GRACIN & MARLOW, LLP

The Chrysler Building

405 Lexington Avenue, 26th Floor

New York, New York 10174

(212) 907-6457

October 2, 2013

VIA EDGAR

United States Securities

and Exchange Commission

100 F Street, NE

Mail Stop 4720

Washington, D.C. 20549

Attention: Tom Kluck

Branch Chief

Re: eBullion, Inc.

Amendment No. 2 to Registration Statement on Form S-1

Filed October 2, 2013

File No. 333-188003

Dear Mr. Kluck:

Thank you for your September 20, 2013 letter regarding eBullion, Inc. (“eBullion”). In order to assist you in your review of eBullion’s Form S-1, we hereby submit a letter responding to the comments and Amendment No. 3 to Form S-1 marked to show changes. For your convenience, we have set forth below the staff’s numbered comments in their entirety followed by our responses thereto.

General

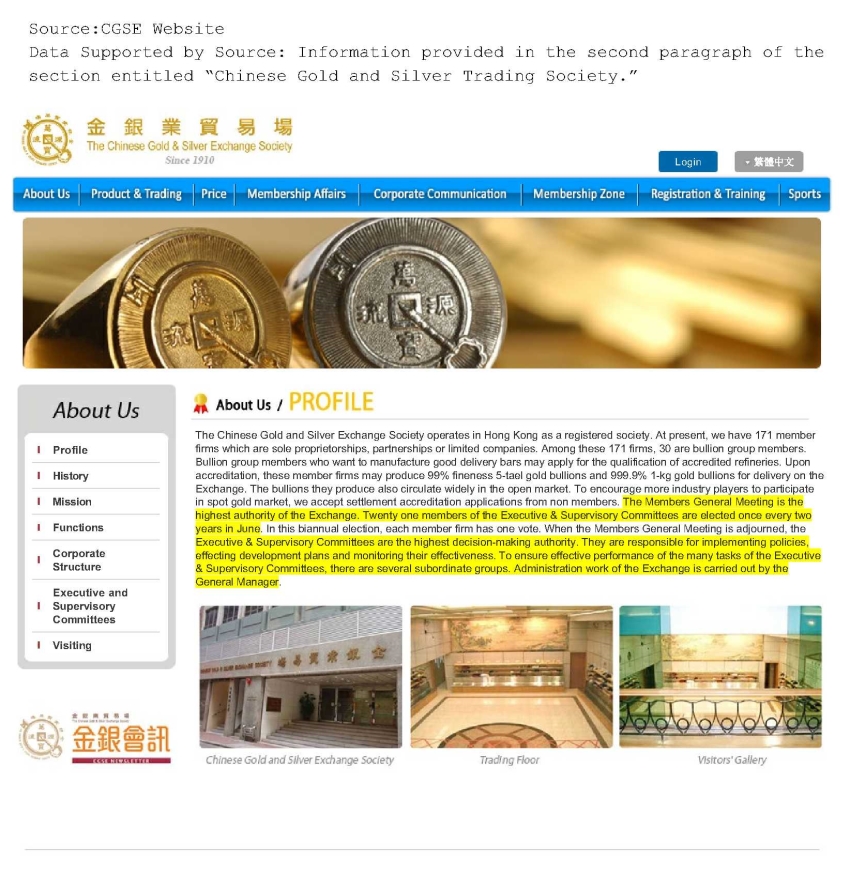

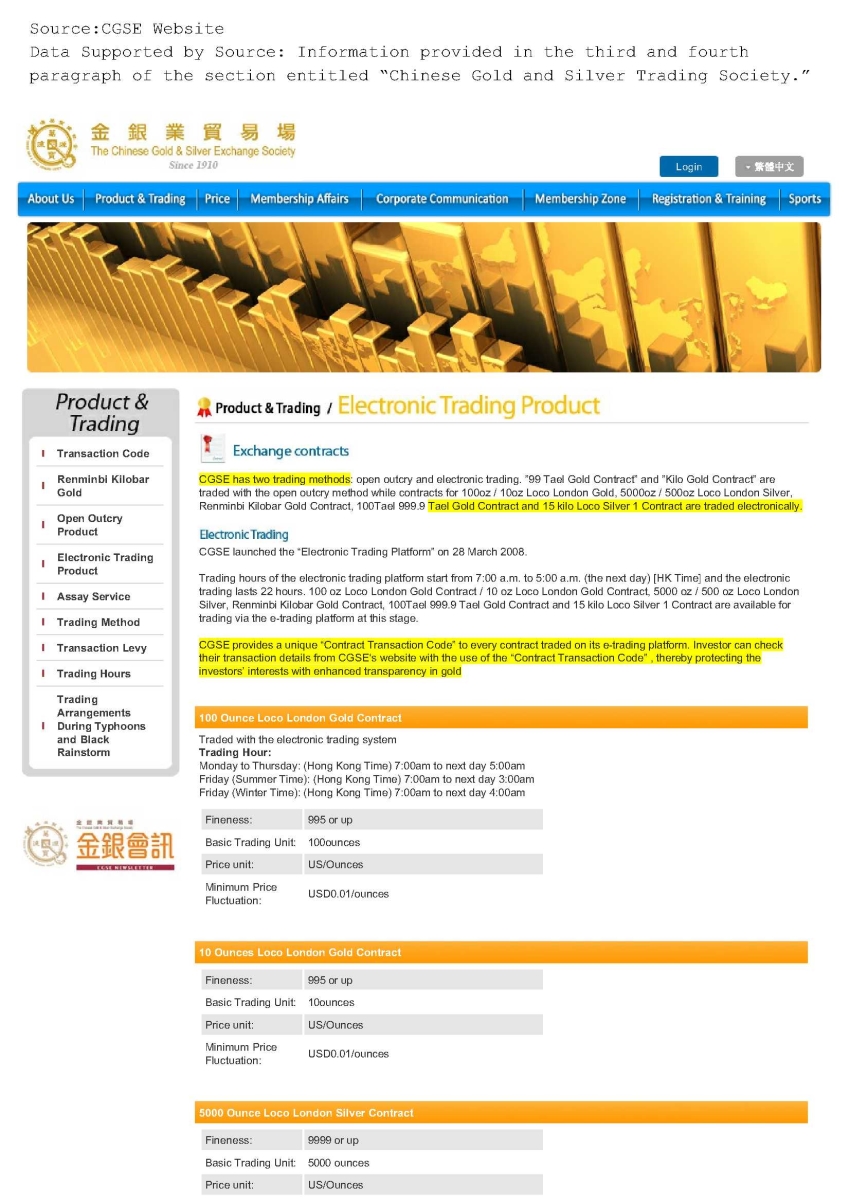

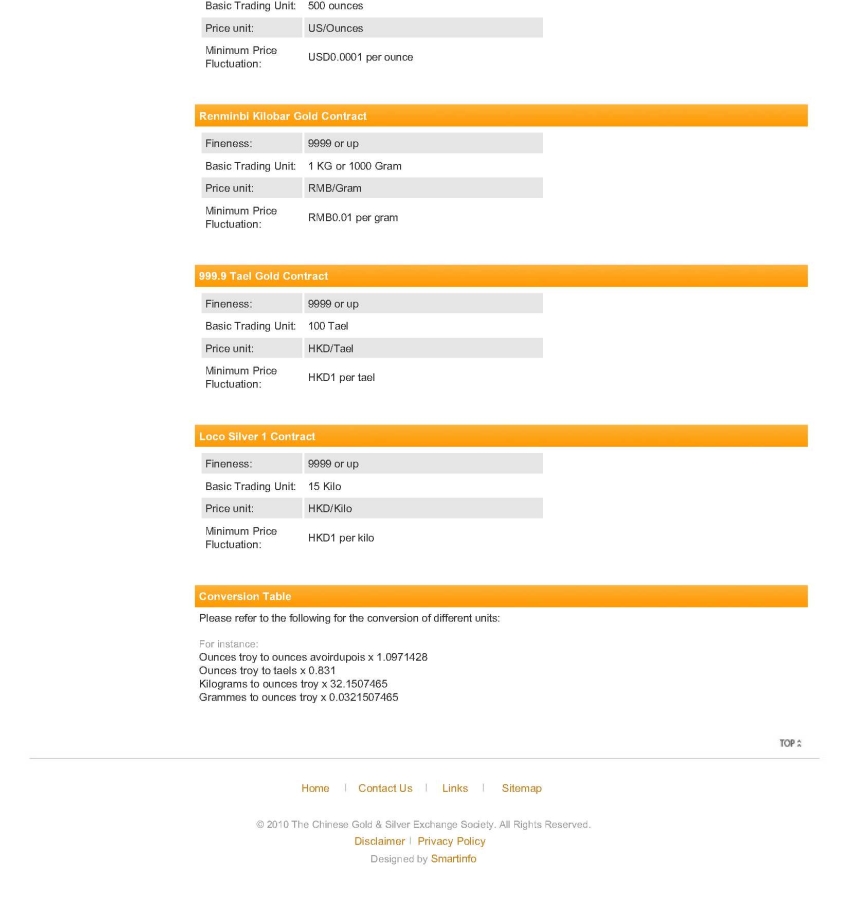

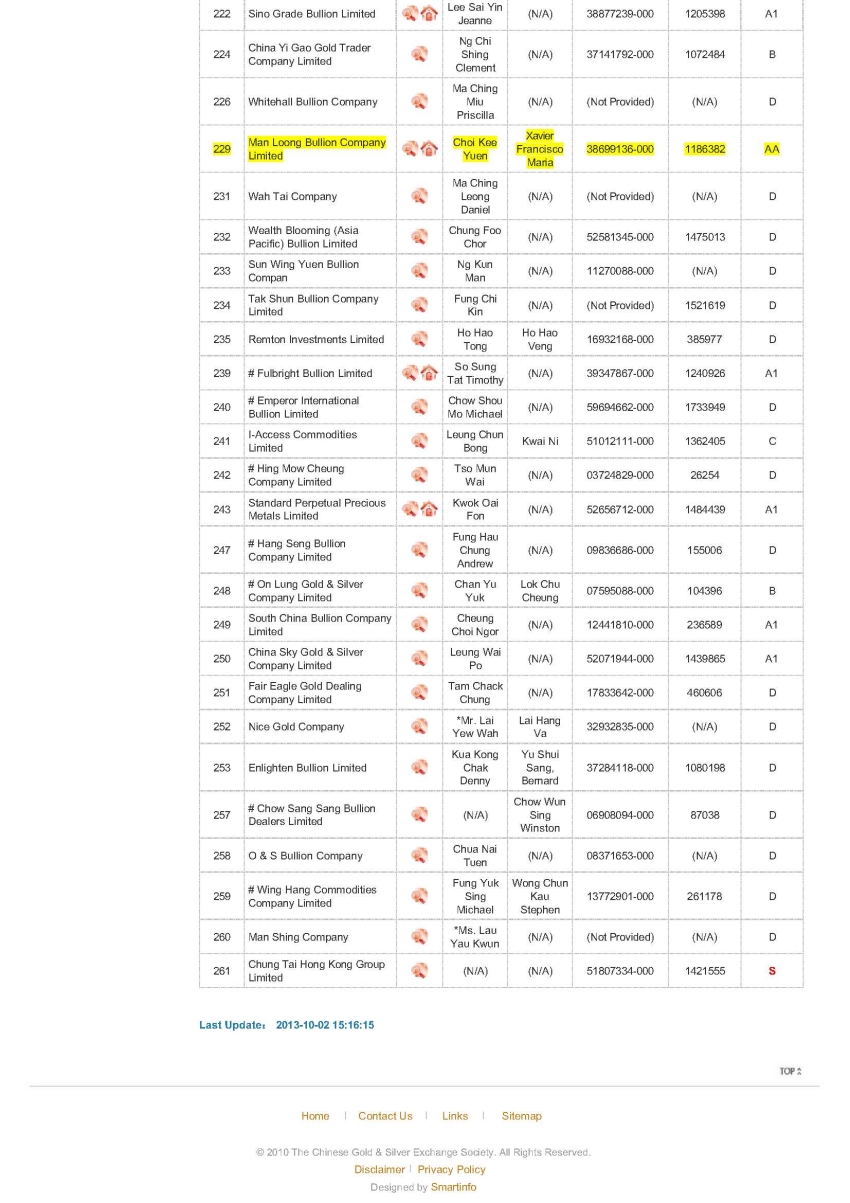

1. We note your response to comment 1 of our comment letter dated July 19, 2013 and the supporting materials you have submitted. We are unable to read the text of the support you labeled “Back Up For Our Industry 3rd Paragraph” and “Back Up For Page 15 Chinese Gold and Silver Society.” Please re-submit these materials in a manner in which they can be read. We also note that, in several instances, the disclosure in your prospectus differs from the support you provided. For example only, we note that you disclose on page 15 in the “Our Industry” section both that “there were 74 companies participating in the trade through the CGSE digital platform, among which 36 were qualified to engage in the trade of Renminbi Kilobar Gold” and “there were 72 companies participating in the trade through the CGSE digital platform, among which 42 were qualified to engage in the trade of Renminbi Kilobar Gold”, while the supporting material labeled “Back Up For Our Industry 4th Paragraph” indicates that “[t]here are . . . 71 companies under the committee participating in the trade through the digital platform, among which 36 are engaging in the trade of Renminbi Kilobar Gold.” In addition, we were unable to locate the support for several quantitative and qualitative business and industry data included in the prospectus. Please provide us with support for all quantitative and qualitative business and industry data used in the prospectus.

Response: We apologize for the quality of the copies of the materials and have resubmitted the materials which we believe provides support for the quantitative and qualitative business and industry data in the Prospectus. Please note that the certain of the information in the Prospectus is more current than the information in the support materials.

United States Securities and Exchange Commission

October 2, 2013

Page 2

2. Please ensure that the disclosure in your registration statement is consistent throughout and revise as appropriate. For example only, we note your disclosure on page 24 identifies that you had dividends paid of $643,984 in the year ended March 31, 2012. However, on page 25 you indicate that Man Loong paid a dividend of $642,984 in the year ended March 31, 2012. Please revise to resolve this inconsistency or advise.

Response: Please note that the difference between $643,984 and $642,984 relates solely to the application in the translation of the dividends in the statement of cash flows of the average exchange rate for the year ended March, 31 2012 and application the actual exchange rate at March 31, 2012 for preparation of the statement of stockholders’ equity. We recognize, there is a slight difference between the amounts reflected, but believe we are following GAAP.

3. We note your disclosure that your membership in the CGSE allows you to facilitate transactions on behalf of your agents’ customers and/or the agents themselves, who can purchase spot contracts in gold and/or silver on the CGSE. We also note your disclosure that you do not become the counterparty to such contracts. Please provide us with a detailed explanation as to how spot contracts are purchased through your trading platform, including an explanation as to who the counterparties are to each contract. Please also provide us with a detailed explanation as to how you are able to facilitate such transactions without being the counterparty.

Response: We have added a detailed, step-by-step, explanation as to how contracts are purchased through the trading platform, including an explanation as to who the counterparties are to each contract and an explanation as to how we are able to facilitate such transactions without being the counterparty. Please note that the identity of the counterparty is not disclosed to Man Loong.

4. We note your disclosure that you act as a clearing house for the spot contracts purchased through your trading platform. Please provide us with a detailed explanation as to what it means to act as a “clearing house” for such contracts.

Response: Please note that we have changed the language in the prospectus to more accurately reflect Man Loong’s role as a facilitator in clearing trades as opposed to stating that Man Loong acts as a clearing agency.

5. We note your disclosure that the spot contracts purchased through your trading platform do not involve the physical transfer or delivery of any actual gold or silver. Please provide us with a detailed explanation as to how such contracts can be characterized as “spot contracts” if there is no possibility for the physical transfer or delivery of any actual gold or silver. In responding to this comment, please provide us with a detailed explanation of the specific contractual terms of the spot contracts that may be purchased through your trading platform.

United States Securities and Exchange Commission

October 2, 2013

Page 3

Response: Although the transactions that Man Loong facilitates are referred to as spot contracts in Hong Kong, because they settle at the market price at the time the trade is matched with a counterparty, we acknowledge that the definition of a spot contract in the United States differs. Therefore, we have removed the reference to spot contracts throughout the prospectus.

6. We note your disclosure that you do not have any direct customers; rather your customers are the customers of certain agents with whom you have contractual arrangements. However, it appears that a person can access your website and create an account to purchase spot contracts through your trading platform, regardless of whether such person has a relationship with one of your agents. In this regard, we note that your website includes a list of the ways in which a person can open an account and using an agent is just one option, with the other options being opening an account directly using your website or calling the company directly. We also note that your website includes a form of customer agreement that appears to be entered into between your company and the customer. Please provide us with a detailed explanation as to the business and contractual relationships between and among your company, your agents, and customers. Please file the customer agreement as an exhibit to the registration statement as required by Item 601(b)(10) of Regulation S-K. Please refer to Rule 403(c) of the Securities Act for filing requirements.

Response: We have added disclosure that clarifies that we do not have agreements directly with customers and that any customer that attempts to open an account with us by completing forms displayed on our website are assigned to agents. Inasmuch as we are not parties to the customer agreements and such agreements are merely on our website as an accommodation to our agents, we do not believe it necessary to supply such contracts.

7. Please advise us as to the extent of your business in the United States, including whether U.S. customers may access your website and purchase spot contracts through your trading platform.

Response: We have added language to the prospectus that we do not have agents in the United States and our agents do not have customers in the United States.

Business, page 13

8. Please revise your disclosure to identify Man Loong’s website or advise. Please refer to Item 101(h)(5)(iii) of Regulation S-K.

Response: We have added a reference to the website.

9. We note your response to comment 10 of our comment letter dated July 19, 2013 and your related disclosure that the spot contracts are settled at the market price of gold or silver at the moment the CGSE matches the trade with a counterparty. However, we also note your disclosure that the spot contracts do not involve the actual physical transfer or delivery of any gold or silver. Please revise your disclosure to explain how these spot contracts are settled without the physical transfer or delivery of any gold or silver or advise.

Response: Please see our response to comment number 5.

United States Securities and Exchange Commission

October 2, 2013

Page 4

History, page 13

10. We note your response to comment 12 of our comment letter dated July 19, 2013. We note your disclosure on page 14 that Man Loong calculates and collects the amount of commissions due from agents on a monthly basis. However, on page 14, you then disclose that Man Loong charges its commission to the agents’ accounts when each trade is processed. Please revise your disclosure to resolve this inconsistency or advise. In addition, please revise your disclosure to clarify whether or not Man Loong’s agents maintain accounts with Man Loong.

Response: We have revised the disclosure to clarify that the agent’s account is charged a commission when a trade is executed; however bills are sent out monthly and payment of the commission by the agent is due 30 days after invoice date.

11. We note your disclosure regarding Man Loong’s monitoring of the deposit balances of customers of the agents. Please revise your disclosure to explain who bears the risk that the customer’s net trading position is closed at a loss that exceeds the customer’s deposit balance.

Response: We have added disclosure to clarify that the agent and not Man Loong bears such risk.

Intellectual Property, page 20

12. We note your response to comment 16 of our comment letter dated July 19, 2013 and the related revisions to your registration statement. We also note your disclosure that True Technology has modified the licensed technology at the request of Man Loong and that all enhancements or modifications to the software requested by Man Loong are the property of Man Loong. However, we also note that True Technology granted Man Loong a non-exclusive license to the underlying software. Please revise your disclosure to explain whether Man Loong has any intellectual property rights in underlying technology licensed.

Response: We have added disclosure regarding True Technology’s right to the underlying technology.

Summary Compensation Table, page 26

13. We note you added footnote (1) to the summary compensation table on page 26 to identify the compensation Mr. Choi received for his services as a director, which is not otherwise reflected in the summary compensation table. Please revise your disclosure of the compensation received by Mr. Choi in the summary compensation table to include the compensation he received as a director and include footnote disclosure to delineate such compensation as director compensation or reflect the director compensation received by Mr. Choi in the director compensation table on page 27. Please refer to Item 402(r)(2)(i) of Regulation S-K and Instruction 3 to Item 402(n) of Regulation S-K. In addition, we note your disclosure on page 27 in the “Director Compensation” section that “[o]ther than as set forth above no member of [y]our Board of Directors received any compensation for his services as a director during the year ended March 31, 2013.” Please revise your disclosure here to clarify that both Mr. Choi and Mr. Wong received director compensation during the year ended March 31, 2013 or advise.

Response: We have removed the footnote as it was incorrectly included.

United States Securities and Exchange Commission

October 2, 2013

Page 5

Director Compensation, page 27

14. We note your response to comment 23 of our comment letter dated July 19, 2013 and the related revisions to your registration statement. Please revise your disclosure regarding the financial consulting fees of $5,200 received by Mr. Havlin to identify the period to which these fees relate.

Response: We have added the requested disclosure.

Security Ownership of Certain Beneficial Owners and Management, page 27

15. We note your response to comment 24 of our comment letter dated July 19, 2013 and the related revisions to your registration statement. We note that in the introduction to the beneficial ownership table you disclose that there are “currently no” persons for which you have reason to believe may be deemed the beneficial owner of more than 5% of your common stock. However, in the table you identify two persons who own greater than 5% of your common stock. Please revise your disclosure as appropriate to resolve this inconsistency or advise.

Response: We have deleted the words “currently no.”

Selling Stockholders, page 28

16. We note your response to comment 25 of our comment letter dated July 19, 2013 and the related revisions to your registration statement. We note that in the introduction to your selling stockholder table you identify Cheung Siu Yin, the spouse of your chief executive officer, and Lau Ka Ming, the spouse of your chief financial officer, as selling shareholders. However, we were unable to locate these individuals in the selling shareholder table. Please revise your selling stockholder table as appropriate or advise.

In addition, please confirm that the shares owned by Cheung Siu Yin and Lau Ka Ming are included in the beneficial ownership table on page 27 as shares deemed to be owned by the spouses of these individuals or advise. Please refer to our Exchange Act Sections 13(d) and 13(g) of Regulation 13D-G Beneficial Ownership Reporting Compliance and Disclosure Interpretation 105.05.

Response: We apologize for the confusion. The names in the table were presented in English format and the names above the table were presented in Chinese format. We have conformed the disclosure and amended the Beneficial Ownership chart.

United States Securities and Exchange Commission

October 2, 2013

Page 6

Certain Relationships and Related Transactions, page 31

17. We note your response to comment 15 of our comment letter dated July 19, 2013 and your revisions to the “Our Electronic Trading Services” section on page 18. We also note your disclosure regarding your agreement with True Technology on page 31. Please revise your disclosure on page 31 so that it is consistent with the disclosure included on page 18. For example only, please clarify that the monthly fee of $12,894 relates to the license and the hosting services provided by True Technology.

Response: We have revised the disclosure as requested.

18. We note your disclosure that Mr. Choi and Mr. Wong were paid a dividend of $642,908. Please revise your disclosure to specify the portion of this dividend paid to Mr. Choi and the portion of this dividend paid to Mr. Wong.

Response: We have added the requested disclosure.

19. We note your response to comment 27 of our comment letter dated July 19, 2013 and the related revisions to your registration statement. We also note your disclosure regarding the transaction wherein you acquired Man Loong. Please revise your disclosure to include the information required by Item 404(a) of Regulation S-K for this transaction or advise.

Response: We have added the required disclosure.

United States Securities and Exchange Commission

October 2, 2013

Page 7

Item 16. Exhibits, page II-2

20. We note your response to comment 31 of our comment letter dated July 19, 2013. We also note that you have filed as exhibit 10.6 a schedule to the form of agency agreement. Please ensure that in this schedule you have identified the material details in which the omitted documents differ from the form of agency agreement. Please refer to Instruction 2 to Item 601 of Regulation S-K. For example only, we note that the parties on the agreements, the terms of the agreements, and the execution dates of the agreements may differ. In addition, please re-file the exhibits that were previously filed as exhibits 10.6 through 10.8 so that their exhibit numbers correspond to the appropriate numbers in the exhibit index.

Response: We have revised the chart to include termination dates of the contracts and believe that we have provided all material details. We have also added disclosure in the prospectus that the commission that each contract provides that the commission will be determined by agreement between the parties.

We acknowledge that the adequacy and accuracy of the disclosure in our filings is our responsibility. We acknowledge that the staff comments or changes to disclosure do not foreclose the Commission from taking any action with respect to the filings. We acknowledge that the company may not assert staff comments as a defense in any proceedings initiated by the Commission or any person under the federal securities laws of the United States.

If you have any questions or need additional information, please contact the undersigned at (516) 496-2223 or (212) 907-6457.

Sincerely,

/s/ Leslie Marlow

Leslie Marlow

Partner

��