UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-22852)

Loeb King Trust

(Exact name of registrant as specified in charter)

125 Broad Street, 14th Floor

New York, New York 10004

(Address of principal executive offices) (Zip code)

David S. Hampson

125 Broad Street, 14th Floor

New York, New York 10004

(Name and address of agent for service)

212-483-7000

Registrant’s telephone number, including area code

Date of fiscal year end: 08/31/2014

Date of reporting period: 02/28/2014

Item 1. Reports to Stockholders.

Loeb King Alternative Strategies Fund

Investor Class: LKASX

Institutional Class: LKAIX

SEMI-ANNUAL REPORT

February 28, 2014

![]()

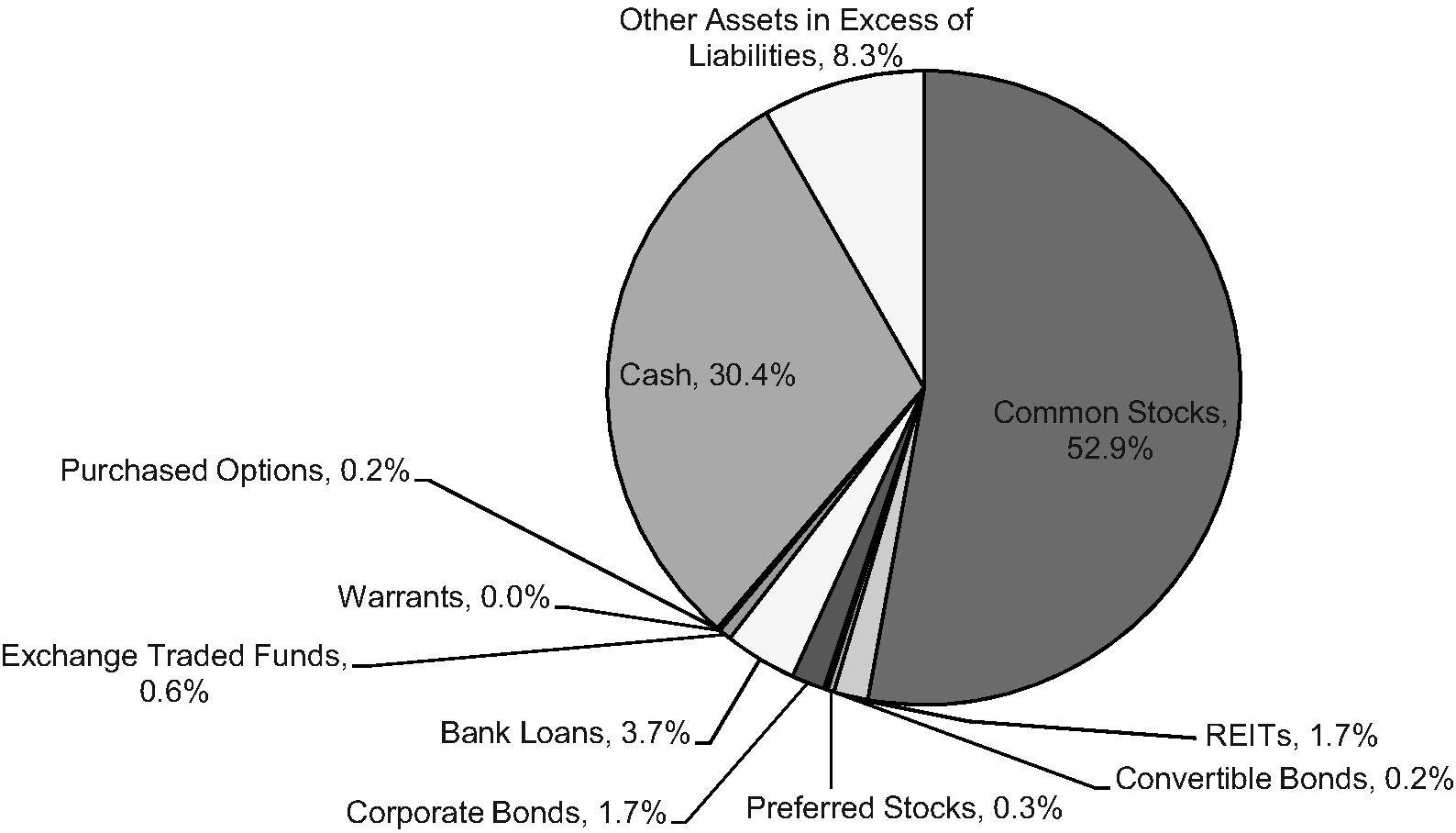

Loeb King Alternative Strategies Fund

As of February 28, 2014

Percentages represent market value of long positions as a percentage of net assets.

1

Loeb King Alternative Strategies Fund

Schedule of Investments

February 28, 2014 (Unaudited)

Shares | Fair Value | |||||

| COMMON STOCKS - 52.9% | ||||||

| Consumer Discretionary - 9.1% | ||||||

| Aarons, Inc. | 2,941 | $ | 90,377 | |||

| Beazer Homes USA, Inc. (a) | 500 | 11,595 | ||||

| Bob Evans Farms, Inc. | 674 | 34,873 | ||||

| Canadian Tire Ltd. (b) | 3 | 271 | ||||

| Charter Communications, Inc. (a) | 435 | 55,145 | ||||

| Chinaedu Corp. - ADR (a) | 53 | 363 | ||||

| Coastal Contacts, Inc. (a)(b) | 5,541 | 62,451 | ||||

| Cooper Tire & Rubber Co. | 3,680 | 91,742 | ||||

| Daimler AG (b) | 601 | 56,012 | ||||

| Darden Restaurants, Inc. | 2,194 | 112,026 | ||||

| Dish Network Corp. (a) | 1,144 | 67,313 | ||||

| Freds, Inc. | 601 | 11,978 | ||||

| General Motors Co. (a) | 1 | 36 | ||||

| The Jones Group, Inc. | 583 | 8,710 | ||||

| Jos A Bank Clothiers, Inc. (a) | 240 | 14,899 | ||||

| KB Home | 400 | 8,160 | ||||

| Lennar Corp. | 200 | 8,776 | ||||

| Longview Oil Corp. (a)(b) | 937 | 4,553 | ||||

| Loral Space & Communications, Inc. (a) | 464 | 36,665 | ||||

| Mega Brands, Inc. (a)(b) | 1,499 | 23,988 | ||||

| MGM Resorts International (a) | 490 | 13,499 | ||||

| Mood Media Corp. (a)(b) | 220 | 173 | ||||

| Morgans Hotel Group Co. (a) | 1,676 | 13,408 | ||||

| New York & Co, Inc. (a) | 9,286 | 41,137 | ||||

| Omnicom Group, Inc. | 2,788 | 210,996 | ||||

| Sirius XM Holdings, Inc. (a) | 21,882 | 78,994 | ||||

| Sizmek, Inc. (a) | 586 | 7,261 | ||||

| Sothebys | 600 | 28,206 | ||||

| TRI Pointe Homes, Inc. (a) | 2,989 | 419,506 | ||||

| Tri Pointe Homes, Inc. (a) | 1,542 | 28,095 | ||||

| Tribune Co. (a) | 704 | 55,792 | ||||

| Vitacost Com, Inc. (a) | 2,389 | 17,798 | ||||

| Total Consumer Discretionary | 1,614,798 | |||||

| Consumer Staples - 3.7% | ||||||

| B & G Foods, Inc. | 615 | 18,425 | ||||

| Beam, Inc. | 2,608 | 216,360 | ||||

| CVS Caremark Corp. | 140 | 10,240 | ||||

| Magic Holdings International (b) | 26,015 | 20,884 | ||||

| Maple Leaf Foods, Inc. (a)(b)(e) | 6,865 | 100,746 | ||||

| Reynolds American, Inc. | 909 | 46,205 | ||||

| Safeway, Inc. | 2,387 | 89,393 | ||||

| Shoppers Drug Mart Corp. (b) | 1,594 | 86,804 | ||||

| Sysco Corp. | 1,694 | 61,018 | ||||

| Total Consumer Staples | 650,075 | |||||

| Energy - 2.6% | ||||||

| Anadarko Petroluem Corp. | 1,339 | 112,690 | ||||

| Baytex Energy Corp. (a)(b) | 594 | 21,656 | ||||

Shares | Fair Value | |||||

| Energy (continued) | ||||||

| BP PLC - ADR (e) | 734 | $ | 37,148 | |||

| Equal Energy Ltd. | 17,996 | 96,099 | ||||

| Fission Uranium Corp. (a)(b) | 7,027 | 8,948 | ||||

| Goodrich Petroluem Corp. (a) | 283 | 3,854 | ||||

| Harvest Natural Resources, Inc. (a) | 6,799 | 28,556 | ||||

| Noble Corp. PLC | 1,178 | 36,577 | ||||

| Pacific Drilling S.A. (a) | 814 | 8,840 | ||||

| Syntroleum Corp. (a) | 5,048 | 20,141 | ||||

| Talisman Energy, Inc. (a)(b) | 1,903 | 19,592 | ||||

| Weatherford International Ltd. (a) | 3,668 | 61,146 | ||||

| Total Energy | 455,247 | |||||

| Financials - 7.3% | ||||||

| Aareal Bank AG (b) | 626 | 27,564 | ||||

| Ambac Financial Group, Inc. (a) | 853 | 29,480 | ||||

| Aozora Bank Ltd. (b)(e) | 45,456 | 132,210 | ||||

| BGC Partners, Inc. | 13,216 | 89,869 | ||||

| Brookfield Office Properties, Inc. | 7,974 | 152,622 | ||||

| CapitalSource, Inc. | 2,775 | 40,792 | ||||

| Chong Hing Bank Ltd. (a)(b)(f) | 2,101 | 2,908 | ||||

| Commerzbank AG (a)(b) | 7,229 | 131,113 | ||||

| Connectone Bancorp, Inc. (a) | 11 | 523 | ||||

| DIC Asset AG (b) | 6,702 | 63,238 | ||||

| Federal Home Loan Mortgage Corp. (a) | 144 | 665 | ||||

| Federal National Mortgage Association (a) | 636 | 3,053 | ||||

| First Merchants Corp. | 1,260 | 26,989 | ||||

| Home Federal Bancorp, Inc. | 6,441 | 97,195 | ||||

| Hudson City Bancorp, Inc. | 9,020 | 85,690 | ||||

| Mediobanca SPA (b) | 2,483 | 24,762 | ||||

| MPHB Capital Berhad (a)(b) | 60,220 | 34,553 | ||||

| National Interstate Corp. | 1,944 | 58,845 | ||||

| Nicholas Financial, Inc. | 908 | 14,328 | ||||

| SLM Corp. | 1,349 | 32,295 | ||||

| SWS Group, Inc. (a) | 4,626 | 37,702 | ||||

| Synovus Financial Corp. | 20,136 | 70,073 | ||||

| United Bankshares, Inc. | 2,612 | 76,871 | ||||

| Valley National Bancorp | 3,675 | 37,044 | ||||

| Washington Banking Co. | 1,071 | 19,728 | ||||

| Total Financials | 1,290,112 | |||||

| Health Care - 9.3% | ||||||

| AbbVie, Inc. | 342 | 17,411 | ||||

| Actavis PLC (a) | 49 | 10,820 | ||||

| Aetna, Inc. | 166 | 12,070 | ||||

| Alkermes PLC (a) | 152 | 7,398 | ||||

| Allergan, Inc. | 346 | 43,942 | ||||

| Amerisourcebergen Corp. | 142 | 9,635 | ||||

| Amgen, Inc. | 119 | 14,758 | ||||

| Arthrocare Corp. (a) | 2,349 | 113,339 | ||||

| Basilea Pharmaceutica AG (b) | 43 | 6,322 | ||||

The accompanying notes are an integral part of these financial statements.

2

Loeb King Alternative Strategies Fund

Schedule of Investments

February 28, 2014 (Unaudited)

Shares | Fair Value | |||||

| Health Care (continued) | ||||||

| Baxter International, Inc. | 793 | $ | 55,114 | |||

| BioDelivery Sciences International, Inc. (a) | 3,225 | 30,218 | ||||

| Biogen Idec, Inc. (a) | 33 | 11,243 | ||||

| Biomarin Pharmaceutical, Inc. (a) | 121 | 9,801 | ||||

| Bluebird Bio, Inc. (a) | 194 | 4,947 | ||||

| Bristol-Myers Squibb Co. | 306 | 16,454 | ||||

| Cadence Pharmaceuticals, Inc. (a) | 4,289 | 60,003 | ||||

| Cardinal Health, Inc. | 115 | 8,226 | ||||

| Celgene Corp. (a) | 88 | 14,146 | ||||

| Cempra, Inc. (a) | 703 | 8,007 | ||||

| Centene Corp. (a) | 168 | 10,698 | ||||

| Cerner Corp. (a) | 102 | 6,260 | ||||

| Chindex International, Inc. (a) | 313 | 6,025 | ||||

| Cigna Corp. | 142 | 11,302 | ||||

| Clovis Oncology, Inc. (a) | 47 | 3,742 | ||||

| Community Health Systems, Inc. (a) | 142 | 5,894 | ||||

| Concordia Healthcare Corp. (a)(b) | 193 | 2,775 | ||||

| Conmed Corp. | 464 | 21,632 | ||||

| Covidien PLC | 232 | 16,692 | ||||

| Cubist Pharmaceuticals, Inc. (a) | 102 | 8,111 | ||||

| Davita Healthcare Partners, Inc. (a) | 181 | 12,440 | ||||

| Durata Therapeutics, Inc. (a) | 478 | 6,553 | ||||

| Enanta Pharmaceuticals, Inc. (a) | 198 | 7,294 | ||||

| Endo Health Solutions, Inc. (a) | 440 | 35,121 | ||||

| Enteromedics, Inc. (a) | 2,078 | 5,050 | ||||

| Epizyme, Inc. (a) | 176 | 5,262 | ||||

| Express Scripts Holding Co. (a) | 219 | 16,493 | ||||

| Forest Labs, Inc. (a) | 880 | 85,862 | ||||

| Furiex Pharmaceuticals, Inc. (a) | 507 | 46,913 | ||||

| Gilead Sciences, Inc. (a) | 240 | 19,870 | ||||

| Grifols SA - ADR | 401 | 16,874 | ||||

| HCA Holdings, Inc. | 343 | 17,562 | ||||

| Heartware International, Inc. (a) | 49 | 4,706 | ||||

| Impax Laboratories, Inc. (a) | 359 | 9,251 | ||||

| Intermune, Inc. (a) | 276 | 8,291 | ||||

| Jazz Pharmaceuticals PLC (a) | 51 | 7,749 | ||||

| Lipocine, Inc. (a) | 697 | 5,576 | ||||

| Macrogenics, Inc. (a) | 133 | 4,655 | ||||

| Mckesson Corp. | 79 | 13,987 | ||||

| Medivation, Inc. (a) | 121 | 8,701 | ||||

| Medtronic, Inc. | 200 | 11,852 | ||||

| Merck & Co., Inc. | 292 | 16,641 | ||||

| Merge Healthcare, Inc. (a) | 2,442 | 6,129 | ||||

| Momenta Pharmaceuticals, Inc. (a) | 244 | 3,611 | ||||

| Morphosys (a)(b) | 105 | 9,751 | ||||

| Mylan, Inc. (a) | 167 | 9,280 | ||||

| Nektar Therapeutics (a) | 569 | 7,300 | ||||

| Novartis AG (b) | 177 | 14,782 | ||||

| Omnicare, Inc. | 191 | 11,250 | ||||

Shares | Fair Value | |||||

| Health Care (continued) | ||||||

| Ovascience, Inc. (a) | 929 | $ | 10,024 | |||

| Paladin Labs, Inc. (a)(b) | 1,410 | 180,895 | ||||

| Patheon, Inc. (a) | 916 | 8,492 | ||||

| Patheon, Inc. (a)(b) | 7,659 | 70,828 | ||||

| Patient Safety Technologies, Inc. (a) | 579 | 1,280 | ||||

| PerkinElmer, Inc. | 245 | 11,103 | ||||

| Pernix Therapeutics Holdings, Inc. (a) | 1,729 | 6,345 | ||||

| Pfizer, Inc. | 564 | 18,110 | ||||

| Portola Pharmaceuticals, Inc. (a) | 201 | 4,902 | ||||

| QLT, Inc. | 965 | 5,800 | ||||

| Receptos, Inc. (a) | 24 | 1,113 | ||||

| Regado Biosciences, Inc. (a) | 637 | 4,567 | ||||

| Regeneron Pharmaceuticals (a) | 21 | 6,983 | ||||

| Retrophin, Inc. (a) | 221 | 3,905 | ||||

| Rhoen-Klinikum AG (b) | 1,496 | 48,257 | ||||

| Roche Holdings AG (b) | 65 | 20,058 | ||||

| Synageva BioPharma Corp. (a) | 58 | 6,651 | ||||

| Team Health Holdings, Inc. (a) | 163 | 7,338 | ||||

| Teleflex, Inc. | 118 | 12,035 | ||||

| Tetraphase Pharmaceuticals, Inc. (a) | 512 | 6,963 | ||||

| Teva Pharmaceutical Industries, Ltd. - ADR (e) | 3,552 | 177,209 | ||||

| Thermo Fisher Scientific, Inc. | 66 | 8,220 | ||||

| Thoratec Corp. (a) | 258 | 9,582 | ||||

| UnitedHealth Group, Inc. | 167 | 12,904 | ||||

| Universal Health Services, Inc. | 193 | 15,494 | ||||

| VIVUS, Inc. (a) | 384 | 2,316 | ||||

| Wright Medical Group, Inc. (a) | 306 | 9,737 | ||||

| Total Health Care | 1,646,902 | |||||

| Industrials - 1.8% | ||||||

| Dover Corp. | 394 | 37,154 | ||||

| Edwards Group Ltd. - ADR (a)(f) | 3,587 | 3,659 | ||||

| Foster Wheeler AG (a)(b) | 3,545 | 113,865 | ||||

| Pacer International, Inc. (a) | 11,167 | 100,168 | ||||

| Titan Internatoinal, Inc. | 1,769 | 33,540 | ||||

| Vitran Corp, Inc. (a) | 3,685 | 23,916 | ||||

| Total Industrials | 312,302 | |||||

| Information Technology - 12.0% | ||||||

| Accelrys, Inc. (a) | 5,412 | 67,542 | ||||

| ATMI, Inc. (a) | 3,869 | 131,585 | ||||

| Autonavi Holdings Ltd. - ADR (a) | 337 | 7,013 | ||||

| Blackberry Ltd. (a) | 2,405 | 24,050 | ||||

| Blackhawk Network Holdings, Inc. (a) | 1,061 | 26,292 | ||||

| Cabot Microelectronics Corp. (a) | 1,587 | 70,098 | ||||

| Camelot Information Systems, Inc. - ADR (a) | 23,874 | 48,703 | ||||

| Compuware Corp. | 5,668 | 62,065 | ||||

| Diebold, Inc. | 1,829 | 68,386 | ||||

| Ebay, Inc. (a) | 4,257 | 250,184 | ||||

| Entropic Communications, Inc. (a) | 4,761 | 20,853 | ||||

The accompanying notes are an integral part of these financial statements.

3

Loeb King Alternative Strategies Fund

Schedule of Investments

February 28, 2014 (Unaudited)

Shares | Fair Value | |||||

| Information Technology (continued) | ||||||

| Knowles Corp. (a) | 1,720 | $ | 55,298 | |||

| LSI Corp. | 9,618 | 106,664 | ||||

| Mitel Networks Corp. (a)(b) | 6,721 | 63,734 | ||||

| Ninetowns Internet Technology Group Co., Ltd. - ADR (a) | 3,627 | 6,311 | ||||

| Nokia Corp. - ADR (a) | 31,141 | 236,049 | ||||

| Nuance Communications, Inc. (a) | 7,655 | 117,045 | ||||

| NXP Semiconductors NV (a) | 337 | 18,949 | ||||

| Pactera Technology International Ltd. - ADR (a) | 8,957 | 64,490 | ||||

| Pandora Media, Inc. (a) | 439 | 16,427 | ||||

| QLogic Corp. (a) | 3,565 | 40,712 | ||||

| Quantum Corp. (a) | 14,591 | 17,071 | ||||

| RDA Microelectronics, Inc. - ADR | 3,033 | 54,776 | ||||

| RealD, Inc. (a) | 2,358 | 26,056 | ||||

| RF Micro Devices, Inc. (a) | 2,914 | 20,631 | ||||

| Shanda Games Ltd. - ADR (a) | 3,367 | 22,289 | ||||

| Sina Corp. (a) | 600 | 40,998 | ||||

| Supertex, Inc. (a) | 2,463 | 81,107 | ||||

| Tokyo Electron Ltd. (b) | 593 | 34,041 | ||||

| Tokyo Electron Ltd. - ADR (a) | 7,938 | 113,910 | ||||

| TriQuint Semiconductor, Inc. (a) | 5,577 | 68,262 | ||||

| Trunkbow International Holdings Ltd. (a) | 14,056 | 19,819 | ||||

| Violin Memory, Inc. (a) | 4,212 | 18,322 | ||||

| Xerox Corp. | 1,542 | 16,947 | ||||

| Xyratex Ltd. | 6,019 | 79,391 | ||||

| Zynga, Inc. (a) | 4,032 | 20,402 | ||||

| Total Information Technology | 2,136,472 | |||||

| Materials - 3.4% | ||||||

| Amcol International Corp. | 1,227 | 54,454 | ||||

| Asanko Gold, Inc. (a)(b) | 2,297 | 4,978 | ||||

| Augusta Resource Corp. (a)(b) | 7,286 | 22,767 | ||||

| Barrick Gold Corp. | 782 | 15,937 | ||||

| Bayer AG (b) | 120 | 17,044 | ||||

| Brigus Gold Corp. (a)(b) | 54,601 | 62,624 | ||||

| Gold Reserve, Inc. (a) | 2,571 | 8,356 | ||||

| KWG Resources, Inc. (a)(b) | 1,355,985 | 55,106 | ||||

| LSB Industries, Inc. (a) | 715 | 23,373 | ||||

| Martin Marietta Materials, Inc. | 550 | 67,089 | ||||

| Material Sciences Corp. (a) | 2,563 | 32,576 | ||||

| Minerals Technologies, Inc. | 585 | 31,298 | ||||

| Newmont Mining Corp. | 770 | 17,910 | ||||

| Osisko Mining Corp. (a)(b) | 9,396 | 59,823 | ||||

| Solitario Exploration & Royalty Corp. (a) | 26,598 | 41,493 | ||||

| Verso Paper Corp. (a) | 612 | 1,499 | ||||

| Yongye International, Inc. (a) | 12,378 | 81,571 | ||||

| Zoltek Companies, Inc. (a) | �� | 740 | 12,395 | |||

| Total Materials | 610,293 | |||||

Shares | Fair Value | |||||

| Telecommunication Services - 3.4% | ||||||

| Fairpoint Communications, Inc. (a) | 638 | $ | 8,473 | |||

| Globalstar, Inc. (a) | 4,810 | 10,919 | ||||

| Leap Wireless International, Inc. (a) | 6,347 | 111,199 | ||||

| NTS, Inc. (a) | 16,419 | 32,674 | ||||

| Telephone & Data Systems, Inc. | 2,005 | 45,694 | ||||

| T-Mobile US, Inc. (a)(e) | 6,628 | 202,154 | ||||

| Verizon Communications, Inc. (e) | 1,536 | 73,104 | ||||

| Vodafone Group PLC - ADR (e) | 2,661 | 110,599 | ||||

| Total Telecommunication Services | 594,816 | |||||

| Utilities - 0.3% | ||||||

| China Hydroelectric Corp. - ADR (a) | 9,377 | 31,975 | ||||

| UNS Energy Corp. | 482 | 29,166 | ||||

| Total Utilities | 61,141 | |||||

| TOTAL COMMON STOCKS (Cost $9,094,534) | 9,372,158 | |||||

| REITS - 1.7% | ||||||

| American Realty Capital Properties, Inc. | 748 | 10,988 | ||||

| BRE Properties, Inc. | 1,271 | 78,510 | ||||

| Chatham Lodging Trust | 4,200 | 87,654 | ||||

| Commonwealth REIT | 1,232 | 33,449 | ||||

| Spirit Realty Capital, Inc. | 6,959 | 75,992 | ||||

| Strategic Hotels & Resorts, Inc. (a) | 981 | 9,800 | ||||

| Strategic Hotels & Resorts, Inc. - Preferred Series B | 236 | 5,891 | ||||

| Strategic Hotels & Resorts, Inc. - Preferred Series C | 243 | 6,075 | ||||

| TOTAL REITS (Cost $298,012) | 308,359 | |||||

| PREFERRED STOCKS - 0.3% | ||||||

| Financials - 0.2% | ||||||

| Ally Financial, Inc. (c) | 17 | 16,759 | ||||

| Astoria Financial Corp. | 786 | 18,620 | ||||

| Fannie Mae (a)(d) | 536 | 6,459 | ||||

| Federal Home Loan Mortgage Corp. (a)(d) | 35 | 429 | ||||

| Federal Home Loan Mortgage Corp. (a) | 105 | 1,092 | ||||

| Total Financials | 43,359 | |||||

| Telecommunication Services - 0.1% | ||||||

| Oi SA | 11,134 | 16,924 | ||||

| TOTAL PREFERRED STOCKS (Cost $59,266) | 60,283 | |||||

Principal Amount | Fair Value | |||||

| CONVERTIBLE BONDS - 0.2% | ||||||

| Information Technology - 0.2% | ||||||

| Nortel Networks Corp., 1.75%, 4/15/2014 (g) | $ | 33,000 | $ | 32,720 | ||

| TOTAL CONVERTIBLE BONDS (Cost $32,720) | 32,720 | |||||

The accompanying notes are an integral part of these financial statements.

4

Loeb King Alternative Strategies Fund

Schedule of Investments

February 28, 2014 (Unaudited)

Principal Amount | Fair Value | |||||

| CORPORATE BONDS - 1.7% | ||||||

| Consumer Discretionary - 0.3% | ||||||

| Paris Las Vegas Holding, 11.00%, 10/1/2021 (c) | $ | 36,000 | $ | 38,070 | ||

| River Cree Enterprises Ltd., 11.00%, 1/20/2021 (b)(c) | 27,000 | 25,633 | ||||

| Total Consumer Discretionary | 63,703 | |||||

| Materials - 0.2% | ||||||

| Hexion U.S. Financial Corp., 6.625%, 4/15/2020 | 30,000 | 31,012 | ||||

| Utilities - 0.1% | ||||||

| Energy Future International Holding Co., 11.00%, 10/1/2021 | 16,000 | 17,680 | ||||

| Financials - 0.8% | ||||||

| Lehman Brothers Holdings, Inc., 5.625%, 12/31/2014 (g) | 626,000 | 142,415 | ||||

| Information Technology - 0.3% | ||||||

| Avaya, Inc., 10.50%, 3/1/2021 (c) | 45,000 | 42,638 | ||||

| Northern Telecom Ltd., 6.875%, 9/1/2023 (g) | 9,000 | 4,500 | ||||

| Total Information Technology | 47,138 | |||||

| TOTAL CORPORATE BONDS (Cost $292,112) | 301,948 | |||||

| BANK LOANS - 3.7% | ||||||

| Avaya, Inc., 4.736%, 10/26/2017 (d) | 29,822 | 29,019 | ||||

| Caesars Entertainment Corp., 7.00%, 10/11/2020 (d) | 24,000 | 24,356 | ||||

| Clear Channel Communications, 6.91%, 1/30/2019 (d) | 47,750 | 46,855 | ||||

| Fairpoint Communications, Inc., 7.50%, 1/30/2019 (d) | 40,000 | 41,033 | ||||

| Harland Clarke, 6.00%, 8/17/2019 (d) | 23,000 | 23,029 | ||||

| HD Supply, Inc. 4.50%, 10/12/2017 (d) | 78,802 | 79,023 | ||||

| Kinetic Concepts, Inc., 4.00%, 5/4/2018 (d) | 19,950 | 20,009 | ||||

| Manwin Licensing International, 14.00%, 10/18/2018 (d) | 75,000 | 79,688 | ||||

| NRG Energy, Inc., 2.75%, 07/01/2018 (d) | 52,867 | 52,483 | ||||

| Reynolds Group, Inc., 4.00%, 12/1/2018 (d) | 23,000 | 23,155 | ||||

| Samson Investment, 5.00%, 9/25/2018 (d) | 29,000 | 29,225 | ||||

| Servicemaster Co., 4.42%, 01/31/2017 (d) | 27,430 | 27,457 | ||||

| TransDigm Group, Inc., 3.50%, 02/14/2017 (d) | 51,869 | 52,154 | ||||

| Travelport LLC, 9.50%, 1/31/2016 (d) | 48,000 | 49,740 | ||||

| Valeant Pharmaceuticals International, Inc., 3.75%, 02/13/2019 (d) | 78,000 | 78,207 | ||||

| TOTAL BANK LOANS (Cost $650,485) | 655,433 | |||||

Shares | Fair Value | |||||

| EXCHANGE TRADED FUNDS - 0.6% | ||||||

| ProShares Short 20+Year Treasury (a) | 1,625 | $ | 49,790 | |||

| SPDR Gold Shares (a) | 500 | 63,810 | ||||

| TOTAL EXCHANGE TRADED FUNDS (Cost $116,249) | 113,600 | |||||

| WARRANTS - 0.0% | ||||||

| General Motors Co. | ||||||

| Expiration July 2016, Exercise Price: $10.00 (a) | 1 | 27 | ||||

| Expiration July 2019, Exercise Price: $18.33 (a) | 1 | 18 | ||||

| TOTAL WARRANTS (Cost $53) | 45 | |||||

Contracts | Fair Value | |||||

| PURCHASED OPTIONS - 0.2% | ||||||

| Call Options - 0.1% | ||||||

| BGC Partners, Inc. | ||||||

| Expiration: May 2014, Exercise Price: $7.50 | 3 | $ | 30 | |||

| Cablevision Systems Corp. | ||||||

| Expiration: March 2014, Exercise Price: $20.00 | 4 | 20 | ||||

| Charter Communications, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $130.00 | 2 | 380 | ||||

| Nuance Communications, Inc. | ||||||

| Expiration: July 2014, Exercise Price: $17.00 | 30 | 2,250 | ||||

| ProShares UltraPro Short S&P 500 | ||||||

| Expiration: March 2014, Exercise Price: $1,830.00 | 2 | 7,780 | ||||

| SPDR S&P 500 | ||||||

| Expiration: March 2014, Exercise Price: $186.00 | 1 | 222 | ||||

| Expiration: March 2014, Exercise Price: $187.00 | 1 | 162 | ||||

10,844 | ||||||

| Put Options - 0.1% | ||||||

| Beazer Homes USA, Inc. | ||||||

| Expiration: April 2014, Exercise Price: $22.00 | 5 | 365 | ||||

| eBay, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $52.50 | 18 | 108 | ||||

| Expiration: March 2014, Exercise Price: $55.00 | 6 | 138 | ||||

| iShares iBoxx $ High Yield Corporate Bond | ||||||

| Expiration: March 2014, Exercise Price: $91.00 | 4 | 0 | ||||

The accompanying notes are an integral part of these financial statements.

5

Loeb King Alternative Strategies Fund

Schedule of Investments

February 28, 2014 (Unaudited)

Contracts | Fair Value | |||||

| Put Options (continued) | ||||||

| Expiration: March 2014, Exercise Price: $92.00 | 5 | $ | 50 | |||

| iShares Russell 2000 | ||||||

| Expiration: March 2014, Exercise Price: $117.00 | 5 | 870 | ||||

| Expiration: April 2014, Exercise Price: $117.00 | 16 | 4,464 | ||||

| Expiration: April 2014, Exercise Price: $118.00 | 2 | 654 | ||||

| KB Home | ||||||

| Expiration: April 2014, Exercise Price: $19.00 | 4 | 220 | ||||

| Nokia Corp. | ||||||

| Expiration: March 2014, Exercise Price: $7.00 | 30 | 270 | ||||

| Expiration: April 2014, Exercise Price: $6.00 | 74 | 370 | ||||

| Expiration: April 2014, | ||||||

| Exercise Price: $7.00 | 149 | 2980 | ||||

| Nuance Communications, Inc. | ||||||

| Expiration: April 2014, | ||||||

| Exercise Price: $14.00 | 7 | 175 | ||||

| SPDR Gold Shares | ||||||

| Expiration: April 2014, Exercise Price: $126.00 | 5 | 960 | ||||

| SPDR S&P 500 | ||||||

| Expiration: March 2014, Exercise Price: $181.00 | 1 | 78 | ||||

Contracts | Fair Value | |||||

| Put Options (continued) | ||||||

| Expiration: March 2014, Exercise Price: $182.00 | 1 | $ | 98 | |||

| Expiration: March 2014, Exercise Price: $183.00 | 4 | 476 | ||||

| Expiration: March 2014, Exercise Price: $184.00 | 2 | 282 | ||||

| Expiration: April 2014, Exercise Price: $185.00 | 22 | 6,380 | ||||

| T-Mobile US, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $28.00 | 14 | 938 | ||||

| Expiration: April 2014, Exercise Price: $30.00 | 6 | 1,134 | ||||

| Total Put Options | 21,010 | |||||

| TOTAL PURCHASED OPTIONS (Cost $38,263) | 31,854 | |||||

| Total Investments (Cost $10,581,694) - 61.3% | $ | 10,876,400 | ||||

| Cash (e) - 30.4% | 5,404,778 | |||||

| Other Assets in Excess of Liabilities - 8.3% | 1,473,478 | |||||

| TOTAL NET ASSETS - 100.0% | $ | 17,754,656 | ||||

Percentages are stated as a percent of net assets.

ADR American Depository Receipt

| (a) | Non-income producing. |

| (b) | Foreign issued security. |

| (c) | Restricted security as defined in Rule 144(a) under the Securities Act of 1933. Purchased in private placement transaction; resale to the public may require registration or may extend only to qualified institutional buyers. At February 28, 2014, the market value of these securities total $34,690 which represents 0.2% of total net assets. |

| (d) | Variable Rate Security. The rate shown represents the rate at February 28, 2014. |

| (e) | All or a portion of the security has been pledged in connection with open short securities and written options contracts. |

| (f) | Securities for which market quotations are not readily available are valued at fair value determined by the Adviser. Such values are approved on a quarterly basis by the Board of Trustees. The total fair value of such securities at February 28, 2014 is $6,567, which represents 0.04% of total net assets. |

| (g) | Represents a security in default. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

6

Loeb King Alternative Strategies Fund

Schedule of Securities Sold Short

February 28, 2014 (Unaudited)

Shares | Fair Value | |||||

| COMMON STOCKS - 9.0% | ||||||

| Consumer Discretionary - 1.6% | ||||||

| Amazon Com, Inc. (b) | 47 | $ | 17,019 | |||

| Best Buy, Inc. | 237 | 6,311 | ||||

| Comcast Corp. | 120 | 6,203 | ||||

| Hyatt Hotels Corp. (b) | 103 | 5,372 | ||||

| Las Vegas Sands Corp. | 40 | 3,410 | ||||

| Liberty Global PLC (b) | 922 | 79,799 | ||||

| Liberty Global PLC (b) | 727 | 61,548 | ||||

| Liberty Media Corp. (b) | 371 | 50,886 | ||||

| Marriott International, Inc. | 108 | 5,857 | ||||

| Rent-A-Center, Inc. | 702 | 17,648 | ||||

| Sinclair Broadcast Group, Inc. | 230 | 6,813 | ||||

| Starwood Hotels & Resorts Worldwide, Inc. | 68 | 5,607 | ||||

| Ulta Salon, Cosmetics & Fragrance, Inc. (b) | 79 | 7,086 | ||||

| Wyndham Worldwide Corp. | 72 | 5,247 | ||||

278,806 | ||||||

| Consumer Staples - 0.5% | ||||||

| Lorillard, Inc. | 925 | 45,381 | ||||

| George Weston Ltd (a)(b) | 511 | 37,112 | ||||

82,493 | ||||||

| Energy - 0.2% | ||||||

| Apache Corp. | 77 | 6,105 | ||||

| Cameco Corp. (a)(b) | 117 | 2,833 | ||||

| Noble Energy, Inc. | 194 | 13,339 | ||||

| Renewable Energy Group, Inc. (b) | 1,625 | 18,964 | ||||

41,241 | ||||||

| Financials - 1.6% | ||||||

| Assured Guaranty Ltd. | 195 | 4,787 | ||||

| Cascade Bancorp (b) | 4,456 | 21,745 | ||||

| Center Bancorp, Inc. | 35 | 651 | ||||

| First Merchants Corp. | 1,260 | 26,989 | ||||

| Heritage Financial Corp. | 953 | 16,897 | ||||

| M & T Bank Corp. | 758 | 88,375 | ||||

| MBIA, Inc. (a) | 494 | 6,694 | ||||

| PacWest Bancorp | 787 | 34,156 | ||||

| Prospect Capital Corp. Com | 317 | 3,500 | ||||

| United Bankshares, Inc. | 2,613 | 76,901 | ||||

280,695 | ||||||

| Health Care - 1.7% | ||||||

| Acorda Therapeutics, Inc. (b) | 51 | 1,869 | ||||

| Actavis PLC (b) | 229 | 50,568 | ||||

| Ampio Pharmaceuticals, Inc. (b) | 364 | 2,592 | ||||

| Aratana Therapeutics, Inc. (b) | 121 | 2,828 | ||||

| Cepheid (b) | 100 | 5,366 | ||||

| Endo Health Solutions, Inc. (b) | 2,302 | 183,745 | ||||

| Haemonetics Corp. (b) | 91 | 3,320 | ||||

| Insys Therapeutics, Inc. (b) | 61 | 4,104 | ||||

Shares | Fair Value | |||||

| Health Care (continued) | ||||||

| Intercept Pharmaceuticals, Inc. (b) | 28 | $ | 11,494 | |||

| Invacare Corp. | 275 | 5,450 | ||||

| Mednax, Inc. (b) | 62 | 3,771 | ||||

| MiMedx Group, Inc. (b) | 485 | 3,468 | ||||

| Osiris Therapeutics, Inc. (b) | 243 | 3,710 | ||||

| Raptor Pharmaceutical Corp. (b) | 355 | 5,620 | ||||

| Sangamo Biosciences, Inc. (b) | 146 | 2,657 | ||||

| Stemline Therapeutics, Inc. (b) | 97 | 2,508 | ||||

| Team Health Holdings, Inc. (b) | 134 | 6,033 | ||||

299,103 | ||||||

| Industrials - 0.1% | ||||||

| XPO Logistics, Inc. (b) | 194 | 6,099 | ||||

| Information Technology - 1.8% | ||||||

| Apple, Inc. | 48 | 25,259 | ||||

| Applied Materials, Inc. | 9,305 | 176,423 | ||||

| Linkedin Corp. (b) | 46 | 9,386 | ||||

| Mitel Networks Corp. (b) | 6,722 | 63,859 | ||||

| Qualcomm, Inc. | 241 | 18,145 | ||||

| Riverbed Technology, Inc. (b) | 364 | 8,110 | ||||

| Sierra Wireless, Inc. (b) | 1,087 | 22,240 | ||||

323,422 | ||||||

| Materials - 0.9% | ||||||

| Asanko Gold, Inc. (a)(b) | 2,297 | 4,979 | ||||

| Primero Mining Corp. (a)(b) | 9,555 | 61,957 | ||||

| Goldcorp, Inc. | 862 | 23,214 | ||||

| Texas Industries, Inc. (b) | 890 | 75,561 | ||||

165,711 | ||||||

| Telecommunication Services - 0.6% | ||||||

| Verizon Communications, Inc. | 2,374 | 112,955 | ||||

| TOTAL COMMON STOCKS (Proceeds $1,520,427) | 1,590,525 | |||||

Principal Value | Fair Value | |||||

| CORPORATE BONDS - 2.0% | ||||||

| Consumer Discretionary - 0.1% | ||||||

| Servicemaster Co., 7.00%, 8/15/2020 | 20,000 | 20,750 | ||||

| Consumer Staples - 0.1% | ||||||

| Constellation Brands, Inc., 4.25%, 5/1/2023 | 17,000 | 16,660 | ||||

| Health Care - 0.7% | ||||||

| Kinetic Concepts, Inc., 10.50%, 11/1/2018 | 26,000 | 30,063 | ||||

| Valeant Pharmaceuticals International, Inc. | ||||||

| 6.750%, 8/15/2018 (c) | 44,000 | 48,510 | ||||

| 7.500%, 7/15/2021 (c) | 35,000 | 39,900 | ||||

88,410 | ||||||

118,473 | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

7

Loeb King Alternative Strategies Fund

Schedule of Securities Sold Short

February 28, 2014 (Unaudited)

Principal Value | Fair Value | |||||

| Information Technology - 0.0% | ||||||

| Ipayment, Inc., 10.250%, 5/15/2018 | 9,000 | $ | 7,020 | |||

| Industrials - 0.5% | ||||||

| HD Supply Holdings, Inc., 7.50%, 7/15/2020 | 51,000 | 55,845 | ||||

| Transdigm, Inc., 7.50%, 7/15/2021 | 34,000 | 37,485 | ||||

93,330 | ||||||

| Materials - 0.2% | ||||||

| Hexion U.S. Financial Corp. | ||||||

| 9.00%, 11/15/2020 | 10,000 | 10,275 | ||||

| 8.875%, 2/1/2018 | 20,000 | 20,850 | ||||

31,125 | ||||||

| Telecommunication Services - 0.2% | ||||||

| Verizon Communications, Inc., 6.55%, 9/15/2043 | 24,000 | 29,380 | ||||

| Utilities - 0.2% | ||||||

| NRG Energy, Inc., 7.875%, 5/15/2021 | 32,000 | 35,520 | ||||

| TOTAL CORPORATE BONDS (Proceeds $343,345) | 352,258 | |||||

Shares | Fair Value | |||||

| EXCHANGE TRADED FUNDS - 10.7% | ||||||

| First Trust ISE-Revere Natural Gas Index Fund | 767 | 15,217 | ||||

| iShares China Large-Cap ETF | 213 | 7,538 | ||||

| iShares iBoxx $ High Yield Corporate Bond ETF | 702 | 66,641 | ||||

| iShares MSCI Germany Index | 1,616 | 51,243 | ||||

| iShares MSCI Malaysia Index | 784 | 12,019 | ||||

| iShares MSCI United Kingdom Index | 5,068 | 107,746 | ||||

Shares | Fair Value | |||||

| EXCHANGE TRADED FUNDS (continued) | ||||||

| iShares Nasdaq Biotechnology ETF | 17 | $ | 4,495 | |||

| iShares Russell 2000 Index ETF | 1,840 | 216,237 | ||||

| iShares U.S. Real Estate ETF | 178 | 12,166 | ||||

| Market Vectors Oil Services ETF | 1,343 | 65,565 | ||||

| Market Vectors Semiconductor ETF | 414 | 18,071 | ||||

| Nomura Tokyo Price Index ETF (a) | 3,367 | 40,826 | ||||

| PowerShares QQQQ Trust, Series 1 | 872 | 78,777 | ||||

| SPDR Health Care Select Fund | 664 | 39,468 | ||||

| SPDR Energy Select Sector Fund | 299 | 26,207 | ||||

| SPDR Financial Select Sector Fund | 1,406 | 30,510 | ||||

| SPDR Barclays High Yield Bond ETF | 432 | 17,941 | ||||

| SPDR S&P 500 ETF | 3,368 | 627,459 | ||||

| SPDR S&P Biotech ETF | 804 | 131,631 | ||||

| SPDR S&P Oil & Gas Exploration & Production ETF | 1,130 | 78,750 | ||||

| SPDR S&P Regional Banking ETF | 2,260 | 90,151 | ||||

| Vanguard REIT Index ETF | 2,081 | 147,231 | ||||

| WisdomTree Japan Hedged Equity Fund | 316 | 15,076 | ||||

| TOTAL EXCHANGE TRADED FUNDS (Proceeds $1,843,126) | 1,900,965 | |||||

| REITS - 0.4% | ||||||

| American Capital Agency Corp. | 133 | 2,965 | ||||

| Essex Property Trust, Inc. | 378 | 63,220 | ||||

| Host Hotels & Resorts, Inc. | 267 | 5,252 | ||||

| TOTAL REITS (Proceeds $64,970) | 71,437 | |||||

| Total Securities Sold Short (Proceeds $3,771,868) | $ | 3,915,185 | ||||

Percentages are stated as a percent of net assets.

As of February 28, 2014, securities and cash collateral of $6,157,010 has been pledged in connection with open short securities and written options contracts.

| (a) | Foreign issued security. |

| (b) | Non-income producing. |

| (c) | Restricted security as defined in Rule 144(a) under the Securities Act of 1933. Purchased in private placement transaction; resale to the public may require registration or may extend only to qualified institutional buyers. At February 28, 2014, the market value of these securities total $34,690 which represents 0.2% of total net assets. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these consolidated financial statements.

8

Loeb King Alternative Strategies Fund

Schedule of Options Written

February 28, 2014 (Unaudited)

Number of Contracts | Fair Value | |||||

| CALL OPTIONS | ||||||

| ArthroCare Corp. | ||||||

| Expiration: March 2014, Exercise Price: $50.00 | 2 | $ | 50 | |||

| Beazer Homes USA, Inc. | ||||||

| Expiration: April 2014, Exercise Price: $23.00 | 5 | 750 | ||||

| BioDelivery Sciences International, Inc. | ||||||

| Expiration: April 2014, Exercise Price: $10.00 | 6 | 462 | ||||

| Christopher & Banks Corp. | ||||||

| Expiration: April 2014, Exercise Price: $13.00 | 6 | 521 | ||||

| Charter Communications, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $120.00 | 2 | 1,560 | ||||

| Compuware Corp. | ||||||

| Expiration: May 2014, Exercise Price: $11.00 | 12 | 660 | ||||

| Cooper Tire & Rubber Co. | ||||||

| Expiration: March 2014, Exercise Price: $22.00 | 7 | 2,310 | ||||

| Expiration: March 2014, Exercise Price: $23.00 | 8 | 1,776 | ||||

| Expiration: March 2014, Exercise Price: $24.00 | 11 | 1,540 | ||||

| Expiration: April 2014, Exercise Price: $23.00 | 5 | 1,300 | ||||

| Darden Restaurants, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $49.00 | 8 | 1,624 | ||||

| Dish Network Corp. | ||||||

| Expiration: March 2014, Exercise Price: $55.00 | 5 | 2,050 | ||||

| Dover Corp. | ||||||

| Expiration: March 2014, Exercise Price: $85.00 | 3 | 2,700 | ||||

| eBay, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $55.00 | 6 | 2,490 | ||||

| Expiration: March 2014, Exercise Price: $57.50 | 18 | 3,960 | ||||

| Expiration: March 2014, Exercise Price: $60.00 | 6 | 570 | ||||

| Endo International PLC | ||||||

| Expiration: April 2014, Exercise Price: $75.00 | 2 | 1,520 | ||||

| Harvest Natural Resources, Inc. | ||||||

| Expiration: June 2014, Exercise Price: $5.00 | 7 | 315 | ||||

| KB Home | ||||||

| Expiration: April 2014, Exercise Price: $20.00 | 4 | 560 | ||||

| Lennar Corp. | ||||||

| Expiration: April 2014, Exercise Price: $40.00 | 2 | 890 | ||||

| Nokia Corp. | ||||||

| Expiration: April 2014, Exercise Price: $8.00 | 164 | 4,592 | ||||

Number of Contracts | Fair Value | |||||

| Nuance Communications, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $15.00 | 8 | $ | 424 | |||

| Expiration: April 2014, Exercise Price: $15.00 | 7 | 665 | ||||

| Expiration: July 2014, Exercise Price: $20.00 | 30 | 750 | ||||

| NXP Semiconductors NV | ||||||

| Expiration: March 2014, Exercise Price: $50.00 | 2 | 1,380 | ||||

| Pandora Media, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $37.00 | 2 | 408 | ||||

| ProShares UltraPro Short S&P 500 | ||||||

| Expiration: March 2014, Exercise Price: $1,820.00 | 2 | 9,820 | ||||

| Safeway, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $38.00 | 6 | 720 | ||||

| Expiration: March 2014, Exercise Price: $39.00 | 12 | 1,080 | ||||

| SINA Corp. | ||||||

| Expiration: March 2014, Exercise Price: $70.00 | 6 | 1,158 | ||||

| Sotheby's | ||||||

| Expiration: March 2014, Exercise Price: $47.00 | 6 | 804 | ||||

| SPDR Gold Shares | ||||||

| Expiration: April 2014, Exercise Price: $128.00 | 5 | 1,215 | ||||

| SPDR S&P 500 | ||||||

| Expiration: March 2014, Exercise Price: $184.00 | 1 | 365 | ||||

| Expiration: March 2014, Exercise Price: $185.00 | 4 | 1,148 | ||||

| Teva Pharmaceutical Industries Ltd. | ||||||

| Expiration: March 2014, Exercise Price: $44.00 | 12 | 7,380 | ||||

| Expiration: March 2014, Exercise Price: $46.00 | 5 | 2,125 | ||||

| Time Warner Cable, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $135.00 | 1 | 670 | ||||

| Expiration: April 2014, Exercise Price: $135.00 | 2 | 1,628 | ||||

| T-Mobile US, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $29.00 | 6 | 1,512 | ||||

| Expiration: March 2014, Exercise Price: $30.00 | 14 | 2,758 | ||||

| Expiration: April 2014, Exercise Price: $33.00 | 6 | 690 | ||||

| Expiration: May 2014, Exercise Price: $36.00 | 4 | 312 | ||||

| XPO Logistics, Inc. | ||||||

| Expiration: March 2014, Exercise Price: $25.00 | 1 | 670 | ||||

| Expiration: March 2014, Exercise Price: $30.00 | 1 | 205 | ||||

| Total Options Written (Premiums received $42,921) | $ | 70,087 | ||||

As of February 28, 2014, securities and cash collateral of $6,157,010 has been pledged in connection with open short securities and written options contracts.

The accompanying notes are an integral part of these consolidated financial statements.

9

Loeb King Alternative Strategies Fund

Schedule of Total Return Swaps

February 28, 2014 (Unaudited)

Reference Entity | Counterparty | Termination Date | Interest Rate Receive/(Pay) (a) | Number of Contracts Long/(Short) | Notional Amount (b) | Unrealized Appreciation/ (Depreciation) | ||||||

| Abcam PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 1,204 | $ | 9,924 | $ | 18 | ||||

| Ablynx NV | JP Morgan Chase | 7/31/2014 | (0.72)% | 311 | 4,151 | 327 | ||||||

| Active Biotech AB | JP Morgan Chase | 7/31/2014 | (1.47)% | 708 | 4,362 | 361 | ||||||

| Airbus Group NV | JP Morgan Chase | 7/31/2014 | (0.72)% | 319 | 23,508 | 468 | ||||||

| Algeta ASA | JP Morgan Chase | 7/31/2014 | (2.22)% | 3,115 | 185,281 | 685 | ||||||

| Almirall SA | JP Morgan Chase | 7/31/2014 | (0.72)% | 807 | 14,191 | 354 | ||||||

| AMEC PLC | JP Morgan Chase | 1/23/2015 | (0.06)% | (3,190 | ) | (59,988 | ) | (3,639 | ) | |||

| Assicurazioni Generali SPA | JP Morgan Chase | 7/31/2014 | 0.41% | (1,889 | ) | (42,474 | ) | 147 | ||||

| Aurora Oil & Gas Ltd. | JP Morgan Chase | 2/17/2015 | (3.11)% | 7,119 | 26,554 | 277 | ||||||

| AZ Electronic Materials SA | JP Morgan Chase | 1/23/2015 | (1.08)% | 18,306 | 122,432 | 910 | ||||||

| C&C Group PLC | JP Morgan Chase | 7/31/2014 | (0.85)% | 7,127 | 48,272 | 1,996 | ||||||

| Caisse Regionale Credit Agricole Mutuel d'Ille et Vilaine | JP Morgan Chase | 7/31/2014 | (0.72)% | 117 | 9,108 | 98 | ||||||

| Caisse Regionale de Credit Agricole Mutuel Alpes Provence | JP Morgan Chase | 7/31/2014 | (0.72)% | 67 | 6,528 | 62 | ||||||

| Cellectis | JP Morgan Chase | 7/31/2014 | (0.72)% | 844 | 5,615 | (17 | ) | |||||

| Coloplast AS | JP Morgan Chase | 7/31/2014 | (0.68)% | 78 | 6,570 | 351 | ||||||

| Credit Agricole Atlantique Vendee-CCI | JP Morgan Chase | 7/31/2014 | (0.72)% | 112 | 14,683 | 373 | ||||||

| Credit Agricole de la Touraine et du Poitou | JP Morgan Chase | 7/31/2014 | (0.72)% | 86 | 7,710 | 195 | ||||||

| Credit Agricole de Normandie-Seine | JP Morgan Chase | 7/31/2014 | (0.72)% | 176 | 26,514 | 607 | ||||||

| Credit Agricole Loire Haute-Loire | JP Morgan Chase | 7/31/2014 | (0.72)% | 60 | 4,783 | 18 | ||||||

| Credit Agricole Nord de France CCI | JP Morgan Chase | 7/31/2014 | (0.72)% | 567 | 12,624 | 417 | ||||||

| Deutsche Wohnen AG-BR | JP Morgan Chase | 7/31/2014 | (0.72)% | (2,009 | ) | (42,566 | ) | (3,714 | ) | |||

| Deutsche Wohnen AG NPV Young | JP Morgan Chase | 7/31/2014 | 0.41% | 2,369 | 48,738 | 1,089 | ||||||

| Dixons Retail PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 14,093 | 12,130 | 240 | ||||||

| Ericsson | JP Morgan Chase | 7/31/2014 | (0.25)% | (1,235 | ) | (16,007 | ) | (1,088 | ) | |||

| F&C Asset Management PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 10,807 | 22,892 | 327 | ||||||

| Genfit | JP Morgan Chase | 7/31/2014 | (0.72)% | 1,007 | 41,907 | 4,053 | ||||||

| Genmab A/S | JP Morgan Chase | 7/31/2014 | (0.68)% | 153 | 6,911 | 97 | ||||||

| GlaxoSmithKline PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 323 | 9,041 | (11 | ) | |||||

| Innate Pharma SA | JP Morgan Chase | 7/31/2014 | (0.72)% | 590 | 8,551 | (155 | ) | |||||

| iShares FTSE 100 UCITS ETF | JP Morgan Chase | 1/23/2015 | 0.84% | (1,033 | ) | (11,719 | ) | 33 | ||||

| Ipsen SA | JP Morgan Chase | 7/31/2014 | (0.72)% | 166 | 7,134 | 81 | ||||||

| Lyxor STOXX Europe 600 Banks ETF | JP Morgan Chase | 7/31/2014 | 2.46% | (4,041 | ) | (121,931 | ) | (3,017 | ) | |||

| Lyxor CAC 40 ETF | JP Morgan Chase | 7/31/2014 | 1.41% | (603 | ) | (36,514 | ) | (1,262 | ) | |||

| Mediobanca SPA | JP Morgan Chase | 7/31/2014 | (0.72)% | 4,373 | 43,611 | 520 | ||||||

| Medivir AB | JP Morgan Chase | 7/31/2014 | (1.47)% | 370 | 6,608 | 1,097 | ||||||

| Publicis Groupe | JP Morgan Chase | 7/31/2014 | 0.41% | (2,269 | ) | (215,475 | ) | (7,962 | ) | |||

| Rautaruukki Oyj | JP Morgan Chase | 7/31/2014 | (0.72)% | 3,523 | 41,285 | 156 | ||||||

| Sanofi | JP Morgan Chase | 7/31/2014 | (0.72)% | 98 | 10,190 | 284 | ||||||

| Scania AB | JP Morgan Chase | 7/31/2014 | (1.47)% | 2,356 | 72,389 | 1,664 | ||||||

| Shire PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 335 | 18,624 | 58 | ||||||

| SSAB AB-A | JP Morgan Chase | 7/31/2014 | 2.46% | (1,674 | ) | (13,211 | ) | (97 | ) | |||

| SSAB AB-B | JP Morgan Chase | 7/31/2014 | 8.16% | (4,275 | ) | (30,104 | ) | (345 | ) | |||

| Swedish Orphan Biovitrum AB | JP Morgan Chase | 7/31/2014 | (1.47)% | 458 | 6,072 | 180 | ||||||

| Telecom Italia SPA | JP Morgan Chase | 7/31/2014 | 0.41% | (39,341 | ) | (44,718 | ) | (590 | ) | |||

| Telecom Italia SPA-RSP | JP Morgan Chase | 7/31/2014 | (0.72)% | 47,616 | 41,735 | (2,357 | ) | |||||

| Telekom Austria AG | JP Morgan Chase | 7/31/2014 | 0.00% | 1,681 | 16,370 | (344 | ) | |||||

| Transgene SA | JP Morgan Chase | 7/31/2014 | 0.00% | 206 | 3,672 | – | ||||||

| Unit4 NV | JP Morgan Chase | 7/31/2014 | (0.72)% | 2,909 | 155,010 | 140 | ||||||

| Vectura Group PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 4,419 | 11,988 | (457 | ) | |||||

The accompanying notes are an integral part of these consolidated financial statements.

10

Loeb King Alternative Strategies Fund

Schedule of Total Return Swaps

February 28, 2014 (Unaudited)

Reference Entity | Counterparty | Termination Date | Interest Rate Receive/(Pay) (a) | Number of Contracts Long/(Short) | Notional Amount (b) | Unrealized Appreciation/ (Depreciation) | ||||||

| Verizon Communications Inc. | JP Morgan Chase | 1/23/2015 | (0.42)% | 742 | $ | 35,202 | $ | 232 | ||||

| Vodafone Group PLC | JP Morgan Chase | 1/23/2015 | (1.08)% | 14,386 | 59,984 | 1,842 | ||||||

| Ziggo NV | JP Morgan Chase | 7/31/2014 | (0.68)% | 4,435 | 202,932 | (1,861 | ) | |||||

$ | (7,159 | ) | ||||||||||

| (a) | The interest rate represents the average financing rate as of February 28, 2014. |

| (b) | Notional value represents the market value (including any fees or commissions) of the long and short positions when they are established. |

The accompanying notes are an integral part of these consolidated financial statements.

11

Loeb King Alternative Strategies Fund

Statement of Assets & Liabilities

February 28, 2014 (Unaudited)

| ASSETS | |||

| Investments, at value (cost $10,581,694) | $ | 10,876,400 | |

| Cash | 5,404,778 | ||

| Foreign Currency, at value (cost $265,044) | 265,669 | ||

| Receivables: | |||

| Swap contracts dividends and interest | 17,396 | ||

| Unrealized appreciation on open swap contracts | 19,756 | ||

| Investments sold | 926,347 | ||

| Fund shares sold | 50,000 | ||

| Dividends and interest | 63,720 | ||

| Deposits at brokers for securities sold short | 4,967,116 | ||

| Deposits at brokers for open swap contracts | 680,000 | ||

| Deferred offering costs | 9,580 | ||

| Prepaid expenses | 38,117 | ||

| Due from Adviser | 30,057 | ||

| TOTAL ASSETS | 23,348,936 | ||

| LIABILITIES | |||

| Written options, at value (premiums received $42,921) | 70,087 | ||

| Short securities, at value (proceeds received $3,771,868) | 3,915,185 | ||

| Payables: | |||

| Investments purchased | 1,517,374 | ||

| To distributor | 2,198 | ||

| To custodian | 17,893 | ||

| Dividends and interest on short positions | 6,785 | ||

| Swap contracts dividends and interest | 49 | ||

| Unrealized depreciation on open swap contracts | 26,915 | ||

| Accrued expenses and other liabilities | 37,794 | ||

| TOTAL LIABILITIES | 5,594,280 | ||

| NET ASSETS | $ | 17,754,656 | |

| Net assets consist of: | |||

| Paid-in capital | 17,683,124 | ||

| Accumulated net investment loss | (79,806 | ) | |

| Accumulated net realized gain | 11,919 | ||

| Net unrealized appreciation (depreciation) on: | |||

| Investments | 323,470 | ||

| Swap contracts | (7,159 | ) | |

| Securities sold short | (143,317 | ) | |

| Purchased options | (6,409 | ) | |

| Written options | (27,166 | ) | |

| NET ASSETS | $ | 17,754,656 | |

| Investor Class | |||

| Net assets | $ | 3,458,794 | |

| Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 345,045 | ||

| Net asset value, offering, and redemption price per share | $ | 10.02 | |

| Institutional Class | |||

| Net assets | $ | 14,295,862 | |

| Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 1,424,374 | ||

| Net asset value, offering, and redemption price per share | $ | 10.04 |

The accompanying notes are an integral part of these consolidated financial statements.

12

Loeb King Alternative Strategies Fund

Statement of Operations

For the Period Ended February 28, 2014(1) (Unaudited)

| INVESTMENT INCOME | |||

| Dividend income(2) | $ | 49,185 | |

| Interest income | 10,912 | ||

| Term loan fee income | 2,149 | ||

| TOTAL INVESTMENT INCOME | 62,246 | ||

| EXPENSES | |||

| Advisory fees (Note 5) | 78,089 | ||

| Administration and accounting fees | 41,211 | ||

| Dividend and interest expenses on securities sold short | 35,568 | ||

| Transfer agent fees and expenses | 20,083 | ||

| Federal and state registration fees | 19,089 | ||

| Custody fees | 44,555 | ||

| Audit and tax fees | 7,678 | ||

| Legal fees | 32,497 | ||

| Distribution fees - Investor Class (Note 5) | 2,603 | ||

| Reports to shareholders | 5,206 | ||

| Trustees' fees | 8,745 | ||

| Organizational costs (Note 2) | 45,560 | ||

| Other expenses | 22,572 | ||

| TOTAL EXPENSES | 363,456 | ||

| Less waivers and reimbursement by Adviser (Note 5) | (221,623 | ) | |

| NET EXPENSES | 141,833 | ||

| NET INVESTMENT LOSS | (79,587 | ) | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | |||

| Net realized gain (loss) on: | |||

| Investments | 231,132 | ||

| Swap contracts | 73,964 | ||

| Securities sold short | (150,087 | ) | |

| Purchased options | (115,595 | ) | |

| Written options | (1,422 | ) | |

37,992 | |||

| Net change in unrealized appreciation (depreciation) on: | |||

| Investments | 323,470 | ||

| Swap contracts | (7,159 | ) | |

| Securities sold short | (143,317 | ) | |

| Purchased options | (6,409 | ) | |

| Written options | (27,166 | ) | |

139,419 | |||

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 177,411 | ||

| NET INCREASE IN NET ASSETS FROM OPERATIONS | $ | 97,824 |

| (1) | The Fund commenced operations on September 27, 2013. |

| (2) | Net of $1,348 in foreign withholding taxes and issuance fees. |

The accompanying notes are an integral part of these consolidated financial statements.

13

Loeb King Alternative Strategies Fund

Statement of Changes in Net Assets

Period Ended February 28, 2014(1) (Unaudited) | |||

| FROM OPERATIONS | |||

| Net investment loss | $ | (79,587 | ) |

| Net realized gain (loss) on: | |||

| Investments | 231,132 | ||

| Swap contracts | 73,964 | ||

| Securities sold short | (150,087 | ) | |

| Purchased options | (115,595 | ) | |

| Written options | (1,422 | ) | |

| Net change in unrealized appreciation (depreciation) on: | |||

| Investments | 323,470 | ||

| Swap contracts | (7,159 | ) | |

| Securities sold short | (143,317 | ) | |

| Purchased options | (6,409 | ) | |

| Written options | (27,166 | ) | |

| Net increase in net assets from operations | 97,824 | ||

| FROM DISTRIBUTIONS | |||

| Net investment income - Investor Class | — | ||

| Net investment income - Institutional Class | (219 | ) | |

| Net realized gain on investments - Investor Class | (5,372 | ) | |

| Net realized gain on investments - Institutional Class | (20,701 | ) | |

| Net decrease in net assets resulting from distributions paid | (26,292 | ) | |

| FROM CAPITAL SHARE TRANSACTIONS | |||

| Proceeds from shares sold: | |||

| Investor Class | 4,443,071 | ||

| Institutional Class | 22,382,468 | ||

| Proceeds from shares issued to holders in reinvestment of dividends: | |||

| Investor Class | 1,634 | ||

| Institutional Class | 20,919 | ||

| Payments for shares redeemed: | |||

| Investor Class | (996,192 | ) | |

| Institutional Class | (8,168,776 | ) | |

| Net increase in net assets from capital share transactions | 17,683,124 | ||

| TOTAL INCREASE IN NET ASSETS | 17,754,656 | ||

| NET ASSETS: | |||

| Beginning of Period | — | ||

| End of Period | $ | 17,754,656 | |

| ACCUMULATED NET INVESTMENT LOSS | $ | (79,806 | ) |

| (1) | The Fund commenced operations on September 27, 2013. |

The accompanying notes are an integral part of these consolidated financial statements.

14

Loeb King Alternative Strategies Fund

Statement of Changes in Net Assets(continued)

Period Ended February 28, 2014(1) (Unaudited) | |||

| CHANGES IN SHARES OUTSTANDING: | |||

| Shares sold: | |||

| Investor Class | 444,515 | ||

| Institutional Class | 2,234,290 | ||

| Shares issued to holders as reinvestment of dividends: | |||

| Investor Class | 163 | ||

| Institutional Class | 2,090 | ||

| Shares redeemed: | |||

| Investor Class | (99,633 | ) | |

| Institutional Class | (812,006 | ) | |

| Net increase in shares outstanding | 1,769,419 | ||

| (1) | The Fund commenced operations on September 27, 2013. |

The accompanying notes are an integral part of these consolidated financial statements.

15

Loeb King Alternative Strategies Fund

Statement of Cash Flows

For the Period Ended February 28, 2014 (Unaudited)

| Increase (decrease) in cash— | |||

| Cash flows from operating activities: | |||

| Net increase (decrease) in net assets from operations | $ | 97,824 | |

| Adjustments to reconcile net increase (decrease) in net assets from operations to net cash provided (used) in operating activities: | |||

| Payments to purchase securities | (44,929,610 | ) | |

| Payments to cover short securities | (13,163,820 | ) | |

| Payments to close written options | (190,183 | ) | |

| Proceeds from sale of securities | 34,617,311 | ||

| Proceeds from securities sold short | 16,785,601 | ||

| Proceeds from written options | 231,682 | ||

| (Purchase) sale of short term investments, net | (154,056 | ) | |

| Realized gain on investments in securities | (115,537 | ) | |

| Realized loss on securities sold short | 150,087 | ||

| Realized loss on written options | 1,422 | ||

| Change in unrealized appreciation on investments in securities | (317,061 | ) | |

| Change in unrealized depreciation on securities sold short | 143,317 | ||

| Change in unrealized depreciation on written options | 27,166 | ||

| (Increases) decreases in operating assets: | |||

| Increase in foreign currencies | (265,669 | ) | |

| Increase in deposits at broker | (5,647,116 | ) | |

| Unrealized appreciation on open swap contracts | (19,756 | ) | |

| Increase in dividends and interest receivable | (81,116 | ) | |

| Increase in receivable for securities sold | (926,347 | ) | |

| Increase in due from Adviser | (30,057 | ) | |

| Increase in prepaid expenses and other assets | (47,697 | ) | |

| Increases (decreases) in operating liabilities: | |||

| Unrealized depreciation on open swap contracts | 26,915 | ||

| Increase in payable for securities purchased | 1,517,374 | ||

| Increase in payable for dividends and interest on short positions | 6,834 | ||

| Increase in distribution fees | 2,198 | ||

| Increase in custody fees | 17,893 | ||

| Increase in other accrued expenses | 37,794 | ||

| Net cash used in operating activities | (12,224,607 | ) | |

| Cash flows from financing activities: | |||

| Proceeds from shares sold | 26,798,092 | ||

| Payment on shares redeemed | (9,164,968 | ) | |

| Distributions paid in cash | (3,739 | ) | |

| Net cash provided by financing activities | 17,629,385 | ||

| Net increase in cash | 5,404,778 | ||

| Cash: | |||

| Beginning balance | — | ||

| Ending balance | $ | 5,404,778 | |

| Supplemental information: | |||

| Non-cash financing activities not included herein consists of dividend reinvestment of dividends and distributions | $ | 22,553 | |

| Cash paid for interest | $ | 6,418 | |

The accompanying notes are an integral part of these consolidated financial statements.

16

Loeb King Alternative Strategies Fund-Investor Class

Financial Highlights

Per Share Data for a Share Outstanding Throughout the Period

Period Ended February 28, 2014(1) (Unaudited) | |||

| Net Asset Value, Beginning of Period | $ | 10.00 | |

| Income (loss) from investment operations: | |||

| Net investment loss(2) | (0.07) | ||

| Net realized and unrealized gain on investments | 0.11 | ||

| Total from investment operations | 0.04 | ||

| Less distributions paid: | |||

| From net realized gain on investments | (0.02) | ||

| Total distributions paid | (0.02) | ||

| Net Asset Value, End of Period | $ | 10.02 | |

| Total return(3) | 0.42% | ||

| Supplemental Data and Ratios: | |||

| Net assets, end of period (000's) | $ | 3,459 | |

| Ratio of expenses to average net assets(4) | |||

| Before reimbursements and/or waivers | 6.98% | ||

| After reimbursements and/or waivers | 2.98% | ||

| Ratio of expenses excluding dividend and interest expense on short positions to average net assets(4) | |||

| Before reimbursements and/or waivers | 6.24% | ||

| After reimbursements and/or waivers | 2.24% | ||

| Ratio of net investment loss to average net assets(4)(5) | |||

| Before reimbursements and/or waivers | -5.69% | ||

| After reimbursements and/or waivers | -1.69% | ||

| Portfolio turnover rate(3)(6) | 377% | ||

| (1) | The Fund commenced operations on September 27, 2013. |

| (2) | Per share net investment loss was calculated using average shares outstanding. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The net investment loss ratios include dividend and interest expense on short positions. |

| (6) | Consists of long-term investments only; excludes securities sold short and derivative instruments. |

The accompanying notes are an integral part of these consolidated financial statements.

17

Loeb King Alternative Strategies Fund-Institutional Class

Financial Highlights

Per Share Data for a Share Outstanding Throughout the Period

Period Ended February 28, 2014(1) (Unaudited) | |||

| Net Asset Value, Beginning of Period | $ | 10.00 | |

| Income (loss) from investment operations: | |||

| Net investment loss(2) | (0.06) | ||

| Net realized and unrealized gain on investments | 0.12 | ||

| Total from investment operations | 0.06 | ||

| Less distributions paid: | |||

| From net realized gain on investments | (0.02) | ||

| Total distributions paid | (0.02) | ||

| Net Asset Value, End of Period | $ | 10.04 | |

| Total return(3) | 0.62% | ||

| Supplemental Data and Ratios: | |||

| Net assets, end of period (000's) | $ | 14,296 | |

| Ratio of expenses to average net assets(4) | |||

| Before reimbursements and/or waivers | 6.98% | ||

| After reimbursements and/or waivers | 2.66% | ||

| Ratio of expenses excluding dividend and interest expense on short positions to average net assets(4) | |||

| Before reimbursements and/or waivers | 6.31% | ||

| After reimbursements and/or waivers | 1.99% | ||

| Ratio of net investment loss to average net assets(4)(5) | |||

| Before reimbursements and/or waivers | -5.81% | ||

| After reimbursements and/or waivers | -1.49% | ||

| Portfolio turnover rate(3)(6) | 377% | ||

| (1) | The Fund commenced operations on September 27, 2013. |

| (2) | Per share net investment loss was calculated using average shares outstanding. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The net investment loss ratios include dividend and interest expense on short positions. |

| (6) | Consists of long-term investments only; excludes securities sold short and derivative instruments. |

The accompanying notes are an integral part of these consolidated financial statements.

18

Loeb King Alternative Strategies Fund

Notes to the Financial Statements

February 28, 2014 (Unaudited)

1. Organization

The Loeb King Alternative Strategies Fund (the “Fund”) is a series of the Loeb King Trust (the “Trust”) which was formed as a Delaware statutory trust on May 22, 2013, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund is an open-end, diversified, management investment company. The Fund is managed by Carl M. Loeb Advisory Partners L.P. (the “Adviser”). The Fund’s investment objective is to seek positive absolute returns and income with lower volatility than global capital markets and traditional investment strategies. The Fund commenced operations on September 27, 2013.

The Fund currently offers Investor Class and Institutional Class shares. Each class of shares differs principally in its distribution expenses. The Fund may issue an unlimited number of shares of beneficial interest, with no par value. Each class of shares has identical rights to earnings, assets and voting privileges, except for class-specific expenses and exclusive rights to vote on matters affecting only individual classes.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of the financial statements. These policies are in conformity with U.S. generally accepted accounting principles.

A. Securities Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3.

B. Use of Estimates: The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of revenue and expenses and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

C. Federal Income Taxes: The Fund intends to qualify each year as a regulated investment company under Subchapter M of the Internal Revenue Code, provided it complies with all applicable requirements regarding the source of its income, diversification of its assets and timing and amount of distributions. The Fund intends to distribute substantially all of its taxable income and net capital gains to shareholders. In addition, by distributing in each calendar year substantially all of its net investment income and capital gains, if any, the Fund will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required.

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions expected to be taken in the Fund’s 2014 tax returns. The Fund identifies its major tax jurisdictions as U.S. Federal and the state of Delaware; however, the Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

D. Securities Transactions, Income and Distributions: Securities transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on a specific identification basis. Interest income is recorded on an accrual basis. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates.

The Fund distributes substantially all net investment income, if any, and net realized capital gains, if any, annually. The amount of dividends and distributions to shareholders from net investment income and net realized capital gains is determined in accordance with Federal income tax regulations, which differ from accounting principles generally accepted in the United States of America. To the extent these book/tax differences are permanent, such amounts are reclassified within the capital accounts based on their Federal tax treatment.

Investment income, expenses (other than those specific to the class of shares), and realized and unrealized gains and losses on investments are allocated to the separate classes of the Fund’s shares based upon their relative net assets on the date income is earned or expensed and realized and unrealized gains and losses are incurred.

E. Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the prevailing exchange rates of such currencies against the U.S. dollar. The market value of investment securities and the other assets and liabilities are translated at the exchange rate as of the valuation date. Purchases and sales of investment securities, income and expenses are translated at the exchange rate prevailing on the respective dates of such transactions.

Although the net assets of the Fund are presented at the foreign exchange rates and market values at the close of the period, the Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of securities held or sold during the period. Accordingly, such foreign currency gains (losses) are included in the reported net realized and unrealized gains (losses) on investment transactions.

Reported realized foreign currency gains or losses arise from the disposition of foreign currency and forward foreign currency exchange contracts, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books on the transaction date and the U.S. dollar equivalent of the amounts actually received or paid. Unrealized foreign exchange gains and losses arise from changes (due to the changes in the exchange rate) in the value of foreign currency and assets and liabilities (other than investments) denominated in foreign currencies, which are held at period end.

F. Loan Participations and Assignments: The Fund may invest in loan participations and assignments. When the Fund purchases a loan participation, the Fund typically enters into a contractual relationship with the lender or a third party selling such participations (“Selling Participant”), but not the borrower. In this case, the Fund assumes the credit risk of the borrower and the Selling Participant and any other persons inter-positioned between the Fund and the borrower (“Intermediate Participants”). In contrast, when the Fund purchases an assignment, the contractual relationship is with the borrower and the credit risk assumed by the Fund is only with the borrower. Although certain loan participations or assignments are secured by collateral, the Fund could experience delays or limitations in realizing proceeds on such collateral or have its interest subordinated to other indebtedness of the obligor. The Fund may also enter into unfunded loan commitments, which are contractual obligations for future funding. These unfunded commitments represent a future obligation in full, even though a

19

Loeb King Alternative Strategies Fund

Notes to the Financial Statements

February 28, 2014 (Unaudited)

percentage of the loan may not be utilized by the borrower. These types of investments may include standby financing commitments, such as revolving credit facilities, which obligate the Fund to supply additional cash to the borrower on demand. The value of the unfunded portion of the investment is determined using a pro-rata allocation, based on its par value relative to the par value of the entire investment. The unrealized appreciation (depreciation) from unfunded commitments is reported in the Statements of Assets and Liabilities. In addition, loan participations and assignments are vulnerable to market conditions such that economic conditions or other events may reduce the demand for loan participations and assignments and certain loan participations and assignments which were liquid, when purchased, may become illiquid.

G. Convertible Securities: The Fund invests in preferred stocks and fixed-income securities which are convertible into common stock. Convertible securities may be converted either at a stated price or rate within a specified period of time into a specified number of shares of common stock. By investing in a convertible security, the Fund may participate in any capital appreciation or depreciation of a company’s stock, but to a lesser degree than if it had invested in that company’s common stock. Convertible securities rank senior to common stock in a corporation’s capital structure and, therefore, entail less risk than the corporation’s common stock. The Fund may attempt to hedge some of its investments in convertible debt securities by selling short the issuer’s common stock.

H. Short Sales: The Fund sells securities it does not own as a hedge against some of its long positions and/or in anticipation of a decline in the market value of that security (short sale). When the Fund makes a short sale, it must borrow the security sold short and deliver it to the broker-dealer through which it made the short sale. The Fund may have to pay a fee to borrow the particular security and may be obligated to remit any interest or dividends received on such borrowed securities. Dividends declared on short positions open are recorded on the ex-date as an expense. A gain, limited to the price at which the Fund sold the security short, or a loss, unlimited in magnitude, will be recognized upon the termination of a short sale if the market price at termination is less than or greater than, respectively, the proceeds originally received. The Fund is also subject to the risk that they may be unable to reacquire a security to terminate a short position except at a price substantially in excess of the last quoted price. The Fund is also subject to risk of loss if the broker were to fail to perform its obligations under the contractual terms. Liabilities for securities sold short are reported at market value on the Statement of Assets and Liabilities and the change in market value is recorded as unrealized gain or loss on the Statement of Operations.

The Fund is required to pledge cash or securities to the broker as collateral for the securities sold short. Collateral requirements are calculated daily based on the current market value of the short positions. Cash deposited with broker for collateral for securities sold short is recorded as an asset on the Statement of Assets and Liabilities and securities segregated as collateral are denoted in the Schedule of Investments. The Fund may receive or pay the net of the following amounts: (i) a portion of the income from the investment of cash collateral; (ii) the broker’s fee on the borrowed securities; and (iii) a financing charge for the difference in the market value of the short position and cash collateral deposited with the broker. This income or fee is calculated daily based upon the market value of each borrowed security and a variable rate that is dependent on the availability of the security. The net amount of fees incurred is included in dividend and interest on securities sold short in the Statement of Operations.

I. Master Agreements: The Fund is a party to ISDA (International Swap and Derivatives Association, Inc.) Master Agreements (“Master Agreements”) with certain counterparties that govern over-the-counter derivative (including Total Return, Credit Default and Interest Rate Swaps) and foreign exchange contracts entered into by the Fund. The Master Agreements may contain provisions regarding, among other things, the parties’ general obligations, representations, agreements, collateral requirements, events of default and early termination. Termination events applicable to the Fund may occur upon a decline in the Fund’s net assets below a specified threshold over a certain period of time. Termination events applicable to counterparties may occur upon a decline in the counterparty’s long-term and short-term credit ratings below a specified level. In each case, upon occurrence, the other party may elect to terminate early and cause settlement of all derivative and foreign exchange contracts outstanding, including the payment of any losses and costs resulting from such early termination, as reasonably determined by the terminating party. Any decision by one or more of the Fund’s counterparties to elect early termination could impact the Fund’s future derivative activity. Collateral and margin requirements differ between exchange traded derivatives and over-the-counter (“OTC”) derivatives. Margin requirements are established by the broker or clearing house for exchange-traded and centrally cleared derivatives (futures contracts, options and centrally cleared swaps) pursuant to the governing agreements for those investment types. For OTC derivatives traded under an ISDA Master Agreement, posting of collateral is required by either the Fund or the applicable counterparty if the total net exposure of all OTC derivatives with the applicable counterparty exceeds the minimum transfer amount and can vary depending on the counterparty and the type of the agreement. For swaps, futures and forward foreign currency exchange contracts, the Fund may be required to post collateral if the Fund is in a net liability position with the counterparty exceeding certain amounts. Generally, collateral is determined at the close of fund business each day. Collateral posted for the benefit of the Fund is held in a segregated account by a custodian of the Fund’s custodian and with respect to those amounts which can be sold or repledged, are presented in the Fund’s Schedule of Investments. Collateral pledged by the Fund is segregated by the Fund’s custodian and identified in the Fund’s Schedule of Investments. Collateral can be in the form of cash, debt securities issued by the U.S. Government and related agencies, other securities or money market funds as agreed to by the Fund and the applicable counterparty. Collateral requirements are generally determined based on the Fund’s net position with each counterparty. The Fund’s derivative assets and liabilities on the Statement of Assets and Liabilities are presented net only within a derivative type when a legally enforceable master netting agreement exists between the Fund and a derivative counterparty. For additional information regarding the offsetting of assets and liabilities at February 28, 2014, please reference the table in Note 4.

J. Futures Contracts: The Fund may invest in futures contracts as part of its investment strategy. Investments in futures may increase or decrease exposure to a particular market. In the event of a bankruptcy or insolvency of a futures commission merchant that holds margin on behalf of the Fund, the Fund may not be entitled to the return of all of the margin owed to the Fund, potentially resulting in a loss. No monies are paid to or received by the Fund upon the purchase or sale of a futures contract. Initially, the Fund will be required to deposit with the broker an amount of cash or cash equivalents, known as initial margin, based on the value of the contract. Subsequent payments to and from the broker, will be made on a periodic basis as the price of the underlying instruments fluctuates. Changes in market value of open futures contracts are recorded as unrealized appreciation or depreciation in the Statement of Operations. Realized gains or losses represent the difference between the value of the contract at the time it was opened and the value at the time it was closed or expired, and are reported on the Statement of Operations. Securities deposited as initial margin are designated in the Schedule of Investments and cash deposited is presented as Due from Broker on the Statement of Assets and Liabilities. The use of long futures contracts subjects the Fund to risk of loss in excess of the amounts shown on the Statement of Assets and Liabilities, up to the contract amount of the futures contracts. The use of short futures contracts subjects the Fund to unlimited risk of loss. Futures contracts outstanding at period end, if any, are listed after the Fund’s Schedule of Investments.

20

Loeb King Alternative Strategies Fund

Notes to the Financial Statements

February 28, 2014 (Unaudited)

K. Forward Foreign Currency Exchange Contracts: The Fund may buy and sell forward foreign currency exchange contracts, which are agreements between two parties to buy and sell currencies at a set price on a future date. These contracts are used to protect against a decline in value relative to the U.S. dollar of the currencies in which portfolio securities are denominated or quoted (or an increase in the value of a currency in which securities the Fund intends to buy are denominated, when the Fund holds cash reserves and short term investments), or for other investment purposes. The U.S. dollar value of forward foreign currency exchange contracts is determined using current forward currency exchange rates supplied by a quotation service. The market value of the contract will fluctuate with changes in currency exchange rates. The contract is marked to market daily and the change in market value is recorded as an unrealized appreciation or depreciation. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. The Fund could be exposed to risk if the value of the currency changes unfavorably, if the counterparties to the contracts are unable to meet the terms of their contracts or if the Fund is unable to enter into a closing position. Risks may exceed amounts recognized on the Statement of Assets and Liabilities. Non-deliverable forward foreign currency exchange contracts are settled with the counterparty in U.S. dollar without the delivery of foreign currency. Forward foreign currency exchange contracts outstanding at period end, if any, are listed after the Fund’s Schedule of Investments.