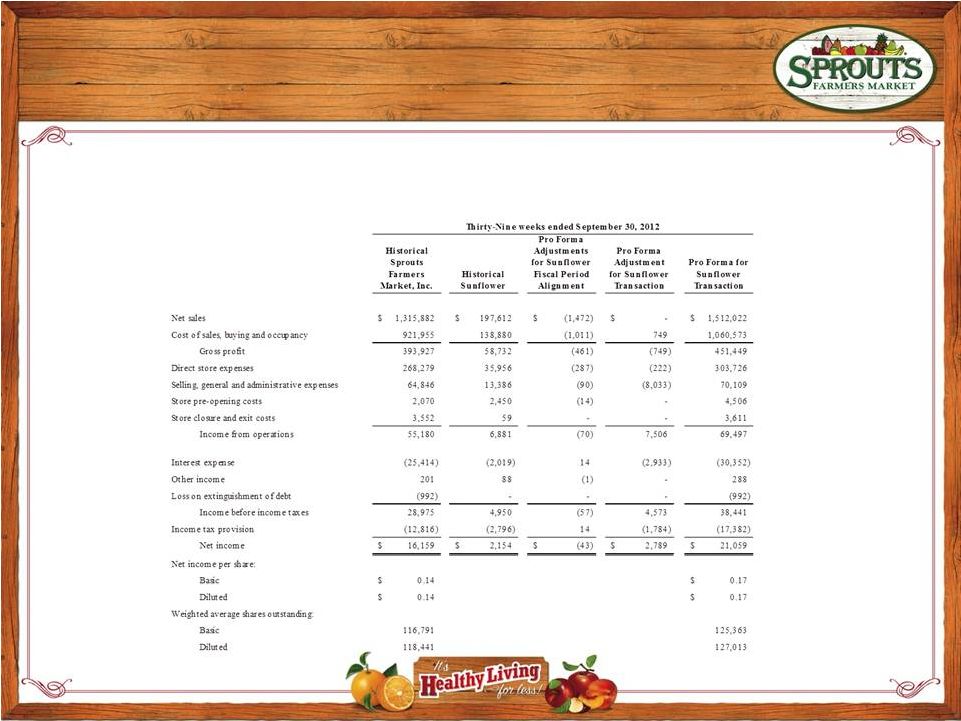

Forward-Looking Statements and Non- Forward-Looking Statements and Non- GAAP Financial Measures GAAP Financial Measures 1 Certain statements in this presentation are forward-looking as defined in the Private Securities Litigation Reform Act of 1995. Any statements contained herein (including, but not limited to, statements to the effect that Sprouts Farmers Market, Inc. (the “Company”)or its management "anticipates," "plans," "estimates," "expects," "believes," or the negative of these terms and other similar expressions) that are not statements of historical fact should be considered forward-looking statements. These statements involve certain risks and uncertainties that may cause actual results to differ materially from expectations as of the date of this presentation. These risks and uncertainties include, without limitation, risks associated with the Company’s ability to successfully compete in its intensely competitive industry; the Company’s ability to successfully open new stores; the Company’s ability to manage its rapid growth; the Company’s ability to maintain or improve its operating margins; the Company’s ability to identify and react to trends in consumer preferences; product supply disruptions; general economic conditions; and other factors as set forth from time to time in the Company’s Securities and Exchange Commission filings. The Company intends these forward- looking statements to speak only as of the date of this presentation and does not undertake to update or revise them as more information becomes available, except as required by law. In addition to reporting financial results in accordance with GAAP, the Company has presented adjusted net income, adjusted diluted earnings per share and adjusted EBITDA. These measures are not in accordance with, or an alternative to GAAP. The Company's management believes that these presentations provide useful information to management, analysts and investors regarding certain additional financial and business trends relating to its results of operations and financial condition. In addition, management uses these measures for reviewing the financial results of the Company as well as a component of incentive compensation. The Company defines adjusted net income as net income excluding store closure and exit costs, one-time costs associated with its April 2011 combination (the “Henry’s Transaction”) with Henry’s Holdings, LLC (“Henry’s”) and its May 2012 business combination with Sunflower Farmers Market, Inc. (the “Sunflower Transaction,” and together with the Henry’s Transaction, the “Transactions”), gain and losses from disposal of assets, the loss on extinguishment of debt and the related tax impact of those adjustments. The Company defines adjusted diluted earnings per share as adjusted net income divided by the weighted average diluted shares outstanding. The Company defines EBITDA as net income before interest expense, provision for income tax, and depreciation and amortization, and defines adjusted EBITDA as EBITDA excluding store closure and exit costs, one-time costs associated with the Transactions, gains and losses from disposal of assets and the loss on extinguishment of debt. These non-GAAP measures are intended to provide additional information only and do not have any standard meanings prescribed by GAAP. Use of these terms may differ from similar measures reported by other companies. Because of their limitations, none of these non-GAAP measures should be considered as a measure of discretionary cash available to use to reinvest in growth of the Company’s business, or as a measure of cash that will be available to meet the Company’s obligations. Each of these non-GAAP measures has its limitations as an analytical tool, and you should not consider them in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. See the Appendix for reconciliation for these non-GAAP measure to the comparable GAAP measures. In addition, in comparing its results to the comparable periods of 2012, the Company has presented 2012 financial results on a pro forma basis as if the Sunflower Transaction had occurred on the first day of the Company’s 2012 fiscal year. See the Appendix for unaudited supplemental pro forma condensed consolidated financial information. |