UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-36051

JASON INDUSTRIES, INC.

(Exact name of registrant as specified in its charter

| Delaware | 46-2888322 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

411 East Wisconsin Avenue Suite 2100 Milwaukee, Wisconsin 53202 |

| (Address of principal executive offices) |

| (414) 277-9300 |

| (Registrant’s telephone number, including area code) |

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Common Stock, $0.0001 par value per share | The NASDAQ Stock Market LLC | |

| Warrants to purchase Common Stock | The NASDAQ Stock Market LLC | |

| (Title of class) | (Name of exchange on which registered) | |

| Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ | Accelerated filer ý | |

Non-accelerated filer ¨ | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant, as of June 26, 2015, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $130.8 million (based upon the closing price of $7.34 per share on The NASDAQ Stock Market as of such date). Solely for the purposes of this disclosure, shares of common stock held by executive officers and directors of the registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination of executive officers and directors as affiliates is not necessarily a conclusive determination for any other purposes.

There were 22,309,615 shares of common stock issued and outstanding as of March 1, 2016.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement relating to its 2016 Annual Meeting of Shareholders (the “2016 Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K. The 2016 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

JASON INDUSTRIES, INC.

TABLE OF CONTENTS

1

Cautionary Note Regarding Forward-Looking Statements

Unless otherwise indicated, references to “Jason Industries,” the “Company,” “we,” “our” and “us” in this Annual Report on Form 10-K refer to Jason Industries, Inc. and its consolidated subsidiaries.

This report contains forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. Specifically, forward-looking statements may include statements relating to the Company’s future financial performance, changes in the markets for the Company’s products, the Company’s expansion plans and opportunities, and other statements preceded by, followed by or that include the words “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target” or similar expressions.

These forward-looking statements are based on information available to the Company as of the date of this report and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing the Company’s views as of any subsequent date, and the Company does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, the Company’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include the following:

| • | level of demand for the Company’s products; |

| • | competition in the Company’s markets; |

| • | the Company’s ability to grow and manage growth profitably; |

| • | the Company’s ability to access additional capital; |

| • | changes in applicable laws or regulations; |

| • | the Company’s ability to attract and retain qualified personnel; |

| • | the possibility that the Company may be adversely affected by other economic, business, and/or competitive factors; and |

| • | other risks and uncertainties indicated in this report, including those discussed under “Risk Factors” in Item 1A of Part I of this report. |

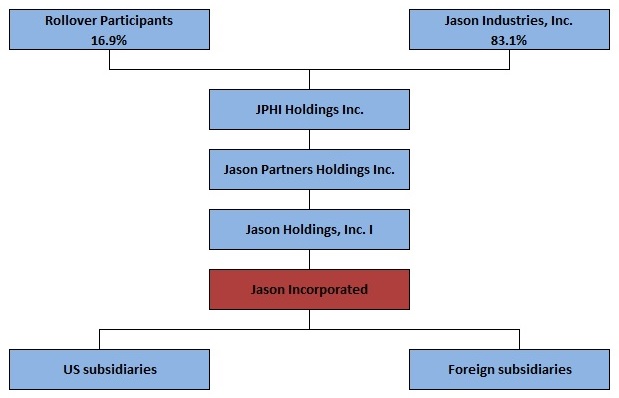

Introductory Note

On June 30, 2014, the Company (formerly known as Quinpario Acquisition Corp.) and Jason Partners Holdings Inc. (“Jason”) completed a transaction in which JPHI Holdings Inc. (“JPHI”), a majority owned subsidiary of the Company, acquired 100 percent of the capital stock of Jason from its then current owners, Saw Mill Capital, LLC, Falcon Investment Advisors, LLC and other investors (the “Business Combination”). In connection with the closing of the Business Combination, the Company changed its name to Jason Industries, Inc., and commenced trading of its common stock and warrants under the symbols, “JASN” and “JASNW”, respectively, on The NASDAQ Stock Market. This transaction is further described in Note 2 to the Company’s consolidated financial statements included herein.

PART I

ITEM 1. BUSINESS

Corporate History

Jason Industries, a Delaware corporation, was originally formed in May 2013 as a blank check company under the name Quinpario Acquisition Corp. (“QPAC”) for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination involving QPAC and one or more businesses. Until the consummation of the Business Combination, QPAC’s securities were traded on The NASDAQ Stock Market (“Nasdaq”) under the ticker symbols “QPAC,” “QPACU” and “QPACW.”

On June 30, 2014, the Company completed the Business Combination pursuant to a stock purchase agreement, dated as of March 16, 2014 (the “Purchase Agreement”), that provided for the acquisition of all of the capital stock of Jason, the indirect parent company of Jason Incorporated, by JPHI from Jason Partners Holdings LLC (“Seller”) and certain members of Seller. In connection with the Business Combination, we entered into new senior secured credit facilities with a syndicate of lenders led by Deutsche Bank AG New York Branch, as administrative agent, in the aggregate amount of approximately $460.0 million, which was primarily used to refinance Jason Incorporated’s existing indebtedness, pay transaction fees and expenses and pay a

2

portion of the purchase price under the Purchase Agreement. The purchase price under the Purchase Agreement was also funded with cash held in our trust account, the contribution of Jason common stock to JPHI by certain members of Seller and certain directors and management of Jason Incorporated (collectively, the “Rollover Participants”) in exchange for JPHI stock, and the proceeds from the sale of our 8% Series A Convertible Perpetual Preferred Stock (the “Series A Preferred Stock”) in a private placement that closed simultaneously with the Business Combination.

Following the Business Combination, Jason Incorporated became an indirect majority-owned subsidiary of the Company and our only significant asset, with the Rollover Participants indirectly owning approximately 16.9% of Jason Incorporated and the Company indirectly owning approximately 83.1% of Jason Incorporated. We also changed our name from “Quinpario Acquisition Corp.” to “Jason Industries, Inc.” and continued the listing of our Common Stock and Warrants on Nasdaq under the symbols “JASN” and “JASNW,” respectively, effective July 1, 2014.

Presentation of Financial and Operating Data

The Business Combination was accounted for using the acquisition method of accounting under the provisions of Accounting Standards Codification Topic 805, “Business Combinations.” Accordingly, we are treated as the legal and accounting acquirer and Jason is treated as the legal and accounting acquiree. However, Jason is considered to be our accounting predecessor, and therefore unless otherwise indicated, the financial information and operating data presented in this Annual Report on Form 10-K is that of Jason Partners Holdings Inc.

Organizational Chart

Our Business

We are a global industrial manufacturing company operating the following four businesses: seating, finishing, acoustics and components. Jason Incorporated was founded in 1985 and today provides critical components and manufacturing solutions to customers across a wide range of end markets, industries and geographies through a global network of 35 manufacturing facilities and 19 sales offices, warehouses and joint venture facilities throughout the United States and 14 foreign countries. The Company has embedded relationships with long standing customers, superior scale and resources and specialized capabilities to design and manufacture specialized products on which our customers rely.

Our goal is to focus on markets with sustainable growth characteristics and where we believe we are, or have the opportunity to become, the industry leader. Our finishing business focuses on the production of industrial brushes, buffing wheels and buffing compounds that are used in a broad range of industrial and infrastructure applications. The Company’s seating business supplies seating solutions to equipment manufacturers in the motorcycle, lawn and turf care, industrial, agricultural, construction and power sports end markets and is a major supplier of original equipment manufacturer (“OEM”) seating to US-based manufacturers of heavyweight motorcycles. The acoustics business manufactures engineered non-woven, fiber-based acoustical products for the North American auto industry. The components business is a diversified manufacturer of stamped, formed, expanded and perforated metal components and subassemblies for rail and filtration applications, outdoor power equipment, small gas engines and smart utility meters.

3

Jason Incorporated History

The formation of Jason Incorporated’s platform began in 1985 when Vincent Martin and Mark Train completed the management buyout of three businesses, collectively generating $71.6 million of revenue, from AMCA International, a manufacturing conglomerate that served a variety of industries. The acquired businesses consisted of (i) Osborn Manufacturing, the largest manufacturer of industrial brushes in the United States; (ii) Janesville Products, the largest manufacturer of automotive acoustical fiber insulation in the United States; and (iii) Jackson Buff, the largest manufacturer of industrial buffs in the United States, each of which has a history spanning decades.

Description of Business Segments

Jason Industries’ global industrial platform encompasses a diverse group of industries, geographies and end markets. Through our four businesses, we deliver an array of industrial consumables and critical manufactured components to a number of industries, including industrial equipment, motorcycles, outdoor lawn and power equipment, rail, automotive and smart meters. The highly fragmented nature of the Company’s end markets creates growth opportunities given our established global footprint and leading share positions. Our businesses serve multiple industries, which we believe, based on our market research, together represent a global market of more than $20.0 billion and can be categorized under four businesses: seating, finishing, acoustics and components.

Net sales are distributed amongst the four segments as follows:

| Successor | Combined* | Predecessor | ||||||

| Year ended December 31, | ||||||||

| 2015 | 2014 | 2013 | ||||||

| Net sales | ||||||||

| Seating | 25.0 | % | 24.5 | % | 24.3 | % | ||

| Finishing | 27.0 | % | 26.7 | % | 26.5 | % | ||

| Acoustics | 30.8 | % | 31.1 | % | 30.0 | % | ||

| Components | 17.2 | % | 17.7 | % | 19.2 | % | ||

| 100.0 | % | 100.0 | % | 100.0 | % | |||

*We have combined our net sales in the period June 30, 2014 through December 31, 2014 with our predecessor’s net sales in the period January 1, 2014 through June 29, 2014. Net sales were not affected by acquisition accounting.

See more information regarding our segments and sales by geography within Part II, Item 8, Note 16 to the Consolidated Financial Statements.

Seating

Market/Industry Overview

Within the overall market for seating products, we estimate that the addressable North American and global (including North America) markets for our current product offerings are approximately $400 million and $1.5 billion per year, respectively. The Company’s product line includes motorcycle seats; operator seats for the construction, agriculture, lawn and garden and other industrial equipment markets; and seating for the power sports market. The market for seating products is dominated by several large domestic and international participants, who are often awarded contracts as the sole supplier for a particular motorcycle, lawn mower or other construction, agriculture or material handling platform. We believe that competition is based mostly on innovative styling, manufacturing flexibility, quality, prices and delivery.

Motorcycle production has experienced a rebound in recent years, and we believe demand in the global motorcycle market will continue to grow in the coming years. Demand for power lawn and garden equipment is primarily dependent on weather and trends in personal consumption expenditures, recreational and leisure activities, and residential and commercial real estate construction and sales. The market for lawn and garden equipment has also rebounded in recent years and we expect it to mirror general economic conditions.

Key Products

Through the seating business, which represented 25.0% of the Company’s 2015 revenue, the Company provides seating solutions for a variety of applications, including motorcycle, agricultural, construction, industrial, lawn and turf care, and power sports. The seating business was established in 1995 through the acquisition of Milsco Manufacturing Company, which has provided high-quality seats since 1934. The seating business operates under the Milsco brand, which was originally established as a harness maker in 1924 and, early in its history, gained notice as the first company to put padded seating on tractors and farm equipment.

4

Headquartered in Milwaukee, Wisconsin, the seating business offers a distinct vertically integrated operating model, which includes a full range of functions, such as research and development, design and engineering, manufacturing of components and final assembly. Through our broad manufacturing capabilities and high quality products, we have established longstanding relationships with our top customers, which average over 30 years.

Finishing

Market/Industry Overview

Within the overall market for finishing products, we estimate that the addressable North American and global (including North America) markets for our primary product offerings are approximately $1.7 billion and $6.0 billion per year, respectively. The Company’s product lines are comprised of industrial brushes, polishing buffs and compounds, and abrasives used primarily in the metalworking, welding and construction industries. The market for finishing products is highly fragmented with most participants having single or limited product lines and serving specific geographic markets. While the finishing business competes with numerous domestic and international companies across a variety of product lines, we do not believe that any one competitor directly competes with us on all of our product lines. We believe we are the only market participant that reaches all regions of the world. End users of finishing products are broadly diversified across many sectors of the economy. In the long-term, the finishing market is closely tied to overall growth in industrial production, which we believe has fundamental long-term growth potential. The abrasives market has been deemed strategically important and is a targeted growth market for the Company. In May 2015, the Company acquired DRONCO GmbH (“DRONCO”), a leading European manufacturer of bonded abrasives. The DRONCO acquisition expands the finishing segment’s product portfolio and advances its entry to adjacent abrasives markets.

The finishing market is also characterized by the need for sophisticated manufacturing equipment, the ability to produce a broad number of niche products and the flexibility in manufacturing operations to adapt to ever-changing customer demands and schedules. We believe entry into markets by competitors with lower labor costs, including foreign competitors, will be limited because labor is a relatively small portion of total manufacturing costs. The cost of labor, manufacturing, shipping and logistics is dramatically rising in countries such as China and customers continue to have increasing demand for shorter lead times and lower inventory and carrying costs.

Key Products

Through the finishing business, which represented 27.0% of the Company’s 2015 revenue, Jason Industries produces and supplies industrial brushes, buffing wheels and buffing compounds, and abrasives. We established the finishing business in 1985 by acquiring the business of Osborn Manufacturing, which has been in operation since 1889. Our products are used in a variety of applications with no single customer or industry accounting for a significant portion of business revenue. The Company has strategic facilities located globally, including labor-intensive production sites in low-cost locations such as Brazil, China, Portugal, Romania, Mexico and Taiwan.

The finishing business is a one-stop provider of over 10,000 standard and 100,000 customized brush, buffing wheel and buffing compound, and abrasives products used across multiple industries, including aerospace, engineering, plastic, finishing, building, leisure, steel, hardware, welding and naval, among others. For some of the product lines, such as snow protect brushes and brushes for the power generation market, the Company is the only provider in the industry. Our broad product suite is composed of brush types used for a variety of applications, including power, maintenance, strip, punch, and roller brushes. These products are marketed under leading brand names that include Osborn®, Sealeze® and Dendix®. Our buff products are sold under the Jackson®, Lea®, JacksonLea®, Langsol® and Unipol® brands and are comprised of industrial buffs and abrasives used primarily to finish parts requiring a high degree of luster and/or a satin or textured surface. In addition to manufacturing buffs, the Company also produces the industry’s broadest product line of buffing compounds available in liquid or bar form that are customized to specific end use requirements. Our abrasives products are marketed under the DRONCO® brand and include bonded abrasives such as cutting and grinding wheels and flap discs, as well as diamond cutting wheels and tools. We also service customers with products complementing our brush, polishing, and abrasives lines, including heavy-duty idler rollers for high-capacity precision load handling sold under the Load Runners® brand.

The Company has representatives who reach more than 30,000 customers in approximately 130 countries worldwide. During 2015, the finishing segment derived approximately 42% of finishing sales from North America and the majority of the remaining revenue from Europe and South America. We service our diverse customer base through U.S. facilities in Ohio, Indiana, California and Virginia and 13 foreign countries, including joint ventures in China and Taiwan. Our manufacturing and service locations allow us to work on a regional and local basis with customers to develop custom products and provide significant technical support, resulting in strong relationships with our top customers that average 25 years. In addition, the Company has invested state-of-the-art laboratories in Richmond, Indiana and Burgwald, Germany to provide further technical design capabilities for its North American and European customers.

5

Acoustics

Market/Industry Overview

Within the overall market for automotive acoustical products, we estimate that the addressable North American and global (including North America) markets for current product offerings are approximately $2.5 billion and $12.0 billion per year, respectively. The market for automotive acoustical products is dominated by several large domestic and international participants. These participants are often awarded contracts as the sole supplier for a particular automotive platform. Competition includes manufacturers of mechanically bonded non-woven products, resin-bonded products and urethane foam. Competition is based on innovative styling, price, acoustical performance and weight. Engineering, design and innovation are key distinguishing factors because acoustical products represent a small percentage of the total cost to manufacture an automobile.

Growth in the automotive acoustics market is driven by increasing demand for enhanced acoustics and improved noise, vibration and harshness characteristics within the automotive market. As overall vehicle quality has improved, consumers have increasingly equated quality with the acoustic performance of a vehicle. As a result, car manufacturers have recently expended significant capital for sophisticated acoustical testing systems and laboratories. In addition, an increasing regulatory focus on reducing vehicle mass, increasing fuel-efficiency and stringent end of vehicle life recycling standards have driven the penetration of non-woven materials that are lighter than other acoustical products and that utilize recycled post-industrial textile fibers and recycled PET containers. The replacement of interior products previously served by plastic-based materials has created a trend in new vehicle designs to substitute structured non-woven acoustical products with vehicle manufacturers, which has helped to expand non-woven acoustical content per vehicle.

Key Products

Through the acoustics business, which represented 30.8% of the Company’s 2015 revenue, we manufacture engineered non-woven, fiber-based acoustical products for the automotive industry. The acoustics business was established in 1985 through the acquisition of Janesville Products, which has developed extensive design and manufacturing expertise over its 139 year history that allows it to provide custom acoustical solutions for each vehicle platform it serves. We market our products as being lighter, improving acoustical performance, enhancing aesthetics, and being easier to install than other acoustical products manufactured by our competitors. As a result, our products are used in approximately 50% of light vehicles manufactured in North America today, including 9 of 2015’s top 15 models.

Headquartered in Southfield, Michigan, we believe the acoustics business offers the broadest product line of value-added, higher margin components used in a wide range of vehicles, including automobiles, sport utility vehicles and light trucks, as well as in the industrial and transportation markets. The Company has focused on developing premier lightweight fiber-based solutions that provide competitive or superior acoustical properties. Our production of non-woven fiber-based products is organized by the form in which it is supplied: (i) die cut, (ii) molded, (iii) rolls and blanks, and (iv) other non-woven products.

The acoustics business operates principally as an automotive OEM and Tier-1 supplier. Recently, the Company has focused on increasing sales directly to automotive OEMs, which allows us to integrate our technology and value-added capabilities within OEM organizations. These efforts have shifted sales to what we believe is a more desirable balance between OEMs and Tier-1 suppliers while also broadening the number of vehicle platforms that utilize the Company’s products. Additionally, the Company has increased its share of the content per vehicle on a compound annual growth rate of approximately 6% over the past three years. Substantially all automotive products are sole sourced by customers for a particular vehicle and are used for the life of the platform.

Components

Market/Industry Overview

Within the overall market for component products, the Company estimates that the addressable North American and global (including North America) markets for current product offerings are approximately $750 million and $2.0 billion per year, respectively. The market for component products is highly fragmented with most participants having single or limited product lines, serving specific geographic markets or providing niche capabilities applicable to a limited customer base. While there are numerous competitors with limited product offerings, there are only a few national and international competitors of a size comparable to the Company. While we compete with certain domestic and international competitors across a portion of our product lines, we believe that no one competitor directly competes with us across all of our product lines. End users of component products are broadly diversified across many sectors of the economy.

Demand in the components market is influenced by the broader industrial manufacturing market, which we believe has fundamental and significant long-term growth potential, as well as trends in the perforated and expanded metal, rail and

6

outdoor power equipment industries. The best gauge of domestic industrial production is the U.S. Industrial Production Index, which measures the monthly level of output arising from the manufacturing, mining and gas sectors.

In addition to industrial production, demand for new rail freight cars is expected to be an important growth driver for the Company. Freight car production is expected to experience significant growth as the current fleet reaches the end of its useful life and replacement freight cars are needed. Currently, based on the Company’s market analysis, 26% of U.S. railcars have been in service for more than 30+ years and the average useful life of these railcars is generally considered to be 30 years. As the oil and gas industry demand for tank cars decreases, the industry demand is expected to shift to the other car types. In addition, tank car retrofits remain a potential driver of demand as the industry determines how to comply with federal regulations enacted in 2015.

Key Products

Through the components business, which represented 17.2% of the Company’s 2015 revenue, we manufacture a broad range of stamped, formed, expanded and perforated metal components and subassemblies. The Company is a provider of components that are used in a broad array of products, including small gas engines, smart meters, outdoor equipment, hardware, railcars and off-road equipment. The components business was originally acquired in 1993 through the purchase of the Koller Group, a producer of metal formed components such as stampings, subassemblies, wire forms and expanded metal products. Today, the components business operates through the Assembled Products and Metalex brands.

Within each of the components business product categories, our strategy is to have engineers work alongside customers to create value-added components and solutions for various end products. Our engineering resources, manufacturing capabilities and low cost production availability through our operations in Mexico provide opportunities to deliver value to customers. These characteristics drive long-standing relationships with our top customers that average over 20 years.

Competitive Strengths

The Company believes the following key characteristics provide a competitive advantage and position us for future growth:

Established Industry Leader Across Our Four Businesses

The Company’s businesses have developed leading positions across various niche markets. For example, in our turf care seats, buffing wheels and buffing compounds and automotive acoustical insulation product lines, we believe we are more than twice the size of the next largest direct competitor. The Company’s market share positions have created a stable platform with strong profitability upon which to grow. Our products’ significant brand recognition helps to sustain our market share positions. The Company’s products are often viewed as a brand of choice for quality, dependability, value and continuous innovation. In several niche markets, the Company is the only provider of certain products or manufacturing capabilities. We have served many of our customers for over 25 years. Additionally, our significant market share within highly fragmented niche businesses offers potential attractive acquisition opportunities. Despite leading positions in many of our markets, we face competitive challenges in others. In the Company’s finishing and components segments, we believe certain of our competitors are small and family-owned, operate with lower operating expenses, have lower profit expectations and/or supply lower cost commodity products, which allows such competitors to provide lower cost products and compete with us on pricing. In our seating segment, specifically with respect to highly technical seats for the agricultural and construction vehicle markets, the cost to customers of switching from a current supplier’s products to ours is high, and we believe certain of our competitors have established long-term and entrenched relationships with such customers. These costs and relationships make it challenging to convince such customers to purchase products from us instead of from their existing supplier.

Superior Design & Manufacturing Solutions

The Company has a track record of providing customers with innovative, customized solutions through production flexibility and collaboration with their design and manufacturing teams. We have consistently refined manufacturing processes to incorporate design technologies that improve design capabilities, breadth of product offering, product quality and manufacturing efficiency.

Across our businesses, we maintain teams of designers and a diverse product selection in numerous geographic regions, which allows us to respond quickly to real-time customer needs. Our versatile design and manufacturing capabilities enable us to deliver differentiated and highly-customized solutions for customers by leveraging experienced engineering staff and technologically advanced manufacturing equipment. We believe our diverse product offerings and customized design and manufacturing capabilities have made us a preferred choice within many industries and an entrenched key solutions provider to customers. Some of the Company’s competitors focus on commodity products and lower-value-added products that appeal to certain end users and markets.

We believe we have become a partner at each stage in product development, which has deepened our relationships with an already entrenched customer base and driven revenue growth from existing accounts and new customers.

7

Scalable and Highly Effective Business Philosophy

We use a consistent strategy and focus and deploy capital and resources across our businesses to projects with the highest returns on invested capital. Through corporate strategic planning initiatives, we annually assess our three-year outlook and goals, by using a policy deployment matrix disseminated throughout the organization. The Company’s management utilizes the strategic plan and resulting policy deployment matrix to develop an annual budget and profit plan and monitors progress towards long-term strategic goals.

Across the Company’s businesses, our management team is focused on enhancing product innovation, efficiency, global accessibility and competitiveness. Shared best practices serve to continually improve the processes and products that our customers depend on by delivering customized, value-added solutions across the platform. This global reach offers customers a consistent and fully integrated manufacturing partner capable of serving their needs on a global, regional and local basis.

Proven Acquisition Platform

Since Jason Incorporated’s inception in 1985, we have completed 40 acquisitions and integrated the acquired companies into our existing platform. The Company continually reviews potential acquisitions to expand our market leading positions. However, there is no certainty in the expectation of future acquisitions. The Company’s return expectations or purchase price expectations and integration risk may impact the ability to complete successful acquisitions.

Diverse, Global Footprint with Growing Presence in Emerging Markets

The Company maintains 35 global manufacturing locations, consisting of 15 in the United States and 20 in foreign countries, giving each business a strong international presence. Approximately 28.0% of the Company’s 2015 revenue was generated from products manufactured outside of the United States. In addition, our global presence enables us to take advantage of low-cost manufacturing at our facilities in China, India, Romania, Brazil, Mexico, Portugal and other countries and to meet the needs of local customers with operations in those regions. The Company continues to build upon its established presence in low-cost production locations through the expansion of owned operations and the development of joint ventures and sourcing relationships in Asia, Europe and South America. Our management believes that this global footprint also provides channels of organic growth through the introduction of products into new markets. Our management frequently evaluates our manufacturing, warehouse, distribution and sales locations to identify revenue enhancement opportunities, optimize production costs and ensure proximity to key customers.

Growth Strategies

The Company is focused on delivering sustained profitable growth through a number of avenues. Our growth initiatives are developed based on strategic plans conducted on an annual basis within each business. These plans are regularly reviewed and updated by our leadership team. As a result, we have a uniform strategy that focuses all of our resources on the following key initiatives:

Margin Growth

We are focused on continuous improvement in our profit margins through the development of higher-margin products, continued operational improvements and active product portfolio management. We anticipate our strategy of shifting toward innovative higher-value engineered products will continue to improve our pricing power and profitability. Among other initiatives, the Company is focused on redesigning products to reduce materials costs, continuing to reduce labor-intensive manufacturing processes and reducing logistics costs, which have traditionally been a significant component of overall costs and an important consideration when choosing its strategic manufacturing locations.

The Company is focused on creating operational effectiveness at each of its business segments through deployment of lean principles and implementation of continuous operational improvement initiatives. While many of these activities have focused on implementing shop floor improvements, we have also targeted our selling and administrative functions in order to reduce the cost of serving our customers. The Company is also focused on improving profitability through an active evaluation of customer pricing and a reduction in the number of parts and product variations that are produced. While these initiatives may result in lower overall sales, they are focused on creating shareholder value through higher margins and profitability, as well as lower inventory levels and working capital requirements.

Market Share Gains

While our four businesses pursue growth within new and existing markets through customized strategies targeted for the markets we serve, all businesses are tasked with identifying and pursuing key growth opportunities through new products, end markets, geographies and sales channels. Management believes we have the potential to increase market share due to the highly fragmented nature of our end markets. Each business has identified specific opportunities to expand market share, with associated incremental revenue targets.

8

Product Innovation

Management believes that the Company’s strategy of developing innovative products will position us for continued growth. Working in collaboration with key customers, the design and manufacture of customized products that deliver value will support this growth. We believe that developing new products will allow us to deepen our value-added relationships with customers, open new opportunities for revenue generation, improve pricing power and enhance profitability. The Company has a focused and dedicated strategy for continuous innovation, which is supported by sophisticated manufacturing capabilities and engineering expertise. This continued focus on innovation has driven many successful new product introductions, which we believe will enable continued growth.

Further Geographic Expansion and Penetration

Through the Company’s established global footprint, we look to further penetrate key customers and end markets. Since approximately 28.0% of our total 2015 revenue was derived from foreign manufacturing, our management believes significant opportunity exists for the continued penetration of target international markets. The Company has identified several emerging markets as strong opportunities for new customer growth. Our finishing business has led the Company’s growth into attractive, untapped markets and spearheaded the development of 17 manufacturing facilities throughout 14 countries and two joint venture operations in Asia.

The successful global expansion into new markets and continued penetration of existing markets by the finishing business have paved the way for the Company’s other businesses to capitalize on international growth opportunities. The seating business, for example, has leveraged the finishing business’s presence in India by taking advantage of finishing’s supply chain, human resources, sales force and facility capacity to quickly and economically expand production with limited new capital expenditures.

Acquisitions

Since inception, Jason Incorporated has successfully acquired and integrated 40 businesses. The Company leverages acquisitions to continually drive its position in the markets it serves. The Company has a well-defined post-acquisition integration process and actively evaluates potential acquisitions that could create significant synergies with its existing business portfolio, such as the DRONCO acquisition in 2015. The Company intends to only pursue an acquisition if it is accretive to EBITDA (earnings before interest, income taxes, depreciation and amortization) margins post-synergies and does not result in a significant increase in the ratio of its total debt to EBITDA.

Customers

The Company has an entrenched base of blue chip customers that are leaders in their respective markets. Our customer relationships often span decades in each business. Additionally, our customer base is diversified. In our finishing segment, no customer accounts for more than 10% of the revenue of such segment. In our seating and acoustics segments, only two customers in each segment account for more than 10% of the revenues of such segments. In our components segment, only one customer accounts for more than 10% of the revenue of such segment. Across all of Jason Industries, our largest customer accounts for 10% of 2015 revenues and our next four largest customers represent a combined 16% of 2015 revenues.

Suppliers and Raw Materials

Polyurethane foam, vinyl, plastics, steel, polyester fiber, bicomponent fiber and machined fiber are the primary raw materials that we use to manufacture our products. There are a limited number of domestic and foreign suppliers of these raw materials. The Company generally orders supplies on a purchase order basis. Although our contracts and long term arrangements with our customers generally do not expressly allow us to pass through increases in our raw materials, energy costs and other inputs to our customers, we endeavor to discuss price adjustments with our customers on a case by case basis where it makes business sense. For the year ended December 31, 2015, the spend with our top three material suppliers accounted for less than 10% of total material spend and no single supplier accounted for greater than 3% of total spend. The Company makes an ongoing effort to reduce and contain raw material costs. We do not engage in raw material commodity hedging contracts. The Company attempts to reflect raw material price changes in the sale price of our products.

Seasonality

We experience seasonality of demand for our products in the seating business. Due to our experience in this market, we have adapted our business operations to manage this seasonality. The business also depends upon general economic conditions and other market factors beyond our control, and the Company serves customers in cyclical industries. See “Seasonality and Working Capital” in the accompanying “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained herein for further discussion.

9

Employees

As of December 31, 2015, the Company had approximately 4,600 employees and manufactured products in 35 locations around the world. Approximately 38% of the seating segment’s hourly employees and 37% of the components segment’s hourly employees are unionized. Contracts are negotiated on a local basis, significantly mitigating the risk of a company-wide or segment level work stoppage. Additionally, approximately 1,000 of the Company’s employees reside in Europe, where trade union membership is common. We believe we have a strong relationship with our employees, including those represented by labor unions.

Environmental Matters

The Company’s operations and facilities are subject to extensive federal, state, local and foreign laws and regulations related to pollution and the protection of the environment, health, safety and natural resources, including those governing, among other things, emissions to air, discharges to water, the use, generation, handling, storage, treatment and disposal of hazardous substances and wastes and other materials and the remediation of contaminated sites. The operation of manufacturing plants entails risks in these areas, and a failure by the Company to comply with applicable environmental laws and regulations, or to obtain and comply with the permits required for its operations, could result in civil or criminal fines, penalties, enforcement actions, third party claims for property damage and personal injury, requirements to clean up property or to pay for the capital or operating costs of cleanup, or regulatory or judicial orders enjoining or curtailing operations or requiring corrective measures, including the installation of pollution control equipment or remedial actions. Moreover, if applicable environmental, health and safety laws and regulations, or the interpretation or enforcement thereof, become more stringent in the future, the Company could incur capital or operating costs beyond those currently anticipated.

Compliance with environmental laws has not historically had a material adverse effect on the Company’s capital expenditures, earnings or competitive position, and we anticipate that such compliance will not have a material effect on its business or financial condition in the future.

Available Information

The Company’s Internet website address is www.jasoninc.com. The Company makes available free of charge (other than an investor’s own Internet access charges) through its Internet website its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports, on the same day they are electronically filed with, or furnished to, the U.S. Securities and Exchange Commission (the “SEC”). The Company is not including the information contained on or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K.

Executive Officers of the Registrant

The following table sets forth information concerning our executive officers as of March 1, 2016:

| Name | Age | Position | ||

| Jeffry N. Quinn | 57 | Chief Executive Officer, Chairman of the Board and Director | ||

| A. Craig Ivey | 58 | Interim President and Chief Operating Officer | ||

| Sarah C. Sutton | 44 | Senior Vice President and Chief Financial Officer | ||

| Thomas L. Doerr, Jr. | 41 | Vice President, General Counsel and Secretary | ||

| John J. Hengel | 57 | Vice President—Finance, Treasurer and Assistant Secretary | ||

| Srivas Prasad | 47 | Senior Vice President and General Manager—Seating and Acoustics | ||

| Steven G. Carollo | 44 | Senior Vice President and General Manager—Finishing and Components | ||

Jeffry N. Quinn is currently our Chief Executive Officer, a director and the Chairman of our Board of Directors. Mr. Quinn served as our interim Chief Executive Officer from November 2015 until his election as Chief Executive Officer in December 2015. Prior to the Business Combination, Mr. Quinn served as President, Chief Executive Officer and Chairman of the Company from inception in May 2013 until June 30, 2014. He is also the founder, Chairman, Chief Executive Officer and Managing Member of Quinpario Partners LLC, and has served in such role since 2012. Prior to forming Quinpario Partners LLC, Mr. Quinn was President, Chief Executive Officer and Chairman of the Board of Solutia Inc. (formerly NYSE: SOA), a global specialty chemical and performance materials company. From 2004 to 2012, Mr. Quinn served as the President and Chief Executive Officer of Solutia, and served as the Chairman of the Board from 2006 to 2012. Mr. Quinn became President and Chief Executive Officer of Solutia after it had filed for bankruptcy in 2003. Over eight years as CEO of Solutia, Mr. Quinn oversaw its transformation from a domestically oriented commodity chemical company to one of the world’s leading specialty chemical firms. Solutia was sold to Eastman Chemical in 2012. Mr. Quinn joined Solutia in 2003 as Executive Vice President, Secretary, and General Counsel. In mid-2003 he added the duties of Chief Restructuring Officer to help prepare the company for its eventual filing for reorganization under Chapter 11 (Solutia emerged from bankruptcy in 2008). During his tenure at Solutia, the company completed a number of divestitures and acquisitions as it reshaped its portfolio of businesses. It also

10

completed a number of debt and equity offerings. Prior to joining Solutia, Mr. Quinn was Executive Vice President, Chief Administrative Officer, Secretary and General Counsel for Premcor Inc. (formerly NYSE: PCO), which at the time was one of the nation’s largest independent refiners. At that time Premcor was a portfolio company of Blackstone Capital Partners, a private equity fund. As general counsel of Premcor, Mr. Quinn was involved in the company’s initial public offering and listing on the New York Stock Exchange in 2002. Premcor was eventually sold to Valero Energy Corporation (NYSE: VLO) in 2005. Prior to Premcor, Mr. Quinn was Senior Vice President-Law & Human Resources, Secretary and General Counsel for Arch Coal, Inc. (NYSE: ACI). Mr. Quinn started at Arch Coal in 1986 when it was known as Arch Mineral Corporation. He became General Counsel in 1989. For the next eleven years, Mr. Quinn was a member of the executive management team that grew Arch from a small regional coal producer to the nation’s second largest coal company. Mr. Quinn was involved in a number of mergers and acquisitions at Arch Coal as well as the company’s initial public offering in 1997. Mr. Quinn is currently a member of the Board of Directors of Tronox Limited (NYSE: TROX), a fully integrated producer and marketer of titanium ore and titanium dioxide pigment, Ferro Corporation (NYSE: FOE), a global supplier of technology-based performance materials and chemicals for manufacturers, and W.R. Grace & Co. (NYSE: GRA), a global supplier of catalysts, engineered and packaging materials and specialty construction chemicals and building materials. Mr. Quinn currently serves as Chairman of the Human Resources and Compensation Committee of Tronox, as a member of the Compensation and Strategy Committees of Ferro and as Chairman of the Compensation Committee and as a member of the Audit, Nominating and Governance and Corporate Responsibility Committees of W.R. Grace. Mr. Quinn is also the Chairman of the Board of Quinpario Acquisition Corp. 2 (NASDAQ: QPACU), a blank check company formed for the purpose of entering into a business combination. Mr. Quinn received both a Bachelor’s degree in Mining Engineering and a Juris Doctorate degree from the University of Kentucky.

A. Craig Ivey has served as our interim President and Chief Operating Officer since January 2016. He is a partner of Quinpario Partners LLC, an investment, operating and management firm based in St. Louis, Missouri, and Vice President - Operations of Quinpario Acquisition Corporation 2, a blank check company. Mr. Ivey was previously Vice President - Operations of Quinpario Acquisition Corp. and served in such position from its inception in May 2013 until its business combination with the Company in June 2014. Prior to July 2012, he served as President and General Manager of the Performance Films Division for Solutia Inc., a global chemical and performance materials company (the Performance Films division of Solutia was a leader in aftermarket window film with annual revenues of $300 million and operations in Europe, Asia and the Americas, and as President and General Manager, Mr. Ivey had responsibility for all commercial, manufacturing, technology, and strategic aspects of the business). Mr. Ivey joined Solutia at the company’s inception in 1997 and possesses over 30 years of manufacturing, supply chain, business and leadership expertise, including service in the Asia Pacific region. Mr. Ivey holds a Bachelors degree in Chemical Engineering from Auburn University. Mr. Ivey has served as a consultant to the Company since December 1, 2015.

Sarah C. Sutton has served as Senior Vice President since January 2016 and as our Chief Financial Officer since April 20, 2015. Prior to joining Jason Industries, Ms. Sutton served as Vice President, Financial Planning and Analysis at Regal-Beloit Corporation, a $3.2 billion global manufacturer of electric motors, generators and controls, as well as mechanical motion control products, from 2011 until April 2015. Ms. Sutton previously served as Chief Financial Officer of A.O. Smith Corporation’s Electrical Products Company (“EPC”), a $700 million global manufacturer of electric motors for residential and commercial applications, from 2002 until EPC was acquired by Regal-Beloit in 2011. Ms. Sutton began her career as an accountant at KPMG, and is a certified public accountant and member of the AICPA. Ms. Sutton earned a Bachelor of Science in administration, with an accounting concentration, from California State University, San Bernardino, and an Executive Master of Business Administration from Northwestern University, Kellogg School of Management.

Thomas L. Doerr, Jr. has served as Vice President since January 2016 and as our General Counsel and Secretary since November 9, 2015. Prior to joining Jason Industries, Mr. Doerr served as Associate General Counsel for The Manitowoc Company, Inc. where he was responsible for overseeing the legal matters for Manitowoc’s crane segment. Mr. Doerr joined Manitowoc in 2006 as legal counsel; in 2008 he expatriated to London, England, and in 2009 to Lyon, France where he was serving as Assistant General Counsel - International and responsible for all legal matters for both Manitowoc’s crane segment and Manitowoc’s foodservice segment in Europe, Middle East, Africa and Asia Pacific. After spending four years abroad, Mr. Doerr moved back to the United States and assumed global legal responsibility for Manitowoc’s crane segment. While at Manitowoc, he was closely involved in numerous of the company’s domestic and international alliances, acquisitions and divestitures. Prior to joining Manitowoc, Mr. Doerr was most recently with the law firm von Briesen & Roper, s.c. in the firm’s Milwaukee office with a broad-based practice focused on both corporate and real estate matters. Mr. Doerr is a graduate of Marquette University Law School and the University of St. Thomas.

John J. Hengel has served as our Vice President—Finance, Treasurer and Assistant Secretary since June 30, 2014 and previously served as Vice President of Finance of Jason Incorporated since 1999. Prior to joining Jason Incorporated, he was a director in the audit and business advisory services practice at PricewaterhouseCoopers LLP from 1992 to 1999. Mr. Hengel is a Certified Public Accountant and a member of both the American and Wisconsin Institutes of Certified Public Accountants. He holds a Bachelor of Science in accounting from Carroll University.

11

Srivas Prasad has served as our Senior Vice President and General Manager—Seating and Acoustics since January 2016. Prior to that, he served as the President of our Seating segment since June 30, 2014 and previously served in the same position of Jason Incorporated since April 2014. Prior to serving as the President of the Seating segment, he served as Vice President—Business Development at Jason Incorporated from 2011 to 2014 and held key leadership positions in Jason Incorporated’s Acoustics segment from 2006 to 2010. Mr. Prasad holds a Bachelor’s degree in engineering from Bangalore University and a Masters in engineering from Lamar University.

Steven G. Carollo has served as our Senior Vice President & General Manager—Finishing and Components since January 2016. Prior to that, he served as the Vice President and General Manager of our Components segment since June 30, 2014 and previously served in the same position of Jason Incorporated since July 2012. Prior to serving as the Vice President and General Manager of the Components segment, he served as Vice President and General Manager at Assembled Products from 2006 to 2013 and held key leadership positions in Jason Incorporated’s Acoustic and Components segments from 1994 to 2006. Mr. Carollo holds a Bachelor’s degree in Accounting from Central Michigan University and will receive his Masters in Business Administration from Notre Dame in May 2016.

12

ITEM 1A. RISK FACTORS

An investment in our securities involves a high degree of risk. You should consider carefully all of the risks described below and all of the other information contained in this report before deciding to invest in our securities. If any of the events or developments described below occur, our business, financial condition and/or results of operations could be negatively affected. In that case, the trading price of our securities could decline, and you could lose all or part of your investment.

Risk Factors Relating to Our Business

We are affected by developments in the industries in which our customers operate.

We derive our revenues largely from customers in the following industry sectors: agricultural, automotive, motorcycles, construction and industrial manufacturing. Factors affecting any of these industries in general, or any of our customers in particular, could adversely affect us because our revenue growth largely depends on the continued growth of our customers’ businesses in their respective industries. These factors include:

| • | seasonality of demand for our customers’ products which may cause our manufacturing capacity to be underutilized for periods of time; |

| • | our customers’ failure to successfully market their products, to gain or retain widespread commercial acceptance of their products or to compete effectively in their industries; |

| • | loss of market share for our customers’ products, which may lead our customers to reduce or discontinue purchasing our products and to reduce prices, thereby exerting pricing pressure on us; |

| • | economic conditions in the markets in which our customers operate, in particular, the United States and Europe, including recessionary periods such as the 2008/2009 global economic downturn; and |

| • | product design changes or manufacturing process changes that may reduce or eliminate demand for the components we supply. |

We expect that future sales will continue to depend on the success of our customers. If economic conditions and demand for our customers’ products deteriorate, we may experience a material adverse effect on our business, operating results and financial condition.

Some of our business segments are cyclical. A downturn or weakness in overall economic activity can have a material negative impact on us.

Historically, sales of products that we manufacture have been subject to cyclical variations caused by changes in general economic conditions. During recessionary periods, we have been adversely affected by reduced demand for our products. In addition, the strength of the economy generally may affect the rates of expansion, consolidation, renovation and equipment replacement in the industries we serve.

Volatility in the prices of raw materials and energy prices and our ability to pass along increased costs to our customers could adversely affect our results of operations.

The prices of raw materials critical to our business and performance, such as steel, are based on global supply and demand conditions. Certain raw materials used by us, including polyurethane foam, vinyl, plastics, steel, polyester fiber, bicomponent fiber and machined fiber are only available from a limited number of suppliers, and it may be difficult to find alternative suppliers at the same or similar costs. Although our contracts and long term arrangements with our customers generally do not expressly allow us to pass through increases in our raw materials, energy costs and other inputs to our customers, we endeavor to discuss price adjustments with our customers on a case by case basis where it makes business sense. While we strive to pass through the price of raw materials to our customers (other than increases in order amounts which are subject to negotiation), we may not be able to do so in the future, and volatility in the prices of raw materials may affect customer demand for certain products. In addition, we, along with our suppliers and customers, rely on various energy sources for a number of activities connected with our business, such as the transportation of raw materials and finished products. Energy and utility prices, including electricity and water prices, and in particular prices for petroleum-based energy sources, are volatile. Increased supplier and customer operating costs arising from volatility in the prices of energy sources, such as increased energy and utility costs and transportation costs, could be passed through to us and we may not be able to increase our product prices sufficiently or at all to offset such increased costs. The impact of any volatility in the prices of energy or the raw materials on which we rely, including the reduction in demand for certain products caused by such price volatility, could result in a loss of revenue and profitability and adversely affect our results of operations.

13

We compete with numerous other manufacturers in each of our segments and competition from these providers may affect the profitability of our business.

The industries we serve are highly competitive. We compete with numerous companies that manufacture finishing, seating, automotive acoustics and components products. Many of our competitors have international operations and significant financial resources and some have substantially greater manufacturing, research and design and marketing resources than us. These competitors may, among others:

| • | respond more quickly to new or emerging technologies; |

| • | have greater name recognition, critical mass or geographic market presence; |

| • | be better able to take advantage of acquisition opportunities; |

| • | adapt more quickly to changes in customer requirements; |

| • | devote greater resources to the development, promotion and sale of their products; |

| • | be better positioned to compete on price for their products, due to any combination of low-cost labor, raw materials, components, facilities or other operating items, or willingness to make sales at lower margins than us; |

| • | consolidate with other competitors in the industry which may create increased pricing and competitive pressures on our business; and |

| • | be better able to utilize excess capacity which may reduce the cost of their products or services. |

Competitors with lower cost structures may have a competitive advantage when bidding for business with our customers. We also expect our competitors to continue to improve the performance of their current products or services, to reduce prices of their existing products or services and to introduce new products or services that may offer greater performance and improved pricing. Additionally, we may face competition from new entrants to the industry in which we operate. Any of these developments could cause a decline in sales and average selling prices, loss of market share of our products or profit margin compression.

We face risks related to sales through distributors and other third parties.

We sell a portion of our products through third parties such as distributors, agents and channel partners (collectively referred to as distributors). Using third parties for distribution exposes us to many risks, including competitive pressure, concentration, credit risk, and compliance risks. Distributors may sell products that compete with our products, and we may need to provide financial and other incentives to focus distributors on the sale of our products. We may rely on one or more key distributors for a product, and the loss of these distributors could reduce our revenue. Distributors may face financial difficulties, including bankruptcy, which could harm our collection of accounts receivable and financial results. Violations of FCPA or similar laws by distributors or other third-party intermediaries could have a material impact on our business. Failing to manage risks related to our use of distributors may reduce sales, increase expenses, and weaken our competitive position.

We may not be able to maintain our engineering, technological and manufacturing expertise.

The markets for our products are characterized by changing technology and evolving process development. The continued success of our business will depend upon our ability to:

| • | hire, retain and expand our pool of qualified engineering and technical personnel; |

| • | maintain technological leadership in our industry; |

| • | successfully anticipate or respond to changes in manufacturing processes in a cost-effective and timely manner; and |

| • | successfully anticipate or respond to changes in cost to serve in a cost-effective and timely manner. |

We cannot be certain that we will develop the capabilities required by our customers in the future. The emergence of new technologies, industry standards or customer requirements may render our equipment, inventory or processes obsolete or uncompetitive. We may have to acquire new technologies and equipment to remain competitive. The acquisition and implementation of new technologies and equipment may require us to incur significant expense and capital investment, which could reduce our margins and affect our operating results. When we establish or acquire new facilities, we may not be able to maintain or develop our engineering, technological and manufacturing expertise due to a lack of trained personnel, effective training of new staff or technical difficulties with machinery. Failure to anticipate and adapt to customers’ changing technological needs and requirements or to hire and retain a sufficient number of engineers and maintain engineering, technological and manufacturing expertise may have a material adverse effect on our business.

14

We may not be able to manage the expansion of our operations effectively in order to achieve projected levels of growth.

Our business plan calls for further expansion over the next several years. We anticipate that further development of our infrastructure and an increase in the number of our employees will be required to achieve our planned broadening of our product offerings and client base, improvements in our machines and materials used in our machines, and our planned international growth. In particular, we must increase our marketing and services staff to support new marketing and service activities and to meet the needs of both new and existing customers. Our future success will depend in part upon the ability of our management to manage our growth effectively. If our management is unsuccessful in meeting these challenges, we may not be able to achieve our anticipated level of growth or profitability, which would adversely affect our business and results of operations.

We may be unable to realize the expected benefits of capital expenditures, which could adversely affect our profitability and operations.

We expect to continue to invest significant amounts of money in our business through capital expenditures to support new facilities, the expansion of existing facilities, purchases of production equipment and acquisitions. There can be no assurance that these investments will generate any specific return on investment.

We may encounter difficulties in completing or integrating acquisitions, which could adversely affect our operating results.

We expect to expand our presence in new end markets, expand our capabilities and acquire new customers, some of which may occur through acquisitions. These transactions may involve acquisitions of entire companies, portions of companies, the entry into joint ventures and acquisitions of businesses or selected assets. Potential challenges related to our acquisitions and joint ventures include:

| • | paying an excessive price for acquisitions and incurring higher than expected acquisition costs; |

| • | difficulty in integrating acquired operations, systems, assets and businesses; |

| • | difficulty in implementing financial and management controls, reporting systems and procedures; |

| • | difficulty in maintaining customer, supplier, employee or other favorable business relationships of acquired operations and restructuring or terminating unfavorable relationships; |

| • | ensuring sufficient due diligence prior to an acquisition and addressing unforeseen liabilities of acquired businesses; |

| • | making acquisitions in new end markets, geographies or technologies where our knowledge or experience is limited; |

| • | failing to realize the benefits from goodwill and intangible assets resulting from acquisitions which may result in write-downs; |

| • | failing to achieve anticipated business volumes; and |

| • | making acquisitions which force us to divest other businesses. |

Any of these factors could prevent us from realizing the anticipated benefits of an acquisition, including additional revenue, operational synergies and economies of scale. Our failure to realize the anticipated benefits of acquisitions could adversely affect our business and operating results.

Acquisitions, expansions or infrastructure investments may require us to increase our level of indebtedness or issue additional equity.

Should we desire to consummate significant additional acquisition opportunities, undertake significant additional expansion activities or make substantial investments in our infrastructure, our capital needs would increase and we may need to increase available borrowings under our credit facilities or access public or private debt and equity markets. There can be no assurance, however, that we will be successful in raising additional debt or equity on terms that we would consider acceptable.

An increase in the level of indebtedness could, among other things:

| • | make it difficult for us to obtain financing in the future for acquisitions, working capital, capital expenditures, debt service requirements or other purposes; |

| • | limit our flexibility in planning for or reacting to changes in our business; |

| • | affect our ability to pay dividends; |

| • | make us more vulnerable in the event of a downturn in our business; and |

15

| • | affect certain financial covenants with which we must comply in connection with our credit facilities. |

Additionally, a further equity issuance could dilute the ownership interest of existing stockholders.

Our goodwill and other intangible assets represent a substantial amount of our total assets. A decline in future operating performance at one or more of our reporting units could result in the further impairment of goodwill or other intangible assets, which could have a material adverse effect on our financial condition and results of operations.

At December 31, 2015, goodwill and other intangible assets totaled $264.1 million, or approximately 37% of our total assets. The goodwill results from our acquisitions, representing the excess of cost over the fair value of the net tangible and other identifiable intangible assets we have acquired. We assess annually whether there has been impairment in the value of our goodwill. If future operating performance at one or more of our reporting units were to fall significantly below current levels, we could be required to recognize a non-cash charge to operating earnings for goodwill or record an impairment charge related to other intangible assets. In the fourth quarter of 2015, the Company recorded charges of $58.8 million and $35.3 million for the impairment of goodwill and other intangible assets, respectively. Given the continued significance of the Company’s goodwill and intangible assets, any significant goodwill or intangible asset impairment could reduce earnings in such period and have a material adverse effect on our financial condition and results of operations.

Divestitures and discontinued operations could negatively impact our business, and contingent liabilities from businesses that we sell could adversely affect our financial results.

As part of our portfolio management process, we review our operations for businesses which may no longer be aligned with our strategic initiatives and long-term objectives. Divestitures pose risks and challenges that could negatively impact our business. For example, when we decide to sell a business, we may be unable to do so on satisfactory terms and within our anticipated time-frame, and even after reaching a definitive agreement to sell a business, the sale may be subject to satisfaction of pre-closing conditions, which may not be satisfied, as well as regulatory and governmental approvals, which may prevent us from completing a transaction on acceptable terms. In addition, the impact of the divestiture on our revenue and net earnings may be larger than projected, which could distract management, and disputes may arise with buyers. Dispositions may also involve continued financial involvement, as we may be required to retain responsibility for, or agree to indemnify buyers against contingent liabilities related to businesses sold, such as lawsuits, tax liabilities, product liability claims or environmental matters. Under these types of arrangements, performance by the divested businesses or other conditions outside our control could affect our future financial results.

If we fail to develop new and innovative products or if customers in our markets do not accept them, our results could be negatively affected.

Our products must be kept current to meet our customers’ needs. To remain competitive, we therefore must develop new and innovative products on an ongoing basis. If we fail to make innovations or the market does not accept our new products, our sales and results would likely suffer. We invest significantly in the research and development of new products. These expenditures do not always result in products that will be accepted by the market. To the extent they do not, whether as a function of the product or the business cycle, we will have increased expenses without significant sales to benefit us. Failure to develop successful new products may also cause potential customers to purchase competitors’ products, rather than invest in products manufactured by us.

The potential impact of failing to deliver products on time could increase the cost of the products.

In most instances, we guarantee that we will deliver a product by a scheduled date. If we subsequently fail to deliver the product as scheduled, we may be held responsible for cost impacts and/or other damages resulting from any delay. To the extent that these failures to deliver may occur, the total damages for which we could be liable could significantly increase the cost of the products; as such, we could experience reduced profits or, in some cases, a loss for that contract. Additionally, failure to deliver products on time could result in damage to customer relationships, the potential loss of customers, and reputational damage which could impair our ability to attract new customers.

Increasing costs of doing business in many countries in which we operate may adversely affect our business and financial results.

Increasing costs such as labor and overhead costs in the countries in which we operate may erode our profit margins and compromise our price competitiveness. Historically, the low cost of labor in certain of the countries in which we operate has been a competitive advantage but labor costs in these countries, such as China, have been increasing. Our profitability also depends on our ability to manage and contain our other operating expenses such as the cost of utilities, factory supplies, factory space costs, equipment rental, repairs and maintenance and freight and packaging expenses. In the event we are unable to manage any increase in our labor and other operating expenses in an environment where revenue does not increase proportionately, our financial results would be adversely affected.

16

Our international scope will require us to obtain financing in various jurisdictions.

We operate manufacturing facilities in the United States and 14 foreign countries, which creates financing challenges for us. These challenges include navigating local legal and regulatory requirements associated with obtaining debt or equity financing in the respective foreign jurisdictions in which we operate. In the event that we are not able to obtain financing on satisfactory terms in any of these jurisdictions, it could significantly impair our ability to run our foreign operations on a cost effective basis or to grow such operations. Failure to manage such challenges may adversely affect our business and results of operations.

We have operations in many countries and such operations may be subject to a number of risks specific to these countries.

Our international operations across many different jurisdictions may be subject to a number of risks specific to these countries, including:

| • | less flexible employee relationships which can be difficult and expensive to terminate; |

| • | labor unrest; |

| • | political and economic instability (including war and acts of terrorism); |

| • | inadequate infrastructure for our operations (i.e., lack of adequate power, water, transportation and raw materials); |

| • | health concerns and related government actions; |

| • | risk of governmental expropriation of our property; |

| • | less favorable, or relatively undefined, intellectual property laws; |

| • | unexpected changes in regulatory requirements and laws; |

| • | longer customer payment cycles and difficulty in collecting trade accounts receivable; |