SECOND QUARTER 2014 Supplemental Operating & Financial Data Exhibit 99.2 Starwood Waypoint Residential Trust (“SWAY”) acquires, renovates, leases, maintains and manages single family homes. We also invest in non-performing loans to supplement growth and seek optimal resolutions for each loan. Our mission is to reinvent the home rental experience by providing quality homes, great service and rewarding lease programs that offer valuable benefits to our residents while generating attractive returns for our investors. |

Table of Contents Pages ABOUT SWAY 1-6 FINANCIAL INFORMATION Selected Financial & Other Information 7 Consolidated Balance Sheets 8 Consolidated Statements of Operations 9 FFO & Core FFO 10 NOI 11 CAPITAL MARKETS 12 PORTFOLIO INFORMATION Total Rental Homes Portfolio 13-14 Leasing Statistics 15 Non-Performing Loan Portfolio 16 TRANSACTION ACTIVITY 17 DEFINITIONS AND RECONCILIATIONS 18-19 |

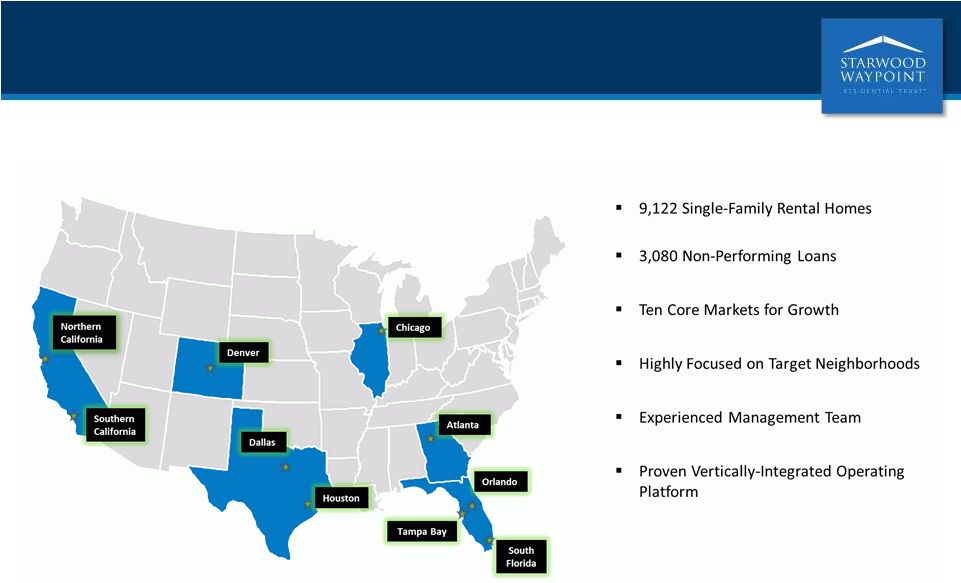

1 ABOUT SWAY Attractive Markets for Growth |

ABOUT SWAY Hybrid Business Model Stable cash flow from a growing SFR portfolio and income generated from our NPL business supports our Board’s approval of an initial dividend. 2 Stability Growth Growing book of cash-flowing assets Fully supports $0.14 per share dividend Homes in renovation and lease-up phase Provides meaningful upside opportunities to enhance value and downstream cash flow Attractive channel to acquire SFRs at 20%- 30% discount to broker price opinion (“BPO”) Alternative resolutions have potential for high return on equity |

3 SFRs (77% of portfolio) (1) NPLs (23% of portfolio) (1) Number of Homes (2) 9,122 Aggregate Investment ($mm) (4) $1,345 Aggregate Investment per Home (4) $147,434 Average Monthly Rent per Leased Home (5) $1,416 Percent of Total Homes That Are Leased (%) 77.5% Percent of Homes Owned 180 Days or Longer That Are Leased (%) (7) 94.9% Percent of 90+ Days Rent Ready Homes That Are Leased (%) (7) 98.8% Number of Loans (3) 3,080 Total Purchase Price ($mm) $397.0 Total Unpaid Principal Balance (“UPB”) ($mm) $681.7 Total BPO ($mm) $635.3 Weighted Average Loan-to-Value (“LTV”) (6) 135.8% Purchase Price as a Percentage of UPB 58.2% Purchase Price as a Percentage of BPO 62.5% SWAY has a high quality and diverse portfolio of SFRs and NPLs ABOUT SWAY Portfolio Overview Note: As of June 30, 2014. (1) (2) (3) (4) (5) (6) (7) Excludes 277 unsecured, second and third liens with an aggregate purchase price of $1.9 million. Based on aggregate investment for SFRs and purchase price for NPLs. Excludes 285 homes that we did not intend to hold for the long term. Includes acquisition costs and actual and estimated upfront renovation costs. Actual renovation costs may exceed estimated renovation costs, and we may acquire homes in the future with different characteristics that result in higher renovation costs. Represents average monthly contractual cash rent as of June 30, 2014. Average monthly cash rent is presented before rent concession and credits (“Waypoints”). To date, rent concessions and Waypoints have been utilized on a limited basis and have not had a significant impact on our average monthly rent. If the use of rent concessions and Waypoints or other leasing incentives increases in the future, they may have a greater impact by reducing the average monthly rent we receive from leased homes. Weighted average LTV is based on the ratio of UPB to BPO weighted by UPB as of the respective acquisition dates. References to “rent ready homes” refer to homes that have both completed renovations and been deemed, pursuant to an inspection from one of our agents, to be in a condition to be rented. Our policy is to have the agent perform this inspection promptly after the renovations have been completed. |

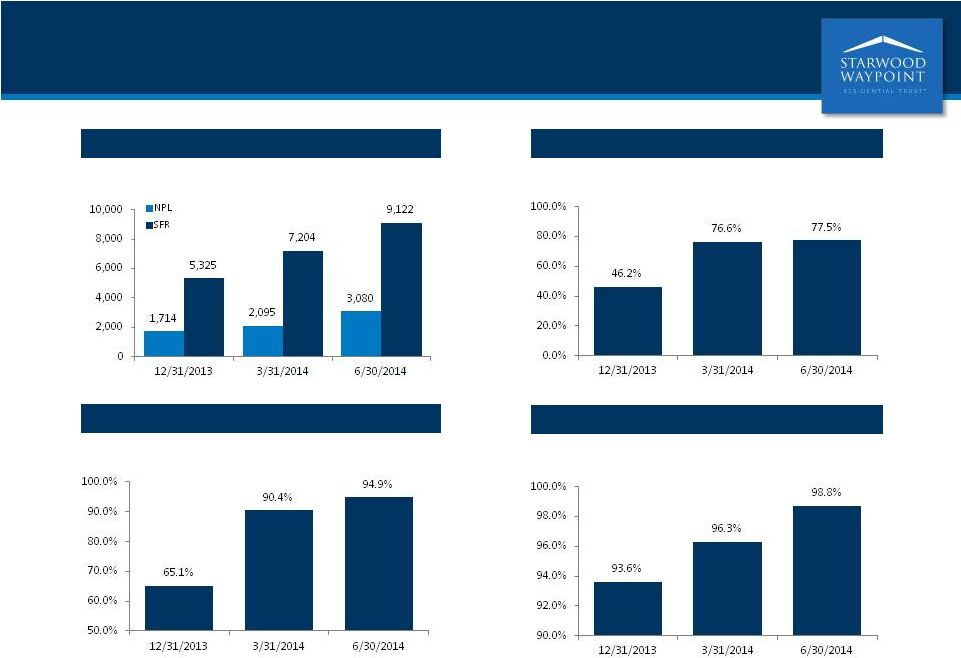

4 ABOUT SWAY Q2 Highlights and Recent Developments (1) Portfolio Growth Increased SFR portfolio by 27% to 9,122 homes Acquired a $117 million portfolio of 1,441 NPLs at 68.2% of BPO Purchased 1,294 NPLs in August for $202 million at 72.2% of BPO Estimated Net Asset Value (“NAV”) per share increased to $31.84; book value per share of $27.97 as of June 30, 2014 Leasing Momentum 180-Day Owned Portfolio: 94.9% up from 90.4% in Q1 90-Day Rent-Ready Portfolio: 98.8% up from 96.3% in Q1 Portfolio-wide lease percentage: 77.5% up from 76.6% in Q1 Grew SFR revenue 74% quarter-over-quarter Expanded Capacity Upsized our two credit facilities by a total of $650 million in Q2 Raised $230 million in gross proceeds from convertible note offering (July) Total financing capacity now $1.73 billion with convertible debt as of July 2014 Positive Results Achieved positive Q2 Core Funds from Operations (“FFO”) of $3.0 million or $0.08 per share, an $8.5 million or $0.22 per share increase over reported Q1 SWAY Board approves initial dividend of $0.14 per share Achieved stabilized net operating income (“NOI”) margin of 65.1% (1) Core FFO, NOI and Estimated NAV are non-GAAP measures. For a definition of these non-GAAP measures, please refer to pages 18 and 19. |

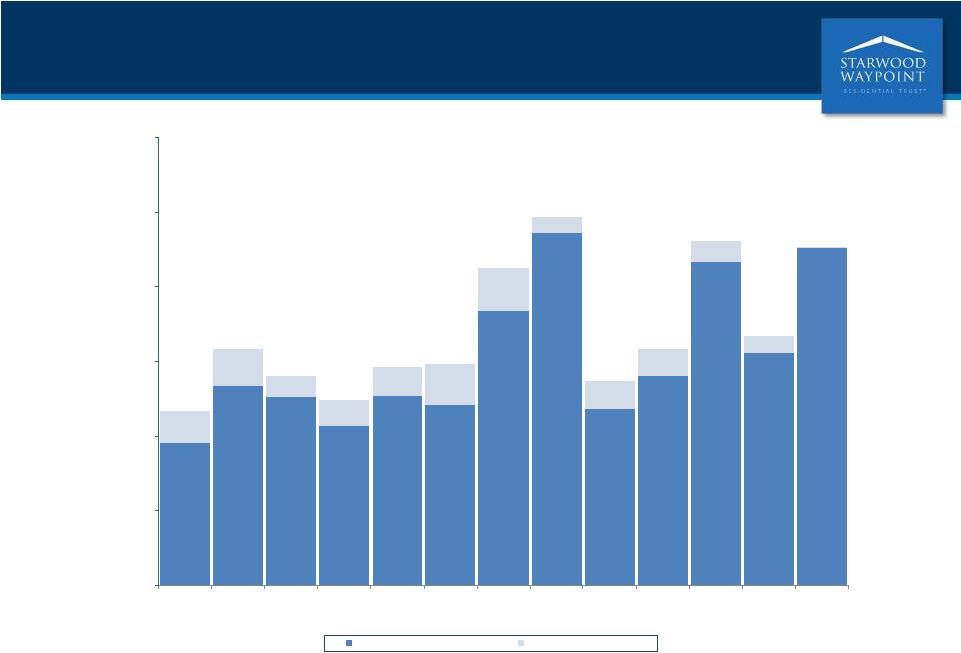

Total SFRs and NPLs (1),(2) % Leased: Total Rental Portfolio 5 ABOUT SWAY Robust Growth, Well Executed (1) Excludes 285, 154, and 146 homes that we did not intend to hold for the long term as of June 30, 2014, March 30, 2014 and December 31, 2013, respectively. (2) Excludes 277 unsecured, second and third liens as of June 30, 2014. % Leased: Homes Owned 180 Days or Longer % Leased: Homes 90 Days Past Rent Ready |

ABOUT SWAY Financing Overview Added $650 million of capacity, with $729 million undrawn as of June 30, 2014 2014 Financing Activity (1) Capacity (1) ($ in millions) Total Capacity Drawn NPL: $252 million Undrawn NPL: $248 million $519 $252 6 SFR Drawn: $519 million Undrawn SFR: $481 million (1) As of June 30, 2014. NPL SFR Upsized SFR Credit Facility by $500 million in Q2 to total capacity of $1 billion Upsized NPL Credit Facility by $150 million in Q2 to total capacity of $500 million $500 $1,000 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 Drawn |

7 FINANCIAL INFORMATION Selected Financial & Other Information (1) Please refer to page 18 for a definition of Core FFO. Core FFO is a non-generally accepted accounting principle (“GAAP”) measure. For a reconciliation of Core FFO to net loss attributable to common shareholders determined in accordance with GAAP, please refer to page 10. (2) Stabilized portfolio NOI margin and Leased home portfolio NOI are non-GAAP measures. For a reconciliation of stabilized portfolio NOI margin and leased home portfolio NOI to net loss attributable to common shareholders determined in accordance with GAAP, please refer to page 19. (3) Please refer to page 18 for a definition of stabilized homes. (4) Excludes 285, 154, and 146 homes that we did not intend to hold for the long term as of June 30, 2014, March 30, 2014 and December 31, 2013, respectively. (5) Three Months Ended Six Months Ended ($ in thousands, except share and per share data) June 30, 2014 June 30, 2014 (unaudited) (unaudited) Total revenues 34,332 $ 55,833 $ Net loss attributable to common shareholders (12,116) $ (27,424) $ Core FFO (1) 2,978 $ (2,734) $ Per common share - diluted Net earnings attributable to common shareholders (0.31) $ (0.70) $ Core FFO (1) 0.08 $ (0.07) $ Weighted Average Shares Outstanding, Basic and Diluted 39,079,365 39,091,796 (2) 65.1% 62.3% (2) 66.0% 63.9% June 30, 2014 March 31, 2014 December 31, 2013 Home Count: (3) 7,076 5,142 2,666 Non-stabilized homes 2,046 2,062 2,659 Total Homes (4) 9,122 7,204 5,325 Leased Percentages (5) 95.0% 96.4% 91.6% Homes 90 days past rent ready 98.8% 96.3% 93.6% Homes owned 180 days or longer 94.9% 90.4% 65.1% (4) 77.5% 76.6% 46.2% As of Stabilized homes SWAY targets leased percentages on stabilized homes to be in the range of 94% to 96%. Leased Home Portfolio NOI Margin Stabilized Portfolio NOI Margin Stabilized homes Total rental portfolio |

8 FINANCIAL INFORMATION Consolidated Balance Sheets ($ in thousands) June 30, 2014 December 31, 2013 (unaudited) ASSETS Investments in real estate Land 272,610 $ 140,076 $ Building and improvements 1,170,016 604,839 Total investment in properties 1,442,626 744,915 Less: accumulated depreciation (17,525) (5,730) Investment in real estate properties, net 1,425,101 739,185 Real estate held for sale, net 13,383 10,168 Total investments in real estate, net 1,438,484 749,353 Non-performing loans 178,311 214,965 Non-performing loans (fair value option) 218,797 - Resident and other receivables, net 8,029 1,261 Cash and cash equivalents 17,151 44,613 Restricted cash 35,261 3,331 Deferred financing costs, net 13,318 - Other assets 22,709 4,885 Total assets 1,932,060 $ 1,018,408 $ LIABILITIES AND EQUITY Liabilities: Credit facilities 770,541 $ - $ Accounts payable and accrued expenses 58,199 22,434 Resident security deposits and prepaid rent 11,742 3,918 Total liabilities 840,482 26,352 Equity: Shareholders' equity: Common shares, at par 391 - Additional paid-in capital 1,117,026 1,018,267 Accumulated deficit (26,503) (27,848) Total shareholders' equity 1,090,914 990,419 Non-controlling interests 664 1,637 Total equity 1,091,578 992,056 Total liabilities and equity 1,932,060 $ 1,018,408 $ As of |

9 FINANCIAL INFORMATION Consolidated Statements of Operations ($ in thousands, except share and per share data) 2014 2013 2014 2013 Revenues: Rental revenues 23,602 $ 2,889 $ 37,367 $ 4,013 $ Other property revenues 890 64 1,369 105 �� Realized gain on non-performing loans, net 3,357 1,114 5,200 1,473 Realized gain on loan conversions, net 6,483 - 11,897 - Total revenues 34,332 4,067 55,833 5,591 Expenses: Property operating and maintenance 7,791 1,161 13,823 1,711 Real estate taxes and insurance 4,468 720 7,611 1,343 Mortgage loan servicing costs 5,139 2,378 10,021 2,378 Non-performing loan management fees and expenses 1,871 1,575 4,286 2,425 General and administrative 4,444 3,834 9,814 5,645 Share-based compensation 2,130 - 2,459 - Investment management fees 3,993 - 6,750 - Separation costs - - 3,543 - Acquisition fees expensed and property management engagement costs 186 290 447 588 Interest expense, including amortization 5,191 - 6,691 - Depreciation and amortization 7,243 767 12,716 1,424 Finance related expenses and write-off of loan costs 5,441 - 5,441 - Impairment of real estate 1,233 192 2,067 247 Total expenses 49,130 10,917 85,669 15,761 Loss before other income, income tax expense and non-controlling interests (14,798) (6,850) (29,836) (10,170) Other income (expense) Realized (loss) gain on sales of investments in real estate, net (56) 578 (201) 665 Unrealized gain on non-performing loans, net 3,641 - 3,641 - Loss on derivative financial instruments, net (470) - (470) - Total other income (expense) 3,115 578 2,970 665 Loss before income tax expense and non-controlling interests (11,683) (6,272) (26,866) (9,505) Income tax expense 350 46 485 208 Net loss (12,033) (6,318) (27,351) (9,713) Net (income) loss attributable to non-controlling interests (83) 10 (73) 16 Net loss attributable to common shareholders (12,116) $ (6,308) $ (27,424) $ (9,697) $ Net loss per share - basic and diluted (0.31) $ (0.16) $ (0.70) $ (0.25) $ Number of shares used in per share computations - basic and diluted 39,079,365 39,110,969 39,091,796 39,110,969 Six Months Ended June 30, Three Months Ended June 30, (unaudited) (unaudited) |

10 FINANCIAL INFORMATION FFO & Core FFO (1) (1) Please refer to page 18 for definitions of FFO and Core FFO. Commencing with the three months ended June 30, 2014, we have changed our definition of Core FFO to include adjustments related to share-based compensation and exclude adjustments related to acquisition pursuit costs. ($ in thousands, except share and per share data) 2014 2013 2014 2013 Reconciliation of net loss to FFO Net loss attributable to common shareholders (12,116) $ (6,308) $ (27,424) $ (9,697) $ Add (deduct) adjustments to net loss to get to FFO: Depreciation and amortization on real estate assets 7,243 767 12,716 1,424 Non-controlling interests 83 (10) 73 (16) Subtotal - FFO (4,790) (5,551) (14,635) (8,289) Add (deduct) adjustments to FFO to get to Core FFO: Share-based compensation 2,130 - 2,459 - Separation costs - - 3,543 - Acquisition fees expensed and property management engagement costs 186 290 447 588 Write-off of loan costs 5,032 - 5,032 - Loss on derivative financial instruments, net 470 - 470 - Amortization of derivative financial instruments cost (50) - (50) - Core FFO 2,978 $ (5,261) $ (2,734) $ (7,701) $ Core FFO per share - basic and diluted 0.08 $ (0.13) $ (0.07) $ (0.20) $ Weighted average shares - basic and diluted 39,079,365 39,110,969 39,091,796 39,110,969 Six Months Ended June 30, Three Months Ended June 30, (unaudited) (unaudited) |

11 FINANCIAL INFORMATION NOI (1) (1) Total Stabilized Portfolio NOI, Total Non-Stabilized Portfolio NOI, Total NPL NOI, Total NOI and Total Leased Home Portfolio NOI are non-GAAP measures. For a reconciliation of these non-GAAP measures to net loss attributable to common shareholders determined in accordance with GAAP, please refer to Page 19. (2) Allowance for doubtful accounts (“bad debt”) is included in property operating and maintenance in the consolidated statements of operations in accordance with GAAP. However, we believe bad debt represents revenue lost and not an operating expense to the portfolio so for purposes of calculating margins we treat bad debt as a reduction of revenue. (3) Property operating expenses is defined as property operating and maintenance expense plus real estate taxes and insurance less bad debt. (4) Margin is calculated as total stabilized portfolio NOI or total leased home portfolio NOI divided by total rental revenues. ($ in thousands, unaudited) Stabilized Portfolio Non-Stabilized Portfolio NPL Total Stabilized Portfolio Non-Stabilized Portfolio NPL Total Revenues Rental revenues 23,602 $ - $ - $ 23,602 $ 37,367 $ - $ - $ 37,367 $ Less: Allowance for doubtful accounts (2) (614) - - (614) (1,123) - - (1,123) Total rental revenues 22,988 - - 22,988 36,244 - - 36,244 Other property revenues 890 - - 890 1,369 - - 1,369 Realized gain on non-performing loans, net - - 3,357 3,357 - - 5,200 5,200 Realized gain on loan conversions, net - - 6,483 6,483 - - 11,897 11,897 Unrealized gain on non-performing loans, net - - 3,641 3,641 - - 3,641 3,641 Total revenues as adjusted 23,878 - 13,481 37,359 37,613 - 20,738 58,351 Expenses Property operating expenses (3) 8,919 2,726 - 11,645 15,022 5,289 - 20,311 Mortgage loan servicing costs - - 5,139 5,139 - - 10,021 10,021 Total expenses 8,919 2,726 5,139 16,784 15,022 5,289 10,021 30,332 Total NOI 14,959 $ (2,726) $ 8,342 $ 20,575 $ 22,591 $ (5,289) $ 10,717 $ 28,019 $ Stabilized portfolio NOI margin (4) 65.1% 62.3% Leased Home Portfolio Leased Home Portfolio Total stabilized portfolio NOI 14,959 $ 22,591 $ Add: Property operating expenses on vacant stabilized homes 221 576 Total leased home portfolio NOI 15,180 $ 23,167 $ Leased home portfolio NOI margin (4) 66.0% 63.9% Three Months Ended June 30, 2014 SFR Six Months Ended June 30, 2014 SFR |

12 Capital Markets (1) Maturity dates include extension terms. (2) Please refer to page 18 for a definition of enterprise value. As of June 30, 2014 ($ in thousands, except share and per share data) Debt Maturities (1) Credit Facility - SFR Credit Facility - NPL Total Security Shares Price Value 2014 - $ - $ - $ Common shares 39,007,239 26.21 $ 1,022,380 $ 2015 - - - 2016 - 251,599 251,599 2017 - - - 2018 518,942 - 518,942 Total debt to enterprise value (2) 43.4% Thereafter - - - Total debt to total assets 39.9% Total 518,942 $ 251,599 $ 770,541 $ Weighted average interest rate 3.14% 3.15% 3.14% Weighted average remaining maturity in years 3.6 2.2 3.1 Market equity Debt Debt Metrics |

13 PORTFOLIO INFORMATION Total Rental Homes Portfolio – June 30, 2014 (1) Excludes 285 homes that we did not intend to hold for the long-term. (2) Includes acquisition costs and actual and estimated upfront renovation costs. Actual renovation costs may exceed estimated renovation costs, and we may acquire homes in the future with different characteristics that result in higher renovation costs. Markets Stabilized Homes Non- Stabilized Homes Total Homes (1) Total Homes Leased (%) Average Acquisition Cost per Home Average Investment per Home (2) Aggregate Investment ($ in millions) Average Home Size (sq. ft.) Weighted Average Age (year) Average Monthly Rent Per Leased Home (3) Atlanta 1,698 601 2,299 71.1% 95,551 $ 117,265 $ 269.6 $ 1,909 22 1,155 $ South Florida 1,429 320 1,749 82.1% 133,741 $ 158,740 $ 277.7 1,588 44 1,557 $ Houston 959 190 1,149 79.5% 126,273 $ 140,974 $ 162.0 2,060 28 1,489 $ Tampa 763 209 972 83.2% 106,884 $ 124,699 $ 121.2 1,476 40 1,250 $ Dallas 662 253 915 70.5% 127,312 $ 146,091 $ 133.7 2,050 22 1,457 $ Chicago 316 139 455 76.0% 121,385 $ 148,162 $ 67.4 1,555 41 1,662 $ Denver 211 130 341 63.9% 183,932 $ 212,859 $ 72.6 1,512 31 1,708 $ Southern California 267 73 340 82.9% 235,913 $ 247,210 $ 84.1 1,617 36 1,791 $ Orlando 264 63 327 83.8% 118,158 $ 137,110 $ 44.8 1,644 37 1,295 $ Phoenix 206 42 248 83.9% 140,329 $ 158,213 $ 39.2 1,543 39 1,190 $ Northern California 218 26 244 89.3% 216,462 $ 230,903 $ 56.3 1,494 45 1,727 $ Las Vegas 42 - 42 95.2% 155,717 $ 167,481 $ 7.0 1,966 27 1,296 $ California Valley 41 - 41 100.0% 226,226 $ 227,085 $ 9.3 1,728 25 1,612 $ Total/Average 7,076 2,046 9,122 77.5% 127,087 $ 147,434 $ 1,344.9 $ 1,760 32 1,416 $ Status Total Homes (1) Total Homes Leased (%) Average Acquisition Cost Average Investment per Home (2) Aggregate Investment ($ in millions) Average Home Size (sq. ft.) Weighted Average Age (year) Leased Rent Stabilized 7,076 95.0% 127,126 $ 146,053 $ 1,033.5 1,746 32 1,413 $ Non-Stabilized 2,046 16.6% 126,952 $ 152,210 $ 311.4 1,811 32 1,482 $ Total/Average 9,122 77.5% 127,087 $ 147,434 $ 1,344.9 $ 1,760 32 1,416 $ (3) Represents average monthly contractual cash rent. Average monthly cash rent is presented before rent concession and Waypoints. To date, rent concessions and Waypoints have been utilized on a limited basis and have not had a significant impact on our average monthly rent. If the use of rent concessions and Waypoints or other leasing incentives increases in the future, they may have a greater impact by reducing the average monthly rent we receive from leased homes. $ |

14 PORTFOLIO INFORMATION Total Rental Homes Portfolio – June 30, 2014 (cont’d) $95.6 $133.7 $126.3 $106.9 $127.3 $121.4 $183.9 $235.9 $118.2 $140.3 $216.5 $155.7 $226.2 $21.7 $25.0 $14.7 $17.8 $18.8 $26.8 $29.0 $11.3 $18.9 $17.9 $14.4 $11.8 $0.9 $117.3 $158.7 $141.0 $124.7 $146.1 $148.2 $212.9 $247.2 $137.1 $158.2 $230.9 $167.5 $227.1 $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 Atlanta South Florida Houston Tampa Dallas Chicago Denver Southern California Orlando Phoenix Northern California Las Vegas California Valley Average Investment per Home ($ in thousands) Average Acquisition Cost per Home Estimated Renovation Costs |

Average Average Total Monthly Monthly Number of Number of Percent Rent per Number of Percent Rent per Markets Homes (1) Homes Leased Leased Home (2) Homes Leased Leased Home (2) Atlanta 2,299 1,292 97.6% 1,140 $ 1,213 93.0% 1,138 $ South Florida 1,749 1,143 99.4% 1,552 $ 1,430 94.0% 1,553 $ Houston 1,149 759 99.1% 1,478 $ 823 94.5% 1,470 $ Tampa 972 573 99.1% 1,229 $ 654 95.2% 1,218 $ Dallas 915 481 99.6% 1,436 $ 484 96.7% 1,422 $ Chicago 455 278 97.8% 1,653 $ 261 95.0% 1,651 $ Denver 341 149 99.3% 1,700 $ 161 97.5% 1,704 $ Southern California 340 230 96.5% 1,799 $ 231 95.7% 1,814 $ Orlando 327 199 100.0% 1,308 $ 222 98.6% 1,314 $ Phoenix 248 176 100.0% 1,181 $ 152 97.4% 1,186 $ Northern California 244 192 100.0% 1,714 $ 195 97.9% 1,706 $ Las Vegas 42 36 100.0% 1,309 $ 42 95.2% 1,296 $ California Valley 41 37 100.0% 1,589 $ 41 100.0% 1,612 $ Total/Average 9,122 5,545 98.8% 1,406 $ 5,909 94.9% 1,413 $ Homes 90 Days Past Rent Ready Homes Owned 180 Days or Longer 15 PORTFOLIO INFORMATION Leasing Statistics – June 30, 2014 97.6% 99.4% 99.1% 99.1% 99.6% 97.8% 99.3% 96.5% 100.0% 100.0% 100.0% 100.0% 100.0% 93.0% 94.0% 94.5% 95.2% 96.7% 95.0% 97.5% 95.7% 98.6% 97.4% 97.9% 95.2% 100.0% 82.0% 84.0% 86.0% 88.0% 90.0% 92.0% 94.0% 96.0% 98.0% 100.0% 102.0% Atlanta South Florida Houston Tampa Dallas Chicago Denver Southern California Orlando Phoenix Northern California Las Vegas California Valley Homes 90 Days Past Rent Ready Homes Owned 180 Days or Longer (1) Excludes 285 homes that we did not intend to hold for the long-term. (2) Represents average monthly contractual cash rent. Average monthly cash rent is presented before rent concession and Waypoints. To date, rent concessions and Waypoints have been utilized on a limited basis and have not had a significant impact on our average monthly rent. If the use of rent concessions and Waypoints or other leasing incentives increases in the future, they may have a greater impact by reducing the average monthly rent we receive from leased homes. |

16 PORTFOLIO INFORMATION Non-Performing Loan Portfolio – June 30, 2014 Total Loan Purchase Price Total UPB Total BPO Purchase Price Purchase Price Weighted State Count (1),(2) ($ in millions) ($ in millions) ($ in millions) as % of UPB as % of BPO Average LTV (3) Florida 762 94.4 $ 187.5 149.0 50.3% 63.3% 152.9% Illinois 373 47.8 76.0 74.3 62.8% 64.3% 141.0% Arizona 230 19.9 33.8 29.4 58.7% 67.5% 198.0% Wisconsin 207 17.4 24.2 27.7 71.6% 62.8% 114.0% New York 165 32.6 62.8 64.6 51.8% 50.4% 114.0% California 148 42.9 60.8 68.6 70.6% 62.6% 100.4% Indiana 152 10.8 15.1 17.1 71.9% 63.5% 109.8% New Jersey 144 20.7 44.0 37.7 47.2% 54.9% 141.6% Maryland 100 17.9 31.3 26.6 57.1% 67.1% 132.3% Pennsylvania 74 6.9 11.7 10.5 58.8% 65.2% 137.7% Georgia 65 8.0 13.2 12.2 60.8% 66.0% 131.0% Other 660 77.7 121.3 117.6 64.1% 66.0% 124.4% Total/Average 3,080 397.0 $ 681.7 635.3 58.2% 62.5% 135.8% Total Loan Purchase Price Total UPB Total BPO Purchase Price Purchase Price Weighted Status Count (1),(2) ($ in millions) ($ in millions) ($ in millions) as % of UPB as % of BPO Average LTV (3) Foreclosure 2,146 $ 285.5 $ 506.5 $ 457.2 56.4% 62.4% 137.4% Delinquent 557 61.8 95.9 96.4 64.5% 64.1% 144.4% Performing 377 49.7 79.3 81.7 62.6% 60.8% 115.3% Total/Average 3,080 $ 397.0 $ 681.7 $ 635.3 58.2% 62.5% 135.8% (1) Represents first liens on 2,920 homes and 160 parcels of land. (2) Excludes 277 unsecured, second and third liens with an aggregate purchase price of $1.9 million. (3) Weighted average LTV is based on the ratio of UPB to BPO weighted by UPB for each state as of the respective acquisition dates. $ $ $ $ |

17 TRANSACTION ACTIVITY Acquisitions – Three Months Ended June 30, 2014 (1) Includes acquisition costs and actual and estimated upfront renovation costs. Actual renovation costs may exceed estimated renovation costs, and we may acquire homes in the future with different characteristics that result in higher renovation costs. (2) Estimated average monthly rent per home represents (1) for vacant homes, management’s estimates of what rent would be generated if such homes were leased based on rents estimated by examining multiple rent data sources (such as realized rents for comparable homes in neighborhood, a proprietary rent setting algorithm, third-party vendors, etc.) and using localized knowledge to establish rent for a given property and (2) for leased homes, average monthly contractual rent. No assurance can be given that these estimates will prove to be accurate, and you should not place undue reliance on them. Rental Homes: Markets Homes Average Home Size (sq. ft.) Average Acquisition Cost per Home Average Estimated Upfront Renovation Cost per Home Average Estimated Investment per Home (1) Aggregate Investment ($ in millions) Estimated Average Monthly Rent per Home (2) Atlanta 514 2,013 104,084 $ 24,404 $ 128,489 $ 66.0 $ 1,220 $ Dallas 298 2,198 138,546 $ 21,444 $ 159,990 $ 47.7 1,594 $ South Florida 272 1,685 149,994 $ 32,316 $ 182,310 $ 49.6 1,730 $ Houston 219 2,044 126,776 $ 22,095 $ 148,872 $ 32.6 1,572 $ Tampa 200 1,486 106,847 $ 19,773 $ 126,619 $ 25.3 1,297 $ Denver 120 1,703 206,201 $ 31,644 $ 237,845 $ 28.5 1,781 $ Chicago 109 1,528 114,382 $ 35,399 $ 149,781 $ 16.3 1,664 $ Orlando 86 1,422 101,497 $ 23,979 $ 125,476 $ 10.8 1,241 $ Southern California 52 1,649 225,980 $ 18,514 $ 244,494 $ 12.7 1,888 $ Phoenix 45 1,475 128,498 $ 28,740 $ 157,237 $ 7.1 1,202 $ Northern California 28 1,525 226,929 $ 18,552 $ 245,481 $ 7.0 1,866 $ Total/Average 1,943 1,843 131,007 $ 25,224 $ 156,231 $ 303.6 $ 1,490 $ Non-Performing Loans: Total Purchase Purchase Purchase Price Total UPB Total BPO Price as % Price as % Number of Loans ($ in millions) ($ in millions) ($ in millions) of UPB of BPO 1,441 $ 117.0 $ 189.4 $ 171.6 61.8% 68.2% |

18 Definitions and Reconciliations ($ in thousands, except share and per share data) Amount Per Share Investments in real estate properties, gross 1,442,626 $ 36.98 $ Less: Accumulated depreciation (17,525) (0.44) Add: Real estate held for sale, net 13,383 0.34 Investments in real estate, net 1,438,484 36.88 Add: Increase in estimated fair value of investments in real estate 250,459 6.42 Less: Estimated renovation reserve (155,551) (3.99) Estimated SFR Value 1,533,392 39.31 Non-performing loans 178,311 4.57 Non-performing loans (fair value option) 218,797 5.61 Add: Increase in estimated fair value of non-performing loans 56,076 1.44 Estimated NPL Value 453,184 11.62 Estimated SFR & NPL Value 1,986,576 $ 50.93 $ Total shareholders' equity 1,090,914 $ 27.97 $ Less: Investments in real estate, net (1,438,484) (36.88) Less: Non-performing loans (178,311) (4.57) Less: Non-performing loans (fair value option) (218,797) (5.61) Add: Estimated SFR & NPL Value 1,986,576 50.93 Estimated NAV 1,241,898 $ 31.84 $ Number of Shares 39,007,239 June 30, 2014 (unaudited) or as measures of profitability or liquidity. Further, not all real estate investment trusts (“REITs”) compute the same non-GAAP measure; therefore, there can be no assurance that our basis for computing this non- GAAP measure is comparable with that of other REITs. Funds From Operations (“FFO”) and Core FFO. FFO is used by industry analysts and investors as a supplemental performance measure of an equity REIT. FFO is defined by the National Association of Real Estate Investment Trusts (“NAREIT”) as net income or loss (computed in accordance with GAAP) excluding gains or losses from sales of previously depreciated real estate assets, plus depreciation and amortization of real estate assets and adjustments for unconsolidated partnerships and joint ventures. We believe that FFO is a meaningful supplemental measure of the operating performance of our single- family home business because historical cost accounting for real estate assets in accordance with GAAP assumes that the value of real estate assets diminishes predictably over time, as reflected through depreciation. Because real estate values have historically risen or fallen with market conditions, management considers FFO an appropriate supplemental performance measure because it excludes historical cost depreciation, as well as gains or losses related to sales of previously depreciated homes, from GAAP net income. By excluding depreciation and gains or losses on sales of real estate, management uses FFO to measure returns on its investments in real estate assets. However, because FFO excludes depreciation and amortization and captures neither the changes in the value of the homes that result from use or market conditions nor the level of capital expenditures to maintain the operating performance of the homes, all of which have real economic effect and could materially impact our results from operations, the utility of FFO as a measure of our performance is limited. We believe that Core FFO is a meaningful supplemental measure of our operating performance for the same reasons as FFO and adjusting for non-routine items that when excluded allows for more comparable periods. Our Core FFO begins with FFO as defined by the NAREIT White Paper and is adjusted for: share- based compensation, non-recurring costs associated with the separation, acquisition fees expensed and property management engagement costs, write-off of loan costs, loss on derivative financial instruments, amortization of derivative financial instruments cost and other non-comparable items as applicable. Management also believes that FFO/Core FFO, combined with the required GAAP presentations, is useful to investors in providing more meaningful comparisons of the operating performance of a company’s real estate between periods or as compared to other companies. FFO/Core FFO does not represent net income or cash flows from operations as defined by GAAP and is not intended to indicate whether cash flows will be sufficient to fund cash needs. It should not be considered an alternative to net income as an indicator of the REIT’s operating performance or to cash flows as a measure of liquidity. Our FFO/Core FFO may not be comparable to the FFO of other REITs due to the fact that not all REITs use the NAREIT or similar Core FFO definition. For a reconciliation of FFO and Core FFO to net loss attributable to common shareholders determined in accordance with GAAP, please refer to page 10. occupancy or subsequent occupancy after a renovation. Homes are considered stabilized even after subsequent resident turnover. However, homes may be removed from the stabilized home portfolio and placed in the non-stabilized home portfolio due to renovation during the home lifecycle. We define Estimated NAV as the estimated value of all assets net of liabilities. To calculate the Estimated NAV, the historical net investments in real estate and NPLs at carrying value are deducted from total shareholders’ equity and the Estimated SFR Value and NPL Value are added (see table below). The costs of selling properties in the portfolio, including commissions and other related costs are not deducted for the purpose of calculating the Estimated SFR Value and Estimated NAV. Further, future promoted interests on the NPL portfolio are not deducted for the purpose of calculating Estimated SFR & NPL Value and Estimated NAV. We consider Estimated NAV to be an appropriate supplemental measure as it illustrates the estimated imbedded value in our SFR portfolio and NPL portfolio that is carried on our balance sheet primarily at cost. The Estimated SFR Value, Estimated NPL Value and Estimated NAV are non-GAAP financial measures. However, they are provided for informational purposes to be used by investors in assessing the value of the assets. A reconciliation of total shareholders’ equity to Estimated NAV is provided below. These metrics should be considered along with other available information in valuing and assessing us, including our GAAP financial measures and other cash flow and yield metrics. These metrics should not be viewed as a substitute for book value, net investments in real estate, equity, net income or cash flows from operations prepared in accordance with GAAP, non-controlling interests less cash and cash equivalents. Enterprise Value. We define enterprise value as market value of equity plus debt plus We define the stabilized home portfolio to include homes from the first day of initial Stabilized Homes. Estimated NAV. |

19 Definitions and Reconciliations (cont’d) Total NOI, Total NPL NOI, Total Non-Stabilized Portfolio NOI, Total Stabilized Portfolio NOI and Total Leased Home Portfolio NOI. We define Total NOI as total revenues less property operating and maintenance expenses and real estate taxes and insurance expenses (“property operating expenses”) and mortgage loan servicing costs. We define Total NPL Portfolio NOI as gains on NPLs, net and gains on loan conversions, net less mortgage loan servicing costs. We define Total Non- Stabilized Portfolio NOI as total revenues on the non-stabilized portfolio less property operating expenses on the non-stabilized portfolio. We define Total Stabilized Portfolio NOI as total revenues on the stabilized portfolio less property operating expenses on the stabilized portfolio. We define Total Leased Home Portfolio NOI as the Total Stabilized Portfolio NOI less property operating expenses on vacant stabilized homes. We consider these NOI measures to be appropriate supplemental measures of operating performance to net income attributable to common shareholders because they reflect the operating performance of our homes without allocation of corporate level overhead or general and administrative costs and reflect the operations of the segments and sub-segments of our business. A reconciliation of net loss attributable to common shareholders to these NOI measures is provided below: These NOI measures should not be considered alternatives to net loss or net cash flows from operating activities, as determined in accordance with GAAP, as indications of our performance or as measures of liquidity. Although we use these non-GAAP measures for comparability in assessing their performance against other REITs, not all REITs compute the same non-GAAP measures. Accordingly, there can be no assurance that our basis for computing these non-GAAP measures are comparable with that of other REITs. Total Rental Portfolio. We define total rental portfolio to exclude homes designated as non-rental. Non-rental homes are homes we do not intend to hold for the long term. Three Months Ended Six Months Ended ($ in thousands, unaudited) June 30, 2014 June 30, 2014 Reconciliation of net loss to stabilized portfolio NOI and leased home portfolio NOI Net loss attributable to common shareholders $ (12,116) $ (27,424) Add (deduct) adjustments to get to total NOI Non-performing loan management fees and expenses 1,871 4,286 General and administrative 4,444 9,814 Shared-based compensation 2,130 2,459 Investment management fees 3,993 6,750 Separation costs - 3,543 Acquisition fees expensed and property management engagement costs 186 447 Interest expense, including amortization 5,191 6,691 Depreciation and amortization 7,243 12,716 Finance related expenses and write-off of loan costs 5,441 5,441 Impairment of real estate 1,233 2,067 Realized loss (gain) on sales of investments in real estate, net 56 201 Loss on derivative financial instruments, net 470 470 Income tax expense 350 485 Net income attributable to non-controlling interests 83 73 Total NOI 20,575 28,019 Add (deduct) adjustments to get to total stabilized home portfolio NOI NPL portfolio NOI components: Realized gain on non-performing loans, net (3,357) (5,200) Realized gain on loan conversions, net (6,483) (11,897) Mortgage loan servicing costs 5,139 10,021 Unrealized gain on non-performing loans, net (3,641) (3,641) Deduct: Total NPL portfolio NOI (8,342) (10,717) Non-stabilized portfolio NOI components: Property operating expenses on non-stabilized homes 2,726 5,289 Add: Total Non-stabilized portfolio NOI 2,726 5,289 Total stabilized portfolio NOI 14,959 22,591 Add (deduct) adjustments to get to total leased home portfolio NOI Property operating expenses on vacant stabilized homes 221 576 Total leased home portfolio NOI 15,180 $ 23,167 $ |

Forward-Looking Statements The statements herein that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements involve significant risks and uncertainties, which are difficult to predict, and are not guarantees of future performance. Such statements can generally be identified by words such as “anticipates,” “expects,” “intends,” “will,” “could,” “believes,” “estimates,” “continue,” and similar expressions. Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, contain financial and operating projections or state other forward-looking information. Our ability to predict results or the actual effect of future events, actions, plans or strategies is inherently uncertain. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in, or implied by, the forward-looking statements. Factors that could materially and adversely affect our business, financial condition, liquidity, results of operations and prospects, as well as our ability to make distributions to our shareholders, include, but are not limited to: expectations regarding the timing of generating revenues; changes in our business and growth strategies; volatility in the real estate industry, interest rates and spreads, the debt or equity markets, the economy generally or the rental home market specifically; events or circumstances that undermine confidence in the financial markets or otherwise have a broad impact on financial markets; declines in the value of homes, and macroeconomic shifts in demand for, and competition in the supply of, rental homes; the availability of attractive investment opportunities in homes that satisfy our investment objective and business and growth strategies; the impact of changes to the supply of, value of and the returns on distressed and non-performing residential mortgage loans; our ability to convert the homes and distressed and non-performing residential mortgage loans we acquire into rental homes generating attractive returns; our ability to successfully modify or otherwise resolve distressed and non-performing residential mortgage loans; our ability to lease or re-lease our rental homes to qualified residents on attractive terms or at all; the failure of residents to pay rent when due or otherwise perform their lease obligations; our ability to manage our portfolio of rental homes; the concentration of credit risks to which we are exposed; the availability, terms and deployment of short-term and long-term capital; the adequacy of our cash reserves and working capital; our relationships with Starwood Capital Group and our manager and their ability to retain qualified personnel; potential conflicts of interest; unanticipated increases in financing and other costs; our expected leverage; changes in governmental regulations, tax laws and rates and similar matters; limitations imposed on our business and our ability to satisfy complex rules in order for us to qualify as a REIT for U.S. federal income tax purposes; and estimates relating to our ability to make distributions to our shareholders in the future. You should not place undue reliance on any forward-looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by us with the Securities and Exchange Commission from time to time. Furthermore, except as required by law, we are under no duty to, and we do not intend to, update any of our forward-looking statements appearing herein, whether as a result of new information, future events or otherwise. |