Annual Report September 30, 2019

Advised by: SKBA Capital Management, LLC www.baywoodfunds.com |

Beginning in January 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds or your financial intermediary electronically by contacting the Funds at (855) 409-2297 or baywoodfunds.ta@apexfs.com or by contacting your financial intermediary directly.

You may elect to receive all future reports in paper free of charge. You can inform the Funds or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting the Funds at (855) 409-2297 or baywoodfunds.ta@apexfs.com or by contacting your financial intermediary directly. Your election to receive reports in paper will apply to all funds held with Baywood Funds.

BAYWOOD VALUEPLUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

Dear Shareholders,

We’d like to begin the discussion on what took place in the Baywood ValuePlus strategy over the last fiscal year by highlighting one of the issues we discovered with one of the large capitalization benchmarks we are compared against.

As value investors, one of our benchmarks is the S&P 500 Value Index; the other is the Morningstar Large Cap Value Index. Another index we might choose is the Russell 1000 Value Index. All have their strengths and shortcomings; today, let’s focus on some of the S&P 500 Value’s.

The S&P 500 Value has 382 constituent companies out of the 500 in the broader index, of which some companies market capitalizations are split between the Growth and Value indexes. The mismatch is not unique to this index as over 700 stocks in the Russell 1000 are in the Value benchmark. Although the two are quite similar in overall characteristics, each methodology can lead to significant differences in sector and individual stock weights, and this is where significant holding differences can lead to significant return variances. We decided to take a closer look.

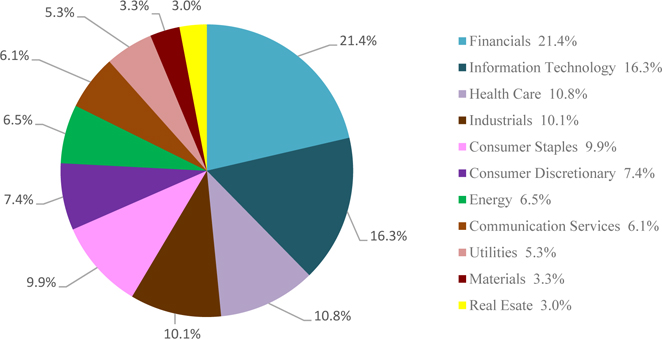

Looking at the sector breakdown chart below, slightly over 20% of the S&P 500 Value index is invested in financials, 16% or so in technology, 11% or so in healthcare and approximately 10% in industrials and consumer staples. Some might quibble over the appropriateness of such weights but generally speaking, this seems to us to be a generally acceptable view of a large capitalization value index.

Sector* Breakdown

*Based on GICS® sectors

The weightings for each sector of the index are rounded to the nearest tenth of a percent; the aggregate weights for the index may not equal 100%.

The S&P 500 Value index is market capitalization weighted and it is float-adjusted; S&P calls this FMC – Float Adjusted Market Capitalization. Breaking FMC down into its component parts, firstly, the S&P 500 index is market capitalization weighted. The largest companies in terms of size, not revenues or profits mind you, are given the largest weights. Old fashioned investors might think that the level of revenues or profits would contribute prominently to a company’s weight in an index like the S&P 500; they do not. Being of a different mindset, we would consider that to be an issue for the sustainability of the index’s return longer-term.

Secondly, the S&P 500 Value index is float-adjusted. The more shares outstanding (float) a company has the better. As long-term investors, again being of a different mindset, we like to see companies repurchase their shares over time; in other words, we like to see them reduce their float. We also like to see managements be significant owners of their shares, not simply of options. Shares are typically purchased whereas options tend to be granted. Owning shares outright in one’s company speaks highly of management’s alignment of

BAYWOOD VALUEPLUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

interests with those of its shareholders. While we recognize that there are bad apples and exceptions to every rule, shareholder alignment tends to reduce perverse incentives. Perverse incentives include compensation not tied to the well-being of the company and all its stakeholders. Perverse incentives destroy sustainability and economic goodwill. Perverse incentives are widespread in corporations as compensation packages created by outside consultants are typically laden with generous options grants. Owner-operators and vested managers tend to be better operators. Yet float-adjusted benchmarks like the S&P 500 discourage this from taking place by selling companies that reduce their public float. The more management is aligned with shareholders and the more is purchased by companies with the goal of reducing shares outstanding, the less it will be owned in the index.

We would add a caveat that not all share buybacks are created equal. Buybacks should not be done in the place of investing in one’s business. This is another endemic problem we notice with managements and is a direct result of their short term horizons; not enough has been spent in the businesses they run precisely because they are primarily incented with short-term objectives - not the long term well-being of the enterprise and its stakeholders. So one needs to carefully judge when reading about companies initiating significant buybacks. Are they truly significant? Will they in fact reduce the public float – a good outcome for long term shareholders? They most likely will not. Does this mindset make any sense? None whatsoever in the longer term but then benchmarks and most managements cannot concern themselves with the long-term.

So the S&P 500 Value is market cap weighted and it is float-adjusted; two significant issues in and of themselves but secondary to the point of this note. Ignoring those two issues, looking at the S&P 500 Value’s top ten holdings pictured below also seems to us to be a fairly reasonable representation of large companies that may generally not be egregiously overpriced. There are perhaps too many large banks, which makes us ask why not be somewhat more selective, but the point of an index is to be diversified. The list below appears to be diversified since it includes telecom, financials, technology, healthcare; which represent a wide swath of America’s corporate giants. One would likely assume that diversification would increase as companies are added to the list. All appropriate in the construction of the index.

Top 10 Constituents By Index Weight

| CONSTITUENT | SYMBOL | SECTOR* |

| Apple Inc. | AAPL | Information Technology |

| JP Morgan Chase & Co | JPM | Financials |

| AT&T Inc | T | Communication Services |

| Bank of America Corp. | BAC | Financials |

| Chevron Corp | CVX | Energy |

| Unitedhealth Group Inc. | UNH | Health Care |

| Berkshire Hathaway B | BRK.B | Financials |

| Wells Fargo & Co | WFC | Financials |

| Walmart Inc. | WMT | Consumer Staples |

| Citigroup Inc | C | Financials |

| * | Based on GICS® sectors |

What S&P does not state in the index factsheet, for obvious reasons, is that Apple is the largest single position of all companies by a factor of three at minimum. The top holdings table above conveniently and perhaps intentionally fails to disclose the weight of each of the largest holdings. So let us do it for them.

Apple has a weight of 8.5%! To state the obvious, that is nearly a tenth of the entire index – one company – nearly 10% in an index, an index which by its own definition is intended to be diversified. To put this in perspective, 8.5% is over half of the index’s technology weight. So it really doesn’t matter that the index has 16% in technology; all that matters is Apple at half that weight.

One might rightfully question whether Apple should, in a large value index, have a weight that is nearly three times that of JPMorgan, over four times that of ExxonMobil, six times that of WalMart and Citigroup and seven times that of Johnson & Johnson.

The above snapshot is perfectly illustrative of the main driver behind the index; it is one company. The snapshot happens to be taken during an up day in the market; should Apple have a bad day, it won’t matter how the rest of the other 381 companies fare. As we are all aware, indexes tout themselves as being diversified. As such, despite the index being comprised of 382 holdings, the impact that one single security has on the overall returns strikes us as somewhat, if not meaningfully, misleading. In our investment process, we limit the maximum size of a holding to 5% to avoid undue company specific risk, unreasonable volatility which may compromise desirable

BAYWOOD VALUEPLUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

full cycle return characteristics.

Before we leave the topic of the S&P 500 Value, we also find it worth mentioning that periodic updates in index holdings can include a number of growth-stock companies that can scarcely be described as belonging in a value benchmark. Recently, those would include Costco, Home Depot, Starbucks, Booking Holdings (aka Booking.com), Danaher, Zoetis, Charter, and Estee Lauder. All very large companies, which is why they have found their way in the benchmark, but all clearly displaying characteristics tied to growth, NOT value. Each one of these companies trade at a premium to the S&P 500 (regular, not value) and as a group trade at an average of 29X next year’s EPS targets, which is 12X more than the S&P 500’s lofty level of 17X.

At a minimum, we believe it is worthwhile bringing this to prospective investors’ attention.

With respect to the Baywood ValuePlus strategy, the last fiscal year was a difficult one from a relative standpoint. Over the last twelve months, the strategy is essentially flat. The broad U.S. stock market declined significantly in the fourth calendar quarter of last year and has since had a strong rebound. ValuePlus declined in the fourth quarter as well given the degree to which value stocks underperformed growth in that period. Furthermore, another not often noticed side-effect of indexation is that in the most recent downturn, any stock that was not considered a “mega-cap” underperformed significantly. The average stock in the fourth quarter of 2018 declined over 16%, while the most represented stocks in the indices, those with market capitalizations above $200B only declined 6%. That difference in performance meant that if an active manager was indeed different than the index, then chances are they underperformed materially. The rebound in 2019 was just enough to overcome fall of 2018 declines. A single year does not make a full cycle, however, and maintaining a disciplined strategy over time has been more important than chasing trends at the wrong time. Prevailing themes that defy the logic of valuation and fundamental discipline continue to pervade markets. This has happened before and it is taking place as we speak. Over the last year we have continued to purchase industry leading companies selling at discount prices due to the wholesale abandonment of the investing majority, which is perversely becoming narrower and narrower.

For example, at less than 5%, energy has the smallest representation in the S&P 500 that it has had in over forty years. Forty years ago, the allocation to energy was the highest of any sector. S&P’s sector allocation has implications for and is correlated to many of the other benchmarks that are in some way tied to this particular index. Ironically, despite barely being represented, energy companies are much more profitable today than they were three years ago, yet their representation has shrunk dramatically. When sector weights reach extremes, small changes can have dramatic impacts; this goes for sectors at historically high weights as well as those at historically low weights. Technology had the largest allocation of all sectors in the late 1990s. Being cautious and underweight was ultimately proven right. More importantly, it was the prudent thing to do. Financials were nearly 40% of the Russell 1000 Value at the peak of the credit cycle in 2006. The prudent asset allocation at that time would have been to underweight risky financials and overweight neglected sectors. Today, we once again find sectors being neglected. As value investors, this is where we often find opportunities. We currently happen to be overweight energy compared with our benchmarks. We are overweight not simply because of their general absence in most benchmarks but because of their profits and cash flow distributions to shareholders. The same can be said about basic materials. Companies like Dow and DuPont are not becoming disintermediated or eliminated from the industrial supply chain. Yet that is exactly what is taking place in benchmarks; they are being eliminated from economic representation in what are supposed to be diversified benchmarks. At just over 3% in the S&P 500 Value and under 2% in the Morningstar Large Value; the basic materials sector is becoming a rounding error. We also are overweight basic materials.

The reverse is also true. The competitive global currency devaluation, which is directly tied to the decline in rates in most developed countries has also led to excesses in interest sensitive sectors. Those clearly include utilities and many consumer staples. Ultimately, valuations and fundamentals trump momentum and trend following; for this reason we are under-represented compared with our benchmarks and this hurt over the last year. It is striking to us how severe the disappearance of valuation discipline is so soon following the global financial crisis. What is all the more striking is that we are in the midst of real-time examples of excesses being unwound. Yet investors are choosing to ignore any parallels.

Let’s take a look at WeWork, or We Co, as it is now called. No one with any common sense believes that the We Company operates a sustainable business model. We Co has not re-designed the house of cards. What it is doing is quite simply dangerous and has been tried time and time before; it has never succeeded. In short the company has a massive asset-liability mismatch. This is the downfall of any company that has attempted such a scheme before the We Company. Assets, rents in this case, are short-term, typically month-to-month. Liabilities, leases on buildings, tend to be long-term, however, say five to ten years on average. So We Co is locking in long-term obligations while suffering the vagaries of customers which choose to rent every month. Any downturn and this model will self-destruct; and it will do so quickly. In fact, even without a downturn, it appears that the model is imploding. Investors have been content to mostly watch the drama unfold from the sidelines knowing the absurdity of it all. Yet those same investors are ignoring similar excesses in other

BAYWOOD VALUEPLUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

much more liquid markets. In fact, investors are ignoring similar excesses in much more significant asset classes. If We Co disappears, this may not be a significant problem on its own. However, more broadly speaking the impacts could be fairly significant when you consider its effect on commercial real estate prices and the banks with exposure to such real estate. If bond proxies stop being purchased simply due to trend following and momentum, however, the effect will be much more significant. In conclusion, despite being shown a real time example of what to stay away from due to inevitably bad consequences, most refuse to draw comparisons to the much bigger elephant in the room.

We will continue to steer clear of excesses in the marketplace and focus our attention on sectors that are being neglected. Over the last year, this resulted in underperformance compared to benchmarks. But this is a marathon, not a sprint and we find solace in the fact that over time, common sense has prevailed in equity markets. We also take solace in companies that have sound or improving balance sheets, not the other way around. This will be rewarded at some point in time.

We do not lay all the blame on index construction, excesses and abuses. Nevertheless, over half of ValuePlus’ gap with the S&P 500 Value resulted from sector allocation differences. We also were responsible for owning stocks whose investment hypotheses failed to materialize in our favor. Within energy, Schlumberger, Occidental and H&P all detracted from overall returns. Due to their inclusion within energy, it is difficult to specify whether those declines were stock specific or due to the wholesale elimination of energy stocks. Not all is rosy within energy and both Schlumberger and Helmerich & Payne need to experience an improvement in their customers’ orders in order to benefit. Until large energy companies start spending in order to improve their production growth, servicing the sector will be difficult. We will also fault Occidental for its unflattering stock. We exited our position following what we believe to be an overpriced acquisition of Anadarko Petroleum with high priced debt. Management can take complete responsibility for the decline in their stock and we cannot fault other investors for seeking management changes. This is not simply optically bad; it appears bad on all fronts.

Tapestry, CenturyLink and Taubman also detracted significantly during the fiscal year. The three companies fall in distinct categories of underperformers. Ultimately, the question we ask ourselves is whether the issue is temporary or permanent and if it the issues can be resolved within our investment horizon. In the case of Tapestry, trade tensions have clearly had a negative impact. While we believe that US China relationship will improve, the passage of time is not in Tapestry’s favor. Fashion is fickle and products need to be able to sell within a compressed timeframe. Without the ability to do so, the restructuring that the company has been implementing may not succeed, or do so within an indeterminate timeframe. For these reasons, we exited despite attractive valuation. Fundamentals trump valuations whether they be expensive or inexpensive stocks.

In a completely different sector, CenturyLink is a company that generates high levels of cash flow. We simply need it to reduce debt with the proceeds. It is that simple. We have given the company until the end of 2019, more or less, to notice an improvement in its balance sheet. If we fail to see this desired improvement, we will conclude that management is not taking the steps necessary to strengthen itself enough in the case of an economic downturn and we will very likely exit.

Taubman falls in yet another category of high-grading our portfolio in times of general price declines. It should be no secret that mall REIT’s have suffered recently due to retailer bankruptcies. Yet there are good mall operators and there are poor mall operators. Taubman belongs in the former category. Nevertheless, all mall REIT’s have declined significantly, including a couple of more diversified companies, Brookfield Properties and Simon Property Group. We took the opportunity to high-grade into Brookfield due to the decline in all of the companies’ stocks. It is not that we completely lost faith in Taubman; it is simply that we were able to get similar upside potential with a lower probability assigned to a negative outcome.

As we look out towards a new fiscal year, we have no idea what the broad markets will do. Over a reasonable time period, however, we would encourage investors to moderate their overall return expectations. As always, we will continue to manage this strategy with sound investment principles. We will continue to do this because we ourselves are large investors in the fund and we therefore would have it no other way. As a result, while differences between the fund and markets may differ over short to medium time periods, we are confident that we will continue to build wealth over time while being prudent, all the more so during times of excess.

Current and future portfolio holdings are subject to change and risk.

The Morningstar category is used to compare fund performance to its peers. It is not possible to invest directly into an index or category. Past performance is no guarantee of future results.

BAYWOOD VALUEPLUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

Risk Considerations: Mutual fund investing involves risk, including the possible loss of principal. The Fund primarily invests in undervalued securities, which may not appreciate in value as anticipated by the Advisor or remain undervalued for longer than anticipated. The Fund may invest in American Depositary Receipts (ADRs), which involves risks relating to political, economic or regulatory conditions in foreign countries and may cause greater volatility and less liquidity. The Fund may also invest in convertible securities and preferred stock, which may be adversely affected as interest rates rise.

BAYWOOD VALUEPLUS FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

SEPTEMBER 30, 2019

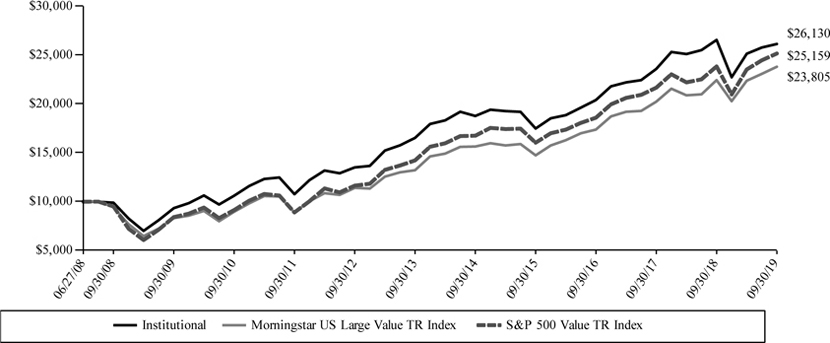

The following chart reflects the change in the value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Baywood ValuePlus Fund (the “Fund”) compared with the performance of the benchmarks, Morningstar US Large Value TR Index, and the secondary benchmark, S&P 500 Value TR Index (the “indices”), since inception. The Morningstar US Large Value TR Index measures the performance of large-cap stocks with relatively low prices given anticipated per share earnings, book value, cash flow, sales and dividends. The S&P 500 Value TR Index is a market capitalization weighted index. The total return of the indices include the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the indices do not include expenses. The Fund is professionally managed, while the indices are unmanaged and are not available for investment.

Comparison of Change in Value of a $10,000 Investment

Institutional Shares vs. Morningstar US Large Value TR Index and S&P 500 Value TR Index

| Average Annual Total Returns Periods Ended September 30, 2019 | One Year | Five Year | Ten Year | Since Inception 06/27/08 | ||||

| Baywood ValuePlus Fund* | -1.55% | 6.84% | 10.84% | 8.90% | ||||

| Morningstar US Large Value TR Index | 6.12% | 8.76% | 11.09% | 8.01% | ||||

| S&P 500 Value TR Index | 5.56% | 8.47% | 11.56% | 8.54% |

| * | The Fund’s Institutional Shares performance for periods prior to the commencement of operations (12/2/13) is that of a collective investment trust managed by the Fund’s Advisor and portfolio management team. The Institutional Shares of the collective investment trust commenced operations on May 2, 2011. |

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating expense ratio (gross) is 8.83%. However, the Fund’s advisor has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 0.70%, through January 31, 2020 (the “Expense Cap”). The Expense Cap may be raised or eliminated only with the consent of the Board of Trustees. The advisor may be reimbursed by the Fund for fees waived and expenses reimbursed by the advisor pursuant to the Expense Cap if such payment is approved by the Board, made within three years of the fee waiver or expense reimbursement and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current Expense Cap and (ii) the Expense Cap in place at the time the fees/expenses were waived/reimbursed. Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement will increase if exclusions from the Expense Cap apply. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (855) 409-2297.

BAYWOOD VALUEPLUS FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2019

| Shares | Security Description | Value | ||||||

| Common Stock - 97.1% | ||||||||

| Basic Materials - 6.3% | ||||||||

| 966 | Corteva, Inc. | $ | 27,048 | |||||

| 733 | Dow, Inc. | 34,928 | ||||||

| 366 | DuPont de Nemours, Inc. | 26,099 | ||||||

| 1,160 | Nutrien, Ltd. | 57,861 | ||||||

| 300 | Packaging Corp. of America | 31,830 | ||||||

| 177,766 | ||||||||

| Capital Goods / Industrials - 8.7% | ||||||||

| 600 | Cummins, Inc. | 97,602 | ||||||

| 500 | Eaton Corp. PLC | 41,575 | ||||||

| 1,300 | Johnson Controls International PLC | 57,057 | ||||||

| 500 | TE Connectivity, Ltd. | 46,590 | ||||||

| 242,824 | ||||||||

| Communication Services - 6.2% | ||||||||

| 2,100 | CenturyLink, Inc. | 26,208 | ||||||

| 1,400 | Comcast Corp., Class A | 63,112 | ||||||

| 1,400 | Verizon Communications, Inc. | 84,504 | ||||||

| 173,824 | ||||||||

| Consumer Discretionary - 7.2% | ||||||||

| 700 | Kontoor Brands, Inc. | 24,570 | ||||||

| 600 | Lear Corp. | 70,740 | ||||||

| 1,000 | Target Corp. | 106,910 | ||||||

| 202,220 | ||||||||

| Consumer Staples - 8.9% | ||||||||

| 200 | Kimberly-Clark Corp. | 28,410 | ||||||

| 1,000 | Molson Coors Brewing Co., Class B | 57,500 | ||||||

| 700 | Mondelez International, Inc., Class A | 38,724 | ||||||

| 300 | PepsiCo., Inc. | 41,130 | ||||||

| 700 | Walmart, Inc. | 83,076 | ||||||

| 248,840 | ||||||||

| Energy - 10.2% | ||||||||

| 700 | BP PLC, ADR | 26,593 | ||||||

| 600 | Chevron Corp. | 71,160 | ||||||

| 900 | ConocoPhillips | 51,282 | ||||||

| 500 | Helmerich & Payne, Inc. | 20,035 | ||||||

| 600 | Phillips 66 | 61,440 | ||||||

| 1,600 | Schlumberger, Ltd. | 54,672 | ||||||

| 285,182 | ||||||||

| Financials - 20.7% | ||||||||

| 2,000 | American International Group, Inc. | 111,400 | ||||||

| 300 | Ameriprise Financial, Inc. | 44,130 | ||||||

| 700 | BOK Financial Corp. | 55,405 | ||||||

| 1,200 | Citigroup, Inc. | 82,896 | ||||||

| 700 | Fidelity National Financial, Inc. | 31,087 | ||||||

| 300 | M&T Bank Corp. | 47,391 | ||||||

| 1,500 | MetLife, Inc. | 70,740 | ||||||

| 1,000 | Morgan Stanley | 42,670 | ||||||

| 800 | Prosperity Bancshares, Inc. | 56,504 | ||||||

| 700 | U.S. Bancorp | 38,738 | ||||||

| 580,961 | ||||||||

| Health Care - 12.7% | ||||||||

| 200 | AbbVie, Inc. | 15,144 | ||||||

| 300 | Amgen, Inc. | 58,053 | ||||||

| 1,000 | AstraZeneca PLC, ADR | 44,570 | ||||||

| 600 | Cardinal Health, Inc. | 28,314 | ||||||

| 400 | CVS Health Corp. | 25,228 | ||||||

| 800 | Gilead Sciences, Inc. | 50,704 | ||||||

| 1,700 | Koninklijke Philips NV, ADR | 78,421 | ||||||

| 500 | Medtronic PLC | 54,310 | ||||||

| 354,744 | ||||||||

| Shares | Security Description | Value | ||||||

| Real Estate - 4.2% | ||||||||

| 2,100 | Brookfield Property REIT, Inc. | $ | 42,819 | |||||

| 4,600 | VEREIT, Inc. REIT | 44,988 | ||||||

| 1,100 | Weyerhaeuser Co. REIT | 30,470 | ||||||

| 118,277 | ||||||||

| Technology - 7.6% | ||||||||

| 1,800 | Cisco Systems, Inc. | 88,938 | ||||||

| 1,300 | HP, Inc. | 24,596 | ||||||

| 1,100 | Intel Corp. | 56,683 | ||||||

| 800 | NetApp, Inc. | 42,008 | ||||||

| 212,225 | ||||||||

| Transportation - 2.4% | ||||||||

| 1,900 | Seaspan Corp. | 20,197 | ||||||

| 300 | Union Pacific Corp. | 48,594 | ||||||

| 68,791 | ||||||||

| Utilities - 2.0% | ||||||||

| 700 | Dominion Energy, Inc. | 56,728 | ||||||

| Total Common Stock (Cost $2,355,598) | 2,722,382 | |||||||

| Shares | Security Description | Value | ||||||

| Money Market Fund - 2.9% | ||||||||

| 80,976 | Federated Government Obligations Fund, Institutional Class, 1.85% (a) | |||||||

| (Cost $80,976) | 80,976 | |||||||

| Investments, at value - 100.0% (Cost $2,436,574) | $ | 2,803,358 | ||||||

| Other Assets & Liabilities, Net - 0.0% | (1,078 | ) | ||||||

| Net Assets - 100.0% | $ | 2,802,280 | ||||||

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

| REIT | Real Estate Investment Trust |

| (a) | Dividend yield changes daily to reflect current market conditions. Rate was the quoted yield as of September 30, 2019. |

The following is a summary of the inputs used to value the Fund's instruments as of September 30, 2019.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

| Valuation Inputs | Investments in Securities | |||

| Level 1 - Quoted Prices | $ | 2,722,382 | ||

| Level 2 - Other Significant Observable Inputs | 80,976 | |||

| Level 3 - Significant Unobservable Inputs | – | |||

| Total | $ | 2,803,358 | ||

The Level 1 value displayed in this table is Common Stock. The Level 2 value displayed in this table is a Money Market Fund. Refer to this Schedule of Investments for a further breakout of each security by industry.

See Notes to Financial Statements.

BAYWOOD VALUEPLUS FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2019

| PORTFOLIO HOLDINGS (Unaudited) | ||||

| % of Total Investments | ||||

| Basic Materials | 6.3 | % | ||

| Capital Goods / Industrials | 8.7 | % | ||

| Communication Services | 6.2 | % | ||

| Consumer Discretionary | 7.2 | % | ||

| Consumer Staples | 8.9 | % | ||

| Energy | 10.2 | % | ||

| Financials | 20.7 | % | ||

| Health Care | 12.7 | % | ||

| Real Estate | 4.2 | % | ||

| Technology | 7.6 | % | ||

| Transportation | 2.4 | % | ||

| Utilities | 2.0 | % | ||

| Money Market Fund | 2.9 | % | ||

| 100.0 | % | |||

See Notes to Financial Statements.

BAYWOOD VALUEPLUS FUND

STATEMENT OF ASSETS AND LIABILITIES

SEPTEMBER 30, 2019

| ASSETS | ||||

| Investments, at value (Cost $2,436,574) | $ | 2,803,358 | ||

| Receivables: | ||||

| Fund shares sold | 1,781 | |||

| Dividends | 4,140 | |||

| From investment advisor | 9,464 | |||

| Prepaid expenses | 8,684 | |||

| Total Assets | 2,827,427 | |||

| LIABILITIES | ||||

| Accrued Liabilities: | ||||

| Fund services fees | 4,766 | |||

| Other expenses | 20,381 | |||

| Total Liabilities | 25,147 | |||

| NET ASSETS | $ | 2,802,280 | ||

| COMPONENTS OF NET ASSETS | ||||

| Paid-in capital | $ | 2,411,519 | ||

| Distributable earnings | 390,761 | |||

| NET ASSETS | $ | 2,802,280 | ||

| SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED) | ||||

| Institutional Shares | 164,506 | |||

| NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE | ||||

| Institutional Shares (based on net assets of $2,802,280) | $ | 17.03 | ||

See Notes to Financial Statements.

BAYWOOD VALUEPLUS FUND

STATEMENT OF OPERATIONS

YEAR ENDED SEPTEMBER 30, 2019

| INVESTMENT INCOME | ||||

| Dividend income (Net of foreign withholding taxes of $604) | $ | 87,081 | ||

| Total Investment Income | 87,081 | |||

| EXPENSES | ||||

| Investment advisor fees | 13,469 | |||

| Fund services fees | 64,935 | |||

| Transfer agent fees: | ||||

| Investor Shares | 15,150 | |||

| Institutional Shares | 18,977 | |||

| Distribution fees: | ||||

| Investor Shares | 3,992 | |||

| Custodian fees | 5,000 | |||

| Registration fees: | ||||

| Investor Shares | 18,905 | |||

| Institutional Shares | 15,512 | |||

| Professional fees | 23,346 | |||

| Trustees' fees and expenses | 2,528 | |||

| Other expenses | 19,497 | |||

| Total Expenses | 201,311 | |||

| Fees waived and expenses reimbursed | (178,264 | ) | ||

| Net Expenses | 23,047 | |||

| NET INVESTMENT INCOME | 64,034 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | ||||

| Net realized gain on investments | 30,295 | |||

| Net change in unrealized appreciation (depreciation) on investments | (139,596 | ) | ||

| NET REALIZED AND UNREALIZED LOSS | (109,301 | ) | ||

| DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (45,267 | ) | |

See Notes to Financial Statements.

BAYWOOD VALUEPLUS FUND

STATEMENTS OF CHANGES IN NET ASSETS

| For the Years Ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| OPERATIONS | ||||||||

| Net investment income | $ | 64,034 | $ | 52,117 | ||||

| Net realized gain | 30,295 | 113,563 | ||||||

| Net change in unrealized appreciation (depreciation) | (139,596 | ) | 143,093 | |||||

| Increase (Decrease) in Net Assets Resulting from Operations | (45,267 | ) | 308,773 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Investor Shares | (113,003 | ) | (82,827 | )* | ||||

| Institutional Shares | (72,133 | ) | (39,334 | )** | ||||

| Total Distributions Paid | (185,136 | ) | (122,161 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Sale of shares: | ||||||||

| Investor Shares | 7,750 | 12,064 | ||||||

| Institutional Shares | 2,204,983 | 137,213 | ||||||

| Reinvestment of distributions: | ||||||||

| Investor Shares | 112,658 | 82,750 | ||||||

| Institutional Shares | 72,102 | 39,334 | ||||||

| Redemption of shares: | ||||||||

| Investor Shares | (1,805,831 | ) | (1,103 | ) | ||||

| Institutional Shares | (435,150 | ) | (8,552 | ) | ||||

| Increase in Net Assets from Capital Share Transactions | 156,512 | 261,706 | ||||||

| Increase (Decrease) in Net Assets | (73,891 | ) | 448,318 | |||||

| NET ASSETS | ||||||||

| Beginning of Year | 2,876,171 | 2,427,853 | ||||||

| End of Year | $ | 2,802,280 | $ | 2,876,171 | *** | |||

| SHARE TRANSACTIONS | ||||||||

| Sale of shares: | ||||||||

| Investor Shares | 477 | 649 | ||||||

| Institutional Shares | 137,725 | 7,574 | ||||||

| Reinvestment of distributions: | ||||||||

| Investor Shares | 7,217 | 4,630 | ||||||

| Institutional Shares | 4,519 | 2,189 | ||||||

| Redemption of shares: | ||||||||

| Investor Shares | (112,284 | ) | (62 | ) | ||||

| Institutional Shares | (27,993 | ) | (474 | ) | ||||

| Increase in Shares | 9,661 | 14,506 | ||||||

| * | Distribution was the result of net investment income and net realized gain of $31,550 and $51,277, respectively, at September 30, 2018. |

| ** | Distribution was the result of net investment income and net realized gain of $16,732 and $22,602, respectively, at September 30, 2018. |

| *** | Includes undistributed net investment income of $5,683 at September 30, 2018. The requirement to disclose the corresponding amount as of September 30, 2019 was eliminated. |

See Notes to Financial Statements.

BAYWOOD VALUEPLUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year or period presented.

| For the Year Ended September 30, 2019 | For the Year Ended September 30, 2018 | For the Year Ended September 30, 2017 | For the Period Ended September 30, 2016 (a) | For the Year Ended November 30, 2015 | December 2, 2013 (b) Through November 30, 2014 | |||||||||||||||||||

| INSTITUTIONAL SHARES | ||||||||||||||||||||||||

| NET ASSET VALUE, Beginning of Period | $ | 18.63 | $ | 17.36 | $ | 15.59 | $ | 17.00 | $ | 19.42 | $ | 17.56 | ||||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||||||

| Net investment income (c) | 0.44 | 0.38 | 0.38 | 0.29 | 0.39 | 0.41 | ||||||||||||||||||

| Net realized and unrealized gain (loss) | (0.84 | ) | 1.76 | 2.02 | 0.94 | (1.06 | ) | 1.50 | ||||||||||||||||

| Total from Investment Operations | (0.40 | ) | 2.14 | 2.40 | 1.23 | (0.67 | ) | 1.91 | ||||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||||||

| Net investment income | (0.39 | ) | (0.35 | ) | (0.36 | ) | (2.27 | ) | (0.35 | ) | (0.05 | ) | ||||||||||||

| Net realized gain | (0.81 | ) | (0.52 | ) | (0.27 | ) | (0.37 | ) | (1.40 | ) | – | |||||||||||||

| Total Distributions to Shareholders | (1.20 | ) | (0.87 | ) | (0.63 | ) | (2.64 | ) | (1.75 | ) | (0.05 | ) | ||||||||||||

| NET ASSET VALUE, End of Period | $ | 17.03 | $ | 18.63 | $ | 17.36 | $ | 15.59 | $ | 17.00 | $ | 19.42 | ||||||||||||

| TOTAL RETURN | (1.55 | )% | 12.57 | % | 15.60 | % | 8.65 | %(d) | (3.58 | )% | 10.87 | %(d) | ||||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||||||

| Net Assets at End of Period (000s omitted) | $ | 2,802 | $ | 936 | $ | 711 | $ | 536 | $ | 426 | $ | 11,067 | ||||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||||||

| Net investment income | 2.66 | % | 2.10 | % | 2.28 | % | 2.30 | %(e) | 2.23 | % | 2.26 | %(e) | ||||||||||||

| Net expenses | 0.70 | % | 0.70 | % | 0.70 | % | 0.70 | %(e) | 0.70 | % | 0.70 | %(e) | ||||||||||||

| Gross expenses (f) | 8.13 | % | 8.83 | % | 11.16 | % | 14.43 | %(e) | 2.09 | % | 2.50 | %(e) | ||||||||||||

| PORTFOLIO TURNOVER RATE | 49 | % | 34 | % | 48 | % | 22 | %(d) | 32 | % | 35 | %(d) | ||||||||||||

| (a) | Effective March 24, 2016, the Fund changed its fiscal year end from November 30 to September 30. The information presented is for the period December 1, 2015 to September 30, 2016. |

| (b) | Commencement of operations. |

| (c) | Calculated based on average shares outstanding during each period. |

| (d) | Not annualized. |

| (e) | Annualized. |

| (f) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

BAYWOOD SOCIALLYRESPONSIBLE FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

Dear Shareholder,

We are pleased to report our economic and financial market perspectives and the investment activities for the Baywood SociallyResponsible Fund (the “Fund”) for the 12 months ended September, 2019. The Fund is a mid-to-large capitalization value-oriented portfolio of stock holdings selected from a universe of stocks created through the application of inclusionary and exclusionary social screens and assessments of the ESG profile of each company. Among these stocks, we further evaluate and assess each prospective holding’s valuation and fundamental business attraction to determine the current portfolio holdings. In selecting investments, we consider social criteria such as an issuer’s community relations, corporate governance, employee diversity, employee relations, environmental impact and sustainability, human rights record and product safety. Using both quantitative and qualitative data, we also evaluate an issuer’s involvement in specific revenue generating activities to determine whether the issuer’s involvement was meaningful or incidental with respect to that activity.

We would like to take a moment to address a troubling trend that has been gaining in popularity in recent years. Indexation has been a boon to the asset-gathering fund supermarkets and a bane to active managers who attempt to keep up with the S&P 500 and all of its offshoots. Without rehashing what is mostly common knowledge by now, we’d like to highlight a single example which perfectly illustrates the situation in which some investors find themselves. Beginning with the conclusion, when this trend breaks down, as it inevitably will, it will pose significant risks to most investors’ and plans’ capital preservation objective.

MSCI, the owner of S&P and its ubiquitous indices recently expanded its list to include an ESG version of the S&P 500, as all good index providers know a large untapped market when they see one. What started as a noble and worthwhile cause—that of owning sustainably run companies across industries for the long-term benefit of all stakeholders—has very quickly morphed into a race for assets. The desired end has shifted as have the means—it is purely and simply about capturing as many assets as possible rather than serving client needs, desires and objectives.

SKBA begins its process by recognizing that for clients that have a passion for investing in companies that, for example, are environmentally responsible and avoiding those that are not, the portfolio that meets their needs, desires and objectives ought to be quite different than the broader index holdings and weights. Just reshuffling the deck of cards (stocks and weights) doesn’t accomplish this.

Indexation, in general, has the beneficial or perverse effect, depending on which side of the table one might be, of lowering profitability for mutual fund and ETF complexes. As with many ideas before it, what started out as a noble cause under Vanguard’s Jack Bogle, has been taken too far and become a dangerous one. The resulting profit compression has prompted the explosion of variants of existing products in order to make up for the deteriorating business model. As such, said supermarkets have been on a frenzied pursuit of growth in order to satisfy their own shareholders’ thirst for higher and higher earnings. One might ask how that, in and of itself, might demonstrate responsibility or sustainability. It does not.

Being students and practitioners of the industry for a number of decades, we have witnessed many examples of such behavior; our observation is that they rarely end well. Financial Products at AIG were not in fact a bad business as long as they remained a small part of the overall business. But a change in management ushered Financial Products to its extreme to which it brought the destruction of AIG.

Attempting to have deeper customer relationships at inception was not a bad idea for Wells Fargo until new management decided that “if some was good, more would be better.” Financial companies aren’t the only ones to fall for this trap but they do figure prominently. Enter ESG.

MSCI, the owner behind the S&P 500 index, introduced the S&P 500 ESG index early this year. As investors in the ESG/SRI space on behalf of many of our clients and shareholders since the inception of our firm in the late 1980s, our curiosity obviously led us to perform some basic investigating.

The S&P 500 index is market capitalization weighted, the same way many indexes are constructed. The largest companies in terms of size, not revenues or profits mind you, are given the largest weights. The size of revenues or profits, in fact, are not considered in constructing the S&P 500. Old fashioned investors might think that the level of revenues or profits should contribute to a company’s weight in an index like the S&P 500; they do not. Being of a different mindset, we would consider that to be an issue for the sustainability of the index’s return longer-term.

There is another issue; the S&P 500 and the S&P 500 ESG are float-adjusted. The more shares outstanding a company has, the better. As long term investors, again being of a different mindset, we like to see companies repurchase their shares over time. We also like to

BAYWOOD SOCIALLYRESPONSIBLE FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

see managements be significant owners of their shares, not simply of options. Shares are typically purchased whereas options tend to be granted. Owning shares outright in one’s company can speak highly of management’s alignment of interests with those of shareholders. While we recognize that there are bad apples and exceptions to every rule, shareholder alignment tends to reduce perverse incentives. Perverse incentives include compensation not tied to the well-being of the company and all its stakeholders. Perverse incentives destroy sustainability and economic goodwill. Perverse incentives are widespread in corporations as compensation is laden with generous options grants. Owner-operators and vested managers tend to be better operators. Yet float-adjusted benchmarks like the S&P 500 discourage this from taking place by selling companies that reduce their public float. The more management is aligned with shareholders and the more that is purchased by companies with the goal of reducing shares outstanding, the less it will be owned in the index.

So the S&P 500 ESG is market cap weighted and it is float adjusted; two significant issues in and of themselves but secondary to the point of this note. Let’s assume that the motives behind creating an ESG index are virtuous and that the construction is improved over its unscreened relative. Recall that good motives and ideas can lead to bad outcomes when taken to excess.

Below you’ll find the constitution of the largest ten holdings in each, the S&P 500 on the left, the screened S&P 500 ESG on the right.

| S&P 500 | S&P 500 ESG | |||||

| Name | Sector | Weight | Name | Sector | Weight | |

| Alphabet Inc. Class A | Technology | 3.24% | Alphabet Inc. Class A | Communication Services | 1.97% | |

| Amazon.com, Inc. | Consumer Non-Cyclicals | 3.35% | Alphabet Inc. Class C | Communication Services | 2.03% | |

| Apple, Inc. | Technology | 3.75% | Amazon.com, Inc. | Consumer Discretionary | 3.92% | |

| Berkshire Hathaway Inc. Class B | Finance | 1.94% | Apple, Inc. | Information Technology | 5.07% | |

| Facebook, Inc. Class A | Technology | 2.02% | Exxon Mobil Corp. | Energy | 1.61% | |

| Johnson & Johnson | Healthcare | 1.32% | Johnson & Johnson | Health Care | 1.85% | |

| JPMorgan Chase & Co. | Finance | 1.44% | JPMorgan Chase & Co. | Financials | 2.05% | |

| Microsoft Corp. | Technology | 4.03% | Microsoft Corp. | Information Technology | 5.64% | |

| Visa Inc. Class A | Finance | 1.18% | Proctor & Gamble Co. | Consumer Staples | 1.63% | |

| Walmart, Inc. | Consumer Non-Cyclicals | 1.27% | Visa, Inc. Class A | Information Technology | 1.62% | |

Eight of the largest ten holdings are identical, and because the weights in subsequent holdings tend to decline significantly in importance, having this level of overlap is no small detail. In the S&P 500, those holdings represent nearly a fifth of the overall index, a meaningful level, leaving 493 companies to duke it out for the rest. In the S&P 500 ESG, those same holdings account for nearly a fourth of the overall index, an even higher concentration. So, seven companies, or 3% of all of the holdings (the index holds 319 companies as a result of its exclusionary screens), account for one fourth of the index. Seven companies account for a quarter of the index! The ESG index may have as one of its objectives similar sector weights as the overall index—it says nothing about concentration risk, however, for obvious reasons.

Tangentially, some might also find it interesting that Exxon Mobil has found its way in the largest holdings of the ESG index. To anyone with a modicum of ESG sensibilities, energy has been front and center as a significant actor in climate change discussions. Yet, apparently, index providers and their algorithms have short memories. We are not making a judgement as to the merits or lack thereof of the energy complex. We do find it ironic, however, that a company with one of the largest carbon footprints in the world finds its way in the largest holdings of an ESG index by the most widely followed index provider.

The takeaway is that by selecting the ESG index, one gets identical holdings but with even greater concentration of returns from very few securities. At its most basic, everything about the screened index is in fact constructed in a way that should be anathema to an ESG screened benchmark.

Conclusion: if you want an S&P 500 ESG fund that is less socially IR-responsible than the S&P 500 ESG fund, you will be better served by simply buying the unscreened index. The lesson for investors concerned about ESG is to buy the regular S&P, not the one that portends to be ESG focused.

Another lesson might be to diversify away from the S&P 500 and its offshoots altogether. We’d argue that may in fact be a desirable source of risk mitigation.

Now that we have espoused the ways in which we may be different than others in our thinking of how things should be versus how they are, let us begin a discussion of how they are for us, and our shareholders. As significant owners in the fund, our interests are aligned. This year our firm is celebrating its 30th year in business. We have seen many cycles and each one is different than the other, however

BAYWOOD SOCIALLYRESPONSIBLE FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

when taken as a whole, they tend not to be that dissimilar. For example, the robust returns witnessed in 2019 are no big surprise when you consider how the year began, reeling from the declines witnessed in the fourth quarter of last year, where the average stock in the broad market was down over 16%. Most investors understand that if a stock declines 50%, it takes 100% growth just to get back to the original price. Similarly, since the average stock declined over 16% in the fourth quarter, then it would take nearly a 20% increase in the average stock to regain what it lost. We aren’t quite there yet, but the returns so far this year have driven the average stock pretty close to where it was at the beginning of the year.

We believe it’s prudent to discuss the fiscal year as a tale of two time periods. The first being the fourth quarter of 2018, the second being the calendar year of 2019. We believe the fourth quarter of 2018 was a great buying opportunity, not one to head for the exits. The fact that the Baywood SociallyResponsible strategy has outperformed its benchmark for the calendar year 2019 is testament to the will it took to buy in the face of the major declines. The companies we either initiated a position in or added to existing holdings, have returned an average of 35% this year, which is nearly double the index’s return of 18%. Companies like Disney, Aptiv, CarMax and NXP Semiconductors were initiated in the fourth quarter of 2018 while we increased our holdings in AIG, Mondelez and TRI Pointe Group. Each one of these companies outperformed the benchmark for the calendar year. The top performers in the calendar year are NXP Semiconductors, American International Group, Aptiv and Mondelez which returned 50%, 44%, 43% and 40% respectively and together represent 11% of the portfolio.

The fourth quarter of 2018 was an entirely different animal, however, and the severe declines witnessed were what provided the opportunity for better relative performance in 2019. The market reacted to an intensified trade war and interest rate volatility in somewhat of a predictable fashion (yet not entirely rational in our opinion) given the knee-jerk flight to safety and the largest capitalization companies. We have discussed, ad nauseam, the elevated valuations for bond-proxy and “defensive sectors” that run counter to each group’s collective fundamentals. Currently, in our view, utilities represent a high risk due to the market’s current view of the sector as a safe-haven asset AND a bond-proxy. Yet, we see challenged fundamentals that are likely to become more acute over the near-term. Utilities are likely to suffer as renewable portfolio standards enacted by the individual state regulatory bodies mean that a greater percentage of higher cost renewable energy sources will be forced upon rate payers. This, in turn, is likely to drive further demand for solar, and other consumer focused renewable solutions, as rate payers will continue to put up panels on their roofs to help offset the higher rates. This “spiral” will likely continue, forcing rate payers to exit the market and the burden of a higher level of fixed costs will be placed on a smaller number of rate payers. Combine this with high valuations due to the safe-haven and bond proxy status and we don’t see much of anything good in utilities right now, yet, as with any “knee-jerk reaction,” the market didn’t care for fundamentals, only what it perceived as safe.

One could easily argue the same for consumer staples, and more specifically, packaged food companies, with the exception that a large portion of the group has already had its “day of reckoning.” Up until recently ALL consumer staples enjoyed the dual “safe-haven/bond proxy” status with elevated valuations and low relative yields, until the overwhelmingly poor fundamentals of the food stocks began to be priced in. For example, Kraft-Heinz, loaded up on cheap debt for years to make acquisitions, in an attempt to mask the reality that people are no longer attracted to their products in the middle of the grocery store. As consumers gravitate towards healthier, less processed food, declining revenue problems become compounded by the high levels of debt. This finally pushed their unsustainably high valuations back down to reality, along with dividend cuts and as debt rating downgrades. We believe some utilities may see a similar correction in the not so distant future. Being underweight staples and utilities account for nearly one-third of the relative performance versus the benchmark for the fiscal year, yet we believe that maintaining our underweight in these fundamentally challenged and highly valued sectors is the prudent choice long-term.

Another issue unique to the fourth quarter of 2018 was the difference in returns between the largest, call it mega-capitalization stocks (greater than $200B), and everything else. The average stock in the broad market declined about 16% in the fourth quarter, yet mega-caps’ declines were less than 6%. This is the due to the general effect of indexation, which it is an identity of sorts that the largest companies tend to stay that way as they will become an increasingly larger percent of the indices due to their size, which continues to reinforce itself as investors blindly pour money into the indices or ETF’s that track them. That is, of course, until it doesn’t. The expectations of returns will eventually become so great that not even the best run company can deliver, as any large company knows how difficult it is to grow revenues and earnings at high rates once you achieve scale. The result is that unless an active manager “hugged” the benchmark (which by definition would make her a passive not active manager), in a reactive quarter like the fourth quarter of 2018, it would have been very difficult to outperform. This is not a new phenomenon, by the way. It is part and parcel a phenomenon of investing during ebullient times. While the hit to performance is never easy in the short-run, in the long-run our strategy has benefitted by avoiding these short-term fits and instead using the opportunity to purchase stocks at extremely depressed levels, like we did in the fourth quarter of 2018. The other two-thirds of relative performance versus the benchmark can be explained by our holdings in communications and energy, whereby the average stock’s capitalization is less than $20B. We believe our jobs as active value managers

BAYWOOD SOCIALLYRESPONSIBLE FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

SEPTEMBER 30, 2019

is not to choose when to look like the index or not, it is simply to purchase companies where the market price is substantially lower than the intrinsic value we place on a company.

This notion is best represented by examining the holdings of the Baywood SociallyResponsible fund over the last year. The changes that were made to the portfolio in this volatile one-year period are fairly stark compared to prior years. The holdings in communication services and real estate have increased more than 50% year-over-year, while our holdings in energy and health care have declined by nearly the same amount. In health care, our holdings decreased as a result of exiting and lowering our holdings in successful long-term investments Encompass Health, Royal Philips, Medtronic and Becton, Dickinson & Co. One common thread is that all of these successful investments either service or produce medical equipment for the healthcare industry. By far, majority of our holdings fall into this category as we chose to avoid headwinds facing many pharmaceutical companies, insurers, and hospitals during a time of bi-partisan support for changes to healthcare pricing. In favor of the holdings in health care and energy we have found opportunities in communications and consumer discretionary. After four years of underperformance, media companies under assault from cord cutting and streaming companies like Netflix finally arrived at valuation extremes, which allowed us to purchase the two companies best positioned to take advantage of the industry transformation. Both Disney and Comcast have massive content and distribution assets to offer exclusive viewing experiences, regardless of how its distributed. While Comcast still has its legacy cable-subscriber base in decline, it is in a much better position as both an internet and content provider than the majority of its peers. Beyond the battle for content, both are well run companies that were trading at a significant discount to their fair values due to concerns their businesses were going to be displaced by Netflix.

In consumer discretionary, we added two companies to the portfolio as of fiscal year-end which were both a result of recent spin-offs and market volatility. Aptiv, formerly known as Delphi, spun-off its powertrain business to focus on its faster growing segments aligned with the content growth in autos. As electric vehicles, hybrids, entertainment and safety features become a much larger part of the overall auto fleet, Aptiv has been capitalizing, growing its revenues well above market rates for a number of years. The content per vehicle, addressable by companies like Aptiv, for a traditional internal combustion engine is approximately $550. Compare that to the content per vehicle addressable by companies like Aptiv for an electrical vehicle of $1,100. The growth in the fleet of electric vehicles, over time, will allow companies like Aptiv to grow for an extended period of time. Furthermore, Aptiv provides autonomous content to one out of every three cars on the road. And, as more safety features tied to levels of autonomous driving like automatic emergency braking and lane assist become standard for fleets like Honda, Toyota, Ford and others, Aptiv should continue to benefit. During the fourth quarter, when stocks related to the auto industry declined on average greater than 40%, we were able to purchase this growth-like company at value-like prices.

Celebrating our 30th year in business and value investing demonstrates tenacity as we tend to lean away from popular investment trends, particularly during extremes. We’ve witnessed many such trends coming and going in and out of favor, whether it be from the perspective of investment style like value versus growth, management styles like active versus passive or from within an ESG/SRI perspective. The one common thread with most trends is that they also predominantly exhibit mean reversion. We’ve already expressed our trepidation when it comes to the trends involved with indexation. When it comes to an ESG/SRI perspective, our thought is that for too long the investment community favored profits first, everything else second. We are clearly now on a long-term trend back towards appreciation for all of a company’s constituents, including putting people and the environment back in focus. This trend should prove to be positive; we can’t say the same for the others. However, if one can glean something positive from the adoption of ESG criteria by the index providers, it could be taken as a sign of more widespread demand and acknowledgement from individual investors towards investing for a cause.

Current and future portfolio holdings are subject to change and risk.

The MSCI KLD 400 Social Index and the Morningstar Category are used to compare fund performance to its peers. It is not possible to invest directly into an index or category. Past performance is no guarantee of future results.

Risk Considerations: Mutual fund investing involves risk, including the possible loss of principal. Socially responsible investment criteria may limit the number of investment opportunities available to the Fund or it may invest a larger portion of its assets in certain sectors which could be more sensitive to market conditions, economic, regulatory and environmental developments. These factors could negatively impact the Fund’s returns. The Fund primarily invests in undervalued securities, which may not appreciate in value as anticipated by the Advisor or remain undervalued for longer than anticipated. The Fund may invest in American Depositary Receipts (ADRs), which involves risks relating to political, economic or regulatory conditions in foreign countries and may cause greater volatility and less liquidity. The Fund may also invest in convertible securities and preferred stock, which may be adversely affected as interest rates rise.

BAYWOOD SOCIALLYRESPONSIBLE FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

SEPTEMBER 30, 2019

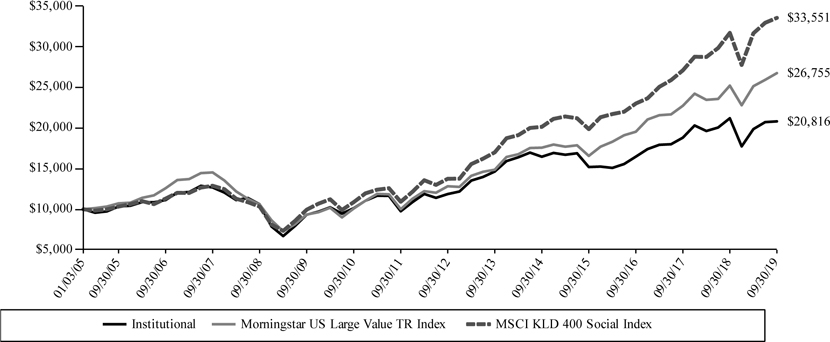

The following chart reflects the change in the value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Baywood SociallyResponsible Fund (the “Fund”) compared with the performance of the primary benchmark, Morningstar U.S. Large Value TR Index, and the secondary benchmark, MSCI KLD 400 Social Index (the “indices”), since inception. The Morningstar US Large Value TR Index measures the performance of large-cap stocks with relatively low prices given anticipated per share earnings, book value, cash flow, sales and dividends. The MSCI KLD 400 Social Index is a capitalization weighted index of 400 US securities that provides exposure to companies with outstanding Environmental, Social and Governance ratings and excludes companies whose products have negative social or environmental impacts. The total return of the indices include the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the indices do not include expenses. The Fund is professionally managed, while the indices are unmanaged and are not available for investment.

Comparison of Change in Value of a $10,000 Investment

Institutional Shares vs. Morningstar US Large Value TR Index and MSCI KLD 400 Social Index

| Average Annual Total Returns Periods Ended September 30, 2019 | One Year | Five Year | Ten Year | Since Inception 01/03/05 | ||||

| Baywood SociallyResponsible Fund* | -1.79% | 4.80% | 8.35% | 5.10% | ||||

| Morningstar US Large Value TR Index | 6.12% | 8.76% | 11.09% | 6.90% | ||||

| MSCI KLD 400 Social Index | 5.81% | 10.75% | 12.93% | 8.56% |

| * | Performance for Institutional Shares for periods prior to January 8, 2016, reflects the performance and expenses of City National Rochdale Socially Responsible Equity Fund, a series of City National Rochdale Funds (the “Predecessor Fund”). |

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating expense ratio (gross) is 3.03%. However, the Fund’s advisor has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 0.89%, through January 31, 2020 (the “Expense Cap”). The Expense Cap may be raised or eliminated only with the consent of the Board of Trustees. The advisor may be reimbursed by the Fund for fees waived and expenses reimbursed by the advisor pursuant to the Expense Cap if such payment is approved by the Board, made within three years of the fee waiver or expense reimbursement and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current Expense Cap and (ii) the Expense Cap in place at the time the fees/expenses were waived/reimbursed. Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement will increase if exclusions from the Expense Cap apply. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (855) 409-2297.

BAYWOOD SOCIALLYRESPONSIBLE FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2019

| Shares | Security Description | Value | ||||||

| Common Stock - 96.3% | ||||||||

| Basic Materials - 4.6% | ||||||||

| 1,900 | Nutrien, Ltd. | $ | 94,772 | |||||

| 300 | Packaging Corp. of America | 31,830 | ||||||

| 2,400 | The Mosaic Co. | 49,200 | ||||||

| 175,802 | ||||||||

| Capital Goods / Industrials - 4.8% | ||||||||

| 500 | Cummins, Inc. | 81,335 | ||||||

| 2,000 | Sensata Technologies Holding PLC (a) | 100,120 | ||||||

| 181,455 | ||||||||

| Communication Services - 11.0% | ||||||||

| 3,300 | CenturyLink, Inc. | 41,184 | ||||||

| 1,700 | Comcast Corp., Class A | 76,636 | ||||||

| 3,300 | Discovery, Inc., Class C (a) | 81,246 | ||||||

| 900 | The Walt Disney Co. | 117,288 | ||||||

| 1,700 | Verizon Communications, Inc. | 102,612 | ||||||

| 418,966 | ||||||||

| Consumer Discretionary - 6.4% | ||||||||

| 1,100 | Aptiv PLC | 96,162 | ||||||

| 800 | Kontoor Brands, Inc. | 28,080 | ||||||

| 8,100 | TRI Pointe Group, Inc. (a) | 121,824 | ||||||

| 246,066 | ||||||||

| Consumer Staples - 5.1% | ||||||||

| 2,000 | Mondelez International, Inc., Class A | 110,640 | ||||||

| 600 | PepsiCo., Inc. | 82,260 | ||||||

| 192,900 | ||||||||

| Energy - 3.4% | ||||||||

| 3,800 | Devon Energy Corp. | 91,428 | ||||||

| 1,100 | Schlumberger, Ltd. | 37,587 | ||||||

| 129,015 | ||||||||

| Financials - 25.1% | ||||||||

| 3,300 | Air Lease Corp. | 138,006 | ||||||

| 1,300 | American Express Co. | 153,764 | ||||||

| 2,200 | American International Group, Inc. | 122,540 | ||||||

| 3,700 | Bank of America Corp. | 107,929 | ||||||

| 1,600 | BOK Financial Corp. | 126,640 | ||||||

| 3,490 | Brookfield Asset Management, Inc., | |||||||

| Class A | 185,259 | |||||||

| 400 | M&T Bank Corp. | 63,188 | ||||||

| 2,800 | Radian Group, Inc. | 63,952 | ||||||

| 961,278 | ||||||||

| Health Care - 13.6% | ||||||||

| 1,300 | AstraZeneca PLC, ADR | 57,941 | ||||||

| 500 | Becton Dickinson and Co. | 126,480 | ||||||

| 700 | Gilead Sciences, Inc. | 44,366 | ||||||

| 2,400 | Koninklijke Philips NV, ADR | 110,712 | ||||||

| 400 | Laboratory Corp. of America Holdings (a) | 67,200 | ||||||

| 800 | Medtronic PLC | 86,896 | ||||||

| 100 | Regeneron Pharmaceuticals, Inc. (a) | 27,740 | ||||||

| 521,335 | ||||||||

| Real Estate - 5.2% | ||||||||

| 4,000 | Brookfield Property Partners LP | 81,200 | ||||||

| 6,000 | VEREIT, Inc. REIT | 58,680 | ||||||

| 2,100 | Weyerhaeuser Co. REIT | 58,170 | ||||||

| 198,050 | ||||||||

| Technology - 12.9% | ||||||||

| 2,800 | Cisco Systems, Inc. | 138,348 | ||||||

| 3,500 | Corning, Inc. | 99,820 | ||||||

| 3,400 | HP, Inc. | 64,328 | ||||||

| 1,800 | Intel Corp. | 92,754 | ||||||

| 900 | NXP Semiconductors NV | 98,208 | ||||||

| 493,458 | ||||||||

| Shares | Security Description | Value | ||||||

| Transportation - 4.2% | ||||||||

| 4,400 | AP Moller - Maersk A/S, ADR | $ | 24,728 | |||||

| 5,300 | Seaspan Corp. | 56,339 | ||||||

| 500 | Union Pacific Corp. | 80,990 | ||||||

| 162,057 | ||||||||

| Total Common Stock (Cost $2,917,721) | 3,680,382 | |||||||

| Shares | Security Description | Value | ||||||

| Money Market Fund - 3.1% | ||||||||

| 119,394 | Morgan Stanley Institutional Liquidity Funds Government Portfolio, Institutional Class, 1.85% (b) | |||||||

| (Cost $119,394) | 119,394 | |||||||

| Investments, at value - 99.4% (Cost $3,037,115) | $ | 3,799,776 | ||||||

| Other Assets & Liabilities, Net - 0.6% | 24,607 | |||||||

| Net Assets - 100.0% | $ | 3,824,383 | ||||||

| ADR | American Depositary Receipt |

| LP | Limited Partnership |

| PLC | Public Limited Company |

| REIT | Real Estate Investment Trust |

| (a) | Non-income producing security. |

| (b) | Dividend yield changes daily to reflect current market conditions. Rate was the quoted yield as of September 30, 2019. |

The following is a summary of the inputs used to value the Fund's instruments as of September 30, 2019.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

| Valuation Inputs | Investments in Securities | |||

| Level 1 - Quoted Prices | $ | 3,680,382 | ||

| Level 2 - Other Significant Observable Inputs | 119,394 | |||

| Level 3 - Significant Unobservable Inputs | – | |||

| Total | $ | 3,799,776 | ||

The Level 1 value displayed in this table is Common Stock. The Level 2 value displayed in this table is a Money Market Fund. Refer to this Schedule of Investments for a further breakout of each security by industry.

| PORTFOLIO HOLDINGS (Unaudited) | ||||

| % of Total Investments | ||||

| Basic Materials | 4.6 | % | ||

| Capital Goods / Industrials | 4.8 | % | ||

| Communication Services | 11.0 | % | ||

| Consumer Discretionary | 6.5 | % | ||

| Consumer Staples | 5.1 | % | ||

| Energy | 3.4 | % | ||

| Financials | 25.3 | % | ||

| Health Care | 13.7 | % | ||

| Real Estate | 5.2 | % | ||

| Technology | 13.0 | % | ||

| Transportation | 4.3 | % | ||

| Money Market Fund | 3.1 | % | ||

| 100.0 | % | |||

See Notes to Financial Statements.

BAYWOOD SOCIALLYRESPONSIBLE FUND

STATEMENT OF ASSETS AND LIABILITIES

SEPTEMBER 30, 2019

| ASSETS | ||||

| Investments, at value (Cost $3,037,115) | $ | 3,799,776 | ||

| Cash | 575 | |||

| Receivables: | ||||

| Fund shares sold | 1,242 | |||

| Investment securities sold | 38,457 | |||

| Dividends | 7,076 | |||

| From investment advisor | 9,515 | |||

| Prepaid expenses | 6,409 | |||

| Total Assets | 3,863,050 | |||

| LIABILITIES | ||||

| Payables: | ||||

| Fund shares redeemed | 12,753 | |||

| Accrued Liabilities: | ||||

| Fund services fees | 5,044 | |||

| Other expenses | 20,870 | |||

| Total Liabilities | 38,667 | |||

| NET ASSETS | $ | 3,824,383 | ||

| COMPONENTS OF NET ASSETS | ||||

| Paid-in capital | $ | 3,070,047 | ||

| Distributable earnings | 754,336 | |||

| NET ASSETS | $ | 3,824,383 | ||

| SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED) | ||||

| Institutional Shares | 341,013 | |||

| NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE | ||||

| Institutional Shares (based on net assets of $3,824,383) | $ | 11.21 | ||

See Notes to Financial Statements.

BAYWOOD SOCIALLYRESPONSIBLE FUND

STATEMENT OF OPERATIONS

YEAR ENDED SEPTEMBER 30, 2019

| INVESTMENT INCOME | ||||

| Dividend income (Net of foreign withholding taxes of $1,598) | $ | 92,552 | ||

| Total Investment Income | 92,552 | |||

| EXPENSES | ||||

| Investment advisor fees | 27,266 | |||

| Fund services fees | 68,582 | |||

| Transfer agent fees: | ||||

| Investor Shares | 15,150 | |||

| Institutional Shares | 18,977 | |||

| Distribution fees: | ||||

| Investor Shares | 5,107 | |||

| Custodian fees | 5,000 | |||

| Registration fees: | ||||

| Investor Shares | 18,265 | |||

| Institutional Shares | 15,131 | |||

| Professional fees | 23,187 | |||

| Trustees' fees and expenses | 2,656 | |||

| Other expenses | 21,814 | |||

| Total Expenses | 221,135 | |||

| Fees waived and expenses reimbursed | (181,188 | ) | ||

| Net Expenses | 39,947 | |||

| NET INVESTMENT INCOME | 52,605 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | ||||

| Net realized gain on investments | 102,477 | |||

| Net change in unrealized appreciation (depreciation) on investments | (260,772 | ) | ||

| NET REALIZED AND UNREALIZED LOSS | (158,295 | ) | ||

| DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (105,690 | ) | |

See Notes to Financial Statements.

BAYWOOD SOCIALLYRESPONSIBLE FUND

STATEMENTS OF CHANGES IN NET ASSETS

| For the Years Ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| OPERATIONS | ||||||||

| Net investment income | $ | 52,605 | $ | 68,010 | ||||

| Net realized gain | 102,477 | 890,310 | ||||||

| Net change in unrealized appreciation (depreciation) | (260,772 | ) | (186,732 | ) | ||||

| Increase (Decrease) in Net Assets Resulting from Operations | (105,690 | ) | 771,588 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Investor Shares | (204,892 | ) | (51,496 | )* | ||||

| Institutional Shares | (149,124 | ) | (120,653 | )** | ||||

| Total Distributions Paid | (354,016 | ) | (172,149 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Sale of shares: | ||||||||

| Investor Shares | 167,328 | 48,352 | ||||||

| Institutional Shares | 2,373,806 | 190,483 | ||||||

| Reinvestment of distributions: | ||||||||

| Investor Shares | 193,403 | 48,772 | ||||||

| Institutional Shares | 146,187 | 120,102 | ||||||

| Redemption of shares: | ||||||||

| Investor Shares | (2,701,698 | ) | (542,020 | ) | ||||

| Institutional Shares | (295,860 | ) | (4,342,445 | ) | ||||

| Decrease in Net Assets from Capital Share Transactions | (116,834 | ) | (4,476,756 | ) | ||||

| Decrease in Net Assets | (576,540 | ) | (3,877,317 | ) | ||||

| NET ASSETS | ||||||||

| Beginning of Year | 4,400,923 | 8,278,240 | ||||||

| End of Year | $ | 3,824,383 | $ | 4,400,923 | *** | |||

| SHARE TRANSACTIONS | ||||||||

| Sale of shares: | ||||||||

| Investor Shares | 14,949 | 3,910 | ||||||

| Institutional Shares | 218,445 | 15,647 | ||||||

| Reinvestment of distributions: | ||||||||

| Investor Shares | 19,029 | 4,058 | ||||||

| Institutional Shares | 14,302 | 10,021 | ||||||

| Redemption of shares: | ||||||||

| Investor Shares | (248,092 | ) | (44,965 | ) | ||||

| Institutional Shares | (26,646 | ) | (363,462 | ) | ||||

| Decrease in Shares | (8,013 | ) | (374,791 | ) | ||||

| * | Distribution was the result of net investment income and net realized gain of $14,499 and $36,997, respectively, at September 30, 2018. |

| ** | Distribution was the result of net investment income and net realized gain of $45,236 and $75,417, respectively, at September 30, 2018. |

| *** | Includes undistributed net investment income of $1,735 at September 30, 2018. The requirement to disclose the corresponding amount as of September 30, 2019 was eliminated. |

See Notes to Financial Statements.

BAYWOOD SOCIALLYRESPONSIBLE FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended September 30, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| INSTITUTIONAL SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 12.60 | $ | 11.43 | $ | 10.15 | $ | 10.18 | $ | 11.45 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.18 | 0.12 | 0.10 | 0.14 | 0.14 | |||||||||||||||

| Net realized and unrealized gain (loss) | (0.53 | ) | 1.31 | 1.33 | 0.66 | (0.99 | ) | |||||||||||||

| Total from Investment Operations | (0.35 | ) | 1.43 | 1.43 | 0.80 | (0.85 | ) | |||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||