|

Exhibit 99.1

|

INVESTOR DECK March 2015

Forward-Looking Statements and Non-GAAP Financial Measures

Certain statements in this presentation are forward-looking as defined in the Private Securities Litigation Reform Act of 1995. Any statements contained herein (including, but not limited to, statements to the effect that Sprouts Farmers Market, Inc. (the “Company”) or its management “anticipates,” “plans,” “estimates,” “expects,” “believes,” or the negative of these terms and other similar expressions) that are not statements of historical fact should be considered forward-looking statements, including, without limitation, statements regarding the Company’s estimated growth, expected results and long-term financial targets. These statements involve certain risks and uncertainties that may cause actual results to differ materially from expectations as of the date of this presentation. These risks and uncertainties include, without limitation, risks associated with the Company’s ability to successfully compete in its intensely competitive industry; the Company’s ability to successfully open new stores; the Company’s ability to manage its rapid growth; the Company’s ability to maintain or improve its comparable store sales and operating margins; the Company’s ability to identify and react to trends in consumer preferences; product supply disruptions; general economic conditions; and other factors as set forth from time to time in the Company’s Securities and Exchange Commission filings. The Company intends these forward-looking statements to speak only as of the date of this presentation and does not undertake to update or revise them as more information becomes available, except as required by law.

In addition to reporting financial results in accordance with GAAP, the Company has presented adjusted net income, adjusted earnings per share and adjusted EBITDA. These measures are not in accordance with, or an alternative to GAAP. The Company’s management believes that these presentations provide useful information to management, analysts and investors regarding certain additional financial and business trends relating to its results of operations and financial condition. In addition, management uses these measures for reviewing the financial results of the Company as well as a component of incentive compensation. The Company defines adjusted net income as net income excluding store closure and exit costs, one-time costs associated with its April 2011 combination (the “Henry’s Transaction”) with Henry’s Holdings, LLC (“Henry’s”) and its May 2012 business combination with Sunflower Farmers Market, Inc. (“the Sunflower Transaction,” and collectively, the “Transactions”), gain and losses from disposal of assets, IPO bonus, expenses incurred by the Company in its secondary public offerings and employment taxes paid by the Company in connection with options exercised in those offerings (“Public Offering Expenses”), the loss on extinguishment of debt and the related tax impact of those adjustments. The Company defines adjusted basic and diluted earnings per share as adjusted net income divided by the weighted average basic and diluted shares outstanding. The Company defines EBITDA as net income before interest expense, provision for income tax, and depreciation, amortization and accretion, and defines adjusted EBITDA as EBITDA excluding store closure and exit costs, onetime costs associated with the Transactions, gains and losses from disposal of assets, Public Offering Expenses, and the loss on extinguishment of debt.

These non-GAAP measures are intended to provide additional information only and do not have any standard meanings prescribed by GAAP. Use of these terms may differ from similar measures reported by other companies. Because of their limitations, none of these non-GAAP measures should be considered as a measure of discretionary cash available to use to reinvest in growth of the Company’s business, or as a measure of cash that will be available to meet the Company’s obligations. Each of these non-GAAP measures has its limitations as an analytical tool, and you should not consider them in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. See the Appendix for reconciliation for these non-GAAP measures to the comparable GAAP measures.

OVERVIEW OF SPROUTS

Sprouts is Well Positioned to Meet the

Needs of Today’s Health Conscious Consumers

Healthy grocery store that offers fresh, natural and organic foods at great prices Broad consumer appeal One of the largest and fastest growing natural and organic retailers Industry leading results Significant white space opportunity and strong new store economics

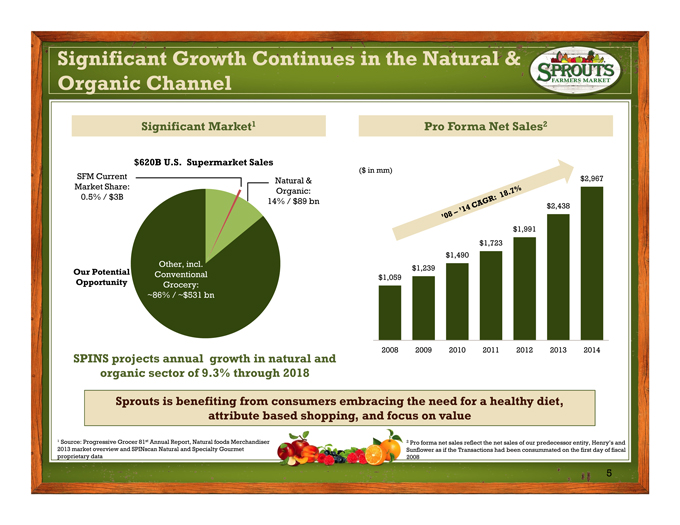

Significant Growth Continues in the Natural & Organic Channel

Significant Market1

$620B U.S. Supermarket Sales

SFM Current

Natural & Market Share: Organic: 0.5% / $3B

14% / $89 bn

Our Potential Other, incl.

Opportunity Conventional Grocery:

~86% / ~$531 bn

SPINS projects annual growth in natural and organic sector of 9.3% through 2018

Pro Forma Net Sales2

($ in mm) $2,967

$2,438

$1,991 $1,723 $1,490 $1,239 $1,059

2008 2009 2010 2011 2012 2013 2014

Sprouts is benefiting from consumers embracing the need for a healthy diet, attribute based shopping, and focus on value

¹ Source: Progressive Grocer 81st Annual Report, Natural foods Merchandiser 2013 market overview and SPINscan Natural and Specialty Gourmet proprietary data

2 Pro forma net sales reflect the net sales of our predecessor entity, Henry’s and Sunflower as if the Transactions had been consummated on the first day of fiscal 2008

Sprouts is Changing the Way People Perceive And Shop for Fresh, Natural and Organic Foods

HEALTH

Sprouts has evolved from a Specialty Food Store into a Healthy Grocery Store

Continue to benefit from consumer’s growing interest in eating healthier

SELECTION

Full-line healthy grocery store with more than 17,000 fresh, natural & organic products Full selection of unique specialty items: 2400+ organic 2700+ gluten-free 2000+ non-GMO

VALUE

Produce prices significantly below competitors

Highly promotional -communicate our competitive prices week in and week out

Promote value across the store

SERVICE

Convenient,

Friendly and easy-to-shop

Trusted, knowledgeable and engaging customer service focused on educating customers

Sprouts—A Healthy Grocery Store

Produce surrounded by a complete grocery offering Differentiated assortment of high-quality, healthy foods

High standard private label Fresh, natural & organic offering Don’t sell most national branded packaged goods

Farmers market inspired, open store layout with low profile displays Convenient, small-box: average 28k sq. ft. Comfortable, easy to shop environment

Reaching a Broad Base of Consumers Throughhrough Both Traditional and Digital Mediums

Broad Customer Demographics

Middle income and up Medium to above average education Wide spectrum of demographics & ethnic makeups Wanting to eat healthier Looking for value

Brand Awareness & Recognition

Strong marketing and pre-opening programs reaching customers through a variety of channels

More than 14 million weekly circulars 30+ annual promotions1 Digital & social platforms

Increasing word-of-mouth and grass-root efforts driving traffic Over 1 million Facebook fans

¹ Represents planned promotions at each store during FY 2014.

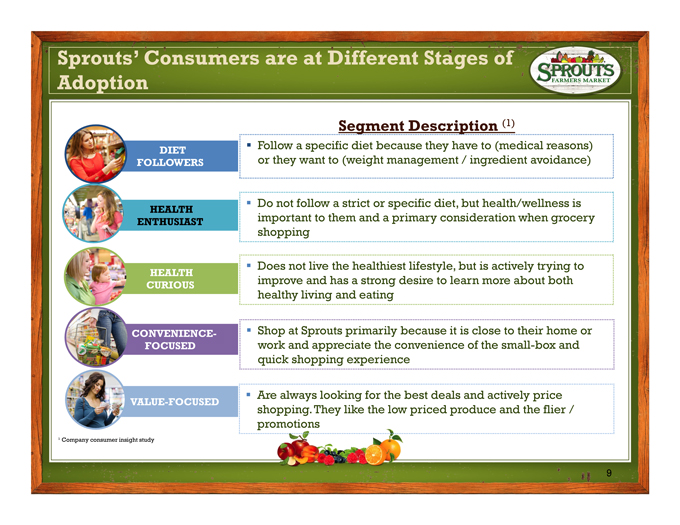

Sprouts’ Consumers are at Different Stages of Adoption

DIET FOLLOWERS

HEALTH ENTHUSIAST

HEALTH CURIOUS

CONVENIENCE-FOCUSED

VALUE-FOCUSED

¹ Company consumer insight study

Segment Description (1)

Follow a specific diet because they have to (medical reasons) or they want to (weight management / ingredient avoidance)

Do not follow a strict or specific diet, but health/wellness is important to them and a primary consideration when grocery shopping

Does not live the healthiest lifestyle, but is actively trying to improve and has a strong desire to learn more about both healthy living and eating

Shop at Sprouts primarily because it is close to their home or work and appreciate the convenience of the small-box and quick shopping experience

Are always looking for the best deals and actively price shopping. They like the low priced produce and the flier / promotions

9

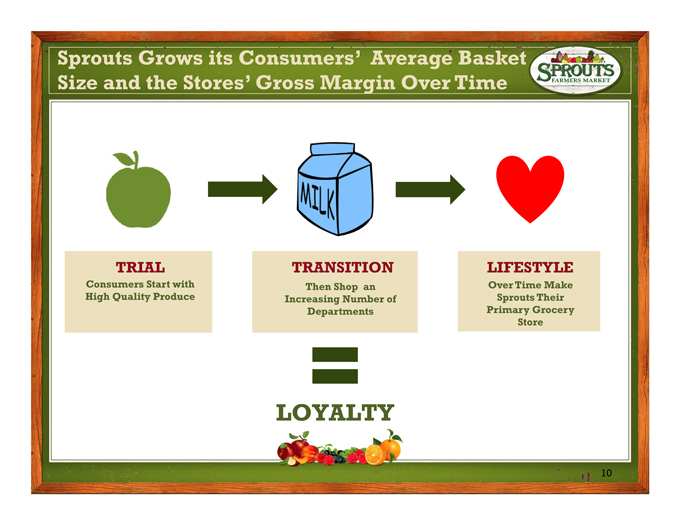

Sprouts Grows its Consumers’ Average Basket Size and the Stores’ Gross Margin Over Time

TRIAL TRANSITION LIFESTYLE

Consumers Start with Then Shop an Over Time Make High Quality Produce Increasing Number of Sprouts Their Departments Primary Grocery Store

LOYALTY

10

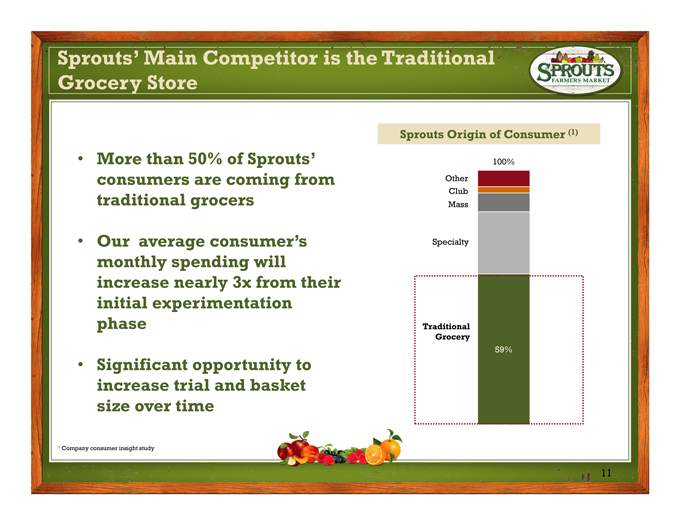

Sprouts’ Main Competitor is the Traditional Grocery Store

More than 50% of Sprouts’ consumers are coming from traditional grocers

Our average consumer’s monthly spending will increase nearly 3x from their initial experimentation phase

Significant opportunity to increase trial and basket size over time

¹ Company consumer insight study

Sprouts Origin of Consumer (1)

100% Other Club Mass

Specialty

Traditional Grocery

59%

11

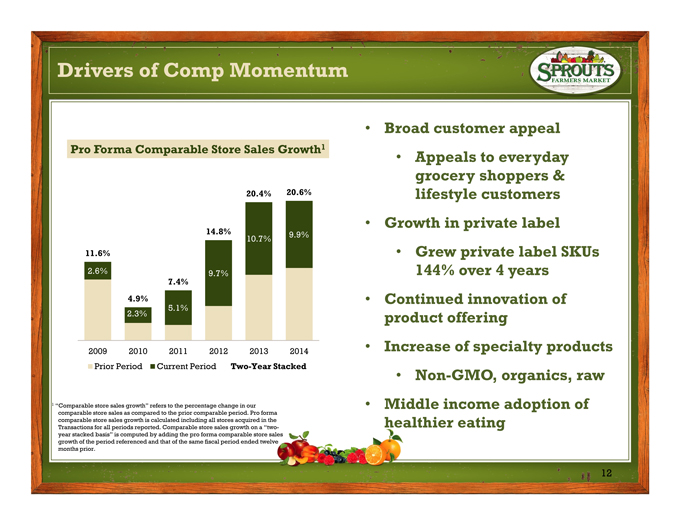

Drivers of Comp Momentum

Pro Forma Comparable Store Sales Growth1

20.4% 20.6%

14.8% 9.9%

10.7%

11.6%

2.6% 9.7%

7.4% 4.9%

5.1% 2.3%

2009 2010 2011 2012 2013 2014 Prior Period Current Period Two-Year Stacked

1 “Comparable store sales growth” refers to the percentage change in our comparable store sales as compared to the prior comparable period. Pro forma comparable store sales growth is calculated including all stores acquired in the Transactions for all periods reported. Comparable store sales growth on a “two-year stacked basis” is computed by adding the pro forma comparable store sales growth of the period referenced and that of the same fiscal period ended twelve months prior.

Broad customer appeal

Appeals to everyday grocery shoppers & lifestyle customers

Growth in private label

Grew private label SKUs 144% over 4 years

Continued innovation of product offering Increase of specialty products

Non-GMO, organics, raw

Middle income adoption of healthier eating

12

Estimated 15+ Years of New Store Growth

Proven Concept: 198 stores in twelve states as of February 25, 2015

Sprouts’ footprint and near-term expansion covers high growth areas, providing opportunity to serve Boomers, Gen-X as well as the rising Millennial demographic Demographics allow for deep penetration in markets Model works well in densely populated, urban areas as well as smaller metropolitan markets

Successful in

“natural/lifestyle” markets and more “traditional” markets Balanced unit growth with 70% coming from existing markets 14% unit growth for the near-term 1200 potential store count (1)

¹ Based on an assumed new store growth rate of 14% per year and research conducted by Buxton Company in 2012.

Note: Store count as of February 25, 2015

Nevada

5 Utah

Colorado

5 Kansas 1

81 25 2

Missouri

California North Arizona New Oklahoma Tennessee Carolina Arkansas Mexico

28 6

South

6 Georgia

1 Carolina Texas 5 33 Louisiana Alabama Mississippi Florida

Existing Market

Mid-Term Expansion Market Coming Soon

13

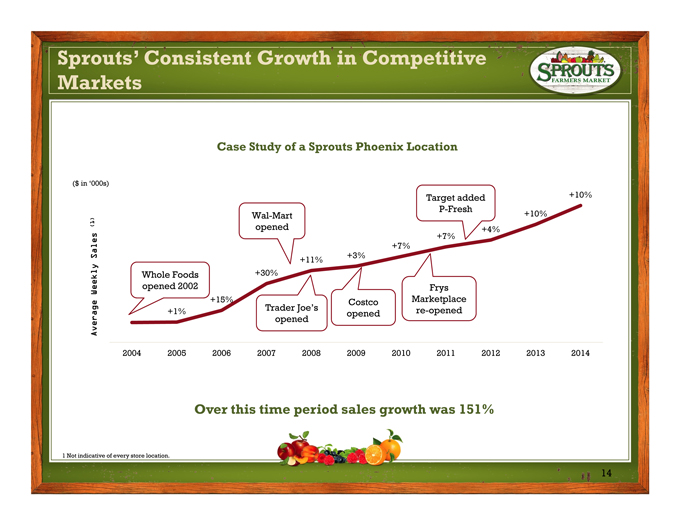

Sprouts’ Consistent Growth in Competitive Markets

Case Study of a Sprouts Phoenix Location

($ in ‘000s)

Target added +10% P-Fresh Wal-Mart +10% (1) opened

+4% +7% +7%

Sales +3%

+11%

Whole Foods +30%

Weekly opened 2002 Frys +15% Costco Marketplace +1% Trader Joe’s re-opened opened

Average opened

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Over this time period sales growth was 151%

1 | | Not indicative of every store location. |

14

Growing Responsibly

Responsible retailing for Sprouts is comprised of four main focus areas:

RESPONSIBLE OPERATIONS • RESPONSIBLE CONSTRUCTION RESPONSIBLE CITIZEN • RESPONSIBLE SOURCING

RESPONSIBLE OPERATIONS

Food Rescue Program – Donated approximately 8 million lbs of safe food in 2014

Cardboard, pallet and plastic recycling at all stores

Piloting composting at 46 stores

Launched “Green Sproutie” program

RESPONSIBLE CONSTRUCTION

LED lighting and retrofits in 2014

LEED equivalent in all new stores

Launched EMC motor/night curtains/anti-sweat control

Transcritical CO2 refrigeration pilot in GA

Energy retro commissioning

RESPONSIBLE CITIZEN $2M Donated to non almost -profits and in scholarships

Established Charitable Sprouts Foundation

Created 3000 jobs more in 2014 than wellness • Building programs health & for team members

Promoted more than 20% of our team members in 2014

RESPONSIBLE SOURCING

Received Leaping Bunny certifications

Working with vendors on Non-GMO Project certification

Developing produce traceability & tracking requirements and Animal Welfare standards

Developing private label sustainability requirements

15

BUSINESS & FINANCIAL PERFORMANCE

16

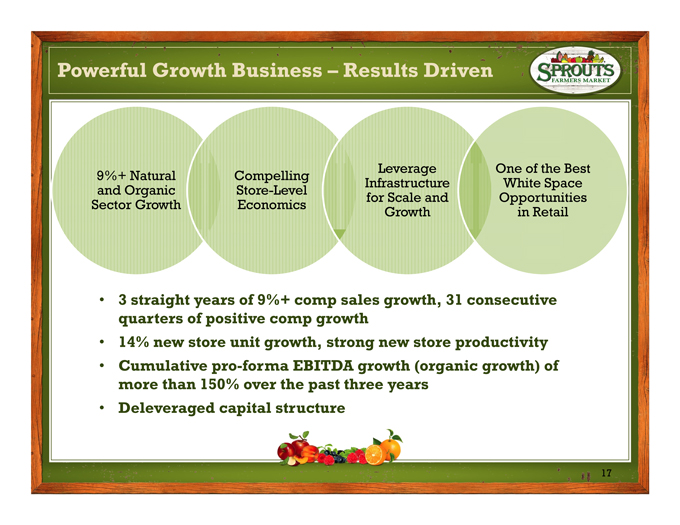

Powerful Growth Business – Results esults Driven

Leverage One of the Best 9%+ Natural Compelling Infrastructure White Space and Organic Store-Level for Scale and Opportunities Sector Growth Economics Growth in Retail

3 straight years of 9%+ comp sales growth, 31 consecutive quarters of positive comp growth 14% new store unit growth, strong new store productivity Cumulative pro-forma EBITDA growth (organic growth) of more than 150% over the past three years Deleveraged capital structure

17

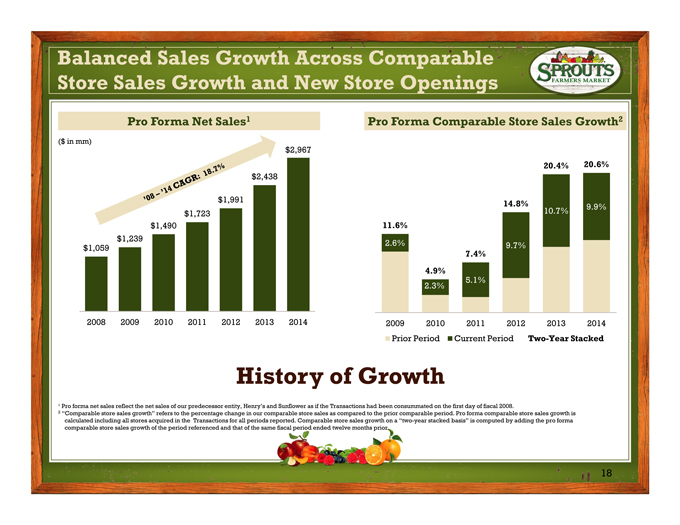

Balanced Sales Growth Across Comparable Store Sales Growth and New Store Openings

Pro Forma Net Sales1

($ in mm) $2,967

$2,438

$1,991 $1,723 $1,490 $1,239 $1,059

2008 2009 2010 2011 2012 2013 2014

’08-’14 CAGR: 18.7%Pro Forma Comparable Store Sales Growth2

20.4% 20.6%

14.8% 9.9%

10.7%

11.6%

2.6% 9.7%

7.4% 4.9%

5.1% 2.3%

2009 2010 2011 2012 2013 2014 Prior Period Current Period Two-Year Stacked

History of Growth

¹ Pro forma net sales reflect the net sales of our predecessor entity, Henry’s and Sunflower as if the Transactions had been consummated on the first day of fiscal 2008.

2 “Comparable store sales growth” refers to the percentage change in our comparable store sales as compared to the prior comparable period. Pro forma comparable store sales growth is calculated including all stores acquired in the Transactions for all periods reported. Comparable store sales growth on a “two-year stacked basis” is computed by adding the pro forma comparable store sales growth of the period referenced and that of the same fiscal period ended twelve months prior.

18

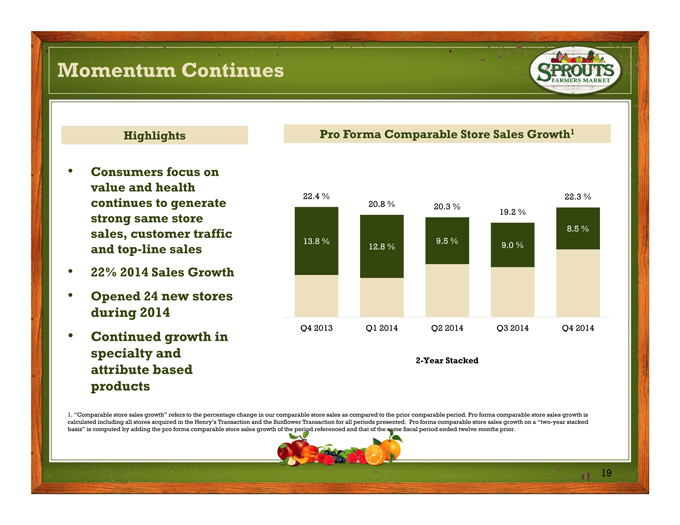

Momentum Continues

Highlights

Consumers focus on value and health continues to generate strong same store sales, customer traffic and top-line sales 22% 2014 Sales Growth Opened 24 new stores during 2014 Continued growth in specialty and attribute based products

Pro Forma Comparable Store Sales Growth1

22.4 % 20.8 % 22.3 %

20.3 %

19.2 %

85 . %

13.8 % 9.5 %

12.8 % 9.0 %

Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

2-Year Stacked

1. “Comparable store sales growth” refers to the percentage change in our comparable store sales as compared to the prior comparable period. Pro forma comparable store sales growth is calculated including all stores acquired in the Henry’s Transaction and the Sunflower Transaction for all periods presented. Pro forma comparable store sales growth on a “two-year stacked basis” is computed by adding the pro forma comparable store sales growth of the period referenced and that of the same fiscal period ended twelve months prior.

19

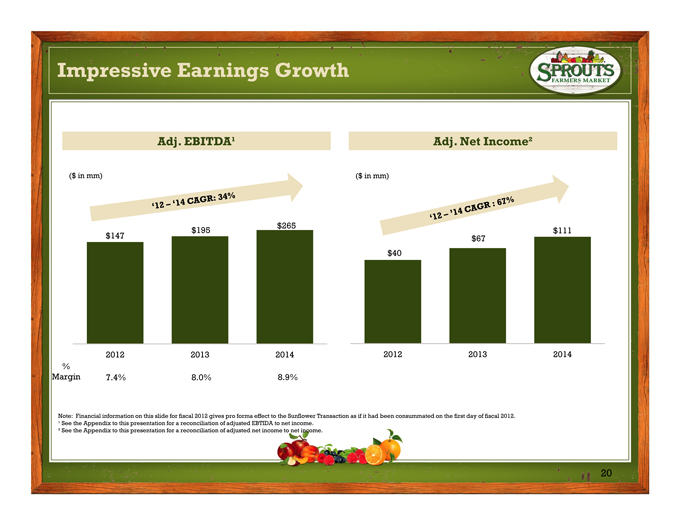

Impressive Earnings Growth

Adj. EBITDA¹

($ in mm)

$265 $195 $147

2012 2013 2014 % Margin 7.4% 8.0% 8.9%

’12 – ’14 CAGR: 34%

Adj. Net Income²

($ in mm)

$67 $111 $40

2012 2013 2014

’12 – ’14 CAGR:67%

Note: Financial information on this slide for fiscal 2012 gives pro forma effect to the Sunflower Transaction as if it had been consummated on the first day of fiscal 2012.

¹ See the Appendix to this presentation for a reconciliation of adjusted EBTIDA to net income.

² See the Appendix to this presentation for a reconciliation of adjusted net income to net income.

20

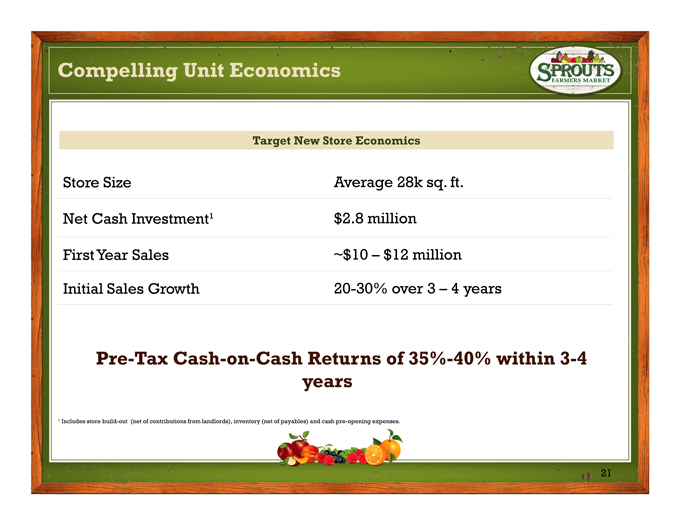

Compelling Unit Economics

Target New Store Economics

Store Size Average 28k sq. ft. Net Cash Investment¹ $2.8 million First Year Sales ~$10 – $12 million Initial Sales Growth 20-30% over 3 – 4 years

Pre-Tax Cash-on-Cash Returns of 35%-40% within 3-4 years

¹ Includes store build-out (net of contributions from landlords), inventory (net of payables) and cash pre-opening expenses.

21

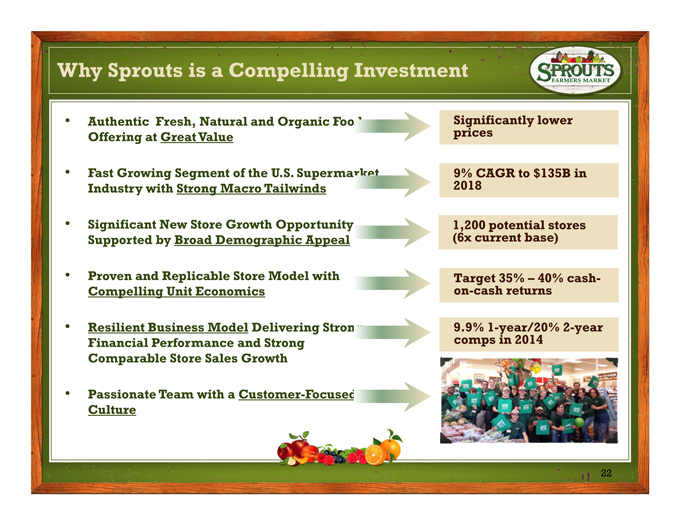

Why Sprouts is a Compelling Investment

Authentic Fresh, Natural and Organic Food Offering at Great Value

Fast Growing Segment of the U.S. Superm Industry with Strong Macro Tailwinds

Significant New Store Growth Opportunity Supported by Broad Demographic Appeal

Proven and Replicable Store Model with Compelling Unit Economics

Resilient Business Model Delivering Strong Financial Performance and Strong Comparable Store Sales Growth

Passionate Team with a Customer-Focused Culture

prices Significantly lower 2018 9% CAGR to $135B in 1,200 (6x current potential base) stores Target on-cash 35% returns – 40% cash-9.9% comps 1- year/20% in 2014 2-year

22

APPENDIX: SUPPLEMENTAL MATERIALS

23

Appendix

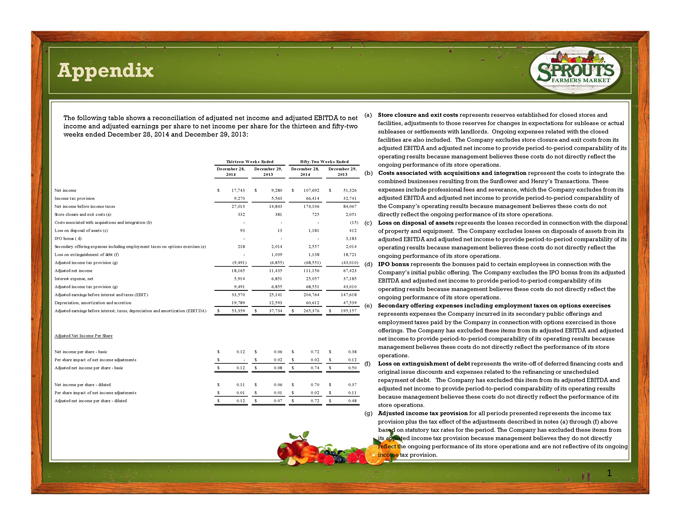

The following table shows a reconciliation of adjusted net income and adjusted EBITDA to net income and adjusted earnings per share to net income per share for the thirteen and fifty-two weeks ended December 28, 2014 and December 29, 2013:

Thirteen Weeks Ended Fifty-Two Weeks Ended

December 28, December 29, December 28, December 29,

2014 2013 2014 2013

Net income $ 17,743 $ 9,280 $ 107,692 $ 51,326

Income tax provision 9,270 5,563 66,414 32,741

Net income before income taxes 27,013 14,843 174,106 84,067

Store closure and exit costs (a) 332 381 725 2,051

Costs associated with acquisitions and integration (b) - - - (15)

Loss on disposal of assets (c) 93 13 1,181 412

IPO bonus ( d) - - - 3,183

Secondary offering expenses including employment taxes on options exercises (e) 218 2,014 2,557 2,014

Loss on extinguishment of debt (f) - 1,039 1,138 18,721

Adjusted income tax provision (g) (9,491) (6,855) (68,551) (43,010)

Adjusted net income 18,165 11,435 111,156 67,423

Interest expense, net 5,914 6,851 25,057 37,185

Adjusted income tax provision (g) 9,491 6,855 68,551 43,010

Adjusted earnings before interest and taxes (EBIT ) 33,570 25,141 204,764 147,618

Depreciation, amortization and accretion 19,789 12,593 60,612 47,539

Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) $ 53,359 $ 37,734 $ 265,376 $ 195,157

Adjusted Net Income Per Share

Net income per share - basic $ 0.12 $ 0.06 $ 0.72 $ 0.38

Per share impact of net income adjustments $ - $ 0.02 $ 0.02 $ 0.12

Adjusted net income per share - basic $ 0.12 $ 0.08 $ 0.74 $ 0.50

Net income per share - diluted $ 0.11 $ 0.06 $ 0.70 $ 0.37

Per share impact of net income adjustments $ 0.01 $ 0.01 $ 0.02 $ 0.11

Adjusted net income per share - diluted $ 0.12 $ 0.07 $ 0.72 $ 0.48

(a) Store closure and exit costs represents reserves established for closed stores and facilities, adjustments to those reserves for changes in expectations for sublease or actual subleases or settlements with landlords. Ongoing expenses related with the closed facilities are also included. The Company excludes store closure and exit costs from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of its operating results because management believes these costs do not directly reflect the ongoing performance of its store operations.

(b) Costs associated with acquisitions and integration represent the costs to integrate the combined businesses resulting from the Sunflower and Henry’s Transactions. These expenses include professional fees and severance, which the Company excludes from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of the Company’s operating results because management believes these costs do not directly reflect the ongoing performance of its store operations.

(c) Loss on disposal of assets represents the losses recorded in connection with the disposal of property and equipment. The Company excludes losses on disposals of assets from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of its operating results because management believes these costs do not directly reflect the ongoing performance of its store operations.

(d) IPO bonus represents the bonuses paid to certain employees in connection with the Company’s initial public offering. The Company excludes the IPO bonus from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of its operating results because management believes these costs do not directly reflect the ongoing performance of its store operations.

(e) Secondary offering expenses including employment taxes on options exercises represents expenses the Company incurred in its secondary public offerings and employment taxes paid by the Company in connection with options exercised in those offerings. The Company has excluded these items from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of its operating results because management believes these costs do not directly reflect the performance of its store operations.

(f) Loss on extinguishment of debt represents the write-off of deferred financing costs and original issue discounts and expenses related to the refinancing or unscheduled repayment of debt. The Company has excluded this item from its adjusted EBITDA and adjusted net income to provide period-to-period comparability of its operating results because management believes these costs do not directly reflect the performance of its store operations.

(g) Adjusted income tax provision for all periods presented represents the income tax provision plus the tax effect of the adjustments described in notes (a) through (f) above based on statutory tax rates for the period. The Company has excluded these items from its adjusted income tax provision because management believes they do not directly reflect the ongoing performance of its store operations and are not reflective of its ongoing income tax provision.

1