Table of Contents

Filed pursuant to Rule 424(b)(5)

SEC File No. 333-187808

PROSPECTUS SUPPLEMENT

(To prospectus dated May 9, 2013)

8,500,000 Shares

Matador Resources Company

Common Stock

We are offering 8,500,000 shares of our common stock. Our common stock is traded on the New York Stock Exchange (“NYSE”) under the symbol “MTDR.” On September 4, 2013, the last sale price of our common stock as reported on the NYSE was $15.79 per share.

| Per share | Total | |||||||

Public offering price | $ | 15.25000 | $ | 129,625,000 | ||||

Underwriting discounts and commissions(1) | $ | 0.68625 | $ | 5,833,125 | ||||

Proceeds, before expenses, to us | $ | 14.56375 | $ | 123,791,875 | ||||

| (1) | Please read “Underwriting (Conflicts of Interest)” for a description of all underwriting compensation payable in connection with this offering. |

We have granted the underwriters a 30-day option to purchase up to 1,275,000 additional shares of our common stock.

Investing in our common stock involves a high degree of risk. See “Risk Factors’’ beginning on page S-21 of this prospectus supplement and on page 3 of the accompanying prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on September 10, 2013.

| RBC CAPITAL MARKETS | CITIGROUP | SCOTIABANK / HOWARD WEIL |

SUNTRUST ROBINSON HUMPHREY

| STEPHENS INC. | BMO CAPITAL MARKETS | COMERICA SECURITIES |

| CAPITAL ONE SECURITIES | IBERIA CAPITAL PARTNERS L.L.C. | WUNDERLICH SECURITIES |

The date of this prospectus supplement is September 4, 2013.

Table of Contents

Table of Contents

MATADOR’S CONTINUED GROWTH

|  |  | ||

|  |  | ||

| (1) | Adjusted EBITDA is a non-GAAP financial measure. For a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to our net income (loss) and net cash provided by operating activities, see “Summary—Summary Historical Financial Data—Non-GAAP Financial Measures” in this prospectus supplement. |

Table of Contents

| Prospectus Supplement | ||||

| Page | ||||

| ii | ||||

| iii | ||||

| iv | ||||

| S-1 | ||||

| S-21 | ||||

| S-25 | ||||

| S-26 | ||||

| S-27 | ||||

| S-27 | ||||

Material United States Federal Income Tax Considerations for Non-U.S. Holders | S-28 | |||

| S-33 | ||||

| S-41 | ||||

| S-41 | ||||

| A-1 | ||||

| Prospectus | ||||

| Page | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 6 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 18 | ||||

| 21 | ||||

| 22 | ||||

| 24 | ||||

| 24 | ||||

You should rely only on the information contained in this prospectus supplement, the accompanying prospectus and the documents we have incorporated by reference into this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus supplement or the accompanying prospectus, as well as the information we previously filed with the Securities and Exchange Commission, or SEC, that is incorporated by reference in this prospectus, is accurate as of any date other than its respective date.

i

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts. The first part is this prospectus supplement and the information incorporated by reference herein, which, among other things, describes the specific terms of this offering. The second part is the accompanying prospectus and the information incorporated by reference therein, which, among other things, gives more general information, some of which may not apply to this offering. Generally, when we refer to the prospectus, we are referring to both this prospectus supplement and the accompanying prospectus. If any information varies between this prospectus supplement and the accompanying prospectus, you should rely on the information in this prospectus supplement.

Additional information about us, including our financial statements and the notes thereto, is incorporated in this prospectus by reference to certain of our filings with the SEC. You are urged to read carefully this prospectus and the information incorporated by reference in this prospectus, including the risk factors and other cautionary statements described under the heading “Risk Factors” included elsewhere in this prospectus and in Item 1A of Part I of our Annual Report on Form 10-K for the year ended December 31, 2012 before investing in our common stock. See “Where You Can Find More Information” in this prospectus supplement.

ii

Table of Contents

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available to the public over the Internet at the SEC’s web site at http://www.sec.gov and at our website at http://www.matadorresources.com. You may also read and copy any document we file with the SEC at the SEC’s public reference room at 100 F Street, NE, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room and its copy charges.

We are incorporating by reference in this prospectus the information we file with the SEC, which means that we can disclose important information to you by referring you to those documents. The information incorporated by reference in this prospectus is an important part of this prospectus, and information that we file later with the SEC will automatically update and supersede this information. We incorporate by reference the documents listed below and any future filings made with the SEC under Sections 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act (excluding any information furnished pursuant to Item 2.02 or Item 7.01 on any Current Report onForm 8-K):

| Ÿ | Annual Report on Form 10-K for the year ended December 31, 2012, as filed with the SEC on March 18, 2013; |

| Ÿ | Quarterly Reports on Form 10-Q for the quarters ended March 31, 2013, as filed with the SEC on May 10, 2013, and June 30, 2013, as filed with the SEC on August 9, 2013; |

| Ÿ | Current Reports on Form 8-K filed with the SEC on March 14, 2013, April 15, 2013, June 6, 2013 and June 10, 2013, in each case other than information furnished under Items 2.02 or 7.01 of Form 8-K; and |

| Ÿ | Description of our common stock contained in our registration statement on Form 8-A filed with the SEC on January 27, 2012. |

Any statement contained in a document incorporated by reference herein shall be deemed to be modified or superseded for all purposes to the extent that a statement contained in this prospectus or in any other subsequently filed document which is also incorporated, or deemed to be incorporated by reference, modifies or supersedes such statement. Any statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this prospectus.

You may request a copy of any of the documents summarized or incorporated by reference in this prospectus, at no cost, by writing or telephoning us at the following address and phone number:

Matador Resources Company

Attention: Corporate Secretary

One Lincoln Centre

5400 LBJ Freeway, Suite 1500

Dallas, Texas 75240

(972) 371-5200

iii

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus supplement and the documents incorporated by reference herein constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Exchange Act. Additionally, forward-looking statements may be made orally or in press releases, conferences, reports, on our website or otherwise, in the future, by us or on our behalf. Such statements are generally identifiable by the terminology used such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “potential,” “predict,” “project,” “should” or other similar words.

By their very nature, forward-looking statements require us to make assumptions that may not materialize or that may not be accurate. Forward-looking statements are subject to known and unknown risks and uncertainties and other factors that may cause actual results, levels of activity and achievements to differ materially from those expressed or implied by such statements. Such factors include, among others: changes in oil or natural gas prices, the success of our drilling program, the timing of planned capital expenditures, availability of acquisitions, uncertainties in estimating proved reserves and forecasting production results, operational factors affecting the commencement or maintenance of producing wells, the condition of the capital markets generally, as well as our ability to access them, the proximity to and capacity of transportation facilities, uncertainties regarding environmental regulations or litigation and other legal or regulatory developments affecting our business, and the other factors discussed below and elsewhere in this prospectus and in other documents that we file with or furnish to the SEC, all of which are difficult to predict. Forward-looking statements may include statements about:

| Ÿ | our business strategy; |

| Ÿ | our reserves; |

| Ÿ | our technology; |

| Ÿ | our cash flows and liquidity; |

| Ÿ | our financial strategy, budget, projections and operating results; |

| Ÿ | our oil and natural gas realized prices; |

| Ÿ | the timing and amount of future production of oil and natural gas; |

| Ÿ | the availability of drilling and production equipment; |

| Ÿ | the availability of oil field labor; |

| Ÿ | the amount, nature and timing of capital expenditures, including future exploration and development costs; |

| Ÿ | the availability and terms of capital; |

| Ÿ | our drilling of wells; |

| Ÿ | government regulation and taxation of the oil and natural gas industry; |

| Ÿ | our marketing of oil and natural gas; |

| Ÿ | our exploitation projects or property acquisitions; |

| Ÿ | our costs of exploiting and developing our properties and conducting other operations; |

| Ÿ | general economic conditions; |

| Ÿ | competition in the oil and natural gas industry; |

iv

Table of Contents

| Ÿ | the effectiveness of our risk management and hedging activities; |

| Ÿ | environmental liabilities; |

| Ÿ | counterparty credit risk; |

| Ÿ | developments in oil-producing and natural gas-producing countries; |

| Ÿ | our future operating results; |

| Ÿ | estimated future reserves and the present value thereof; |

| Ÿ | our plans, objectives, expectations and intentions contained in this prospectus supplement that are not historical; and |

| Ÿ | other factors discussed in our Annual Report on Form 10-K for the year ended December 31, 2012 and our Quarterly Reports on Form 10-Q for the quarters ended March 31, 2013 and June 30, 2013, as applicable. |

Although we believe that the expectations conveyed by the forward-looking statements are reasonable based on information available to us on the date such forward-looking statements were made, no assurances can be given as to future results, levels of activity, achievements or financial condition.

You should not place undue reliance on any forward-looking statement and should recognize that the statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described above, as well as others not now anticipated. The impact of any one factor on a particular forward-looking statement is not determinable with certainty as such factors are interdependent upon other factors. The foregoing statements are not exclusive and further information concerning us, including factors that potentially could materially affect our financial results, may emerge from time to time. We do not intend to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements, except as required by law, including the securities laws of the United States and the rules and regulations of the SEC.

v

Table of Contents

The following summary highlights selected information contained elsewhere in this prospectus supplement, the accompanying prospectus and in the documents incorporated by reference in this prospectus supplement and does not contain all the information you will need in making your investment decision. You should read carefully this entire prospectus supplement, the accompanying prospectus and the documents incorporated by reference in this prospectus supplement. See “Where You Can Find More Information.” Certain oil and natural gas terms used in this prospectus supplement and the accompanying prospectus are defined in the “Glossary of Oil and Natural Gas Terms” included as Appendix A hereto.

In this prospectus supplement, references to “we,” “our” or the “Company” refer to Matador Resources Company and its subsidiaries as a whole (unless the context indicates otherwise) and references to “Matador” refer solely to Matador Resources Company.

The Company

Introduction

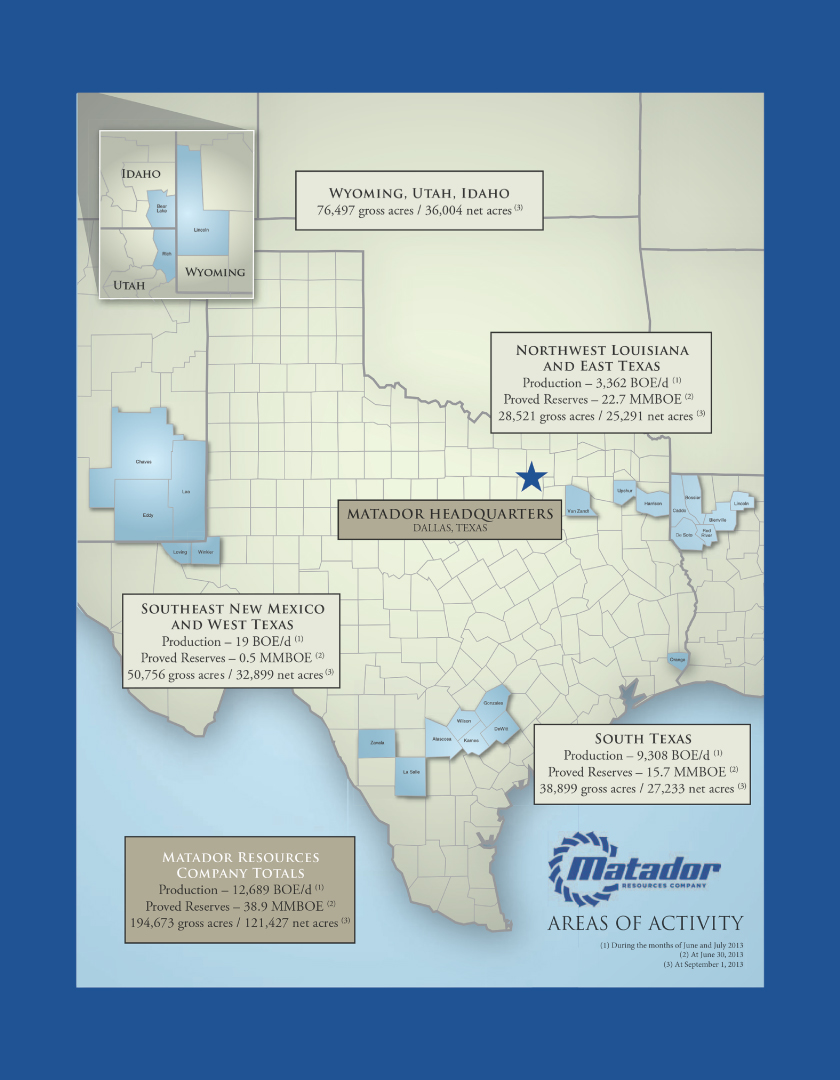

Matador Resources Company is an independent energy company engaged in the exploration, development, production and acquisition of oil and natural gas resources in the United States, with an emphasis on oil and natural gas shale and other unconventional plays. Our current operations are focused primarily on the oil and liquids-rich portion of the Eagle Ford shale play in South Texas (38,900 gross (27,200 net) acres at September 1, 2013) and the Wolfcamp and Bone Spring plays in the Permian Basin in Southeast New Mexico and West Texas (50,800 gross (32,900 net) acres at September 1, 2013). We also operate in the Haynesville shale and Cotton Valley plays in Northwest Louisiana and East Texas (28,500 gross (25,300 net) acres at September 1, 2013). At September 1, 2013, approximately 97% of our Haynesville acreage was held by production or consisted of fee mineral interests that we owned and approximately 72% of our Eagle Ford acreage was held by production. In addition, we have a large exploratory leasehold position in Southwest Wyoming and adjacent areas of Utah and Idaho (76,500 gross (36,000 net) acres at September 1, 2013) where we are testing the Meade Peak shale.

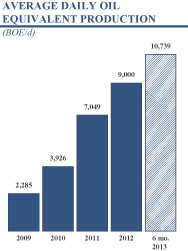

For the six months ended June 30, 2013, our average daily oil equivalent production was 10,739 BOE per day, of which 5,015 Bbl per day, or 47%, was oil and 34.3 MMcf per day, or 53%, was natural gas. During the months of June and July 2013, our average daily oil equivalent production increased to 12,689 BOE per day, including 6,200 Bbl of oil per day and 38.9 MMcf of natural gas per day. At June 30, 2013, we had estimated total proved oil and natural gas reserves of 38.9 million BOE, of which 12.1 million Bbl, or 31%, was oil and 160.8 Bcf, or 69%, was natural gas.

We had two contracted drilling rigs operating continuously during the six months ended June 30, 2013. During the first quarter of 2013, both of these rigs were operating in the Eagle Ford shale in South Texas, and all of our operated drilling and completion activities were focused on the Eagle Ford shale. In late April 2013, we moved one of these contracted drilling rigs to Southeast New Mexico to begin a three-well exploration program testing portions of our growing leasehold position in the Permian Basin. At September 1, 2013, we were testing potential completion intervals on our first test well and were drilling a horizontal lateral in the Second Bone Spring sand in our second test well. Between January 1, 2013 and September 1, 2013, we acquired approximately 35,000 gross (26,800 net) acres in Southeast New Mexico and West Texas, primarily in Lea and Eddy Counties, New Mexico. Including these acreage acquisitions, at September 1, 2013, our total acreage position in Southeast New Mexico and West Texas was approximately 50,800 gross (32,900 net) acres, of which we consider 43,100 gross (32,300 net) acres to be prospective for

S-1

Table of Contents

multiple oil and liquids-rich targets, including the Wolfcamp and Bone Spring plays, as well as other potential shallower targets (Delaware) and deeper targets (Atoka, Morrow). As a result of these recent acreage acquisitions, the preliminary indications from our drilling program and the production results from nearby operators, we now intend to continue operating one rig full-time in Southeast New Mexico and West Texas for the remainder of 2013 and throughout 2014. In addition, in mid-August 2013, we added a third drilling rig and returned to operating a two-rig drilling program for the exploration and development of our Eagle Ford shale assets in South Texas. Accordingly, we intend to operate three rigs, two in South Texas and one in Southeast New Mexico and West Texas, for the remainder of 2013 and throughout 2014.

In 2012, more than 90% of our total capital expenditures of $334.6 million were directed to our operations in South Texas, primarily in the Eagle Ford shale, as we sought to transition to a more balanced commodity portfolio through the drilling of wells that were prospective for oil and liquids. As a result of our decision to continue the exploration of our leasehold position in Southeast New Mexico and West Texas for the remainder of 2013, and given the recent addition of a third rig to return to a two-rig drilling program in the Eagle Ford in South Texas, we have increased our 2013 capital expenditure budget from $325.0 million to $370.0 million. We expect that approximately 98% of our increased 2013 capital expenditure budget will be oil and liquids focused and approximately 78% will be directed to increasing our oil production and reserves in South Texas, primarily in the Eagle Ford shale play. We also plan to allocate approximately 20% of our increased 2013 capital expenditure budget to the exploration and acquisition of additional interests in the Wolfcamp, Bone Spring and other oil and liquids-rich plays in Southeast New Mexico and West Texas. Through June 30, 2013, we had incurred approximately $168.6 million, or approximately 46%, of our increased 2013 capital expenditure budget.

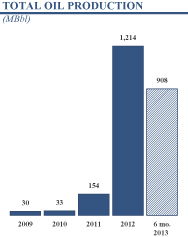

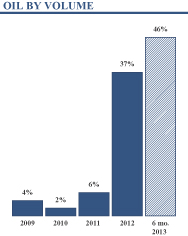

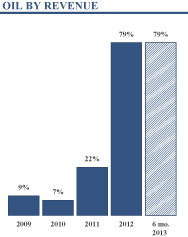

Beginning with the initial exploration wells we drilled in 2010 to test portions of our leasehold position in the Eagle Ford shale in South Texas, we have successfully directed our operations over the past three years to significantly increase our oil production and reserves in order to develop a more balanced commodity portfolio. Oil constituted approximately 47% of our average daily production, 79% of our oil and natural gas revenues and 31% of our estimated proved reserves at and for the six months ended June 30, 2013, as compared to approximately 4% of our average daily production, 9% of our oil and natural gas revenues and 1% of our estimated proved reserves at and for the year ended December 31, 2009.

S-2

Table of Contents

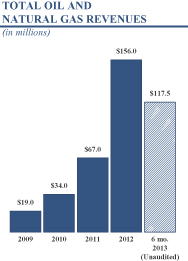

The following table presents a comparison of our proved reserves, average daily production and oil and natural gas revenues at and for the years ended December 31, 2009 and December 31, 2012 and at and for the six months ended June 30, 2013.

| Six Months Ended June 30, 2013 | Year Ended December 31, 2012 | Year Ended December 31, 2009 | ||||||||||

Selected Operating Data: | ||||||||||||

Production Data | ||||||||||||

Average daily oil production (Bbl/d) | 5,015 | 3,317 | 82 | |||||||||

Average daily natural gas production (MMcf/d) | 34.3 | 34.1 | 13.2 | |||||||||

Average daily oil equivalent production (BOE/d) | 10,739 | 9,000 | 2,285 | |||||||||

Percent oil | 47 | % | 37 | % | 4 | % | ||||||

Revenues (Dollars in millions)(1) | ||||||||||||

Oil and natural gas revenues | $ | 117.5 | $ | 156.0 | $ | 19.0 | ||||||

Oil revenues | $ | 93.3 | $ | 123.7 | $ | 1.7 | ||||||

Natural gas revenues | $ | 24.2 | $ | 32.3 | $ | 17.3 | ||||||

Percent oil | 79 | % | 79 | % | 9 | % | ||||||

| At June 30, 2013 | At December 31, 2012 | At December 31, 2009 | ||||||||||

Selected Reserves Data: | ||||||||||||

Estimated Proved Reserves | ||||||||||||

Oil (MBbl) | 12,128 | 10,485 | 103 | |||||||||

Natural gas (Bcf) | 160.8 | 80.0 | 63.9 | |||||||||

Total (MBOE) | 38,931 | 23,819 | 10,758 | |||||||||

Percent oil | 31 | %(2) | 44 | % | 1 | % | ||||||

PV-10(3) (In millions) | $ | 522.3 | $ | 423.2 | $ | 70.4 | ||||||

Standardized Measure(4) (In millions) | $ | 477.6 | $ | 394.6 | $ | 65.1 | ||||||

| (1) | Revenues for the six months ended June 30, 2013 are unaudited. |

| (2) | Decrease from December 31, 2012 due to the improvement in natural gas prices, which resulted in the addition of approximately 80.1 Bcf (13.3 million BOE) of proved undeveloped natural gas reserves in the Haynesville shale in Northwest Louisiana to our total proved reserves at June 30, 2013. |

| (3) | PV-10 is a non-GAAP financial measure and generally differs from Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues. PV-10 is not an estimate of the fair market value of our properties. We and others in the industry use PV-10 as a measure to compare the relative size and value of proved reserves held by companies and of the potential return on investment related to the companies’ properties without regard to the specific tax characteristics of such entities. Our PV-10 at June 30, 2013, December 31, 2012 and December 31, 2009 may be reconciled to our Standardized Measure of discounted future net cash flows at such dates by reducing our PV-10 by the discounted future income taxes associated with such reserves. The discounted future income taxes at June 30, 2013, December 31, 2012 and December 31, 2009 were, in millions, $44.7, $28.6 and $5.3, respectively. |

| (4) | Standardized Measure represents the present value of estimated future net cash flows from proved reserves, less estimated future development, production, plugging and abandonment costs and income tax expenses, discounted at 10% per annum to reflect the timing of future cash flows. Standardized Measure is not an estimate of the fair market value of our properties. |

S-3

Table of Contents

The following table presents certain summary data for each of our operating areas at and for the six months ended June 30, 2013, except as otherwise provided below:

| Net Acreage(1) | Producing Wells(1) | Total Engineered Drilling Locations(2) | Estimated Net Proved Reserves(3) | PV-10(4) | Avg. Daily Production | |||||||||||||||||||||||||||||||

| Gross | Net | Gross | Net | MBOE(5) | % Developed | (In millions) | (BOE/d)(5)(6) | |||||||||||||||||||||||||||||

South Texas: | ||||||||||||||||||||||||||||||||||||

Eagle Ford(7) | 27,233 | 59.0 | 51.3 | 269.0 | 218.4 | 15,664 | 58.7 | $ | 467.2 | 9,308 | ||||||||||||||||||||||||||

NW Louisiana/East Texas: | ||||||||||||||||||||||||||||||||||||

Haynesville | 14,499 | 136.0 | 12.9 | 515.0 | 102.1 | 20,998 | 24.6 | 41.9 | 2,732 | |||||||||||||||||||||||||||

Cotton Valley(8) | 22,469 | 106.0 | 69.7 | 71.0 | 49.3 | 1,765 | 100.0 | 10.3 | 630 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Area Total(9) | 25,291 | 242.0 | 82.6 | 586.0 | 151.4 | 22,763 | 30.4 | 52.2 | 3,362 | |||||||||||||||||||||||||||

Permian Basin: | ||||||||||||||||||||||||||||||||||||

SE New Mexico, West Texas(10) | 32,899 | 13.0 | 5.8 | 107.0 | 74.5 | 504 | 18.9 | 2.9 | 19 | |||||||||||||||||||||||||||

Other: | ||||||||||||||||||||||||||||||||||||

Wyoming, Utah, Idaho | 36,004 | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total | 121,427 | 314.0 | 139.7 | 962.0 | 444.3 | 38,931 | 41.7 | $ | 522.3 | 12,689 | ||||||||||||||||||||||||||

| (1) | Net acreage and producing well information is presented at September 1, 2013. |

| (2) | Identified and engineered drilling location information is presented at September 1, 2013. These locations have been identified for potential future drilling (other than the two test wells already drilled or in process, which are included in the drilling locations for the Permian Basin) and are not currently producing. In addition, the total net engineered drilling locations is calculated by multiplying the gross engineered drilling locations in an operating area by our working interest participation in such locations. At September 1, 2013, these engineered drilling locations included 25 gross (23.0 net) locations to which we have assigned proved undeveloped reserves in the Eagle Ford, 92 gross (12.1 net) locations to which we have assigned proved undeveloped reserves in the Haynesville and two gross (1.2 net) locations to which we have assigned proved undeveloped reserves in the Wolfcamp. We had no proved undeveloped reserves assigned to identified drilling locations in the Cotton Valley at September 1, 2013. |

| (3) | These estimates were prepared by our engineering staff and audited by Netherland, Sewell & Associates, Inc., independent reservoir engineers. |

| (4) | See Note 3 to the table on page S-3. Our PV-10 at June 30, 2013 may be reconciled to our Standardized Measure of discounted future net cash flows at such date by reducing our PV-10 by the discounted future income taxes associated with such reserves. The discounted future income taxes at June 30, 2013 were approximately $44.7 million. |

| (5) | Estimated using a conversion ratio of one Bbl of oil per six Mcf of natural gas. |

| (6) | During the months of June and July 2013. |

| (7) | Includes two wells producing small quantities of natural gas from the San Miguel formation, two wells producing from the Austin Chalk formation in Zavala County, Texas and one well producing from the Buda formation in Atascosa County, Texas. |

| (8) | Includes the Cotton Valley formation and shallower zones and also includes one well producing from the Frio formation in Orange County, Texas. |

| (9) | Some of the same leases cover the net acres shown for both the Haynesville formation and the Cotton Valley formation, a shallower formation than the Haynesville formation. Therefore, the sum of the net acreage for both formations is not equal to the total net acreage for Northwest Louisiana and East Texas. This total includes acreage that we are producing from or that we believe to be prospective for these formations. |

| (10) | Includes potential future drilling locations identified in either the Wolfcamp or Bone Spring plays on our acreage in Southeast New Mexico and West Texas at September 1, 2013. |

S-4

Table of Contents

At September 1, 2013, our interests included approximately 38,900 gross (27,200 net) acres in the Eagle Ford shale play in Atascosa, DeWitt, Gonzales, Karnes, La Salle, Wilson and Zavala Counties in South Texas. We believe that approximately 87% of our Eagle Ford acreage is prospective predominantly for oil or liquids production. In addition, we believe that portions of this acreage may also be prospective for other targets, such as the Austin Chalk, Buda, Edwards and Pearsall formations, from which we would expect to produce predominantly oil and liquids.

At September 1, 2013, we had 54 gross (47.1 net) wells producing from the Eagle Ford shale in South Texas, and we had identified 269 gross (218.4 net) locations for potential future drilling on our Eagle Ford acreage. Of these locations, at September 1, 2013, we consider 155 gross (129.3 net) locations as Tier 1 locations. We define Tier 1 Eagle Ford locations as those locations that we anticipate to have estimated ultimate recoveries of 225,000 Bbl of oil or greater. Of these Tier 1 locations, 117 gross (114.1 net) locations would be operated by us. These identified locations presume that we will be able to develop our Eagle Ford properties on 40-acre to 80-acre spacing, depending on the specific property and the wells we have already drilled.

At September 1, 2013, our interests also included approximately 50,800 gross (32,900 net) acres in the Permian Basin in Southeast New Mexico and West Texas where we are developing new oil prospects. At September 1, 2013, we had identified 107 gross (74.5 net) locations for potential future drilling in the Wolfcamp or Bone Spring plays on our acreage in Southeast New Mexico and West Texas, including the two test wells already drilled or in process.

In addition, at September 1, 2013, we had leasehold and mineral interests in approximately 22,600 gross (14,500 net) acres in the Haynesville shale play. This acreage includes approximately 6,100 net acres in what we believe to be the core area of the play. Approximately 97% of our Haynesville acreage is held by production or consists of fee mineral interests that we own. Portions of this acreage are also producing from and, we believe, prospective for the Cotton Valley, Hosston (Travis Peak) and other shallower formations. At September 1, 2013, we had identified 515 gross (102.1 net) locations for potential future drilling in the Haynesville shale, including 440 gross (51.2 net) locations within the 6,100 net acres that we believe are located in the core area of the play. We also had identified 71 gross (49.3 net) locations for potential future drilling in the Cotton Valley. We have no plans to drill any operated Haynesville shale or Cotton Valley wells in 2013, but during the six months ended June 30, 2013, we participated in five gross (0.4 net) non-operated Haynesville wells, and we expect to participate in additional non-operated Haynesville wells in the second half of 2013. As a result of the improvement in natural gas prices, we added approximately 80.1 Bcf (13.3 million BOE) of proved undeveloped natural gas reserves in the Haynesville shale in Northwest Louisiana to our total proved reserves at June 30, 2013, most of which are attributable to non-operated properties.

We may identify and develop additional locations across our asset portfolio as we further evaluate our properties, particularly in South Texas and Southeast New Mexico and West Texas. We believe our multi-year, engineered drilling inventory and exploration portfolio should provide near-term growth in our production and reserves.

S-5

Table of Contents

Business Strategies

Our goal is to increase shareholder value by building reserves, production and cash flows at an attractive rate of return on invested capital. We plan to achieve our goal by executing the following strategies:

| Ÿ | Focus exploration and development activity on our Eagle Ford acreage. |

We have established a core acreage position in the Eagle Ford shale play in South Texas. We currently intend to allocate 78% of our increased 2013 capital expenditure budget to the exploration, development and acquisition of additional interests in the Eagle Ford shale play. At September 1, 2013, approximately 72% of our Eagle Ford acreage was held by production. This acreage position provides us the flexibility to develop our Eagle Ford properties in a disciplined and economical manner in order to maximize the resource recovery from these assets. We intend to operate two drilling rigs in the Eagle Ford shale for the remainder of 2013 and throughout 2014.

| Ÿ | Explore and develop our Wolfcamp and Bone Spring acreage in the Permian Basin. |

We also have established a core acreage position in the Permian Basin in Southeast New Mexico and West Texas, which we believe is prospective for the Wolfcamp, Bone Spring and other oil and liquids-rich targets. Between January 1, 2013 and September 1, 2013, we added approximately 35,000 gross (26,800 net) acres to this leasehold position, primarily in Lea and Eddy Counties, New Mexico. We currently intend to allocate 20% of our increased 2013 capital expenditure budget to the exploration, development and acquisition of additional interests in the Wolfcamp and Bone Spring plays. We moved a contracted drilling rig to this area in late April 2013 and are currently drilling a three-well test program to evaluate various portions of our acreage in Southeast New Mexico and West Texas. As a result of our recent acreage acquisitions in this area, the preliminary indications from our drilling program and the production results from nearby operators, we now expect to keep this rig operating continuously for the remainder of 2013 and throughout 2014.

| Ÿ | Identify, evaluate and develop oil and natural gas plays to maintain a balanced portfolio. |

In late 2010, we began to focus on oil and liquids-rich shale plays to create a more balanced portfolio of oil and natural gas producing properties. Oil production comprised approximately 47% of our total production during the first six months of 2013, and approximately 31% of our total estimated proved reserves at June 30, 2013 were attributable to oil. We believe our interests in the Eagle Ford shale play and the Wolfcamp and Bone Spring plays will enable us to maintain a more balanced commodity portfolio through the drilling of locations that are prospective for oil and liquids. We estimate that approximately 98% of our increased 2013 and our preliminary 2014 capital expenditure budgets will be directed to oil and liquids opportunities. We expect to continue to create and opportunistically acquire additional prospects for the exploration and production of oil and liquids. We also have an established acreage position in the Haynesville shale play that is prospective for natural gas, with approximately 6,100 of our net acres, at September 1, 2013, located in what we believe is the core area of the play. Approximately 97% of our Haynesville acreage was held by production or consisted of fee mineral interests that we owned at September 1, 2013, and, as a result, the potential drilling locations we have identified remain available to be drilled by us or the operator at a future time.

S-6

Table of Contents

| Ÿ | Continue to improve operational and cost efficiencies. |

We focus on optimizing the development of our resource base by seeking ways to maximize our recovery per well relative to the cost incurred and to minimize our operating cost per BOE produced. We apply an analytical approach to track and monitor the effectiveness of our drilling and completion techniques and service providers. This allows us to manage more effectively operating costs, the pace of development activities, technical applications, the gathering and marketing of our production and capital allocation. Additionally, we concentrate on our core areas, which allows us to achieve economies of scale and reduce operating costs. Largely as a result of these factors, between early 2011 and September 1, 2013, we have reduced average drilling and completion costs per gross well from approximately $9.9 million to approximately $6.3 million in our western Eagle Ford acreage, from approximately $11.0 million to approximately $7.1 million in our central Eagle Ford acreage and from approximately $10.4 million to approximately $8.3 million in our eastern Eagle Ford acreage. We have also achieved a decrease in drilling days from spud to total depth over this timeframe from approximately 19 days to approximately eight days in our western Eagle Ford acreage, from approximately 19 days to approximately 14 days in our central Eagle Ford acreage and from approximately 25 days to approximately 17 days in our eastern Eagle Ford acreage. In mid-August 2013, we began drilling certain wells on our western Eagle Ford acreage from four-well batch drilled pads, which we anticipate may reduce costs by an additional $300,000 per well. Over the past 18 months, we have also refined the design of our hydraulic fracture treatments to enhance well productivity, increasing proppant volumes from approximately 1,250 pounds per foot to approximately 1,715 pounds per foot and increasing fluid volumes from approximately 19 Bbl per foot to approximately 39 Bbl per foot.

| Ÿ | Maintain our financial discipline. |

We seek to maintain a strong balance sheet and have conducted our drilling and completion operations since inception using equity capital contributions from our investors, revolving borrowings under our credit facility and cash flows from our operations. In addition, from time to time, we use derivative financial instruments to mitigate our exposure to commodity price risk associated with oil, natural gas and natural gas liquids prices and to protect our cash flows and borrowing capacity. At August 26, 2013, we had the following hedges in place, in the form of costless collars and swaps, for the remainder of 2013 and for 2014: (i) approximately 0.8 million Bbl and 2.3 million Bbl of oil, respectively, (ii) approximately 3.3 Bcf and 8.4 Bcf of natural gas, respectively, and (iii) approximately 5.0 million and 5.1 million gallons of natural gas liquids, respectively.

| Ÿ | Pursue opportunistic acquisitions. |

We believe our management team’s familiarity with our key operating areas and its contacts with the operators and mineral owners in those regions enable us to identify high-return opportunities at attractive prices. We actively pursue opportunities to acquire unproved and unevaluated acreage, drilling prospects and low-cost producing properties within our core areas of operations where we have operational control and can enhance value and performance. We view these acquisitions as an important component of our business strategy and intend to selectively pursue acquisitions on attractive terms that complement our strategy and help us achieve economies of scale.

S-7

Table of Contents

Competitive Strengths

We believe our prior success is, and our future performance will be, directly related to the following combination of strengths that will enable us to implement our strategies:

| Ÿ | High quality asset base in the Eagle Ford shale and the Wolfcamp and Bone Spring plays in the Permian Basin. |

We have key acreage positions in active areas of the Eagle Ford shale play in South Texas and the Wolfcamp and Bone Spring plays in the Permian Basin in Southeast New Mexico and West Texas. The commodity mix of our production and reserves has become more balanced as a result of our activities on our Eagle Ford acreage, approximately 87% of which is located in oil and liquids-rich areas of the play. We believe that portions of this acreage may also be prospective for other targets, such as the Austin Chalk, Buda, Edwards and Pearsall formations. We believe our acreage in the Permian Basin is prospective for multiple oil and liquids-rich targets, including the Wolfcamp and Bone Spring formations, as well as other potential shallower (Delaware) and deeper (Atoka, Morrow) targets. In addition, our acreage position in the Haynesville shale provides us with a natural gas option as we have 515 gross (102.1 net) locations that could be developed from the play should natural gas prices improve from recent levels. In addition to the Haynesville shale play, our East Texas and Northwest Louisiana assets have multiple, recognized geologic horizons, including the Cotton Valley and Hosston (Travis Peak) formations from which we have previously established production, as well as the Middle Bossier shale.

| Ÿ | Large, multi-year, development drilling inventory that is responding to new technologies. |

In South Texas, at September 1, 2013, we had 59 gross (51.3 net) producing wells and had identified 269 gross (218.4 net) additional drilling locations in the Eagle Ford shale play, of which we consider 155 gross (129.3 net) locations as Tier 1 locations. In the Permian Basin, we have identified 107 gross (74.5 net) locations for potential future drilling in the Wolfcamp and Bone Spring plays. We have also identified 586 gross (151.4 net) drilling locations in the Haynesville and Cotton Valley plays. At September 1, 2013, these identified drilling locations included 25 gross (23.0 net) locations in the Eagle Ford shale, two gross (1.2 net) locations in the Wolfcamp play and 92 gross (12.1 net) locations in the Haynesville shale to which we have assigned proved undeveloped reserves. Additionally, we may identify and develop additional locations across our asset portfolio as we further evaluate our properties and apply new technologies to develop such assets, particularly in South Texas and Southeast New Mexico and West Texas. We believe our multi-year, engineered drilling inventory and exploration portfolio provide visible near-term growth in our production and reserves and highlight the long-term resource potential across our asset base.

| Ÿ | Financial flexibility to fund expansion. |

We maintain a financial profile that provides operational flexibility, and our capital structure provides us with the ability to execute our business plan. At August 31, 2013, the borrowing base under our revolving credit facility was $350.0 million, and we had outstanding borrowings of $275.0 million. At June 30, 2013, on an as adjusted basis after giving effect to this offering and the use of proceeds therefrom, we expect to have at least $156.6 million available for borrowings under our revolving credit facility after giving effect to approximately $1.2 million of outstanding letters of credit. See “—Recent Developments—Credit Facility.” Excluding any possible significant acquisitions, we expect to maintain our current financial flexibility by funding the remainder of our 2013 and our 2014 capital expenditure budget through the net proceeds we receive from this

S-8

Table of Contents

offering, together with our cash flows and future potential borrowings under our revolving credit facility assuming anticipated increases to our borrowing base, primarily as a result of anticipated increases in our proved developed oil and natural gas reserves. Our availability of capital should allow us to maintain our competitiveness in seeking to acquire additional oil and natural gas leasehold acreage in the ordinary course of our business and to accelerate the evaluation and development of our Wolfcamp and Bone Spring plays as a result of our decision to operate one drilling rig continuously in the Permian Basin in Southeast New Mexico and West Texas for the remainder of 2013 and throughout 2014. In addition, since a large portion of our acreage, excluding the acreage acquired during 2013 in Southeast New Mexico and West Texas, is held by production, we have the financial flexibility to allocate our capital when and where we believe it is economical and justified.

| Ÿ | Experienced and incentivized management, technical teams and board. |

As an operator, we leverage advanced technologies and integrate the knowledge, judgment and experience of our management and senior technical teams. Our management team averages eight years of service to the Company, and our management and senior technical teams possess extensive oil and natural gas expertise with an average of over 25 years of relevant industry experience from companies such as Matador Petroleum Corporation, S. A. Holditch & Associates, Inc., Schlumberger Limited, Conoco and ARCO, and we believe they have a demonstrated record of growth and financial discipline over many years. Additionally, we have a group of board members and special advisors with considerable experience and expertise in the oil and natural gas industry and in managing other successful enterprises who provide insight and perspective regarding our business and the evaluation, exploration, engineering and development of our prospects. Our directors and special advisors average over six years of service to the Company. Many of our directors and advisors were also involved in our predecessor, Matador Petroleum Corporation, as directors, advisors or shareholders. In addition to their considerable experience, our management team and board own a significant ownership interest in the Company. We believe our management team’s and board’s ownership interest of over 11% of our outstanding common stock, at September 1, 2013, as well as their ability to increase their holdings over time through our long-term incentive plan, aligns management’s and the board’s interests with those of our shareholders.

| Ÿ | Extensive geologic, engineering and operational experience in unconventional reservoir plays. |

The individuals on our technical team are highly experienced in analyzing unconventional reservoir plays and in horizontal drilling, completion and production operations in a number of geographic areas. Our geologists have extensive experience in analyzing unconventional reservoir plays throughout the United States, including our principal areas of interest, by using advanced imaging technology, such as 2-D and 3-D seismic interpretation, and petrophysical analysis. By employing the latest technologies, since 2011 our technical team has been able to reduce drilling times, improve our hydraulic fracturing design and increase production from our wells. In addition, our technical team has been directly involved in over 30 different horizontal well drilling and/or operations programs in both onshore and offshore formations located in the United States and abroad. Our team’s experience also includes drilling and completing hundreds of vertical and horizontal wells in unconventional resource plays, including the Cotton Valley, Bossier, Wilcox/Vicksburg, Austin Chalk, Haynesville, Eagle Ford and Wolfcamp and Bone Spring plays. Our team’s diverse and broad drilling experience includes most, if not all, techniques used in modern day drilling. Additionally, our team has in-depth experience with various horizontal completion techniques and their

S-9

Table of Contents

applications in multiple unconventional plays. We intend to leverage our team’s geological expertise and horizontal drilling and completion experience to continue to develop and exploit our large, multi-year development drilling inventory.

| Ÿ | Multi-disciplined approach to new opportunities. |

Our process for evaluating and developing new oil and natural gas prospects is a result of what we believe is an organizational philosophy that is dedicated to a systematic, multi-disciplinary approach to new opportunities with an emphasis on incorporating petroleum systems, geosciences, technology and finance into the decision-making process. We recognize the importance of consulting multiple individuals in our organization across all disciplines and all levels of responsibility prior to making exploration, acquisition or development decisions. In order to enhance our decision-making, we also identify what we believe to be key criteria for successful exploration and development projects in any given play. After major decisions are made, we conduct a post-completion review to determine what we did right and where we need to improve. At times, this approach results in a decision to accelerate our drilling program or expand our positions in certain areas. Other times, this approach results in a decision to mitigate risk associated with our exploration and development programs by sharing operational risks and costs with other industry participants or exiting an area altogether. We believe this multi-disciplined approach underpins our track record of value creation and represents the best way to deliver consistent, year-over-year results to our shareholders.

2013 Capital Program and 2014 Outlook

Our drilling activity has been and will continue to be focused on increasing our oil production and reserves in South Texas, primarily in the Eagle Ford shale play. We had two contracted drilling rigs operating continuously during the six months ended June 30, 2013. During the first quarter of 2013, both of these rigs were operating in the Eagle Ford shale in South Texas, and all of our operated drilling and completion activities were focused on the Eagle Ford shale. In late April 2013, we moved one of our two contracted drilling rigs to Southeast New Mexico to begin a three-well exploration program testing portions of our growing leasehold position in the Permian Basin. In mid-August 2013, we added a third drilling rig and returned to operating two contracted drilling rigs in the Eagle Ford shale play in South Texas. At September 1, 2013, one rig was drilling on our leasehold acreage in Karnes County, Texas, and the second rig was drilling on our leasehold acreage in La Salle County, Texas. We expect to operate two rigs in the Eagle Ford shale for the remainder of 2013 and throughout 2014. As a result of our recent acreage acquisitions in Southeast New Mexico and West Texas, the preliminary indications from our drilling program and the production results from nearby operators, we intend to operate one contracted drilling rig continuously in Southeast New Mexico and West Texas for the remainder of 2013 and throughout 2014. As a result of adding a third drilling rig, we have increased our 2013 capital expenditure budget to approximately $370.0 million, of which $168.6 million, or approximately 46%, was incurred in the first six months of 2013.

We expect that approximately 78% of our increased 2013 capital expenditure budget will be directed to increasing our oil production and oil reserves in South Texas. We also plan to allocate approximately 20% of our increased 2013 capital expenditure budget to the exploration and acquisition of additional interests in the Wolfcamp, Bone Spring and other oil and liquids-rich plays in Southeast New Mexico and West Texas. As a result of these anticipated capital expenditures in South Texas, Southeast New Mexico and West Texas, we plan to allocate approximately 98% of our 2013 anticipated capital expenditure budget to opportunities prospective for oil and liquids production. We also expect to participate in additional non-

S-10

Table of Contents

operated Haynesville shale wells during the remainder of 2013 and in 2014. Our preliminary 2014 capital expenditure budget is estimated at between $425 million and $450 million, and includes approximately $400 million for drilling and completing oil and natural gas exploration and development wells with the remainder allocated to lease acquisitions, seismic data, pipelines and other infrastructure. We intend to allocate approximately 98% of our preliminary 2014 capital expenditure budget to opportunities prospective for oil and liquids production.

Our remaining 2013 and 2014 capital expenditure budgets are subject to change depending upon a number of factors, including additional well results and other data from the Eagle Ford shale and the Wolfcamp and Bone Spring plays, results of horizontal and vertical drilling and recompletions, economic and industry conditions, prevailing and anticipated prices for oil, natural gas liquids and natural gas, the availability of sufficient capital resources for drilling prospects, potential acquisitions and our financial results.

Recent Developments

Credit Facility

On September 28, 2012, we entered into the third amended and restated Credit Agreement, which increased the maximum facility amount to $500.0 million from $400.0 million. On August 7, 2013, the borrowing base under our revolving credit facility was increased to $350.0 million from $280.0 million, and the conforming borrowing base was increased to $275.0 million, based on the lenders’ review of our proved oil and natural gas reserves at June 30, 2013. Also on August 7, 2013, we amended the Credit Agreement to provide that the borrowing base will automatically be reduced to the then applicable conforming borrowing base at the earlier of (i) June 30, 2014 or (ii) concurrent with our issuance of senior unsecured notes in an amount greater than or equal to $10.0 million.

We intend to use this additional borrowing capacity, along with our estimated cash flows from operations, to fund our drilling operations and for the acquisition of additional leasehold interests primarily in South Texas and Southeast New Mexico and West Texas. We expect additional increases to the borrowing base will primarily be a result of anticipated increases in our proved oil and natural gas reserves, and particularly our proved developed oil and natural gas reserves.

Additional Drilling Rig

We had two contracted drilling rigs operating continuously during the six months ended June 30, 2013. During the first quarter of 2013, both of these rigs were operating in the Eagle Ford shale in South Texas, and all of our operated drilling and completion activities were focused on the Eagle Ford shale in that area. In late April 2013, we moved one of these contracted drilling rigs to Southeast New Mexico to begin a three-well exploration program testing portions of our leasehold position in the Permian Basin in Southeast New Mexico and West Texas. In mid-August 2013, we added a third drilling rig and returned to operating two contracted drilling rigs in the Eagle Ford shale play. As a result, at September 1, 2013, we had three contracted drilling rigs operating — one each in Karnes County, Texas, La Salle County, Texas and Lea County, New Mexico. We plan to operate three rigs for the remainder of 2013 and throughout 2014.

Acreage Acquisitions

Between January 1 and September 1, 2013, we acquired approximately 35,000 gross (26,800 net) acres in the Permian Basin in Southeast New Mexico and West Texas, primarily in Lea and Eddy Counties, New Mexico. Including these acreage acquisitions, at September 1, 2013, our total acreage position in

S-11

Table of Contents

Southeast New Mexico and West Texas was approximately 50,800 gross (32,900 net) acres, of which we consider 43,100 gross (32,300 net) acres to be prospective for multiple oil and liquids-rich targets, including the Wolfcamp and Bone Spring plays.

Recent Production

During June and July 2013, our average daily production increased to 6,200 Bbl of oil per day, as compared to 4,825 Bbl per day for the first five months of 2013. In addition, following the recent completion of three new wells on our Cowey lease in DeWitt County, Texas, our natural gas production increased to an average of approximately 38.9 MMcf of natural gas per day during June and July, as compared to 33.8 MMcf per day for the first five months of 2013.

Initial Results from 40-Acre and 50-Acre Downspacing in the Eagle Ford

During the second quarter of 2013, we completed our first 40-acre test well, the Martin Ranch #35H, on our Martin Ranch leasehold in northeast La Salle County. On a 24-hour initial potential test following completion, the well flowed at an average rate of 464 Bbl of oil per day at 1,450 psi surface pressure on a 14/64-in choke, comparable to other recently completed wells on our Martin Ranch lease, and consistent with our practice of flowing back our newly-completed wells on smaller chokes to preserve and manage bottomhole pressure to try and improve long-term well performance and ultimate recoveries. During its first sixty days, this 40-acre offset well’s performance was in line with our expectations and was flowing at an average rate of approximately 300 Bbl of oil per day.

We completed three new wells at approximately 50-acre spacing on our Sickenius lease in Karnes County in July 2013. On 24-hour initial potential tests following completion, these wells flowed at average rates of between 580 and 850 Bbl of oil per day at 2,500 to 3,000 psi surface pressure on 14/64-in chokes. As a result of the initial performance of these downspaced wells, we plan to drill 40-acre infill wells on our nearby Danysh and Pawelek leases in Karnes County beginning this fall.

Corporate Information

We were incorporated in 2003 as a Texas corporation. Our corporate headquarters are located at 5400 LBJ Freeway, Suite 1500, Dallas, Texas 75240, and our telephone number is (972) 371-5200. Our website is located at http://www.matadorresources.com. We have not incorporated by reference into this prospectus supplement or the accompanying prospectus the information included on, or linked from, our website, and you should not consider it to be part of this prospectus supplement or the accompanying prospectus.

S-12

Table of Contents

The Offering

Issuer | Matador Resources Company |

Common Stock Offered | 8,500,000 shares (or up to 9,775,000 shares if the underwriters exercise in full their option to purchase an additional 1,275,000 shares). |

Common Stock to be Outstanding after the Offering(1) | 64,346,162 shares (or up to 65,621,162 shares if the underwriters exercise in full their option to purchase an additional 1,275,000 shares). |

Use of Proceeds | The net proceeds from this offering will be approximately $122.8 million ($141.4 million if the underwriters exercise in full their option to purchase additional shares) after deducting underwriters’ discounts and commissions and estimated offering expenses. We intend to use the net proceeds from this offering, including any net proceeds from the underwriters’ exercise of their option, primarily to fund a portion of our capital expenditures, including for the addition of a third rig to our current two-rig drilling program, allowing us to operate two drilling rigs for the development of our acreage in the Eagle Ford shale play and one drilling rig for the exploration and development of our acreage in the Wolfcamp and Bone Spring plays in the Permian Basin. We also intend to use net proceeds from this offering to fund the acquisition of additional acreage in the Eagle Ford shale, the Permian Basin and the Haynesville shale and for other general working capital needs. Pending such uses, we intend to repay outstanding borrowings under our revolving credit facility, which amounts may be reborrowed in accordance with the terms of that facility. See “Use of Proceeds.” |

Conflicts of Interest | Because affiliates of RBC Capital Markets, LLC, Citigroup Global Markets Inc., Scotia Capital (USA) Inc., SunTrust Robinson Humphrey, Inc., Bank of Montreal, Comerica Securities, Inc. and Capital One Securities, Inc. are lenders under our revolving credit facility and will each receive more than 5% of the net proceeds of this offering due to the repayment of a portion of the revolving credit facility by us, RBC Capital Markets, LLC, Citigroup Global Markets Inc., Scotia Capital (USA) Inc., SunTrust Robinson Humphrey, Inc., Bank of Montreal, Comerica Securities, Inc. and Capital One Securities, Inc. are deemed to have a “conflict of interest” under Rule 5121 (“Rule 5121”) of the Financial Industry Regulatory Authority, Inc. (“FINRA”). Accordingly, this offering is being made in compliance with the requirements of Rule 5121. The appointment |

| (1) | Based on 55,846,162 shares outstanding as of September 1, 2013, and excludes 1,608,594 shares issuable pursuant to the exercise of outstanding stock options and the vesting of restricted stock units. |

S-13

Table of Contents

of a “qualified independent underwriter” is not required in connection with this offering as a “bona fide public market,” as defined in Rule 5121, exists for our common stock. See “Use of Proceeds” and “Underwriting (Conflicts of Interest).” |

Risk Factors | Investing in our common stock involves substantial risks. You should carefully consider the risk factors set forth in the section entitled “Risk Factors” and the other information contained in this prospectus supplement and the accompanying prospectus and the documents incorporated by reference herein, prior to making an investment in our common stock. See “Risk Factors” beginning on page S-21 of this prospectus supplement. |

NYSE Symbol | MTDR |

S-14

Table of Contents

Summary Historical Financial Data

We derived the summary historical financial data as of and for the years ended December 31, 2010, 2011, and 2012 from our audited consolidated financial statements included in our Annual Reports on Form 10-K for the years ended December 31, 2011 and December 31, 2012. We derived the summary historical financial data as of and for the six months ended June 30, 2012 and 2013 from our unaudited condensed consolidated financial statements included in our Quarterly Reports on Form 10-Q for the quarters ended June 30, 2012 and June 30, 2013.

The following table should be read together with, and is qualified in its entirety by reference to, the historical combined financial statements and the accompanying notes incorporated by reference into this prospectus supplement. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the year ended December 31, 2012 and in our Quarterly Report on Form 10-Q for the quarter ended June 30, 2013, which are incorporated by reference into this prospectus supplement, for a discussion of the factors that affect comparability of the information reflected in the summary consolidated financial and operating data.

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||

| (In thousands, except per share data) | (Unaudited) | (Unaudited) | ||||||||||||||||||

Statement of operations data: | ||||||||||||||||||||

Revenues | ||||||||||||||||||||

Oil and natural gas revenues | $ | 155,998 | $ | 67,000 | $ | 34,042 | $ | 117,498 | $ | 65,242 | ||||||||||

Realized gain on derivatives | 13,960 | 7,106 | 5,299 | 646 | 7,776 | |||||||||||||||

Unrealized (loss) gain on derivatives | (4,802 | ) | 5,138 | 3,139 | 2,701 | 11,844 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total revenues | 165,156 | 79,244 | 42,480 | 120,845 | 84,862 | |||||||||||||||

Expenses | ||||||||||||||||||||

Production taxes and marketing | 11,672 | 6,278 | 1,982 | 8,548 | 4,783 | |||||||||||||||

Lease operating | 28,184 | 7,244 | 5,284 | 21,040 | 11,020 | |||||||||||||||

Depletion, depreciation and amortization | 80,454 | 31,754 | 15,596 | 48,466 | 31,119 | |||||||||||||||

Accretion of asset retirement obligations | 256 | 209 | 155 | 161 | 111 | |||||||||||||||

Full-cost ceiling impairment | 63,475 | 35,673 | — | 21,229 | 33,205 | |||||||||||||||

General and administrative | 14,543 | 13,394 | 9,702 | 8,751 | 7,882 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total expenses | 198,584 | 94,552 | 32,719 | 108,195 | 88,120 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating (loss) income | (33,428 | ) | (15,308 | ) | 9,761 | 12,650 | (3,258 | ) | ||||||||||||

Other income (expense) | ||||||||||||||||||||

Net loss on asset sales and inventory impairment | (485 | ) | (154 | ) | (224 | ) | (192 | ) | (60 | ) | ||||||||||

Interest expense | (1,002 | ) | (683 | ) | (3 | ) | (2,880 | ) | (309 | ) | ||||||||||

Interest and other income | 224 | 315 | 364 | 115 | 103 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total other (expense) income | (1,263 | ) | (522 | ) | 137 | (2,957 | ) | (266 | ) | |||||||||||

Net (loss) income | $ | (33,261 | ) | $ | (10,309 | ) | $ | 6,377 | $ | 9,615 | $ | (2,875 | ) | |||||||

Earnings (loss) per common share | ||||||||||||||||||||

Basic | ||||||||||||||||||||

Class A | $ | (0.62 | ) | $ | (0.25 | ) | $ | 0.15 | $ | 0.17 | $ | (0.06 | ) | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Class B(1) | $ | (0.35 | ) | $ | 0.02 | $ | 0.42 | $ | — | $ | 0.07 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Diluted | ||||||||||||||||||||

Class A | $ | (0.62 | ) | $ | (0.25 | ) | $ | 0.15 | $ | 0.17 | $ | (0.06 | ) | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Class B(1) | $ | (0.35 | ) | $ | 0.02 | $ | 0.42 | $ | — | $ | 0.07 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Class B dividend declared, per share(1) | $ | 0.27 | $ | 0.27 | $ | 0.27 | $ | — | $ | 0.13 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

S-15

Table of Contents

| At December 31, | At June 30, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||

| (In thousands) | (Unaudited) | (Unaudited) | ||||||||||||||||||

Balance sheet data (end of period): | ||||||||||||||||||||

Cash and cash equivalents | $ | 2,095 | $ | 10,284 | $ | 21,060 | $ | 5,105 | $ | 9,432 | ||||||||||

Certificates of deposit | 230 | 1,335 | 2,349 | 61 | 266 | |||||||||||||||

Net property and equipment | 591,090 | 399,865 | 303,880 | 690,255 | 482,592 | |||||||||||||||

Total assets | 632,029 | 439,469 | 346,382 | 734,711 | 537,689 | |||||||||||||||

Current liabilities | 96,492 | 74,576 | 30,228 | 91,738 | 64,062 | |||||||||||||||

Long-term liabilities | 156,433 | 93,378 | 34,277 | 252,948 | 65,850 | |||||||||||||||

Total shareholders’ equity | $ | 379,104 | $ | 271,515 | $ | 281,877 | $ | 390,025 | $ | 407,777 | ||||||||||

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||

| (In thousands) | (Unaudited) | (Unaudited) | ||||||||||||||||||

Other financial data: | ||||||||||||||||||||

Net cash provided by operating activities | $ | 124,228 | $ | 61,868 | $ | 27,273 | $ | 83,912 | $ | 51,526 | ||||||||||

Net cash used in investing activities | (306,916 | ) | (160,088 | ) | (147,334 | ) | (175,901 | ) | (136,877 | ) | ||||||||||

Oil and natural gas properties capital expenditures | (300,689 | ) | (156,431 | ) | (159,050 | ) | (173,989 | ) | (134,425 | ) | ||||||||||

Expenditures for other property and equipment | (7,332 | ) | (4,671 | ) | (1,610 | ) | (2,081 | ) | (3,521 | ) | ||||||||||

Net cash provided by financing activities | 174,499 | 87,444 | 36,891 | 94,999 | 84,499 | |||||||||||||||

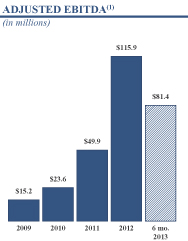

Adjusted EBITDA(2) | $ | 115,923 | $ | 49,911 | $ | 23,635 | $ | 81,444 | $ | 49,264 | ||||||||||

| (1) | Concurrent with the completion of our initial public offering in February 2012, all outstanding shares of Class B common stock were converted to Class A common stock on a one-for-one basis. |

| (2) | Adjusted EBITDA is a non-GAAP financial measure. For a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to our net income (loss) and net cash provided by operating activities, see “—Non-GAAP Financial Measures” below. |

Non-GAAP Financial Measures

We define Adjusted EBITDA as earnings before interest expense, income taxes, depletion, depreciation and amortization, accretion of asset retirement obligations, property impairments, unrealized derivative gains and losses, certain other non-cash items and non-cash stock-based compensation expense, and net gain or loss on asset sales and inventory impairment. Adjusted EBITDA is not a measure of net income or cash flows as determined by GAAP. Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our consolidated financial statements, such as industry analysts, investors, lenders and rating agencies.

Management believes Adjusted EBITDA is necessary because it allows us to evaluate our operating performance and compare the results of operations from period to period without regard to our financing methods or capital structure. We exclude the items listed above from net income (loss) in calculating Adjusted EBITDA because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which certain assets were acquired.

S-16

Table of Contents

Adjusted EBITDA should not be considered an alternative to, or more meaningful than, net income or cash flows from operating activities as determined in accordance with GAAP or as an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDA are significant components of understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure. Our Adjusted EBITDA may not be comparable to similarly titled measures of another company because all companies may not calculate Adjusted EBITDA in the same manner. The following table presents our calculation of Adjusted EBITDA and the reconciliation of Adjusted EBITDA to the GAAP financial measures of net income (loss) and net cash provided by operating activities, respectively.

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2013 | 2012 | |||||||||||||||||||

| (In thousands) | ||||||||||||||||||||||||

Unaudited Adjusted EBITDA Reconciliation to Net Income (Loss): | ||||||||||||||||||||||||

Net (loss) income | $ | (33,261 | ) | $ | (10,309 | ) | $ | 6,377 | $ | (14,425 | ) | $ | 9,615 | $ | (2,875 | ) | ||||||||

Interest expense | 1,002 | 683 | 3 | — | 2,880 | 309 | ||||||||||||||||||

Total income tax (benefit) provision | (1,430 | ) | (5,521 | ) | 3,521 | (9,925 | ) | 78 | (649 | ) | ||||||||||||||

Depletion, depreciation and amortization | 80,454 | 31,754 | 15,596 | 10,743 | 48,466 | 31,119 | ||||||||||||||||||

Accretion of asset retirement obligations | 256 | 209 | 155 | 137 | 161 | 111 | ||||||||||||||||||

Full-cost ceiling impairment | 63,475 | 35,673 | — | 25,244 | 21,229 | 33,205 | ||||||||||||||||||

Unrealized loss (gain) on derivatives | 4,802 | (5,138 | ) | (3,139 | ) | 2,375 | (2,701 | ) | (11,844 | ) | ||||||||||||||

Stock-based compensation expense | 140 | 2,406 | 898 | 656 | 1,524 | (172 | ) | |||||||||||||||||

Net loss on asset sales and inventory impairment | 485 | 154 | 224 | 379 | 192 | 60 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted EBITDA | $ | 115,923 | $ | 49,911 | $ | 23,635 | $ | 15,184 | $ | 81,444 | $ | 49,264 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (In thousands) | ||||||||||||||||||||||||

Unaudited Adjusted EBITDA Reconciliation to Net Cash Provided by Operating Activities: | ||||||||||||||||||||||||

Net cash provided by operating activities | $ | 124,228 | $ | 61,868 | $ | 27,273 | $ | 1,791 | $ | 83,912 | $ | 51,526 | ||||||||||||

Net change in operating assets and liabilities | (9,307 | ) | (12,594 | ) | (2,230 | ) | 15,717 | (5,426 | ) | (2,571 | ) | |||||||||||||

Interest expense | 1,002 | 683 | 3 | — | 2,880 | 309 | ||||||||||||||||||

Current income tax (benefit) provision | — | (46 | ) | (1,411 | ) | (2,324 | ) | 78 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted EBITDA | $ | 115,923 | $ | 49,911 | $ | 23,635 | $ | 15,184 | $ | 81,444 | $ | 49,264 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

S-17

Table of Contents

Summary Production and Reserves Data

The following table sets forth certain unaudited summary data with respect to our production volumes, average sales prices and operating expenses for the periods indicated. The following summary should be read in connection with the discussion under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in our Annual Report on Form 10-K for the year ended December 31, 2012 and our Quarterly Report on Form 10-Q for the period ended June 30, 2013. We determine a barrel of oil equivalent (BOE) using a conversion ratio of one Bbl of oil per six Mcf of natural gas.

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2013 | 2012 | ||||||||||||||||

Unaudited Production Data | ||||||||||||||||||||

Net Production Volumes: | ||||||||||||||||||||

Oil (MBbl) | 1,214 | 154 | 33 | 908 | 485 | |||||||||||||||

Natural gas (Bcf) | 12.5 | 14.5 | 8.4 | 6.2 | 6.2 | |||||||||||||||

Total oil equivalent (MBOE) | 3,294 | 2,573 | 1,433 | 1,944 | 1,525 | |||||||||||||||

Average daily production (BOE/d) | 9,000 | 7,049 | 3,926 | 10,739 | 8,380 | |||||||||||||||

Average Sales Prices: | ||||||||||||||||||||

Oil, with realized derivatives (per Bbl) | $ | 103.55 | $ | 93.80 | $ | 76.39 | $ | 102.27 | $ | 106.54 | ||||||||||

Oil, without realized derivatives (per Bbl) | $ | 101.86 | $ | 93.80 | $ | 76.39 | $ | 102.78 | $ | 105.06 | ||||||||||

Natural gas, with realized derivatives (per Mcf) | $ | 3.55 | $ | 4.11 | $ | 4.38 | $ | 4.07 | $ | 3.42 | ||||||||||

Natural gas, without realized derivatives (per Mcf) | $ | 2.59 | $ | 3.62 | $ | 3.75 | $ | 3.89 | $ | 2.29 | ||||||||||

Operating Expenses (per BOE): | ||||||||||||||||||||

Production taxes and marketing | $ | 3.54 | $ | 2.44 | $ | 1.38 | $ | 4.40 | $ | 3.14 | ||||||||||

Lease operating | $ | 8.56 | $ | 2.82 | $ | 3.69 | $ | 10.82 | $ | 7.23 | ||||||||||

Depletion, depreciation and amortization | $ | 24.43 | $ | 12.34 | $ | 10.89 | $ | 24.93 | $ | 20.40 | ||||||||||

General and administrative | $ | 4.42 | $ | 5.21 | $ | 6.77 | $ | 4.50 | $ | 5.17 | ||||||||||

S-18

Table of Contents

The following table presents summary data with respect to our estimated total proved oil and natural gas reserves as of the dates indicated. Our production and proved reserves are reported in two streams: oil and natural gas, including both dry and liquids-rich natural gas. Where we produce liquids-rich natural gas, such as in the Eagle Ford shale in South Texas, the economic value of the natural gas liquids associated with the natural gas is included in the estimated wellhead natural gas price on those properties where the natural gas liquids are extracted and sold. These reserves estimates were based on evaluations prepared by our engineering staff and have been audited for their reasonableness and conformance with SEC guidelines by Netherland, Sewell & Associates, Inc., independent reservoir engineers. These reserves estimates were prepared in accordance with the SEC’s rules for oil and natural gas reserves reporting. The estimated reserves shown are for proved reserves only and do not include any unproved reserves classified as probable or possible reserves that might exist for our properties, nor do they include any consideration that could be attributable to interests in unproved and unevaluated acreage beyond those tracts for which proved reserves have been estimated. Proved oil and natural gas reserves are the estimated quantities of oil and natural gas which geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. Our total proved reserves are estimated using a conversion ratio of one Bbl of oil per six Mcf of natural gas.

| At June 30, 2013 | At December 31, 2012 | At June 30, 2012 | ||||||||||

Estimated Proved Reserves Data:(1)(2) | ||||||||||||

Estimated proved reserves: | ||||||||||||

Oil (MBbl) | 12,128 | 10,485 | 6,728 | |||||||||

Natural Gas (Bcf)(3) | 160.8 | 80.0 | 73.9 | |||||||||

|

|

|

|

|

| |||||||

Total (MBOE)(4) | 38,931 | 23,819 | 19,052 | |||||||||

|

|

|

|

|

| |||||||

Estimated proved developed reserves: | ||||||||||||

Oil (MBbl) | 6,591 | 4,764 | 3,133 | |||||||||

Natural Gas (Bcf) | 57.8 | 54.0 | 54.0 | |||||||||

|

|

|

|

|

| |||||||

Total (MBOE)(4) | 16,221 | 13,771 | 12,130 | |||||||||

|

|

|

|

|

| |||||||

Percent developed | 41.7 | % | 57.8 | % | 63.7 | % | ||||||

Estimated proved undeveloped reserves: | ||||||||||||

Oil (MBbl) | 5,537 | 5,721 | 3,595 | |||||||||

Natural Gas (Bcf)(3) | 103.0 | 26.0 | 20.0 | |||||||||

|

|

|

|

|

| |||||||

Total (MBOE)(4) | 22,710 | 10,048 | 6,922 | |||||||||

|

|

|

|

|

| |||||||

PV-10(5) (In millions) | $ | 522.3 | $ | 423.2 | $ | 303.4 | ||||||

Standardized Measure(6) (In millions) | $ | 477.6 | $ | 394.6 | $ | 281.5 | ||||||

| (1) | Numbers in table may not total due to rounding. |