Table of Contents

As filed with the Securities and Exchange Commission on October 28, 2013

Registration No. 333-190853

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

LGI HOMES, INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 1531 (Primary Standard Industrial Classification Code Number) | 46-3088013 (I.R.S. Employer Identification Number) |

1450 Lake Robbins Drive, Suite 430

The Woodlands, Texas 77380

(281) 362-8998

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Charles Merdian

Chief Financial Officer

LGI Homes, Inc.

1450 Lake Robbins Drive, Suite 430

The Woodlands, Texas 77380

(281) 362-8998

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Warren A. Hoffman Norman R. Miller Winstead PC 1100 JPMorgan Chase Tower 600 Travis Street Houston, Texas 77002 | Timothy S. Taylor Baker Botts L.L.P. One Shell Plaza 910 Louisiana Street Houston, Texas 77002 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price Per Share(2) | Proposed Maximum Aggregate Offering | Amount of Registration | ||||||||||||

Common stock, par value $0.01 per share | 10,350,000 | $ | 15.00 | $ | 155,250,000.00 | $ | 20,946.20 | |||||||||

| (1) | Includes shares of common stock which may be purchased by the underwriters pursuant to their option to purchase additional shares of common stock. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | Of this amount, $17,050.00 has previously been paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated October 28, 2013

PRELIMINARY PROSPECTUS

9,000,000 Shares

Common Stock

This is the initial public offering of our common stock. We are selling 9,000,000 shares of our common stock. We currently expect the initial public offering price to be between $13.00 and $15.00 per share of our common stock.

We have granted the underwriters an option to purchase up to 1,350,000 additional shares of our common stock.

We have applied to list the shares of our common stock on the NASDAQ Global Select Market under the symbol “LGIH.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 18.

We are an “emerging growth company” under the federal securities laws and are eligible for reduced reporting requirements. See “Summary—Implications of Being an Emerging Growth Company.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discount(1) | $ | $ | ||||||

Proceeds to us (before expenses) | $ | $ | ||||||

| (1) | See ”Underwriting” for a description of all underwriting compensation payable in connection with this offering. |

The underwriters expect to deliver the shares to purchasers on or about , 2013.

Joint Book-Running Managers

| Deutsche Bank Securities | JMP Securities | J.P. Morgan | ||||

Co-Managers

| Barclays | BofA Merrill Lynch | BTIG | Builder Advisor Group, LLC |

The date of this prospectus is , 2013

Table of Contents

Table of Contents

We are responsible for the information contained in this prospectus. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not and the underwriters are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date, regardless of the time of delivery of this prospectus or of any sale of our common stock.

| 1 | ||||

| 1 | ||||

| 3 | ||||

| 5 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

Summary Historical and Pro Forma Financial and Operating Data |

| 14 |

| |

| 18 | ||||

| 18 | ||||

| 32 | ||||

Risks Related to this Offering and Ownership of our Common Stock | 38 | |||

| 43 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 50 | ||||

SELECTED HISTORICAL AND PRO FORMA FINANCIAL AND OPERATING DATA | 65 | |||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 68 | |||

| 68 | ||||

| 71 | ||||

| 73 | ||||

| 75 | ||||

| 77 | ||||

| 81 | ||||

| 83 | ||||

| 84 | ||||

| 85 | ||||

| 85 | ||||

| 88 | ||||

| 88 | ||||

| 89 | ||||

Quantitative and Qualitative Disclosures About Interest Rate Risk | 89 | |||

| 90 | ||||

| 141 | ||||

| 143 | ||||

| 148 | ||||

| 150 | ||||

| 151 | ||||

| 152 | ||||

| 154 | ||||

| 155 | ||||

| 155 | ||||

| 156 | ||||

| 156 | ||||

| 157 | ||||

| 157 | ||||

| 157 | ||||

| 157 | ||||

| 158 | ||||

| 158 | ||||

| 158 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 162 | ||||

i

Table of Contents

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 164 | ||||

| 164 | ||||

| 164 | ||||

| 165 | ||||

| 166 | ||||

| 166 | ||||

| 169 | ||||

| 170 | ||||

| 170 | ||||

Management and Warranty Fees from the LGI/GTIS Joint Ventures | 170 | |||

| 170 | ||||

| 171 | ||||

| 171 | ||||

| 171 | ||||

| 173 | ||||

| 173 | ||||

| 173 | ||||

Limitation on Liability and Indemnification of Officers and Directors | 173 | |||

Anti-Takeover Effects of Provisions of Our Certificate of Incorporation, Our Bylaws and Delaware Law | 173 | |||

| 174 | ||||

| 175 | ||||

| 175 | ||||

| 175 | ||||

| 176 | ||||

| 176 | ||||

| 176 | ||||

| 177 | ||||

| 178 | ||||

| 180 | ||||

| 181 | ||||

| 182 | ||||

| 186 | ||||

| 194 | ||||

| 194 | ||||

| 194 | ||||

| F-1 | ||||

Public Homebuilder Peers

References in this prospectus to our “public homebuilder peers” refer to the following domestic homebuilders that file periodic reports with the Securities and Exchange Commission (SEC): AV Homes, Inc., Beazer Homes USA, Inc., D.R. Horton, Inc., Hovnanian Enterprises, Inc., KB Home, Lennar Corporation, M.D.C. Holdings, Inc., M/I Homes, Inc., Meritage Homes Corporation, NVR, Inc., PulteGroup, Inc., The Ryland Group, Inc., Standard Pacific Corp., Taylor Morrison Home Corporation, Toll Brothers, Inc., TRI Pointe Homes, Inc., UCP, Inc., WCI Communities, Inc. and William Lyon Homes. In each of our markets, we face competition from certain of our public homebuilder peers and from private homebuilders. In Phoenix, San Antonio/Austin and Atlanta, at least three of our top five competitors are certain of our public homebuilder peers. In Houston, Dallas/Fort Worth and Central Florida, three of our top five competitors are private homebuilders with the other two of our top five competitors being certain of our public homebuilder peers.

ii

Table of Contents

Explanatory Note

LGI Homes, Inc. is the newly-formed registrant and issuer of the shares of common stock in this offering.

Concurrently with this offering, LGI Homes, Inc. will acquire all the equity interests of LGI Homes Group, LLC, LGI Homes Corporate, LLC, LGI Homes, Ltd., LGI Homes—Sunrise Meadow, Ltd., LGI Homes—Canyon Crossing, Ltd., LGI Homes—Deer Creek, LLC and their direct and indirect subsidiaries (collectively referred to in this prospectus as our “predecessor” or “LGI Homes Group (Predecessor)”). Concurrently with this offering, LGI Homes, Inc. will also acquire from GTIS Partners, LP, a global real estate investment firm, and its affiliated entities (collectively, “GTIS”), all of GTIS’s equity interests in four unconsolidated joint ventures with LGI Homes Group (Predecessor), namely, LGI-GTIS Holdings, LLC, LGI-GTIS Holdings II, LLC, LGI-GTIS Holdings III, LLC and LGI-GTIS Holdings IV, LLC (collectively, the “LGI/GTIS Joint Ventures”). See “Summary—The Transactions.” Our predecessor owns a 15% equity interest in and manages the day-to-day operations of the LGI/GTIS Joint Ventures.

Unless we state otherwise or the context otherwise requires, references in this prospectus to “we,” “us,” “our” or similar terms when used in a historical context refer to LGI Homes Group (Predecessor). When used prospectively, those terms refer to LGI Homes, Inc. and its subsidiaries, including LGI Homes Group (Predecessor) and the LGI/GTIS Joint Ventures as of the closing date of this offering.

Industry and Market Data

We use market data and industry forecasts and projections throughout this prospectus, particularly in the sections entitled “Summary,” “Market Opportunity” and “Our Business.” We have obtained substantially all of this information from a market study prepared for us in connection with this offering by John Burns Real Estate Consulting, LLC (“JBREC”), an independent research provider and consulting firm focused on the housing industry. We have agreed to pay JBREC a fee of $39,000 for that market study, plus an amount charged at an hourly rate for additional information we may require from JBREC from time to time in connection with that market study. Such information is included in this prospectus in reliance on JBREC’s authority as an expert on such matters. Any forecasts prepared by JBREC are based on data (including third-party data), models and experience of various professionals and various assumptions (including the completeness and accuracy of third-party data), all of which are subject to change without notice. See “Experts.” In addition, certain market and industry data has been taken from publicly available industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable but we have not independently verified the data obtained from these sources. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and additional uncertainties regarding the other forward-looking statements in this prospectus.

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. You should read this entire prospectus carefully, including the historical and pro forma financial statements and the notes to those financial statements contained elsewhere in this prospectus, before investing in our common stock. The information presented in this prospectus assumes (1) an initial public offering price of $14.00 per share of common stock (the midpoint of the price range set forth on the cover page of this prospectus) and (2) unless otherwise indicated, that the underwriters have not exercised their option to purchase additional shares of common stock. You should read “Risk Factors” for information about important risks that you should consider before buying shares of our common stock.

We are one of the nation’s fastest growing homebuilders engaged in the design and construction of entry-level homes in high growth markets in Texas, Arizona, Florida and Georgia. Our business model is based on skillfully building and selling high quality, entry-level homes in attractive locations that include well-designed floor plans with features that appeal to renters. We focus on converting renters of apartments and single-family homes into homeowners by offering homes at affordable prices in affordable locations and by utilizing a well-established sales and marketing approach, a culture of customer service excellence and a highly efficient construction process. Our strategy has driven our industry-leading asset turnover and returns on capital. We intend to expand within our existing markets and into new markets where we identify opportunities to build homes that meet our profit and return objectives.

Since commencing operations in 2003, we have constructed and sold over 4,000 homes, have been profitable every year despite the housing downturn, and have never taken an inventory impairment. According toBuilder magazine, we were the only homebuilder among the 200 largest U.S. homebuilders to report closings and revenue growth from 2006 to 2008 when the housing market experienced a significant decline. We increased our revenue from $50.5 million in 2010 to $76.2 million in 2012, and revenues of $143.4 million in 2012 on a pro forma basis. See “Unaudited Pro Forma Financial Information” for our unaudited pro forma financial statements, including a discussion of the adjustments made in such unaudited pro forma financial statements. We increased our closings from 402 homes in 2010 to 536 homes in 2012, and we had 1,062 home closings in 2012 on a pro forma basis. Among our public homebuilder peers, we had one of the highest revenue and closings growth rates between 2010 and 2012. Further, in 2012, we ranked first among our public homebuilder peers in return on assets, asset turnover, closings per active community and return on equity. We generated attractive returns on capital for 2012 with a 32.7% earnings before taxes to average total capitalization ratio, a level far exceeding the average of our public homebuilder peers of 3.5%. In each of our markets, we face competition from certain of our public homebuilder peers and from private homebuilders. In Phoenix, San Antonio/Austin and Atlanta, at least three of our top five competitors are certain of our public homebuilder peers. In Houston, Dallas/Fort Worth and Central Florida, three of our top five competitors are private homebuilders with the other two of our top five competitors being certain of our public homebuilder peers. We have a proven and highly effective operating model and expect to own or control more than 11,000 lots immediately following this offering, representing more than seven years of land supply based on our home closings for the first six months of 2013 on a pro forma basis. We believe we are well-positioned to continue our profitable growth within existing and new markets and capitalize on the U.S. housing recovery.

1

Table of Contents

Our management team has been in the residential land development business since the mid-1990s. In 2003, we commenced homebuilding operations targeting the entry-level market. We developed our unique operating model based on our belief that there was a more effective and efficient method of constructing and selling homes. Our proven operating model has been highly successful, resulting in one of the highest revenue growth rates among our public homebuilder peers. After successfully establishing ourselves as homebuilders in the Houston market, we demonstrated that our operating model could flourish in additional markets including Dallas/Fort Worth, San Antonio, Austin and Phoenix. Since 2010, we achieved profitability within six months of our first home closings in each of our new communities in Texas and Arizona. After conducting extensive due diligence and market studies, we entered the Atlanta and Orlando markets in 2013. Our expansion into Florida leveraged our experience managing one of the LGI/GTIS Joint Ventures’ entry into the Tampa market in 2012. However, if there is a decline in the growth rate in our new markets, we may not be able to successfully replicate our operating model in these markets.

Our success lies within our differentiated strategy as a focused sales and marketing organization targeting the entry-level homebuyer. Our marketing efforts are specifically designed to establish direct communication with local renters in order to educate them on the benefits and affordability of homeownership. At each of our sales offices, we have assembled a team of dedicated sales professionals and an independent on-site loan officer who assist the prospective buyer through the home buying process. Our focus on sales and marketing is a key driver of our high conversion rates, and we believe our unique sales approach has enabled us to differentiate ourselves from our competition. As a result of our operating model and inventory of move-in ready homes, our average closings per active community were 81 in 2012, or approximately seven per month, which far exceeded those of our public homebuilder peers who had average closings per active community of26 in 2012, orapproximately two per month. In each of our markets, we compete with certain of our public homebuilder peers and with certain private homebuilders. If our competitors are more successful than us or offer better value to our potential customers, our average closings per community could be adversely affected.

Our higher sales volume enables us to employ an even-flow, or continuous, construction methodology to establish an inventory of move-in ready homes, resulting in more favorable relationships with subcontractors who prefer the stability afforded by our approach. We focus on entry-level homes with price points and sizes ranging from approximately $115,000 to $260,000 and 1,200 to 3,000 square feet, respectively. All of our homes are built with a defined set of features that appeal to renters, which simplifies our construction and purchasing processes and allows us to optimize the timing of our home starts. Our inventory of move-in ready homes and successful sales methodology have led to generally high closing rates and short escrow periods for customers who are often faced with expiring apartment leases and rising rental costs. As a result, our inventory turnover in 2012 was 2.7x, significantly higher than the average of our public homebuilder peers of 1.0x. If our public homebuilder peers or other competitors are more successful than us or offer better value to our potential customers, our inventory turnover could be adversely affected.

We have been an active and opportunistic acquirer of land for residential development in our markets. We generally acquire finished lots and raw land in affordable locations that are further away from urban centers than many other suburban communities but have access to major thoroughfares, retail districts and centers of business, which, as a result, can be purchased at attractive prices. We test the market and speak with potential homebuyers before proceeding with our land acquisitions. We maintain a large pipeline of desirable land positions

2

Table of Contents

and plan to use the proceeds from this offering to fund several land acquisitions to support our continued growth. We increased our active communities from 4 as of December 31, 2010 to 10 as of June 30, 2013 and 18 as of June 30, 2013 on a pro forma basis, and expect to reach 24 active communities as of December 31, 2013.

Each of our existing markets is experiencing strong momentum in housing demand drivers, including nationally leading population and employment growth trends, favorable migration patterns, general housing affordability and desirable lifestyle and weather characteristics. Our target markets are characterized by high populations of renters who are facing rising rental costs and are interested in homeownership. Many of our existing markets, including Austin, Houston, Dallas/Fort Worth, Phoenix and San Antonio, ranked among the top 10 markets for fastest population growth in the United States from 2000 to 2010, according to the U.S. Census Bureau. However, if there is a decline in the housing demand drivers in our markets, our home sales would likely be adversely affected.

We increased our revenue from $28.9 million for the six months ended June 30, 2012 to $59.3 million for the six months ended June 30, 2013, and $96.0 million for the six months ended June 30, 2013 on a pro forma basis. Similarly, we increased closings from 204 homes for the six months ended June 30, 2012 to 397 homes for the six months ended June 30, 2013, and 664 home closings for the six months ended June 30, 2013 on a pro forma basis. For the six months ended June 30, 2013, we generated adjusted gross margins, on a pro forma basis, of 28.2% and adjusted EBITDA margins, on a pro forma basis, of 12.8%. See “—Summary Historical and Pro Forma Financial and Operating Data” for a reconciliation of adjusted gross margins to gross margins and adjusted EBITDA to net income.

We believe the following strengths provide us with a significant competitive advantage in implementing our business strategy:

Unique operating model generates “best-in-class” returns on capital

Our unique operating model generates “best-in-class” returns on capital through a profitable and scalable platform that has generated strong operating margins, rates of closings per active community and inventory turnover. We attribute our strong margins and our consistent profitability throughout the downturn primarily to our disciplined land acquisition, operating and management approach. We increased our revenue from $50.5 million in 2010 to $76.2 million in 2012, representing a compound annual growth rate of 22.9%, which exceeds the average compound annual growth rate of 8.3% of our public homebuilder peers over the same period. For the six months ended June 30, 2013, our revenue was $59.3 million, and $96.0 million for the six months ended June 30, 2013 on a pro forma basis. However, continued or additional tightening of mortgage lending standards or increases in mortgage costs could result in a decline of our home sales. A decline in the growth rate in our markets or for the homebuilding industry generally could also result in a decline of our home sales. If we are unable to develop new communities successfully or within expected time frames, our results of operations could be adversely affected.

3

Table of Contents

Well-established sales and marketing approach focused on a culture of customer service excellence

We believe our expertise in sales and marketing differentiates us from our public homebuilder peers. We have established a successful, unique marketing system that has proven to create a large volume of potential homebuyers. We make extensive use of advertising, including targeted direct-mail brochures, our website, social media, newspaper advertisements and the placement of strategically located signs and billboards, all of which are designed to encourage potential homebuyers to schedule an appointment to visit one of our active communities. We reach most of our potential homebuyers through our direct marketing program specifically designed to target renters. Each week, we send an average of 12,000 direct mailings to renters within a 25-mile radius of each of our communities.

We sell homes through our own highly trained sales professionals with less than 10% of our sales since 2010 requiring commissions paid to third party realtors, which enhances our profitability and ensures a superior homebuyer experience. In addition, we provide potential homebuyers with a thorough outline of the steps to homeownership and educate them on the advantages homeownership offers compared to renting. The strength of our sales force is largely driven by our emphasis on recruiting and training. However, if we are not able to attract and retain our highly trained sales force, we may lose our sales and marketing advantage. Furthermore, since we generally have a lower market share in each of our markets compared to many of our competitors, our competitors may have an advantage in marketing their products. In addition, many of our competitors are larger than us and are able to spend more money on sales and marketing than us.

Focus on attractive markets with a favorable growth outlook and strong demand fundamentals

Our focused geographic footprint positions us to benefit from the ongoing recovery in the U.S. housing market after the significant downturn from 2006 to 2011. We currently operate in four states, Texas, Arizona, Florida and Georgia, that are benefiting from positive momentum in housing demand drivers, including nationally leading population and employment growth trends, favorable migration patterns, general housing affordability, and desirable lifestyle and weather characteristics. These four states accounted for 29.7% of the 829,658 building permits issued for privately owned homes for the year ended December 31, 2012, and are forecasted to grow at an average annual rate of 3.7% as compared to a national rate of 1.6% between 2010 and 2030, according to the U.S. Census Bureau. However, to the extent housing demand and population growth slow in these states, we may not realize the favorable growth outlook that we have in these markets. Furthermore, if we are unable to effectively compete with the resale home market in our markets, we may not benefit from the housing demand in these states.

Proven ability to expand into new geographic markets

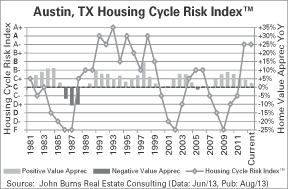

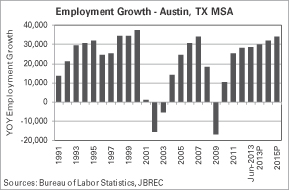

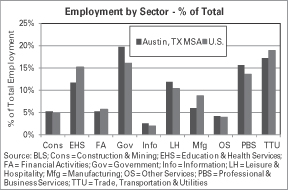

We continually evaluate expansion opportunities in new geographic markets. Our decision to enter a new market is primarily based on the growing demand for single-family housing, favorable home affordability trends, availability of land with access to key elements of major metropolitan areas, high volumes of renters, diverse and growing employment bases and attractive sector competitive dynamics. After conducting thorough due diligence and carefully analyzing the demand through an extensive test marketing program, we leveraged our success in Houston and San Antonio and entered the Dallas/Fort Worth market in 2009 and the Phoenix and Austin markets in 2011. In Dallas/Fort Worth, Austin and Phoenix, we rapidly recouped our

4

Table of Contents

initial investment and have been consistently profitable. In 2012, one of the LGI/GTIS Joint Ventures that we manage entered the Tampa market and in 2013, we entered the Atlanta and Orlando markets. We believe the in-depth local market knowledge of our experienced management team and the local construction and homebuilding experts we hire in each new market has and will continue to enable us to successfully replicate our operating model in new markets. However, if there is a decline in the growth rate in our new geographic markets, including Atlanta and Orlando, our home sales would be affected and we may not be able to successfully replicate our operating model in these markets. Furthermore, if our public homebuilder peers and other competitors are more successful or offer better value to our potential customers in our new markets, we may not be able to successfully replicate our operating model in these markets. If demand for single-family housing slows or if home affordability trends are no longer favorable, we may not find new geographic markets into which to expand.

Superior homeowner experience and service

Our core operating philosophy is centered on making the home buying experience friendly, effective and efficient. By providing personalized service to our potential homebuyers, we facilitate a streamlined home buying process and make the dream of homeownership possible. We believe our focus on providing a superior customer experience leads to a more satisfied homeowner, which in turn enhances the overall attractiveness of our communities, our homes and our reputation with future homebuyers.

Highly experienced and committed management team with a proven track record

With over 50 years of collective real estate experience, our management team is focused on executing our land acquisition, land development, homebuilding, marketing and sales strategy. However, the loss of any of our key personnel could adversely impact our business. Upon completion of this offering, our management team will beneficially own approximately 17.5% of our outstanding common stock (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus).

We are one of the nation’s fastest growing homebuilders, utilizing a well-established sales and marketing approach, a culture of customer service excellence, and a highly efficient home construction process. Our business strategy includes:

Accelerate growth within our existing markets

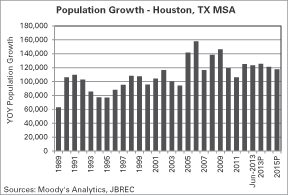

Despite our rapid growth over the past 10 years, we believe there remains a significant opportunity to grow our share of sales in our existing markets. In 2012, our home market of Houston recorded approximately 23,000 new home starts according toMetrostudy, and our market share was approximately 2% of new home sales. Furthermore, our market share was lower in each of our other markets. Given our familiarity with each of our existing markets and the favorable demographic and economic trends that are forecasted in our markets, we expect a significant portion of our near-term growth to come from expansion in these markets. However, the U.S. homebuilding industry is highly competitive. There is no assurance that we will be able to increase our market share in any of our markets.

5

Table of Contents

Aggressively pursue value-oriented land acquisitions

We pursue a flexible land acquisition strategy of purchasing or optioning finished lots, if they can be acquired at attractive prices, or purchasing raw land for residential development. We generally target affordable land acquisitions that are further away from urban centers than many other suburban communities but have access to major thoroughfares, retail districts and centers of business, which, as a result, allows us to provide our potential homebuyers with homes at affordable prices in affordable locations, and with access to the key elements of a metropolitan region. By targeting these locations, we acquire land at attractive prices due to favorable competitive dynamics. Immediately following this offering, we expect to own or control more than 11,000 lots, representing more than seven years of land supply based on our home closings for the first six months of 2013 on a pro forma basis. However, continued or additional tightening of mortgage lending standards or increases in mortgage costs could result in a decline of our home sales.

Selectively expand into new markets

We target markets that are characterized by favorable housing supply and demand dynamics coupled with a large and growing rental market, which generates a large volume of potential first-time homebuyers. We carefully analyze the demand of a market prior to entry through an extensive test marketing program to ensure that we can successfully turn renters into homebuyers. In addition, we evaluate new market expansion opportunities based on our ability to identify and hire local construction and homebuilding experts with detailed knowledge of the local market conditions. We believe our comprehensive new market evaluation process coupled with our unique operating model has and will continue to enable us to profitably expand into new markets. However, if there is a decline in the growth rate in our new markets, we may not be able to successfully replicate our operating model in these markets.

Focus on attracting, training and developing our team

We believe that our people are the backbone of our success. We focus on identifying and attracting the best talent and providing them with world-class training and development. However, if we are not able to attract and retain our highly trained sales force, we may lose our sales and marketing advantage. We directly invest in our sales professionals by conducting an intensive training program. Our continued commitment to our sales personnel is reflected in the ongoing weekly training sessions held in each of our sales offices coupled with the quarterly regional training events and an annual company-wide conference. We also work closely with our subcontractors and construction managers, training them on the most efficient way to build an LGI home.

Utilize Prudent Leverage

We intend to employ debt and equity as part of our ongoing financing strategy, coupled with redeployment of cash flows from our operations, to provide us with the financial flexibility to access capital on the best terms available. In that regard, we intend to employ prudent levels of leverage to finance the acquisition and development of our lots and construction of our homes. As of June 30, 2013, on a pro forma basis, we had $23.1 million in outstanding indebtedness and a total debt-to-total book capitalization of 12.1%. As of June 30, 2013, on a pro forma basis, we maintained $94.8 million of unrestricted cash and approximately $1.7 million of availability under our secured credit agreements.

6

Table of Contents

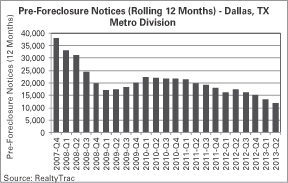

The U.S. housing market continues to improve from the cyclical low points reached during the 2008-2009 national recession. Between the 2005 market peak and 2011, new single-family housing sales declined 76%, according to data compiled by the U.S. Census Bureau (the “Census Bureau”), and median home prices declined 34%, as measured by the CoreLogic Case-Shiller Index. In 2011, some U.S. markets showed early indications of recovery as a result of an improving macroeconomic backdrop and strong housing affordability. In the twelve months ended June 30, 2013, homebuilding permits increased 16% according to the Census Bureau and the median single-family home price increased 14% year-over-year, according to data compiled by the National Association of Realtors. According to the Census Bureau, growth in new home sales outpaced growth in existing home sales over the same period, increasing 38% as compared to 15% for existing homes. Our target markets include Houston, Dallas/Fort Worth, San Antonio, Austin, Phoenix, Tampa, Orlando and Atlanta.

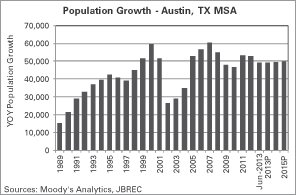

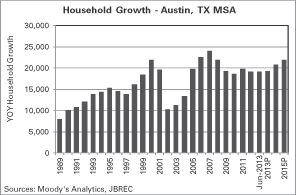

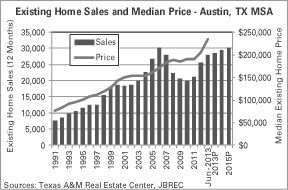

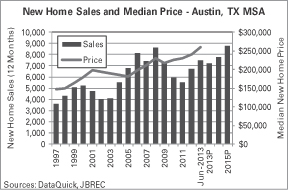

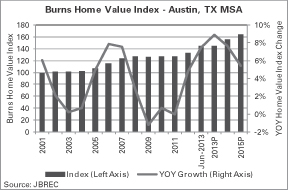

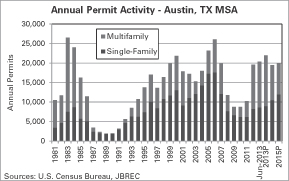

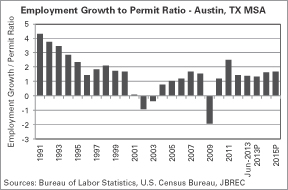

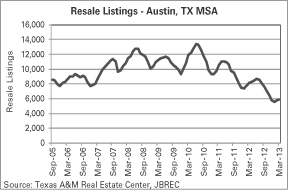

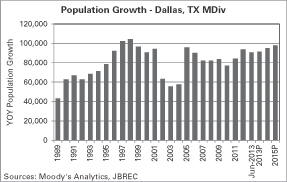

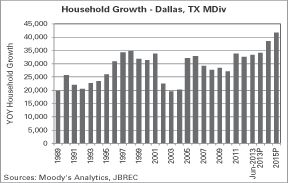

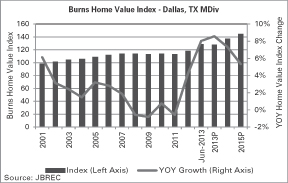

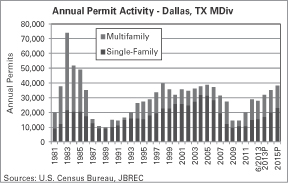

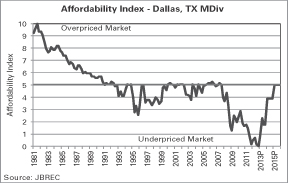

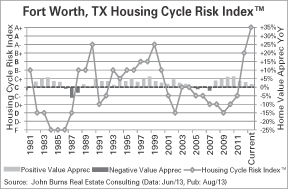

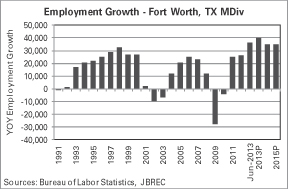

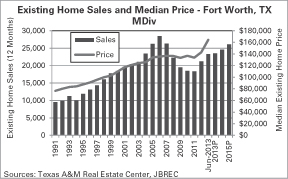

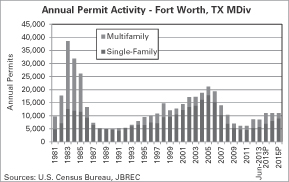

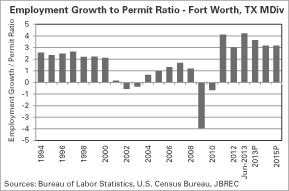

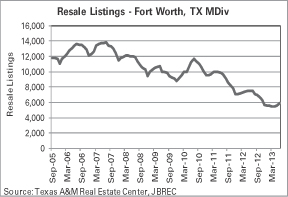

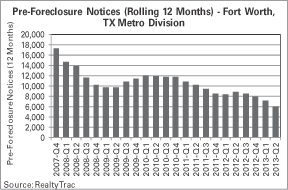

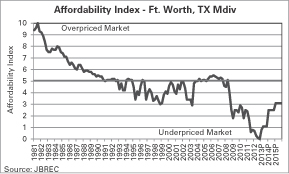

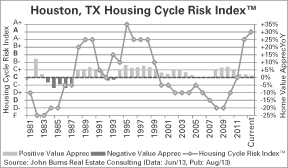

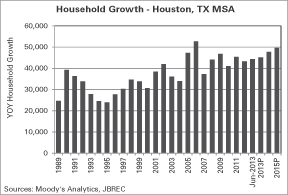

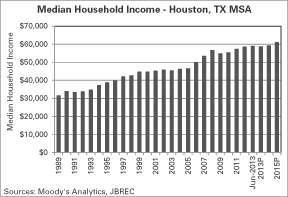

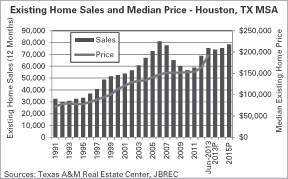

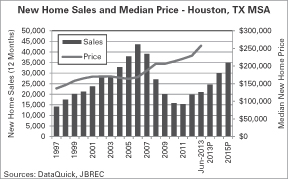

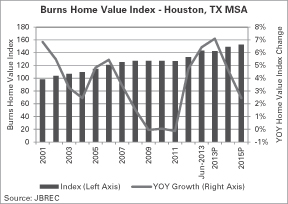

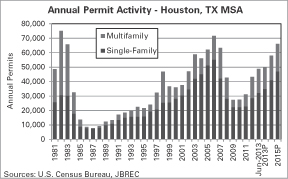

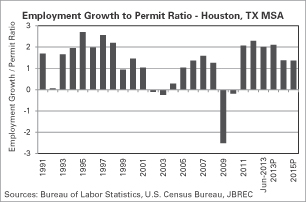

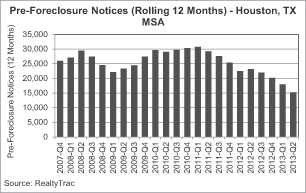

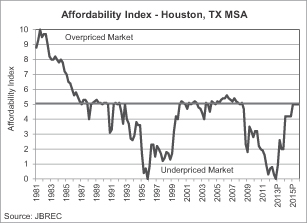

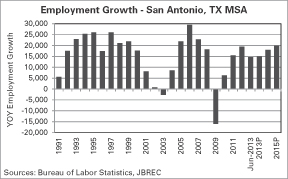

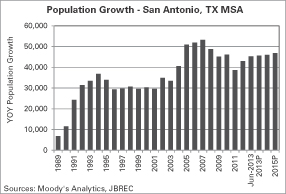

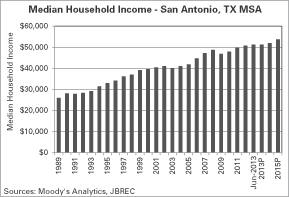

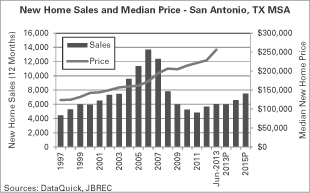

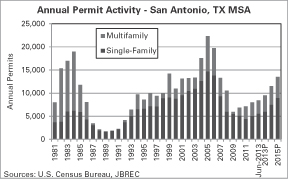

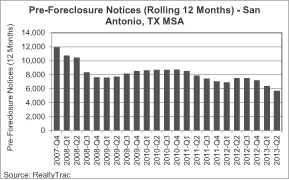

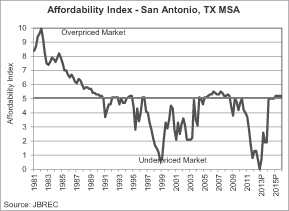

Texas. Texas housing fundamentals have shown considerable improvement in recent years, which is typically a precursor for increasing volume of home sales and home price appreciation. Houston was the first large metro area to recover all jobs lost during the recession and JBREC forecasts job growth in Houston averaging 3.3% per year from 2013 through 2015. For the twelve months ended June 30, 2013, existing homes sales in Houston reached 75,282, as compared to 56,807 in 2010 and sales are forecast to continue to grow at an average annual rate of 4.7% through 2015. Job growth in the Dallas and Fort Worth markets for the twelve months ended June 30, 2013, was 3.0% and 4.0%, respectively, significantly exceeding the 1.7% overall job growth in the U.S. During the same period, the Dallas market saw new home sales expand 25.4% and the Fort Worth market saw existing home sales increase 18.8%. In Austin, existing home sales volume increased 20.3% in 2012 while median single-family home prices rose 8.7% due to the area’s job growth outpacing new permit activity, declining inventory and historically high affordability. In the San Antonio market, low inventory levels paired with recovering demand are driving new home prices higher.

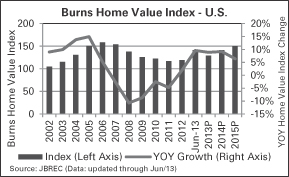

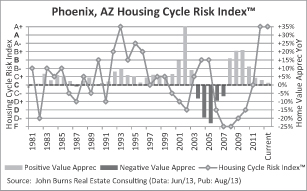

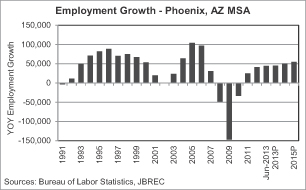

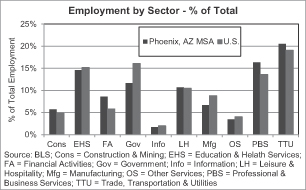

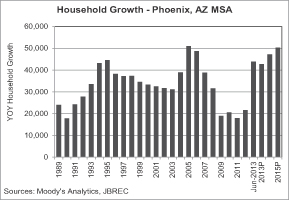

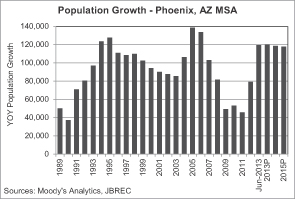

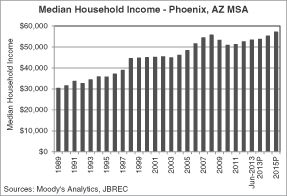

Phoenix. The Phoenix market has recovered significantly with strong job growth fueling housing demand. As of June 30, 2013, the non-seasonally adjusted unemployment rate was 7.2%, down from 7.6% one year prior. In the twelve months ended June 30, 2013, new home sales were up 22.6% from the similar prior year period. Existing home values rose approximately 26% in the twelve months ended June 30, 2013 following five years of declining values, according to the JBREC Burns Home Value Index. Resale inventory has declined rapidly and, as of June 30, 2013, there was only 2.1 months of supply in the Phoenix market.

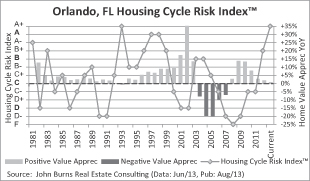

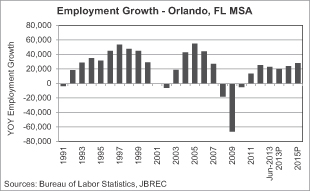

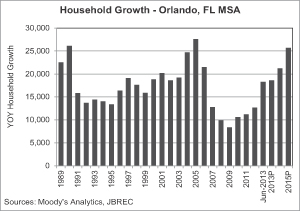

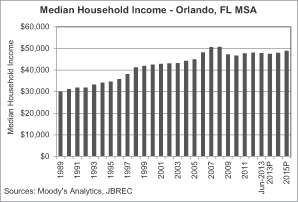

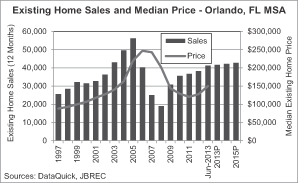

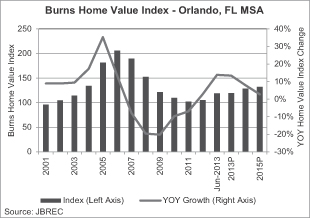

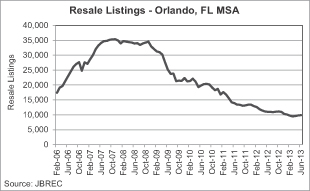

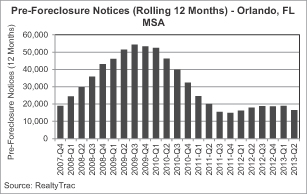

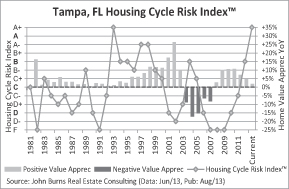

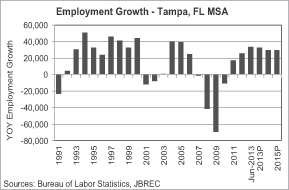

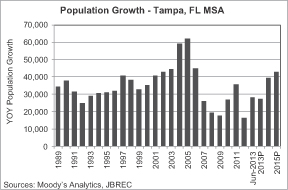

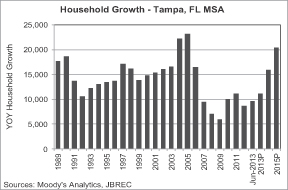

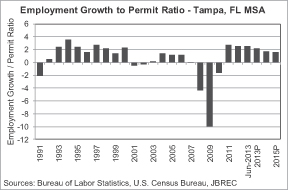

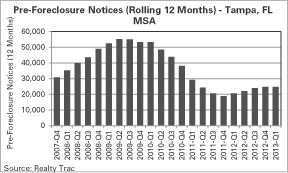

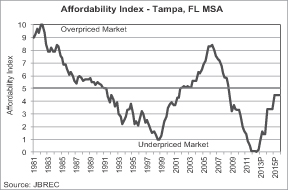

Central Florida. The Central Florida market continues to recover as the local economy adds jobs and low home inventory levels continue to drive price appreciation. In Tampa, the seasonally adjusted unemployment rate in June, 2013 was 7.2%, down from 8.8% one year prior. In June 2013, existing homes sales were up 74% from the trough of 2008. For the twelve months ended June 30, 2013, new home sales were up 23.4% period-over-period. Orlando is benefitting from its vibrant economy and globally recognized tourism industry. In June 2013, the seasonally adjusted unemployment rate was 6.9%, down from 8.7% one year earlier. Throughout the recession, Orlando’s population continued to grow and in 2012 Orlando added 49,000 people (a growth of 2.2%). Existing home sales have been on the rise, growing 117% from the end of 2008 through June 30, 2013. In the twelve months ended June 30, 2013, new home sales increased 33.8% from the similar prior year period.

7

Table of Contents

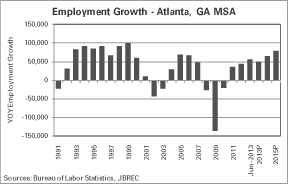

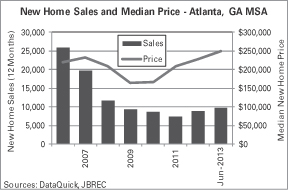

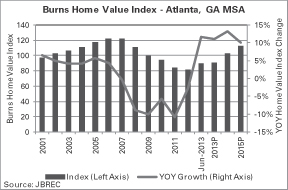

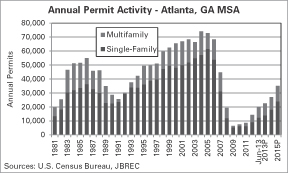

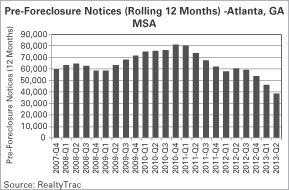

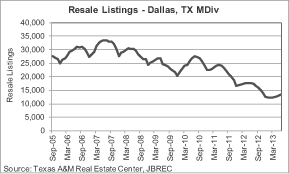

Atlanta. As the fundamentals that drive the Atlanta housing market reflect a more stable environment, the Atlanta housing market is on track for improving sales and pricing. Job growth was 2.4%, exceeding the national average of 1.7%, in the twelve months ended June 30, 2013, and home values appreciated 12.9% according to the JBREC Burns Home Value Index. In the same period, sales of new homes were up 23%, job creation was more than triple the number of homebuilding permits issued and resale listings declined to a level equal to 3.8 months supply.

We are currently in the process of finalizing our financial results for the three and nine months ended September 30, 2013. Set forth below are certain preliminary estimates for the three months ended September 30, 2013, based on the most current information available to management, as of the date of this prospectus. Our actual results may differ materially from these estimates due to the completion of our financial closing procedures, final adjustments and other developments that may arise between now and the time the financial results for the three and nine months ended September 30, 2013, are finalized.

| • | Our revenues for the three months ended September 30, 2013, are expected to be between $36.5 million and $37.5 million. |

| • | On a pro forma basis, we expect revenues for the three months ended September 30, 2013 to be between $67.0 million and $69.0 million. |

| • | We closed 240 homes in 14 active communities during the three months ended September 30, 2013, a decrease of 6 homes, or 2.4%, from 246 home closings in the three months ended June 30, 2013. Our home closings in the third quarter of 2013 included closings for the first time in 4 new communities. |

| • | On a pro forma basis, we closed 448 homes in 22 active communities during the three months ended September 30, 2013, an increase of 37 homes, or 9.0%, from 411 home closings in the three months ended June 30, 2013. Our home closings on a pro forma basis in the third quarter of 2013 included closings for the first time in 4 new communities. |

We expect to complete our financial closing procedures for the three and nine months ended September 30, 2013 in early November 2013. The preliminary unaudited financial and other data set forth in this section has been prepared by, and is the responsibility of, our management. The foregoing information and estimates have not been compiled or reviewed by either our independent registered public accounting firm or the independent registered public accounting firm of the LGI/GTIS Joint Ventures nor have either independent registered public accounting firms performed any procedures with respect to this information or expressed any opinion or any form of assurance on such information. In addition, the foregoing information and estimates are subject to revision as we prepare our financial statements and other disclosures as of and for the three and nine months ended September 30, 2013, including all disclosures required by U.S. GAAP. Because we have not completed our normal quarterly closing and review procedures for the three and nine months ended September 30, 2013, and subsequent events may occur that require material adjustments to these results, the final results and other disclosures for the three and nine months ended September 30, 2013 may differ materially from these estimates. These estimates should not be viewed as a substitute for full financial statements prepared in accordance with U.S. GAAP or as a measure of performance.

8

Table of Contents

In August 2013, we entered the Tucson market where we currently own 24 lots and expect to own 271 lots by December 31, 2013. We began construction on our first homes in Tucson in September 2013 and we expect to close our first home sale in Tucson during the first quarter of 2014. In addition, in September 2013, we entered into a letter of intent to purchase 87 lots in Albuquerque and expect to acquire those lots and begin construction on our first homes in Albuquerque during the fourth quarter of 2013. We expect to close our first home sale in Albuquerque during the second quarter of 2014.

The U.S. federal government shutdown in the first part of October 2013 impacted the Federal Housing Administration and the U.S. Department of Agriculture, among other federal agencies, and their backing of mortgage loans, and negatively affected our closings in October 2013. We believe that a number of closings that would have otherwise occurred in October 2013 will occur in November 2013, and that our closings in the fourth quarter of 2013 will be in line with our annual business plan; however, we make no assurances that our anticipated closings will be realized. See “Risk Factors” and “Cautionary Note Concerning Forward-Looking Statements” for a discussion of factors that may cause our actual results to differ materially from those noted above.

LGI Transaction

Concurrently with this offering, we will acquire from Thomas Lipar, one of our founders, Eric Lipar, our Chief Executive Officer and Chairman of the Board and their respective affiliates, the equity interests of our predecessor, in exchange for 10,091,020 shares of our common stock (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus), including 1,698,214 shares of common stock to be issued to the non-controlling interests in a subsidiary of our predecessor (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus). As a result, the entities which make up our predecessor will become our wholly-owned subsidiaries. See “Certain Relationships and Related Party Transactions.” We collectively refer to the transactions described in this paragraph as the “LGI Transaction.”

GTIS Transaction

Our predecessor owns a 15% equity interest in and manages the day-to-day operations of the LGI/GTIS Joint Ventures. Concurrently with this offering, we will acquire from GTIS all of the GTIS equity interests in the LGI/GTIS Joint Ventures, in exchange for aggregate consideration of $41.4 million, consisting of a cash payment of $36.9 million and an aggregate value of $4.5 million of shares of our common stock (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus, we will issue 321,429 shares of common stock to GTIS in connection with this transaction). We refer to the transactions described in this paragraph as the “GTIS Transaction.”

We will use purchase accounting for the GTIS Transaction. In the pro forma financial information appearing in “Unaudited Pro Forma Financial Information” and elsewhere in this prospectus, we estimate certain adjustments made as a result of this application of purchase accounting, including (i) recording the net tangible assets of the LGI/GTIS Joint Ventures at fair value, (ii) recording goodwill for the excess of the GTIS Transaction purchase price and the

9

Table of Contents

estimated fair value of our equity interests in the LGI/GTIS Joint Ventures over the identifiable net tangible assets of the LGI/GTIS Joint Ventures, (iii) recording a gain as a result of the re-measurement of our equity interests in the LGI/GTIS Joint Ventures at fair value, and (iv) recording deferred income tax related to the purchase accounting adjustments. Following the closing of this offering, we will own all of the equity interests in the LGI/GTIS Joint Ventures and we will account for them on a consolidated basis rather than by using the equity method.

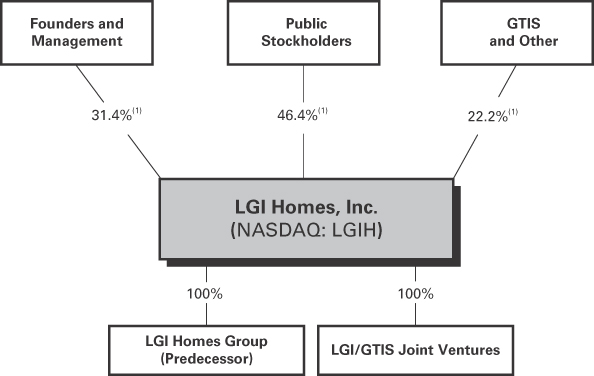

Formation Transactions and The Transactions

We refer to the LGI Transaction and the GTIS Transaction as the “Formation Transactions.” We refer to the Formation Transactions, the issuance and sale of shares of our common stock in this offering (excluding shares issuable upon any exercise of the underwriters’ option to purchase additional shares of our common stock) and the application of the net proceeds from this offering as described in “Use of Proceeds” as the “Transactions.”

The following is a simplified diagram of our organizational structure after giving effect to the Formation Transactions and this offering.

| (1) | Assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus. |

10

Table of Contents

An investment in the shares of our common stock involves risks. You should consider carefully the risks discussed below and described more fully along with other risks under “Risk Factors” in this prospectus before investing in our common stock.

| • | Continued or additional tightening of mortgage lending standards, mortgage financing requirements and rising interest rates could adversely affect the availability of mortgage loans for potential purchasers of our homes and thereby reduce our sales. |

| • | The Dodd-Frank Act may affect the availability or cost of mortgages, which could adversely affect our results of operations. |

| • | Our long-term growth depends, in part, upon our ability to acquire land parcels suitable for residential homebuilding at reasonable prices. |

| • | Risks associated with our land and lot inventories could adversely affect our business or financial results. |

| • | Labor and raw material shortages and price fluctuations could delay or increase the cost of home construction, which could materially and adversely affect us. |

| • | Any limitation on, or reduction or elimination of, tax benefits associated with homeownership would have an adverse effect upon the demand for homes, which could be material to our business. |

| • | The recent growth in the housing market may not continue at the same rate, and any decline in the growth rate in our markets or for the homebuilding industry may materially and adversely affect our business and financial condition. |

| • | We may incur a variety of costs to engage in future growth or expansion of our operations and the anticipated benefits may never be realized. |

| • | Our geographic concentration could materially and adversely affect us if the homebuilding industry in our current markets should experience a decline. |

| • | Our industry is cyclical and adverse changes in general and local economic conditions could reduce the demand for homes and, as a result, could have a material adverse effect on us. |

| • | Fluctuations in real estate values may require us to write-down the book value of our real estate assets. |

| • | We expect to use leverage in executing our business strategy, which may adversely affect the return on our assets. |

| • | Concentration of ownership of the voting power of our capital stock may prevent other stockholders from influencing corporate decisions and create perceived conflicts of interest. |

| • | There is currently no public market for shares of our common stock, a trading market for our common stock may never develop following this offering and our common stock price may be volatile and could decline substantially following this offering. |

| • | The offering price per share of our common stock offered by this prospectus may not accurately reflect the value of your investment. |

11

Table of Contents

Implications of Being an Emerging Growth Company

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. Thus, we are not required to provide more than two years of audited financial statements, selected financial data and related Management’s Discussion & Analysis of Financial Condition and Results of Operations in this prospectus. For as long as we are an emerging growth company, unlike other public companies, we will not be required to:

| • | provide an attestation and report from our auditors on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act; |

| • | comply with certain new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB; |

| • | comply with certain new audit rules adopted by the PCAOB after April 5, 2012, unless the Securities and Exchange Commission, or the SEC, determines otherwise; |

| • | provide disclosures regarding executive compensation required of larger public companies; and |

| • | obtain stockholder approval of any golden parachute payments not previously approved. |

We intend to take advantage of all of these exemptions.

We will cease to be an emerging growth company when any of the following conditions apply:

| • | we have $1.0 billion or more in annual revenues; |

| • | at least $700 million in market value of our common stock are held by non-affiliates; |

| • | we issue more than $1.0 billion of non-convertible debt over a three-year period; or |

| • | the last day of the fiscal year following the fifth anniversary of our initial public offering has passed. |

In addition, an emerging growth company can delay its adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of such extended transition period, and as a result, we will comply with any new or revised accounting standards on the relevant dates on which non-emerging growth companies must adopt such standards. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Our principal executive offices are located at 1450 Lake Robbins Drive, Suite 430, The Woodlands, Texas 77380, and our telephone number is (281) 362-8998. Our website address is www.lgihomes.com. The information contained in, or that can be accessed through, our website is not incorporated by reference and is not part of this prospectus.

12

Table of Contents

Common stock offered by us | 9,000,000 shares |

Common stock to be outstanding immediately following this offering | 19,413,449 shares(1) |

Underwriters’ option | We have granted the underwriters an option to purchase up to 1,350,000 additional shares of our common stock. |

Use of Proceeds | We expect to receive net proceeds from this offering of approximately $114.2 million (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus), after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. |

| We expect to use $36.9 million of the net proceeds from this offering to make a payment to GTIS as the cash portion of the purchase price to acquire all of the joint venture interests of GTIS in the LGI/GTIS Joint Ventures which we do not own, and we expect to use the remainder of the net proceeds for working capital and for general corporate purposes, including the acquisition of land, development of lots and construction of homes. |

Dividend policy | We currently intend to retain our future earnings, if any, to finance the development and expansion of our business and, therefore, do not intend to pay cash dividends on our common stock for the foreseeable future. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on our financial condition, results of operations, capital requirements, restrictions contained in any of our financing arrangements and such other factors as our board of directors deems relevant. See “Dividend Policy.” |

Proposed NASDAQ symbol | We have applied to list our common stock on the NASDAQ Global Select Market under the symbol “LGIH.” |

Risk factors | Investing in our common stock involves a high degree of risk. For a discussion of factors you should consider in making an investment, see “Risk Factors.” |

| (1) | Based on 1,000 shares outstanding as of October 28, 2013 and: |

| • | includes 10,091,020 shares to be issued in connection with the LGI Transaction (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus); |

| • | includes 321,429 shares to be issued in connection with the GTIS Transaction (assuming an initial public offering price of $14.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus); |

| • | excludes 125,186 restricted stock units to be granted to employees, executive officers and non-employee directors upon the consummation of this offering under our Equity Incentive Plan (see “Compensation of Our Directors and Executive Officers—2013 Equity Incentive Plan”); and |

| • | excludes the 1,500,000 shares of common stock authorized to be issued under our Equity Incentive Plan (see “Compensation of Our Directors and Executive Officers — 2013 Equity Incentive Plan”). |

13

Table of Contents

Summary Historical and Pro Forma Financial and Operating Data

The following table presents our summary historical and pro forma financial and operating data as of the dates and for the periods indicated.

The summary historical balance sheet and statement of operations information presented as of December 31, 2012 and 2011 and for the years ended December 31, 2012 and 2011 are derived from the audited historical combined financial statements of our predecessor, LGI Homes Group (Predecessor), that are included elsewhere in this prospectus. The summary historical balance sheet and statement of operations information presented as of June 30, 2013 and for the six months ended June 30, 2013 and 2012 are derived from the unaudited historical combined financial statements of LGI Homes Group (Predecessor) that are included elsewhere in this prospectus. The historical combined financial statements of our predecessor account for investments in the LGI/GTIS Joint Ventures using the equity method. The following table should be read together with, and is qualified in its entirety by reference to, the historical combined financial statements of LGI Homes Group (Predecessor) and the accompanying notes included elsewhere in this prospectus. The table should also be read together with “Capitalization,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The summary pro forma financial information presented as of June 30, 2013 and for the six months ended June 30, 2013 and the year ended December 31, 2012 gives effect to the Formation Transactions, the issuance and sale of shares of our common stock in this offering and the use of proceeds thereof as described under “Use of Proceeds” and is derived from the unaudited and audited combined financial statements of LGI Homes Group (Predecessor) and the unaudited and audited financial statements of the LGI/GTIS Joint Ventures, included elsewhere in this prospectus. See “—The Transactions” for a description of the Formation Transactions. The summary pro forma financial information should be read together with our unaudited pro forma financial statements included elsewhere in this prospectus and “Unaudited Pro Forma Financial Information.”

| Pro Forma Six Months Ended June 30, | Six Months Ended June 30, | Pro Forma Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||

| 2013 | 2013 | 2012 | 2012 | 2012 | 2011 | |||||||||||||||||||

Statement of Operations Data: | (in thousands) | |||||||||||||||||||||||

Home sales | $ | 95,969 | $ | 57,998 | $ | 27,861 | $ | 143,378 | $ | 73,820 | $ | 49,270 | ||||||||||||

Management and warranty fees | — | 1,302 | 992 | — | 2,401 | 1,186 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total revenues | $ | 95,969 | $ | 59,300 | $ | 28,853 | $ | 143,378 | $ | 76,221 | $ | 50,456 | ||||||||||||

Cost of sales | 69,465 | 42,142 | 20,273 | 104,229 | 54,531 | 36,700 | ||||||||||||||||||

Selling expenses | 9,164 | 5,493 | 2,863 | 13,370 | 7,269 | 4,884 | ||||||||||||||||||

General and administrative | 6,073 | 5,026 | 2,451 | 7,649 | 6,096 | 5,126 | ||||||||||||||||||

Income from unconsolidated joint ventures | — | (944 | ) | (586 | ) | — | (1,526 | ) | (715 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Operating income | $ | 11,267 | $ | 7,583 | $ | 3,852 | $ | 18,130 | $ | 9,851 | $ | 4,461 | ||||||||||||

Interest expense | (6 | ) | (6 | ) | (25 | ) | (1 | ) | (1 | ) | (28 | ) | ||||||||||||

Other income, net | 84 | 22 | 24 | 215 | 173 | 204 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net income before income taxes | $ | 11,345 | $ | 7,599 | $ | 3,851 | $ | 18,344 | $ | 10,023 | $ | 4,637 | ||||||||||||

Income taxes | 3,976 | 136 | 65 | 6,395 | 155 | 125 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net income | $ | 7,369 | $ | 7,463 | $ | 3,786 | $ | 11,949 | $ | 9,868 | $ | 4,512 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

(Income) loss attributable to non-controlling interests | — | 146 | (68 | ) | (163 | ) | (163 | ) | (1,162 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net income attributable to owners | $ | 7,369 | $ | 7,609 | $ | 3,718 | $ | 11,786 | $ | 9,705 | $ | 3,350 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

14

Table of Contents

| Pro Forma Six Months Ended June 30, | Six Months Ended June 30, | Pro Forma Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||

| 2013 | 2013 | 2012 | 2012 | 2012 | 2011 | |||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

Other Financial and Operating Data: | ||||||||||||||||||||||||

Active communities during period(1) | 16.7 | 10.0 | 5.3 | 11.4 | 6.6 | 4.8 | ||||||||||||||||||

Active communities at end of period | 18 | 10 | 6 | 15 | 10 | 5 | ||||||||||||||||||

Home closings | 664 | 397 | 204 | 1,062 | 536 | 376 | ||||||||||||||||||

Completed homes | 213 | 115 | 33 | 185 | 116 | 59 | ||||||||||||||||||

Homes in progress | 380 | 225 | 98 | 177 | 124 | 34 | ||||||||||||||||||

Average sales price of homes closed | $ | 145 | $ | 146 | $ | 137 | $ | 135 | $ | 138 | $ | 131 | ||||||||||||

Gross margin(2) | $ | 26,504 | $ | 15,856 | $ | 7,588 | $ | 39,149 | $ | 19,289 | $ | 12,570 | ||||||||||||

Gross margin %(3) | 27.6 | % | 27.3 | % | 27.2 | % | 27.3 | % | 26.1 | % | 25.5 | % | ||||||||||||

Adjusted gross margin(4) | $ | 27,090 | $ | 16,442 | $ | 8,061 | $ | 40,096 | $ | 20,236 | $ | 14,033 | ||||||||||||

Adjusted gross margin %(3)(4) | 28.2 | % | 28.3 | % | 28.9 | % | 28.0 | % | 27.4 | % | 28.5 | % | ||||||||||||

Adjusted EBITDA(5) | $ | 12,289 | $ | 8,300 | $ | 4,402 | $ | 19,863 | $ | 10,983 | $ | 6,005 | ||||||||||||

Adjusted EBITDA margin %(3)(5) | 12.8 | % | 14.3 | % | 15.8 | % | 13.9 | % | 14.9 | % | 12.2 | % | ||||||||||||

Balance Sheet Data (as of end of period): | ||||||||||||||||||||||||

Cash and cash equivalents | $ | 94,812 | $ | 15,205 | $ | 7,069 | $ | 5,106 | ||||||||||||||||

Real estate inventory | $ | 90,159 | $ | 49,191 | $ | 28,489 | $ | 12,526 | ||||||||||||||||

Goodwill | $ | 9,481 | — | — | — | |||||||||||||||||||

Total assets | $ | 204,876 | $ | 79,803 | $ | 45,556 | $ | 23,513 | ||||||||||||||||

Notes payable | $ | 23,065 | $ | 23,065 | $ | 14,969 | $ | 6,415 | ||||||||||||||||

Total liabilities | $ | 37,602 | $ | 32,526 | $ | 20,345 | $ | 8,878 | ||||||||||||||||

Total equity | $ | 167,274 | $ | 47,277 | $ | 25,211 | $ | 14,635 | ||||||||||||||||

| (1) | With respect to the six months ended June 30, 2013 and 2012, defined as the sum of the number of communities in which we were closing homes as of the first day of the year and the last day of each quarter during the first half of the year divided by three. With respect to the year ended December 31, 2012 and 2011, defined as the sum of the number of communities in which we were closing homes as of the first day of the year and the last day of each quarter during the year divided by five. |

| (2) | Gross margin is home sales revenue less cost of sales. |

| (3) | Calculated as a percentage of home sales revenue. |

| (4) | Adjusted gross margin is a non-GAAP financial measure used by management as a supplemental measure in evaluating operating performance. We define adjusted gross margin as gross margin less capitalized interest included in the cost of sales. Our management believes this information is meaningful, because it isolates the impact that capitalized interest has on gross margin. However, because adjusted gross margin information excludes capitalized interest, which has real economic effects and could impact our results, the utility of adjusted gross margin information as a measure of our operating performance may be limited. In addition, other companies may not calculate adjusted gross margin information in the same manner that we do. Accordingly, adjusted gross margin information should be considered only as a supplement to gross margin information as a measure of our performance. |

15

Table of Contents

The following table reconciles adjusted gross margin to gross margin, which is the GAAP financial measure that our management believes to be most directly comparable:

| Pro Forma Six Months Ended June 30, | Six Months Ended June 30, | Pro Forma Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||

| 2013 | 2013 | 2012 | 2012 | 2012 | 2011 | |||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

Home sales | $ | 95,969 | $ | 57,998 | $ | 27,861 | $ | 143,378 | $ | 73,820 | $ | 49,270 | ||||||||||||

Cost of sales | 69,465 | 42,142 | 20,273 | 104,229 | 54,531 | 36,700 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross margin | $ | 26,504 | $ | 15,856 | $ | 7,588 | $ | 39,149 | $ | 19,289 | $ | 12,570 | ||||||||||||

Capitalized interest charged to cost of sales | 586 | 586 | 473 | 947 | 947 | 1,463 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted gross margin | $ | 27,090 | $ | 16,442 | $ | 8,061 | $ | 40,096 | $ | 20,236 | $ | 14,033 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross margin %(a) | 27.6 | % | 27.3 | % | 27.2 | % | 27.3 | % | 26.1 | % | 25.5 | % | ||||||||||||

Adjusted gross margin %(a) | 28.2 | % | 28.3 | % | 28.9 | % | 28.0 | % | 27.4 | % | 28.5 | % | ||||||||||||

| (a) | Calculated as a percentage of home sales revenue. |

| (5) | Adjusted EBITDA is a non-GAAP financial measure used by management as a supplemental measure in evaluating operating performance. We define adjusted EBITDA as net income before (i) interest expense, (ii) income taxes, (iii) depreciation and amortization, (iv) capitalized interest charged to the cost of sales and (v) other income, net and excluding adjustments resulting from the application of purchase accounting in connection with the GTIS Transaction. Our management believes that the presentation of adjusted EBITDA provides useful information to investors regarding our results of operations because it assists both investors and management in analyzing and benchmarking the performance and value of our business. Adjusted EBITDA provides an indicator of general economic performance that is not affected by fluctuations in interest rates or effective tax rates, levels of depreciation or amortization and items considered to be unusual or non-recurring. Accordingly, our management believes that this measurement is useful for comparing general operating performance from period to period. Other companies may define adjusted EBITDA differently and, as a result, our measure of adjusted EBITDA may not be directly comparable to adjusted EBITDA of other companies. Although we use adjusted EBITDA as a financial measure to assess the performance of our business, the use of adjusted EBITDA is limited because it does not include certain material costs, such as interest and taxes, necessary to operate our business. Adjusted EBITDA should be considered in addition to, and not as a substitute for, net income in accordance with GAAP as a measure of performance. Our presentation of adjusted EBITDA should not be construed as an indication that our future results will be unaffected by unusual or nonrecurring items. Our adjusted EBITDA is limited as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are: |

| • | it does not reflect every cash expenditure, future requirements for capital expenditures or contractual commitments, including for the purchase of land; |

| • | it does not reflect the interest expense or the cash requirements necessary to service interest or principal payments on our debt; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced or require improvements in the future, and adjusted EBITDA does not reflect any cash requirements for such replacements or improvements; |

| • | it is not adjusted for all non-cash income or expense items that are reflected in our statements of cash flows; |

| • | it does not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations; and |

| • | other companies in our industry may calculate it differently than we do, limiting its usefulness as a comparative measure. |

Because of these limitations, our adjusted EBITDA should not be considered a measure of discretionary cash available to us to invest in the growth of our business or as a measure of cash that will be available to us to meet our obligations. We compensate for these limitations by using our adjusted EBITDA along with other comparative tools, together with GAAP measurements, to assist in the evaluation of operating performance. These GAAP

16

Table of Contents

measurements include operating income, net income and cash flow data. We have significant uses of cash flows, including capital expenditures, interest payments and other non-recurring charges, which are not reflected in our adjusted EBITDA.

Adjusted EBITDA is not intended as an alternative to net income as an indicator of our operating performance, as an alternative to any other measure of performance in conformity with GAAP or as an alternative to cash flows as a measure of liquidity. You should therefore not place undue reliance on our adjusted EBITDA calculated using this measure. Our GAAP-based measures can be found in our consolidated financial statements and related notes included elsewhere in this prospectus.

The following table reconciles adjusted EBITDA to net income, which is the GAAP financial measure that our management believes to be most directly comparable:

| Pro Forma Six Months Ended June 30, | Six Months Ended June 30, | Pro Forma Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||

| 2013 | 2013 | 2012 | 2012 | 2012 | 2011 | |||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

Net income | $ | 7,369 | $ | 7,463 | $ | 3,786 | $ | 11,949 | $ | 9,868 | $ | 4,512 | ||||||||||||

Interest expense | 6 | 6 | 25 | 1 | 1 | 28 | ||||||||||||||||||

Income taxes | 3,976 | 136 | 65 | 6,395 | 155 | 126 | ||||||||||||||||||

Depreciation and Amortization | 303 | 131 | 77 | 518 | 185 | 80 | ||||||||||||||||||

Capitalized interest charged to cost of sales | 586 | 586 | 473 | 947 | 947 | 1,463 | ||||||||||||||||||

Other income, net | (84 | ) | (22 | ) | (24 | ) | (215 | ) | (173 | ) | (204 | ) | ||||||||||||

Purchase accounting adjustment(a) | 133 | — | — | 268 | — | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted EBITDA | $ | 12,289 | $ | 8,300 | $ | 4,402 | $ | 19,863 | $ | 10,983 | $ | 6,005 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted EBITDA | 12.8% | 14.3 | % | 15.8 | % | 13.9 | % | 14.9 | % | 12.2 | % | |||||||||||||

| (a) | This adjustment results from the application of purchase accounting in connection with the acquisition of all of the equity interests of GTIS in the GTIS Transaction and represents amortization of the fair value of a marketing-related intangible asset. See “Unaudited Pro Forma Financial Information.” |

| (b) | Calculated as a percentage of home sales revenue. |

17

Table of Contents

An investment in our common stock involves a high degree of risk and should be considered highly speculative. Before making an investment decision, you should carefully consider the specific risk factors set forth below, which we believe address the material risks concerning our business and an investment in our common stock, together with the other information included elsewhere in this prospectus. If any of the risks discussed in this prospectus occur, our business, prospects, liquidity, financial condition and results of operations could be materially impaired, in which case the trading price of our common stock could decline significantly and you could lose all or part of your investment. Some statements in this prospectus, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section entitled “Cautionary Note Concerning Forward-Looking Statements.”

Continued or additional tightening of mortgage lending standards and mortgage financing requirements and rising interest rates could adversely affect the availability of mortgage loans for potential purchasers of our homes and thereby reduce our sales.

Almost all purchasers of our homes finance their acquisition through lenders that provide mortgage financing. According to the Federal Home Loan Mortgage Corporation (“Freddie Mac”), 30-year average mortgage rates rose from approximately 3.5% in March 2013 to approximately 4.4% in July 2013. As mortgage interest rates increase, and, as a result, the ability of prospective homebuyers to finance home purchases is adversely affected, our operating results may be significantly negatively impacted. Our homebuilding activities are dependent upon the availability of mortgage financing to homebuyers. The availability of mortgage financing remains constrained, due in part to lower mortgage valuations on properties, various regulatory changes and lower risk appetite by lenders. Lenders currently require increased levels of financial documentation, larger down payments and more restrictive income to debt ratios. First-time homebuyers are generally more affected by the availability of mortgage financing than other potential homebuyers. These homebuyers are a key source of demand for our new homes. A limited availability of home mortgage financing may adversely affect the volume and sales price of our home sales.

Due to the recent volatility and uncertainty in the credit markets and in the mortgage lending and mortgage finance industries, the federal government has taken on a significant role in supporting mortgage lending through its conservatorship of Federal National Mortgage Association (“Fannie Mae”) and Freddie Mac, both of which purchase or insure mortgage loans and mortgage loan-backed securities, and its insurance of mortgage loans through or in connection with the Federal Housing Administration (“FHA”), the Veterans Administration (“VA”) and the U.S. Department of Agriculture (“USDA”). FHA and USDA backing of mortgage loans has been particularly important to the mortgage finance industry and to our business. If either the FHA or USDA raised their down payment requirements, our business could be materially affected. The USDA rural development program provides for zero down payment and 100% financing for homebuyers in qualifying areas. As of June 30, 2013, the USDA program is available in all our markets and is available to approximately 70% of our active communities. If the USDA program was discontinued or if funding was decreased, then our business could be adversely affected. In addition, if the USDA changed its determination of areas that are eligible to qualify for the program, it could have an adverse effect on our business.

The availability and affordability of mortgage loans, including interest rates for such loans, could also be adversely affected by a scaling back or termination of the federal government’s

18

Table of Contents

mortgage loan-related programs or policies. Because Fannie Mae-, Freddie Mac-, FHA-, USDA- and VA-backed mortgage loans have been an important factor in marketing and selling many of our homes, any limitations or restrictions in the availability of, or higher consumer costs for, such government-backed financing could reduce our business, prospects, liquidity, financial condition and results of operations could be materially and adversely affected. The elimination or curtailment of state bonds utilized by us could materially and adversely affect our business, prospects, liquidity, financial condition and results of operations.

The U.S. federal government shutdown in the first part of October 2013, and any future government shutdowns or slowdowns, may materially adversely affect our business or financial results.

The U.S. federal government shutdown in the first part of October 2013 which impacted the FHA and the USDA, among other federal agencies, and their backing of mortgage loans, negatively affected our closings in October 2013. Any future government shutdowns or slowdowns may materially adversely affect our business or financial results. We can make no assurances that potential closings affected by any such shutdown or slowdown will occur after the shutdown or slowdown has ended.

The Dodd-Frank Act may affect the availability or cost of mortgages, which could adversely affect our results of operations.