March 10, 2015

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F Street NE

Washington, D.C. 20549

Attn: Gregory Dundas, Attorney-Advisor

| Re: | PureBase Corporation | |

| Amendment No. 1 to Current Report on Form 8-K | ||

| Filed December 24, 2015 | ||

| File No. 333-188575 |

Dear Mr. Dundas:

On behalf of PureBase Corporation, (formerly Port of Call Online, Inc.) (the “Company” or “we”), we are responding to the comments in your letter dated February 27, 2015 relating to the above referenced Form 8-K. The responses below were provided by the Company and have been numbered to correspond with the comments given in your February 27, 2015 comment letter.

As the Staff is aware, the Company changed its fiscal year end from December 31 to November 30. As a result its 2014 annual report on Form 10-K was due on March 2, 2015. Due to the Staff’s comments, the Company has extended its 10-K filing deadline in order to incorporate many of the changes being made to the Form 8-K which is the subject of the Staff’s comment letter. Our responses will denote those changes which have been replicated in the 10-K and those comments in which the responses are being deferred in favor of disclosures already existing in the Company’s Form 10-K.

comment no. 1

1. Please remove your reference to reliance on the safe harbor provided by the Private Securities Litigation Reform Act of 1995. Reliance by issuers whose stock is considered “penny stock” is not permitted.

response

The reference to the Private Securities Litigation Reform Act of 1995 has been removed from the section Cautionary Note About Forward-Looking Statements on page 2 of the 8-K.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 2

comment no. 2

2. In the first sentence, rather than describing the company as an “exploration and mining company,” revise to use the description “exploration-stage” company. In addition, state clearly and prominently that all your operations are exploratory in nature, and that you have no proven or probable reserves of any of the minerals you list. Similarly, revise to avoid the implication that your focus in the immediate and foreseeable future will be on exploitation of known reserves of minerals rather than on exploration. For example, in the first paragraph you state that the company “intends to engage in the identification, acquisition, development, mining and full-scale exploitation of industrial and natural mineral properties. . . ,” while you also state that the company “will seek to develop deposits of pozzolan, white silica, copper and potassium sulfate.” We also note that the first half of this section discusses how you hope to exploit such minerals once you discover and mine them, and only later do you get around to discussing the properties you plan to explore.

response

The Company does not believe it is an “exploration stage” company as defined in Industry Guide 7 because the Company is not primarily engaged in searching for mineral deposits. As the Company’s original 8-K disclosed and as further elaborated below and in this Amendment #1, the Company’s properties contain deposits of the minerals indicated in this 8-K, some of which is readily available for mining. The following is a description of existing development on each property. Two Reports are being filed as exhibits to the Company’s Form 10-K so as to be more readily available to the readers of the 10-K.

Esmeralda Project – Potassium Sulfur Mineral Project - Production Phase – Probable Reserves

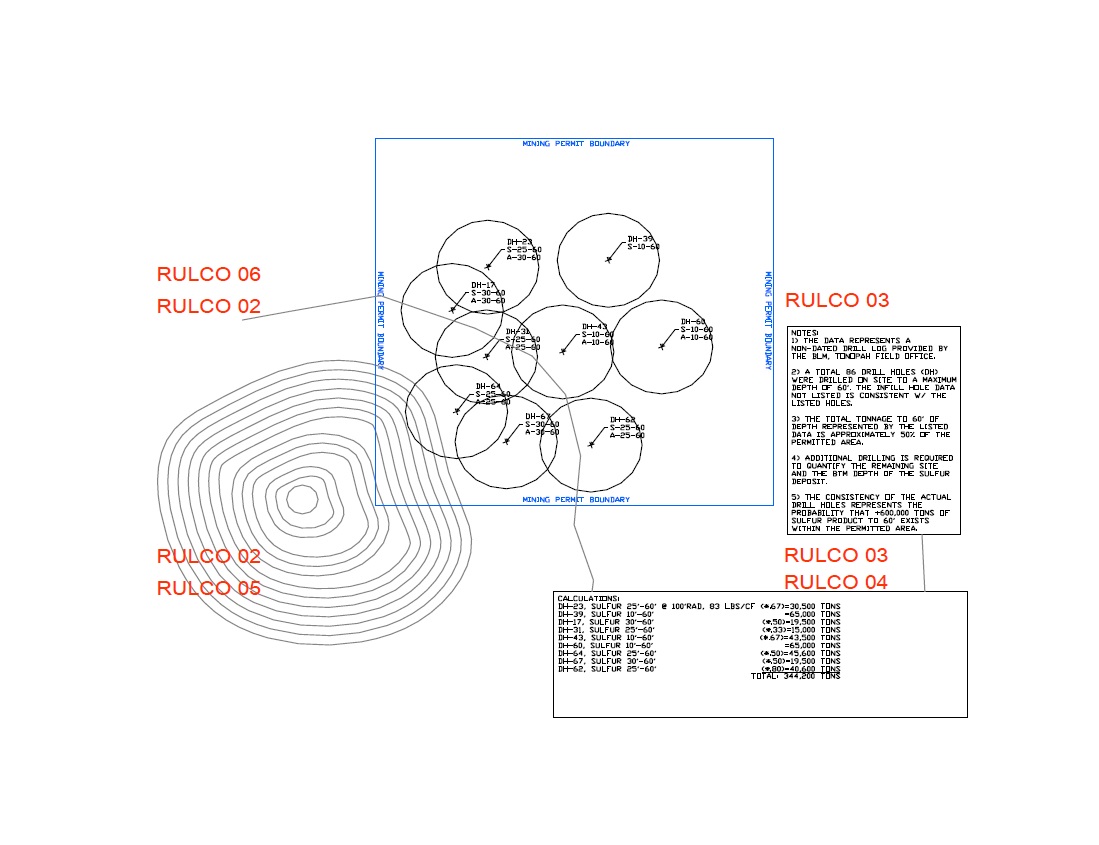

2501 acres of land held with a Federal Mineral Preference Right Lease. This fully permitted 15.5 acre site is partially developed with entry roads, secured entry, processing pad, equipment storage, pit development, process water storage and 8,200 tons of finished processed product in a stockpile at the site ready for shipment. Production and further development will restart late spring 2015.

This site has had detailed sampling and drilling and inspection. We have attached a site map showing the drill locations within the boundaries of the permitted area see Attachment A. The drill holes are only 60’ deep so the reserves listed are only per the drill data. But there is an adjacent operation to the Company’s mine site where the deposit goes hundreds of feet deep so we are confident that there are significant deposits above those listed on our site drawings. An expanded exploration and development plan for the property is being developed now beyond the fully permitted 15.5 acres.

Long Valley – Pozzolan Mineral Project – Exploration and Permitting Phase Probable or indicated Reserves

This property consists of 1145 acres of contiguous non-patented placer claims. These claims are within the identified boundaries of a known and previously developed and produced deposit. To better explain this we are filing as Exhibit 10.6 to the 10-K a state sponsored report with maps that discusses and shows the defined boundaries of this pozzolan mineral deposit. This deposit was mined and the extracted minerals used in large scale projects such as, Palo Verde Nuclear Generating Station, AZ, Graduate Theological Union Building, University of California, Berkeley, CA, George R. Moscone Convention Center, CA, Dumbarton Bridge, CA, Bechtel Engineering Center University of

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 3

California, Berkeley, CA and Bullards Bar Dam among others from 1965 through the mid 70’s. It was again mined and developed in the mid 80’s and from 2000 through 2012. The report has attached maps that show the defined area of this deposit. We have also included a Company generated drawing (Attachment B and C) that shows the location of the Company owned placer claims as they relate to this report and its defined mineral deposit location and our area of interest for the phase I exploration and permitting.

Snow White – Pozzolan Project – Pre-Production Phase - Probable or Indicated Reserves.

280 total acres for this project including 200 acres of Non-Patented placer claims on Bureau of Land Management (“BLM”) land and 80 acres of fee property all of it contiguous. This Project is a conditionally permitted site with an approved reclamation plan and an approved Plan of Operations from San Bernardino County and the BLM. The Company obtained a third party executive summary that was given to us and prepared by the seller of this mine site. It contains privately collected data and is being filed as Exhibit 10.7 to the 10-K. The Company believes this summary along with our physical inspections of the property are sufficient to support indicated reserves.

While such deposits have not been adequately measured to represent “proven or probable reserves” as defined in Guide 7, the Company believes existing mining reports and past mining activity indicate that mineral reserves do exist which could be economically and legally extracted and produced once necessary permits are obtained. Consequently, the Company’s implication that it currently has known reserves which can be exploited in the foreseeable future is accurate. However, we have revised this section to state clearly that the Company does not have any proven or probable reserves as defined in Industry Guide 7. This issue is also addressed in the 3rd Risk Factor on page 11 of the 8-K.

With regard to describing the Company’s properties separately, we believe grouping and disclosing each property together in a separate section entitled “CORE BUSINESS ASSETS” is entirely appropriate and helpful to the reader.

comment no. 3

3. Please revise to include all the information required by Industry Guide 7.

response

The descriptions of the three properties owned by PureBase and Purebase Agricultural, Inc. have been expanded to include further disclosures required by Industry Guide 7 as requested. These changes have also been replicated in Item 2 of the Company’s Form 10-K.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 4

comment no. 4

4. Please revise to provide a fuller discussion of the uses of and markets for the minerals you are interested in.

response

We have added additional information relating to the markets the Company plans to serve under the sections “Agricultural Sector” and “Construction Sector” at pages 4-7 of the amended 8-K. As for the uses of the minerals for the Company’s products, we believe the descriptions of the Purebase Solu-Sol, Purebase Humate INU, Purebase Pozzolan Ag for agricultural uses and Supplementary Cemetitious Material (“SCM”) for construction uses are fully and adequately described in the 8-K.

While the Company eventually may identify additional uses for its minerals, such a discussion would be speculative at this time. Consequently, we believe the current description of mineral uses is sufficient and no further changes to the 8-K are necessary.

comment no. 5

5. Please revise to discuss more specifically the nature of your current activities in each of the properties you discuss, the current state of those activities. Also disclose your business plan with greater specificity, including what steps you intend to take over the next several years, and the expected costs involved with those activities.

response

The description of the Company’s properties has been expanded to discuss current and planned mining operations at each project. In addition, we have added a new paragraph at page 12 discussing possible future projects or minerals that might be considered by the Company over the next several years. These changes have been replicated in the Company’s Form 10-K as well.

comment no. 6

6. Revise to delete statistics and other background information that is not directly relevant to your business plan. For example, the first paragraph under the subheading “Agricultural Sector” discusses the economic output of agricultural industries as whole, without any clear tie-in to the minerals you hope to exploit. Similarly, it is not clear that the discussion of fertilizers in general in the following paragraph is directly relevant. Please clarify or delete all such disclosure.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 5

response

The Company believes the relatively limited description of the overall size of the agricultural and construction industries is appropriate to give the reader a sense of the immense size of the markets in which the Company’s products can be used. However, we did delete the paragraph dealing with the industrialized world’s taste for meat on page 4 and in the Form 10-K. As for the “tie-in to the minerals you hope to exploit” we believe the descriptions of the Company’s proposed products which clearly discloses their uses as a soil conditioners or supplements to enhance agricultural output and the use of pozzolan as a SCM to make concrete for the construction industry seems clear to us without the need for further elaboration.

comment no. 7

7. You state under “Agricultural Sector” that you intend to “develop innovative solutions. . . for our agricultural customers.” Please revise to clarify throughout, if true, that all such developments are conditional on the success of your exploration and mining activities.

response

As stated earlier, the Company believes it has adequate deposits of minerals currently existing on its mining properties to satisfy most of its foreseeable needs for its agricultural and SCM needs. Certain additional minerals such as humate can be readily acquired from other existing sources or from additional properties the Company may decide to acquire. Consequently, the Company does not believe the success of its products is dependent on further exploration. However, we have revised the sections on Agricultural and Construction Sectors at page 6 to disclose that the Company’s products are dependent on the ability to mine adequate amounts of minerals from its existing projects or acquire certain minerals from other available sources.

comment no. 8

8. Please revise to clarify the names given to the three properties discussed. For example, why does the “Long Valley Pozzolan Deposit” bear that name if there are no confirmed deposits?

response

We have revised the description of the Company’s properties to refer to the “Snow White Mine”, the “USMC Placer Claims” and the “Esmeralda Project”. The names “Long Valley Pozzolan Deposit” and “Chimney 1 Potassium/Sulfur Deposit” simply denote long established mining references to these particular mining properties. We have made appropriate revisions to the property descriptions on pages 7-8 of the 8-K and in the Company’s Form 10-K.

comment no. 9

9. In your discussion of the Snow White Mine, you refer to minerals and ores, such as pumice, tuff/brecia, and perlite, which are not among those that you stated previously that the company had interest in. Please clarify the relevance of these substances to your business plan.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 6

response

A “pozzolan” is a siliceous or siliceous and aluminous material which, in itself, possesses little or no cementitious value but which will, in finely divided form and in the presence of water, react chemically with calcium hydroxide to form compounds possessing cementitious properties. The broad definition of a pozzolan imparts no bearing on the origin of the material, only on its capability of reacting with calcium hydroxide and water. A quantification of this capability is comprised in the term “pozzolanic activity”.

The general definition of a pozzolan embraces a large number of materials which vary widely in terms of origin, composition and properties. These minerals referred to in your Comment 9 are, by the above definition, examples of “pozzolans” and can be used as “SCM’s”.

As far as natural “Pozzolans” there are many minerals that fit that definition such as:

| Volcanic ashes | Zeolites | |

| Pumice | Tuff/Breccia | |

| Diatoms | Perlite | |

| Silica fume |

Most of these are of volcanic origin and classify as a Pozzolan which, as stated previously, can be used as an SCM.

comment no. 10

10. You refer to several reports regarding the properties discussed. For example, you mention a “state-sponsored report” which shows that the Long Valley Deposit is “underlain by mineral deposits.” Please explain more specifically how such information is pertinent to your claims. If any such reports are material, file them as exhibits.

response

The referenced state-sponsored report relating to the USMC Placer Claims is being filed as Exhibit 10.6 to the Form 10-K. A privately prepared summary relating to the Snow White Mine is being filed as Exhibit 10.7 to the Form 10-K.

comment no. 11

11. With respect to the Esmerelda County land, you refer to “[t]his deposit of potassium and sulfur,” which sounds as though there are proven reserves there. We also note in this regard the statement at the bottom of page 8 that USAM has done extensive research and testing on this deposit. Please revise to clarify.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 7

response

As the Company has stated previously, the use of the term “deposit” only refers to the presence of a given mineral but does not imply that such presence is so thoroughly measured as to represent “proven reserves”. Given the additional disclosure on page 8 and existing risk factor on page 15 which clearly state that the Company is not claiming to have proven mineral reserves, we do not believe the use of the term mineral “deposit” would make a reader think otherwise.

We have revised the section “Intellectual property applicable to cement and other products of interest to Purebase” on page 12 to clarify that USAM’s research and testing has been on the minerals themselves and not the mining projects from which they are derived. We have made a similar change to the Form 10-K.

comment no. 12

12. Please disclose whether your officers and/or directors have visited your claims, and if so, when and for how long. If they have not visited your claims, please add risk factor disclosure.

response

Both CEO Scott Dockter and Director John Bremer have visited the Company’s mining projects. Mr. Dockter has visited all three projects numerous times often spending one or more full days assessing the minerals present, creating development plans and often operating heavy equipment in the mining of the project.

Mr. Bremer has also visited the Company’s project sites on numerous occasions helping work through the mining plan, defining mining limits and product quality control.

comment no. 13

13. Please revise to include a risk factor discussing the high rate of failure of mineral exploration companies.

response

A risk factor such as the one the Staff is requesting would be entirely appropriate for a gold or silver mining venture. However, in the Company’s case, we strongly disagree with the characterization of the Company as an exploration company as previously explained. Consequently, we do not believe a risk factor relating to exploration companies is necessary or appropriate in the Company’s case.

comment no. 14

14. Please revise to quantify how much capital you expect to need to raise in the near term.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 8

response

We have added a section entitled “Budget for Implementation of the Company’s Business Plan” which now appears on page 8 of the amended 8-K. This section now discloses the Company’s plans to develop its mining projects, develop its products and the marketing of those products and minerals and the estimated costs of each over the next approximately 6 months. A similar section has been added to the Form 10-K.

comment no. 15

15. Please revise to quantify in general terms the amounts that you are required to pay in order to maintain your rights to the properties. Disclose these amounts in greater detail in the Business or MD&A section.

response

We ask that the Staff defer this 8-K comment since the Business section in the Company’s 10-K already provides a tabular disclosure of the various obligations required to maintain our rights in the three mining projects.

comment no. 16

16. It is not clear why you state that a discussion of past operations would not be indicative of the company’s new line of business. We note that your income statement shows approximately $800,000 for fiscal year 2014, and those expenses do not appear to relate to the company’s predecessor. Please revise to include a discussion of those expenses or explain in your response why they are not relevant.

response

Item 303 of Regulation S-K normally requires a discussion of the “Registrant’s” business for the past 3 years which in this case would reflect the Company’s prior business of providing online services to boaters which, going forward will not represent the Company’s business operations. However, we ask that the Staff defer this 8-K comment as a full MD&A relating to the Company’s new business is presented in the Company’s Form 10-K which will be filed on or before March 16, 2015.

comment no. 17

17. Please revise to provide a more robust description of the facts alleged in the complaint as well as the relief sought. Refer to Item 103 of Regulation S-K.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 9

response

We have expanded the section “Legal Proceeding” to include the Defendants’ primary allegation against the Plaintiffs and the relief sought by each as well as an update on Court proceedings in the matter. We have replicated these changes in the 10-K.

comment no. 18

18. Please revise to include more specific dates of service for each officer and director, covering at least the last five years. For example, it is not clear what Mr. Dockter’s business activities were prior to 2012.

response

The background information on each officer/director appearing on page 19-20 of the amended 8-K has been revised to provide more specific detail as to activities during the last 5 years. These changes also appear in the 10-K.

comment no. 19

19. On page 17, under Transactions with Related Parties, you describe Todd Gauer and Kevin Wright as officers and directors, yet they are not listed here. Please revise or advise.

response

Todd Gauer and Kevin Wright were officers and Directors of Purebase Agricultural, Inc., a subsidiary of the Company. However, they both have since resigned from the management and Board of Purebase Agricultural, Inc. and their Board positions have been assumed by Calvin Lim and John Bremer.

comment no. 20

20. We note that PureBase Corp. has a different fiscal year end than Port of Call Online. If you intend to adopt the November 30 fiscal year of PureBase, please amend the filing to include the disclosure required by Item 503 of Form 8-K. Also please note the disclosure requirements of Item 304 of Regulation S-K under Item 401 of 8-K for a change in independent accountants, if applicable.

response

Actually PureBase Corp. and Port of Call Online, Inc. had the same fiscal year ending December 31 (since they are one and the same corporation). However, the changing of the Company’s fiscal year to end on November 30 was previously reported in a Form 8-K filed with the SEC on January 12, 2015.

The change of accounting firms was previously reported in a Form 8-K filed with the SEC on October 31, 2014.

Gregory Dundas, Attorney Advisor

Re: PureBase Corporation

March 10, 2015

Page 10

comment no. 21

21. We note your statement on page F-14 that, “During the year ended November 30, 2014, PureBase acquired the Placer Mining Claims, “USMC 1-50”, from Scott Dockter, the Company’s Chief Executive Officer, in exchange for 12,708,000 pre-split (29,228,400 post-split)founders’ shares of common stock. These mining claims were recorded at the CEO’s historical cost basis of $0.” In this regard, the issuance of these shares does not appear to be included in your consolidated statement of stockholders’ deficit on page F-4 or in your weighted average shares outstanding. Please explain or revise accordingly.

response

The 29,228,400 founders’ shares issued to Scott Dockter are included in the 45,540,000 shares under the caption “Founders’ shares in Purebase, Inc.” on the consolidated Statement of Stockholders’ Deficit on page F-4. These shares are also included in the weighted average shares outstanding.

Conclusion

A marked copy of the Company’s amended Form 8-K showing the changes made in the Amendment No. 1 to the Form 8-K has been filed on edgar with the Staff in order to expedite your review period.

Please feel free to contact the undersigned if you should have any further questions regarding the responses to the Staffs’ comment letter of February 27, 2015 or any of the updated information provided in the amended Form 8-K.

| Very truly yours, | ||

| /s/ Roger D. Linn | ||

| Roger D. Linn |

cc: Scott Dockter/Amy Clemens

Attachment A

Attachment B

Attachment C