Exhibit (c)(7)

Confidential – Preliminary and Subject to Change Discussion Materials Regarding Project Houston October 24, 2022

Confidential – Preliminary and Subject to Change These materials have been prepared by Evercore Group L.L.C. (“Evercore”) for the Conflicts Committee (the “Conflicts Committee”) of the Board of Directors of Sisecam Resource Partners LLC, the general partner of Sisecam Resources LP (the “Partnership”), to whom such materials are directly addressed and delivered and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Evercore. These materials are based on information provided by or on behalf of the Conflicts Committee, from public sources or otherwise reviewed by Evercore. Evercore assumes no responsibility for independent investigation or verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the management of the Partnership and/or other potential transaction participants or obtained from public or other third party sources, Evercore has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Partnership. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials have been developed by and are proprietary to Evercore and were prepared exclusively for the benefit and internal use of the Conflicts Committee. These materials were compiled on a confidential basis for use exclusively by the Conflicts Committee and not with a view to public disclosure or filing thereof under state or federal securities laws, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without the prior written consent of Evercore or as provided in the engagement letter between Evercore and the Conflicts Committee. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Evercore or any of its affiliates to provide or arrange any financing for any transaction or to purchase any security in connection therewith. Evercore assumes no obligation to update or otherwise revise these materials. These materials may not reflect information known to other professionals in other business areas of Evercore and its affiliates. Evercore and its affiliates do not provide legal, accounting or tax advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by Evercore or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the impact of the transactions or matters described herein.

Confidential – Preliminary and Subject to Change Table of Contents Section Executive Summary SIRE Situation Analysis Preliminary Valuation of SIRE Common Units Appendix Weighted Average Cost of Capital Analysis Preliminary Valuation Detail – SIRE Financial Projections Financial Projections and Preliminary Valuation Detail – Sensitivity Case Supplemental Soda Ash Pricing Data I II III

Confidential – Preliminary and Subject to Change I. Executive Summary

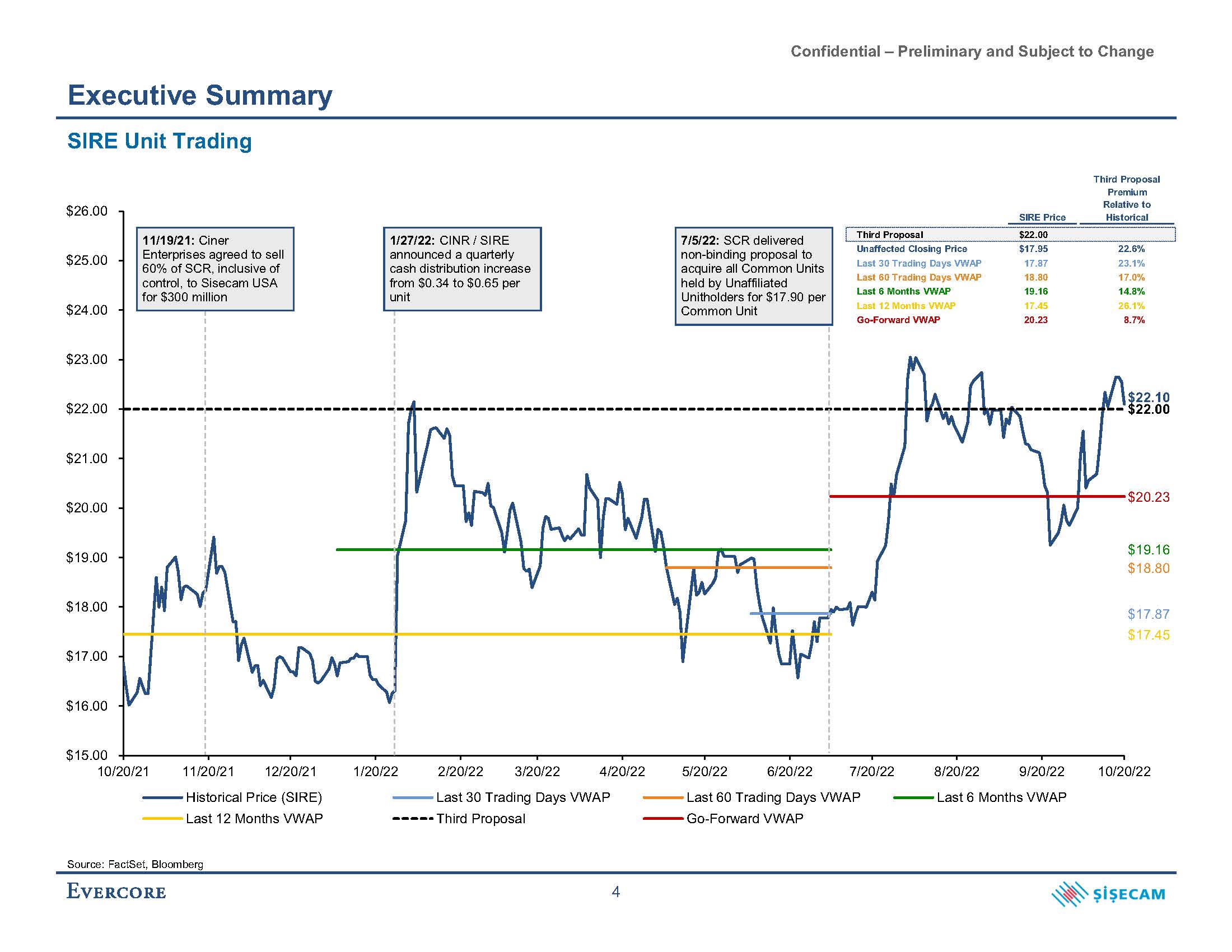

Confidential – Preliminary and Subject to Change Executive Summary 1 Introduction Evercore Group L.L.C. (“Evercore”) is pleased to provide the following materials to the Conflicts Committee (the “Conflicts Committee”) of the Board of Directors of Sisecam Resource Partners LLC (the “General Partner” or “SIRE GP”), the general partner of Sisecam Resources LP (“SIRE” or the “Partnership”), regarding Sisecam Chemicals Resources LLC’s (“Sisecam Chemicals” or “SCR”) proposal to acquire all common units representing limited partner interests in the Partnership (each, a “Common Unit”) from the holders of such units other than Common Units held by Sisecam Chemicals, the General Partner or their respective affiliates (the “Unaffiliated Unitholders”) (the “Proposed Transaction”) Sisecam Chemicals Wyoming LLC (“SCW LLC”) is a wholly-owned subsidiary of Sisecam Chemicals that currently owns: 14,551,000 Common Units (72% limited partner interest in the Partnership) SIRE GP, which owns a 2.0% general partner interest in the Partnership On July 5, 2022, Sisecam Chemicals proposed to acquire each outstanding Common Unit owned by the Unaffiliated Unitholders for $17.90 in cash (the “Initial Proposal”) On September 20, 2022, the Conflicts Committee countered at $29.50 (the “First Conflicts Committee Counterproposal”) On September 27, 2022, Sisecam Chemicals proposed to acquire each outstanding Common Unit owned by the Unaffiliated Unitholders for $19.00 in cash (the “Second Proposal”) On October 11, 2022, the Conflicts Committee countered at $28.50 (the “Second Conflicts Committee Counterproposal”) On October 20, 2022, Sisecam Chemicals proposed to acquire each outstanding Common Unit owned by the Unaffiliated Unitholders for $22.00 price in cash (the “Third Proposal”) as its “best and final” offer The Third Proposal represents a 22.6% premium to SIRE’s closing Common Unit price of $17.95 as of July 5, 2022, the last unaffected trading date before the Initial Proposal The Third Proposal represents a 23.1% premium to SIRE’s 30-day volume weighted average price (“VWAP”) as of July 5, 2022

Confidential – Preliminary and Subject to Change Executive Summary 2 Changes Since Conflicts Committee Meeting on October 11, 2022 Evercore made the following updates and adjustments from the draft presentation dated October 11, 2022, as requested by the Conflicts Committee: Updated market prices to October 20, 2022 Adjusted the weighted average cost of capital (“WACC”) utilized for discounted cash flow (“DCF”) analyses from a range of 8.25% to 9.25% to a range of 8.50% to 9.50% based on market changes Adjusted the equity cost of capital utilized for discounted distributions analyses from a range of 9.0% to 11.0% to a range of 10.0% to 12.0% based on market changes Added an analysis of SIRE’s historical enterprise value to run-rate EBITDA (latest quarter annualized) trading multiple over the past five years compared to its peer group

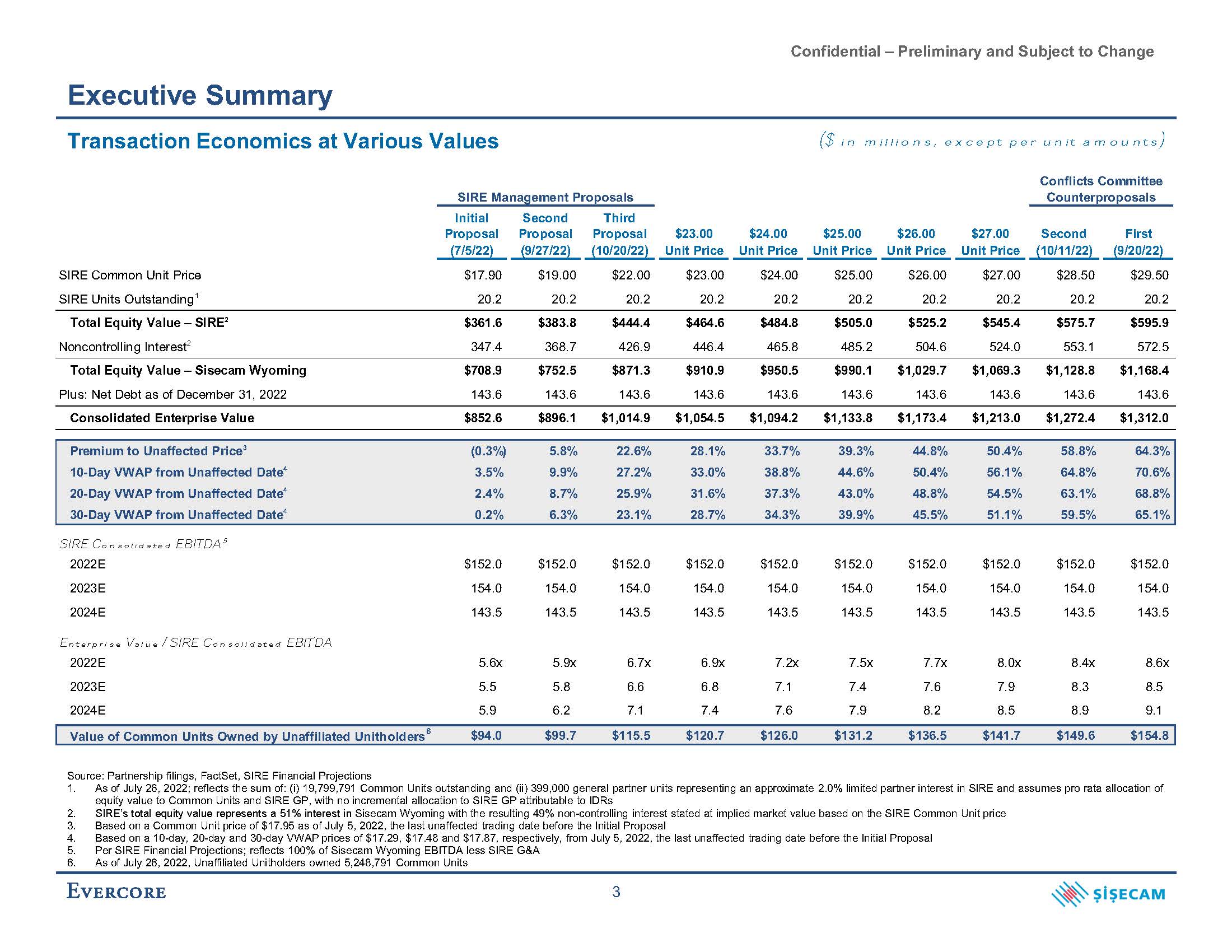

Confidential – Preliminary and Subject to Change Executive Summary 3 Transaction Economics at Various Values ($ in millions, except per unit amounts) As of July 26, 2022; reflects the sum of: (i) 19,799,791 Common Units outstanding and (ii) 399,000 general partner units representing an approximate 2.0% limited partner interest in SIRE and assumes pro rata allocation of equity value to Common Units and SIRE GP, with no incremental allocation to SIRE GP attributable to IDRs SIRE’s total equity value represents a 51% interest in Sisecam Wyoming with the resulting 49% non-controlling interest stated at implied market value based on the SIRE Common Unit price Based on a Common Unit price of $17.95 as of July 5, 2022, the last unaffected trading date before the Initial Proposal Based on a 10-day, 20-day and 30-day VWAP prices of $17.29, $17.48 and $17.87, respectively, from July 5, 2022, the last unaffected trading date before the Initial Proposal Per SIRE Financial Projections; reflects 100% of Sisecam Wyoming EBITDA less SIRE G&A As of July 26, 2022, Unaffiliated Unitholders owned 5,248,791 Common Units SIRE Management Proposals Conflicts Committee Counterproposals Initial Second Third Proposal Proposal Proposal $23.00 $24.00 $25.00 $26.00 $27.00 Second First (7/5/22) (9/27/22) (10/20/22) Unit Price Unit Price Unit Price Unit Price Unit Price (10/11/22) (9/20/22) SIRE Common Unit Price $17.90 $19.00 $22.00 $23.00 $24.00 $25.00 $26.00 $27.00 $28.50 $29.50 SIRE Units Outstanding1 20.2 20.2 20.2 20.2 20.2 20.2 20.2 20.2 20.2 20.2 Total Equity Value – SIRE2 $361.6 $383.8 $444.4 $464.6 $484.8 $505.0 $525.2 $545.4 $575.7 $595.9 Noncontrolling Interest2 347.4 368.7 426.9 446.4 465.8 485.2 504.6 524.0 553.1 572.5 Total Equity Value – Sisecam Wyoming $708.9 $752.5 $871.3 $910.9 $950.5 $990.1 $1,029.7 $1,069.3 $1,128.8 $1,168.4 Plus: Net Debt as of December 31, 2022 143.6 143.6 143.6 143.6 143.6 143.6 143.6 143.6 143.6 143.6 Consolidated Enterprise Value $852.6 $896.1 $1,014.9 $1,054.5 $1,094.2 $1,133.8 $1,173.4 $1,213.0 $1,272.4 $1,312.0 Premium to Unaffected Price3 (0.3%) 5.8% 22.6% 28.1% 33.7% 39.3% 44.8% 50.4% 58.8% 64.3% 10-Day VWAP from Unaffected Date4 3.5% 9.9% 27.2% 33.0% 38.8% 44.6% 50.4% 56.1% 64.8% 70.6% 20-Day VWAP from Unaffected Date4 2.4% 8.7% 25.9% 31.6% 37.3% 43.0% 48.8% 54.5% 63.1% 68.8% 30-Day VWAP from Unaffected Date4 0.2% 6.3% 23.1% 28.7% 34.3% 39.9% 45.5% 51.1% 59.5% 65.1% SIRE Consolidated EBITDA 5 2022E $152.0 $152.0 $152.0 $152.0 $152.0 $152.0 $152.0 $152.0 $152.0 $152.0 2023E 154.0 154.0 154.0 154.0 154.0 154.0 154.0 154.0 154.0 154.0 2024E 143.5 143.5 143.5 143.5 143.5 143.5 143.5 143.5 143.5 143.5 Enterprise Value / SIRE Consolidated EBITDA 2022E 5.6x 5.9x 6.7x 6.9x 7.2x 7.5x 7.7x 8.0x 8.4x 8.6x 2023E 5.5 5.8 6.6 6.8 7.1 7.4 7.6 7.9 8.3 8.5 2024E 5.9 6.2 7.1 7.4 7.6 7.9 8.2 8.5 8.9 9.1 Value of Common Units Owned by Unaffiliated Unitholders6 $94.0 $99.7 $115.5 $120.7 $126.0 $131.2 $136.5 $141.7 $149.6 $154.8 Source: Partnership filings, FactSet, SIRE Financial Projections

Confidential – Preliminary and Subject to Change $19.16 $18.80 $17.87 $17.45 $22.10 $22.00 $20.23 $15.00 $17.00 $16.00 $18.00 $19.00 $20.00 $21.00 $22.00 $23.00 $24.00 $25.00 $26.00 10/20/21 1/20/22 10/20/22 8/20/22 9/20/22 Last 6 Months VWAP 11/20/21 12/20/21 Historical Price (SIRE) Last 12 Months VWAP 2/20/22 3/20/22 4/20/22 Last 30 Trading Days VWAP Third Proposal 5/20/22 6/20/22 7/20/22 Last 60 Trading Days VWAP Go-Forward VWAP Executive Summary SIRE Unit Trading SIRE Price Third Proposal Premium Relative to Historical Third Proposal $22.00 Unaffected Closing Price Last 30 Trading Days VWAP Last 60 Trading Days VWAP Last 6 Months VWAP Last 12 Months VWAP Go-Forward VWAP $17.95 17.87 18.80 19.16 17.45 20.23 22.6% 23.1% 17.0% 14.8% 26.1% 8.7% 7/5/22: SCR delivered non-binding proposal to acquire all Common Units held by Unaffiliated Unitholders for $17.90 per Common Unit 11/19/21: Ciner Enterprises agreed to sell 60% of SCR, inclusive of control, to Sisecam USA for $300 million 1/27/22: CINR / SIRE announced a quarterly cash distribution increase from $0.34 to $0.65 per unit Source: FactSet, Bloomberg 4

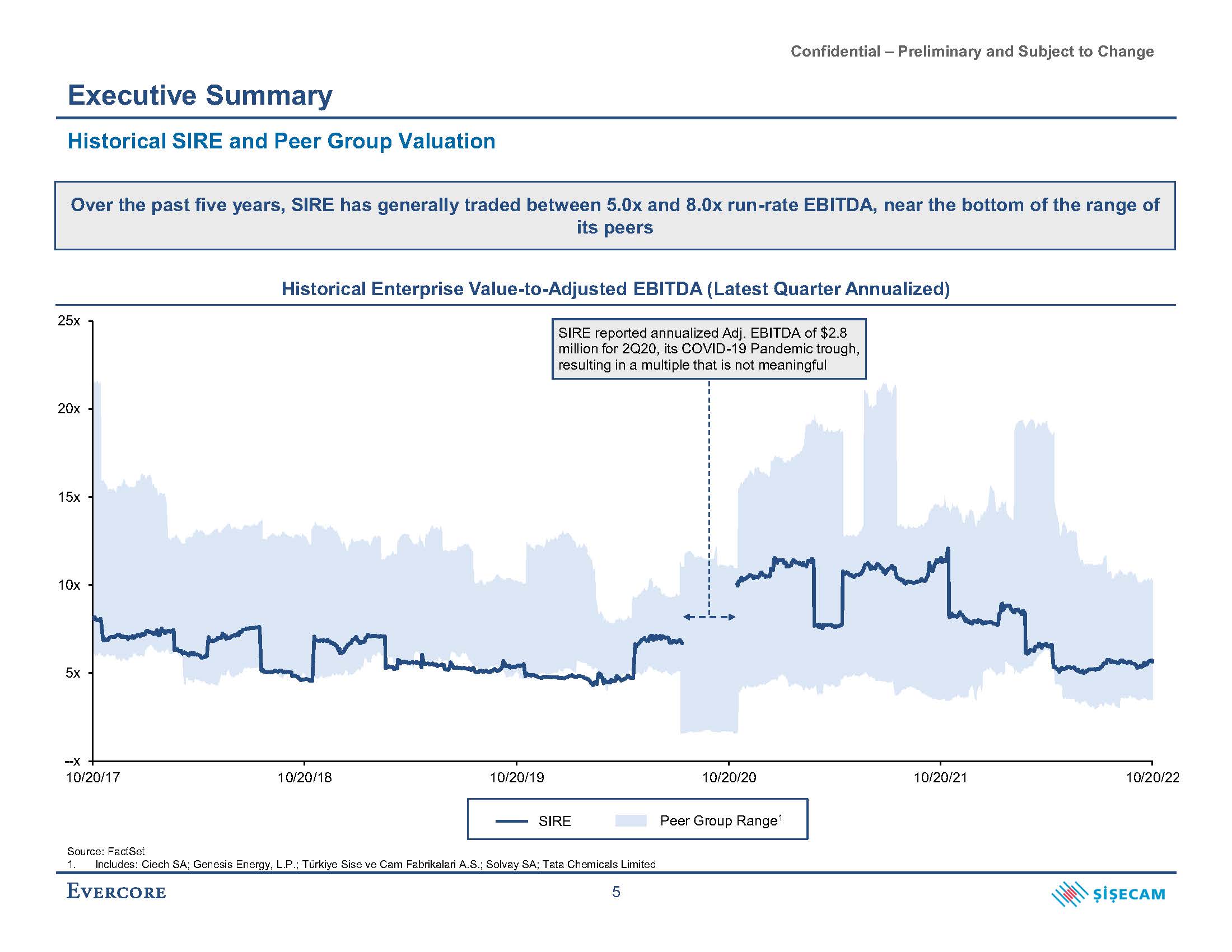

Confidential – Preliminary and Subject to Change Executive Summary Historical SIRE and Peer Group Valuation Source: FactSet --x 5x 10x 15x 20x 25x 10/20/17 10/20/18 10/20/19 10/20/20 10/20/21 10/20/22 Historical Enterprise Value-to-Adjusted EBITDA (Latest Quarter Annualized) SIRE reported annualized Adj. EBITDA of $2.8 million for 2Q20, its COVID-19 Pandemic trough, resulting in a multiple that is not meaningful SIRE Peer Group Range1 1. Includes: Ciech SA; Genesis Energy, L.P.; Türkiye Sise ve Cam Fabrikalari A.S.; Solvay SA; Tata Chemicals Limited 5 Over the past five years, SIRE has generally traded between 5.0x and 8.0x run-rate EBITDA, near the bottom of the range of its peers

Confidential – Preliminary and Subject to Change II. SIRE Situation Analysis

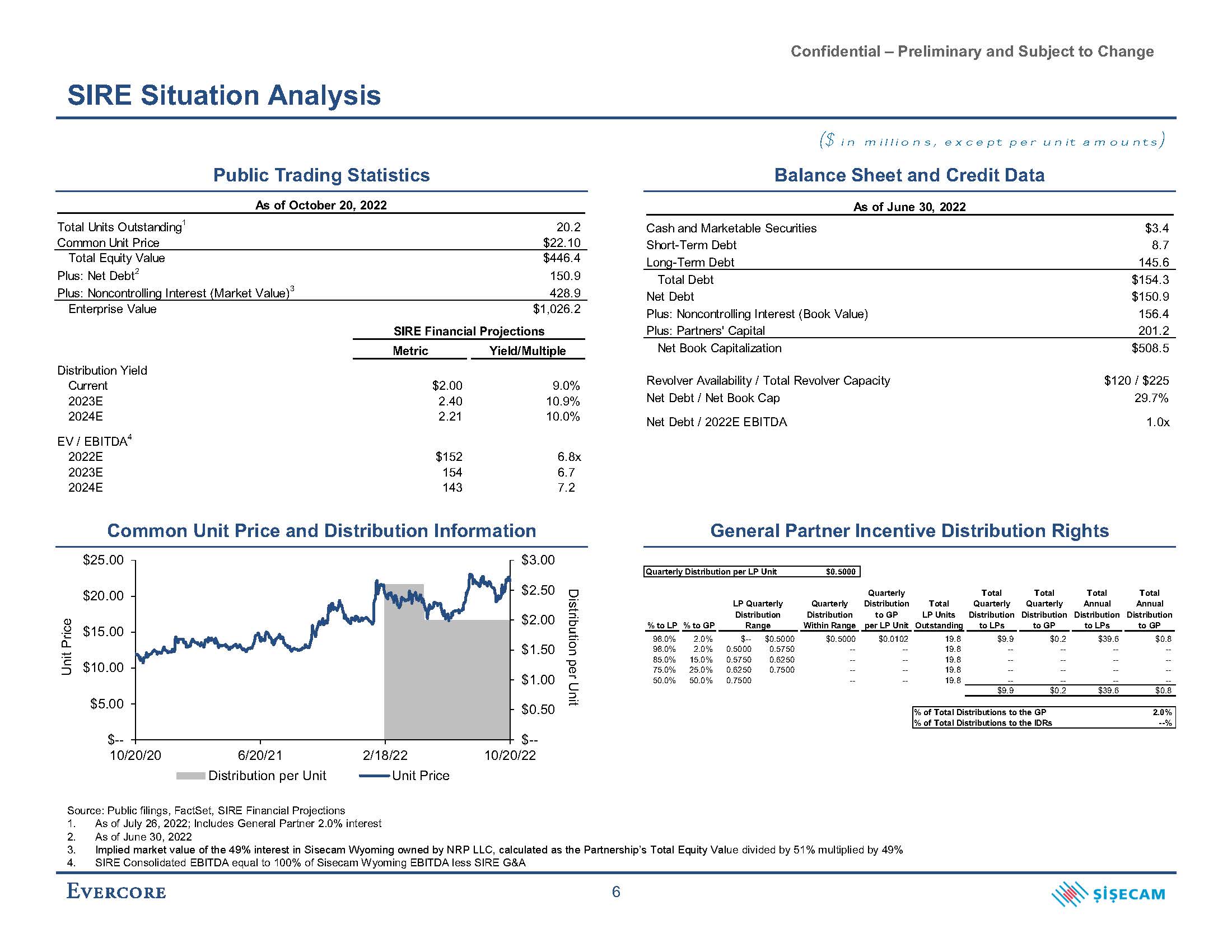

Confidential – Preliminary and Subject to Change SIRE Situation Analysis Public Trading Statistics ($ in millions, except per unit amounts) Balance Sheet and Credit Data General Partner Incentive Distribution Rights As of June 30, 2022 Cash and Marketable Securities Short-Term Debt Long-Term Debt $3.4 8.7 145.6 Plus: Noncontrolling Interest (Book Value) Plus: Partners' Capital 156.4 201.2 Net Book Capitalization $508.5 Revolver Availability / Total Revolver Capacity $120 / $225 Plus: Net Debt2 150.9 Total Debt $154.3 Plus: Noncontrolling Interest (Market Value)3 428.9 Net Debt $150.9 Common Unit Price and Distribution Information $25.00 $3.00 $-- $0.50 $1.00 $1.50 $2.00 $2.50 $-- $5.00 $10.00 $15.00 $20.00 10/20/20 6/20/21 Distribution per Unit 10/20/22 Distribution per Unit Unit Price 2/18/22 Unit Price Quarterly Distribution per LP Unit $0.5000 Total Total Total Quarterly Quarterly Total Annual Total Annual Quarterly Quarterly Distribution Distribution to GP LP Units Distribution Distribution Distribution Distribution % to LP % to GP LP Quarterly Distribution Range Within Range per LP Unit Outstanding to LPs to GP to LPs to GP 98.0% 98.0% 85.0% 75.0% 50.0% 2.0% 2.0% 15.0% 25.0% 50.0% $-- 0.5000 0.5750 0.6250 0.7500 $0.5000 0.5750 0.6250 0.7500 $0.5000 -- -- -- -- $0.0102 -- -- -- -- 19.8 19.8 19.8 19.8 $9.9 -- -- -- $0.2 -- -- -- $39.6 -- -- -- $0.8 -- -- -- 19.8 -- -- -- -- $9.9 $0.2 $39.6 $0.8 % of Total Distributions to the GP % of Total Distributions to the IDRs 2.0% --% Source: Public filings, FactSet, SIRE Financial Projections As of July 26, 2022; Includes General Partner 2.0% interest As of June 30, 2022 Implied market value of the 49% interest in Sisecam Wyoming owned by NRP LLC, calculated as the Partnership’s Total Equity Value divided by 51% multiplied by 49% As of October 20, 2022 Total Units Outstanding1 Common Unit Price 20.2 $22.10 Total Equity Value $446.4 Enterprise Value Distribution Yield Current $1,026.2 SIRE Financial Projections Metric Yield/Multiple $2.00 9.0% 2023E 2024E EV / EBITDA4 2.40 2.21 10.9% 10.0% Net Debt / Net Book Cap Net Debt / 2022E EBITDA 29.7% 1.0x 2022E $152 6.8x 2023E 154 6.7 2024E 143 7.2 4. SIRE Consolidated EBITDA equal to 100% of Sisecam Wyoming EBITDA less SIRE G&A 6

Confidential – Preliminary and Subject to Change SIRE Situation Analysis Source: SIRE Financial Projections 7 SIRE Financial Projections – Assumptions Revenue Long-term domestic / export revenue breakout of 50% / 50% Domestic and export pricing based on SIRE management’s forecast Export revenue is broken out into ANSAC and direct export projects with no sales attributable to ANSAC in 2023E+ Expenses Expenses based on historical costs per unit, the majority of which are projected to increase 5.8% in 2023E and 2.2% in 2024E and each year thereafter Costs per unit for domestic freight and personnel are projected to increase 5.8% in 2023E and 3.0% in 2024E and each year thereafter Energy costs per unit are expected to increase 5.8% in 2023E, then decline in 2024E to a level which is 2.2% greater than 2022E and increase at a 2.2% annual rate thereafter SIRE-Level G&A Annual cash G&A incurred at the Partnership level after distributions received from Sisecam Wyoming equal to $2.9 million in 2022E and $4.0 million each year thereafter Deducted from Sisecam Wyoming EBITDA to arrive at SIRE Consolidated EBITDA Deducted from SIRE's 51% share of Sisecam Wyoming EBITDA to arrive at EBITDA Attributable to SIRE Capital Expenditures Maintenance capital expenditures of $25.0 million in 2022E are projected to increase 2.2% annually thereafter No growth capital expenditures contemplated in the forecast Detailed engineering work on Unit 8 Expansion completed, but SIRE management has stated that the project was postponed due to COVID-19 market conditions and is not currently contemplated given SIRE management’s view of global demand as well as increased projected capital costs for the project Credit Facility Assumptions Sisecam Wyoming’s existing $225 million revolving credit facility includes an accordion provision to increase the commitment to $475 million subject to certain lender approvals $105 million drawn as of June 30, 2022 2.05% interest rate Distribution Coverage / Total Leverage Sisecam Wyoming to maintain a distribution coverage ratio of 1.50x in 2022E, 1.25x in 2023E and 2024E, and 1.10x thereafter SIRE to distribute 100% of distributions received from Sisecam Wyoming less G&A incurred at the Partnership Sisecam Wyoming to use all remaining cash flow to pay down debt

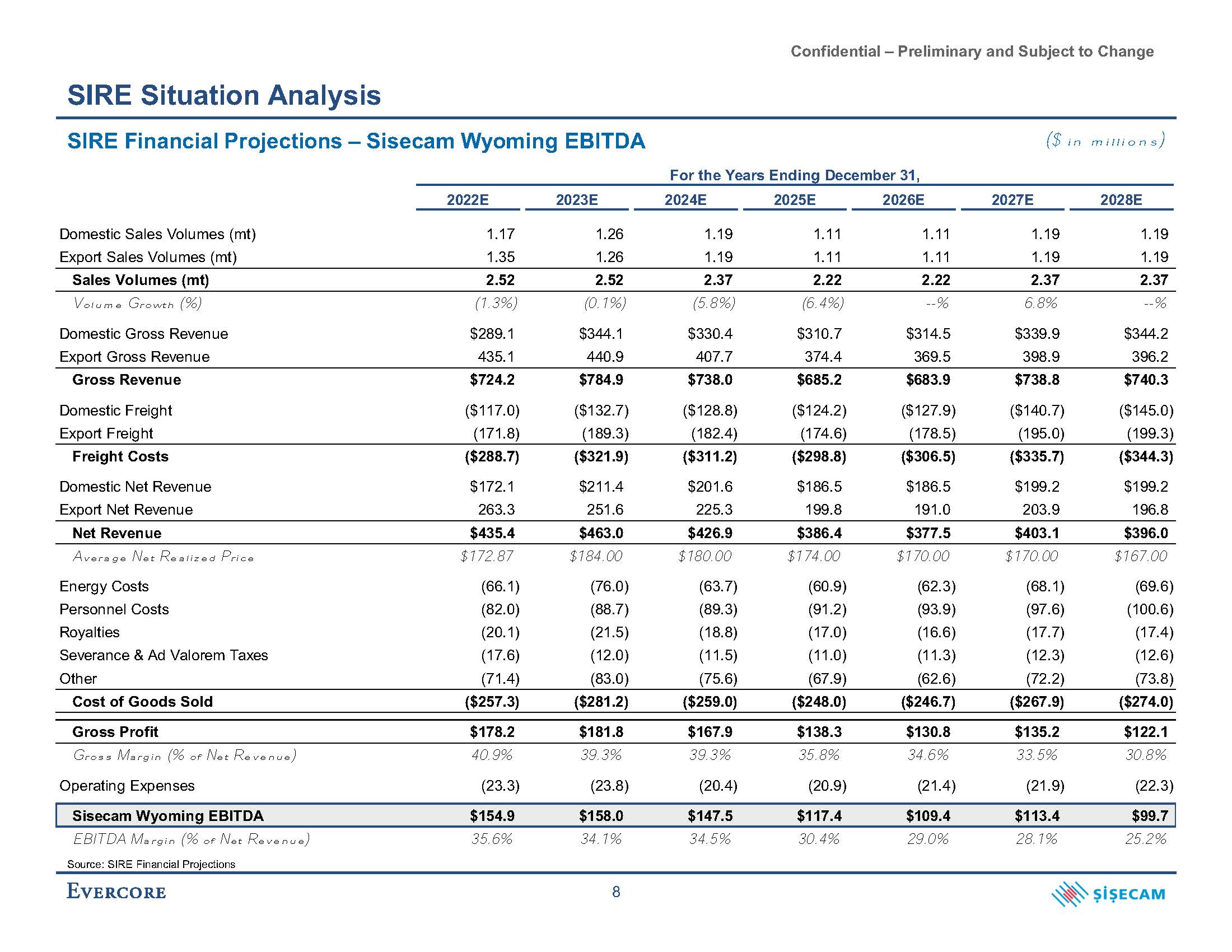

Confidential – Preliminary and Subject to Change SIRE Situation Analysis Source: SIRE Financial Projections 8 SIRE Financial Projections – Sisecam Wyoming EBITDA 2022E 2023E 2024E 2025E 2026E 2027E 2028E Domestic Sales Volumes (mt) 1.17 1.26 1.19 1.11 1.11 1.19 1.19 Export Sales Volumes (mt) 1.35 1.26 1.19 1.11 1.11 1.19 1.19 Sales Volumes (mt) 2.52 2.52 2.37 2.22 2.22 2.37 2.37 Volume Growth (%) (1.3%) (0.1%) (5.8%) (6.4%) --% 6.8% --% Domestic Gross Revenue $289.1 $344.1 $330.4 $310.7 $314.5 $339.9 $344.2 Export Gross Revenue 435.1 440.9 407.7 374.4 369.5 398.9 396.2 Gross Revenue $724.2 $784.9 $738.0 $685.2 $683.9 $738.8 $740.3 Domestic Freight ($117.0) ($132.7) ($128.8) ($124.2) ($127.9) ($140.7) ($145.0) Export Freight (171.8) (189.3) (182.4) (174.6) (178.5) (195.0) (199.3) Freight Costs ($288.7) ($321.9) ($311.2) ($298.8) ($306.5) ($335.7) ($344.3) Domestic Net Revenue $172.1 $211.4 $201.6 $186.5 $186.5 $199.2 $199.2 Export Net Revenue 263.3 251.6 225.3 199.8 191.0 203.9 196.8 Net Revenue $435.4 $463.0 $426.9 $386.4 $377.5 $403.1 $396.0 Average Net Realized Price $172.87 $184.00 $180.00 $174.00 $170.00 $170.00 $167.00 Energy Costs (66.1) (76.0) (63.7) (60.9) (62.3) (68.1) (69.6) Personnel Costs (82.0) (88.7) (89.3) (91.2) (93.9) (97.6) (100.6) Royalties (20.1) (21.5) (18.8) (17.0) (16.6) (17.7) (17.4) Severance & Ad Valorem Taxes (17.6) (12.0) (11.5) (11.0) (11.3) (12.3) (12.6) Other (71.4) (83.0) (75.6) (67.9) (62.6) (72.2) (73.8) Cost of Goods Sold ($257.3) ($281.2) ($259.0) ($248.0) ($246.7) ($267.9) ($274.0) Gross Profit $178.2 $181.8 $167.9 $138.3 $130.8 $135.2 $122.1 Gross Margin (% of Net Revenue) 40.9% 39.3% 39.3% 35.8% 34.6% 33.5% 30.8% Operating Expenses (23.3) (23.8) (20.4) (20.9) (21.4) (21.9) (22.3) Sisecam Wyoming EBITDA $154.9 $158.0 $147.5 $117.4 $109.4 $113.4 $99.7 EBITDA Margin (% of Net Revenue) 35.6% 34.1% 34.5% 30.4% 29.0% 28.1% 25.2% For the Years Ending December 31, ($ in millions)

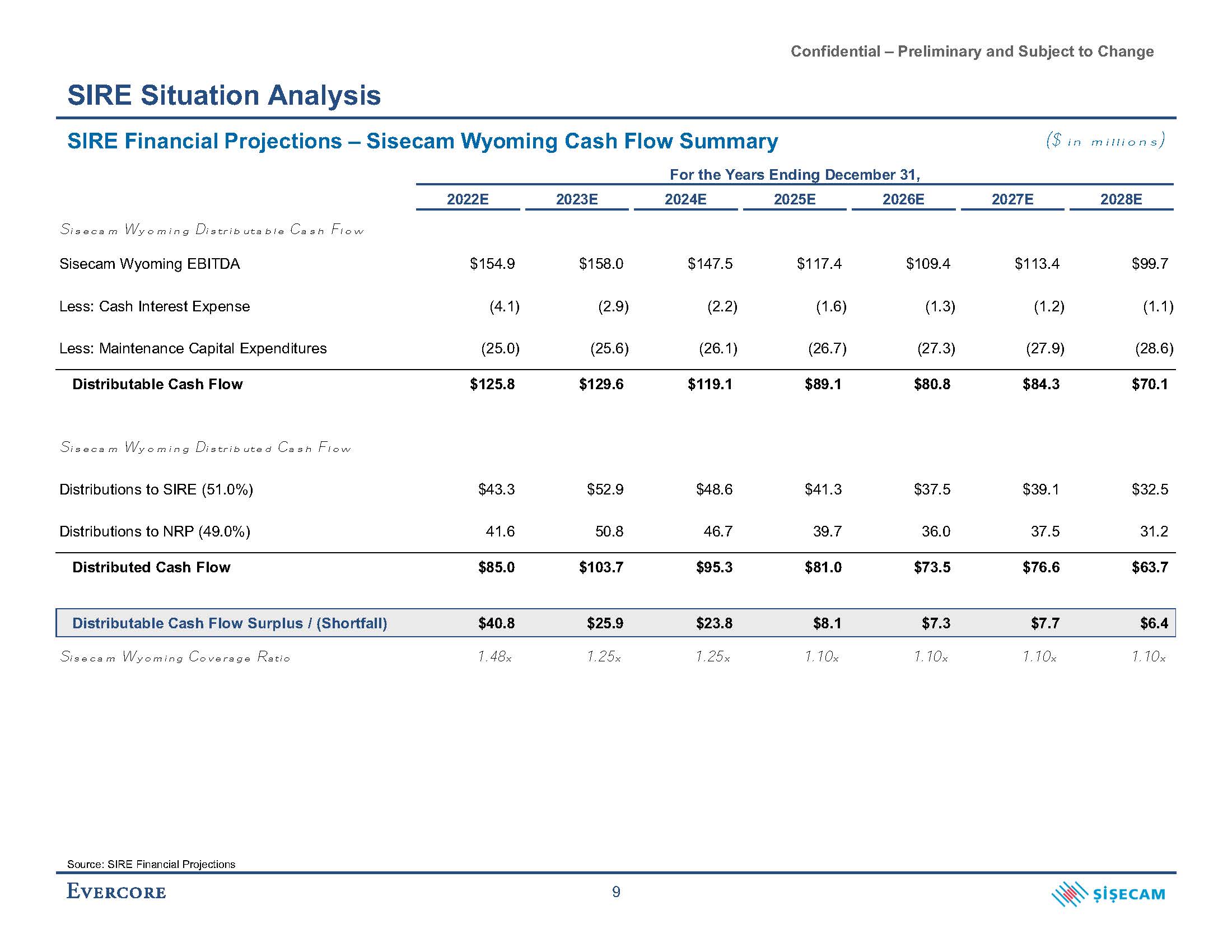

Confidential – Preliminary and Subject to Change SIRE Situation Analysis ($ in millions) Sisecam Wyoming EBITDA $154.9 $158.0 $147.5 $117.4 $109.4 $113.4 $99.7 Less: Cash Interest Expense (4.1) (2.9) (2.2) (1.6) (1.3) (1.2) (1.1) Less: Maintenance Capital Expenditures (25.0) (25.6) (26.1) (26.7) (27.3) (27.9) (28.6) Distributable Cash Flow $125.8 $129.6 $119.1 $89.1 $80.8 $84.3 $70.1 Sisecam Wyoming Distributed Cash Flow Distributions to SIRE (51.0%) $43.3 $52.9 $48.6 $41.3 $37.5 $39.1 $32.5 Distributions to NRP (49.0%) 41.6 50.8 46.7 39.7 36.0 37.5 31.2 Distributed Cash Flow $85.0 $103.7 $95.3 $81.0 $73.5 $76.6 $63.7 Distributable Cash Flow Surplus / (Shortfall) $40.8 $25.9 $23.8 $8.1 $7.3 $7.7 $6.4 Sisecam Wyoming Coverage Ratio 1.48x 1.25x 1.25x 1.10x 1.10x 1.10x 1.10x SIRE Financial Projections – Sisecam Wyoming Cash Flow Summary For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E 2028E Sisecam Wyoming Distributable Cash Flow Source: SIRE Financial Projections 9

Confidential – Preliminary and Subject to Change SIRE Situation Analysis ($ in millions) Distributable Cash Flow Surplus / (Shortfall) $40.8 $25.9 $23.8 $8.1 $7.3 $7.7 $6.4 Increase / (Decrease) in Net Working Capital (27.5) 0.4 15.7 8.2 0.8 (9.8) (1.0) Cash from Revolver / (Cash to Revolver) -- -- -- -- 1.4 5.7 -- Total Sources $13.3 $26.3 $39.5 $16.3 $9.5 $3.5 $5.4 Uses Growth Capital Expenditures $0.1 $-- $-- $-- $-- $-- $-- Mandatory Debt Paydown 8.6 8.8 9.1 9.3 9.5 3.5 4.9 Discretionary Debt Paydown 1.3 17.4 30.5 7.0 -- -- 0.5 Cash to (from) Balance Sheet (5.2) -- -- -- -- -- -- Other 8.4 -- -- -- -- -- -- Total Uses $13.3 $26.3 $39.5 $16.3 $9.5 $3.5 $5.4 Capital Structure Total Debt $148.6 $122.4 $82.8 $66.5 $58.4 $60.6 $55.2 Less: Cash (5.0) (5.0) (5.0) (5.0) (5.0) (5.0) (5.0) Net Debt $143.6 $117.4 $77.8 $61.5 $53.4 $55.6 $50.2 Net Debt / Adjusted EBITDA 0.9x 0.7x 0.5x 0.5x 0.5x 0.5x 0.5x SIRE Financial Projections – Sisecam Wyoming Sources and Uses For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E 2028E Sources Source: SIRE Financial Projections 10

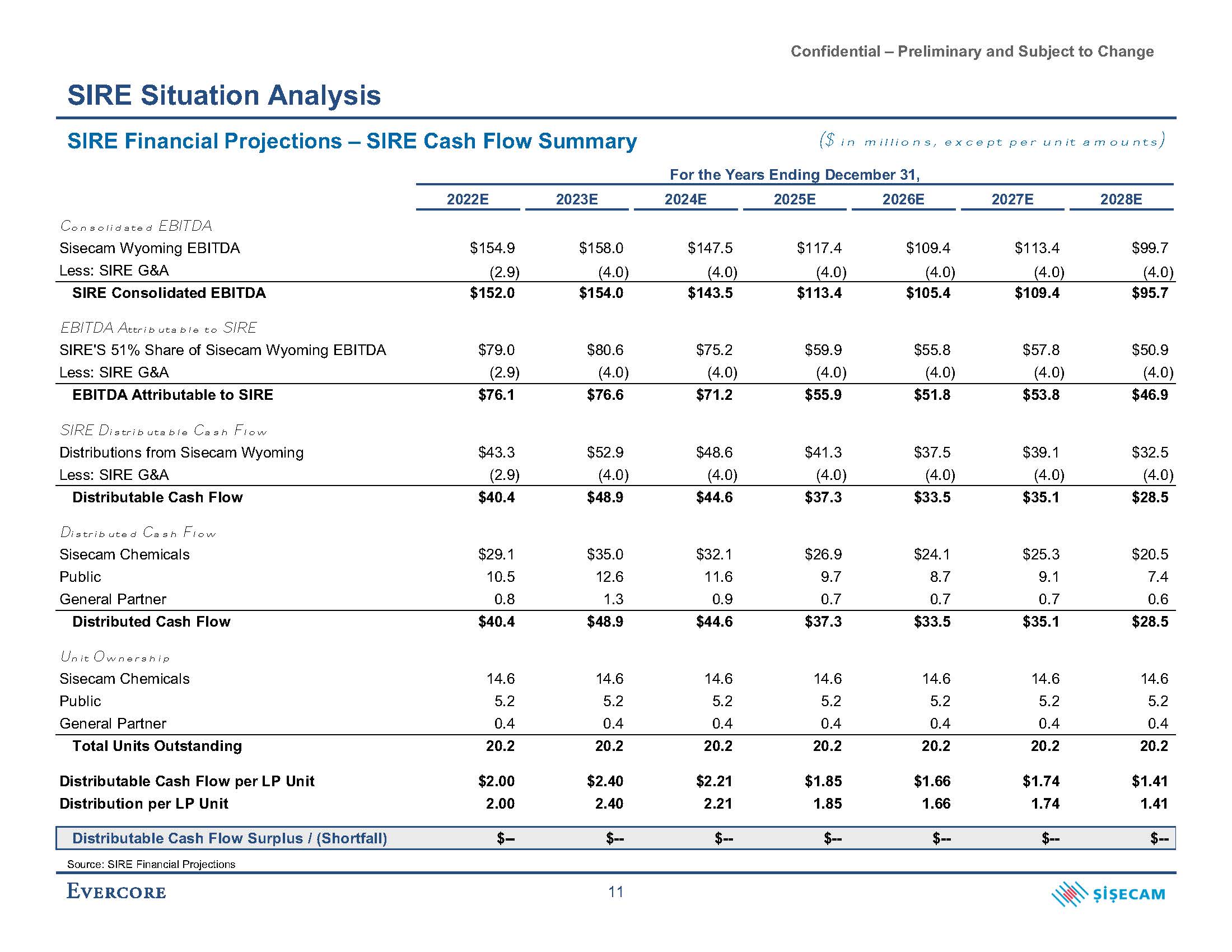

Confidential – Preliminary and Subject to Change SIRE Situation Analysis Source: SIRE Financial Projections 11 SIRE Financial Projections – SIRE Cash Flow Summary ($ in millions, except per unit amounts) For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E 2028E Consolidated EBITDA Sisecam Wyoming EBITDA $154.9 $158.0 $147.5 $117.4 $109.4 $113.4 $99.7 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) SIRE Consolidated EBITDA $152.0 $154.0 $143.5 $113.4 $105.4 $109.4 $95.7 EBITDA Attributable to SIRE SIRE'S 51% Share of Sisecam Wyoming EBITDA $79.0 $80.6 $75.2 $59.9 $55.8 $57.8 $50.9 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) EBITDA Attributable to SIRE $76.1 $76.6 $71.2 $55.9 $51.8 $53.8 $46.9 SIRE Distributable Cash Flow Distributions from Sisecam Wyoming $43.3 $52.9 $48.6 $41.3 $37.5 $39.1 $32.5 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) Distributable Cash Flow $40.4 $48.9 $44.6 $37.3 $33.5 $35.1 $28.5 Distributed Cash Flow Sisecam Chemicals $29.1 $35.0 $32.1 $26.9 $24.1 $25.3 $20.5 Public 10.5 12.6 11.6 9.7 8.7 9.1 7.4 General Partner 0.8 1.3 0.9 0.7 0.7 0.7 0.6 Distributed Cash Flow $40.4 $48.9 $44.6 $37.3 $33.5 $35.1 $28.5 Unit Ownership Sisecam Chemicals 14.6 14.6 14.6 14.6 14.6 14.6 14.6 Public 5.2 5.2 5.2 5.2 5.2 5.2 5.2 General Partner 0.4 0.4 0.4 0.4 0.4 0.4 0.4 Total Units Outstanding 20.2 20.2 20.2 20.2 20.2 20.2 20.2 Distributable Cash Flow per LP Unit $2.00 $2.40 $2.21 $1.85 $1.66 $1.74 $1.41 Distribution per LP Unit 2.00 2.40 2.21 1.85 1.66 1.74 1.41 Distributable Cash Flow Surplus / (Shortfall) $-- $-- $-- $-- $-- $-- $--

Confidential – Preliminary and Subject to Change III. Preliminary Valuation of SIRE Common Units

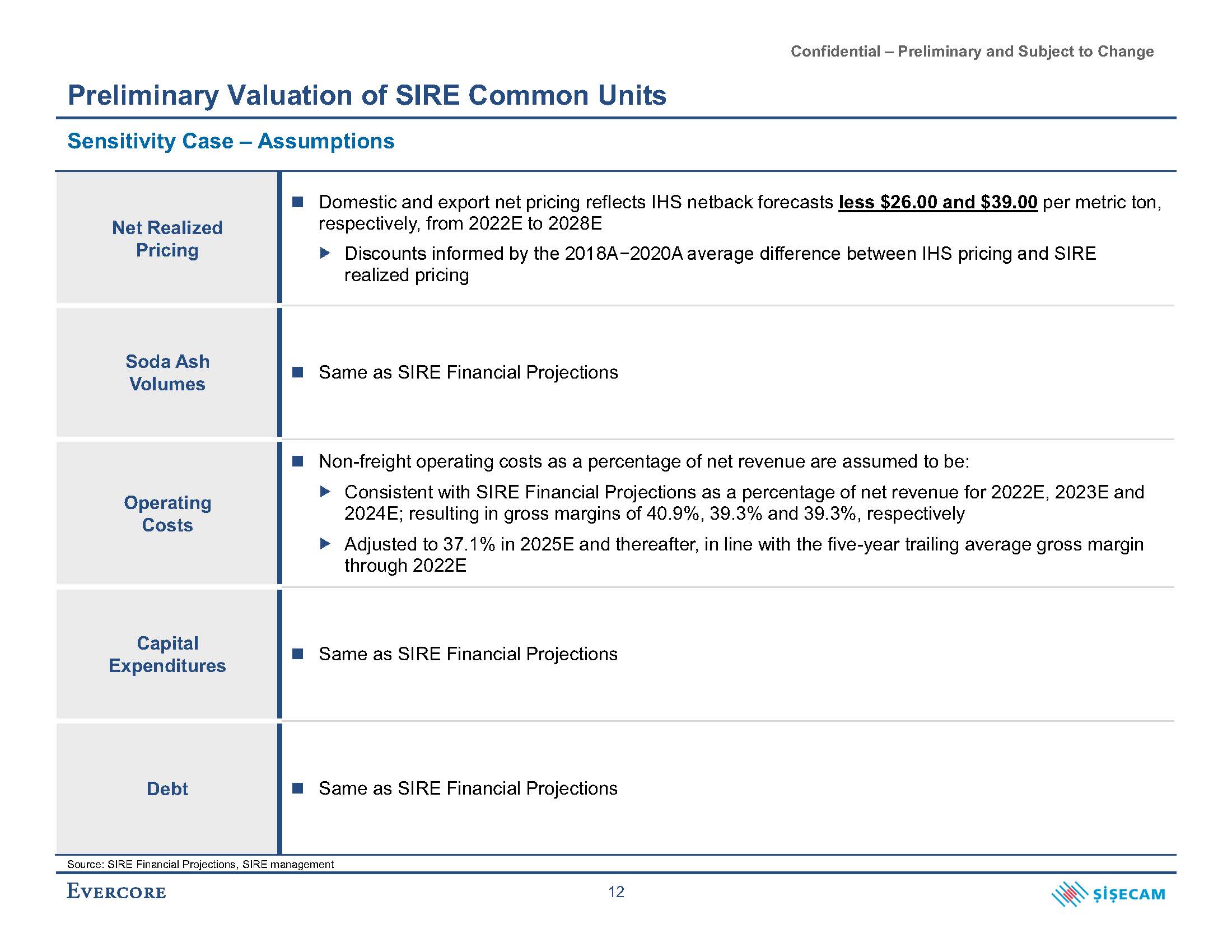

Confidential – Preliminary and Subject to Change Preliminary Valuation of SIRE Common Units Source: SIRE Financial Projections, SIRE management 12 Sensitivity Case – Assumptions Net Realized Pricing Domestic and export net pricing reflects IHS netback forecasts less $26.00 and $39.00 per metric ton, respectively, from 2022E to 2028E Discounts informed by the 2018A−2020A average difference between IHS pricing and SIRE realized pricing Soda Ash Volumes Same as SIRE Financial Projections Operating Costs Non-freight operating costs as a percentage of net revenue are assumed to be: Consistent with SIRE Financial Projections as a percentage of net revenue for 2022E, 2023E and 2024E; resulting in gross margins of 40.9%, 39.3% and 39.3%, respectively Adjusted to 37.1% in 2025E and thereafter, in line with the five-year trailing average gross margin through 2022E Capital Expenditures Same as SIRE Financial Projections Debt Same as SIRE Financial Projections

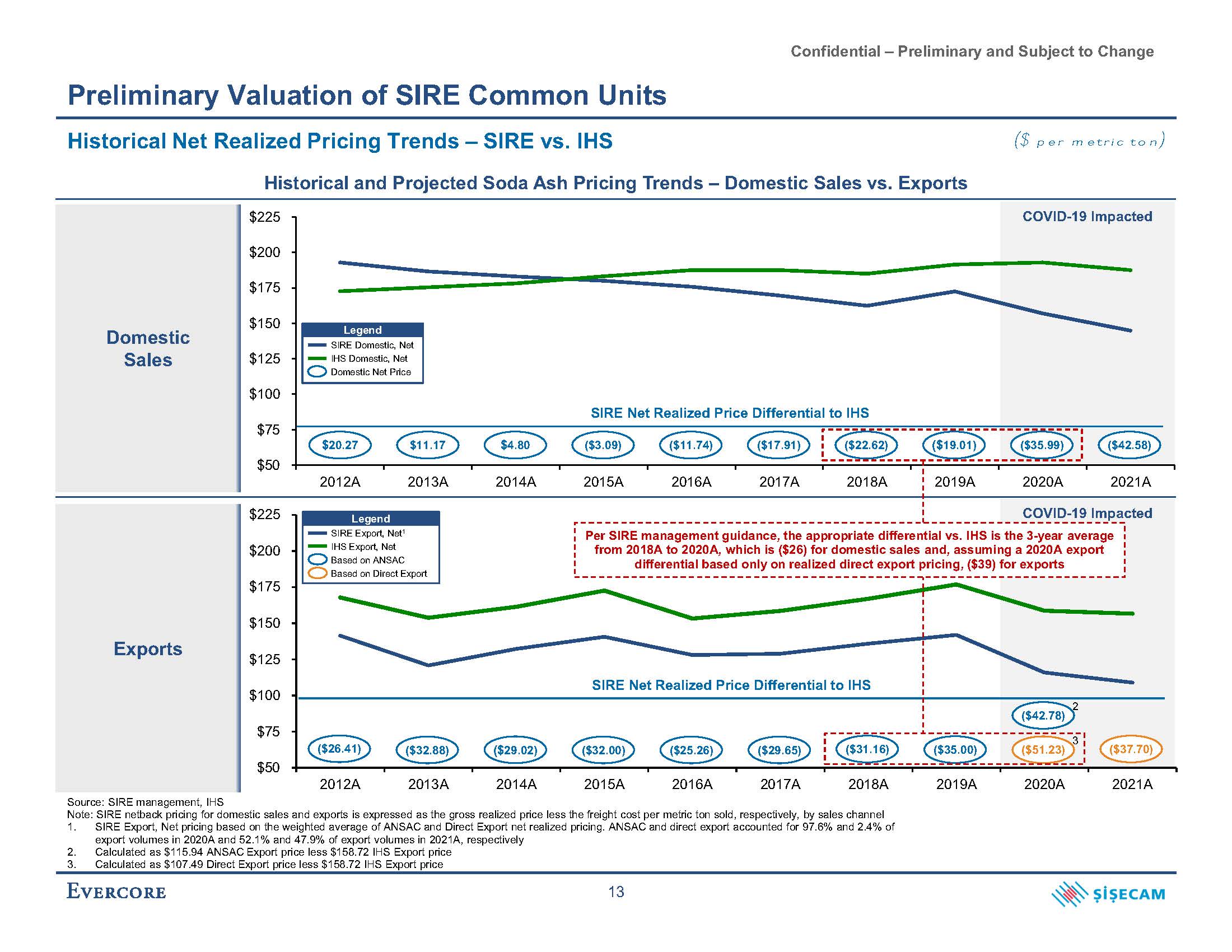

Confidential – Preliminary and Subject to Change $50 $75 $100 $125 $175 $150 $200 $225 2012A 2013A 2014A 2015A 2016A 2017A 2018A 2019A 2020A 2021A COVID-19 Impacted $50 $75 $100 $125 $150 $200 $175 $225 2012A 2013A 2014A 2019A 2020A 2021A COVID-19 Impacted Exports SIRE Net Realized Price Differential to IHS Preliminary Valuation of SIRE Common Units Historical Net Realized Pricing Trends – SIRE vs. IHS Historical and Projected Soda Ash Pricing Trends – Domestic Sales vs. Exports ($ per metric ton) Source: SIRE management, IHS Note: SIRE netback pricing for domestic sales and exports is expressed as the gross realized price less the freight cost per metric ton sold, respectively, by sales channel SIRE Export, Net pricing based on the weighted average of ANSAC and Direct Export net realized pricing. ANSAC and direct export accounted for 97.6% and 2.4% of export volumes in 2020A and 52.1% and 47.9% of export volumes in 2021A, respectively Calculated as $115.94 ANSAC Export price less $158.72 IHS Export price Calculated as $107.49 Direct Export price less $158.72 IHS Export price Domestic Sales $20.27 $11.17 $4.80 SIRE Net Realized Price Differential to IHS ($3.09) ($11.74) ($17.91) ($22.62) 2015A 2016A 2017A 2018A ($19.01) ($35.99) ($42.58) ($29.65) ($31.16) ($35.00) ($42.78) ($37.70) Per SIRE management guidance, the appropriate differential vs. IHS is the 3-year average from 2018A to 2020A, which is ($26) for domestic sales and, assuming a 2020A export differential based only on realized direct export pricing, ($39) for exports Legend SIRE Domestic, Net IHS Domestic, Net Domestic Net Price Legend SIRE Export, Net1 IHS Export, Net Based on ANSAC Based on Direct Export ($51.23) ($26.41) ($32.88) ($29.02) ($32.00) ($25.26) 2 13 3

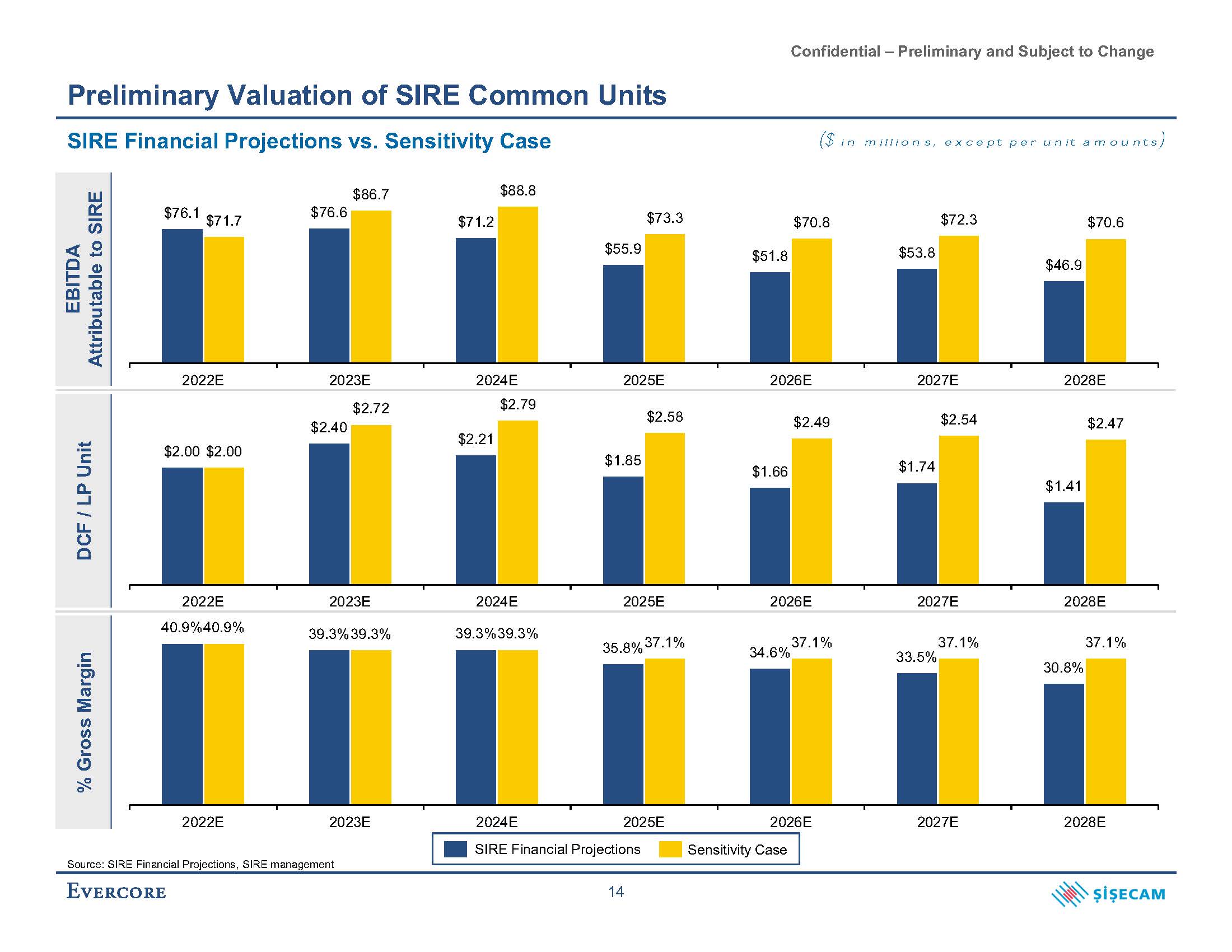

Confidential – Preliminary and Subject to Change $76.6 $71.2 $55.9 $51 $76.1 $71.7 $86.7 $88.8 $73.3 $70.8 20 $2.40 $2.21 $1.85 $1.66 $2.00 $2.00 $2.72 $2.79 $2.58 $2.49 $2.54 20 35.8% 34.6% 33.5% 30.8% 40.9%40.9% 39.3%39.3% 39.3%39.3% 37.1% 37.1% 37.1% 37.1% 2024E 2025E 2026E 2027E 2028E Preliminary Valuation of SIRE Common Units SIRE Financial Projections vs. Sensitivity Case SIRE Financial Projections Sensitivity Case EBITDA Attributable to SIRE DCF / LP Unit % Gross Margin 2022E 2023E Source: SIRE Financial Projections, SIRE management 14 ($ in millions, except per unit amounts)

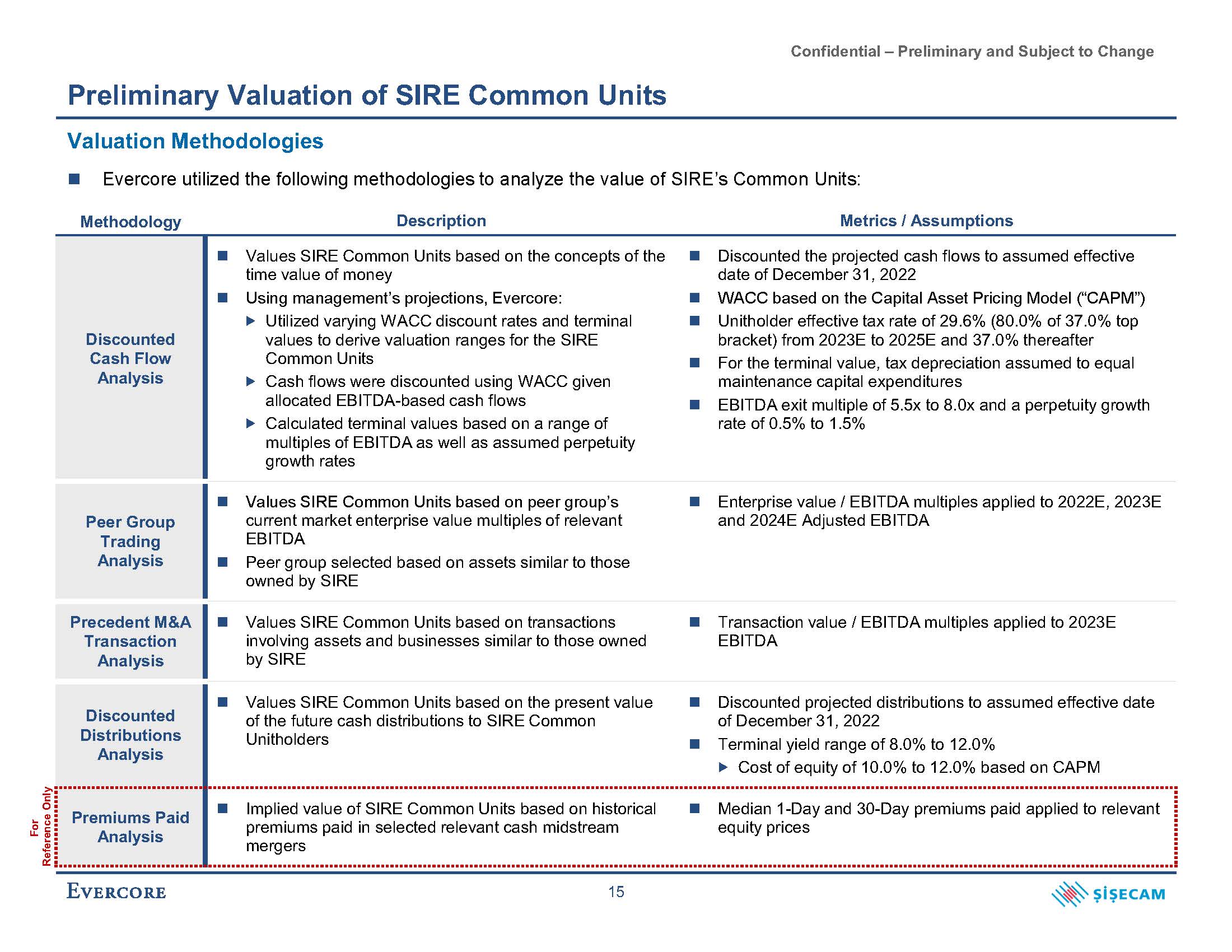

Confidential – Preliminary and Subject to Change Methodology Description Metrics / Assumptions Discounted Cash Flow Analysis Values SIRE Common Units based on the concepts of the time value of money Using management’s projections, Evercore: Utilized varying WACC discount rates and terminal values to derive valuation ranges for the SIRE Common Units Cash flows were discounted using WACC given allocated EBITDA-based cash flows Calculated terminal values based on a range of multiples of EBITDA as well as assumed perpetuity growth rates Discounted the projected cash flows to assumed effective date of December 31, 2022 WACC based on the Capital Asset Pricing Model (“CAPM”) Unitholder effective tax rate of 29.6% (80.0% of 37.0% top bracket) from 2023E to 2025E and 37.0% thereafter For the terminal value, tax depreciation assumed to equal maintenance capital expenditures EBITDA exit multiple of 5.5x to 8.0x and a perpetuity growth rate of 0.5% to 1.5% Peer Group Trading Analysis Values SIRE Common Units based on peer group’s current market enterprise value multiples of relevant EBITDA Peer group selected based on assets similar to those owned by SIRE Enterprise value / EBITDA multiples applied to 2022E, 2023E and 2024E Adjusted EBITDA Precedent M&A Transaction Analysis Values SIRE Common Units based on transactions involving assets and businesses similar to those owned by SIRE Transaction value / EBITDA multiples applied to 2023E EBITDA Discounted Distributions Analysis Values SIRE Common Units based on the present value of the future cash distributions to SIRE Common Unitholders Discounted projected distributions to assumed effective date of December 31, 2022 Terminal yield range of 8.0% to 12.0% Cost of equity of 10.0% to 12.0% based on CAPM Premiums Paid Analysis Implied value of SIRE Common Units based on historical premiums paid in selected relevant cash midstream mergers Median 1-Day and 30-Day premiums paid applied to relevant equity prices 15 Preliminary Valuation of SIRE Common Units Valuation Methodologies Evercore utilized the following methodologies to analyze the value of SIRE’s Common Units: For Reference Only

Confidential – Preliminary and Subject to Change Discounted Cash Flow Analysis Peer Group Trading Analysis Precedent M&A Transactions Analysis EBITDA Exit Multiple Perpetuity Growth 2022E EBITDA 2023E EBITDA 2024E EBITDA 2023E EBITDA EBITDA Exit Multiple: 5.5x - 8.0x Perpetuity Growth Rate: 0.5% - 1.5% 2022E EBITDA Multiple: 2023E EBITDA Multiple: 2024E EBITDA Multiple: 2023E EBITDA Multiple: 5.5x - 8.0x 5.0x - 7.5x 4.5x - 7.0x 6.0x - 8.5x Range of 24.4% - 29.6% Discount Rate: WACC of 8.5% - 9.5% Terminal Yield of: 8.0% - 12.0% Equity Cost of Capital of: 10.0% - 12.0% Premiums Paid Analysis Discounted Distributions Analysis $14.18 $21.54 $12.92 $21.35 $17.09 $15.84 $15.34 $17.76 $12.24 $16.09 $19.13 $22.05 $14.39 $21.79 $18.71 $28.21 $15.61 $25.96 $26.51 $24.72 $24.82 $28.49 $21.05 $27.08 $28.61 $32.78 $18.76 $29.33 $-- $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $50.00 $45.00 $40.00 $22.23 $23.27 Preliminary Valuation of SIRE Common Units Third Proposal: $22.00 SIRE Financial Projections vs. Sensitivity Case SIRE Financial Projections Sensitivity Case FOR REFERENCE ONLY 16

Confidential – Preliminary and Subject to Change Appendix

Confidential – Preliminary and Subject to Change A. Weighted Average Cost of Capital Analysis

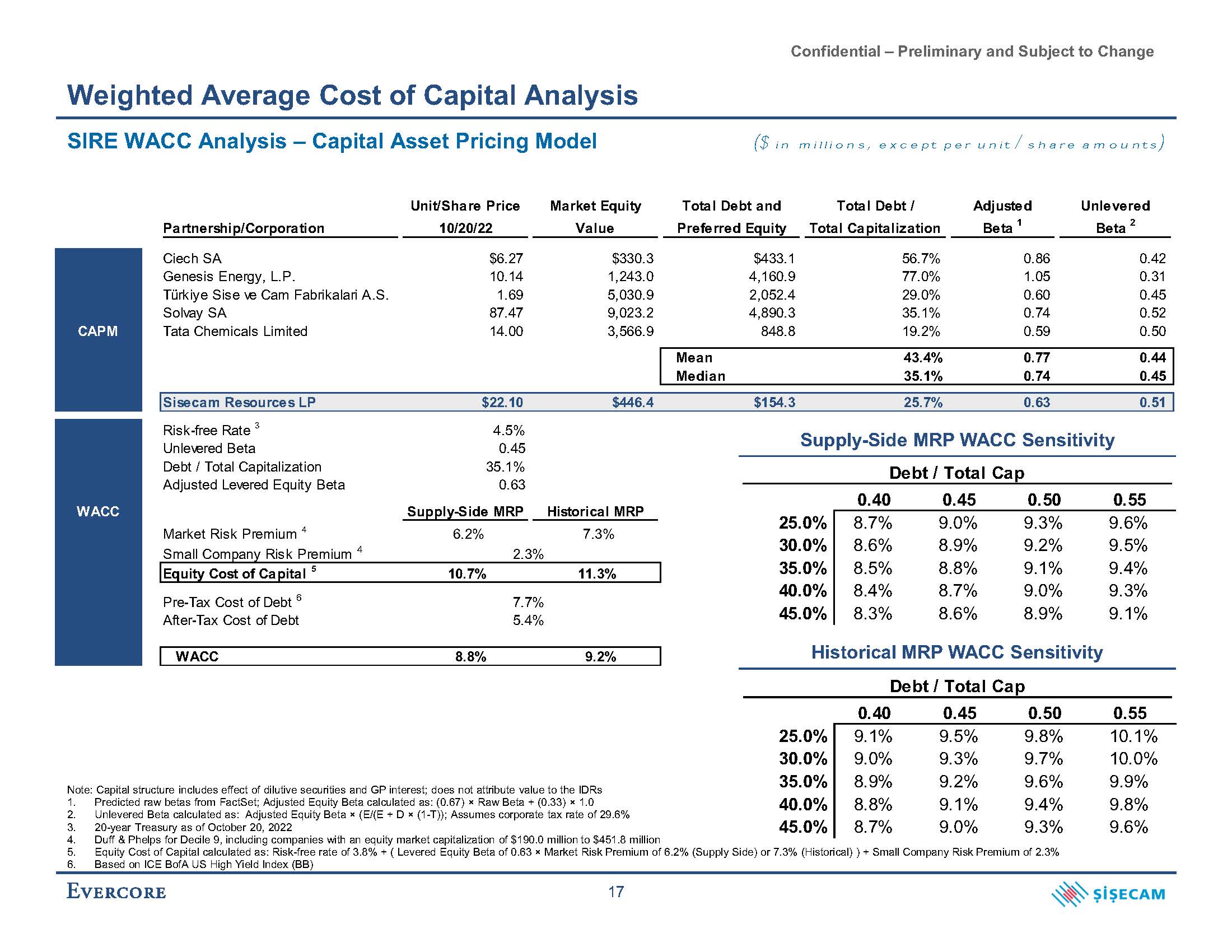

Confidential – Preliminary and Subject to Change Debt / Total Cap 0.40 0.45 0.50 0.55 25.0% 8.7% 9.0% 9.3% 9.6% 30.0% 8.6% 8.9% 9.2% 9.5% 35.0% 8.5% 8.8% 9.1% 9.4% 40.0% 8.4% 8.7% 9.0% 9.3% 45.0% 8.3% 8.6% 8.9% 9.1% Debt / Total Cap 0.40 0.45 0.50 0.55 25.0% 9.1% 9.5% 9.8% 10.1% 30.0% 9.0% 9.3% 9.7% 10.0% 35.0% 8.9% 9.2% 9.6% 9.9% 40.0% 8.8% 9.1% 9.4% 9.8% 45.0% 8.7% 9.0% 9.3% 9.6% Unit/Share Price Market Equity Total Debt and Total Debt / Partnership/Corporation 10/20/22 Value Preferred Equity Total Capitalization Adjusted Beta 1 Unlevered Beta 2 Ciech SA $6.27 $330.3 $433.1 56.7% 0.86 0.42 Genesis Energy, L.P. 10.14 1,243.0 4,160.9 77.0% 1.05 0.31 Türkiye Sise ve Cam Fabrikalari A.S. 1.69 5,030.9 2,052.4 29.0% 0.60 0.45 Solvay SA 87.47 9,023.2 4,890.3 35.1% 0.74 0.52 CAPM Tata Chemicals Limited 14.00 3,566.9 848.8 19.2% 0.59 0.50 Mean 43.4% 0.77 0.44 Median 35.1% 0.74 0.45 Sisecam Resources LP $22.10 $446.4 $154.3 25.7% 0.63 0.51 Risk-free Rate 3 Unlevered Beta Debt / Total Capitalization Adjusted Levered Equity Beta WACC 4.5% 0.45 35.1% 0.63 Supply-Side MRP Historical MRP Market Risk Premium 4 Small Company Risk Premium 4 6.2% 2.3% 7.3% Equity Cost of Capital 5 10.7% 11.3% Pre-Tax Cost of Debt 6 7.7% After-Tax Cost of Debt 5.4% WACC 8.8% 9.2% Weighted Average Cost of Capital Analysis SIRE WACC Analysis – Capital Asset Pricing Model ($ in millions, except per unit / share amounts) Note: Capital structure includes effect of dilutive securities and GP interest; does not attribute value to the IDRs Predicted raw betas from FactSet; Adjusted Equity Beta calculated as: (0.67) × Raw Beta + (0.33) × 1.0 Unlevered Beta calculated as: Adjusted Equity Beta × (E/(E + D × (1-T)); Assumes corporate tax rate of 29.6% 20-year Treasury as of October 20, 2022 Duff & Phelps for Decile 9, including companies with an equity market capitalization of $190.0 million to $451.8 million Equity Cost of Capital calculated as: Risk-free rate of 3.8% + ( Levered Equity Beta of 0.63 × Market Risk Premium of 6.2% (Supply Side) or 7.3% (Historical) ) + Small Company Risk Premium of 2.3% Based on ICE BofA US High Yield Index (BB) Supply-Side MRP WACC Sensitivity Historical MRP WACC Sensitivity 17

Confidential – Preliminary and Subject to Change B. Preliminary Valuation Detail – SIRE Financial Projections

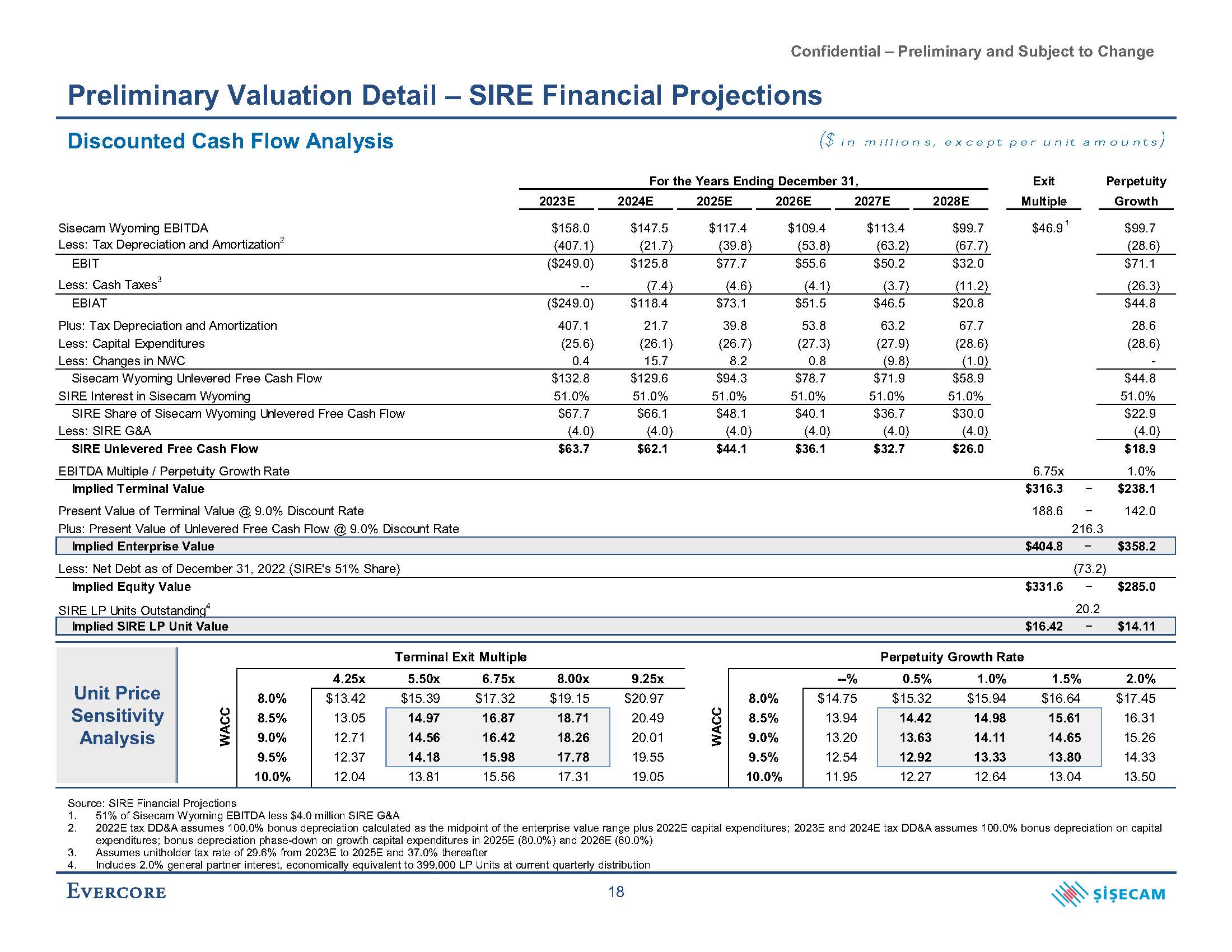

Confidential – Preliminary and Subject to Change Source: SIRE Financial Projections 51% of Sisecam Wyoming EBITDA less $4.0 million SIRE G&A 2022E tax DD&A assumes 100.0% bonus depreciation calculated as the midpoint of the enterprise value range plus 2022E capital expenditures; 2023E and 2024E tax DD&A assumes 100.0% bonus depreciation on capital expenditures; bonus depreciation phase-down on growth capital expenditures in 2025E (80.0%) and 2026E (60.0%) Assumes unitholder tax rate of 29.6% from 2023E to 2025E and 37.0% thereafter Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution Sisecam Wyoming EBITDA $158.0 $147.5 $117.4 $109.4 $113.4 $99.7 $46.9 1 $99.7 Less: Tax Depreciation and Amortization2 (407.1) (21.7) (39.8) (53.8) (63.2) (67.7) (28.6) EBIT ($249.0) $125.8 $77.7 $55.6 $50.2 $32.0 $71.1 Less: Cash Taxes3 -- (7.4) (4.6) (4.1) (3.7) (11.2) (26.3) EBIAT ($249.0) $118.4 $73.1 $51.5 $46.5 $20.8 $44.8 Plus: Tax Depreciation and Amortization 407.1 21.7 39.8 53.8 63.2 67.7 28.6 Less: Capital Expenditures (25.6) (26.1) (26.7) (27.3) (27.9) (28.6) (28.6) Less: Changes in NWC 0.4 15.7 8.2 0.8 (9.8) (1.0) - Sisecam Wyoming Unlevered Free Cash Flow $132.8 $129.6 $94.3 $78.7 $71.9 $58.9 $44.8 SIRE Interest in Sisecam Wyoming 51.0% 51.0% 51.0% 51.0% 51.0% 51.0% 51.0% SIRE Share of Sisecam Wyoming Unlevered Free Cash Flow $67.7 $66.1 $48.1 $40.1 $36.7 $30.0 $22.9 Less: SIRE G&A (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) SIRE Unlevered Free Cash Flow $63.7 $62.1 $44.1 $36.1 $32.7 $26.0 $18.9 EBITDA Multiple / Perpetuity Growth Rate 6.75x 1.0% Implied Terminal Value $316.3 − $238.1 Present Value of Terminal Value @ 9.0% Discount Rate Plus: Present Value of Unlevered Free Cash Flow @ 9.0% Discount Rate 188.6 − 216.3 142.0 Implied Enterprise Value $404.8 − $358.2 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (73.2) Implied Equity Value $331.6 − $285.0 SIRE LP Units Outstanding4 20.2 Implied SIRE LP Unit Value $16.42 − $14.11 For the Years Ending December 31, Exit Perpetuity 2023E 2024E 2025E 2026E 2027E 2028E Multiple Growth Discounted Cash Flow Analysis Preliminary Valuation Detail – SIRE Financial Projections Terminal Exit Multiple Perpetuity Growth Rate WACC Unit Price 4.25x 5.50x 6.75x 8.00x 9.25x WACC --% 0.5% 1.0% 1.5% 2.0% 8.0% $13.42 $15.39 $17.32 $19.15 $20.97 8.0% $14.75 $15.32 $15.94 $16.64 $17.45 Sensitivity 8.5% 13.05 14.97 16.87 18.71 20.49 8.5% 13.94 14.42 14.98 15.61 16.31 Analysis 9.0% 12.71 14.56 16.42 18.26 20.01 9.0% 13.20 13.63 14.11 14.65 15.26 9.5% 12.37 14.18 15.98 17.78 19.55 9.5% 12.54 12.92 13.33 13.80 14.33 10.0% 12.04 13.81 15.56 17.31 19.05 10.0% 11.95 12.27 12.64 13.04 13.50 ($ in millions, except per unit amounts)

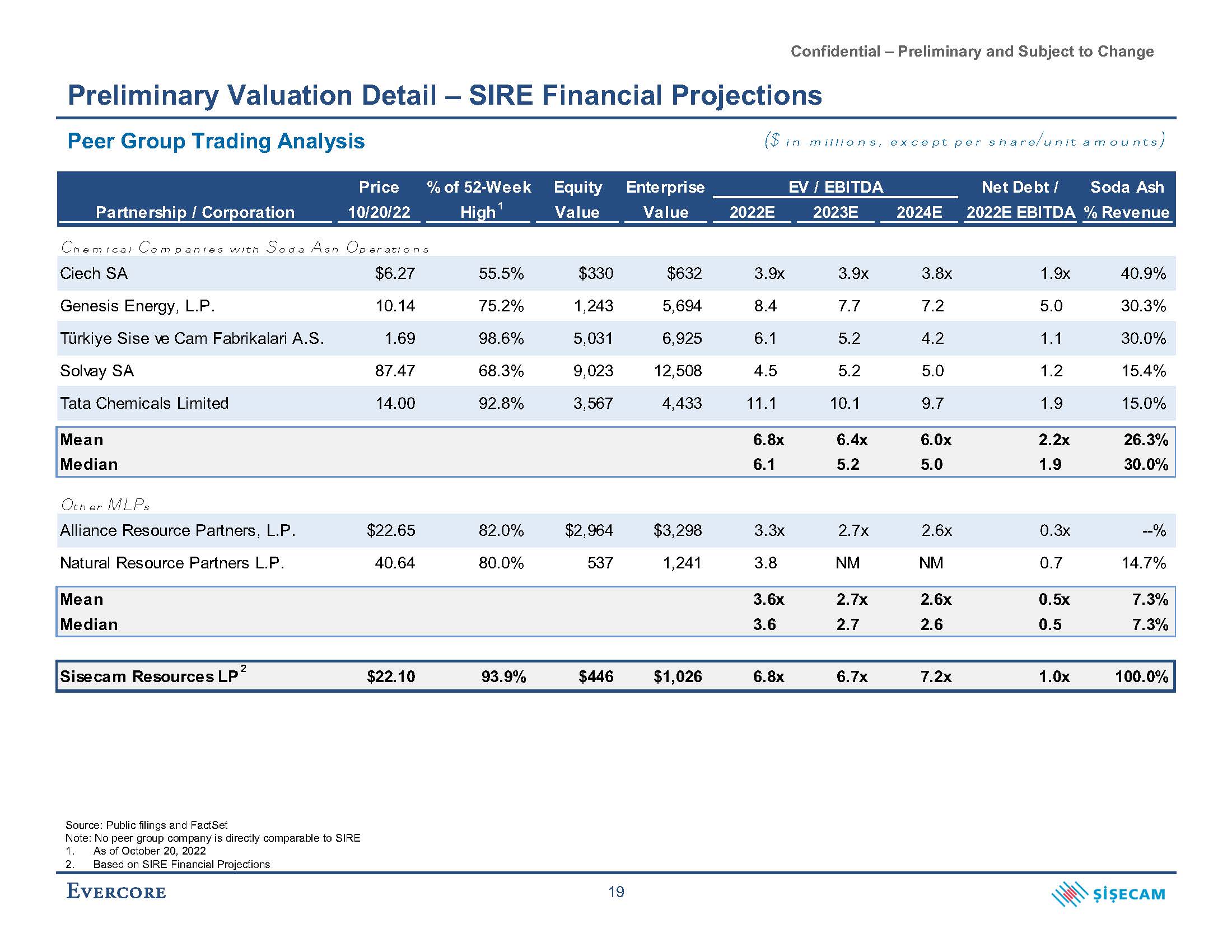

Confidential – Preliminary and Subject to Change Preliminary Valuation Detail – SIRE Financial Projections Peer Group Trading Analysis Source: Public filings and FactSet Note: No peer group company is directly comparable to SIRE 1. As of October 20, 2022 ($ in millions, except per share/unit amounts) Equity Enterprise EV / EBITDA Net Debt / Soda A Value Value 2022E 2023E 2024E 2022E EBITDA % Price % of 52-Week Partnership / Corporation 10/20/22 High 1 Chemical Companies with Soda Ash Operations Ciech SA $6.27 55.5% $330 $632 3.9x 3.9x 3.8x Genesis Energy, L.P. 10.14 75.2% 1,243 5,694 8.4 7.7 Türkiye Sise ve Cam Fabrikalari A.S. 1.69 98.6% 5,031 6,925 6.1 Solvay SA 87.47 68.3% 9,023 12,508 Tata Chemicals Limited 14.00 92.8% 3,567 4,4 Mean Median Other MLPs Alliance Resource Partners, L.P. $22.6 Natural Resource Partners L.P. Mean Median Sise 2 2. Based on SIRE Financial Projections 19

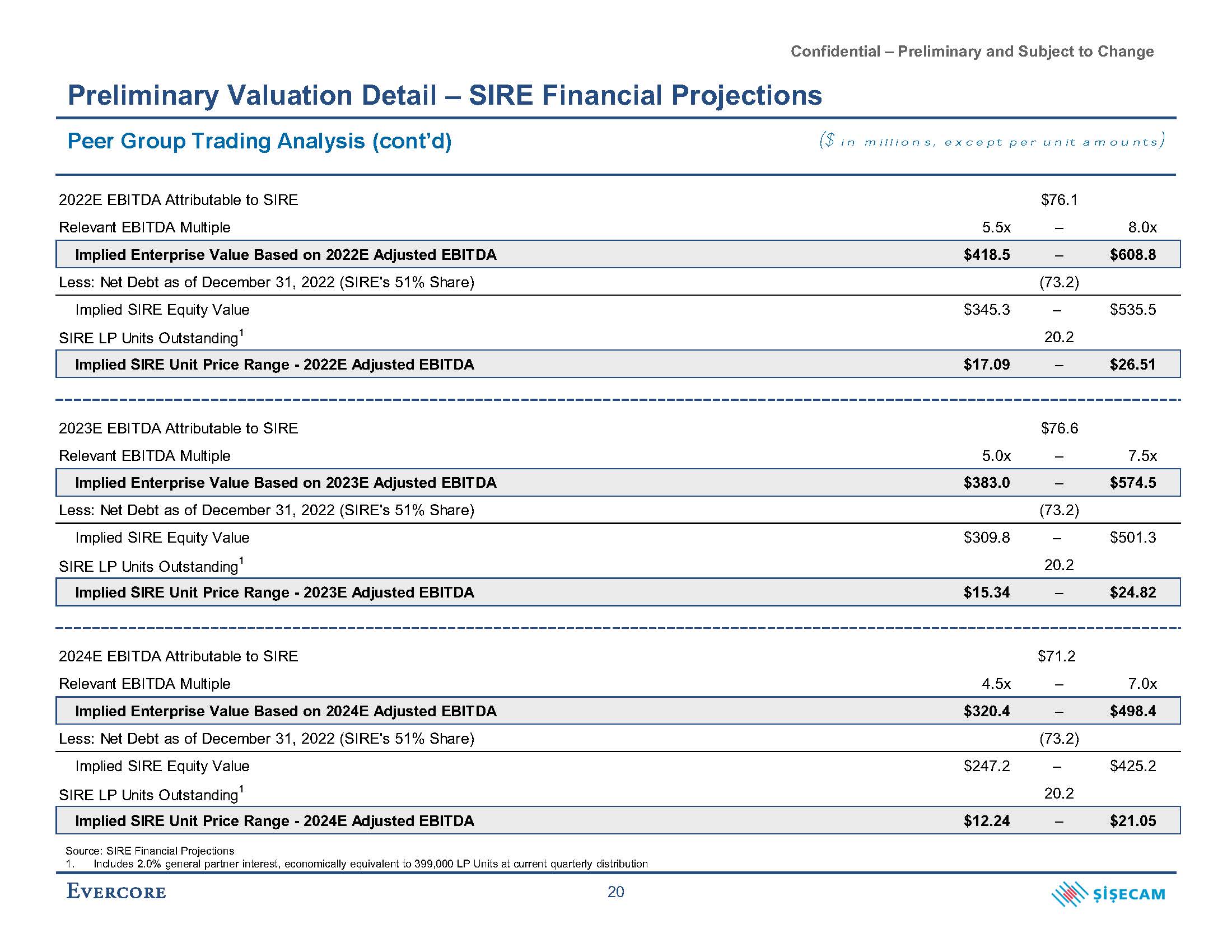

Confidential – Preliminary and Subject to Change Preliminary Valuation Detail – SIRE Financial Projections Peer Group Trading Analysis (cont’d) ($ in millions, except per unit amounts) 2022E EBITDA Attributable to SIRE Relevant EBITDA Multiple 5.5x $76.1 – 8.0x Implied Enterprise Value Based on 2022E Adjusted EBITDA $418.5 – $608.8 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (73.2) Implied SIRE Equity Value SIRE LP Units Outstanding1 $345.3 – 20.2 $535.5 Implied SIRE Unit Price Range - 2022E Adjusted EBITDA $17.09 – $26.51 2023E EBITDA Attributable to SIRE Relevant EBITDA Multiple 5.0x $76.6 – 7.5x Implied Enterprise Value Based on 2023E Adjusted EBITDA $383.0 – $574.5 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (73.2) Implied SIRE Equity Value SIRE LP Units Outstanding1 $309.8 – 20.2 $501.3 Implied SIRE Unit Price Range - 2023E Adjusted EBITDA $15.34 – $24.82 2024E EBITDA Attributable to SIRE Relevant EBITDA Multiple 4.5x $71.2 – 7.0x Implied Enterprise Value Based on 2024E Adjusted EBITDA $320.4 – $498.4 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (73.2) Implied SIRE Equity Value SIRE LP Units Outstanding1 $247.2 – 20.2 $425.2 Implied SIRE Unit Price Range - 2024E Adjusted EBITDA $12.24 – $21.05 Source: SIRE Financial Projections 1. Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution 20

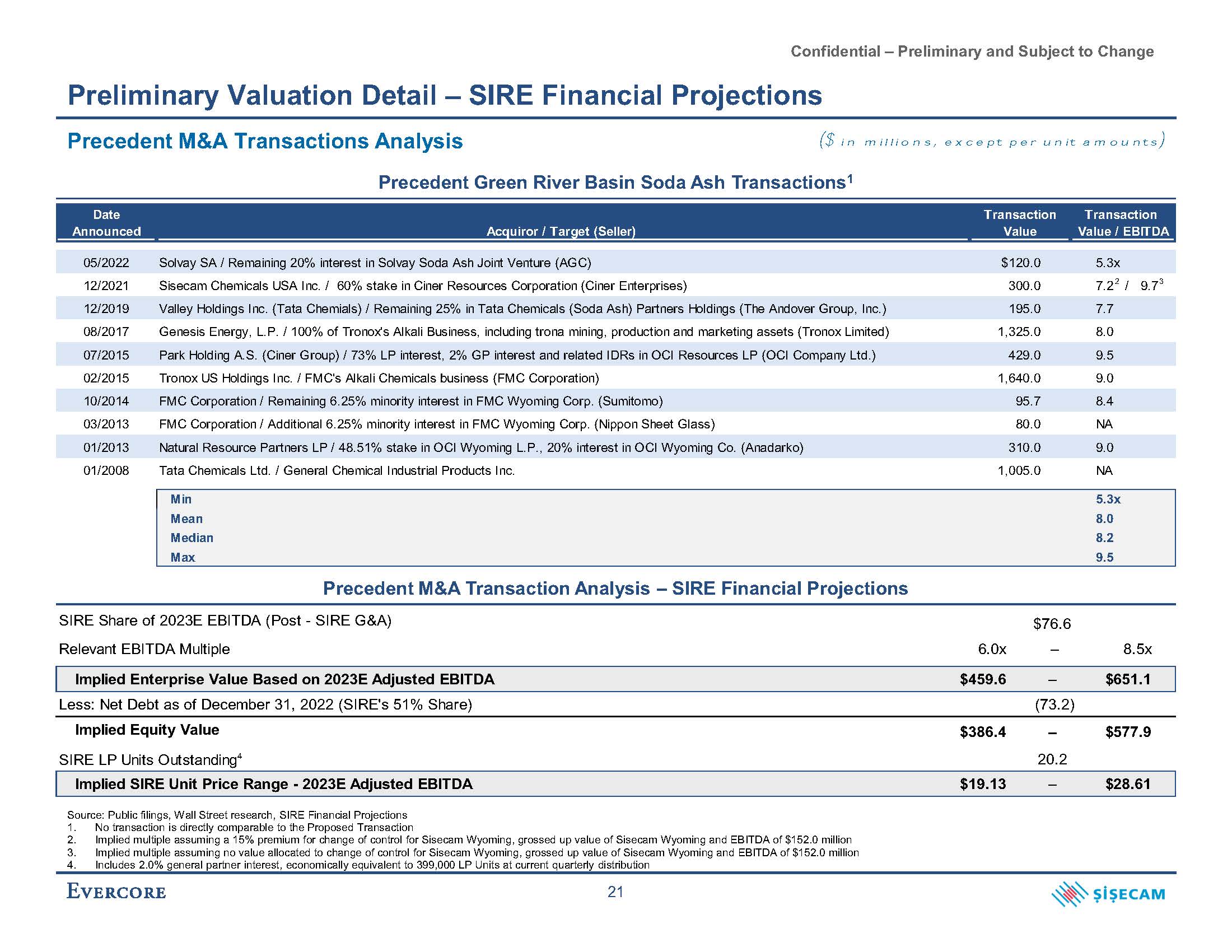

Confidential – Preliminary and Subject to Change Precedent Green River Basin Soda Ash Transactions1 Date Announced Acquiror / Target (Seller) Transaction Value Transaction Value / EBITDA 05/2022 Solvay SA / Remaining 20% interest in Solvay Soda Ash Joint Venture (AGC) $120.0 5.3x 12/2021 Sisecam Chemicals USA Inc. / 60% stake in Ciner Resources Corporation (Ciner Enterprises) 300.0 7.2 2 / 9.73 12/2019 Valley Holdings Inc. (Tata Chemials) / Remaining 25% in Tata Chemicals (Soda Ash) Partners Holdings (The Andover Group, Inc.) 195.0 7.7 08/2017 Genesis Energy, L.P. / 100% of Tronox's Alkali Business, including trona mining, production and marketing assets (Tronox Limited) 1,325.0 8.0 07/2015 Park Holding A.S. (Ciner Group) / 73% LP interest, 2% GP interest and related IDRs in OCI Resources LP (OCI Company Ltd.) 429.0 9.5 02/2015 Tronox US Holdings Inc. / FMC's Alkali Chemicals business (FMC Corporation) 1,640.0 9.0 10/2014 FMC Corporation / Remaining 6.25% minority interest in FMC Wyoming Corp. (Sumitomo) 95.7 8.4 03/2013 FMC Corporation / Additional 6.25% minority interest in FMC Wyoming Corp. (Nippon Sheet Glass) 80.0 NA 01/2013 Natural Resource Partners LP / 48.51% stake in OCI Wyoming L.P., 20% interest in OCI Wyoming Co. (Anadarko) 310.0 9.0 01/2008 Tata Chemicals Ltd. / General Chemical Industrial Products Inc. 1,005.0 NA Min 5.3x Mean 8.0 Median 8.2 Max 9.5 Precedent M&A Transaction Analysis – SIRE Financial Projections SIRE Share of 2023E EBITDA (Post - SIRE G&A) $76.6 Relevant EBITDA Multiple 6.0x – 8.5x Implied Enterprise Value Based on 2023E Adjusted EBITDA $459.6 – $651.1 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (73.2) Implied Equity Value $386.4 – $577.9 SIRE LP Units Outstanding4 20.2 Implied SIRE Unit Price Range - 2023E Adjusted EBITDA $19.13 – $28.61 4. Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution 21 Source: Public filings, Wall Street research, SIRE Financial Projections No transaction is directly comparable to the Proposed Transaction Implied multiple assuming a 15% premium for change of control for Sisecam Wyoming, grossed up value of Sisecam Wyoming and EBITDA of $152.0 million Implied multiple assuming no value allocated to change of control for Sisecam Wyoming, grossed up value of Sisecam Wyoming and EBITDA of $152.0 million Preliminary Valuation Detail – SIRE Financial Projections Precedent M&A Transactions Analysis ($ in millions, except per unit amounts)

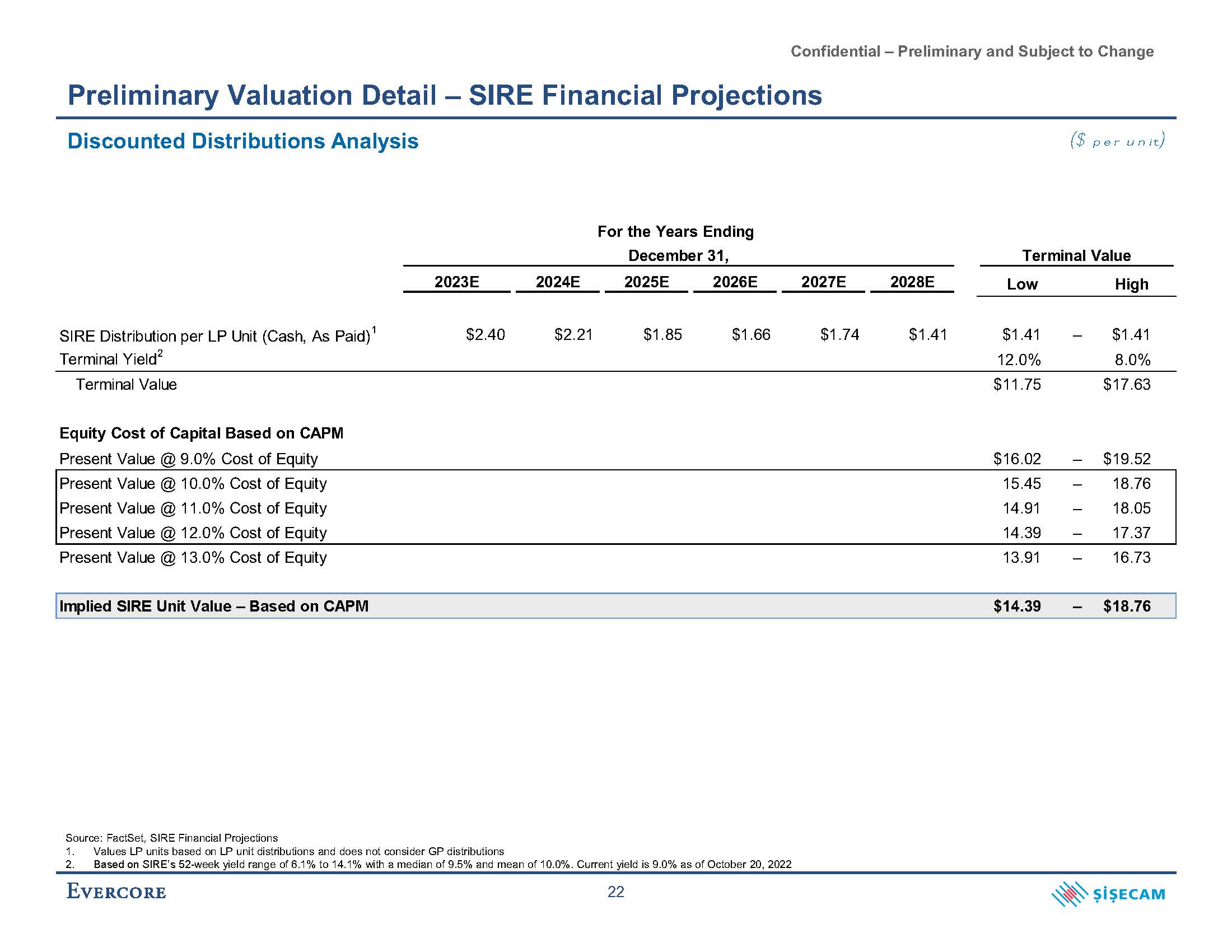

Confidential – Preliminary and Subject to Change Preliminary Valuation Detail – SIRE Financial Projections Discounted Distributions Analysis SIRE Distribution per LP Unit (Cash, As Paid)1 $2.40 $2.21 $1.85 $1.66 $1.74 $1.41 $1.41 – $1.41 Terminal Yield2 12.0% 8.0% Terminal Value $11.75 $17.63 Equity Cost of Capital Based on CAPM Present Value @ 9.0% Cost of Equity $16.02 – $19.52 Present Value @ 10.0% Cost of Equity 15.45 – 18.76 Present Value @ 11.0% Cost of Equity 14.91 – 18.05 Present Value @ 12.0% Cost of Equity 14.39 – 17.37 Present Value @ 13.0% Cost of Equity 13.91 – 16.73 Implied SIRE Unit Value – Based on CAPM $14.39 – $18.76 For the Years Ending December 31, 2023E 2024E 2025E 2026E 2027E 2028E Terminal Value Low High ($ per unit) 2. Based on SIRE’s 52-week yield range of 6.1% to 14.1% with a median of 9.5% and mean of 10.0%. Current yield is 9.0% as of October 20, 2022 22 Source: FactSet, SIRE Financial Projections 1. Values LP units based on LP unit distributions and does not consider GP distributions

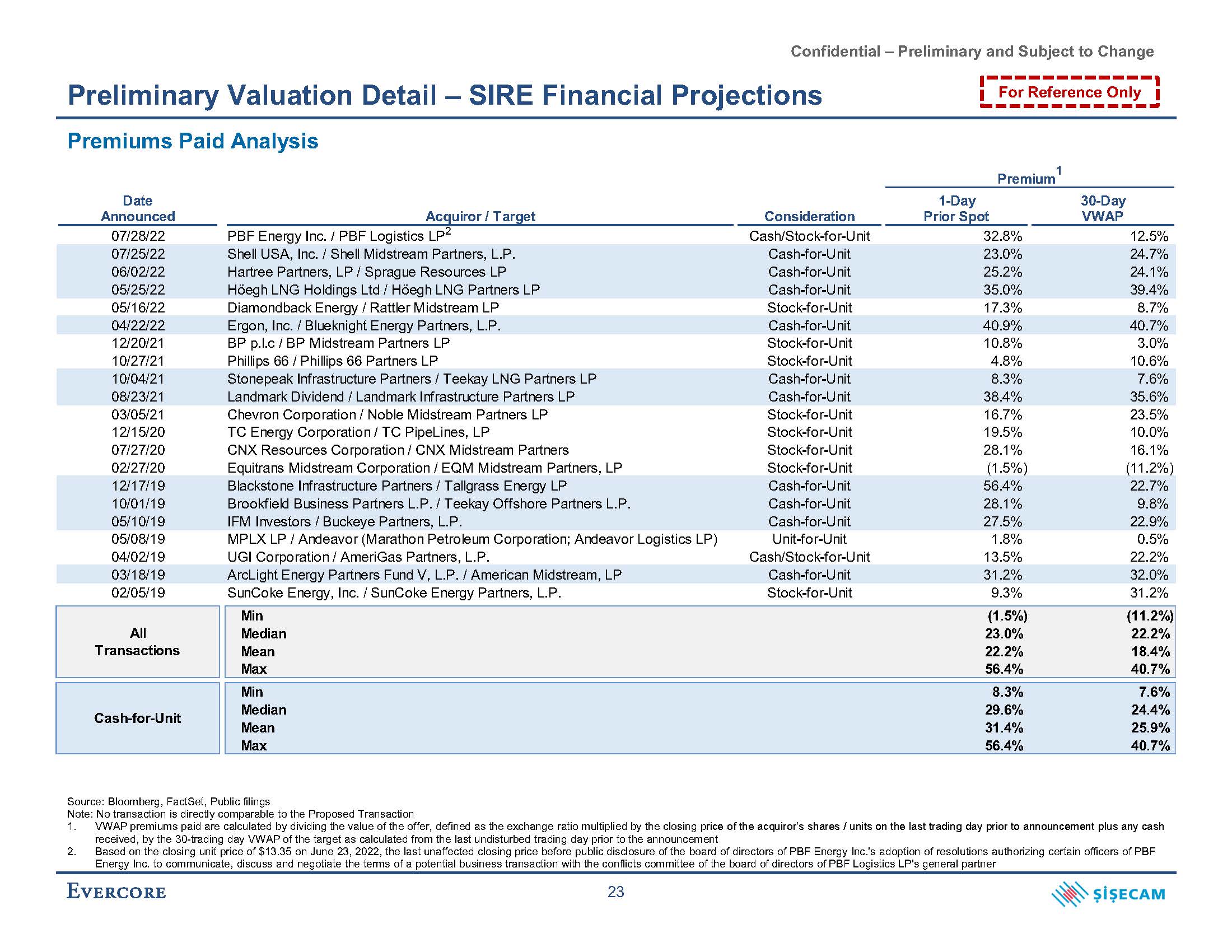

Confidential – Preliminary and Subject to Change Premiums Paid Analysis Premiu 1 m Date Announced Acquiror / Target Consideration 1-Day Prior Spot 30-Day VWAP 07/28/22 PBF Energy Inc. / PBF Logistics LP2 Cash/Stock-for-Unit 32.8% 12.5% 07/25/22 Shell USA, Inc. / Shell Midstream Partners, L.P. Cash-for-Unit 23.0% 24.7% 06/02/22 Hartree Partners, LP / Sprague Resources LP Cash-for-Unit 25.2% 24.1% 05/25/22 Höegh LNG Holdings Ltd / Höegh LNG Partners LP Cash-for-Unit 35.0% 39.4% 05/16/22 Diamondback Energy / Rattler Midstream LP Stock-for-Unit 17.3% 8.7% 04/22/22 Ergon, Inc. / Blueknight Energy Partners, L.P. Cash-for-Unit 40.9% 40.7% 12/20/21 BP p.l.c / BP Midstream Partners LP Stock-for-Unit 10.8% 3.0% 10/27/21 Phillips 66 / Phillips 66 Partners LP Stock-for-Unit 4.8% 10.6% 10/04/21 Stonepeak Infrastructure Partners / Teekay LNG Partners LP Cash-for-Unit 8.3% 7.6% 08/23/21 Landmark Dividend / Landmark Infrastructure Partners LP Cash-for-Unit 38.4% 35.6% 03/05/21 Chevron Corporation / Noble Midstream Partners LP Stock-for-Unit 16.7% 23.5% 12/15/20 TC Energy Corporation / TC PipeLines, LP Stock-for-Unit 19.5% 10.0% 07/27/20 CNX Resources Corporation / CNX Midstream Partners Stock-for-Unit 28.1% 16.1% 02/27/20 Equitrans Midstream Corporation / EQM Midstream Partners, LP Stock-for-Unit (1.5%) (11.2%) 12/17/19 Blackstone Infrastructure Partners / Tallgrass Energy LP Cash-for-Unit 56.4% 22.7% 10/01/19 Brookfield Business Partners L.P. / Teekay Offshore Partners L.P. Cash-for-Unit 28.1% 9.8% 05/10/19 IFM Investors / Buckeye Partners, L.P. Cash-for-Unit 27.5% 22.9% 05/08/19 MPLX LP / Andeavor (Marathon Petroleum Corporation; Andeavor Logistics LP) Unit-for-Unit 1.8% 0.5% 04/02/19 UGI Corporation / AmeriGas Partners, L.P. Cash/Stock-for-Unit 13.5% 22.2% 03/18/19 ArcLight Energy Partners Fund V, L.P. / American Midstream, LP Cash-for-Unit 31.2% 32.0% 02/05/19 SunCoke Energy, Inc. / SunCoke Energy Partners, L.P. Stock-for-Unit 9.3% 31.2% Preliminary Valuation Detail – SIRE Financial Projections Energy Inc. to communicate, discuss and negotiate the terms of a potential business transaction with the conflicts committee of the board of directors of PBF Logistics LP's general partner 23 For Reference Only Source: Bloomberg, FactSet, Public filings Note: No transaction is directly comparable to the Proposed Transaction VWAP premiums paid are calculated by dividing the value of the offer, defined as the exchange ratio multiplied by the closing price of the acquiror’s shares / units on the last trading day prior to announcement plus any cash received, by the 30-trading day VWAP of the target as calculated from the last undisturbed trading day prior to the announcement Based on the closing unit price of $13.35 on June 23, 2022, the last unaffected closing price before public disclosure of the board of directors of PBF Energy Inc.'s adoption of resolutions authorizing certain officers of PBF Min (1.5%) (11.2%) All Median 23.0% 22.2% Transactions Mean 22.2% 18.4% Max 56.4% 40.7% Min 8.3% 7.6% Cash-for-Unit Median Mean 29.6% 31.4% 24.4% 25.9% Max 56.4% 40.7%

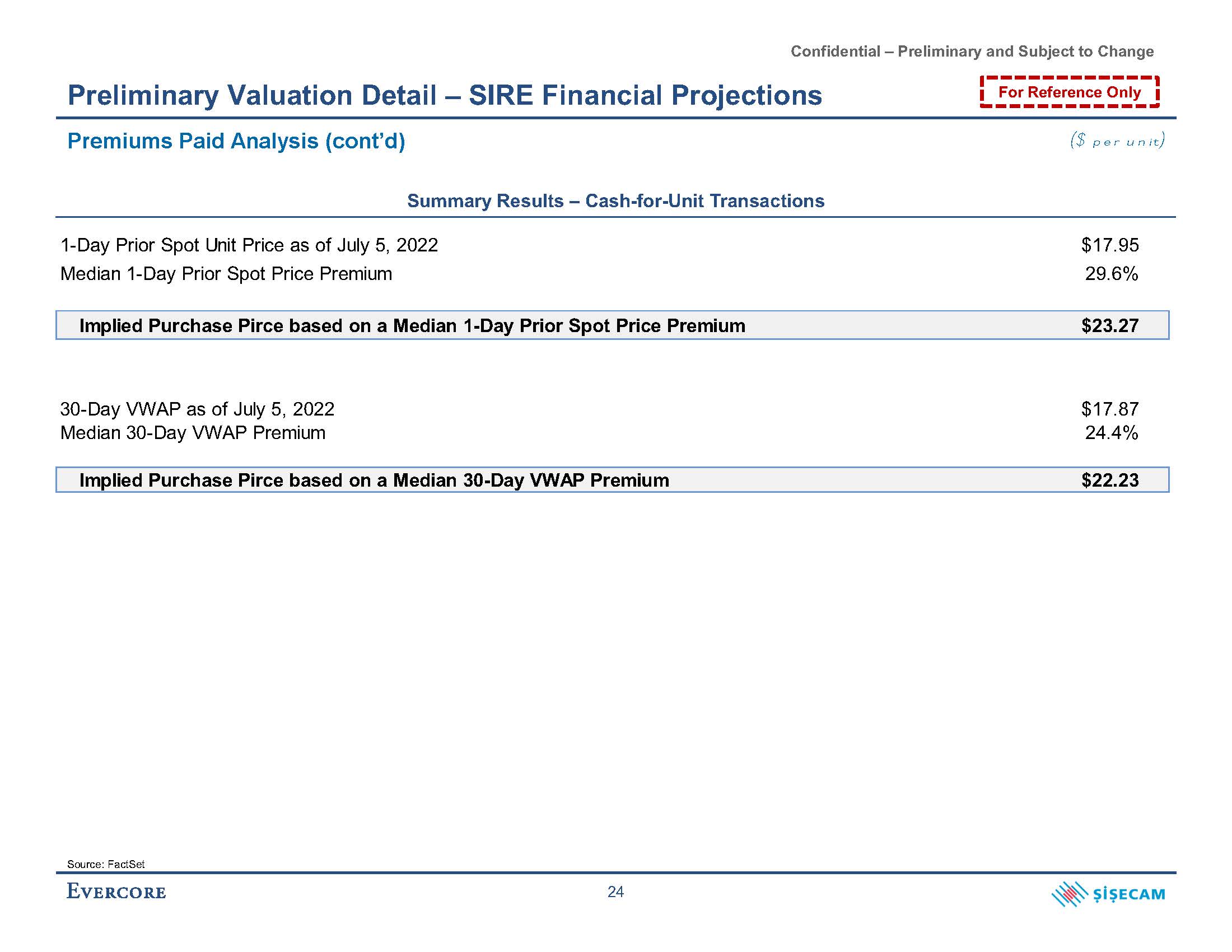

Confidential – Preliminary and Subject to Change Preliminary Valuation Detail – SIRE Financial Projections Premiums Paid Analysis (cont’d) Summary Results – Cash-for-Unit Transactions Source: FactSet 24 For Reference Only ($ per unit) 1-Day Prior Spot Unit Price as of July 5, 2022 Median 1-Day Prior Spot Price Premium $17.95 29.6% Implied Purchase Pirce based on a Median 1-Day Prior Spot Price Premium $23.27 30-Day VWAP as of July 5, 2022 Median 30-Day VWAP Premium $17.87 24.4% Implied Purchase Pirce based on a Median 30-Day VWAP Premium $22.23

Confidential – Preliminary and Subject to Change C. Financial Projections and Preliminary Valuation Detail – Sensitivity Case

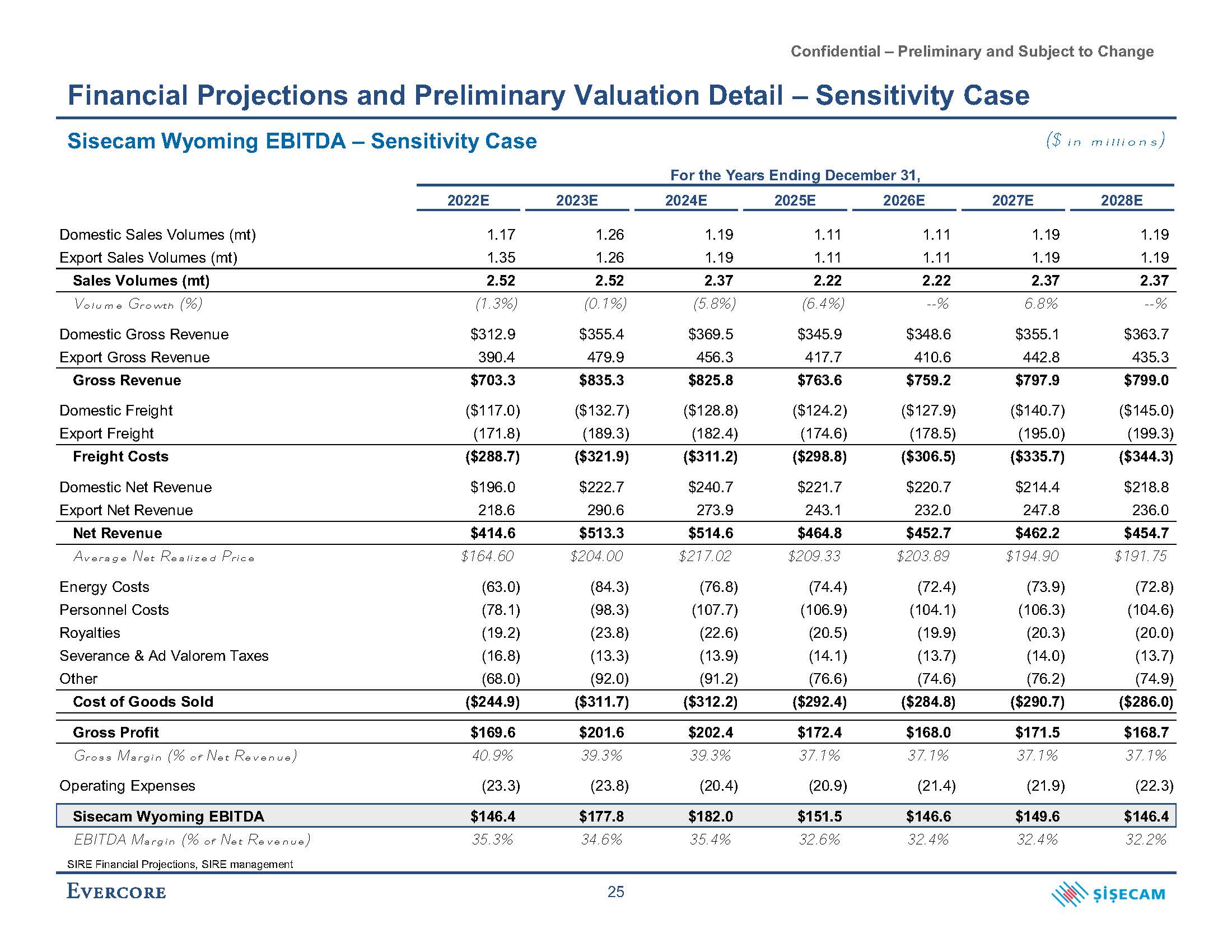

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case SIRE Financial Projections, SIRE management 25 Sisecam Wyoming EBITDA – Sensitivity Case 2022E 2023E 2024E 2025E 2026E 2027E 2028E Domestic Sales Volumes (mt) 1.17 1.26 1.19 1.11 1.11 1.19 1.19 Export Sales Volumes (mt) 1.35 1.26 1.19 1.11 1.11 1.19 1.19 Sales Volumes (mt) 2.52 2.52 2.37 2.22 2.22 2.37 2.37 Volume Growth (%) (1.3%) (0.1%) (5.8%) (6.4%) --% 6.8% --% Domestic Gross Revenue $312.9 $355.4 $369.5 $345.9 $348.6 $355.1 $363.7 Export Gross Revenue 390.4 479.9 456.3 417.7 410.6 442.8 435.3 Gross Revenue $703.3 $835.3 $825.8 $763.6 $759.2 $797.9 $799.0 Domestic Freight ($117.0) ($132.7) ($128.8) ($124.2) ($127.9) ($140.7) ($145.0) Export Freight (171.8) (189.3) (182.4) (174.6) (178.5) (195.0) (199.3) Freight Costs ($288.7) ($321.9) ($311.2) ($298.8) ($306.5) ($335.7) ($344.3) Domestic Net Revenue $196.0 $222.7 $240.7 $221.7 $220.7 $214.4 $218.8 Export Net Revenue 218.6 290.6 273.9 243.1 232.0 247.8 236.0 Net Revenue $414.6 $513.3 $514.6 $464.8 $452.7 $462.2 $454.7 Average Net Realized Price $164.60 $204.00 $217.02 $209.33 $203.89 $194.90 $191.75 Energy Costs (63.0) (84.3) (76.8) (74.4) (72.4) (73.9) (72.8) Personnel Costs (78.1) (98.3) (107.7) (106.9) (104.1) (106.3) (104.6) Royalties (19.2) (23.8) (22.6) (20.5) (19.9) (20.3) (20.0) Severance & Ad Valorem Taxes (16.8) (13.3) (13.9) (14.1) (13.7) (14.0) (13.7) Other (68.0) (92.0) (91.2) (76.6) (74.6) (76.2) (74.9) Cost of Goods Sold ($244.9) ($311.7) ($312.2) ($292.4) ($284.8) ($290.7) ($286.0) Gross Profit $169.6 $201.6 $202.4 $172.4 $168.0 $171.5 $168.7 Gross Margin (% of Net Revenue) 40.9% 39.3% 39.3% 37.1% 37.1% 37.1% 37.1% Operating Expenses (23.3) (23.8) (20.4) (20.9) (21.4) (21.9) (22.3) Sisecam Wyoming EBITDA $146.4 $177.8 $182.0 $151.5 $146.6 $149.6 $146.4 EBITDA Margin (% of Net Revenue) 35.3% 34.6% 35.4% 32.6% 32.4% 32.4% 32.2% For the Years Ending December 31, ($ in millions)

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case Sisecam Wyoming EBITDA $146.4 $177.8 $182.0 $151.5 $146.6 $149.6 $146.4 Less: Cash Interest Expense (4.1) (2.9) (2.1) (1.4) (1.0) (0.8) (0.7) Less: Maintenance Capital Expenditures (25.0) (25.6) (26.1) (26.7) (27.3) (27.9) (28.6) Distributable Cash Flow $117.2 $149.3 $153.8 $123.4 $118.3 $120.8 $117.1 Sisecam Wyoming Distributed Cash Flow Distributions to SIRE (51.0%) $43.3 $60.9 $62.7 $57.2 $54.8 $56.0 $54.3 Distributions to NRP (49.0%) 41.6 58.5 60.3 55.0 52.7 53.8 52.2 Distributed Cash Flow $84.9 $119.5 $123.0 $112.2 $107.5 $109.9 $106.5 Distributable Cash Flow Surplus / (Shortfall) $32.3 $29.9 $30.8 $11.2 $10.8 $11.0 $10.6 Sisecam Wyoming Coverage Ratio 1.38x 1.25x 1.25x 1.10x 1.10x 1.10x 1.10x Sisecam Wyoming Cash Flow Summary – Sensitivity Case For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E 2028E Sisecam Wyoming Distributable Cash Flow SIRE Financial Projections, SIRE management 26 ($ in millions)

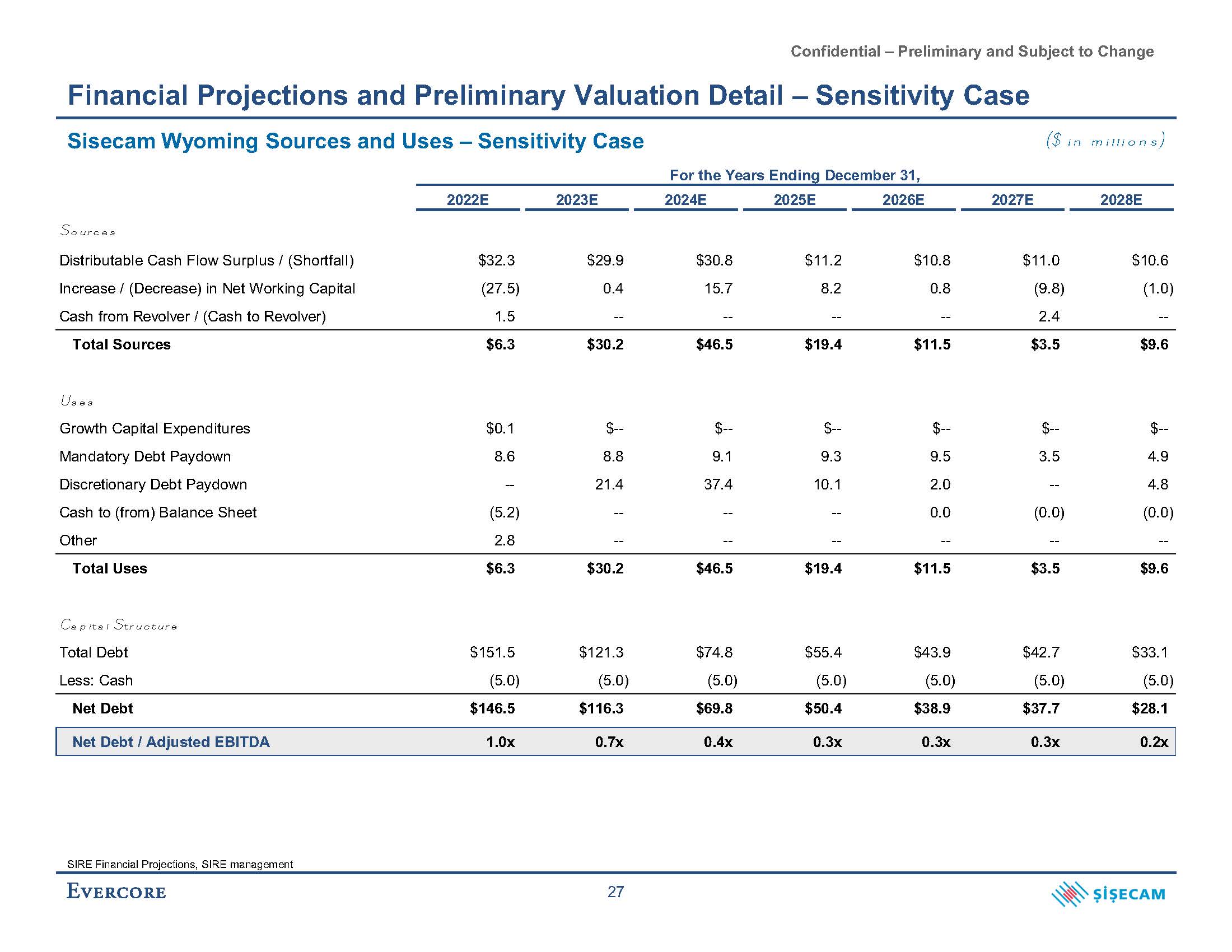

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case Sisecam Wyoming Sources and Uses – Sensitivity Case 2022E 2023E For the Years Ending December 31, 2024E 2025E 2026E 2027E 20 Sources Distributable Cash Flow Surplus / (Shortfall) $32.3 $29.9 $30.8 $11.2 $10.8 Increase / (Decrease) in Net Working Capital (27.5) 0.4 15.7 8.2 0. Cash from Revolver / (Cash to Revolver) 1.5 -- -- -- Total Sources $6.3 $30.2 $46.5 $19.4 Uses Growth Capital Expenditures $0.1 $-- Mandatory Debt Paydown Discretionary Debt Paydown Cash to (from) Balance Sheet Other 8.6 -- (5.2) 8.8 Total Uses Capital Structure Total Debt Less: Cash Net Debt N ($ in millions) SIRE Financial Projections, SIRE management 27

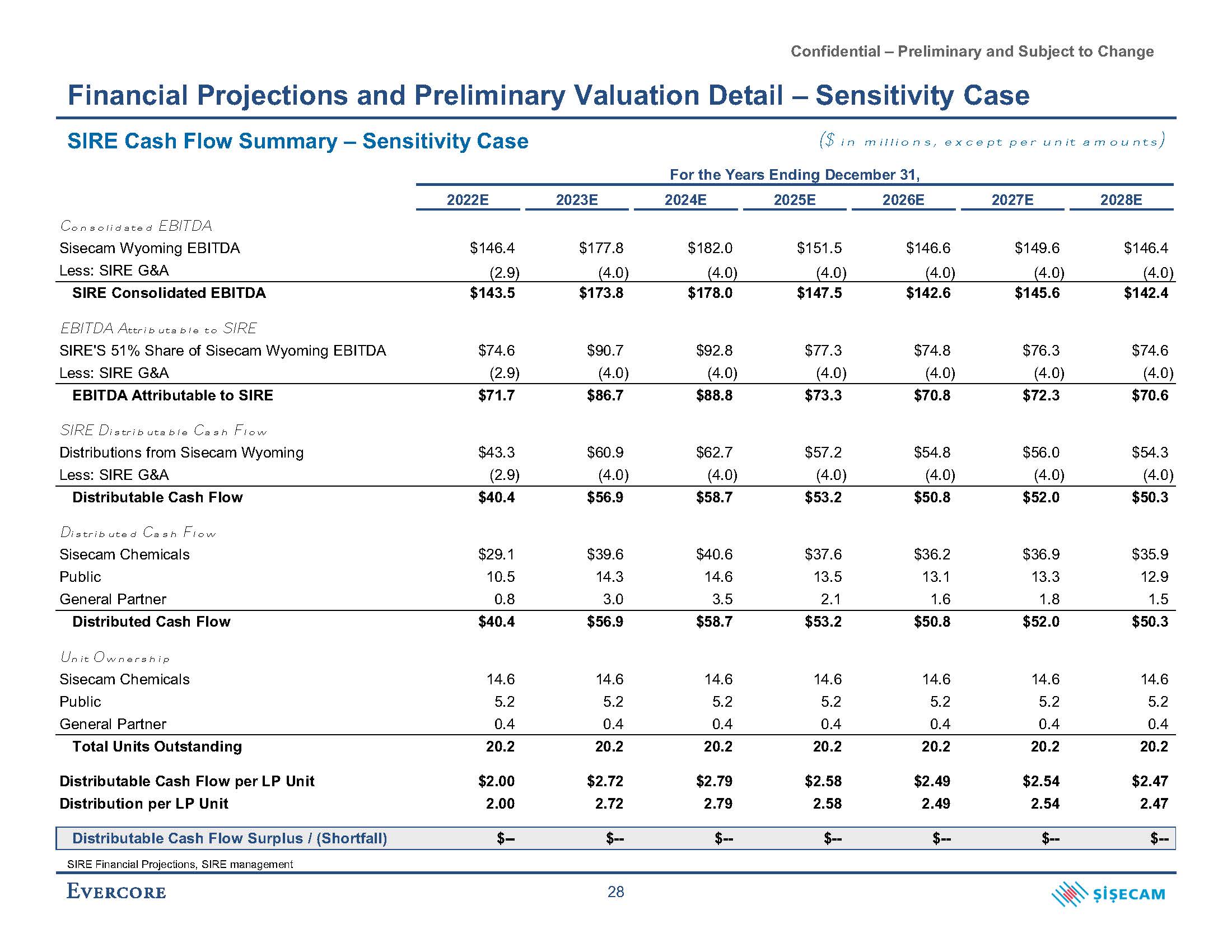

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case SIRE Financial Projections, SIRE management 28 SIRE Cash Flow Summary – Sensitivity Case 2022E 2023E 2024E 2025E 2026E 2027E 2028E Consolidated EBITDA Sisecam Wyoming EBITDA $146.4 $177.8 $182.0 $151.5 $146.6 $149.6 $146.4 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) SIRE Consolidated EBITDA $143.5 $173.8 $178.0 $147.5 $142.6 $145.6 $142.4 EBITDA Attributable to SIRE SIRE'S 51% Share of Sisecam Wyoming EBITDA $74.6 $90.7 $92.8 $77.3 $74.8 $76.3 $74.6 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) EBITDA Attributable to SIRE $71.7 $86.7 $88.8 $73.3 $70.8 $72.3 $70.6 SIRE Distributable Cash Flow Distributions from Sisecam Wyoming $43.3 $60.9 $62.7 $57.2 $54.8 $56.0 $54.3 Less: SIRE G&A (2.9) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) Distributable Cash Flow $40.4 $56.9 $58.7 $53.2 $50.8 $52.0 $50.3 Distributed Cash Flow Sisecam Chemicals $29.1 $39.6 $40.6 $37.6 $36.2 $36.9 $35.9 Public 10.5 14.3 14.6 13.5 13.1 13.3 12.9 General Partner 0.8 3.0 3.5 2.1 1.6 1.8 1.5 Distributed Cash Flow $40.4 $56.9 $58.7 $53.2 $50.8 $52.0 $50.3 Unit Ownership Sisecam Chemicals 14.6 14.6 14.6 14.6 14.6 14.6 14.6 Public 5.2 5.2 5.2 5.2 5.2 5.2 5.2 General Partner 0.4 0.4 0.4 0.4 0.4 0.4 0.4 Total Units Outstanding 20.2 20.2 20.2 20.2 20.2 20.2 20.2 Distributable Cash Flow per LP Unit $2.00 $2.72 $2.79 $2.58 $2.49 $2.54 $2.47 Distribution per LP Unit 2.00 2.72 2.79 2.58 2.49 2.54 2.47 Distributable Cash Flow Surplus / (Shortfall) $-- $-- $-- $-- $-- $-- $-- ($ in millions, except per unit amounts) For the Years Ending December 31,

Confidential – Preliminary and Subject to Change 4.25x 5.50x 6.75x 8.00x 9.25x --% 0.5% 1.0% 1.5% 2.0% 8.00% $20.42 $23.36 $26.11 $28.87 $31.62 8.00% $24.44 $25.39 $26.47 $27.72 $29.19 8.50% 19.86 22.72 25.53 28.21 30.89 8.50% 23.08 23.96 24.90 25.96 27.18 9.00% 19.33 22.11 24.89 27.58 30.19 9.00% 21.82 22.58 23.43 24.40 25.46 9.50% 18.82 21.54 24.24 26.94 29.50 9.50% 20.69 21.35 22.09 22.92 23.87 10.00% 18.33 20.98 23.61 26.23 28.83 10.00% 19.67 20.25 20.90 21.62 22.43 Sisecam Wyoming EBITDA $177.8 $182.0 $151.5 $146.6 $149.6 $146.4 $70.61 $146.4 Less: Tax Depreciation and Amortization2 (588.3) (21.7) (39.8) (53.8) (63.2) (67.7) (28.6) EBIT ($410.5) $160.3 $111.8 $92.8 $86.4 $78.7 $117.8 Less: Cash Taxes3 -- (9.5) (6.6) (6.9) (6.4) (10.8) (43.6) EBIAT ($410.5) $150.8 $105.2 $86.0 $80.0 $67.8 $74.2 Plus: Tax Depreciation and Amortization 588.3 21.7 39.8 53.8 63.2 67.7 28.6 Less: Capital Expenditures (25.6) (26.1) (26.7) (27.3) (27.9) (28.6) (28.6) Less: Changes in NWC 0.4 15.7 8.2 0.8 (9.8) (1.0) - Sisecam Wyoming Unlevered Free Cash Flow $152.6 $162.1 $126.4 $113.2 $105.4 $106.0 $74.2 SIRE Interest in Sisecam Wyoming 51.0% 51.0% 51.0% 51.0% 51.0% 51.0% 51.0% SIRE Share of Sisecam Wyoming Unlevered Free Cash Flow $77.8 $82.7 $64.5 $57.7 $53.8 $54.0 $37.8 Less: SIRE G&A (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) (4.0) SIRE Unlevered Free Cash Flow $73.8 $78.7 $60.5 $53.7 $49.8 $50.0 $33.8 EBITDA Multiple / Perpetuity Growth Rate 6.75x 1.0% Implied Terminal Value $476.8 − $427.3 Present Value of Terminal Value @ 9.00% Discount Rate Plus: Present Value of Unlevered Free Cash Flow @ 9.00% Discount Rate 284.3 − 254.8 293.2 Implied Enterprise Value $577.5 − $548.0 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (74.7) Implied Equity Value $502.8 − $473.3 SIRE LP Units Outstanding4 20.2 Implied SIRE LP Unit Value $24.89 − $23.43 Terminal Exit Multiple Perpetuity Growth Rate WACC WACC For the Years Ending December 31, Exit Perpetuity 2023E 2024E 2025E 2026E 2027E 2028E Multiple Growth Financial Projections and Preliminary Valuation Detail – Sensitivity Case Unit Price Sensitivity Analysis Source: SIRE Financial Projections, SIRE management 51% of Sisecam Wyoming EBITDA less $4.0 million SIRE G&A 2022E tax DD&A assumes 100.0% bonus depreciation calculated as the midpoint of the enterprise value range plus 2022E capital expenditures; 2023E and 2024E tax DD&A assumes 100.0% bonus depreciation on capital expenditures; bonus depreciation phase-down on growth capital expenditures in 2025E (80.0%) and 2026E (60.0%) Assumes unitholder tax rate of 29.6% from 2023E to 2025E and 37.0% thereafter 4. Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution 29 Discounted Cash Flow Analysis – Sensitivity Case ($ in millions, except per unit amounts)

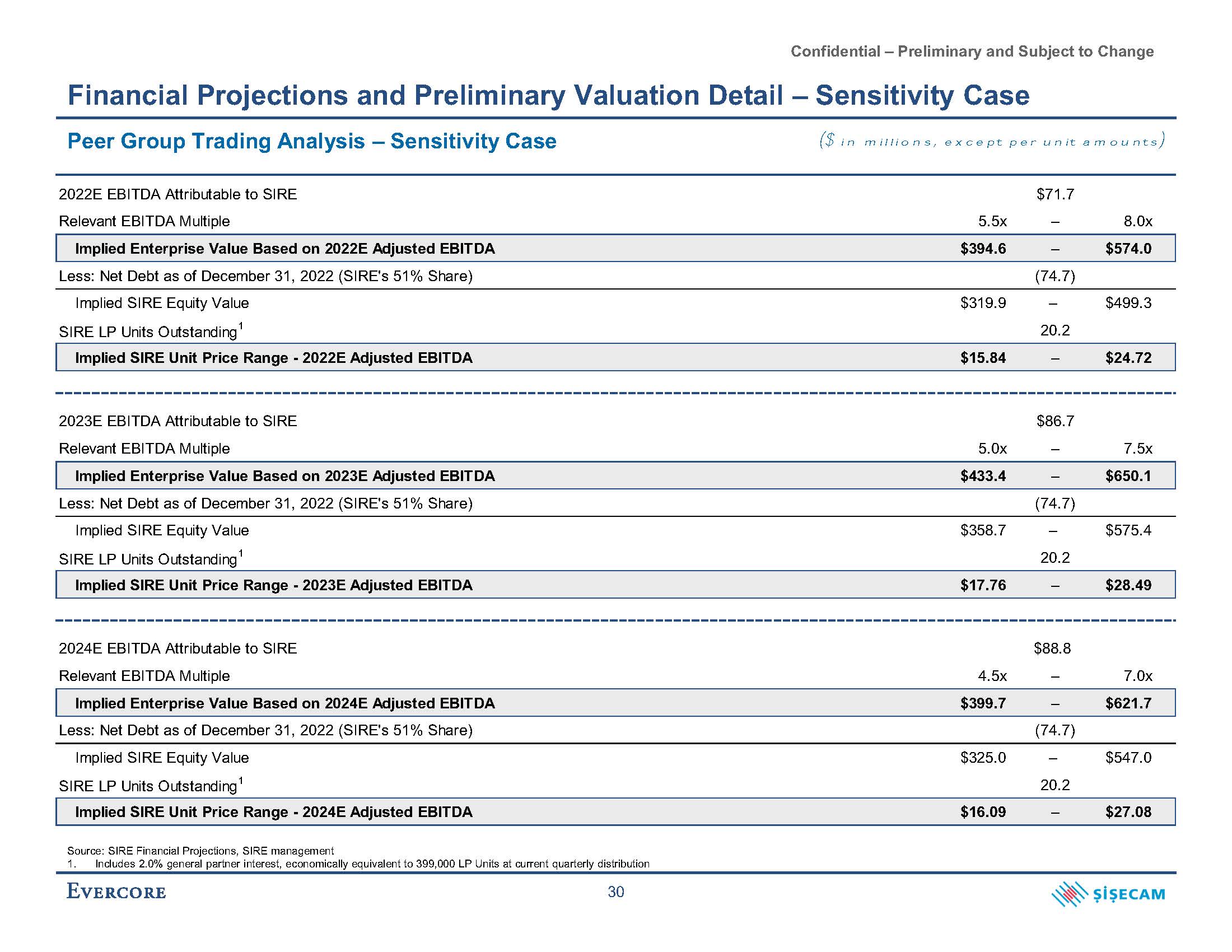

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case Peer Group Trading Analysis – Sensitivity Case 2022E EBITDA Attributable to SIRE Relevant EBITDA Multiple 5.5x $71.7 – 8.0x Implied Enterprise Value Based on 2022E Adjusted EBITDA $394.6 – $574.0 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (74.7) Implied SIRE Equity Value SIRE LP Units Outstanding1 $319.9 – 20.2 $499.3 Implied SIRE Unit Price Range - 2022E Adjusted EBITDA $15.84 – $24.72 2023E EBITDA Attributable to SIRE Relevant EBITDA Multiple 5.0x $86.7 – 7.5x Implied Enterprise Value Based on 2023E Adjusted EBITDA $433.4 – $650.1 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (74.7) Implied SIRE Equity Value SIRE LP Units Outstanding1 $358.7 – 20.2 $575.4 Implied SIRE Unit Price Range - 2023E Adjusted EBITDA $17.76 – $28.49 2024E EBITDA Attributable to SIRE Relevant EBITDA Multiple 4.5x $88.8 – 7.0x Implied Enterprise Value Based on 2024E Adjusted EBITDA $399.7 – $621.7 Less: Net Debt as of December 31, 2022 (SIRE's 51% Share) (74.7) Implied SIRE Equity Value SIRE LP Units Outstanding1 $325.0 – 20.2 $547.0 Implied SIRE Unit Price Range - 2024E Adjusted EBITDA $16.09 – $27.08 ($ in millions, except per unit amounts) Source: SIRE Financial Projections, SIRE management 1. Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution 30

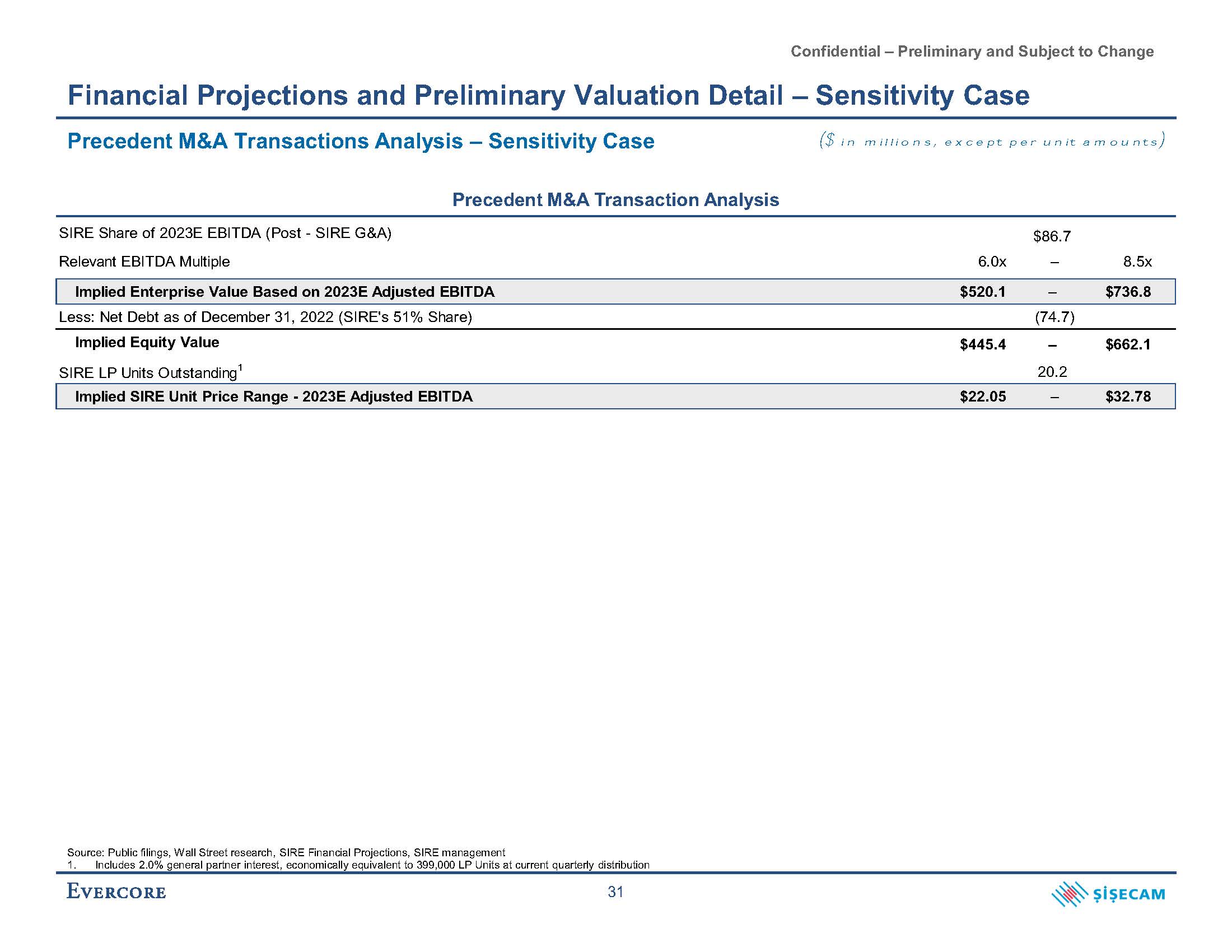

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case Precedent M&A Transactions Analysis – Sensitivity Case Precedent M&A Transaction Analysis Source: Public filings, Wall Street research, SIRE Financial Projections, SIRE management 1. Includes 2.0% general partner interest, economically equivalent to 399,000 LP Units at current quarterly distribution 31 ($ in millions, except per unit amounts)

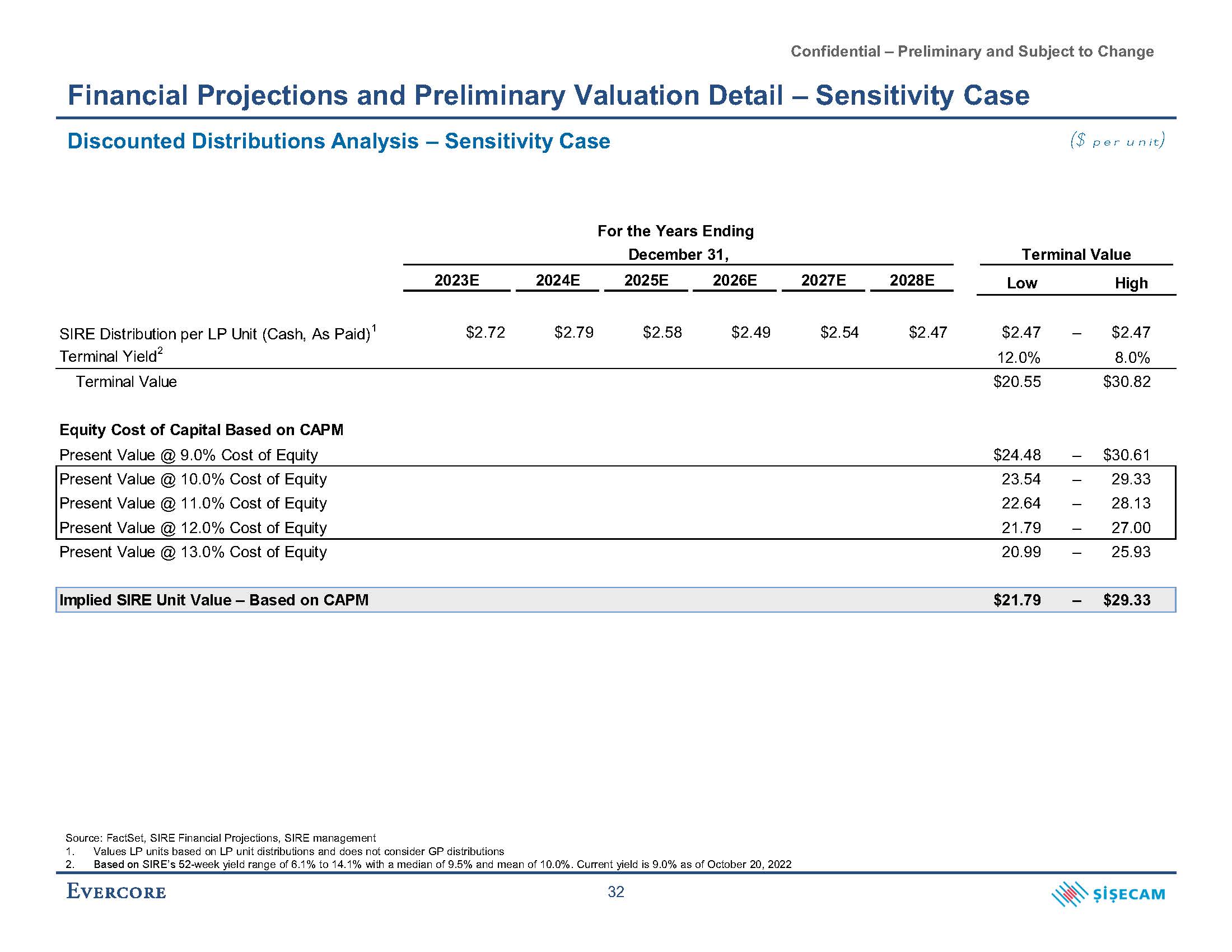

Confidential – Preliminary and Subject to Change Financial Projections and Preliminary Valuation Detail – Sensitivity Case Discounted Distributions Analysis – Sensitivity Case ($ per unit) SIRE Distribution per LP Unit (Cash, As Paid)1 $2.72 $2.79 $2.58 $2.49 $2.54 $2.47 $2.47 – $2.47 Terminal Yield2 12.0% 8.0% Terminal Value $20.55 $30.82 Equity Cost of Capital Based on CAPM Present Value @ 9.0% Cost of Equity $24.48 – $30.61 Present Value @ 10.0% Cost of Equity 23.54 – 29.33 Present Value @ 11.0% Cost of Equity 22.64 – 28.13 Present Value @ 12.0% Cost of Equity 21.79 – 27.00 Present Value @ 13.0% Cost of Equity 20.99 – 25.93 Implied SIRE Unit Value – Based on CAPM $21.79 – $29.33 For the Years Ending December 31, 2023E 2024E 2025E 2026E 2027E 2028E Terminal Value Low High Source: FactSet, SIRE Financial Projections, SIRE management 1. Values LP units based on LP unit distributions and does not consider GP distributions 2. Based on SIRE’s 52-week yield range of 6.1% to 14.1% with a median of 9.5% and mean of 10.0%. Current yield is 9.0% as of October 20, 2022 32

Confidential – Preliminary and Subject to Change D. Supplemental Soda Ash Pricing Data

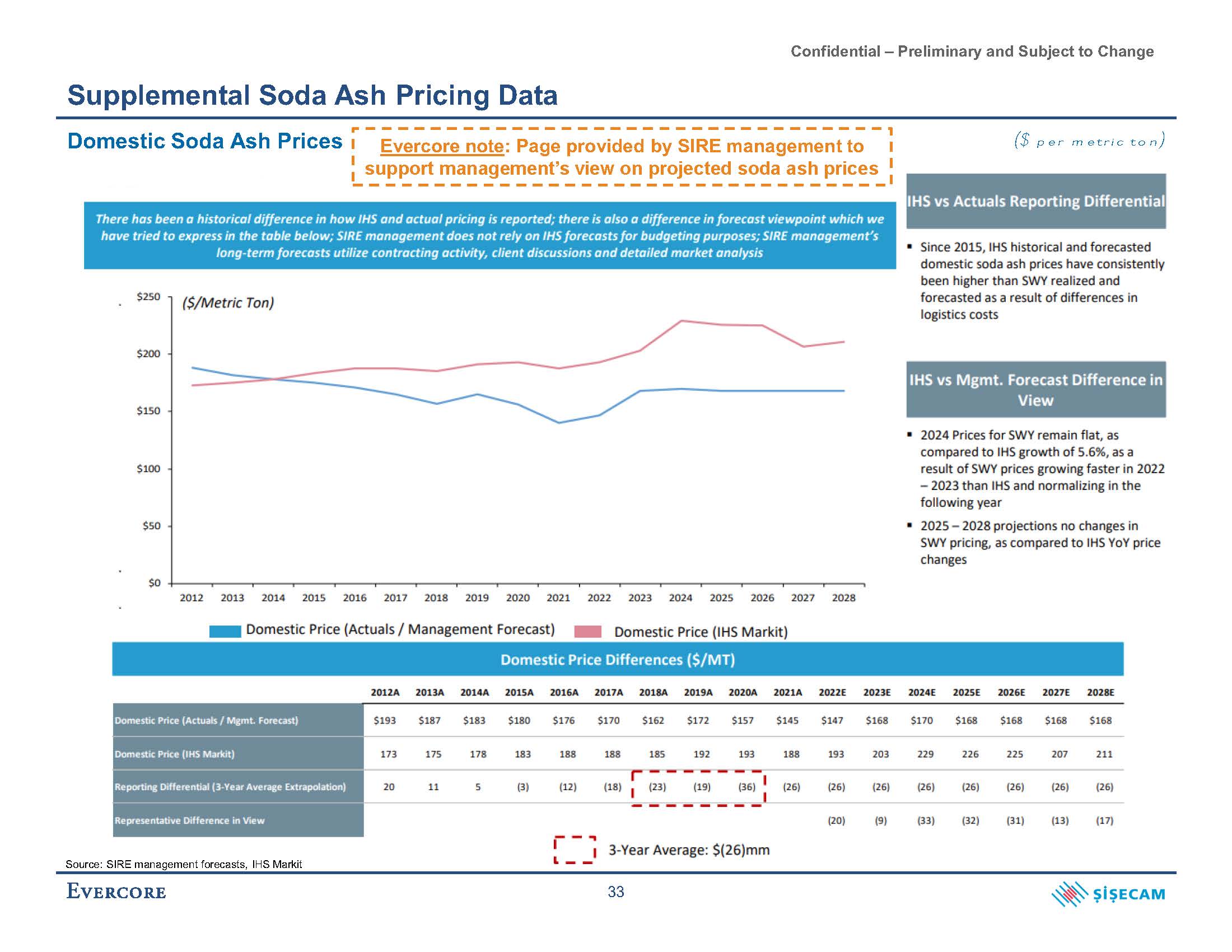

Confidential – Preliminary and Subject to Change Supplemental Soda Ash Pricing Data Source: SIRE management forecasts, IHS Markit 33 Domestic Soda Ash Prices ($ per metric ton) Evercore note: Page provided by SIRE management to support management’s view on projected soda ash prices

Confidential – Preliminary and Subject to Change Supplemental Soda Ash Pricing Data Export Soda Ash Prices ($ per metric ton) Evercore note: Page provided by SIRE management to support management’s view on projected soda ash prices Source: SIRE management forecasts, IHS Markit 34