the Company’s Organic and Inorganic Photovoltaic Technologies and on its related intellectual property portfolio. He also demonstrated an extraordinary ability to understand the business and technological aspects of the Company as they relate to the Company’s strategic roll moving forward.

Amy B. Kornafel, age 42, is the Chief Financial Officer of GPEC since March 2005 and also serves as the Company’s Secretary. She was elected as the Chief Financial Officer and Secretary of the Company on September 24, 2013. From 2003 through 2005, Ms. Kornafel served as GPEC’s Controller. Previously Ms. Kornafel worked as a Consultant and Senior Financial Statement Assurance Auditor for Arthur Andersen LLP. From 1995 to 1997, Ms. Kornafel served as a tax accountant for Alloy, Silverstein, Shapiro, Adams, Mulford and Company. Ms. Kornafel’s experience includes extensive financial, accounting and audit experience with software, hardware, manufacturing, venture capital, bio-tech, development stage and retail enterprises. Ms. Kornafel is a graduate of Rutgers University (B.S., Accounting 1995).

Joey S. Stone, age 50, has served as the Senior Vice President of Corporate Development of GPEC since September 2010 and he was elected to the same positions with the Company on September 24, 2013. Mr. Stone is a senior executive with over 20 years of experience in the financial services sector. From 2001 to 2010, Mr. Stone was a Senior Vice President at Morgan Stanley, a global financial services firm. From 1991 to 2001, Mr. Stone was a financial consultant with J.C. Bradford & Co. and from 1988 to 1991, with PaineWebber. Mr. Stone is a graduate of Louisiana State University (B.S., Business, 1987).

We do not have a standing nominating, compensation or audit committee. Rather, our full board of directors performs the functions of these committees. Also, we do not have a “audit committee financial expert” on our board of directors as that term is defined by Item 401(d)(5)(ii) of Regulation S-K. We do not believe it is necessary for our board of directors to appoint such committees because the volume of matters that come before our board of directors for consideration permits the directors to give sufficient time and attention to such matters to be involved in all decision making. Additionally, because our Common Stock is not listed for trading or quotation on a national securities exchange, we are not required to have such committees.

Code of Ethics

On January 28, 2013, we adopted a Code of Ethics and Business Conduct which is applicable to our employees and which also includes a Code of Ethics for our CEO and principal financial officer and persons performing similar functions. A copy of our Code of Business Conduct and Ethics has been filed with the Securities and Exchange Commission as an exhibit to the Company’s Registration Statement on Form S-1 filed March 15, 2013. A code of ethics is a written standard designed to deter wrongdoing and to promote:

| | ● | honest and ethical conduct, |

| | | |

| | ● | full, fair, accurate, timely and understandable disclosure in regulatory filings and public statements, |

| | ● | compliance with applicable laws, rules and regulations, |

| | | |

| | ● | the prompt reporting violation of the code, and |

| | | |

| | ● | accountability for adherence to the code. |

Our securities are not listed on a national securities exchange or in an inter-dealer quotation system which has requirements that directors be independent. We believe that two of our four directors, Robert J. Fasnacht and Dean L. Ledger, would not be considered to be independent, as that term is defined in the listing standards of NASDAQ.

Meetings of the Board of Directors

During its fiscal year ended December 31, 2012, the Board of Directors of GPEC had 4 board meetings in by conference telephone and took action by unanimous written consent 13 times.